tax 2 can - lss | cans dbcans.allardlss.com/application/media/cans/christian_law... · web viewtax...

TRANSCRIPT

Tax 2 CAN

CHAPTER ONE: “BASE CASE”.............................................................................................................................................4

TAX RATE TO BE APPLIED TO CORP’S INCOME:.........................................................................................................................4GROSS-UP AND DIVIDEND TAX CREDIT...................................................................................................................................4INTER-CORPORATE DIVIDENDS..................................................................................................................................................5

CHAPTER 2: CLASSIFICATION OF CORPORATIONS (FOR SPECIAL RATES AND RULES)...............................5

PRIVATE CORPORATION:...........................................................................................................................................................5CANADIAN CONTROLLED PRIVATE CORPORATION (CCPC).....................................................................................................6

s.251(5)(b): deeming rule re: legal control:........................................................................................................................6Silicon Graphics: de facto control.......................................................................................................................................6Transport Couture...............................................................................................................................................................6Taber Solids TCC- Control in fact s.256(5.1)......................................................................................................................6

CHAPTER 3: SPECIAL RATE FOR ACTIVE BUSINESS INCOME OF A CCPC..........................................................7

SMALL BUSINESS RATE:............................................................................................................................................................7CORPORATE INCOME THAT QUALIFIES FOR THE SMALL BUSINESS RATE.................................................................................7

Lerric v. the Queen: 5 or more employees, not fractions....................................................................................................8S & C Ross Enterprises Ltd v. the Queen- PSB test............................................................................................................8489599 BC LTd: 5FT + 2PT= >5FT...................................................................................................................................8

ASSOCIATED CORPORATIONS - NOTE: CAN BE RELATED WITHOUT BEING ASSOCIATED!!....................................................9Hughes Homes- no s.256(2.1) b/c had valid business purpose..........................................................................................10

RELATED PERSONS - NOTE: DISTINCT FROM ASSOCIATED CORPS!!!!!!!................................................................10

CHAPTER 4: SPECIAL REFUNDABLE TAX SYSTEM FOR INVESTMENT INCOME OF CERTAIN PRIVATE CORPORATIONS - RDTOH..................................................................................................................................................11

POLICY GOALS OF REFUNDABLE TAX:.....................................................................................................................................11INVESTMENT INCOME EXCEPT DIVIDENDS FROM OTHER CANADIAN CORPORATIONS..........................................................11

Shamita Inc –income from active business test.................................................................................................................11TAX RATE THAT APPLIES TO CCPC’S AGGREGATE INVESTMENT INCOME:...........................................................................11PRIVATE CORPORATIONS THAT RECEIVE DIVIDENDS FROM OTHER CANADIAN CORPORATIONS...........................................12FIRST ASPECT OF PART IV TAX: NOT CONNECTED................................................................................................................12SECOND ASPECT OF PART IV TAX: CONNECTED CORPS........................................................................................................13

Canwest Capital- s.129(2.1) test.......................................................................................................................................13CAPITAL DIVIDEND ACCOUNT (CDA)- TAX FREE PORTION OF CAPITAL GAINS.....................................................................13

CHAPTER 5: GENERAL RATE INCOME POOL (GRIP) AND ELIGIBLE DIVIDENDS...........................................14

GRIP AND ELIGIBLE DIVIDEND SYSTEM................................................................................................................................14EXCESSIVE ELIGIBLE DIVIDEND DESIGNATIONS....................................................................................................................14

CHAPTER SIX: SHAREHOLDER BENEFITS AND SHAREHOLDER LOANS...........................................................15

COMPUTING VALUE OF BENEFIT: NOT SETTLED LAW..............................................................................................................15Hinkson: FMV outlay for cabin.........................................................................................................................................15Pillsbury: benefit on SH qua SH.......................................................................................................................................15Youngman FCA- equity rate of return/ cost of capital- fancy house.................................................................................15Fingold FCA- florida condo: cost of capital......................................................................................................................15Franklin- bookkeeping error, no actual benefit.................................................................................................................15

SHAREHOLDER LOAN..............................................................................................................................................................16EXCEPTIONS TO LOAN INCLUSION...........................................................................................................................................16

Meeuse, - succession of loans not series for s.15(2.6).......................................................................................................16DEEMED BENEFIT: INTEREST..................................................................................................................................................16

CHAPTER 7: SHARE CAPITAL AND DEEMED DIVIDEND..........................................................................................16

TWO CALCULATIONS: 1) DEEMED DIVIDEND, 2) CAPITAL GAIN-LESS THE DEEMED DIVIDEND...............................................17

1

EXCEPTIONS TO DEEMED DIVIDENDS:.....................................................................................................................................17SOME TYPICAL SITUATIONS:...................................................................................................................................................17

CHAPTER 8: SECTION 85.1 SHARE FOR SHARE MERGER........................................................................................18

S.85.1 PRE- CONDITIONS:.......................................................................................................................................................18S.85.1(1)(A) EFFECT OF EXCHANGE ON VENDOR/TRANSFEROR (CORP GETTING RID OF OLD SHARES).................................18S.85.1(1)(B) EFFECT OF EXCHANGE ON PURCHASER (CORP ISSUING NEW SHARES)..............................................................18TAX PUC OF PURCHASERS (NEW) SHARES ISSUED TO VENDOR:...........................................................................................19

CHAPTER 9: SECTION 85 TRANSFERS: TRANSFER OF PROPERTY TO A CORPORATION.............................19

S.85(1) PRECONDITIONS:.........................................................................................................................................................19ELECTED AMOUNT..................................................................................................................................................................19S.85(2.1): COMPUTING PUC:..................................................................................................................................................20INDIRECT BENEFITS RULE.......................................................................................................................................................21FREEZE TRANSACTION:...........................................................................................................................................................21

CHAPTER 10: SECTION 86 AND 51 SHARE EXCHANGES...........................................................................................21

S.86 EXCHANGE OF SHARES BY SH IN COURSE OF RE-ORG OF CAPITAL...............................................................................21S.86(2.1): COMPUTATION OF PAID-UP CAPITAL.....................................................................................................................22DEEMED DIVIDEND.................................................................................................................................................................23S.86(2): GIFT PORTION RULE:.................................................................................................................................................23S.51(1) CONVERTIBLE PROPERTY...........................................................................................................................................24

CHAPTER 11: AMALGAMATION.......................................................................................................................................24

S.87(1) AMALGAMATION........................................................................................................................................................25S.87(4) SHARES OF PREDECESSOR CORP:................................................................................................................................25PUC........................................................................................................................................................................................25EXCEPTIONS TO NEW CORPORATION RULE:............................................................................................................................25ANTI AVOIDANCE RULES:......................................................................................................................................................25

CHAPTER 12: LIQUIDATION..............................................................................................................................................25

S.88(1) WINDING-UP:.............................................................................................................................................................25S.88(1)(B): WINDING-UP DISPOSITION (CANCELING) SUBCO SHARES BY PARENTCO:...........................................................26S.88(1)(C): COST OF PROPERTY RECEIVED BY PARENT:.........................................................................................................26THE BUMP: S.88(1)(D): ADDITION TO COST OF CAPITAL PROPERTY ACQUIRED BY PARENT (“THE BUMP”):...................26VERTICAL AMALGAMATION:...................................................................................................................................................26

CHAPTER 13: CAPITAL GAIN EXEMPTION FOR QSBC SHARES.............................................................................27

(A) 90% ASSET TEST:..............................................................................................................................................................27(B) 2 YEAR HOLD TEST:..........................................................................................................................................................27(C) 50% ASSET TEST:..............................................................................................................................................................27ANTI-STACKING RULE WRT 50% ASSET TEST S.110.6(1)(D).................................................................................................28WHAT IF EXCESS CASH IS “USED” IN AN ACTIVE BUSINESS?..................................................................................................28STEPS TO CONSIDER BEFORE A SALE, SO CAN USE CAPITAL GAIN EXEMPTION:......................................................................28S.110.6(14)(A): FIFO AND OPTION TIME...............................................................................................................................28

Hudon- Active business perimeters...................................................................................................................................28

CHAPTER 14: S.84.1 INDIVIDUAL SHARE GAINS DEEMED TO BE DIVIDENDS...................................................29

S.84.1(1): NON ARM’S LENGTH SALE OF SHARES CHRISTIAN: #1 CAUSE OF INSURANCE CLAIMS BY LAWYERS, ACCOUNTANTS 29S.84(1) (B) DEEMED DIVIDEND:..............................................................................................................................................29S.84(1)(A) PUC REDUCTION:..................................................................................................................................................29S.84.1(2)(A) AND (A.1):...........................................................................................................................................................29ANTI-AVOIDANCE RULE: NOT AT ARM’S LENGTH..................................................................................................................30

Queen v. McLarty (SCC) 2008- arm’s length test.............................................................................................................30

2

CHAPTER 15: ACQUISITION OF CONTROL RULES AND USE OF CORPORATE LOSSES.................................30

ORDINARY RULES ON USE OF LOSSES:....................................................................................................................................30LOSS UTILIZATION RULES:.....................................................................................................................................................30ACQUISITION OF CONTROL: ONLY LEGAL CONTROL..............................................................................................................30

Effect of Acquisition of Control on Losses (and other rules)............................................................................................31CANNOT Carryover of Net Capital Losses......................................................................................................................31Carry-over of Non-capital losses.......................................................................................................................................31Depreciable Property.........................................................................................................................................................31Effect on GRIP/LRIP:........................................................................................................................................................31Amalgamation (losses)......................................................................................................................................................32Wind up.............................................................................................................................................................................32

CHAPTER 16: S.55 INTER-CORPORATE DIVIDENDS DEEMED TO BE GAINS.....................................................32

S.55(2):....................................................................................................................................................................................32S.55(3) : EXCEPTIONS..............................................................................................................................................................32

Internal Corporate Reorg fits within exception in s.55(3):................................................................................................32S.55(2) EXCEPTION “SAFE INCOME”: - SAFE INCOME IS CONSOLIDATED............................................................................33

729 AB v. 729 AB...............................................................................................................................................................33VIH Logging......................................................................................................................................................................33

CHAPTER 18: BUTTERFLY TRANSACTIONS:...............................................................................................................34

BUTTERFLY REQUIREMENTS...................................................................................................................................................35BUTTERFLY ANTI-AVOIDANCE RULES...................................................................................................................................35CONTINUITY TEST:..................................................................................................................................................................36

3

Chapter One: “Base case”

tax rate to be applied to corp’s income:

“Base case” tax rate to be applied to the corporation’s taxable income to arrive at the tax owing by the corporation

% Section references and notes

start with (historical) federal tax rate 38 123(1)(a) - most recent, but still historical, base federal rate

subtract the federal “general rate reduction” 11.5 123.4(2) - this gives us the current base federal rate of 28% before making “room” for the provincial and territorial taxes - assume here the corporation’s income is basic “full rate taxable” income

subtract the “provincial abatement” 10 124(1) – makes “room” for the provinces and territories to impose their own tax rate on the corporation’s “taxable income earned in a province” – this gives us the net current federal rate of 18% where the corporation’s income is subject to provincial or territorial tax

add the base case provincial tax rate on the corporation’s income earned in the province

10 the provincial rate here is the base rate of 10.5% in subsection 14(2) the “BC Act”

thus, the total tax “base case” tax rate on the corporation’s taxable income in Canada is 26.5

the base corporate tax will vary across Canada

Base case for individual at top tax bracket: 29% (federal rate) s.117(2)(c) + 14.7% (provincial rate) s.4.1(1)(e) in BC Act = 43.7% combined fed-prov tax rate.

Gross-Up and Dividend Tax Credit

Policy: individual SH is given some credit for corp tax that is assumed to have been paid. Avoids double taxation. Corp’s taxes imputed to SH as if they had paid them, tax credit equal to the gross-up.

Ordinary dividends: Taxable dividends that aren’t eligible for the enhanced dividend tax credit. the corporation’s tax on the $100 at the base rate of 28% is

$28.50

the actual dividend paid to the shareholder, being the $100 less the $28.50 is $71.50

“gross-up” the dividend by ¼ of the actual dividend, or $17.88, for a total amount included in the shareholder’s income of

$89.38

shareholder tax at the top federal-provincial tax rate of 43.7% $39.06

deduct the “dividend tax credit”, being the 83.67% of the $17.88 gross-up, or $14.96

net shareholder tax $24.10

the total $52.60 of tax on $100 of income translates to an effective tax rate of 52.6%, or rounded to 53%

Eligible dividends: Taxable dividends paid from corp income taxed at the “base case” (GRIP) are eligible for higher dividend tax credit.

4

the corporation’s tax on the $100 at the base rate of 28.5% is $28.50

the actual dividend paid to the shareholder, being the $100 less the $28.50 is $71.50

“gross-up” the dividend by 44% of the actual dividend, or $31.46, for a total amount included in the shareholder’s income of

$102.96

shareholder tax at the top federal-provincial tax rate of 43.7% $44.99

deduct the “enhanced dividend tax credit”, which is equal to 94.26% of the gross-up, or $29.65

net shareholder tax $15.34

the total $43.84 of tax on $100 of income translates to an effective tax rate of 43.84%, or rounded to 44%

So with enhanced dividend tax credit the SH pays at 44% instead of at 53% absent the enhanced credit.

Dividend received by individual shdr must be included in shdr income by reason of: 12(1)(j) – include in income dividends paid by resident Can corp (as required by subdivision h)Subdivision h: 82(1)(a) – include in income taxable dividends [see (b)(i) below: also include gross-up] 82(1)(a.1) – include in income eligible dividends [see (b)(ii) below: incl. gross-up]

82(1)(b)(i) – for ordinary dividends [paid out of income taxed at low rate], include an additional amount equal to: ¼ (25%) of the dividend Then deduct a tax a credit of 83.67% of this gross-up amount

82(1)(b)(ii) – for “eligible dividends” [paid out of income taxed at base rate 28.5% (formula for GRIP determines amount in this pool s.89(1)], include an additional amount equal to:

44% of the dividend Then deduct a credit of 94.26% of this gross-up amount

NOTE: Individual shdr with no other source of income (p.12) Low rate of income tax applies Can receive up to approx $38,600 of dividends and pay no tax (fully credited, due to both personal tax credit, and fed & prov. tax

credits)

Inter-corporate dividends

tax-free b/w corporations: corp must include the dividend in income s.82(1)(a), but is entitled to a deduction equal to that amount s.112(1). Policy: there has already been corporate tax on the income, so to then tax the corporate SH would be “corporate double taxation.”

Chapter 2: Classification of Corporations (for Special Rates and Rules)

Private corporation:

s.89(1): resident in cda, not public corp, not controlled by one or more public corps. a) resident in Canada: s. 250(4) and s.250(5.1): corp deemed to be resident where: incorporated in Cda after 1965 or cont’d into

Cda after July 1994 from another jurisdiction. “resident” common-law: for corp incorporated outside of cda can be resident if its central management and control abides in

Cda. The place where the directors meet and guide the business, not necessarily where day to day business is run or where SH live.

s.250(5) even if resident under common-law test will be deemed not to be if deemed resident in another jurisdiction under tax treaty.

b) Public corporation: s.89(1): resident in cda, any class of it shares is listed on a designated stock exchange. It has elected to be a public corp, it used to be a public corp and hasn’t elected not to be.

c) Not controlled by one or more public corps: Legal “de jure” control generally is control over affairs and fortunes of the corporation by owning that number of shares that carries with it the right to elect the board of directors (usually 50%, varies by articles of corp.)

5

Canadian Controlled Private Corporation (CCPC)

s.248 and s.125(7): any private corp that is a “Canadian corporation” other than:

a corp that has any class of its shares listed on a designated stock exchange; a corp that is controlled directly or indirectly in any manner whatever (factual control) by: one or more non-residents, one or

more public corps; one or more corps with shares on stock exchange any combination of these or a corp that would be controlled (legal control) by one fictional person, if that person owned all shares of the corp that are in fact

owned by a non-resident, public corp or listed corp (the consolidation rule). Canadian corporation: s.89(1) resident in Canada and incorporated in Canada Controlled in…whatever: s.256(5.1): if a person or group has any direct or indirect influence that, if exercised, would result in

control in fact of the corporation. Exceptions: franchiser and arrangements whereby the main purpose is to govern the manner in which a business is conducted.

s.251(5)(b): deeming rule re: legal control:

if person has an absolute or contingent right to acquire shares that person is deemed to own those shares in ascertaining whether the corp is a CCPC.

Same with contingent or absolute right to control or reduce votes or redeem, acquire or cancel shares. CRA has administration exception for SH agreements that contain a shot-gun or right of first refusal clause.

Silicon Graphics: de facto control

Facts: CCPC prior to 1990, but then issued shares to US residents. Alias was a corp publicly traded in US and relatively widely held, no SH held more than 13% of its shares, but more than 50% of its shares held by non-resident persons with no evidence of any common connection among them. TP wanted to be a CCPC for SR&ED tax credits (plus small business subsidies)Held: in order for SH to be in control there must be coordinating their activities in some way, not just a numerical majority of foreigners. Thus, the definition is looking for someone who is actually legally controlling the corporation. R: de facto control requires the ability to effect a significant change in the BOD or its powers, or to influence in a very direct way the SH who otherwise have the ability to else the board. shareholders who have no ties to each other cannot do this, must be some connection/agreement/common mind merely >50% not good enough, MUST HAVE MOREElements of factual control : 1) clear direct influence to effect a significant change in BOD 2) influence powers of directors 3) influence SH who would chose directors.** NOTE: overruled by s.248(1)(c). “mythical person” created that holds all non-resident shares, regardless of connection between.

Transport Couture

- Old Mr. Couture liked trucks, started a company to play with trucks (TC1)- His kids liked business, and started a huge enterprise. (TC)- Minister argued that TC controlled TC1 as TC1 was TC’s only customer, and was in effective (de facto) control

o Because TC was entirely economically dependent on TC1, there was control like a pornography test, very subjective “you know it when you see it” type of test.

Held: Factual control found because of (1) economic dependence (2) operational control and (3) family relationship between the shareholders.

Taber Solids TCC- Control in fact s.256(5.1)

Facts: Taber solids reorganized into old Taber and Taber. B held all shares in OT, and K all shares in T. Previously equally owned Taber. Post-reorg, companies were split one rented the equipment from the other and one-let equipment to customers. Shares split between spouses accordingly. Court upheld Minister's finding that companies were associated corporations 40% of rent owed by new taber went back to old taber. Said separated the two businesses out to protect themselves from liability and protect some of their assets. Also said trust planning and there was tax advantage. They said would have done it or not whether there was tax advantage or not. Ct accepted that purpose wasn’t to get the tax advantage.Key Issue: person has control if they have the ability to (if they choose to exercise it) affect control of the companyTEST: Control factors: (rolled Transport Couture test into Silicon Graphics test)

operational control, (not the power to affect board powers, but the potential to make board decicions) family relations and econ independence to determine whether there is ability to effect a significant change in BOD. Don’t need to find evidence that influence was exercised just need to find that there was potential for influence of exercise. Also just has to be some influence at some time in the year, doesn’t need to be throughout the yr.

6

Held: Post-reorg, Ken, through Taber, still had direct and actual influence that resulted in control of OT, based on Ken's expertise with respect to the operational side of the business. Moreover, Ken could have carried on the equipment rental business through Taber w/o any need to rent equipment from OT due to his expertise. The converse was not true. OT was entirely economically dependent on Taber and the two companies were inextricably linked by family and contract .

Chapter 3: Special Rate for Active Business Income of a CCPC

Small business Rate:

Arrived at through entitlement to “small business deduction”:

Notes % Sections

start with the 38% rate 38 123(1)(a) and 123.2

apply the general rate reduction 0 123.4

deduct the provincial abatement 10 124

deduct the “small business deduction rate" 17 125(1.1)

net federal “small business rate” 11

Apply provincial small business rate 2.5 s. 16 BC

NET COMBINED 13.5

Note : no general rate reduction under s.123.4 b/c it only applies to full rate taxable income. Income eligible for small business deduction is excluded from “full rate taxable income.”

In BC the small business rate is 2.5% the combined federal/provincial tax is 13.5% for active business income eligible for the small business deduction under s.125.

Corporate Income that qualifies for the small business Rate

s.125(1): Small Business Deduction: federal small business rate is available for up to a max of $500,000 of net income from an active business carried on in Canada,

of a corporation that was throughout the year, a CCPC. o Note: Corporate bonuses: - “bonus down” pay bonus to decrease taxable income to below cap

Administrative Policy: CRA won’t challenge bonuses paid to decrease taxable corporate income on the basis of reasonableness

Exception: must be paid to a sh-employee involved in the day-to-day running of business (so will challenge income splitting)

Not necessary anymore, since deduction no longer goes away if income exceeds cap (just doesn’t apply to anything over).

s.125(1)(a)(i) and (ii): Can deduct the small business deduction rate from CCPC: a) (i) income from an active business, unless owned through

partnership and (ii) income earned through a specified partnership business and income that is otherwise earned from an active business.

Any corporate income above $500K is subject to base case corporate tax rate of 28.5%. Active business most be carried on in Canada, low threshold.

“Active Business”: s.125(7) Any business including AINT other than “specified investment business” or “personal services business.” [SIB and PSB

not eligible]. o note: section refers to a business, not to a corporation! (corporation can carry on multiple businesses)

“Specified Investment Business” s.125(7) business, principal purpose of which is to earn income from property including: interest (lending), dividends (stocks),

rents (holding real estate), royalties (holding copyrights and patents).

7

Exceptions: o a business leasing property other than real property, ORo a business that employs 5 or more full-time employees, ORo a corp associated with the corporation provides services that it would take 5 FT employees to do may qualify as

active business b/c excluded from SIB. Exceptions are b/c at some point investment businesses become sufficiently active to qualify as active businesses.

Lerric v. the Queen: 5 or more employees, not fractions.

Facts: co-owners in joint venture of real estate rentals. Argued that had 5 full-time employees by multiplying ownership by number of employees (ie. 17 employees, he owns >33% of shares = more than 5 FT employees employed for his benefit)Issue: definition of 5 or more FT employees?Held: s. 125(7)(e) says the corporation employs which connotes a direct relationship between the employer and employee. The co-owners employ the employees together. Act doesn’t contemplate fractional allocation of employees

Personal Services Business (PSB) s.125(7): Business that is:

o providing serviceso an individual (or related person) is a “specified shareholder” of the corp

“specified shareholder” = >10% of voteso BUT FOR corp, person could reasonably considered an EMPLOYEE of the person receiving the services

Exception:o Employes MORE THAN 5 full-time employees, OR

As per 489599 BC, this means at least 5 pt + 1 pto Where amount paid to corp for services is received by an associated* corporation

* Note: associated buinesses all have to share the small business deduction PSB expenses severely constrained by s.18(1)(p) to basically what an employee could deduct Look at distinction between independent contractor and employee (Wiebe Door) If small business then taxed at 13.5%. If PSB then taxed at 28.5% (general corporate rate). If not incorporated then taxed

at 43.7% (income rate)

S & C Ross Enterprises Ltd v. the Queen- PSB test.

Facts: specified SH’s corp provided services to CC whom he also worked for as VP and exec.Issue: PSB? If so, not eligible for small business deduction.Test: whether the incorporated employee would be an employee to the person services are provided for, but for the corporation? Held: Distinct services provided through corp, than he does through his employee role. Independent contractor, not employee not PSB. one “PSB” had to incur a risk of loss not something an employee would have to do therefore not PSB

489599 BC LTd: 5FT + 2PT= >5FT

5 FT and 2PT meets the test of more than 5 FT employees.

Specified partnership income s.125(7): partnership shares one 500K limit of the partnership’s active business income. Split the first 500K b/w partners on pro rata

partnership share. Must still be from Canadian active business.o NOTE: if the ‘partners’ can claim that they are actually a joint venture, then they can get the full $500k limit each

to be a true “joint venture,” they need to split all expenses (lots of work) CRA doesn’t usually challenge though.

Anti-avoidance Rules for partnerships: s.125(6.2) and s.125(6.3): o if there is factual control by non-resident or public corporation at any time in the year, there will be NO small business

deduction. This is trying to preserve the deduction for at partnership level similar to CCPC status. Factual control is if any partner exceeds 50%.

Income of the corporation for the year from an active business s.125(7): includes any income for the year “pertaining to or incident to that business” other than income for the year from a source in

Canada that is property.

8

If the income was actually incidental or necessary to the business then it’s active business income. Test: if removal of those funds would be detrimental* to keeping the corporation going then it’s necessary and not just excess property held by the corp for investment.

o Detrimental = “an inherently destabilizing effect”

Investment income from associated corporation deemed to be active business income (Source Preservation Rule): s. 129(6) deems certain income to be active business income. Deems property (rent, interest, royalties) income between

associated corporations to be active business income. Where rental or property income is paid by one corp to an associated corp it is active business income, rather than property income.

Business Limit Reduction s.125(5.1): small business corporate rate “phases out” for a CCPC that has debt and share capital employed in Canada greater than 15

million. Capital tax instead of income tax. For highly capitalized large entities.

Associated Corporations - note: can be related without being associated!!

small business limit must be shared among “associated corporations” and they must allocate a percentage of the limit amongst themselves, failure to do so and the limit might be nil or the CRA will allocate. s.125(2), (3), and (4).

Associated corporations s.256(1): (can be related without being associated!!) One corporation is associated w/ another in a taxation year, if at any time in the year:

(a) one corp is controlled “directly or indirectly in any manner whatever” “any manner whatever” = (legal or factual control) by the other corp.

(b) both corps controlled legal or factual by same person or “group of persons”(c) both corps controlled legal or factual by a person who is related to the person who controls the other corp AND

either of these people own 25% or more of any class of shares of the other corp, other than “specified class.” “Spec class” def’n = s. 256(1.1)(c)

(d) both corps controlled legal or factual by one person that is related to each member of a “group of persons” who controls the other corp. And the one person who controls the first corp owns 25% of shares of the other corp.

(e) both corps controlled by “related groups.” Each member of first group is related to each member of second group and one or more persons who are members of BOTH groups, either alone or together own 25% of shares of BOTH corps (Cross- shareholding).

Corporations associated through a third corporation s.256(2): connective rule. Where two corporations not otherwise associated are associated with the same third corporation, they

are deemed to be associated with another. The third corporation can elect out of any entitlement to the small business rate in s.125.

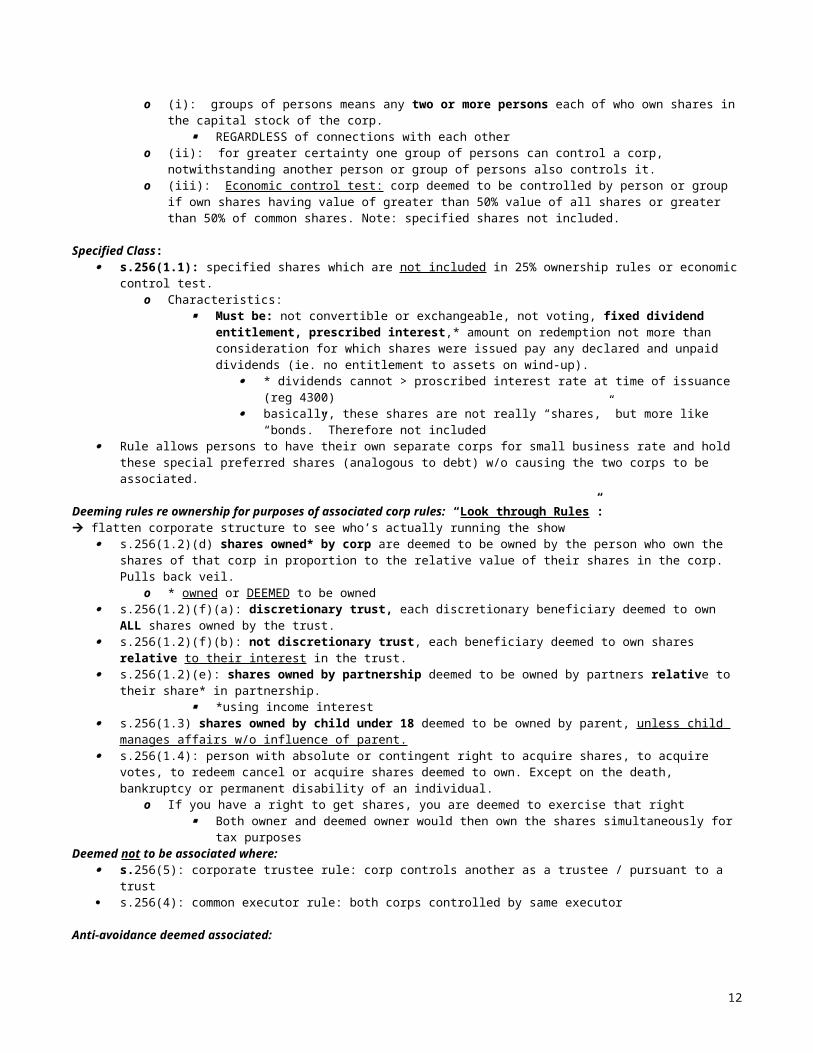

Group of persons s.256(1.2)(c):

o (i): groups of persons means any two or more persons each of who own shares in the capital stock of the corp. REGARDLESS of connections with each other

o (ii): for greater certainty one group of persons can control a corp, notwithstanding another person or group of persons also controls it.

o (iii): Economic control test: corp deemed to be controlled by person or group if own shares having value of greater than 50% value of all shares or greater than 50% of common shares. Note: specified shares not included.

Specified Class: s.256(1.1): specified shares which are not included in 25% ownership rules or economic control test.

o Characteristics: Must be: not convertible or exchangeable, not voting, fixed dividend entitlement, prescribed interest,*

amount on redemption not more than consideration for which shares were issued pay any declared and unpaid dividends (ie. no entitlement to assets on wind-up).

* dividends cannot > proscribed interest rate at time of issuance (reg 4300) basically, these shares are not really “shares,” but more like “bonds.” Therefore not included

Rule allows persons to have their own separate corps for small business rate and hold these special preferred shares (analogous to debt) w/o causing the two corps to be associated.

Deeming rules re ownership for purposes of associated corp rules: “Look through Rules”: flatten corporate structure to see who’s actually running the show

s.256(1.2)(d) shares owned* by corp are deemed to be owned by the person who own the shares of that corp in proportion to the relative value of their shares in the corp. Pulls back veil.

9

o * owned or DEEMED to be owned s.256(1.2)(f)(a): discretionary trust, each discretionary beneficiary deemed to own ALL shares owned by the trust. s.256(1.2)(f)(b): not discretionary trust, each beneficiary deemed to own shares relative to their interest in the trust. s.256(1.2)(e): shares owned by partnership deemed to be owned by partners relative to their share* in partnership.

*using income interest s.256(1.3) shares owned by child under 18 deemed to be owned by parent, unless child manages affairs w/o influence of parent. s.256(1.4): person with absolute or contingent right to acquire shares, to acquire votes, to redeem cancel or acquire shares

deemed to own. Except on the death, bankruptcy or permanent disability of an individual. o If you have a right to get shares, you are deemed to exercise that right

Both owner and deemed owner would then own the shares simultaneously for tax purposesDeemed not to be associated where:

s.256(5): corporate trustee rule: corp controls another as a trustee / pursuant to a trust s.256(4): common executor rule: both corps controlled by same executor

Anti-avoidance deemed associated: s.256(2.1): two corps otherwise not related deemed to be associated if:

o reasonable to conclude that one of the main reasons for their separate existence is to reduce amt of tax paid (ie. multiply the small business deduction).

Hughes Homes- no s.256(2.1) b/c had valid business purpose.

Facts: Had 2 corps, 50/50, then she incorporated her own and held 100% shares in it. Reduced shares in other corp to 10% so they were no longer associated. Mr. had home building business, new corp of Mrs. did design services for it (for a fee). Both claimed small business deduction. MNR attacked under s.256(2.1) purpose of split was to reduce taxIssue: was separate existence just to reduce tax?Held: Main reason was not to reduce tax, main reason was limiting liability. Had valid business purpose.- while Mr. and Mrs. ran complimentary businesses, they were adequately distinct to be considered separately.RATIO: s. 256(2.1) won’t apply if there is two separate activites being carried on in two corps.

Related Persons - note: DISTINCT FROM ASSOCIATED CORPS!!!!!!!

Some rules apply for associated corps rules and other rules for other sections of the Act too. if related then deemed not to be dealing at arm’s length. NOTE: related corporations are distinct from associated corporations. For associated corporations need to have the cross-

shareholding. Not necessary for related corps.O CAN BE RELATED WITHOUT BEING ASSOCIATED

Definition of Related Persons s.251(2)(a): blood relationship - s.251(6)(a) lineal up and down, brother, sister, grandma, parents marriage - s.251(6)(b) marriage partner and their blood relations common-law partnership - s.251(6)(b.1) common-law partner and their blood relations or adoption- s.251(6)(c) adopted family only vertically, not brothers and sisters.

Corporation and one person related s.251(2)(b): (i) person controls the corporation de jure (legal only) ,

o (ii) person is member of “related group” that controls the corp, o (iii) person related to person in (i) or (ii).

Two corporations related s.251(2)(c)(i) if controlled (legal only) by the same person or group of persons. (Group of persons: not defined for related

provisions, don’t use associated provision definition. Silicon Graphics: Beyond simple mathematical majority. Need common connection such as voting agreement, agreement to act in concert, business or family relationship.)

s.251(2)(c)(ii): if each controlled by person, and those people are related. s.251(2)(c)(iii): one corp controlled by a person and that person is related to any member of a “related group” that controls the

other corp.

Related Group: s.251(4): group of persons EACH member of which is related to EVERY other member.

Corps related through a third Corp:

10

s.251(3): if 2 corps are related to the same corp then deemed to be related for the purposes of s.251(1)&(2)

Control by related groups, options etc: s.251(5):

(a) a related group that is in position to control corp is deemed to be a related group that controls the corp. (b) Contingent rights: If person has absolute or contingent right to acquire shares, votes or cancel shares that person is deemed

to own. (c) If person owns shares in 2 or more corps, deemed to be related to self.

Chapter 4: Special Refundable Tax System for Investment Income of Certain Private Corporations - RDTOH

Policy goals of refundable tax:

prevent deferral of tax by earning the investment income inside a corporation; and permit integration of tax when comparing the earning of investment income personally or inside a corporation.

Investment Income Except Dividends from Other Canadian Corporations

Special tax on: “aggregate investment income” (AII): s.129(4) which is excess of capital gains over allowable capital losses from Canada

(taxable capital gains) And “income from a source that is property”: s. 129(4)(a)

o INCLUDE: income from specified investment business (SIB) of the CCPC (carried on in Can) [eg. Rental apt building, franchising biz]

s.129(4)(b)o EXCLUDE: income from property that is incident to or pertains to an active business of the CCPC (b/c included in

small biz deduction) o EXCLUDE income from “property that is used or held” principally to gain or produce income from active business…

Exclude dividends from other Cdn corps

NOTE: s.129(1.2) Anti Avoidance rule against purchasing corporations to access their tax accounts

Shamita Inc –income from active business test

Issue: was the investment (interest) income active biz income… does it qualify as “property used or held for purpose of gaining or producing income from an active biz” Held: no—the relation between the income from property & the activities of the biz not close enoughIndication of close relation: losing the income from property has a “decidedly destabilizing effect…” on the income from biz – need interdependence between the income from property and the income from the biz

Tax Rate that applies to CCPC’s Aggregate Investment Income:

start with initial base federal tax rate 38 123(1)(a) - most recent, but still historical, base federal rate.

general federal rate reduction 0 s.123.4(1) (b)(iii) of the definition of “full-rate taxable income” backs-out of the income qualifying for the general rate reduction a CCPC’s “aggregate investment income”.

11

subtract the “provincial abatement” (10) 124(1) – recall this makes “room” for the provinces and territories to impose their own tax rate on the corporation’s “taxable income earned in a province” – this gives us the net current federal rate of 28% before the “special” additional tax on aggregate investment income.

add the special tax:

that is the refundable tax

6.67 123.3 - this is the special additional tax applies to a CCPC’s aggregate investment income. This gives us the net federal rate of 34.67% -

provincial tax 10 the corporate rate in British Columbia.

Total initial corporate tax on a CCPC’s aggregate investment income

44.67 Note: This is the tax rate before any refund out of the RDTOH account below.

Dividend refund to private corporation s.129(1): Minister refunds “dividend refund” amt equal to the lower of: (i) 1/3rd of all taxable dividends paid by the CCPC that yr

and (ii) the CCPCs Refundable Dividend Tax on Hand Account (RDTOH) at end of yr.o For ever $3 in dividends, $1 of RDTOH is refunded

Definition of RDTOH s.129(3): A-B. A = 26 2/3% of the CCPC’s aggregate investment income for the current year + taxes payable under part iv for current yr on

dividends from other corps + RDTOH account at end of preceding year. B = CCPC’s dividend refund for its preceding year.

$100 Aggregate investment income (AII) in one yr$44.67 44.67% tax on AII$54.83 Remainder of AII$26.67 RDTOH account at end of year one$82.00 Div to SH in yr two (54.83 +26.67)$26.67 Payment of Div triggers refund from RDTOH account$18.50 Net tax on AII: 45.17(initial tax)- 26.67 (refund)= 18.50$20.38 SH gross-up = Div (81.50) x ¼ $101.88 SH gross up (20.38) + Div (81.50)$44.52 Tax at top rate 43.7% x $101.88-$17.05 Deduct div tax credit= 83.67% x SH gross up ($20.38)$27.47 Individual Tax$45.97 Total tax= 18.50 (corp tax) + 27.47 (indiv tax)** table not correct

Private Corporations that receive dividends from other Canadian Corporations

Aggregate investment income excludes any dividends from other Cdn corps that are deductible under s.112 in computing the corp’s taxable income. not subject to any Part I tax.

This potential to receive tax free dividends under Part I tax spawns many rules, such as refundable Part IV tax. What is effective tax rate on a dividend from a Cdn corp received from a SH- focusing on actual dividend received and actual tax

paid?

Base Rate Small Business “AII”Actual dividend 71.50 86.50 81.50Actual tax paid 15.33 29.15 27.47Effective Tax 21.44% 33.7% 33.7%**not right?

Effective tax rate on a dividend is same on all income (other than eligible dividends: eligible for enhanced div credit) paid from income taxed at top corporate rate (GRIP): 33.7%

If private company pays dividend to other private company they will receive them and get the deduction in s.112(1) so there is no Part I tax payable at all on the dividends until the private co pays them to an individual.

This leads to potential for unlimited deferral of tax on dividends. So need Part IV tax.

12

First Aspect of Part IV Tax: not connected

Part IV prevents the deferral of tax on dividends when received by corps rather than individual, by imposing 33.33% refundable tax on dividends, which would otherwise be tax free under Part I.

Assessable dividends s.186(3): taxable dividend that is deductible under s.112 Part IV tax is based on: (a) 1/3 assessable dividends from non-connected corporations and (b) an amt equivalent to the recipient’s

portion of the dividend refund to assessable dividends from connected corporations.

“Not connected” 186(1)(a): if payor and recipient are not connected then recipient liable for Part IV tax on its taxable dividends from payor. Pays the part IV tax into the RDTOH account.

33.33% tax on “assessable dividends” received by private corp or a subject corp.

Add the taxes due under Part IV into RDTOH account. Payment of dividend by corp will trigger refund out of RDTOH account per s.129(1).

Dividends received by Private Co 100

Part IV tax paid (and addition to the RDTOH account) (33.33)

Dividend paid by Private Co 100

Refund to the Private Co out its RDTOH account below, subject to the 129(1)(a) limit of 1/3rd of the dividend paid by the Private Co

33.33

Private Co’s net tax on dividends received. 0

slight deferral on non-eligible dividends (.38%) and significant interim cost on eligble dividends (11.89%).

Second Aspect of Part IV tax: Connected Corps

“Connected with” s.186(2) and (4): Control test: private or subject corp has de jure* control (50%) of paying corp or non-arms length control of

it (related: question of fact). OR ten% votes and value test : private or subject corp has >10% of voting shares and more than 10%** of value of all shares in paying corp.

o * no de facto controlo ** bright line test 9.99% doesn’t count.

s.186(1)(b) applies when paying and receiving corps are connected, and the dividend paid to the receiving corp triggers a refund to private corp out of RDTOH account.

Example: Private Can. corp A pays dividend to private corp B: when the dividend paid triggers a refund to corp A out of its RDTOH account – that same amount is owed in tax by corp B (and then also added to B’s RDTOH account) so the whole tax payment and RDTOH is shifted from A to B purpose of this part of the Part IV tax : “preserve” the tax effect of a prior addition to the RDTOH account of payer corp that

is connected so when corp A does NOT have an RDTOH account (eg. Treats all income as active biz, not agg invest income), there will

be no Part IV tax for the connected corps.

$100 Private A Co’s rental income its “AII”$45.17 Initial tax on AII $26.67 Addition to Private A co’s RDTOH account$81.50 Dividend paid to Private B co$26.67 Dividend refund to Private A co from RDTOH, triggered by div payment to Private B co.$18.50 Net tax paid by Private A co. (45.17-26.67= 18.50)$26.67 Part iv tax payable by connected Private B (s.186(1)(b))$81.50 Div to indiv. SH of Private B co$26.67 Div refund to Private B co (s.129(1)(a))0 Net tax paid by Private B co after refund

Anti-avoidance rule: RDTOH s.129(1.2): Dividends deemed not to be taxable dividends: prevents a corp from obtaining a div refund if the share on which div

was paid was acquired, in a transaction, one of the main purposes of which was to enable the corp to get the dividend refund.

13

Canwest Capital- s.129(2.1) test

Div refund paid w/out corresponding part iv tax (fell within exception) when dividends paid back out. CRA applied s129(2.1) to get at those dividends. Test: one of the main purposes of the transaction was to obtain a div refund.Held: business plan was executed for business reasons, not to avoid paying part iv tax. Didn’t know at time that would be free of part iv tax couldn’t be on of the main purposes or purpose at all.

Capital Dividend Account (CDA)- tax free portion of capital gains

CDA account: the untaxed ½ of capital gains go into this account and are then available to be paid as tax free dividends out of the corporation b/c wouldn’t be subject to tax if SH realized gain personally.

the other ½ of the gain is the taxable capital gain that was included in AII.

Capital dividend account: s.89(1): Account includes:

o (a) tax free one half of capital gains (less the ½ of capital losses), o (b) inter-corp capital dividends, o (c) tax free portions of gains from eligible capital property, o (d) life insurance proceeds, o (e) tax free portion of capital gains flowed through trusts.

s.83(2) must file an election to pay a tax free capital dividend before paid, must be private co if elect too high, the dividend is greater than CDA, a penalty tax of 60% is payable on the excess punitive tax.

s.184(3) and (4): possible to make further election to treat the excess as normal taxable dividend, then penalty is removed. The election must be made by both corp and SH

Anti-avoidance: trying to stop trading in CDAs. eg./ co with no assets to pay dividends, trying to transfer the CDA to another co in order to pay out div to SH.

s.83(2.1): if acquired in transaction where one of main purposes was to receive capital dividend then deemed to be received by SH and paid by corp as taxable div and not as capital dividend.

Chapter 5: General Rate Income Pool (GRIP) and Eligible Dividends

GRIP and Eligible Dividend System

Account, with purpose to track eligible dividends.Private corps have GRIPS, but these create no other preferential tax treatment. Includes $ from FA’s.All dividends paid by private corporations are NOT eligible dividends, unless paid out of GRIP account

dividends paid can be either, so long as eligible dividends paid is LESS THAN GRIP account at end of year.

s.89(1): eligible dividends: Eligible dividends paid by CCPC are paid from GRIP: (income pool where private co paid general rate tax) All public co dividends are eligible, except if they have an LRIP account. Can’t pay eligible divs until LRIP account exhausted. Eligible for enhanced div tax credit w/ gross-up on 44%, SH ends up paying less tax.

s.89(14): dividend becomes eligible by designation of corporate payor, must be in writing. for public co: notice on website is sufficient for private co: must be written notice contemporaneous w/ time div is declared.

s.89(1): GRIP: income for the year before losses carried back A-B A= full rate taxable income

o Amount that CCPC was paying in tax at the general corporate rate.o Includes previous year’s GRIP + dividends from subsidiaries, foreign affiliates, etc.

B= reduction for losses carried back

Backs out income eligible for small business deduction and AII income. cumulative account only CCPCs have GRIP

14

not CCPC then have LRIP, not computed at yr end, determined at any time a dividend is paid. LRIP is low rate income pool. Public Co must pay out all LRIP before can pay out eligible dividends out of GRIP. NOTE: GRIP can be NEGATIVE.

Private Corps MUST NOTIFY SHAREHOLDERS when paying out eligible dividends.

Excessive Eligible Dividend Designations

s.89(1) Excess eligible dividend designation: Have to pay 20% Part III.1 tax if have excess eligible dividend. Anti-avoidance rule , if pay dividends in excess of GRIP and its reasonable to consider that one of the main reasons of paying

eligible dividend was to artificially maintain or increase GRIP. And if anti-avoidance rule applies then 10% add’l tax.

s.185.1(2): rather than paying the 20% tax, corp can elect that the excess amount be treated as an ordinary taxable dividend rather than eligble dividend.

SH must concur within 30 months, and corp has 90 days to make the election after Part III.1 tax assessed.

Chapter Six: Shareholder Benefits and Shareholder Loans

s.15(1): Benefit conferred on shareholder: any benefit conferred on SH that is not in form of dividend, return of capital or salary. Included in TP’s income as ordinary income and not as dividend no gross-up and no dividend tax credit.

No deduction to corp under s.18(1)(a) b/c not for purpose of earning income, no integration. Purposeful b/c it’s a penalty.

Computing value of benefit: not settled law

Methods:- Cost of benefit (ie. cost of cabin, cost of jet skis)- Cost of rent (ie. how much it would cost to rent for period used / available to use)- Cost of capital (ie. what it cost the corp. in terms of lost investment opportunities to give the benefit)

Hinkson: FMV outlay for cabin

Personal use of corp’s cottage. CRA: value of the benefit was the saving by TP in the capital outlay otherwise necessary to use cabin. Not just the FMV of rent for period that cabin used.Most accepted method: what it costs the corp to be able to provide the SH w. the benefit.

Pillsbury: benefit on SH qua SH

The benefit on the SH has to be conferred on the SH qua SH.

Youngman FCA- equity rate of return/ cost of capital- fancy house.

Got corp to buy land and build fancy house, said it would make development more attractive. Paid $1100/month, and gave corp 100K interest free loan. Valued: corp’s equity in house, return on investment (equity x prescribed rate) {what the corp would get if had invested that money elsewhere at prescribed rate}+ corps payment of mortgage taxes= gross benefit – rent paid= net amt of benefit.But TP had lent the 100K interest free, so the net amt of benefit would have been swallowed up by interest owed to SH anyways, so no net benefit.Benefit = (value of home) x (prescribed rate) : as the TP couldn’t prove

Fingold FCA- florida condo: cost of capital

Got corp to buy condo in Florida, 1.8 million, 2.2 million in renos= 4 million asset. Minor business use, only 1 over-night guest.TJ: b/c found there was a business purpose only had to pay for actual use not for tying up business asset. FCA: Tj incorrect assessment. Should use cost of capital approach: what corp has given up to put the money into the asset for the SH’s benefit. Assessment on equity rate of return by minister was correct valuation method.

15

Consider what SH would have had to pay if got it from arm’s length person.

Fingold approach: Back to basics1) What is the benefit?2) What is the proper valuation?

*note: when interest rates are very low (as they now are), the cost of capital approach is no longer an adequate valuation of the benefit.

Franklin- bookkeeping error, no actual benefit

Didn’t tell corp that his loan to corp had been repaid. Never more taken out of corp than was owed to him. Minister said if hadn’t caught him, eventually he would have taken more out beyond what was owed. FCA: No actual benefit to SH, never used incorrect financials to get benefit.

Shareholder Loan

s.15(2): Shareholder debt: where a person is SH, connected w. SH, member of partnership or beneficiary that is SH and gets a loan from corp must include it in income. No deduction for corporation.Exception: loans to corps and loans to partnerships not included.

s.15(2.1): persons connected with a SH: for purposes of (2) connected with means don’t deal at arm’s length (related or question of fact: degree of influence or control, circumstances, directing mind, separate interests).

Exceptions to loan inclusion

s.15(2.6): Repayment within one year: (2) doesn’t apply to loan repaid after 1 yr from end of taxation year of year when received. BUT if it is a series of loans then it does get included in tax for the year received. Rationale: if not included then could just keep doing 1 yr bridge loans that would never be included.

Meeuse, - succession of loans not series for s.15(2.6)

Co had yr end in April. Borrowed 20K in Feb, repaid in Aug. Had car loan repaid within 1 yr, another 20K to erect storage building, repaid within one yr. Crown: 20k repayment wasn’t bona fide was just part of seriesHeld: no evidence of sham or artificiality, bona fide loan repaid within 1 yr. Mere succession of loans not sufficient to equal series for s.15(2.6). Must be some sort of connection b/w the loans w/out explanation.

s.15(2.3): Ordinary Lending Business: (2) doesn’t apply when loan made in OCB and bona fide arrangements made for repayment w/in reasonable time.

s.15(2.4): Certain employees: (2) doesn’t apply for loans to employee for house, shares or car for employment. Two conditions: onus to show loan b/c employee not b/c SH and credible arrangements for repayment. (Note: Can’t be specified employees: 10% SH or non-arm’s length from that person)

s.15(2.5): Certain trusts: doesn’t apply for certain employee share ownership trusts.

Repayments.20(1)(j): if repay loan that was previously included in income then can deduct it from income in the year repaid.

Deemed Benefit: Interest

s.15(9): if SH gets loan from corp under s.80.4(1) and the interest paid is less than prescribed rate than deemed to have received a benefit.

Two exceptions: s.80.4(3)(a): not deemed interest benefit if: (1) OCB is lending money, 2) loan NOT made by reason of SHing or employment, 3) parties at arm’s length, s.80.4(3)(b): not deemed benefit if the loan is included in income, b/c then already captured.

Deemed Interest:

16

- s.80.5 deemed interest amounts under s.80.4 are deductible to the extent that the borrowed money is used for income-earning purposes under s.20(1)(c) or s.8(1)(j).

Dividends in kindo s.89(1) taxable dividend means any kind. o s.82 Taxable dividends received: takes into account the amt of the dividend in kind. No tax difference, just need to figure out

FMV of dividend in kind.

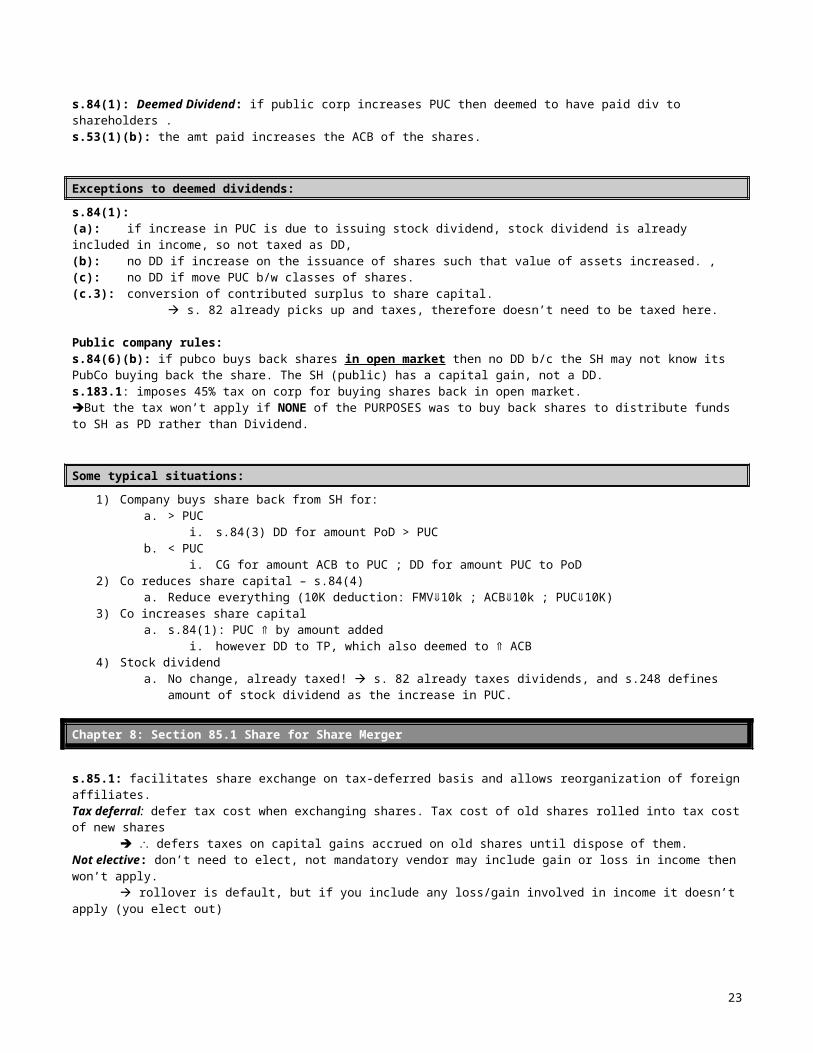

Chapter 7: Share Capital and Deemed Dividend

s.84(3): Deemed dividend on redemption or cancellation of sharesCompany deemed to have paid dividend equal to an amount by which: the amt paid to the SH on the buy-back exceeds the PUC of the shares acquired by the co.Deemed dividend= Amount paid- PUC.Rules attempt to make transactions carried out in capital form, taxed in income form.

s.89(1): PUC per share: (a): amt of paid up capital / number of shares. (b)(iii): Share capital of the class for corporate law purposes. (issue price or par value if pv shares).* If it’s a BCBCA company, then par value = PUC.* if CBCA, look at the stated capital.** otherwise, look at the consideration paid to the COMPANY for shares

* PUC is a class concept later s/h purchasing new shares for increased price will increase the per-share PUC.

s.54(j) Proceeds of disposition: does not include the amount that is deemed to be a dividend under s. 84(2) or (3).

Two calculations: 1) deemed dividend, 2) capital gain-less the deemed dividend

1) deemed dividend= Amt paid- taxPUC of share.2) Capital gain= PD(amt paid-deemed div)- ACB

s.84(2): Distribution on winding up: Amt that distribution exceeds PUC it’s a deemed dividend and not included in POD. Same calculation as in s.84(3) b/c the share is disposed of. s.84(4) Reduction of PUC: Corp can reduce PUC and distribute to SH. No disposal of shares. Tax free to extent that it doesn’t exceed the reduction in PUC of the class.

s.53(2)(a)(ii): the amt paid on a reduction of capital reduces the ACB of the share to the SH unless the amt is deemed to be a dividend. (makes sense b/c haven’t disposed of the shares and now with the “refund” they actually cost the SH less).s.40(3) if ACB goes negative a capital gain is realized by the SH.

s.84(4.1): Deemed Dividend on reduction of PUC: for public co only, any amt paid on reduction of PUC is a DD. Policy: to prevent disguised dividends.

s.84(1): Deemed Dividend: if public corp increases PUC then deemed to have paid div to shareholders .s.53(1)(b): the amt paid increases the ACB of the shares.

Exceptions to deemed dividends:

s.84(1):(a): if increase in PUC is due to issuing stock dividend, stock dividend is already included in income, so not taxed as DD, (b): no DD if increase on the issuance of shares such that value of assets increased. , (c): no DD if move PUC b/w classes of shares. (c.3): conversion of contributed surplus to share capital.

s. 82 already picks up and taxes, therefore doesn’t need to be taxed here.

Public company rules:

17

s.84(6)(b): if pubco buys back shares in open market then no DD b/c the SH may not know its PubCo buying back the share. The SH (public) has a capital gain, not a DD. s.183.1: imposes 45% tax on corp for buying shares back in open market. But the tax won’t apply if NONE of the PURPOSES was to buy back shares to distribute funds to SH as PD rather than Dividend.

Some typical situations:

1) Company buys share back from SH for:a. > PUC

i. s.84(3) DD for amount PoD > PUCb. < PUC

i. CG for amount ACB to PUC ; DD for amount PUC to PoD2) Co reduces share capital – s.84(4)

a. Reduce everything (10K deduction: FMV10k ; ACB10k ; PUC10K)3) Co increases share capital

a. s.84(1): PUC by amount addedi. however DD to TP, which also deemed to ACB

4) Stock dividenda. No change, already taxed! s. 82 already taxes dividends, and s.248 defines amount of stock dividend as the

increase in PUC.

Chapter 8: Section 85.1 Share for Share Merger

s.85.1: facilitates share exchange on tax-deferred basis and allows reorganization of foreign affiliates. Tax deferral: defer tax cost when exchanging shares. Tax cost of old shares rolled into tax cost of new shares

defers taxes on capital gains accrued on old shares until dispose of them.Not elective: don’t need to elect, not mandatory vendor may include gain or loss in income then won’t apply.

rollover is default, but if you include any loss/gain involved in income it doesn’t apply (you elect out)

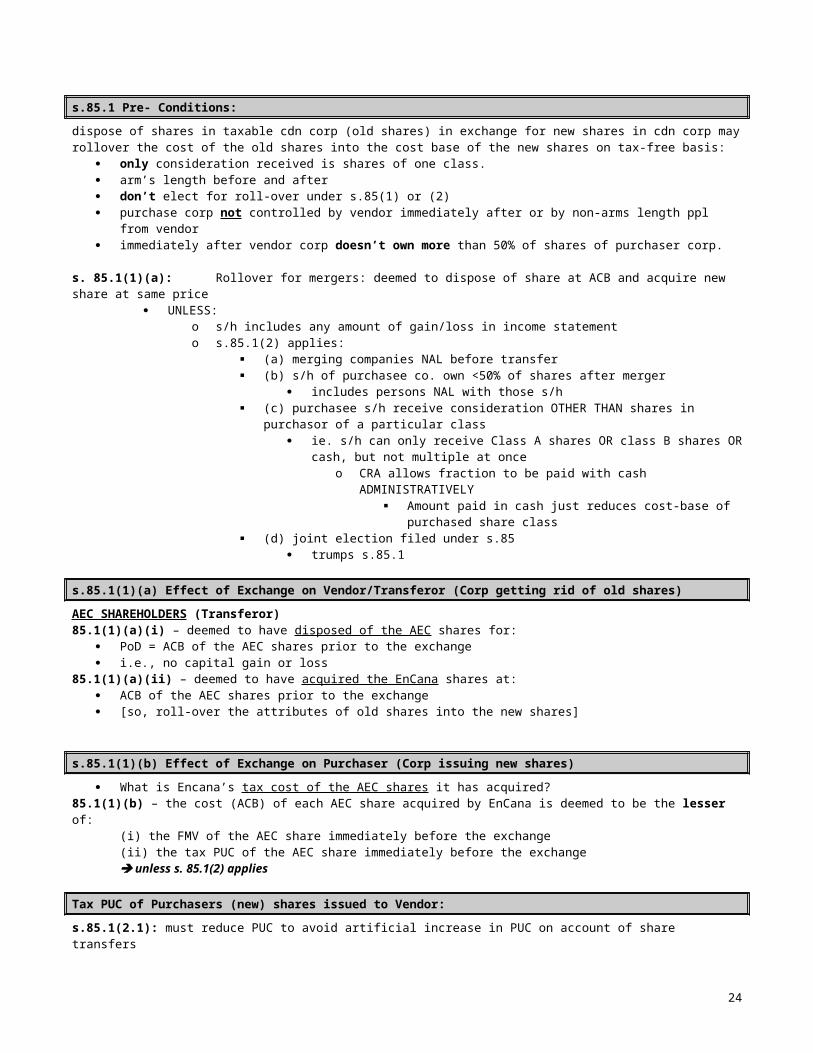

s.85.1 Pre- Conditions:

dispose of shares in taxable cdn corp (old shares) in exchange for new shares in cdn corp may rollover the cost of the old shares into the cost base of the new shares on tax-free basis:

only consideration received is shares of one class. arm’s length before and after don’t elect for roll-over under s.85(1) or (2) purchase corp not controlled by vendor immediately after or by non-arms length ppl from vendor immediately after vendor corp doesn’t own more than 50% of shares of purchaser corp.

s. 85.1(1)(a): Rollover for mergers: deemed to dispose of share at ACB and acquire new share at same price UNLESS:

o s/h includes any amount of gain/loss in income statemento s.85.1(2) applies:

(a) merging companies NAL before transfer (b) s/h of purchasee co. own <50% of shares after merger

includes persons NAL with those s/h (c) purchasee s/h receive consideration OTHER THAN shares in purchasor of a particular

class ie. s/h can only receive Class A shares OR class B shares OR cash, but not multiple at

onceo CRA allows fraction to be paid with cash ADMINISTRATIVELY

Amount paid in cash just reduces cost-base of purchased share class

(d) joint election filed under s.85 trumps s.85.1

s.85.1(1)(a) Effect of Exchange on Vendor/Transferor (Corp getting rid of old shares)

AEC SHAREHOLDERS (Transferor)

18

85.1(1)(a)(i) – deemed to have disposed of the AEC shares for: PoD = ACB of the AEC shares prior to the exchange i.e., no capital gain or loss

85.1(1)(a)(ii) – deemed to have acquired the EnCana shares at: ACB of the AEC shares prior to the exchange [so, roll-over the attributes of old shares into the new shares]

s.85.1(1)(b) Effect of Exchange on Purchaser (Corp issuing new shares)

What is Encana’s tax cost of the AEC shares it has acquired?85.1(1)(b) – the cost (ACB) of each AEC share acquired by EnCana is deemed to be the lesser of:

(i) the FMV of the AEC share immediately before the exchange(ii) the tax PUC of the AEC share immediately before the exchange unless s. 85.1(2) applies

Tax PUC of Purchasers (new) shares issued to Vendor:

s.85.1(2.1): must reduce PUC to avoid artificial increase in PUC on account of share transfers Capital Stock: TAX PUC OF ENCANA SHARES ISSUED TO AEC SHDRSPurpose of “PUC grind”:

Tax PUC of purchaser shares issued to the transferor must be reduced to equal the tax PUC of the vendor shares before the exchange

The “grind” effectively means that the increase in PUC as a result of the issuance of shares by purchaser is limited to the PUC of the transferor’s shares

PUC grind is done to eliminate any artificial increase in tax PUC of the new “corporate group” – tax PUC is supposed to reflect what company received by issuing shares and in reality they only received the tax PUC from the vendor’s old shares in a straight exchange

85.1(2.1) - Opening PUC of EnCana shares = value of new shares issued by EncanaTax PUC of EnCana shares = opening amount – (X-Y)

X = the value of the new shares issued Y = the tax PUC of the AEC shares acquired

Merged Tax PUC = APUC + BPUC + (to A corp. share capital - t in A PUC from new shares)** should = 0

Chapter 9: Section 85 Transfers: Transfer of Property to a Corporation

s.85(1) Preconditions:

TP disposes of “eligible property” s.85(1.1) defines. Note: (f) “inventory” real estate CANNOT be transferred. To a taxable cdn corp in exchange for consideration that includes shares (must include) and parties elect (jointly!) in prescribed form to have the section apply

Elected Amount

s.85(1)(a): Elected Amount: deemed to be Taxpayers PD and Corporations cost of the property

s.85(1)(f)(g)(h): Cost of Consideration Received by Taxpayer: Agreed amt allocated first to: 1) NSC which is FMV 2) next to P/S (Agreed amt- NSC), 3) next to C/S (Agreed amt- NSC-P/S).

Example: $50 cash and 1000 C/S (FMV $950), Elected amt= $100Allocated: NSC= $50, C/S=$50.Shares: FMV=$950, ACB=$50. Rollover gain of $900.

Agreed Amount Limitations:

19

s. 85(1): (b): must treat NSC as PD cannot elect below FMV of NSC.

o [Treats NSC as actual payment can’t defer consequences]. (c): Cannot elect above FMV of property transferred

o [Stops ppl from triggering capital gain, to use capital losses]. (c.1):Cannot elect below tax cost of property transferred. [Stops ppl from triggering loss]. (e) & (e.1): For depreciable property can’t elect lower than lesser of:

o (i): UCC of whole class, o (ii): original cost of particular property, o (iii): FMV of the particular property.

[Stops from triggering artificial loss].

“tax cost”s. 248(1) defines as ACB for capital property, cost for inventory

s.85(5) Depreciable Property: (a) capital cost to transferor is deemed to be capital cost to transferee, (b) excess is deemed to have been deducted by the transferee.[Ensures that any built-in recapture isn’t converted into capital gain when transferee disposes of property].

s. 85(1)(d): “eligible capital property”*: can elect the lesser of: (i) 4/3 of the taxpayer's cumulative eligible capital in

respect of the business immediately before the disposition

(ii) the cost to the taxpayer of the property, and (iii) the fair market value of the property at the time

of the disposition, the amount agreed on by the taxpayer and the corporation in their election in respect of the property

shall, irrespective of the amount actually so agreed on by them, be deemed to be the least of the amounts described in subparagraphs 85(1)(d)(i) to 85(1)(d)(iii);

“Eligible Property” s.85(1.1) –

o (a) a capital property (other than real property, or an interest in or an option in respect of real property, owned by a non-resident person);

o (b) a capital property that is real property (or option on) owned by a non-resident insurer where that property and the property received as consideration for that property are designated insurance property for the year;

o (c) a Canadian resource property; o (d) a foreign resource property; o (e) an eligible capital property; (intangibles, non-depreciably bus assets, goodwill, and other purchased, non depreciable intangibles)o (f) an inventory [other than real property(or interest in/option for)]o (g) a property that is a security or debt obligation used by the taxpayer in the year in, or held by it in the year in the course of, carrying on the business of insurance or

lending money, other than (i) a capital property, (ii) inventory, OR (iii) where the taxpayer is a financial institution in

the year, a mark-to-market property for the year; o (g.1) where the taxpayer is a financial institution

in the year, a specified debt obligation (other than a mark-to-market property of the taxpayer for the year);

o (h) a capital property that is real property, an interest in real property or an option in respect of real property, owned by a non-resident person (other than a non-resident insurer) and used in the year in a business carried on in Canada by that person; or

(i) a NISA Fund No. 2, if that property is owned by an individual.

s.248(28) Can’t have two taxes on same thing, so wouldn’t have capital gain and recapture on same amount.

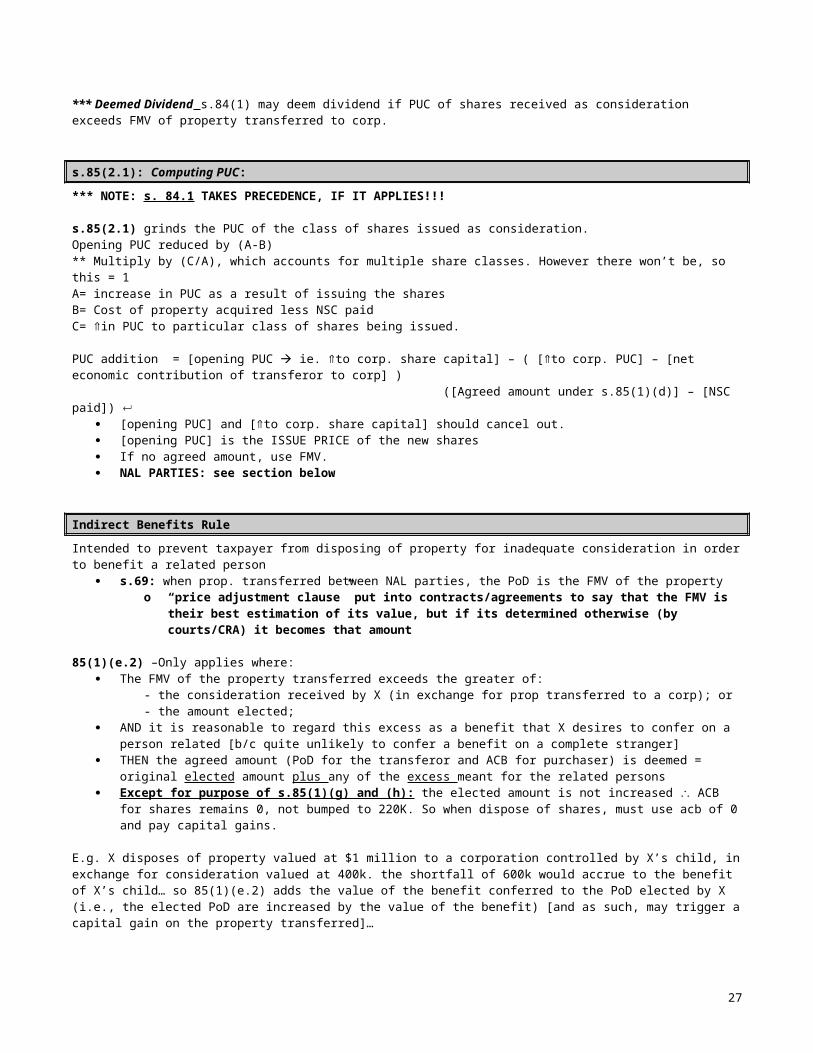

*** Deemed Dividend s.84(1) may deem dividend if PUC of shares received as consideration exceeds FMV of property transferred to corp.

20

s.85(2.1): Computing PUC:

*** NOTE: s. 84.1 TAKES PRECEDENCE, IF IT APPLIES!!!

s.85(2.1) grinds the PUC of the class of shares issued as consideration. Opening PUC reduced by (A-B) ** Multiply by (C/A), which accounts for multiple share classes. However there won’t be, so this = 1A= increase in PUC as a result of issuing the sharesB= Cost of property acquired less NSC paidC= in PUC to particular class of shares being issued.

PUC addition = [opening PUC ie. to corp. share capital] – ( [to corp. PUC] – [net economic contribution of transferor to corp] ) ([Agreed amount under s.85(1)(d)] – [NSC paid])

[opening PUC] and [to corp. share capital] should cancel out. [opening PUC] is the ISSUE PRICE of the new shares If no agreed amount, use FMV. NAL PARTIES: see section below

Indirect Benefits Rule

Intended to prevent taxpayer from disposing of property for inadequate consideration in order to benefit a related person s.69: when prop. transferred between NAL parties, the PoD is the FMV of the property

o “price adjustment clause” put into contracts/agreements to say that the FMV is their best estimation of its value, but if its determined otherwise (by courts/CRA) it becomes that amount

85(1)(e.2) –Only applies where: The FMV of the property transferred exceeds the greater of:

- the consideration received by X (in exchange for prop transferred to a corp); or- the amount elected;

AND it is reasonable to regard this excess as a benefit that X desires to confer on a person related [b/c quite unlikely to confer a benefit on a complete stranger]

THEN the agreed amount (PoD for the transferor and ACB for purchaser) is deemed = original elected amount plus any of the excess meant for the related persons

Except for purpose of s.85(1)(g) and (h): the elected amount is not increased ACB for shares remains 0, not bumped to 220K. So when dispose of shares, must use acb of 0 and pay capital gains.

E.g. X disposes of property valued at $1 million to a corporation controlled by X’s child, in exchange for consideration valued at 400k. the shortfall of 600k would accrue to the benefit of X’s child… so 85(1)(e.2) adds the value of the benefit conferred to the PoD elected by X (i.e., the elected PoD are increased by the value of the benefit) [and as such, may trigger a capital gain on the property transferred]…

Effect is that SH realizes higher CG on transfer to co. (b/c deemed elected amount higher than ACB) So: can’t get less value in the new shares than you gave up in the old shares

To cover this risk, standard practice to employ a “price adjustment clause” says that the redemption value is the parties’ best estimate of the value. If the CRA subsequently evaluates at a different value,

then the redemption value of the shares will be adjusted

Freeze Transaction:

Value of property is trapped into another form of property that is frozen at current value, usually P/S. Freezing allows any future gain to be taken up by new C/S SH

Example: FMV 720K business. Client wants to freeze his interest so transfers the business assets to the corp in exchange for fixed rate shares. So assets are frozen at the value of the fixed rate shares, here 590K p/s.Client can take back amt up to tax cost w/o consequence, here tax cost is 130K, so elected amount is 130K.FMV=720k, tax cost= 130K, p/s=590K FMV Elected amt=130K promissory note.So cost is 130K NSC and shares=0.

Accrued gain in business is reflected in the shares: A-B

21

Puc Grind= 590- (720-130)590-590Reduce PUC by=0Client ends up with 130K promissory notes and shares redeemable for 590K b/c that is the PUC that can be taken out.

Chapter 10: Section 86 and 51 Share Exchanges

s.86 Exchange of shares by SH in course of Re-org of Capital

s.86 defers any CG/loss which would otherwise be recognized during reorganization.