tangible property regulations “what tax professionals need ... · strategic discussions. tax...

TRANSCRIPT

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Tangible Property Regulations“What Tax Professionals need

to Know for Tax Year 2015”

AWSCPA 33rd Annual Conference

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Journal of Accountancy Article

“Clearly, the new repair regulations pose considerable compliance risks both for CPAs and the businesses they advise.”

Journal of Accountancy Feb 2014Implementing the New Tangible Property Regulations Christian Wood. J.D.

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

© 2015

Our goal is to share better ideas on the Implementation of the Tangible Property Regulations…FAST.

Steps to the Solution:

1. Analyze economic Impact of 2014 Repair Regulations– Are your clients Compliant? – Have you made them aware of their tax savings?

2. Predict impact of the regulations for their property portfolio

3. CSSI provides the calculations of the repair regulations for your implementing in the tax record.

– Provides for compliance.– Provides economic benefits – Cash Flow.– Coordinated with you, the CPA

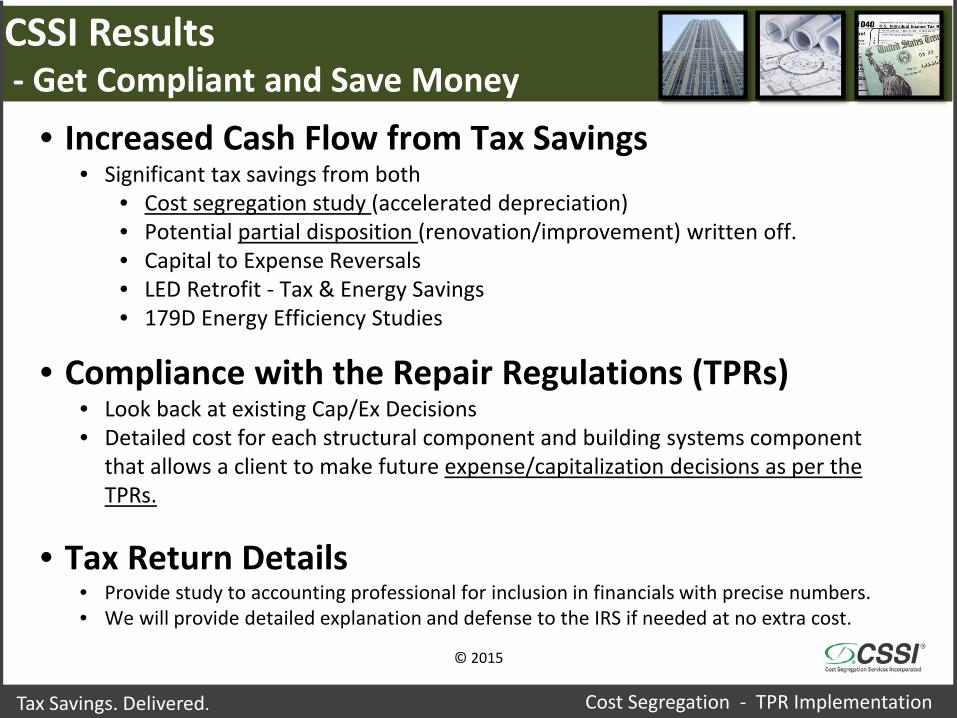

CSSI Results - Get Compliant and Save Money

Tax Savings. Delivered. Cost Segregation - TPR Implementation

© 2015

• Increased Cash Flow from Tax Savings • Significant tax savings from both

• Cost segregation study (accelerated depreciation) • Potential partial disposition (renovation/improvement) written off.• Capital to Expense Reversals• LED Retrofit - Tax & Energy Savings• 179D Energy Efficiency Studies

• Compliance with the Repair Regulations (TPRs)• Look back at existing Cap/Ex Decisions• Detailed cost for each structural component and building systems component

that allows a client to make future expense/capitalization decisions as per the TPRs.

• Tax Return Details• Provide study to accounting professional for inclusion in financials with precise numbers. • We will provide detailed explanation and defense to the IRS if needed at no extra cost.

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Latest Update with TPRs

–2 New Rev Procs issued–New 3115s and related

instructions

Eric WallaceTPRToolsandTemplates.com © 2015

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Preparing for the coming tax season relating to TPRs

–Fixing 2014 /Filing 2015–Most missed opportunities–What Deductions are still

available from past years?Eric WallaceTPRToolsandTemplates.com © 2015

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Preparing for the coming tax season relating to TPRs

–Can I still go back and fix it?–Looking Forward to Filing 2015–De minimis Safe Harbor prep

Eric WallaceTPRToolsandTemplates.com © 2015

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Preparing for the coming tax season relating to TPRs

–TPRs are based on a Cost Segregation Depreciation model

Eric WallaceTPRToolsandTemplates.com © 2015

Explaining Cost Segregation

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

The process of analyzing and identifying commercial building components that are eligible for accelerated depreciation providing a significant tax benefit for the taxpayer.

Personal Property is Segregated from Real Property

$50k to $80k per $1 Million in CostWorks on $250k buildings

Explaining Cost SegregationInput calculation to the Regulations

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Explaining Cost Segregation

Straight-Line• Hamburger

Cost Segregation• 2 All Beef Patties• Special Sauce• Lettuce • Cheese• Pickles• Onions on a • Sesame Seed Bun

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Explaining Cost Segregation

Straight-Line• Hamburger $3.99

Cost Segregation $3.99• 2 All Beef Patties $1.99• Special Sauce $0.15• Lettuce $0.18• Cheese $0.45• Pickles $0.18• Onions on a $0.29• Sesame Seed Bun $0.75

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Explaining Cost Segregation

Straight-Line

• Looks at the building as a Whole

• Structural Building Components

• Depreciated over 39yrs (27.5yrs)

• Real Property Only

Cost Segregation

• Identifies Parts and Pieces of the building

• Non-Structural Building Components

• Depreciated over 5, 7 & 15 years

• Personal Property & Real Property

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

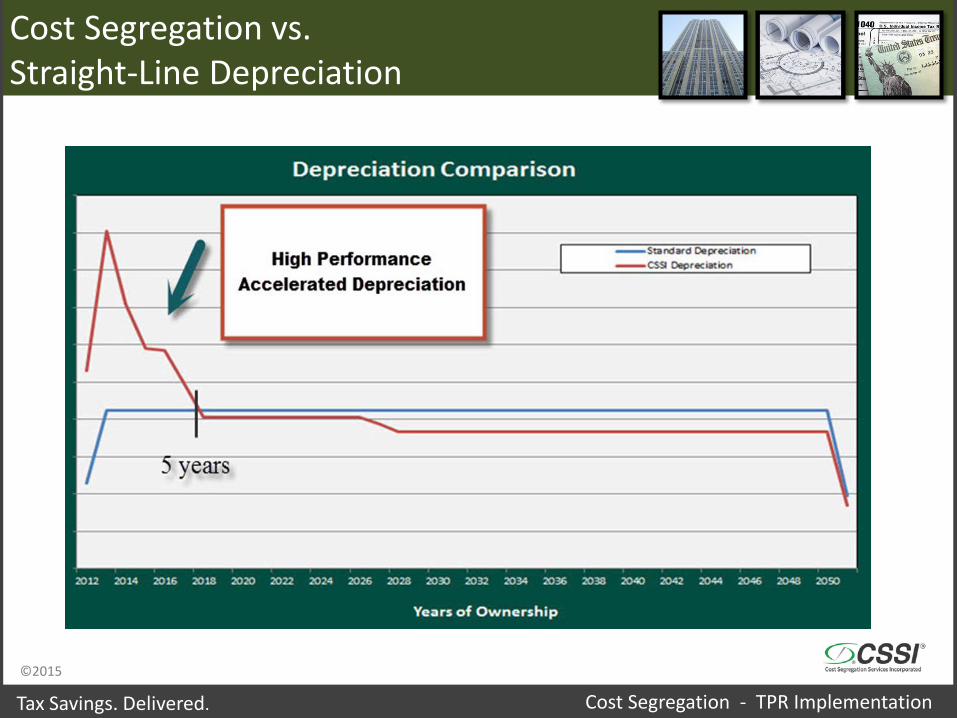

Cost Segregation vs.Straight-Line Depreciation

Tax Savings. Delivered. Cost Segregation - TPR Implementation

DispositionsBenefit to your Client

Section 168• Includes:– Sale or Exchange– Retirement– Physical Abandonment– Destruction– Transfer to supplies or scrap– Involuntary conversion– Retirement of a structural component

of (or improvement to) a building.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

DispositionsBenefit to your Client

Ability to write off assets that are no longer in use with Partial Disposition Election• Renovations• Remodels • Replacements• Abandoned in Place• Common Items – Roofs, HVAC, Electrical

©2015

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Dispositions

• Know the Value of what went into the Dumpster.

• Relative to the value that your client paid for the building.

• Disposed of as a Partial Disposition.

• Write down to the basis of the property in current year.

• Looking for Improvements or Repairs on Depreciation Schedule.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

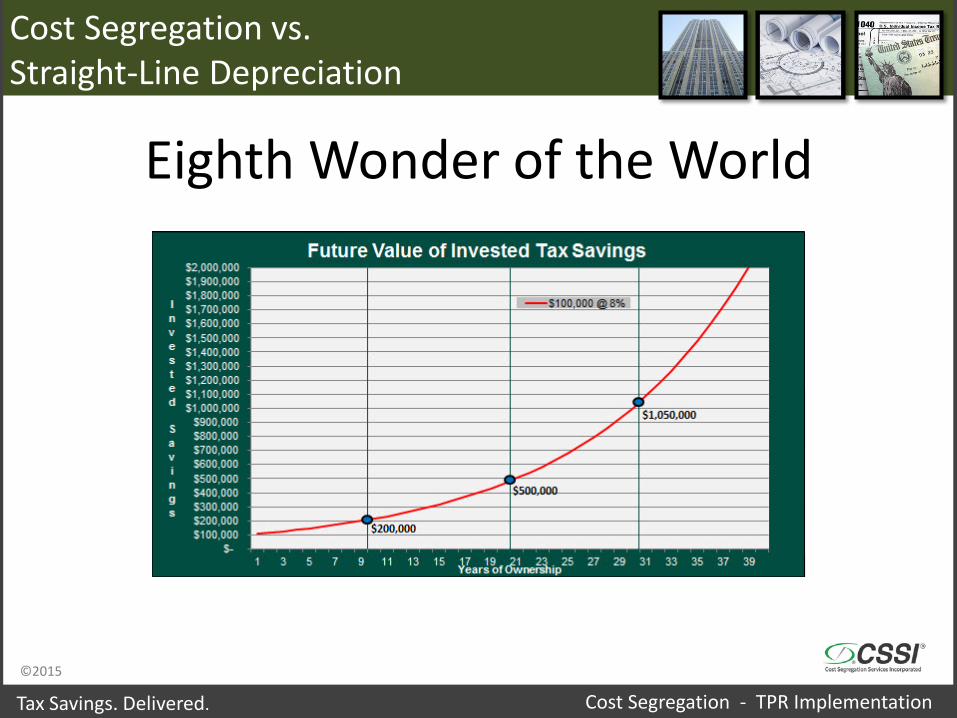

Cost Segregation vs.Straight-Line Depreciation

Eighth Wonder of the World

Financial Results of Cost Segregation and Partial Disposition

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Climate Control Self-Storage $3,150,750Tax Savings Benefit: $ 164,682ROI: 32:1

Office Condo $324,000Tax Savings Benefit: $ 30,609ROI: 14:1

Office Warehouse $5,246,900Tax Savings Benefit: $ 312,687ROI: 33:1

Cost Segregation Partial Disposition

Auto Dealership

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Unit of Property 1.263(a)(3)(i)Functional Interdependence Standard

• The Unit of Property determination is generally based upon the functional interdependence standard.

• Components of property are functionally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer.

• But there are…

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Unit of Property 1.263(a)(3)(i)Functional Interdependence Standard

• Special Rules for • Buildings- Each building is a Unit of

Property• Plant Property• Network Assets• Leased buildings and leased property• Improvements to Property

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Listed Building Systems

• The Building U of P Determination Is Based Upon §1.48-1(e)

• Each building and its structural components (as defined in §1.48-1(e)(2)) is a single unit of property.

• A building structure consists of the building (as defined in §1.48-1(e)(1)), and its structural components other than the building systems.

• Each of the following structural components including the following components constitutes a building system that is separate from the building structure, and to which the improvement rules (RABI) must be applied.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Listed Building Systems

• (1) Heating, ventilation, and air conditioning (“HVAC”) systems

• (2) Plumbing systems• (3) Electrical systems• (4) All escalators• (5) All elevators• (6) Fire-protection and alarm systems• (7) Security systems for the protection of the building and

its occupants• (8) Gas distribution system• (9) Or within the building systems or building structure,

any item that performs a major and discrete function, i.e. doors, windows, toilets, cabinetry, lighting fixtures etc.

STRATEGIC DISCUSSIONS

Tax Savings. Delivered. Cost Segregation - TPR Implementation

“Latest Developments”

• What’s new that I need to know about

• Good News

Eric WallaceTPRToolsandTemplates.com © 2015

Latest Updates - Great News

Tax Savings. Delivered. Cost Segregation - TPR Implementation

De minimis SH raised to $2500

• Rev Proc. 2015-86• Non-AFS Taxpayer limit raised• Capitalization Policy Changes• Best Practice – Put it in writing• Sample Capitalization Policy

Eric WallaceTPRToolsandTemplates.com © 2015

Latest Updates - Great News

Tax Savings. Delivered. Cost Segregation - TPR Implementation

What to do to Implement DMSH – Action Steps

• Need Capitalization Policy• Alert Clients with Plan of Action• Documentation of Action– Best Practices• Required to be in place before Jan 1, 2016

Eric WallaceTPRToolsandTemplates.com © 2015

Latest Updates - Great News

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Change in 3115 Form

• Takes effect December 15, 2015• New Form, new instructions • Clear that the IRS is expecting many more

TPR method changes• There are many new answers and

information that must be suppliedEric WallaceTPRToolsandTemplates.com © 2015

Latest Updates Great News

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Rev Proc 2015-56 DCN 221 & DCN 222 November 20, 2015

• Safe Harbor Method for Restaurant and Retail Refresh-Remodeling Cost

• Requires Audited Returns, 20%, Restaurant or Retail, new GAA

• 25% of qualifying remodel-refresh cost are Capitalized and remaining are Deductible as Repairs and Maintenance…can be Retroactive

© 2015

Focus

Tax Savings. Delivered. Cost Segregation - TPR Implementation

What should Tax Professionals focus on to prepare for the coming tax season?

• “Going Back in Time”• Adopt the TPRs if they have not.• Opportunities to look for in the portfolio for

client deductions• Year 2015 & Future Years

Eric WallaceTPRToolsandTemplates.com © 2015

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

TPRs

Applying the Improvement Standards

The RABI Rules

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

TPRs

R - Restoration

A – Adaptation

B – Betterment

I – Major Improvement

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Cost to Improve Tangible PropertyImprovement Standards

Capitalize…Amounts paid for new building or improvements 1.263(a)-3.

- that increase value of property

- bring property to new or different use

- return of original condition

Expense... Amounts paid for incidental repairs and maintenance of property 1.263 (a)-1.

- keeps in ordinary operating conditionRepair / Refresh

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

When to Capitalize or Expense? 1. The Expense Decision!

Must Capitalize ifAn Improvement (RABI) or Major Expenditure

1. Improvement = Restoration, Adaptation, Betterment, Improvement (RABI) 2. Major Expenditure = More than 30%-35% of the REPLACEMENT cost of the

building system, structural component or unit of property (40% of Roof Replaced = Capitalize)

A capital expenditure is generally considered to be a more permanent increment in the longevity, utility, or worth of the property.

Must Expense if = Repair• If the expenditure does not materially increase capacity, productivity, efficiency, strength,

quality or improve output of the building system, structural component, or Building(Unit of Property) it must be expensed.

A repair keeps the building structure and building system in ordinary and efficient operating condition.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

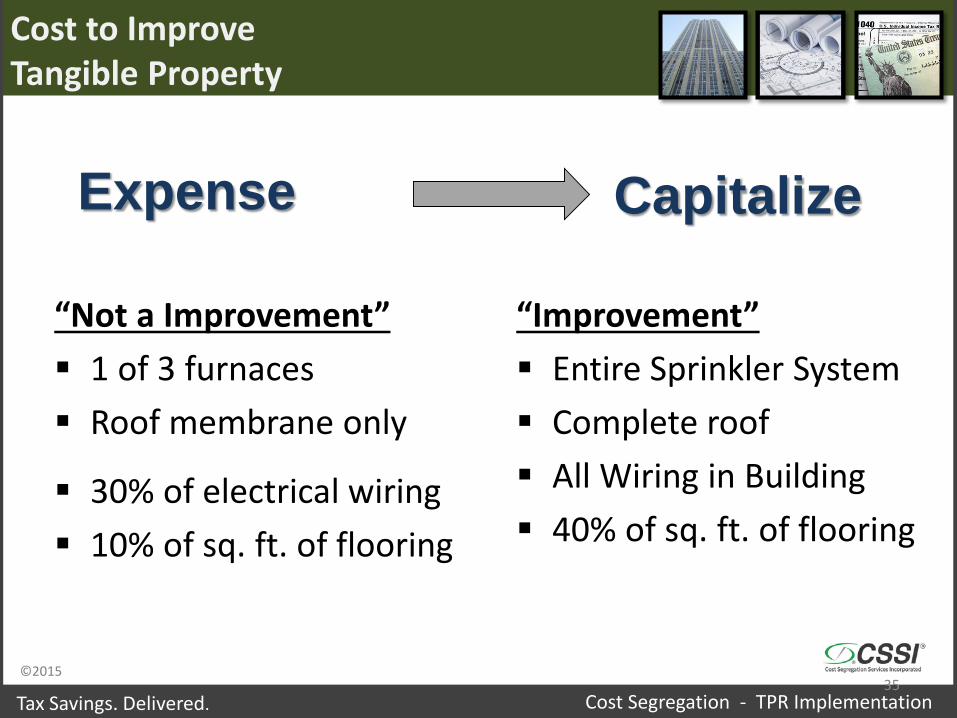

Capitalize

Cost to Improve Tangible Property

“Not a Improvement” 1 of 3 furnaces Roof membrane only

30% of electrical wiring 10% of sq. ft. of flooring

“Improvement” Entire Sprinkler System Complete roof All Wiring in Building 40% of sq. ft. of flooring

35

Expense

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Cost to Improve Tangible Property

Compare future Invoices to:• Building Systems Valuation• Building Structural Components Valuation• Components perform Major and Discrete

Function within Systems and Structure• Any Large Physical Portion of the Building

Cost of Items

One of above %

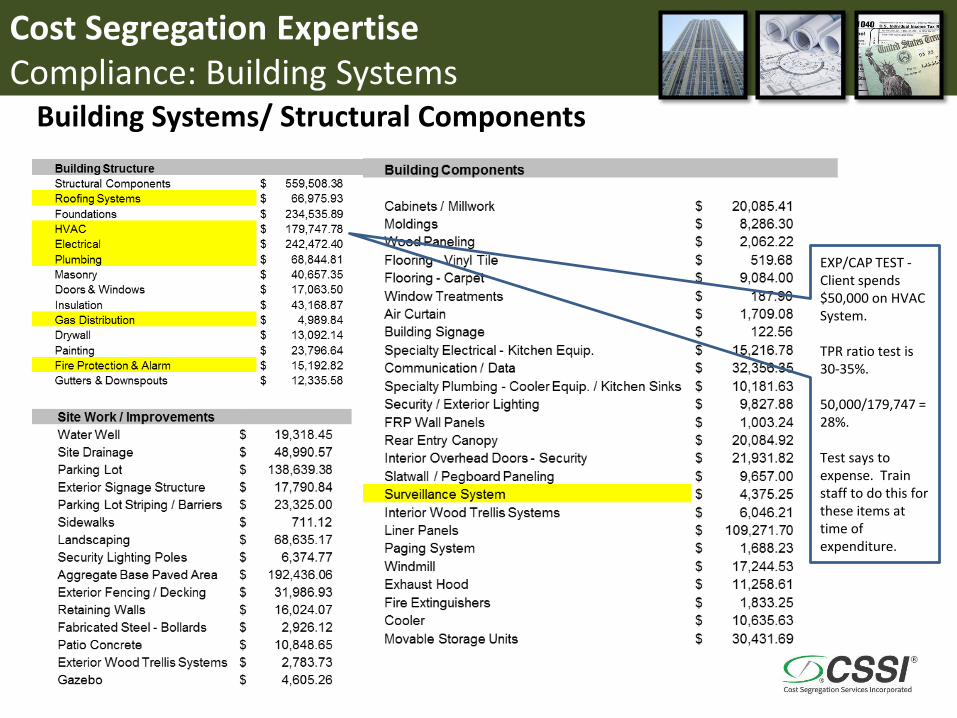

Cost Segregation Expertise Compliance: Building Systems DefinitionBuilding Systems/ Structural Components

EXP/CAP TEST -Client spends $50,000 on HVAC System.

TPR ratio test is 30-35%.

50,000/179,747 = 28%.

Test says to expense. Train staff to do this for these items at time of expenditure.

Tax Extender Advantage

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Tax Extenders and Cost Segregation

– Bonus Depreciation at 50% in 2016-2017.– Section 179 extended permanently– New Items with a Depreciable Life less than

20yrs qualify.– New 5,7,15 year life items all qualify.– Can look back at past years.– New Construction or Remodels

Eric WallaceTPRToolsandTemplates.com © 2015

Going Back in Time

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Opportunities for Write Offs in your portfolio from past years.

• Gutted Building Removal Cost• Buildings in service with

Improvements/Repairs over years.• Buildings in service with Tenant/Leasehold

Space Improvements• State what your Unit of Property is

Eric WallaceTPRToolsandTemplates.com © 2015

Going Back in Time

Tax Savings. Delivered. Cost Segregation - TPR Implementation

“Can I still go back and reverse Capitalized Items to Expense?”

Eric WallaceTPRToolsandTemplates.com © 2015

Historical Capitalized Items3. Capital Reversal to Expense Decision!

Tax Savings. Delivered. Cost Segregation - TPR Implementation

The regulations, require you to go back to your depreciation schedule — and your repair costs — for all prior years and ask one key question:

“Under the new regulations, would these expenditures have to be capitalized or could they be expensed?”

Look back at items you may have capitalized since you owned the building and expense them in the current tax year.

This creates economic opportunities. Cash Flow!

Let CSSI calculate and implement this for you in partnership with

Eric Wallace, CPA –Foremost Expert on the TPRs in the US.

Adopting the TPRs

Tax Savings. Delivered. Cost Segregation - TPR Implementation

“Can I still go back and reverse Capitalized Items to Expense?”

• How did the Taxpayer file in 2014?• Did Taxpayer adopt the TPRs?

– Filed a 3115– Put a statement of adoption on the return under

2015-20– If TPRs adopted…no changes can be made to past

years before 2014Eric WallaceTPRToolsandTemplates.com © 2015

Adopting the TPRs

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Small Taxpayer can go back and scrub if:– Did not file the 3115s with 481(a) – Did not file the “0” 481a– Used Rev Proc 2015-20

• Those with and without an adoption statement.

Large Taxpayer can go back and scrub if:– Did not file the 3115s to adopt TPRs

Eric WallaceTPRToolsandTemplates.com © 2015

Capital to Expense Reversal Examples $$

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Eric WallaceTPRToolsandTemplates.com © 2015

The CSSI Study

Multiple Story Apartment Complex (Purchased in 1993)Cost $1.1 millImprovements over years -$4 mill, $160k, $2.7mill, $70k, $26K, $900k

Created -481(a) adjustments of $1,387,016.00@ 40% Tax rate

Resulted in Tax Savings of $554,000

Going Back in Time Example

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Eric WallaceTPRToolsandTemplates.com © 2015

The CSSI Study

Office Building Converted to Hotel11 story (Purchased in 2000)Cost $1.6 millMultiple Improvements over years-$10 mill, $1.2 mill, $41K, $30K

Created -481(a) adjustments of $3,138,017@ 34% Tax rate

Resulted in Tax Savings of $1.1 million

Year 2015 & Future Years

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Questions to ask your client• Did you have any renovations or remodels of your

building? - Dispositions

• Did you remove or throw anything away? - Remaining Basis can be written off.

• Removal Cost breakout on invoice? -No documents? Cost study can provide

• Tenant Improvements?• Unit of Property issues?

Eric WallaceTPRToolsandTemplates.com © 2015

Year 2015 & Future Years

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Examples of Client Situations

• Did you have any renovations or remodels of your building? Dispositions– Apartment Complex– Office Building moved walls– Addition to a building– Strip Center Remodel

Eric WallaceTPRToolsandTemplates.com © 2015

Year 2015 & Future Years

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Examples of Client Situations• Did you remove or throw anything away?

Remaining Basis can be written off.• Removal Cost breakout on invoice?

– Changed out a Roof– Changed out HVAC units– Upgraded Wiring, Plumbing– Cost Segregation Study can provide clarity with

our without supporting documentation. Eric WallaceTPRToolsandTemplates.com © 2015

Year 2015 & Future Years

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Examples of Client Situations

• Tenant Improvements?– Old Tenant leaves– Space Remodeled– New Client build out.– Who pays to the build out?

Eric WallaceTPRToolsandTemplates.com © 2015

Year 2015 & Future Years

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Unit of Property Issues• Multiple Building Sites • Basis for buildings• Invoice Decisions – Expense or Capitalize?• Building Systems Baseline

Eric WallaceTPRToolsandTemplates.com © 2015

5 Action Items for Year 2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

1. Written Capitalization Policy in place2. File 3115s that did not get filed3. Scrub Schedules for CAP/EX Reversals4. Establish Units of Property

– Building Systems– Multiple Buildings assigned Correct Basis

5. Review Portfolio for Cost Segregation Opportunities. CAP/EX opportunities

Eric WallaceTPRToolsandTemplates.com © 2015

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Information NeededTo Run Preliminary Analysis

• Depreciation Schedule is best

• What type of Building?• What did they pay for the building? (without the land)

• When did they purchase it?• Have there been any major renovations or

remodels?• Send this info to Rep that invited you to the call.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

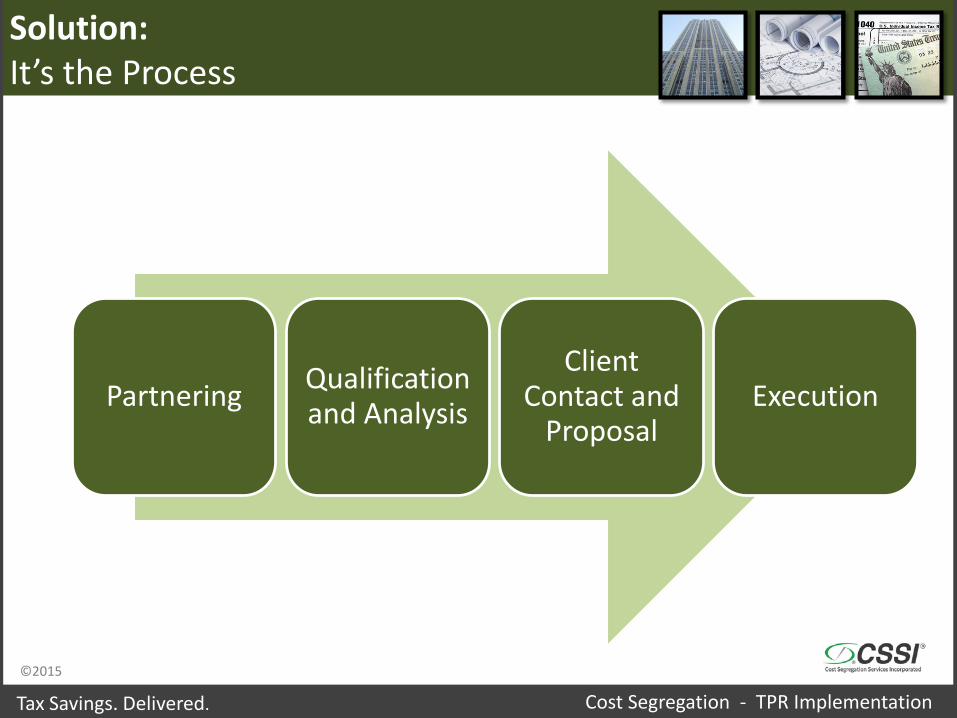

Solution:It’s the Process

Partnering Qualification and Analysis

Client Contact and

ProposalExecution

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Solution:.. It’s the Process

Ease of ComplianceCPA: 1-2 hrs per client

Timely completion

Client Satisfaction100%: Grateful for effort to save taxes

Additional RevenueFor Tax

Professional

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Resources

Education Resources:

• CSSI – www.CSSIstudy.com

• CCH Seminars– https://www.cchgroup.com/training-and-

support/cch-seminars

• Eric Wallace– www.TPRtoolsandtemplates.com

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Use the CSSI ExperienceTax Savings. Delivered.

Performing Engineering-based Studies for over 14 years, National capability, 15,000 Studies completed across the U.S., always on-time.

Qualify the tax savings estimates within 48 hrs. for your client.

Full Engineering-based Studies completed in 4-8 weeks.

Perform CAP/EX Reversals with Eric Wallace

Use CSSI as your engineering-based service provider for your clients.

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

CSSI Today – Your Calculation Experts

• Cost Segregation Study• Tangible Repair Regulations

– Consulting for Spending Analysis for Capital or Expense Decision – Partial Disposition Study– Building Systems Definition Study– Capital Reversal To Expense Study

• LED– The economic solution for sustainable energy savings– Related write downs and partial dispositions

• Section 179D Energy Credit Analysis• R&D Tax Credit Analysis• VIPCO

– Forensic Business Spending Analysis

©2015

Tax Savings. Delivered. Cost Segregation - TPR Implementation

Thank You

Let us provide pre-analysis for your clients.

David H. [email protected]

832.971.2885

Rick [email protected]

281.798.9580