tamil nadu infrastructurepre fund … · final report april 2018 internal ... as the client) is an...

TRANSCRIPT

TAMIL NADU INFRASTRUCTURE FUND

MANAGEMENT CORPORATION PRE-FEASIBILITY STUDY FOR TAMIL NADU COMMERCE HUB Located on Anna Salai, Chennai

,

FINAL REPORT

APRIL 2018

Internal Ref: 2018_MAR_ADV_CHE_27

1

The Tamil Nadu Infrastructure Fund Management Corporation Ltd [TNIFMC], (hereinafter referred to

as the client) is an asset management company formed under the Tamil Nadu Infrastructure

Development Board (TNIDB).

Under the vision 2023 of GoTN and decongestion of residential areas in Chennai city - An iconic,

modern commercial office space development christened ‘Tamil Nadu Commerce Hub’ (hereinafter

referred to as the subject development) has been envisaged to accommodate public and private sector

entities.

The same is proposed to be developed on two land parcels along Anna Salai:

Land Parcel 1 (Subject Property 1) – Comprises for 2 non-contiguous land parcels located on either

side of Anna Salai, Nandanam admeasuring approx. 9.65 acres

Land Parcel 2 (Subject Property 2) – Comprises for 1 contagious parcel located of Anna Salai,

Teynampet admeasuring approx. 1.4 acres

In this context, the Client has appointed CBRE to advice on the ‘Pre-Feasibility Study’ for the envisaged

development with a view to opine on the optimal product mix, potential demand of commercial

development and devise development strategies for the same.

A. PROJECT INTRODUCTION

2

The key objectives for the envisaged development (Tamil Nadu Commerce Hub) are:

B. KEY OBJECTIVES

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 3

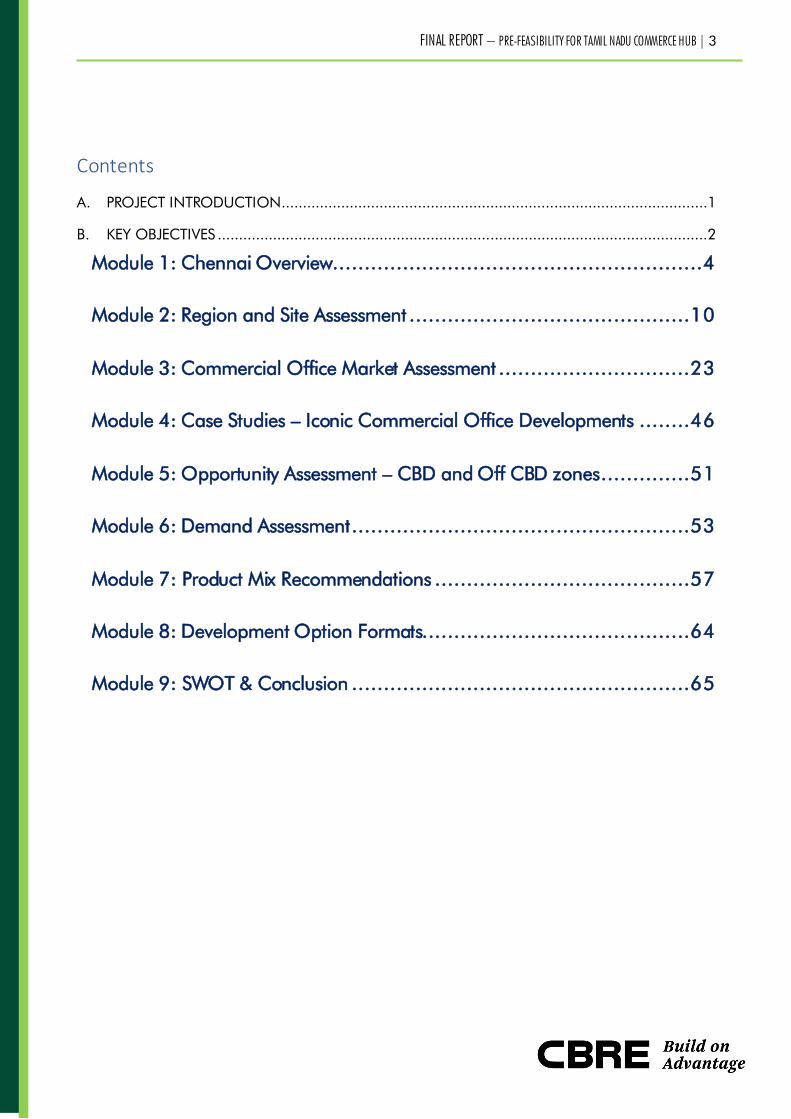

Contents

A. PROJECT INTRODUCTION ....................................................................................................1

B. KEY OBJECTIVES ...................................................................................................................2

Module 1: Chennai Overview..........................................................4

Module 2: Region and Site Assessment ............................................10

Module 3: Commercial Office Market Assessment ..............................23

Module 4: Case Studies – Iconic Commercial Office Developments ........46

Module 5: Opportunity Assessment – CBD and Off CBD zones ..............51

Module 6: Demand Assessment .....................................................53

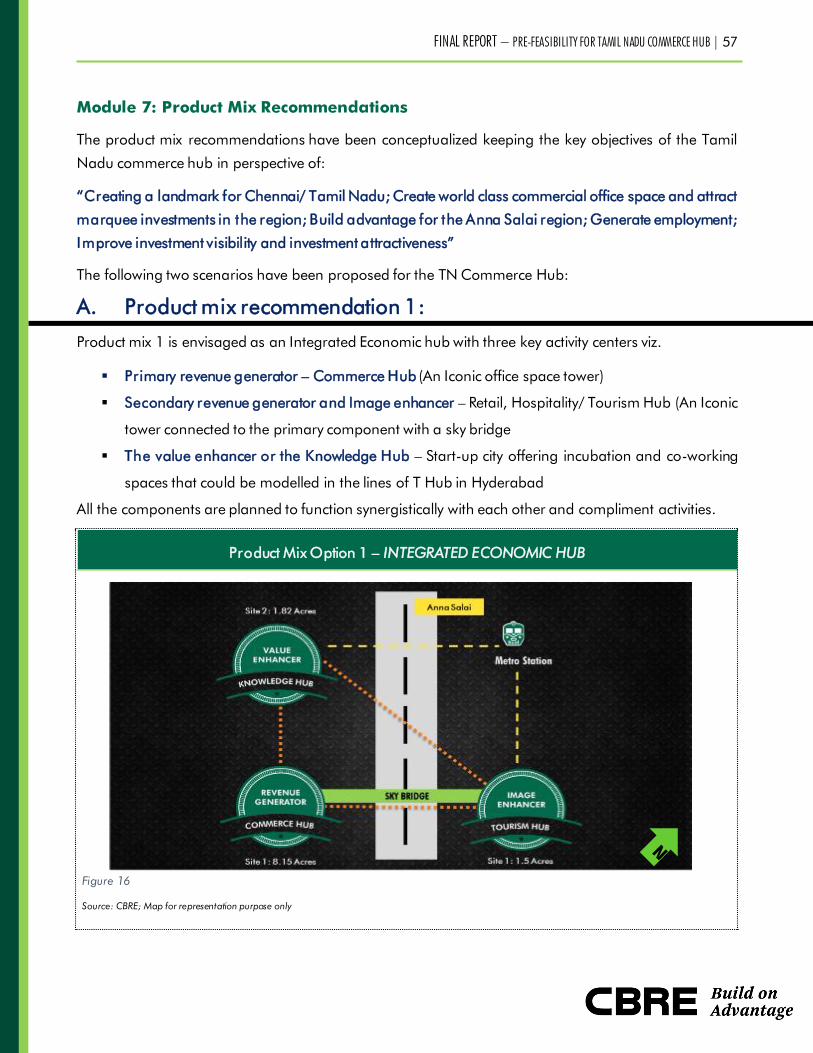

Module 7: Product Mix Recommendations ........................................57

Module 8: Development Option Formats..........................................64

Module 9: SWOT & Conclusion .....................................................65

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 4

Module 1: Chennai Overview

A. Brief overview of Chennai City

Chennai, the capital of the state of Tamil Nadu is located along the eastern sea coast in the south of

India. As per census 2011, Chennai houses a population of 8.65 million and is the fourth largest urban

agglomeration in the country in terms of population.

The Chennai Metropolitan area spans 8,989 sq.km covering the districts of Chennai, Kancheepuram,

Thiruvallur and parts of Vellore district. The development in the Chennai Metropolitan area is regulated

by the Chennai Metropolitan Development Authority (CMDA).

Location of Chennai with context to India

Source: CBRE Research

As per the budget of 2018 – 2019, the state has witnessed moderate growth and the GSDP growth rate

at constant prices in 2017 – 2018 is estimated to be 8.03%. I t is also anticipated that the economy will

grow faster and thereby enabling the State to reach 9% growth rate in 2018-2019.

Chennai, in the year 2016 – 2017 was a key contributor to the nation’s GDP, contributing approx. USD

66 billion. The economic base of the city is primarily constituted by Automobile Manufacturing, IT/ITeS

enabled services and Banking & Finance sectors.

The city boasts of a designated IT/ITeS corridor called the Rajiv Gandhi Salai, which is a 25-km long

corridor located in the south of the city which was an initiative by the Government of Tamil Nadu to attract

large scale IT investments in to the city and also create an eco-system for the sector. The city is home to

approx. 1million IT/ITeS Professionals professionals, working in over 4,200 companies.1

1 Estimated by CBRE Research as an extrapolation of commercial office space activity in the market

Figure 1

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 5

The city is also known as ‘Detroit of India’ owing to the presence of a robust automobile sector. The city

also witnesses the presence of prominent automobile companies such as Nissan, Hyundai, Ashok

Leyland, TVS, Royal Enfield etc.

Chennai has a strong workforce across the cross section of industries which is a reflection of the robust

education infrastructure present in the city coupled by the prevailing industry eco-system. As per census

2011, the literacy rate of the city is 90.18%, which is the second highest in the country. The city witnesses

the presence of more than 170 engineering colleges with an annual intake of approx. 53,000 students.

A few reputed colleges in the city are Indian Institute of Madras, College of Engineering, Madras Institute

of Technology, SRM University.

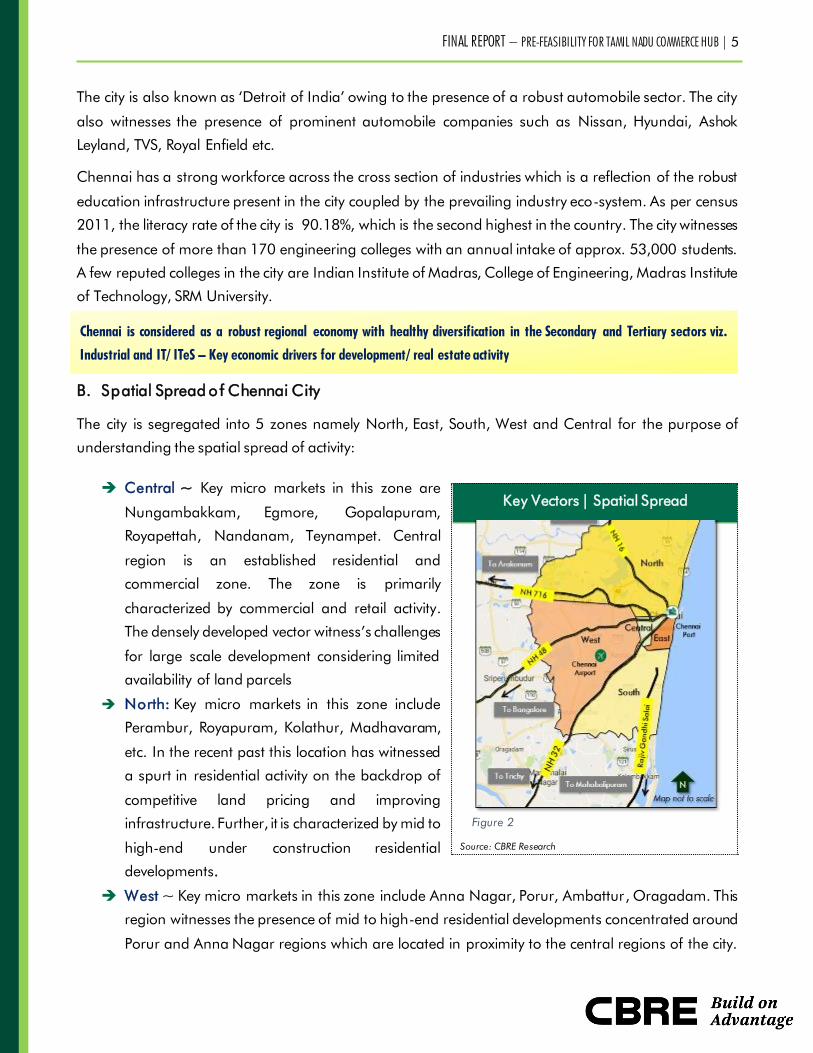

B. Spatial Spread o f Chennai City

The city is segregated into 5 zones namely North, East, South, West and Central for the purpose of

understanding the spatial spread of activity:

Central ~ Key micro markets in this zone are

Nungambakkam, Egmore, Gopalapuram,

Royapettah, Nandanam, Teynampet. Central

region is an established residential and

commercial zone. The zone is primarily

characterized by commercial and retail activity.

The densely developed vector witness’s challenges

for large scale development considering limited

availability of land parcels

North: Key micro markets in this zone include

Perambur, Royapuram, Kolathur, Madhavaram,

etc. In the recent past this location has witnessed

a spurt in residential activity on the backdrop of

competitive land pricing and improving

infrastructure. Further, it is characterized by mid to

high-end under construction residential

developments.

West ~ Key micro markets in this zone include Anna Nagar, Porur, Ambattur, Oragadam. This

region witnesses the presence of mid to high-end residential developments concentrated around

Porur and Anna Nagar regions which are located in proximity to the central regions of the city.

Key Vectors | Spatial Spread

Source: CBRE Research

Chennai is considered as a robust regional economy with healthy diversification in the Secondary and Tertiary sectors viz.

Industrial and IT/ ITeS – Key economic drivers for development/ real estate activity

Figure 2

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 6

Regions located further away like Oragadam, Sriperumbudur, etc. are key industrial/logistics hub

of the city primarily catering to the automobile and manufacturing industries.

East ~ Key micro markets in this zone include Alwarpet, Santhome, MRC Nagar, etc. Considering

the premium-ness of the location owing to the proximity to sea and the CBD areas, the region

has evolved into a luxury/ high end residential vector; Additionally, the region witnesses fair

amount of commercial and support retail activity

South ~ Key micro markets in this zone are Adyar, Velachery, Taramani, Shollingnallur,

Semmancheri. Both Rajiv Gandhi Salai (designated IT/ITeS corridor) and the Grand Southern

Trunk (GST) Road, have been key vectors and contribute to majority share of supply and

absorption from a residential and commercial front. Peripheral markets in this region is further

characterized by the availability of large land parcels.

C. Chennai - Connectivity

The city is well connected across the globe via air, rail, road and sea. Chennai city enjoys the strategic

locational advantage of being well connected via all modes of transportation thereby positioning itself as

an attractive investment destination. Furthermore, below is a broad overview of air, rail, road and sea

connectivity of Chennai.

Air Connectivity: Chennai International Airport is located along GST in the South-Western part of

the city with recorded passenger traffic of approx. 18.4 million passengers during 2016 – 17

(Ranked 4th in terms of passenger

traffic). The airport is the third busiest

airport in India in terms of international

passengers. Further, there is a

proposed terminal expansion and

passenger traffic is expected to reach

35 million by 2030. In addition to the

above, the government is evaluating

development of a greenfield airport.

Rail: The city has a robust rail network

with two intercity railway terminals viz.

Chennai Central which act as a hub for

trains travelling to Western and

Northern India and Chennai Egmore

which connects the city to the Southen

parts of Tamil Nadu and Kerala.

Key Intra City Connectivity Hubs

Source: CBRE Research

Figure 3

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 7

Approx. 550,000 passengers use these terminals on a daily basis.

Road: Four major national highways traverse through Chennai, connecting it with other major

cities both within and outside Tamil Nadu.

o NH 716 – connects Chennai with Kadappa in Andhra Pradesh. Traverses through

Tiruvallu, Tiruttani in Tamil Nadu and Renigunta in Andhra Pradesh

o NH 16 – forms a part of the golden quadrilateral and connects the city to Kolkata.

Traverses through 4 states viz. Tamil Nadu, Andhra Pradesh, Odisha and West Bengal

o NH 48 – connects Chennai with Bengaluru ~ a prominent economic destination in

South India.

o NH 32 – also called as GST road runs along the spine of the state, connecting

prominent cities of the state viz. Tindivanam, Trichy, Madurai etc.

Sea: Chennai is well connected to south east Asia, countries in Africa and middle-east via sea.

Chennai houses 3 ports namely Chennai Port, Kamarajar Port and Adani Kattupalli Port.

D. Intra-City Connectivity / Key Physical Infrastructure Initiatives

Strong road and rail network have ensured excellent connectivity to key activity hubs in the city. Rail

network comprising of MRTS and Suburban rail ensure seamless connectivity from major residential

pockets to economic hubs. Development activity in Chennai is mostly radial although it is a coastal city.

Therefore, infrastructure initiatives like the inner ring road, outer ring road and the peripheral ring road

along multiple circumference layers of the city provide good connectivity to various nodes. Below is a

broad level outline of the existing and proposed infrastructure initiatives in the city:

Suburban Rail: Three lines each traversing through the north, south and west of the city have

ensured smooth connectivity across key economic hubs in the city, connecting micro-markets in

the CBD such as Egmore, Nungambakkam, Saidapet to peripheral markets of Tambaram,

Villivakkam, Avadi etc. The suburban rail plys over 550 services on a daily basis and more than

1.46 million people use the suburban rail network. Thus, the existing suburban rail network shall

ensure good connectivity of the subject properties to peripheral locations of the city where there

is presence of significant residential activity

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 8

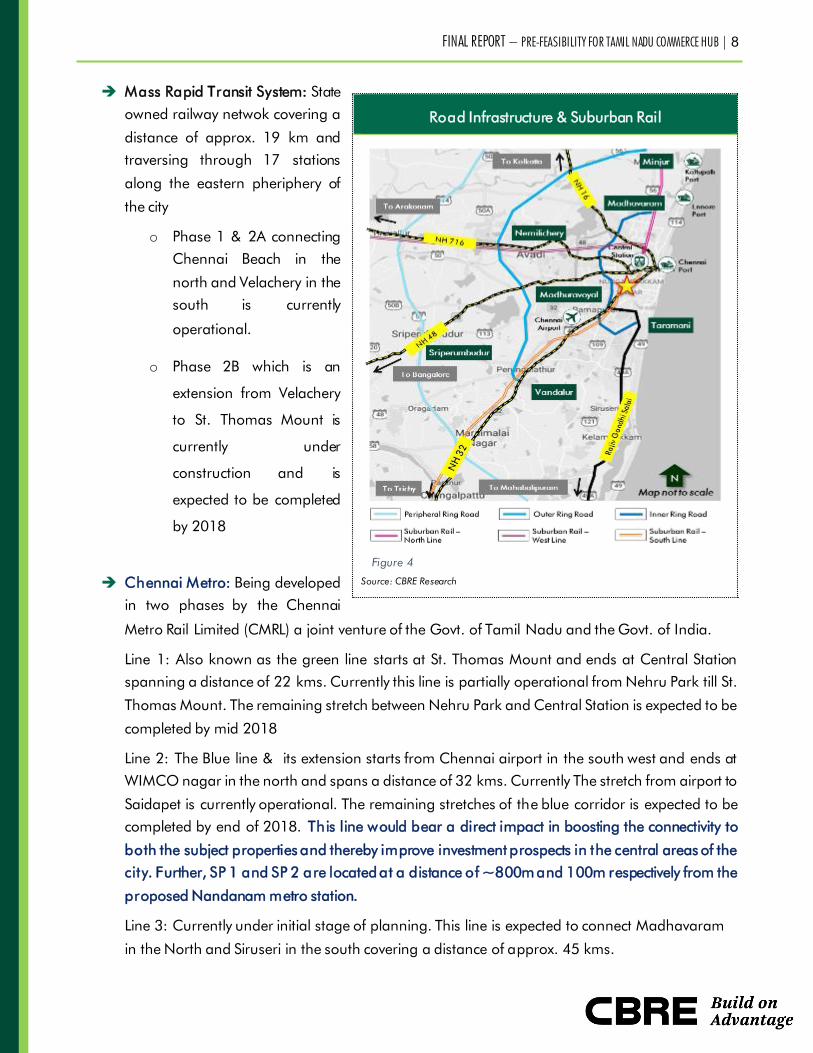

Mass Rapid Transit System: State

owned railway netwok covering a

distance of approx. 19 km and

traversing through 17 stations

along the eastern pheriphery of

the city

o Phase 1 & 2A connecting

Chennai Beach in the

north and Velachery in the

south is currently

operational.

o Phase 2B which is an

extension from Velachery

to St. Thomas Mount is

currently under

construction and is

expected to be completed

by 2018

Chennai Metro: Being developed

in two phases by the Chennai

Metro Rail Limited (CMRL) a joint venture of the Govt. of Tamil Nadu and the Govt. of India.

Line 1: Also known as the green line starts at St. Thomas Mount and ends at Central Station

spanning a distance of 22 kms. Currently this line is partially operational from Nehru Park till St.

Thomas Mount. The remaining stretch between Nehru Park and Central Station is expected to be

completed by mid 2018

Line 2: The Blue line & its extension starts from Chennai airport in the south west and ends at

WIMCO nagar in the north and spans a distance of 32 kms. Currently The stretch from airport to

Saidapet is currently operational. The remaining stretches of the blue corridor is expected to be

completed by end of 2018. This line would bear a direct impact in boosting the connectivity to

both the subject properties and thereby improve investment prospects in the central areas of the

city. Further, SP 1 and SP 2 are located at a distance of ~800m and 100m respectively from the

proposed Nandanam metro station.

Line 3: Currently under initial stage of planning. This line is expected to connect Madhavaram

in the North and Siruseri in the south covering a distance of approx. 45 kms.

Road Infrastructure & Suburban Rail

Source: CBRE Research

Figure 4

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 9

Line 4: Currently under initial stage of planning. The line spanning a distance of approx. 17

kms is expected to connect Koyambedu in the west and Lighhouse in the east bisecting the city

horizontally.

Line 5: Currently under initial stages of planning. This line is expected to run along the eastern

pheriphery of the city from Madhavaram in the north till Shollinganallur in the south covering a

distance of approx. 44 kms

Inner Ring Road: This key transport corridor located within the city, acts as a decongester of traffic

along a 25 km stretch which includes key micro-markets such as Thiruvanmiyur, Velachery,

Guindy, Koyambedu, Anna Nagar, Padi and Madhavaram

Outer Ring Road: A 62.3 km stretch running along the external parts of the city. Phase 1 connects

Vandalur micro market on NH 32 till Nemilichery via Nazarethpettai and running along micro-

markets of Perungalathur, Thirumazhaisai, Pattabhiram etc. Phase 2 connects Nemilichery with

Nallur on NH 716. Currently Phase 1 is fully completed and operationnal, Phase 2 is partially

operational and is expected to be completed by 2018 end

Peripheral Ring Road: A proposed radial road covering 162 kms connecting Poonjeri in the South

with Kaatupalli in the North. The road is designed to cut across the National Highway in the

pheriphery of the city.

With robust connectivity via all modes of transportation and excellent intra city physical infrastructure availability, Chennai is

considered to offer one of the best infrastructure quality in South India;

Further, both the subject properties are extremely well positioned to benefit from the mega infrastructure initiative of metro

connectivity, suburban rail and road accessibility.

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 10

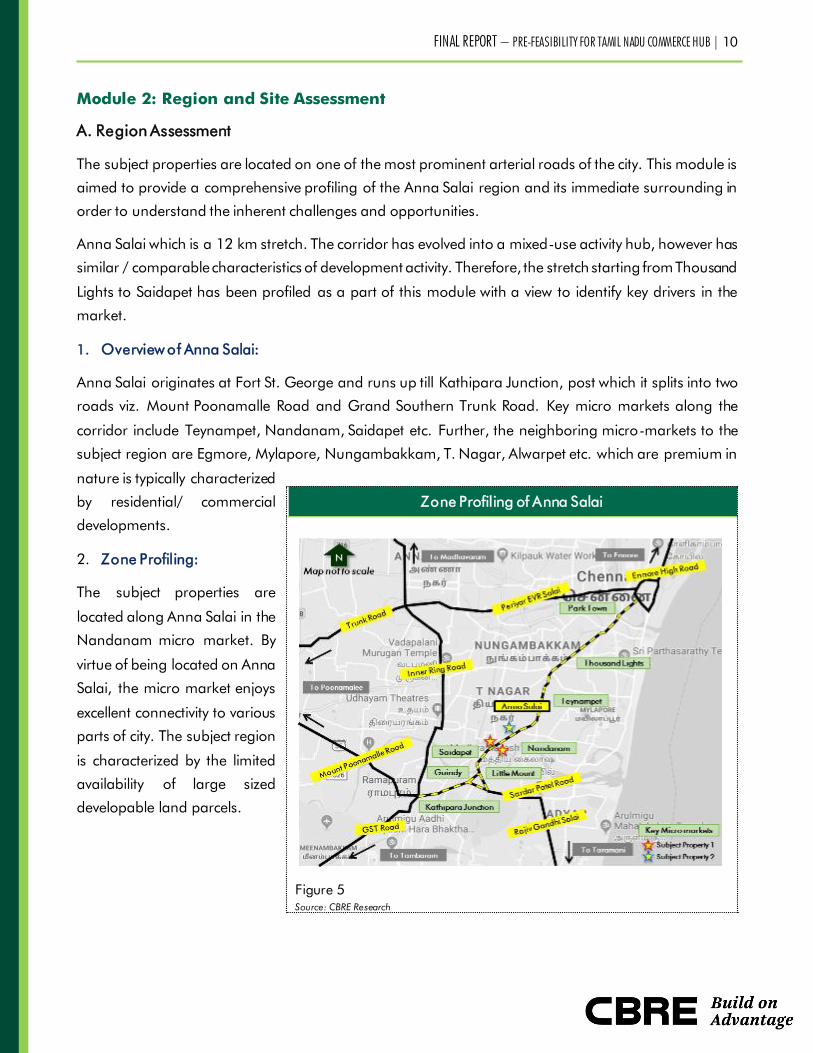

Module 2: Region and Site Assessment

A. Region Assessment

The subject properties are located on one of the most prominent arterial roads of the city. This module is

aimed to provide a comprehensive profiling of the Anna Salai region and its immediate surrounding in

order to understand the inherent challenges and opportunities.

Anna Salai which is a 12 km stretch. The corridor has evolved into a mixed-use activity hub, however has

similar / comparable characteristics of development activity. Therefore, the stretch starting from Thousand

Lights to Saidapet has been profiled as a part of this module with a view to identify key drivers in the

market.

1. Overview of Anna Salai:

Anna Salai originates at Fort St. George and runs up till Kathipara Junction, post which it splits into two

roads viz. Mount Poonamalle Road and Grand Southern Trunk Road. Key micro markets along the

corridor include Teynampet, Nandanam, Saidapet etc. Further, the neighboring micro-markets to the

subject region are Egmore, Mylapore, Nungambakkam, T. Nagar, Alwarpet etc. which are premium in

nature is typically characterized

by residential/ commercial

developments.

2. Zone Profiling:

The subject properties are

located along Anna Salai in the

Nandanam micro market. By

virtue of being located on Anna

Salai, the micro market enjoys

excellent connectivity to various

parts of city. The subject region

is characterized by the limited

availability of large sized

developable land parcels.

Zone Profiling of Anna Salai

Figure 5

Source: CBRE Research

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 11

3. Mapping of key developments: Development activity in the corridor has been classified under the heads of commercial office spaces, retail mall

developments, hospitality developments and independent office building by corporates/ business houses.

Mapping of Key Developments in the Zone

Source: CBRE Research

Figure 6

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 12

The subject corridor viz. Anna Salai owing to its location attributes of being in the city of the city with

excellent connectivity and accessibility has evolved into one of the coveted and busy real estate corridors

in the city witnessing commercial and retail activity.

Commercial office space activity – Majority of development activity in the corridor is characterized by

commercial office space developments. A fair share of developments in the region are old, and hence are

categorized as Grade B developments. However, new supply additions in the market are typically Grade A

developments. A few investment grade developments in the vicinity of the subject property are Prestige

Palladium, Prestige Polygon, etc. A premium image is associated with the micro market considering

visibility, connectivity and accessibility of the region.

Additionally, the region also witnesses the presence of a few individual campuses/office developments of

large corporates viz. MRF, TVS, Balmer & Lawrie, Sundaram Group, etc.

Retail office space activity - Spencer plaza on Anna Salai marked the development of organized retail mall

activity in the city in early 2000s; Currently the location witness’s presence of another retail mall

development viz. Express Avenue Mall. Additionally, the lower floors of commercial office developments

are used as a h street retail area catering to banks, auto showrooms, food and beverage, etc.

Hospitality activity - Anna Salai contributes to to approx. 20% of hospitality in the city catering to both

business and leisure segment travelers. Anna Salai is home to national and international hotel brands in

the city viz. viz. ITC Grand Chola, Park Hyatt, Hyatt Regency etc.

Residential real estate activity - The region is densely populated and is mostly characterized by independent

dwelling units located in the central part of the city. Further, there is also a considerable supply of

unorganized residential apartments in the region. A few under construction residential developments in the

region are Olympia Goodwood Residences, Casa Grande Monte Carlo, etc.

Over time, this region has established into a self-sustained economic hub with presence of evolved real

estate activities across segments.

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 13

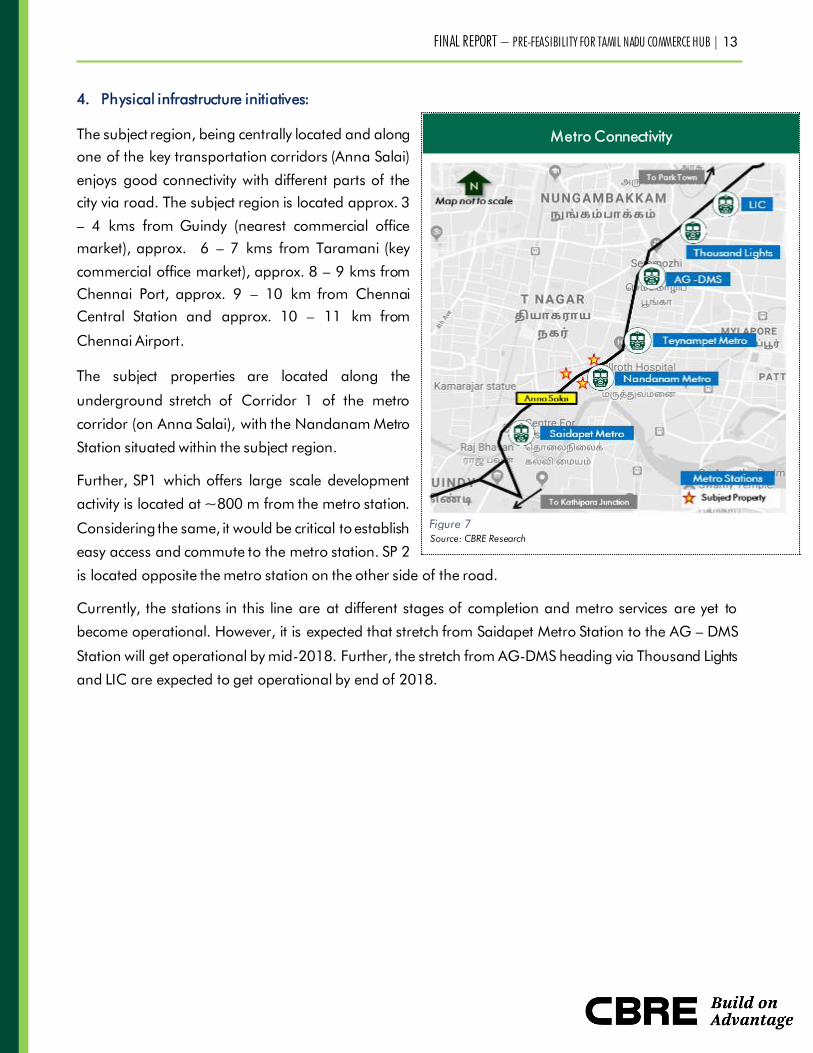

4. Physical infrastructure initiatives:

The subject region, being centrally located and along

one of the key transportation corridors (Anna Salai)

enjoys good connectivity with different parts of the

city via road. The subject region is located approx. 3

– 4 kms from Guindy (nearest commercial office

market), approx. 6 – 7 kms from Taramani (key

commercial office market), approx. 8 – 9 kms from

Chennai Port, approx. 9 – 10 km from Chennai

Central Station and approx. 10 – 11 km from

Chennai Airport.

The subject properties are located along the

underground stretch of Corridor 1 of the metro

corridor (on Anna Salai), with the Nandanam Metro

Station situated within the subject region.

Further, SP1 which offers large scale development

activity is located at ~800 m from the metro station.

Considering the same, it would be critical to establish

easy access and commute to the metro station. SP 2

is located opposite the metro station on the other side of the road.

Currently, the stations in this line are at different stages of completion and metro services are yet to

become operational. However, it is expected that stretch from Saidapet Metro Station to the AG – DMS

Station will get operational by mid-2018. Further, the stretch from AG-DMS heading via Thousand Lights

and LIC are expected to get operational by end of 2018.

Metro Connectivity

Source: CBRE Research

Figure 7

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 14

B. Si te Assessment

This section provides a detailed understanding of the subject land parcels and the various attributes it

possesses that determine the development potential at the subject site. A detailed overview of the subject

land parcels has been enumerated below:

Land parcel 1 (9.65 acres):2

Parameter Detail CBRE Comments

Area

9.65 acres (North side parcel: 8.15 acres3, South side parcel:

1.50 acres)

Fairly large sized land

parcel located on Anna

Salai; There is limited

avalability of similar sized

developable land parcels in

the CBD region

Contiguity &

Shape

Two non-contiguous land parcels located on either sides of Anna

Salai

North side land parcel is irregular in shape and cut across by

multiple roads. However, based on client inputs, we understand

that certain adjustments to the exisiting roads will be made to

derive a large continuous developable area.

Additionally, the secondary access for the SP of the North side

land, further divides the land parcel into smaller chunk of <1acre

South side land parcel is fairly regular in shape

Non contiguous nature

would help us develop a

distingished product mix

where there would be an

opportunity to segregate /

zone / asset classes based

on proposed best use on

each of the sites, however

still function as a single unit

Current

Usage

The North side land parcel currently houses Periyar EVR building,

HIG apartments, TNHB staff quarters, TNHB land (with built up

structure for varied use). The South side land parcel currenty

houses the TNHB head office

We understand that

applicable compensations

will be made to existing

occupiers; However, we feel

that it is a great opportunity

to house key government

departments in the

proposed development

Access Roads

The primary access for the subject properties is via Anna Salai.

The North side land parcel enjoys a secondary access via Model

Hutment Road (situated off Anna Salai)

Excellent connectivity and

accessibility from one of the

key arterial roads of the city;

Additional roads provide

opportunity in ease of

2 Based on discussions with the client, we understand that the current land would be realigned and the new land

layout as provided has been used for this study

3 Inclusive of proposed roads

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 15

Parameter Detail CBRE Comments

operations for a large scale

development

Frontage

North side land has a frontage of approx. 400 ft and for South

side land has a frontage of approx. 200 ft

Post the proposed

consolidation of the site, the

North side land parcel will

enjoy signigicant frontage

on three sides

The South side land parcel

enjoys considerable

frontage along Anna Salai

Metro

Connectivity

SP is located at a distance of ~800 m from the proposed

Nandanam Metro Station

Considering, the possible

large scale development on

the subject property, it

would be critical to provide

seamless connectivity to the

metro station so that the

proposed development can

directly benefit

Development

Potential4

S ite 1 - North

Particulars Scenario 1 Scenario 2 Scenario 3

Ground Coverage 30% 30 - 40% 40 - 50%

Total land area

(acres) 8.15 8.15 8.15

Proposed road 1

(acres) 1.66 1.66 1.66

Proposed road 2

(acres) 0.2 0.2 0.2

Balance net extent

(acres) 6.29 6.29 6.29

FSI applicable5 6

2.5 2.25 2

Built-up Area (sft)

(FSI x Balance net

ex tent)

684,981 616,483 547,985

Site 1 - South

Adequate road width and

frontage would aid in

accomplishment of

maximum permissible FSI at

a 30% ground coverage.

The land parcels would also

be eligible for a premium

FSI of 40% (if required)

4 As per Development control regulations illustrated in Second master plan for Chennai Metropolitan Area, 2026

and Client Inputs

5 A premium FSI of 40% of the current achievable FSI could also be purchased from CMDA to increase development

potential

6 If the subject property is developed as an IT/ITeS development, the site extent is not less than 2,000 sqm and

conforms to the other regulations, the FSI shall be allowed at 1.5 times the ordinarily permissible FSI

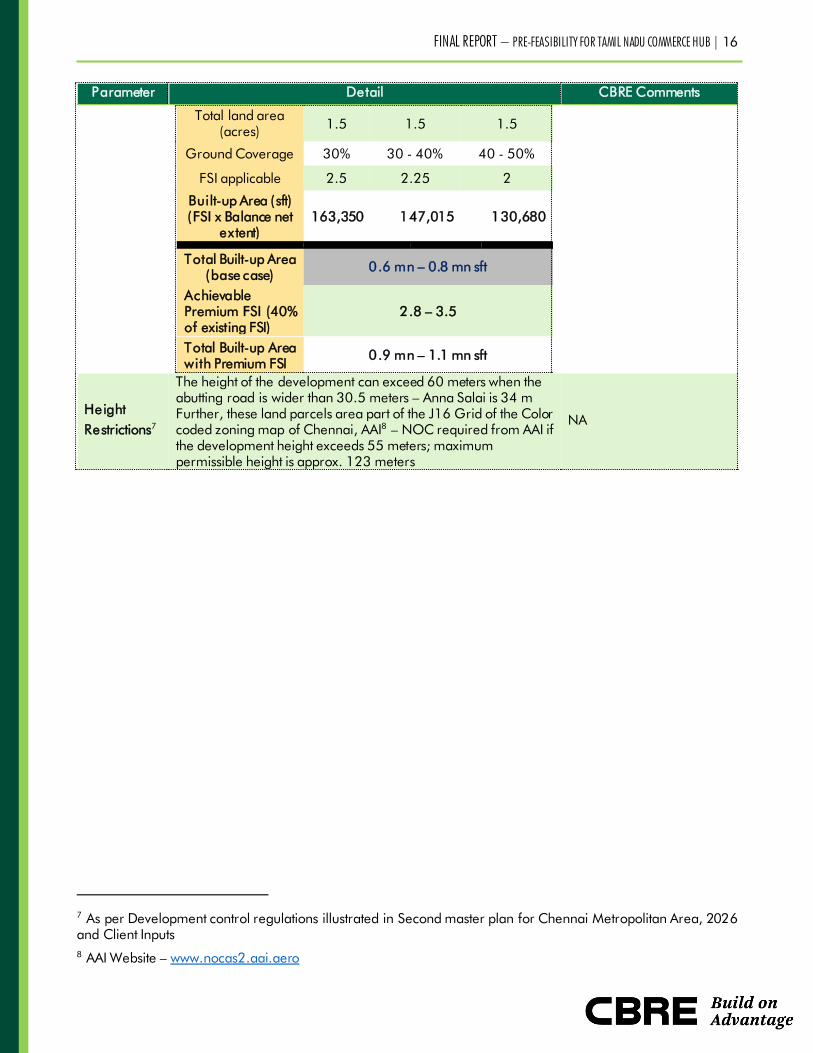

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 16

Parameter Detail CBRE Comments

Total land area

(acres) 1.5 1.5 1.5

Ground Coverage 30% 30 - 40% 40 - 50%

FSI applicable 2.5 2.25 2

Built-up Area (sft)

(FSI x Balance net

ex tent)

163,350 147,015 130,680

Total Built-up Area

(base case) 0.6 mn – 0.8 mn sft

Achievable

Premium FSI (40%

of existing FSI)

2.8 – 3.5

Total Built-up Area

with Premium FSI 0.9 mn – 1.1 mn sft

Height

Restrictions7

The height of the development can exceed 60 meters when the

abutting road is wider than 30.5 meters – Anna Salai is 34 m

Further, these land parcels area part of the J16 Grid of the Color

coded zoning map of Chennai, AAI8 – NOC required from AAI if

the development height exceeds 55 meters; maximum

permissible height is approx. 123 meters

NA

7 As per Development control regulations illustrated in Second master plan for Chennai Metropolitan Area, 2026

and Client Inputs

8 AAI Website – www.nocas2.aai.aero

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 17

Property Map:

Site 1 | 9.65 acres

Source: CBRE Research

Figure 8

Property Layout:

Existing land utilization Proposed land utilization

Source: The Client Source: The Client

Figure 10 Figure 9

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 18

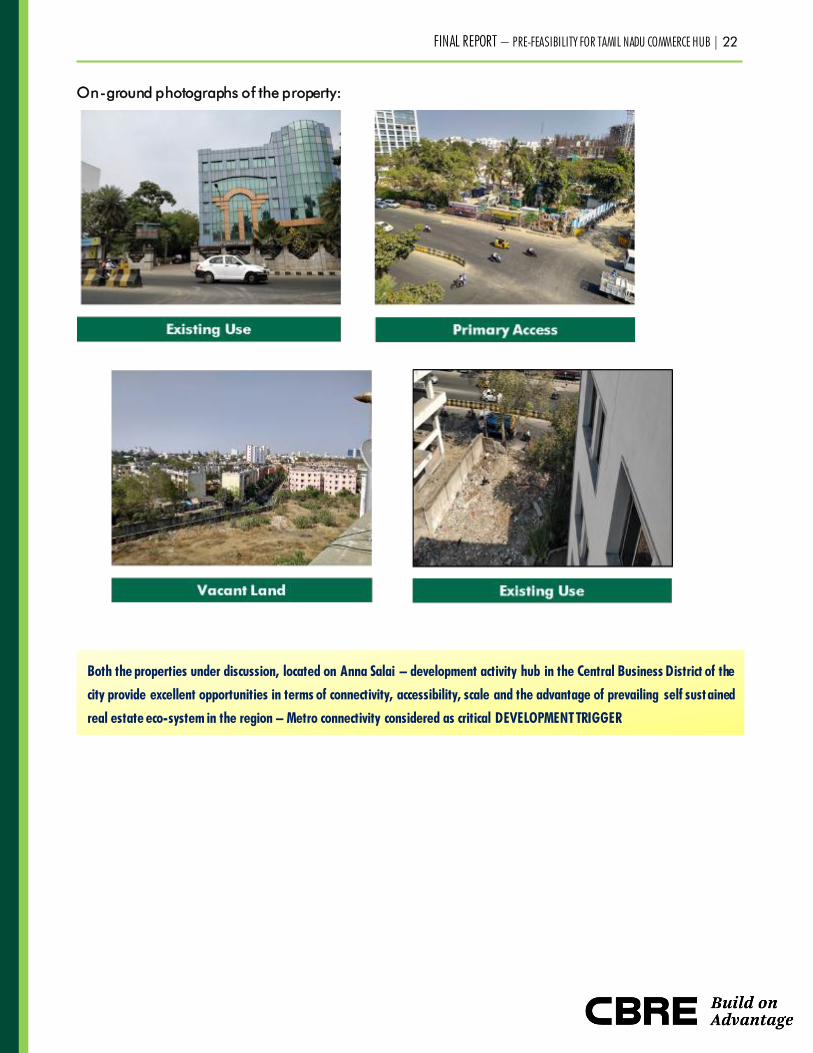

On-ground photographs of the property:

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 19

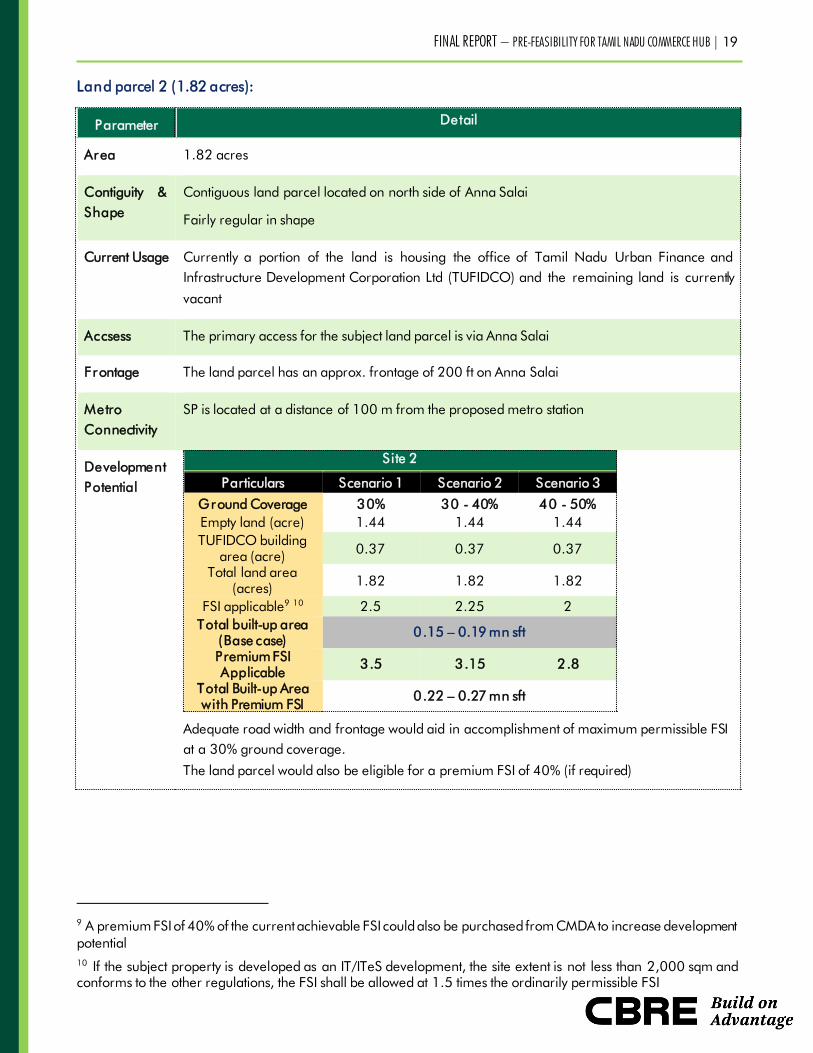

Land parcel 2 (1.82 acres):

Parameter Detail

Area 1.82 acres

Contiguity &

Shape

Contiguous land parcel located on north side of Anna Salai

Fairly regular in shape

Current Usage Currently a portion of the land is housing the office of Tamil Nadu Urban Finance and

Infrastructure Development Corporation Ltd (TUFIDCO) and the remaining land is currently

vacant

Accsess The primary access for the subject land parcel is via Anna Salai

Frontage The land parcel has an approx. frontage of 200 ft on Anna Salai

Metro

Connectivity

SP is located at a distance of 100 m from the proposed metro station

Development

Potential

S ite 2

Particulars Scenario 1 Scenario 2 Scenario 3

Ground Coverage 30% 30 - 40% 40 - 50%

Empty land (acre) 1.44 1.44 1.44

TUFIDCO building

area (acre) 0.37 0.37 0.37

Total land area

(acres) 1.82 1.82 1.82

FSI applicable9 10

2.5 2.25 2

Total built-up area

(Base case) 0.15 – 0.19 mn sft

Premium FSI

Applicable 3.5 3.15 2.8

Total Built-up Area

with Premium FSI 0.22 – 0.27 mn sft

Adequate road width and frontage would aid in accomplishment of maximum permissible FSI

at a 30% ground coverage.

The land parcel would also be eligible for a premium FSI of 40% (if required)

9 A premium FSI of 40% of the current achievable FSI could also be purchased from CMDA to increase development

potential

10 If the subject property is developed as an IT/ITeS development, the site extent is not less than 2,000 sqm and

conforms to the other regulations, the FSI shall be allowed at 1.5 times the ordinarily permissible FSI

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 20

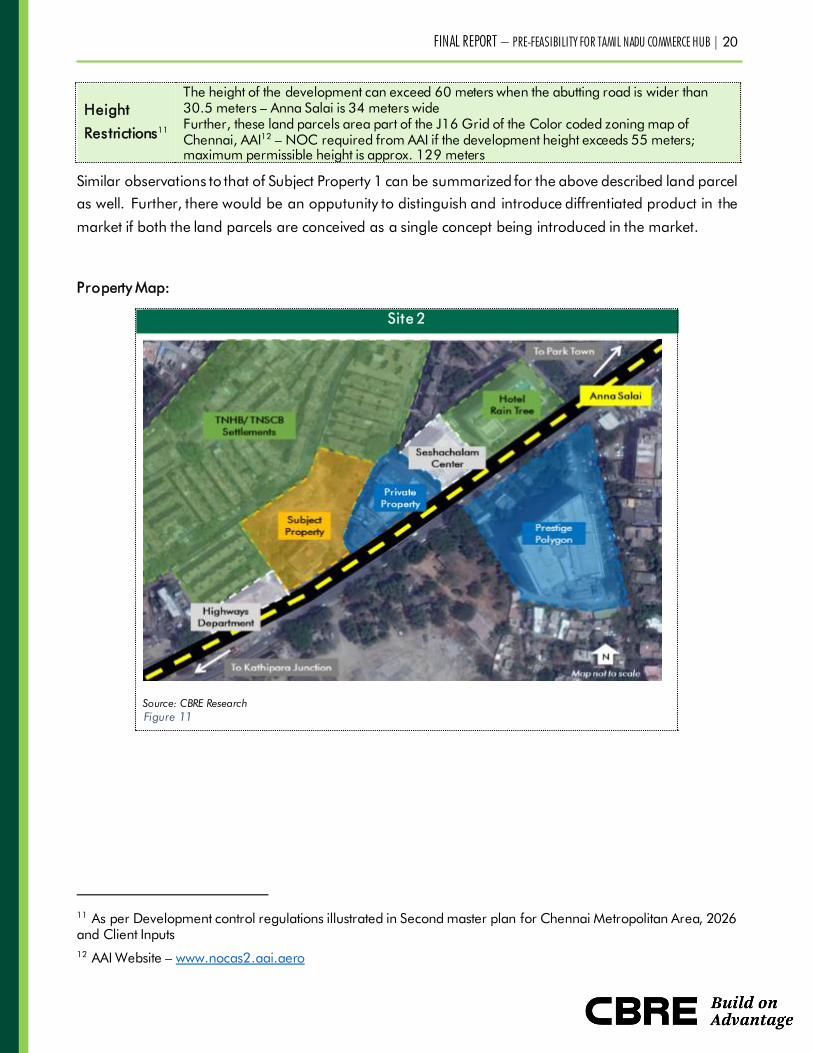

Height

Restrictions11

The height of the development can exceed 60 meters when the abutting road is wider than

30.5 meters – Anna Salai is 34 meters wide

Further, these land parcels area part of the J16 Grid of the Color coded zoning map of

Chennai, AAI12

– NOC required from AAI if the development height exceeds 55 meters;

maximum permissible height is approx. 129 meters

Similar observations to that of Subject Property 1 can be summarized for the above described land parcel

as well. Further, there would be an opputunity to distinguish and introduce diffrentiated product in the

market if both the land parcels are conceived as a single concept being introduced in the market.

Property Map:

Site 2

Source: CBRE Research

11 As per Development control regulations illustrated in Second master plan for Chennai Metropolitan Area, 2026

and Client Inputs

12 AAI Website – www.nocas2.aai.aero

Figure 11

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 21

Property Layout:

Proposed Use

Source: The Client

Figure 12

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 22

On-ground photographs of the property:

Both the properties under discussion, located on Anna Salai – development activity hub in the Central Business District of the

city provide excellent opportunities in terms of connectivity, accessibility, scale and the advantage of prevailing self sustained

real estate eco-system in the region – Metro connectivity considered as critical DEVELOPMENT TRIGGER

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 23

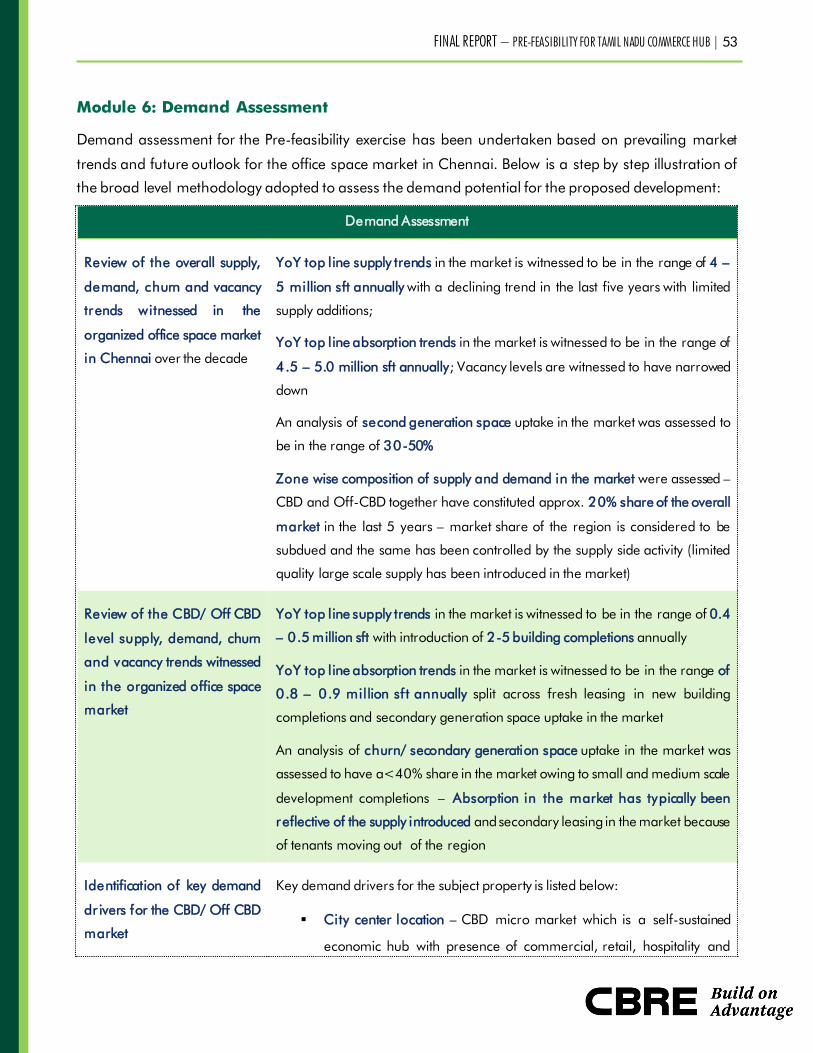

Module 3: Commercial Office Market Assessment

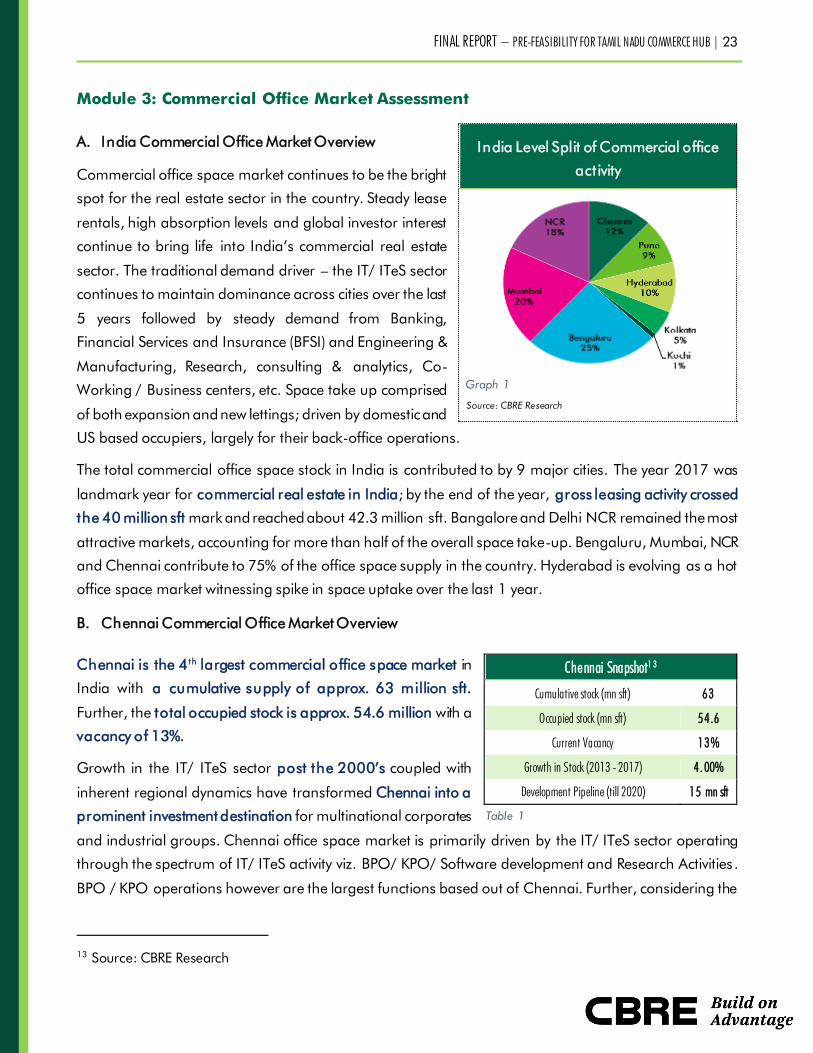

A. India Commercial Office Market Overview

Commercial office space market continues to be the bright

spot for the real estate sector in the country. Steady lease

rentals, high absorption levels and global investor interest

continue to bring life into India’s commercial real estate

sector. The traditional demand driver – the IT/ ITeS sector

continues to maintain dominance across cities over the last

5 years followed by steady demand from Banking,

Financial Services and Insurance (BFSI) and Engineering &

Manufacturing, Research, consulting & analytics, Co-

Working / Business centers, etc. Space take up comprised

of both expansion and new lettings; driven by domestic and

US based occupiers, largely for their back-office operations.

The total commercial office space stock in India is contributed to by 9 major cities. The year 2017 was

landmark year for commercial real estate in India; by the end of the year, gross leasing activity crossed

the 40 million sft mark and reached about 42.3 million sft. Bangalore and Delhi NCR remained the most

attractive markets, accounting for more than half of the overall space take-up. Bengaluru, Mumbai, NCR

and Chennai contribute to 75% of the office space supply in the country. Hyderabad is evolving as a hot

office space market witnessing spike in space uptake over the last 1 year.

B. Chennai Commercial Office Market Overview

Chennai is the 4th largest commercial office space market in

India with a cumulative supply of approx. 63 million sft.

Further, the total occupied stock is approx. 54.6 million with a

vacancy of 13%.

Growth in the IT/ ITeS sector post the 2000’s coupled with

inherent regional dynamics have transformed Chennai into a

prominent investment destination for multinational corporates

and industrial groups. Chennai office space market is primarily driven by the IT/ ITeS sector operating

through the spectrum of IT/ ITeS activity viz. BPO/ KPO/ Software development and Research Activities .

BPO / KPO operations however are the largest functions based out of Chennai. Further, considering the

13 Source: CBRE Research

India Level Split of Commercial office

act ivity

Source: CBRE Research

Chennai Snapshot1 3

Cumulative stock (mn sft) 63

Occupied stock (mn sft) 54.6

Current Vacancy 13%

Growth in Stock (2013 - 2017) 4. 00%

Development Pipeline (till 2020) 15 mn sft

Table 1

Graph 1

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 24

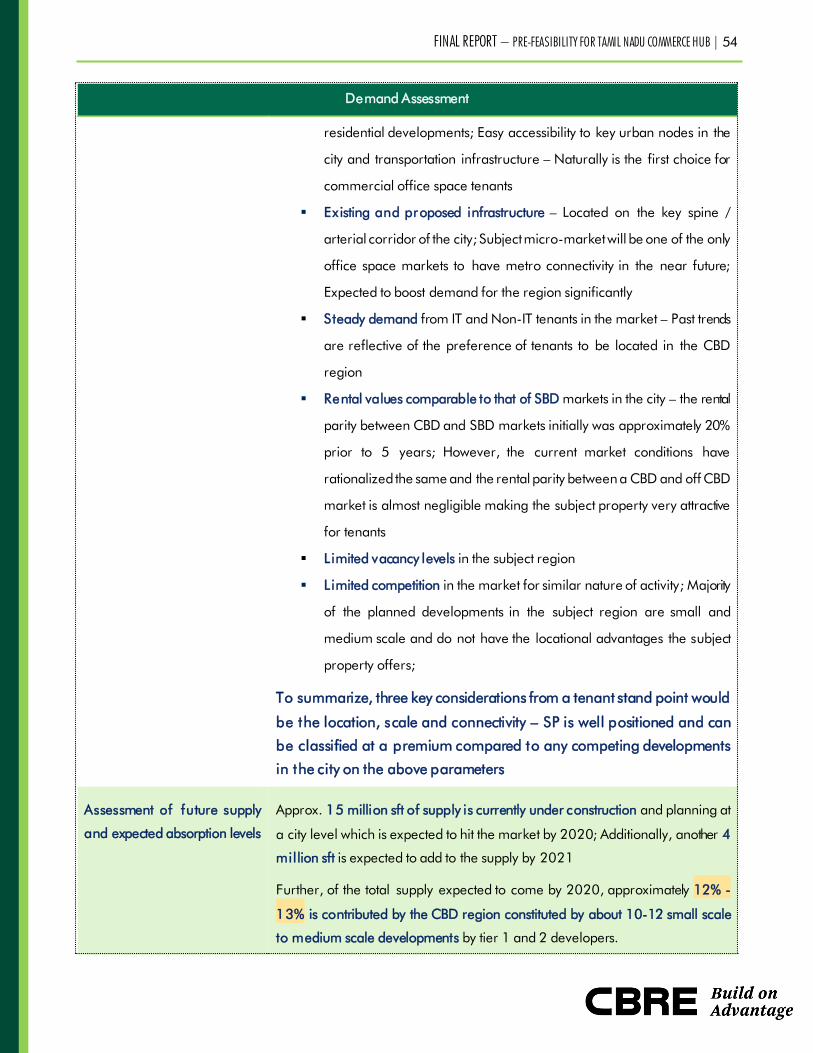

diversified economic base of Chennai, key non-IT tenant sectors of BFSI, engineering & manufacturing,

research & consulting, etc. also have small to medium scale operations.

The evolution of organized office space activity in the city traditionally commenced in the CBD region in

the micro markets of Nungambakkam, RK Salai, etc. Office space buildings in the CBD region primarily

catered to non-IT tenants viz. front offices of industrial corporates, corporate offices of business houses

and BFSI segments.

Inauguration of TIDEL Park in the Pre 2000’s and establishment of Rajiv Gandhi Salai (OMR) as the

designated IT corridor of the city marked the onset of IT/ ITeS activity in the city. Onset of large scale

commercial office space activity commenced with the development of OMR which was planned as IT

investment destination around the same time where India was emerging as a global outsourcing

destination. Several large-scale IT Parks, Software Tech Parks, SEZ etc. got developed in the OMR and

other markets in the Secondary Business District during 2000 – 2010. Chennai emerged as one of the

key office space markets in India. Chennai after Bangalore was considered as a preferred office space

destination in South India for Global outsourcing companies. Key developments that were completed

during these years include Ascendas IT Park, RMZ Millenia, Mahindra World City SEZ, DLF Tech Park,

etc. Further, during this phase, pro-active measures were taken by the Tamil Nadu government by

development of IT Parks/ SEZs (land allotments to TCS, CTS, Wipro, Syntel, Polaris, etc.) along with policy

level benefits offering additional FSI for development of IT/ ITeS buildings.

Supply and Absorption Trends – 2013 to 2017

Source: CBRE Research

Graph 2

The supply-demand trends of commercial office space activity in Chennai has witnessed a steady phase

primarily controlled by the supply additions introduced into the market and vacancy levels at various

intervals.

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 25

Chennai witnessed an average annual absorption of approx. 4.5 – 5.5 million sft with relatively lower

levels of activity on the supply side - approx. 2.5 – 3.0 million sft for the past 5 years. Majority of the

stock that has been introduced from 2013 to 2017 are later phases of large developments / SEZ’s set up

in prior years. Therefore, a decline in the supply trend has been witnessed in the last few years thereby

leading to graduation reduction in vacancy levels to approx. 13%.

C. Spatial spread of Commercial activity in Chennai

The commercial office market space in Chennai is divided into the following vectors:

Spatial Spread Split of Cumulative supply by region

( t otal 63 mn sft)

CBD: CBD & Off CBD – 25%

SBD: MPR & Taramani + OMR 1 – 41%

PBD: Ambattur, GST, OMR 2 & 3 – 34%

Source: CBRE Research

Figure 13

Graph 3

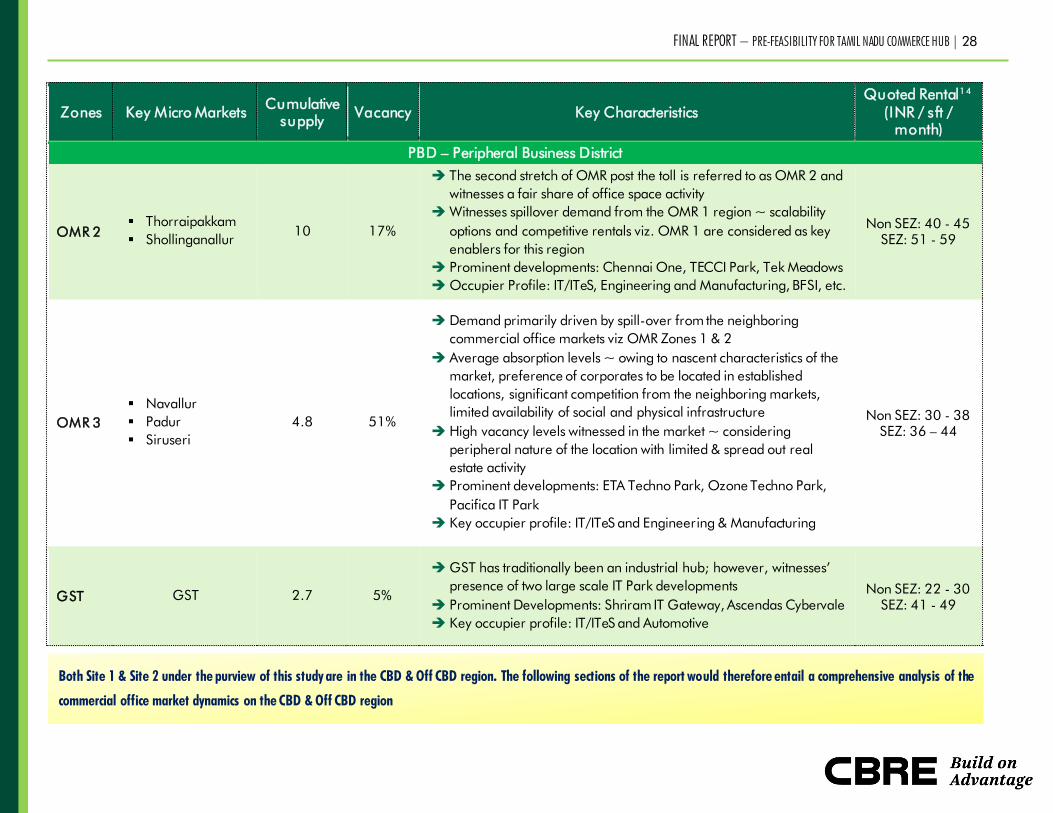

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 26

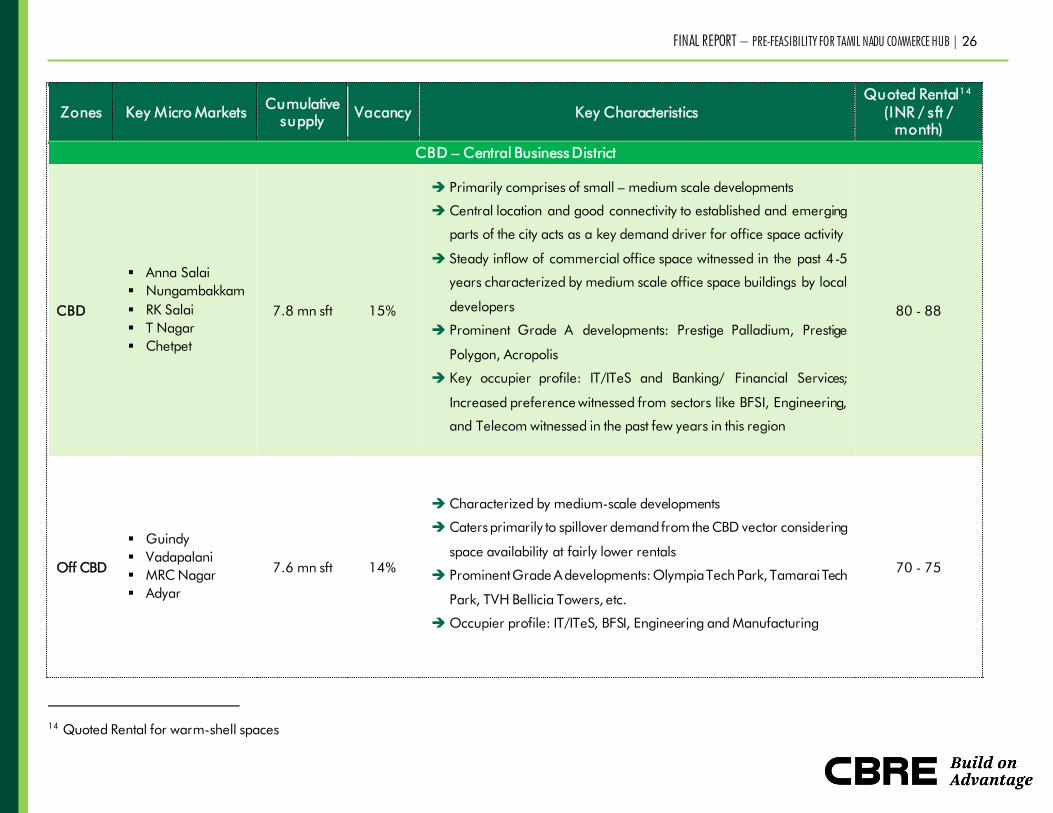

Zones Key Micro Markets Cumulative

supply Vacancy Key Characteristics

Quoted Rental1 4

(INR / sft /

month)

CBD – Central Business District

CBD

▪ Anna Salai

▪ Nungambakkam

▪ RK Salai

▪ T Nagar

▪ Chetpet

7.8 mn sft 15%

Primarily comprises of small – medium scale developments

Central location and good connectivity to established and emerging

parts of the city acts as a key demand driver for office space activity

Steady inflow of commercial office space witnessed in the past 4-5

years characterized by medium scale office space buildings by local

developers

Prominent Grade A developments: Prestige Palladium, Prestige

Polygon, Acropolis

Key occupier profile: IT/ITeS and Banking/ Financial Services;

Increased preference witnessed from sectors like BFSI, Engineering,

and Telecom witnessed in the past few years in this region

80 - 88

Off CBD

▪ Guindy

▪ Vadapalani

▪ MRC Nagar

▪ Adyar

7.6 mn sft 14%

Characterized by medium-scale developments

Caters primarily to spillover demand from the CBD vector considering

space availability at fairly lower rentals

Prominent Grade A developments: Olympia Tech Park, Tamarai Tech

Park, TVH Bellicia Towers, etc.

Occupier profile: IT/ITeS, BFSI, Engineering and Manufacturing

70 - 75

14 Quoted Rental for warm-shell spaces

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 27

Zones Key Micro Markets Cumulative

supply Vacancy Key Characteristics

Quoted Rental1 4

(INR / sft /

month)

SBD – Secondary Business District

OMR 1

▪ Taramani

▪ Perungudi

▪ Kandanchavadi

18.6 mn sft 3%

Most preferred IT/ITeS destination in the city ~ highest share of

investment grade commercial office space supply is present in this

micro-market

Majority of the supply in the region is constituted by investment grade

large IT Parks/ SEZ developments by Tier 1 National level developers

The location has emerged as the most preferred office space market

for IT/ ITeS tenants and witnesses limited/ negligible vacancy levels

Prominent Grade A developments: Ramanujam IT City, SP Infocity,

RMZ Millenia

Occupier Profile: IT/ITeS, Engineering and Manufacturing,

Automotive, etc.

Non SEZ: 76 - 84

SEZ: 91 – 99

MPR

▪ Manapakkam,

▪ Mount

Poonamallee

Road

7.2 5%

Evolved as an Alternate Business District and an established

commercial office space destination owing to the presence of a single

large Grade A SEZ development viz. DLF Tech Park (approx. 6.4

million sft)

DLF IT Park is considered as one of the most successful IT SEZ

developments in the city owing to the quality of development,

branding of the developer in the office space business, connectivity

attributes, proximity to residential markets, etc. ~ reflective of

consistent demand, negligible vacancy levels and pre-commitments

witnessed across under construction blocks

Prominent Grade A developments: DLF IT Park, Jayant Tech Park

Occupier Profile: IT/ITeS, BFSI, etc.

Non SEZ: 61 - 69

SEZ: 71 – 79

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 28

Zones Key Micro Markets Cumulative

supply Vacancy Key Characteristics

Quoted Rental1 4

(INR / sft /

month)

PBD – Peripheral Business District

OMR 2

▪ Thorraipakkam

▪ Shollinganallur 10 17%

The second stretch of OMR post the toll is referred to as OMR 2 and

witnesses a fair share of office space activity

Witnesses spillover demand from the OMR 1 region ~ scalability

options and competitive rentals viz. OMR 1 are considered as key

enablers for this region

Prominent developments: Chennai One, TECCI Park, Tek Meadows

Occupier Profile: IT/ITeS, Engineering and Manufacturing, BFSI, etc.

Non SEZ: 40 - 45

SEZ: 51 - 59

OMR 3

▪ Navallur

▪ Padur

▪ Siruseri

4.8 51%

Demand primarily driven by spill-over from the neighboring

commercial office markets viz OMR Zones 1 & 2

Average absorption levels ~ owing to nascent characteristics of the

market, preference of corporates to be located in established

locations, significant competition from the neighboring markets,

limited availability of social and physical infrastructure

High vacancy levels witnessed in the market ~ considering

peripheral nature of the location with limited & spread out real

estate activity

Prominent developments: ETA Techno Park, Ozone Techno Park,

Pacifica IT Park

Key occupier profile: IT/ITeS and Engineering & Manufacturing

Non SEZ: 30 - 38

SEZ: 36 – 44

GST GST 2.7 5%

GST has traditionally been an industrial hub; however, witnesses’

presence of two large scale IT Park developments

Prominent Developments: Shriram IT Gateway, Ascendas Cybervale

Key occupier profile: IT/ITeS and Automotive

Non SEZ: 22 - 30

SEZ: 41 - 49

Both Site 1 & Site 2 under the purview of this study are in the CBD & Off CBD region. The following sections of the report would therefore entail a comprehensive analysis of the

commercial office market dynamics on the CBD & Off CBD region

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 29

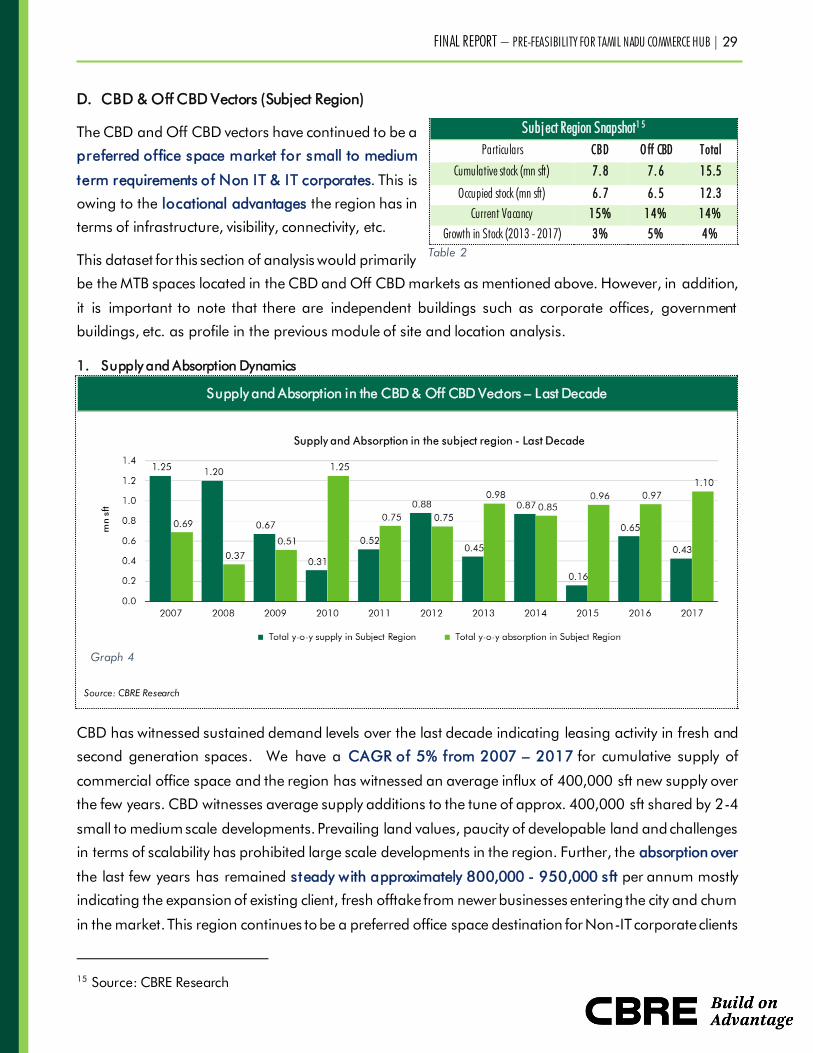

D. CBD & Off CBD Vectors (Subject Region)

The CBD and Off CBD vectors have continued to be a

preferred office space market for small to medium

term requirements of Non IT & IT corporates. This is

owing to the locational advantages the region has in

terms of infrastructure, visibility, connectivity, etc.

This dataset for this section of analysis would primarily

be the MTB spaces located in the CBD and Off CBD markets as mentioned above. However, in addition,

it is important to note that there are independent buildings such as corporate offices, government

buildings, etc. as profile in the previous module of site and location analysis.

1. Supply and Absorption Dynamics

Supply and Absorption in the CBD & Off CBD Vectors – Last Decade

Source: CBRE Research

CBD has witnessed sustained demand levels over the last decade indicating leasing activity in fresh and

second generation spaces. We have a CAGR of 5% from 2007 – 2017 for cumulative supply of

commercial office space and the region has witnessed an average influx of 400,000 sft new supply over

the few years. CBD witnesses average supply additions to the tune of approx. 400,000 sft shared by 2-4

small to medium scale developments. Prevailing land values, paucity of developable land and challenges

in terms of scalability has prohibited large scale developments in the region. Further, the absorption over

the last few years has remained steady with approximately 800,000 - 950,000 sft per annum mostly

indicating the expansion of existing client, fresh offtake from newer businesses entering the city and churn

in the market. This region continues to be a preferred office space destination for Non-IT corporate clients

15 Source: CBRE Research

Subj ect Region Snapshot1 5

Particulars CBD O ff CBD Total

Cumulative stock (mn sft) 7. 8 7. 6 15.5

Occupied stock (mn sft) 6. 7 6. 5 12.3

Current Vacancy 15% 14% 14%

Growth in Stock (2013 - 2017) 3% 5% 4%

Table 2

Graph 4

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 30

and front offices of large IT Corporates. Also, the current vacancy is at approx. 14% which is comparable

to the overall vacancy levels in the city. Majority of the vacancy in the market is reflective of newer

development completions (40% of developments that are completed over the last 3 years) and vacancy

in older buildings that are not attractive for clients. Further, based on the current trend of absorption and

considering the new supply which would enter the market in the next two years, we understand that there

would is a supply overhang of ~1.5 - 2 years for marketable spaces in the region.

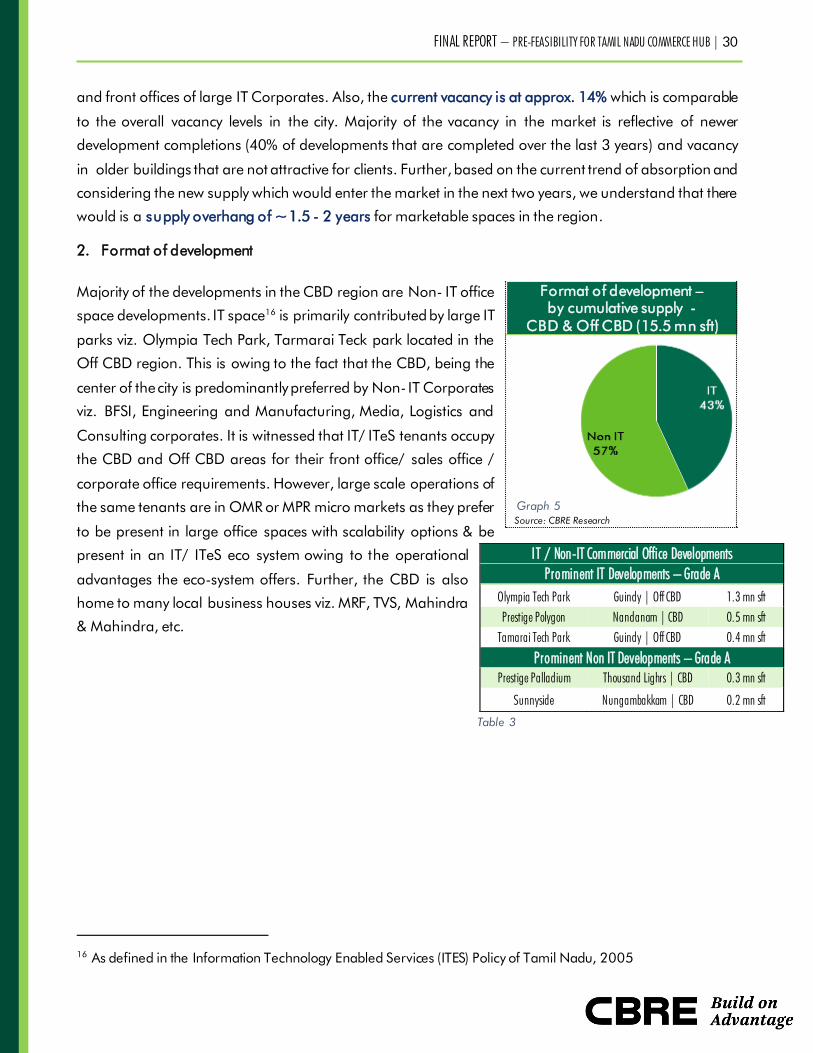

2. Format of development

Majority of the developments in the CBD region are Non- IT office

space developments. IT space16

is primarily contributed by large IT

parks viz. Olympia Tech Park, Tarmarai Teck park located in the

Off CBD region. This is owing to the fact that the CBD, being the

center of the city is predominantly preferred by Non- IT Corporates

viz. BFSI, Engineering and Manufacturing, Media, Logistics and

Consulting corporates. It is witnessed that IT/ ITeS tenants occupy

the CBD and Off CBD areas for their front office/ sales office /

corporate office requirements. However, large scale operations of

the same tenants are in OMR or MPR micro markets as they prefer

to be present in large office spaces with scalability options & be

present in an IT/ ITeS eco system owing to the operational

advantages the eco-system offers. Further, the CBD is also

home to many local business houses viz. MRF, TVS, Mahindra

& Mahindra, etc.

16 As defined in the Information Technology Enabled Services (ITES) Policy of Tamil Nadu, 2005

Format of development –

by cumulative supply -

CBD & Off CBD (15.5 mn sft)

Source: CBRE Research

IT / Non-IT Commercial Office Developments

Prominent IT Developments – Grade A

Olympia Tech Park Guindy | Off CBD 1.3 mn sft

Prestige Polygon Nandanam | CBD 0.5 mn sft

Tamarai Tech Park Guindy | Off CBD 0.4 mn sft

Prominent Non IT Developments – Grade A

Prestige Palladium Thousand Lighrs | CBD 0.3 mn sft

Sunnyside Nungambakkam | CBD 0.2 mn sft

Table 3

Graph 5

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 31

3. Grade of Commercial Office Space Developments

Further, the grade of office space development from a

CBD and Off CBD context have played a major role as

they are one of the areas to offer organized office

spaces. Considering the same viz. the age of the

building and the specifications offered, a significant

share of the supply in the CBD & Off CBD region are

today classified as Grade B & C developments.

However, large scale IT Parks in the off CBD region are

predominantly Grade A quality.17

IT commercial office space developments contribute to

approx. 43% of the cumulative supply ~ majority of

which are located in the Off CBD region. Further, we

understand that rentals for developments typically take

the Grade of development as an important parameter

~ the lack of amenities / specifications provided in

Grade B & C developments act as a deterrent for demand & achieving rentals

4. Scale of development

Considering the location, availability of land, prevailing land values and development potential, small to

medium scale buildings are predominant in the CBD & Off CBD regions.

Scale of Developments - By number of developments & size in sft

Source: CBRE Research

17 Grade of development is typically reflective of the specifications and amenities offered, age of the building, parking,

professional building and facilities management, maintenance and upkeep, etc.

Format of development – by cumulative

supply in the CBD & Off CBD (15.5 mn sft)

Source: CBRE Research

Graph 7

Graph 8

Graph 6

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 32

Majority of the developments in the subject region are typically less than 150,000 sft in scale (~75%).

Olympia Tech Park and Tamarai Tech Park in Guindy (Off CBD region) are the largest campus style

developments upwards of 300,000 sft. SBD and PBD areas in the city offer large scale IT Parks and SEZ

developments over 1 mn sft.

5. Analysis of Occupiers

5.1. Typical Occupier Profile

The exhibit below represents the occupier profile of tenants located in the commercial off space

developments in the CBD and Off CBD region. The exhibit below is an illustration of the office space

uptake by specific sectors in the region:

Current Occupier Profile in Subject

Region

Occupier profile split in CBD & Off CBD

Source: CBRE Research

Majority of occupiers in the region are (~36%) are IT / BPO /

KPO Corporates; however, it is observed that approx. 65% of

these are located in the Off CBD region, particularly

contributed by the presence of large scale IT developments viz.

Olympia Tech Park & Tamarai Tech park in the region ~

IT/ITeS prefer large spaces and larger floor plates which are

not prevalent in the CBD region.

Further, the Non IT tenant categories driving demand for office

space include BFSI, Engineering and Manufacturing, Research

& Consulting, Media and logistics. We also understand, that

these occupiers typically are present in the CBD Region viz.

the Off CBD region.

Prominent occupiers by segments

IT / ITeS

Verizon TCS Oracle

HP Wipro HCL

BFSI

BNP Paribas HDFC Citibank

ABN AMRO RBS ICICI Bank

Engineering and Manufacturing

Ansaldo Siemens Exide industries ltd

Philips Future Metals St. Gobain

Others

RR Donelley Hewitt Regus

HTC Mascon global Samsung

Table 4

Graph 9

Graph 10

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 33

5.2. Scale of transactions (in sft)

In this section, we have analyzed the scale / size of transactions (in sf) that have been witnessed in CBD

and off CBD regions in the last three years.

The CBD and off CBD region witnesses majority of

t ransactions in the 5,000 – 15,000 sft range per transaction

~ approx. 55%

< 5,000 sft: Key absorption witnessed in Media, Logistics,

Research & consulting occupier segments

5,000 – 10,000 sft: Majority of these transactions comprise

of tenants in the IT/ITeS, BFSI & Engineering segments

10,000 – 15,000 sft: Approx. 50% of occupiers in this size

segment are IT/ITeS occupiers; further, majority of them are located in the off CBD owing to availability of

IT developments, large floor plates, etc. are present in the off CBD region

The IT/ITeS sector followed by BFSI, Engineering and Manufacturing, Research & Consulting are the key

occupier segments in this region. Further, average space per transaction offtake is highest in IT

Commercial developments & in developments located in the off CBD zone.

Majority of the leases in the CBD and off CBD region are witnessed to be warm shell spaces with

typically lease terms of 3+ 3+ 3 years with 15% escalations built in every three years

Typical scale of transaction

Source: CBRE Research

Development Name Company Name Area transacted (sft) Rentals (psft / month)

CBD

Prestige Palladium Pfizer 16,000 sft INR 75

Prestige Polygon Gigamon 17,000 sft INR 82

Arihant Nitco Park Benteler 7,700 sft INR 60

Prestige Polygon Toray Industries 5,500 sft INR 75

Lebera Towers BAF 4,500 sft INR 65

Off CBD

Kochar Bliss Apex Knowledge

Solutions 9,000 sft INR 63

TVH Beliciaa towers CAMS 29,000 sft INR 60

Table 5

Graph 11

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 34

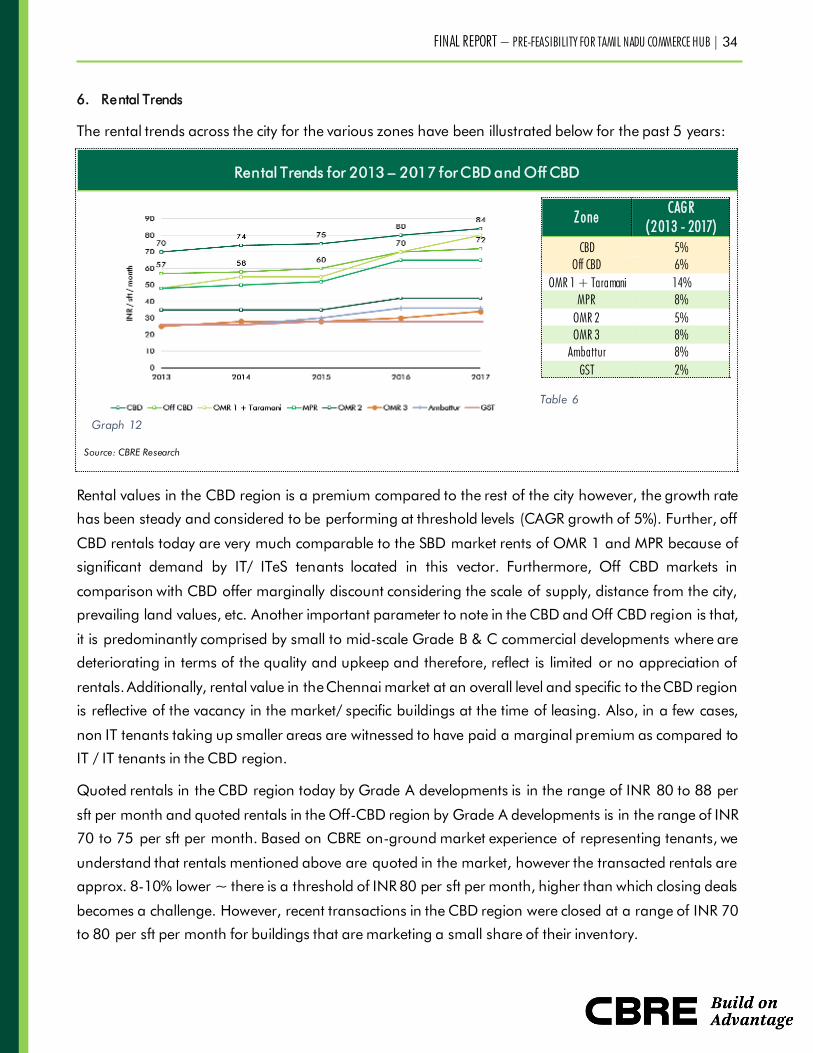

6. Rental Trends

The rental trends across the city for the various zones have been illustrated below for the past 5 years:

Rental Trends for 2013 – 2017 for CBD and Off CBD

Table 6

Source: CBRE Research

Zone CAGR

(2013 - 2017)

CBD 5%

Off CBD 6%

OMR 1 + Taramani 14%

MPR 8%

OMR 2 5%

OMR 3 8%

Ambattur 8%

GST 2%

Rental values in the CBD region is a premium compared to the rest of the city however, the growth rate

has been steady and considered to be performing at threshold levels (CAGR growth of 5%). Further, off

CBD rentals today are very much comparable to the SBD market rents of OMR 1 and MPR because of

significant demand by IT/ ITeS tenants located in this vector. Furthermore, Off CBD markets in

comparison with CBD offer marginally discount considering the scale of supply, distance from the city,

prevailing land values, etc. Another important parameter to note in the CBD and Off CBD region is that,

it is predominantly comprised by small to mid-scale Grade B & C commercial developments where are

deteriorating in terms of the quality and upkeep and therefore, reflect is limited or no appreciation of

rentals. Additionally, rental value in the Chennai market at an overall level and specific to the CBD region

is reflective of the vacancy in the market/ specific buildings at the time of leasing. Also, in a few cases,

non IT tenants taking up smaller areas are witnessed to have paid a marginal premium as compared to

IT / IT tenants in the CBD region.

Quoted rentals in the CBD region today by Grade A developments is in the range of INR 80 to 88 per

sft per month and quoted rentals in the Off-CBD region by Grade A developments is in the range of INR

70 to 75 per sft per month. Based on CBRE on-ground market experience of representing tenants, we

understand that rentals mentioned above are quoted in the market, however the transacted rentals are

approx. 8-10% lower ~ there is a threshold of INR 80 per sft per month, higher than which closing deals

becomes a challenge. However, recent transactions in the CBD region were closed at a range of INR 70

to 80 per sft per month for buildings that are marketing a small share of their inventory.

Graph 12

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 35

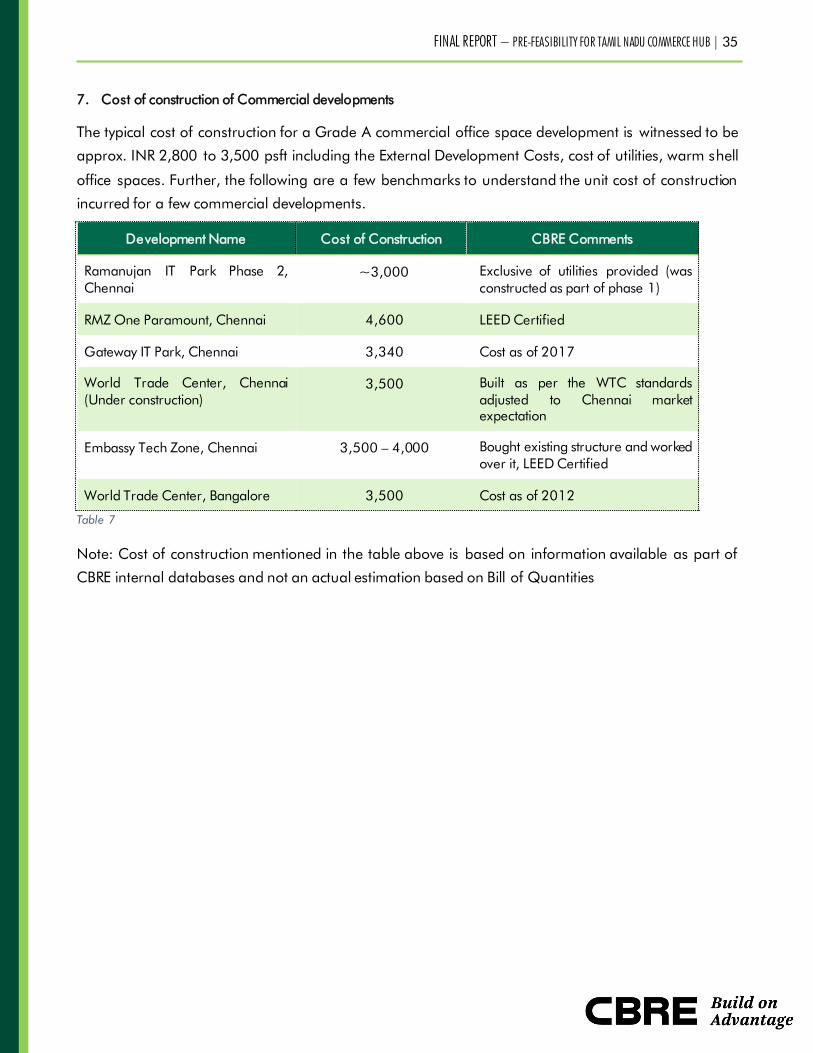

7. Cost of construction of Commercial developments

The typical cost of construction for a Grade A commercial office space development is witnessed to be

approx. INR 2,800 to 3,500 psft including the External Development Costs, cost of utilities, warm shell

office spaces. Further, the following are a few benchmarks to understand the unit cost of construction

incurred for a few commercial developments.

Development Name Cost of Construction CBRE Comments

Ramanujan IT Park Phase 2,

Chennai

~3,000 Exclusive of utilities provided (was

constructed as part of phase 1)

RMZ One Paramount, Chennai 4,600 LEED Certified

Gateway IT Park, Chennai 3,340 Cost as of 2017

World Trade Center, Chennai

(Under construction)

3,500 Built as per the WTC standards

adjusted to Chennai market

expectation

Embassy Tech Zone, Chennai 3,500 – 4,000 Bought existing structure and worked

over it, LEED Certified

World Trade Center, Bangalore 3,500 Cost as of 2012

Table 7

Note: Cost of construction mentioned in the table above is based on information available as part of

CBRE internal databases and not an actual estimation based on Bill of Quantities

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 36

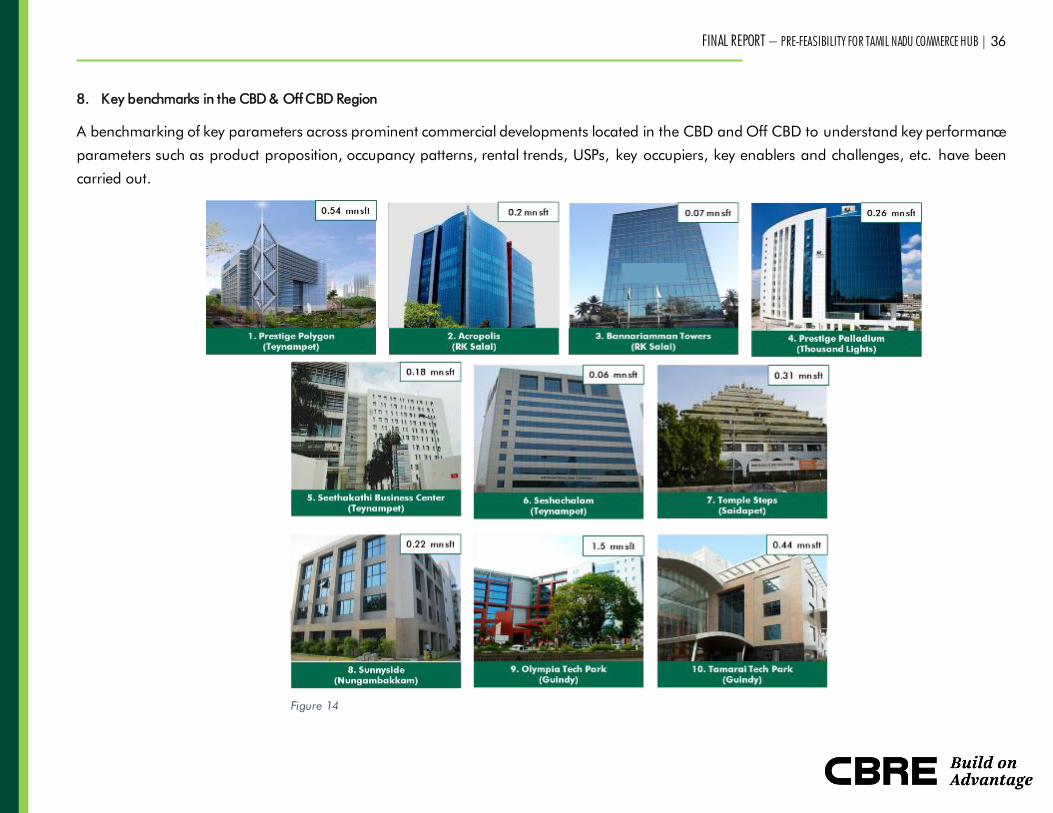

8. Key benchmarks in the CBD & Off CBD Region

A benchmarking of key parameters across prominent commercial developments located in the CBD and Off CBD to understand key performance

parameters such as product proposition, occupancy patterns, rental trends, USPs, key occupiers, key enablers and challenges, etc. have been

carried out.

Figure 14

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 37

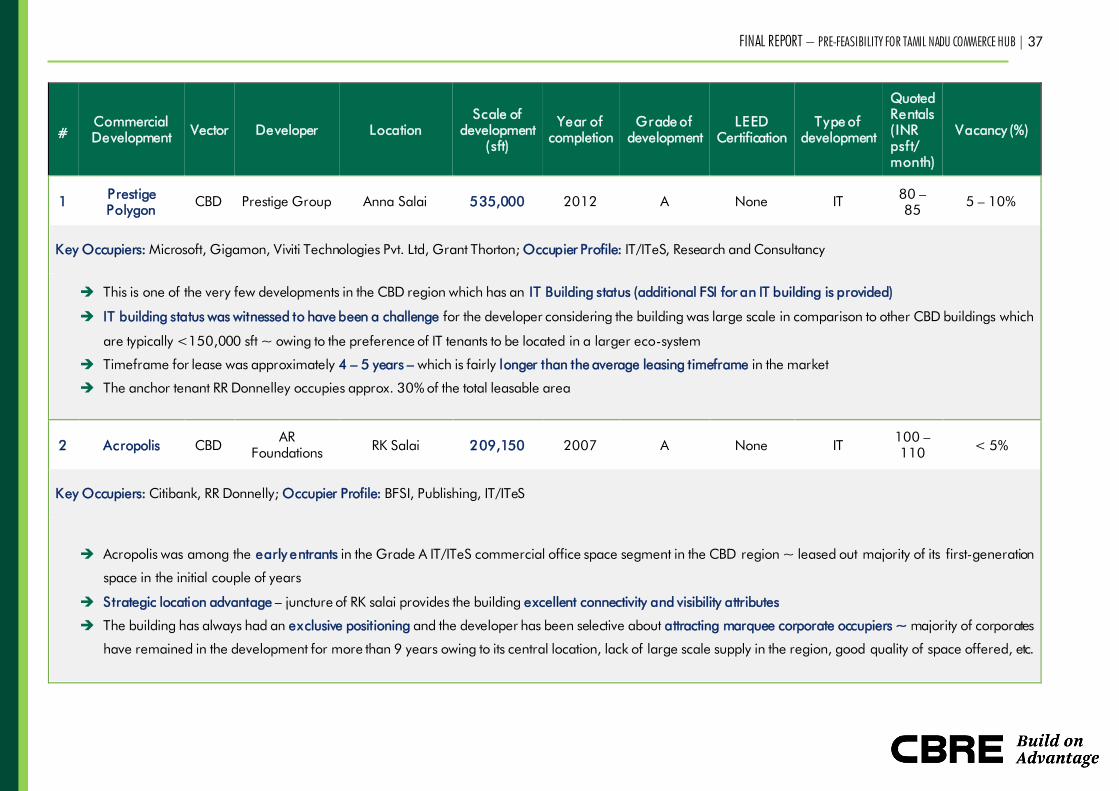

#

Commercial

Development Vector Developer Location

Scale of

development

(sft)

Year of

completion

Grade of

development

LEED

Certification

Type of

development

Quoted

Rentals

( INR

psft/

month)

Vacancy (%)

1 Prestige

Polygon CBD Prestige Group Anna Salai 535,000 2012 A None IT

80 –

85 5 – 10%

Key Occupiers: Microsoft, Gigamon, Viviti Technologies Pvt. Ltd, Grant Thorton; Occupier Profile: IT/ITeS, Research and Consultancy

This is one of the very few developments in the CBD region which has an IT Building status (additional FSI for an IT building is provided)

IT building status was witnessed to have been a challenge for the developer considering the building was large scale in comparison to other CBD buildings which

are typically <150,000 sft ~ owing to the preference of IT tenants to be located in a larger eco-system

Timeframe for lease was approximately 4 – 5 years – which is fairly longer than the average leasing timeframe in the market

The anchor tenant RR Donnelley occupies approx. 30% of the total leasable area

2 Acropolis CBD AR

Foundations RK Salai 209,150 2007 A None IT

100 –

110 < 5%

Key Occupiers: Citibank, RR Donnelly; Occupier Profile: BFSI, Publishing, IT/ITeS

Acropolis was among the early entrants in the Grade A IT/ITeS commercial office space segment in the CBD region ~ leased out majority of its first-generation

space in the initial couple of years

Strategic location advantage – juncture of RK salai provides the building excellent connectivity and visibility attributes

The building has always had an exclusive positioning and the developer has been selective about attracting marquee corporate occupiers ~ majority of corporates

have remained in the development for more than 9 years owing to its central location, lack of large scale supply in the region, good quality of space offered, etc.

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 38

#

Commercial

Development Vector Developer Location

Scale of

development

(sft)

Year of

completion

Grade of

development

LEED

Certification

Type of

development

Quoted

Rentals

( INR

psft/

month)

Vacancy (%)

3 Bannariamman

Towers CBD Bannariamman RK Salai 67,000 2010 A None Non IT

75 –

80 5 - 10%

Key Occupiers: Mitsubishi, Zynergy Solar, Schneider Electric, French Consulate, Korean Trade Center; Occupier Profile: Automobile, Electronics, Foreign Bodies

Bannariamman towers been judicious while leasing space to occupiers in order to maintain the positioning for the development - houses a consulate, foreign

trade bodies, FMCG & Automobile giants

This development has occupiers across various non IT tenant categories and would be one of the very few developments which does not house a single IT/ ITeS

tenant (no significant need to have an anchor tenant considering the scale of development)

4 Prestige

Palladium CBD Prestige Greams Road 260,000 2011 A None Non IT 80 < 5%

Key Occupiers: Saipem, PWC, Mitsubishi, HP, Hospira; Occupier Profile: Engineering & Manufacturing, IT/ITeS, Professional Services

Prestige Palladium majorly houses Non IT occupiers across various tenant categories

The key USPs of this development would be its central location, developer branding, rational rental for a grade A space offered, etc.

5

Seethakathi

Business

Center

CBD ETA Star Teynampet 182,000 2014 A Gold Rated Non IT 80 55-60%

Key Occupiers: Siemens, Cresent School of Business; Occupier Profile: Engineering & Manufacturing

One of the drawbacks that the development has faced is that it has been strata sold. Multiple owner developments are typically less preferred by occupiers

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 39

#

Commercial

Development Vector Developer Location

Scale of

development

(sft)

Year of

completion

Grade of

development

LEED

Certification

Type of

development

Quoted

Rentals

( INR

psft/

month)

Vacancy (%)

6 Seshachalam

Center CBD Ceebros Anna Salai 64,000 2008 B None Non IT 75 15-20%

Key Occupiers: Bank of Tokyo, JETRO, Butterfly, Hero Motocorp; Occupier Profile: BFSI, Engineering & Manufacturing

A unique factor witnessed in this development is the predominant presence of Japanese corporates which has enabled a specific positioning for the building

7 Temple Steps CBD Individual Anna Salai 307,000 2005 B None Non IT 60 <5%

Key Occupiers: Citigroup, DHL, Zifo Group, Stayzilla, Agility Logistics; Occupier Profile: IT/ ITeS, Logistics, Media

Temple steps was one of the first commercial office spaces constructed in the city; Further, the development has been strata sold and has multiple ownership

It is an old development ~ provides for a significant discount from the market

8 Sunnyside CBD Sabari Group Nungambakkam 220,000 2012 A None Non IT 75 <5%

Key Occupiers: Bosch, Deutsche Bank, PPP Power Generation Company, Pfizer, Apollo Hospitals; Occupier Profile: Engineering & Manufacturing, Banks, Healthcare

9 Olympia Tech

Park

Off

CBD Olympia Guindy 1,453,000 2006 A Green IT 85 5-10%

Key Occupiers: HP, Verizon, RBS, Visteon, Dell; Occupier Profile: IT/ITeS

One and only IT Park development offering the benefits of being in a large campus style development with amenities such as food court, good car parking, etc.

in the CBD region. This development had a f irst mover advantage when it was constructed in Guindy in 2006

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 40

#

Commercial

Development Vector Developer Location

Scale of

development

(sft)

Year of

completion

Grade of

development

LEED

Certification

Type of

development

Quoted

Rentals

( INR

psft/

month)

Vacancy (%)

Further, it was one of first developments to receive an IGBC certification which was one of its USPs

Average achieved rentals in the building is significantly lower than the market on account of more than 50% of the space being leased to anchor tenants of HP

and Verizon who have stayed in the building since inception

It is important to note that HP who is a large space occupier from a overall Chennai context has expanded in multiple locations but continues to hold space in the

development; Attractive lease rentals have been negotiated at the time of lease renewals to continue occupancy in the building

10 Tamarai Tech

Park

Off

CBD

Ashok Matches

& Timber

Industries Pvt.

Ltd

Guindy 440,000 2007 A None IT 75 < 5%

Key Occupiers: ABCO Advisory, Matt McDonald, Erricson; Occupier Profile: Research and Consulting, Engineering & Manufacturing

Tamarai tech park located adjacent to Olympia was the next largest development in the region which witnessed good traction as an IT Park development in an

off CBD market

Majority of the pr imary leasing occurred in the f irst two years to anchor tenants ~ Approx. 50% of space was leased to a large Engineering and Manufacturing

sector tenant who still occupies the development

Table 8

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 41

Case Study – TIDEL Park, Chennai

TIDEL Park, Chennai has been developed as a joint venture between TIDCO & ELCOT in 2000. The development

marked the beginning of commerical office space activity along ‘Rajiv Gandhi Salai’, the designated IT

corridor of Chennai. The IT park comprises of a built up area of approx. 1.2 million sft ~ a iconic development

of its time considered to be a forerunner for IT/ITeS activity in the city. The success of the development posed as a

catalyst to TIDCO who also ventured into joint developments with Tata Realty and Ascendas to mark a start of the

IT eco-system in the city.

The key objective of TIDEL Park was to provide necessary infrastructure for IT/ITeS clients therby promoting the

IT/ITeS industry in the city. TIDEL park had achieved 100% accupancy post 3 months of its inaguration. Approx.

20% of the commerical space developed was strata sold to nine companies and approx. 820,000 sft of

commercial space was leased out to 30 – 35 corporates.

In the initial phase, the development witnessed absorption from 6 – 7 corporates who took up approx. 50% of the

leasable area ranging between 35,000 – 100,000 sft per corporate. Further, we also understand that TIDEL has

maintained a 100% occupancy for most part of its existence. The rental realised for the development in its early

stages was approx. INR 50 – 55 psft per month, however the same declined to INR 40 – 45 psft per month owing

to the global economic crisis in 2008. The same has improved over time and currenlty, the average achived rental

is INR 49 – 50 psft per month. Additionally, a flat rental system is followed, wherin all the tenants pay the same

rental irrespective of the space occupied by them.

Apart from commercial office space, the development also houses a food court, retail outlets, gymnasium, day care, auditorium facilities, etc. to cater to the

working populace in the development. The building has been designed as 4 blocks and 8 modules with large common areas resuling in an efficiency of 60

– 65% which is significatly lower than the market average of effeciency of 80 – 85%. This has posed as a great challenge to them while the consideration of

rental escalations. Further, we also witnessed that approx. 75% of the tenants (INautix, TCS, Ajuba Solutions, Cognizant, etc.) who are currently present in

TIDEL Park have occupied the development from 2000 – 2001 ~ tendancy to stay at TIDEL over a long period owing to locational and rental advantage.

Snapshot

Commencement 2000

Location Taramani, Chennai

Ownership Government

Key Partners TIDCO, ELCOT

Area 1.28 mn sft

TIDEL Park, Chennai

Table 9

Table 10

TIDEL Park was one of the first IT developments in the country to be backed by the Government. The development was instrument al to mark the start the IT revolution in the

city. The product mix offered in terms of specifications and amenities was considered futuristic and the building was perceived to be an iconic lan dmark in the region. The

world class development motivated large national and international corporates to be part of this monumenta l development.

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 42

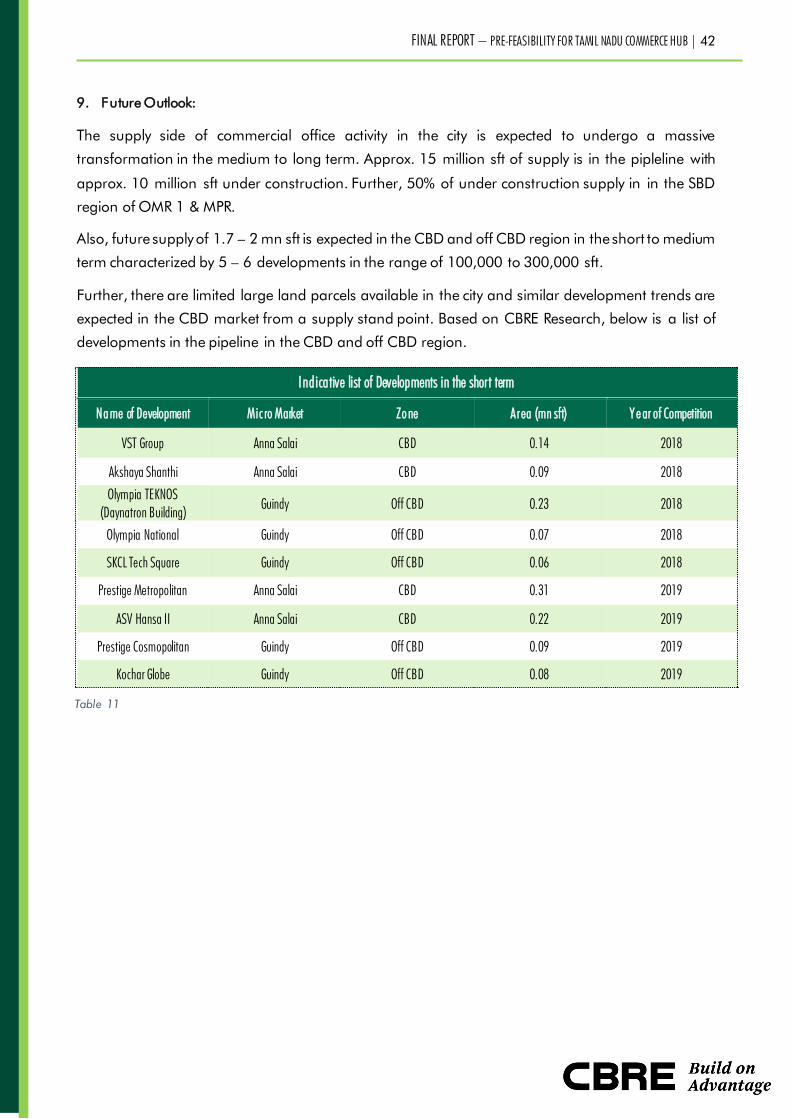

9. Future Outlook:

The supply side of commercial office activity in the city is expected to undergo a massive

transformation in the medium to long term. Approx. 15 million sft of supply is in the pipleline with

approx. 10 million sft under construction. Further, 50% of under construction supply in in the SBD

region of OMR 1 & MPR.

Also, future supply of 1.7 – 2 mn sft is expected in the CBD and off CBD region in the short to medium

term characterized by 5 – 6 developments in the range of 100,000 to 300,000 sft.

Further, there are limited large land parcels available in the city and similar development trends are

expected in the CBD market from a supply stand point. Based on CBRE Research, below is a list of

developments in the pipeline in the CBD and off CBD region.

Indicative list of Developments in the short term

Name of Development Mic ro Market Zone Area (mn sft) Y e ar of Competition

VST Group Anna Salai CBD 0.14 2018

Akshaya Shanthi Anna Salai CBD 0.09 2018

Olympia TEKNOS

(Daynatron Building) Guindy Off CBD 0.23 2018

Olympia National Guindy Off CBD 0.07 2018

SKCL Tech Square Guindy Off CBD 0.06 2018

Prestige Metropolitan Anna Salai CBD 0.31 2019

ASV Hansa II Anna Salai CBD 0.22 2019

Prestige Cosmopolitan Guindy Off CBD 0.09 2019

Kochar Globe Guindy Off CBD 0.08 2019

Table 11

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 43

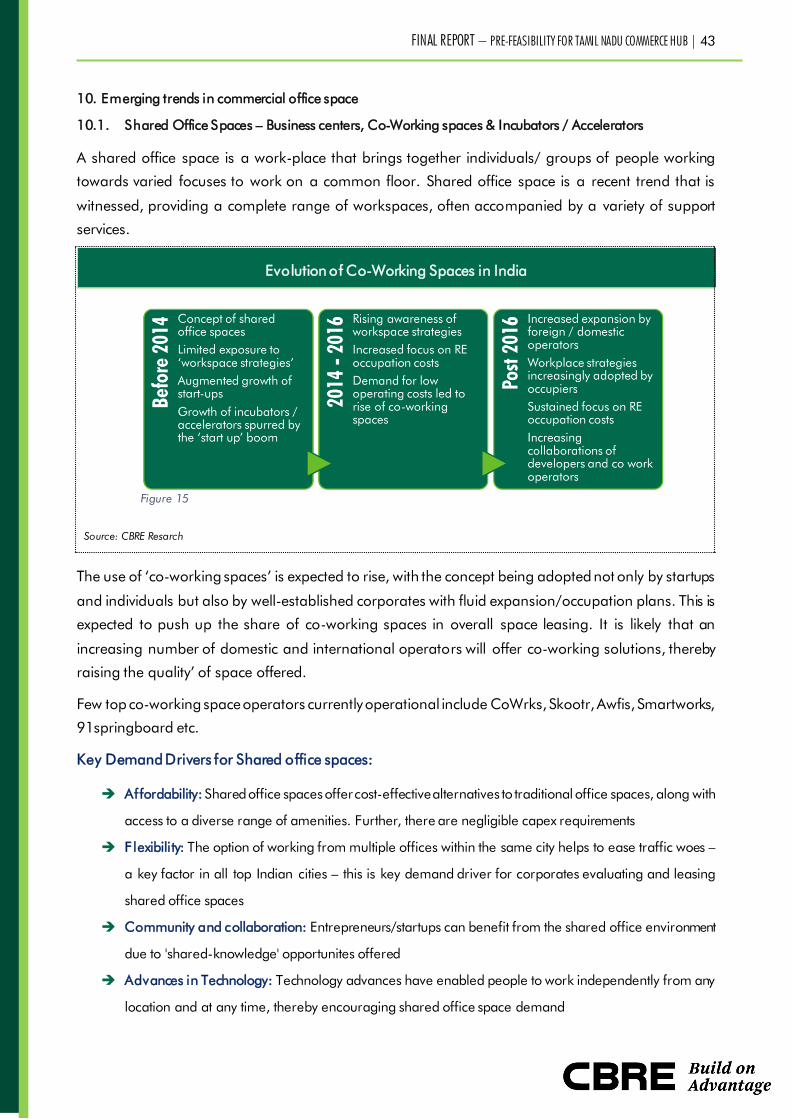

10. Emerging trends in commercial office space

10.1. Shared Office Spaces – Business centers, Co-Working spaces & Incubators / Accelerators

A shared office space is a work-place that brings together individuals/ groups of people working

towards varied focuses to work on a common floor. Shared office space is a recent trend that is

witnessed, providing a complete range of workspaces, often accompanied by a variety of support

services.

Evolution of Co-Working Spaces in India

Source: CBRE Resarch

The use of ‘co-working spaces’ is expected to rise, with the concept being adopted not only by startups

and individuals but also by well-established corporates with fluid expansion/occupation plans. This is

expected to push up the share of co-working spaces in overall space leasing. It is likely that an

increasing number of domestic and international operators will offer co-working solutions, thereby

raising the quality’ of space offered.

Few top co-working space operators currently operational include CoWrks, Skootr, Awfis, Smartworks,

91springboard etc.

Key Demand Drivers for Shared office spaces:

Affordability: Shared office spaces offer cost-effective alternatives to traditional office spaces, along with

access to a diverse range of amenities. Further, there are negligible capex requirements

Flexibility: The option of working from multiple offices within the same city helps to ease traffic woes –

a key factor in all top Indian cities – this is key demand driver for corporates evaluating and leasing

shared office spaces

Community and collaboration: Entrepreneurs/startups can benefit from the shared office environment

due to 'shared-knowledge' opportunites offered

Advances in Technology: Technology advances have enabled people to work independently from any

location and at any time, thereby encouraging shared office space demand

Figure 15

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 44

The Startup Boom: Startups are among the major users of shared office spaces, with India estimated to

have 11,500 startups18

by 2020

Forign entrant corporates: Co-working spaces are an ideal option for corporates testing Indian waters

due to their cost-effective and flexible leasing term

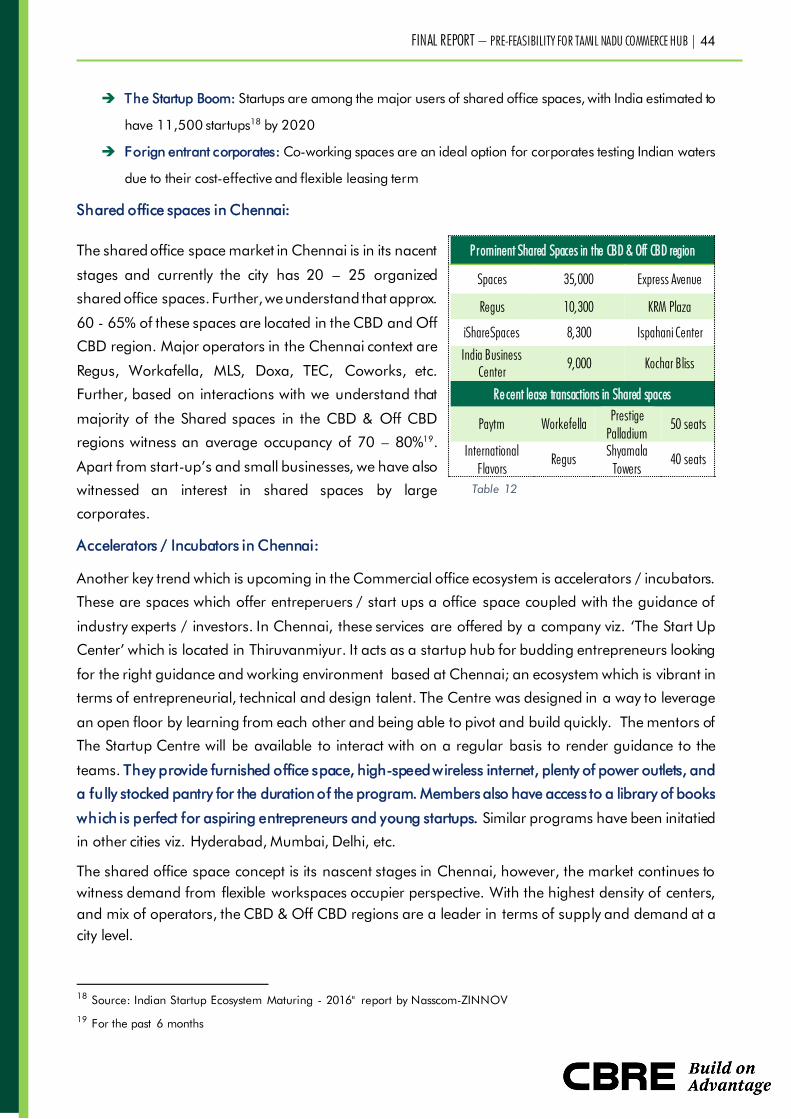

Shared office spaces in Chennai:

The shared office space market in Chennai is in its nacent

stages and currently the city has 20 – 25 organized

shared office spaces. Further, we understand that approx.

60 - 65% of these spaces are located in the CBD and Off

CBD region. Major operators in the Chennai context are

Regus, Workafella, MLS, Doxa, TEC, Coworks, etc.

Further, based on interactions with we understand that

majority of the Shared spaces in the CBD & Off CBD

regions witness an average occupancy of 70 – 80%19

.

Apart from start-up’s and small businesses, we have also

witnessed an interest in shared spaces by large

corporates.

Accelerators / Incubators in Chennai:

Another key trend which is upcoming in the Commercial office ecosystem is accelerators / incubators.

These are spaces which offer entreperuers / start ups a office space coupled with the guidance of

industry experts / investors. In Chennai, these services are offered by a company viz. ‘The Start Up

Center’ which is located in Thiruvanmiyur. It acts as a startup hub for budding entrepreneurs looking

for the right guidance and working environment based at Chennai; an ecosystem which is vibrant in

terms of entrepreneurial, technical and design talent. The Centre was designed in a way to leverage

an open floor by learning from each other and being able to pivot and build quickly. The mentors of

The Startup Centre will be available to interact with on a regular basis to render guidance to the

teams. They provide furnished office space, high-speed wireless internet, plenty of power outlets, and

a fully stocked pantry for the duration of the program. Members also have access to a library of books

which is perfect for aspiring entrepreneurs and young startups. Similar programs have been initatied

in other cities viz. Hyderabad, Mumbai, Delhi, etc.

The shared office space concept is its nascent stages in Chennai, however, the market continues to

witness demand from flexible workspaces occupier perspective. With the highest density of centers,

and mix of operators, the CBD & Off CBD regions are a leader in terms of supply and demand at a

city level.

18 Source: Indian Startup Ecosystem Maturing - 2016" report by Nasscom-ZINNOV

19 For the past 6 months

Prominent Shared Spaces in the CBD & Off CBD region

Spaces 35,000 Express Avenue

Regus 10,300 KRM Plaza

iShareSpaces 8,300 Ispahani Center

India Business

Center 9,000 Kochar Bliss

Re cent lease transactions in Shared spaces

Paytm Workefella Prestige

Palladium 50 seats

International

Flavors Regus

Shyamala

Towers 40 seats

Table 12

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 45

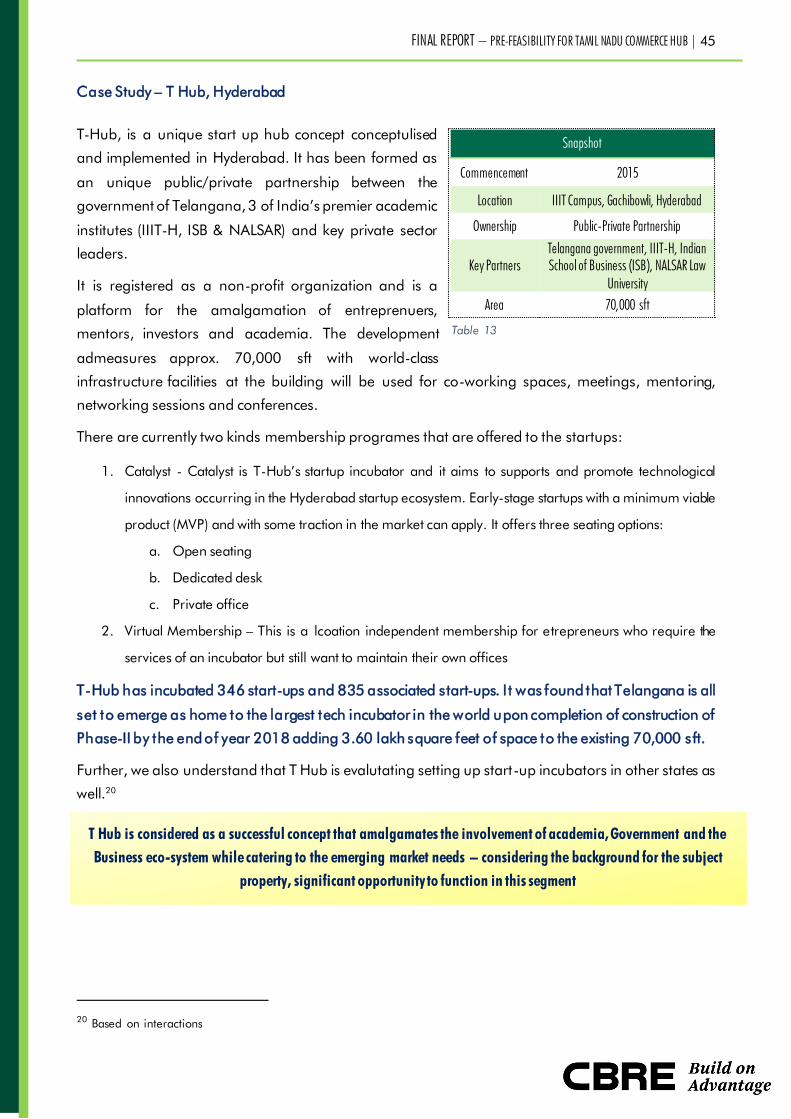

Case Study – T Hub, Hyderabad

T-Hub, is a unique start up hub concept conceptulised

and implemented in Hyderabad. It has been formed as

an unique public/private partnership between the

government of Telangana, 3 of India’s premier academic

institutes (IIIT-H, ISB & NALSAR) and key private sector

leaders.

It is registered as a non-profit organization and is a

platform for the amalgamation of entreprenuers,

mentors, investors and academia. The development

admeasures approx. 70,000 sft with world-class

infrastructure facilities at the building will be used for co-working spaces, meetings, mentoring,

networking sessions and conferences.

There are currently two kinds membership programes that are offered to the startups:

1. Catalyst - Catalyst is T-Hub’s startup incubator and it aims to supports and promote technological

innovations occurring in the Hyderabad startup ecosystem. Early-stage startups with a minimum viable

product (MVP) and with some traction in the market can apply. It offers three seating options:

a. Open seating

b. Dedicated desk

c. Private office

2. Virtual Membership – This is a lcoation independent membership for etrepreneurs who require the

services of an incubator but still want to maintain their own offices

T-Hub has incubated 346 start-ups and 835 associated start-ups. I t was found that Telangana is all

set to emerge as home to the largest tech incubator in the world upon completion of construction of

Phase-II by the end of year 2018 adding 3.60 lakh square feet of space to the existing 70,000 sft.

Further, we also understand that T Hub is evalutating setting up start-up incubators in other states as

well.20

20 Based on interactions

Snapshot

Commencement 2015

Location IIIT Campus, Gachibowli, Hyderabad

Ownership Public-Private Partnership

Key Partners

Telangana government, IIIT-H, Indian

School of Business (ISB), NALSAR Law

University

Area 70,000 sft

Table 13

T Hub is considered as a successful concept that amalgamates the involvement of academia, Government and the

Business eco-system while catering to the emerging market needs – considering the background for the subject

property, significant opportunity to function in this segment

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 46

Module 4: Case Studies – Iconic Commercial Office Developments

Case studies of Iconic commercial developments have been undertaken21

in this module to

understand their product concept, development strategy, best practices followed, demand drivers of

such iconic buildings, etc.

21 Secondary research

FINAL REPORT – PRE-FEASIBILITY FOR TAMIL NADU COMMERCE HUB | 47

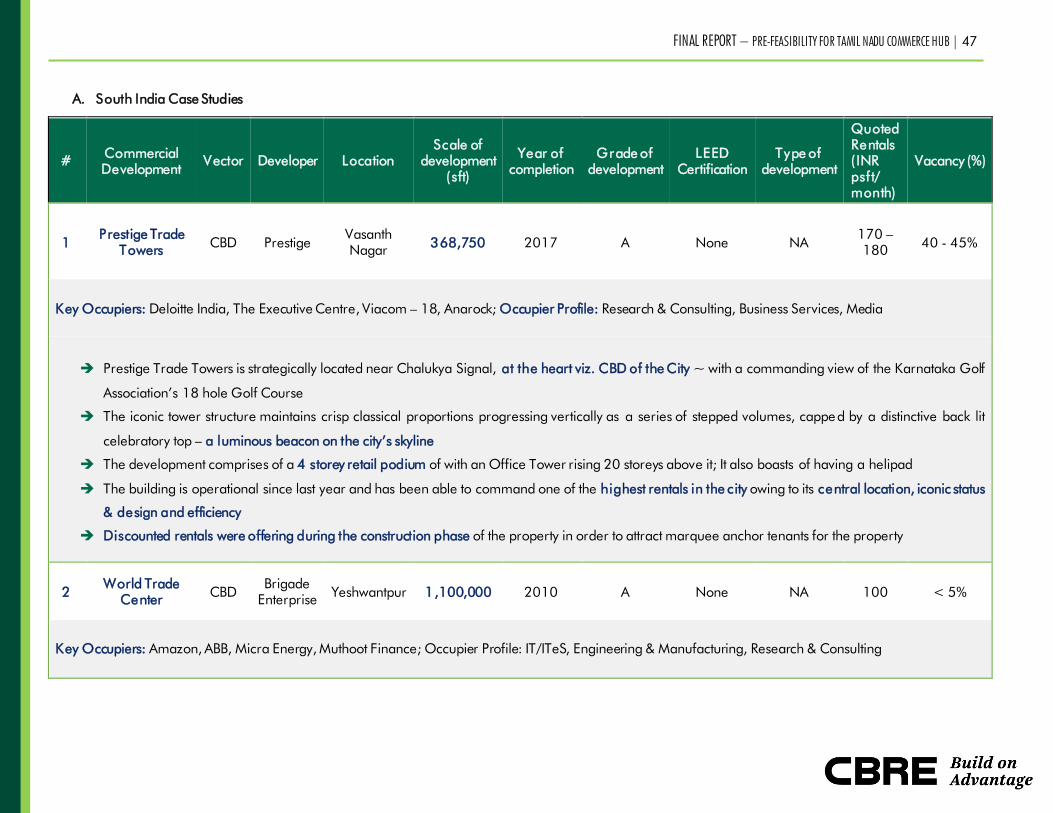

A. South India Case Studies

# Commercial

Development Vector Developer Location

Scale of

development

(sft)

Year of

completion

Grade of

development

LEED

Certification

Type of

development

Quoted