take control of your employee benefit spend

TRANSCRIPT

TAKE CONTROL OF YOUR EMPLOYEE BENEFIT SPEND

Utilize The Power of a Collective Voice Without Giving Up Independent Decision Making

1. Lessons from the outside - SMaC

2. Process vs. Product:

– Where have we been?

– Where are we today?

– Where are we going?

3. Edgerton SD Case Study

4. Wrap Up / Questions

TODAY’S AGENDA

2

“Nearly all men die of their remedies, NOT of their

illnesses.”

–Moliere

SMAC RECIPE = SPECIFIC, METHODICAL, AND CONSISTENT

As the uncertainty, fast-changing, and unforgiving nature of your environment changes, the more SMaC is necessary

• Set of durable operating

practices, create a replicable and consistent success formula

• Clear and concrete, allows enterprise to unify and organize its efforts

• Clear guidance for what to do and what not to do

• Reflects empirical validation and insight

4

SOUTHWEST AIRLINES SMAC

1. Remain a short-haul carrier, under two-

hour segments.

2. Utilize the 737 as our primary aircraft for

ten to twelve years.

3. Continued high aircraft utilization and quick

turns, ten minutes in most cases.

4. The passenger is our #1 product. Do not

carry air freight or mail, only small

packages which have high profitability and

low handling costs.

5. Continued low fares and high frequency of

service.

6. Stay out of food services.

7. Keep the family and people feeling in our

service and fun atmosphere aloft. We’re

proud of our employees.

8. Keep it simple.

5

SOUTHWEST AIRLINES RESULTS

1. Most passengers flown

2. Most flights on time (arrivals

and departures)

3. Lowest Fares

4. Shortest downtimes for

service

5. Highest employee satisfaction

rating

6. Highest customer satisfaction

rating

*Most efficient airline BY FAR

6

“A solid SMaC recipe is the operating code for turning strategic

concepts into reality, a set of practices more enduring than mere

tactics. Tactics change from situation to situation,

whereas SMaC practices can last for decades and

apply across a wide range of circumstances.”

- Jim Collins

7

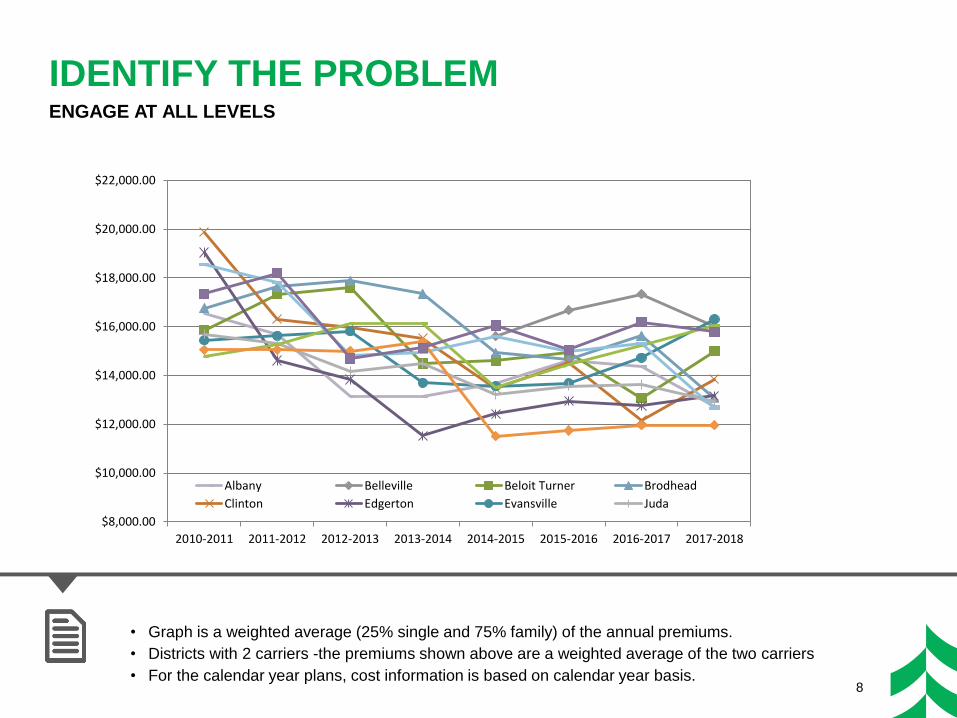

DEEP DOWN WE ALL KNOW…

$8,000.00

$10,000.00

$12,000.00

$14,000.00

$16,000.00

$18,000.00

$20,000.00

$22,000.00

2010-2011 2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017 2017-2018

Albany Belleville Beloit Turner Brodhead

Clinton Edgerton Evansville Juda

8

IDENTIFY THE PROBLEM ENGAGE AT ALL LEVELS

• Graph is a weighted average (25% single and 75% family) of the annual premiums.

• Districts with 2 carriers -the premiums shown above are a weighted average of the two carriers

• For the calendar year plans, cost information is based on calendar year basis.

9

FOUNDATION OF STRATEGIC PLANNING KEY CONSIDERATIONS FOR HIGH-LEVEL DECISION-MAKING

• Cost

– Understanding of cost-drivers

– Understanding of how consumers

purchase health services

• Culture

– Understanding of employees’

health benefit needs

– Understanding model for various

employee groups

• Compliance

– Understanding of ACA/Play or Pay

compliance

10

COMPLICATED COORDINATION =

UNNECESSARY COSTS AND LACK OF FOCUS

HEATHCARE IS A

FRAGRMENTED MAZE…

How they navigate this maze determines:

• Unnecessary cost

• Delayed diagnosis and treatment

• Frustrated patients and families

• Physicians who lose control of their

patient

11

OUR SMAC RECIPE

Have a documented 3-5 year strategy

Have a documented annual plan

that supports long-term

goals

Benchmark against your

peers and best-in-class

performers

Be open to ideas from everywhere

Use data to drive decisions

Communicate strategic

initiatives and results to all

key stakeholders

12

13

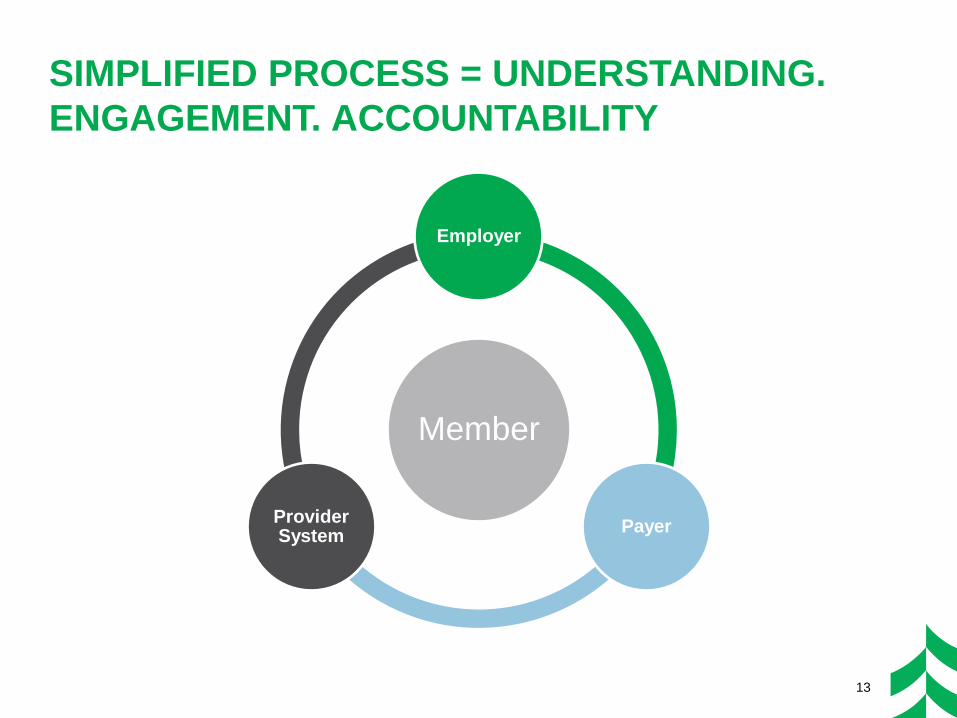

SIMPLIFIED PROCESS = UNDERSTANDING.

ENGAGEMENT. ACCOUNTABILITY

Member

Employer

Payer Provider System

14

WHAT WE NEED TO HEAR

It’s not about tools or products, it’s

about PROCESS.

FOCUS ON WHAT IS DRIVING THE

COST AND ENGAGE ACCORDINGLY!

15

EVOLUTION OF DATA ANALYTICS

No data

on statewide

pool

2002

MedInsight

and other

reports

2015

2016

Manual

benchmarking

2005

Direct data

feeds on

large groups

Today

STATEWIDE

DASHBOARD

Future

16

WHAT WE WANTED TO HEAR…

*Average increase of 12%

**Post Act 10 WEA hasn’t had a single year where entire book averaged 12% when not pool rated.

“If we all pool

together we can

maintain status

quo and deliver

the best value”

17

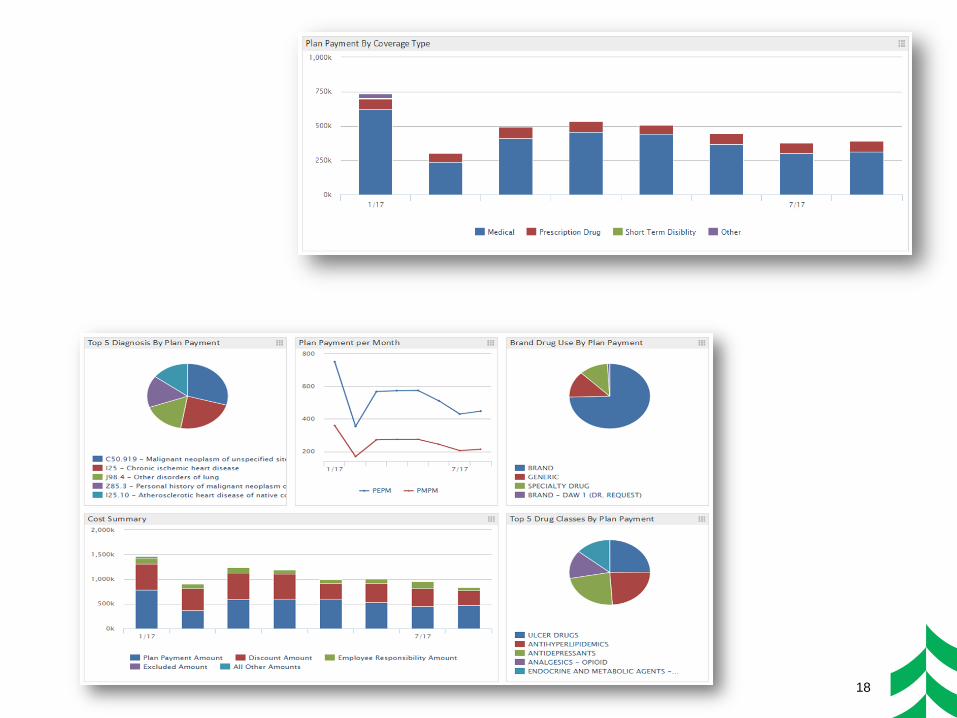

BENCHMARKING TOOL / SCORECARD

Provider

Accountability

Employee

Accountability

Employer

Accountability

18

19

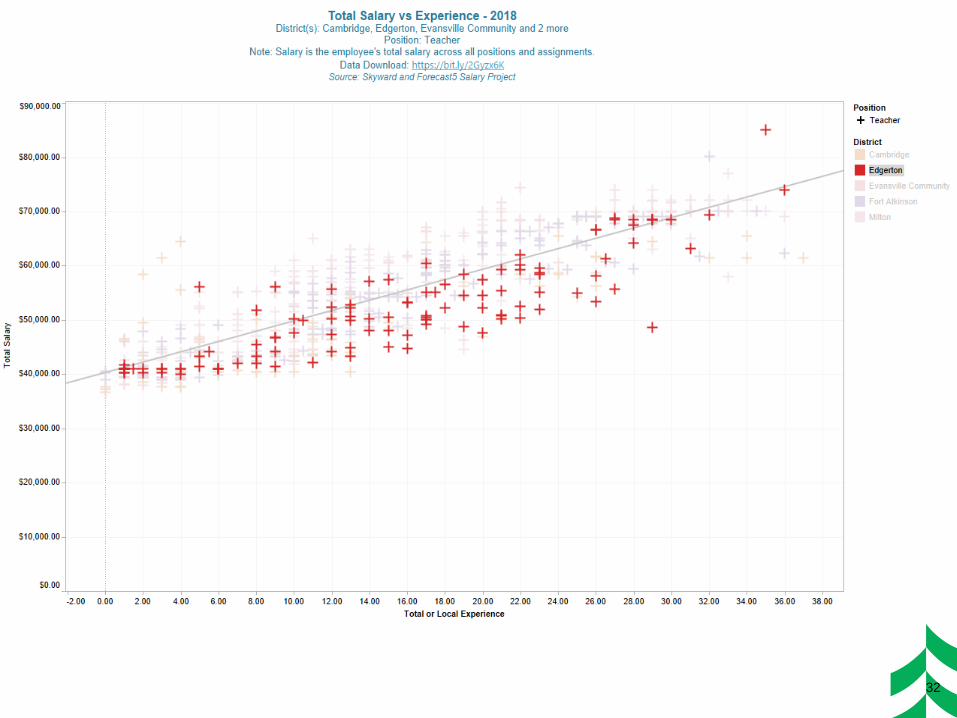

EDGERTON SCHOOL DISTRICT CASE STUDY

• Health plan design

• Understanding the organizational

challenge

• Total Compensation Benchmarking -

“Coopetition”

• Results

20

1). Post - Act 10 Employee Mobility Trends

– Pre-Act 10: Collective Bargaining Established a “Market”

• Wages and Benefits

– Post-Act 10: Comp Partnership supports Evidence-Based Outcomes

• Wages and Benefits

2). Compensation = Emotions vs. Evidence

– “Fair” Compensation

– Reliable Compensation Data for Measurement

– Outline and Communicate Leadership Strategy

3) “Hard-to-Fill” Identification

– Madison-Area Partnership will Address this Outcome

4) Is your “Comp Plan” keeping Pace?

POST-ACT 10 MARKET AND ORGANIZATIONAL VULNERABILITY: IS YOUR ORGANIZATION AWARE AND WHAT IS YOUR STRATEGY?

21

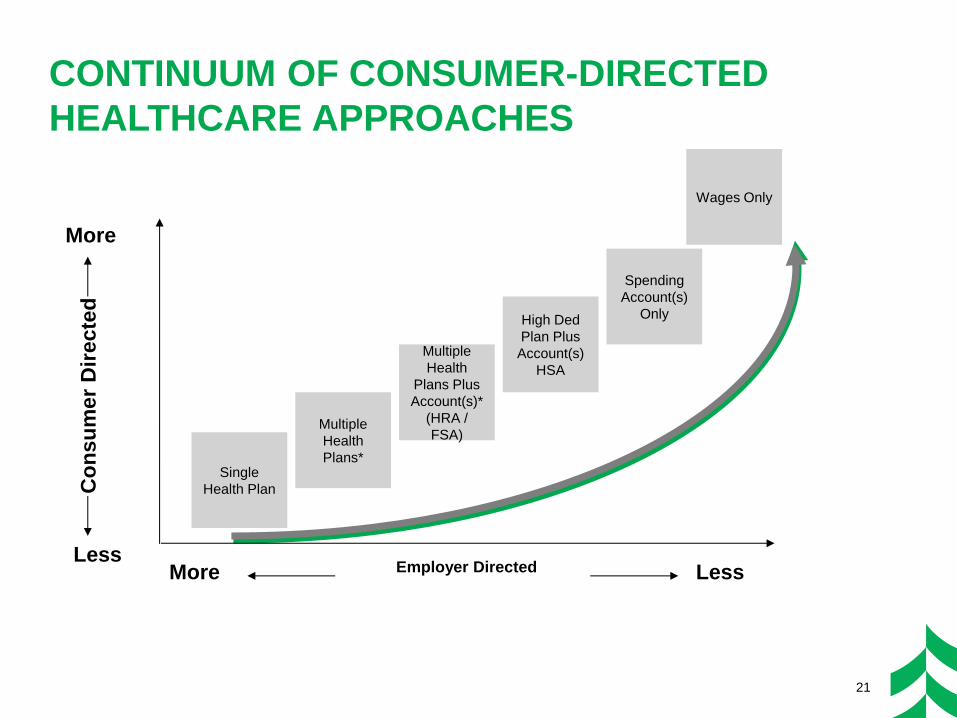

CONTINUUM OF CONSUMER-DIRECTED

HEALTHCARE APPROACHES C

on

su

mer

Dir

ecte

d

More Less Employer Directed

Single

Health Plan

Multiple

Health

Plans*

Multiple

Health

Plans Plus

Account(s)*

(HRA /

FSA)

High Ded

Plan Plus

Account(s)

HSA

Spending

Account(s)

Only

Wages Only

More

Less

22

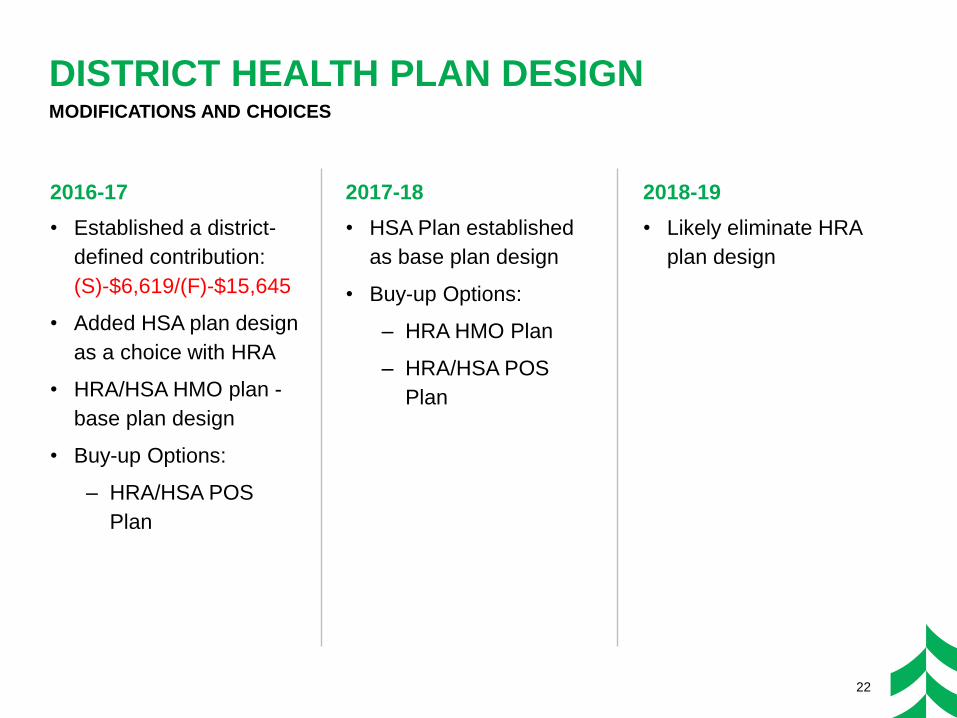

DISTRICT HEALTH PLAN DESIGN

2016-17

• Established a district-

defined contribution:

(S)-$6,619/(F)-$15,645

• Added HSA plan design

as a choice with HRA

• HRA/HSA HMO plan -

base plan design

• Buy-up Options:

– HRA/HSA POS

Plan

MODIFICATIONS AND CHOICES

2017-18

• HSA Plan established

as base plan design

• Buy-up Options:

– HRA HMO Plan

– HRA/HSA POS

Plan

2018-19

• Likely eliminate HRA

plan design

23

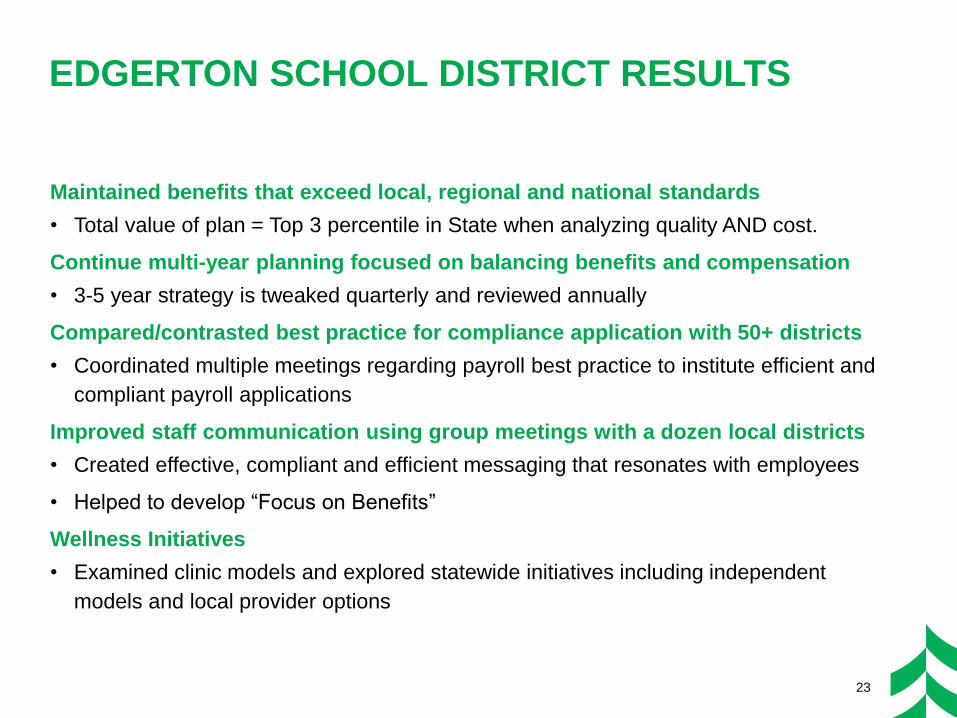

Maintained benefits that exceed local, regional and national standards

• Total value of plan = Top 3 percentile in State when analyzing quality AND cost.

Continue multi-year planning focused on balancing benefits and compensation

• 3-5 year strategy is tweaked quarterly and reviewed annually

Compared/contrasted best practice for compliance application with 50+ districts

• Coordinated multiple meetings regarding payroll best practice to institute efficient and

compliant payroll applications

Improved staff communication using group meetings with a dozen local districts

• Created effective, compliant and efficient messaging that resonates with employees

• Helped to develop “Focus on Benefits”

Wellness Initiatives

• Examined clinic models and explored statewide initiatives including independent

models and local provider options

EDGERTON SCHOOL DISTRICT RESULTS

• Retain and attract employees

• Everything wages and benefits

*Local evaluation: Total compensation

regional partnership to support

accurate compairsons

FINANCIAL ACCOUNTABILITY PERSONNEL ACCOUNTABILITY

• Weathering the State Budget:

effectively manage a budget

• But not w/out consequence….

– Employee benefit changes

– Deferred capital maintenance

– Mindful budget approach (limit

spending commitments)

• Avoid fiscal cliff (often result in layoffs

and/or wage freezes)

*Local evaluation: What is the impact

of current budget trends (revenue

cap)

24

ORGANIZATIONAL CHALLENGES TWO LAYERS OF ACCOUNTABILITY

25

WHERE DO YOU STAND? We are NOT all on equal footing…

26

LOCAL EVALUATION OF STATE REV. CAPS

PROGRAMS/STAFFING

TRENDS

• Purpose: Evaluation of

programs (student

opportunities) and class

size

• Goal: Retain and

Attract families to the

Edgerton School

District

3 MAIN “PRESSURE POINTS”

BUDGET

ALLOCATIONS

• Purpose: Evaluation of

budget allocations to

support instructional

materials and capital

maintenance

obligations

• Goal: Support and

maintain instructional

materials and capital

maintenance

expectations

COMPENSATION

COMPARISONS

• Purpose: Evaluation of

wage/benefit trends to

support that employees

(in each employee

group) access "fair"

compensation for their

individual role and

responsibility

• Goal: Retain and

attract highly qualified

and/or licensed staff

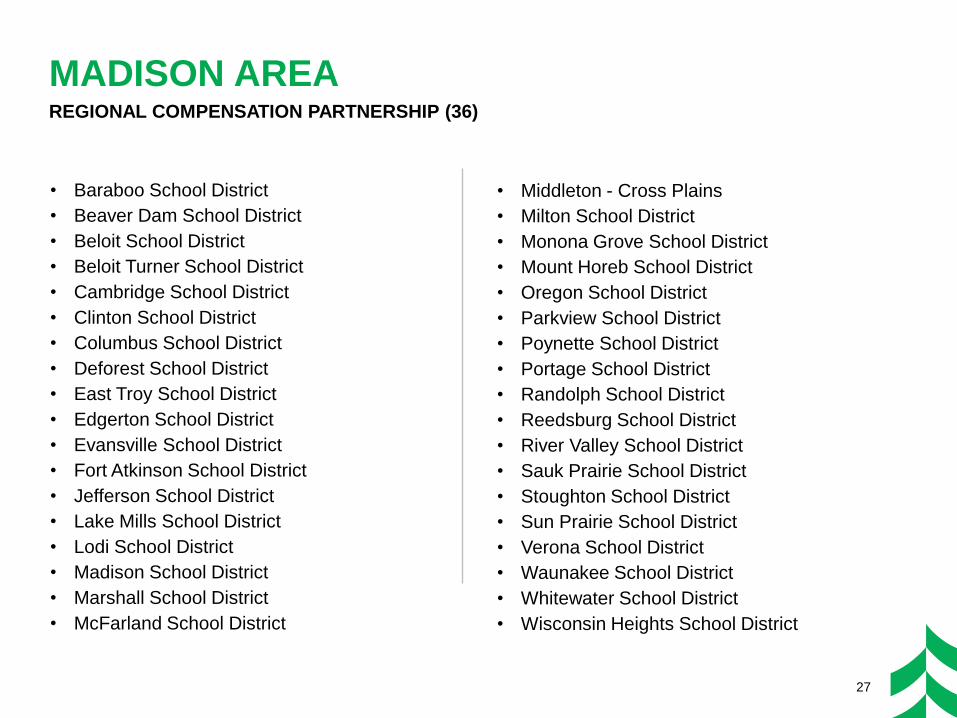

• Middleton - Cross Plains

• Milton School District

• Monona Grove School District

• Mount Horeb School District

• Oregon School District

• Parkview School District

• Poynette School District

• Portage School District

• Randolph School District

• Reedsburg School District

• River Valley School District

• Sauk Prairie School District

• Stoughton School District

• Sun Prairie School District

• Verona School District

• Waunakee School District

• Whitewater School District

• Wisconsin Heights School District

27

MADISON AREA REGIONAL COMPENSATION PARTNERSHIP (36)

• Baraboo School District

• Beaver Dam School District

• Beloit School District

• Beloit Turner School District

• Cambridge School District

• Clinton School District

• Columbus School District

• Deforest School District

• East Troy School District

• Edgerton School District

• Evansville School District

• Fort Atkinson School District

• Jefferson School District

• Lake Mills School District

• Lodi School District

• Madison School District

• Marshall School District

• McFarland School District

28

REGIONAL COMPENSATION PARTNERSHIP COMMON CHALLENGES (Fall 2016)

AFFORDABLE COMPENSATION

• Funding to support new comp systems

• Health insurance costs

HOW TO PLACE NEW EMPLOYEES

• “Leapfrogging” effect

DISTRICTS “CHERRY PICKING”

• District-to-district headhunting

HARD-TO-FILL POSITIONS

• How is this determined?

• Are existing employees honored by

this classification?

29

REGIONAL COMPENSATION PARTNERSHIP COMMON GOALS (Fall 2016)

COMMUNICATION

• Openly communication compensation

structures

DATA SUBMISSION PRACTICES

• Establish practices that are clear,

consistent and sustainable

COMMITMENT

• Submit expected outcomes

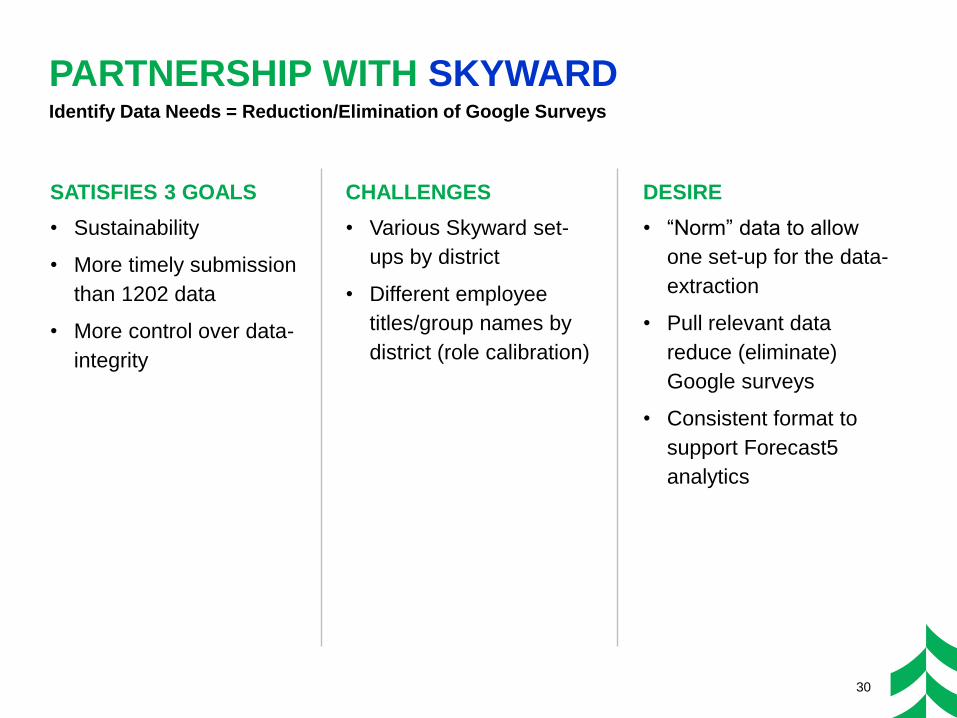

RELATIONSHIPS

• Establish relationships with support

organizations

– Skyward, Forecast5, and

Associated

30

PARTNERSHIP WITH SKYWARD

SATISFIES 3 GOALS

• Sustainability

• More timely submission

than 1202 data

• More control over data-

integrity

Identify Data Needs = Reduction/Elimination of Google Surveys

CHALLENGES

• Various Skyward set-

ups by district

• Different employee

titles/group names by

district (role calibration)

DESIRE

• “Norm” data to allow

one set-up for the data-

extraction

• Pull relevant data

reduce (eliminate)

Google surveys

• Consistent format to

support Forecast5

analytics

31

1). Role Identification and Coding (Position Type Codes)

– Closing 1202 Reporting Gaps

2). Skyward Data-Mining:

– Role Identification

– Wage Detail

– Experience (Local/Total)

– Educational Attainment

3). Forecast5 Result: Salary/Experience and Hourly-Rate/Experience (and

More!)

ESTABLISHING A SUSTAINABLE SUBMISSION PROCESS: OUR 18 MONTH QUEST…….

32

34

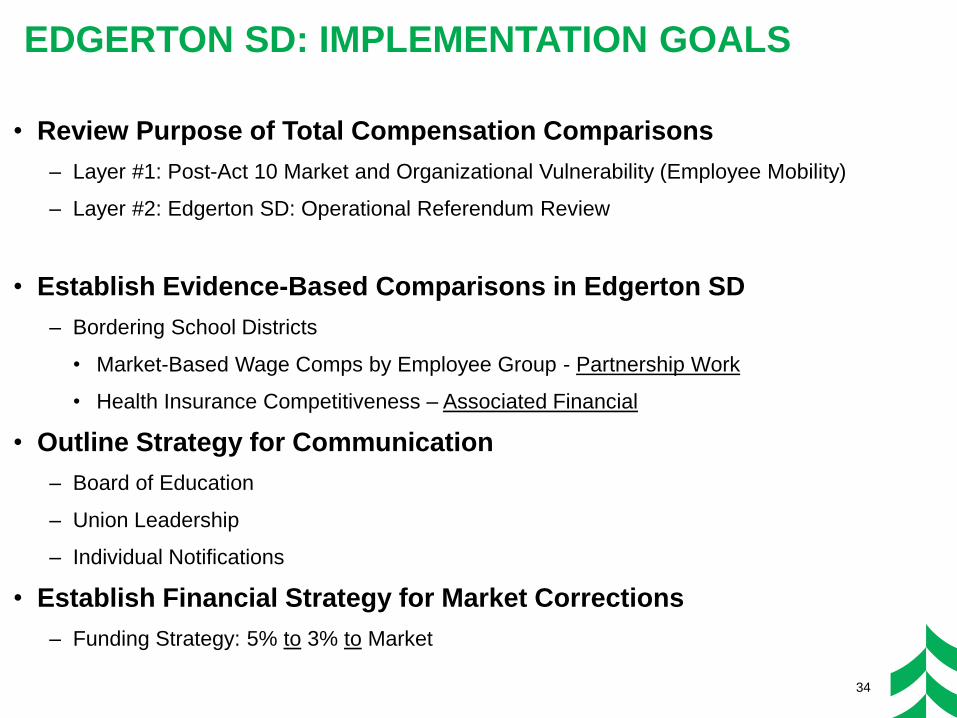

• Review Purpose of Total Compensation Comparisons

– Layer #1: Post-Act 10 Market and Organizational Vulnerability (Employee Mobility)

– Layer #2: Edgerton SD: Operational Referendum Review

• Establish Evidence-Based Comparisons in Edgerton SD

– Bordering School Districts

• Market-Based Wage Comps by Employee Group - Partnership Work

• Health Insurance Competitiveness – Associated Financial

• Outline Strategy for Communication

– Board of Education

– Union Leadership

– Individual Notifications

• Establish Financial Strategy for Market Corrections

– Funding Strategy: 5% to 3% to Market

EDGERTON SD: IMPLEMENTATION GOALS

Reporting through “Employee Group” Buckets: 5% to 3% to Market

• Certified Teaching Staff

• Support Staff

• Occupational Therapy/Physical Therapy

• Maintenance/Custodial

• Technology

• Administrative Office Personnel

• Administration

EGERTON SD: MARKET COMPARISON OUTCOMES

36

LEADERSHIP ISN’T EASY…

“A genuine leader is not a

searcher for consensus but a

molder of consensus”

QUESTIONS?

37

IMPORTANT DISCLOSURES

Investments, securities and insurance products:

Insurance products are offered by licensed agents of Associated Financial Group, LLC (d/b/a Associated BRC

Insurance Solutions in California). The financial consultants at Associated Financial Group are registered

representatives with, and securities and advisory services are offered through LPL Financial “LPL”, a

registered investment advisor and member FINRA/SIPC. Associated Financial Group uses Associated Benefits and

Risk Consulting (“ABRC”) as a marketing name. ABRC is a wholly-owned subsidiary of Associated Bank, N.A. (“AB”).

AB is a wholly-owned subsidiary of Associated Banc-Corp (“AB-C”). LPL is NOT an affiliate of either AB or AB-C. AB-C

and its subsidiaries do not provide tax, legal, or accounting advice. Please consult with your tax, legal, or accounting

advisors regarding your individual situation. ABRC’s standard of care and legal duty to the insured in providing

insurance products and services is to follow the instructions of the insured, in good faith. (4/17)

38 Copyright © 2018 Associated Financial Group, LLC.