takaful in bangladesh seeking a framework for growth · takaful in bangladesh ... anomalies in...

TRANSCRIPT

www.meinsurancereview.com December 2013 47

Takaful MarkeT Profile – SouTh aSia

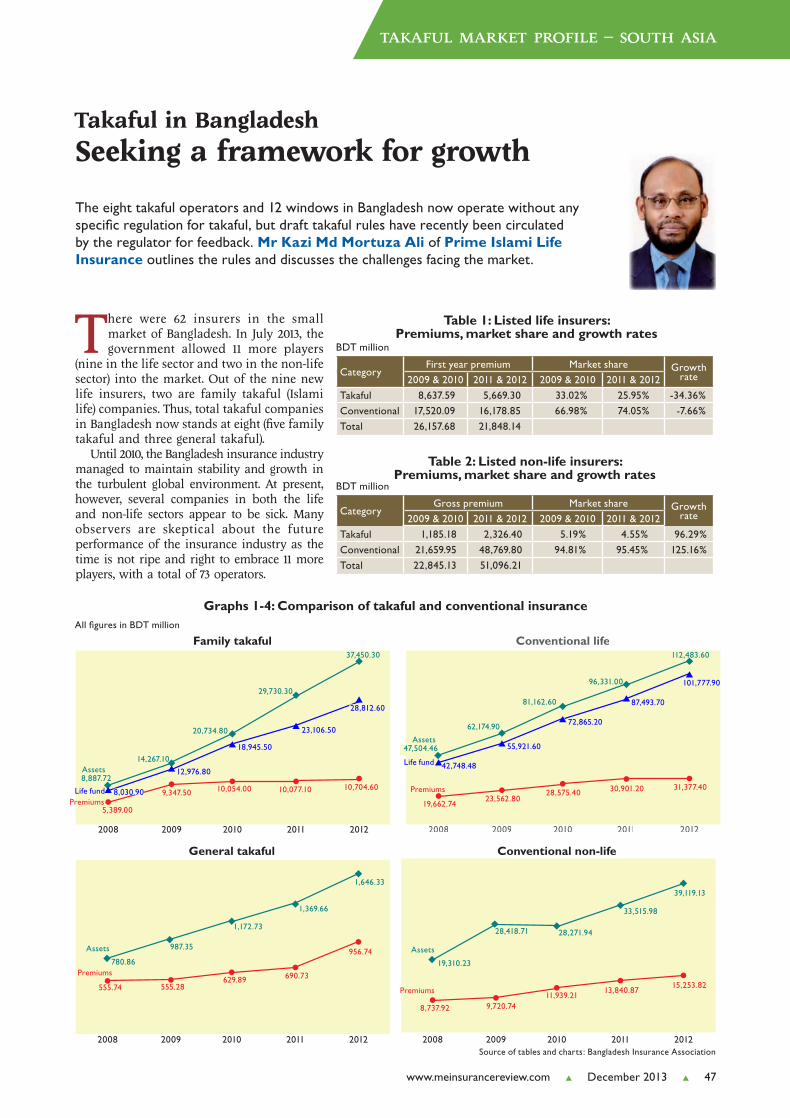

There were 62 insurers in the small market of Bangladesh. In July 2013, the government allowed 11 more players

(nine in the life sector and two in the non-life sector) into the market. Out of the nine new life insurers, two are family takaful (Islami life) companies. Thus, total takaful companies in Bangladesh now stands at eight (five family takaful and three general takaful).

Until 2010, the Bangladesh insurance industry managed to maintain stability and growth in the turbulent global environment. At present, however, several companies in both the life and non-life sectors appear to be sick. Many observers are skeptical about the future performance of the insurance industry as the time is not ripe and right to embrace 11 more players, with a total of 73 operators.

Takaful in Bangladesh

Seeking a framework for growth

The eight takaful operators and 12 windows in Bangladesh now operate without any specific regulation for takaful, but draft takaful rules have recently been circulated by the regulator for feedback. Mr Kazi Md Mortuza Ali of Prime Islami Life Insurance outlines the rules and discusses the challenges facing the market.

CategoryFirst year premium Market share Growth

rate2009 & 2010 2011 & 2012 2009 & 2010 2011 & 2012

Takaful 8,637.59 5,669.30 33.02% 25.95% -34.36%

Conventional 17,520.09 16,178.85 66.98% 74.05% -7.66%

Total 26,157.68 21,848.14

Table 1: Listed life insurers: Premiums, market share and growth rates

BDT million

Table 2: Listed non-life insurers: Premiums, market share and growth rates

CategoryGross premium Market share Growth

rate2009 & 2010 2011 & 2012 2009 & 2010 2011 & 2012

Takaful 1,185.18 2,326.40 5.19% 4.55% 96.29%

Conventional 21,659.95 48,769.80 94.81% 95.45% 125.16%

Total 22,845.13 51,096.21

BDT million

All figures in BDT million

General takaful

Assets

Premiums780.86

987.35

1,172.73

1,369.66

1,646.33

555.74 555.28629.89 690.73

956.74

2008 2009 2010 2011 2012

Family takaful

Assets

Life fundPremiums

8,887.72

14,267.10

20,734.80

29,730.30

37,450.30

8,030.90

12,976.80

5,389.00

9,347.50 10,054.00 10,077.10 10,704.60

2008 2009 2010 2011 2012

18,945.50

23,106.50

28,812.60

Conventional life

Assets

Life fund

Premiums

47,504.46

62,174.90

81,162.60

96,331.00

112,483.60

19,662.7423,562.80

28,575.40

2008 2009 2010 2011 2012

42,748.48

55,921.60

72,865.20

87,493.70

101,777.90

31,377.4030,901.20

Conventional non-life

Assets

Premiums

28,271.94

33,515.98

39,119.13

8,737.92 9,720.7411,939.21

13,840.8715,253.82

2008 2009 2010 2011 2012

28,418.71

19,310.23

Graphs 1-4: Comparison of takaful and conventional insurance

Source of tables and charts: Bangladesh Insurance Association

Tak_South_Asia.indd 47 22/11/2013 11:43:35

48 December 2013 www.meinsurancereview.com

Takaful MarkeT Profile – SouTh aSia

This is more alarming for the life insurance industry, as the market growth rate of new life business has been declining since 2010 and now faces negative growth in the new business, meaning that renewal business growth will be negative in the near future (Tables 1 and 2).

Under the present scenario, acute manpower shortage and slow or negative growth may lead to a crisis situation, unless some positive measures are taken to address the problems of life insurance sector. The performance of takaful and conventional companies are shown in Graphs 1-4.

Anomalies in Insurance Act 2010One of the most important ingredients for takaful to succeed is effective regulations. Unfortunately, eight takaful companies in Bangladesh along with 12 takaful windows of conventional life insurers are operating without any specific regulation for takaful. Although the contribution of family takaful to total first year premiums is more than 20%, takaful companies are facing extreme difficulties in operating business.

Sections 23, 72 and 146 of the Insurance Act, 2010 are important and need to be addressed for solving problems of takaful sector.

In the new Act, “Islami insurance business” has been defined for the first time, stating that Islamic insurance business means insurance business carried on according to the “Islami Shariah”. The Act has not mentioned any guideline as to how the principles of Islami Shariah will be applied in the case of insurance business, the criteria determining the exact application of Islami Shariah and how the regulatory body will be supervising Shariah issues.

Section 23 provides for deposits with the Bangladesh Bank in cash and in approved securities. Islami insurance companies cannot invest in interest-based securities. The Act is silent on how the deposits of Islami insurers is kept with Bangladesh Bank under Shariah principles. The rate of return from the Bangladesh government’s Islami Investment Bond (BGIIB) is 70% less than the return of government securities. This has put takaful companies at a disadvantage.

Section 72 states that interest shall be payable by an insurer for the period in which the claim amount has not been paid after 90 days at 5% higher than the prevailing bank rate. Islami insurers are not supposed to pay interest under the principles of Shariah. This anomaly needs to be addressed appropriately.

Section 146 states that the government may make rules for Islami insurers. Since the proposed Takaful Act is not going to be enacted in the near future, the appropriate rules for Islami insurance need to be framed immediately, otherwise some of the provisions of the Insurance Act 2010 will conflict with Shariah principles.

Long-awaited regulationsIn Bangladesh, a new regulatory body was formed in January 2011 and since then, it has undertaken the tremendous task of improving market practices and encouraging the market players to practise good corporate governance in functional activities. Despite manpower shortage, the Insurance Development and Regulatory Authority (IDRA) has framed 11 regulations and rules, and several more are in the pipeline. It needs to frame as many as 50 rules and regulations to

bring discipline and stability in the industry. In the present situation, it is quite difficult to predict when the regulator can finalise the remaining 40 rules and regulations.

The new regulations promulgated so far by IDRA are in the areas of fund management, CEO appointment, registration fees, obligations to the rural & social sector, dispute resolutions, rules for Central Rating Committee, rules for asset investments and paid-up capital & shareholding, and so on.

Proposed takaful rulesIDRA circulated draft Takaful Rules in October 2013 for stakeholders’ feedback. The draft rules cover, among others, the following aspects of takaful operation: operational models, fund segregation and management, relationship between participants and operator, sharing of surplus and deficit, solvency margin requirements and Shariah Council formation.

It has been stated that unless otherwise stated, the model to be followed by the operators shall be based on the combination of wakala and mudharaba. Other important provisions are as follows:

• Takaful operators (TO) shall maintain and administer two funds: the Participants’ Takaful Fund (PTF) and the Shareholders’ Fund (SHF). For family takaful, a separate participant’s investment fund shall also be maintained.

• The operators shall frame the PTF guidelines as per the guidelines of the Shariah Council, to be approved by the Authority.

• The SHF shall be maintained under the guidelines provided by the TO’s Shariah Council and should be approved by the regulator.

• When the PTF, including other reserves (if any), is insufficient to meet current payments less receipts, the deficit shall be funded by way of an interest-free loan (Qard hasan) from the SHF.

• TOs shall evaluate the assets and liabilities of the PTF annually to determine whether it has produced a surplus for sharing among the participants. Distribution of surplus of family takaful should be done after each actuarial valuation.

• All the administrative and management expenses of the TO shall be borne by the shareholders in consideration of receiving the wakalah fee and/ or the share of surplus.

• The TO’s actuary shall ensure that the products are sound and workable, and the Shariah Council shall ensure that these conform to the Islami principles.

Main obstaclesThe growth of takaful has been obstructed for several reasons. For example, due to the extremely low returns from BGIIB, takaful companies have become, to a great extent, non-compliant with the provision in Insurance Act regarding the 30% compulsory investment in government bonds and securities. Although initiatives had been taken by IDRA and the Central Bank to enhance the profit ratio of BGIIB, the matter has been with the Ministry of Finance for more than one year.

There is only one qualified actuary dealing with the valuations of the 27 life insurance companies. Takaful companies are facing extreme difficulties in getting certification from the actuary for new products, and thus

Tak_South_Asia.indd 48 22/11/2013 11:43:40

www.meinsurancereview.com December 2013 49

Takaful MarkeT Profile – SouTh aSia

have not introduced any new products in the last three years. It is argued that as there are no rules of takaful operation prescribed by IDRA, it may not be desirable to design any takaful product unless requests are made by the TO to develop insurance products in specific manner. The draft Takaful Rules in this respect seem to be clear as it states that the actuary of the TO shall ensure that the products are sound and workable and the concerned Shariah Council shall ensure that the products conform to Shariah laws.

The present socio-economic scenario of the Bangladesh takaful market appears to be not very conducive and supportive for its growth and development. The framework

of takaful regulations and guidelines in Bangladesh is almost absent. It takes a long time to formulate policies and guidelines. The government’s bureaucracy and lack of understanding about the takaful industry has made it extremely difficult for the operators and the regulator to prove dynamism.

Growth to be promisingDespite temporary impediments in the takaful journey, operators believe that the growth of takaful in the coming years will be promising. This is because the demand for takaful will grow with the increase in public awareness coupled with more efficient and diversified distribution channels, which will provide greater access to a larger segment of the population.

The challenge in the takaful sector is to develop an enabling environment through the provision of legal, regulatory and Shariah framework. This is necessary to support the sound and efficient growth of the takaful industry. Product innovation and excellent customer service are the key enablers for future growth.

Enhanced capacity and the availability of resources, particularly human capital, are essential in expediting the pace of progress. For the regulator, the challenge lies in providing a level playing field, removing the barriers and facilitating product innovation, while at the same time, encouraging and ensuring enterprise risk management principles and procedures. Mr Kazi Md Mortuza Ali is the Managing Director of Prime Islami Life Insurance.

7th India Rendezvous22-24 January 2014, Taj Mahal Palace Hotel, Mumbai, IndiaTheme “Lessons from the Basics for a Sustainable Future”

Organised by: Co-organiser: Supported by: Media Partner:

7th India Rendezvous22-24 January 2014, Taj Mahal Palace Hotel, Mumbai, IndiaTheme “Lessons from the Basics for a Sustainable Future”

Organised by: Co-organiser: Supported by: Media Partner:

Mark Your Diary

Cocktail Sponsor:

Tak_South_Asia.indd 49 25/11/2013 14:54:31