table 5: worksheet for estimating the use value of orchard ... · table 5: worksheet for estimating...

TRANSCRIPT

Table 5: Worksheet for estimating the use value of orchard land in .Example The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $18.69 c) Net return attributable to trees only (3a - 3b) ($18.69) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0043 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1109 f) "Other" Orchard Capitalization Rate 0.1276 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($134.77) $226.44 ($117.17) $244.04 II 1.00 ($168.46) $156.63 ($146.46) $178.63 III 1.00 ($168.46) $72.35 ($146.46) $94.35 IV 1.00 ($168.46) $24.19 ($146.46) $46.19 V 0.75 ($126.34) $18.14 ($109.84) $34.64 VI 0.60 ($101.07) $19.33 ($87.87) $32.53 VII 0.40 ($67.38) $4.86 ($58.58) $13.66 VIII 0.00 $0.00 $24.08 $0.00 $24.08

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:1

Table 5: Worksheet for estimating the use value of orchard land in Accomack The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $14.00 c) Net return attributable to trees only (3a - 3b) ($14.00) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0058 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1124 f) "Other" Orchard Capitalization Rate 0.1291 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($99.62) $165.93 ($86.76) $178.80 II 1.00 ($124.53) $114.47 ($108.45) $130.55 III 1.00 ($124.53) $52.51 ($108.45) $68.59 IV 1.00 ($124.53) $17.10 ($108.45) $33.18 V 0.75 ($93.40) $12.83 ($81.34) $24.89 VI 0.60 ($74.72) $13.80 ($65.07) $23.45 VII 0.40 ($49.81) $3.30 ($43.38) $9.73 VIII 0.00 $0.00 $17.70 $0.00 $17.70

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:2

Table 5: Worksheet for estimating the use value of orchard land in Albemarle The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $12.28 c) Net return attributable to trees only (3a - 3b) ($12.28) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0068 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1134 f) "Other" Orchard Capitalization Rate 0.1301 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($86.61) $143.36 ($75.51) $154.46 II 1.00 ($108.26) $98.71 ($94.39) $112.58 III 1.00 ($108.26) $45.05 ($94.39) $58.92 IV 1.00 ($108.26) $14.39 ($94.39) $28.26 V 0.75 ($81.19) $10.79 ($70.79) $21.20 VI 0.60 ($64.95) $11.70 ($56.63) $20.02 VII 0.40 ($43.30) $2.69 ($37.76) $8.24 VIII 0.00 $0.00 $15.33 $0.00 $15.33

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:3

Table 5: Worksheet for estimating the use value of orchard land in Alleghany The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $2.43 c) Net return attributable to trees only (3a - 3b) ($2.43) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0058 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1124 f) "Other" Orchard Capitalization Rate 0.1291 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($17.32) $28.84 ($15.08) $31.08 II 1.00 ($21.65) $19.90 ($18.85) $22.69 III 1.00 ($21.65) $9.13 ($18.85) $11.92 IV 1.00 ($21.65) $2.97 ($18.85) $5.77 V 0.75 ($16.24) $2.23 ($14.14) $4.32 VI 0.60 ($12.99) $2.40 ($11.31) $4.08 VII 0.40 ($8.66) $0.57 ($7.54) $1.69 VIII 0.00 $0.00 $3.08 $0.00 $3.08

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:4

Table 5: Worksheet for estimating the use value of orchard land in Amelia The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $23.37 c) Net return attributable to trees only (3a - 3b) ($23.37) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0046 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1112 f) "Other" Orchard Capitalization Rate 0.1279 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($168.09) $281.98 ($146.18) $303.89 II 1.00 ($210.11) $194.95 ($182.73) $222.34 III 1.00 ($210.11) $89.93 ($182.73) $117.32 IV 1.00 ($210.11) $29.93 ($182.73) $57.31 V 0.75 ($157.58) $22.44 ($137.04) $42.98 VI 0.60 ($126.07) $23.96 ($109.64) $40.39 VII 0.40 ($84.04) $5.97 ($73.09) $16.92 VIII 0.00 $0.00 $30.00 $0.00 $30.00

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:5

Table 5: Worksheet for estimating the use value of orchard land in Amherst The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $3.93 c) Net return attributable to trees only (3a - 3b) ($3.93) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0047 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1113 f) "Other" Orchard Capitalization Rate 0.1280 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($28.26) $47.38 ($24.58) $51.06 II 1.00 ($35.32) $32.75 ($30.72) $37.36 III 1.00 ($35.32) $15.10 ($30.72) $19.71 IV 1.00 ($35.32) $5.02 ($30.72) $9.62 V 0.75 ($26.49) $3.76 ($23.04) $7.21 VI 0.60 ($21.19) $4.02 ($18.43) $6.78 VII 0.40 ($14.13) $1.00 ($12.29) $2.84 VIII 0.00 $0.00 $5.04 $0.00 $5.04

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:6

Table 5: Worksheet for estimating the use value of orchard land in Augusta The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $20.77 c) Net return attributable to trees only (3a - 3b) ($20.77) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0053 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1119 f) "Other" Orchard Capitalization Rate 0.1286 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($148.50) $248.09 ($129.25) $267.34 II 1.00 ($185.63) $171.30 ($161.56) $195.37 III 1.00 ($185.63) $78.77 ($161.56) $102.83 IV 1.00 ($185.63) $25.89 ($161.56) $49.95 V 0.75 ($139.22) $19.42 ($121.17) $37.47 VI 0.60 ($111.38) $20.82 ($96.94) $35.26 VII 0.40 ($74.25) $5.07 ($64.62) $14.69 VIII 0.00 $0.00 $26.44 $0.00 $26.44

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:7

Table 5: Worksheet for estimating the use value of orchard land in Bedford The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $7.10 c) Net return attributable to trees only (3a - 3b) ($7.10) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0052 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1119 f) "Other" Orchard Capitalization Rate 0.1285 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($50.80) $84.89 ($44.21) $91.47 II 1.00 ($63.50) $58.62 ($55.27) $66.85 III 1.00 ($63.50) $26.96 ($55.27) $35.19 IV 1.00 ($63.50) $8.86 ($55.27) $17.10 V 0.75 ($47.63) $6.65 ($41.45) $12.82 VI 0.60 ($38.10) $7.13 ($33.16) $12.07 VII 0.40 ($25.40) $1.74 ($22.11) $5.03 VIII 0.00 $0.00 $9.05 $0.00 $9.05

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:8

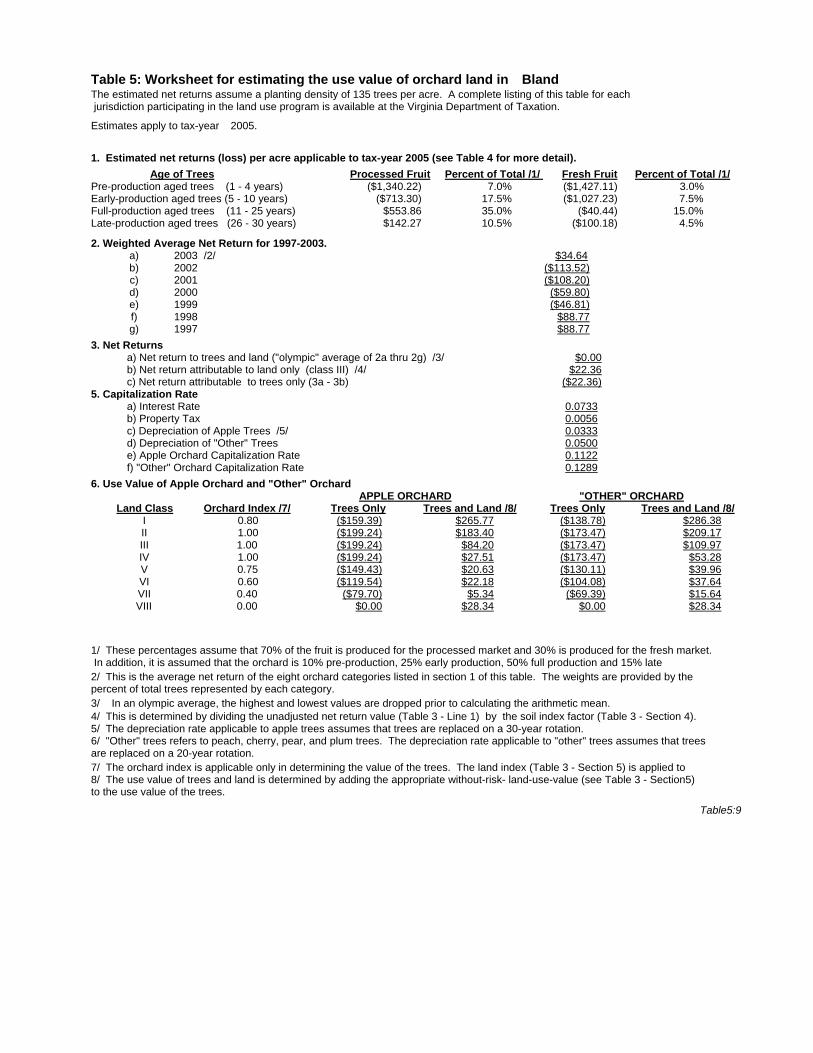

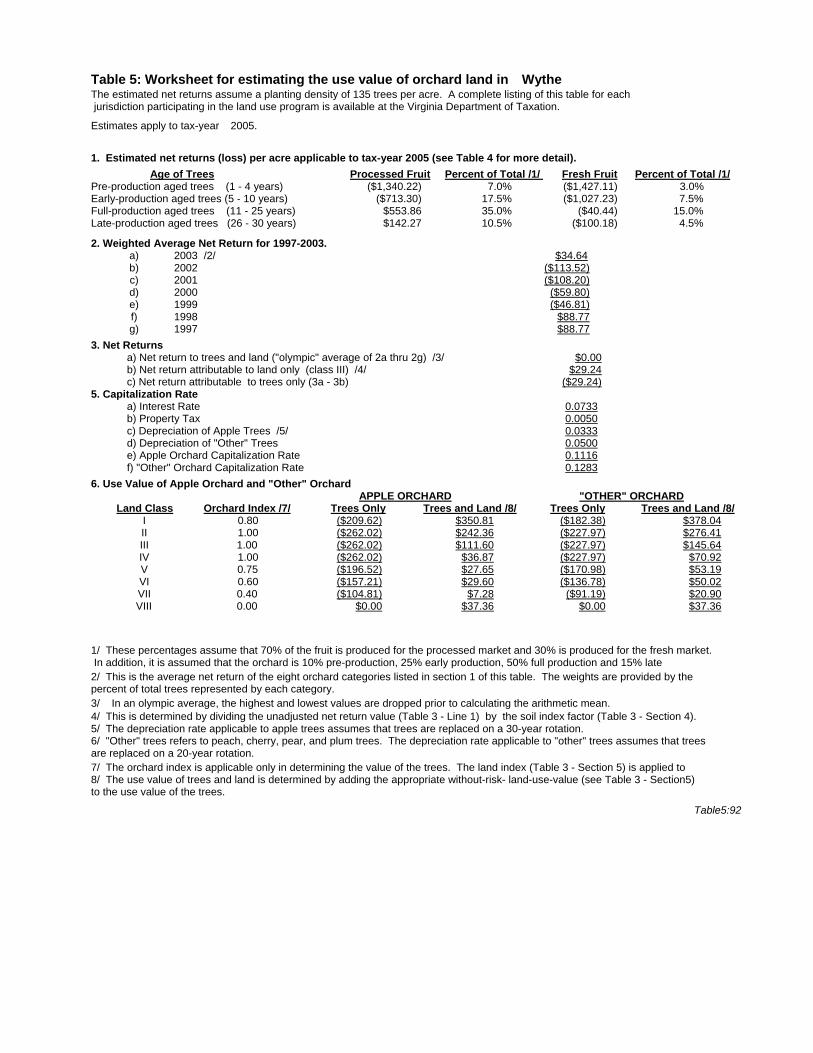

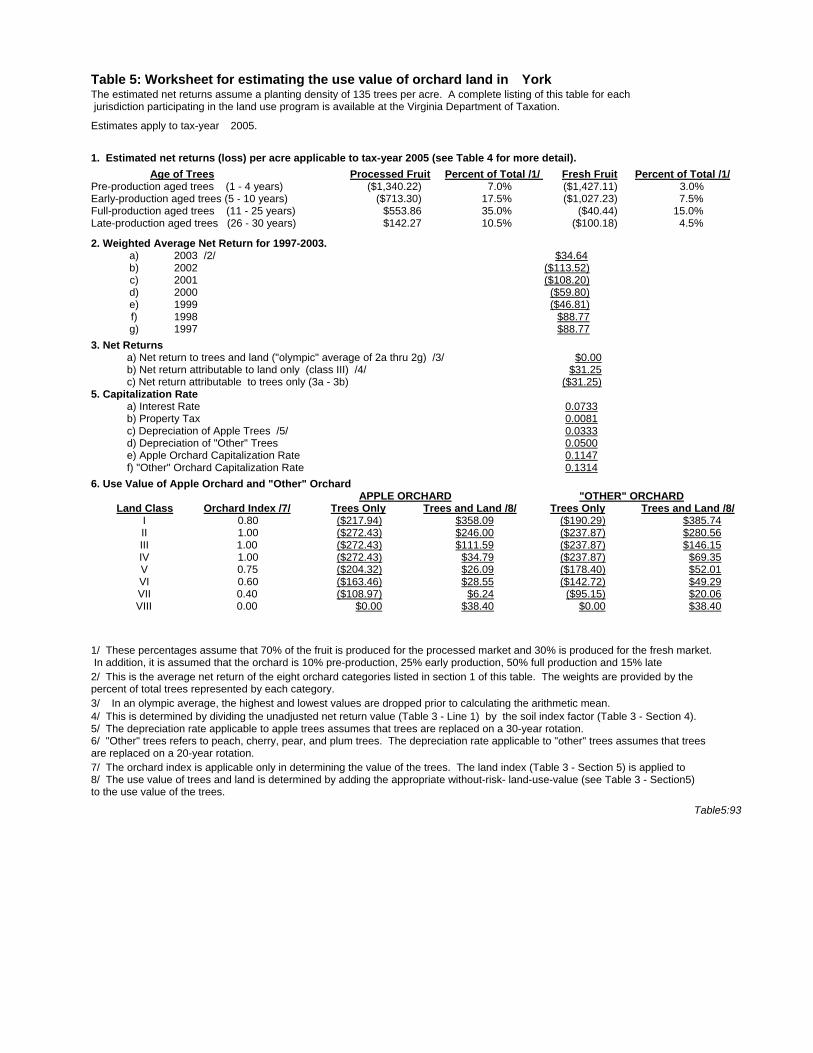

Table 5: Worksheet for estimating the use value of orchard land in Bland The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $22.36 c) Net return attributable to trees only (3a - 3b) ($22.36) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0056 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1122 f) "Other" Orchard Capitalization Rate 0.1289 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($159.39) $265.77 ($138.78) $286.38 II 1.00 ($199.24) $183.40 ($173.47) $209.17 III 1.00 ($199.24) $84.20 ($173.47) $109.97 IV 1.00 ($199.24) $27.51 ($173.47) $53.28 V 0.75 ($149.43) $20.63 ($130.11) $39.96 VI 0.60 ($119.54) $22.18 ($104.08) $37.64 VII 0.40 ($79.70) $5.34 ($69.39) $15.64 VIII 0.00 $0.00 $28.34 $0.00 $28.34

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:9

Table 5: Worksheet for estimating the use value of orchard land in Botetourt The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $15.33 c) Net return attributable to trees only (3a - 3b) ($15.33) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0064 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1131 f) "Other" Orchard Capitalization Rate 0.1297 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($108.51) $180.01 ($94.57) $193.95 II 1.00 ($135.64) $124.03 ($118.21) $141.46 III 1.00 ($135.64) $56.71 ($118.21) $74.14 IV 1.00 ($135.64) $18.24 ($118.21) $35.67 V 0.75 ($101.73) $13.68 ($88.66) $26.75 VI 0.60 ($81.38) $14.79 ($70.93) $25.25 VII 0.40 ($54.25) $3.45 ($47.28) $10.42 VIII 0.00 $0.00 $19.23 $0.00 $19.23

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:10

Table 5: Worksheet for estimating the use value of orchard land in Buena Vista 21/ The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $11.10 c) Net return attributable to trees only (3a - 3b) ($11.10) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0077 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1143 f) "Other" Orchard Capitalization Rate 0.1310 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($77.65) $127.85 ($67.78) $137.73 II 1.00 ($97.07) $87.89 ($84.72) $100.24 III 1.00 ($97.07) $39.94 ($84.72) $52.29 IV 1.00 ($97.07) $12.54 ($84.72) $24.88 V 0.75 ($72.80) $9.40 ($63.54) $18.66 VI 0.60 ($58.24) $10.26 ($50.83) $17.67 VII 0.40 ($38.83) $2.27 ($33.89) $7.21 VIII 0.00 $0.00 $13.70 $0.00 $13.70

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:11

Table 5: Worksheet for estimating the use value of orchard land in Campbell The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $9.97 c) Net return attributable to trees only (3a - 3b) ($9.97) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0047 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1113 f) "Other" Orchard Capitalization Rate 0.1280 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($71.67) $120.15 ($62.34) $129.48 II 1.00 ($89.59) $83.05 ($77.93) $94.71 III 1.00 ($89.59) $38.29 ($77.93) $49.96 IV 1.00 ($89.59) $12.71 ($77.93) $24.38 V 0.75 ($67.19) $9.53 ($58.44) $18.28 VI 0.60 ($53.75) $10.19 ($46.76) $17.19 VII 0.40 ($35.84) $2.53 ($31.17) $7.19 VIII 0.00 $0.00 $12.79 $0.00 $12.79

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:12

Table 5: Worksheet for estimating the use value of orchard land in Caroline The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $19.53 c) Net return attributable to trees only (3a - 3b) ($19.53) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0064 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1130 f) "Other" Orchard Capitalization Rate 0.1297 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($138.21) $229.32 ($120.45) $247.08 II 1.00 ($172.77) $158.01 ($150.57) $180.21 III 1.00 ($172.77) $72.25 ($150.57) $94.45 IV 1.00 ($172.77) $23.25 ($150.57) $45.45 V 0.75 ($129.58) $17.44 ($112.93) $34.09 VI 0.60 ($103.66) $18.85 ($90.34) $32.17 VII 0.40 ($69.11) $4.40 ($60.23) $13.28 VIII 0.00 $0.00 $24.50 $0.00 $24.50

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:13

Table 5: Worksheet for estimating the use value of orchard land in Carroll The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average of 2a thru 2g) /3/ . Net Returns

$0.00 b) Net return attributable to land only (class III) /4/ c) Net return attributable to trees only (3a - 3b) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0041 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1107 f) "Other" Orchard Capitalization Rate 0.1274 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard Index /7/ Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 II 1.00 III 1.00 IV 1.00 V 0.75 VI 0.60 VII 0.40 VIII 0.00

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:14

Table 5: Worksheet for estimating the use value of orchard land in Chesapeake City The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $25.29 c) Net return attributable to trees only (3a - 3b) ($25.29) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0122 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1188 f) "Other" Orchard Capitalization Rate 0.1355 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($170.26) $273.41 ($149.32) $294.35 II 1.00 ($212.82) $186.48 ($186.65) $212.65 III 1.00 ($212.82) $82.96 ($186.65) $109.13 IV 1.00 ($212.82) $23.80 ($186.65) $49.97 V 0.75 ($159.61) $17.85 ($139.98) $37.48 VI 0.60 ($127.69) $20.20 ($111.99) $35.90 VII 0.40 ($85.13) $3.60 ($74.66) $14.07 VIII 0.00 $0.00 $29.58 $0.00 $29.58

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:15

Table 5: Worksheet for estimating the use value of orchard land in Chesterfield 17/ The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $23.37 c) Net return attributable to trees only (3a - 3b) ($23.37) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0100 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1166 f) "Other" Orchard Capitalization Rate 0.1333 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($160.28) $260.51 ($140.24) $280.55 II 1.00 ($200.35) $178.36 ($175.30) $203.41 III 1.00 ($200.35) $80.18 ($175.30) $105.23 IV 1.00 ($200.35) $24.07 ($175.30) $49.12 V 0.75 ($150.26) $18.05 ($131.47) $36.84 VI 0.60 ($120.21) $20.05 ($105.18) $35.08 VII 0.40 ($80.14) $4.02 ($70.12) $14.04 VIII 0.00 $0.00 $28.05 $0.00 $28.05

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:16

Table 5: Worksheet for estimating the use value of orchard land in Clarke The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $15.85 c) Net return attributable to trees only (3a - 3b) ($15.85) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0076 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1142 f) "Other" Orchard Capitalization Rate 0.1309 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($111.05) $183.00 ($96.91) $197.15 II 1.00 ($138.82) $125.84 ($121.14) $143.51 III 1.00 ($138.82) $57.22 ($121.14) $74.90 IV 1.00 ($138.82) $18.01 ($121.14) $35.69 V 0.75 ($104.11) $13.51 ($90.85) $26.77 VI 0.60 ($83.29) $14.73 ($72.68) $25.34 VII 0.40 ($55.53) $3.28 ($48.46) $10.36 VIII 0.00 $0.00 $19.60 $0.00 $19.60

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:17

Table 5: Worksheet for estimating the use value of orchard land in Culpeper The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $20.96 c) Net return attributable to trees only (3a - 3b) ($20.96) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0071 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1137 f) "Other" Orchard Capitalization Rate 0.1304 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($147.45) $243.66 ($128.60) $262.51 II 1.00 ($184.31) $167.69 ($160.75) $191.25 III 1.00 ($184.31) $76.43 ($160.75) $99.99 IV 1.00 ($184.31) $24.28 ($160.75) $47.84 V 0.75 ($138.23) $18.21 ($120.56) $35.88 VI 0.60 ($110.59) $19.78 ($96.45) $33.92 VII 0.40 ($73.73) $4.50 ($64.30) $13.92 VIII 0.00 $0.00 $26.07 $0.00 $26.07

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:18

Table 5: Worksheet for estimating the use value of orchard land in Cumberland The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $4.47 c) Net return attributable to trees only (3a - 3b) ($4.47) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0047 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1114 f) "Other" Orchard Capitalization Rate 0.1280 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($32.09) $53.79 ($27.92) $57.97 II 1.00 ($40.12) $37.18 ($34.90) $42.40 III 1.00 ($40.12) $17.14 ($34.90) $22.36 IV 1.00 ($40.12) $5.69 ($34.90) $10.91 V 0.75 ($30.09) $4.27 ($26.17) $8.18 VI 0.60 ($24.07) $4.56 ($20.94) $7.69 VII 0.40 ($16.05) $1.13 ($13.96) $3.22 VIII 0.00 $0.00 $5.73 $0.00 $5.73

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:19

Table 5: Worksheet for estimating the use value of orchard land in Danville 16/ The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $12.22 c) Net return attributable to trees only (3a - 3b) ($12.22) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0065 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1132 f) "Other" Orchard Capitalization Rate 0.1298 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($86.42) $143.28 ($75.32) $154.37 II 1.00 ($108.02) $98.70 ($94.15) $112.57 III 1.00 ($108.02) $45.11 ($94.15) $58.97 IV 1.00 ($108.02) $14.48 ($94.15) $28.35 V 0.75 ($81.02) $10.86 ($70.61) $21.26 VI 0.60 ($64.81) $11.75 ($56.49) $20.07 VII 0.40 ($43.21) $2.73 ($37.66) $8.28 VIII 0.00 $0.00 $15.31 $0.00 $15.31

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:20

Table 5: Worksheet for estimating the use value of orchard land in Dinwiddie County, Coastal Plain The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $15.08 c) Net return attributable to trees only (3a - 3b) ($15.08) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0066 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1132 f) "Other" Orchard Capitalization Rate 0.1299 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($106.55) $176.59 ($92.88) $190.26 II 1.00 ($133.19) $121.64 ($116.10) $138.73 III 1.00 ($133.19) $55.57 ($116.10) $72.66 IV 1.00 ($133.19) $17.82 ($116.10) $34.91 V 0.75 ($99.89) $13.37 ($87.07) $26.18 VI 0.60 ($79.91) $14.47 ($69.66) $24.72 VII 0.40 ($53.27) $3.35 ($46.44) $10.19 VIII 0.00 $0.00 $18.88 $0.00 $18.88

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:21

Table 5: Worksheet for estimating the use value of orchard land in Dinwiddie County, Piedmont 6/ The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $7.83 c) Net return attributable to trees only (3a - 3b) ($7.83) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0066 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1132 f) "Other" Orchard Capitalization Rate 0.1299 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($55.32) $91.68 ($48.22) $98.78 II 1.00 ($69.14) $63.15 ($60.27) $72.02 III 1.00 ($69.14) $28.85 ($60.27) $37.72 IV 1.00 ($69.14) $9.25 ($60.27) $18.12 V 0.75 ($51.86) $6.94 ($45.20) $13.59 VI 0.60 ($41.49) $7.51 ($36.16) $12.83 VII 0.40 ($27.66) $1.74 ($24.11) $5.29 VIII 0.00 $0.00 $9.80 $0.00 $9.80

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:22

Table 5: Worksheet for estimating the use value of orchard land in Fairfax* 18/ The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $17.53 c) Net return attributable to trees only (3a - 3b) ($17.53) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0106 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1172 f) "Other" Orchard Capitalization Rate 0.1339 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($119.62) $193.81 ($104.73) $208.70 II 1.00 ($149.53) $132.56 ($130.91) $151.17 III 1.00 ($149.53) $59.42 ($130.91) $78.04 IV 1.00 ($149.53) $17.63 ($130.91) $36.25 V 0.75 ($112.15) $13.23 ($98.18) $27.19 VI 0.60 ($89.72) $14.76 ($78.55) $25.93 VII 0.40 ($59.81) $2.87 ($52.36) $10.32 VIII 0.00 $0.00 $20.90 $0.00 $20.90

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:23

Table 5: Worksheet for estimating the use value of orchard land in Fauquier The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $10.22 c) Net return attributable to trees only (3a - 3b) ($10.22) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0090 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1156 f) "Other" Orchard Capitalization Rate 0.1323 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($70.73) $115.61 ($61.81) $124.52 II 1.00 ($88.41) $79.30 ($77.27) $90.44 III 1.00 ($88.41) $35.82 ($77.27) $46.96 IV 1.00 ($88.41) $10.97 ($77.27) $22.11 V 0.75 ($66.31) $8.23 ($57.95) $16.58 VI 0.60 ($53.04) $9.07 ($46.36) $15.75 VII 0.40 ($35.36) $1.90 ($30.91) $6.36 VIII 0.00 $0.00 $12.42 $0.00 $12.42

1/ These percentages assume that 70% of the fruit is produced for the processed market and 30% is produced for the fresh market. In addition, it is assumed that the orchard is 10% pre-production, 25% early production, 50% full production and 15% late 2/ This is the average net return of the eight orchard categories listed in section 1 of this table. The weights are provided by the percent of total trees represented by each category. 3/ In an olympic average, the highest and lowest values are dropped prior to calculating the arithmetic mean. 4/ This is determined by dividing the unadjusted net return value (Table 3 - Line 1) by the soil index factor (Table 3 - Section 4). 5/ The depreciation rate applicable to apple trees assumes that trees are replaced on a 30-year rotation. 6/ "Other" trees refers to peach, cherry, pear, and plum trees. The depreciation rate applicable to "other" trees assumes that trees are replaced on a 20-year rotation. 7/ The orchard index is applicable only in determining the value of the trees. The land index (Table 3 - Section 5) is applied to 8/ The use value of trees and land is determined by adding the appropriate without-risk- land-use-value (see Table 3 - Section5) to the use value of the trees. Table5:24

Table 5: Worksheet for estimating the use value of orchard land in Floyd The estimated net returns assume a planting density of 135 trees per acre. A complete listing of this table for each jurisdiction participating in the land use program is available at the Virginia Department of Taxation. Estimates apply to tax-year 2005.

1. Estimated net returns (loss) per acre applicable to tax-year 2005 (see Table 4 for more detail). Age of Trees Processed Fru ti Percent of To al /1/ t Fresh Fruit Percent of Total /1/ Pre-production aged trees (1 - 4 years) ($1,340.22) 7.0% ($1,427.11) 3.0% Early-production aged trees (5 - 10 years) ($713.30) 17.5% ($1,027.23) 7.5% Full-production aged trees (11 - 25 years) $553.86 35.0% ($40.44) 15.0% Late-production aged trees (26 - 30 years) $142.27 10.5% ($100.18) 4.5% 2 e a) 2003 /2/ . Weight d Average Net Return for 1997-2003.

$34.64 b) 2002 ($113.52) c) 2001 ($108.20) d) 2000 ($59.80) e) 1999 ($46.81) f) 1998 $88.77 g) 1997 $88.77 3 a) Net return to trees and land ("olympic" average o 2a thru 2g) /3/ . Net Returns

$0.00 f b) Net return attributable to land only (class III) /4/ $17.90 c) Net return attributable to trees only (3a - 3b) ($17.90) 5 a) Interest Rate . Capitalization Rate

0.0733 b) Property Tax 0.0053 c) Depreciation of Apple Trees /5 0.0333 / d) Depreciation of "Other" Trees 0.0500 e) Apple Orchard Capitalization Rate 0.1119 f) "Other" Orchard Capitalization Rate 0.1285 . Use Value of Apple Orchard and "Other" Orchard 6

APPL ORCHARDE "OTH R" ORCHARDE Land Class Orchard In ex /7/d Trees Only Trees and Land /8/ Trees Only Trees and Land /8/ I 0.80 ($127.98) $213.82 ($111.39) $230.41 II 1.00 ($159.98) $147.64 ($139.23) $168.39 III 1.00 ($159.98) $67.89 ($139.23) $88.63 IV 1.00 ($159.98) $22.32 ($139.23) $43.06 V 0.75 ($119.98) $16.74 ($104.43) $32.29 VI 0.60 ($95.99) $17.95 ($83.54) $30.39 VII 0.40 ($63.99) $4.37 ($55.69) $12.67 VIII 0.00 $0.00 $22.79 $0.00 $22.79