tab 2 law society of ontario motion to be ......debate resume and a vote be put on the following...

TRANSCRIPT

Tab 2

LAW SOCIETY OF ONTARIO

MOTION TO BE MOVED AT THE MEETING OF CONVOCATION ON APRIL 25, 2019

MOVED BY:

SECONDED BY:

THAT Convocation approve the consent agenda set out at Tab 2 of the Convocation Materials.

Convocation - Consent Agenda - Motion

5

D R A F T

MINUTES OF CONVOCATION

Thursday, 28th February, 2019 8:30 a.m.

PRESENT:

The Treasurer (Malcolm M. Mercer), Anand, Banack, Beach, Bickford, Boyd (by telephone), Braithwaite, Bredt (by telephone), Burd, Callaghan, Chrétien (by telephone), Clément, Cooper, Copeland (by telephone), Corsetti, Criger, Donnelly, Durcan, Earnshaw, Epstein, Evans, Falconer, Ferrier (by telephone), Go, Goldblatt, Gottlieb (by telephone), Groia, Haigh, Hartman, Horvat, Howell, Krishna, Leiper (by telephone), Lem, Lerner, Lippa, MacLean, Manes (by telephone), McDowell, McGrath, Merali, Murchie, Papageorgiou, Pawlitza, Richardson, Richer, Rosenthal, Ross, Ruby (by telephone), Sharda, Sheff, Sikand, Spurgeon, C. Strosberg, H. Strosberg (by telephone), Troister, Udell (by telephone), Vespry, Wardle, Wright and Zordel.

………

Secretary: James Varro The Reporter was sworn.

Convocation - Consent Agenda - Motion

6

3

………

IN PUBLIC

……… TREASURER’S REMARKS The Treasurer welcomed those joining Convocation by webcast.

The Treasurer recognized that Convocation is meeting in Toronto which is a Mohawk word that means “where there are trees standing in the water”.

The Treasurer acknowledged that Convocation is meeting on the traditional territory of

the Mississaugas of New Credit First Nation and acknowledged the Haudenosaunee, and the long history of all of the First Nations in Ontario and the Métis and Inuit peoples. The Treasurer thanked the First Nations people who lived and live in these lands for sharing them with us in peace.

The Treasurer addressed the protocol for Convocation in the Lamont Learning Centre.

The Treasurer noted the call to the bar on January 25, 2019 and congratulated Angela Swan on receiving an honorary LL.D. at the call. The Treasurer announced that at the call, benchers also approved a list of licensing candidates and transfers from outside the province who met the requirements of By-Law 4. The list is at Tab 2.4.2 of the Convocation Materials.

The Treasurer noted the Human Rights Award bestowed last evening on Fiona Sampson and congratulated her on her achievements. The Treasurer offered congratulations to Dianne Corbiere who recently received an Indspire Award. The Treasurer noted the bencher election on April 30, 2019. The Treasurer advised that there are 128 lawyer candidates and 18 paralegal candidates. The Treasurer announced that Jack Braithwaite was acclaimed as the regional bencher for the Northeast Region. The Treasurer noted the following reports for information in the Convocation agenda:

Access to Justice Committee Report and the call for comment on the Law Society’s Access to Justice strategy;

The Discrimination and Harassment Counsel Activity Report for July 1 to December 31, 2018;

The Professional Development and Competence Program and Resource Report for 2018.

Convocation - Consent Agenda - Motion

8

4

LAW FOUNDATION OF ONTARIO PRESENTATION Tanya Lee, Chief Executive Officer of the Law Foundation of Ontario, presented the Foundation’s 2017 Annual Report. MOTION – CONSENT AGENDA – Tab 2 It was moved by Ms. Horvat, seconded by Mr. Wardle that the consent agenda at Tab 2 of the Convocation Materials be approved.

Carried

Tab 2.1 – DRAFT MINUTES OF CONVOCATION

The draft minutes of Convocation of November 30 and December 10, 2018 were confirmed. Tab 2.2 – MOTIONS Re: Tab 2.2.1

THAT Convocation approve Wednesday, May 8, 2019 at 5:15 p.m. at Osgoode Hall, 130 Queen Street West, Toronto as the time and place of the 2018 Annual General Meeting, in accordance with Section 5 of By-Law 2 [Corporate Provisions].

Carried Re: Tab 2.2.2

THAT the following be reappointed to the Hearing Division of the Law Society Tribunal for a term from March 1, 2019 to February 28, 2021:

Murray Walter Chitra

Margaret Leighton

Shayne Kert

THAT Marian Lippa be removed from the Hearing Division of the Law Society Tribunal at her own request.

Carried Re: Tab 2.2.3

THAT, pursuant to a Notice of Motion made under Section 93 of By-Law 3 by Jacqueline Horvat and Peter Wardle on January 25, 2019 and sent to benchers on February 1, 2019, debate resume and a vote be put on the following motion in the November 30, 2018 report of the Governance Task Force 2016, which motion was tabled at November 30, 2018 Convocation:

That Convocation adopt the Governance Policies and Practices incorporating the Bencher Code of Conduct and the Declaration of Adherence, set out at Tab 3.1.

Carried

Convocation - Consent Agenda - Motion

9

5

Tab 2.3 – EQUITY AND INDIGENOUS AFFAIRS COMMITTEE/COMITÉ SUR L’ÉQUITÉ ET LES AFFAIRES AUTOCHTONES REPORT Re: Human Rights Monitoring Group Requests for Interventions That Convocation approve the interventions in the cases set out at paragraphs a. through f. of the motion at Tab 2.3 (page 122 of Diligent Boards).

Carried Tab 2.4.1 – EXECUTIVE DIRECTOR’S REPORT ON ADMINISTRATIVE CALLS TO THE BAR THAT the Report of the Executive Director of Professional Development and Competence listing the names of the call to the bar candidates be adopted.

Carried POINT OF PERSONAL PRIVILEGE Bencher Heather Ross addressed Convocation, in advance of her retirement as a bencher in May 2019, on her experience as a bencher. GOVERNANCE TASK FORCE 2016 REPORT Ms. Criger presented the Report. Re: Law Society Governance Practices and Policies

It was moved by Ms. Criger, seconded by Ms. Papageorgiou, that Convocation adopt the Governance Policies and Practices incorporating the Bencher Code of Conduct and the Declaration of Adherence, set out at Tab 3.1.

Ms. Vespry moved, seconded by Mr. Sharda, that paragraph 32 of the Governance

Practices and Policies be struck. Lost

Mr. Groia moved, seconded by Mr. Troister, that paragraph 32 of the Governance Practices and Policies be amended by adding “and a duty of care, being the duty to exercise the care, diligence and skill of a reasonably prudent person” after the word “loyalty”.

Lost Ms. Criger accepted an amendment proposed by Mr. Falconer to delete the words “Benchers are seen from afar and it is for this reason that” from paragraph 32 of the Bencher Code of Conduct.

Convocation - Consent Agenda - Motion

10

6

The main motion carried.

ROLL-CALL VOTE

Anand For Howell For

Beach Abstain Leiper For

Bickford For Lem For

Boyd For Lerner For

Braithwaite For Lippa For

Bredt For MacLean For

Burd For McDowell For

Callaghan For McGrath For

Chrétien For Merali For

Clément For Murchie For

Cooper For Papageorgiou For

Corsetti For Richardson For

Criger For Richer Abstain

Donnelly Against Rosenthal For

Durcan For Sharda Against

Earnshaw For Sheff Against

Epstein For Sikand For

Evans For Spurgeon For

Falconer For C. Strosberg Against

Ferrier For H. Strosberg Against

Go For Troister For

Goldblatt For Udell For

Groia Against Vespry Against

Haigh For Wardle For

Hartman For Zordel Against

Horvat For

Vote: 41 For; 8 Against; 2 Abstentions

Convocation - Consent Agenda - Motion

11

7

TRIBUNAL COMMITTEE REPORT Ms. Merali presented the Report. Re: Proposed Law Society Tribunal Rules of Practice and Procedure

It was moved by Ms. Merali, seconded by Ms. Murchie: That Convocation revoke, effective April 1, 2019, the current Law Society Tribunal

Hearing Division and Appeal Division Rules of Practice and Procedure and the forms under those rules; and

that Convocation make, to be effective April 1, 2019, the Law Society Tribunal Rules of

Practice and Procedure in English and French and corresponding forms, as set out at Tabs 4.1 and 4.2 in English and 4.3 and 4.4 in French, pursuant to s. 61.2 of the Law Society Act, RSO 1990, c. L. 8.

Not Put Mr. Cooper moved, seconded by Ms. Vespry, that Rule 11.7 in the proposed Rules of Practice and Procedure to be made by Convocation be replaced with the text of Rule 11.7 in English and French set out at Tab 4.6 of the report.

Not Put Mr. Groia moved, seconded by Ms. Hartman, that the report be tabled.

Convocation - Consent Agenda - Motion

12

8

ROLL-CALL VOTE

Anand Against Howell Against

Beach For Krishna For

Bickford Against Leiper Against

Braithwaite Against Lem For

Bredt Against Lerner For

Burd For MacLean Against

Chrétien Against McDowell Against

Clément For McGrath Against

Cooper For Merali Against

Corsetti Against Murchie Against

Criger Against Papageorgiou Against

Donnelly For Richardson Against

Durcan Against Richer For

Earnshaw For Sharda For

Epstein For Sheff For

Evans Against Sikand For

Go For Spurgeon For

Goldblatt Against C. Strosberg For

Groia For Troister For

Haigh Against Vespry For

Hartman For Wardle Against

Horvat For Zordel For

Vote: 23 For; 21 Against Carried

PROFESSIONAL REGULATION COMMITTEE REPORT Re: Final Report of the Alternative Business Structures Working Group Ms. McGrath presented the Report.

It was moved by Ms. McGrath, seconded by Ms. Clément, that Convocation approve the

following, effective April 1, 2019, in order to implement a regulatory framework that permits

Convocation - Consent Agenda - Motion

13

9

lawyers and paralegals to provide legal services through registered civil society organizations

to the public:

a. Amendments to sections 1.1, 3.1, 3.4, and 3.6 of the Rules of Professional Conduct

as set out in Tab 5.1.1 (English) and Tab 5.1.2 (French);

b. Amendments to sections 1.02, 3.04 and 5.01 of the Paralegal Rules of Conduct as set

out in Tab 5.1.3 (English) and Tab 5.1.4 (French);

c. Request the Paralegal Standing Committee to amend the related Paralegal

Guidelines as set out in Tab 5.1.3 (English) and Tab 5.1.4 (French);

d. Amendments to By-Law 7, Part VI, regarding services delivered by lawyers and

paralegals to the public though civil society organizations, and minor amendments

to multi-discipline practices and affiliations, as set out in the motion at Tab 5.1.5

(English and French), shown in clean format at Tab 5.1.6 (English and French) and

shown in redline format at Tab 5.1.7 (English and French).

Carried Re: Review of the Good Character Process Ms. Horvat presented the Report.

It was moved by Ms. Horvat, seconded by Mr. Howell, that Convocation approve enhancements and improvements to the good character assessment process and the materials that communicate that process to applicants, licensees, and members of the public as set out in paragraphs 1 through 4 of the motion in the report at Tab 5.2 of the Convocation Materials.

Ms. Horvat accepted an amendment proposed by Ms. Donnelly to replace “convictions” with “findings of guilt” in paragraph 4. i) of the motion. The main motion carried.

Convocation - Consent Agenda - Motion

14

12

………

IN PUBLIC

………

REPORTS FOR INFORMATION ONLY

AUDIT & FINANCE COMMITTEE REPORT LawPRO Financial Statements for the Nine Months Ended September 30, 2018 EQUITY AND INDIGENOUS AFFAIRS COMMITTEE/COMITÉ SUR L’ÉQUITÉ ET LES AFFAIRES AUTOCHTONES REPORT Report of the Activities of the Discrimination and Harassment Counsel for the period of July

1 to December 31, 2018 Human Rights Monitoring Group January 2019 Interventions Human Rights Award Ceremony – Highlight Report Equity Legal Education and Rule of Law Series Calendar PROFESSIONAL DEVELOPMENT AND COMPETENCE COMMITTEE REPORT Professional Development and Competence Division 2018 Program and Resource Report ACCESS TO JUSTICE COMMITTEE REPORT Call for Comment: Law Society of Ontario Access to Justice Approach Family Law Working Group Update

CONVOCATION ROSE AT 1:27 P.M.

Convocation - Consent Agenda - Motion

16

Tab 2.2

LAW SOCIETY OF ONTARIO

MOTION TO BE MOVED AT THE MEETING OF CONVOCATION ON APRIL 25, 2019

THAT Jack Braithwaite be reappointed as the Law Society's representative on the Canadian National Exhibition Association for a term of one year commencing June 5, 2019. THAT Evelyn Baxter be appointed to the Access to Justice Committee and the Legal Aid Working Group.

To the Benchers of the Law Society of Ontario Assembled in Convocation

The Executive Director of Professional Development and Competence reports as follows:

CALL TO THE BAR AND CERTIFICATE OF FITNESS

Licensing Process and Transfer from another Province – By-Law 4

Attached is a list of candidates who have successfully completed the Licensing Process and have met the requirements in accordance with section 9.

All candidates now apply to be called to the bar and to be granted a Certificate of Fitness on Thursday, April 25th 2019

ALL OF WHICH is respectfully submitted

DATED this 25th day of April, 2019

Convocation - Consent Agenda - Motion

19

CANDIDATES FOR CALL TO THE BARApril 25th 2019

Transfer from another province (Mobility)

Michael William ClarkeAndrea Stephanie Collins-FitzpatrickCarolle Shannon FernandoEric William FeunekesJessica Lyn GreenSuzanne HathawajKelly Patricia KeenanOliver David Thomas LoxleyMeaghan McConnellSunil SharmaDevlin John Steers

Licensing Candidates

Rafiga Gurbanzade

Transfer Candidates (from Québec)

Caroline BélairJordan BélangerElissa Lauren BrockElizabeth Marie ChenAndrée-Anne Marie Chantal LavoieÉrik Cléroux Claude Tremblay

Convocation - Consent Agenda - Motion

20

April 25, 2019

Report of the Equity and Indigenous Affairs

Committee

Report for Decision

Committee Members:

Dianne Corbiere (Chair) Isfahan Merali (Vice-Chair)

Robert Burd Gisèle Chrétien

Robert Evans Julian Falconer

Avvy Go Marian Lippa

Gina Papageorgiou Andrew Spurgeon

Sidney Troister Tanya Walker

Prepared by: Laura Wilson-Lewis, Equity Initiatives

Tab 2.4

Convocation - Consent Agenda - Motion

21

Report of the Equity and Indigenous Affairs Committee

1

Table of Contents

FOR DECISION

Human Rights Monitoring Group: Requests for Intervention ...................................................... TAB 2.4.1

Convocation - Consent Agenda - Motion

22

1

Tab 2.4.1

FOR DECISION

Human Rights Monitoring Group: Requests for Intervention

Motion

That Convocation approve the interventions in the following cases:

a. Conviction and sentencing of lawyer Nasrin Sotoudeh – Iran

b. Murder of lawyer Rex Jasper Lopoz – Philippines

c. Surveillance and restrictions on freedom of movement of lawyer Jiang Tianyong – China

Rationale

The request for interventions falls within the mandate of the Human Rights Monitoring Group (the “Monitoring Group”) to:

a. review information that comes to its attention about human rights violations that target members of the profession and the judiciary, here and abroad, as a result of the discharge of their legitimate professional duties;

b. review information that comes to its attention about human rights violations that target human rights defenders in the same event or circumstances as a member of the legal profession or the judiciary as described in a) above;

c. determine if the matter is one that requires a response from the Law Society; and

d. prepare a response for review and approval by Convocation.

Key Issues and Considerations

The Monitoring Group considered the following factors when making a decision about the letters and public statements above:

a. there are no concerns about the quality of sources used for this report; and

b. the letters and public statements above fall within the mandate of the Monitoring Group.

Convocation - Consent Agenda - Motion

23

2

Key Background

Iran – Conviction and sentencing of lawyer Nasrin Sotoudeh

Sources of Information

The background information for this report was retrieved from the following sources:

a. Council of Bars and Law Societies of Europe (CCBE);1

b. Al Jazeera;2

c. United Nations, Office of the High Commissioner of Human Rights;3

d. CBC;4

e. U.S. Department of State;5

f. Amnesty International;6

g. Human Rights Watch;7 and

h. Radio Free Europe/Radio Liberty.8

1 Re: Sentencing of lawyer Nasrin Sotoudeh, Council of Bars and Law Societies of Europe, 13 March 2019, online: <https://www.ccbe.eu/fileadmin/speciality_distribution/public/documents/HUMAN_RIGHTS_LETTERS/Iran_-_Iran/2019/EN_HRL_20190313_Iran_Sentencing-of-lawyer-Nasrin-Sotoudeh.pdf> [CCBE Iran].2 Amnesty: Sentencing of Iran lawyer Sotoudeh 'outrageous', Al Jazeera, 12 Mar 2019, online: < https://www.aljazeera.com/news/2019/03/amnesty-sentencing-iran-lawyer-sotoudeh-outrageous-190312102532646.html> [Al Jazeera Iran]. 3 Iran: UN experts “shocked” at lengthy prison sentence for human rights lawyer Nasrin Sotoudeh, OHCHR, 14 Mar 2019, online: <https://www.ohchr.org/EN/NewsEvents/Pages/DisplayNews.aspx?NewsID=24333&LangID=E> [UN Iran].4 Iranian human rights lawyer Nasrin Sotoudeh sentenced to 38 years, 148 lashes, husband says, CBC News, 11 Mar 2019, online: < https://www.cbc.ca/news/world/nasrin-sotoudeh-iran-human-rights-lawyer-sentence-1.5051631> [CBC Iran].5 Robert Palladino (Deputy Spokesperson), Department Press Briefing, US Department of State, 12 Mar 2019, online: <https://www.state.gov/r/pa/prs/dpb/2019/03/290298.htm> [US State Iran].6 Iran: Shocking 33-year prison term and 148 lashes for women’s rights defender Nasrin Sotoudeh, Amnesty International, 11 Mar 2019, online: <https://www.amnesty.org/en/latest/news/2019/03/iran-shocking-33-year-prison-term-and-148-lashes-for-womens-rights-defender-nasrin-sotoudeh/> [Amnesty Iran]; Urgent Action: 38 Years and 148 Lashes for Women’s Rights Defender, Amnesty International, 14 Mar 2019, online: <https://www.amnesty.org/download/Documents/MDE1300242019ENGLISH.pdf> [Amnesty Iran 2]. 7 Iran: Decades-Long Sentence for Women’s Rights Defender, Human Rights Watch, 12 Mar 2019, online: <https://www.hrw.org/news/2019/03/12/iran-decades-long-sentence-womens-rights-defender> [HRW Iran]. 8 Prison Sentence For Iran Rights Lawyer 'Beyond Barbaric,' U.S. Says, RadioFreeEurope/RadioLiberty, 13 Mar 2019, online: <https://www.rferl.org/a/prison-sentence-for-iran-rights-lawyer-beyond-barbaric-u-s-says/29818748.html> [RadioFree].

Convocation - Consent Agenda - Motion

24

3

Background

Nasrin Sotoudeh is a human rights lawyer in Iran who faces ongoing detention for her work representing women who were prosecuted for removing their headscarves in public.9 Nasrin Sotoudeh has been detained at Evin prison since June 2018 to serve a five-year sentence issued against her on September 3, 2016, in absentia. She was not aware of the charges and sentence she received until her June 13, 2018 arrest.10 Credible reports indicate this five-year sentence was based solely on her human rights activism.11

Nasrin Sotoudeh has recently been convicted on seven charges, and sentenced to 33 years in prison and 148 lashes in addition to her 2016 sentence.12 According to credible reports, the charges stem solely from her human rights work and for having spoken out against the death penalty in Iran.13

On February 9, 2019, authorities at Evin prison informed her of the sentence and the conviction on seven charges which include, “inciting corruption and prostitution”, “openly committing a sinful act by...appearing in public without a hijab”, “disrupting public order”, and “assembly and collusion against national security”.14 However, Judge Mohammad Moghiseh, who rendered the sentencing decision, told the Iranian Student News Agency on March 11 that his court had sentenced her to five years on the charge of “assembly and collusion against the state” and two years on the charge of “insulting the supreme leader”.15 It has been reported that he also told journalists that “the verdict was not issued in her absence because she had a lawyer”.16

Credible reports indicate that her trial, which took place on December 30, 2018 at Branch 28 of the Revolutionary Court in Tehran, was held in her absence.17 She had refused to attend this trial in protest of its unjust nature. Reports state that, in particular, she was denied the right to a lawyer of her own choosing and instead asked to choose from a list of lawyers pre-approved by the Iranian judiciary.18

We are deeply concerned by Nasrin Sotoudeh’s conviction and sentence as this is the harshest sentence that has been documented by Amnesty International against a human rights defender

9 CBC Iran, supra note 4. 10 UN Iran, supra note 3; Amnesty Iran, supra note 6. 11 HRW Iran, supra note 7. 12 Amnesty Iran, supra note 6; CCBE Iran, supra note 1.13 Amnesty Iran 2, supra note 6. 14 Amnesty Iran, supra note 6; HRW Iran, supra note 7.15 HRW Iran, ibid.16 Amnesty Iran 2, supra note 6.17 Amnesty Iran 2, ibid.18 UN Iran, supra note 3.

Convocation - Consent Agenda - Motion

25

4

in Iran in recent years.19 Credible reports suggest that the Iranian government has been increasing its repression on activists and rights defenders,20 and that Nasrin Sotoudeh’s situation is representative of an increase in the harassment, arrest and detention of human rights lawyers in Iran in recent months.21

The Law Society has previously intervened on Nasrin Sotoudeh’s behalf. We have urged the government of Iran to address Nasrin Sotoudeh’s situation in previous letters of intervention dated September 2010, October 30, 2013, December 9, 2014, September 2018 and February 2019. In our most recent letter, we expressed our concerns with respect to the harsh treatment faced by Nasrin Sotoudeh and other female detainees at Evin Prison’s Women’s Ward. We understand that Nasrin Sotoudeh has endured two hunger strikes at Evin prison in protest against such conditions, including repeated denials of her rights to see her son and daughter.22

Governments and human rights organizations around the world have collectively expressed shock at the recent conviction and sentencing of Nasrin Sotoudeh.23 United Nations human rights experts have called on Iran to “immediately free prominent human rights lawyer and defender Nasrin Sotoudeh from jail pending a review of her conviction and sentence”.24

The Law Society strongly condemns the charges, conviction and sentence against Nasrin Sotoudeh.

Philippines – Murder of lawyer Rex Jasper Lopoz

Sources of Information

The background information for this report was retrieved from the following sources:

a. Human Rights Watch;25

19 Amnesty Iran, supra note 6. 20 Al Jazeera Iran, supra note 2; Amnesty Iran, supra note 6.21 UN Iran, supra note 3. 22 Al Jazeera Iran, supra note 2. See also, Evin Prison Repeatedly Blocking Nasrin Sotoudeh From Seeing Her Children, Center for Human Rights in Iran, 18 Jan 2019, online: <https://www.iranhumanrights.org/2019/01/evin-prison-repeatedly-blocking-nasrin-sotoudeh-from-seeing-her-children/>. 23 Amnesty Iran, supra note 6; RadioFree, supra note 8; US State Iran, supra note 5.24 UN Iran, supra note 3.25 Philippine Lawyer Possible Victim of ‘Drug War’ Murder, Human Rights Watch, 15 Mar 2019, online: < https://www.hrw.org/news/2019/03/15/philippine-lawyer-possible-victim-drug-war-murder> [HRW Philippines].

Convocation - Consent Agenda - Motion

26

5

b. Amnesty International;26 and

c. CNN.27

Background

Rex Jasper Lopoz was a lawyer who had been representing defendants in drug-related cases in the Philippines. Reports state that he was shot and killed outside of a shopping mall in Tagum City, Davao del Norte, on March 13, 2019 by unidentified individuals.28

Rex Jasper Lopoz is the 38th lawyer to have been killed in the Philippines since President Rodrigo Duterte began his presidency in 2016.29 According to credible reports, Rex Jasper Lopoz’s family believes that he was killed because of his work representing the accused in drug cases, and that his murder is connected to the anti-drugs campaign of the current administration.30

Members of the legal profession and the judiciary in the Philippines, including Chief Justice Lucas Bersamin and the Integrated Bar of the Philippines (IBP), have condemned the killing of Rex Jasper Lopoz. According to credible reports, IBP President Abdiel Dan Elijah Fajardo stated that Rex Jasper Lopoz's death is the latest incident of a recent series of violence against lawyers,31 and that lawyers, prosecutors and judges are being targeted with increasing frequency and impunity.32 These murders are among the thousands of extrajudicial killings in the Philippines since President Duterte took office.33

According to credible reports, President Duterte has suggested in the past that the killing of people suspected of using and selling drugs will not be punished, and that such calls have encouraged police and armed civilians to commit murder with impunity.34 The Law Society urges His Excellency to publicly denounce these acts of violence.

26 Philippines: Withdrawal from the ICC must spur UN action, Amnesty International, 17 Mar 2019, online: < https://www.amnesty.org/en/latest/news/2019/03/philippines-withdrawal-icc-spur-un-action/> [Amnesty Philippines]. 27 IBP: 38 lawyers killed since August 2016, CNN, 15 Mar 2019, online: <http://cnnphilippines.com/news/2019/3/15/IBP-lawyer-deaths.html> [CNN Philippines]. 28 HRW Philippines, supra note 25. 29 HRW Philippines, ibid.30 HRW Philippines, ibid.31 CNN Philippines, supra note 27. 32 CNN Philippines, ibid.33 Amnesty Philippines, supra note 26.34 Amnesty Philippines, ibid.

Convocation - Consent Agenda - Motion

27

6

China – Surveillance and restrictions on freedom of movement of lawyer Jiang Tianyong

Sources of Information

The background information for this report was retrieved from the following sources:

a. Front Line Defenders;35

b. Radio Free Asia;36 and

c. Amnesty International.37

Background

Jiang Tianyong is a human rights lawyer in China who has defended a number of persecuted groups including Tibetan activists and Falun Gong practitioners. He has been detained several times in the past, disbarred and denied applications for the renewal of his legal license for his work representing such clients.38

On February 28, 2019, Jiang Tianyong was released from prison at the end of a two-year sentence for “incitement to subvert state power”, according to credible reports.39 Since his release, he has been subjected to oppressive conditions such as heavy surveillance by state security police, being followed by an unidentified group of people dressed in black, and restrictions on his freedom to choose his employment and residence.40

The Law Society has previously intervened on Jiang Tianyong’s behalf after he was arrested, detained and sentenced for exercising his legitimate professional duties. The Law Society has

35 Jiang Tianyong Subjected to Unfair Trial, Front Line Defenders, 29 Nov 2016 – 25 Feb 2018, online: <https://www.frontlinedefenders.org/en/case/jiang-tianyong-subjected-unfair-trial#case-update-id-5300> [FLD China]; Jiang Tianyong: HRD, Lawyer, Front Line Defenders, online: <https://www.frontlinedefenders.org/en/profile/jiang-tianyong> [FLD China Profile].36 Wife of Tortured Chinese Rights Lawyer Calls For Him to Leave China, Radio Free Asia, 11 Mar 2019, online: < https://www.rfa.org/english/news/china/leave-03112019100918.html> [RFA China].37 Urgent Action: Restrictions on Released Human Rights Lawyer, Amnesty International, 15 Mar 2019, online: < https://www.amnesty.org/download/Documents/ASA1700212019ENGLISH.pdf> [Amnesty China].38 FLD China Profile, supra note 35. 39 Amnesty China, supra note 37; RFA China, supra note 36. 40 Amnesty China, ibid.

Convocation - Consent Agenda - Motion

28

7

expressed its concerns regarding violations of his human rights in previous letters of intervention dated February 2017, October 2017 and February 2018.

On November 21, 2016, Jiang Tianyong was forcibly disappeared by Chinese authorities at a Changsha train station after trying to visit human rights lawyer, Xie Yang. Jiang Tianyong was held incommunicado in an unknown location until his formal arrest and detention in a Changsha detention centre in Wuhan Province on May 31, 2017.41 His first trial took place on August 22, 2017 in the Changshua City Intermediate Court, in which he admitted to the charges of “inciting subversion of state power”. In his trial of November 21, 2017, Jiang Tianyong pled guilty to the charges based on guarantees from authorities that he would be released in August 2018 if he pled guilty.42

Jiang Tianyong’s health severely declined during his detention and he remains in serious condition following his release.43 According to credible reports, his friends and family have communicated the following details regarding the treatment he endured in prison: he was forced by prison officials to sit on equipment which caused spine injury making him no longer able to sit upright, he faced psychological trauma which has caused significant memory loss, he was regularly forced to consume unknown medication, his hands and feet were bound to an iron chair, he faced sleep deprivation and beatings, and he was forced to sit on cold concrete for prolonged periods of time during efforts to obtain a confession from him.44

Reports indicate that Jin Bianling, wife of Jiang Tianyong, has called on the government to allow Jiang Tianyong to travel overseas to seek medical treatment.45 The Law Society implores His Excellency to ensure that Jiang Tianyong can safely leave the country to receive necessary medical treatment. As Jiang Tianyong is no longer serving his sentence, the Law Society urges the government of China to take steps so that the surveillance, harassment and other restrictions against him and his family are ceased.

41 FLD China, supra note 35. 42 Amnesty China, supra note 37. Sources conflict regarding the exact date on which Jiang pleaded guilty: August 22, 2017 (RFA China, supra note 36) and November 21, 2017 (Amnesty China, supra note 37). As the latter date has been cited by a specially-weighted source, that date was stated in the letter. 43 RFA China, supra note 36. 44 Amnesty China, supra note 37; RFA China, ibid; FLD China, supra note 35. 45 RFA China, ibid.

Convocation - Consent Agenda - Motion

29

April 25, 2019

Treasurer’s Report -LawPRO Annual Shareholder Resolutions

LibraryCo Inc. Annual Meeting

Authored By:James Varro, Director, Office of the CEO and Corporate Secretary

Tab 2.5

Convocation - Consent Agenda - Motion

30

Treasurer’s Report

1

Table of Contents

Motion - LAWPRO ANNUAL SHAREHOLDER RESOLUTIONS ......................................................... 2

Background ............................................................................................................................... 2

Motion - LIBRARYCO INC. ANNUAL MEETING ............................................................................. 2

Background ............................................................................................................................... 2

Convocation - Consent Agenda - Motion

31

Treasurer’s Report

2

Motion - LAWPRO ANNUAL SHAREHOLDER RESOLUTIONS

That Convocation authorize the Treasurer to sign the shareholder resolutions for the Lawyers’ Professional Indemnity Company (LawPRO) set out at Tab 2.5.1.

Background

As a result of amendments to LawPRO's By-law No. 1, which the Law Society and all shareholders approved in 2014, the Law Society became the sole shareholder of LawPRO effective January 1, 2015.

Accordingly, Convocation's approval is sought to direct the Treasurer to sign the annual Resolutions of the Shareholder. The proposed shareholder resolutions appear at Tab 2.5.1

Also included for the information of Convocation is biographical information on the members of the LawPRO Board at Tab 2.5.2 and LawPRO’s 2018 Financial Statements which are included in the LawPRO Annual Report at Tab 2.5.3.

Motion - LIBRARYCO INC. ANNUAL MEETING

That Convocation authorize the Treasurer to sign the proxy, in favour of the proposed shareholder resolutions, set out at Tab 2.5.4.

Background

The Annual and General Meeting of Shareholders of LibraryCo Inc. will be held next month. The notice of the meeting is attached at Tab 2.5.5.

At the meeting, the shareholder will be asked to vote on the proposed shareholder resolutions set out at Tab 2.5.6.

Traditionally, the Treasurer has signed the proxy to vote the Law Society’s shares in favour of the resolutions. The proxy is set out at Tab 2.5.4.

The Treasurer seeks Convocation’s authorization to sign the proxy on behalf of the Law Society.

Convocation - Consent Agenda - Motion

32

1

LAWYERS’ PROFESSIONAL INDEMNITY COMPANY (the “Corporation”)

RESOLUTIONS OF THE SHAREHOLDER

Dated as of the 25th day of April, 2019

FINANCIAL STATEMENTS WHEREAS the Board of Directors has approved the financial statements of the Corporation for the year ending December 31, 2018; AND WHEREAS the shareholder has received a report of the auditor which includes statements regarding management’s responsibility and the auditor’s responsibility and an opinion from the auditor; RESOLVED that the financial statements of the Corporation for the year ended December 31, 2018 are approved. ELECTION OF DIRECTORS RESOLVED that the following individuals are elected directors of the Corporation to hold office until the next annual meeting of the shareholder or until their successors are elected or appointed: Susan M. Armstrong Clare A. Brunetta Frederick W. Gorbet Malcolm L. Heins Rita Hoff Susan T. McGrath Diana C. Miles Barbara J. Murchie David R. Oliver Daniel E. Pinnington Andrew N. Smith Andrew J. Spurgeon Mark D. Tamminga John C. Thompson Heather L. Zordel

Convocation - Consent Agenda - Motion

33

2

APPOINTMENT OF AUDITOR RESOLVED that PricewaterhouseCoopers LLP is appointed as auditor of the Corporation to hold office until the next annual meeting of the shareholder at such remuneration as may be fixed by the directors and the directors are authorized to fix such remuneration. CONFIRMATION OF ACTS OF DIRECTORS AND OFFICERS RESOLVED that all acts, contracts, by-laws, proceedings, appointments, elections and payments enacted, made, done and taken by the directors and officers of the Corporation to the date hereof, as the same are set out or referred to in the resolutions of the board of directors, the minutes of the meetings of the board of directors or in the financial statements of the Corporation are approved, sanctioned and confirmed. Consented to in writing by the sole shareholder of the Corporation. THE LAW SOCIETY OF ONTARIO Per: ___________________________________ MALCOLM MERCER Treasurer, The Law Society of Ontario

Convocation - Consent Agenda - Motion

34

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Susan T. McGrath

Chair, LAWPRO

Board of Directors

Principal, Susan T. McGrath

A sole practitioner from the northeastern Ontario community of Iroquois Falls, Law Society Bencher Susan McGrath is well-known for being a dedicated advocate for sole practitioners, small firms, and lawyers working in remote areas, and for their access to quality continuing legal education and peer support.

Ms. McGrath was elected as Chair of the LAWPRO Board of Directors in May, 2012, and acts as an ex-officio member of all committees.

Since graduating from Osgoode Hall, Ms. McGrath has been an active member of her local legal community as well as contributing at the national level. She has served on her local legal aid area committee, including a stint as Deputy Area Director, has acted as a Deputy Judge for the Temiskaming Small Claims Court and has served on the Personal Rights Panel of the Office of the Children’s Lawyer.

She has served as President of the Cochrane Law Association (1983-1984), the Ontario Bar Association (1999-2000), and the Canadian Bar Association (2004-2005). As well, she has served in many capacities on committees of these and other legal associations.

As a Bencher of the Law Society of Upper Canada, Ms. McGrath serves on the Hearing Panel, the Appeal Panel, the Government Relations Committee and the Priority Planning Committee. She also serves as Co-Chair of the Alternative Business Structures Working Group and the Vice-Chair of the Paralegal Standing Committee.

Convocation - Consent Agenda - Motion

35

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Malcolm L. Heins, LSM

Vice-Chair, LAWPRO

Board of Directors

Lawyer & Director

A lawyer and former insurance industry executive, Malcolm Heins was appointed Chief Executive Officer of The Law Society of Upper Canada in 2001, retiring in early 2012.

Mr. Heins joined the Counsel Public Affairs team in June 2012, resigning in April of 2015 when he was appointed by the Ontario Minister of Finance to chair The Special Committee to Consider Financial Advisory and Financial Policy Alternatives. The Committee’s report was delivered in November of 2016.

Mr. Heins also served as an interim Chief Executive Officer of the Federation of Law Societies of Canada from November 2005 to June 2006, and from 1994 to 2001, he served as LAWPRO’s first President and Chief Executive Officer.

Prior to that, Mr. Heins was the President and Chief Operating Officer of Gan Canada, formerly Simcoe Erie Group, then one of the largest underwriters of professional liability insurance in Canada. Before joining Gan Canada in 1981, he practised insurance and commercial litigation in Toronto.

With his background in insurance, regulatory oversight, business and law, Mr. Heins now provides consulting services and is a Corporate Director. He is a graduate of the University of Toronto and Dalhousie Law School.

Mr. Heins chairs LAWPRO’s Risk Committee and is a member of LAWPRO’s Executive, Conduct Review, Audit, Governance and Investment committees.

Mr. Heins is a member of the Law Society of Ontario and in addition to LAWPRO, serves as a Director of OMEX, Pro Bono Law Ontario and Cancer Care Ontario. He received the Law Society Medal in June 1999, the 2002 Award of Distinction from the Metropolitan Toronto Lawyers Association and, in March 2005, Communicator of the Year by the International Association of Broadcasters (Toronto).

Convocation - Consent Agenda - Motion

36

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Susan M. Armstrong, FCPA, FCA, ICD.D

Corporate Director

Sue is an experienced Corporate Director and retired President & CEO of CDSPI, a company providing advisory, wealth management, insurance and health and wellness services exclusively to the Canadian dental community.

Sue has over 25 years of experience at the senior executive level in the insurance and reinsurance industries. During this time, she served as Senior Vice-President of Swiss Reinsurance Company Canada, with previous roles at CIBC Insurance and Dominion of Canada General Insurance Company. Prior to her senior executive roles, Sue was a senior manager at PricewaterhouseCoopers’ (PwC).

In addition to serving on the Board of Directors of Lawyers' Professional Indemnity Company (LAWPRO), she serves on the Board of Directors of Canadian Premier Life Insurance Company and Legacy General Insurance Company. Previously, she served as director and Chair of the Audit Committee of McGraw-Hill Ryerson Limited, a public company in the educational publishing industry.

Sue has also made a long-term commitment to the Canadian healthcare sector. She serves as Chair of the Board of Directors of Michael Garron Hospital and as a director of West Park Healthcare Centre. Previously, she served on the boards of the Toronto Rehabilitation Institute and The George Hull Centre for Children and Families, which she chaired for three years.

In recognition of her career accomplishments and contribution to the community, Sue received the FCPA, FCA designation in 2016 from the Chartered Professional Accountants Ontario. She has also earned the ICD.D designation from the Institute of Corporate Directors. Active in organizations focused on networking and executive professional development, Sue is a member of Financial Executives International, International Women’s Forum, Women’s Executive Network and Women Get on Board.

Convocation - Consent Agenda - Motion

37

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Clare A. Brunetta

Principal, Clare A. Brunetta

Clare A. Brunetta is a general practitioner whose office is located in Fort Frances. Primarily serving the District of Rainy River in northwestern Ontario, he practises with his son Paul Brunetta. Mr. Brunetta is former President of the Rainy River Law Library Association, a Charter Member of the Canadian Italian Advocates Society, a past member of the Law Society of Upper Canada Joint Working Group on Real Estate, a past Chair of the Real Estate committee of the County and District Law Presidents Association (CDLPA), and past Co-Chair of the Working Group on Lawyers and Real Estate. He has been a Deputy Judge of the Small Claims Court since 1991.

Mr. Brunetta serves on the LAWPRO Governance and Risk Committees.

Convocation - Consent Agenda - Motion

38

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Frederick W. Gorbet, O.C.

Fred Gorbet has extensive experience in public policy advice and formulation, particularly with regard to financial institutions and energy policy. Following a 25-year career in the Canadian public service, where he served as Associate Secretary to the Cabinet and as Deputy Minister of Finance for Canada, Mr. Gorbet has held several senior executive positions in the life insurance industry and in academe, serving for many years as the CIT Chair in Financial Services and Director of the Financial Services Program at the Schulich School of Business (York University).

A member of the LAWPRO Board of Directors since 2004, Mr. Gorbet currently chairs the Audit Committee and is a member of the Executive, Conduct Review, Governance and Risk committees.

Since leaving government service, he has continued his involvement with public policy by serving as the Executive Director of the MacKay Task Force on the future of the financial services sector of Canada, the Executive Director of the Saucier Task Force on Corporate Governance, the Senior Policy Advisor to the Credit Union Central of Canada on the National Initiative, and the founding Chair of the Market Surveillance Panel for administered electricity markets in Ontario. His most recent assignment was as Chair of the Task Force on Auto Insurance Fraud in Ontario.

Mr. Gorbet has also served as a corporate director of many firms in the private and public sectors. He is currently a Trustee and past Chair of the North American Electric Reliability Corporation.

Mr. Gorbet has a B.A. from York University and a Ph.D. in Economics from Duke University. He was appointed to the Order of Canada in 2000 and was promoted to Officer of the Order of Canada in 2014.

Convocation - Consent Agenda - Motion

39

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Rita Hoff

President, R. Hoff Financial Management Ltd.

Rita Hoff joined the LAWPRO Board of Directors in 1996, bringing with her extensive experience in the investment industry. She was most recently Vice-President and Director, Debt Capital Markets at Canaccord Capital Corporation.

Prior to that, she served as President and Chief Executive Officer of First Canada Securities Corporation, a firm she co-founded.

Ms. Hoff chairs the LAWPRO Investment Committee and serves on the Governance and Risk committees.

Ms. Hoff serves as a Director and Treasurer of her condominium in Mexico. She has previously served as a Director of CAA Central Ontario, Investment Dealers Association of Canada and as Chair of Ontario District Council of the IDA.

Ms. Hoff has a Bachelor of Commerce from the University of Bombay, India.

She is currently pursuing studies in Spanish language and Mexican culture at the University of Guadalajara.

Convocation - Consent Agenda - Motion

40

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Diana C. Miles

Chief Executive Officer

Law Society of Ontario

Diana Miles is the Chief Executive Officer of the Law Society of Ontario. The Law Society licenses, regulates and disciplines Ontario’s more than 52,000 lawyers and 8,700 paralegals pursuant to the Law Society Act and the Law Society’s Rules of Professional Conduct, by-laws, regulations and guidelines.

Diana joined the Law Society in 2001 as the Executive Director of Professional Competence, and has also held positions in the organization including Executive Director, Organizational Strategy, Executive Director of Communications and Executive Director of Professional Regulation. Throughout her career with the Law Society, Diana has been responsible for strategic and operational planning, the creation of defensible and valid licensing and credentialing systems, the development and provision of high quality supports and resources for members of the public and licensees, and the regulation and quality assurance of the conduct, competence and practice management of lawyers and paralegals.

Prior to joining the Law Society, Diana was the Chief Operating Officer of a large Toronto law firm and in that capacity she supported the organization’s business development and client services provision and firm administration.

Diana has extensive governance experience. She is accredited as a Chartered Director and has been a director on a variety of private and not-for-profit boards. Diana was called to the Bar in Ontario in 1990. She is a member of LAWPRO’s Audit Committee.

Convocation - Consent Agenda - Motion

41

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Barbara J. Murchie

Partner, Bennett Jones LLP

Ms. Murchie practises intellectual property litigation at Bennett Jones LLP in Toronto and is a Bencher of the Law Society of Ontario. She is Chair of the Tribunals Committee and is also a member of the Law Society Tribunal, and regularly sits on discipline panels as an adjudicator. She is a member of LAWPRO’s Governance Committee.

Since 1986, when she was called to the bar, she has appeared at all levels of the Ontario and Federal courts on litigation matters that include intellectual property, professional negligence, construction law, municipal liability and general civil litigation. Over the course of her career at small and large firms, she has acted for a broad range of individual, corporate and institutional clients. Since becoming a Bencher, she has become engaged in administrative law, chairing hearing panels and writing decisions on cases involving lawyers who are alleged to have breached their professional obligations.

During her 30 year legal career, Ms. Murchie has held leadership roles with a number of legal organizations including, most recently, the Law Society of Ontario, and between 2002-2005, the Advocates Society where she was a Director. She participates in numerous professional development programs as a teacher and is regional Co-Chair of the long-running, province-wide, Courthouse program for the Advocates Society. She is a member of a wide array of legal associations including the Intellectual Property Institute of Canada, the Ontario Bar Association, the Canadian Bar Association, the Toronto Lawyers Association, and the Women's Law Association of Ontario.

Ms. Murchie's community service includes roles as Director and Chair of Ovarian Cancer Canada and Casey House Foundation.

Convocation - Consent Agenda - Motion

42

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

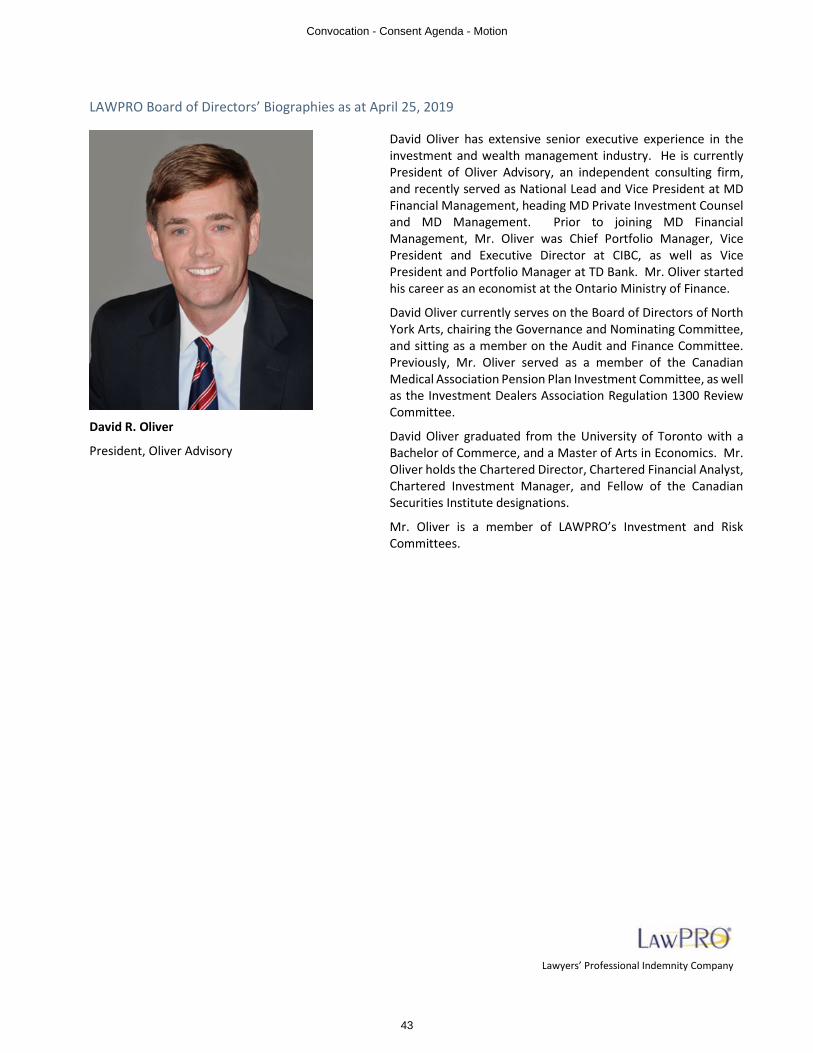

David R. Oliver

President, Oliver Advisory

David Oliver has extensive senior executive experience in the investment and wealth management industry. He is currently President of Oliver Advisory, an independent consulting firm, and recently served as National Lead and Vice President at MD Financial Management, heading MD Private Investment Counsel and MD Management. Prior to joining MD Financial Management, Mr. Oliver was Chief Portfolio Manager, Vice President and Executive Director at CIBC, as well as Vice President and Portfolio Manager at TD Bank. Mr. Oliver started his career as an economist at the Ontario Ministry of Finance.

David Oliver currently serves on the Board of Directors of North York Arts, chairing the Governance and Nominating Committee, and sitting as a member on the Audit and Finance Committee. Previously, Mr. Oliver served as a member of the Canadian Medical Association Pension Plan Investment Committee, as well as the Investment Dealers Association Regulation 1300 Review Committee.

David Oliver graduated from the University of Toronto with a Bachelor of Commerce, and a Master of Arts in Economics. Mr. Oliver holds the Chartered Director, Chartered Financial Analyst, Chartered Investment Manager, and Fellow of the Canadian Securities Institute designations.

Mr. Oliver is a member of LAWPRO’s Investment and Risk Committees.

Convocation - Consent Agenda - Motion

43

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Daniel E. Pinnington

President & Chief Executive Officer, LAWPRO

Daniel E. Pinnington was appointed President & Chief Executive Officer of LAWPRO in 2018. From 2012 to 2018, he served as Vice-President, Claims Prevention and Stakeholder Relations, overseeing LAWPRO's claims prevention and outreach initiatives.

Dan joined LAWPRO in 2001 as Director, practicePRO and was the driving force behind the practicePRO program - LAWPRO’s innovative and internationally recognized claims prevention initiative. He used his unique combination of practice experience and technology expertise to provide lawyers with tools and resources to assist them in avoiding malpractice claims and succeeding in the practice of law.

Before joining LAWPRO, Dan practised for eight years in the Litigation Department of a Niagara-area law firm. Dan was called to the bar in 1993, having graduated with a combined LL.B./J.D. from the University of Windsor and Detroit Mercy College of Law.

Dan is a Fellow of the College of Law Practice Management and is a prolific writer, speaker and blogger on risk management, legal technology and law practice management issues. He has given hundreds of presentations all over North America and has chaired more than a dozen major conferences.

Dan is currently the President of the National Association of Bar-Affiliated Insurance Companies (NABRICO). He is very active in the American Bar Association's Law Practice Division, was Chair of ABA TECHSHOW 2007 and Editor-in-Chief of Law Practice magazine from 2009-2012. He was co-author of The Busy Lawyer's Guide to Success: Essential Tips to Power Your Practice, he has contributed chapters to several other books published by the ABA LPM section. He was a long-standing member of the ABA Legal Professional Liability Standing Committee. Over the years, Dan has also been very active in the Canadian and Ontario Bar Associations in a variety of roles.

Convocation - Consent Agenda - Motion

44

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Andrew N. Smith

President, Natnook Inc.

Andrew N. Smith is a Chartered Financial Analyst (CFA) and Certified Director (ICD.D) with over 45 years of experience in the financial services industry. He is a member of numerous boards, including Pro-Demnity Insurance Company, the Auto Sector Retirees’ Health Care Trust, GE Canada pension investment committee, University of Ottawa pension investment committee and Sun Life Global Investments independent review committee. Mr. Smith was a senior executive with National Trust and in 1985 became a partner and co-owner at James P. Marshall, Inc., an investment consulting firm.

In 2004, he established a personal consulting practice to assist organizations in achieving their financial and investment goals.

A member of the LAWPRO Board of Directors since 2009, Mr. Smith serves on the Executive, Audit, Conduct Review, Investment and Risk committees.

Andrew J. Spurgeon

Partner, Ross & McBride LLP

Andrew is a Partner of Ross & McBride LLP. He received his LLB from Osgoode Hall Law School; his B.A. and M.A. from York University. He has appeared in all levels of Court in Ontario. He frequently speaks at legal education events relating to advocacy, tort, insurance, civil procedure and legal ethics.

Andrew is a past President of the Hamilton Law Association; a former Director of the Advocates Society; and a recipient of the Ontario Trial Lawyers Association's: Distinguished Service Award.

Andrew is an Adjunct Professor of Law at Western University and a Bencher of the Law Society of Ontario.

Convocation - Consent Agenda - Motion

45

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Mark D. Tamminga

Partner, Gowling WLG

Mark Tamminga is a partner in Gowling WLG's Hamilton office. He provides strategic and practical advice in the areas of real estate law and recovery services, with a focus on mortgage remedies and creditors' rights.

He has pioneered the use of practice automation software tools for lawyers, having automated the firm's recovery services practice and having designed, built and implemented a number of additional practice systems in the areas of debt collection, loan placement and civil litigation.

Mark has taken on various management roles in the firm, including acting as managing partner of the Hamilton office from 2008-2012. In his current role as Leader, Innovation Initiatives, Mark is leading the firm's transformational process improvement and project management program.

He is a regular presenter on the subject of automation in legal practice, and has participated in numerous technology conferences in Canada and the United States. He has chaired the American Bar Association's Techshow legal technology conference and co-chaired the College of Law Practice Management's Futures Conference.

John C. Thompson, FCPA FCA

Chartered Accountant, Retired KPMG Partner

John C. Thompson has had a distinguished career with KPMG and its predecessor firms, serving as Managing Partner of the Hamilton, Ottawa and London offices, as well as serving as the Partner-In-Charge of audit services for southwestern Ontario.

He also served on the firm’s Partnership Board and its Management Committee.

While on the Partnership Board, he chaired the partners’ compensation committee. Working with some of KPMG’s largest clients, Mr. Thompson has developed skills in financial reporting, management systems, and business and strategic planning. He has experience in business acquisitions, reorganizations, and private and public financing activities both in Canada and the United States.

He obtained his chartered accountant designation in 1971 and was awarded an FCA in 1991.

Mr. Thompson joined the LAWPRO Board of Directors in 2010 and currently chairs the Conduct Review Committee and is a member of the Audit Committee.

Convocation - Consent Agenda - Motion

46

Lawyers’ Professional Indemnity Company

LAWPRO Board of Directors’ Biographies as at April 25, 2019

Heather L. Zordel

Partner, Gardiner Roberts

Heather is a corporate and securities lawyer with 30 years of experience, including as a partner in private practice and with the Toronto Stock Exchange. Her current practice includes corporate finance for listed and private companies and investment funds, corporate restructurings and regulatory compliance for registrants.

Heather has Board experience with reporting issuer, not-for-profits, crowns and condominium corporations and is currently on the Board and Audit Committee of Toronto Hydro Corporation. Experience with high level committees and in developing public policy, she is also Co-director of Osgoode LL.M. program in Securities Law and adjunct professor and Bencher of the Law Society of Ontario.

Heather holds a Bachelor of Commerce from University of Saskatchewan and LL.B. and LL.M. from Osgoode Hall Law School.

Convocation - Consent Agenda - Motion

47

2

Contents

3 About LAWPRO

4 Vision, Mission, Values

5 LAWPRO Statement on Corporate Social Responsibility

6 Remarks of the Chair

7 Remarks of the President & CEO

8 Management Discussion and Analysis

18 Management Statement on Responsibility for Financial Information

19 Independent Auditor’s Report

21 Appointed Actuary’s Report

22 Statement of Financial Position

23 StatementofProfitorLoss

24 Statement of Comprehensive Income

24 Statement of Changes in Equity

25 Statement of Cash Flows

26 Notes to Financial Statements

64 Board of Directors

65 Management

65 Committees of the Board

66 Corporate Governance

Convocation - Consent Agenda - Motion

49

3

About LAWPRO

Lawyers’ Professional Indemnity Company (LAWPRO®) is licensed to provide professional liability insurance and title insurance in numerous jurisdictions across Canada.

In 2018, LAWPRO provided liability insurance to over 27,300 members of the Law Society of Ontario. We also insured 1,512 law firms (representing over 3,800 lawyers) under our optional Excess Insurance program.

Through our TitlePLUS® operation, LAWPRO also provides comprehensive title insurance to property owners and lenders throughout Canada. LAWPRO’s practicePRO® risk management program assists lawyers in managing their potential exposure to professional liability claims.

Convocation - Consent Agenda - Motion

50

4

Vision, Mission, Values

Our VisionTo be regarded as the preferred insurer in all markets and product lines in which we do business.

Our MissionTo be an innovative provider of insurance products and services that enhance the viability and competitive position of the legal profession.

Our ValuesProfessionalismIndividually and as a team, we hold ourselves to the highest professional standards. We deliver programs and services known for quality and cost-effectiveness, and for being practical, helpful and relevant.

We demand the best of ourselves every day and in everything we do.

InnovationWe foster a climate in which creativity, innovation and change can flourish. We share ideas, skills and knowledge and encourage continual learning.

We value teamwork and collaboration, and the diverse strengths and perspectives of others.

IntegrityWe act with the highest levels of integrity in all of our interactions and decisions. We aim to always be consistent, fair, ethical and accountable.

ServiceWe strive for excellence in customer service. We share our knowledge, experience and expertise with our customers and with each other, so that together we can identify, prevent and solve problems.

We take the time to listen and understand, so we can respond effectively and empathetically to our customers and to each other.

We demonstrate courtesy and genuine respect for all.

LeadershipWe try to make the world a better place, and to that end lend our energy and expertise to many communities.

Convocation - Consent Agenda - Motion

51

5

LAWPRO Statement on Corporate Social Responsibility

LAWPRO’s vision is to be regarded as the preferred insurer in all product lines and markets in which it does business.

Implicit in this vision – and in the values that support our vision – is a commitment to being a responsible, involved and accountable citizen of the many communities in which we hold membership: the employer community, the insurance community, the legal community, and of course the larger community in which we all live.

The LAWPRO Corporate Social Responsibility Statement is informed by this spirit of community and accountability, while acknowledging that we are governed and profoundly shaped by our unique role as the provider of the primary professional liability insurance program for all lawyers in Ontario. Our social responsibility commitment as a corporate body is focused on four principal areas:

Providing a Healthy and Rewarding WorkplaceWe respect and value our employees and the vital role they play in enabling the company to fulfill its mandate. To that end we adopt policies and practices that not only comply with applicable law and fair labour practices, but also respect diversity, promote inclusion and fellowship, cultivate professional growth through education and service, and promote health, safety and wellness, in the workplace and in personal life.

Respecting the EnvironmentWe believe that individually and as a company we have a role to play as stewards of our environment and its resources. To that end we support and promote initiatives in our company that help advance the goal of a sustainable environment.

The company aims to educate LAWPRO employees about the role individuals and organizations can play in protecting and improving the environment. LAWPRO also has spearheaded a company-wide campaign to reduce reliance on paper and related products, and facilitate use of technology in all aspects of the company’s operations. The company actively encourages initiatives such as these that meet a dual mandate of being stewards of the environment and the bar’s resources.

Fostering the Legal CommunityWe view a committed, healthy and diverse bar as essential to the functioning of a democracy and to the protection of individual rights in society.

We have over the years provided financial and in-kind support to organizations that promote and deliver lawyer wellness programs. As well, we make available wellness information and resources electronically at no cost.

We support and sponsor a range of legal-related charitable and non-profit causes that advance the role and reputation of lawyers in our community and by implication, foster access to justice in Canada. We also work to support charitable initiatives which have captured the interest and imagination of the bar and their clients. We promote the enrichment of the bar through our promotion of legal education, both internally and externally, and by fostering the building of relationships within the legal community.

Supporting the Broader Canadian CommunityWe acknowledge that as highly skilled and employed individuals, we are among the fortunate in our community. LAWPRO employees give back by selecting five registered charities annually and partner with the company to fundraise for their benefit. In addition, each LAWPRO employee may request one “charity day” per year to undertake work for the registered charity of the employee’s choice.

We actively contribute to the advancement of the Canadian insurance industry, and engage in a dialogue with government in the interests of the bar and the Canadian consumer.

We promote inclusion by working to expand the range of our materials available in both official languages and by providing materials in other languages based on level of demand.

Convocation - Consent Agenda - Motion

52

6

ANNUAL REPORT

2018Remarks of the Chair Lawyers’ Professional Indemnity Company

LAWPRO navigates a careful balancing act: keeping revenues high enough to cover claims and satisfy regulators that the company is financially healthy while carefully controlling premiums to maintain affordability and properly reflect the cost of risk.

Revenues are a combination of premiums, levies, and investment returns and each of these amounts fluctuate based on variables including the number of lawyers in private practice, the health of the economy, and the volatility of financial markets. As we know, none of these can be perfectly predicted. In addition, claims that are reported today may not be resolved for many years. It is the company’s task to attempt to extrapolate the future cost of those claims without over-estimating that cost or running out of funds when it is time to pay. Management makes educated calculations to ensure it meets the Financial Services Commission of Ontario (FSCO) standards as well as those of the other provincial regulators’ capital requirements.

The details in the financial statements in the following pages demonstrate our attention to maintaining a stable and reliable financial base for our insureds.

How important is the insurance program? The primary errors and omissions policy covers over 27,000 lawyers in Ontario. In 2018, almost 3,000 new claims were reported, a 25 per cent increase over the last decade. And, of all the claims closed in 2018, 86 per cent were closed with a successful defence of our insureds.

Good claims service and financial stability not only protect Ontario lawyers, but also indirectly, the public. I believe the trust given to LAWPRO by the Law Society of Ontario and its members has been well earned by LAWPRO’s consistent performance as seen in this Annual Report.

Susan T. McGrathSusan T. McGrath Chair

Convocation - Consent Agenda - Motion

53

7

ANNUAL REPORT

2018Remarks of the President & CEO Lawyers’ Professional Indemnity Company

My first year as CEO has flown by as it seems like just yesterday that I was writing remarks as the incoming President & CEO for LAWPRO’s 2017 Annual Report. I would like to thank the LAWPRO Board and staff for their support through the year. I believe it was a successful year of transition, for both myself and the company.

LAWPRO’s commitment to excellent service and financial stability are of the utmost importance to the success of the bar and to the well-being of the Ontario public. We remain committed to offering fair coverage at an affordable premium that is in alignment with the risks faced by lawyers.

In addition to offering various premium discounts and special coverages (see a list of them at page 11), we also try to match risk to premiums through transaction levies. In 2018, we became even more granular in our levies by eliminating the transaction levy for family litigation, which sees fewer claims on average, while increasing the civil litigation levy for non-family litigation, which sees a comparatively greater number of claims and higher claims costs.

Thanks to groundwork done with the Law Society of Ontario in 2018, as part of our commitment to access to justice, we added a 75 per cent premium reduction to lawyers working exclusively for Civil Society Organizations to our menu of discounts for 2019. This is an example of how we fine tune the program in response to the changing nature of legal services. We continue to match premiums to risk, as best we can, to spread the costs widely enough to keep the insurance program financially healthy and as fair as possible to all our insureds.

As my first full year as CEO comes to a close, I am looking forward to the future with LAWPRO and the Ontario bar. While we have always been a leader in using technology – an amazing 97 per cent of our insureds e-filed in 2019 – we are exploring how existing and new technologies could better support our corporate goals and core business functions. There will be challenges and opportunities ahead for us all and I look forward to meeting them together.

Daniel E. PinningtonDaniel E. Pinnington President & CEO

Convocation - Consent Agenda - Motion

54

8

ANNUAL REPORT

2018Management Discussion and Analysis Lawyers’ Professional Indemnity Company

The following Management Discussion and Analysis provides a review of the activities, results of operations and financial condition of Lawyers’ Professional Indemnity Company (“LAWPRO” or the “Company”) for the year ended December 31, 2018, in comparison with the year ended December 31, 2017. These comments should be read in conjunction with the corresponding audited financial statements, including the accompanying notes.

Financial Highlights Statement of profit or lossDuring 2018, the Company generated a profit of $16.9 million, an increase in earnings of $16.3 million over 2017, and experienced a comprehensive loss of $0.2 million compared to $0.2 million income during the prior year.

Net premiums earned Premiums earned, net of reinsurance ceded, decreased by $1.0 million to $107.5 million in 2018. Premiums from the mandatory Ontario errors and omissions (“E&O”) insurance program were $0.5 million lower than 2017 results, driven by a drop in real estate transaction levies in the current year. The optional Excess Insurance program remained steady in the year, while TitlePLUS premiums dipped slightly.

Net claims and adjustment expenses Incurred claims and adjustment expenses in 2018, net of reinsurance recoveries, decreased by $25.2 million from 2017. The 2018 results benefitted from a $31.4 million net reduction to the E&O program’s reserves due to favourable development of prior Fund Years’ loss experience, compared to $10.4 million in 2017, as well as $2.2 million of income relating to the effect of the increase in the market interest yields during the year on reserve discounting, compared with a $2.5 million income in 2017. A continued moderation of claims severity sustained over recent fiscal years has been a key driver for the prior year development.

Reinsurance Similar to recent years, the Company purchased two layers of excess-of-loss clash reinsurance coverage, which limits its exposure to one or more large aggregations of multiple claims arising from the same proximate cause. Furthermore, the Company maintained its 10 per cent retention in the optional Excess program, whereas prior to 2011 the program was fully reinsured. The high level of reinsurance significantly mitigates exposure to the Company from claims in this program.

General expenses LAWPRO’s general expenses in 2018 were $1.8 million higher than 2017, though in-line with its annual budget, primarily due to general inflationary pressures on the operating costs utilized in the Company’s day-to-day operations.

Commissions earned The Company earned reinsurance commissions of $1.5 million on premium ceded in respect of its 2018 optional Excess Insurance program, a similar result to 2017. In addition, the Company also earned $0.3 million of profit commissions for favourable claims development on the quota share reinsurance arrangements that it had prior to January 1, 2003, up slightly from $0.1 million in 2017. As claims estimates become more certain with time, there is generally less potential for favourable development on claims relating to older fund years, resulting in a tendency towards lower profit commissions.

Investment income Income generated from investments decreased by $0.8 million to $19.7 million in 2018, a result higher than budget by $1.3 million. Investment income from interest and dividend receipts decreased by $0.3 million to $18.4 million, primarily due to a decrease in the amount the Company invested in fixed income securities during the current year. As a result of the higher market yields during 2018, the Company experienced a $1.1 million decrease in net unrealized gains on its fixed income security portfolio used to match its

Convocation - Consent Agenda - Motion

55

Management Discussion and Analysis Lawyers’ Professional Indemnity Company

9

ANNUAL REPORT

2018

claims liabilities, compared to a decrease of $3.2 million in 2017. The 2018 results also included net capital gains of $7.0 million realized on disposition of investments, compared to $8.2 million in 2017. In addition, during 2018 the Company recognized $3.2 million of unrealized losses as an impairment due to the significant or prolonged decline of some of its equity securities, compared to $1.7 million in 2017.

Statement of comprehensive incomeOther comprehensive lossDuring 2018, LAWPRO experienced other comprehensive loss of $17.1 million, primarily due to a significant decrease in net unrealized losses on its surplus investments in the equity security markets. These results compare to other comprehensive loss of $0.4 million experienced during 2017.

Statement of financial position Overall, the Company ended 2018 in a satisfactory financial position, with shareholder’s equity down by $0.2 million year over year, as the net income achieved during the year was more than offset by the other comprehensive loss experienced during the same period.

Investments As at December 31, 2018, the market value of the Company’s investment portfolio exceeded its cost by $17.6 million, compared to 2017 where the market value exceeded cost by $35.6 million. Investment assets, inclusive of cash and cash equivalents and investment income due and accrued, decreased by $11.4 million to $668.3 million as at December 31, 2018. The decrease was primarily the result of the volatile equity markets more than offsetting the positive cash flow provided by operations and investment receipts generated by the portfolio.

The investment portfolio is managed in accordance with the investment policy approved by the Company’s Board of Directors in diversified, high-quality assets. A portion of the investment portfolio, which is composed of primarily fixed income securities, is invested in a manner that is expected to substantially match in maturity to the payment of claims liabilities in future years. The portion of the Company’s investment portfolio which is considered surplus to the requirements of settling claims liabilities is managed separately and includes fixed income securities and equity investments in publicly traded companies, the values of which are more subject to market volatility.

Provision for unpaid claims and adjustment expenses and reinsurers’ share thereof The provision for unpaid claims represents the amount required to satisfy all of the Company’s obligations to claimants prior to reinsurance recoveries. This balance has decreased by $10.5 million. Reinsurance recoverables have increased by $1.0 million and accordingly the decrease in the net provision is $11.5 million. This decrease is attributable to the fact that the reductions to the claims provision from both the settlement of previously existing claims during 2018, and the net favourable development of prior years’ reserves experienced during the year, more than offset the claims expense relating to the additional risk associated with underwriting the 2018 program.

Report on LAWPRO Operations LAWPRO is an insurance company with three product lines: a mandatory E&O Insurance program, as required by the Law Society for all lawyers in private practice in Ontario; an optional Excess Insurance program that enables Ontario law firms to increase their insurance coverage limit to a maximum of $9 million per claim/$9 million in the aggregate above the $1 million per claim/ $2 million aggregate levels provided by the mandatory E&O program; and, an optional TitlePLUS title insurance product that real estate practitioners across Canada can make available to their clients.

Convocation - Consent Agenda - Motion

56

Management Discussion and Analysis Lawyers’ Professional Indemnity Company

10

ANNUAL REPORT

2018

The mandatory E&O Insurance programIn each of the last two years, the number of lawyers insured under the LAWPRO program has increased by approximately two per cent. In 2018, the Company provided E&O coverage to just over 27,300 lawyers, up from about 26,700 in 2017. The E&O base premium has varied since the Company assumed active responsibility for the Law Society’s insurance operations in 1995 (see Graph 1), depending on the outlook of key factors such as claims costs and investment income. In order to address rising claims trends, the base premium was increased by $400 to $3,350 per lawyer in 2011. For 2012 through 2016, the base premium was held at $3,350 per lawyer – a level selected with a view to the longer-term stability and sustainability of the program. Given LAWPRO’s solid capital level as at December 31, 2016, the Company was well-positioned to lower the base premium to $2,950 for the 2017 program. LAWPRO’s 2018 results have supported the Company’s ability to maintain this rate for the 2019 program.

Graph 1 – Base premium per lawyer