systems thinking and the theory of constraints

DESCRIPTION

Systems Thinking and the Theory of Constraints. The “Job-Shop” Simulation. 4 types of products. Product #1. Product #2. B. Start. B. Start. Finish. Finish. A. D. A. D. C. C. Product #3. Product #4. Finish. B. B. Start. Start. A. D. A. D. C. C. Finish. - PowerPoint PPT PresentationTRANSCRIPT

2008, M.

Srinivasan1

Systems Thinking and the Theory of Constraints

2008, M.

Srinivasan2

The “Job-Shop” Simulation

4 types of products

A

B

C

D A

B

C

D

A

B

C

D A

B

C

D

Product #1 Product #2

Product #3 Product #4

StartStart

Start Start

Finish

Finish

Finish

Finish

2008, M.

Srinivasan3

The “Job-Shop” Simulation

Objective: Produce “kits” of products Each kit requires one job of each type

Number of days given to complete kits: 20 days Scorecard: Teams will be “graded” based on:

No. of kits produced Tie-breaker 1: Max. flow days Tie-breaker 2: Total no. of products produced

2008, M.

Srinivasan4

The “Job-Shop” Simulation: Scorecard

Team 1

Team 2

Team 3

Team 4

Team 5

Team 6

Team 7

Team 8

#Blue

#Pink

#Green

#Brown

# KitsMax Flow Days

No. of Products

2008, M.

Srinivasan5

The “Job-Shop” Simulation

What could we have done better? Manage the bottleneck better, right? How can we do that?

2008, M.

Srinivasan6

Systems Thinking

Integrated decision making “Big Picture” Thinking

Thinking “Globally” rather than “Locally”

Understanding how localized decision making can affect the overall goal

2008, M.

Srinivasan7

The Theory of Constraints

Eli Goldratt, a physicist. OPT: a scheduling package. The Goal and the Theory of Constraints.

TOC provides a way of thinking globally.

Goldratt challenges the conventional approach to managing organizations.

2008, M.

Srinivasan8

Traditional Decision Making

The “Cost World” Perspective

2008, M.

Srinivasan9

Traditional Decision Making

How are investment decisions usually made? Usually based on cost considerations (right)? “The Cost-World” Perspective

Consider how the cost-world perspective affects the push towards parts per million (PPM) quality and “Zero” inventory.

2008, M.

Srinivasan10

The Cost World Perspective: Cost and PPM Quality

ReducingScrap

From To

AnnualCost

Savings

AnnualInvestment

NeededThe CostJudgment

Do It!

Maybe?

Do NOT Do

8% 2%

2% 0.5%

0.5% 0.1%

$60,000$15,000

$4,000

$20,000$20,000

$20,000

2008, M.

Srinivasan11

Is 99.5% Quality Good Enough For You?

Doctors in New York State hospitals drop 1,291 babies per year

Chicago O’Hare International Airport has 4,197 unsafe arrivals / departures per year

Post Offices in New York State lose 9,315 pieces of mail per day

No problem. Everything is OK!

If it is, then you won’t mind if:I’ll do better

next time!

2008, M.

Srinivasan12

The Cost World Perspective: Cost and Inventory Turns

IncreasingInventory

Turns

AnnualCost

Savings*

AnnualInvestment

NeededThe CostJudgment

3 6 $2M $2M6 12 $1M $2M12 24 $0.5M $2M

* Assuming starting inventory of $15M and 25% carrying cost

Do It

Maybe?

Do NOT Do

2008, M.

Srinivasan13

The Real Cost of Inventory

Inventory adversely affects all the factors that give you a competitive edge (namely, Price, Quality, and Delivery). Higher inventory leads to: Longer lead times and poorer delivery performance, Defects not being detected soon enough, Increased costs due to obsolescence, storage costs,

overtime, etc.

2008, M.

Srinivasan14

Traditional Decision Making

Inventory Valuation and Cost Accounting

2008, M.

Srinivasan15

An Inventory Conundrum

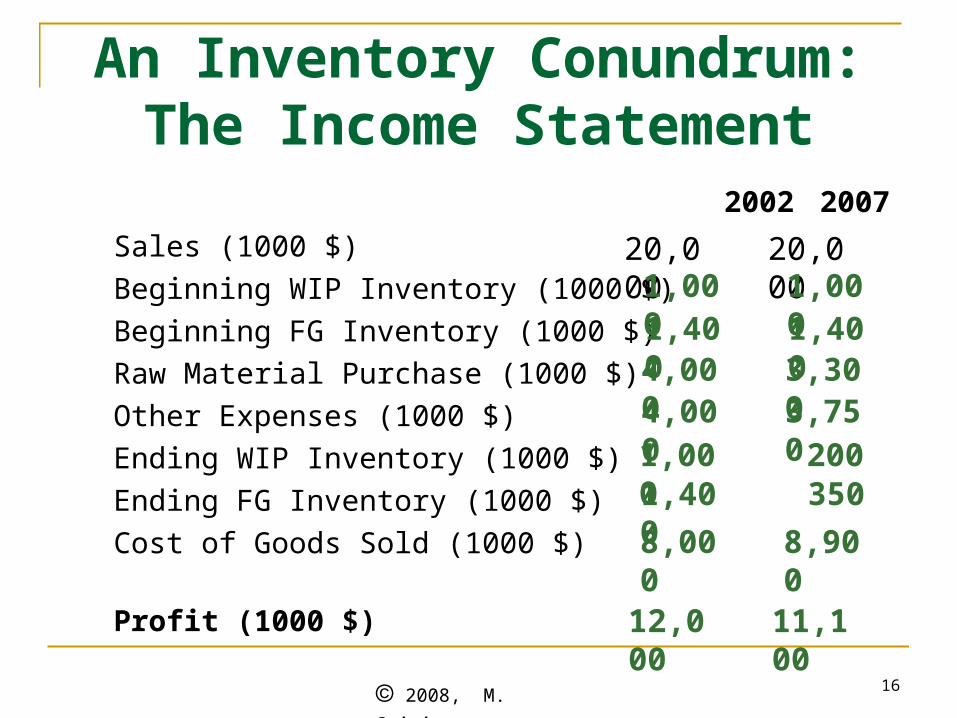

Raw Material cost per unit: $10WIP value per unit: $20Finished Goods value per unit: $35Sale Price per unit: $50

Other Operating Expenses: $4 Million in 2006; $3.75 Million in 2007

2006 2007

Beginning WIP Inventory (1000 units) 50 50

Beginning FG Inventory (1000 units) 40 40

Raw Material (1000 units) 400 330

Sales (1000 units) 400 400

Ending WIP Inventory (1000 units) 50 10

Ending FG Inventory (1000 units) 40 10

2008, M.

Srinivasan16

An Inventory Conundrum: The Income Statement

2002 2007

Sales (1000 $)

Beginning WIP Inventory (1000 $)

Beginning FG Inventory (1000 $)

Raw Material Purchase (1000 $)

Other Expenses (1000 $)

Ending WIP Inventory (1000 $)

Ending FG Inventory (1000 $)

Cost of Goods Sold (1000 $)

Profit (1000 $)

20,000 20,0001,000 1,0001,400 1,4004,000 3,3004,000 3,7501,000 2001,400 350

8,000 8,900

12,000 11,100

2008, M.

Srinivasan17

Traditional Decision Making:Product Costs

How can we calculate a company’s profit?

Net Profit = p Revenuep - c Expensec.

But how do we use this information to, say, decide on launching a new product?

Net Profitp = Revenuep - Expensep, and so,

Net Profit = p Net Profitp

Allocate! If we allocate overhead costs correctly:

2008, M.

Srinivasan18

Obtaining Accurate Product Costs

How do we allocate overhead costs properly so that product costs are accurate? Standard Costing

Activity Based Costing (ABC)

2008, M.

Srinivasan19

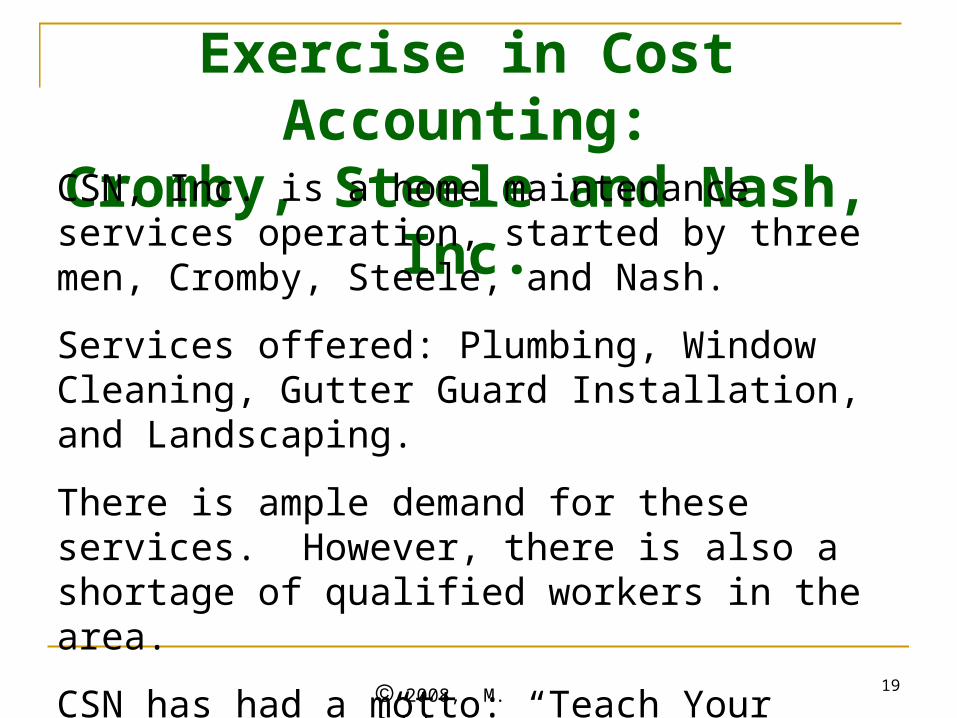

Exercise in Cost Accounting:Cromby, Steele and Nash, Inc.

CSN, Inc. is a home maintenance services operation, started by three men, Cromby, Steele, and Nash.

Services offered: Plumbing, Window Cleaning, Gutter Guard Installation, and Landscaping.

There is ample demand for these services. However, there is also a shortage of qualified workers in the area.

CSN has had a motto: “Teach Your Children Well,” ever since their young-er days. They have employed their children, 5 high-school graduates, to run operations.

2008, M.

Srinivasan20

Monthly wage per employee = $2,000 including benefits

Hours budgeted per employee per month = 200 hours

Monthly capacity with 5 employees = 1,000 hours

Total Direct Labor cost per month = $10,000

Direct labor rate = $10,000/1,000 = $10 per hour

CSN, Inc.: Labor Costs

2008, M.

Srinivasan21

CSN, Inc.: Revenue & Cost DataJob Type Plumbing Window

CleaningGutter Guards

Landscaping

Labor Hours/job 2 hours 4 hours 3 hours 5 hours

Revenue/job $130 $170 $200 $250

Material Cost $30 $10 $70 $75

Labor Cost $20 $40 $30 $50

Current Monthly Output

90 jobs 70 jobs 80 jobs 60 jobs

Note:

Total number of jobs per month = 90 + 70 + 80 + 60 = 300 jobs.

At current output level, capacity used = 90 x 2 + 70 x 4 + 80 x 3 + 60 x 5

= 1,000 hours per month

2008, M.

Srinivasan22

Monthly Administrative Overhead (Salaries) = $18,000.

Monthly Non-Administrative Overhead (Rent, Truck Fleet Maintenance, Marketing, Depreciation) = $9,000.

Overhead is currently allocated to products based on production volume. Current volume is 300 jobs per month.

Administrative Overhead per job $18,000/300 = $60.

Non-Administrative Overhead per job = $9,000/300 = $30.

CSN, Inc.: Overheads

2008, M.

Srinivasan23

CSN, Inc.: Summary Cost TableJob Type Plumbing Window

CleaningGutter Guards

Landscaping

Labor Hours/job 2 hours 4 hours 3 hours 5 hours

Revenue/job $130 $170 $200 $250

Material Cost $30 $10 $70 $75

Labor Cost $20 $40 $30 $50

Administrative Overhead Allocation

$60 $60 $60 $60

Non-Administrative Overhead Allocation

Profit -$10 $30 $10 $35

$30 $30 $30 $30

Current Output 90 jobs 70 jobs 80 jobs 60 jobs

2008, M.

Srinivasan24

CSN is using all its labor capacity, and is absorbing all overheads. So there is no labor variance or overhead absorption variance to worry about.

Therefore, the total profit is:

90 x (-$10) + 70 x $30 + 80 x $10 + 60 x $35 =

$4,100 per month.

Cromby, Steele & Nash, Inc.

2008, M.

Srinivasan25

CSN, Inc.: Activity-Based Costing

CSN, Inc. wants to use a better method to allocate the overheads (using Activity-Based Costing).

To accurately allocate Administrative Overhead, CSN gathers data on the time the administrators, Cromby, Steele and Nash, devote to the four products, each month. The data reveals the following breakdown on the time administration spends on the 4 products:

Plumbing: 30%; Window Cleaning: 35%

Gutter Guards: 20%; Landscaping: 15%

2008, M.

Srinivasan26

Job Type Plumbing Window Cleaning

Gutter Guards

Landscaping

Admin O/H Allocated = %age effort x $18,000

$5,400 $6,300 $3,600

Number of Jobs 90 jobs 70 jobs 80 jobs 60 jobs

Administrative O/H Allocation per job

$60 $90 $45

Percentage Effort 30% 35% 20% 15%

CSN, Inc.: Administrative Overhead Allocation using ABC

$45

$2,700

Administrative Overhead to be allocated = $18,000

2008, M.

Srinivasan27

CSN, Inc.: Non-Administrative Overhead Allocation using ABC

Non-Administrative Overhead to be allocated = $9,000.

The allocation is made based on labor hours.

Total labor hours = 1,000. So,

Non-Admin. O/H rate = $9,000/1,000 = $9.00 per labor hour.

Since Plumbing takes 2 hours, the Non-Admin. Overhead allocated to a Plumbing job is = $9 x 2 = $18.

Thus the Non-Administrative Overhead allocation per job is:

Plumbing (2 hours): $18; W. Cleaning (4 hours): $36

G. Guards (3 hours): $27;Landscaping (5 hours): $45

2008, M.

Srinivasan28

Job Type Plumbing Window Cleaning

Gutter Guards

Landscaping

Labor Hrs./job 2 hours 4 hours 3 hours 5 hours

Revenue/job $130 $170 $200 $250

Material Cost $30 $10 $70 $75

Labor Cost $20 $40 $30 $50

Administrative Overhead Allocation

$60 $90 $45 $45

Non-Administrative Overhead Allocation

CSN, Inc.: Improved Allocation with ABC

Profit $2 -$6 $28 $35

$18 $36 $27 $45

Current Output 90 jobs 70 jobs 80 jobs 60 jobs

2008, M.

Srinivasan29

CSN, Inc., Demand for Services

Suppose the monthly demand for these services is:

Plumbing: 250 jobs

Window cleaning: 160 jobs

Gutter guard installs: 145 jobs

Landscaping: 120 jobs

Suppose, too, that CSN, Inc., can choose which products to go after.

What is the best product offering for CSN, Inc., that will maximize its profit?

2008, M.

Srinivasan30

Cromby, Steele & Nash, Inc.

Can CSN do better? Let’s use ABC cost figures.

Which is the most profitable product?

Compute profits if they first complete meeting the demand for the most profitable product, then focus on the next most profitable product, and so on. Use the following pages for your calculations.

Landscaping

2008, M.

Srinivasan31

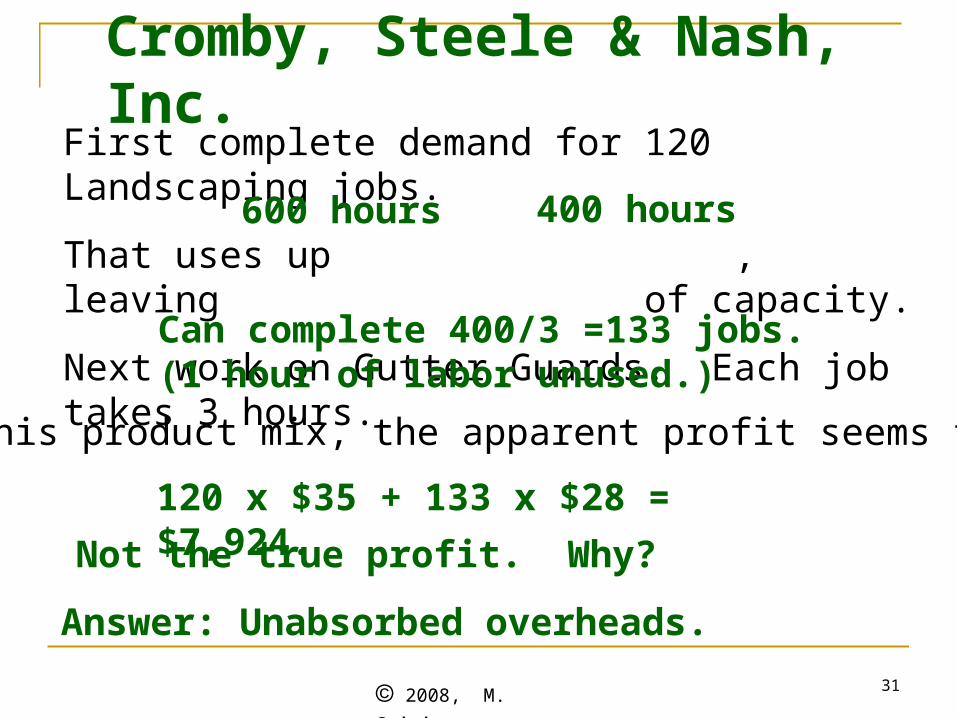

First complete demand for 120 Landscaping jobs.

That uses up , leaving of capacity.

Next work on Gutter Guards. Each job takes 3 hours.

600 hours 400 hours

Can complete 400/3 =133 jobs.(1 hour of labor unused.)

120 x $35 + 133 x $28 = $7,924.

With this product mix, the apparent profit seems to be:

Not the true profit. Why?

Answer: Unabsorbed overheads.

Cromby, Steele & Nash, Inc.

2008, M.

Srinivasan32

CSN, Inc.: Reconciling Variances120 Landscaping and 133 Gutter Guard jobs will each recover $45 of Administrative Overhead, that is:

$45 x 120 + $45 x 133 = $11,385.

Admin. Overhead Variance = $18,000 - $11,385 = $6,615.

So, “optimal” profit is less than earlier profit! Why?

The 1 hour of unused labor gives a Labor Usage Variance of $10 and Non-Admin. Overhead Variance of $9.

So, the total of all the Variances is:

Actual profit with ABC is thus:

$6,634.

$7924 - $6,634 = $1,290.

2008, M.

Srinivasan33

Systems Thinking and the Theory of Constraints

The “Throughput World” Perspective

2008, M.

Srinivasan34

The Theory of Constraints

The Theory of Constraints (TOC) is based on two premises: The Goal of a business is to make more money, … in

the present and in the future.

A system’s constraint(s) determine its output.

2008, M.

Srinivasan35

TOC Performance Measures

Throughput (T): The rate at which the system generates money through sales.

Inventory (I): All the money invested in purchasing things needed by the system to sell its products.

Operating Expenses (OE): All the money the system spends, turning inventory into throughput.

2008, M.

Srinivasan36

The Goal: To Make Money

Bottom Line Measurements

NET PROFIT

RETURN ONINVESTMENT

CASH FLOW(Relative)

(Survival)

(Absolute)

2008, M.

Srinivasan37

Relating TOC Measures to Traditional Measures

Net Profit = T - OE

T = Sales Revenue - Variable Cost (Materials)

OE = Fixed Costs (DL + Overhead)

Asset = Throughput = TTurns “Inventory” I

Return on = Net Profit = T - OE Investment “Inventory” I

2008, M.

Srinivasan38

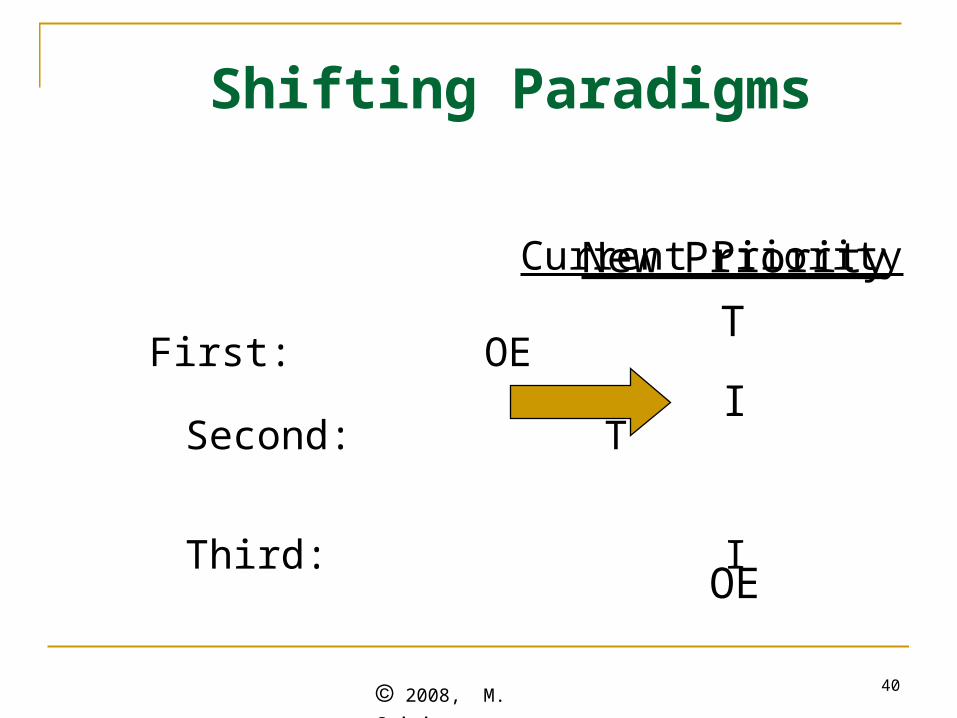

Priorities in Traditional World

First: OE

Second: T

Distant Third: I

2008, M.

Srinivasan39

Where is the Bang for the Buck? (T vs. OE)

$

Revenue 100

RM 40

DL 10

OH 40

Cost 90

NP 10

100 114

1084040

9888

1612

40 48

Leverage fromDecreasing OE

Leverage fromIncreasing T

Assume a) you have 20% excess capacity, and b) sales will increase by 20% if you can effect a 5% price reduction.

0.95(100) = 951.20(95) = 114

2008, M.

Srinivasan40

Shifting Paradigms

Current PriorityFirst: OE

Second: T

Third: I

T

I

OE

New Priority

2008, M.

Srinivasan41

Decisions should promote a growth strategy. While enterprises should try to simultaneously increase throughput, decrease inventory, and decrease operating expenses, the focus must be on improving throughput.

Lean Supply Chain Principle 12:

How to Make Money:The Importance of Throughput

2008, M.

Srinivasan42

CSN, Inc.: A Better Approach

a) Consider only the variable costs in the profit equation – use marginal profits.

b) Focus on the constraint. Evaluate rate at which marginal profits are generated at the constraint (Throughput). Best product is the one with the highest Throughput. Complete demand on this product, move to next most profitable product, and so on, till you run out of capacity at constraint.

c) Find total marginal profit, and subtract out fixed costs to get total net profit.

2008, M.

Srinivasan43

Cromby, Steele & Nash, Inc.

Product Plumbing W. Clean G. Guard Landscape

Demand for product 250 jobs 160 jobs 145 jobs 120 jobs

Marginal Profit (Rev. – Var. Cost)

$130-$30 = $100

$170-$10 = $160

$200-$70 = $130

$250-$75 = $175

# of hours needed per job

2 hours 4 hours 3 hours 5 hours

Profit Generation Rate (Throughput)

$50.00 per hour

$40.00 per hour

$43.33 per hour

$35.00 per hour

Capacity at the constraint (total labor hours) = 1,000 hours.

Fixed costs are: Labor + Administrative O/H + Non-Admin. Overhead

= $10,000 + $18,000 + $9,000 = $37,000.

2008, M.

Srinivasan44

Cromby, Steele & Nash, Inc.

This approach is known as Throughput Accounting

Do 250 plumbing jobs first (250 x 2 = 500 hours).

Next, do 145 gutter guards (145 x 3 = 435 hours).

With the remaining 65 hours, you can complete 65/4 = 16 window cleaning jobs (64 hours)

Net Marginal Profit = 250*$100 + 145*$130 + 16*$160 = $46,410.

Subtract fixed costs ($37,000) for net profit = $9,410.

2008, M.

Srinivasan45

CSN, Inc.: Summary

Summary:Profit with arbitrary product mix: $4,100

“Optimal profit” with ABC: $1,290

Optimal profit with Throughput Accounting: $9,410

2008, M.

Srinivasan46

Systems Thinking and the Theory of Constraints

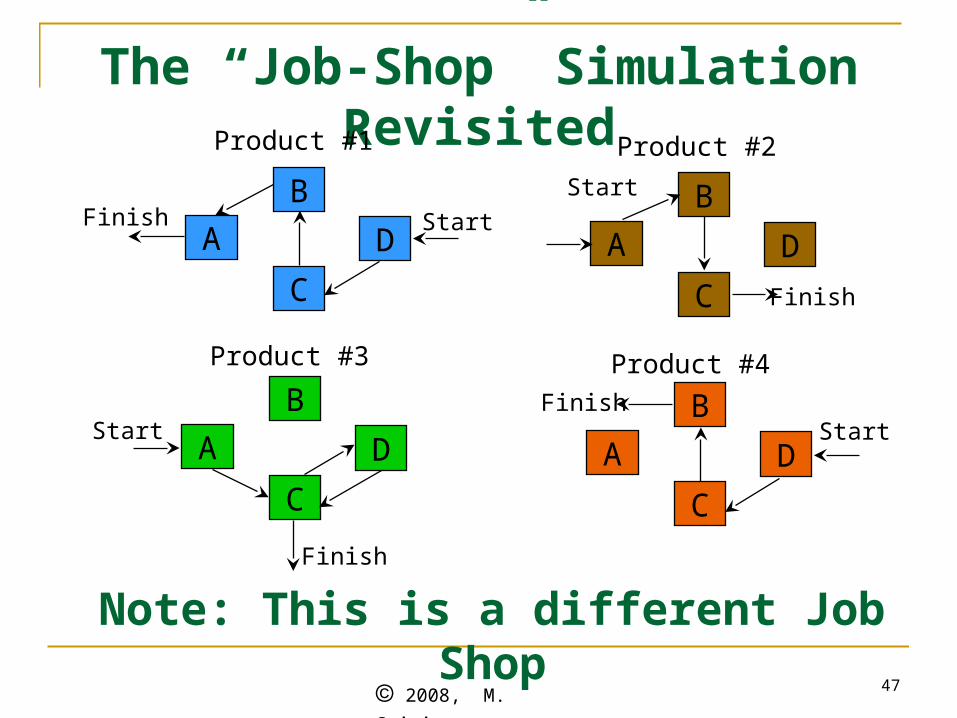

The Job Shop Simulation Revisited

2008, M.

Srinivasan47

The “Job-Shop” Simulation Revisited

A

B

C

D A

B

C

D

A

B

C

D A

B

C

D

Product #1 Product #2

Product #3 Product #4

FinishStart

Start Start

Start

Finish

Finish

Finish

Note: This is a different Job Shop

2008, M.

Srinivasan48

The “Job-Shop” Simulation

• There are 4 operators. Each operator works 20 days a month at a salary of $2,400 per month.

• The wage rate is set at $120 per operator per day.

• Total labor cost is $9,600.

• The overhead cost (salaries, depreciation, utilities, maintenance, etc.) adds up to $33,600 per month.

• Overhead is allocated based on labor cost as follows: $33,600/$9,600 = 350% of direct labor cost.

2008, M.

Srinivasan49

Job Shop Simulation: Product Costs

• Suppose material costs for the 4 products are:

• Labor Cost is $120 per operator per day

• Overheads are charged at 350% of direct labor cost

• Selling price markup is 30% over total cost.

• Which product(s) should the company focus on?

Product 1: $1,500 Product 2 : $2,500

Product 3 : $2,500 Product 4 : $2,000

2008, M.

Srinivasan50

4

3

2

1

Contri-bution

Sales Price

Sales Mark-up (%)

Product Cost = M+L+O

Over-head (O)

Labor

(L)

Matl. Cost (M)

Product

Profit Contribution Calculations for the 4 Products

1500

2500

2500

2000

480

360

480

360

1680

1260

1680

1260

3660

4120

4660

3620

0.30

0.30

0.30

0.30

4758

5356

6058

4706

1098

1236

1398

1086

Which job(s) will make the company the most money?

Rank them

3

2

1

4

2008, M.

Srinivasan51

The “Job-Shop” Simulation: Scorecard

Team 1

Team 2

Team 3

Team 4

Team 5

Team 6

Team 7

Team 8

#Blue#Brown

#Green

#Orange

$ Profit

Max Flow Days

2008, M.

Srinivasan52

The Theory of Constraints

The Five-Step Focusing Process

2008, M.

Srinivasan53

The Throughput World: The Five Step Focusing Process of TOC

Step 1: Identify the System’s Constraint(s) Step 2: Decide how to Exploit the

System’s Constraints Step 3: Subordinate Everything Else to

that Decision Step 4: Elevate the System’s Constraints Step 5: If a Constraint Was Broken in

Previous Steps, Go to Step 1

2008, M.

Srinivasan54

Types of Constraints

Physical Constraints Physical, tangible; easy to recognize as constraint.

Machine capacity, material availability, space availability, etc.

Market Constraints Demand for company’s products and services is less

than capacity of organization, or not in desired proportion.

Policy Constraints Not physical in nature. Includes entire system of

measures and methods and even mindset that governs the strategic and tactical decisions of the company.

2008, M.

Srinivasan55

Policy Constraints

Mindset Constraints A constraint if thought process or culture of the organization

blocks design & implementation of measures & methods required to achieve goals

Measures Constraints A constraint if the measurement system drive behaviors that

are incongruous with organizational goals

Methods Constraints A constraint when procedures and techniques used result in

actions incompatible with goals

2008, M.

Srinivasan56

Example of a Measures Constraint:The Sales Department

A 1% sales commission: 2 products: Cadillacs: $40,000 Beetles: $20,000

Which product will the sales person push?

Suppose the profit margins are Cadillac: $1,500 Beetle: $2,500

Which product will the CEO want you to push?

Conflicting goals (local and global).

2008, M.

Srinivasan57

Effect of Performance Measures

“Tell me how you will measure me and I will tell you how I will behave.”

“If you measure me in an illogical way, … do not complain about illogical behavior.”

2008, M.

Srinivasan58

Effect of Performance Measures

“If you measure me in an unreasonable way, no one knows how I will behave...”.

“Not even me.”

2008, M.

Srinivasan59

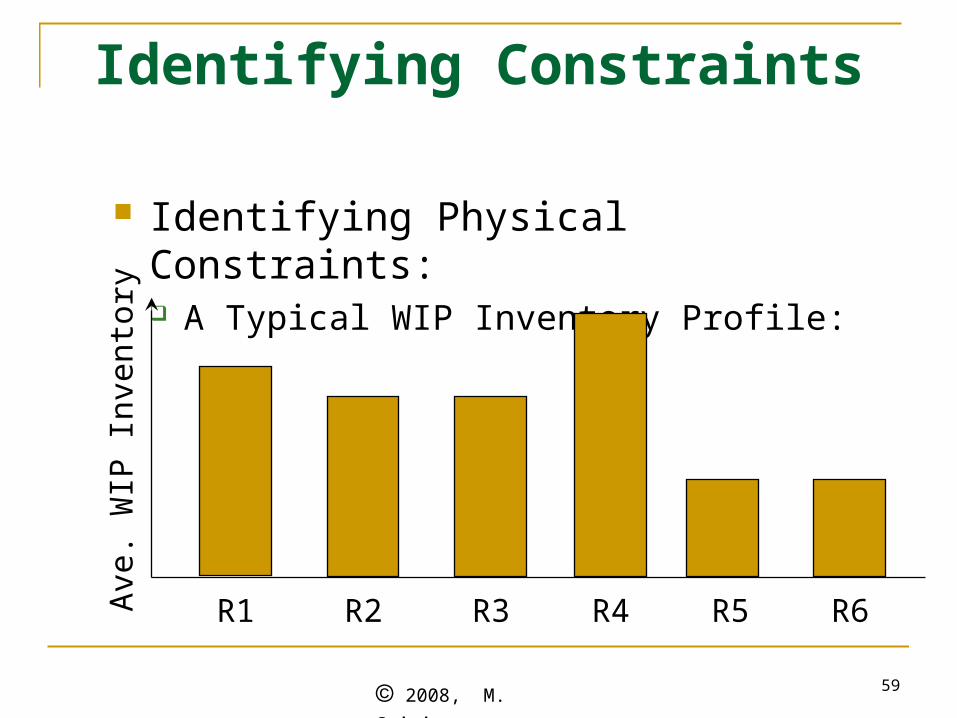

Identifying Constraints

Identifying Physical Constraints: A Typical WIP Inventory Profile:

Ave

. WIP

Inv

ento

ry

R1 R2 R3 R4 R5 R6

2008, M.

Srinivasan60

How can we get the most from Physical Constraints?

Techniques for getting the most from capacity constraints: Eliminate periods of idle time Reduce setup time and run time per unit Improve quality control Purchase additional capacity

Is there anything else we can do?

2008, M.

Srinivasan61

An Example: A Plant Producing 2 Products

Purchased Part$5 / unit

RM1$20 per

unit

RM2$20 per

unit

RM3$20 per

unit

$90 / unit100 units / week

$100 / unit50 units / week

P: Q:

D15 min.

D5 min.

C10 min.

C5 min.

B15 min.

A15 min.

B15 min.

A10 min.

Time available at each work center: 2,400 minutes per weekOperating expenses per week: $6,000

A Production System Manufacturing Two Products, P and Q

2008, M.

Srinivasan62

Can We Meet The Demand?

Perform a Capacity Analysis

Product A B C DP 15 15 15 15

Q 10 30 5 5

Processing Requirements (all times in minutes)

Available time / week on each resource: 2400 min.

2008, M.

Srinivasan63

Can We Meet The Demand?

Resource requirements for 100 P’s and 50 Q’s:

Resource A: 100 x + 50 x = minutes

Resource B: 100 x + 50 x = minutes

Resource C: 100 x + 50 x = minutes

Resource D: 100 x + 50 x = minutes

15 10 2000

15 30 3000

15 5 1750

15 5 1750

2008, M.

Srinivasan64

Any Bottlenecks?

B is a bottleneck.

A, C, & D are not bottlenecks.

We cannot achieve desired levels of production

due to the capacity constraint on B.

What production levels do we set for P & Q?

2008, M.

Srinivasan65

So, is the star and is the “dog.” First we’ll offer the star to the market. If we have residual capacity, we’ll offer the dog! Okay?

The Production Decision Which product has higher profit margin?

Product P: Product Q:

Which product requires less effort? Product P: Product Q:

$45

$60

60 min.

50 min.

Q P

2008, M.

Srinivasan66

What Is The Net Profit?

For 50 units of Q, need 50 x = min. on B, leaving min. on B, for product P.

Each unit of P requires minutes on B. So, we can produce units of P.

If we sell 50 units of Q and units of P, we get 50 x $60 + x $45 = $ per week.

After factoring in operating expense ($6,000), we

30 1500

900

15900/15 = 60

6060 5700

LOSE $300! (Whoops!)

2008, M.

Srinivasan67

Do We Shut The Plant Down?

Is this a “throughput world” perspective? We dealt with “product profits.” Are there

any product profits in the throughput world?

What is the second focusing step? DECIDE HOW TO EXPLOIT THE

CONSTRAINT.

2008, M.

Srinivasan68

Exploiting The Constraint

Each unit of Q brings $ to the company. How many minutes of B for one unit of Q? So, with Q, we receive $ per

constraint minute. Each unit of P brings $ to the company.

How many minutes of B for one unit of P? So, with P, we receive $ per constraint

minute.

60

30

60/30 = $2

45

15

45/15 = $3

2008, M.

Srinivasan69

Throughput World vs. Cost World

The throughput world perspective indicates that we should first focus on producing product .P

The cost world perspective had indicated that we should first focus on producing product .Q

2008, M.

Srinivasan70

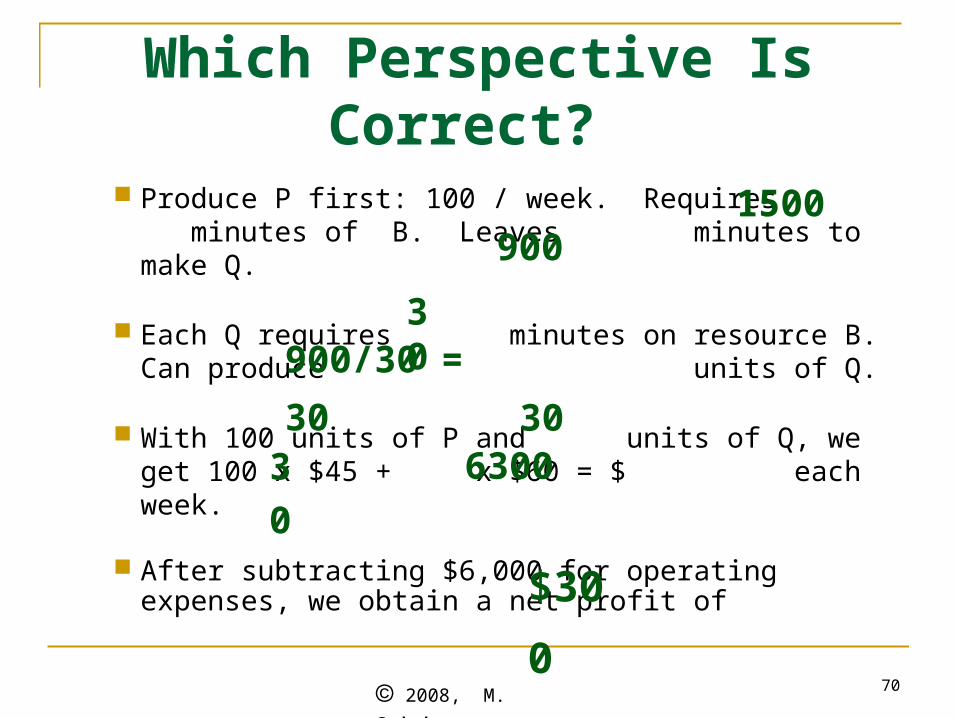

Produce P first: 100 / week. Requires minutes of B. Leaves minutes to make Q.

Each Q requires minutes on resource B. Can produce units of Q.

With 100 units of P and units of Q, we get 100 x $45 + x $60 = $ each week.

After subtracting $6,000 for operating expenses, we obtain a net profit of

1500900

30900/30 = 30

3030 6300

$300

Which Perspective Is Correct?

2008, M.

Srinivasan71

Cost World or Throughput World?

What product will you focus on?

P

But in the long run,“Yes, there are two paths you can go by, …

There’s still time to change the road you’re on.”

2008, M.

Srinivasan72

The “Job-Shop” Simulation

A

B

C

D A

B

C

D

A

B

C

D A

B

C

D

Product #1 Product #2

Product #3 Product #4

FinishStart

Start Start

Start

Finish

Finish

Finish

2008, M.

Srinivasan73

4

3

2

1

Marginal Contribution

Sales Price

Material Cost

Product

Profit Contribution Calculations for the 4 Products

1500

2500

2500

2000

3258

2856

3558

2706

1 (3)

2 (2)

4 (1)

3 (4)

Marginal Contribution / Bottleneck

Days

3258

2856

1779

2706

Revised Ranking

(Old Rank)

# Bottle- Neck Days

Needed

1

1

2

1

4758

5356

6058

4706

2008, M.

Srinivasan74

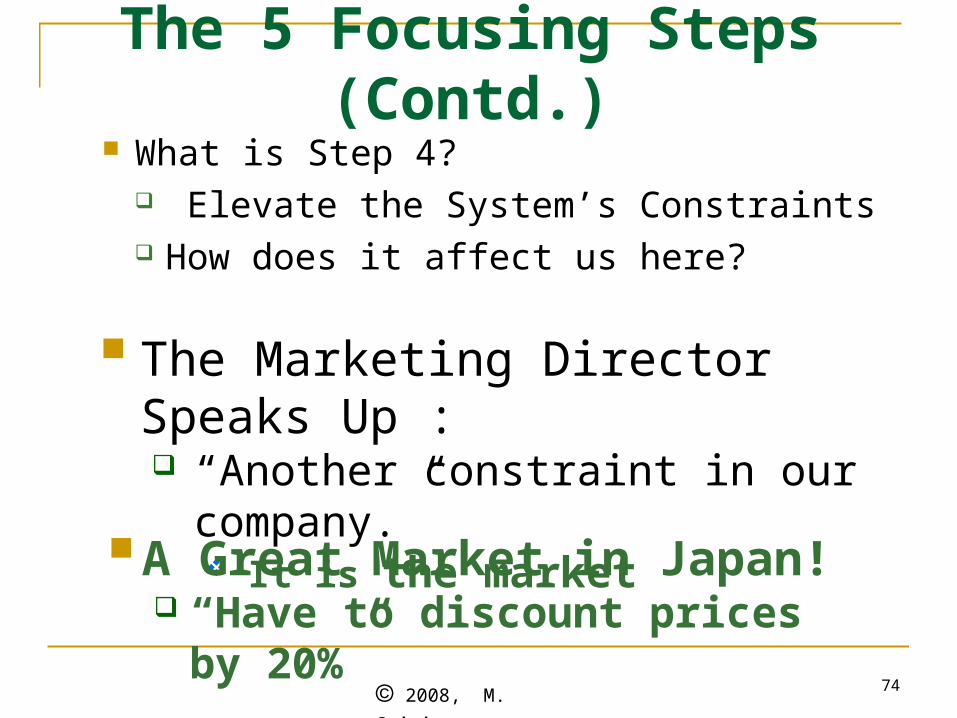

The 5 Focusing Steps (Contd.) What is Step 4?

Elevate the System’s Constraints How does it affect us here?

The Marketing Director Speaks Up : “Another constraint in our company.”

It is the market

A Great Market in Japan! “Have to discount prices by 20%”

2008, M.

Srinivasan75

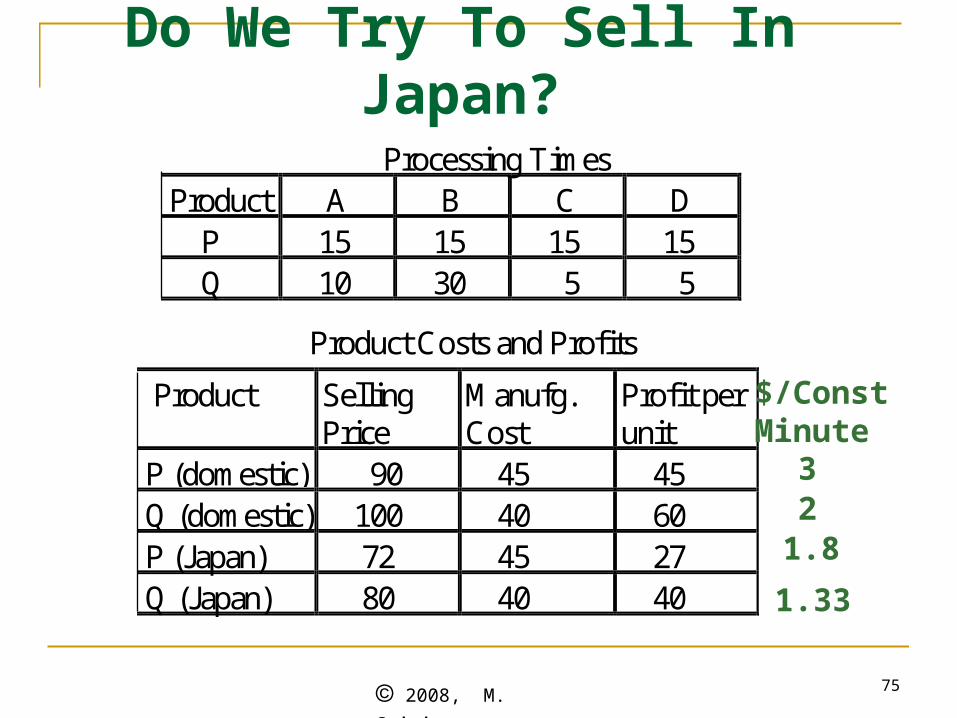

Do We Try To Sell In Japan?

Processing Times Product A B C D P 15 15 15 15 Q 10 30 5 5

Product Costs and Profits

Product SellingPrice

Manufg.Cost

Profit perunit

P (domestic) 90 45 45 Q (domestic) 100 40 60 P (Japan) 72 45 27 Q (Japan) 80 40 40

$/ConstMinute

321.8

1.33

2008, M.

Srinivasan76

Maybe We Should Not Sell in Japan? Right now, we can get at least $ per

constraint minute in the domestic market.2

B

Okay, suppose we do not go to Japan Is there something else we can do?

So, should we go to Japan at all?

Let’s buy another machine! Which one?

How soon do we recover investment?

Cost of the machine = $100,000. Cost of operator: $400 per week.

Perhaps not.

What is weekly operating expense now? $6,400

2008, M.

Srinivasan77

Recovering Our Investment

$3,000(50)

-

$6,400

Plan BProdType

UnitProfit

$/constminute Plan A

$45 3.00 $4,500(100)

$60 2.00 $1,800(30)

$27 1.80 -

$40 1.33 -

OE $6,000

Profit $300

QD

PD

PJ

QJ

6.00

4.00

$4,185(93)

$2,000(50)

$2,785

2008, M.

Srinivasan78

Welcome to the “Paradise Plant!”

2008, M.

Srinivasan79

IF:Clients never change their mind,

Vendors always supply what we ask for, on time,

We do not have any absenteeism,

Our workers are excellently trained,

Our processes are extremely reliable,

Our quality is superb,

Data is readily available and accurate, and

Managing production will be a piece of cake, …

THEN:

You can decide on whatever policies you want.

right?

The Paradise Plant!

2008, M.

Srinivasan80

The Simulator provided you with aparadise plant because all external causeswere eliminated.

Nevertheless,

Was it easy to manage production?

The Paradise Plant!

2008, M.

Srinivasan81

Rethinking Project Management

The Critical Chain

2008, M.

Srinivasan82

Generally a “one-off” type of activity Typically involves completing a set of tasks Tasks typically have long durations that are

also highly variable

Project Management: Characteristics

2008, M.

Srinivasan83

Project Management: Problems Usually Faced

Project is not clearly defined “Known Work” + “Known Unknown Work” + “Unknown Work”

Existing project work is not complete before new projects shift priorities leading to multi-tasking

Problems in a project cascade into another project Constant pressure to increase staff for peak loads A lot of uncertainty involved in estimating task durations

2008, M.

Srinivasan84

First, consider a simple project with 2 tasks performed by 2 different operators:

Managing Projects Under Uncertainty

Task 1 Task 2

If each task takes 15 days on average, what is average project completion time? 30 days

Assume task durations are uniformly distributed (5,25)

5 25

2008, M.

Srinivasan85

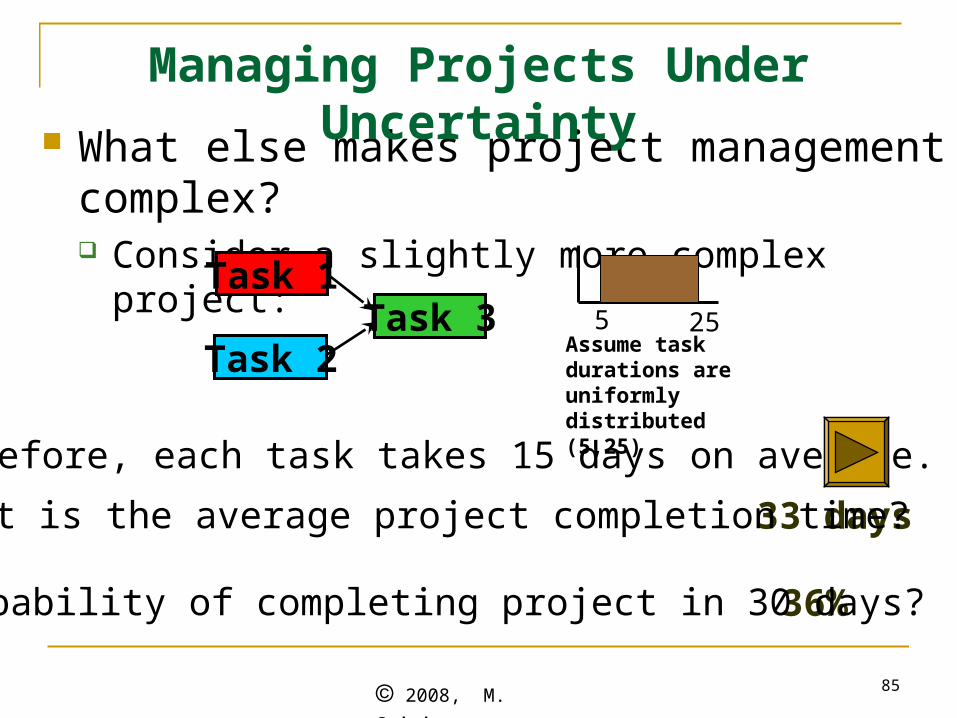

What else makes project management complex? Consider a slightly more complex project:

Task 1

Task 2Task 3

As before, each task takes 15 days on average.

36%Probability of completing project in 30 days?

33 days

5 25Assume task durations are uniformly distributed (5,25)

What is the average project completion time?

Managing Projects Under Uncertainty

2008, M.

Srinivasan86

The affect of resource interdependencies on a simple project:

Task 1

Task 2

Task 3

Task 4Task 5

If each task takes 15 days on average, what is theprobability that the project finishes in 45 days?

Srini; Here we get about 35% slide 86

< 25%

5 25

Managing Projects

2008, M.

Srinivasan87

Conclusion: A project’s most likely completion time is much larger than the sum of the averages of the tasks making up it’s longest path (due to synchronization or due to task dependencies)

So, how do we quote estimated completion time of the project? Do people give a number that they know has

a high (50% or more) chance of missing?

Determining Task Durations

2008, M.

Srinivasan88

Determining Task and Project Durations – the Traditional Way

So, the average task times are “padded” to accommodate any possible delays. Instead of specifying a 50% time estimate (which fails half the time), a 98% confidence estimate is developed for the tasks and project duration.

The project is now estimated to take 70 days, not 45.

What is the chance the project will complete in 70 days?

98% of [5,25] = 5+.98*20 = 5+19.6 = 24.6

5 25

Task 1

Task 2

Task 3

Task 4Task 5

2008, M.

Srinivasan89

A network is drawn up, representing tasks, and precedence relationships between tasks

The task durations are buffered to accommodate uncertainty surrounding the tasks.

Milestones (due dates) are developed for each task.

The Critical Path is determined.

The padded project duration (with safety buffers) is conveyed to the customer and to supervisors

The project is monitored. So, why is it very unlikely that the project will complete on time?

Project Management - The Traditional Way

2008, M.

Srinivasan90

Project Management The TOC Way

The Genesis of the Critical Chain

2008, M.

Srinivasan91

Theory of Constraints and the Critical Chain

Eli Goldratt, a physicist. The Goal (1982, 3rd edition published 2004) The Critical Chain (1997)

Goldratt challenges the conventional approach to managing organizations.

TOC tools for Production: Drum-Buffer-Rope Project Management: Critical Chain

2008, M.

Srinivasan92

The Critical Chain implementation begins with 3 questions:

What to change?

What to change to?

How to cause the change?

Managing the Critical Chain

2008, M.

Srinivasan93

Erroneous assumptions:

It is good to induct work as soon as possible

Protecting task times with buffers will improve on-time performance (this is a biggie)

Multitasking is beneficial

Providing milestones for each task is good

…

What to Change?

2008, M.

Srinivasan94

Parkinson’s Law: “Work expands to fill the time available.” People tend to continue working on a task that could have been completed earlier if they are given a pre-specified completion time.

The Continue to Polish syndrome (aka: the 3-Minute Egg Rule): “It’s not quality if it’s finished before time is up.”

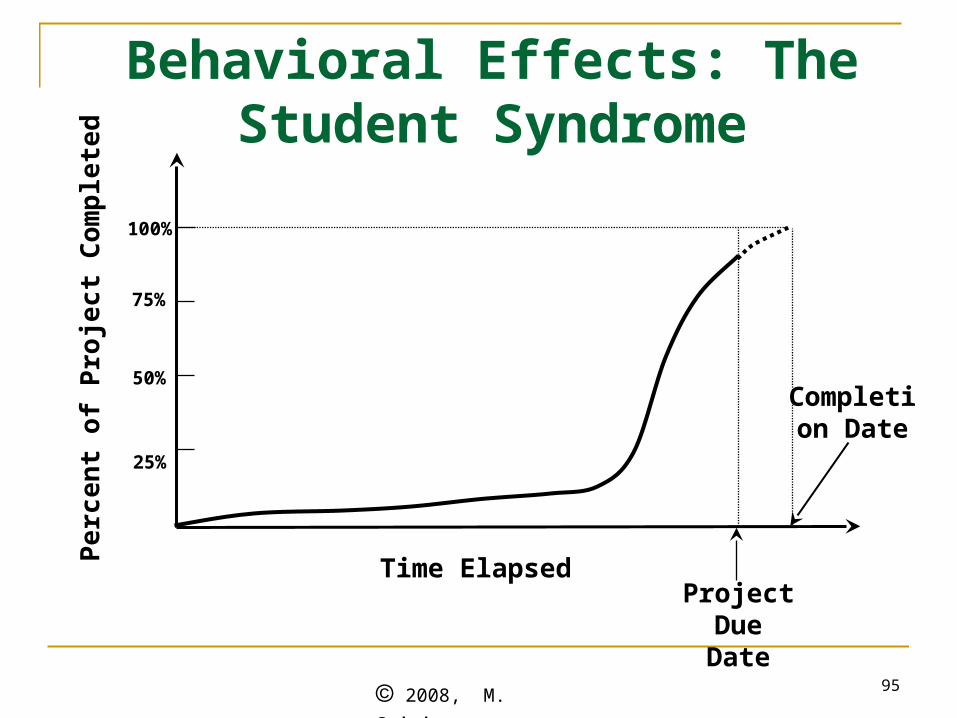

The Student Syndrome: When people feel there is plenty of time to complete a task, other things become important and they procrastinate on the task.

What to Change: Behavioral Effects

2008, M.

Srinivasan95

Behavioral Effects: The Student Syndrome

Time ElapsedProject

Due Date

Per

cen

t of

Pro

ject

Com

ple

ted

25%

50%

75%

100%

Completion Date

2008, M.

Srinivasan96

People do not want to hurt their future negotiating power by finishing too soon.

There is a sense of urgency, promoting a tendency to induct work as soon as possible.

More Behavioral Effects that Increase Task and Project Durations

2008, M.

Srinivasan97

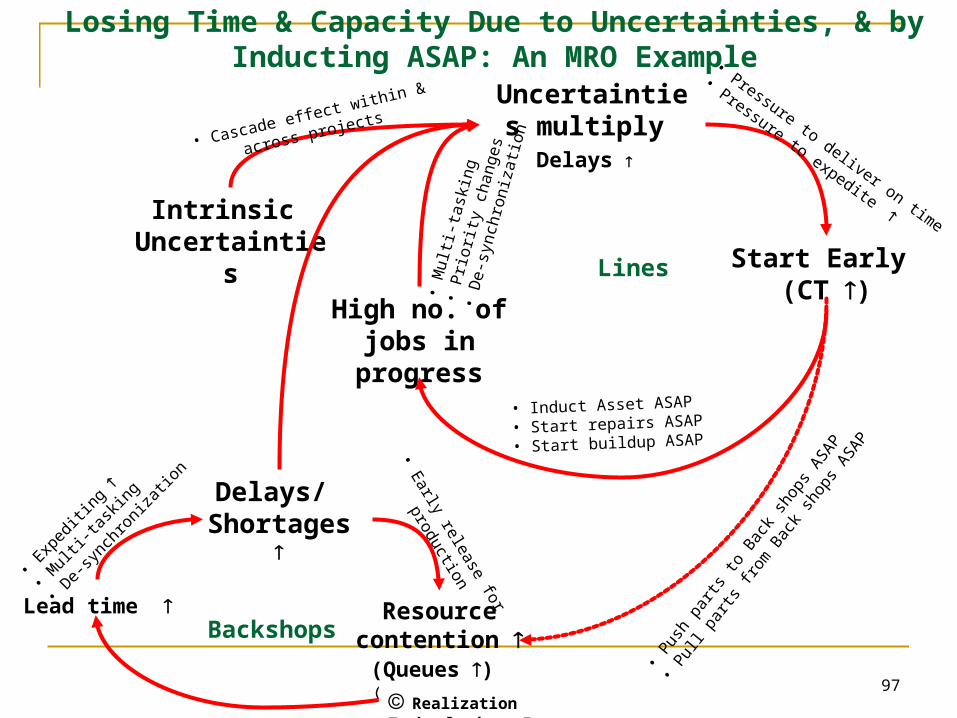

Losing Time & Capacity Due to Uncertainties, & by Inducting ASAP: An MRO Example

Resource contention

(Queues )

Lead time

Delays/ Shortages

Backshops

Start Early (CT )

High no. ofjobs in progress

Uncertainties multiply Delays

• Induct Asset ASAP

• Start repairs ASAP

• Start buildup ASAP

Lines

Intrinsic Uncertainties

•Pressure to deliver on time

•Pressure to expedite

• Cascade effect within &

across projects

•M

ulti-

task

ing

•P

riorit

y ch

ange

s•

De-

sync

hron

izat

ion

•Pus

h pa

rts to

Bac

k sh

ops

ASAP

•Pul

l par

ts fr

om B

ack

shop

s ASAP

•Exp

editin

g

•M

ulti-t

askin

g

•De-

sync

hron

izatio

n •E

arly release for

production

Realization Technologies, Inc.

2008, M.

Srinivasan98

Summary: Sources of Project Delays

A. Synchronization Delays Integration (assembly) points Resources and tasks

B. Delays due to Behavioral Effects Parkinson’s Law “Student” Syndrome “Continue to Polish” Syndrome

C. Queuing Delays Induct work ahead of schedule Multitasking

Realization Technologies, Inc.

2008, M.

Srinivasan99

The Affect of Multitasking

3 Tasks, A, B, C, each of duration 6 days, that have to be executed by one resource. How should you schedule these tasks?

A2 B2 C2 A2 B2 C2 A2 B2 C2

A6 B6 C6

Lead Time for Task A?

Lead Time for Task A?

2008, M.

Srinivasan100

Project Planning (aka Network Building): A meeting of project stakeholders for clarity on intended objectives and success criteria (how to deliver on the order winners)

Identify resource dependencies

Capture time estimates – and build the right safety net – determine “Aggressive But Possible” times

What to Change to?

2008, M.

Srinivasan101

Identify the longest path of dependent events. This is the Critical Chain

Put in place Project Buffer and Feeding Buffers

Avoid displaying milestones (EST, EFT, LST, LFT).

Rather, emphasize the “Relay Runner” work ethic (this is a biggie).

What to Change To?

2008, M.

Srinivasan102

What to Change to?

The Rules of the Critical Chain:

1. Do not schedule Project tasks/ resources precisely at planning time.

2. Pipelining: Do not start projects ASAP.

3. Allow explicit buffer time in projects.

Realization Technologies, Inc.

2008, M.

Srinivasan103

Rationale: Project Buffers are more efficient than safeties within each task

1. Critical Chain Buffering: Aggressive plans without precise resource schedules

• Determine “Aggressive but Possible” times for each activity – remove the padding within each task.

• Determine the critical chain of tasks with these times.

• Provide a project buffer to protect the critical chain.

Traditional Approach:

Critical ChainApproach:

Realization Technologies, Inc.

2008, M.

Srinivasan104

• Most heavily loaded shared resource (constraint), determines throughput

• Project starts are based on constraint’s capacity,

• Pressure to multitask also comes down

Most heavily loaded

resource

Pipelining

Pipelining is more efficient than starting projects ASAP

2. Pipelining: Release Projects Based on Constraints Instead of Starting ASAP

Realization Technologies, Inc.

2008, M.

Srinivasan105

3. Buffer Management: Allocate Resources to Tasks Based on “Buffer Burn Rate”

Realization Technologies, Inc.

Buffer

50% work completed 60% buffer consumed

Chain 2

Burn Rate: % of buffer consumed vs. % of work completed. Automatically calculated on an ongoing basis to assess how much buffer is still available for future uncertainties.

Task Priorities: Tasks that lie on chains with less safety remaining are given top priority. This ensures that buffers are not wasted, and also reduces pressure to multitask.

Buffer

33% work completed 20% buffer consumed

Chain 1

2008, M.

Srinivasan106

Secure agreement on problem to be solved and agreement on direction of solution

Verify that proposed solution will deliver desired results. Ensure that all negative side effects are identified and prevented from happening

Identify all significant potential obstacles that could block implementation of solution

Ensure that necessary leadership is committed to making implementation successful – the RIGHT METRICS

How to Cause the Change?

2008, M.

Srinivasan107

MRO Setting: WR-ALC, NavAir – Cherry Point, MCLB – Albany, Israeli Air Force

Software: Lucent, Microsoft, Intel

Production Supply: Boeing, Lockheed Martin, Larsen & Toubro, Tata Iron & Steel

Testing: AFOTEC, AFFTC (C-17, F-15)

Product Development: Seagate, Harris, BAE Systems

The Critical Chain: Does It Work?