sustaining world economic recovery pythe file copy jean …

TRANSCRIPT

SWP737

Sustaining World Economic Recovery

laE C O pyThe Challenges Ahead

FILE COPY Jean BanethEnzo Grilli

WORLD BANK STAFF WORKING PAPERSNumber 737

4FILE COPY

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

WORLD BANK STAFF WORKING PAPERS ,W7Number 737

Sustaining World Economic Recovery

The Challenges Ahead

Jean BanethEnzo Grilli

The World BankWashington, D.C., U.S.A.

Copyright (C 1985The International Bank for Reconstructionand Development/THE WORLD BANK

1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing May 1985

This is a working document published informally by the World Bank. To present theresults of research with the least possible delay, the typescript has not been preparedin accordance with the procedures appropriate to formal printed texts, and the WorldBank accepts no responsibility for errors. The publication is supplied at a token chargeto defray part of the cost of manufacture and distribution.

The World Bank does not accept responsibility for the views expressed herein, whichare those of the authors and should not be attributed to the World Bank or to itsaffiliated organizations. The findings, interpretations, and conclusions are the resultsof research supported by the Bank; they do not necessarily represent official policy ofthe Bank. The designations employed, the presentation of material, and any maps usedin this document are solely for the convenience of the reader and do not imply theexpression of any opinion whatsoever on the part of the World Bank or its affiliatesconcerning the legal status of any country. territory, city, area, or of its authorities, orconcerning the delimitation of its boundaries, or national affiliation.

The most recent World Bank publications are described in the annual spring and falllists; the continuing research program is described in the annual Abstracts of CurrentStudies. The latest edition of each is available free of charge from the Publications SalesUnit, Department T, The World Bank, 1818 H Street, N.W., Washington, D.C. 20433,U.S.A., or from the European Office of the Bank, 66 avenue d'lena, 75116 Paris, France.

Jean Baneth is director of the Economic Analysis and Projections Department of theWorld Bank; Enzo Grilli is an assistant director.

Library of Congress Cataloging in Publication Data

Baneth, Jean, 1936-Sustaining world economic recovery.

(World Bank staff working papers ; no. 737)1. Developing countries--Economic conditions.

2. International economic relations. 3. Economichistory--1971- . I. Grilli, Enzo R. II. Title.III. Series.HC59.7.B327 1985 338.9'009172'4 85-9529ISBN 0-8213-0546-8

ABSTRACT

The paper analyzes the characteristics of the 1983-84 world economic

recovery and its effects on developing countries adjustment. It looks at the

conditions for medium-term non-inflationary growth in the world economy and at

the changes in policies necessary to cope with and redress over, time the real

and financial imbalances that threaten the sustainability of the current

recovery. It presents a scenario for medium-term growth, resulting from

moderate policy changes in industrial countr-ies, within which-the room for

growth and continued policy adjustment in developing countries is' examined in

some detail. The risks of failure inherent in a continuation -of present

policy trends are also examined.

ACKNOWLEDGEMENTS

This paper draws extensively on work done in the Global Analysis &

Projections Division of EPD. In addition, Messrs. Peter Miovic, Christian

Moran, Paul Armington, Denis Richard and Charles Larkum contributed in various

ways to the preparation of this paper. Their help is gratefully acknowledged.

RESUME

Cette note analyse les characteristiques de la reprise

economique mondiale en 1983-84, et ses effets sur l'ajustement des

pays en developpement. Elle examine les conditions d'une croissance

a moyen terme dans la stabilite des prix, et les modifications qu'il

faut apporter aux politiques economiques afin de corriger les

desequilibres, financiers et reels, qui risquent de compromettre la

poursuite de la reprise actuelle. Elle presente un scenario de

croissance a moyen terme qui serait le resultat d'adaptations modestes

des politiques economiques des pays industriels, et elle examine

l'impact de ce scenario sur la croissance economique des pays en

developpement, et sur leur capacite a mener a bien des politiques

d'ajustement. Finalement, la note examine aussi les risques que

presenterait une continuation des politiques actuelles.

REMERCIEMENTS

Cette note est en grande partie basee sur le travail de la

Division d'Analyse et Projections Globales du Departement d'Analyses

et de Projections Economiques. De plus, Messieurs Peter Miovic,

Christian Moran, Paul Armington, Denis Richard et Charles Larkum ont

beaucoup contribue a sa preparation. Les remercient vivement de leur

aide.

RESUMEN

El trabajo analiza las caracterfsticas de la recuperacio'n

economica mundial de los anios 1983-84 y sus efectos en el ajuste de los

pafses en vias de desarrollo. Describe las condiciones para un

crecimiento no-inflacionario a mediano plazo en la economfa mundial, y

los cambios en las polfticas necesarios para enfrentar y revertir los

desequilibrios reales y financieros que amenazan el sostenimiento de la

recuperaci6n actual. Presenta un escenario a mediano plazo que supone

un ajuste moderado en las polfticas econo'micas de los palses

industrializados, y que sirve para examinar en detalle las posibilidades

de crecimiento y ajuste en las poifticas de los pafses en desarollo.

Los riesgos inherentes a una continuacion de las polfticas econo'micas

actuales son tambien examinados.

AGREDECIMIENTOS

Este estudio descansa en gran parte en el trabajo efectuado en

la Division de Analisis Global y Proyeciones del Banco Mundial. Los

seniores Peter Miovic, Cristian Moran, Paul Armington, Denis Richard y

Charles Larkum contribuyeron en variadas formar a la preparacio'n de este

trabajo. Agradezco enormemente la colaboracion que ellos prestaron.

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ............................................ ix

I. INTRODUCTION ................................................. 1

II. THE ENVIRONMENT FOR THE DEVELOPING COUNTRIES: ECONOMICRECOVERY IN THE INDUSTRIAL COUNTRIES, 1983-84 .............. 3

III. FINANCIAL ADJUSTMENT IN DEVELOPING COUNTRIES: 1982-84 ... ..... 11

IV. THE CHALLENGES AHEAD: TRANSITION TOWARDS SUSTAINABLE LONG-TERM GROWTH ................................................ 28

V. MEDIUM TERM ALTERNATIVES FOR INDUSTRIAL AND DEVELOPINGCOUNTRIES ........ 34

A. A Medium-Term Scenario with Moderate PolicyAdjustments: 1985-90 ............................ 36

A.1. The Industrial Countries .... .......... 36A.2. The Developing Countries .... .......... 43

B. The Risks of Non-Adjustment and the Effects onDeveloping Countries ............................. 55

SUMMARY AND CONCLUSIONS

i. The world economy is now in a revival phase. In 1981-82 it suffered

its deepest and most widespread recession in half a century, and in 1982-83

the debt servicing problems of many developing countries imposed strains on

the international financial system that at times threatened it with breakdown.

ii. Real output increased by 2.6 percent in 1983 and by an estimated 4.2

percent in 1984. World trade has also recovered strongly. After declining in

both volume and value terms in 1982 and showing only a modest volume increase

in 1983, world exports are estimated to have grown by between 8 and 9 percent

in 1984. Despite the pace of this recovery, inflation in the industrialized

countries has continued to moderate. In 1984, expressed in terms of the GDP

deflator, it fell to its lowest level since the late 1960s, and a further

modest improvement is anticipated for 1985.

iii. This performance shows important gains from the policy changes

adopted by industrialized countries in response to the 1979-80 oil price

shock, when aggregate demand was adjusted downwards (in contrast to the demand

supporting policies widely pursued after the 1973-74 oil shock) and monetary

policies were tightened. It has also provided a vital respite for debtor

countries facing the need both to allocate a higher proportion of foreign

exchange earnings to debt service and to shift resources within their

economies to more productive sectors. The recovery in world trade, strongly

fuelled by US import demand, has encouraged exports, enabling adjustment--

- ix -

especially for the major Latin American debtor countries--to be undertaken in

an environment of positive economic growth. Internal policies, however, were

critical to the progress made by developing countries in financial adjustment

during the 1982-84 period.

iv. Progress in recovering from the economic and financial difficulties

of the years immediately following the second oil shock has thus been

tangible. Important imbalances and disequilibrium persist, however. This is

true of the progress in adjustment made by different groups of debtor

countries and of the economic stances of the developed countries. It is also

true of real interest rates, exchange rates, and, very importantly, of

attitudes towards trade and the reviving tendency of protectionism. Given the

scale of the problems that developed in the 1970s--quantitatively reflected in

such variables as the size of developing countries' debts and their debt

ratios, and the current account imbalances of key industrial countries--these

disequilibria will need to be addressed and progressively corrected over a

period of years for real stability to return as an inherent property of the

world economy.

v. For both developed and developing economies the necessary changes

will be more easily effected against a background of steady, reliable and

strong overall output growth. Indeed, without such a background it is

questionable whether rigidities in the developed economies could be

successfully removed, and whether--in circumstances of continuing high real

interest rates and uncertain access to export markets--developing countries

could maintain the momentum of adjustment needed to sustain creditor

confidence and, avoid a recurrence of widespread financial disruption. For

both groups of countries a failure of growth would involve high, social and

political, as well.-as economic, costs.

vi. This paper examines the issues involved in moving from the present

recovery phase in the economic cycle to a sustainable level of world output

growth adequate to permit a workable resolution of the problem of present debt

levels carried by the developing countries.

vii. Three factors precipitated the debt and-payments crisis-of the early

1980s: the deterioration in the debtors terms of trade, the sharp rise in

interest rates, and the weakness in export demand that resulted from recession

in the- industrialized countries. These undermined the basis on "which the

rapid growth of lending had previously been undertaken--namely, the relative

stability of debtor countries debt servicing ratios through the 1970s--and

precipitated a sudden loss of confidence by creditors.

viii. Underlying these visible causes were other, more fundamental

factors. Borrowing had been used by many countries to sustain policies that

delayed necessary adjustment and allocated investment inefficiently. Exchange

rates were -left to go out of balance reducing price competitiveness in export

markets that had become less assured because of growing -trade protectionism.,

ix. Both for internal and external reasons, therefore, all debtor

countries faced the need to reduce domestic consumption relative to output and

to achieve a new balance of resource allocation in their economies through

appropriate policy change. As the paper shows, the need for adjustment, in

nature and scale, was different in different groups of countries, and

structural flexibilities and policy capabilities were also different across

countries. Some countries, by timely action and as a result of long-

established patterns in the orientation of their economies, avoided the need

to reschedule their debts, thereby retaining some flexibility in their access

to external finance. Others responded early and vigorously and have achieved

substantial progress in adjusting their external payments position. Others

have scarcely begun the process. While still others, mainly among sub-Saharan

African countries, appear to have little prospect of restoring growth through

adjustment without considerable further financial assistance on concessional

terms.

x. Even among those major debtors, however, whose progress in improving

their payments position has been of vital importance in reducing financial

tensions, the balance and durability of adjustment so far achieved leave room

for uncertainties. Investment has borne the brunt of domestic demand

compression, falling by 40 percent between 1981 and 1983 in the four major

Latin American oil importing debtor countries. While the tempo of domestic

policy reform needs to be maintained and, for many debtor countries,

quickened, the emphasis must shift towards patterns sustainable in the longer-

term.

xi. The external environment in which this shift is undertaken is likely

to be crucial to its outcome. In this regard the role of economic policies in

the developed and developing economies is both critical and clear. Industrial

countries policies will largely determine the level of real interest rates,

the freedom of world trade movements and, through the aggregate current

account position maintained by the developed countries, the levels of

financing available to the developing countries. Developing countries

policies will determine to a significant extent where better external

conditions are translated into domestic growth.

xii. The paper focuses on the changes in policies that industrialized

countries will need to implement over the period 1985-90 in order to establish

the basis for sustainable growth in the world economy after 1990 and on the

scope that this will leave to developing countries trade, finance and

growth. The necessary adjustments to policy are moderate and should be

implemented gradually, but they cannot be long delayed. A key component is a

change in the current fiscal stance of the United States and a corresponding

realignment of US monetary policy, together with a sympathetic untightening of

monetary conditions in Europe and a reduction of the degree of restrictiveness

of fiscal policies in those countries where room for manouver exists from the

standpoint of inflation. Japan also falls in this category of countries.

xiii. The remainder of this decade could be either a period of transition

to renewed worldwide economic growth in a reasonably stable price environment,

or one of disorder and decline. This sombre scenario is easy to imagine.

Continued budget deficits in the United States at the level now assumed by the

Congressional Budget Office in case no policy is initiated to contain them,

would feed a continued and growing current account deficit. This would become

increasingly difficult to finance, putting upward pressure on interest

rates. In such an environment, a growing trade deficit in the U.S. and

continued slow growth in Europe would feed pressures which would easily lead

to increased trade protectionism. Growth in the industrial countries would

falter and reach an average of only 2.5 percent for the rest of the decade.

Exports of the developing countries would suffer both from a slow growth of

overall demand and protectionism, and would grow only at a rate of perhaps 3

percent. Overall GNP growth in developing countries would amount to only

about 4 percent; only about 3 percent excluding India and China whose relative

inward orientation and low debt would, for a time, somewhat protect them from

the implications of this scenario. Taking into account the decline in their

terms of trade, most developing countries would face stagnating or declining

per capita incomes.

xiv. But this picture might be overoptimistic. The financing crisis of

U.S. deficits might emerge suddenly and precipitate a sharp recession with

growth much below the average for a year or two. This would have obvious

implications for the developing countries' debt servicing ability. Even under

the scenario depicted above, the developing countries would have to generate

continuous large trade surpluses to service their debt, under conditions of

slow growth. Industrial countries would have to be willing to accept

corresponding trade deficits despite their unemployment. Commercial banks,

through involuntary lending or rescheduling would have to continue slowly

increasing their exposure in developing countries, despite the latters

impaired prospects.

xv. However, this scenario is not unavoidable. Timely, moderate, but

credible reduction in U.S. fiscal deficits could still bring about a much

better outcome. The US dollar could decline gradually, and allow gradual

decline in real dollar interest rates. If this is accompanied by some

relaxation of financial policies in other industrial countries (mostly

monetary in Europe, largely fiscal in Japan), and by adequate wage and other

factor cost restraints, industrial countries could grow at a rate of 3 percent

for the remainder of the decade and somewhat faster thereafter. Protectionism

could then be more easily contained and developing countries exports grow at a

rate of about 5 percent. Middle-income developing countries would then have

an environment which could allow them to rebuild their debt service capacity

and commercial banks gradually return towards modest, voluntary lending to

them. Under this scenario, overall developing countries GNP could grow at 5

percent allowing room for growth in per capita incomes. Only in Sub-Saharan

Africa would income growth not resume till the end of the period; but at least

declines would halt.

xvi. Of course, the international environment, determined by the

industrial countries policies, is only a necessary, not a sufficient

condition, for such an outcome. Developing country policies would also have

to continue to improve, both in moving towards reduction of internal and

external imbalances and in terms of greater factor movement flexibility and

improved pricing.

xvii. The acceptable outcome outlined above is not the best possible. One

can imagine better ones. They would require firmer correction of financial

imbalances in the industrial countries, roll back rather than containment of

protectionism, and more official capital flows. They would also require

bolder movement toward improved policies in the majority of developing

countries. While one cannot realistically count on this happening within the

transition period under consideration, it is perhaps not too much to fix such

improved policies and the faster growth they entail as a realistic and

attainable goal for the 1990s.

I. INTRODUCTION

1. In 1981 and 1982 the world economy suffered its deepest and most

widespread recession in half a century. By 1983, recovery was under way, and

it strengthened and spread further in 1984. It helped to relax payments

tensions, to ease the path of domestic adjustment policies in developing

countries and to contain the "debt crisis". Beyond these positive results,

however, causes for concerns remain. Not the least of which is that a major

driving force behind the recovery so far has been the emergence of new

disequilibria in domestic finances, external payments and factor employment

within industrial countries, which are themselves not sustainable in the

medium term.

2. The world economy has not yet returned to an even growth path. Aside

from the real and financial imbalances that still need to be corrected, trade

protectionism is still a major threat and the danger of financial insolvency

is still present for several countries. Furthermore, many industrial and

developing countries will continue to face serious structural adjustment

problems for several years, as adaptation to past price, demand and supply

changes necessary to ensure fuller employment of existing factor supplies,

especially labor, is still far from complete in many of them.

3. The present economic recovery presents both opportunities and

challenges to policy makers in industrial and developing countries. Its

continuation in the medium term, which is in their strong common interest,

requires that economic policies be consistent with this objective. Current

- 2 -

policies must therefore be continuously reassessed, to identify the changes

needed to achieve and maintain such consistency. Sustaining the current

recovery, moreover, both depends upon and is a precondition for a return to

durable trade and financial equilibria and for making steady progress in

redressing the structural imbalances that stand in the way towards sustainable

long-term non-inflationary growth.

4. Transition from the present cyclical recovery to steady long-term

growth will have to be managed during the remainder of this decade, and this

is the focus of this paper. The first part deals briefly with the overall

impact on developing countries of the 1983-84 economic recovery in industrial

countries. The second part examines in some detail the external adjustment

paths followed by developing countries. The third part sums up the policy

challenges that lie ahead. The last section deals specifically with the

medium term prospects for the world economy and for developing countries in

particular, in the event of moderate policy adjustments in industrial

countries, and also assuming continuation of present policy trends.

- 3 -

II. THE ENVIRONMENT OF THE DEVELOPING COUNTRIES: GLOBAL ECONOMIC

RECOVERY IN THE INDUSTRIAL COUNTRIES, 1983-84

5. The world economy now appears to be on the mend. In 1983-84 the

major industrial countries succeeded in setting their economies on a recovery

path, while also reducing inflation. In developing countries the growth of

output was less fast and domestic inflation rates were still on the rise, but

despite rising interest rates and associated debt service burdens, many of

them made substantial progress in dealing with the payment difficulties. they

faced. On the whole, financial tensions were eased and world output and trade

once again grew.

6. World real output increased by 2.4 percent in 1983 and by an

estimated 4.2 percent in 1984. World trade, which had declined in both volume

and value in 1982 and had returned to a positive, if modest, volume growth in

1983 registered a strong increase in 1984, pulled by the expansion in economic

activity in both industrial and developing countries. The growth of world

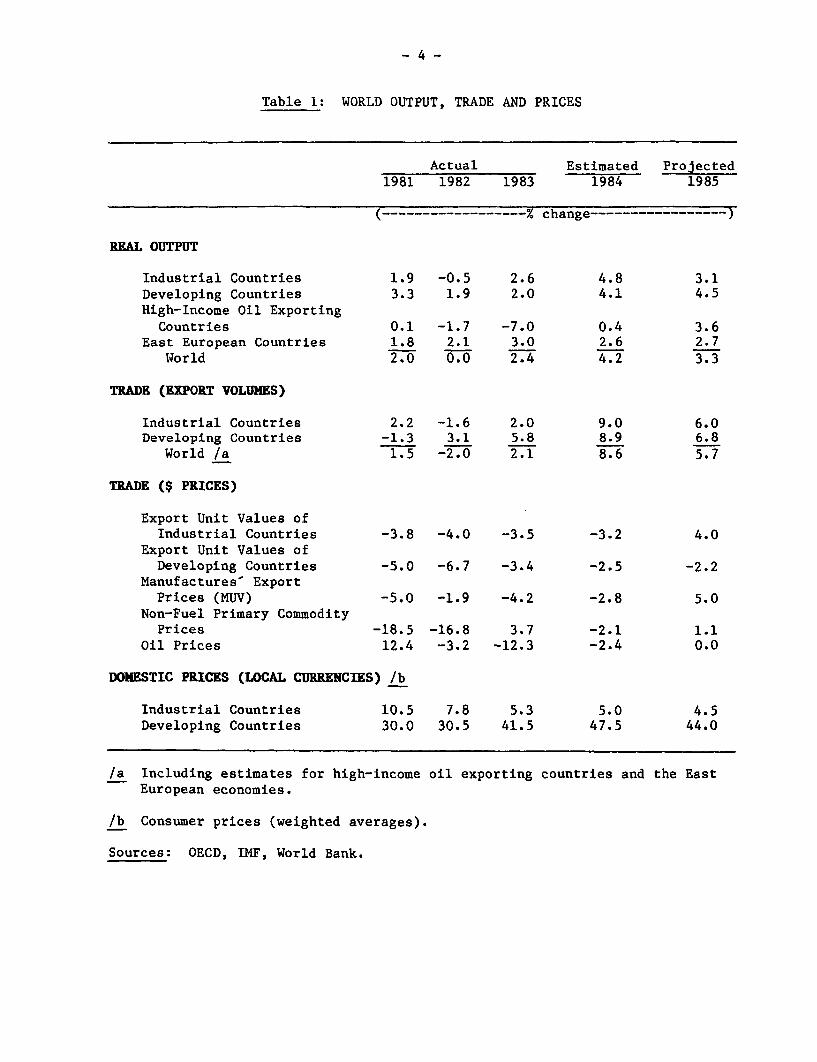

exports is estimated at about 9 percent in 1984 (Table 1).

7. Industrial countries- real output grew by 2.6 percent in 1983 and,

according to preliminary estimates, by 4.8 percent in 1984. Recovery in

industrial countries was still regionally unbalanced. Real growth was fastest

in the United States, whose economic expansion fueled the world recovery.

Japan followed, with the second highest rate of growth of real domestic

product for the whole year, and resumed its traditional place as the fastest

growing industrial economy in the second half of 1984. Europe's recovery was

at best tentative and slow, and unemployment there continued to increase.

- 4 -

Table 1: WORLD OUTPUT, TRADE AND PRICES

Actual Estimated Projected1981 1982 1983 1984 1985

(------------------% change…-----------------

REAL OUTPUT

Industrial Countries 1.9 -0.5 2.6 4.8 3.1Developing Countries 3.3 1.9 2.0 4.1 4.5High-Income Oil Exporting

Countries 0.1 -1.7 -7.0 0.4 3.6East European Countries 1.8 2.1 3.0 2.6 2.7

World 2.0 0.0 2.4 4.2 3.3

TRADE (EXPORT VOLUMES)

Industrial Countries 2.2 -1.6 2.0 9.0 6.0Developing Countries -1.3 3.1 5.8 8.9 6.8

World /a 1.5 -2.0 2.1 8.6 5.7

TRADE ($ PRICES)

Export Unit Values ofIndustrial Countries -3.8 -4.0 -3.5 -3.2 4.0

Export Unit Values ofDeveloping Countries -5.0 -6.7 -3.4 -2.5 -2.2

Manufactures' ExportPrices (MUV) -5.0 -1.9 -4.2 -2.8 5.0

Non-Fuel Primary CommodityPrices -18.5 -16.8 3.7 -2.1 1.1

Oil Prices 12.4 -3.2 -12.3 -2.4 0.0

DOMESTIC PRICES (LOCAL CURRENCIES) /b

Industrial Countries 10.5 7.8 5.3 5.0 4.5Developing Countries 30.0 30.5 41.5 47.5 44.0

/a Including estimates for high-income oil exporting countries and the EastEuropean economies.

/b Consumer prices (weighted averages).

Sources: OECD, IMF, World Bank.

- 5 -

8. Despite the pace of the recovery, inflation generally continued to

moderate in the industrial countries. Overall, the rate of increase of the

GDP deflator expressed in national currencies fell to its lowest level since

the late 1960s. Continued restraint in monetary policy, moderation in the

growth of wages and other industrial input costs were the key to this positive

performance. In the United States and in Japan price stability was bolstered

by rising exchange rates (Table 2). But the progress made against inflation

was equally solid in Europe, and given the cost-push impact of depreciating

exchange rates, this is perhaps even more remarkable.

9. The recovery of world demand did not exert any significant upward

pressure on traded good prices. The prices of manufactures exported by

industrial countries rose even less than their GDP deflators. Reductions in

domestic inflation rates, coupled with improvements in manufacturing

productivity, and strong competition in export markets helped contain the

increase in manufactured goods prices in terms of domestic currencies. In

dollar terms, their prices continued to fall in 1984 as the dollar continued

to appreciate. The prices of primary commodities also fell in 1984, under the

impact of dollar appreciation and of interest rate increases (Table 2).

10. That the cause of the continued appreciation of the US dollar are not

well understood is illustrated by most observers' having forecast that it

would decline in 1984. What is clear, however, is that the high value of the

dollar, coupled with the early and vigorous resumption of growth in the United

States contributed to a surge of imports. The Federal budget deficit

Table 2: SELECTED MONETARY INDICATORS FOR INDUSTRIAL COUNTRIES

1981 1982 1983 1983 1984iQ 2Q 3Q 4Q iQ 2Q 3Q 4Q

(- %)

A. Short-Term Domestic Interest Rates /a

United States 14.1 10.7 8.6 8.1 8.4 9.2 8.8 9.1 9.8 10.3 9.1Japan 7.7 7.1 6.7 6.9 6.7 6.8 6.5 6.3 6.3 6.3 6.3Germany 12.1 8.9 5.8 5.7 5.4 5.7 6.3 6.0 6.0 6.0 5.9France 15.3 14.7 12.6 12.9 12.6 12.6 12.5 12.7 12.5 11.6 10.8United Kingdom 13.0 11.5 9.6 10.5 9.7 9.3 8.9 8.7 8.7 10.4 9.4

B. Short-Term International Interest Rates

Eurodollar Rate /b 16.5 13.1 9.6 9.2 9.3 10.1 9.9 10.1 11.4 11.9 9.9London Interbank Rate /b 16.8 13.2 9.6 9.3 9.3 10.0 9.8 10.2 11.4 11.8 10.0London Interbank Rate 7T 16.6 13.5 9.8 9.5 9.5 10.4 10.0 10.4 11.8 12.2 10.4

C. Effective Exchange Rates /d (--yearly % change--) (---------- change from previous quarter----------)

United States 12.7 11.7 5.8 -2.8 2.9 3.6 0.3 0.7 0.9 6.0 2.7Japan 13.1 -5.7 10.1 9.2 1.1 0.4 4.4 2.1 1.0 -2.4 1.0Germany -9.5 4.1 2.4 1.7 0.1 -2.4 0.3 0.0 -0.1 -2.1 -1.6France -10.6 -9.1 -8.7 0.5 -5.5 -2.6 -1.6 -1.0 0.1 -2.0 -1.5Italy -13.3 -7.5 -5.1 0.2 -2.0 -2.3 -2.4 -1.5 -0.4 -1.7 -1.9United Kingdom -1.1 -4.8 -8.0 -9.5 4.6 0.6 -2.0 -1.7 -2.5 -2.2 -3.8Australia 10.4 -5.0 -7.3 -2.2 -5.6 3.3 3.9 2.8 -2.4 -3.9 2.8Canada 2.9 1.9 3.2 -0.6 1.1 1.4 -0.3 -1.2 -2.7 0.9 0.8

/a Three months treasury bill rates or private bill rates, except for France and Germany, for which interbank moneyrates are quoted.

/b Three months, on US dollar deposits.7T Six month, on US dollar deposits.7- MERM weights.

Source: IMF, International Financial Statistics (various issues).

- 7 -

constituted a parallel influence, also clearly related to the appreciating

dollar. As a result, US import expenditure rose by 6 percent in 1983 and by

26 percent in 1984, while export revenue grew much less. The trade deficit of

the US rose from $43 billion in 1982 to $108 billion in 1984, and the current

account deficit increased by more than $90 billion over the same period (Table

3).

11. The corresponding increase in the net surplus outside the United

States exercised a powerful expansionary influence on the rest of the world,

equivalent to about 1 percent of world GDP. However, the distribution of this

impulse was uneven. Although emphasis on absolute values is rendered

difficult by the errors and omissions in the world current account balance, 1/

the broad trends are clear. Among industrial areas, the improvement in the

current accounts of Japan and Europe over the 1982-84 period was of about

equal magnitude: $28 billion. However, while improvement in the position of

Japan came as an addition to existing surpluses, Europe reached equilibrium in

its overall current account only in 1983, and improved slightly upon it in

1984. Some European countries are still running sizable deficits, offset by

surpluses in others. One consequence of this is that concerns about balance

of payments, and about the effects of deficits on exchange rates and on

domestic inflation still constrain some European governments' willingness to

relax financial policies in order to stimulate output and employment growth.

1/ "Errors and omissions" have increased rapidly since 1980. See Table 8.

Table 3: ECONOMIC PERFORMANCE OF INDUSTRIAL COUNTRIES: 1981-85

Actual Estimated Projected1981 1982 1983 1984 1985

(-------------------% change----------------)

RETA GNr

United States 2.5 -2.1 3.7 6.8 3.0Japan 4.0 3.2 3.0 5.7 5.0Europe -0.1 0.6 1.3 2.3 2.5

Total OECD 1.9 -0.5 2.6 4.8 3.1

REAL TOTAL DOMESTIC DEMAND

United States 3.1 -1.2 5.0 8.7 3.7Japan 2.1 3.1 1.6 4.2 4.5Europe -1.8 0.8 1.0 2.0 2.0

Total OECD 1.1 0.0 2.7 5.2 3.0

PRIVATE CONSUMPTION DEFLATORS

United States 8.6 5.9 3.7 3.2 3.5Japan 4.5 2.7 1.6 2.2 2.7Europe 11.6 10.7 8.4 8.0 7.0

Total OECD 9.4 8.0 5.4 5.0 4.7

(…--------$ billion---------------)

CURRENT ACCOUNT BALANCES

United States 6.3 -9.2 -41.6 -100.0 -130.0Japan 4.8 6.9 20.8 35.0 40.0Europe -21.5 -17.8 0.9 10.0 14.0

Total OECD -25.0 -27.5 -25.2 -61.5 -86.0

(--------------% of labor force------------)

UNEMPLOYMENT

United States 7.6 9.7 9.6 7.5 7.0Japan 2.2 2.4 2.6 2.7 2.5Europe 8.2 9.5 10.5 11.0 11.5

Total OECD 6.9 8.4 9.0 8.5 8.5

Source: OECD: Economic Outlook (various issues).

12. Table 3 shows the relationship between the movements in GNP, domestic

demand and the balance of payments in the three major industrial areas. In

the United States, real domestic demand grew much faster than real GNP. This

was largely due to the impact of the rapidly growing fiscal deficit in a

country where private savings, traditionally quite low, have barely exceeded

private investments. Demand expansion fueled the growth of GNP, but also gave

rise to the current payments gap, as in the past two years the growth of real

domestic demand exceeded that of domestic product by more than 3 percentage

points. In Europe, in part because of concern with the balance of payments,

the growth of real domestic demand remained below that of GNP, thereby acting

as a break on the growth of real domestic output. As for Japan, where the

balance of payments constraint was never operative and domestic price rises

were also contained more successfully than even in the United States and in

most European countries, the growth in domestic demand accelerated only

recently and remained on average lower than that of GNP, thus contributing to

rising payments surpluses.

13. On the whole, the current account deficit of industrial countries

increased from $25.2 billion in 1982 to $61.5 billion in 1984. This growing

overall payments deficit and the rising imports of the industrial countries

have contributed to easing the developing countries' financial adjustment to

the particular problems of the early 1980s. Their own mounting debt, the

changes intervened in the attitudes of commercial lenders and of aid

suppliers, as well as the rise in interest rates, required the developing

countries to move towards a trade surplus position. This was facilitated by

the developments in the overall trade and payments position of industrial

countries just described.

- 10 -

14. Developing countries' export revenues increased by 8 percent in 1984,

while import expenditure grew by 2.4 percent. Their trade balance went from

an overall deficit of $49 billion in 1982 to a surplus of about $3 billion in

1984. 1/ Their current account imbalance was reduced by two-thirds during the

same period. The upsurge of exports to the United States, and, to a smaller

extent, to Europe and Japan also helped the recovery of domestic output in

most developing countries. On the whole, their real GDP growth rate nearly

doubled between 1983 and 1984. The impact of improved world demand and

relative price conditions 2/ for developing countries exports varied,

depending on individual country's export structure (by product and

destination), capacity to respond to outside stimuli, external financial

position and the nature and extend of the imbalances affecting it. It also

depended critically on the domestic policies that were followed by the various

countries, not only during the 1983-84 recovery period, but also earlier.

1/ See further Table 4.

2/ Developing countries' terms of trade improved in 1984 on account of thedecline in the price of both manufactured products exported by industrialcountries and oil (Table 10).

- 11 -

III. FINANCIAL ADJUSTMENT IN DEVELOPING COUNTRIES: 1982-84

15. In mid-1982, when Mexico's inability to meet its contractual debt

service obligations suddenly transformed the "debt problem" into a "debt

crisis", the world economic recession was at its worst. Economic activity,

export prices and volumes were declining. The sharp reduction of voluntary

private lending to developing countries (for many, a virtual cessation) left

to those countries faced with a pressing need to reduce their balance of

payments deficits no alternative to cutting back their imports. In some

countries, which had either tried to anticipate the- emergence of financial

difficulties or had already been affected by them (e.g. Turkey, Brazil), the

adjustment process began earlier. On the whole, however, developing

countries' imports began to be cut severely in 1982. 1/ In that year overall

import expenditure by developing countries fell by almost 8 percent. Low-

income Sub-Saharan African countries, hit by a dramatic decline in commodity

export revenues, and middle-income Latin American countries, facing the most

acute debt problems, reduced their import outlays most sharply; but. import

cutbacks were general across geographical regions and income groups (Table

4). Except for China and some of the agricultural Asian countries, most

developing countries also suffered declines in GDP growth rates. In the

1/ Unless otherwise specified, the developing countries' data quoted in thispaper refer to a panel of 90 countries, which account for 97 percent- oftotal developing countries' population, 92 percent of total GNP and 86percent of total-exports. The list is provided in Annex Table 1, togetherwith the components of the various regional and analytical subgroups usedin this paper. The IMF grouping. of developing countries that is mostcomparable with the 90 country panel totals is "non-oil developingcountries".

Table 4: IMPORTS, EXPORTS AND TRADE BALANCES OF DEVELOPING COUNTRIES

Export Values Import Values Trade Balances1981 1982 1983 1984 1981 1982 1983 1984 1981 1982 1983 1984

(--…-------------------- % change-------------------- --) ( ----Billions US$------)

LJOR. am GROUPS

1. Sub-Saharan Africa /a -22.2 -11.2 -9.6 8.0 5.9 -11.8 -16.7 -14.8 -7.1 -6.1 -2.7 4.3

2. East Asia 8.5 -0.6 4.3 9.8 10.1 -3.0 5.6 4.5 -9.8 -5.8 -8.0 -3.3

3. South Asia 3.8 -3.1 5.9 4.3 -2.0 -4.3 -0.7 0.9 -10.3 -9.7 -8.8 -8.5

4. EMENA 3.4 -6.1 -2.0 5.5 8.0 -3.9 -4.0 -2.3 -36.0 -35.9 -33.4 -29.6

5. Latin American 6Caribbean 3.1 -4.8 3.8 7.0 7.1 -20.7 -26.9 10.9 -10.9 6.2 31.9 35.4

ANALTTICAL C2DUPS

1. Low-Income Countries 3.0 -1.2 2.1 13.9 -3.9 -8.6 2.0 3.5 -15.2 -10.8 -11.0 -11.5

Africa -23.0 -6.8 -3.0 8.6 -13.2 -10.0 -6.4 1.0 -4.9 -4.2 -3.7 -3.3

Asia 10.2 -0.2 3.0 14.8 -1.2 -8.2 4.1 3.8 -10.3 -6.6 -7.3 -8.2

2. Middle-Income Countries 0.4 -3.3 1.8 7.1 9.9 -7.8 -7.2 1.7 -57.7 -38.2 -6.1 14.4

2.1 Oil Importers 4.9 -2.5 6.4 7.4 6.1 -7.0 -3.8 2.2 -61.2 -47.4 -24.8 -11.9

Major Exporters ofManufactures 7.1 -2.6 6.7 7.5 5.8 -6.2 -3.4 2.8 -35.8 -27.4 -9.3 -1.4

Other Non-Oil -5.1 -1.6 4.8 6.6 7.3 -10.1 -5.3 -0.4 -25.4 -20.0 -15.5 -13.3

2.3 Oil Exporters -6.3 -4.6 -5.9 6.5 19.3 -9.5 -15.0 0.6 3.5 9.2 18.7 26.3

ALL DEVKLOPING COUNTRIES /b 0.7 -3.1 1.9 7.9 7.9 -7.9 -6.1 1.9 -72.9 -49.0 -17.0 2.9

/a Excluding South Africa. The IMF definition excludes both South Africa and Nigeria.

71 Figures refer to a sample of 90 developing countries.

Source: World Bank, Economic Analysis and Projections Department.

- 13 -

regions where import reductions were sharpest, the absolute level of output

actually fell, by about 1 percent in Latin America and by 1.2 percent in Sub-

Saharan Africa (Table 5).

16. In 1983, middle-income Latin American countries, whose debt servicing

difficulties had reached a peak, again reduced their imports expenditure by

compressing real domestic absorption, including investments. Import

expenditure fell by 27 percent and the decline in their real output also

accelerated (to -2.9 percent). The combined effect of such a strong reduction

of imports and of increased exports to the United States and other industrial

countries was a first strong improvement in current accounts during the year.

17. In the course of the adjustment process, private incomes and

consumption expenditures were reduced throughout Latin America. However, the

brunt of the compression of domestic demand fell on investment. In Brazil,

for instance, the value of investment in constant prices was reduced by well

over one-third in three years; in the four major oil-importing debtor

countries (Argentina, Brazil, Chile, and Colombia) total real investments in

1983 were 40 percent below their 1981 level.

18. East Asian middle-income countries provided the sharpest contrast to

Latin America. These countries, and particularly the major exporters of

manufactures, had weathered the 1982 fall in their trade with only a moderate

slowdown in their traditionally fast growth of real output. Recovery of

demand for their exports, particularly in the United States, allowed them to

restore normal import growth rates in 1983, and to raise the growth rate of

- 14 -

Table 5: REAL GDP GROWTH IN DEVELOPING COUNTRIES

Actual Estimated Projected1982 1983 1984 1985

(---------% change--------)MAJOR BANK GROUPS

1. Sub-Saharan Africa /a -1.2 -2.4 -0.8 2.0East Africa 0.1 1.0 1.3 2.6West Africa -1.8 -3.9 -1.7 1.7

2. East Asia 5.4 7.3 7.2 6.3China 7.4 9.0 9.0 7.0Other East Asia 3.8 5.9 5.5 5.8

3. South Asia 2.8 6.2 4.4 5.3India 2.6 6.5 4.2 3-7Other South Asia 3.5 5.2 4.9 6.4

4. EMENA 3.5 2.5 2.6 3.6

5. Latin America and Caribbean -0.9 -2.9 2.8 3.6

WDR ANALYTICAL GROUPS

1. Low-Income Countries 5.0 7.2 6.6 6.0Africa 0.7 07 19 -Asia 5.4 7.8 7.1 6.3

2. Middle-Income Countries 0.8 0.0 3.1 3.8

2.1 Oil Importers 0.8 0.7 3.3 3.8

Major Exporters of 1.3 0.7 3.5 4.0Manufactures

Other Non-Oil -0.7 0.4 2.7 3.2

2.2 Oil Exporters 0.9 -1.0 2.7 3.9

ALL DEVELOPING COUNTRIES /b 1.9 2.0 4.1 4.5

Memorandum Items:

Low-Income Countries (excludingChina and India) 2.3 3.0 3.2 4.3

All Developing Countries(excluding China and India) 0.9 0.2 3.1 3.9

/a Excluding South Africa.lb Including South Africa. Total refers to a panel of 90 developing countries.

Source: World Bank, Economic Analysis and Projections Department.

- 15 -

domestic output while also reducing their external deficits. This pattern

continued and was consolidated in, among others, Korea, Thailand, Hong Kong

and Singapore, whose joint current account balance improved by $4 billion and

whose output growth was in excess of 5 percent during 1983. Better domestic

policies, reflected in lower domestic inflation rates, lower budget deficits

and more adroit exchange rate managements than in other middle-income

developing countries, coupled with greater capacity to respond to changes in

external conditions (built up through years of export-oriented fast

development) helped this fast and relatively painless adjustment.

19. In the middle-income countries of the Middle East, North Africa and

Southern Europe, 1/ the pattern of events followed a course mid-way between

Latin America and the Far East. Turkey, for instance, became unable to meet

its debt service obligations well before the onset of the world recession.

Its adjustment thus begun at a time when external circumstances were more

favorable. In the early 1980s, its exports and real GDP never stopped

growing, and by 1983 private per capita consumption, and by 1984 investments

could also start to recover.

20. As for Asian low-income countries, limited dependence on external

trade partly insulated India and China from external shock. More broadly,

these countries continued to improve their domestic policies, maintaining and

even accelerating their output growth rates. They had contained their balance

of payments deficits in the 1970s, and generally reduced them in the early

1/ These are the countries included in the Bank's EMENA region.

- 16 -

1980s. China moved into substantial surplus. Only in the case of India and

China, however, was the size of the payments deficit policy determined, in the

sense that few, if any, of the other countries in this group had the ability

to borrow much on commercial terms. India and China pursued very cautious

foreign borrowing policies, with the deliberate aim of avoiding excessive

dependence on external capital.

21. Sub-Saharan Africa continued to face the most severe difficulties in

the early 1980s. The value of its exports, almost exclusively primary

commodities, fell by more than 40 percent in 1981-83. Import expenditure had

to be drastically reduced over the same period. The improved trade balance,

however, was not enough to allow the region's debtor countries to meet their

debt service obligations. GDP continued to fall, and per capita incomes, now

frequently below their pre-independence levels, fell even more sharply.

Undoubtedly, domestic policy improvements in the region remained limited and

the policy thrust often unstable; but for these raw material exporters, with

often very trade-dependent economies, the negative evolution of raw material

prices, the lack of recovery in their traditional European markets and the

decline of aid left very little room for sustained adjustment measures which

did not require politically unenforceable sacrifices.

22. The consolidation of economic recovery in industrial countries during

1984, together with the significant shift in policy response that occurred in

many developing countries, determined a major turnaround in adjustment

results. Increased demand for their exports and greater ability to take

advantage of improved export market conditions created by a combination of

- 17 -

expenditure reduction and expenditure switching policies, put developing

countries in a position to resume output growth, while at the same time

reducing further their payment deficits (Table 6).

23. The changes in terms of trade that occurred in 1984 and the relative

import-export volume performances determined final outcomes in terms of trade

balances. Middle-income countries accounted for most of the improvement that

occurred from 1983 to 1984 ($14.5 billion). Among them the largest movements

towards surplus were made by the major exporters of manufactures, in both East

Asia and Latin America. Quantity factors played the major role, as the

improvement in middle-income countries terms of trade was minimal in 1984.

Low-income developing countries only marginally reduced their overall trade

deficit. Sub-Saharan African countries and, to a smaller extent, India and

China showed the largest improvement in trade balances. The former were

helped by a strong improvement in terms of trade, largely determined by a fall

in the prices of imported food and manufactures and a sharp increase in the

prices of exported tropical beverages (Table 4).

24. Middle-income countries registered the strongest improvements in

current account balances during 1984, despite sharply rising interest

payments. Middle-income oil importing countries registered a $15 billion

reduction in deficit, while oil exporters managed to reduce their current

account imbalance by almost $7 billion. Net private lending to middle-income

countries continued to fall in 1984, although by less than in 1983. Despite a

small increase in official lending, this group of countries registered a net

outflow of about $14 billion in 1984, as interest payments on existing and new

- 18 -

Table 6: DEVELOPING COUNTRIES CURRENT ACCOUNT BALANCE AND ITS FINANCING, 1970-84

(Billions of Current US$)

1970 1980 1981 1982 1983 1984

A. OWW-INCOME COUNTRIES

Asia

Net Exports (GNFS) -1.358 -15.755 -11.498 -6.831 -7.246 -8.687Net Factor Income -0.390 0.078 -0.212 -0.983 -0.523 -0.605Interest on KLT Debt -0.286 -1.363 -1.560 -1.515 -1.598 -1.833

Official -0.241 -0.689 -0.657 -0.762 -0.962 -1.079Private -0.045 -0,674 -0.904 -0.752 -0.636 -0.754

Current Account Balance -1.551 -9.685 -6.164 -1.364 -1.001 -3.083(Excl. Official Transfers)

Net Official Transfers 0.370 1.952 2.084 1.884 2.011 1.952MLT Loans 0.987 4.878 3.227 3.957 4.199 6.541

Official 0.971 3.410 3.452 3.883 3.542 4.222Private 0.016 1.468 -0.225 0.074 0.657 2.319

Net Direct Investment 0.029 0.159 0.422 0.488 0.546 0.643Change in Reserves -0.187 0.449 2.406 2.135 -4.224 -3.184Debt Outstandtng and Disbursed 11.524 38.412 39.545 42.941 46.290 52.831

As Percent of GNP 6.958 7.798 8.175 8.850 9.058 9.741*As Percent of Exp. GS 183.636 96.704 89.501 95.064 98.880 100.032

Debt Service Ratio 12.423 7.996 9.295 10.929 8.311 8.443

Africa

Net Exports (GNFS) -0.381 -5.385 -5.391 -4.135 -4.339 -3.784Net Factqr Income -0.161 -0.901 -1.098 -1.004 -1.049 -1.294Interest on MLT Debt -0.080 -0.698 -0.643 -0.567 -0.662 -1.000

Official -0.042 -0.312 -0.259 -0.267 -0.315 -0.435Private -0.038 -0.386 -0.384 -0.300 -0.348 -0.565

Current Account Balance -0.679 -5.837 -5.882 -4.978 -4.900 -4.594(Excl. Official Transfers)

Net Official Transfers 0.297 2.109 1.813 1.515 2.008 1.925MLT Loans 0.276 3.349 2.862 2.198 1.910 2.025

Official 0.247 2.366 2.249 1.858 1.922 2.231Private 0.030 0.983 0.614 0.340 -0.012 -0.206

Net Direct Investment 0.173 0.236 0.221 0.223 0.211 0.086Change in Reserves -0-111 0.555 0.377 0.500 0.171 0.607Debt Outstanding and Disbursed 2.874 20.787 22.905 24.487 25.399 26.583

As Percent of GNP 17.931 39.936 43.753 47.765 52.223 54.550As Percent of Exp. GS 75.232 175.807 216.466 260.561 279.452 278.067

Debt Service Ratio 6.065 12.541 13.801 15.654 16.507 19.893

B. MIDDLE-INCOME COUNTRIES

Major Exporters of Manufactures

Net Exports (GNFS) -5.719 -28.892 -26.983 -17.988 0.487 19.590Net Factor Income -1.768 -17.058 -25.505 -30.822 -32.135 -38.481Interest on MLT Debt -1.120 -14.880 -19.504 -22.510 -20.139 -25.839

Official -0.217 -2.158 -2.381 -2.948 -3.320 -3.818Private -0.903 -12.722 -17.123 -19.562 -16.819 -22.021

Current Account Balance -5.500 -35.260 -41.696 -38.294 -21.969 -9.345(Excl. Official Transfers)

Net Official Transfers 0.502 2.483 2.550 2.608 3.180 3.735MLT Loans 3.590 21.401 29.160 25.043 16.617 17.474

Official 0.868 5.065 5.139 4.827 6.525 7.626Private 2.722 16.336 24.021 20.216 10.092 9.848

Net Direct Investment 1.076 4.356 6.106 5.888 4.478 4.605Change in Reserves -0.503 1.606 0.127 4.098 4.369 -10.554Debt Outstanding and Disbursed 24.357 166.602 191.029 215.801 242.016 266.818

As Percent of GNP 15.871 22.848 24.839 28.017 34.746 37.638As Percent of Exp. GS 91.507 77.315 81.728 97.079 105.221 109.099

Debt Service Ratio 15.100 16.060 17.067 19.350 16.189 15.997

- 19 -

Table 6: DEVELOPING COUNTRIES' CURRENT ACCOUNT BALANCE AND-ITS FINANCING,1970-84 (CONTINUED)

(Billions 'of Current US$)

1970 1980 1981 1982 1983 1984

Other Non-Oil

Net Exports (GNFS) -1.345 -18.179 -23.517 -17.146 -12.721 -9.617Net Factor Income -0.960 -5.188 -6.005 -7.761 -9.900 -10.567Interest on MLT Debt -0.445 -4.457 -5.551 -6.762 -6.733 -8.002

Official -0.194 -.136 -1.353 -1.604 -1.927 -2.418Private -0.251 -3.321 -4.198 -5.157 -4.805 -5.584

Current Acdount Balance -1.923 -18.564 -24.056 -19.804 -17.743 -15.022(Excl. Official Transfers)

Net Official Transfers 0.583 3.084 3.'278 3.228 2.653 2.539MLT Loans - 1.747 11.789 12.866' 11.873' 7.918 10.798

Official 0.800 5.931 6.119 5.905 5.160 5.333Private 0.947 5.857 6.748 5.968 2.758 5.466

Net Direct Investment 0.149 1.653 1.875 1.355 1.390 1.126Change ih Reserves -0.635 -3.420 0.397 3.619 3.003 1.461Debt Outstanding and Disbursed 11.916 68.327 78.850 88.932 97.751 108.035-

As Percent of GNP 21.986 30.187 33.831 40.713 48.658 52.966As Percent of Exp. GS 110.987 120.672 136.398 155.433 175.472 183.860

Debt Service Ratio 13.577 17.184 20.765 22.697 23.094 24.929

Oil Exporters

Net Exports (GNFS) -0.915 14.628 -10.713 -13.701 7.854 .16.666Net Factor Income -2.207 -16.186 -19.006 -23.981 -22.631 -24.692Interest on MLT Debt -0.693 -11.454 -13.903 -16.660 -17.463 -21.252

Official -0.209 -1.656 -2.045 -2.132 -2.508 -2.830Private -0.485 -9.798 -11.859 -14.529 -14.956 -18.421

Current Account Balance -2.930 1.509 -27.297 -35.680 -11.052 -3.543(Excl. Official Transfers)

Net Official Transfers 0.595 2.007 2.485 1.918 1.918 1.809MLT Loans 1.643 16.998 23.559 20.503 18.133 13.323

Official 0.i61 4.'800 - 4.706 5.314 3.660 ' 6.194Private 0.881 12.198 18.853 15.190 14.473 7.129

Net Direct Investment 0.8i0 4.192 6.369 5.283 3.717' 2.922Change in Reserves -0.499 -17.077 2.217 15.767 3.549 -7.339Debt Outstanding and Disbursed 17.631 135.564 155.326 173.586 208.176 232.153

As Percent of GNP 18.519 24.863 25.058 32.386 39.893 43.849As Percent of Exp. GS 115.298 87.431 98.507- 123.694 157.769 164.274

Debt Service Ratio 18.073 17.848 19.776 24.977 26.132 28.090

C. ALL DEVELOPING COUNTRIES

Net Exports (GNFS) -9.717 -53.582 -78.102 -59.802 -15.966 14.168Net Factor Income -5.486 -39.255 -51.827 -64.551 -66.238 -75.640Interest on MLT Debt -2.624 -32.851 -41.161 -48.014 -46.596 -57.925

Official -0.902 -5.951 -6.694 -7.714 -9.032 -10.580Pri'vate -1.721' -26.899 -34.'467 -40.301 -37.564 -47.345

Current Account Balance -12.583 -67.837 -105.095.-100.121 -56.665 -35.588(Excl. Official Transfers)

Net Official Transfers 2.347 11.635 12.209 11.153 11.768 11.960MLT Loans 8.243 58.414 71.675 63.575 48.778 50.162

Official 3.646 -21.572 21.665 21.786 20.810 25.606Private 4.596 36.842 50.010 41.788 27.969 24.556

Net Direct Investment 2.317 10.595 14.992 13.237 10.342 9.383Change in Reserves -1.935 -17.887 5.524 26.119 6.868 -19.008Debt Outstanding and Disbursed 68.303 429.692 487.655 545.748 619.631 686.420

As Percent of GNP 14.096 21.008 22.596 26.477 31.311 33.758As Percent of Exp. GS 108.863 89.761 96.759 115.'037 130.843 135.383

Debt Service Ratio 14.746 16.016 17.589 20.543 18.999 19.690

Notes: GNFS. - Goods and Non-Factor Services; MLT - Medium-and Long Term; Debt ServiceRatio - Ratio of interest and amortization payments to exports.

Source: World Bank, Economic Analysis and Projections Department.

- 20 -

debt increased sharply during the year, and exceeded new loan receipts by that

amount. The current account deficit of Asian low-income countries widened by

about $2 billion in 1984, while that of African low-income countries remained

virtually unchanged. Rising interest payments offset the small improvement in

trade balances experienced by low-income African countries during 1984 (Table

6).

25. Growth in demand for developing countries exports was stimulated

mostly by the US recovery and the strong dollar, and, to a more limited

extent, by similar quantity and relative price impulses in Japan. Regionally,

it affected most positively those developing countries which are traditional

trading partners of the United States and of Japan. In terms of commodity

composition, it most strongly affected exports of manufactures. The demand

for non-fuel primary commodities and for petroleum remained surprisingly weak

by historical standards. These demand factors largely explain the differences

in observed trade patterns. Obviously, policy performance differences also

intervened, but the weakness of primary commodity markets, particularly in

1984, left little room for export expansion to those countries which had not

already developed a manufactures export potential in earlier years.

26. Generally speaking, the Latin American and East Asian countries, more

deeply tied to booming demand in North America and to Japan, and also

generally possessing relatively advanced manufacturing sectors were able to

expand their exports most easily. African countries, more tied to Europe

(where import demand grew much less than in North America and Japan) and, at

the same time, more dependent on exports of primary commodities, found

- 21 -

themselves in a less favorable position. The same applies to South Asian

countries (with India being a partial exception), for which exports of primary

products are of great importance.

27. The differences in external pull faced by various developing regions

are evident from their exports to the United States, Japan and the three major

European countries (Germany, France and the United Kingdom) over the 1982-84

period. Africa's exports to these countries grew more slowly in 1984 than

those of East Asia and Latin America, and recouped barely three-fifths of the

loss experienced in 1983. Exports of East Asia to the major industrial

countries increased in dollar value by about 6 percent in 1983, and by almost

25 percent in 1984. Latin American exports expanded by 13 percent in 1984

(about one-third faster than in the previous year), and South Asia's by about

12 percent (Table 7).

28. Within these total increases, developing countries' exports of

manufactured goods to the major industrial countries increased in dollar value

by 15.5 percent in 1983 and by almost 29 percent in 1984, pulled by a 31

percent increase in exports to the United States in 1983, followed by a 44

percent increase in 1984. Exports to Japan rose much less, and to Europe

least, although even exports to Europe rose at least twice as fast as overall

demand for manufactures in that region. Still incomplete data appear to

indicate that primary commodity exports to industrial countries, including

petroleum, also began to recover in 1984, even though they remained the

weakest component of the developing countries' overall export picture.

- 22 -

Table 7: MAJOR INDUSTRIAL COUNTRIES' IMPORTS FROM DEVELOPING COUNTRIESBY GEOGRAPHICAL ORIGIN

(% change)

1983 1984 (Jan.-Sept.)

UNITED STATES

from: Africa -24.3 4.0East Asia 16.3 38.5South Asia 47.8 17.8Latin America 10.9 16.0Total /a 6.0 22.0

JAPAN

from: Africa -11.8 11.1East Asia -4.0 21.6South Asia 3.0 -1.8Latin America 6.4 15.3

Total /a -2.0 17.7

EC3 /b

from: Africa -1.4 11.4East Asia 5.2 3.1South Asia -18.5 14.8Latin America 6.5 0.0

Total /a -0.5 4.7

MAJOR INDUSTRIAL COUNTRIES /c

from: Africa -13.7 8.1East Asia 6.4 24.5South Asia 8.1 12.2Latin America 9.5 12.6

Total /a 2.3 15.4

/a Including imports from EMENA countries.lb United Kingdom, France and Federal Republic of Germany.7E United States + Japan + EC3.

Source: IMF, Direction of Trade (various issues) and DRI, Trade System.

- 23 -

29. Expanding exports directly contributed to GDP growth in all

regions. In many countries, improved balance of payments positions also

allowed the relaxation of direct import control measures and, somewhat less

broadly, of financial stringency. Real GDP growth in 1984 was enough to

ensure some increase in real per capita GNP in most developing regions, with

the exception of Sub-Saharan Africa. 1/ Particularly remarkable was the

turnaround in real output growth that occurred in Latin America: from -2.6

percent in 1983 to 2.6 percent in 1984.

30. Domestic adjustment policies played a key role in determining these

outcomes. In the impact phase (1982 and the first part of 1983) a combination

of direct restraint of imports (through quantitative controls and devaluation)

and reduction in domestic absorption was predominant. This is particularly

evident in the case of middle-income Latin American countries (Chart 1).

Sometimes, direct import controls led to the reduction of production and

income-generation through the scarcity of raw materials, and of machinery and

other inputs into investment projects; sometimes, financial and other

restraints on income (including depreciation of effective exchange rates)

brought about the desired reduction of imports, also at the cost of lower

production; most often, these two effects were combined.

31. Expenditure switching measures, among which currency devaluations

were paramount, together with the onset of the recovery in industrial

countries, set the stage for a recovery of exports that began in late 1983 and

streugthened in 1984 (Chart 2). However, reduced domestic absorption still

1/ Per capita GDP growth is shown in Table 12.

- 24 -

Chart 1: REAL DOMESTIC ABSORPTION AND REAL INVESTMENT, 1980-84

(1980-100)

Developing Countries /a Middle-Income Latin America /b

O3 06=m. -bmrption 4' riI t rrm.t O __A_IIry-strn-r.t

Chart 2: REAL EXPORTS AND REAL EFFECTIVE EXCHANGE RATES, 1980-84

(1980-100)

Developing Countries /a Middle-Income Latin America /b

,f1a -

Oao so

lo *§lt*we Iga 19 19ao *"t lo lt 1064

O .es F.nl E:-. r--t=4 Rft=l E co,eRmte O3 M.er,-j,zr.:ie EF__=rt2; 4 R.ewnl Ex-hN=r9s- R=.nt_

/a Based on a sample of 26 developing countries.A7 Argentina, Brazil, Chile, Colombia and Mexico.

Source: World Bank, Economic Analysis and Projections Department.

- 25 -

played a considerable role during 1984. In most of Latin America, and in many

Mediterranean and several Asian developing countries, as well as in Sub-

Saharan Africa, per capita consumption continued to decline in 1984.

Investment was also generally lower than in earlier years, and mostly

concentrated on- the completion of old projects.

32. Developing countries as a group succeeded in reducing their external

imbalance by two-thirds in a relatively short time (between 1981 and 1984),

despite interest rates which remained exceptionally high both in nominal and

real terms throughout the period, and despite further growth in their stock of

debt. The remarkable success attained in adjusting external imbalances is

most evident in Latin America, whose trade balance went from -1.5 percent of

GDP in 1981 to about 5 percent in 1984 (in absolute amounts, from a deficit of

$11 billion to a surplus of about $35 billion).

33. Developing countries as a group have made dramatic progress in

fitting the growth of their economies to that of available resources, not only

by cutting overall demand through financial policies, but also by switching

production from the domestic market to exports through effective

devaluations. - The only major exception was Sub-Saharan Africa. African

governments were either laggard in appreciating fully the need for policy

change or were unable to implement them. However, the resources available in

many African countries made it extremely difficult to implement policy changes

that involved further reduction in domestic demand in the short term. More

importantly still, the economic structures of these countries, with embryonic

manufacturing sectors, greatly limit the scope that they have in the short run

- 26 -

for switching production to import substitution and, pending the revival of

commodity markets, to exports.

34. While financial adjustment has made considerable progress in 1982-84,

adjustment in the deeper sense of modified economic structures has barely

begun in many developing countries. As shown by falling investment, resources

continue to be scarce. In addition, high present and projected interest

rates, and the uncertainties of financial markets, render even those

developing countries that could borrow hesitant to do so and impel present

borrowers (like those in East Asia) to reduce their current account

deficits. Paradoxically, with Europe barely emerging from its current account

deficit and Latin American countries still barely able either to service or to

refinance their debt service obligations despite their current account

surpluses, only the country with the largest payments deficit, the United

States, is pursuing its expansion totally unconstrained by balance of payments

considerations (while Japan's huge surplus has not provided it an incentive to

accelerate growth). This unusual situation raises concerns as to what will

happen to world economic growth when the US current account deficit is

reduced, either by deliberate policy choice or by the emergence of a financing

constraint.

35. Another concern relates to trade. One can no longer deny that

protectionism is renascent and active. This is even better illustrated by

Bangladesh shirts than by Japanese automobiles and Brazilian and Korean

steel. When one of the world's poorest countries took a miniscule fraction of

the world market in a product whose strategic importance for industrial

countries is minor, it soon ran into quotas. Protectionism, and the threat of

- 27 -

it, most strongly affect the poorer developing countries by slowing down the

process of specialization in labor-intensive expotts.

36. Finally, capital flows to developing countries have not yet been

restored to normal levels. Financial market conditions - high real interest

rates, high debt stocks, -reduced present willingness to lend (as compared to

pre-1980 conditions) and the increased risk of sudden future changes in

lending conditions continue to impose on developing countries strong pressures

to reduce the growth of real domestic demand. Official flows have also fallen

dramatically.. With few exceptions, middle-income countries have to do wi.thout

significant development assistance at earlier stages of development than did

their predecessors ten or twenty years ago. Poor countries, including those

in Sub-Saharan Africa, whose needs are most acute, have to do with- lower

concessional flows than was generally expected-. before the, worsening of

external payments conditions in the early 1980s.

- 28 -

IV. THE CHALLENGES AHEAD: TRANSITION TOWARDS SUSTAINABLE

LONG-TERM GROWTH

37. The current recovery presents opportunities and challenges to

policymakers in industrial and developing countries both. Sustaining it is a

matter of strong, common interest. Unemployment is still very high in

industrial countries, particularly in Europe. Productive capital is also

generally underutilized. Shifts in the composition of demand, and the

reallocation of factor uses (in response to these shifts and to past and

ongoing changes in factor prices) continue to require considerable structural

adjustments in many industrial countries. Steady, reliable and strong overall

output growth would facilitate the management of these changes. Conversely,

the rigidities which have often contributed to past problems tend to be

reinforced by an environment of slow growth in which unemployment is rife. On

the financial side, debt, particularly public debt is very high in all

industrial countries and still growing. The resulting large interest rate

payments will have to be shouldered for many years. If inflation is kept

under control, only accelerated income growth will ease management of

corporate and public finances.

38. Developing countries are completing their financial adjustment

phase. They need a continuation of the world recovery to complete it, to

fully restore their creditworthiness, to regain access to the world capital

market and to concentrate on the structural adjustments of their economies

that are necessary to achieve long-term growth. The domestic costs, and

- 29 -

social and political pressures associated with the current financial

adjustment phase, are already quite high, and would become even more difficult

to bear without continued growth in export markets, a reduction in real

interest rates and resumption of capital inflows. Without them the momentum

of policy reform in developing countries would also falter and the attainment

of structural adjustment goals would again be postponed.

39. To cope with the sharp reduction in the net inflows of medium and

long term capital that occurred in 1982-84 as a consequence of the cutbacks in

international private lending, developing countries had no alternative but to

reduce their current account deficits. To do so, in the face of rising

interest payments on existing and new debt, they had to move rapidly towards a

trade surplus. This was facilitated in 1983-84 by the widening of the trade

deficit in the United States. In fact, developing countries reached a

substantial positive balance in goods and non-factor services in 1984, as

their payments on interest and amortization on medium and long term debt

exceeded the value of the new loans they were able to obtain from official and

private sources.

40. While most industrial and developing countries were drastically

reducing their current account deficits (or increasing their surpluses), the

payments deficit of the-United States was rapidly growing, as the mirror image

of the expanding US budget imbalance (Table 8). The channelling of the rest

of the world's (ex-ante) excess savings into the United States in 1983-84

helped generate a level of world economic activity higher than would have

otherwise been possible. However, this pattern cannot last if output growth

- 30 -

Table 8: WORLD TRADE AND CURRENT ACCOUNT BALANCE

1970-72 1976-78 1981 1982 1983 1984(Est.)

(-------------------Billions US$----------------)

TRADE BALANCE

Industrial Countries 10.5 -7.0 -28.0 -20.0 -16.0 -42.0of which:United States -2.0 -26.0 -28.0 -36.5 -61.0 -108.0Japan 7.0 17.0 20.0 18.1 31.5 44.0Europe 1.7 -4.0 -24.0 -14.2 -1.0 5.0

High Income Oil Exporters 4.0 39.0 132.0 62.0 37.0 56.0

Developing Countries -7.5 -23.0 -73.0 -48.0 -15.0 2.0

Other Countries -2.5 5.0 -2.0 15.0 17.0 18.0

Total /a 4.5 14.0 29.0 9.0 23.0 34.0

CURRENT ACCOUNT BALANCE /b

Industrial Countries 14.5 12.0 -4.0 -5.0 -3.0 -38.0of which:

United States 1.0 -4.5 10.7 -3.8 -35.5 -100.0Japan 5.0 10.5 6.2 8.1 22.3 35.0Europe 8.5 12.0 -6.3 -2.1 14.3 23.4

High Income Oil Exporters /c 3.5 24.0 60.0 10.0 -11.5 -4.5

Developing Countries -16.0 -38.0 -105.0 -100.0 -56.5 -35.5

Other Countries 1.0 -16.0 -8.0 8.0 10.0 12.0

Total /a -0.5 -18.0 -57.0 -87.0 -61.0 -66.0

/a Reflects statistical errors and asymmetrics.lb Excluding official transfers.7-c Partially estimated in 1983 and 1984.

Source: IBRD, OECD and IMF.

31 -

in Europe and Japan rise towards their potentials and developing countries

restore a measure of creditworthiness. It is unlikely that the United States

can continue to draw on external savings at the same rate as in 1984. It is

also undesirable that it should do sp. In the medium-term, a return to a

pattern of savings allocation more in line with the capital endowments of the

world's major regions would seem to be necessary on efficiency grounds.

Without renewed access to world capital markets and to the rest of the world's

excess savings, not only would the growth prospects of developing countries be

considerably reduced, but also those of the whole world economy. This implies

a return of industrial countries to a position of overall surplus on current

account and to a net flow of savings to developing countries.

41. A period of sufficiently high and steady non-inflationary economic

growth is needed to allow the progressive reabsorption of idle resources

(particularly of unemployed labor), the correction of existing disequilibria

in financial stocks and flows, and the completion of structural adjustments

underway in industrial and developing countries and their fruition, in terms

of greater efficiency in resource use and in capital accumulation. The

challenge lies in that a partial solution to these problems is a precondition

for sustained, non-inflationary growth, but it can hardly be achieved without

adequate growth already taking place. Credible, sustained non-inflationary

growth constitutes both a means and an end, which could become even more

elusive unless it -is pursued without delay.

42. The developing countries are seeking to regain a reasonable medium-

term balance in domestic and external finance. They need a more stable

- 32 -

external environment in terms of market access and finance to complete their

financial adjustment processes. Once this phase is over, they will have to

concentrate their efforts on the achievement conditions favorable to long term

growth, that is on the shifts in prices, in expenditures and in factor uses

most conducive to the sustained expansion of domestic output.

43. The tempo of domestic policy reform in developing countries needs to

be maintained and whenever possible quickened for the second phase of their

adjustment process to bear maximum results. Reform needs, though country

specific, have some common threads. Better utilization of existing productive

resources is clearly paramount. Greater efficiency is in large part a

function of internal price relationships and of correct balance between

domestic and world prices. Subsidies which distort prices and encourage waste

must be reduced, along with those which directly sustain undesirable

activities or inefficient enterprises. Reduction in subsidies is often a key

precondition for reducing fiscal deficits, themselves an indirect cause of

inflationary pressure. Reduced budget deficits, complemented by appropriate

monetary policies, are a precondition for the build-up of efficient financial

markets, which can attract renewed inflows of foreign capital and serve to

channel efficiently domestic savings into domestic investments. Allocation of

available capital resources, whether market or state determined, needs to be

inspired by stringent performance objectives. The more flexible the domestic

price system and the lower trade and exchange rate distortions, the greater

the chances that private and public investment decisions will be economically

and socially productive.

- 33 -

44. In shaping the future, the role of economic policies is central and

clear. In the short-term, a key objective of policies in both industrial and

developing countries must be to ensure the continuation of the present

economic recovery. In the medium-term, the objective of policies is to ensure

sustained non-inflationary growth. The industrial countries bear a particular

responsibility for ensuring, through appropriate domestic policies, that

freedom of trade is maintained, that capital flows from the richer towards the

poorer countries are renewed, and that national economic objectives are

compatible with each other and with international efficiency in the use of

resources. International cooperation for these objectives, so effective

during the past three decades, is both a necessary condition for resumed

growth and dependent upon it.

- 34 -

V. MEDIUM TERM ALTERNATIVES FOR INDUSTRIAL AND DEVELOPING COUNTRIES

45. The next 10 years, viewed schematically for the purpose of analyzing

macroeconomic policy and setting priorities, can be divided into two phases: a

period of unwinding the existing financial tensions, restoring more

sustainable global payment balances, normalizing interest and exchange rates,

decisively reducing inflationary expectations, and achieving a better

equilibrium in net flows of funds; followed by a period of faster output

growth in industrial countries and of overall development in developing

countries, funded by sustainable patterns of domestic capital accumulation and

of net foreign borrowing. These two phases roughly coincide with the medium

and the long term perspectives normally taken in World Bank World Development

Reports. Attention is focused here on the first phase.

46. Reasonably favorable central assumptions for the medium-term policy

scenarios are that industrial countries will attempt to bring about a

convergence of real interest rates with the trend growth rates of their

outputs, and to reduce the deficit in their current accounts without

disrupting the present phase of recovery in world economic activity. It is

further assumed, in part as a result of a correct growth perspective being

maintained by policymakers, and in part as the result of the postulated fiscal

and monetary adjustments, that trade protection will not increase during this

period. This assumption would be a break from recent trends. The effects of

an increase in trade protectionism will be examined as part of the downside

risks to the main scenario.

- 35 -

47. Given the short-term dynamics-of the.4984-85 situation, characterized

by strong financial tensions and considerable imbalances in trade and

payments flows .within and across regions, progress towards these objectives

will not be easy. Dealing in a positive and anticipatory fashion with the

risks inherent in the current situation will require moving away from policies

which have been successful in the short run. Good timing, and a degree.of

compatibility (whether planned or coincidental) --of financial policies within

and across countries are also prerequisites. An added difficulty is that

correcting existing internal and external imbalances may, at least in the