sustainable investment research featuring ‘the voice of the adviser’ robert norum commercial...

TRANSCRIPT

Sustainable Investment Research featuring ‘The Voice of the Adviser’

Robert NorumCommercial Director

Blue & Green Tomorrow

© Blue & Green Communications 2

Background

Four years surveying state of financial advisory market

Market for advice generally – and sustainable, responsible and ethical investment specifically

We also ask IFAs about how they win new clients and their views on the state of the economy

April 2014

© Blue & Green Communications 3

The Macro View

April 2014

© Blue & Green Communications 4

76% of financial advisers in the UK say they get requests for ethical

financial advice

£8.6 trillion representing 21.8% of assets under management is now invested sustainably. The UK leads

the world in this sector

The average ethical fund posted gains of 24% over the last year, compared

with 18% from the average non-ethical fund

Sustainable investments made by Europe’s HNWIs increased by 60% – compared to just an 18% rise in their

total wealth

60% 76%

24%22%

April 2014

© Blue & Green Communications 5

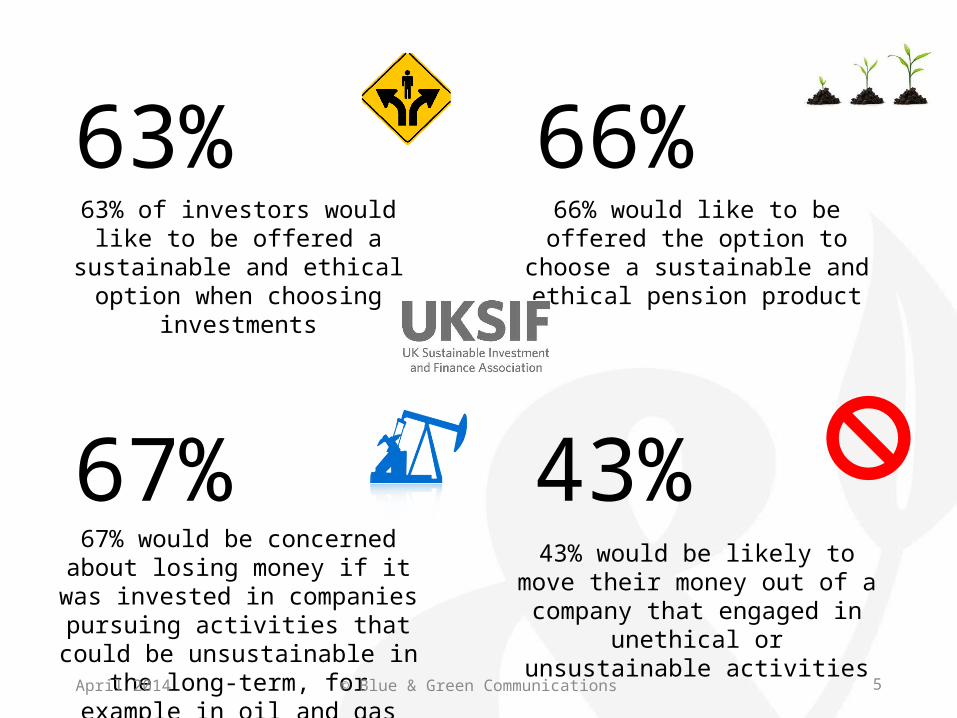

43% would be likely to move their money out of a company that

engaged in unethical or unsustainable activities

63% of investors would like to be offered a sustainable and ethical

option when choosing investments

66% would like to be offered the option to choose a sustainable and

ethical pension product

67% would be concerned about losing money if it was invested in

companies pursuing activities that could be unsustainable in the long-

term, for example in oil and gas

67% 43%

66%63%

April 2014

© Blue & Green Communications

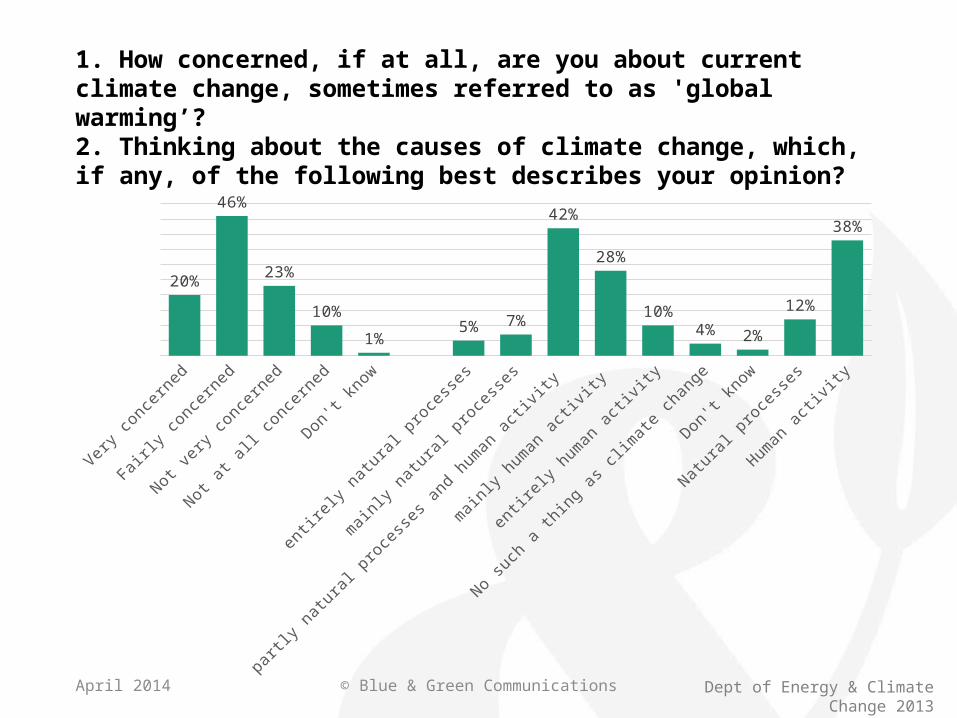

1. How concerned, if at all, are you about current climate change, sometimes referred to as 'global warming’?2. Thinking about the causes of climate change, which, if any, of the following best describes your opinion?

Very co

ncern

ed

Fairl

y conce

rned

Not very

conce

rned

Not at a

ll conce

rned

Don't know

entirely

natural p

roce

sses

mainly natura

l pro

cesse

s

partly n

atural p

roce

sses a

nd human activit

y

mainly human acti

vity

entirely

human activit

y

No such

a thing as c

limate ch

ange

Don't know

Natural p

roce

sses

Human activit

y

20%

46%

23%

10%

1%5%

7%

42%

28%

10%

4%2%

12%

38%

April 2014 Dept of Energy & Climate Change 2013

© Blue & Green Communications 7

“Latest UN median estimate for global population is 9.6 billion by 2050. That’s 2.5 billion more than today. That

was the global population in 1960. ”

April 2014

Extraordinary Facts around Sustainability: # 1

© Blue & Green Communications 8

The Economy

April 2014

© Blue & Green Communications 9

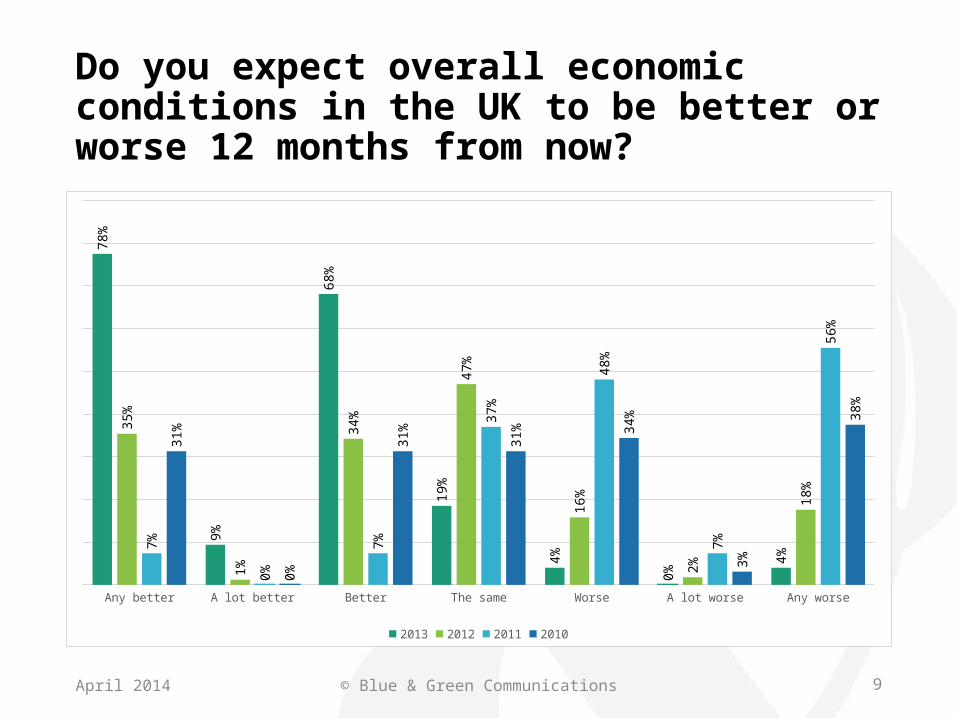

Do you expect overall economic conditions in the UK to be better or worse 12 months from now?

April 2014

Any better A lot better Better The same Worse A lot worse Any worse

78%

9%

68%

19%

4%

0%

4%

35%

1%

34%

47%

16%

2%

18%

7%

0%

7%

37%

48%

7%

56%

31%

0%

31%

31% 34

%

3%

38%

2013 2012 2011 2010

© Blue & Green Communications 10

Do you believe the Coalition Government’s economic plans will improve or worsen the economic outlook over the next 12 months?

April 2014

Any better Improve a lot Improve Make no difference Worsen Worsen a lot Any worse0%

10%

20%

30%

40%

50%

60%

70%

65%

5%

61%

29%

6%

0%

6%

36%

2%

34%

51%

10%

3%

13%

22%

0%

22% 26

%

48%

4%

52%

38%

0%

38%

16%

47%

0%

47%

2013 2012 2011 2010

© Blue & Green Communications 11

The Market for Advice

April 2014

© Blue & Green Communications 12

In the last 12 months has the number of clients you work with increased, stayed the same or declined?

April 2014

Any increased Increased a lot Increased Stayed the same Decreased Decreased a lot Any decreased

62%

6%

56%

26%

11%

2%

12%

58%

9%

50%

28%

13%

2%

14%

2013 2012

© Blue & Green Communications 13

In the next 12 months do you expect the number of clients you work with to increase, stay the same or decline?

April 2014

Any increase Increase a lot Increase Stay the same Decrease Decrease a lot Any decrease

73%

6%

66%

20%

7%

1%

7%

51%

7%

45%

22%24%

3%

27%

2013 2012

© Blue & Green Communications 14

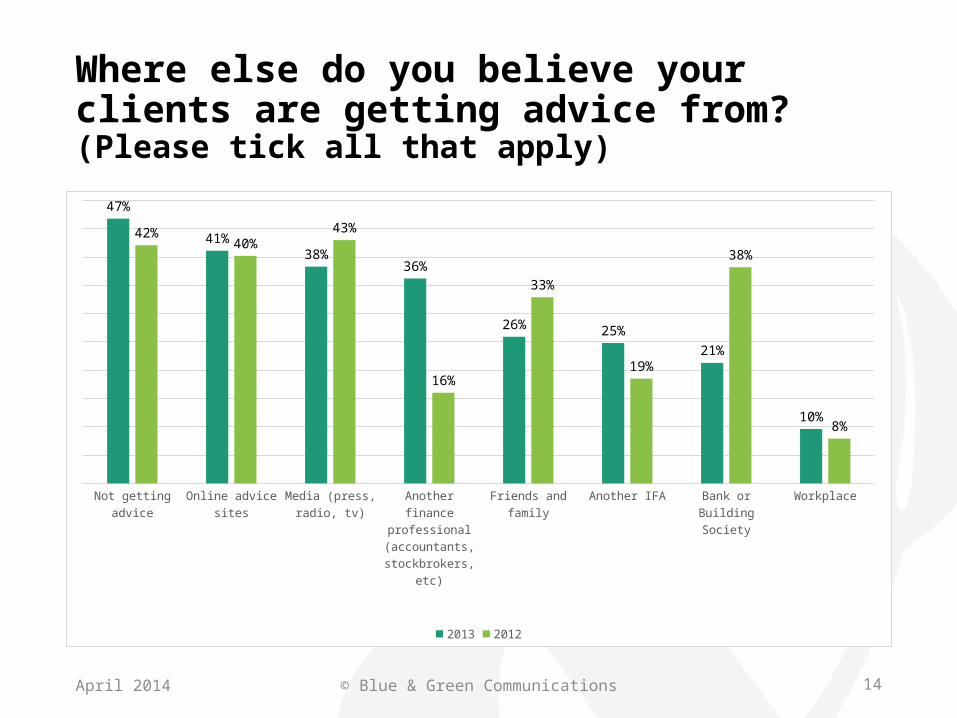

Where else do you believe your clients are getting advice from? (Please tick all that apply)

April 2014

Not getting advic

e

Online advic

e sites

Media (press,

radio, tv

)

Another finance

professional (a

ccountants,

stockb

rokers,

etc)

Friends a

nd family

Another IFA

Bank or B

uilding Socie

ty

Workp

lace

47%

41%38% 36%

26% 25%21%

10%

42% 40%43%

16%

33%

19%

38%

8%

2013 2012

© Blue & Green Communications 15

Do you see more or less advised clients turning to any of the following over the next 12 months?

April 2014

Direct purchase Restricted/tied advice Platforms

45%

29%

56%58%

31%

54%

6%

17%

6%5%

18%

7%

More 2013 More 2012 Less 2013 Less 2012

© Blue & Green Communications 16

On average, in the last 12 months are your clients requiring more or less advice/management/ planning from you?

April 2014

Any "More advice"

A lot more advice

More advice The same level of advice

Less advice A lot less advice Any "Less advice"

50%

4%

46%48%

2% 1%2%

50%

5%

46% 46%

3%1%

4%

2013 2012

© Blue & Green Communications 17

“We’re going to need more food in the next 40 years than has been produced in the last 8000.”

April 2014

Extraordinary Facts around Sustainability: # 2

© Blue & Green Communications 18

Retail Distribution Review

April 2014

© Blue & Green Communications 19

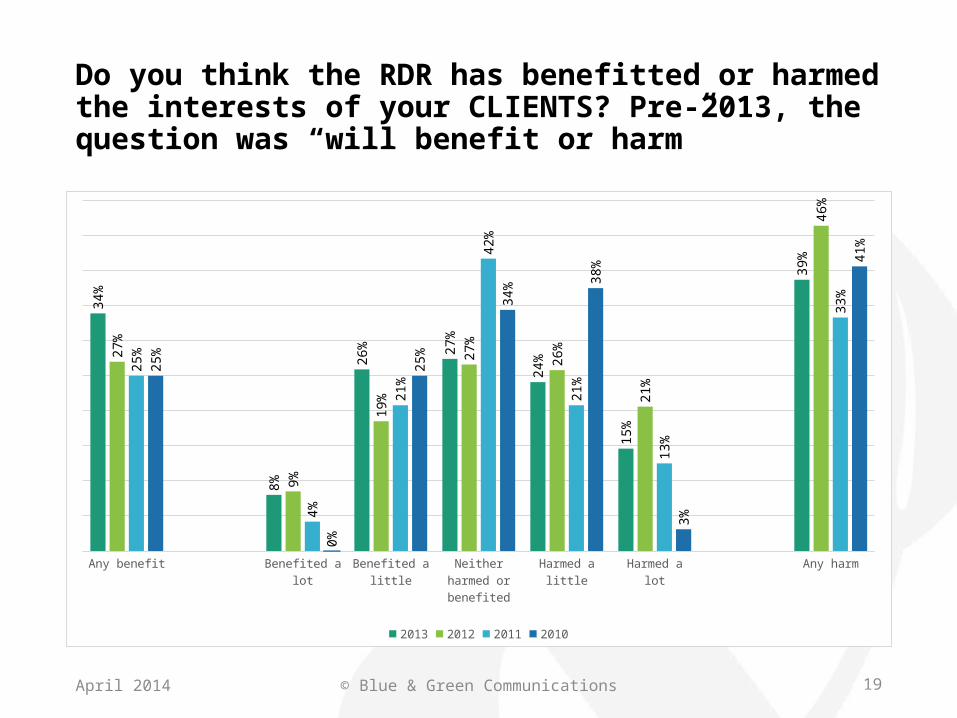

Do you think the RDR has benefitted or harmed the interests of your CLIENTS? Pre-2013, the question was “will benefit or harm”

April 2014

Any benefit Benefited a lot Benefited a little Neither harmed or benefited

Harmed a little Harmed a lot Any harm

34%

8%

26% 27

%

24%

15%

39%

27%

9%

19%

27%

26%

21%

46%

25%

4%

21%

42%

21%

13%

33%

25%

0%

25%

34%

38%

3%

41%

2013 2012 2011 2010

© Blue & Green Communications 20

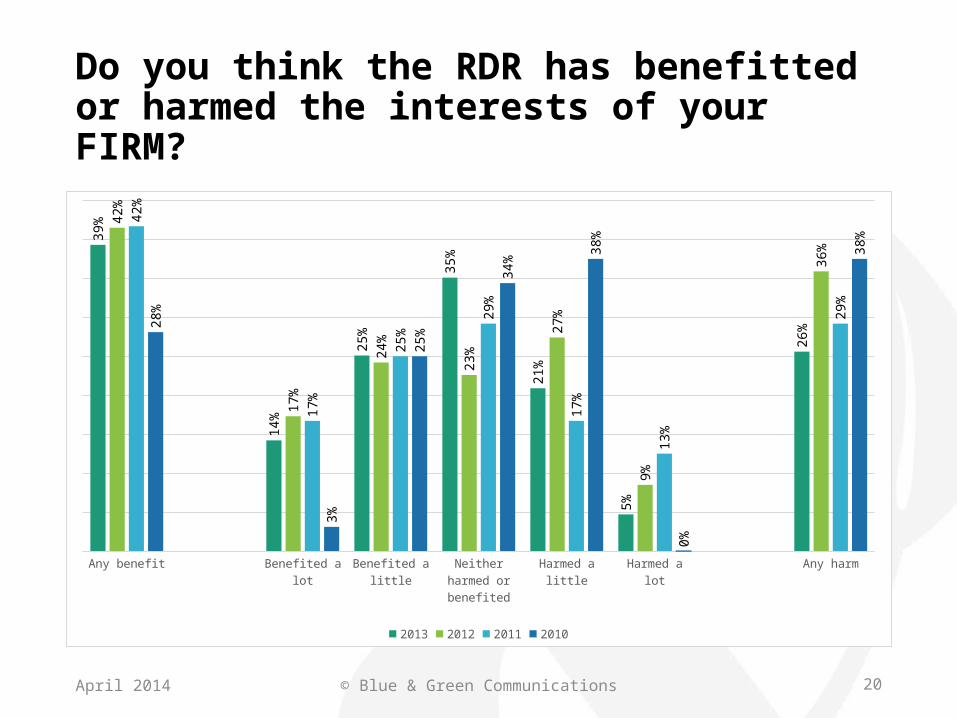

Do you think the RDR has benefitted or harmed the interests of your FIRM?

April 2014

Any benefit Benefited a lot Benefited a little Neither harmed or benefited

Harmed a little Harmed a lot Any harm

39%

14%

25%

35%

21%

5%

26%

42%

17%

24%

23%

27%

9%

36%

42%

17%

25%

29%

17%

13%

29%

28%

3%

25%

34%

38%

0%

38%

2013 2012 2011 2010

© Blue & Green Communications 21

Overall, has RDR been a success or failure in your experience?

April 2014

Any succe

ss

A succe

sss

Qualified su

ccess

Neither a

succe

ss nor a

failu

re

Qualified fa

ilure

A failu

re

Any failu

re

26%

9%

17%

45%

19%

10%

30%

2013

The biggest changes are seen as being greater transparency, increased professionalism for the industry but fewer clients served.

© Blue & Green Communications 22

“Half of all the carbon put into the atmosphere by mankind has been since 1973.”

April 2014

Extraordinary Facts around Sustainability: # 3

© Blue & Green Communications 23

Winning new clients

April 2014

© Blue & Green Communications 24

What is the SINGLE most important piece of information, other than their name and contact details, that you need from a prospective client to win their trust and business?

April 2014

Objective

s and goals

Attitude to ris

k

Family si

tuation

Wealth

Ethical p

erspecti

ves

Tax inform

ation

Investm

ent exp

erience Age

Income

74%

13%

7%3% 2% 1% 1% 1% 0%

© Blue & Green Communications 25

What percentage of your firm's income do you spend per annum on new client generation/marketing?

April 2014

Less than 10% 11-20% 21-30% 31%+

82%

15%

2% 1%

79%

17%

3%1%

79%

17%

4%0%

81%

16%

3%0%

2013 2012 2011 2010

© Blue & Green Communications 26

On average how much money (£s) would you invest to acquire a single new client

April 2014

2013 2012

559.60

508.53

312.66 303.96

246.93

204.57

Total Your time Advertising/marketing spend

© Blue & Green Communications 27

IFA spend based on 2013 growth segments

April 2014

Clients increased Clients stayed the same Clients decreased

1239.24

413.06

528.06

775.3

237.72

320.83

463.94

176.34207.22

Total Time Advertising & Marketing

© Blue & Green Communications 28

What methods do you mainly use to generate new clients?

April 2014

Yourethicalmoney.org

Email - bought list

Radio advertising

Direct mail - bought list

UK Sustainable Investment and Finance Association (UKSIF)

Worldwise Investor/Blue & Green Investor

Telemarketing - bought list

Ethical Investment Association (EIA)

External marketing agency

Telemarketing - own list

Press advertising

Direct mail - own list

Internal marketing team

MyLocalAdviser.co.uk

Exhibitions/conferences/events

Email - own list

Online marketing

Unbiased.co.uk

Worth of mouth/recommendation

0.0%

1.0%

1.0%

1.5%

2.0%

2.0%

2.5%

4.0%

7.1%

9.1%

10.6%

14.1%

15.2%

15.7%

17.7%

23.7%

25.3%

34.3%

83.8%

2013

© Blue & Green Communications 29

“Recent FAO analysis suggests that wasted food is the largest emitter of greenhouse gases – after the

US and Chinese economies.”

April 2014

Extraordinary Facts around Sustainability: # 4

© Blue & Green Communications 30

Sustainable, responsible and ethical investment

April 2014

© Blue & Green Communications 31

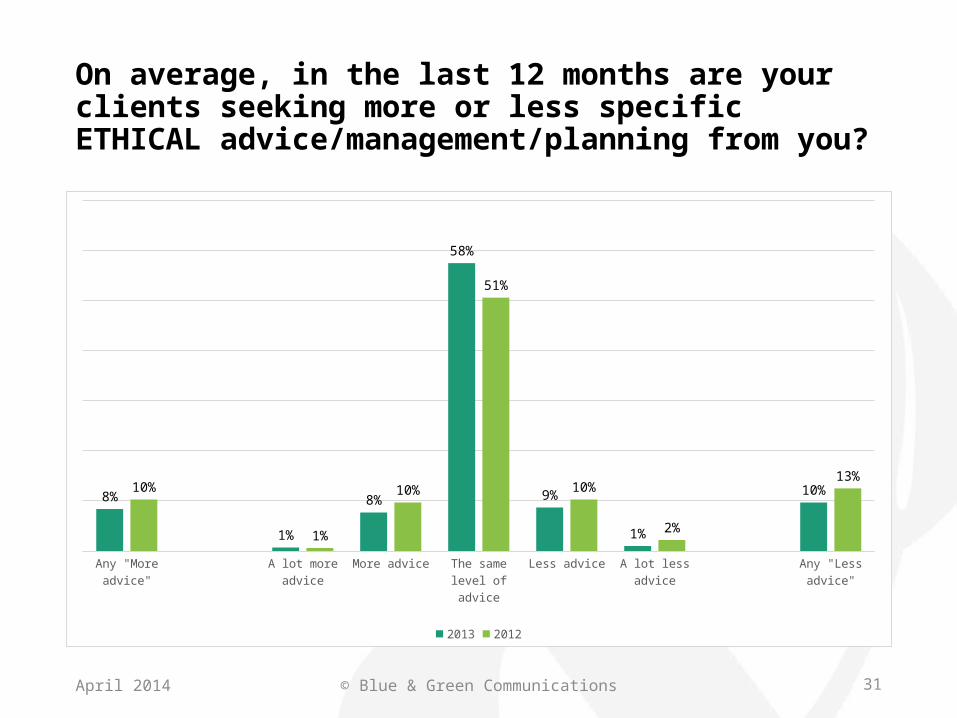

On average, in the last 12 months are your clients seeking more or less specific ETHICAL advice/management/planning from you?

April 2014

Any "More advice"

A lot more advice

More advice The same level of advice

Less advice A lot less advice Any "Less advice"

8%

1%

8%

57%

9%

1%

10%10%

1%

10%

51%

10%

2%

13%

2013 2012

© Blue & Green Communications 32

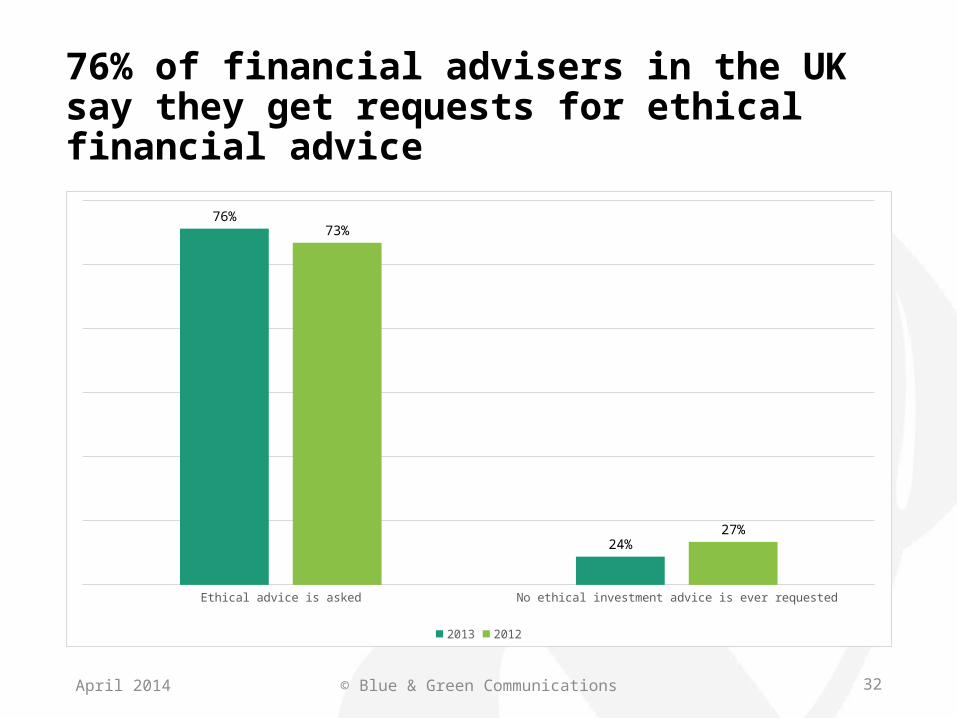

76% of financial advisers in the UK say they get requests for ethical financial advice

April 2014

Ethical advice is asked No ethical investment advice is ever requested

76%

24%

73%

27%

2013 2012

© Blue & Green Communications 33

Genetic engineering

Alcohol production

Poor relations with employees, customers or suppliers

Nuclear power generation

Gambling

Exploitation of animals for medicine

Poor environmental practices

Pornography or violent material

Exploitation of animals for cosmetics

Human rights abuses

Tobacco production

Manufacture or sale of weapons

7%

10%

10%

15%

18%

27%

32%

47%

48%

49%

60%

77%

Sector clients are MOST KEEN TO AVOID investing in?

Sectors clients are MOST KEEN to invest in?

Mass transportation

Sustainable travel/tourism

Organic food

Social enterprise/profit-for-purpose businesses

Biofuel

Water supply and treatment

Sustainable forestry

Sustainable agriculture and fishing

Recycling

Clean technology (non-energy)

Fair trade

Renewable energy

3%

4%

14%

21%

25%

30%

33%

34%

42%

48%

48%

78%

April 2014

© Blue & Green Communications

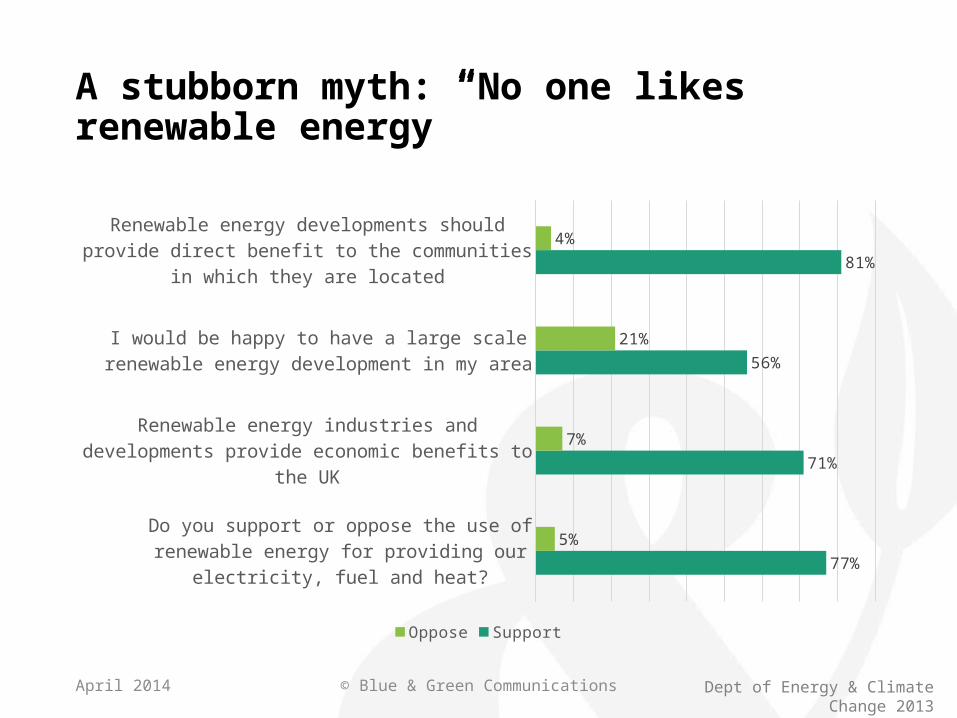

A stubborn myth: “No one likes renewable energy”

Do you support or oppose the use of renewable energy for providing our electricity, fuel and heat?

Renewable energy industries and developments provide economic benefits to the UK

I would be happy to have a large scale renewable energy development in my area

Renewable energy developments should provide direct benefit to the communities in which they are located

77%

71%

56%

81%

5%

7%

21%

4%

Oppose Support

April 2014 Dept of Energy & Climate Change 2013

© Blue & Green Communications 35

Which of these ethical fund providers do you use most often?

April 2014

Friends P

rovident S

tewardship

Ecclesia

stica

l

Aberdeen

Kames

Jupiter

Standard Life

Alliance

Trust

Rathbone

Aviva In

vesto

rsF&C

Henderson

42%

36%

32%

30%

28%

23%

18%

15%

14%

13%

12%

36%

31% 34

%

23%

31%

24%

12%

27%

25%

17%

2013 2012

© Blue & Green Communications 36

Biggest risers

2013 2012 Growth

Premier 5.1% 2.3% 122%

Quilter Cheviot 5.6% 3.3% 70%

Wheb AM 5.6% 3.3% 70%

Schroders 7.3% 5.1% 43%

Rathbone 15.3% 11.6% 32%

Kames 29.9% 23.3% 28%

Scottish Widows 7.9% 6.5% 22%

Friends Provident Stewardship 41.8% 35.8% 17%

Ecclesiastical 35.6% 30.7% 16%

April 2014

© Blue & Green Communications 37

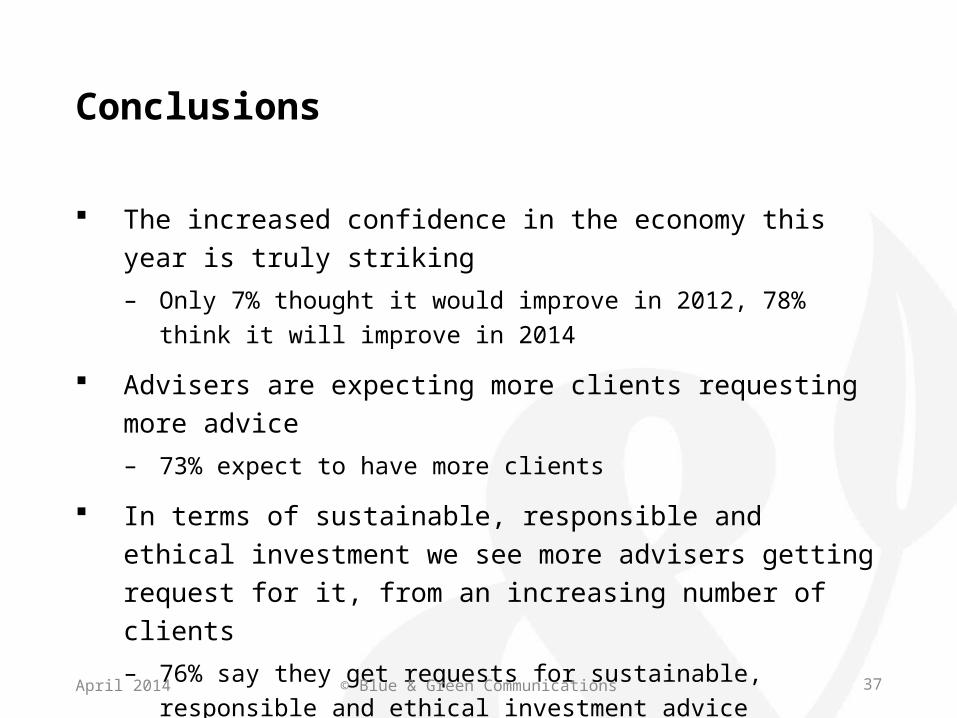

Conclusions

The increased confidence in the economy this year is truly striking– Only 7% thought it would improve in 2012, 78% think it will improve in

2014

Advisers are expecting more clients requesting more advice– 73% expect to have more clients

In terms of sustainable, responsible and ethical investment we see more advisers getting request for it, from an increasing number of clients– 76% say they get requests for sustainable, responsible and ethical

investment advice

April 2014

© Blue & Green Communications 38

”We do a lot of things for reasons besides profit motive.”

“We want to leave the world better than we found it.”

“When we work on making our devices accessible by the blind, I don’t consider the bloody ROI.”

“If you want me to do things only for [return on investment] reasons, you should get out of this stock.”

April 2014

Tim CookCEO - Apple

Final word

© Blue & Green Communications 39

Future Boot Camp Dates

22nd May: Liverpool

26th June: Edinburgh

16th September: London

23rd October: Birminghan

27th November: Bristol

April 2014