supply chain resilience - logistics quarterly

TRANSCRIPT

Yossi Sheffi, Ph.D.,Professor, Massachusetts Institute of Technology, Director of the MIT Center for Transportation and Logistics

David J. Closs, Ph.D.,John H. McConnell Chaired Professor of the Eli Broad College of Business, Department of Marketing and Supply Chain Management, Michigan State University and LQ Executive Editor

Jim Davidson,President, iWheels Dedicated Logistics

Dan French, MBA

Benjamin Gordon,Managing Director, BG Strategic Advisors

Robert Martichenko,President, LeanCor LLC

Dr. John T. (Tom) Mentzer, Ph.D.,is the Harry J. and Vivienne R. BruceChair of Excellence in Business Policy in the Department of Marketing, Logistics and Transportation at theUniversity of Tennessee

Christopher Norek, Ph.D.,Senior Partner, Chain Connectors, Inc.

Nicholas Seiersen,B.Sc.(Hons.), M.B.A., P.Log.,Senior Manager, KPMG, and LQExecutive Editor

Theodore Stank, Ph.D.,is the John H. Dove DistinguishedProfessor of Logistics and Head,Department of Marketing and Logistics at The University of Tennessee

The Official Magazine of The Logistics Institute

Volume 12, Issue 1, March 2006

PM

400

3260

2

Supply Chain ResilienceHow Can You Transcend Vulnerability In Your Supply Chain to Gain Competitive Advantage?

Eastern North America 877.253.5766 Western North America 888.453.5766

If you are looking for a reputable and reliable logistics partner that will moveyou to the next level of success, call Kelron Logistics today, or visit www.kelron.com

Kelron offers a comprehensive and personalized range of

logistics services throughout North America. Whether

you need transportation, warehousing and distribution,

freight management or logistics consulting, our

complete portfolio of customized and fully integrated

solutions are designed to increase your profitability.

Our core services are supported by a dedicated team of

logistics professionals, a unique and proprietary

Supplier Quality & Compliance Program, and advanced

technology that provides complete visibility throughout

the entire supply chain to give you and your customers

incredible value and the peace of mind you deserve.

Get the right products to the right marketsat the right time with Kelron Logistics.

Imagine the efficiency and cost savings you’ll realize throughgreater stock-turns, expanded product lines, increased

visibility, reduced inventory and faster order times...

5 Announcements 6 Contributors

8 Is It Time To Review Your Supply Chain Design?Substantial fuel price increases, coupled withincreases in driver pay, may prompt manyexecutives to consider a change in the number of North American distribution centers they use. Here’s an analysis that can

help you to evaluate where your firm stands.

12 Resilience Reduces RiskEconomic problems, political risks and environmental disasters can cause significantharm to companies investing in emergingmarkets and growing their global supplychains. This overview offers insights to

executives on how they can build supply chains that areresilient enough to withstand unexpected disruptions andhelp their organization to excel.

16 Transportation Management Trends: The Gathering Storm

The current environment shaping transporta-tion has often been likened to the perfectstorm. These trends threaten to turn our viewof transportation and logistics on its headunless major changes are forthcoming in the

near future. Here’s a look at the primary changes convergingon the industry and how they will help you act proactively.

19 Asian Emergence: The Brave New World of Logistics

Innovation was once viewed as the bastion of the United States. In 1790, GeorgeWashington authorized the first U.S. patent,granting Samuel Hopkins the right to a newmanufacturing method for potash. Today,

216 years later, a lot of manufacturing and innovation have gone west, from the United States to Asia. As a result, we are in the midst of a sea of change that is revolutionizing, not just the global economy, but also the logistics world. The implications for North American companies are monumental.

22 Inventory Reduction: The Path to SupplyChain Management (Commentary)Inventory is not only a critical part of supply chain management, it often obscures problems and inefficiencies that results in a painfully slow progression

toward genuine supply chain management. Here’s how to change that.

25 Procurement Solutions:A Guide to Help You Choose the Right Technology SolutionProcurement, know in the past as‘Purchasing’, was once viewed as an unglamorous back-office function. It

included negotiations with suppliers, procuring the parts and ensuring they were sent to the manufacturer of the products. Today, procurement’s status in the supply chainincludes a wide array of requirements, encompassing everything from determining client requirements, to a global sourcing strategy. Here is a look at how technology and its application can help improve your company’s growing procurement practice.

28 Spotting the TrendsIdentifying trends in today’s fast changing marketplace can help drive your company forward and ensure you make the most of your supply chain in global and domestic markets.

CONTENTSLQ™

3LQ™ March 2006LogisticsQuarterly.com

The Program

Where is the C Level Value in the Supply Chain?

Supply Chain Management for CFOs:Where's the Beef

Where is the Logistics Service Provider (LSP) Industry Going?

Sales and Operations Planning

Executive Speakers & Chairmen

APRIL 20, 2006 Toronto Board of Trade, 830 Dixon Road

FOR MORE INFORMATION www.logisticsquarterly.comor Fred Moody 416-461-8355 Seating is limited.

LQ’s Executive Exchange is design to provide applied and tangible insights into leadership in logistics and supply chain management strategies in today’s global economy.

LQ’s North American Leadership in Logistics Symposium

Platinum Sponsor

Richard Armstrong, Co-editor and Publisher ofWho’s Who In Logistics, President of Armstrong & Associates

Rick Blasgen, President and CEO of the Council of Supply Chain Management Professionals (CSCMP)

David J. Closs, LQ Executive Editor, and the John H. McConnell Chaired Professor of the Eli Broad College of Business, Department of

Marketing and Supply Chain management, Michigan State University

Jim Davidson, President, iWheels Dedicated Logistics

Victor Deyglio, Executive Editor,and President and CEO of The Logistics Institute

John Ferguson, General Manager of Canadian Operations,Schneider National Inc.

Susan Gadsby, C.P.P. C.P.M., Director, Procurement, Apotex Inc.

Joe Gallick, Senior Vice President, Sales, Penske Logistics

Claude Germain, Executive Vice President & COO,Schenker of Canada Limited

Tom Goldsby, Ph.D., University of Kentucky

Benjamin Gordon, Managing Director ofBG Strategic Advisors

David Griffith, Vice President, Global Supply Chain Management, BAX Global

Dipan Karumsi, Project Manager,Supply Chain Consultant, IBM

Gene Long, President of UPS SCS Consulting Services

Charles (Chuck) Lounsbury, former Senior Vice President of Strategy, Marketing & Acquisitions of Ryder System, Inc.

Jason Reiman, Director of Demand Planning, Hershey

Kurt Ritcey, Partner, Deloitte

Nick Seiersen, Senior Manager, KPMG

Walter Zinn, Ph.D., Ohio State University

“The LQ Executive Exchangewas a pleasure to attend. I met interesting people and I feel that the Exchangewas very well organized. I guess I should expect nothing less of a group ofprofessional logisticians.”

Walter Zinn, Ph.D.,Ohio State University

“I was impressed by the lineup of speakers and the caliber of those in attendance. Great job.”

John Langley Jr., Ph.D.,Georgia Institute of Technology

Gold Sponsors

5LQ™ March 2006LogisticsQuarterly.com

LQ™ ADVISORY BOARDDavid J. Closs, Ph.D.Department of Marketing and Supply Chain Management,Michigan State UniversityExecutive Editor, LQKaren CooperSenior Media Relations Specialist,FedEx Canada Ltd.Jim DavidsonPresident,iWheels Dedicated LogisticsBruce DanielsonExecutive Communications Manager,UPSRuss DixonSenior Manager,TNT Logistics North AmericaRuss J. DoakDirector, Global Logistics, Kodak Graphics & Communications.David FaoroDirector, Supply Chain The International Group, Inc.John FirminoVice President, Director Solutions andExecution Standards, Ryder CanadaSue Gadsby, C.P.P. C.P.M.,Director, Procurement, Apotex Inc.Benjamin GordonManaging Director, BG Strategic AdvisorsThomas J. Goldsby, Ph.D.Associate Professor,Supply Chain Management,University of KentuckyDavid GriffithVP Global Supply Chain Management,BAX GlobalJoe GrubicSenior Manager, Alliance/Network Management, Nortel Networks Global LogisticsGeorge KuhnExecutive Director,CIFFARobert MartichenkoPresident,LeanCorJames MahoneyStrategic Business DevelopmentExecutive,GeoLogistics CorporationJeff MooreManaging Director,Lakeside Logistics Inc.Mark Morrison, Senior Vice President of Business Development, TNT North AmericaTom NightingaleVice President, Corporate Marketing, Schneider National, Inc.Christopher Norek, Ph.D.Senior Partner, Chain Connectors, Inc.Peruvemba S. RaviAssistant Professor,Wilfrid Laurier UniversityKurt M. RitceyPartner, Deloitte Consulting Nicholas SeiersenSenior Manager, KPMGExecutive Editor, LQMichael SneddenManager of Distribution Operations, IBM-Canada Ltd.Diane MollenkopfAssistant Professor, Marketing and Logistics, University of Tennessee.

Volume 12 Issue 1

PUBLISHER & EDITORFred [email protected]

CPLI PRESIDENT & EDITORIAL DIRECTORVictor [email protected]

CREATIVE DIRECTORCraig [email protected]

WEB DESIGNER & COPY EDITORBeylah [email protected]

ADVERTISING SALESJeanette PolenychoMarketing and Sales [email protected] MartichenkoU.S. Marketing [email protected]

CIRCULATION & WEBSITE DEVELOPMENTBill [email protected]

ACCOUNTINGChristine Raffan, CGA Independant [email protected]

LQ™2 Bloor Street W., Suite 100, Box 473, Toronto, Ontario, M4W 3E2,Telephone: (416) 461-8355Toll Free: 1-800-843-1687Fax: (416) 465-7832 Email: [email protected]

Logistics Quarterly (LQ™) (ISSN 1488-3309) is published six times annually by LQ™ Inc. LQ™ is written for professionals in logistics. Subscription Services at: www.LogisticsQuarterly.comCanada Post Publications Mail Sales Agreement Number: 40032602. CANADIAN POSTMASTER: send subscription orders, address change notices and undeliverable copies to LQ™, 2 Bloor Street West, Suite 100, Box 473, Toronto, Ontario, Canada M4W 3E2

EDITORIAL POLICYThe opinions expressed in this publication do not necessarily reflect the policy of The Logistics Institute or LQ™ Inc. The editors reserve the right to select and edit material submitted for publication. Not responsible for unsolicited material. LQ™ Inc. is a Toronto-based corporation and publisher. All rights reserved © by LQ™ Inc. 2005. Reproduction without written permission of the publisher is forbidden. LQ™ welcomes your comments, letters to the editor, or written submissions for consideration.(LQ™ is available on-line at:www.LogisticsQuarterly.com)

LQ MAGAZINE’S STATEMENT OF OWNERSHIP The trademark LQ™, LQ Magazine (ISSN 1488-3309), LQ Newsletters and theLQ Conference, including the “ExecutiveExchange,” its trade marks and publishedmaterial are wholly owned by LQ Inc., a private Canadian family-owned and operatedcorporation. LQ’s valued sponsors are independent of LQ Inc., and LQ’s editors dotheir utmost to uphold independent andimpartial views in all of their publishing initiatives.

We are honored to announce thefollowing new participants haveaccepted LQ’s invitation to join itsAdvisory Board: SUE GADSBY, C.P.P. C.P.M., is Director, Procurement,Apotex Inc. Ms. Gadsby has more than 20 yearsexperience in supply and logistics managementand more than 10 years experience in travel man-agement in various manufacturing and distributionenvironments. She specializes in re-engineeringpurchasing functions into a strategic resourcewithin organizations. Prior to joining Apotex, shehad similar responsibilities for Bayer Inc., whereshe reshaped the organization, along with the pur-chasing practices and supplier relationships. Ms.Gadsby has been on global teams to develop andimplement best practices in the area of procure-ment, has been an active member on variousindustry advisory boards, featured in leading pur-chasing, legal and travel management publications,and lecturers in public forums in the area of pro-curement, bid law, and travel management. ApotexInc., a global organization, is the largest privatelyowned pharmaceutical company in Canada,employing over 4,000.

DIANE MOLLENKOPF is an Assistant Professor,Marketing and Logistics, University of Tennessee.Before joining the University of Tennessee, Ms.Mollenkopf served as assistant professor of mar-keting and supply chain management at MichiganState University. Prior to that, she was a senior lec-turer in marketing and distribution at LincolnUniversity in Canterbury, New Zealand. She alsowas an award-winning instructor and teachingassistant at Drexel University in Philadelphia,where she earned her doctorate in marketingchannels with an emphasis in international busi-ness. Ms. Mollenkopf pursued her Ph.D. afterworking at Avon Products, Inc., where her improve-ments to Avon’s dispatch and return-products sys-tems at the Newark, DE distribution center nettedthe company significant annual savings. Later,working for Yves Rocher, Inc., she managed thelogistics operations for the start-up of its U.S. sub-sidiary. She was responsible for liaising with theEuropean factories and managing internationaltransportation for all products sold in the UnitedStates. She also helped launch the company’smulti-million-dollar, home-shopping operations.Currently, Ms. Mollenkopf is focusing her researchefforts in two main areas: strategic logistics inte-gration and environmentally responsible logisticspractices, including reverse logistics. She teachesboth undergraduate and graduate level courses.

Hans-Jörg Hager and JosephCarnes Join SchenkerManagement Board HANS-JÖRG HAGER, Chairman of the ManagementBoard of Schenker Deutschland AG, and Joseph L.Carnes, President of BAX Global Inc., have

recently joined the Management Board ofSchenker AG, Essen. On the Schenker Manage-ment Board, Mr. Hager represents the company’sLand Transport business unit, and Mr. Carnesrepresents the American logistics service compa-ny BAX Global, which Deutsche Bahn AG acquiredon Jan. 31 this year.

The Management Board ofSchenker AG now includes the following members:• Joseph L. Carnes, BAX Global

• Hans-Jörg Hager, Land Transport

• Dr. Thomas C. Lieb, Air and Sea Freight

• Dr. Marco Schröter, Finance

• Peter Schumann, IT Management

• Dr. Detlef Trefzger, Logistics

• Steffen W. Wurst, Human Resources.

With its four business units – Schenker, StinnesFreight Logistics, Stinnes Intermodal and Railion –DB Logistics, the Transportation and LogisticsDivision of Deutsche Bahn, combines logisticscompetence with rail know-how in the fields ofland transportation, air and sea freight, as well asglobal supply chain management. With a sales vol-ume of 12.4 billion euros, a workforce of 65,000employees and more than 1,100 locations in 110different countries, DB Logistics is one of theleading transportation and logistics serviceproviders worldwide.

John Kincheloe, is Named NewAmericas Senior VP, Sales &Marketing at GeoLogisticsGeoLogistics Corporation has named JohnKincheloe as its new Senior Vice President,Sales and Marketing, Americas. Mr. Kincheloejoins GeoLogistics from EGL, where he heldseveral leadership roles, including VicePresident, Northeast Region, responsible forall management and operations. Prior to EGL,he was with Emery for over 21 years in a varietyof sales and management positions. Mostrecently, he was Vice President, South Asia,based in Singapore. Mr. Kincheloe reportsdirectly to Alex Leivici, GeoLogistics’ ChiefExecutive Officer, Americas. He will be basedin the company's Santa Ana, California corpo-rate office. Mr. Kincheloe is a graduate ofPortland State University, Portland, Ore.

GeoLogistics Corporation is a leading globallogistics provider with a global network spanningmore than 100 countries. GeoLogistics offers cus-tomers a broad range of freight management andcustomized logistics solutions backed by a single,company-wide IT system. GeoLogistics is part ofthe PWC Logistics family, an organization withannual revenues of over U.S.$3 billion and 17,000employees.

ANNOUNCEMENTS

LogisticsQuarterly.com6 LQ™ March 2006

MARCH CONTRIBUTORS

LQ’s mandate to provide “Ideas for Leadership in Logistics,” is clearly evidenced thisissue with articles written by professionals and logisticians from America and Canada who are leading and transforming

business by creating new roadmaps and definitions for leadership in this exciting field.

OUR CONTRIBUTORS

DAVID J. CLOSS, Ph.D, LQ ExecutiveEditor: Dr. Closs is the John H.McConnell Chaired Professor of the EliBroad College of Business, Departmentof Marketing and Supply Chain manage-ment, Michigan State University. He hasconsulted with more than 100 of theworld’s Fortune 500 corporations regard-ing logistics strategies and systems. He isan active member of the Council of theSupply Chain Management professionals.

JIM DAVIDSON, President, iWheels dedi-cated Logistics, began his career in logis-tics at The Ford Motor Company in 1963working in all aspects of logistics for 17years. Mr. Davidson joined TNT in 1983and held various management roles,including roles in operations, staff,administration and general managementfor a number of different divisions. Healso served as the TNT board memberrepresenting North America at theirEuropean-based board meetings. He hasserved on the executive of the CanadianGeneral Motors Supplier Council as wellas Executive Vice President of the ATACouncil of Logistics located inAlexandria, Va.

DONAVON FAVRE is an Assistant Profes-sor of Supply Chain Management in theCollege of Management at NorthCarolina State University. Prior to that,he was a managing partner ofAccenture’s Global Sourcing and Pro-curement consulting practice where heconsulted to companies including Pepsi,Corning, ExxonMobil, Scholastic, andDeutsche Bank.. Mr. Favre serves on theadvisory board for Emptoris (eSourcingsoftware company). He also worked forWestinghouse prior to his consultingcareer. Mr. Favre has a B.S. in Industrialand Systems Engineering and an M.A. inOperations Management from The OhioState University.

DAN FRENCH is a graduate student in theMBA Program at the Broad GraduateSchool of Management at Michigan StateUniversity. Prior to returning to businessschool, Mr. French was a Manager withAccenture.

BENJAMIN GORDON is Managing Direc-tor of BG Strategic Advisors, a Boston-based consulting firm providing supplychain companies with CEO-level advisoryservices in the areas of strategy, technologyand finance. Mr. Gordon is responsible forleading key client engagements and settingthe direction of the firm. Prior to BGStrategic Advisors, he founded 3PLex, theInternet solution enabling third-party logis-tics companies to automate their business.Mr. Gordon received a Masters in Businessadministration from Harvard BusinessSchool and a Bachelor of Arts degree fromYale College.

ROBERT MARTICHENKO is President ofLeanCor LLC. Headquartered in Florence,Kentucky, LeanCor delivers logistics andsupply chain management services to com-panies embracing Lean manufacturing andSix Sigma. Mr. Martichenko is a student ofLogistics, Lean and Six Sigma, has pub-lished in several industry journals and con-tributed the chapter on “Lean Six SigmaLogistics” in Michael George’s book “LeanSix Sigma.” Mr. Martichenko holds aBachelor Degree in Mathematics from theUniversity of Windsor and an MBA inFinance from Baker College. Mr.Martichenko is involved with the Councilof Supply Chain Management Profession-als (CSCMP), the Lean Enterprise Institute,the Supply Chain Consortium at SaintLouis University, and LQ Magazine.

DR. JOHN T. (TOM) MENTZER, Ph.D., isthe Harry J. and Vivienne R. Bruce Chair ofExcellence in Business Policy in theDepartment of Marketing, Logistics andTransportation at the University of Ten-nessee. He has written more than 160papers and articles, and five books. Hisresearch has focused on the contributionof marketing and logistics to customer sat-isfaction and strategic advantage; theapplication of computer decision modelsto marketing, logistics, and forecasting;and the management of the sales forecast-ing function. He serves on the editorialreview boards of five journals and as occa-sional reviewer for six others. He presentlyserves on the Executive Committee and is

Immediate Past President of the Council ofLogistics Management. He was formerlyPresident of the Academy of MarketingScience and is a Distinguished Fellow of theAcademy of Marketing Science. He hasserved as a consultant for over seventy cor-porations and government agencies, is onthe boards of directors of several corpora-tions, and previously worked for GeneralMotors Corporation.

CHRISTOPHER D. NOREK, Ph.D. is afounding Senior Partner with Chain con-nectors, Inc., an Atlanta-based supplychain consulting firm specializing in strate-gy, technology, transportation operations,returns management and supply chaintraining. He has been in the logistics fieldfor over 15 years both in industry withAccenture, Kimberly-Clark, Apple comput-er, and CSC as well as a professor at bothAuburn University and the University ofTennessee. Mr. Norek has consulted forfirms including SAP, amazon.com, accen-ture, Office Depot, Cingular Wireless, TheSports Authority, Party City, and AramarkUniform Services. He has been active inpublishing for journals in the field andspeaking for many organizations and uni-versity executive development programsincluding the Council of Logistics manage-ment, NASSTRAC, Georgia institute ofTechnology, University of Tennessee, uni-versity of North Florida, and University ofLouisville. He holds logistics degrees fromPenn State, Tennessee, and Ohio State.

NICHOLAS SEIERSEN, B.Sc.(Hons.),M.B.A., P.Log. LQ Executive Editor: Mr.Seiersen is a Senior Manager with KPMG,based in Toronto, Ontario. He specializesin Supply Chain consulting, with particu-lar attention to Strategic Sourcing andSupply Chain Planning & Operations. Mr.Seiersen holds a B.Sc. (hons.) inBiochemistry and an M.B.A. in IndustrialManagement. He teaches executive devel-opment courses at top universities inEurope and North America. He has writ-ten for numerous publications in NorthAmerica and Europe on ePurchasing,Logistics, Supply Chain Management andCost-to-Serve. He is the past President of

LogisticsQuarterly.com 7LQ™ March 2006

the Toronto Roundtable of the Council ofLogistics Management, (now CSCMP),Vice President of the French Logisticsassociation (ASLOG), and a member ofthe European Logistics Association Busi-ness Management committee.

YOSSI SHEFFI, Ph.D., is a professor at theMassachusetts Institute of Technology,where he serves as Director of the MITCenter for Transportation and Logistics.He is an expert in systems optimization,risk analysis and supply chain manage-ment, which are the subjects he researchesand teaches at MIT, both at the MITSchool of Engineering and at the SloanSchool of Management. He is the authorof dozens of scientific publications andtwo books: a textbook on transportationnetworks optimization and the recentlypublished The Resilient Enterprise: Over-coming Vulnerability for CompetitiveAdvantage (MIT Press, October 2005).Under his leadership, the Center launchedmany new educational, research, andindustry/government outreach programs,leading to substantial growth. He is thedirector of MIT’s Master of Engineering inLogistics degree which he founded andlaunched in 1998. In 2003 he launched theMIT-Zaragoza program, building a newlogistics university in Spain based on aunique international academia, govern-ment and industry partnership. Outsidethe university Professor Sheffi has consult-ed with numerous government agencies aswell as leading manufacturing, retail andtransportation enterprises all over theworld. He is also an active entrepreneur,having founded five successful companies,and a sought-after speaker in corporateand professional events. Dr. Sheffi wasrecognized in numerous ways in academicand industry forums and was on the coverof Purchasing Magazine and Transporta-tion and Distribution Magazine. In 1997 hewon the Distinguished Service Award givenby the Council of Supply Chain Manage-ment Professionals. In 2002/03 he was onsabbatical in the Judge Institute of Man-agement in Cambridge University, UK. Heis also a life fellow of Cambridge Universi-ty’s Clare Hall College. He obtained hisB.Sc. from the Technion in Israel in 1975,his S.M. from MIT in 1977, and Ph.D. fromMIT in 1978. He now resides in Boston,Massachusetts.

THEODORE P. STANK, Ph.D., is the JohnH. Dove Distinguished Professor ofLogistics and Head, Department ofMarketing and Logistics at The Universityof Tennessee. Prior to arriving at UT, hetaught at Michigan State University, IowaState University, and the University of Texasat El Paso. He holds a Ph.D. in Marketingand Distribution from The University of

Georgia, an M.A. in Business Administra-tion from Webster University, and a B.S.from the United States Naval Academy. Dr.Stank’s business background includes salesand marketing experience as an employeeof Abbott Laboratories Diagnostic Division.He served as a Surface Warfare Officer inthe United States Navy prior to his industryand academic experience. He has also per-formed consulting and executive educationservices for numerous manufacturing andlogistics firms. He is an active member of theCouncil of Logistics Management. His

research interests focus on the strategicimplications and performance benefitsassociated with integrated logistics and sup-ply chain management concepts, specifical-ly related to logistics integration, communi-cations and information exchange, out-sourcing, and operational flexibility/respon-siveness. He is a co-author of 21st CenturyLogistics: Making Supply Chain Integrationa Reality, has published over 55 articles inacademic and professional journals, andhas received numerous awards for outstand-ing teaching.

EDITORIAL

In a recent class, while discussing sup-ply chain design and distribution centerlocation, a student asked if the recentrun up in diesel prices will have anyimpact on the optimum number of dis-tribution centers. I replied that the pre-cise answer depends on the specificfirm’s transportation characteristics, butwe may be able to determine theapproximate sensitivity using somegeneric data. Specifically, the questionis: Do the current increases in the priceof diesel fuel suggest a need to re-evalu-ate the number and location of a firm’sdistribution centers?

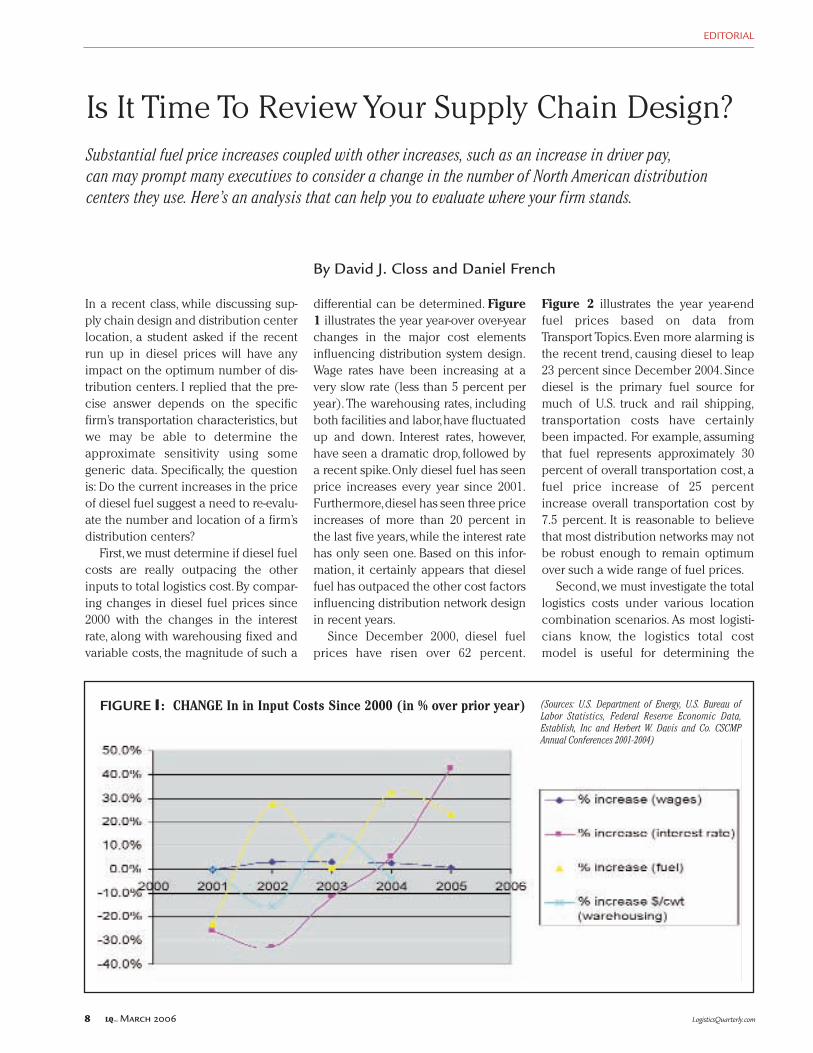

First,we must determine if diesel fuelcosts are really outpacing the otherinputs to total logistics cost.By compar-ing changes in diesel fuel prices since2000 with the changes in the interestrate, along with warehousing fixed andvariable costs, the magnitude of such a

differential can be determined. Figure1 illustrates the year year-over over-yearchanges in the major cost elementsinfluencing distribution system design.Wage rates have been increasing at avery slow rate (less than 5 percent peryear). The warehousing rates, includingboth facilities and labor,have fluctuatedup and down. Interest rates, however,have seen a dramatic drop, followed bya recent spike.Only diesel fuel has seenprice increases every year since 2001.Furthermore,diesel has seen three priceincreases of more than 20 percent inthe last five years, while the interest ratehas only seen one. Based on this infor-mation, it certainly appears that dieselfuel has outpaced the other cost factorsinfluencing distribution network designin recent years.

Since December 2000, diesel fuelprices have risen over 62 percent.

Figure 2 illustrates the year year-endfuel prices based on data fromTransport Topics.Even more alarming isthe recent trend, causing diesel to leap23 percent since December 2004. Sincediesel is the primary fuel source formuch of U.S. truck and rail shipping,transportation costs have certainlybeen impacted. For example, assumingthat fuel represents approximately 30percent of overall transportation cost, afuel price increase of 25 percentincrease overall transportation cost by7.5 percent. It is reasonable to believethat most distribution networks may notbe robust enough to remain optimumover such a wide range of fuel prices.

Second, we must investigate the totallogistics costs under various locationcombination scenarios. As most logisti-cians know, the logistics total costmodel is useful for determining the

By David J. Closs and Daniel French

Is It Time To Review Your Supply Chain Design?Substantial fuel price increases coupled with other increases, such as an increase in driver pay, can may prompt many executives to consider a change in the number of North American distribution centers they use. Here’s an analysis that can help you to evaluate where your firm stands.

LogisticsQuarterly.com8 LQ™ March 2006

FIGURE 1: CHANGE In in Input Costs Since 2000 (in % over prior year) (Sources: U.S. Department of Energy, U.S. Bureau ofLabor Statistics, Federal Reserve Economic Data,Establish, Inc and Herbert W. Davis and Co. CSCMPAnnual Conferences 2001-2004)

9LQ™ March 2006LogisticsQuarterly.com

optimal number of distribution centersfor a geographic area such as NorthAmerica. The trade-offs used in themodel include transportation to andfrom distribution centers, inventory car-rying cost, and fixed and variable facili-ty costs. However, due to their relativemagnitude, transportation and invento-ry carrying cost are the major drivers,having the largest impact.

The hypothesis is that distribution net-work design will be sensitive to 25-40 per-cent increases in diesel fuel prices. Totest the hypothesis, we used LogicNet6.1™ modeling and optimization soft-ware produced by Logic Tools, Inc. Weused the “Metal Works Case”which is oneof the standard examples and replicatesthe distribution network for a durableproduct with two plants, 11 productgroups, and a combination of truckloadand LTL (less than truckload) deliveries.Using the optimizer, we successivelyidentified the total cost curve at a baselevel,and then increased the fuel cost by25, 50, and 100 percent respectively.Assuming that 30 percent of transportcost is related to fuel, these fuel costincreases resulted in 7.5, 15, and 30 per-cent increases in overall transport cost.The simulation results contain represen-tative values for transportation,inventorycarrying as well as,facility fixed and vari-able cost. Table 1 summarizes the total(non-production related) costs for arange of distribution centers for eachfuel cost scenario. The minimum cost

Base Fuel 25 % Fuel 50% Fuel 100% Fuel Price Price Increase Price Increase Price

Increase Increase Increase

Albany AlbanyChattanooga Chattanooga Chattanooga ChattanoogaDallas Dallas Dallas DallasDes Moines Des Moines Des Moines Des MoinesDover Dover Dover Dover

Indianapolis IndianapolisOrlando Orlando Orlando OrlandoPhoenix Phoenix Phoenix Phoenix

Portland PortlandSacramento Sacramento Sacramento Sacramento

TABLE 2: Location Of of Distribution Centers By by Fuel Price

Base Fuel 25 % Fuel 50% Fuel 100% Fuel Price Price Price Price

Increase Increase Increase

$ 44,744 $ 46,620 $ 47,734$ 44,373 $ 46,514 $ 47,174 $ 50,037$ 44,268 $ 46,293 $ 46,916 $ 49,567$ 44,340 $ 46,323 $ 46,775 $ 49,172$ 44,431 $ 46,688 $ 46,721 $ 48,966$ 44,475 $ 46,725 $ 46,649 $ 48,751

$ 47,041 $ 49,024

Number of Distribution Centers

567891011

TABLE 1: Optimal Number Of of Distribution Centers By by Fuel Price(Non-production costs in 000 USD)

FIGURE 2: U.S. Diesel Fuel Prices Since 2000 (in USD per gallon)(Source:U.S. Department of Energy)

LogisticsQuarterly.com10 LQ™ March 2006

number of distribution centers is illus-trated by the bordered cell. Table 2 illus-trates the particular distribution centerlocations in each network.

The results illustrate the impact offuel price increases. In the base case,the optimum number of distributioncenters is seven.A fuel price increase of25 percent (i.e.,an overall transport costincrease of 7.5 percent) results in nochange in the optimum number of dis-tribution centers; however, it is veryclose to shifting to an optimum of eightdistribution centers. A fuel increase of50 or 100 percent increases the opti-mum number of distribution centers toten. In particular, the optimization sug-gests that distribution centers should beopened in New England (Albany),Northwest (Portland), and a secondfacility in the Midwest (Indianapolis).

Although these results should not begeneralized, particularly across firmsthat have unique transportation charac-teristics, they do suggest that optimumdistribution system design is sensitive tothe fuel price increases that we haveseen over the past year.Nevertheless,the

25 percent increase is not enough toforce a change. Above the 25 percentlevel, however, it appears that the opti-mum number increases by one distribu-tion center for each 25 percent increasein fuel cost. Hopefully, we don’t see fuelprice increase of that magnitude for along time.

These results indicate the relativesensitivity of the number of distributioncenters to fuel prices. So now I can tellmy student that even with the 25 per-cent increases in fuel over the last year,there should not be any major impacton the number or location of distribu-tion centers.This is undoubtedly due tothe fact that 25 per increase in fuelyields a relatively minor (7.5 percent)impact on transport rates. However, a25 percent increase in fuel in conjunc-tion with a 25 percent increase in driv-er pay (due to the shortage of drivers)would yield a 15 percent increase intransport rates and would have thesame result as a 50 increase in fuel.Under this potential scenario (which isreasonably likely), this analysis suggeststhat a change in the number of distribu-

tion centers would be recommended.In summary, these results suggest that

the combination of fuel price increasesand driver wage increases could havesome impact on the optimum numberand possibly the location of distributioncenters to serve North America.However, the impact of the change ontotal cost may not be particularly signif-icant given the other cost components.Specifically, at the 100 percent fuelincrease level, the total (non-produc-tion) cost for seven distribution centersis (U.S.) $49,567 USD while the cost atthe optimum number of distributioncenters is $48,751 USD. The resultingchange in non-production costs are isonly 1.7 percent, which is probably notsubstantial enough to justify significantchange. So, for my students and themanagers who have wondered regard-ing the nature of the impact, 25 to 50percent increases in fuel prices anddriver wages certainly makes andimpact on the total cost but it may notbe enough to justify substantial designchanges and the required efforts tomake the changes.

3PL Summit4th

June 26-28, 2006 InterContinental Buckhead, Atlanta, Georgia, USA

Take part in the Summit that helps you define your business priorities for the next 12 months

VISIT WWW.EYEFORTRANSPORT.COM/3PL FOR FURTHER INFORMATION OR CALL 1 800 814 3459

Pre-Summit Workshops June 26

1: Performance Metrics & PricingStrategies

2: Contract Negotiations

Two open debates for 3PLs and customers.Come and learn how others formulate theirpricing policies. Can you save – or makemoney? Plus top tips and techniques that

guarantee successful, win-win contract outcomes. Your chance to ask questions

and make your voice heard.

Network with over 500 senior logistics executives

Get 2 events for the price of 1!

4th eyefortransport 3PL Summit+

2nd Outsourcing Logistics Conference

The 3PL Summit is co-located withOutsourcing Logistics – which will

attract 150+ 3PL customers as delegates. To maximize your business opportunities,

all networking events, lunches and some Summit sessions will be shared

with these major customers.

NEW!

Cutting edge insights from 3PL industry leaders, major customers and world-renowned experts and analysts:

• Hear fascinating customer comments – and learn how to gain extra business

• Evaluate new sales strategies that can significantly boost your profits

• Learn how to overcome the challenge of high cost and low return on your IT investments

• Best practice to profit from booming low-cost markets such as China, India – and otheremerging territories

• Find out about the next phase of 3PL consolidation – and how it will affect your business

• Discuss employee issues, customer selectivity, continuing downward pressure on prices – and much more

To see the full list of speakers and to download the program please go to www.eyefortransport.com/3pl/brochure.shtml

THE WORLD’S NO. 1 MEETING PLACE FOR SENIOR 3PL EXECUTIVESAND COMPANIES WHO OUTSOURCE TO 3PLS

NEW!

LQ advert 6/2/06 2:46 pm Page 1

YOU NAME IT

We’ll Customize A Supply Chain Solution For ItWherever you manufacture, however you store inventory and distribute products, Ryder designs and operatesend-to-end supply chain solutions that deliver a competitive advantage for businesses like yours. Unmatchedexperience, flexibility and expertise make Ryder the company that other companies rely on around the globe. So, if youwant to maximize efficiency, enhance visibility and improve customer satisfaction, just name it, and we'll get it done.Call 1-888-88-RYDER or visit www.ryder.com.

S U P P L Y C H A I N , W A R E H O U S I N G & T R A N S P O R T A T I O N S O L U T I O N S

©2005 Ryder System, Inc. All rights reserved.

RTR-983 Laptop_Log.Quarterly Ad ƒ 9/14/05 4:32 PM Page 1

Resilience Reduces Risk How can enterprises build supply chains that

are resilient enough to withstand unexpecteddisruptions and help the organization to excel?

By Yossi Sheffi

LogisticsQuarterly.com12 LQ™ March 2006

LogisticsQuarterly.com 13LQ™ March 2006

To deliver products in the right quantity and at theright place and time in increasingly volatile mar-kets,and subject to relentless cost pressures,com-panies have built complex supply chains thatspan the globe.These supply chains have enabled

companies to access worldwide markets and adapt quickly toshifting demand – providing there are no serious breaks inoperational performance. The problem is that the very com-plexity and global reach that are intrinsic to modern supplychain management; the low inventory level and lack of redun-dancies required to achieve efficient operations,expose com-panies to a wider range of unexpected disruptions.The chal-lenge is to make supply chains robust enough not only to con-tinue operating in this risky business environment, but also toturn this resilience into competitive advantage.

Supply chains can be disrupted in many ways. There arenatural disasters such as hurricanes and earthquakes; thereare accidents, and disasters perpetrated by humans such asterrorist attacks and sabotage.These dislocations are in addi-tion to the “normal” ones that arise from the nature of globaltrade, such as labor disputes, border inspection delays andtraffic congestion.

In cases of large disruptions, government overreactionwhich exacerbates the emergency adds to the disruption.For example,after the 9/11 terrorist attacks the United Statesgovernment imposed restrictions on flights and the move-ment of goods at U.S. borders. These actions compoundedthe damage wrought by the attack itself. The intermittentplant closings by Chrysler in the weeks that followed andthe 13 percent reduction in output at Ford Motor Companyduring the fourth quarter of 2001, were not the direct resultof the terrorist attack. They resulted from the shutdown ofthe Canadian and Mexican borders for truck movementsand subsequent delays because of tighter border security.The U.S. government’s reactions disrupted numerous just-in-time manufacturing systems that depended on reliableinternational shipping.

How can enterprises build supply chains that are resilientenough to withstand these incidents and help the organiza-tion to excel? First, (use a different word because there is nosecond number in the sequence) they need to define theobjective. Resilience is a notion borrowed from the materialssciences,and represents the ability of a material to recover itsoriginal shape following a deformation. For companies, itmeasures their ability to, and speed at which they can, returnto their normal performance level (production, services, fillrate, etc.) following a disruption.

Resilience can be achieved either through redundancy orthrough building flexibility into supply chains. The standarduse of redundancy includes either underutilized capacity –which most companies can ill-afford, or the use of safetystock of material and finished goods.Such inventory can givea company time to plan its recovery following a disruption.Indeed, many companies have increased inventories whenpreparing for a disruption.

Extra inventory, however, is expensive to hold in particularwhen preparing for large, infrequent disruptions. And asdemonstrated by “lean” and “six sigma” processes, it can alsolead to sloppy operations that result in increased costs and

reduced quality.By contrast, increasing supply chain flexibili-ty can help a company not only withstand disruptions butalso better respond to the day-to-day vagaries of the market-place.

To build in flexibility for resilience, companies mustinvolve many facets of supply chain design by:• Developing the ability to move production among plants,use interchangeable and generic parts in many products,andcross-train employees.• Using concurrent processes of product development, rampup, and production/distribution.• Designing products and processes for maximum postpone-ment of as many operations and decisions as possible in thesupply chain.• Aligning their procurement strategy with their supplier rela-tionships.

These principles create not only resilient supply chainsthat can recover from disruptions but also flexible supplychains that can respond to day-to-day demand changes. Onebegets the other, because a supply shortage and a demandspike are, at their core, a problem of supply/demand mis-match. Companies who have built their supply chains torespond to significant demand fluctuations have also built inthe ability to respond to supply shortages.

How exactly do these supply chain principles increaseresilience? Postponement and built-to-order operations allowfor diversions of parts and semi-finished material from sur-plus areas and products to satisfy shortages elsewhere.Thus,with only a few days of committed orders, Dell was able tofare much better than Apple during the 1999 Taiwan earth-quake,which disrupted the worldwide supply of memory andgraphic chips. Hewlett-Packard (HP) sells printers all overEurope. HP often faced the problem of having, for instance,too many printers for the Danish market and not enough forHungary. Using the concept of postponement (delaying thefinal configuration of a product until as late as possible in thesupply chain when more accurate demand information isavailable) HP builds “vanilla”printers that include everythingbut the power supply, the wall plug, the decals, and the lan-guage of the instruction manuals. Once HP receives ordersfrom particular countries, it adds that country's particularpower supply, plug and language materials through a cleveraccess hole in the side of the box and sends it to the country.This creates resilience because it is much easier for HP torespond to supply/demand mismatches.

The use of a small number of commodity parts not onlysimplifies operations and concentrates the procurement out-lays, it also creates flexibility to move the business amongsuppliers should one falter. When Intel’s Systems Groupreduced its mix of 2,000 types of resistors, capacitors, anddiodes to only 35 types, it not only simplified procurementand reduced costs but also increased Intel’s ability torespond to demand changes and supply disruptions.

Reducing time to market also means that the time to recov-er from disruptions is likely to be short. To this end, Lucentcreated a special Supply Chain Network organization in 2001.Cutting across the company’s engineering, procurement,manufacturing, distribution, and even sales divisions, the net-work increased the company’s agility.

LogisticsQuarterly.com14 LQ™ March 2006

The use of multiple suppliers with different characteristicsallows HP to not only have redundancy but also builds inflexibility.HP’s choice of supply plants for its printers divisionmeans that during ramp-up and end-of-life they can use theiragile (yet more expensive) plant, but during the steadydemand period of each printer, they can use the more effi-cient plant.

Supplier relationships are key to firm resilience. Indeed,unsound supplier relationships can pose a major threat inany business. British car company Land Rover learned thislesson in 2001 when it suddenly lost its sole source of chas-sis for the popular Discovery vehicle. Its key supplier wentbankrupt. Land Rover eventually had to pay down some ofthe supplier’s debts to restore supplies, suffering severeproduction delays in the process.The car manufacturerwas unaware of the financial dealing the caused its criticalsupplier to bankruptcy. Such oversights are common. Forexample, last summer British Airways’ (BA) operations atHeathrow Airport in the UK ground to a halt when itsground workers staged a sympathy strike with the lay-offworkers at its core supplier, Gate Gourmet. The airline wascaught off guard by Gate Gourmet’s actions and failed toanticipate the response of its own workers. The result wascanceled flights, irate customers and negative publicity.Having a close relationship with Gate Gourmet may havealerted BA to their impending actions and their possibleeffect on BA’s workers, giving it time to prepare and possi-bly stop the strike before it started. Yet Willie Walsh, thecompany’s CEO who joined BA recently, said that theAugust strikes had “nothing to do with British Airways” andBA could not have seen it coming.On the other side of theAtlantic, General Motors is paying dearly for its flawed rela-tionship with supplier Delphi Corp. The enterprise wasspun off from GM in 1999, and with annual sales of $28 bil-lion is a major supplier. Since it cut loose from its parent,Delphi has been unable to compete effectively with lean-er, more efficient competitors, and recently filed for bank-ruptcy. GM was caught unprepared for the fall out from thefailure of a key supplier.

Contrast this to the approach taken by auto companyToyota to its suppliers. The highly successful Japanese car-maker holds stock in many of its suppliers, and they recipro-cate by holding Toyota shares. Respective companies arebound together by mutual interest and are committed to thelong-term health of their businesses. For instance, one partssupplier, Aisin, part of the Japanese company Aisin Seiki Co.Ltd., customarily shares testing sites with Toyota to help theautomaker cut costs.

A strong, stable supplier network greatly enhances marketresilience, and companies can lay the foundation for such anetwork by forging the right links with suppliers. It is unrealis-tic,however,to expect such close relationships with all suppli-ers. Instead, companies should recognize that there are twobasic types of supplier relationships and each has differentdemands. Core suppliers are the one on which the companychoose to depend not only for parts but also for innovation;these companies build parts whose characteristics the ulti-mate customers recognize. The dependency on these coresuppliers requires a company to have a deep knowledge of

each vendor, not only because it is trying to draw on theirinnovation but also because the unexpected failure of onecould be disastrous. Conversely, the preference may be forarms-length relationships which do not require such invest-ment in supplier relations. In this case, the supplier networkneeds to include multiple suppliers so that the company canfind an alternative source quickly should one of its vendorsbecome problematic. Neither approach is right or wrong, thepoint is to commit to one and develop the appropriate strate-gy.Note, that this is not an “all-or-nothing”proposition.Dell, forexample, has strong single-supplier relationships with itsprocessors and boards vendor (Intel) and its operating sys-tems vendor (Microsoft). By contrast, it has several vendorsfor components such as disk drives.

Although supplier relationships are integral to resiliency,the most important factor that clearly distinguishes betweencompanies who bounce back from a disruption and thosewho do not is the corporate culture. Organizations likeNokia, Toyota, UPS, Schneider National, FedEx, Dell, and theU.S. Navy can be studied to understand the principles thatmake them flexible and resilient.While on the surface, com-panies such as Dell and the U.S. Navy may not seem to havemuch in common, a closer look shows these resilient com-panies share several common traits, especially within theircorporate culture.

A flexibility culture is one where communication is perva-sive and continues. At Dell, for example, executives receiveproduction reports every two hours on their pagers, so thateverybody is continuously aware of what is going on.Anothercharacteristic of a flexibility culture is power distribution: giv-ing even low-level employees the power to make decisions.For example, any employee on the Toyota assembly line hasthe power to stop the line if they notice a quality (or other)problem. Similarly, any sailor on the deck of a U.S. Navy carri-er has the power (and the responsibility) to stop flight opera-tions if they sense something wrong.At Spanish retailer Zara,young designers have the power to redesign and authorizemanufacturing and replenishment of garments, based oninformation about which products are in the highestdemand. This policy lets Zara respond to customer prefer-ences in three weeks compared to Marks & Spencers’ ninemonths.

Unfortunately, culture is difficult to define and even moredifficult to change. But this is not an impossible task. Thesuccess of the quality movement in the 1980’s and the safe-ty campaign in the early part of the last century serve asstrong examples of how corporate culture can change dra-matically. Several corporate turn-around cases, like that ofContinental Airlines under Gordon Bethune, also show theimportance and the plausibility of changing corporate cul-ture. Even the culture of populations can change as demon-strated by the anti-smoking and anti-drinking and drivingcampaigns in the U.S.These successful cases should serve asblueprints for companies striving towards resiliency,because the right culture means that the entire organizationis deputized to serve as the eyes and ears of the corporatesecurity and resilience efforts, and can take the necessaryactions to recover from any disruptions when the normalhierarchy is not operational.

LogisticsQuarterly.com16 LQ™ March 2006

The transport management landscape has under-gone dramatic change in the last 26 years.Beginning in 1980,after nearly six decades of regulation characterized only byglacial change, the transportation environment has been in aconstant state of flux.The first 20 years of deregulation chal-lenged managers with the task of confronting increased safe-ty and social regulation, escalating customer expectations,increased globalization, improved technologies, labor andequipment shortages, and industry mergers and consolida-tion.To their everlasting credit, transportation managers were

able to achieve staggering improvements that helped reducethe percentage of the U.S. Gross Domestic Product spent onlogistics almost in half during that period (from over 16 per-cent in 1980 to just under 9 percent in 2000). Managers fromthat era have many interesting tales regarding exactly howthose changes were accomplished.

The degree of change experienced in the transportationenvironment from 1980 to 2000,however,pales in comparisonto the changes that have occurred since 2000.While some ofthis change can be correlated with the changing sociopoliti-

Transportation Management Trends

The Gathering StormThe current environment shaping transportation

has often been likened to the perfect storm. These

trends threaten to turn our view of transportation

and logistics on its head unless major changes are

forthcoming in the near future. Here’s a look at

the primary changes converging on the industry to

help you act proactively.

By Theodore P. (Ted) Stank and J. Thomas Mentzer

17LQ™ March 2006LogisticsQuarterly.com

cal landscape emerging as a result of 9/11,many of the trendswhich transportation managers must consider today havemuch longer histories.Regardless of their genesis, the currentenvironment impacting transportation has frequently beenlikened to the perfect storm – a reference to the interactionof a number of unique but related trends that threaten to turnour view of transportation and logistics on its head unlessmajor changes are forthcoming in the next several years.Welike to call this, instead, the Gathering Storm – because thePerfect Storm will not be perfect (a bad thing in this case) ifwe recognize the storm signals that are gathering and addressthem.The following list highlights the three most critical ele-ments of the Gathering Storm and identifies some of the pri-mary causes for them.

1. Fuel prices – The $1 increase experienced at thepumps over the last year hurts more than just the averageconsumer. Fuel is the second largest expenditure for mosttransportation companies (behind labor; and it is the mostexpensive for fuel-intensive modes like air). The increasehas dramatically changed relative transport economics andthe logistics decisions that it influences. The major causesof the increase include the political instability of theMiddle East, damage to refining capacity from the series ofnatural disasters that have rocked the U.S. Gulf coast, andincreased consumer demand (9/11 sent people to theroads in record numbers). An interesting side note is thatfuel prices are rising at the same time that regulation isincreasing emissions standards for truck engines, challeng-ing engine makers to develop technology that provides thesame towing power with similar fuel efficiency.

2. Driver shortage – Transportation experts estimate anapproximate 80,000 driver shortfall given today’s demandrequirement, with some experts estimating the shortage willgrow to 120,000 by 2010.The shortage stems from both eco-nomic and demographic trends, including a diminishingpool of available driver talent due to increased competitionamong driving jobs.Competition with the construction indus-try is also increasing (the greatest competitor for those likelyto take jobs as truck drivers and railroad engineers is the con-struction industry; so the boom in home building and officeconstruction significantly impacts the available driver pool).The shortage may be exacerbated by stiffer driver hours ofservice regulations that can have the effect of further reduc-ing available driver work hours

3. Capacity constraints – The United States has notenjoyed unified national transportation spending anddevelopment policy since 1950’s. Estimates are that the lat-est transportation spending bill, while mind-bogglinglyenormous, is still not enough to cover the basic mainte-nance of existing road and bridge systems, let alone makethe improvements necessary to deal with the level of trafficexperienced today. If you don’t believe us, drive your newfuel efficient hybrid sedan on any one of our interstatehighways and tell us how comfortable you feel when youare hemmed-in on all 4 sides by tractors towing 53 foottrailers at 70 plus mph on uneven lanes.

And don’t look to rail to relieve the problem. Untilrecently, railroads had not made enough money to coverthe cost of capital investment for over 20 years, resulting in

the retirement of track and merger/consolidation to makea profit. Then consider that it costs millions per mile tobuild new rail lines. Rail has figured out that better utiliz-ing, and in some cases shrinking, its present network androlling stock capacity is a better formula for profitability.

Further,port facilities are inadequate to handle the volumeof freight growth resulting from the historic levels of foreigntrade imbalances, predominantly caused by growth of tradewith China. On any given day there are dozens of shipsanchored in the harbor at the ports of Long Beach and LosAngeles waiting for dockside availability. Such delays arecaused by inefficient labor to offload and insufficient roadand rail access to facilitate the movement of containers fromportside facilities.

Finally,increased security regulations as a result of 9/11 arefurther slowing movement through ports, and promises fromregulatory bodies to increase the number of inspectionscould cripple the flow of international freight. Although thesituation is more dramatic in maritime ports, it is similar tothat experienced in airport facilities.

So how are we to deal with this “Gathering Storm”and pre-vent the realization of the “Perfect Storm?” Below is a list ofmajor implications to the shipping community and thebroader economy as a result of the elements of the storm.• Reliable transportation availability is no longer a given –smart shippers are no longer leading negotiations with carri-ers on price,but rather are trying to lock in capacity with reli-able service providers.• Increased collaboration with carriers – shippers can nolonger afford to keep drivers waiting hours at the docks. Bythe time shippers are ready, drivers may not be able to oper-ate due to Hours of Service regulations. In any event, carriersare tracking shipper performance on waiting time and reduc-ing or eliminating service to those that routinely performpoorly.• Continued increase of port congestion and traffic slow-downs on major highways will cause companies to look foralternative transportation modes (we are experiencing aboom in rail intermodal movements), alternative ports (onthe West Coast, Tacoma and Vancouver are seeing a briskincrease in volume, and there is even talk of investing in theconstruction of new ports in Mexico), and alternative routesor routing times to take advantage of low traffic density.• Higher consumer prices – while the elements of theGathering Storm have not yet had a major impact on con-sumer pricing, there is no way that the supply chain can pro-tect consumers from heightened costs forever.• Creative labor incentives by carriers to induce more peopleto drive trucks and trains. In an absurd way, the transportationpicture may benefit from a housing bubble burst.• Increasing political visibility and dialog on the loomingtransportation capacity crisis, including the possibility of fueltax increases to fund improvement and increased discussionof alternative fuel sources such as fuel cell technology.

The Perfect Storm cannot be prevented by ignoring it. Itcan only be managed by recognizing the signs of theGathering Storm and taking proactive actions to lessen theimpact on individual companies, supply chains, and theeconomy (both U.S. and global) as a whole.

LogisticsQuarterly.com18 LQ™ March 2006

This article highlights the global changes driven by the trendtoward Asia, and the resulting winners and losers in logistics.

India and China: Getting Big FastTo understand the changes in Asia, it is instructive to startwith China, since China along with the United States repre-sent a combined 60 percent of global trade.

Today China, along with India, stands at the epicenter ofthe Asian miracle. The two countries represent a populationof 2.2 billion. In addition, both are attracting foreign directinvestment, with China attracting $60 billion, and India draw-ing $3 billion. Overseas firms like Yellow Roadway (YRC),DHL,and GeoLogistics are attracted by the significant growthpotential in India and China.The Indian logistics market rep-resents $15 billion, according to Frost & Sullivan, and is grow-ing at a rate of 7 percent annually. Meanwhile, China weighsin at $250 billion of logistics spend according to UPS, and isgrowing 16 percent annually.

An important engine of growth is China’s 2001 acceptanceby the World Trade Organization (WTO). As a result, Chinamust now adhere to WTO’s rules,and is liberalizing rapidly. In

the past four years, China has reduced tariffs from 25 to lessthan 10 percent. Continued legal changes attract more over-seas investment and fuel accelerated expansion.

Another key driver of Asian logistics growth is the low levelof logistics outsourcing. Both China and India have under-penetrated,third-party logistics (3PL) markets.India’s 3PL sec-tor represents 3 percent of the country’s total logistics spend.China’s 3PL sector represents just 2 percent of its country’stotal logistics spend. In contrast, the U.S. 3PL sector is muchmore penetrated, at approximately 10 percent, with Europeeven higher, at 25 percent. Clearly the Asian 3PL sector has alot of room to grow.

A core reason for this low penetration in the Asia marketis their low efficiency. In the United States, over the past 25years, logistics costs as a percentage of GDP has declinedfrom 17 to 9 percent. In China, logistics costs today repre-sent 21 percent of GDP. In the U.S., logistics costs declineddue to a combination of government infrastructure invest-ments and high-growth, asset-light outsourcing logisticscompanies.These trends are also increasing in both Chinaand India.

AsianEmergenceInnovation was once viewed as the bastion of the United States. In 1790, George Washington

authorized the first U.S. patent, granting Samuel Hopkins the right to a new manufacturing

method for potash. Today, 216 years later, both manufacturing and innovation have gone

west, from the United States to Asia. As a result, we are in the midst of a sea of change

that is revolutionizing the global economy, and in tandem, the logistics world.

By Benjamin Gordon

THE BRAVE NEW WORLD OF LOGISTICS

19LQ™ March 2006LogisticsQuarterly.com

LogisticsQuarterly.com20 LQ™ March 2006

The governments of India and China are investing aggres-sively to fuel accelerated growth. India, for example, whoselogistics market is approximately 0.7 percent of the U.S. logis-tics market,announced plans for $17 billion in transport infra-structure investment between 2006 and 2010. In contrast, theUnited States just signed into law SAFETEA-LU, a $286.4 bil-lion, six-year spending plan for transportation infrastructurethat equates to 5 percent of its annual logistics market.Thus,on a per-annum basis, while the United States is investing 5percent of its annual logistics spend on infrastructure,India isinvesting 23 percent or over four times as much.

Asian business leaders see these trends and are respond-ing by seeking outsourcing solutions. A survey by HarrisInteractive and sponsored by UPS indicated that Asian exec-utives are seeking to outsource at a rate three times fasterthan that of their U.S. and European counterparts. Whenasked whether they are moving “very extensively” or “com-pletely” to outsourcing, 29 percent of Asian executives saidyes. In contrast, just 11 percent of U.S. and European execu-tives agreed with this assertion. As a result, logistics marketsare opening up and growing rapidly throughout China, India,and indeed much of Asia.

Impact on U.S. Logistics Markets The impact of Asia’s ascendance on U.S. logistics markets

has been swift.First, manufacturing has shifted from the United States to

Asia. In November 2005,General Motors (GM) declared plansto slash 30,000 jobs in Canada and the United States. Dayslater, GM announced plans to add 450 workers in India, and200 in China. In the next 3 years, GM intends to raise autoparts sourcing in India from $120 million to $1 billion,and upto $80 billion in China.

Second, carriers and freight forwarders have gained signif-icant benefits. In November 2005, three North American carri-ers – American, Continental, and Air Canada – initiated serv-ice to Delhi.

Third, the West Coast of the United States has continued toregister record levels of demand.As Asian-based manufactur-ing is shipped to the United States for consumption, the portsof Los Angeles and Long Beach are reporting record vol-umes. Los Angeles, for instance, handled over 700,000 TrailerEquivalent Units (TEUs) in the month of October alone.In thecoming year,China will originate over 48 percent of all importfreight into the United States, much of it via the West Coast.California-based firms have grown correspondingly.For exam-ple,California-based freight forwarders GeoLogistics and BAXGlobal have both completed successful turnarounds in thepast five years, expanding from unprofitable operations in2000-2001 to over $50 and $100 million in operating profit,respectively,on the basis of dramatic Asia-U.S. freight forward-ing growth.

Consolidation is Coming, in China and throughout Asia

The rapid ascent of China has caught the attention of glob-al logistics leaders.

In China, over 150 merger and acquisition transactionshave taken place with U.S. companies over the past decade.

Companies like GeoLogistics,YellowRoadway (YRC),and oth-ers have forged deals to enter China. Historically, U.S. compa-nies seeking growth in Asia have targeted the Western-friend-ly markets of Hong Kong and Singapore. Mainland China,after all,didn’t even have a stock market until 1990,and manyof the core assets of the country remain under governmentownership.

However, this acquisition approach is changing rapidly, ascompanies target mainland China as well as neighboringmarkets.According to MidMarket Capital Advisors, two-thirdsof Chinese acquisitions in the United States have been con-ducted as 100 percent transactions through Hong Kong enti-ties. In contrast, two-thirds of U.S. acquisitions in China haveinvolved majority investments in mainland China.This activi-ty is expected to continue to surge.

This trend is also seen in other parts of Asia. In India, DHLpurchased Blue Dart, establishing a foothold in the domesticcourier and express marketplace. FedEx and UPS are alsostrengthening their positions in the country, and recentlyincreased the number of flights in and out of China.

Implications for U.S. CompaniesFor U.S.-based logistics providers, the implications are

monumental.On the one hand, companies that gain a successful

foothold in Asia can expect to see significant growth. U.S.-based companies like Expeditors, BAX Global andGeoLogistics now derive a majority of their profits from Asia.In a market where logistics companies were historically val-ued at 5-7 times operating profit, or EBITDA, the high valua-tions (Expeditors trades at close to 20 times EBITDA,BAX soldfor 11 times EBITDA,and GeoLogistics sold for 14 times EBIT-DA) reflect the premium markets, investors, and buyers placeon Asian growth opportunities. Similarly, when PWC Logisticsannounced a string of three acquisitions to strengthen itspresence in Asia in 2005, its market valuation skyrocketedfrom less than $2 billion to over $8 billion, in a large part dueto the premium that investors placed on the company’s Asianexpansion.

On the other hand, companies that overlook Asia do so attheir peril. Much like the European manufacturers of the1800s,who found themselves supplanted by Samuel Hopkinsand other leaders of the U.S. manufacturing golden era, U.S.companies today who fail to invest in Asia will eventually slipbehind.For example,Expeditors grew its market value by 20.3percent over the past five years. In contrast,EGL,a firm with aweaker Asian presence,grew its market value at half that rate,or 9.5 percent. Smaller firms face an even more dramaticimpact, as freight forwarders with a subscale presence inAsia-U.S. trade lanes are finding themselves increasingly shutout of lucrative markets by larger competitors.

Smart logistics companies have several options forresponding.Some, like BAX and GeoLogistics,sought mergerswith the global firms of Deutsche Bahn and PWC Logistics,respectively, gaining resources to fund accelerated growth inAsia.Others are raising capital in a bid to fund acquisition-ledgrowth while maintaining independence.What is clear is thatevery U.S. logistics firm needs a strategy for growth in whatmay be known as the Asian century.

800.663.6331

.com.com

The fabled duel between the tortoise and the hare is symbolic of the strategies required to

consistently win the supply chain race. It’s as much about managing information as

selecting the best modes of transport. Wheels can effectively integrate all available resources

to provide winning management solutions for your supply chain.

Sometimes the tortoise, sometimes the hare, but every time the professionals at Wheels can

put you across the finish line, with the best bottom line…everytime.

LogisticsQuarterly.com22 LQ™ March 2006

INVENTORY IS NOT ONLY a critical part

of supply chain management; too often

it is the main cause of a painfully incre-

mental progression toward effective and

genuine supply chain management.

Reading this article will enable you

to see inventory from a perspective

contrary to most conventional views

defining inventory as an asset.

Perhaps the greatest incentive to

change our viewpoint is the unprece-

dented speed at which corporate envi-

ronments are transforming. Not surpris-

ingly, many organizations and individu-

als are seeking shelter against these

transformational changes, which result

in either corporate growth or rapid

decline.The old guard,which has tradi-

tionally been comprised of stable

organizations, is now oftentimes star-

ing down bankruptcy.

What will differentiate the winners

from the losers in this context? Many

will respond to this question with

answers that pertain to profitable

growth, the ability to embrace global-

ization or, perhaps, a commitment to

embrace technology to realize produc-

tivity gains. These items are the effects

of doing the right things, but they are

not the strategies that define today’s

industry leaders.

The one element that will define

organizational survival is, in a word:

“inventory;”I am referring to the unwa-

vering, relentless and even fanatical

drive to reduce excess inventories.

Why can inventory reduction lead to

organizational success? It goes

beyond the reduction of inventory car-

rying costs. The most powerful result

of inventory reduction is the relation-

ship between inventory, waste elimina-

tion, problem solving and teamwork.

Because of the extreme of today’s

business issues, it is time to talk in

absolutes. Topping our list of

absolutes are

1. An organizational culture focused

upon and committed to the elimina-

tion of waste at all levels.

2. Individuals within successful

companies will be problem solvers

By Robert Martichenko

Inventory Reduction:The Path to Supply Chain ManagementInventory is not only a critical part of supply chain management; too often it is the main cause of a painfully incremental progression toward effective and genuine supply chain management.

23LQ™ March 2006LogisticsQuarterly.com

first and process owners second.

3. Companies who have problem

solving cultures will achieve and bene-

fit from the riches of teamwork and

true supply chain management.

4. Eliminating waste, problem solv-

ing, teamwork and supply chain man-

agement are achieved through the

elimination of excess inventories.

At this point, you are probably ask-

ing yourself a few questions, such as:

How can inventory reduction pertain

to waste elimination, problem solving

and teamwork, and be critical to quali-

ty measure in order to realize optimal

supply chain management?

Waste Elimination - ProblemSolving – Teamwork andInventoryTo draw an analogy,picture your organ-

ization as a boat navigating down a

river. The river represents the business

environment, flowing fast, with treach-

erous unknown obstacles ahead. Just

below the water are many rocks wait-

ing to puncture the hull of your boat.

These rocks represent waste of all

sorts, such as waste of transportation,

space, inventory, time,knowledge,pack-

aging, internal silos and poor supply

chain relationships. Building on this

analogy, the inventory is the water level

of the river. As inventory rises, so does

the water level.

As we flow down the river, we are

very cognizant of the rocks (waste)

below. In fact, some of these rocks have

now protruded above the water and we

are at risk of sinking this boat. We can

opt for one of three things to stay afloat:

1. Try to navigate around the rocks,

relying on people and brute force to

get us through. The equivalent of daily

fire fighting.

2. Raise the water level (inventory

level) in order to ensure the river flows

on top of the rocks to avoid puncturing

the boat.

3. Eliminate the rocks permanently,

making the river void of waste and

obstacles.

Unfortunately, for many organizations,

we choose to raise inventory levels as

soon as obstacles surface.For example:

1. We do not have confidence in our

supply base (a rock), so we increase

safety stock (the water level) to gain a

sense of security.

2. We have unstable transportation

lead times (a rock), so we increase

buffer stocks (raise the water level) in

order to cover ourselves for the uncon-

trolled variability in lead times.

3. We have a lack of teamwork

between internal departments (a

rock), so we build inventories up

between departments (raising the

water level) in order to protect our-

selves from perceptions of incompe-

tence in other departments.

4. We do not communicate with cus-

tomers (another rock), so we hedge

against demand uncertainties by rais-

ing finished goods inventory levels

(raising the water level).

These examples show that we often

use inventory to hide waste and other

problems. Secondly, inventory devel-

ops and promotes cultures where inter-

nal and external silos are built and

maintained. In other words, functional

solos are not invisible walls, as we all

believe; they are physical walls con-

structed with inventory. This inventory

builds walls that deter any efforts for

horizontal and vertical integration in

the supply chain.

Completing the river analogy, one of

two things will result in the end.

1. We will continue to ignore waste

(the rocks) and continue to raise the

water level (inventory) in order to

avoid the rocks. Eventually, the water

level will spill over the river banks,

grounding us and rendering us inoper-

able. This is equivalent to bankruptcy

caused by uncontrolled internal costs

as a result of waste perpetuating itself

throughout the organization.

2. We can recognize that we need to

eliminate the rocks immediately and

permanently. The goal is to create a

river that is calm and navigable. This

will only be accomplished if we elimi-

nate the rocks.To achieve this , howev-

er, we need to see them and therefore

it’s imperative that we reduce invento-

ries to expose this waste.

To be sure, this is not an easy task. It

is counter intuitive for us to think the

best step forward is to reduce invento-

ries in order to highlight many of the

problems inside our organization. The

process may shut plants down, short

ship customers and expose lack of

teamwork at senior levels of the organ-

ization. Who in their right mind would

sign up for that?

It’s a Matter of SurvivalThere is no question that our vision of

true supply chain management is not

being realized as quickly as needed.

Many people think that people issues

and the proverbial internal silo cause

this delay. Organizations that continue

to allow functional silos to exist, and

fail to foster teamwork will not survive.

Organizations that do not relentlessly

eliminate waste will not survive. These

are the “absolutes” I alluded to.

Much research into learning models

has shown that human beings learn

best by solving problems. As Aristotle

said,“we learn by doing”. Teamwork is

about solving problems together, hav-

ing a common goal and leveraging the

strengths of each team member to

maximize the overall potential of the

team. Cross-functional teamwork is not

something that results from training

programs or feel good pep talks.

Teamwork happens when we are

forced to solve problems together and

realize that inventory is hiding the

problems we need to solve.

Once this is accomplished, supply

chain management will be a bonus

byproduct. That is, supply chain man-

agement is not something we directly

implement; it is simply a result of doing

the right things. It evolves when we

decide to fight against waste in the sys-

tem. Organizational survival depends

on this one crucible.

100 Business Park CircleSuite 202Stoughton, WI 53589 USAP: (608) 873-8929URL: www.3PLogistics.com

Current Guides and ResearchWho’s Who in North American Logisticsand Supply Chain Management

Who’s Who In International Logistics—Armstrong’s Guide to Global Supply ChainManagement

An Overview of Warehousing in NorthAmerica—Market Size, Major 3PLs,Benchmarking Prices and Practices

Bigger and Better—3PL Financial Results, 2004