supervisory challenges of fintech

TRANSCRIPT

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory challenges of FintechArcada, Fintech I: Fintech in the past, present and future

19.11.2016 0Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

About the speaker

■ MSc, Computer Science, CISA– Financial Supervision, 25+ years,

various positions– Helsinki University, lecturer– Nokia, Software Engineer

■ Bank of Finland workgroup and report ”Digitalisation in Financial Sector”, member

■ Launching the work for Innovation HelpDesk in FSA-Finland

19.11.2016

Markku KoponenHead of Division Operational RisksFinancial Supervisory Authority

markku.koponen(at)finanssivalvonta.fi

1Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Agenda

■ History of Fintech (”short version”)■ Fintech – growing business – statistics■ Introduction – regulation vs. innovation; digital lipstick?■ Digitalisation – consequences in financial sector■ Driving factors for innovations■ Fintech – opportunities and risks■ Scenarios for banking■ Challenges for industry and supervisors■ Supervisory response■ FIN-FSA response■ Supervisory response – other supervisors

19.11.2016 2Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

History of Fintech

■ Google: Fintech 33 600 6000 hits, ”history of Fintech” 20 400 hits■ ”Fintech is a relatively new term”■ ”Fintech is a very broad sector with a long history”■ ”Last 65 years paint a picture of continued innovation and evolution”

– (the telegraph is introduced in 1838)– 1950s credit cards– 1960s ATM´s– 1970s electronic stock trading– 1980 bank mainframes (1958 ENSI in Postisäästöpankki!)– 1990s Internet, web banking, e-commerce, PayPal

■ 2010s– mobile wallets, payment apps– robo-advisors– crowdfunding, online lending platforms– etc.

■ http://www.forbes.com/sites/falgunidesai/2015/12/13/the-evolution-of-fintech/2/#5f5a17aa61e3■ http://www.nytimes.com/2016/04/07/business/dealbook/the-evolution-of-fintech.html?_r=0

19.11.2016 3Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

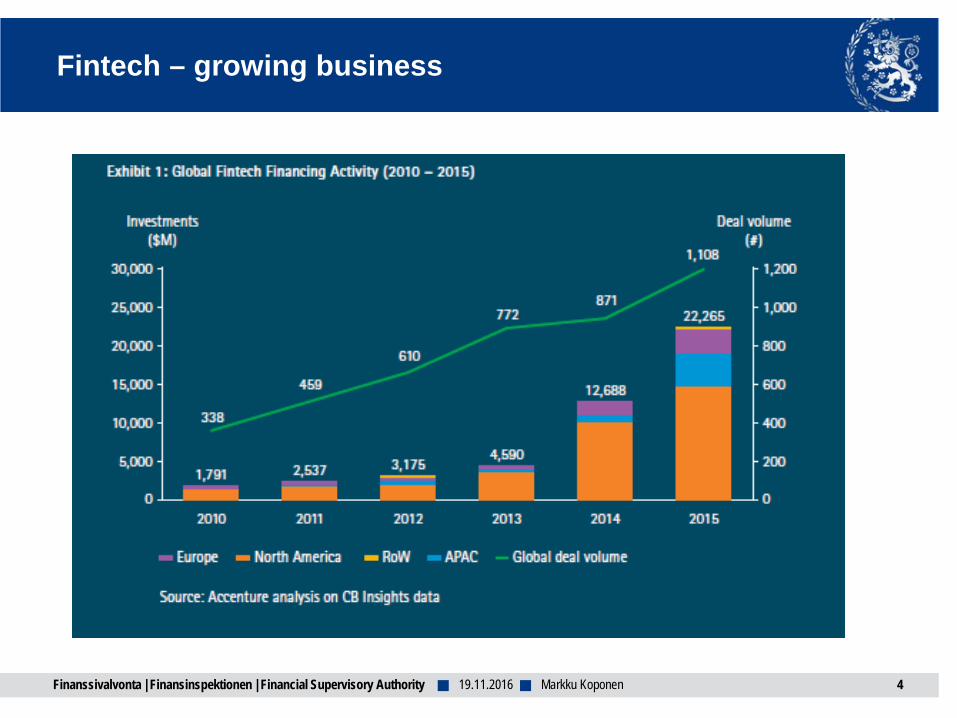

Fintech – growing business

19.11.2016 4Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Introduction I: Financial Conduct Authority, UK

Christopher Woolard, FCA Director of Strategy and Competition■ “How can regulation foster innovation in financial services? And as

part of that how can we ensure that we have a regulatory environment fit for future innovation?”

■ “…why does the FCA care about innovation? Primarily because of our duty to promote competition in the interests of consumers. One of the best ways we can promote competition is to foster disruptive innovation.”

■ “The key challenge for government, industry and regulators is to continue to ensure the regulatory environment fosters the best of financial innovation. Our ultimate goal is that the benefits of competition can be realised in the interest of UK consumers”

19.11.2016 5Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Introduction II: Digital lipstick?

■ "Banks are trying to be cool and hip and build super cool digital front ends... But it’s like putting lipstick on a pig - ultimately it’s still a pig and the new front end is still running into an awful digital back end."– Mark Mullen, Chief Executive Atom, Durham, UK

19.11.2016 6Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Digitalisation, consequences in financial sector I

■ Internal processes in banks and customer experience in services have changed strongly

■ Structural changes in financial sector due to digitalisationpretty low so far– same products offered via digital channels– new entrants (innovators) pretty small

■ Structural changes expected to grow– new entrants, global markets, regulation

■ No major changes in payment infrastructures so far■ Banks recruiting new knowhow: chief digital officers■ Banks setting up start up acceletors, partnering with Fintechs■ Potential of new technologies, e.g. blockchain, recognized in

financial sector

19.11.2016 7Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Digitalisation, consequences in financial sector II

■ Big european players in banking industry invest in digitalisation: e.g. BBvA, BNP Baribas

■ Small agile Fintechs: payment innovations, mobile payments, crowdfunding, peer-to-peer lending, Roboadvisorsetc.

■ Innovations in insurance sector, e.g. intelligent insurances, usage based insurances (UBI)

■ Mobile services and apps: still growing popularity

19.11.2016 8Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

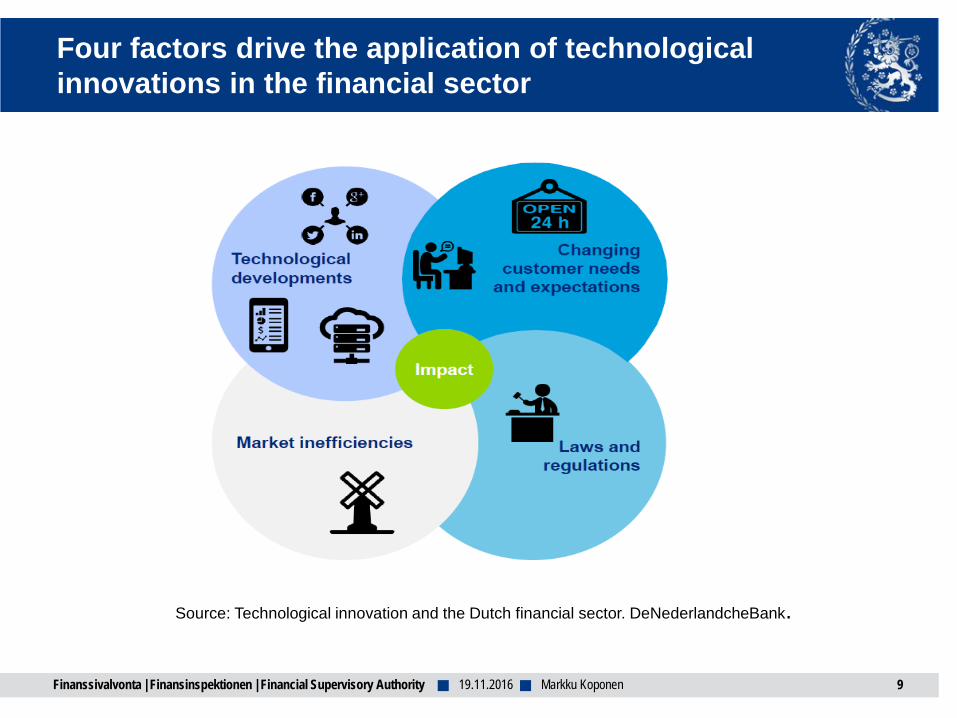

Four factors drive the application of technological innovations in the financial sector

19.11.2016

Source: Technological innovation and the Dutch financial sector. DeNederlandcheBank.

9Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Fintech – opportunities and risks

19.11.2016

Source: Technological innovation and the Dutch financial sector. DeNederlandcheBank.

10Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Dilemma: regulation and supervision vs. innovations

■ Supervisors ensure that– requirements for authorisation are fullfilled– supervised entities obey legislation, regulations and guidelines– supervised entities are professionally managed and they have adequate risk

management systems in place ■ Supervisors also

– promote compliance with good practice in financial markets– require capital adequacy and liquidity buffers to adequately cover material

risks– etc.

■ On the other hand supervisors are expected– to foster innovations and competition (at least by innovators)– support and help innovators applying authorisation

■ Preconditions– financial sector is heavily regulated– possibilities for interpretations of EU-legislation are limited

19.11.2016 11Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Scenarios for banking

19.11.2016

■ In the first, established financial institutions embrace and successfully exploit innovation, thereby changing the structure of the financial sector relatively little.

■ In the second, the market becomes fragmented as new, specialist players compete effectively with established financial institutions.

■ In the third, large technology companies such as Google and Apple displace established institutions by exploiting their scale and innovative capacity.

Source: Technological innovation and the Dutch financial sector. DeNederlandcheBank.

12Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Challenges for supervisors

19.11.2016

■ Ability to analyse– how do technological innovations impact the financial sector?– to which structural changes in the financial sector does technological

innovation lead?

■ Ability to recognise opportunities and potential risks for new business models and Fintech– potential risks: data security and privacy issues (e.g. information leaks),

cyber risks, misselling, misconduct in markets, etc.

■ Which actions should supervisors take in order to mitigate potential risks? Develop supervisory framework International supervisory coordination needed

The ESAs could play a central role in coordinating policy cooperation in the EU context

13Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Challenges for supervisors II

19.11.2016

■ Cultural differences: start-ups vs. supervisors– start-ups agile, innovative, high risk appetite– supervisors emphasise risk management, consumer protection

■ Overlapping regulation for– payment services– banking– securities markets– consumer credits

■ Lacking regulation, e.g.– crowdfunding– virtual currencies

14Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Some challenges - Finnish innovators

■ Heavy regulation, authorisation process■ Demand of strong authentication in

payments– no common model or services for strong

authentication in EU■ Agility typical for startups – challenging in

financial sector– possibility to pilot services before launching

suggested■ According to innovators ”There is a certain

threshold to approach authorities”– web pages could be more user friendly– help desk for innovators suggested

■ On the other hand– EU regulation helps to access markets within

EU: same regulation in EU area and EU passport

19.11.2016 15Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

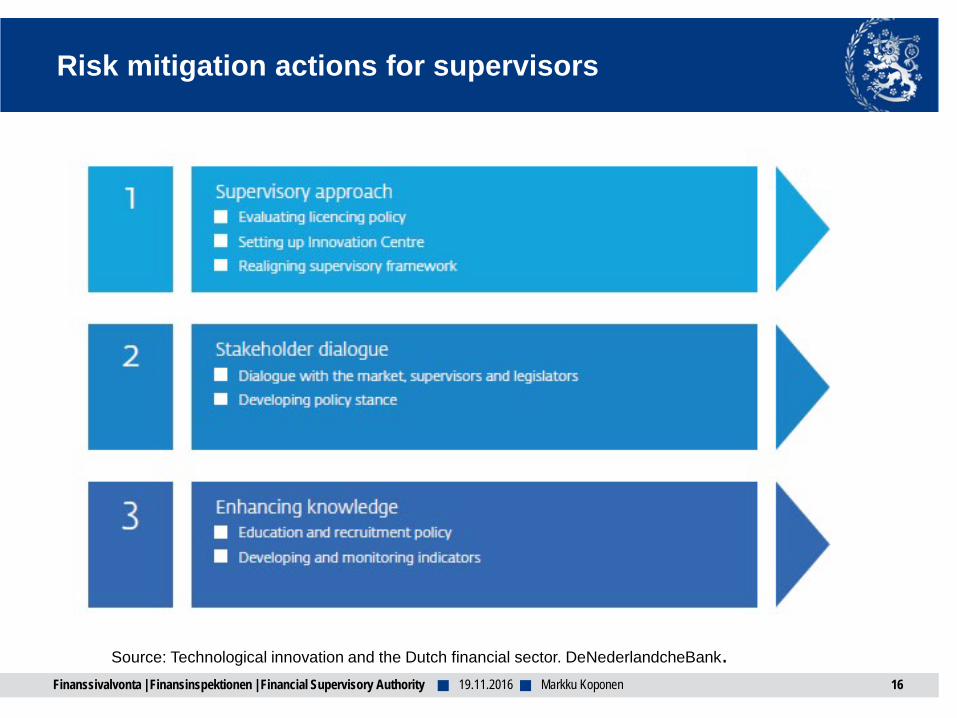

Risk mitigation actions for supervisors

19.11.2016

Source: Technological innovation and the Dutch financial sector. DeNederlandcheBank.16Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory response I

19.11.2016

■ Resources: supervisors need new expertise to understand– technological innovations and new business models– risks characteristic for innovators: e.g. cyber risks, data privacy risks,

business model risks

■ Setting up innovation hubs to support Fintechs– Regulatory Sandbox – possibility for innovators to pilot services (“test in

live environment”)?

■ Networking with industry and other supervisors: co-operation needed to understand new technological innovations and risks

17Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory response II

19.11.2016

■ No compromising in AML and CFT regulation

■ Further work is needed on:– do we need Regulatory Sandbox – possibility for innovators to pilot

services (“test in live environment”)– operational risk regulation (outsourcing, IT) needs further development:

should we directly supervise critical service providers? – tailored regulation (FinTech licence): principle based regulation seems

better suited to fast-changing environment

18Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory response – some FIN-FSA actions I

■ FIN-FSA seminar 4.10.2016: Digitalisation in financialsector: threats and possibilities– questionnaire about digitalisation to supervised entities– http://www.finanssivalvonta.fi/en/Publications/Blogs/Pag

es/digitalisation.aspx

■ Networking with Fintechs– attending Fintech Finland Community, HUB13 and

Slush meetups, giving presentations– Slush side event 30.11 Bank of Finland Museum: PSD2,

regulation, panel https://www.lyyti.in/FinTech_301116

■ Dialogue with innovators– discussions with a few innovators related to setting up

FIN-FSA Innovation HelpDesk– ongoing discussions with innovators about the need for

authorisation

19.11.2016 19Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory response – some FIN-FSA actions II

■ Setting up Innovation HelpDesk– launched 4.10.2016– http://www.finanssivalvonta.fi/fi/Toimiluvat/Innovaatio/Pa

ges/Default.aspx

■ Recruiting Senior Advisor in digitalisation (closing datefor applications 27.11)

19.11.2016 20Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

FIN-FSA Innovation HelpDesk I

Press release 4 October 2016 – 16/2016The Financial Supervisory Authority opens an Innovation HelpDeskThe FIN-FSA today opens a new Innovation HelpDesk for FinTech entities and other innovators in the sector – both old and new.

Objectives■ to increase dialogue between the FIN-FSA and FinTech entities■ to create a positive atmosphere that supports the development of the sector■ to make the supervisory authority more easily approachable■ to increase entities' awareness of financial sector regulation and related interpretations■ to enhance the development of innovations and facilitate the subsequent authorisation or

registration application processes

Preconditions: the HelpDesk■ does not replace the work of innovators themselves – you must still do your homework■ is not a replacement for consultants (e.g. lawyers)■ is not a promise of positive supervisory decisions in the future

19.11.2016 21Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

FIN-FSA Innovation HelpDesk II

■ ‘The purpose of the HelpDesk is to provide general guidance on the regulation related to innovation, as well as on supervisory issues, and to advise entities to provide necessary additional information, eg prior to a possible official authorisation or registration application process,’ says Jarmo Parkkonen, Head of Department.

■ The Innovation HelpDesk provides guidance in the form of replies to e-mail enquiries, advisory calls with an expert (max. 30 mins) and advisory meetings with several experts (max. 1 hr). The first advisory meetings will be held in connection with the Slush event on 1 December 2016.

19.11.2016 22Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

FIN-FSA Innovation HelpDesk III

19.11.2016 23Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Results of the FIN-FSA questionnaire I

19.11.2016 24Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Results of the FIN-FSA questionnaire II

19.11.2016 25Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Results of the FIN-FSA questionnaire III

19.11.2016 26Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Results of the FIN-FSA questionnaire IV

19.11.2016 27Markku Koponen

Finanssivalvonta | Finansinspektionen | Financial Supervisory Authority ■ ■

Supervisory response, other supervisors

■ De Nederlandche Bank (DNB) and supervisor (AFM): innovation hub■ FCA UK

– Project innovative, Innovative Hub, Sandbox: “We assist innovative firms to work with us...We are here to help both types of queries as long as propositions meet our criteria that they are innovative and we can see benefits to consumers.”

– “The Innovation Hub team also offers guidance pre-authorisation ... Firms that have received initial support from the Hub will have their applications handled by a specialised Project Innovate authorisationprocess. After authorisation we will provide dedicated supervisory support, normally for one year.”

– https://innovate.fca.org.uk/■ FSA Japan, Fintech Support Desk 2015

19.11.2016 28Markku Koponen