summer training project

DESCRIPTION

financial statement analysisTRANSCRIPT

A SUMMER TRAINING REPORT

ON

FINANCIAL ANALYSIS

OF

R-TEK MOULD

SUBMITTED TO

S.C.D GOVT COLLAGE LUDHIANA

In partial fulfillment of the requirement for the two years

Full time post graduate degree in

M.COM. Business innovations (M.B.I)

Supervised by: Submitted By:

Prof: Sanded Banal Ramandeep Kaur

(M.B.I)

Department of M.COM Business Innovations

S.C.D GOVT. COLLAGE. LUDHIANA.

2011-2012

CERTIFICATE

This is to certify that the project work done on Quality Management in R-Tek

Mould is a bonafide work carried out by Miss Ramandeep Kaur under my

supervision and guidance. The project report is submitted towards the partial

fulfillment of two year, full time degree of M.Com Business Innovations.

This work has not been submitted anywhere else for any other diploma/degree. The

original work is carried during 1st June 2012 to 15th July 2012 in R-Tek Mould.

Name and Sign of Industry Guide Name and Sign of Faculty

Mr. Ravinder Singh Mr. Ashwani Bhalla

_________________ __________________

Date:

Name of Student Ramandeep kaur

Roll No.

_________________________

ACKNOWLEDGEMENT

This report could not have been possible without the help of certain people and

utilising support of R-Tek Mould.

I would like to express my sincere gratitude towards Mr. Ravinder Singh (General

Manager) for his technical guidance, invaluable and constructive criticism and vital

encouragement throughout the entire project which helped me to get inside into the

working of R-Tek Moulds and to relate the theoretical knowledge imparted by our

esteemed faculty members in the course of M.Com Business Innovations to the

present scenario of corporate body.

I also express my sincere thanks to Dr. Ashwani Bhalla professor and program co-

ordinator and my respective Major Advisor Mr. Sandeep Bansal professor of

Department of Commerce and Business Innovation, S.C.D. Government College

Ludhiana, under whose valuable guidance this project was completed.

I express my sincere thanks to the whole team of R-Tek Mould for giving all the

facilities during my training period.

Indeed, the words at my command are not adequate to convey my heart full thanks

to respective parents for the encouragement and inspiration given by them.

Ramandeep Kaur

Introduction to R-Tek Mould

R-Tek Mould came into existence in 1985 under the very special guidance of Sh.

Kulwant Singh Matharu. Started from a scratch, much more research and

development work was done till 1990 and the lead was taken by Sh. Ravinder Singh

Matharu who is son of Sh. Kulwant Singh Matharu.

The concern was established as a small-scale industrial unit and now it’s one of

leading suppliers of plastic injection Moulding tools, pressure, rubber compression

moulds and polyurethane moulds and their mouldings. It is serving the industry for

about 17 years.

Besides straightening its hold on domestic market, the company has strong potential

in foreign market. The company has done some marvellous jobs dealing with some

leading brands like J.J. Jonex for Sports Die and mould, Indian Air Force for spare

parts, tools and die, Aluminium Casting, with Eastman Industries the company is

dealing Injection Moulds, Hero Cycle Limited is buying tool and die, Em Cee Cee

Sports Private Limited is dealing in tools and dies. R-Tek Mould also provides Turn

Key Projects to its clients.

The company is enjoying a prestigious market all over the globe and working with a

motive of customer satisfaction. The company prioritize is maintaining quality,

accuracy, competitive prices and professional work force.

R-Tek Mould strictly adheres to international quality and safety norms of the

automobile industry followed by leading manufacturers and automobile giants and

works to ensure zero-defect products. The company has a dedicated quality

assurance department along with a team of experienced quality control supervisors,

who ensures quality at all levels of production process. The company was endowed

with ISO 9001:2008 certification and is in process to achieve more in this line. The

company is in process of getting TS 16949 certification.

Autocrat is an integral part of R-Tek Mould. Autocrat is a reputed company since

1992, engaged in manufacture of Automobile parts, Bike Headlights Lens,

Motorcycle parts, Bike Visor, Auto parts, Visors, and other plastic products. It is

one of leading manufacturers, suppliers of Headlight glass. It provides headlight

glass to Bajaj CT 100, Bajaj Discover, Bajaj Platina, Bajaj Pulsar, and Honda

Activa. These products are fabricated with the high grade raw material that is

procured from reliable vendors to ensure that the products are of high quality and

meet the global standards.

R - T E K M O U L D

A young and dynamic organization, which have earned specialization in

manufacturing And supplying a comprehensive range of Plastic Injection mould,

Aluminum Die Casting Moulds, Aluminum Casting Products & Plastic Components.

The die casting machine capacity is from 40 to 250 Tons and also they have complete

infrastructure to finish Pressure Die Casting Components.

In Plastic Injection Moulding Section their portfolio of products includes optimum

quality Head Light Lens, and Wind Shield Glasses of Indian Bikes for replacement

market. For this they are using world’s best injection moulding machines with a

capacity from 60 to 440 Tons.

Fabricated under the supervision of well qualified and experienced professionals,

the products are acclaimed for their outstanding attributes, such as dimensional

accuracy, precise design and reliable service life.

They have developed a state-of-the-art infrastructure that aids us in efficiently

meeting all our business objectives. The Tool and Die manufacturing facility is

furnished with Vertical Machining Centers, Precision Surface Grinders, E.D.M. and

complete conventional tool room machines.

To complete target from concept to finished Product they have 3D Scanner, Cad-

Cam Software.

Objectives of the Company

Excellent distribution network

To achieve and maintain a lead position as manufacturer of automotive

components

To ensure steady growth in business and fulfill its social obligations

To build up high degree of customer confidence by sustaining standards of

excellence in product quality.

To develop human resource to increase their efficiency and productivity

Care of environment and to discharge factory waste responsibly

To build a strong customer base by satisfying them

Maintaining high quality output by implementing various quality checks.

HISTORY:-

DIE IS A BLOCK OF METAL WITH A SPECIAL SHAPE OR WITH A

PATTERN CUT INTO IT THAT IS USED FOR SHAPING OTHER

PIECES OF METAL SUCH AS COINS OR FOR MAKING PATTERNS

A MOULD IS A CONTAINER THAT YOU POUR SIFT LIQUID OR

SUBSTANCE INTO WHICH THEN BECOMES SOLID IN THE SAME

SHAPER AS THE CONTAINER E.G. WHEN IT IS COOLED OR

COOKED. A CLAY MOULD IS USED FOR CASTING BRONZE

STATUES.

R-TEK Mould came into existence in 1975 under the very special guidance of

Sh.Kulwant Singh Matharu . The idea of starting the business came to the mind from

the relatives of S. Ravinder Singh who live in Bombay and were doing the rubber

business. He took training from them in Bombay and then came back to Ludhiana

and started their own business. Started from a scratch, much more research and

development work was done till 1990 and the lead was taken by Sh. Ravinder Singh

Matharu who is the son of Sh. K.S. Matharu. Sh. Ravinder singh matharu is

currently the manager of the company. He strengthens the progress and brings the

company to the new heights.

Third generation Mr. Amrit Singh Matharu is very keen to get the

company up to a higher mark. He has done his masters from abroad and now

providing his creative skills to enhance the business growth and development.

Literature Review of R-Tek

Infrastructure

They have a well constructed infrastructure that is built in a wide area. Our

infrastructure is equipped with sophisticated and latest machineries. The

manufacturing unit is segregated into various departments such as research and

development, quality assurance, production department and packing department,

so that the business can be carried out in a synchronized manner. Our

infrastructure is capable of meeting the bulk needs of the customers.

Infrastructure is segregated into following units:-

Quality Testing

Production

Research & development

Logistics

Inventory and warehouse

Quality Testing: - The Company has its whole focus on quality. The quality testing

department helps the company to check the quality of the product as it measures the

quality so that the product can be produced according to the quality the customer

wish. Their prime motive is to provide exclusive and superior quality products to

our clients. For this, they procure products from trusted and reliable vendors.

Quality being the most crucial factor has helped them in developing a distinct

position in the market. The quality analysts ensure that the end product is free from

all kinds of defects. In order to maintain the uniform size of goods, they store and

label them. They conduct regular tests to determine the quality of products.

The products are checked on the following parameters of quality:-

Durable finish

Efficiency

Long working life

Performance

Product Range

On the strength of its expertise in the development and manufacturing

components R-Tek has explored new horizons to provide diverse range of

products.

Plastic Components

Headlight Glass

Organizational Chart

Departments

The researcher encompassed the study of four departments namely Accounts and

Administration, Designing, Production and Marketing. The basis for

departmentalization was functional.

ACCOUNTS AND ADMINISTRATION DEPARTMENT

This department is headed by Balwinder Singh. Two executives assisted them. This

department is broadly concerned with the acquisition and use of funds by the

company. It also analyze, plan and control the company’s financial affairs.

Moreover, the in house administration of the company is also taken care of. It

includes maintenance of showroom and a look into the requirements and problems

of day to day administration. It also keeps a track of things with regard to civil

construction, architectural services, networking, project co-ordination, electrical

work, etc. It is also concerned with bank facility availed by the employees. Apart

from all these, it also takes into account the installation part at the customer site

after the dispatch of the product. In a nutshell this department deals with the

trouble shooting of any problem.

DESIGNING DEPARTMENT

This department is headed by Inderpal singh. Eight creative designers assist him.

The team of designer tailor makes the products according to the needs of the

customers. Two aspects namely affordability and aesthetics are focused upon. Major

activities undertaken in this department are as follows

Setting the normal design

According to the initial measurement told by the customer, a normal design is set.

Once the normal design is finalized by the customer, a designer accompanied by

marketing personnel visits the construction site and takes the final measurement.

Then according to it a design is set and the price quotations are made.

Setting the production designs.

When the deal is finalized and after receiving 50% of the amount from the

customer, the designers make the production design. This design clearly demarcates

the technicalities so that it becomes easier for the production personnel to

understand.

Innovative designs –

The team of designers also trigger out the brain cells to create innovative

designs.

Marketing Department: This department deals with springboard of all

activities. The department is headed by Mr. Sandeep Sharma. Eight

marketing executives assist him. Various activities like product packaging,

branding, advertisement and sales promotions are taken care under this.

Marketing department is assisted by two IT personals who help in online

advertising and Search Engine Optimisation (SEO).

Human Resource Department: This department is headed by Mr.

Tajinder Singh. He is assisted by 2 executives. Various aspects of HR are

taken care of :

Leave Facility: All employees are entitled to 12 days of casual leave

and 2 days of sick leave (monthly). In case of long leave, say more

than a week, one need to inform it 10-12 days before.

Recruitment: The company spells out its requirements to the

consultancies about the suitable candidates. Candidates are recruited

after proper training.

Training: A selected candidate is put on training for 15 days to 1

month. During this period, he is not given any individual project.

Job Rotation: Job rotation is adopted by the company so that there

is development of multi-faceted skills in vacancies and to cope up with

increasing work load.

Production Department : - This department is headed by Mr.

Abhishek Kumar. Four supervisors are in charge of four different activities

such as quality control, product analyzing, production and dispatching.

Quality Control:

This sub department is mainly concerned with the inspection of raw

materials. The raw materials are supplied mainly by four companies namely

Novapan, Spacewood, Bhutan Board and Nepal Board and Nuwood.

The raw materials obtained are with respected with regard to requirements

and specifications.

Product Analyzing :

This sub-department is mainly concerned with targeting and scheduling.

After receiving the production design, it targets as to when the work needs to be

completed and schedules the whole process. Again, after completion of

production process and before dispatch, the product is thoroughly inspected

here.

Production:

26 persons comprising of machine operators and helpers are involved in

this sub-department. It consists of five operations namely cutting, molding, edge

bending, boring and hot press and post formed.

Research & development: - Research and development (R & D) is a

process intended to create new or improved technology that can provide a

competitive advantage at the business, industry, or national level. Thus this

department is very much helpful to the company. Research and

development (R&D) consortia are formed by manufacturing companies, often with

the support of government, for the purpose of conducting shared research on new

technologies for the benefit of the consortium's member companies.

Inventory and warehouse: - As there is need to store the material in the

factory so warehouse help to store the material. The fully control on the inventory is

made by the company taking EOQ model in mind. So that the wastage of time could

be reduced and production moves as smoothly. Infrastructure is one of the reasons

that provide effective customization services to clients. Their bulk investments in the

infrastructure have ensured that it is equipped with all the requisites facilities in

various sections which are detailed as under:

In Designing Sector it has:

• 3D Scanner

• Intel. Xeon. Computer.

• Cad Cam Software.

In Plastic Moulding Section it has:

• Cincinnati Feromatic 80 Ton to 440.

• Water Chillers,

• Mould temperature controllers.

• Dehumidifiers

• Auto Loaders

In Pressure Die Casting section it has:

• Machines from 80 Tons to 250 Ton Capacity.

• For Tensile test we have UTM machine.

In Tool and Die section it has:

• Surface Grinder IDROMIN -600

• Tig Welding, Mig Welding

• Lathes

• Radial & Bench Drilling Machines.

• Vertical Milling H.M.T makes

• Hydraulic Planners.

• Diamond Polishing Machines.

• Lapping Machines.

• Complete Measuring Instruments.

Annual turnover:-

Up to US$ 0.25 Million (or up to Rs. 1 Crore Approx.) Export percentage: - up to 20%

Company USP Experienced R & D Department

Good Financial Position & TQM

Large Product Line

MAJOR MARKETS:-Australia/NZ , Indian Subcontinent, Caribbean ,East/Middle Africa, North Africa,

South/West Africa, South America, South/West Europe, South East Asia, North

America

Expansion Plan

Backed by the skilled team of professionals, they are planning to launch a new and

innovative range of Tail Lamps, Head Lights & Side Indicators in the replacement

of Indian bike market. The main thing is they are going to make bullet proof head

lights for bikes.

The company has done some marvelous jobs like dealing with some of leading

brands. We are dealing J.J.JONEX for Sports Die and Mould, INDIAN AIR

FORCE for Spare Parts, tool and die, Aluminum Casting, With EASTMAN

INDUSTRIES. They are dealing Injection Moulds, HERO CYCLE LTD.is buying

Tool and Die, EM CEE CEE SPORTS PVT LTD is dealing in Tool and Die. They

are enjoying a prestigious market all over the globe and working with a motive of

"Customer Satisfaction". Their priorities are maintaining of quality, accuracy,

competitive prices and professional work force.

Product Application

Due to premium quality products, they have achieved new hikes in the competitive

market. Their products are widely applauded for its special features and unmatched

quality. The products offered by them are widely used in many sectors. They cater

products to the sectors such as:-

Sports

Sanitary & Water supply

Indian Railways

Hand Tools

Electrical

Indian Defense

Automobile

Textile

Kitchen Ware

Agricultural

WHY R-TEK MOULD???

Their Products are known for accuracy in fitment and quality as

per standards.

State-of-the-art Plastic Moulding Infrastructure.

Excellent distribution network.

Completely safe packing with heavy ply cartoons and boxes to prevent

any kind of damage

Customer oriented services

Lenses are unbreakable and having no coloring effect.

They care for environment safety.

Their workshop is equipped with all safety norms.

M O U L D S E C T I O N

"Autocrat" is a reputed company since 1992, engaged in the manufacture

and supply of Automobile Parts, Bike Headlights Lens, Motorcycle Parts, Bike

Visor, Auto Parts, Visors, and other plastic products.

Committed to impeccable quality of products, timely delivery of

consignments and competitive pricing, they at Autocrat, have successfully earned a

name for us in the market place. With years of experience, their core values have

been innovated with continuous improvements. It is their mission to establish their

wide presence at every corner of the country and offer quality products at

competitive prices. They aim at achieving continued improvement in quality,

reliability, economy and safety so as to retain competitive edge and increase our

market share. The organization incorporates novels of changing technologies and

strives to manufacture the products that confirm to international standards.

Plastic Mould - R-TEK Mould

Make : R-TEK Mould

Model : 1995

Item : Plastic Mould

Part no : Sports T

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Plastic Injection die - R-TEK Mould

Make : R-TEK Mould

Model : 2001

Item : Plastic Injection die

Part no : Y-Cone Textile

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Tool & Die - R-TEK Mould

Make : R-TEK Mould

Model : 2011

Item : Tool & Die

Part no : Agriculture Plastic Part

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Mould design - R-TEK Mould

Make : R-TEK Mould

Model : 2005

Item : Mould design

Part no : Model

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Injection Mould - R-TEK Mould

Make : R-TEK Mould

Model : 2004

Item : Injection Mould

Part no : Battery box cap

Click to view large

Pressure die casting mould - R-TEK Mould

Make : R-TEK Mould

Model : 2010

Item : Pressure die casting mould

Part no : grinder front

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Tool & Die - R-TEK Mould

Make : R-TEK Mould

Model : 2004

Item : Tool & Die

Part no : Battery Both Mould

Click to view large

-------------------------------------------------------------------------------------------------------------------------------------------

Injection Mould - R-TEK Mould

Make : R-TEK Mould

Model : 2001

Item : Injection Mould

Part no : Fork die

Click to view large

----------------------------------------------------------------------------------------------------------------------------------

---------

Pressure die casting mould - R-TEK Mould

Make : R-TEK Mould

Model : 2010

Item : Pressure die casting mould

Part no : Foot Rest design

Click to view large

P R O D U C T O F R - T E K

Mould design - R-TEK Mould (MODEL-2005)

Injection Mould - R-TEK Mould (MODEL-2004)

Pressure dies casting mould - R-TEK Mould (MODEL-2010)-

Unbreakable Headlight lens – Bajaj (MODEL- Pulsar Dtsi Digital)

Unbreakable Headlight lens - Hero Honda (MODEL- Splendor plus)

Unbreakable Headlight lens – Honda (MODEL- Activa)

Unbreakable Headlight lens - Hero Honda (MODEL- passion)

Unbreakable Headlight lens – Bajaj (MODEL- Platina)

Unbreakable Headlight lens – Bajaj (MODEL- Discover)

Unbreakable Headlight lens - Headlight lens- (MODEL- CT 100)

Bike head glasses

To provide the better head light solution, we are offering the superior quality of

Pulsar headlight Glass and we use the fine quality of raw materials to manufacture

these products. The design of these products is such that they can easily fit into

Pulsar. Applicability of these products is in various automobile industries and

service centers. Quality of the products is checked in various parameters to meet the

requirements of our clients.

Features:

On time delivery.

Exact fittings.

1. Long serving life. Visor glass – Baja (MODEL- pulsar)

2. Unbreakable Visor glass – Baja (MODEL- Discover Dtsi)

3. Unbreakable Visor glass - Hero Honda (MODEL- Super Splendor)

4. indicator glass - Hero Honda (MODEL- Splendor Plus)

5. indicator glass – Honda (MODEL- Activa old model)

Plastic Mould - R-TEK Mould (MODEL-1995)

Fabricated under the supervision of well qualified and experienced professionals,

our products are acclaimed for their outstanding attributes, such as dimensional

accuracy, precise design and reliable service life. We have developed a state-of-the-

art infrastructure that aids us in efficiently meeting all our business objectives. Our

Tool and Die manufacturing facility is furnished with Vertical Machining Centers,

Precision Surface Grinders, E.D.M. and complete conventional tool room machines.

An ISO 9001:2008 Certificate has been endowed to us to complete target from

concept to finished Product we have 3D Scanner, Cad-Cam Software. We consider

What they do to make mould Precision?

The function of mould, Type of mould, Flow of plastic melt, Air vents, Clamping

force required, Feeding balance, Contact of parting line, Runner design which

maximize efficiency in both raw material use and energy consumption in molding,

Corrosion resistantDurable,Precise dimension. We use material for moulds;

P-20, H-11, H-13, EN-31. Or as per customer requirement.

Standard ejector pins.

Standard Springs.

Standard Sprue bush

Standard Pillar bushes for our tool & die.

Tool & Die - R-TEK Mould (MODEL-2011)-

Our company is engaged in Tool & Die Profession since 1985.In tool & die we are

leading organization in the regional ISO 9001; 2008 has been awarded us & we are

committed to do as Standard. While designing a mould we consider;

The function of mould

Type of mould

Flow of plastic melt

Air vents

Clamping force required.

Feeding balance

Contact are of parting line

Runner design which maximize efficiency in both raw material use and

energy consumption in moulding.

Corrosion resistant

Durable

Precise dimensions

Head light glass

Being a well known manufacturer, we are engaged in manufacturing and

distributing the superior quality of Headlight Glass that are manufactured using the

fine quality of raw materials. We offer these products in various shapes and sizes to

meet the requirements of our clients. The array of products that are offered by us

includes Passion Head Glass, Ct 100 Head Glass, Pulsar Head Glass, Bajaj Platina

Head Glass, Activa Head Glass and Bajaj Discover Head Glass. (Unbreakable

Glasses)

Injection mould

Our expert teams are engaged in manufacturing and supplying the best quality of

Hot Runner Plastic Injection Mould. To manufacture these products, we use the

premium quality of plastic steel (P20) that make our products to last for longer

period of time. The design of these products is such that they provide the accurate

shape to plastics. Applicability of these products is in various industries such as

automobile electrical, textile, sports Indian defence and agriculture.

Features:-

Sturdy design

Smooth finishing

Minimum maintenance

Visor glass

Our motorcycle visor glasses are made from high quality plastic granules. This part

is unbreakable, Orignal colour, no decolouration effect and easy in fittment.Our

visor glass is as good as OEM.

R - T E K T E A M

They owe their success to dedicated and constant efforts of their proficient team.

They have vast knowledge of concern field and work with common objective of

providing utmost satisfaction to their clients. Due to their dedicated efforts they

have gained a distinct edge in the competitive market.

Team comprises of:-

Skilled employees

Quality analyst

Marketing personnel

R & D personals

QUALITY ASSURANCE OF R-TEK

An ISO 9001: 2008 Certificate has been awarded to them and they are working as per

ISO norms. With such equipped unit they are capable of meeting the mounting

demand of their customers within the given time frame. They keep in mind the safety of

their work team. They follow safety norms.

An ISO 9001:2008 Certificate has been endowed to R-TEK and they are in process

of getting TS 16949.

Quality Assurance of R-Tek Mould

R-Tek Mould is an ISO 9001:2008 certified company. They have a well equipped

unit which is capable of producing quality products thereby meeting the mounting

demand of their customers within the given time frame. They keep in mind safety of

their work team.

ISO 9001:2008

ISO 9001:2008 specifies requirements for a quality management system where an

organization:-

needs to demonstrate its ability to consistently provide product that meets

customer and applicable statutory and regulatory requirements, and

Aims to enhance customer satisfaction through the effective application of the

system, including processes for continual improvement of the system and the

assurance of conformity to customer and applicable statutory and regulatory

requirements.

All requirements of ISO 9001:2008 are generic and are intended to be applicable to

all organizations, regardless of type, size and product provided.

Where any requirement(s) of ISO 9001:2008 cannot be applied due to the nature of

an organization and its product, this can be considered for exclusion.

Where exclusions are made, claims of conformity to ISO 9001:2008 are not

acceptable unless these exclusions are limited to requirements within Clause 7, and

such exclusions do not affect the organization's ability, or responsibility, to provide

product that meets customer and applicable statutory and regulatory requirements.

TS 16949

ISO/TS16949:2002 , the technical specification, was approved and issued in

March 2002, as an automotive sector-specific QMS set of requirements which

uses ISO 9001:2000 (verbatim) as its base.

It replaced ISO/TS16949:1999 based on ISO 9001:1994, and is intended to be an

alternative to QS-9000:1998 and other national automotive OEM supplier

requirements. (See QS-9000:1998 Sanctioned Interpretations released for July 1,

2002, at www.QS-9000.org ).

Corporate Social Responsibility

R-TEK recognizes the importance for corporate social responsibility with its

partners and senior management reaching the goal in a co-ordinate and

committed fashion. They know that there is a need to maintain the highest level

of professional integrity with regard to their clients, staff and professional

regulators, along with others with whom they interact. Their work relationship

is transparent and managed with a view to guarantee personal development of

each employee and recognition for the deserving employees.

The health and safety of their employees is extremely

important and they take every measure to make R-TEK a perfect place to work

offering a cordial working environment. R-TEK specific labour and health &

safety commitments have been formalized in its “Health, Safety and Social

Policy”, which has been communicated to all R-TEK’s employees, to Suppliers

and is hereby published for External Community’s convenience.

They believe that helping the local community is not just something

they choose to do but is actually an important part of business.

R-TEK conscious efforts to monitor the impacts of its operations on

the environment and is committed to further reduce them and to be nominal.

Their objective is to combine the lower environmental impacts with operational

efficiency and cost saving. The manufacturing processes are regularly

monitored, with specific attention paid to energy consumption for which specific

programs are set to increase the efficiency and reduced the negative impact on

nature.

Company Profile

Company Name: R-Tek Mould

Office and Works: Street No. 7 1/2, Hargobind Nagar, Industrial Area - C, Ldh.

Email: [email protected]

Website: www.rtekmould.com, www.autocrat.co.in

Business Type: Manufacturer, Exporter, Service Provider

Year of Establishment: 1985

Annual Turnover: Up to Rupees 1 Crore (approx.)

Export Percentage: Up to 20 per cent

Primary Competitive Advantage:

Experienced Research and Development Department

Good Financial Position and Total Quality Management

Large Product Line

No. of Employees: 50-60 People

Major Markets: Indian Subcontinent, Australia, New Zealand, East Asia, North

Africa, Caribbean

CONTENTS

PREFACE……………….

INTRODUCTION OF FINANCIAL ANALYSIS

OBJECTIVES OF FINANCIAL ANALYSIS

IMPORTANCE OF FINANCIAL ANALISIS

COMPANY PROFILE

HISTORY OF COMPANY

MISSION OF COMPANY

TURNOVER REPORT OF COMPAY

RESEARCH METHODOLOGY:-INTRODUCTION

OBJECTIVES OF STUDY

INTRODUCTION

FINANCIAL ANALYSIS

RATIO ANALYSIS

HYPOTHESIS

RESEARCH PROCESS

OBSERVATION

ANALYSIS OF DATA

ANALYSIS OF DATA $ DATA INTERPRETATION

OBJERVATION & CONCLUSION

SUGGESTIONS AND LIMITATIONS

BIBLOGRAPHY

PREFASE

The project assigned to me was to study the financial health of any organization in

the country. I decided to choose one of India’s biggest companies in a sector that has

rapidly grown over the last few years and a company where leaders like Mr.

Ravinder Singh are made, or rather, a company that has been also made by Mr

Ravinder Singh.

Through a through industry and a company analysis, I am to understand the

external factors influencing the company and its decision making. Later, I try and

evaluate the various ratios to appreciate their impact on company’s performance

over the last three years.

The financial statements of last three years are identified, along with the analysis of

various components of the company vis-à-vis other competitors with the same

segment.

Critical decisions of distributing dividends, Issue of bonus debentures and other

current news are analyzed and their impact on the bottom line of the company is

assessed.

As a benchmark, I finally, I also study the accounting policy of the company is also

studied with respect to valuation of Fixed Asset, Inventory, Investment and

Employee related liabilities for the FY 2011.

OBJECTIVES OF STUDY

To have a deeper insight into the comparative study of R-TEK

mould using ratios.

To know about the past and present trends as well as predict

about the future.

RESEARCH METHODOLOGY

Research problem:

To access the comparative financial position of the company and suggest remedial

measure to improve the financial position in future.

Research objective:

The main objective of this project is to have a deeper insight

into the financial position if the company and make

comparative analysis of balance sheet and profit and loss

account of the company with the major competitor of the

market

.

The study will help us to know about the past and present

trends as well as predict about the future.

Research design:

Research design is a best plan or a model for the collection of formal information.

Descriptive type of research has been used; it is concerned with describing the characteristics of a particular individual or a group.

Collection of data :

Basically there are two sources through which data is collected i.e., primary and

secondary sources.

But in my project report only secondary data is used.

Secondary data :

Secondary data means data that is already available i.e., they refer to that data

which have already been collected. This method involves the study of various

documents available in the organization which may

Contain information required for the study. It includes the following documents:

Annual report and financial statement of the company.

FINANCIAL ANALYSIS

Financial analysis refers to an assessment of the viability, stability and profitability

of a business sub-business or project.

It is performed by professionals who prepare reports using ratios that make use of

information taken from financial statements and other reports. These reports are

usually presented to top management as one of their bases in making business

decisions. Based on these reports, management may:

Continue or discontinue its main operation or part of its business;

Make or purchase certain materials in the manufacture of its product;

Acquire or rent/lease certain machineries and equipment in the production of its

goods;

Issue stocks or negotiate for a bank loan to increase its working capital.

Make decisions regarding investing or lending capital;

Other decisions that allow management to make an informed selection on

various alternatives in the conduct of its business.

INTRODUCTION OF FINANCIAL ANALYSIS

Financial statements are prepared primarily for decision-making. They

play a dominant role in setting the framework of managerial decisions. But the

information provided in financial statements is not an end in itself as no meaningful

conclusion can be drawn from these statements alone. The information provided in

financial statements is of immense use in making decisions through analysis and

interpretation of financial statements. Financial analysis is the process of identifying

the financial strength and weaknesses of the firm by properly establishing

relationship between the items of balance sheet and profit and loss account.’ There

are various methods or techniques used in analyzing financial statements, such as

comparative statements, trend analysis, common-size statements, schedule of

changes in working capital, funds flow and cash flow analysis, cost-volume-profit

analysis and ratio analysis.

MEANING OF

FINANCIAL ANALYSIS

The term ‘financial analysis’, also known as analysis

and interpretation of financial statements’, refer to the process of determining

financial strength and weaknesses of the firm by establishing strategic relationship

between the items of the balance sheet, profit and loss account and other operative

data. Financial statement analysis is largely a study of relationship among the

various financial factors in a business as disclosed by a single set-of statements and

study of the trend of these factors as shown in a series of statements”.

The purpose of financial analysis is to diagnosis the information

contained in financial statements so as to judge the profitability and financial

soundness of the firm. Just like a doctor examines his patient by recording his body

temperature, blood pressure, etc before making a conclusion regarding the illness

and before giving his treatment, a financial analyst analysis the financial statements

with various tools of analysis before commenting upon the financial health or

weakness of an enterprise. By financial statements we mean two statements:-

(1) Profit ant loss account or Income Statement.

(2) Balance sheet or Position Statement.

OBJECTIVES

FINANCIAL ANALYSIS

These are main objectives of financial analysis:-

(1) Measuring the profitability: - The main objective of a business is to earn a

satisfactory return on the funds invested in it. Financial analysis helps in

ascertaining whether adequate profits are being earned on the capital

invested in the business or not. It also helps in knowing the capacity to pay

the interest and dividend.

(2) Indicating the trend of Achievement: - Financial Statements of the previous

years can be compared and the trend regarding various expenses, purchases

sales, gross profit etc. can be ascertained. Values of assets and liabilities can

be compared and the future prospects of the business can be envisaged.

(3) Assessing the growth potential of the business:- The trend and other analysis

of the business provides sufficient information indicating the growth

potential of the business

(5) Assessing the growth potential of the business:-The trend and other analysis of

the business provide Sufficient information indicating the growth potential of

the business.

(6) Assess solvency of the firm: - The different tools of an analysis tell us weather

The firm has sufficient funds to meet its short term and long term liabilities.

Goals

Financial analysts often assess the firm's:

1. Profitability - Its ability to earn income and sustain growth in both short-

term and long-term. A company's degree of profitability is usually based on the

income statement, which reports on the company's results of operations;

2. Solvency - its ability to pay its obligation to creditors and other third

parties in the long-term;

3. Liquidity - its ability to maintain positive cash flow, while satisfying

immediate obligations; Both 2 and 3 are based on the company's balance sheet, which

indicates the financial condition of a business as of a given point in time.

4. Stability- The firm’s ability to remain in business in the long run, without

having to sustain significant losses in the conduct of its business. Assessing a

company’s stability requires the use of the income statement and the balance sheet,

as well as other financial and non-financial indicators.

Methods

Financial analysts often compare financial ratios (of solvency, profitability, growth,

etc.):

Past Performance - Across historical time periods for the same firm (the

last 5 years for example),

Future Performance - Using historical figures and certain mathematical

and statistical techniques, including present and future values, This extrapolation

method is the main source of errors in financial analysis as past statistics can be

poor predictors of future.

Comparative Performance - Comparison between similar firms.

These ratios are calculated by dividing a (group of) account balance(s), taken from

the balance sheet and / or the income statement, by another, for example:

Net income / equity = return on equity (ROE)

Net income / total assets = return on assets (ROA)

Stock price / earnings per share = P/E ratio

Comparing financial ratios is merely one way of conducting financial analysis.

Financial ratios face several theoretical challenges

They say little about the firm's prospects in an absolute sense. Their insights about

relative performance require a reference point from other time periods or similar

firms

They say little about firm’s prospects in an absolute sense. Their insights about

relative performance require a reference point from other time periods or

similar firms.

One ratio holds little meaning. As indicators, ratios can be logically interpreted

in at least two ways. One can partially overcome this problem by combining several

related ratios to paint a more comprehensive picture of the firm's performance.

Seasonal factors may prevent year-end values from being representative. A

ratio's values may be distorted as account balances change from the beginning to

the end of an accounting period. Use average values for such accounts whenever

possible.

Financial ratios are no more objective than the accounting methods employed.

Changes in accounting policies or choices can yield drastically different ratio values.

They fail to account for exogenous factors like investor behavior that are not

based upon economic fundamentals of the firm or the general economy

(fundamental analysis).

Financial analysts can also use percentage analysis which involves reducing a series

of figures as a percentage of some base amounts. For example, a group of items can

be expressed as a percentage of net income. When proportionate changes in the

same figure over a given time period expressed as a percentage is known as

horizontal analysis. Vertical or common-size analysis reduces all items on a

statement to a “common size” as a percentage of some base value which assists in

comparability with other companies of different sizes. Another method is

comparative analysis. This provides a better way to determine trends. Comp-motive

analysis presents the same information for two or more time periods and is

presented side-by side to allow for easy analysis.

Types of Financial Analysis

There are various types of financial analysis into different categories. But

we are classified financial statements into two categories

(1) ON THE BASIS OF MATERIAL USED

(1) External Analysis

(2) Internal Analysis

(2) ON THE BASIS OF MODUS OPERANDI

(1) Horizontal Analysis

(2) Vertical Analysis

METHODS OF

FINANCIAL ANALYSIS

The analysis and interpretation of financial statements is

used to determine the financial position and result of operations as well. A number

of methods and devices are used to study the relationship between different

statements.

The following methods of analysis are generally used:

(1) Comparative statements

(2) Common – size statements

(3) Trend Analysis

(4) Fund flow statements

(5) Cash flow statements

(6) Ratio analysis

COMPARATIVE STATEMENTS

The comparative financial statements are statements of

financial position at different periods; of time. The elements of financial position are

shown in a comparative form so as to give an idea financial position at two or more

periods. Any statement prepared in a comparative form will be covered in

comparative statements. From practical point of view, generally two statements are

prepared in comparative form for financial analysis purposes. Not only the

comparison of the figure of two periods but also be relationship between balance

sheet and income statements enables an in depth study of financial position or

operative results. The comparative statements are show:

(1) Absolute figure (rupee amount)

(2) Change in absolute figure (increase or decrease in absolute figure)

(3) Absolute data in term of percentages.

(4) Increase or decrease of percentage.

The two comparative statements are:-

(1) Comparative Balance sheet

(2) Comparative Income statement

(1) COMPARATIVE BALANCE SHEET

The comparative balance sheet analysis is the study of

the trend of same items, group of items and computed item in two or more balance

sheets of the same business enterprise on different dates. The change in periodic

balance sheet items reflects the conduct of business.

The changes can be observed by comparison of the balance sheet at the beginning

and at the end of a period and these changes can help in forming an opinion about

the progress of an enterprise. The comparative balance sheet has two columns for

the data of original balance sheets. A third column is used to show increase in

figures. The fourth column may be added for giving percentages of increase or

decrease.

Guidelines for Interpretation of Comparative Balance Sheet

While interpretation Comparative Balance Sheet the interpreter is expected

to study the following aspects:

(1) Current financial position and liquidity position.

(2) Long – term financial position.

(3) Profitability of the concern

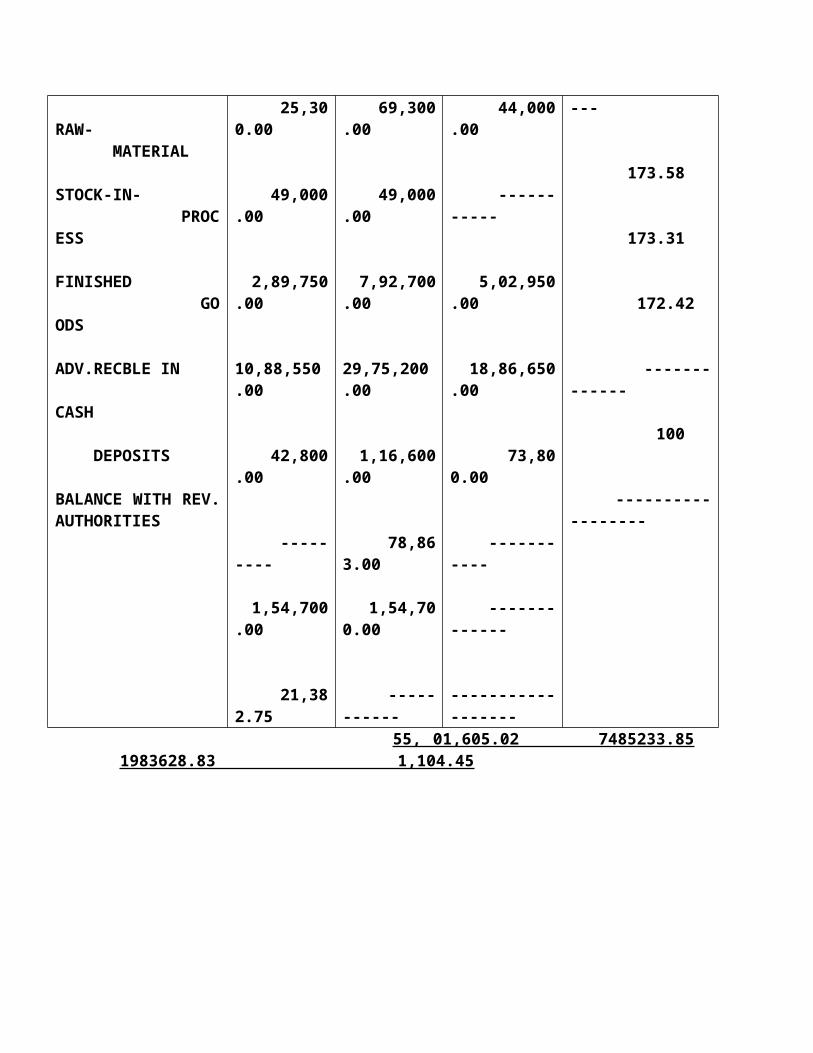

The following is the Balance Sheet of a concern of R-TEK MOULD

for the year 2010 and 2011. Prepare a comparative Balance Sheet

and study the financial position of a concern.

Balance Sheet As on 31st March

LIABILITIES Amount Amount ASSETS Amount Amount 2010 2011 2010 2011

CAPITAL

UNSECURED LOAN

SECURED LOANS(FROM BANK)

SECURED LOANS (FROM OTHERS)

SUNDRY CREDITOR

OTHER PROVISION

10,81,946.77

6,35,181.00

8,93,068.18

11,01,708.07

15,99,493.00

1,90,208.00

23,33,636.95

10,15,181.00

20,95,300.22

--------

19,65,313.60

75,802.08

FIXED ASSETS

CASH IN HAND

BANK BALANCE

SUNDRY DEBTORS

STORES/ CONSUMABLE

INVESTMENTS

RAW- MATERIAL

STOCK-IN- PROCESS

FINISHED GOODS

ADV.RECBLE IN CASH

DEPOSITS

BALANCE WITH REV. AUTHORITIES

20,29,970.23

71,739.73

42,270.91

16,86,141.40

25,300

49,000

2,89,750.00

10,88,550.00

42,800.00

---------

1,54,700.00

21,382.75

24,03,040.23

4,81,272.11

73,336.81

2,91,221.70

69,300

49,000.00

7,92,700.00

29,75,200.00

1,16,600.00

78,863.00

1,54,700.00

-----------

COMPARATIVE BALANCE SHEET

ASSETS 2010 2011 INCREASE/ DECREASE

PERCENTAGE

FIXED ASSETS

CASH IN HAND

BANK BALANCE

SUNDRY DEBTORS

STORES/ CONSUMABLE

INVESTMENTS

RAW- MATERIAL

STOCK-IN- PROCESS

FINISHED GOODS

ADV.RECBLE IN CASH

DEPOSITS

BALANCE WITH REV. AUTHORITIES

20,29,970.23

71,739.73

42,270.91

16,86,141.40

25,300.00

49,000.00

2,89,750.00

10,88,550.00

42,800.00

---------

1,54,700.00

21,382.75

24,03,040.23

4,81,272.11

73,336.81

2,91,221.70

69,300.00

49,000.00

7,92,700.00

29,75,200.00

1,16,600.00

78,863.00

1,54,700.00

-----------

3,73,070.00

4,09,532.38

31,065.90

-1394922.70

44,000.00

-----------

5,02,950.00

18,86,650.00

73,800.00

-----------

-------------

------------------

18.38

570.86

77.14

-82.73

173.91

----------

173.58

173.31

172.42

-------------

100

------------------ 55, 01,605.02 7485233.85 1983628.83 1,104.45

COMPARAIVE BALANCE SHEET

LIABILITIES 2010 2011 INCREASE/ DECREASE

PERCENTAGE

CAPITAL

UNSECURED LOAN

SECURED LOANS(FROM BANK)

SECURED LOANS (FROM OTHERS)

SUNDRY CREDITOR

OTHER PROVISION

10,81,946.77

6,35,181.00

8,93,068.18

11,01,708.07

15,99,493.00

1,90,208.005501605.02

23,33,636.95

10,15,181.00

20,95,300.22

--------

19,65,313.60

75,802.0874,85,233.85

12,51,690.95

3,80,000.00

1,20,22,322.04

--------------

365820..60

1,14,405.92 1983628.92

115.68

134.62

-----------

22.87

-60.15 601.72

INTERPRETATION:-

(1) The comparative balance sheet of company R-TEK reveals that during 2011

there has been increased in fixed assets of 3,73,070 i.e. 18.38% while capital has

been increased during 2011 12,51,690 i.e. 115.68%. This fact depicts that the policy

of the company is to purchase fixed assets from the long-term sources of finance

thereby not affecting the working capital.

(2) The current assets have been increased by 15, 53, and 078. 58 and cash are

also increased and liabilities are less increase compare to assets. Current liabilities

also have been less increase. This further confirms that the company has raised

long-term finances even for the current assets resulting into improvement in

liquidity position of the company.

(3) The overall financial position of the company is satisfactory.

(2) COMMPARATIVE

INCOME STATEMENT

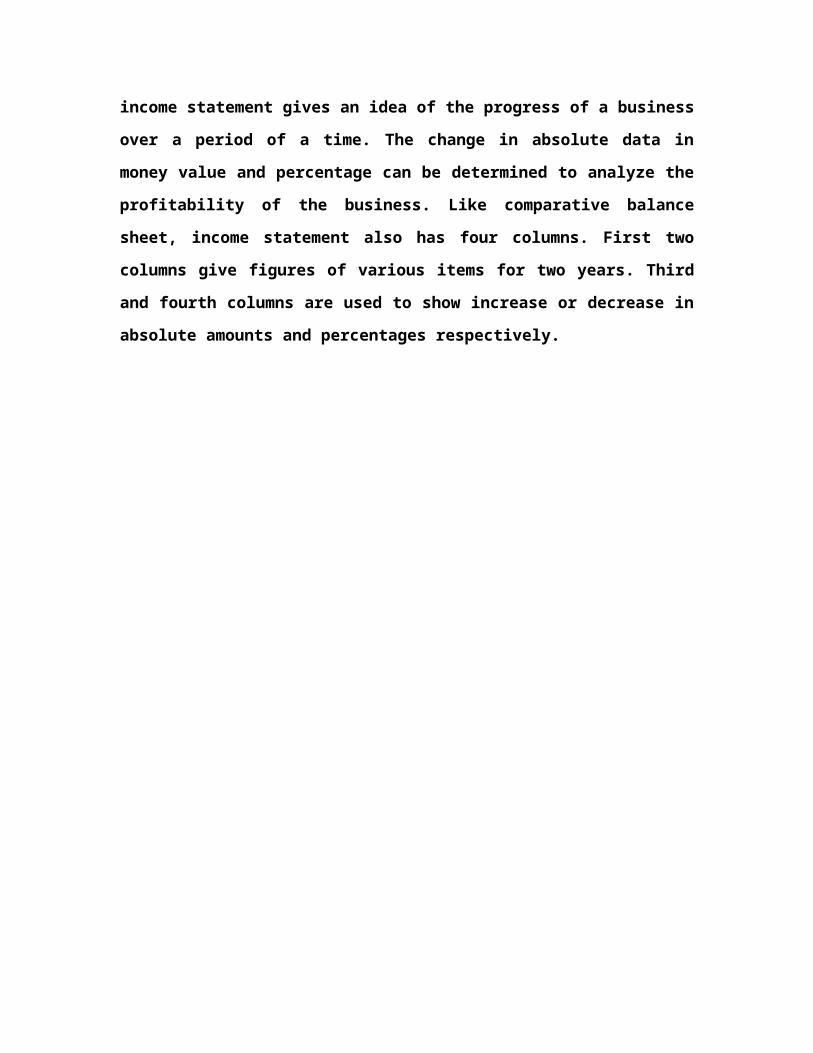

The Income statement gives the results of the operations of a

business. The comparative income statement gives an idea of the progress of a

business over a period of a time. The change in absolute data in money value and

percentage can be determined to analyze the profitability of the business. Like

comparative balance sheet, income statement also has four columns. First two

columns give figures of various items for two years. Third and fourth columns are

used to show increase or decrease in absolute amounts and percentages respectively.

Guidelines for Interpretation of

Income Statements

The analysis and interpretation of income statement will involve the

following steps:

(1) The increase or decrease in sales should be compare with the increase or

decrease in cost of goods sold. An increase in sale will not be always meaning an

increase in profit. The amount of gross profit should be situated in the first step.

(2) The second step of analysis should be the study of operational profit. The

operating expenses such as office and administrative expenses, selling and

distribution expenses should be deducted from gross profit to find out operating

profit. An increase in operating profit will result from the increase in sale position

and control of operating expenses. A decrease in operating profit may be due to an

increase in operating expenses or decrease in sale.

(3)The increase or decrease in net profit will give an idea about the overall

profitability of the concern. Non-operating expenses such as interest paid, losses

from sale of assets, writing of deferred expenses, payment of tax, etc. decrease the

figure of operating profit. When all non-operating expenses are deducted from

operational profit, we get a figure of net profit.

The following information prepares a comparative Income Statement of R-TEK MOULD:-

2010 2011

SALES

COST OF GOODS SOLD

INDIRECT EXPENSES

RATE OF INCOME TAX

70,22,084.40

63,11,825.00

9,51,014.44

-------------

77,48,787.50

62,64,919.00

9,65,034.15

---------------

COMPARATIVE INCOME STATEMENT

PARTICULARS AMOUNT 2010

AMOUNT 2011

ABSOLUTECHANGES

PERCENTAGE %

SALES

LESS:- COST OF

GOODS SOLD

GROSS PROFIT

LESS:- INDIRECT

EXPENSES

PROFIT BEFORE

TAX

LESS:- INCOME

TAX

NET PROFIT

AFTER TAX

70,22,084.40

63,11,825.0014,91,173.60

9,51,014.44

5,40,160.00

----------

5,40,160.00

77,48,787.50

62,64,919.0014,83,868.27

9,65,034.15

5,18,834.20

----------

5,18,834.20

7,26,706.00

-46906.00 7305.33

14,020.00

21325.00

----------

21325.00

10.35

0.74 0.10 0.20

0.30

----------

0.30

INTERPRETATION:-

(1) The comparative income statement given above revel that there has been

increase in net sales of 10.35% while the cost of goods sold has decreased nearly by

0.74% thereby resulting in an decrease in gross profit of 0.10% . The indirect

expenses are increased by 0.20% and gross profit not sufficient to compensate for

the increase in indirect expenses. Net profit also decreased by 0.30%. It may be

conducted that not a sufficient progress in the company and the overall financial

position of the company is not good.

COMMON- SIZE STATEMENT

The common-size statements, balance sheet and income statement

are shown in analytical percentages. The are shown as percentage of total

assets, total liabilities are total sales. The total assets are taken as 100 and

different assets are expressed as a percentage of the total. Similarly, various

liabilities are taken as a part of total liabilities. These statements are also

known as component percentage or 100 percent statements because every

individual item is stated as a percentage of total 100. The short-coming in

comparative statements ant trend percentages where changes in items could

not be compared with the total have been covered up. The analyst is able to

assess the figure in relation to total value. The common-size statements may

be prepared in the following way:

(1) The total of assets or liabilities is taken as 100.

(2) The individual assets are expressed as a percentage of total assets 100

and different liabilities are calculated in relation to total liabilities. For

example, if total assets are rest. 5 laths and inventory value is Rs. 50000, then

it will be 10% of total assets [50000*100/500000].

(1) COMMON-SIZE BALANCE SHEET

A statement in which balance sheet items are expressed as the ratio of

each asset to total assets and the ratios of each liability are expressed as a ratio of

total liabilities is called common-size balance sheet. For example, following assets

are shown in a common-size balance sheet:

Rs. Percentage

Cash in hand and at bank 5,000 2.50

Sundry debtors 20,000 10.00

Stock 25,000 12.50

Land and building 50,000 25.00

Plant and machinery 1, 00,000 50.00

Total Assets: 2, 00,000 100.00

The total figure of assets rest. 2, 00,000, is taken as 100 and all other

assets are expressed as a percentage of total assets. The relation of each asset to total

assets is expressed in the statement. The relation of each liability to total liabilities is

similarly expressed.

The following is the Balance Sheet of a concern of R-TEK MOULD for the year 2010 and 2011. Prepare a common-size Balance Sheet and study the financial position of a concern.

Balance Sheet As on 31st March

LIABILITIES Amount Amount ASSETS Amount Amount 2010 2011 2010 2011

CAPITAL

UNSECURED LOAN

SECURED LOANS(FROM BANK)

SECURED LOANS (FROM OTHERS)

SUNDRY CREDITOR

OTHER PROVISION

10,81,946.77

6,35,181.00

8,93,068.18

11,01,708.07

15,99,493.00

1,90,208.00

23,33,636.95

10,15,181.00

20,95,300.22

--------

19,65,313.60

75,802.08

FIXED ASSETS

CASH IN HAND

BANK BALANCE

SUNDRY DEBTORS

STORES/ CONSUMABLE

INVESTMENTS

RAW- MATERIAL

STOCK-IN- PROCESS

FINISHED GOODS

ADV.RECBLE IN CASH

DEPOSITS

BALANCE WITH REV. AUTHORITIES

20,29,970.23

71,739.73

42,270.91

16,86,141.40

25,300

49,000

2,89,750.00

10,88,550.00

42,800.00

---------

1,54,700.00

21,382.75

24,03,040.23

4,81,272.11

73,336.81

2,91,221.70

69,300

49,000.00

7,92,700.00

29,75,200.00

1,16,600.00

78,863.00

1,54,700.00

-----------

COMMON-SIZE BALANCE SHEET

ASSETS 2010 PERCENTAGE 2011 PERCENTAGE

FIXED ASSETS

CASH IN HAND

BANK BALANCE

SUNDRY DEBTORS

STORES/ CONSUMABLE

INVESTMENTS

RAW- MATERIAL

STOCK-IN- PROCESS

FINISHED GOODS

ADV.RECBLE IN CASH

DEPOSITS

BALANCE WITH REV. AUTHORITIES

20,29,970.23

71,739.73

42,270.91

16,86,141.40

25,300

49,000

2,89,750.00

10,88,550.00

42,800.00

---------

1,54,700.00

21,382.7555,01,605.02

36.90

1.30

0.77

30.65

0.46

0.89

5.27

19.78

0.78

2.81

0.39 100

24,03,040.23

4,81,272.11

73,336.81

2,91,221.70

69,300

49,000.00

7,92,700.00

29,75,200.00

1,16,600.00

78,863.00

1,54,700.00

-----------74,85,233.85

32.10

6.43

0.98

3.89

0.92

0.65

10.59

39.75

1.56

1.05

2.07

----------------------- 100

COMMON-SIZE BALANCE SHEET

LIABILITIES 2010 PERCENTAGE 2011 PERCENTAGE

CAPITAL

UNSECURED LOAN

SECURED LOANS(FROM BANK)

SECURED LOANS (FROM OTHERS)

SUNDRY CREDITOR

OTHER PROVISION

10,81,946.77

6,35,181.00

8,93,068.18

11,01,708.07

15,99,493.00

1,90,208.0055,01,605.02

19.67

16.23

20.00

29.07

3.46 100

23,33,636.95

10,15,181.00

20,95,300.22

--------

19,65,313.60

75,802.08 74,85,233.85

31.17

1.56

8.63

---------------

26.25

1.01 100

INTERPRETATION

(1)

COMMON-SIZE INCOME STATEMENT

The items in income statement can be shown as percentage

of sales to show the relation of each item to sales. A significant relationship can be

established between items of income statement and volume of sales. The increase in

sales will certainly increase selling expenses and not administrative or financial

expenses. In case the volume of sales increases to a considerable extent,

administrative and financial expenses may go up. In case the sales are declining, the

selling expenses should be reduced at once. So, a relationship is established between

sales and other items in income statement and this relationship is helpful in

evaluating operational activities of the enterprise.

The following information prepares a common-size Income Statement of R-TEK MOULD:-

2010 2011

SALES

COST OF GOODS SOLD

INDIRECT EXPENSES

RATE OF INCOME TAX

70,22,084.40

63,11,825.00

9,51,014.44

-------------

77,48,787.50

62,64,919.00

9,65,034.15

---------------

COMMON-SIZE INCOME STATEMENT

PARTICULARS AMOUNT 2010

PERCENTAGE %

AMOUNT 2011

PERCENTAGE

SALES

LESS:- COST OF

GOODS SOLD

GROSS PROFIT

LESS:- INDIRECT

EXPENSES

PROFIT BEFORE

TAX

LESS:- INCOME

TAX

NET PROFIT

AFTER TAX

70,22,084.40

63,11,825.0014,91,173.60

9,51,014.44

5,40,160.00

----------

5,40,160.00

100.00

78.77 21.23

13.54

7.69

------

7.69

77,48,787.50

62,64,919.0014,83,868.27

9,65,034.15

5,18,834.20

----------

5,18,834.20

100.00

80.85 19.15

12.45

6.70

-------

6.70

INTERPRETATION

(1) The sale has been increased in 2011 as compare to 2010 but

percentage of gross profit to sales has gone down.

(2) The decrease in cost of sales as a percentage of sales has down the

profitability from 21.23 to 19.15.

(3) The indirect expenses are increased in 2011 as compare to 2010

So ratio is also goes down from 13.54% to 12.45%.

TREND ANALYSIS

The financial statement may be analyzed by computing

trends of series of information. This method determines the direction upwards or

downwards and involves the computation of the percentage relationship that each

statement item bears to the same item in base year. The information for a number of

years is taken up and one year, generally the first year, is taken as a base year. The

figure of base year are taken as 100 and trend ratios for

Other years are calculated on the basis of base year. The analyst is able to see the

trend of figures, whether upward or downward. For example, if sales figures for the

year 2003 to 2008 are to be studied, then sales of 2003 will be taken as 100 and the

percentage of sales for all other will be calculated in relation to the base year, i.e.,

2003 suppose the following trends are determined.

2003 100

2004 120

2005 110

2006 125

2007 135

2008 140

The trend of sales shows that sales have been more in all the years since 2003.

Procedure for Calculating Trends

(1) One year is taken as a base year. Generally, the first or last year taken as a

Base year.

(2) The figure of base year is taken as 100.

(3) Trend percentages are calculated in relation to base year. If a figure in other

year is less then the figure of base year the trend percentage will be less then

100 and it will be more then 100 if figure is more then base year figure. Each

year‘s figure is divided by the base year’s figure.

The interpretation of trend analysis involves a cautious study.

The mere increase or decrease in trend percentage may give misleading

Results if studied in isolation. An increase of 20% in current assets may be

Treated favorable. If this increase in current assets is accompanied by an

Equivalent increase in current liabilities, then this increase will be

unsatisfactory. The increase in sales may not increase profits if the cost of

Production has also gone up.

FUNDS FLOW STATEMENT

The basic financial statements, the balance sheet and profit and loss

account or income statement of business, reveal the net effect of the various

transactions on the operational and financial position of the company. The balance

sheet gives a summary of the assets and liabilities of an undertaking at a particular

point of time. It reveals the financial status of the company. The assets side of a

balance sheet shows the deployment of resources of an undertaking while the liabilities

side indicates its obligations the manner in which these resources were obtained. The

profit and loss account reflects the results of the business operations for a period of

time. It contains a summary of expenses incurred and the revenue realized in an

accounting period.

THE FUNDS FLOW STATEMENT IS A STATEMENT WHICH

SHOWS THE MOVEMENT OF FUNDS AND IS A REPORT OF THE FINANCIAL

OPERATIONS OF THE BUSINESS UNDERTAKING. IT INDICATES VARIOUS

MEANS BY WHICH FUNDS WERE OBTAINED DURING A PARTICULAR

PERIOD AND THE WAYS IN WHICH THESE FUNDS WERE EMPLOYED. IN

SIMPLE WORDS, IT IS A STATEMENT OF SOURCES AND APPLICATIONS OF

FUNDS.

CASH FLOW STATEMENT

Cash plays a very important role in the entire economic life of a

business. A firm needs cash to make payment to its suppliers, to incur day-to-day

expenses and to pay salaries, wages, interest and dividend, etc. In fact, what blood is to

a human body, cash is to business enterprises? It is very essential for a business to

maintain an adequate balance of cash. But many a time a concern operates profitably

and yet it becomes very difficult to pay taxes and dividends. This may be because

(1) Although huge profit have been earned yet cash may not have been received or

(2) Even if cash have been received, it may have drained out (used) for some other

purpose. This movement of cash is of vital important to the management.

CASH FLOW STATEMENT IS A STATEMENT WHICH

DESCRIBES THE INFLOWS (SOURSES) AND OUTFLOWS (USES) OF CASH

AND EQUIVALANTS IN AN ENTERPRISE DURING A SPESIFIED PERIOD OF

TIME. SUCH A STATEMENT ENUMERATES NET EFFECTS OF VARIOUS

BUSINESS TRANSACTIONS ON CASH AND ITS EQUIVALANENTS AND TAKES

INTO ACCOUNT RECEIPT AND DISBURSEMENT OF CASH. A CASH FLOW

STATEMENT SUMMARIESES THE CAUSES OF CHANGES IN CASH POSITION

OF A BUSINESS ENTERPRISES BETWEEN DATES OF TWO BALANCE

SHEETS.

RATIO ANALYSIS

Meaning

Ratio is an expression of relationship of one figure with another it may be defined as

the relationships or proportion that one amount bears to other financial ratios

express arithmetical relationships between two figures or two groups of figures

which are related to other.

Ratio analysis is a technique of analysis and interpretation of financial

statements. It is the process of establishing and interpreting various ratios for

helping in making certain decisions. However, ratio analysis is not an end in itself. It

is only a means of better understanding of financial strength and weakness of a

firm.

OBJECTIVE OF RATIO ANALYSIS

Ratio analysis is the important technique of financial analysis. It can be called as the

heart of financial analysis. The way, in which we estimate the health of our body

through heart beats, similarly through the technique of ratio analysis, estimation

can be made regarding the financial position of a business concern. The main

objectives of ratio analysis are:

1. Relative study: The facts and figures expressed in financial statements if

studied in isolation, may make no sense but if two related items are studied in

comparison to the others may suggest something significant.

2. Conciseness: - with the help of Ratio, large figures or group of figures are

presented precisely so as to make them understandable.

3. Analysis of business activities: On the basis of the comparative study of

ratios, results related to the progress or failure of a business concern can be easily

obtained.

IMPORTANCE OF RATIO ANALYSIS

Ratio analysis is the most important tool of financial analysis:

1. Helpful to management: The ratio analysis is proves to be of significant

value to the management in the process of discharge of its elementary functions such

as planning, co-ordination, communication and control.

2. Helpful in trend analysis: The ratio analysis facilitates a firm to consider the

time dimension into account, i.e. whether the financial position of a firm is showing

any improvement or deterioration over years. This is affected through the use of

trend analysis. With the help of the financial analysis one can ascertain whether the

trend is favorable or unfavorable.

3. Helpful in communication: Through ratio analysis it is possible to know the

changes that had taken place in business between two periods.

4. Useful in comparative study: Ratio analysis is also helps in comparative

study. It helps to make an inter-firm comparison either between the different

departments of a firm or between two firms employed in the identical types of

business or between the same firms.

5. Helpful in determining the standards: Keeping in mind the old ratios and

present operating efficiency, the standard can be fixed. In this way ratio analysis is

considered to be the essential part of budgetary control and standard costing.

6. Helpful in effective control: On the basis of ratios, by establishing standards

the effective control can be exercised upon the activity of the firm.

On the comparison of standard ratios with actual ratios adverse financial position

can be found out and corrective.

7. Helpful in evaluation of financial soundness: with the help of liquidity,

solvency, profitability and capital gearing ratios is detailed information can be

gathered related to financial soundness of any institutions?

LIMITATIONS OF RATIO ANALYSIS

1. Limited Use of a Single Ratio: A single ratio in itself is meaningless; it does

not furnish a complete picture. In other words, one single ratio used without

reference to other ratios may produce misleading results. Hence, a number of

financial statements. For example, to test the Liquidity, make use of all the

Liquidity ratios.

2. Ignores Qualitative Factors: The ratio facilitates wholly quantitative

analysis only. The qualitative factors which are so important for the successful

functioning of the organization are completely ignored and hence, whatever

conclusion drawn may get distorted. For example, the grant of credit to an

enterprise may depend more upon the character and capacity of the owner than on

the conclusion drawn from the so called Ratio analysis.

3. Only a part of the information needed in the process of decision

taking: It should also be remembered that ratio analysis helps in providing only a

part of the information needed in the process of decision making.

4. Possibility of window-dressing: Ratio depends on figures of the financial

statements. But in most cases, the figures are window dressed. As a result, the

correct picture cannot be drawn up by the ratio analysis.

5. Ignores Qualitative Factors: The ratio facilitates wholly quantitative

analysis only. The qualitative factors which are so important for the successful

functioning of the organization are completely ignored and hence, whatever

conclusion drawn may get distorted. For example, the grant of credit to an

enterprise may depend more upon the character and capacity of the owner than on

the conclusion drawn from the so called Ratio analysis.

6. Limited Use of a Single Ratio: A single ratio in itself is meaningless; it does

not furnish a complete picture. In other words, one single ratio used without

reference to other ratios may produce misleading results. Hence, a number of

financial statements. For example, to test the Liquidity, make use of all the

Liquidity ratios.

Different meaning to accounting terms

Comparisons are also made difficult due to differences in definition of

various terms used in computing ratios.

1. Variations in Accounting Policies: Comparison between two variables

proves worth provided their basis of valuation is identical but in reality it is not

possible.

2. Difficulty in Evolving Standard Ratio: It is very difficult to ascertain the

normal or standard ratio in order to make proper comparison.

3. Historical Analysis: Ratios delve in the past as they are obtaining from the

financial statements which are considered to be historical documents. A financial

analyst is more concerned the probable happenings in the future rather than those

in the past.

4. Effect of price changes are not taken into account: A change in the price

level can seriously affect the validity of comparisons of ratios computed for different

time periods.

5. Personal bias: Ratios are only means of financial analysis and not end in itself.

They can be affected with the personal ability and bias of the analyst.

CLASSIFICATION OF FINANCIAL RATIOS

1. Liquidity Ratios

2. Capital Structure Ratios

3. Activity or Turnover Ratios

4. Profitability or Profit Earning Capacity

ANALYSIS AND INTERPRTATION

KEY RATIOS:-

(1) CURRENT RATIO

(2) LIQUID RATIO

(3) STOCK TURNOVER RATIO

(4) ABSOLUTE LIQUID RATIO

(5) GROSS PROFIT RATIO

(6) NET PROFIT RATIO

(7) FIXED ASSETS TURNOVER RATIO

(8) TOTAL ASSETS TURNOVER RATIO

(9) WORKING CAPITAL TURNOVER RATIO

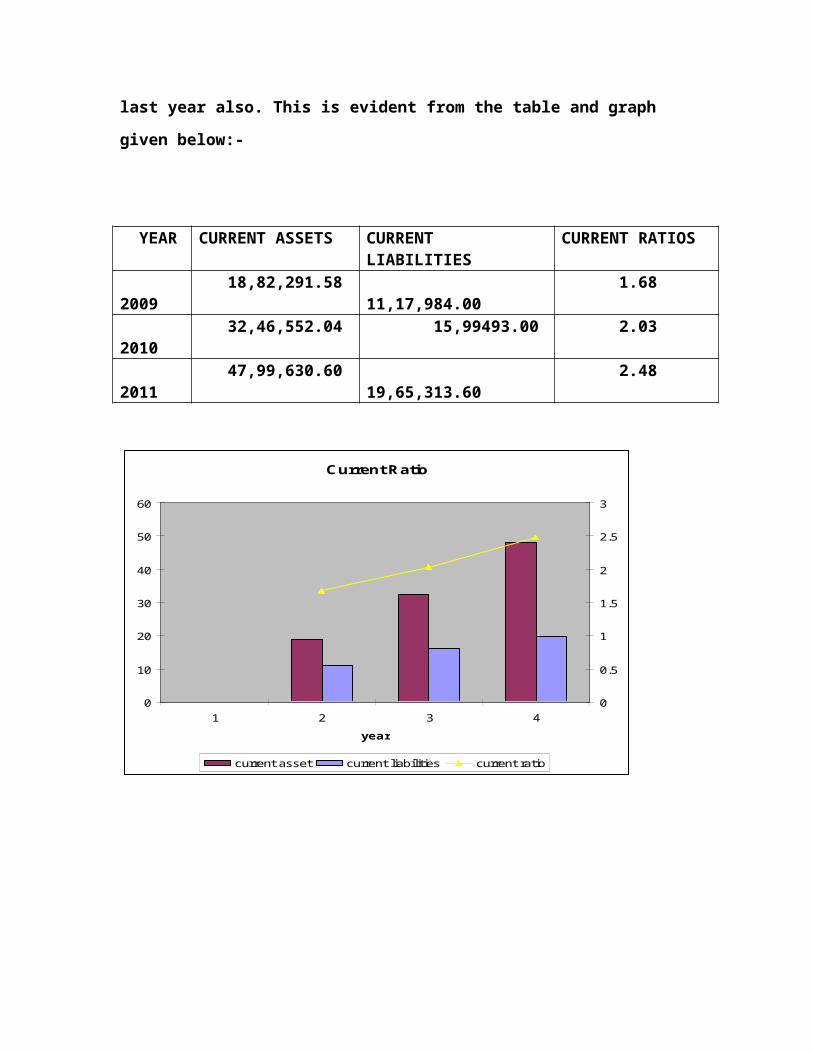

(1) CURRENT RATIO:-

Current ratio is defined as an indicator of short-term debt paying ability of a

company. It is determined by dividing current assets by current liabilities. The

higher the ratio, it is believed that, the more liquid the company.

CURRENT RATIO = CURRENT ASSETS

CURRENT LIBILITIES

Here we observe that the current ratio of R-TEK MOULD is increase in

FY 2009 and 2010 and increase in last year also. This is evident from the table and

graph given below:-

YEAR CURRENT ASSETS

CURRENT LIABILITIES

CURRENT RATIOS

2009 18,82,291.58 11,17,984.00 1.68 2010 32,46,552.04 15,99493.00 2.03 2011 47,99,630.60 19,65,313.60 2.48

Current Ratio

0

10

20

30

40

50

60

1 2 3 4

year

0

0.5

1

1.5

2

2.5

3

current asset current liabilities current ratio

(2) LIQUID RATIO:-

Liquid Ratio also known as Quick Ratio or Acid test ratio is

more rigorous test of liquidity than the current ratio. The term ‘liquidity’ refers to

the ability of a firm to pay its short- term obligations as and when they become due.

Liquid ratio may be defined as the relationship between current or liquid assets or

current or liquid liabilities. An asset is said to be liquid if it can be converted into

cash within a short period without loss of value. It is determined by dividing liquid

assets by current liabilities.

LIQUID RATIO= LIQUID ASSETS

CURRENT LIBILITIES

Here we observe that the liquid ratio of R-TEK MOULD is

increase in FY 2009 and 2010 but decrease in last year. This is evident from the

table and graph given below:-

YEAR LIQUID ASSETS CURRENT LIABILITIES

LIQUID RATIOS

2009 6,15,691.58 11,17,984.00 0.55 2010 18,00,152.04 15,99,493.00 1.125

2011 19,65,313.62 19,65,313.60 0.43

liquid ratio

0

10

20

30

40

50

60

70

1 2 3 4

year

0

0.2

0.4

0.6

0.8

1

1.2

liquid asset current liabilities liqud ratio

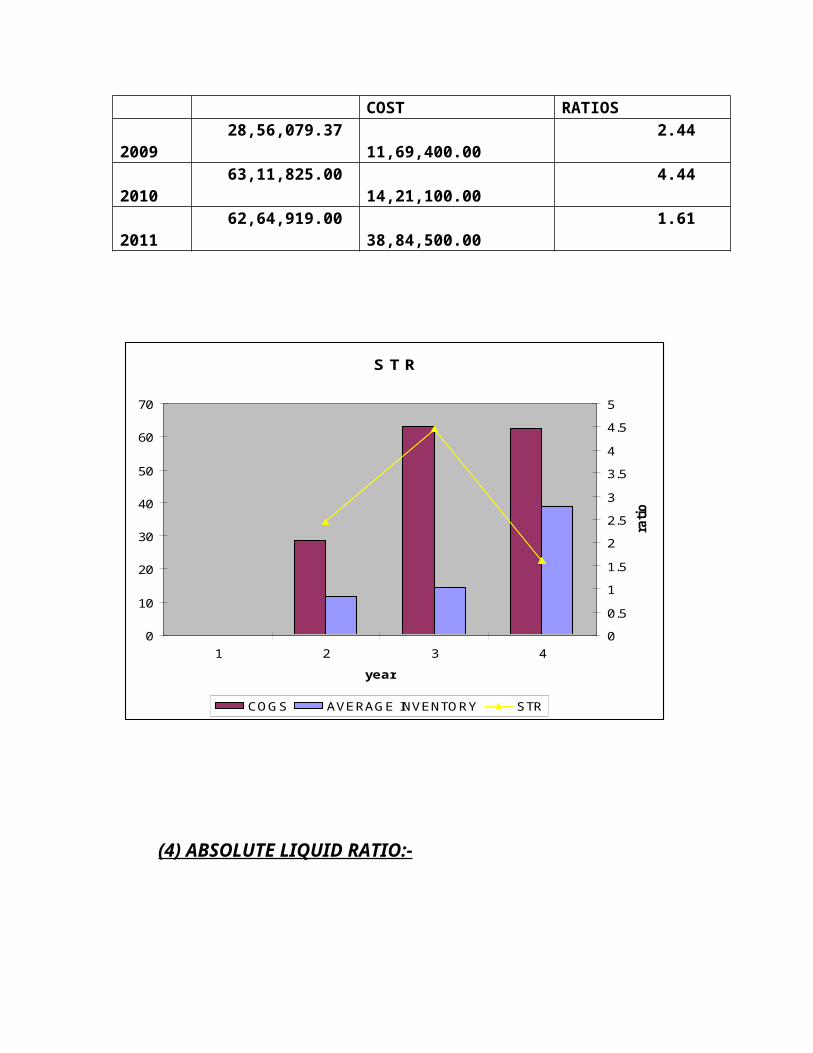

(3) STOCK TURNOVER RATIO:-

Stock turnover ratio is also known as inventory turnover

ratio is normally calculated as sales/average inventory or cost of goods sold/average

inventory. It would indicate whether inventory has been efficiently used or not. The

purpose is to see whether only the required minimum funds have been locked up in

inventory. Inventory turnover ratio indicates the number of times the stock have

been turned over during the period of times the stock have been turned over during

the period and evaluate the efficiency with which a firm is able to manage its

inventory. It is determined by dividing the cost of goods sold by amount of average

inventory at cost.

STOCK TURNOVER RATIO= COST OF GOODS SOLD

AVERAGE INVENTORY AT COST

Here we observe that the stock turnover ratio of