summary appraisal report

TRANSCRIPT

1

SUMMARY APPRAISAL REPORT

Starn Building and Excess Land

2909 Arctic Boulevard in Anchorage, Alaska

FOR Date of Appraisal

Municipal Light and Power, MOA December 15, 2010

12000 East 1st Ave.

Anchorage, AK

Attn. Mr. James Posey, General Manager

Date of Valuation

December 8, 2010

BBC FILE No. Date of Inspection

10-135 December 8, 2010

BY

Brian Bethard, MAI

General Real Estate Appraiser (Cert. #281)

BLACK-SMITH, BETHARD & CARLSON, LLC

1199 E. Dimond Blvd., Ste. 200

Anchorage, Alaska 99515

Black-Smith, Bethard and Carlson LLC. 2

December 15, 2010

Municipal Light and Power, MOA

12000 East 1st Ave.

Anchorage, AK

Attn. Mr. James Posey, General Manager

RE: SUMMARY APPRAISAL REPORT

Starn Building and Excess Land

2909 Arctic Boulevard

Anchorage, Alaska

Dear Mr. Posey:

In fulfillment of our agreement dated November 24, 2010, we are pleased to transmit

our Summary Appraisal Report of the estimated Market Value in the referenced

property. As a result of our analysis, we have formed an opinion that the market value

of the fee simple interest (as defined in the report), subject to the definitions,

certifications, and limiting conditions set forth in the attached report, as of December 8,

2010 is:

Lot 5A, Block 5 (Starn Building): $1,200,000 Lot 4, Block 5 (Excess Land): $184,000

The value opinion is stated in terms of cash. The market exposure period (looking

backward) and the marketing time (looking forward) are both estimated at one year.

The value opinions reported are qualified by certain definitions, assumptions, limiting

conditions, and certifications. We particularly call your attention to the Assumptions

and Limiting Conditions on page 16.

The narrative appraisal report that follows sets forth the identification of the property,

the assumptions and limiting conditions, pertinent facts about the area and the subject

property, comparable data, the results of the investigation and analyses, and the

reasoning leading to the conclusions reached. This report was prepared in accordance

with the standards and regulations as set forth in USPAP and FIRREA.

The report was prepared for and our professional fee was billed to the Municipality of

Anchorage (MOA). It is intended for use by your internal management, municipal

departments, your auditor and appropriate regulatory authorities.

Sincerely, BLACK-SMITH, BETHARD & CARLSON, LLC

Brian Z. Bethard, MAI

BLACK-SMITH, BETHARD & CARLSON, LLC

Appraisers 1199 E. Dimond, Ste. 200

Anchorage, Alaska 99515

Phone 907-274-4654

Fax: 907-274-0889

E-mail: [email protected]

Black-Smith, Bethard and Carlson LLC. 3

TABLE OF CONTENTS

CERTIFICATION ...................................................................................................... 4

EXECUTIVE SUMMARY ......................................................................................... 5

SUBJECT PHOTOGRAPHS .................................................................................... 7

IDENTIFICATION OF THE PROPERTY ................................................................ 9

NATURE OF THE ASSIGNMENT ........................................................................... 10

SCOPE OF WORK ..................................................................................................... 12

ASSUMPTIONS AND LIMITING CONDITIONS ................................................... 13

AREA DATA .............................................................................................................. 14

NEIGHBORHOOD DESCRIPTION ......................................................................... 16

SITE DESCRIPTION ................................................................................................ 18

IMPROVEMENTS DESCRIPTION .......................................................................... 20

MARKET ANALYSIS ................................................................................................ 23

HIGHEST AND BEST USE ...................................................................................... 26

INCOME APPROACH ............................................................................................... 33

ADDENDA

Engagement Letter

Qualifications of Appraisers

Underlying Assumptions and Limiting Conditions

Black-Smith, Bethard and Carlson LLC. 4

CERTIFICATION

We certify that, to the best of our knowledge and belief...

The statements of fact contained in this report are true and correct.

The reported analyses, opinions, and conclusions are limited only by the reported assumptions

and limiting conditions and are my personal, impartial, and unbiased professional analyses,

opinions, and conclusions.

We have no present or prospective interest in the property that is the subject of this report, and

no personal interest with respect to the parties involved.

We have no bias with respect to the property that is the subject of this report or to the parties

involved with this assignment.

Our engagement in this assignment was not contingent upon developing or reporting

predetermined results.

Our compensation for completing this assignment is not contingent upon the development or

reporting of a predetermined value or direction in value that favors the cause of the client, the

amount of the value opinion, the attainment of a stipulated result, or the occurrence of a

subsequent event directly related to the intended use of this appraisal.

Our analyses, opinions, and conclusions were developed, and this report has been prepared, in

conformity with the Uniform Standards of Professional Appraisal Practice as well as the

requirements of the Code of Professional Ethics and the Standards of Professional Practice of the

Appraisal Institute. The use of this report is subject to the requirements of the Appraisal

Institute relating to review by its duly authorized representatives.

Brian Z. Bethard, MAI made a personal inspection of the property that is the subject of this

report.

No one provided significant real property appraisal assistance to the persons signing this

certification.

As of the date of this report I, Brian Z. Bethard, MAI have completed the continuing education

program of the Appraisal Institute.

Brian Z. Bethard, MAI is certified by the State of Alaska as a General Real Estate Appraiser

(Certificate No. 281).

Brian Z. Bethard, MAI has the appropriate knowledge and experience necessary to complete this

appraisal assignment competently.

Dated this 15th day of December 2010.

Brian Z. Bethard, MAI

General Real Estate Appraiser Cert. # 281

Black-Smith, Bethard and Carlson LLC. 5

EXECUTIVE SUMMARY

Property Appraised

Lot 5A is improved with a 2-story, concrete, steel and wood framed office building

containing a gross floor area of 8,086 SF, constructed in 1983. Lot 4 is vacant excess

land.

Location

2909 Arctic Boulevard, Anchorage, Alaska

Legal Description

Lots 4 and 5A, Block 5 Northern Lights Subdivision

Municipality of Anchorage Tax Identification Numbers

009-032-39 and 04

Owners of Record

Glen Starn Credit Shelter Trust; William and Nancy Starn / TTE

Interests Appraised

Fee simple

Land Area

Lot 4: 7,350 SF (excess land)

Lot 5A: 14,725 SF (improved)

Total: 22,075 SF

Black-Smith, Bethard and Carlson LLC. 6

Improvements

Lot 5A is improved with a 2-story, concrete, steel, and wood framed office building

containing a gross floor area of 8,086 SF, constructed in 1983. Lot 4 is vacant excess

land.

Appraisal Date

December 15, 2010

Date of Inspection and Valuation

December 8, 2010

Zoning

B-3 (General Business District)

Highest and Best Use "As Vacant"

Owner/user commercial development

Highest and Best Use “As Improved”

As is

Estimated Market Value Allocation: Lot 4 (excess land): $184,000 Lo 5A (improved): $1,200,000

*The subject property is encumbered by three short term leases. Lease documents were

not provided and information was inadequate to render an opinion of value of the

leased fee estate. If lease documents are made available we retain the right to amend

this report.

Black-Smith, Bethard and Carlson LLC. 7

SUBJECT PHOTOGRAPHS (December 8, 2010)

Northeast at subject Northwest at subject

North on Arctic, sub. to right West down W. 30th Avenue, sub to right

Interior first floor First floor restroom

Black-Smith, Bethard and Carlson LLC. 8

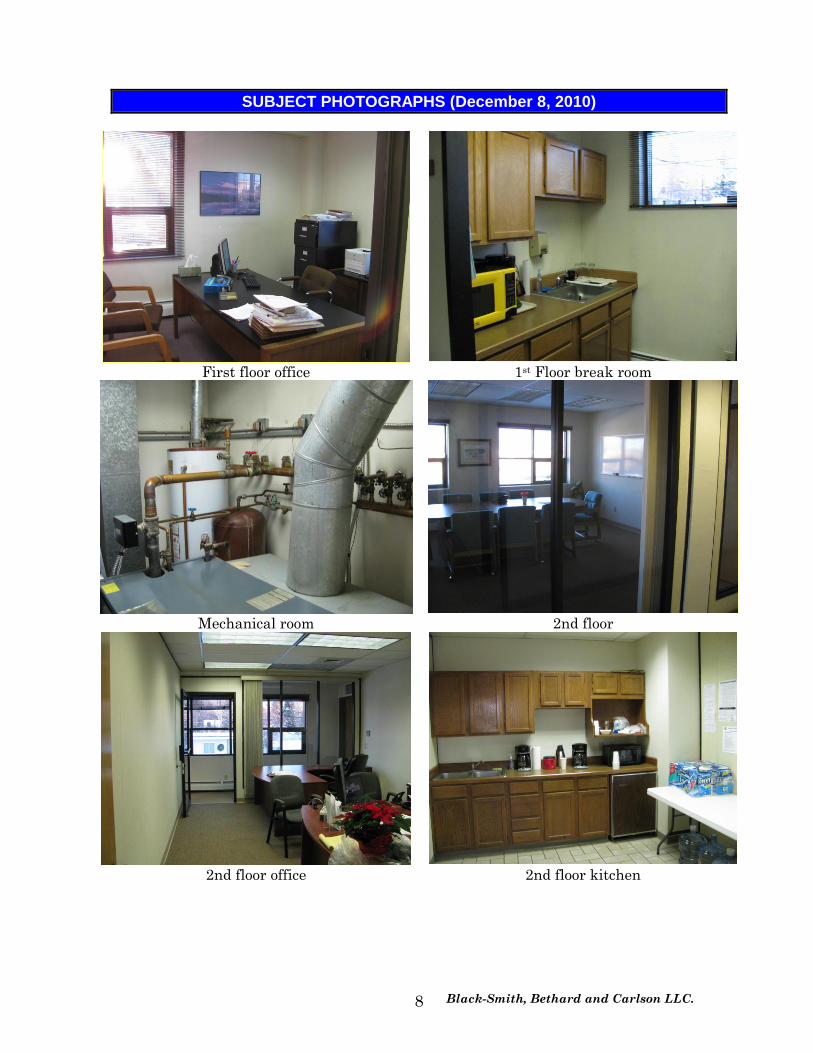

SUBJECT PHOTOGRAPHS (December 8, 2010)

First floor office 1st Floor break room

Mechanical room 2nd floor

2nd floor office 2nd floor kitchen

Black-Smith, Bethard and Carlson LLC. 9

IDENTIFICATION OF THE PROPERTY

Lot 5A is improved with a 2-story, concrete, steel and wood framed office building

containing a gross floor area of 8,086 SF, constructed in 1983. Lot 4 is vacant excess

land.

The property is legally described as Lots 4 and 5A, Block 5 Northern Lights

Subdivision. The property contains an area of 22,075 SF.

The Municipality of Anchorage tax identification numbers are 009-32-39 and 04.

Owners of Record

Glen Starn Credit Shelter Trust; William and Nancy Starn / TTE

Property History

There have been no known sales of the subject during the past three years. There is a

pending sales agreement for $3.5 to MOA, Municipal Light and Power. (see addenda)

The sale price includes the subject and three single family residences with no break

down provided. The owner wants to lease but will sell for the stipulated price. The

property was not marketed and the buyer is motivated.

Lot 5A

Lot 4

Black-Smith, Bethard and Carlson LLC. 10

NATURE OF THE ASSIGNMENT

Client

Municipal Light and Power, MOA

12000 East 1st Ave.

Anchorage, AK

Attn. Mr. James Posey, General Manager

Cc. Mio Johnson, Chief Engineer

Purpose of the Appraisal and Property Rights Appraised

The purpose of the appraisal is to estimate the market value of the fee simple1 interest

as of December 8, 2010.

Market Value2 is defined as:

"The most probable price, which a property should bring in a competitive and open

market under all conditions requisite to a fair sale, the buyer and seller, each acting

prudently, and knowledgeably, and assuming the price is not affected by undue

stimulus. Implicit in this definition is the consummation of a sale as of a specified date

and the passing of title from seller to buyer under conditions whereby:

1) Buyer and seller are typically motivated;

2) Both parties are well informed or well advised, and both acting in what they

consider their own best interest;

3) A reasonable time is allowed for exposure in the open market;

4) Payment is made in terms of cash in U.S. dollars or in terms of

financial arrangements comparable thereto; and

5) The price represents the normal consideration for the property sold unaffected by

special or creative financing or sales concessions granted by anyone associated

with the sale.

Date of Inspection and Valuation

December 8, 2010

Date of Appraisal

December 15, 2010

Intended Use/Users of the Appraisal

The intended use of this appraisal is for the client, MOA and Municipal Light and

Power (ML&P), to use for asset evaluation for the possible purchase of the subject

parcels. In addition, the intended users of the appraisal include the appropriate

1 "Absolute ownership unencumbered by any other interest or estate, subject only to the limitations

imposed by the governmental powers of taxation, eminent domain, police power, and escheat." The

Dictionary of Real Estate Appraisal, Fourth Edition, Appraisal Institute, page 113.

2 Office of the Comptroller of the Currency under 12 CFR, Part 34, Subpart C-Appraisals, 34.43

Definitions [f].

Black-Smith, Bethard and Carlson LLC. 11

municipal departments and regulatory agencies that may be involved in the purchase of

the property.

Black-Smith, Bethard and Carlson LLC. 12

SCOPE OF WORK

Data sources and the steps in the appraisal development process are summarized:

Property Data

Brian Bethard conducted an exterior and interior inspection and photographed the

property on December 8, 2010. Brian Z. Bethard, MAI.

We examined Municipality of Anchorage (MOA) records on the subject

that included platted dimensions, easements, zoning ordinances,

assessed valuations, public utilities and transportation routes.

Area Data

State and local demographics have been examined, including population and

employment trends and overall economic growth patterns. Sources for much of the data

was the Anchorage Economic Development Corporation, economic and business

journals, newspapers, labor statistics published by the U.S. Government and the State

of Alaska.

Market Data

Alaska is a non-disclosure state. Comparable data was obtained by searching the local

multiple listing service (MLS) records, surveying real estate agents/brokers, property

managers and other appraisers. Market data was confirmed with the property owners,

managers or agents.

Valuation Process

All three traditional approaches to value have been considered. The subject was

constructed in 1983 and the cost approach is not applicable. As required by USPAP its

omission is explained. The subject is valued based on a reconciliation of the income and

sales comparison approaches.

The subject consists of two stand alone sites (lots 5A and Lot 4). The improvements are

located on Lot 5A, and the site has adequate parking. Lot 4 is valued as marketable

excess land.

*The subject property is encumbered by three short term leases. Lease documents were

not provided and information was inadequate to render an opinion of value of the

leased fee estate. If lease documents are made available we retain the right to amend

this report.

Black-Smith, Bethard and Carlson LLC. 13

ASSUMPTIONS AND LIMITING CONDITIONS

General assumptions and limiting conditions are contained in the addenda of the

report. Extraordinary assumptions,3 hypothetical conditions,4 and limiting conditions

are summarized as follows:

o We have not been provided with a Phase 1 Environmental Report. The

appraisers have assumed that the property is environmentally clean

and reserve the right to amend this report should facts prove otherwise.

o The appraisal is made according to the extraordinary assumption that

the information provided is reliable.

o It is assumed that the roof, structure and mechanical systems are in

good working order as indicated by the property contact. A building

inspection report was not provided.

o Lease documents were not provided and no survey of rentable area has

been provided. We have assumed that the lease information is as

reported and reserve the right to amend this report if actual leases or

building survey are provided.

o The subject property is encumbered by three short term leases. Lease

documents were not provided and information was inadequate to render an

opinion of value of the leased fee estate. If lease documents are made available

we retain the right to amend this report.

3 "An assumption, directly related to a specific assignment, which, if found to be false, could alter the

appraiser's opinions or conclusions." Uniform Standards of Professional Practice.

4 "That which is contrary to what exists, but is supposed for the purpose of analysis." Uniform Standards of

Professional Practice.

Black-Smith, Bethard and Carlson LLC. 14

AREA DATA

Anchorage is Alaska’s largest city. It

is a strategic hub for the state’s

transportation industry and the

center of commerce. Oil and gas

industries, finance and real estate,

communications, and government

agencies are also headquartered in

Anchorage.

The State of Alaska Department of

Labor reported the 2009 population

of Anchorage at 284,994. The total for

the nearby Matanuska-Susitna

Borough (MSB; a/k/a the Valley) was

82,515.

Like the rest of the state, the region is heavily dependent on the oil industry and

government spending. However; the Anchorage economy has become more diversified

in recent years. The transportation and visitor industries have become significant

economic drivers that assure some resilience. Without any major economic stimulus on

the scale of a gas pipeline or the opening of ANWR, the near term outlook is for

stability to slow growth in the population and employment.

Alaska’s average monthly job count grew by 2,400 in 2008, an increase of 0.7%. It was

the state’s 21st consecutive year of growth, a streak only four other states can match or

exceed. But the nation and world are in economic turmoil heading into 2009 and there

are more questions than answers about how Alaska will be affected. The 2009 forecast

is for a loss of 700 jobs, a number that reflects two conclusions. The first is that Alaska

will not completely escape an economic storm that looks like it will get worse before it

gets better. The second is that the state is in a relatively strong position to weather it.5

“Of the 50 states, only Alaska had shown enough growth to delay a declaration of

recession by the end of March. Add the District of Columbia to that list too. But both

were in recession when April ended.”6

While signs indicate that the worst of the recession may be over; Anchorage is one of

only six metropolitan areas across the country that are expected to regain their pre-

recession employment levels by the end of 2009.7

5 Dan Robinson, Economist in Alaska Economic Trends (January 2009).

6 "Housing starts beat last year's level in cities from Olympia to Palm Coast" by Bill Dedman, Investigative

Reporter, msnbc.com, June 18, 2009.

7 Global Insight in the Anchorage Daily News, June 14, 2009.

Black-Smith, Bethard and Carlson LLC. 15

Anchorage Economy 2009 Year End Report 8

The end of the year report for 2009 indicated slight job losses for 2009 as Anchorage

was dragged into the national recession. All speakers agreed that Anchorage was

better off than most of the country, but the forecast for 2010 is a 1% decline in

employment, which is the benchmark for economic stability.

Excerpts from Alaska Economic Trends January 2010

Alaska’s 21-year streak of job growth ended in 2009. But the recession that

began in late 2007 and probably ended sometime in the fall of 2009 has been

especially severe and none of the 50 states escaped the downturn – including the

four other Western states that also had growth streaks of at least 21 years:

Montana, New Mexico, North Dakota and Wyoming.

Looking forward, there’s considerably less economic uncertainty than there was

a year ago, at least on the national and international scenes. The turmoil that

began in the United States and spread throughout much of the world in the last

two years has calmed considerably, though not completely. Largely as a result,

the 2010 forecast for Alaska is for a loss of 1,400 jobs, a slightly smaller number

than the 2,100 jobs the state lost in 2009. The smaller decline in 2010 is based

on the paired conclusions that broad national and global influences were

primarily responsible for the state’s job losses in 2009 and that improving

economic conditions for the U.S. and world economies will also improve Alaska’s

job situation in 2010.

Aside from those broad conclusions, though, it’s important to acknowledge that

this forecast is based on the somewhat precarious assumption that no large

changes will occur to either employment or prices in Alaska’s all-important oil

and gas industry in 2010.

8 BOMA Annual Economic Forecast Luncheon, 1-8-10

Black-Smith, Bethard and Carlson LLC. 16

NEIGHBORHOOD DESCRIPTION

General Neighborhood The subject is located in the Midtown business district,

about 2 miles southeast of the Anchorage CBD. The

neighborhood is bounded on the north by Chester Creek, on

the east by the New Seward Highway, on the south by

Tudor Road and on the west by the Minnesota By-Pass.

Access Access is good via a network of fully improved arterials.

Utilities Natural gas, water, sewer, electricity and telephone

Services Police, fire protection and road maintenance are provided by

the Municipality of Anchorage. Public transportation and

refuse service is also available.

Land Development The area is roughly 90% developed with a variety of high-

density residential and general commercial uses.

SUBJECT

Black-Smith, Bethard and Carlson LLC. 17

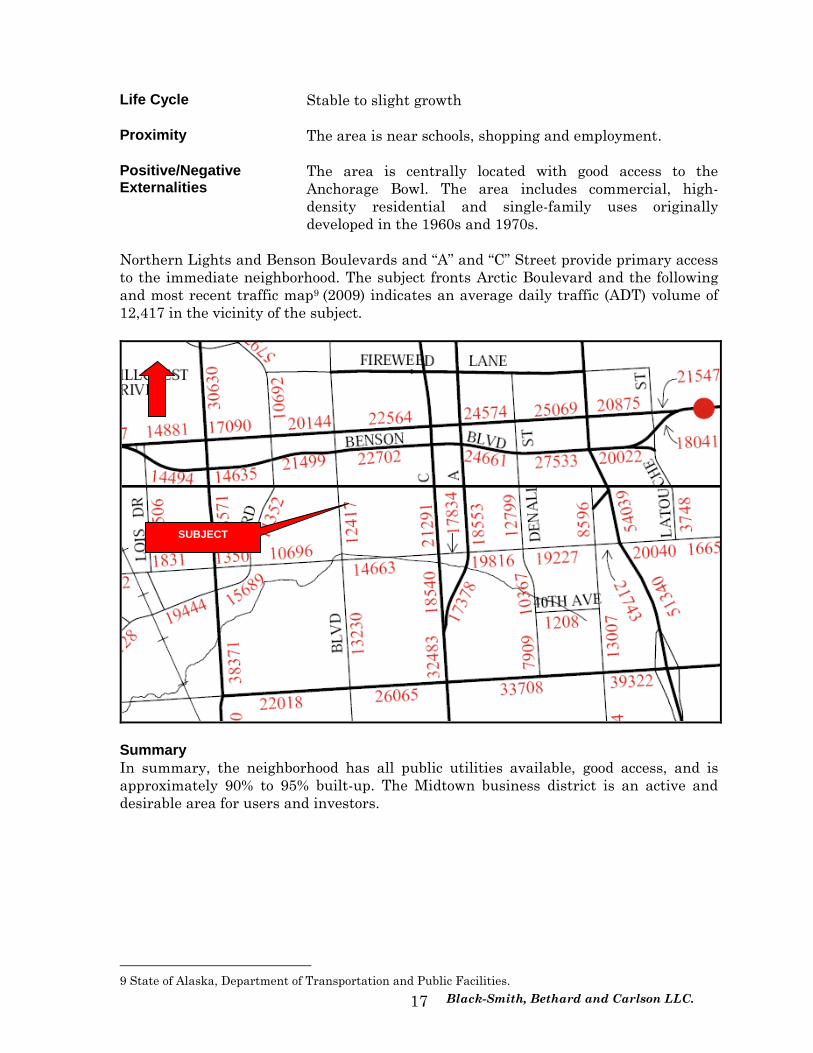

Life Cycle Stable to slight growth

Proximity The area is near schools, shopping and employment.

Positive/Negative Externalities

The area is centrally located with good access to the

Anchorage Bowl. The area includes commercial, high-

density residential and single-family uses originally

developed in the 1960s and 1970s.

Northern Lights and Benson Boulevards and “A” and “C” Street provide primary access

to the immediate neighborhood. The subject fronts Arctic Boulevard and the following

and most recent traffic map9 (2009) indicates an average daily traffic (ADT) volume of

12,417 in the vicinity of the subject.

Summary

In summary, the neighborhood has all public utilities available, good access, and is

approximately 90% to 95% built-up. The Midtown business district is an active and

desirable area for users and investors.

9 State of Alaska, Department of Transportation and Public Facilities.

SUBJECT

Black-Smith, Bethard and Carlson LLC. 18

SITE DESCRIPTION

Location

The sites are located at the NEC of 30th Avenue and Arctic Boulevard in midtown. The

street address is 2909 Arctic Boulevard, Anchorage, AK.

Shape and Area

The sites are rectangular with the following dimensions and area:

Legal Dimensions Area

Lot 4, Block 5 Northern Lights +/- 147' x 59' 7,350 SF Lot 5A, Block 5 Northern Lights +/- 147' x 100' 14,725 SF

Total 22,075 SF

Topography and Soils

The sites are fairly level and near the grade of the bordering streets. No soils data was

available. The site is improved with a two story office building and the soils appear to

be adequate for the existing use

SUBJECT

Black-Smith, Bethard and Carlson LLC. 19

Access

Lot 5a has access from Arctic Boulevard (2 lane, 2 way, fully improved arterial) and

30th Avenue (two way paved connector street). Lot 4 has access from Arctic Boulevard.

Access is adequate.

Utilities

The sites are served by all public utilities including water, sewer, electricity, natural

gas and telephone.

Flood Hazard Information

Flood Insurance Rate Map Panel 235B of 625 of the Federal Emergency Management

Agency, indicates the property is not situated in a flood plain.

Wetlands Information

According to the Municipality of Anchorage Wetlands Atlas, Map No. 31, the subject is

located outside areas of designated wetlands.

Seismic Information

According to the Harding-Lawson Associates 1979 "Geotechnical Hazard Assessment

Study" the subject is described as having “moderate ground failure susceptibility”. The

location in this seismic zone does not appear to have had an adverse affect on the

subject or general neighborhood based on the surrounding developments.

Environmental Issues

No evidence of possible environmental problems was noted during our inspection. We

are not experts in this field and have assumed that there is no impact on value due to

environmental contaminates.

Easements

As noted on the plat map, easements are generally confined to the perimeter of the sites

with limited impact on value. Zoning

The subject is zoned B-3 (General Business District). The B-3 district is “intended for

general commercial uses in areas exposed to heavy automobile traffic. This district

specifically is intended for areas at or surrounding major arterial intersections where

personal and administrative services, convenience and shopping goods, and automobile-

related services are desirable and appropriate land uses.” The existing use conforms to

the regulations of the B-3 district. Suitability of the Site

The sites are well suited for general commercial uses.

Black-Smith, Bethard and Carlson LLC. 20

IMPROVEMENT DESCRIPTION

Lot 5A is improved with a 2-story, concrete and wood framed office building containing

a gross floor area of 8,086 SF, constructed in 1983.

BUILDING AREA SUMMARY

Floor GBA NRA

First 3,968 SF 3,339 SF Second 4,118 SF 3,470 SF

Total 8,086 SF10 6,809 SF

KEY INDICATORS

Gross Building Area 8,086 SF Rentable Area (excl. stairs, mech., elect, & perim.) 6,809 SF Building Efficiency 84% Site Area (Lot 5A) 14,725 SF Land to Building Ratio (GBA) 1.82:1 Age 27 years Effective Age 20± years Remaining Economic Life 25± years

General Construction Details

The following description and general summary of the building specifications based on

our inspection, information provided by the owner and the municipal assessor’s office.

Building plans are located in the addenda.

Structure

Concrete, wood and steel framed.

Foundation and Footings

Reinforced concrete and concrete block.

Exterior Walls

The walls have a height of 11-feet and are painted, reinforced concrete with some metal

siding. The windows and doors are thermal triple pane glass in aluminum frames. Wall

insulation is assumed to be adequate for the local climate.

Roof

Flat, rubber membrane on metal or wood decking over trusses. Roof insulation is

assumed to be adequate for the local climate. The roof is in good condition and was

replaced in 2002 per the property contact.

Floors

The first floor is a reinforced concrete slab while the second floor is wood framed.

10 Based on building plans and inspection. MOA assessors indicate 8,086 SF.

Black-Smith, Bethard and Carlson LLC. 21

Interior Finish

The interior walls and partitions are taped, textured and painted sheetrock with wall

paper accents. The ceilings are suspended acoustic tile. The floor covering is a mix of

carpet and tile. The building has been well maintained and the condition is good for the

age.

Mechanical

Heating is provided by a gas-fired, furnace (replaced 1998) and boiler with baseboard

heating. There is also a roof mounted air exchange system. Several window mounted

air conditioning units are noted. Lighting is typical and adequate, with ceiling mounted

florescent fixtures throughout. There are security cameras and a back up roof mounted

generator for emergency lighting. Each suite is individually metered for electricity.

The each floor contains two 3-fixture, restrooms. Janitor's closets have utility sinks

and double sinks are located in the break rooms. The building is not sprinklered.

There is a no elevator.

Suitability

The improvements are well suited for continued office use.

Compliance with Americans with Disabilities Act (ADA)

The Americans with Disabilities Act (ADA) became effective on January 26, 1992 and

the subject was constructed in 1983. Regardless, a determination of compliance is

outside our area of expertise. The value estimate reflects no financial impact on value

due to any ADA non-compliance.

Parking

The subject is required to have 27 parking spaces for its office use.11 A parking plan

was not provided, but there appears to be adequate parking on Lot 5A as a stand alone

site. The parking is paved and landscaping is typical. There is a pole sign located along

Arctic Boulevard and West 30th Avenue. Lot 4 is paved and used for parking, but it is

not required.

11 Based on MOA reported GBA of 8,086, only 25 spaces are required.

Black-Smith, Bethard and Carlson LLC. 22

Real Estate Taxes and Assessments

State statutes require that real property be assessed at 100% of the “full and true value

(market).” Outstanding taxes or assessments are liens. Verification and reporting is a

function on preliminary title reports. We develop value opinions as if free and clear. We

summarized a 3-year tax history in the following table.

Tax Identification Number: 009-032-39

Year Land Bldg Total Mill Rate R. E. Taxes

2008 $258,400 $388,400 $646,800 14.74 $9,534

2009 $272,700 $403,900 $676,600 15.50 $10,487

2010 $272,700 $432,100 $704,800 15.18 $10,699

Tax Identification Number: 009-032-04

Year Land Bldg Total Mill Rate R. E. Taxes

2008 $129,000 $5,400 $134,400 14.74 $1,981

2009 $136,100 $5,400 $141,500 15.50 $2,193

2010 $136,100 $5,400 $141,500 15.18 $2,148

We will address the reasonableness of the assessed value in the income approach.

Black-Smith, Bethard and Carlson LLC. 23

MARKET ANALYSIS

The Appraisal Institute recognizes two categories of market analysis: inferred and

fundamental. Because the subject is an existing, conventional property type in a stable

market, a lower level of analysis is appropriate. In the following overview demand is

inferred from general market conditions and the available data.

Commercial Land

For more than a decade, local market conditions have not supported speculative

development of most commercial property types. Nearly all of the activity has been

attributable to users. An expansion by regional and national chains continues to

generate demand for strategic sites, both pad sites and stand-alone locations.12

Numerous special purpose facilities have been recently completed, are currently under

construction, or proposed. The available data indicates that:

The market recognizes a price-per-square-foot unit of comparison;

Prices have been trending upward;

Sites containing less than two acres have a market advantage;

Anchored out-lots command a premium over stand-alone sites; and,

Terms are typically cash and a market exposure period of one year is not

unreasonable Summary

Demand for commercial land is down over the last several years, but there is a limited

supply of high exposure sites and prices are stable. Recent sales typically reflect cash

transactions or seller-financed transactions equivalent to cash. The historic data

indicates that market exposure periods typically average less than one year. Given

current market conditions, a marketing period of up to one year is not an unreasonable

expectation for properties professionally marketed at supportable prices.

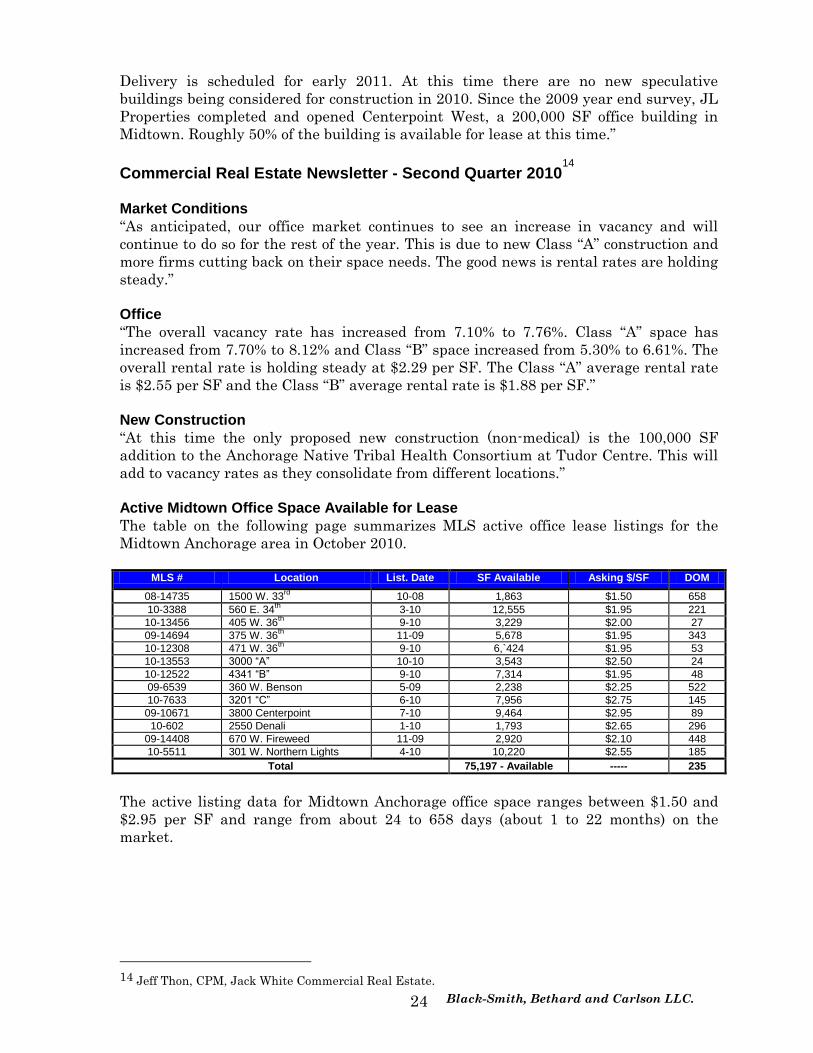

Commercial Real Estate Newsletter - First Quarter 201013

Market Conditions

“As anticipated, our office market is seeing an increase in vacancy and will continue to

do so for the rest of the year. This is due to new Class “A” construction and more firms

cutting back on their space needs. The good news is rental rates are holding steady.”

Office

“The overall vacancy rate has increased from 4.90% to 7.10%. Class “A” space has

increased from 4.70% to 7.70% and Class “B” space decreased slightly from 5.44% to

5.3%. The overall rental rate is holding steady at $2.25 per SF. The Class “A” average

rental rate is $2.49 per SF and the Class “B” average rental rate is $1.85 per SF.”

New Construction

“Currently there is one Class “A” building under development by CIRI in South

Anchorage. The office building is approximately 40,000 SF and is reportedly pre-leased.

12 Big-box national retailers, convenience store chains, franchised restaurants, auto dealerships, specialty

garages (mini-lubes, mufflers/brakes), and lodging facilities.

13 Jeff Thon, CPM, Jack White Commercial Real Estate.

Black-Smith, Bethard and Carlson LLC. 24

Delivery is scheduled for early 2011. At this time there are no new speculative

buildings being considered for construction in 2010. Since the 2009 year end survey, JL

Properties completed and opened Centerpoint West, a 200,000 SF office building in

Midtown. Roughly 50% of the building is available for lease at this time.”

Commercial Real Estate Newsletter - Second Quarter 201014

Market Conditions

“As anticipated, our office market continues to see an increase in vacancy and will

continue to do so for the rest of the year. This is due to new Class “A” construction and

more firms cutting back on their space needs. The good news is rental rates are holding

steady.”

Office

“The overall vacancy rate has increased from 7.10% to 7.76%. Class “A” space has

increased from 7.70% to 8.12% and Class “B” space increased from 5.30% to 6.61%. The

overall rental rate is holding steady at $2.29 per SF. The Class “A” average rental rate

is $2.55 per SF and the Class “B” average rental rate is $1.88 per SF.”

New Construction

“At this time the only proposed new construction (non-medical) is the 100,000 SF

addition to the Anchorage Native Tribal Health Consortium at Tudor Centre. This will

add to vacancy rates as they consolidate from different locations.”

Active Midtown Office Space Available for Lease

The table on the following page summarizes MLS active office lease listings for the

Midtown Anchorage area in October 2010.

MLS # Location List. Date SF Available Asking $/SF DOM

08-14735 1500 W. 33rd

10-08 1,863 $1.50 658

10-3388 560 E. 34th

3-10 12,555 $1.95 221

10-13456 405 W. 36th

9-10 3,229 $2.00 27

09-14694 375 W. 36th

11-09 5,678 $1.95 343

10-12308 471 W. 36th

9-10 6,`424 $1.95 53

10-13553 3000 “A” 10-10 3,543 $2.50 24

10-12522 4341 “B” 9-10 7,314 $1.95 48

09-6539 360 W. Benson 5-09 2,238 $2.25 522

10-7633 3201 “C” 6-10 7,956 $2.75 145

09-10671 3800 Centerpoint 7-10 9,464 $2.95 89

10-602 2550 Denali 1-10 1,793 $2.65 296

09-14408 670 W. Fireweed 11-09 2,920 $2.10 448

10-5511 301 W. Northern Lights 4-10 10,220 $2.55 185

Total 75,197 - Available ----- 235

The active listing data for Midtown Anchorage office space ranges between $1.50 and

$2.95 per SF and range from about 24 to 658 days (about 1 to 22 months) on the

market.

14 Jeff Thon, CPM, Jack White Commercial Real Estate.

Black-Smith, Bethard and Carlson LLC. 25

Office Buildings Sales

Demand and supply of office buildings for sale is generally in balance. In addition, high

construction costs and limited available land contribute to stable demand for existing

office buildings. Recent Alaska Statewide MLS activity for office buildings with a GBA

of over 10,000 SF is presented in the following table:

Sale Date

Sale Price

Address

SF

Yr. Built

DOM

3-06 $6,312,000 3000 A 52,839 1985 83

3-06 $33,450,000 3201/3301 C 208,448 1974/1977 Not reported

5-06 $3,263,150 4200 Lake Otis 22,635 1984 Not reported

6-06 $2,400,000 810 N 16,510 1978 80

7-06 $3,100,000 670 W. Fireweed 35,499 1976 22

2-07 $15,500,000 900 W. 5th

79,381 1979 Not reported

10-07 $720,000 810 E. 9th 10,902 1983 593

10-07 $1,400,000 1231 Gambell 16,818 1985 226

2-08 $1,925,000 2605 Denali 12,656 1982 441

3-08 $1,575,000 1709 S. Bragaw 12,376 1982 65

4-08 $2,900,000 3812 Spenard 20,404 1974 222

9-08 $1,200,000 921 W. 6th 9,227 1968 55

4-09 $2,225,000 3003 Minnesota 14,077 1983 131

2-10 $1,950,000 500 W. 6th

12,952 1962 Not reported

5-10 $4,880,000 431 W. 7th

27,546 1969 Not reported

6-10 $3,800,000 441 W. 5th

32,957 1958/1971 Not reported

Market Time

The overall concept of reasonable exposure encompasses not only adequate, sufficient

and reasonable time but also adequate, sufficient and reasonable marketing effort.

Marketing time is also a function of the amount and quality of the available inventory,

asking prices and investor requirements. Market exposure time may be defined as "the

estimated length of time the property interest being appraised would have been offered

on the market prior to the hypothetical consummation of a sale at market value on the

effective date of the appraisal; a retrospective estimate based upon an analysis of past

events assuming a competitive and open market." 15

Market Exposure Period

For most property types, the data supports exposure period estimates of 6 months to

one year assuming the properties are professionally marketed and priced to reflect

current market conditions.

In summary, our value opinion is stated in terms of cash or its equivalent. The market

exposure period (looking backward) and the marketing time (looking forward) are both

estimated at less than one year.

15 Source: Appraisal Standards Board Statement 6 and Advisory Opinion G-7.

Black-Smith, Bethard and Carlson LLC. 26

HIGHEST AND BEST USE

Highest and Best Use is defined in the Twelfth Edition of the Appraisal of Real Estate,

Appraisal Institute, as:

"The reasonably probable and legal use of vacant land or improved property,

which is physically possible, appropriately supported, financially feasible, and

that results in the highest value."

Highest and Best Use "As Vacant"

Possible Use

The sites are located in midtown Anchorage, contain 22,075 SF, are level and are

served by all public utilities. Access is adequate and the soils appear suitable for

construction. The sites could be developed with almost any legal use permitted under

the B-3 zoning classifications.

Permissible Use [Legal]

Legal restrictions, as they apply to the subject, include easements and the public

restrictions of zoning, as included in Title 21 of the Anchorage Municipal Code "Land

Use Regulations." The subject is zoned B-3 (General Business District) The B-3 district

is “intended for general commercial uses in areas exposed to heavy automobile traffic.

This district specifically is intended for areas at or surrounding major arterial

intersections where personal and administrative services, convenience and shopping

goods, and automobile-related services are desirable and appropriate land uses.” The

existing use conforms to the regulations of the current zoning classifications.

Financially Feasible Uses

The subject is well-suited for commercial development. The high-traffic location with

adequate road frontage and neighborhood characteristics suggests office type uses. The

market is driven by user specific developments but speculative projects have proven

feasible in high exposure locations. Given current market conditions and the national

economy, speculative development is not likely at this time. As of the date of valuation,

the highest and use is speculation.

Maximally Productive Use

The market for suitable sites is driven by a number of uses with a variety of

requirements. As such, the maximally productive use cannot be determined. In

summary, the highest and best use as-vacant, is for speculation or owner/user

commercial.

Highest and Best Use "As Vacant"

The subject's highest and best use as-vacant, is for speculation or owner/user

commercial.

Highest and Best Use “As Improved”

Lot 5A is developed with an average quality office constructed in 1983. The building has

a long term remaining life and provides a positive return to the property. The highest

and best use “as improved” is as developed. Lot 4 is not required for parking and is

marketable excess.

Black-Smith, Bethard and Carlson LLC. 27

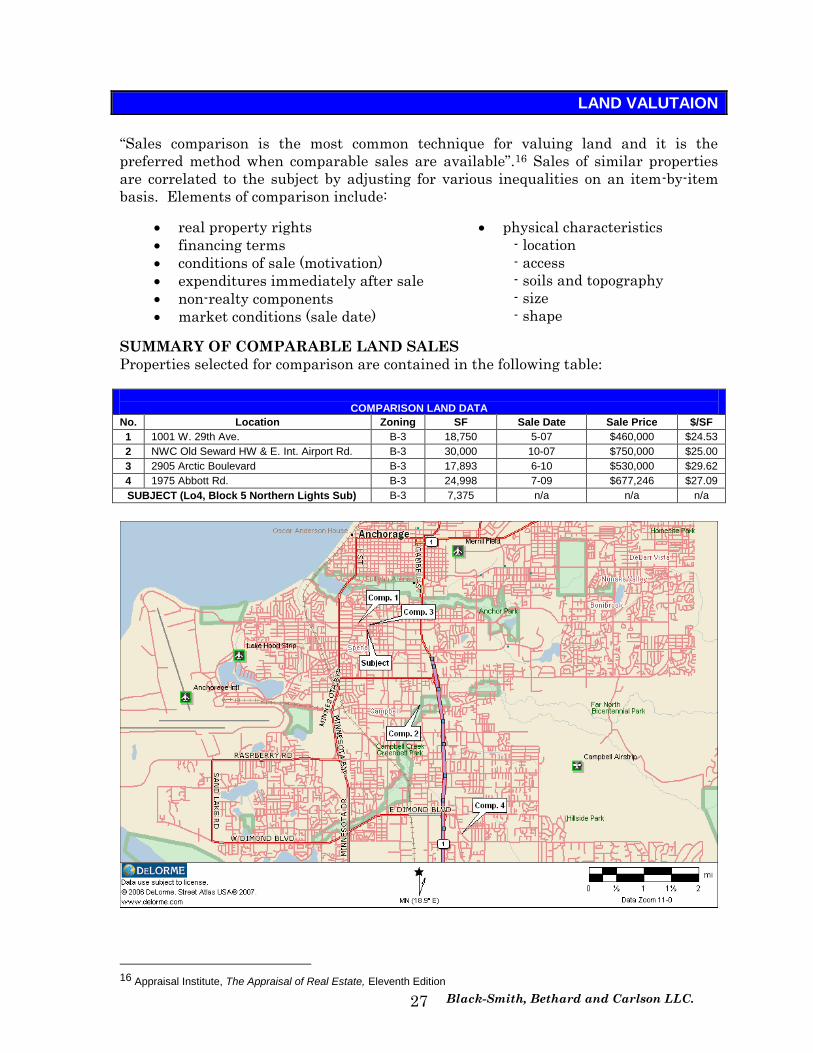

LAND VALUTAION

“Sales comparison is the most common technique for valuing land and it is the

preferred method when comparable sales are available”.16 Sales of similar properties

are correlated to the subject by adjusting for various inequalities on an item-by-item

basis. Elements of comparison include:

real property rights

financing terms

conditions of sale (motivation)

expenditures immediately after sale

non-realty components

market conditions (sale date)

physical characteristics

- location

- access

- soils and topography

- size

- shape

SUMMARY OF COMPARABLE LAND SALES

Properties selected for comparison are contained in the following table:

COMPARISON LAND DATA

No. Location Zoning SF Sale Date Sale Price $/SF

1 1001 W. 29th Ave. B-3 18,750 5-07 $460,000 $24.53

2 NWC Old Seward HW & E. Int. Airport Rd. B-3 30,000 10-07 $750,000 $25.00

3 2905 Arctic Boulevard B-3 17,893 6-10 $530,000 $29.62

4 1975 Abbott Rd. B-3 24,998 7-09 $677,246 $27.09

SUBJECT (Lo4, Block 5 Northern Lights Sub) B-3 7,375 n/a n/a n/a

16 Appraisal Institute, The Appraisal of Real Estate, Eleventh Edition

Black-Smith, Bethard and Carlson LLC. 28

DESCRIPTION OF COMPARABLES

The comparables are identified in the previous table and on the map. The sales selected

for comparison are considered to be the best data available. This is a summary report;

details are contained our work file. We are aware of the dated Carl's Jr. sale that is

proximate to the subject at $27/SF in 2003. The sale was excluded due to date. We are

also aware of the car wash sale at 2301 5th Avenue for $30/SF. This 2008 sale was

influenced by a motivated purchaser.

CORRELATION

All of the comparables reflect arm’s length transactions of the fee simple interest. No

undue stimulus was reported. The indicated unit prices are already adjusted to a cash

equivalent value (if required) and/or expenditures immediately after sale (e.g.,

demolition, curable defects/deficiencies).

Quantitative Adjustments Market Conditions

While a general upward trend in market prices is evident, a universal appreciation rate

is not applicable to all submarkets. More importantly, the market softened and prices

stabilized. We did not apply a quantitative adjustment for time. The impact of market

conditions is recognized in the final reconciliation.

Size

There is no quantifiable relationship between size and price in the comparable data

analyzed. Generally, smaller sites sell for higher unit values.

Soils

The subject and comparison properties reportedly have adequate soils and no

adjustment is required. Factors such as location, access and exposure outweigh slight

differences in soils for developable sites.

Qualitative Adjustments A sufficient number of paired-sales are not available from which to extract reliable

adjustments for other inequalities. We correlated physical inequalities with qualitative

adjustments (superior, inferior, approximately equal).

Comparative Analysis

We have correlated the comparables to the subject in a qualitative analysis described

by the Appraisal of Real Estate, 12th Edition, as a “Relative Comparison Analysis.” In

this analysis, various features and characteristics are perceived as comparable /

approximately equal, superior of inferior. An overall net adjustment based on the

appraiser’s perception is indicated in terms of “positive” or “negative”. This technique

illustrates the relative market position of the subject.

The relative comparison analysis grid is presented on the following page.

Black-Smith, Bethard and Carlson LLC. 29

Relative Comparison Analysis

Comp. No. SUBJECT No. 1 No. 2 No. 3 No. 4

$/SF ---- $24.53 $25.00 $29.62 $27.09

Sale Date (market conditions)

----- 5-07

No adj.

10-07

No adj.

6-10 7-09

No adj.

Adj. $/SF NA $24.53 $25.00 $29.62 $27.09

Location/ Use

Arctic Blvd. Comm.

29th Ave Comm.

(inferior)

Old Seward & International/

Comm. (approx.=)

Arctic/Benson Comm.

(approx.=)

Abbott Rd. Comm.

(approx.=)

Utilities All available

All available

(approx.=)

All available (approx.=)

All available (approx.=)

All available

(approx.=)

Corner No No (equal)

Yes/Major (superior)

Yes/Major (superior)

Yes/Minor (superior)

Zoning B-3 B-3 (approx.=)

B-3 (approx.=)

B-3 (approx.=)

B-3 (approx.=)

SF 7,350 18,750 (larger)

30,000 (larger)

17,893 (larger)

24,998 (larger)

Topography Level at grade

Level at grade

(approx=)

Level at grade

(approx.=)

Level at grade

(approx.=)

Level at grade

(approx.=)

Soils Average Average (approx.=)

Average (approx.=)

Average (approx.=)

Average (approx.=)

Other Typical Typical (approx.=)

Typical (approx.=)

Bisecting Esmt. (inferior)

Typical (approx.=)

Access/Exposure ADT

Arctic, 1-way 12,417- Arctic

29th Ave. N/A

(inferior)

Old Seward & International

1-way in & out 20,146

(superior)

Benson, 1-way; Arctic, 1-way

22,702- Benson 12,417- Arctic

(superior)

Abbott Rd. shared drive with credit

union 21,219 - Abbott

(superior)

Ind. $/SF ---- >$24.53 <$25.00 <$29.62 <$27.09

Reconciliation

The following table reflects the relative market position of the subject:

Conclusion The analysis generates an overall range of adjusted unit values from $24.53 to $29.62 per

SF. The subject’s market position is bracketed by Comparables No. 1 ($24.53) and

Comparable 2 ($25.00).

Considering the subject's small size, a unit value of $25/SF is considered reasonable.

Market value is calculated as follows:

7,350 SF x $25.00 per SF = $184,000

Estimated Current Land Value, rounded: $184,000

No.

Adj. $/SF

Adjustment

Reconciliation

3 $29.62 Negative Not marketed, purchased by lessee, seller paid closing costs, sup. corner.

4 $27.09 Negative Recent sale in developing retail area, superior traffic count and corner.

2 $25.00 Negative Larger parcel, dated sale, but superior traffic count and corner.

Sub. ---- ----- Small, interior lot on Arctic Boulevard

1 $24.53 Positive Dated sale of larger parcel with inferior exposure.

Black-Smith, Bethard and Carlson LLC. 30

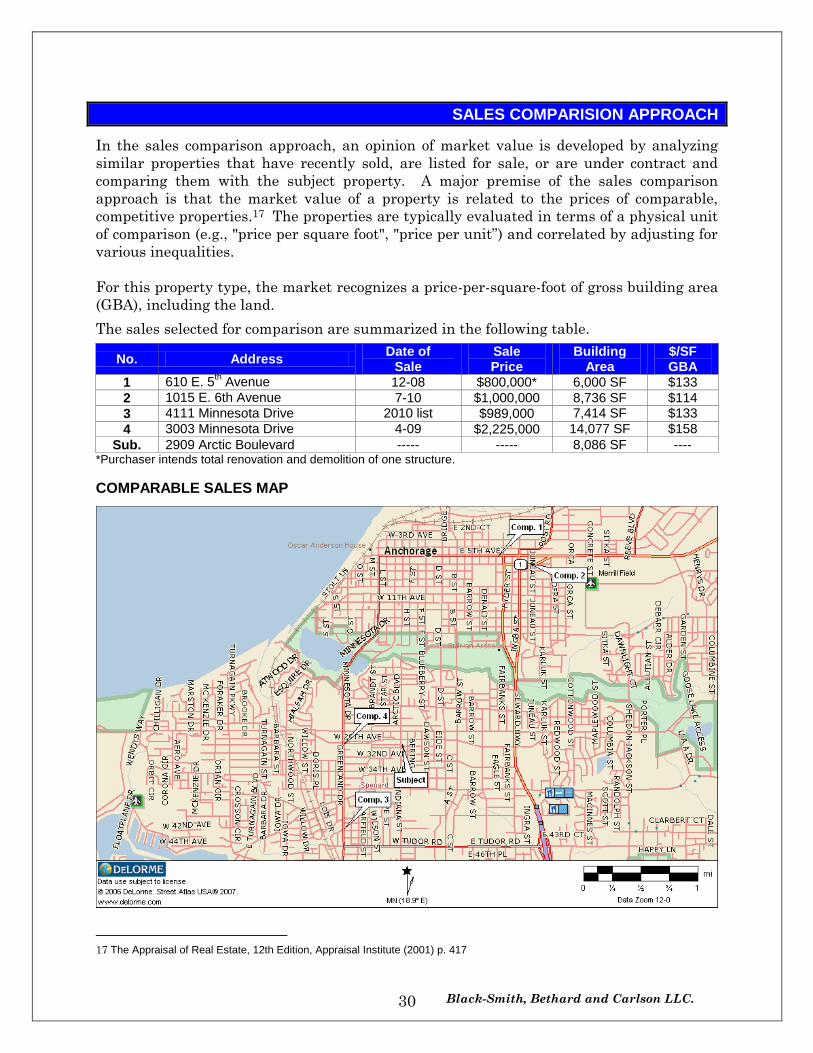

SALES COMPARISION APPROACH

In the sales comparison approach, an opinion of market value is developed by analyzing

similar properties that have recently sold, are listed for sale, or are under contract and

comparing them with the subject property. A major premise of the sales comparison

approach is that the market value of a property is related to the prices of comparable,

competitive properties.17 The properties are typically evaluated in terms of a physical unit

of comparison (e.g., "price per square foot", "price per unit”) and correlated by adjusting for

various inequalities.

For this property type, the market recognizes a price-per-square-foot of gross building area

(GBA), including the land.

The sales selected for comparison are summarized in the following table.

No. Address Date of

Sale Sale Price

Building Area

$/SF GBA

1 610 E. 5th Avenue 12-08 $800,000* 6,000 SF $133

2 1015 E. 6th Avenue 7-10 $1,000,000 8,736 SF $114

3 4111 Minnesota Drive 2010 list $989,000 7,414 SF $133

4 3003 Minnesota Drive 4-09 $2,225,000 14,077 SF $158

Sub. 2909 Arctic Boulevard ----- ----- 8,086 SF ---- *Purchaser intends total renovation and demolition of one structure.

COMPARABLE SALES MAP

17 The Appraisal of Real Estate, 12th Edition, Appraisal Institute (2001) p. 417

Black-Smith, Bethard and Carlson LLC. 31

DESCRIPTION OF THE COMPARABLES

The comparables are identified in the previous table and on the map. The property

characteristics are summarized in the following comparison grid. This is a summary

report; details are retained in the appraiser’s files.

CORRELATION

All of the comparables reflect arm’s length sales/acquisitions of the fee simple or leased fee

interest. No undue stimulus was reported. The indicated unit values are already adjusted

to a cash equivalent value (if required) and/or expenditures immediately after sale (e.g.,

demolition, curable defects/deficiencies).

Adjustments

Market Conditions

The comparables and the date of value bracket a period of just 2 years. A sufficient number

of paired-sales are not available from which to extract a reliable time adjustment. The

market has been relatively flat over the past two years and no adjustment is required.

Sale date is considered in the final reconciliation.

Physical Characteristics

Physical characteristics include location, access, quality, and effective age. However, the

quantity of data is not sufficient to isolate reliable percentage or dollar adjustments. On

that basis, other physical characteristics are correlated with qualitative adjustments (e.g.,

approximately equal, superior, or inferior).

32

Reconciliation

The analysis generates a range from $114 to $158/SF. The relative market position of

the subject is situated between Sales 1 ($133/SF) and 4 ($158/SF). The subject is a well

maintained, average quality, smaller building in midtown. Market value is concluded

towards the upper end of the bracketing range as indicated by Comparable 4, which is

superior for location and overall quality, but larger than the subject. Giving most

weight to Comparable 4, while recognizing that it is slightly superior, market value is

concluded at $155/SF of GBA.

Market value by the sales comparison approach is calculated as follows:

8,086 SF x $155/SF = $1,253,000 (rnd)

Property Subject

2909 Arctic Blvd.

Comp #1 610 E 5th

Ave.

Comp #2 1015 E. 6th

Ave

Comp #3 4111

Minnesota

Comp #4 3003

Minnesota

Sale Price ----- $800,000 $1,000,000 $989,000 $2,225,000

Date of Sale 12-10 10-08 7-10 2010 listing 4-09

Market Cond Adj. None n/a n/a n/a n/a

Adj. Sale Price ----- $800,000 $1,000,000 $989,000 $2,225,000

GBA 8,086 SF 2-story

6,000 SF 2-story

8,736 SF 2-story

7,414 SF 2-story

14,077 SF 2-story, cvrd

prkg

Adjusted $/SF ----- $133 $114 $133 $158

Location Midtown /

Arctic Blvd.

CBD fringe, 5th

slightly inf.

CBD fringe, 6th

slightly inf.

Midtown / Minnesota

slightly sup.

Midtown / Minnesota

slightly sup.

Quality/Type avg concrete, wood & steel

avg cc blk

approx.=

avg stucco / wd frame approx.=

avg cc blk / wd frame

approx.=

avg + steel frame

superior

Age/Condition 1983/good 1976/avg

inferior 1983/avg inferior

1974/avg slightly inferior

1983/good approx. =

Land: Building Ratio

1.82 to 1

1.25 to 1

inferior

1.60 to 1

approx.=

1.79 to 1

approx.=

1.50 to 1, adtl. cov. prkg approx.=

AC no / some

window units no

inferior no

inferior yes

superior yes

superior

Elevator yes no

inferior no

inferior no

inferior yes

approx. =

Sprinkler no

no approx. =

no approx. =

no approx. =

no approx =

Adj. $/SF/GBA ----- >$133 >$114 >$133 <$158

33

INCOME APPROACH

The income capitalization approach to value consists of methods, techniques, and

mathematical procedures that an appraiser uses to analyze a property’s capacity to

generate benefits and convert them into an indication of present value.18 The basis for

this approach is the property operating data (potential income less vacancy and

expenses).

For the purpose of our analysis, NOI is defined as:

"income remaining after deduction of all property expenses including replacement

reserves (if any) and before consideration of leasing commissions and tenant

improvements"19

Contract Rents The following table summarizes the current occupancy of the subject:

SUMMARY OF CONTRACT RENTS

Suite

Floor

Tenant

Date/Term

Current Rent/Mo.

RSF

$/SF/Mo.±

Tenant Exp.

Options / Escalation

101 First CareNet +/- 2009 / 3 yr $1,650 Unk. $1.17 Elec & J n/a

102/3 First Schadt L. Mo/Mo $2,250 Unk. $1.17 Elec & J n/a 200 Second DNH +/- 2009 / 3 yr $4,700 3,470 $1.35 Elec & J n/a Total 2 Story ---- ------ $8,600 6,809 $1.26 Elec & J n/a

The subject's leases were not professionally marketed and were not based on a price per

square foot basis. The rents are below market. Therefore, market rent will be based on

comparable leases.

Market Rent

The subject is Class B/B- office space for the local market. Market rent is adjusted to

reflect a similar expense structure as the subject with tenants responsible for electric

and janitorial.

SUMMARY OF RENTAL COMPARISONS

No.

Location

Date

NRA -SF

Rent/SF/Mo

.

Tenant Exp.

Adj. $/SF.

1 4141 B Street #210 11-10 1,297 $1.75 E & J

--- $1.75

2 121 W Fireweed 8-10 2,261 $1.85 None - $.18

$1.67

3 1225 E International Airport Rd. 7-10 2,100 $1.65 None -$.18

$1.47

4 3330 Arctic Blvd. 2010 list 9,916 $1.60 J

-$.10 $1.50

E= Elec ($.08), J= Janitorial ($.10)20

18 The Appraisal of Real Estate, 12th Edition, Appraisal Institute (2001) p. 472

19 Korpacz Real Estate Investor Survey 20 BBC 09-117

34

Description of the Comparables

The comparables are identified in the previous table and on the map. This is a

summary report; details are contained our work file.

Black-Smith, Bethard and Carlson LLC. 35

SUMMARY OF RENTAL COMPARISONS

Comp. Subject No. 1 No. 2 No. 3 No. 4

Address 2909 Arctic Blvd. 4141 B Street #210 121 W Fireweed

1225 E International Airport Rd.

3330 Arctic Blvd.

Lease Date

Various below market leases

11-10 8-10 7-10 2010 list

Lease Rate (Rentable)

---- $1.75 $1.67 $1.47 $1.50

Tenant Expenses

E & J E & J adj. abv.

None adj. abv.

None adj. abv.

J adj. abv.

Year Built 1983 1984 (approx.=)

1967 (inferior)

1982 (approx.=)

1979 (inferior)

Quality/ Condition

Avg./Good Avg/Good (approx.=)

Avg/Good (approx.=)

Avg./ Avg. (inferior)

Avg./ Avg. (inferior)

Constr. concrete block, steel and wood

Steel & wood frame

(approx. =)

Wood frame

(inferior)

Wood frame

(inferior)

Wood frame

(inferior)

SF Area (Rentable)

6,809 SF

1,297 SF 2,261 SF 2,100 SF 9,916 SF

Elevator No Yes (superior)

No (approx. =)

No (approx. =)

No (approx. =)

AC No / some window units

Yes (superior)

Yes (superior)

Yes (superior)

No (approx. =)

Location Midtown North of Midtown (approx. =)

Midtown (approx. =)

Midtown (approx. =)

Midtown (approx. =)

On-site parking

Adequate Adequate (approx. =)

Adequate (approx. =)

Adequate (approx. =)

Adequate (approx. =)

Adjusted Rent/SF

----- $1.75 $1.67 $1.47 $1.50

Conclusion Market Rent

The following table reflects the relative market position of the subject:

The subject’s relative market position is situated towards the top of the comparable

range between Comp 2 ($1.67/SF) and Comp. 1 ($1.75/SF). Giving most weight to these

comparables market rent is concluded at $1.70/SF, plus electric and janitorial.

6,809 SF @ $1.70/SF x 12 = $138,904

Projected Gross Annual Rental Income: $138,904

No. Adj. $/SF Adjustment Reconciliation

1 $1.75 Approx. = Similar age quality/condition, slightly superior AC/Elv

Subject --- ------ Good condition midtown building

2 $1.67 Approx. = Inferior for age and construction type, off set by AC/Elv

4 $1.50 Positive Inferior quality condition

3 $1.47 Positive Inferior for quality/condition and age

Black-Smith, Bethard and Carlson LLC. 36

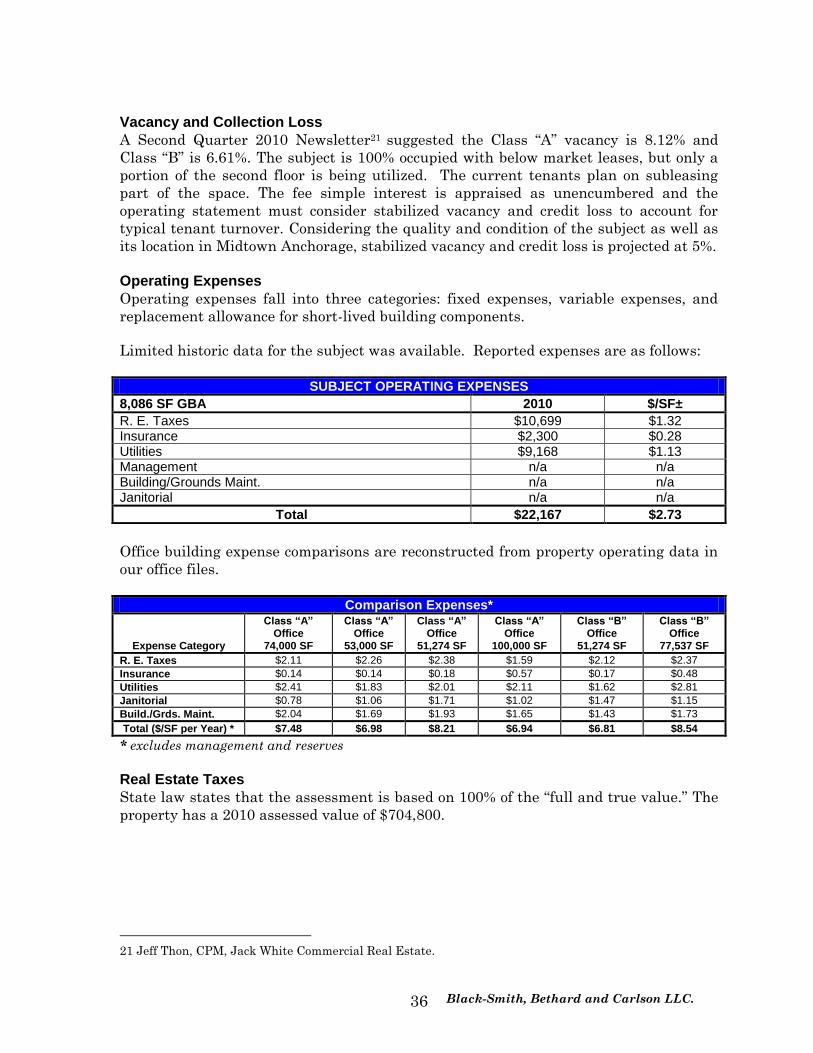

Vacancy and Collection Loss

A Second Quarter 2010 Newsletter21 suggested the Class “A” vacancy is 8.12% and

Class “B” is 6.61%. The subject is 100% occupied with below market leases, but only a

portion of the second floor is being utilized. The current tenants plan on subleasing

part of the space. The fee simple interest is appraised as unencumbered and the

operating statement must consider stabilized vacancy and credit loss to account for

typical tenant turnover. Considering the quality and condition of the subject as well as

its location in Midtown Anchorage, stabilized vacancy and credit loss is projected at 5%.

Operating Expenses

Operating expenses fall into three categories: fixed expenses, variable expenses, and

replacement allowance for short-lived building components.

Limited historic data for the subject was available. Reported expenses are as follows:

SUBJECT OPERATING EXPENSES

8,086 SF GBA 2010 $/SF±

R. E. Taxes $10,699 $1.32 Insurance $2,300 $0.28 Utilities $9,168 $1.13 Management n/a n/a Building/Grounds Maint. n/a n/a Janitorial n/a n/a

Total $22,167 $2.73

Office building expense comparisons are reconstructed from property operating data in

our office files.

Comparison Expenses*

Expense Category

Class “A” Office

74,000 SF

Class “A” Office

53,000 SF

Class “A” Office

51,274 SF

Class “A” Office

100,000 SF

Class “B” Office

51,274 SF

Class “B” Office

77,537 SF

R. E. Taxes $2.11 $2.26 $2.38 $1.59 $2.12 $2.37

Insurance $0.14 $0.14 $0.18 $0.57 $0.17 $0.48

Utilities $2.41 $1.83 $2.01 $2.11 $1.62 $2.81

Janitorial $0.78 $1.06 $1.71 $1.02 $1.47 $1.15

Build./Grds. Maint. $2.04 $1.69 $1.93 $1.65 $1.43 $1.73

Total ($/SF per Year) * $7.48 $6.98 $8.21 $6.94 $6.81 $8.54

* excludes management and reserves

Real Estate Taxes

State law states that the assessment is based on 100% of the “full and true value.” The

property has a 2010 assessed value of $704,800.

21 Jeff Thon, CPM, Jack White Commercial Real Estate.

Black-Smith, Bethard and Carlson LLC. 37

The following table contains a summary of the 2010 building assessed values for several

Midtown Anchorage office properties:

Location 2010 Assessed Value GBA Year Built $/SF of GBA

3003 Minnesota $2,257,100 14,077 1983 $160

1015 E 6th Ave $790,600 8,736 1983 $90

3380 “C” St. $2,190,400 17,900 SF 1972 $122

Subject $704,800 8,086 SF 1983 $95

The office properties reflect a range of assessed values from about $90 to $160/SF. The

subject assessed value is about $95/SF of GBA and is at the low end of the range, but

supported by the data. The projected annual taxes, based on the assessed value of

$704,800 and a mill rate of 15.18, are $10,699.

Insurance

The subject insurance premium averaged $0.28/SF. The comparables range from

$.14/SF to $.57/SF. The subject is a concrete block, steel and wood building with no

sprinkler system. The subject’s historic data is within the range and is given most

weight. Insurance expenses are projected at $.30/SF.

Utilities

The subject utility expense were reported at $1.13/SF. Recognizing that local utility

costs have increased over the past few years and water / waste water utilities are

projecting increases over the next five years, a slightly higher estimate is appropriate.

The comparables range from $1.62 to over $2.00/SF, but include electric expenses.

Considering the subject expense structure, with tenant paid electric, we have estimated

utility expenses at $1.25/SF to recognize projected increases.

Janitorial

Janitorial expenses are projected as a tenant expense. Any minor common area

janitorial is assumed to be covered with typical maintenance.

Management/General Administration, legal and professional Fees

Management fees vary with a project size and number of tenants. Rates for

management fees typically vary from 3% to 7% of effective gross annual income,

depending on the size of a project and amount of work required. Considering the small

size of the subject, we have estimated total management fees, inclusive of

administration expenses, towards the low end of the range, or 3% of effective gross

income.

Building and Grounds Maintenance

Maintenance is difficult to estimate with any degree of precision as this expense item

varies widely from property to property and year-to-year, which is attributable to

differing ownership/management philosophies and accounting methods. In addition,

this expense category is often a 'catch all' for items, which could be funded within the

scope of a reserve account or tenant improvements. The expense comparison data

reflected maintenance and repair costs ranging from $1.43 to $3.66 per SF per year of

GBA. Excluding capital expenditures, we have given most weight to the low end of the

comparable range and this expense is projected at $1.50/SF.

Black-Smith, Bethard and Carlson LLC. 38

Replacement Reserves

The 3rd Quarter 2010 issue of Korpacz Real Estate Investor Survey indicates

replacement reserves for suburban office properties range from $0.15 to $0.50 per SF

with an average of $0.28 per SF. Replacement costs are higher in Anchorage than most

other locales. Using the average indicator for office use and adjusting it upward by a

local cost multiplier; we project replacement reserves at $0.36 per SF ($0.28 per SF x

1.27, rounded)22 of the GBA.

The projected operating statement is presented as follows:

PROJECTED OPERATING STATEMENT -FEE SIMPLE

GBA 8,086 $/SF± PGAI/Mo.± PGAI/Yr

NRA 6,809 $1.70 $11,575.30 $138,904

Projected Gross Annual Rental Income $138,904

Less: Vacancy & Collection Loss 5% ($6,945.18)

Effective Gross Income $131,958

Expenses $/SF GBA± $/Year

R. E. Taxes $1.32 $10,699

Insurance $0.30 $2,426

Utilities $1.25 $10,108

Janitorial $0.00 $0

Management 3% $3,959

Building/Grounds Maintenance $1.50 $12,129

Reserves $0.36 $2,911

Total Estimated Operating Expenses $5.22 $/SF of GBA ($42,231)

32% of EGI

Projected Stabilized NOI $89,727

Income Capitalization

The value of the subject at stabilized occupancy is derived by direct capitalization.

With this technique, the net operating income (NOI) is divided by a market-supported

overall capitalization rate (OAR) to indicate a value.

22 The Marshall Valuation local cost multiplier for Anchorage, October 2010.

Black-Smith, Bethard and Carlson LLC. 39

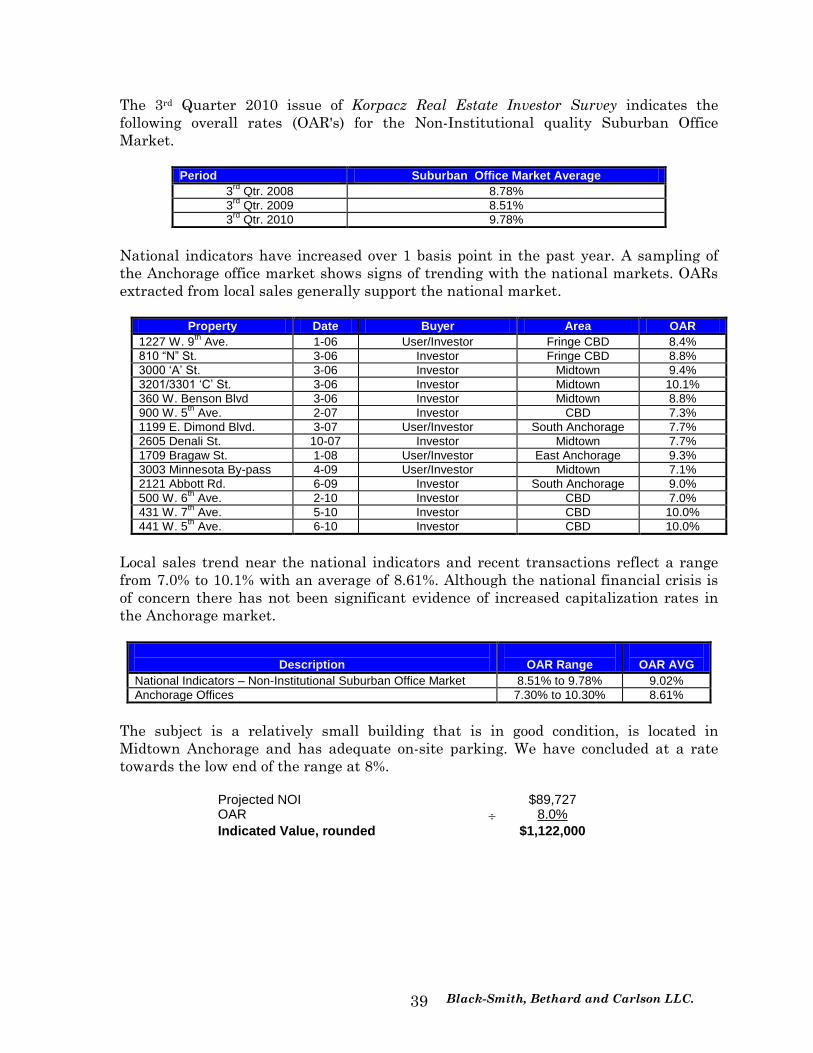

The 3rd Quarter 2010 issue of Korpacz Real Estate Investor Survey indicates the

following overall rates (OAR's) for the Non-Institutional quality Suburban Office

Market.

Period Suburban Office Market Average

3rd

Qtr. 2008 8.78%

3rd

Qtr. 2009 8.51%

3rd

Qtr. 2010 9.78%

National indicators have increased over 1 basis point in the past year. A sampling of

the Anchorage office market shows signs of trending with the national markets. OARs

extracted from local sales generally support the national market.

Property Date Buyer Area OAR

1227 W. 9th

Ave. 1-06 User/Investor Fringe CBD 8.4%

810 “N” St. 3-06 Investor Fringe CBD 8.8%

3000 ‘A’ St. 3-06 Investor Midtown 9.4%

3201/3301 ‘C’ St. 3-06 Investor Midtown 10.1%

360 W. Benson Blvd 3-06 Investor Midtown 8.8%

900 W. 5th

Ave. 2-07 Investor CBD 7.3%

1199 E. Dimond Blvd. 3-07 User/Investor South Anchorage 7.7%

2605 Denali St. 10-07 Investor Midtown 7.7%

1709 Bragaw St. 1-08 User/Investor East Anchorage 9.3%

3003 Minnesota By-pass 4-09 User/Investor Midtown 7.1%

2121 Abbott Rd. 6-09 Investor South Anchorage 9.0%

500 W. 6th

Ave. 2-10 Investor CBD 7.0%

431 W. 7th

Ave. 5-10 Investor CBD 10.0%

441 W. 5th

Ave. 6-10 Investor CBD 10.0%

Local sales trend near the national indicators and recent transactions reflect a range

from 7.0% to 10.1% with an average of 8.61%. Although the national financial crisis is

of concern there has not been significant evidence of increased capitalization rates in

the Anchorage market.

Description

OAR Range

OAR AVG

National Indicators – Non-Institutional Suburban Office Market 8.51% to 9.78% 9.02%

Anchorage Offices 7.30% to 10.30% 8.61%

The subject is a relatively small building that is in good condition, is located in

Midtown Anchorage and has adequate on-site parking. We have concluded at a rate

towards the low end of the range at 8%.

Projected NOI $89,727 OAR 8.0%

Indicated Value, rounded $1,122,000

Black-Smith, Bethard and Carlson LLC. 40

FINAL RECONCILIATION

The value indicators developed are summarized in the following table.

Indicated value by the Sales Comparison Approach $1,253,000 Indicated value by the Income Approach $1,122,000

The sales approach established a range of indicated values for similar office buildings.

Due to the subject’s smaller size, good condition and location in midtown, a unit value

towards the upper end of the range is supported by the data. The approach provides a

reasonable indication of value.

The subject is suitable for users or investors. The market rent estimate, expenses, and

capitalization rate are all well supported by actual data from the subject and

comparable properties. The approach is reasonable given the data available.

In the end, both approaches are reasonable. Giving slightly greater weight to the

income approach, market value is fairly represented at $1,200,000.

Total Market Value Lot 5A, Block 5 (Starn Building): $1,200,000 Lot 4, Block 5 (Excess Land): $184,000

Black-Smith, Bethard and Carlson LLC. 41

ADDENDA

Black-Smith, Bethard and Carlson LLC. 42

Black-Smith, Bethard and Carlson LLC. 43

Black-Smith, Bethard and Carlson LLC. 44

Black-Smith, Bethard and Carlson LLC. 45

FIRST FLOOR

Black-Smith, Bethard and Carlson LLC. 46

SECOND FLOOR

Black-Smith, Bethard and Carlson LLC. 47

QUALIFICATIONS OF BRIAN Z. BETHARD, MAI

State Certification No. 281

General Education Service High School, Anchorage, Alaska - Graduate 1989 The Colorado College, Colorado Springs, CO - Bachelor of Arts, Economics 1993 University of Alaska, Anchorage, Anchorage, AK - MBA 1996

Employment History Black-Smith, Bethard & Carlson, LLC - Managing Member – 2005 + Black-Smith and Richards, Inc. - Fee Appraiser - 1995 to 2005 Randall, Hayes, and Henderson, Inc. - Fee Appraiser - 1993 to 1995

Appraisal Courses/Seminars Taken Residential Case Study - University of Alaska Anchorage - 1994 Uniform Residential Appraisal Report - Appraisal Institute - 1993 Standards of Professional Practice, Part A & B - Appraisal Institute - 1996 Advanced Sales Comparison & Cost Approaches - Appraisal Institute - 1997 Appraisal Principles & Procedures - Appraisal Institute - 1998 Highest and Best Use Market Analysis - Appraisal Institute - 1998 Advanced Applications and Market Analysis - Appraisal Institute - 1998 Report Writing and Valuation Analysis - Appraisal Institute, 1998 Advanced Income Capitalization, Course 510 - Appraisal Institute - 2000 Intro to Statistics & Supporting Adjustments - Appraisal Institute - 2002 Market Studies for Affordable Housing - NH&RA - 2002 Standards of Professional Practice - Appraisal Institute – 2002/03/04/05/07/09 Subdivision Analysis - Appraisal Institute – 2004 Rates & Ratios – Appraisal Institute – 2005 Principles of Real Estate Law – IRWA – 2005 Skills of Expert Testimony – IRWA – 2006 Analyzing Distressed Real Estate – AI – 2006 Condemnation Appraising – AI – 2007 Appraisal Challenges in Declining Markets – AI, 2009 Forcasting Revenue – AI, 2009

Certifications Alaska State Certification: General Real Estate Appraiser #281

Affiliations Member Appraisal Institute (Member No. 11857) President: Alaska Chapter Appraisal Institute – 2005 & 2006 Vice Pres: Alaska Chapter Appraisal Institute - 2004

Black-Smith, Bethard and Carlson LLC. 48

Typical Clients Appraisal Assignments Cook Inlet Housing Authority Various Multifamily, Land and Special Purpose Northrim Bank Attwood Building Rent Study, Anch., AK Alaska Housing Finance Corp. Kenai Senior Housing Market Study, Kenai, AK HDR Engineering Highlands Luxury Apartments, Anch., AK The Municipality of Anchorage The Veco Building, Anch., AK The City of Valdez City of Valdez Assessment, Valdez, AK Alaska Industrial Development & Export Authority Charter North Hospital, Anch., AK Wells Fargo Bank McKay Building, Anch., AK Key Bank Alaska DOT Building, Juneau, AK State of Alaska Department of Natural Resources Alyeska Pipeline Appraisal, Prudhoe - Valdez First National Bank Alaska 15

th Avenue Extension ROW Project, Anch., AK

Alaska First Bank Saint Paul Health Clinic, St. Paul, AK Denali Alaska Credit Union Residential Mortgage Building, Anch., AK Department of Justice Sprucewood Housing; 300 Units Eielson AFB

Black-Smith, Bethard and Carlson LLC. 49

LIMITING CONDITIONS AND ASSUMPTIONS

This appraisal report has been made with the following general assumptions:

1. No responsibility is assumed for the legal description provided or for matters pertaining to

legal or title considerations. Title to the property is assumed to be good and marketable unless

otherwise stated.

2. The property is appraised free and clear of any or all liens or encumbrances unless otherwise

stated.

3. Responsible ownership and competent property management are assumed.

4. The information furnished by others is believed to be reliable, but no warranty is given for its

accuracy.

5. All engineering studies (if any) are assumed to be correct. The plot plans and illustrative

material in this report are included only to help the reader visualize the property.

6. It is assumed that there are no hidden or unapparent conditions of the property, subsoil, or

structures that render it more or less valuable. No responsibility is assumed for such conditions

or for obtaining the engineering studies that may be required to discover them.

7. It is assumed that the property is in full compliance with all applicable federal, state, and local

environmental regulations and laws unless the lack of compliance is stated, described, and

considered in the appraisal report.

8. It is assumed that the property conforms to all applicable zoning and use regulations and

restrictions unless a nonconformity has been identified, described, and considered in the

appraisal report.

9. It is assumed that all required licenses, certificates of occupancy, consents, and other

legislative or administrative authority from any local, state, or national government or private

entity or organization have been or can be obtained or renewed for any use on which the opinion

of value contained in this report is based.

10. It is assumed that the use of the land and improvements is confined within the boundaries or

property lines of the property described and that there is no encroachment or trespass unless

noted in the report.

11. Unless otherwise stated in this report, the existence of hazardous materials, which may or

may not be present on the property, was not observed by the appraiser. The appraiser has no

knowledge of the existence of such materials on or in the property. The appraiser, however, is

not qualified to detect such substances. The presence of substances such as asbestos, urea-

formaldehyde foam insulation and other potentially hazardous materials may affect the value of

the property. The value estimated is predicated on the assumption that there is no such material

on or in the property that would cause a loss in value. No responsibility is assumed for such

conditions or for any expertise or engineering knowledge required to discover them. The intended

user is urged to retain an expert in this field, if desired.

Black-Smith, Bethard and Carlson LLC. 50

This appraisal report has been made with the following general limiting conditions:

1. Any allocation of the total value estimated in this report between the land and the

improvements applies only under the stated program of utilization. The separate values allocated

to the land and buildings must not be used in conjunction with any other appraisal and are

invalid if so used.

2. Possession of this report, or a copy thereof, does not carry with it the right of publication.

3. The appraiser, by reason of this appraisal, is not required to give further consultation or

testimony or to be in attendance in court with reference to the property in question unless

arrangements have been previously made.

4. Neither all nor any part of the contents of this report (especially any conclusions as to value,

the identity of the appraiser, or the firm with which the appraiser is connected) shall be

disseminated to the public through advertising, public relations, news, sales, or other media

without the prior written consent and approval of the appraiser.

Additional Assumptions and Limiting Conditions:

1. Any opinions of value provided in the report apply to the entire property, and any proration or

division of the total into fractional interests will invalidate the opinion of value, unless such

proration or division of interests has been set forth in the report.

2. The client agency provided the area estimates for the larger parcel, area of the acquisition, and

the remainder. Design changes, if any, that result in changes to those area estimates will

require a modification of the appraisal.

3. The forecasts, projections, or operating estimates contained herein are based on current

market conditions, anticipated short-term supply and demand factors, and a continued stable

economy. These forecasts are, therefore, subject to changes with future conditions.

4. The Americans with Disabilities Act (ADA) became effective January 26, 1992. The appraiser

has not made a specific compliance surveyor analysis of the property to determine whether or not

it is in conformity with the various detailed requirements of ADA. It is possible that a compliance

survey of the property and a detailed analysis of the requirements of the ADA would reveal that

the property is not in compliance with one or more of the requirements of the act. If so, this fact

could have a negative impact upon the value of the property. Since the appraiser has no direct

evidence relating to this issue, possible noncompliance with the requirements of ADA was not

considered in estimating the value of the property.