subsidiary of olsen thielen & co., ltd. cpa valuation de-mystified john gurley randy schostag

TRANSCRIPT

Subsidiary of Olsen Thielen & Co., Ltd. CPA

Valuation De-mystified

John GurleyRandy Schostag

Objective

• Give a better understanding of valuation:– When they may be required

– Who should perform the valuation

– What is the process

– What are the results

– Why should I care

Introductions

• John Gurley– Principal and head of the Business Valuation Group at Berry,

Dunn, McNeil & Parker

• Randy Schostag– Founder of Minnesota Business Valuation Group and President

When should I get an appraisal?

When do I get an appraisal?

Why is that?

• Common perceptions of valuation reports:– Expensive

– Complicated

– No relationship to book value

– Have no idea where the number comes from

• Our goal is to help you get more value out of the valuation process

What questions are answered by a valuation?

• Value to whom?• Value on what date?• Value for what purpose?• What is the subject interest is being valued?• Only then can we answer – what is the value?

Who should perform the valuation?

• What to look for in a valuation professional:– Credible

– Credentialed

– Experienced

– Independent (?)

• Determine if you need an advocate or an independent appraisal

Independence and Valuation

• Valuation services for attest clients have to be performed in keeping with the AICPA Code of Professional Conduct

• Independence would be impaired if the results of the valuation would be material to the financial statements

Independence Case Studies

• CEO wants to gift a substantial portion of stock to children– Asks the auditor to value the shares

– Can they do the work?

• Majority shareholder wants to sell his shares to an unrelated third party – Asks the auditor if the CPA firm can value the shares

– Can they do the work?

More Independence Case Studies

• Telco wants to issue new shares to outside investor– Telco President asks accounting firm to opine as to the value of

the shares

– Can they do the work?

• Company wants to issue shares to key employee– Company CEO asks accounting firm to value the stock

– Can they do the work?

What is the valuation process?

What is the valuation process? (continued)

How does SFAS 157 change things?

• The definition of fair value is now based on market participants:– “The price that an asset would receive or that would be paid to

transfer a liability in an orderly transaction between market participants at the measurement date.”

– Market participants are buyers and sellers in the principal or most advantageous market who are independent, knowledgeable, and willing and able to complete the transaction

SFAS 157 is applied to all entities as of 2009

• Application to assets– Assumes highest and best use

• In use – maximum value for an asset working in combination with other assets installed and configured for use

• In exchange – highest and best use is as a stand-alone, or the carve out of a certain business unit

– Which definition depends on market participants

• Application to liabilities– Assumes non-performance risk is the same before and after the

transaction and was taken into consideration in the price

Fair Value on initial recognition

• Assets acquired or liabilities assumed in a transaction represent an “entry” price

• Fair Value is now defined as the “exit” price – the price received to sell the asset or paid to transfer the liability

• For financial assets in a high volume market, may be the same

• Auction analogy may apply for non-financial assets

Combination of assets under SFAS 141(R)

Combination of assets under SFAS 141(R)

• The difference between “book value” and the equity value of the business.

• Increased value of equity.

BALANCE SHEET MUST BALANCE

What are identifiable intangible assets?

• Obtain total Company Fair Value• Ascertain value of tangible & financial assets

– Must apply FASB 157 to all assets

– May create surprises for tangible assets

• Difference between adjusted book and fair value• Remainder is ‘Blue Sky’

– Intangible Assets

– Goodwill

Example

EXAMPLE SOFTWARE COMPANYBalance Sheet

Cash & Eqivalent 50,000 Current Long Term Debt 25,000Accounts Receivable 250,000 Accounts Payble 75,000Pre-paid Taxes 25,000 Accrued Taxes 10,000

Wages, Rent, etc. 15,000 Current Assets 325,000

Current Liabilities 125,000Real Estate 300,000FF&E 75,000 Bank Loan 300,000Intangibles Leases 100,000 Marketing 0 Artistic 0 Long Term Liabilities 400,000 Contract 0 Total Liabililties 525,000 Customer 0 Technology 0 Paid-in Capital 50,000

Retained Earnings 125,000 Long Term Assets 375,000

Total Equity 175,000Goodwill 0

Total Assets 700,000$ Total Liability & Equity 700,000$

Example

EXAMPLE SOFTWARE COMPANY

Selected Financial Highlights

Current Assets 325,000 Current Liabilities 125,000

Long Term Assets 375,000 Long Term Liabilities 400,000 Total Liabililties 525,000

Blue Sky 0 Total Equity 175,000

Total Assets 700,000$ Total Liability & Equity 700,000$

• Appraisal = $1,525,000• Book Value = $700,000• Blue Sky = $825,000

Example

What are identifiable intangible assets?

PREVIOUSLY SIMPLY CALLED ‘BLUE SKY’

Example

EXAMPLE SOFTWARE COMPANY

Selected Financial Highlights

Current Assets 325,000 Current Liabilities 125,000

Long Term Assets 375,000 Long Term Liabilities 400,000 Total Liabililties 525,000

Blue Sky 0 Total Equity 175,000

Total Assets 700,000$ Total Liability & Equity 700,000$

Example

EXAMPLE SOFTWARE COMPANYSelected Financial Highlights

Current Assets 325,000 Current Liabilities 125,000

Long Term Assets 375,000 Long Term Liabilities 400,000 Total Liabililties 525,000

Goodwill 825,000 Total Equity 1,000,000

Total Assets 1,525,000$ Total Liability & Equity 1,525,000$

Example

EXAMPLE SOFTWARE COMPANYSelected Financial Highlights

Current Assets 325,000 Current Liabilities 125,000

Long Term Assets 375,000 Long Term Liabilities 400,000 Intangible Assets 0 Total Liabililties 525,000 Goodwill 825,000

Total Equity 1,000,000Total Assets 1,525,000$ Total Liability & Equity 1,525,000$

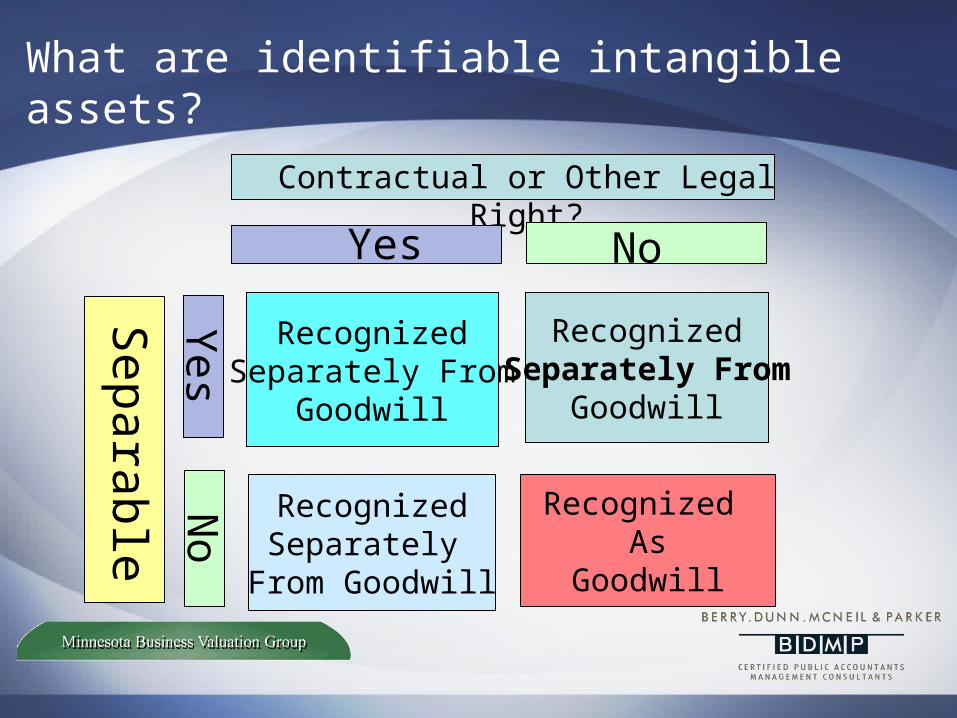

Contractual-Legal Criterion-Intangible assets arising from a distinct contractual or other legal basis, or

Separability Criterion-Intangible assets that do not arise from contractual or other legal rights, but are capable of being separated from the acquired entity and sold, transferred, licensed, rented or otherwise exchanged.

Sold, Licensed, Transferred, Rented, or Exchanged (SLERT)

What are identifiable intangible assets?

Contractual or Other Legal Right?

Yes No

RecognizedSeparately From

Goodwill

RecognizedSeparately

From Goodwill

RecognizedSeparately From

Goodwill

Recognized As

Goodwill

Yes

No

Separable

What are identifiable intangible assets?

EXHIBIT 1: TREATMENT OF INTANGIBLE ASSETS

Acquired Intangible Assets

Internally Arising from Contractual or Legal RightsGeneratedIntangible

Assets GoodwillFinite Lives Indefinite Lives

Not Recognized Recorded at Recorded at Recorded atFair Value/ Fair Value/ Fair Value/

Not Amortized Amortized/ Not AmortizedImpairment Test Impairment Test Impairment Test

(SFAS 142) (SFAS 144) (SFAS 142)

What are identifiable intangible assets?

Combination of assets under SFAS 141(R)

Goodwill becomes the “remaining piece” only after all other tangible and intangible assets have been indentified & valued

Intangible Assets =

•Sold

•Exchanged

•Rented

•Transferred

What are identifiable intangible assets?

SLERT

Intangible Assets =

•Marketing

•Artistic

•Contract

•Customer

•Technology

What are identifiable intangible assets?

MACCT

EXAMPLE SOFTWARE COMPANYSelected Financial Highlights

Marketing, Artistic, Customer, Contract, Technology

Intangible Assets 0 Goodwill 825,000

Example

• Intangibles = $800,000• Goodwill = $25,000• Blue Sky = $825,000

Example

EXAMPLE SOFTWARE COMPANYSelected Financial Highlights

Intangible Assets 800,000 Goodwill 25,000

Example

EXAMPLE SOFTWARE COMPANY EXAMPLE SOFTWARE COMPANYSelected Financial Highlights Selected Financial Highlights

Current Assets 325,000 Current Liabilities 125,000

Long Term Assets 375,000 Long Term Liabilities 400,000 Intangible Assets 800,000 Total Liabililties 525,000 Goodwill 25,000

Total Equity 1,000,000Total Assets 1,525,000$ Total Liability & Equity 1,525,000$

Example

EXAMPLE SOFTWARE COMPANYBalance Sheet

Cash & Eqivalent 50,000 Current Long Term Debt 25,000Accounts Receivable 250,000 Accounts Payble 75,000Pre-paid Taxes 25,000 Accrued Taxes 10,000

Wages, Rent, etc. 15,000 Current Assets 325,000

Current Liabilities 125,000

Real Estate 300,000 EXAMPLE SOFTWARE COMPANYFF&E 75,000 Bank Loan 300,000Intangibles Leases 100,000 Marketing 100,000 Artistic 75,000 Long Term Liabilities 400,000 Contract 125,000 Total Liabililties 525,000 Customer 225,000 Technology 275,000 Paid-in Capital 50,000

Retained Earnings 125,000 Long Term Assets 1,175,000 (Plus Added equity accrual)

Total Equity 1,000,000Goodwill 25,000

EXAMPLE SOFTWARE COMPANYSelected Financial Highlights

Total Assets 1,525,000$ Total Liability & Equity 1,525,000$

Example

Telephone Company Adjustments

• Fair Value of Tangible Assets

– Equipment

– Real Estate

• Fair Value of Investments

– Investment in wireless

– Investment in directory publishing

– Other

• Fair Value of Intangible Assets

– Customer Lists

– Licensing

– Trade name

– Technology

– Joint ventures

Take Aways / Take Home

• Valuing your telephone company• Purpose – Multiple • Standard of Value• From an Accounting Perspective – SFAS 157• Using SFAS 141(R)• Adjusting Assets• Identifying Intangible Assets• What goodwill really means

QUESTIONS?

THANK YOU!!!