subchapter s: vivé le difference - chapman law review

TRANSCRIPT

Subchapter S: Vivé le Difference

Roberta Mann University of Oregon

Chapman Law Symposium March 14, 2014

Presenta(on Outline • Why subchapter S?

– Poli(cians want to help “small businesses” • Why?

– Does subchapter S help small businesses?

• Sta(s(cs – S corps s(ll popular – Returns filed by en(ty type – S corps are generally “small”

• Comparing taxa(on of S corps and LLCs

• Reviewing the arguments for repeal – Having two passthrough regimes is “inefficient”

– Plain vanilla LLCs are just as simple as S corps

– The danger of choice vs. the value of choice

• Conclusion – Taxpayers should have choice

What’s good for small business?

S Corps LLCs

A Brief Overview of Business Types and Their Tax Treatment

Congressional Research Service 2

And third, there have been off and on discussions about moving to a more uniform business tax environment. According to traditional economic theories of taxation there is no reason why otherwise identical businesses should be taxed differently. According to the same theories, when such differences do exist, the result is an inefficient allocation of resources, which occurs at the expense of stronger economic performance. The current tax disparity could be reduced via two general approaches. First, the corporate and individual tax systems could be combined or “integrated” so that corporations were treated similar to pass-throughs.3 Second, pass-throughs could be subjected to the corporate tax.4

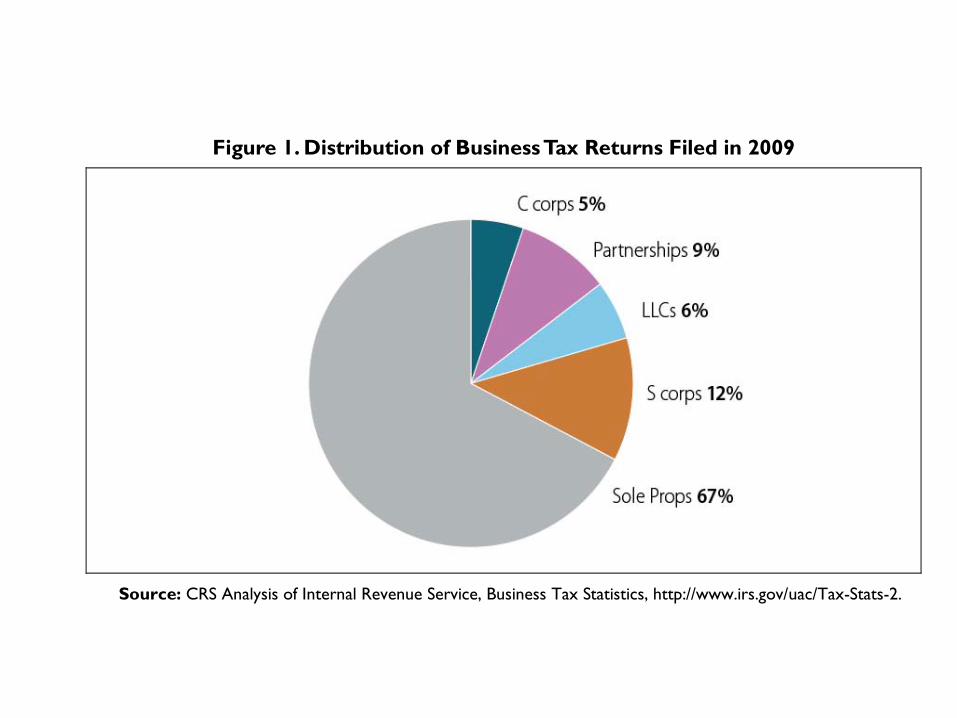

Figure 1. Distribution of Business Tax Returns Filed in 2009

Source: CRS Analysis of Internal Revenue Service, Business Tax Statistics, http://www.irs.gov/uac/Tax-Stats-2.

It is perhaps useful to briefly quantify the business landscape across the various business forms before proceeding. Figure 1 displays the distribution of business tax returns filed in tax year 2009. The Internal Revenue Service (IRS) reports that there were approximately 29.5 million corporate and pass-through tax returns filed.5 The majority (67%) were sole proprietorships. The

3 In 1992, the Department of the Treasury drafted a 268-page report containing a comprehensive analysis of corporate and individual tax integration. See, The Department of the Treasury, Integration of the Individual and Corporate Tax Systems: Taxing Business Income Once, Washington, DC, January 1992, http://www.treasury.gov/resource-center/tax-policy/Documents/integration.pdf. For a summary of the Treasury report, see R. Glenn Hubbard, “Corporate Tax Integration: A View from the Treasury Department,” Journal of Economic Perspectives, vol. 7, no. 1 (Winter 1993), pp. 115-132. 4 In early 2011, Senate Finance Committee Chairman Max Baucus suggested the possibility of taxing pass-throughs with earnings above a certain income as corporations. See, Nicola M. White and Drew Pierson, “Baucus Says Congress Should Look at Taxing Passthroughs as Corporations,” Tax Notes Today, May 5, 2011. The Obama Administration also suggested such a policy change could be needed to lower the corporate tax rate in a report outlining the President’s framework for business tax reform. See, A Joint Report by the White House and the Department of the Treasury Department, The President’s Framework for Business Tax Reform, Washington, DC, February 2012, p. 10, http://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-02-22-2012.pdf. House Ways and Means Committee Chairman Dave Camp, however, has expressed his opposition to such a policy change. See, Bernie Becker, “Members eager for White House tax plan,” The Hill, May 4, 2011, Online edition, http://thehill.com/business-a-lobbying/159351-lawmakers-eager-for-white-house-tax-plan-. 5 Internal Revenue Service, Tax Statistics, various tables, http://www.irs.gov/uac/Tax-Stats-2.

Doc 2013-14370 (12 pgs)

A Brief Overview of Business Types and Their Tax Treatment

Congressional Research Service 3

next most popular was S corporations (12%), followed by partnerships (9%), and LLCs (6%). C corporations comprised the smallest share of business returns filed (5%).

Figure 2. Net Business Income By Business Type, 1980-2008

Source: CRS analysis of Internal Revenue Service, Statistics of Income, Integrated Business Data, http://www.irs.gov/pub/irs-soi/80ot1all.xls.

Figure 2 displays the share of net business income generated by the various business types between 1980 and 2008. The most noticeable trend has been the decline in the share of income generated by C corporations.6 At the same time, the shares generated by S corporations and partnerships have trended upward. LLCs have also slowly increased their share of business income since 1993, when LLCs first appeared as an option on the partnership tax form (this is discussed in the “Limited Liability Companies” section). Sole proprietorships appear to have possibly decreased in importance as a generator of business income, although it is difficult to conclude whether this decrease is the result of a cyclical downturn towards the end of the sample period, or a more permanent trend. In the end, Figure 2 highlights the fact that pass-throughs are just as significant as corporations when it comes to economic activity.

C Corporations A popular business structure is the corporate form, of which there are two types; C corporations, which are discussed in this section, and S corporations, which are discussed later. C corporations, also known as ordinary corporations, are named for Subchapter C of the Internal Revenue Code (IRC), which details their tax treatment. Businesses incorporate under state law and the exact requirements for incorporation may vary from state to state. Typically, a business must first file articles of incorporation at the state level in order to incorporate.7 C corporations are considered

6 For an in-depth analysis of why corporate tax revenues have fallen, see CRS Report R42113, Reasons for the Decline in Corporate Tax Revenues, by Mark P. Keightley. 7 While a business may choose any state in which to incorporate, Delaware is by far the most popular. According to Delaware’s Division of Corporations, 63% of Fortune 500 companies chose Delaware as their state of incorporation. (continued...)

Doc 2013-14370 (12 pgs)

X!

%14/4/%>O!!8$%!1'U.%+!*)!]>U,((_!;!#*+C*+,4/*1>@!4$*>%!`/4$!,>>%4>!(%>>!4$,1!f?BB@BBB@!)%((!.D!,CC+*V/U,4%(D!??B@BBB!*W%+!4$%!>,U%!C%+/*&O!

!

"!!#!!!

$#!!!#!!!

$#"!!#!!!

%#!!!#!!!

%#"!!#!!!

)#!!!#!!!

=.;>> K0H6-.�$&&)

L;1J0 =.;>> K0H6-.�$&&(

L;1J0 =.;>> K0H6-.�%!!)

L;1J0 =.;>> K0H6-.�%!!(

L;1J0

<21�9B65�@-1@250#�5.;>>�/-56705505�;10�9B250�M69B�>055�9B;7�N$!!#!!!�67�;55095O�.0H6-.�/-56705505�B;G0�/09M007�N$!!#!!!�;7H�N$�.6>>627�67�;55095O�;7H#�>;1J0�/-56705505�B;G0�.210�9B;7�N$�.6>>627�67�;55095I

!"#$%&�E(�1C&�)$*+&%�,-�?*>@@7�F&D"$*7�>/D�G>%#&�5$4"/&44�H/��&4+2�123&�,-�G&#>@�H/0"027�'88E7�'88:7�;<<E7�>/D�;<<:

A�A21@

=�A21@

?;197015B6@

=2-1C0D��P2679�A2..69900�27�Q;R;9627�C;>C->;96275�27�=SE�H;9;I�

!

&I8!K;ES9I!E>!@?J?98A!@?GB?@?9C!DEJFG<?8=!

8$%!'>%!*)!4$%!RR;!,>!,1!%14/4D!/>!C+/U,+/(D!,!&%W%(*CU%14!*)!4$%!C,>4!AB!D%,+>O!!=*>4!RR;>!%(%#4!4*!.%!4,V%&!,>!C,+41%+>$/C>!)*+!9%&%+,(!+%C*+4/12!C'+C*>%>!,1&!4$%/+!1'U.%+>!,+%!#*'14%&!,U*12!4$%!C,+41%+>$/C!&,4,!+%C*+4%&!/1!8,.(%!?!,1&!9/2'+%>!?@!A@!,1&!Q!,.*W%O!!9/2'+%!T@!.%(*`@!&%#*UC*>%>!4$%!1'U.%+!*)!C,+41%+>$/C>!)*+!4$%!C%+/*&!?YYB!4$+*'2$!ABBY!/14*!2%1%+,(!C,+41%+>$/C>@!(/U/4%&!C,+41%+>$/C>@!,1&!RR;>OY!!9/2'+%!T!&*#'U%14>!4$%!+,C/&!2+*`4$!*)!RR;>!+%(,4/W%!4*!*4$%+!)*+U>!*)!.'>/1%>>!*+2,1/c,4/*1!4$,4!,+%!4,V%&!,>!C,+41%+>$/C>!*W%+!4$%!C,>4!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!Y!!8$%!&,4,!/1!8,.(%!A!U,D!1*4!>'U!4*!4$%!4*4,(!1'U.%+!*)!C,+41%+>$/C>!+%C*+4%&!/1!8,.(%!?!.%#,'>%!*)!

+*'1&/12O!!7(>*@!4$/>!&%#*UC*>/4/*1!%V#('&%>!4$*>%!.'>/1%>>%>!4$,4!#$%#b%&!4$%!]*4$%+_!.*V!*1!9*+U!?BIS@!"#$%&'(%!3@!(/1%!?O!!"%%@!7(,1!P%UC%(@!]-,+41%+>$/C!J%4'+1>@!?YYX@_!SOI Bulletin@!AB@!9,((!ABBB@!,1&!6/1,!"$'U*)>bD!,1&!R,'+%1!R%%@!]-,+41%+>$/C!J%4'+1>@!ABBY@_!SOI Bulletin@!Q?@!9,((!AB??O!

!

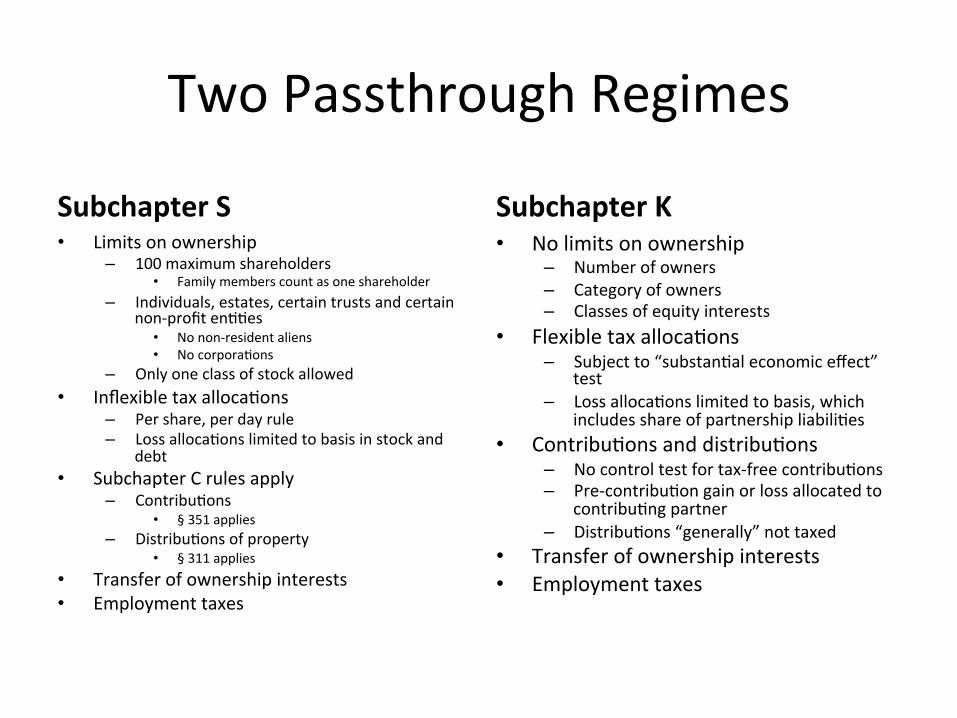

Two Passthrough Regimes

Subchapter S • Limits on ownership

– 100 maximum shareholders • Family members count as one shareholder

– Individuals, estates, certain trusts and certain non-‐profit en((es • No non-‐resident aliens • No corpora(ons

– Only one class of stock allowed • Inflexible tax alloca(ons

– Per share, per day rule – Loss alloca(ons limited to basis in stock and

debt • Subchapter C rules apply

– Contribu(ons • § 351 applies

– Distribu(ons of property • § 311 applies

• Transfer of ownership interests • Employment taxes

Subchapter K • No limits on ownership

– Number of owners – Category of owners – Classes of equity interests

• Flexible tax alloca(ons – Subject to “substan(al economic effect”

test – Loss alloca(ons limited to basis, which

includes share of partnership liabili(es • Contribu(ons and distribu(ons

– No control test for tax-‐free contribu(ons – Pre-‐contribu(on gain or loss allocated to

contribu(ng partner – Distribu(ons “generally” not taxed

• Transfer of ownership interests • Employment taxes

Is choice inefficient? Is efficiency more important than freedom?

More choice? A be5er choice?

Can an en(ty taxed as a partnership be “plain vanilla?”

• Tracking of pre-‐contribu(on gain and loss

• Mixing bowl transac(ons

• Hot asset rules • Alloca(ons of recourse and non-‐recourse debt

Would limi(ng choice limit abuse? • “The elec(ve treatment of

private firms under current law undermines both equity and efficiency objec(ves for the income tax.” – George Yin (1999)

• “There is a significant risk that the uniform system will produce an unhappy combina(on: rules s(ll too complicated for the less sophis(cated and too imprecise and manipulable for the more sophis(cated.” – George Yin (2013)

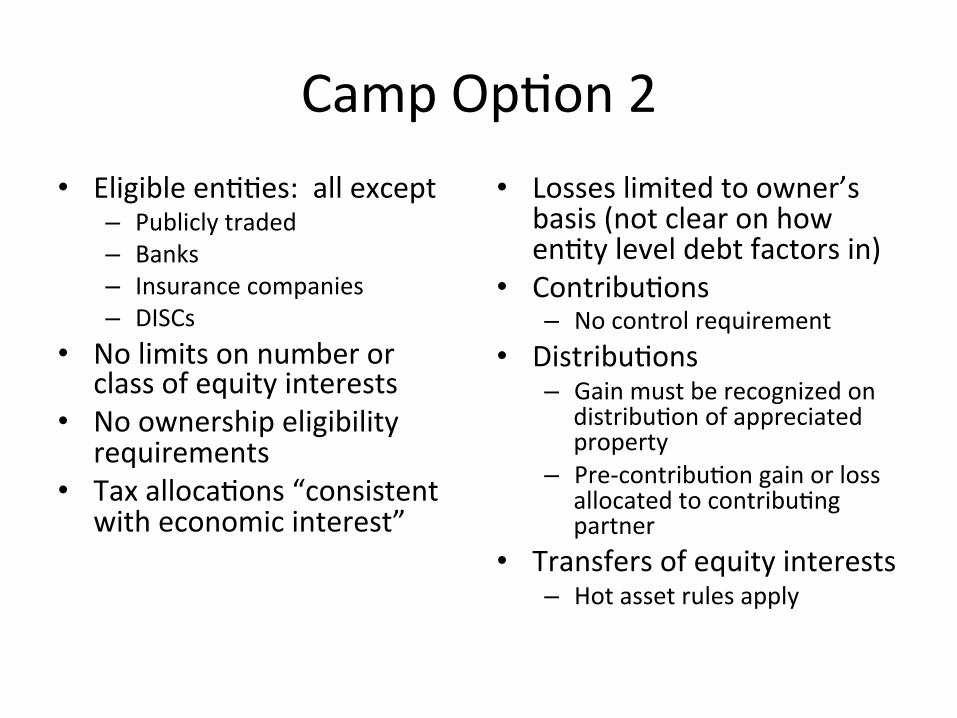

Camp Op(on 2 • Eligible en((es: all except

– Publicly traded – Banks – Insurance companies – DISCs

• No limits on number or class of equity interests

• No ownership eligibility requirements

• Tax alloca(ons “consistent with economic interest”

• Losses limited to owner’s basis (not clear on how en(ty level debt factors in)

• Contribu(ons – No control requirement

• Distribu(ons – Gain must be recognized on

distribu(on of appreciated property

– Pre-‐contribu(on gain or loss allocated to contribu(ng partner

• Transfers of equity interests – Hot asset rules apply

Conclusion Á chacun son goût

Recommenda:ons • Keep subchapter S

– Simplicity advantages • Per share, per day alloca(on • No need to track assets

• Changes – Include en(ty level debt in

owner’s basis – Eliminate employment tax

loophole • Either by repeal OR • By allowing LLC to use

“reasonable compensa(on” as the base for employment tax

Will this help small businesses? • Flow through tax treatment

not a good proxy for small business

• Small businesses not necessarily “job creators”

• BUT • Vast majority of S corpora(ons

have 3 or fewer shareholders • Most S corpora(ons are small

in terms of asset value