study session august 18, 2020

TRANSCRIPT

Study SessionAugust 18, 2020

˃Brief Overview of Office

˃Low Value Exemptions

˃Intercounty Transfers of Base Year Values

˃Split Roll Initiative

˃Unsecured Assessments

˃Assess all taxable property in the county

˃Discover, Inventory, and Value Property

˃Produce an Assessment Roll and Supplemental Roll

˃Administer Property Tax Exemptions

˃Maintain Assessment Maps

˃Enacted by the voters on June 6, 1978

˃Commonly referred to as Proposition 13

˃Applies to locally assessed real property

˃Rolled assessed values back to their 1975 AV

˃Established concept of Base Year Value [BYV]

˃Limited increases to Base Year Value to the lesser of:• 2%• Increase in California CPI

˃Property is reassessed with new base year value when there is

• a Change in Ownership

• New Construction

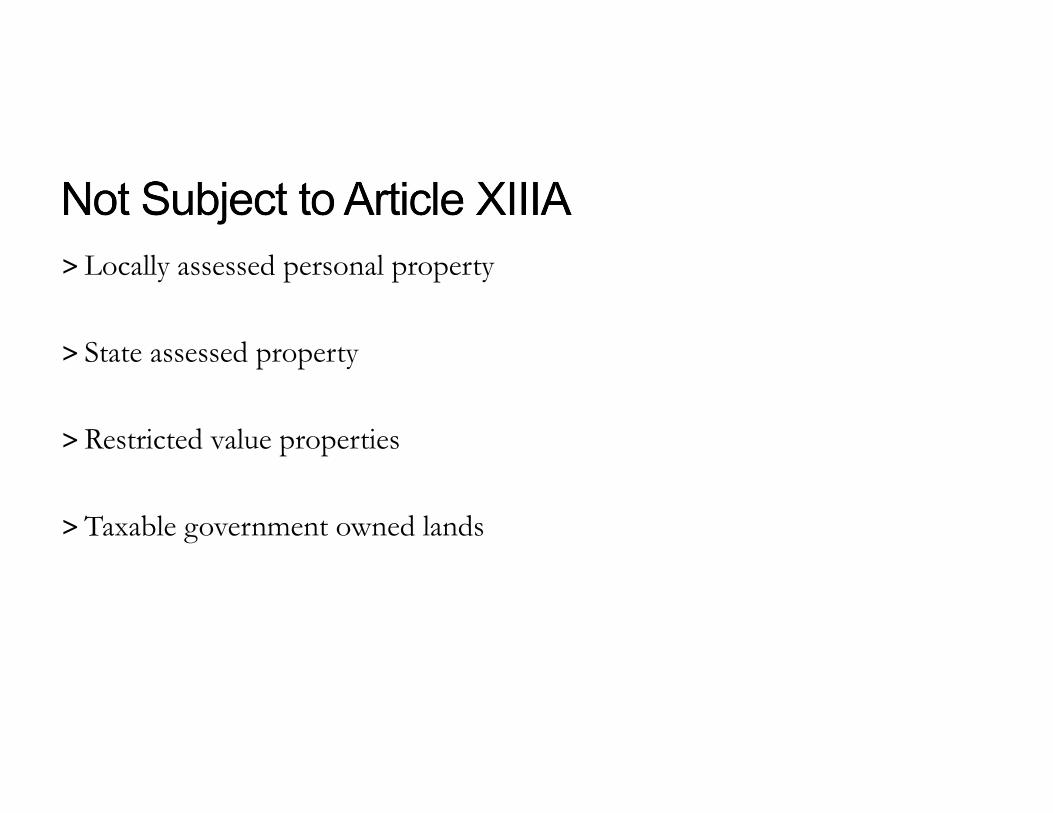

˃Locally assessed personal property

˃ State assessed property

˃Restricted value properties

˃Taxable government owned lands

˃Assessment Roll vs. Tax Roll

˃Assessment Year vs. Fiscal Year

˃Lien Date

˃Regular• Secured• Unsecured

˃Supplemental• Secured• Unsecured

˃Unitary

Parcel Count

Personal Property

Homeowners' Exemptions

Other ExemptionsLand Improvements Total

Secured 45,239 2,015,606,298 5,892,347,063 24,403,538 (72,018,613) (93,657,632) 7,766,680,654

Unsecured 3,747 7,120,122 47,200,851 96,820,995 (21,000) (37,913,007) 113,207,961

Total 48,986 2,022,726,420 5,939,547,914 121,224,533 (72,039,613) (131,570,639) 7,879,888,615

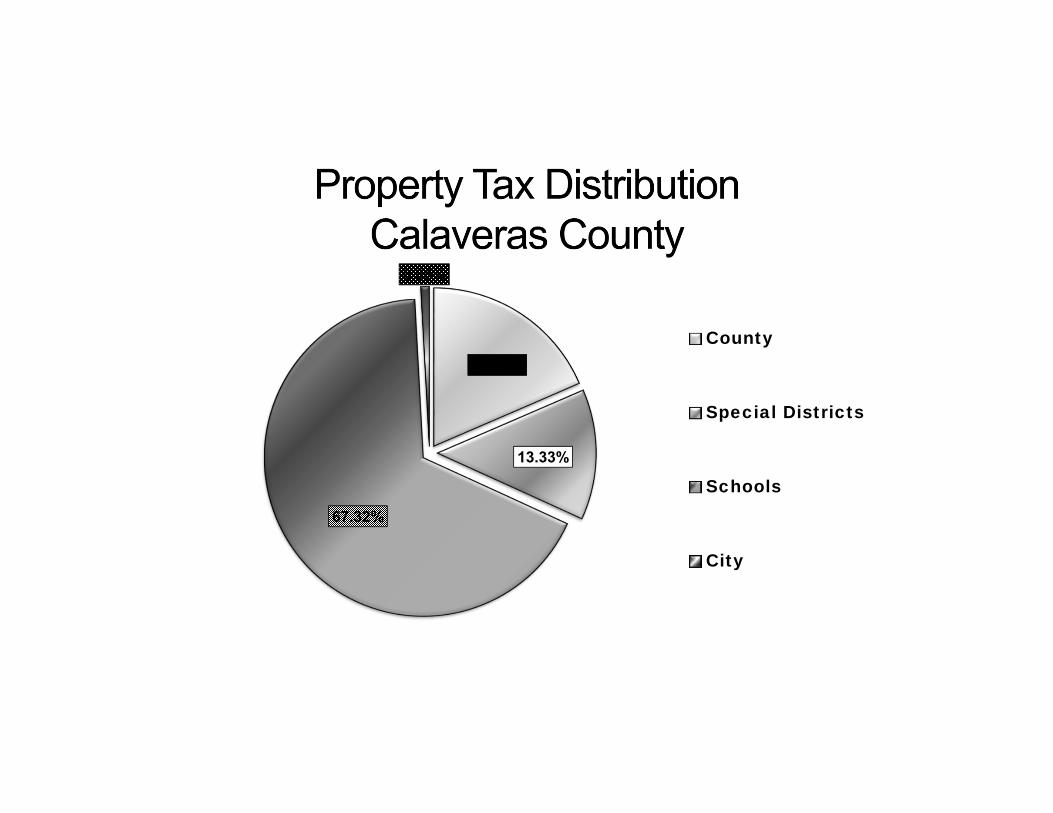

18.50%

13.33%

67.32%

0.85%

County

Special Districts

Schools

City

˃Statutory Authority• Revenue and Taxation Code Section 155.20

˃Legislative Intent• Revenue should exceed cost to assess and collect

˃Current Status in Calaveras County• $2,000 limit• Resolution 91-75

˃Changes to Revenue and Taxation Code• Several changes over the years • 2001 increase to $5,000 exemption• 2010 increase to $10,000 exemption• 2019 increase to $50,000 for all Possessory Interests

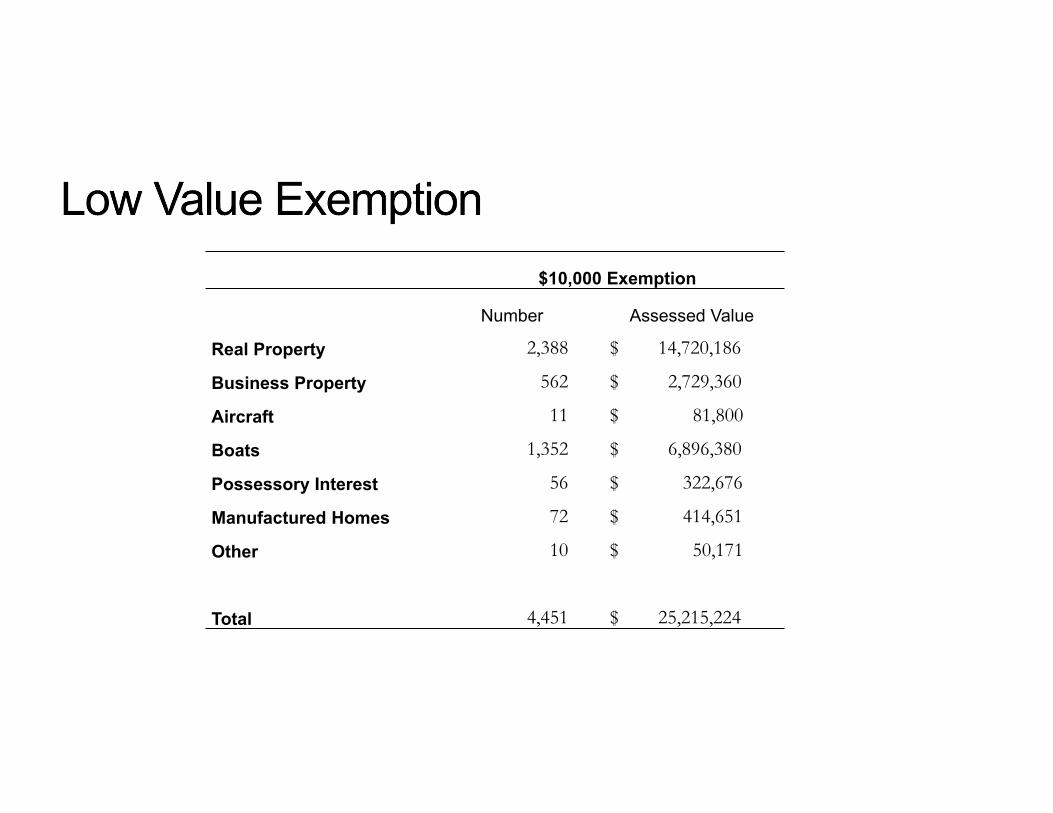

$10,000 Exemption

Number Assessed Value

Real Property 2,388 $ 14,720,186

Business Property 562 $ 2,729,360

Aircraft 11 $ 81,800

Boats 1,352 $ 6,896,380

Possessory Interest 56 $ 322,676

Manufactured Homes 72 $ 414,651

Other 10 $ 50,171

Total 4,451 $ 25,215,224

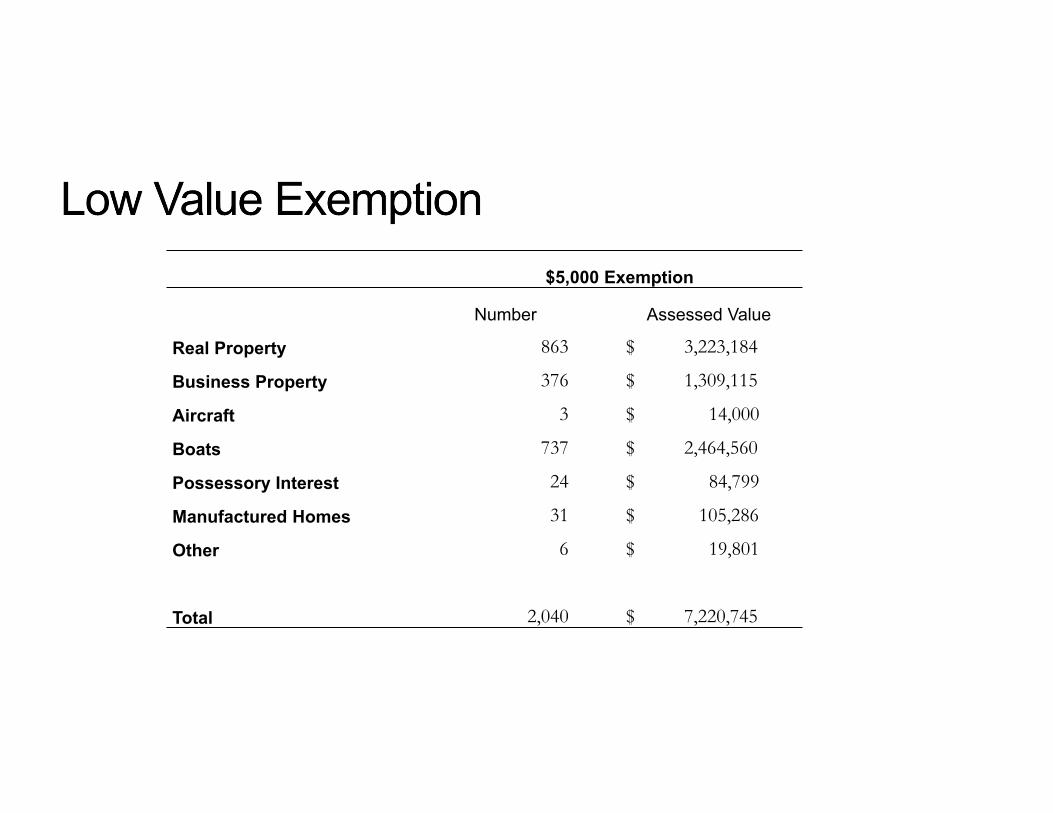

$5,000 Exemption

Number Assessed Value

Real Property 863 $ 3,223,184

Business Property 376 $ 1,309,115

Aircraft 3 $ 14,000

Boats 737 $ 2,464,560

Possessory Interest 24 $ 84,799

Manufactured Homes 31 $ 105,286

Other 6 $ 19,801

Total 2,040 $ 7,220,745

Possessory Interests

Total < $50,000 > $50,000

Number 115 100 15

Assessed Value $ 6,647,394 $ 1,261,607 $ 5,385,787

˃Coordination with other Departments

˃Willing to Amend Exemption?• $10,000 all property types• <$50,000 for all Possessory Interests

˃Statutory Authority

• Amendment to Article XIIIA § 2

• Added Revenue and Taxation Code § 69.5

˃Proposition 90 of 1988

• Effective November 9, 1988

• Both original and replacement property can be in different counties

• Replacement county must have an ordinance participating in the

program

• Claimant or Claimant’s spouse is over 55

˃How it Works• Allow transfers of factored base year value to a replacement property

• Certain conditions must be met

Required of Original AND Replacement Property

o Must own and occupy the residence

o Not required to have an HOX or DAV

□ Just need to qualify for the exemption

˃Current Status in Calaveras County and California

˃Ballot Initiatives

• 2018 Proposition 5

Calaveras 41.7% yes, 58.3% no

• 2020 Proposition 19 [ACA 11]

˃2020 Proposition 19

• ACA 11

• The Home Protection for Seniors, Severely Disabled, Families, and

Victims of Wildfire or Natural Disasters Act

• Alters three earlier Propositions [90/58/193]

˃Expands transfers of Base Year Values

• On or after April 1, 2021

• Primary owner

Over 55 years of age

Severely disabled

Victim of a wildfire or natural disaster

˃Limits to three transfers of base year value

˃Changes Parent-Child and Grandparent-Grandchild Transfers

• On and after February 16, 2021

• Family Home is excluded from reappraisal if:

Children/Grandchildren occupy as their primary residence

˃Creates a California Fire Response Fund

• Revenues and savings resulting from implementation

• Funds for fire suppression staffing

Department of Forestry and Fire Protection

Underfunded fire protection districts

˃County Revenue Protection Fund

• Reimburse local agencies for negative impact

• Excess transferred to State General Fund

˃Legislative Intent

• Remove unfair location restrictions

• Eliminate unfair tax loopholes

˃Key Provisions • Intercounty Transfer of Factored Base Year Value Replacement < Original Property: Transfer FBYV Replacement > Original Property: Difference + Original FBYV

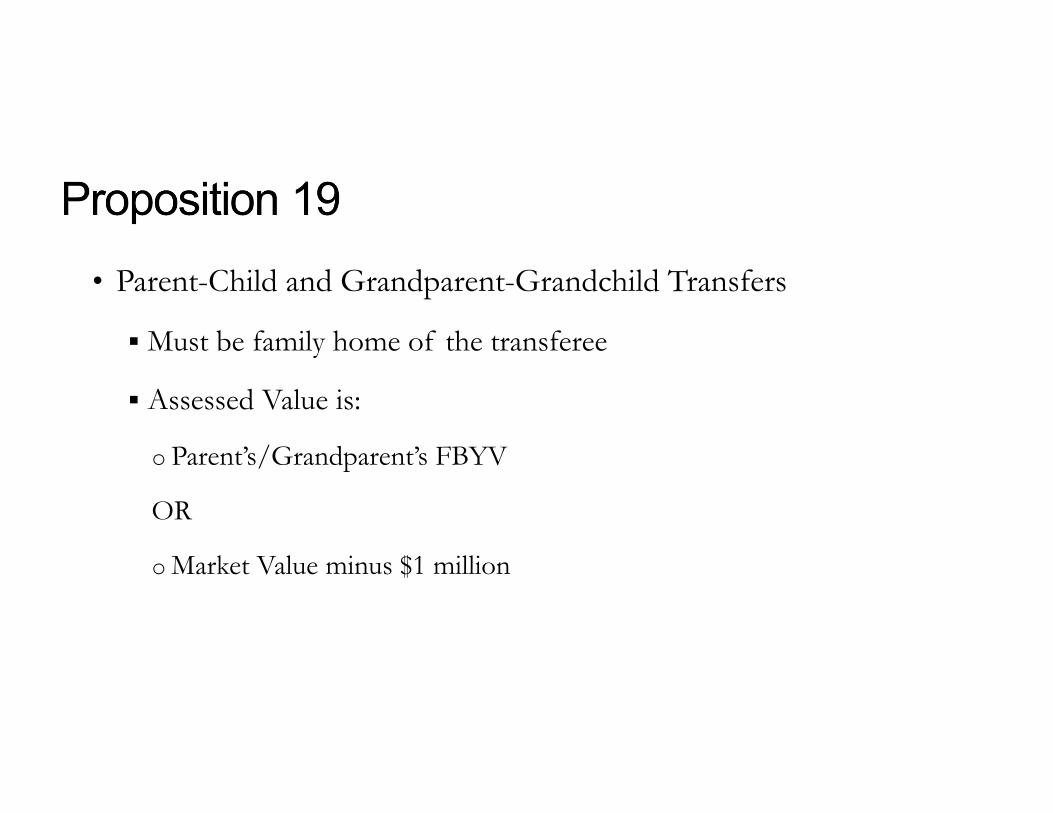

• Parent-Child and Grandparent-Grandchild Transfers

Must be family home of the transferee

Assessed Value is:

o Parent’s/Grandparent’s FBYV

OR

o Market Value minus $1 million

˃Interest in Ordinance?

˃Brief History˃Intent of Proponents

• Preserve Prop 13’s protections for homeowners and residential rental property

• Increase revenues for schools, counties, cities, and other local agencies

• Guarantee new revenues go to schools, community colleges Requires disclosure of new revenues and how spent

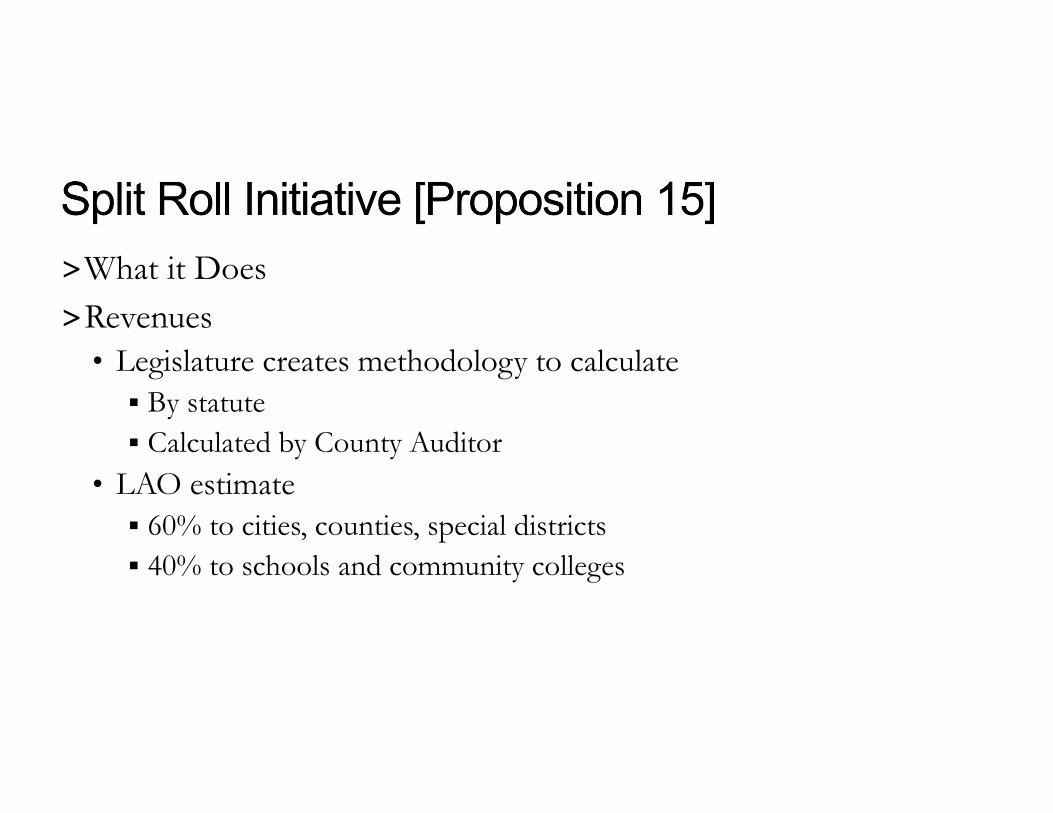

• Applies to commercial and industrial real property

˃What it Does˃Revenues

• Legislature creates methodology to calculate By statute Calculated by County Auditor

• LAO estimate 60% to cities, counties, special districts 40% to schools and community colleges

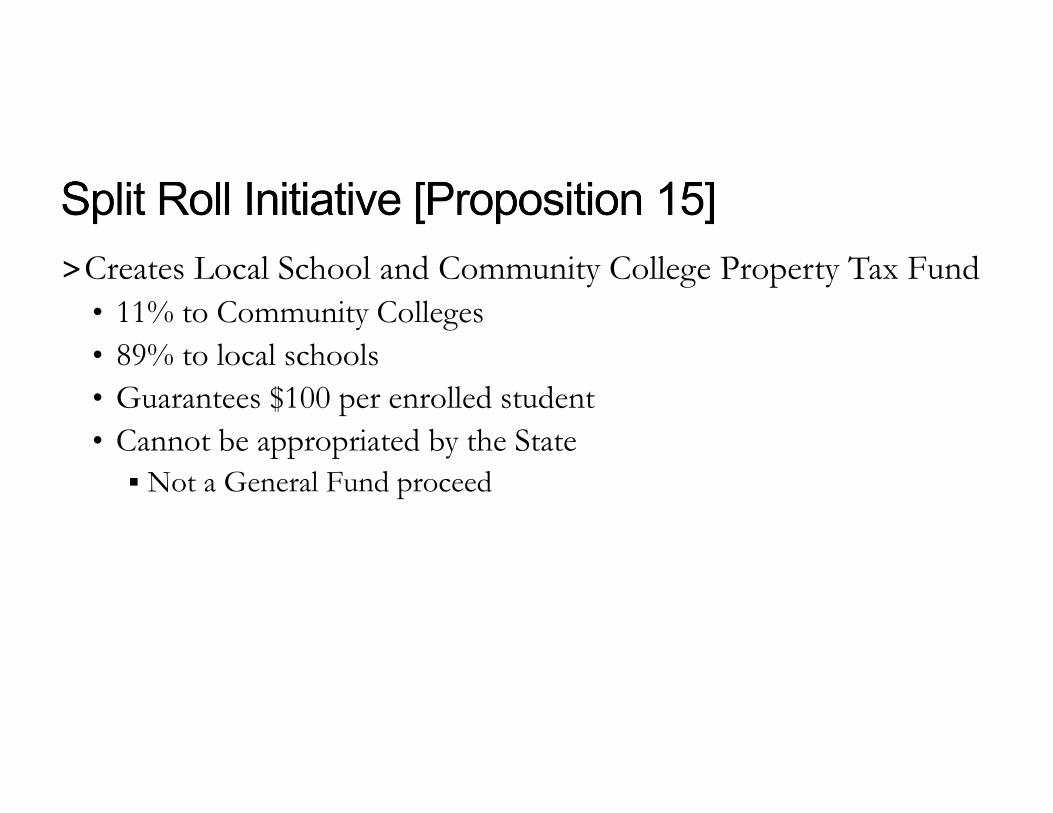

˃Creates Local School and Community College Property Tax Fund• 11% to Community Colleges• 89% to local schools• Guarantees $100 per enrolled student• Cannot be appropriated by the State Not a General Fund proceed

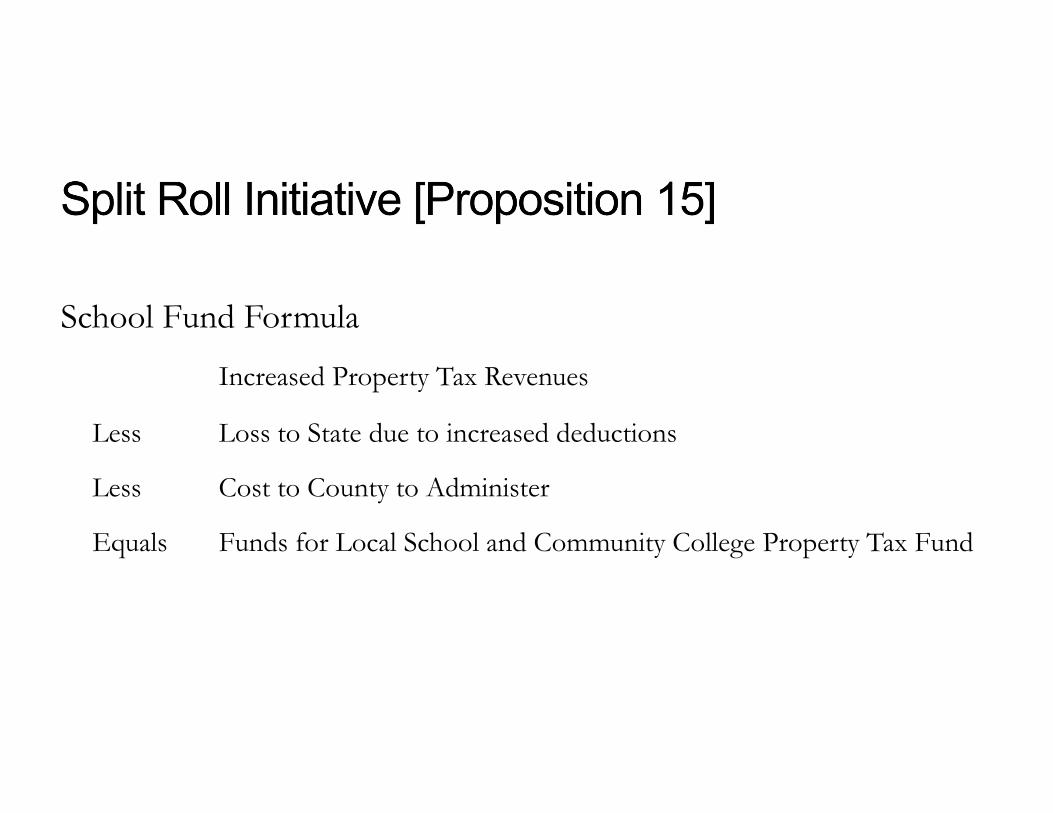

School Fund Formula

Increased Property Tax Revenues

Less Loss to State due to increased deductions

Less Cost to County to Administer

Equals Funds for Local School and Community College Property Tax Fund

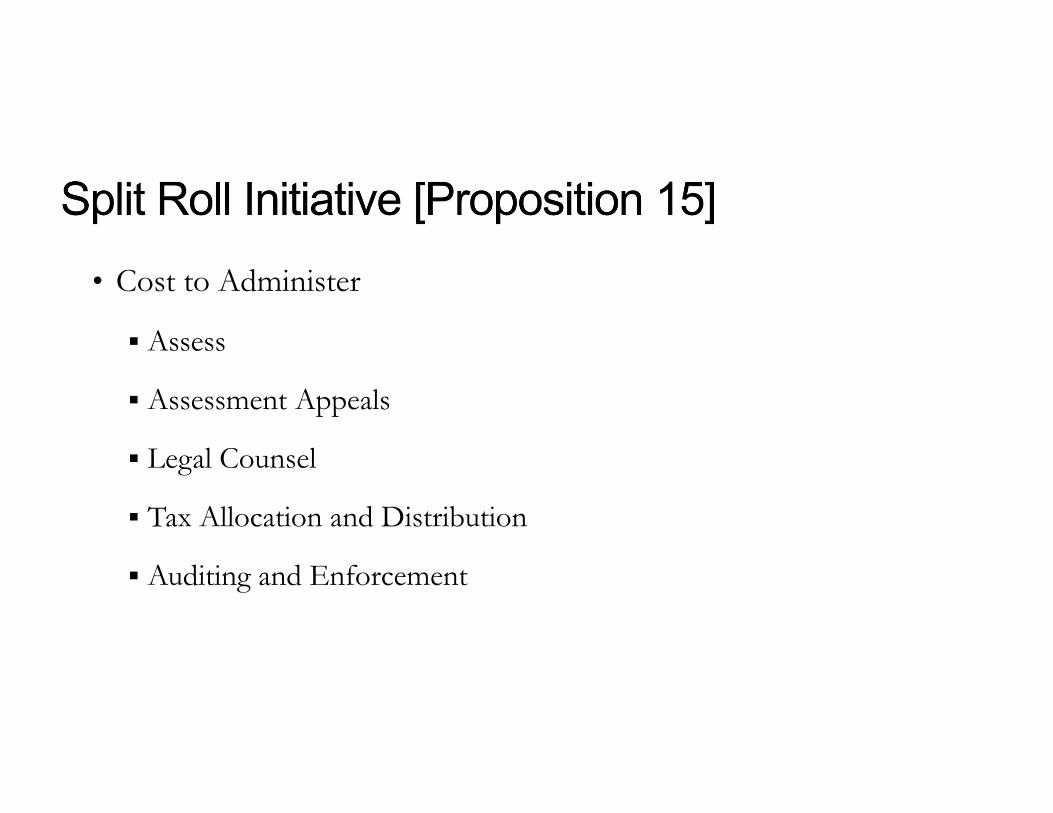

• Cost to Administer

Assess

Assessment Appeals

Legal Counsel

Tax Allocation and Distribution

Auditing and Enforcement

˃Property Reassessment

• Starts with 2022 Lien Date

• Commercial and Industrial Real Property

˃Does Not Apply to:

• Residential Property

Owner Occupied

Renter

Home-Based Business or Short-Term Rental

• Commercial Agricultural Production

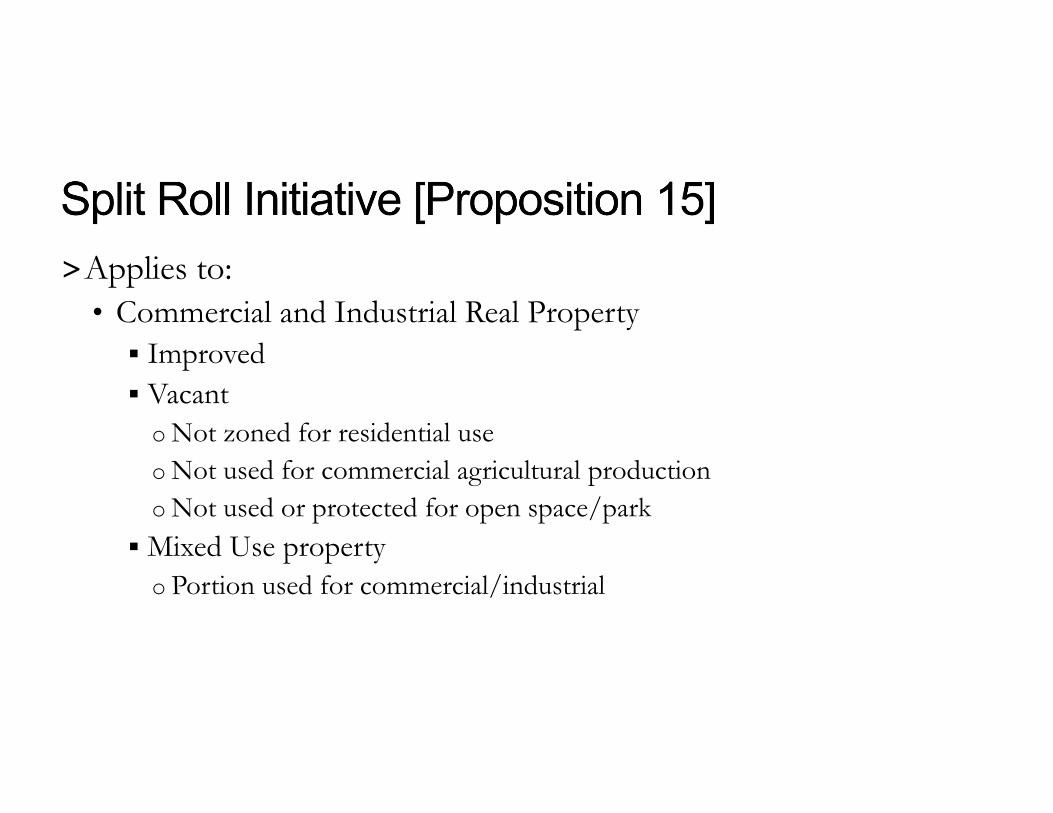

˃Applies to:• Commercial and Industrial Real Property Improved Vacant

o Not zoned for residential useo Not used for commercial agricultural productiono Not used or protected for open space/park

Mixed Use propertyo Portion used for commercial/industrial

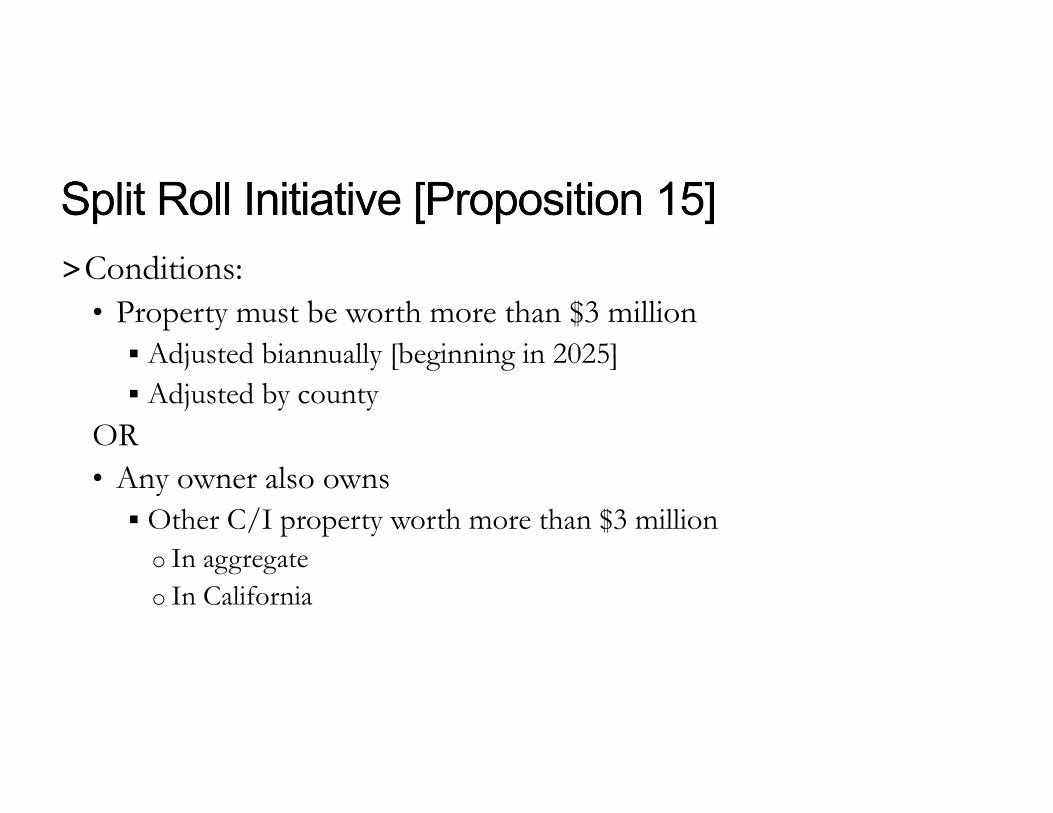

˃Conditions:• Property must be worth more than $3 million Adjusted biannually [beginning in 2025] Adjusted by county

OR• Any owner also owns Other C/I property worth more than $3 million

o In aggregateo In California

˃Phase-In Provisions

• Percentage of properties each year

• Cyclical Reappraisal every three years

• Assessment Appeals – expedited process

• Property Taxes

“reasonable” timeframe to pay increased taxes

˃Exclusions/Exemptions [Problem with terminology]

• $3 million exclusion reviewed annually

• Delays reassessment to 2025

o More than 50% occupied by small business

o Certified by property owner

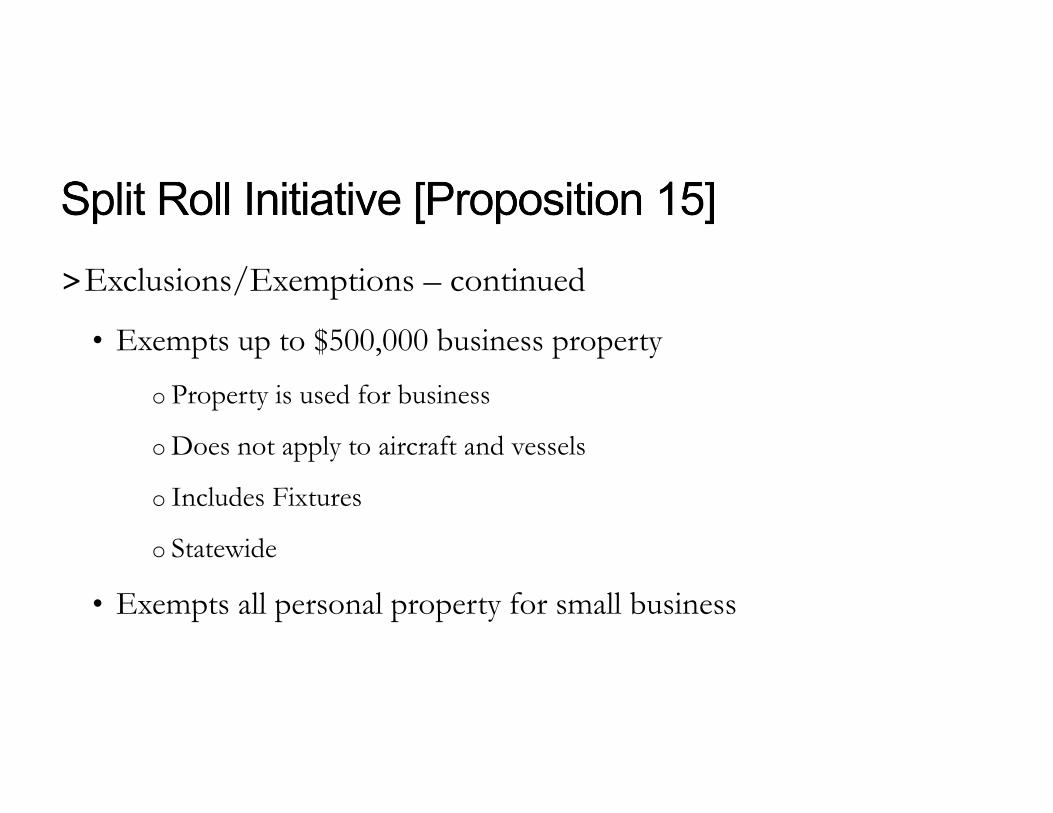

˃Exclusions/Exemptions – continued

• Exempts up to $500,000 business property o Property is used for business

o Does not apply to aircraft and vessels

o Includes Fixtures

o Statewide

• Exempts all personal property for small business

˃Small Business• <51 employees in California

• Independently owned and operated

• Located in California

• Owner and Officers are residents of California

• Not “dominant” in its field of operations Doesn’t control the field of operation

Doesn’t have major influence on a statewide basis

˃What it Does Not Do

• Change the tax rate

• Change Ag Preserve valuations

• Affect VLF adjustments

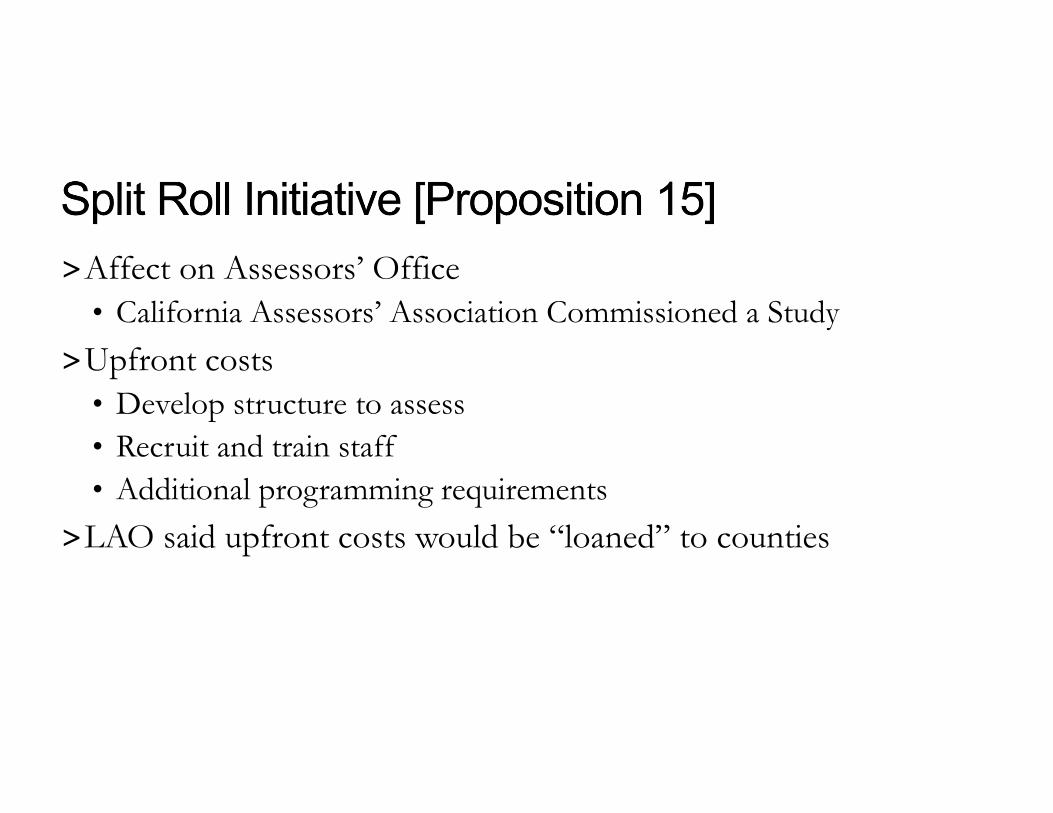

˃Affect on Assessors’ Office• California Assessors’ Association Commissioned a Study

˃Upfront costs• Develop structure to assess• Recruit and train staff• Additional programming requirements

˃LAO said upfront costs would be “loaned” to counties

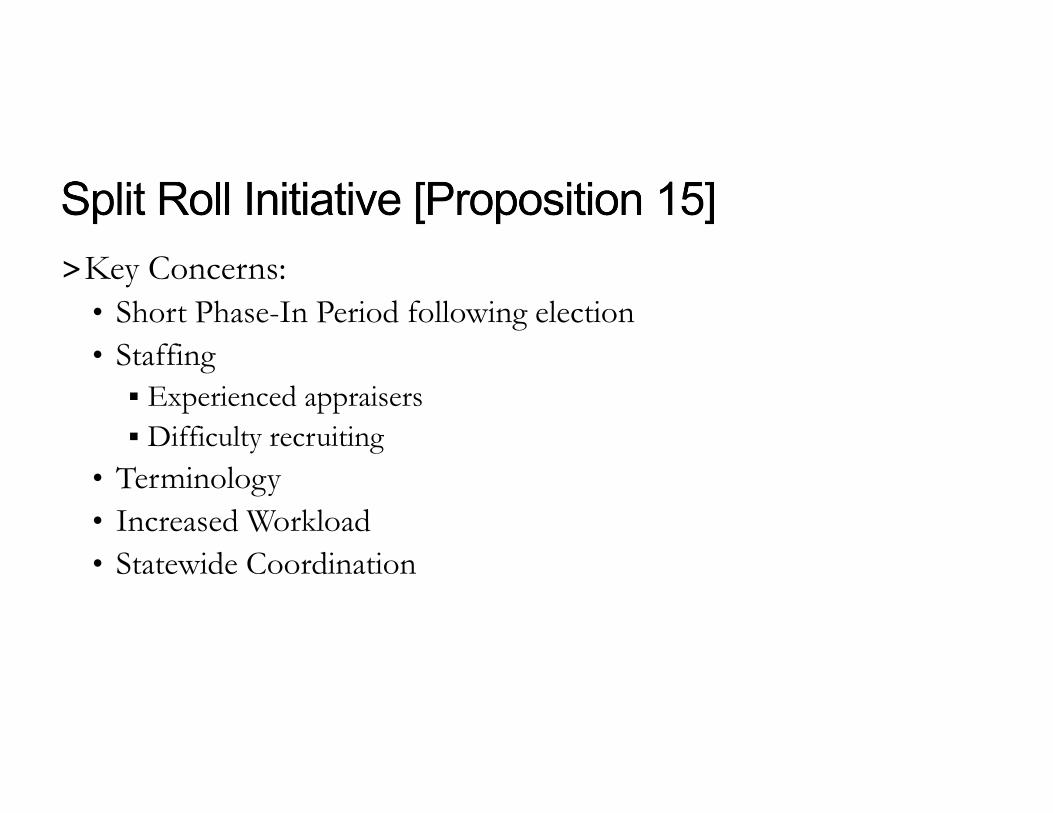

˃Key Concerns:• Short Phase-In Period following election• Staffing Experienced appraisers Difficulty recruiting

• Terminology• Increased Workload• Statewide Coordination

˃Affect on Calaveras County Assessment Roll - Real Property

• 11 parcels with AV > $3 million

• + ¾ of 1% of roll total

• 1,353 potential reassessments

1,040 are in DIV status

• Unlikely to see a huge increase in assessed value

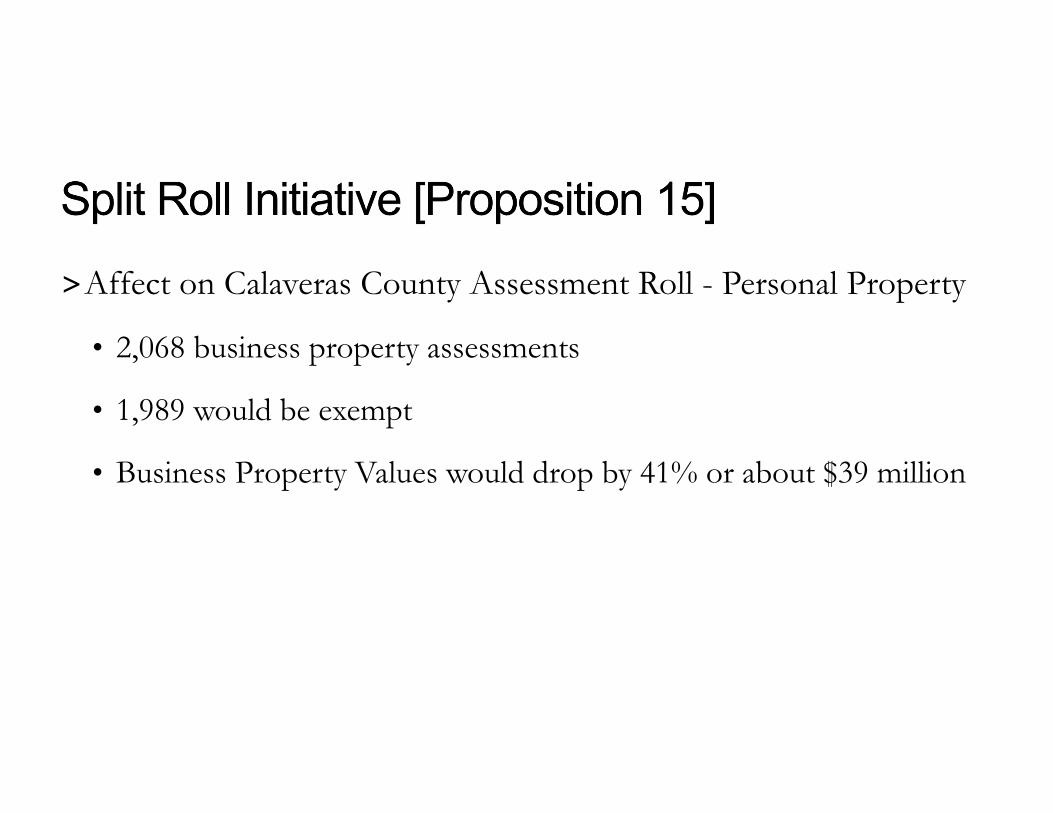

˃Affect on Calaveras County Assessment Roll - Personal Property

• 2,068 business property assessments

• 1,989 would be exempt

• Business Property Values would drop by 41% or about $39 million

˃Brief History• Funding• Staffing Issues

˃Concerns and Priorities

Questions?