stt 455-6: actuarial models - michigan state...

TRANSCRIPT

STT 455-6: Actuarial Models

Albert Cohen

Actuarial Sciences ProgramDepartment of Mathematics

Department of Statistics and ProbabilityA336 Wells Hall

Michigan State UniversityEast Lansing MI

[email protected]@stt.msu.edu

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 1 / 283

Copyright Acknowledgement

Many examples and theorem proofs in these slides, and on in class exampreparation slides, are taken from our textbook ”Actuarial Mathematics forLife Contingent Risks” by Dickson,Hardy, and Waters.

Please note that Cambridge owns the copyright for that material.No portion of the Cambridge textbook material may be reproducedin any part or by any means without the permission of thepublisher. We are very thankful to the publisher for allowing postingof these notes on our class website.

Also, we will from time-to-time look at problems from releasedprevious Exams MLC by the SOA. All such questions belong incopyright to the Society of Actuaries, and we make no claim onthem. It is of course an honor to be able to present analysis of suchexamples here.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 2 / 283

Survival Models

An insurance policy is a contract where the policyholder pays apremium to the insurer in return for a benefit or payment later.

The contract specifies what event the payment is contingent on. Thisevent may be random in nature

Assume that interest rates are deterministic, for now

Consider the case where an insurance company provides a benefitupon death of the policyholder. This time is unknown, and so theissuer requires, at least, a model of of human mortality

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 3 / 283

Survival Models

Define (x) as a human at age x . Also, define that person’s future lifetimeas the continuous random variable Tx . This means that x + Tx representsthat person’s age at death.

Define the lifetime distribution

Fx(t) = P[Tx ≤ t] (1)

the probabiliity that (x) does not survive beyond age x + t years, and it’scomplement, the survival function Sx(t) = 1− Fx(t).

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 4 / 283

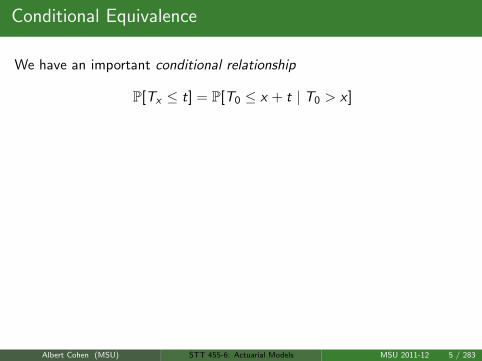

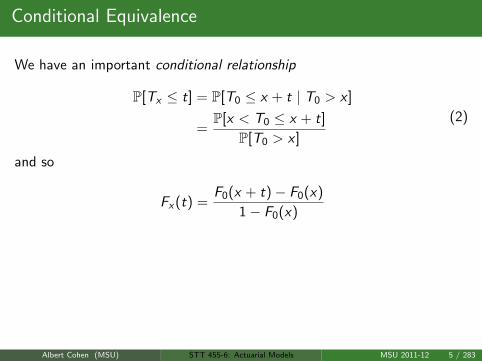

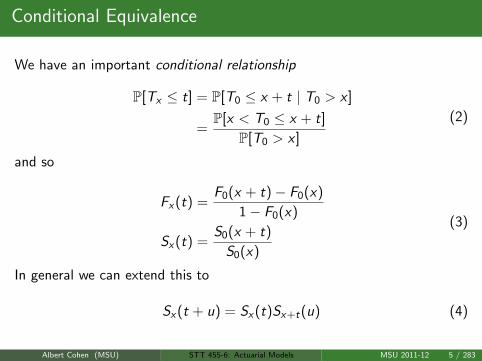

Conditional Equivalence

We have an important conditional relationship

P[Tx ≤ t] = P[T0 ≤ x + t | T0 > x ]

=P[x < T0 ≤ x + t]

P[T0 > x ]

(2)

and so

Fx(t) =F0(x + t)− F0(x)

1− F0(x)

Sx(t) =S0(x + t)

S0(x)

(3)

In general we can extend this to

Sx(t + u) = Sx(t)Sx+t(u) (4)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 5 / 283

Conditional Equivalence

We have an important conditional relationship

P[Tx ≤ t] = P[T0 ≤ x + t | T0 > x ]

=P[x < T0 ≤ x + t]

P[T0 > x ]

(2)

and so

Fx(t) =F0(x + t)− F0(x)

1− F0(x)

Sx(t) =S0(x + t)

S0(x)

(3)

In general we can extend this to

Sx(t + u) = Sx(t)Sx+t(u) (4)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 5 / 283

Conditional Equivalence

We have an important conditional relationship

P[Tx ≤ t] = P[T0 ≤ x + t | T0 > x ]

=P[x < T0 ≤ x + t]

P[T0 > x ]

(2)

and so

Fx(t) =F0(x + t)− F0(x)

1− F0(x)

Sx(t) =S0(x + t)

S0(x)

(3)

In general we can extend this to

Sx(t + u) = Sx(t)Sx+t(u) (4)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 5 / 283

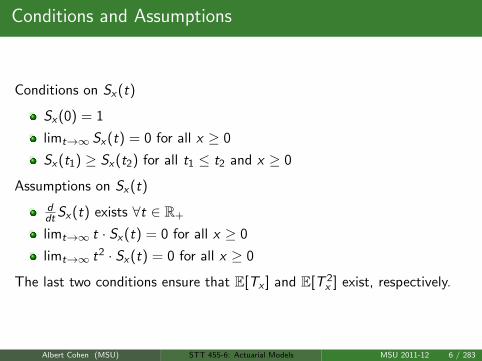

Conditions and Assumptions

Conditions on Sx(t)

Sx(0) = 1

limt→∞ Sx(t) = 0 for all x ≥ 0

Sx(t1) ≥ Sx(t2) for all t1 ≤ t2 and x ≥ 0

Assumptions on Sx(t)

ddt Sx(t) exists ∀t ∈ R+

limt→∞ t · Sx(t) = 0 for all x ≥ 0

limt→∞ t2 · Sx(t) = 0 for all x ≥ 0

The last two conditions ensure that E[Tx ] and E[T 2x ] exist, respectively.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 6 / 283

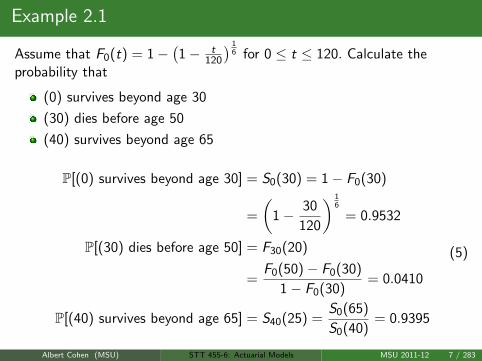

Example 2.1

Assume that F0(t) = 1−(1− t

120

) 16 for 0 ≤ t ≤ 120. Calculate the

probability that

(0) survives beyond age 30

(30) dies before age 50

(40) survives beyond age 65

P[(0) survives beyond age 30] = S0(30) = 1− F0(30)

=

(1− 30

120

) 16

= 0.9532

P[(30) dies before age 50] = F30(20)

=F0(50)− F0(30)

1− F0(30)= 0.0410

P[(40) survives beyond age 65] = S40(25) =S0(65)

S0(40)= 0.9395

(5)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 7 / 283

Example 2.1

Assume that F0(t) = 1−(1− t

120

) 16 for 0 ≤ t ≤ 120. Calculate the

probability that

(0) survives beyond age 30

(30) dies before age 50

(40) survives beyond age 65

P[(0) survives beyond age 30] = S0(30) = 1− F0(30)

=

(1− 30

120

) 16

= 0.9532

P[(30) dies before age 50] = F30(20)

=F0(50)− F0(30)

1− F0(30)= 0.0410

P[(40) survives beyond age 65] = S40(25) =S0(65)

S0(40)= 0.9395

(5)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 7 / 283

The Force of Mortality

Recall from basic probability that the density of Fx(t) is defined asfx(t) := d

dt Fx(t).

It follows that

f0(x) :=d

dxF0(x) = lim

dx→0+

F0(x + dx)− F0(x)

dx

= limdx→0+

P[x < T0 ≤ x + dx ]

dx

(6)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 8 / 283

The Force of Mortality

Recall from basic probability that the density of Fx(t) is defined asfx(t) := d

dt Fx(t).

It follows that

f0(x) :=d

dxF0(x) = lim

dx→0+

F0(x + dx)− F0(x)

dx

= limdx→0+

P[x < T0 ≤ x + dx ]

dx

(6)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 8 / 283

The Force of Mortality

However, we can find the conditional density, also known as the Force ofMortality via

µx = limdx→0+

P[x < T0 ≤ x + dx | T0 > x ]

dx

= limdx→0+

P[Tx ≤ dx ]

dx= lim

dx→0+

1− Sx(dx)

dx

= limdx→0+

1− Sx(dx)

dx

= limdx→0+

1− S0(x+dx)S0(x)

dx=

1

S0(x)lim

dx→0+

S0(x)− S0(x + dx)

dx

= − 1

S0(x)

d

dxS0(x) =

f0(x)

S0(x)

(7)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 9 / 283

The Force of Mortality

In general, we can show

µx+t = − 1

Sx(t)

d

dtSx(t) =

fx(t)

Sx(t)(8)

and integration of this relation leads to

Sx(t) =S0(x + t)

S0(x)

=e−

∫ x+t0 µsds

e−∫ x

0 µsds

= e−∫ x+tx µsds

= e−∫ t

0 µx+sds

(9)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 10 / 283

Example 2.2

Assume that F0(t) = 1−(1− t

120

) 16 for 0 ≤ t ≤ 120. Calculate µx

d

dxS0(x) =

1

6·(

1− x

120

)− 56 ·(− 1

120

)∴ µx = − 1(

1− x120

) 16

·(

1

6·(

1− x

120

)− 56 ·(− 1

120

))=

1

720− 6x

(10)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 11 / 283

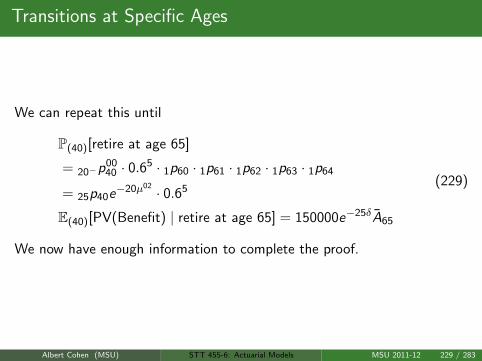

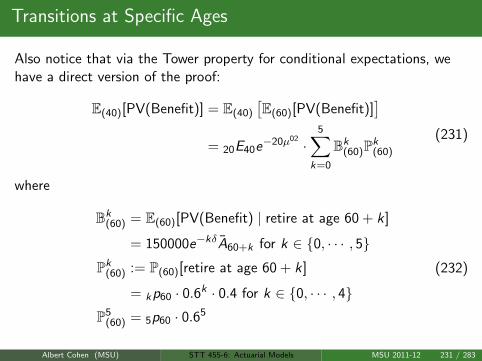

Example 2.2

Assume that F0(t) = 1−(1− t

120

) 16 for 0 ≤ t ≤ 120. Calculate µx

d

dxS0(x) =

1

6·(

1− x

120

)− 56 ·(− 1

120

)∴ µx = − 1(

1− x120

) 16

·(

1

6·(

1− x

120

)− 56 ·(− 1

120

))=

1

720− 6x

(10)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 11 / 283

Gompertz’ Law / Makehams’s Law

One model of human mortality, postulated by Gompertz, is µx = Bcx ,where (B, c) ∈ (0, 1)× (1,∞). This is based on the assumption thatmortality is age dependent, and that the growth rate for mortality isproportional to it’s own value. Makeham proposed that there should alsobe an age independent component, and so Makeham’s Law is

µx = A + Bcx (11)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 12 / 283

Gompertz’ Law / Makehams’s Law

Of course, when A = 0, this reduces back to Gompertz’ Law.

By definition,

Sx(t) = e−∫ x+tx µsds = e−

∫ x+tx (A+Bcs)ds

= e−At−B

ln ccx (ct−1)

(12)

Keep in mind that this is a multivariable function of (x , t) ∈ R2+

Some online resources:

CDC National Vital Statistics report, Dec. 2002 .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 13 / 283

Gompertz’ Law / Makehams’s Law

Of course, when A = 0, this reduces back to Gompertz’ Law.By definition,

Sx(t) = e−∫ x+tx µsds = e−

∫ x+tx (A+Bcs)ds

= e−At−B

ln ccx (ct−1)

(12)

Keep in mind that this is a multivariable function of (x , t) ∈ R2+

Some online resources:

CDC National Vital Statistics report, Dec. 2002 .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 13 / 283

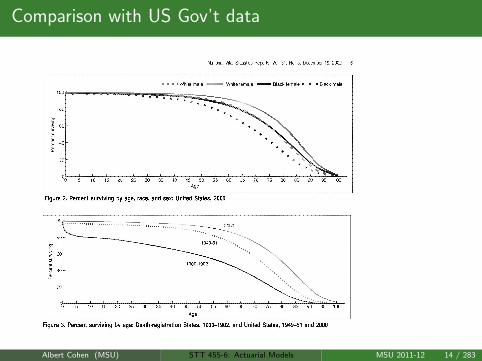

Comparison with US Gov’t data

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 14 / 283

Actuarial Notation

Actuaries make the notational conventions

tpx = P[Tx > t] = Sx(t)

tqx = P[Tx ≤ t] = Fx(t)

u|tqx = P[u < Tx ≤ u + t] = Sx(u)− Sx(u + t)

(13)

u|tqx , also known as the deferred mortality probability, is the probabilitythat (x) survives u years, and then dies in the subsequent t years.

Another convention is that px := 1px and qx := 1qx .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 15 / 283

Actuarial Notation-Relationships

Consequently,

tpx + tqx = 1

u|tqx = upx − u+tpx

t+upx = tpx · upx+t

µx =−1

xp0

d

dx(xp0)

(14)

Similarly,

µx+t =−1

tpx

d

dttpx ⇒

d

dttpx = µx+t · tpx

µx+t =fx(t)

Sx(t)⇒ fx(t) = µx+t · tpx

tpx = e−∫ t

0 µx+sds

(15)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 16 / 283

Actuarial Notation-Relationships

Also, since Fx(t) =∫ t

0 fx(s)ds, we have as a linear approximation

tqx =

∫ t

0spx · µx+sds

qx =

∫ 1

0spx · µx+sds

=

∫ 1

0e−

∫ s0 µx+vdv · µx+sds

≈∫ 1

0µx+sds

≈ µx+ 12

(16)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 17 / 283

Actuarial Notation-Relationships

Also, since Fx(t) =∫ t

0 fx(s)ds, we have as a linear approximation

tqx =

∫ t

0spx · µx+sds

qx =

∫ 1

0spx · µx+sds

=

∫ 1

0e−

∫ s0 µx+vdv · µx+sds

≈∫ 1

0µx+sds

≈ µx+ 12

(16)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 17 / 283

Mean and Standard Deviation of Tx

Actuaries make the notational definition ex := E[Tx ], also known as thecomplete expectation of life. Recall fx(t) = tpx · µx+t = − d

dt tpx , and

ex =

∫ ∞0

t · fx(t)dt

=

∫ ∞0

t · tpx · µx+tdt

=

∫ ∞0

t · − d

dttpxdt

=

∫ ∞0

tpxdt

E[T 2x ] =

∫ ∞0

t2 · fx(t)dt =

∫ ∞0

2t · tpxdt

V [Tx ] := E[T 2x ]− (ex)2

(17)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 18 / 283

Mean and Standard Deviation of Tx

Actuaries make the notational definition ex := E[Tx ], also known as thecomplete expectation of life. Recall fx(t) = tpx · µx+t = − d

dt tpx , and

ex =

∫ ∞0

t · fx(t)dt

=

∫ ∞0

t · tpx · µx+tdt

=

∫ ∞0

t · − d

dttpxdt

=

∫ ∞0

tpxdt

E[T 2x ] =

∫ ∞0

t2 · fx(t)dt =

∫ ∞0

2t · tpxdt

V [Tx ] := E[T 2x ]− (ex)2

(17)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 18 / 283

Mean and Standard Deviation of Tx

Actuaries make the notational definition ex := E[Tx ], also known as thecomplete expectation of life. Recall fx(t) = tpx · µx+t = − d

dt tpx , and

ex =

∫ ∞0

t · fx(t)dt

=

∫ ∞0

t · tpx · µx+tdt

=

∫ ∞0

t · − d

dttpxdt

=

∫ ∞0

tpxdt

E[T 2x ] =

∫ ∞0

t2 · fx(t)dt =

∫ ∞0

2t · tpxdt

V [Tx ] := E[T 2x ]− (ex)2

(17)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 18 / 283

Mean and Standard Deviation of Tx

Actuaries make the notational definition ex := E[Tx ], also known as thecomplete expectation of life. Recall fx(t) = tpx · µx+t = − d

dt tpx , and

ex =

∫ ∞0

t · fx(t)dt

=

∫ ∞0

t · tpx · µx+tdt

=

∫ ∞0

t · − d

dttpxdt

=

∫ ∞0

tpxdt

E[T 2x ] =

∫ ∞0

t2 · fx(t)dt =

∫ ∞0

2t · tpxdt

V [Tx ] := E[T 2x ]− (ex)2

(17)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 18 / 283

Example 2.6

Assume that F0(x) = 1−(1− x

120

) 16 for 0 ≤ x ≤ 120. Calculate ex ,V [Tx ]

for a.)x = 30 and b.)x = 80.

Since S0(x) =(1− x

120

) 16 , it follows that in keeping with the model where

survival is constrained to be les than 120,

tpx =S0(x + t)

S0(x)=

(

1− t120−x

) 16

: x + t ≤ 120

0 : x + t > 120

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 19 / 283

Example 2.6

Assume that F0(x) = 1−(1− x

120

) 16 for 0 ≤ x ≤ 120. Calculate ex ,V [Tx ]

for a.)x = 30 and b.)x = 80.

Since S0(x) =(1− x

120

) 16 , it follows that in keeping with the model where

survival is constrained to be les than 120,

tpx =S0(x + t)

S0(x)=

(

1− t120−x

) 16

: x + t ≤ 120

0 : x + t > 120

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 19 / 283

Example 2.6

So,

ex =

∫ 120−x

0

(1− t

120− x

) 16

dt =6

7· (120− x)

E[T 2x ] =

∫ 120−x

02t ·

(1− t

120− x

) 16

dt

=

(6

7− 6

13

)· 2(120− x)2

(18)

and

(e30, e80) = (77.143, 34.286)

(V [T30],V [T80]) =((21.396)2, (9.509)2

) (19)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 20 / 283

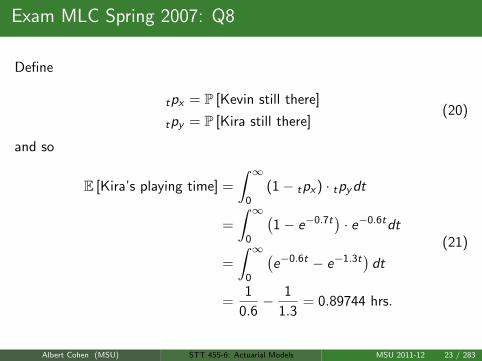

Exam MLC Spring 2007: Q8

Kevin and Kira excel at the newest video game at the local arcade,Reversion. The arcade has only one station for it. Kevin is playing. Kira isnext in line. You are given:

(i) Kevin will play until his parents call him to come home.

(ii) Kira will leave when her parents call her. She will start playing assoon as Kevin leaves if he is called first.

(iii) Each child is subject to a constant force of being called: 0.7 perhour for Kevin; 0.6 per hour for Kira.

(iv) Calls are independent.

(v) If Kira gets to play, she will score points at a rate of 100,000 perhour.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 21 / 283

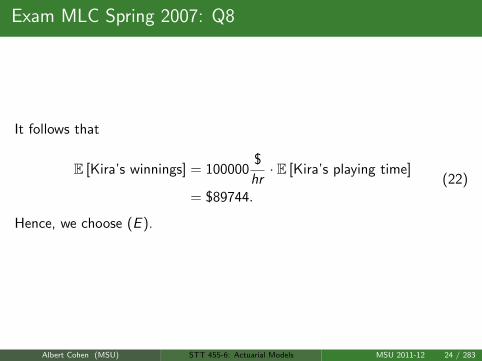

Exam MLC Spring 2007: Q8

Calculate the expected number of points Kira will score before she leaves.

(A) 77,000

(B) 80,000

(C) 84,000

(D) 87,000

(E) 90,000

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 22 / 283

Exam MLC Spring 2007: Q8

Define

tpx = P [Kevin still there]

tpy = P [Kira still there](20)

and so

E [Kira’s playing time] =

∫ ∞0

(1− tpx) · tpydt

=

∫ ∞0

(1− e−0.7t

)· e−0.6tdt

=

∫ ∞0

(e−0.6t − e−1.3t

)dt

=1

0.6− 1

1.3= 0.89744 hrs.

(21)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 23 / 283

Exam MLC Spring 2007: Q8

It follows that

E [Kira’s winnings] = 100000$

hr· E [Kira’s playing time]

= $89744.(22)

Hence, we choose (E ).

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 24 / 283

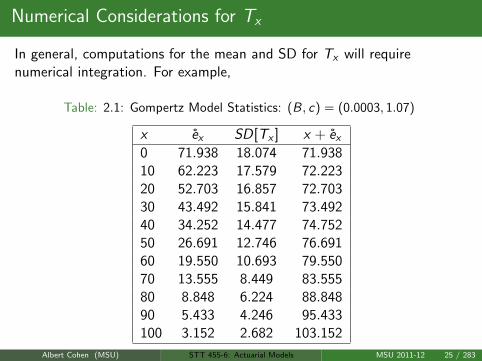

Numerical Considerations for Tx

In general, computations for the mean and SD for Tx will requirenumerical integration. For example,

Table: 2.1: Gompertz Model Statistics: (B, c) = (0.0003, 1.07)

x ex SD[Tx ] x + ex0 71.938 18.074 71.93810 62.223 17.579 72.22320 52.703 16.857 72.70330 43.492 15.841 73.49240 34.252 14.477 74.75250 26.691 12.746 76.69160 19.550 10.693 79.55070 13.555 8.449 83.55580 8.848 6.224 88.84890 5.433 4.246 95.433100 3.152 2.682 103.152

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 25 / 283

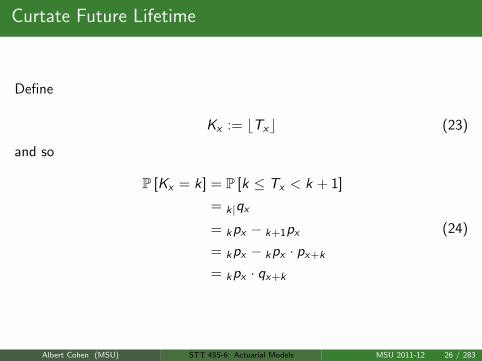

Curtate Future Lifetime

Define

Kx := bTxc (23)

and so

P [Kx = k] = P [k ≤ Tx < k + 1]

= k|qx

= kpx − k+1px

= kpx − kpx · px+k

= kpx · qx+k

(24)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 26 / 283

Curtate Future Lifetime

E [Kx ] := ex =∞∑k=0

k · P [Kx = k]

=∞∑k=0

k · (kpx − k+1px)

=∞∑k=1

kpx by telescoping series..

E[K 2x

]=∞∑k=0

k2 · P [Kx = k]

= 2 ·∞∑k=1

k · kpx −∞∑k=1

kpx

= 2 ·∞∑k=1

k · kpx − ex

(25)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 27 / 283

Curtate Future Lifetime

E [Kx ] := ex =∞∑k=0

k · P [Kx = k]

=∞∑k=0

k · (kpx − k+1px)

=∞∑k=1

kpx by telescoping series..

E[K 2x

]=∞∑k=0

k2 · P [Kx = k]

= 2 ·∞∑k=1

k · kpx −∞∑k=1

kpx

= 2 ·∞∑k=1

k · kpx − ex

(25)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 27 / 283

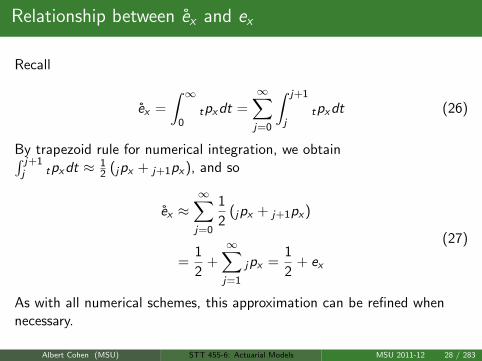

Relationship between ex and ex

Recall

ex =

∫ ∞0

tpxdt =∞∑j=0

∫ j+1

jtpxdt (26)

By trapezoid rule for numerical integration, we obtain∫ j+1j tpxdt ≈ 1

2 (jpx + j+1px), and so

ex ≈∞∑j=0

1

2(jpx + j+1px)

=1

2+∞∑j=1

jpx =1

2+ ex

(27)

As with all numerical schemes, this approximation can be refined whennecessary.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 28 / 283

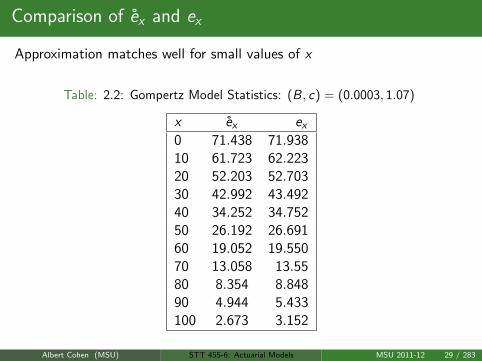

Comparison of ex and ex

Approximation matches well for small values of x

Table: 2.2: Gompertz Model Statistics: (B, c) = (0.0003, 1.07)

x ex ex0 71.438 71.93810 61.723 62.22320 52.203 52.70330 42.992 43.49240 34.252 34.75250 26.192 26.69160 19.052 19.55070 13.058 13.5580 8.354 8.84890 4.944 5.433100 2.673 3.152

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 29 / 283

Notes

An extension of Gompertz - Makeham Laws is the GM(r , s) formulaµx = h1

r (x) + eh2s (x), where h1

r (x), h2s (x) are polynomials of degree r

and s, respectively.

Hazard rate in survival analysis and failure rate in reliability theory isthe same as what actuaries call force of mortality.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 30 / 283

Homework Questions

HW: 2.1, 2.2, 2.5, 2.6, 2.10, 2.13, 2.14, 2.15

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 31 / 283

Life Tables

Define for a model with maximum age ω and initial age x0 the radix lx0 ,where

lx0+t = lx0 · tpx0 (28)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 32 / 283

Life Tables

It follows that

lx+t = lx0 · x+t−x0px0

= lx0 · x−x0px0 · tpx

= lx · tpx

tpx =lx+t

lx

(29)

We assume a binomial model where Lt is the number of survivors to agex + t.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 33 / 283

Life Tables

It follows that

lx+t = lx0 · x+t−x0px0

= lx0 · x−x0px0 · tpx

= lx · tpx

tpx =lx+t

lx

(29)

We assume a binomial model where Lt is the number of survivors to agex + t.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 33 / 283

Life Tables

So, if there are lx independent individuals aged x with probability tpx ofsurvival to age x + t, then we interpret lx+t as the expected number ofsurvivors to age x + t out of lx independent individuals aged x .Symbolically,

E[Lt | L0 = lx ] = lx+t = lx · tpx (30)

Also, define the expected number of deaths from year x to year x + 1 as

dx := lx − lx+1 = lx ·(

1− lx+1

lx

)= lx · (1− px) = lxqx (31)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 34 / 283

Life Tables

So, if there are lx independent individuals aged x with probability tpx ofsurvival to age x + t, then we interpret lx+t as the expected number ofsurvivors to age x + t out of lx independent individuals aged x .Symbolically,

E[Lt | L0 = lx ] = lx+t = lx · tpx (30)

Also, define the expected number of deaths from year x to year x + 1 as

dx := lx − lx+1 = lx ·(

1− lx+1

lx

)= lx · (1− px) = lxqx (31)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 34 / 283

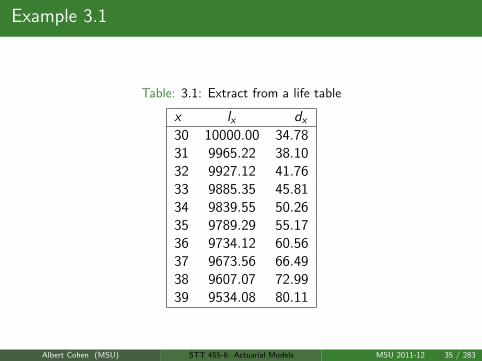

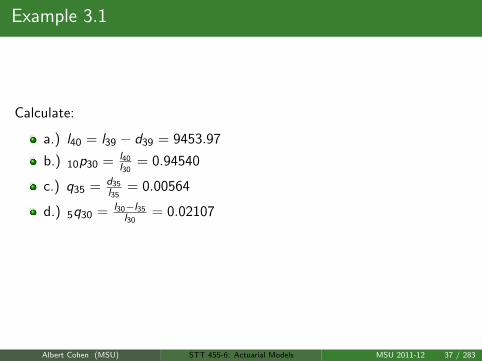

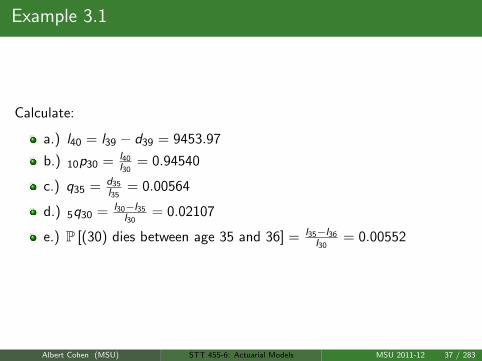

Example 3.1

Table: 3.1: Extract from a life table

x lx dx

30 10000.00 34.7831 9965.22 38.1032 9927.12 41.7633 9885.35 45.8134 9839.55 50.2635 9789.29 55.1736 9734.12 60.5637 9673.56 66.4938 9607.07 72.9939 9534.08 80.11

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 35 / 283

Example 3.1

Calculate:

a.) l40

b.) 10p30

c.) q35

d.) 5q30

e.) P [(30) dies between age 35 and 36]

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 36 / 283

Example 3.1

Calculate:

a.) l40 = l39 − d39 = 9453.97

b.) 10p30 = l40l30

= 0.94540

c.) q35 = d35l35

= 0.00564

d.) 5q30 = l30−l35l30

= 0.02107

e.) P [(30) dies between age 35 and 36] = l35−l36l30

= 0.00552

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 37 / 283

Example 3.1

Calculate:

a.) l40 = l39 − d39 = 9453.97

b.) 10p30 = l40l30

= 0.94540

c.) q35 = d35l35

= 0.00564

d.) 5q30 = l30−l35l30

= 0.02107

e.) P [(30) dies between age 35 and 36] = l35−l36l30

= 0.00552

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 37 / 283

Example 3.1

Calculate:

a.) l40 = l39 − d39 = 9453.97

b.) 10p30 = l40l30

= 0.94540

c.) q35 = d35l35

= 0.00564

d.) 5q30 = l30−l35l30

= 0.02107

e.) P [(30) dies between age 35 and 36] = l35−l36l30

= 0.00552

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 37 / 283

Example 3.1

Calculate:

a.) l40 = l39 − d39 = 9453.97

b.) 10p30 = l40l30

= 0.94540

c.) q35 = d35l35

= 0.00564

d.) 5q30 = l30−l35l30

= 0.02107

e.) P [(30) dies between age 35 and 36] = l35−l36l30

= 0.00552

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 37 / 283

Example 3.1

Calculate:

a.) l40 = l39 − d39 = 9453.97

b.) 10p30 = l40l30

= 0.94540

c.) q35 = d35l35

= 0.00564

d.) 5q30 = l30−l35l30

= 0.02107

e.) P [(30) dies between age 35 and 36] = l35−l36l30

= 0.00552

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 37 / 283

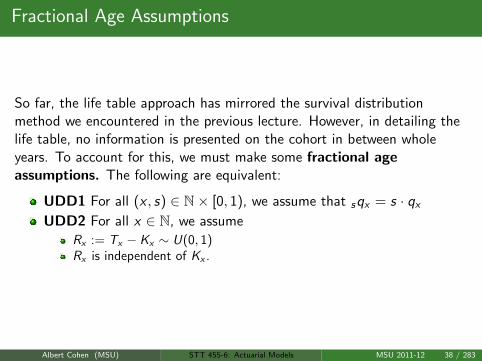

Fractional Age Assumptions

So far, the life table approach has mirrored the survival distributionmethod we encountered in the previous lecture. However, in detailing thelife table, no information is presented on the cohort in between wholeyears. To account for this, we must make some fractional ageassumptions. The following are equivalent:

UDD1 For all (x , s) ∈ N× [0, 1), we assume that sqx = s · qx

UDD2 For all x ∈ N, we assume

Rx := Tx − Kx ∼ U(0, 1)Rx is independent of Kx .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 38 / 283

Fractional Age Assumptions

So far, the life table approach has mirrored the survival distributionmethod we encountered in the previous lecture. However, in detailing thelife table, no information is presented on the cohort in between wholeyears. To account for this, we must make some fractional ageassumptions. The following are equivalent:

UDD1 For all (x , s) ∈ N× [0, 1), we assume that sqx = s · qx

UDD2 For all x ∈ N, we assume

Rx := Tx − Kx ∼ U(0, 1)Rx is independent of Kx .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 38 / 283

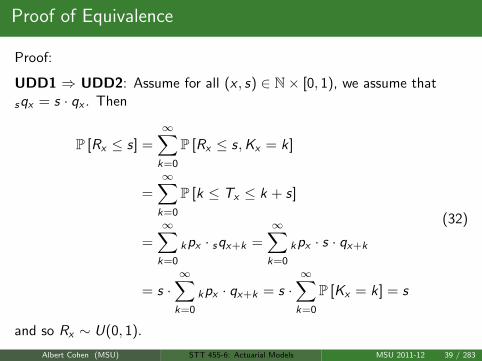

Proof of Equivalence

Proof:

UDD1 ⇒ UDD2: Assume for all (x , s) ∈ N× [0, 1), we assume that

sqx = s · qx . Then

P [Rx ≤ s] =∞∑k=0

P [Rx ≤ s,Kx = k]

=∞∑k=0

P [k ≤ Tx ≤ k + s]

=∞∑k=0

kpx · sqx+k =∞∑k=0

kpx · s · qx+k

= s ·∞∑k=0

kpx · qx+k = s ·∞∑k=0

P [Kx = k] = s

(32)

and so Rx ∼ U(0, 1).

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 39 / 283

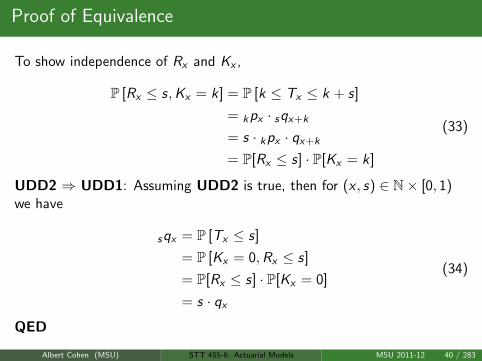

Proof of Equivalence

To show independence of Rx and Kx ,

P [Rx ≤ s,Kx = k] = P [k ≤ Tx ≤ k + s]

= kpx · sqx+k

= s · kpx · qx+k

= P[Rx ≤ s] · P[Kx = k]

(33)

UDD2 ⇒ UDD1: Assuming UDD2 is true, then for (x , s) ∈ N× [0, 1)we have

sqx = P [Tx ≤ s]

= P [Kx = 0,Rx ≤ s]

= P[Rx ≤ s] · P[Kx = 0]

= s · qx

(34)

QED

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 40 / 283

Corollary

Recall that sqx = lx−lx+s

lx. It follows now that

sqx = sqx = sdx

lx=

lx − lx+s

lx

lx+s = lx − s · dx

which is a linear decreasing function of s ∈ [0, 1)

qx =d

ds[sqx ] = fx(s) = spx · µx+s

(35)

But, since qx is constant in s, we have fx(s) is constant for s ∈ [0, 1).

Read over Examples 3.2− 3.5

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 41 / 283

Corollary

Recall that sqx = lx−lx+s

lx. It follows now that

sqx = sqx = sdx

lx=

lx − lx+s

lxlx+s = lx − s · dx

which is a linear decreasing function of s ∈ [0, 1)

qx =d

ds[sqx ] = fx(s) = spx · µx+s

(35)

But, since qx is constant in s, we have fx(s) is constant for s ∈ [0, 1).

Read over Examples 3.2− 3.5

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 41 / 283

Corollary

Recall that sqx = lx−lx+s

lx. It follows now that

sqx = sqx = sdx

lx=

lx − lx+s

lxlx+s = lx − s · dx

which is a linear decreasing function of s ∈ [0, 1)

qx =d

ds[sqx ] = fx(s) = spx · µx+s

(35)

But, since qx is constant in s, we have fx(s) is constant for s ∈ [0, 1).

Read over Examples 3.2− 3.5

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 41 / 283

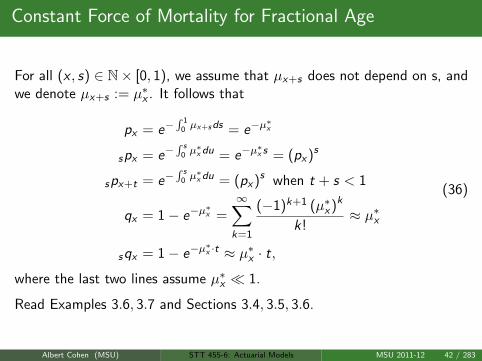

Constant Force of Mortality for Fractional Age

For all (x , s) ∈ N× [0, 1), we assume that µx+s does not depend on s, andwe denote µx+s := µ∗x . It follows that

px = e−∫ 1

0 µx+sds = e−µ∗x

spx = e−∫ s

0 µ∗x du = e−µ

∗x s = (px)s

spx+t = e−∫ s

0 µ∗x du = (px)s when t + s < 1

qx = 1− e−µ∗x =

∞∑k=1

(−1)k+1 (µ∗x)k

k!≈ µ∗x

sqx = 1− e−µ∗x ·t ≈ µ∗x · t,

(36)

where the last two lines assume µ∗x 1.

Read Examples 3.6, 3.7 and Sections 3.4, 3.5, 3.6.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 42 / 283

Homework Questions

HW: 3.1, 3.2, 3.4, 3.7, 3.8, 3.9, 3.10

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 43 / 283

Contingent Events

We have spent the previous two lectures on modeling human mortality.The need for such models in insurance pricing arises when designingcontracts that are event-contingent. Such events include reachingretirement before the end of the underlying life (x) .

However, one can also write contracts that are dependent on a life (x)being admitted to college (planning for school), and also on (x)

′s externalportfolios maintaining a minimal value over a time-interval (insuringexternal investments.)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 44 / 283

Contingent Events: General Case

Consider a probability space (Ω,F ,P) and an event A ∈ F .If we are working with a force of interest δs(ω) and the time of event Was τW , then we have under the stated probability measure P the ExpectedPresent Value of a payoff K (ω) contingent upon W

EPV = E[K (ω)e−∫ τW

0 δs(ω)ds ] (37)

Actuarial Encounters of the Third Kind !!

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 45 / 283

Some Initial Simplifying Assumptions

K (ω) = 1 for all ω ∈ Ω (a.s.)

δs(ω) = δ for all ω ∈ Ω (a.s.)

W := event that (x) dies ⇒ τW := Tx

P is obtained via historical observation and is thus a physicalmeasure. Specifically, we use tpx obtained from life tables or viamodels of human mortality

We do not assume now that a unique risk-neutral pricing measure Pexists.

Standard Ultimate Survival Model with assumes Makeham’s lawwith (A,B, c) = (0.00022, 2.7× 10−6, 1.124)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 46 / 283

Recall...

The equivalent interest rate i := eδ − 1 per year

The discount factor v := 11+i = e−δ per year

The nominal interest rate i (p) = p ·(

(1 + i)1p − 1

)compounded p

times per year

The effective rate of discount d := 1− v = i · v = 1− e−δ per year

The nominal rate of discount d (p) := p ·(

1− v1p

)compounded p

times per year

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 47 / 283

Whole Life Insurance: Continuous Case

Consider now the random variable

Z = vTx = e−δTx (38)

which represents the present value of a dollar upon death of (x). We areinterested in statistical measures of this quantity:

E[Z ] = Ax := E[e−δTx ] =

∫ ∞0

e−δt tpxµx+tdt

E[Z 2] = 2Ax := E[e−2δTx ]

=

∫ ∞0

e−2δttpxµx+tdt

Var(Z ) = 2Ax −(Ax

)2

P[Z ≤ z ] = P[

Tx ≥− ln (z)

δ

](39)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 48 / 283

Whole Life Insurance: Yearly Case

Assuming payments are made at the end of the death year, our randomvariable is now Z = vKx+1 = e−δKx−δ and so

E[Z ] = Ax := E[vKx+1] =∞∑k=0

vk+1P[Kx = k]

=∞∑k=0

vk+1k|qx

E[Z 2] =∞∑k=0

v 2k+2k|qx

Var(Z ) = 2Ax − (Ax)2

P[Z ≤ z ] = P[

Kx ≥−δ − ln (z)

δ

](40)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 49 / 283

Whole Life Insurance: 1m

thlyCase

Instead of only paying at the end of the last whole year lived, an insurancecontract might specify payment upon the end of the last period lived. Inthis case, if we split a year into m periods, and define

K(m)x =

1

mbmTxc (41)

For example, if Kx = 19.78, then

K(m)x =

19 m = 119 1

2 = 19.5 m = 219 3

4 = 19.75 m = 419 9

12 = 19.75 m = 12

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 50 / 283

Whole Life Insurance: 1m

thlyCase

It follows that we need ∀r ∈

0, 1m ,

2m , ...,

m−1m , 1, m+1

m , ...

P[K

(m)x = r

]= P

[r ≤ Tx < r +

1

m

]= r | 1

mqx (42)

to compute statistics for our random variable

Z = vK(m)x + 1

m (43)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 51 / 283

Whole Life Insurance: 1m

thlyCase

E[Z ] = A(m)x := E[vK

(m)x + 1

m ] =∞∑k=0

vk+1m k

m| 1m

qx

E[Z 2] = 2A(m)x =

∞∑k=0

v2k+2m k

m| 1m

qx

Var(Z ) = 2A(m)x −

(A

(m)x

)2

P[Z ≤ z ] = P[

K(m)x ≥ − ln (z)

δ− 1

m

](44)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 52 / 283

Recursion Method

One of the computational tools we share directly with quantitative financeis the method of backwards-pricing. In option pricing, we assume thecontract has a finite term. Here, we assume a finite lifetime maximum ofω <∞. It follows that

Aω−1 = E[vKω−1+1

]= E

[v 1]

= v (45)

At age ω − 2, we have P[Kω−2 = 0] = qω−2 and so

Aω−2 = E[vKω−2+1

]= qω−2 · v + pω−2 · E

[v (1+Kω−1)+1

]= qω−2 · v + pω−2 · v · E

[vKω−1+1

]= qω−2 · v + pω−2 · v 2

(46)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 53 / 283

Recursion Method

One of the computational tools we share directly with quantitative financeis the method of backwards-pricing. In option pricing, we assume thecontract has a finite term. Here, we assume a finite lifetime maximum ofω <∞. It follows that

Aω−1 = E[vKω−1+1

]= E

[v 1]

= v (45)

At age ω − 2, we have P[Kω−2 = 0] = qω−2 and so

Aω−2 = E[vKω−2+1

]= qω−2 · v + pω−2 · E

[v (1+Kω−1)+1

]= qω−2 · v + pω−2 · v · E

[vKω−1+1

]= qω−2 · v + pω−2 · v 2

(46)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 53 / 283

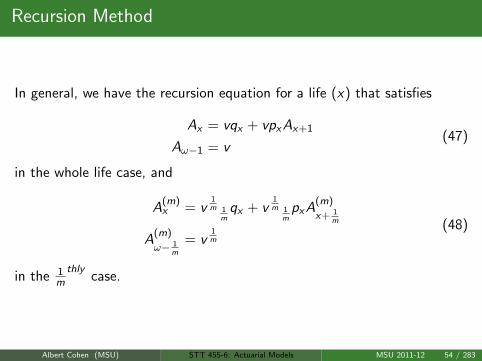

Recursion Method

In general, we have the recursion equation for a life (x) that satisfies

Ax = vqx + vpxAx+1

Aω−1 = v(47)

in the whole life case, and

A(m)x = v

1m 1

mqx + v

1m 1

mpxA

(m)

x+ 1m

A(m)

ω− 1m

= v1m

(48)

in the 1m

thlycase.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 54 / 283

Recursion Method

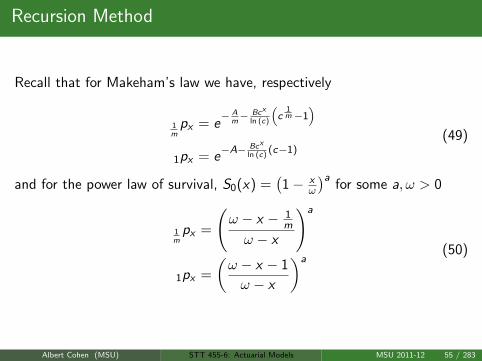

Recall that for Makeham’s law we have, respectively

1m

px = e− A

m− Bcx

ln (c)

(c

1m−1

)

1px = e−A− Bcx

ln (c)(c−1)

(49)

and for the power law of survival, S0(x) =(1− x

ω

)afor some a, ω > 0

1m

px =

(ω − x − 1

m

ω − x

)a

1px =

(ω − x − 1

ω − x

)a(50)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 55 / 283

Recursion Method

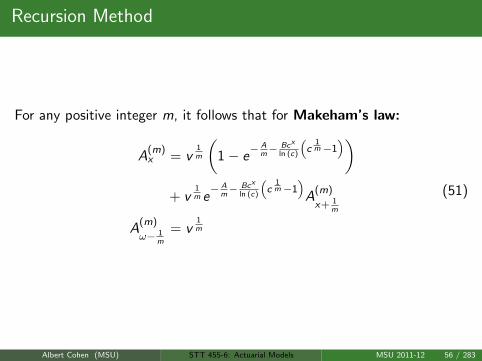

For any positive integer m, it follows that for Makeham’s law:

A(m)x = v

1m

(1− e

− Am− Bcx

ln (c)

(c

1m−1

))+ v

1m e− A

m− Bcx

ln (c)

(c

1m−1

)A

(m)

x+ 1m

A(m)

ω− 1m

= v1m

(51)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 56 / 283

Recursion Method

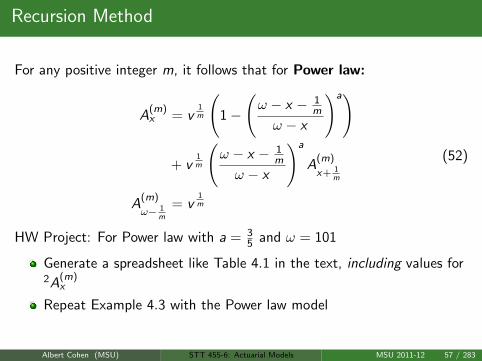

For any positive integer m, it follows that for Power law:

A(m)x = v

1m

(1−

(ω − x − 1

m

ω − x

)a)

+ v1m

(ω − x − 1

m

ω − x

)a

A(m)

x+ 1m

A(m)

ω− 1m

= v1m

(52)

HW Project: For Power law with a = 35 and ω = 101

Generate a spreadsheet like Table 4.1 in the text, including values for2A

(m)x

Repeat Example 4.3 with the Power law model

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 57 / 283

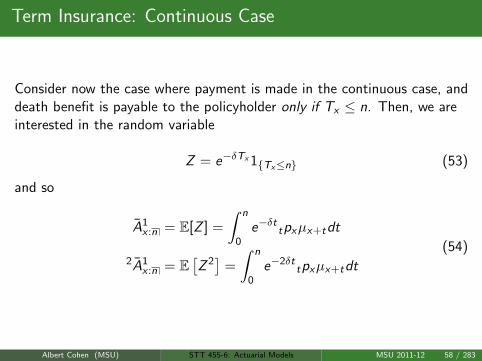

Term Insurance: Continuous Case

Consider now the case where payment is made in the continuous case, anddeath benefit is payable to the policyholder only if Tx ≤ n. Then, we areinterested in the random variable

Z = e−δTx 1Tx≤n (53)

and so

A1x :n = E[Z ] =

∫ n

0e−δt tpxµx+tdt

2A1x :n = E

[Z 2]

=

∫ n

0e−2δt

tpxµx+tdt

(54)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 58 / 283

Term Insurance: 1m

thlyCase

Consider again the case where the death benefit is payable at the end of

the 1m

thlyperiod in the death year to the policyholder only if

K(m)x + 1

m ≤ n. Then, we are interested in the random variable

Z = e−δ(K(m)x + 1

m)1

K(m)x + 1

m≤n (55)

and so

A(m)1x :n = E[Z ] =

mn−1∑k=0

vk+1m k

m| 1m

qx

2A(m)1x :n = E

[Z 2]

=mn−1∑k=0

v2k+2m k

m| 1m

qx

(56)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 59 / 283

Pure Endowment

Pure endowment benefits depend on the survival policyholder (x) until atleast age x + n. In such a contract, a fixed benefit of 1 is paid at time n.This is expressed via

Z = e−δn1Tx≥n

A 1x :n = E[Z ] = vn

npx

= e−δnnpx

(57)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 60 / 283

Endowment Insurance

Endowment insurance is a combination of term insurance and pureendowment. In such a policy, the amount is paid upon death if it occurswith a fixed term n. However, if (x) survives beyond n years, the suminsured is payable at the end of the nth year. The corresponding presentvalue random variable is

Z = e−δminTx ,n

E[Z ] = Ax :n

=

∫ n

0e−δt tpxµx+tdt + e−δnnpx

= A1x :n + A 1

x :n

(58)

This can be generalized once again to the 1m

thlycase and for E[Z 2]

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 61 / 283

Deferred Insurance Benefits

Suppose policyholder on a life (x) receives benefit 1 if u ≤ Tx < u + n.Then

Z = e−δTx 1u≤Tx<u+n

E[Z ] = u|A1x :n

=

∫ u+n

ue−δt tpxµx+tdt

=

∫ n

0e−δ(s+u)

s+upxµx+s+uds

= e−δu∫ n

0e−δsupx · spx+uµx+s+uds

= e−δuupx A 1x+u:n

= A1x :u+n − A1

x :u

(59)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 62 / 283

Relationships

By definition, we have

Ax = A1x :n + n|Ax

= A1x :n + vn

npxAx+n

(60)

What about relationship between Ax and Ax?

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 63 / 283

Relationships

By definition, we have

Ax = A1x :n + n|Ax

= A1x :n + vn

npxAx+n

(60)

What about relationship between Ax and Ax?

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 63 / 283

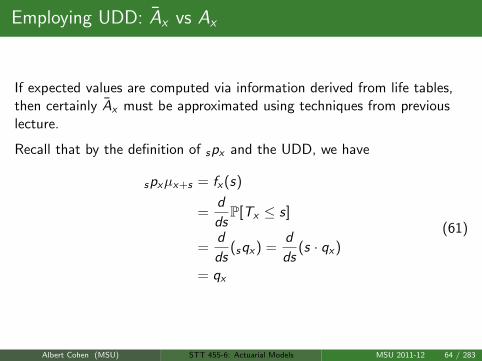

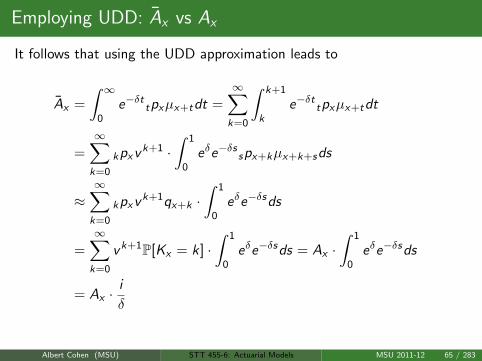

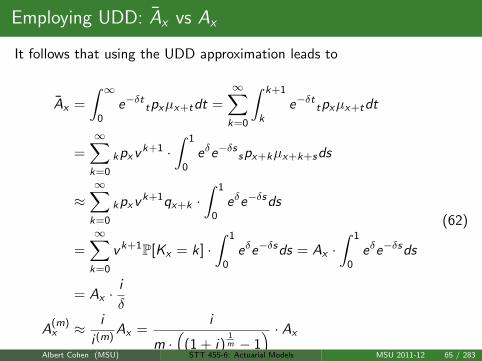

Employing UDD: Ax vs Ax

If expected values are computed via information derived from life tables,then certainly Ax must be approximated using techniques from previouslecture.

Recall that by the definition of spx and the UDD, we have

spxµx+s = fx(s)

=d

dsP[Tx ≤ s]

=d

ds(sqx) =

d

ds(s · qx)

= qx

(61)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 64 / 283

Employing UDD: Ax vs Ax

If expected values are computed via information derived from life tables,then certainly Ax must be approximated using techniques from previouslecture.

Recall that by the definition of spx and the UDD, we have

spxµx+s = fx(s)

=d

dsP[Tx ≤ s]

=d

ds(sqx) =

d

ds(s · qx)

= qx

(61)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 64 / 283

Employing UDD: Ax vs Ax

It follows that using the UDD approximation leads to

Ax =

∫ ∞0

e−δt tpxµx+tdt =∞∑k=0

∫ k+1

ke−δt tpxµx+tdt

=∞∑k=0

kpxvk+1 ·∫ 1

0eδe−δs spx+kµx+k+sds

≈∞∑k=0

kpxvk+1qx+k ·∫ 1

0eδe−δsds

=∞∑k=0

vk+1P[Kx = k] ·∫ 1

0eδe−δsds = Ax ·

∫ 1

0eδe−δsds

= Ax ·i

δ

A(m)x ≈ i

i (m)Ax =

i

m ·(

(1 + i)1m − 1

) · Ax

(62)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 65 / 283

Employing UDD: Ax vs Ax

It follows that using the UDD approximation leads to

Ax =

∫ ∞0

e−δt tpxµx+tdt =∞∑k=0

∫ k+1

ke−δt tpxµx+tdt

=∞∑k=0

kpxvk+1 ·∫ 1

0eδe−δs spx+kµx+k+sds

≈∞∑k=0

kpxvk+1qx+k ·∫ 1

0eδe−δsds

=∞∑k=0

vk+1P[Kx = k] ·∫ 1

0eδe−δsds = Ax ·

∫ 1

0eδe−δsds

= Ax ·i

δ

A(m)x ≈ i

i (m)Ax =

i

m ·(

(1 + i)1m − 1

) · Ax

(62)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 65 / 283

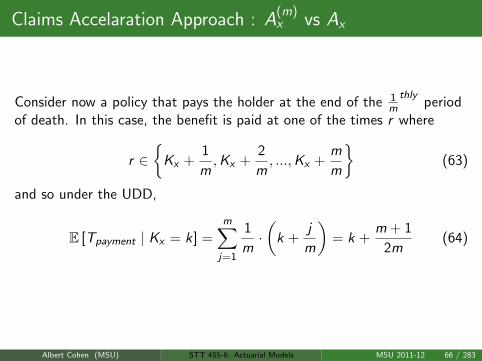

Claims Accelaration Approach : A(m)x vs Ax

Consider now a policy that pays the holder at the end of the 1m

thlyperiod

of death. In this case, the benefit is paid at one of the times r where

r ∈

Kx +1

m,Kx +

2

m, ...,Kx +

m

m

(63)

and so under the UDD,

E [Tpayment | Kx = k] =m∑j=1

1

m·(

k +j

m

)= k +

m + 1

2m(64)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 66 / 283

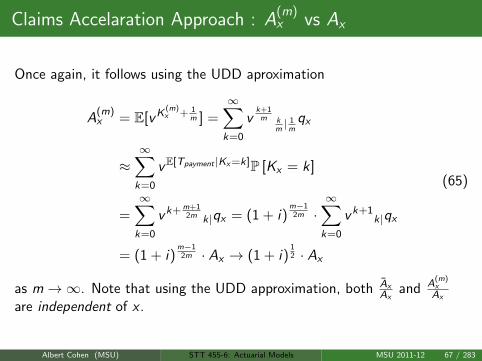

Claims Accelaration Approach : A(m)x vs Ax

Once again, it follows using the UDD aproximation

A(m)x = E[vK

(m)x + 1

m ] =∞∑k=0

vk+1m k

m| 1m

qx

≈∞∑k=0

vE[Tpayment |Kx=k]P [Kx = k]

=∞∑k=0

vk+m+12m k|qx = (1 + i)

m−12m ·

∞∑k=0

vk+1k|qx

= (1 + i)m−12m · Ax → (1 + i)

12 · Ax

(65)

as m→∞. Note that using the UDD approximation, both AxAx

and A(m)xAx

are independent of x .

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 67 / 283

Variable Insurance Benefits

Upon death, we have considered policies that pay the holder a fixedamount. What varied was the method and time of payment. If, however,the actual payoff amount depended on the time Tx of death for (x), thenwe term such a contract a Variable Insurance Contract.

Specifically, if the payoff amount dependent on Tx is h(Tx), then

Z = h(Tx)e−δTx

E[Z ] =

∫ ∞0

h(t)e−δt tpxµx+tdt(I A)x

:=

∫ ∞0

te−δt tpxµx+tdt(I A)

1x :n :=

∫ n

0te−δt tpxµx+tdt

(66)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 68 / 283

Example 4.8

Consider an n−year term insurance issued to (x) under which the deathbenefit is paid at the end of the year of death. The death benefit if deathoccurs between ages x + k and x + k + 1 is valued at (1 + j)k . Hence,using the definition i∗ := 1+i

1+j − 1,

Z = vKx+1(1 + j)Kx

E[Z ] =n−1∑k=0

vk+1(1 + j)kk|qx

=1

1 + j·n−1∑k=0

vk+1(1 + j)k+1k|qx

=1

1 + j·n−1∑k=0

k|qx(1+i1+j

)k+1=

1

1 + j· A1

x :n

(67)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 69 / 283

Homework Questions

HW: 4.1, 4.2, 4.3, 4.7, 4.9, 4.11, 4.12, 4.14, 4.15, 4.16, 4.17, 4.18

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 70 / 283

Life Annuities

A Life Annuity refers to a series of payments to or from an individual aslong as that person is still alive. For a fixed rate i and term n , we recallthe deterministic pricing theory:

an i = 1 + v + ...+ vn−1 =1− vn

d

an i = v + ...+ vn = an i − 1 + vn =1− vn

i

an i =

∫ n

0v tdt =

1− vn

δ

a(m)n i =

1

m·(

1 + v1m + ...+ vn− 1

m

)=

1− vn

d (m)

a(m)n i =

1

m·(

v1m + ...+ vn− 1

m + vn)

=1− vn

i (m)

(68)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 71 / 283

Whole Life Annuity Due

Consider the case where 1 is paid out at the beginning of every perioduntil death. Our present random variable is now

Y := aKx+1 =1− vKx+1

d(69)

and so

ax = E[Y ] = E[

1− vKx+1

d

]=

1− Ax

d(70)

V [Y ] = V

[1− vKx+1

d

]=

1

d2V [1] +

1

d2V [vKx+1]

= 0 +2Ax − A2

x

d2

(71)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 72 / 283

Whole Life Annuity Due

The present value random variable can also be represented as

Y =∞∑k=0

vk1Tx>k (72)

As P[Tx > k] = tpx , we have the alternate expression for ax

ax = E[Y ] = E

[ ∞∑k=0

vk1Tx>k

]

=∞∑k=0

E[vk1Tx>k]

=∞∑k=0

vkkpx =

∞∑k=0

k|qx ak+1

(73)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 73 / 283

Term Annuity Due

Define the present value random variable

Y =

aKx+1 : Kx ∈ 0, 1, 2, ..., n − 1an : Kx ∈ n, n + 1, n + 2, ...

Another expression is

Y = aminKx+1,n =1− v minKx+1,n

d(74)

and so

ax :n = E[Y ] =1− E

[v minKx+1,n]

d

=1− Ax :n

d

=n−1∑t=0

v ttpx =

n−1∑k=0

k|qx ak+1 + npx an

(75)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 74 / 283

Whole Life and Term Immediate Annuity

Define Y ∗ =∑∞

k=1 vk1Tx>k. Then we have an annuity immediate thatbegins payment one unit of time from now. It follows that

ax = ax − 1

V [Y ∗] = V [Y ](76)

Also, if we define Y = aminKx ,n, then

ax :n =n∑

t=1

v ttpx = ax :n − 1 + vn

npx (77)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 75 / 283

Whole Life Continuous Annuity

Define

Y = aTx=

1− vTx

δ=

∫ ∞0

e−δt1Tx>tdt

ax = E[Y ] =1− Ax

δ=

∫ ∞0

e−δt tpxdt

(78)

Note that if δ = 0, then ax = ex

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 76 / 283

Term Continuous Annuity

Define Y = aminTx ,n .

Then

Y =1− v minTx ,n

δ

ax :n = E [Y ] =1− Ax :n

δ

=

∫ n

0e−δt tpxdt

(79)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 77 / 283

Deferred Annuity

Consider now the case of an annuity for (x) that will pay 1 at the end ofeach year, beginning at age x + u and will continue until death agex + Tx . We define u|ax to be the Expected Present Value of this policy. Itshould be apparent that

u|ax = ax − ax :u

=∞∑t=u

v ttpx

= v ttpx ·

∞∑t=0

v ttpx

= v ttpx ax+u

(80)

holds in the discrete case, and similarly in the continuous case,

u|ax = ax − ax :u (81)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 78 / 283

Term Deferred Annuity

For the cases of an annuity for (x) that will pay 1 at the end of each year,beginning at age x + u and will continue until death age x + Tx up to a

term of length n, or annuity-due payable 1m

thly. Then

u|ax :n = vuupxax+u:n

u|a(m)x = vu

upx a(m)x+u

(82)

respectively.These combine with the previous slide to reveal the useful formulae:

ax :n = ax − vnnpx ax+n

a(m)x :n = a

(m)x − vn

npx a(m)x+n

(83)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 79 / 283

Guaranteed Annuities

There are instances where an age (x) wishes to buy a policy wherepayments are guaranteed to continue upon death to a beneficiary. In thiscase, define the present random variable as Y = an + Y1, where

Y1 =

0 : Kx ∈ 0, 1, 2, ..., n − 1aKx+1 − an : Kx ∈ n, n + 1, n + 2, ...

and so

E[Y1] = E[(

aKx+1 − an)

1Kx≥n

]= n|ax = vn

npx ax+n

E[Y ] := ax :n = an + vnnpx ax+n

and E[Y (m)] := a(m)

x :n= a

(m)n + vn

npx a(m)x+n

(84)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 80 / 283

Guaranteed Annuities

There are instances where an age (x) wishes to buy a policy wherepayments are guaranteed to continue upon death to a beneficiary. In thiscase, define the present random variable as Y = an + Y1, where

Y1 =

0 : Kx ∈ 0, 1, 2, ..., n − 1aKx+1 − an : Kx ∈ n, n + 1, n + 2, ...

and so

E[Y1] = E[(

aKx+1 − an)

1Kx≥n

]= n|ax = vn

npx ax+n

E[Y ] := ax :n = an + vnnpx ax+n

and E[Y (m)] := a(m)

x :n= a

(m)n + vn

npx a(m)x+n

(84)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 80 / 283

Example 5.4

A pension plan member is entitled to a benefit of 1000 per month, inadvance, for life from age 65, with no guarantee. She can opt to take alower benefit with a 10−year guarantee. The revised benefit is calculatedto have equal EPV at age 65 to the original benefit. Calculate the revisedbenefit using the Standard Ultimate Survival Model, with interest at 5%per year.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 81 / 283

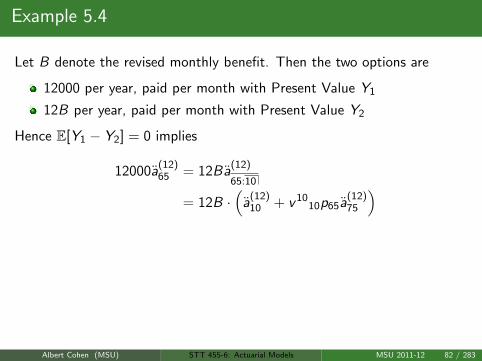

Example 5.4

Let B denote the revised monthly benefit. Then the two options are

12000 per year, paid per month with Present Value Y1

12B per year, paid per month with Present Value Y2

Hence E[Y1 − Y2] = 0 implies

12000a(12)65 = 12Ba

(12)

65:10

= 12B ·(

a(12)10 + v 10

10p65a(12)75

)

∴ B = 1000 ·a

(12)65

a(12)10 + v 10

10p65a(12)75

= 1000 · 13.0870

13.3791= 978.17

V [Y1 − Y2] = 0?

(85)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 82 / 283

Example 5.4

Let B denote the revised monthly benefit. Then the two options are

12000 per year, paid per month with Present Value Y1

12B per year, paid per month with Present Value Y2

Hence E[Y1 − Y2] = 0 implies

12000a(12)65 = 12Ba

(12)

65:10

= 12B ·(

a(12)10 + v 10

10p65a(12)75

)∴ B = 1000 ·

a(12)65

a(12)10 + v 10

10p65a(12)75

= 1000 · 13.0870

13.3791= 978.17

V [Y1 − Y2] = 0?

(85)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 82 / 283

Example 5.4

Let B denote the revised monthly benefit. Then the two options are

12000 per year, paid per month with Present Value Y1

12B per year, paid per month with Present Value Y2

Hence E[Y1 − Y2] = 0 implies

12000a(12)65 = 12Ba

(12)

65:10

= 12B ·(

a(12)10 + v 10

10p65a(12)75

)∴ B = 1000 ·

a(12)65

a(12)10 + v 10

10p65a(12)75

= 1000 · 13.0870

13.3791= 978.17

V [Y1 − Y2] = 0?

(85)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 82 / 283

Linearly Increasing Annuities

Define an annuity where the payments increase linearly at timest = 0, 1, 2, .. provided that (x) is alive at time t

(I a)x =∞∑t=0

(t + 1) · v ttpx

(I a)x :n =n−1∑t=0

(t + 1) · v ttpx

(86)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 83 / 283

Linearly Increasing Annuities

If then the annuity is payable continuously, with payments increasing by 1at each year end and the rate of payment in the tth year constant andequal to t for t ∈ 1, 2, ..m, .., n,then h(t) = m1m≤t<m+1, and the EPV is

(I a)x :n =n−1∑m=0

(m + 1)m|ax :1 (87)

If h(t) = t, then

(I a)x :n =

∫ n

0te−δt tpxdt (88)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 84 / 283

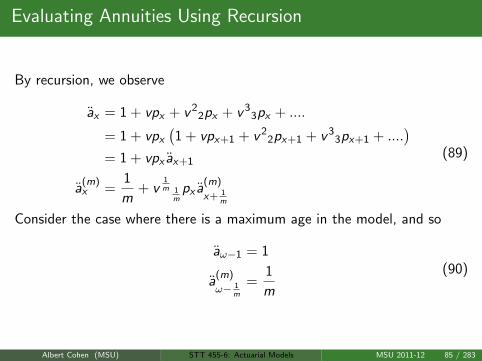

Evaluating Annuities Using Recursion

By recursion, we observe

ax = 1 + vpx + v 22px + v 3

3px + ....

= 1 + vpx

(1 + vpx+1 + v 2

2px+1 + v 33px+1 + ....

)= 1 + vpx ax+1

a(m)x =

1

m+ v

1m 1

mpx a

(m)

x+ 1m

(89)

Consider the case where there is a maximum age in the model, and so

aω−1 = 1

a(m)

ω− 1m

=1

m

(90)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 85 / 283

Evaluating Annuities Using Recursion

By recursion, we observe

ax = 1 + vpx + v 22px + v 3

3px + ....

= 1 + vpx

(1 + vpx+1 + v 2

2px+1 + v 33px+1 + ....

)= 1 + vpx ax+1

a(m)x =

1

m+ v

1m 1

mpx a

(m)

x+ 1m

(89)

Consider the case where there is a maximum age in the model, and so

aω−1 = 1

a(m)

ω− 1m

=1

m

(90)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 85 / 283

Evaluating Annuities Using Recursion

By recursion, we observe

ax = 1 + vpx + v 22px + v 3

3px + ....

= 1 + vpx

(1 + vpx+1 + v 2

2px+1 + v 33px+1 + ....

)= 1 + vpx ax+1

a(m)x =

1

m+ v

1m 1

mpx a

(m)

x+ 1m

(89)

Consider the case where there is a maximum age in the model, and so

aω−1 = 1

a(m)

ω− 1m

=1

m

(90)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 85 / 283

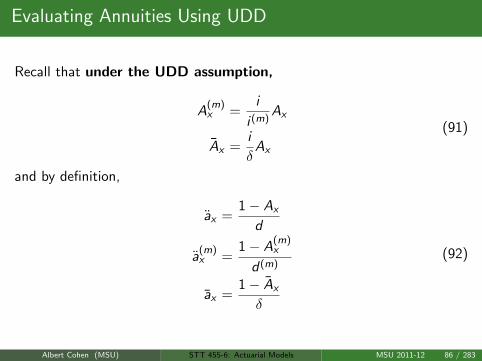

Evaluating Annuities Using UDD

Recall that under the UDD assumption,

A(m)x =

i

i (m)Ax

Ax =i

δAx

(91)

and by definition,

ax =1− Ax

d

a(m)x =

1− A(m)x

d (m)

ax =1− Ax

δ

(92)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 86 / 283

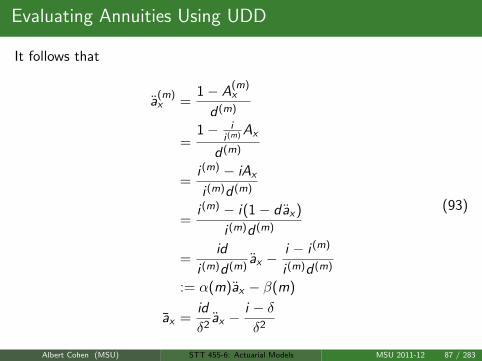

Evaluating Annuities Using UDD

It follows that

a(m)x =

1− A(m)x

d (m)

=1− i

i (m) Ax

d (m)

=i (m) − iAx

i (m)d (m)

=i (m) − i(1− dax)

i (m)d (m)

=id

i (m)d (m)ax −

i − i (m)

i (m)d (m)

:= α(m)ax − β(m)

ax =id

δ2ax −

i − δδ2

(93)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 87 / 283

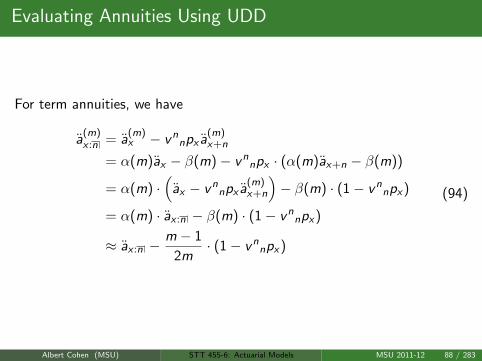

Evaluating Annuities Using UDD

For term annuities, we have

a(m)x :n = a

(m)x − vn

npx a(m)x+n

= α(m)ax − β(m)− vnnpx · (α(m)ax+n − β(m))

= α(m) ·(

ax − vnnpx a

(m)x+n

)− β(m) · (1− vn

npx)

= α(m) · ax :n − β(m) · (1− vnnpx)

≈ ax :n −m − 1

2m· (1− vn

npx)

(94)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 88 / 283

Woolhouse’s Formula

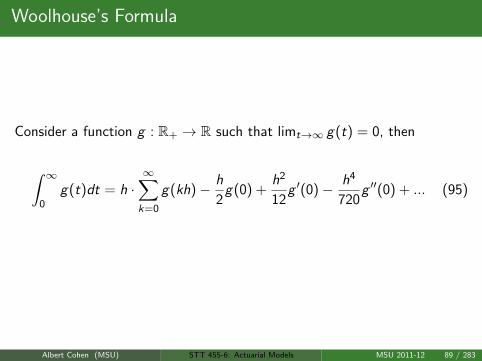

Consider a function g : R+ → R such that limt→∞ g(t) = 0, then

∫ ∞0

g(t)dt = h ·∞∑k=0

g(kh)− h

2g(0) +

h2

12g ′(0)− h4

720g ′′(0) + ... (95)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 89 / 283

Woolhouse’s Formula

Define

g(t) = v ttpx

∴ g ′(t) = −tpxδe−δt − v ttpxµx+t

∴ g ′(0) = −δ − µx

(96)

and so for h = 1,

ax ≈∞∑k=0

g(k)− 1

2+

1

12g ′(0)

=∞∑k=0

vkkpx −

1

2− 1

12(δ + µx)

= ax −1

2− 1

12(δ + µx)

(97)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 90 / 283

Woolhouse’s Formula

Correspondingly, for h = 1m ,

ax ≈1

m

∞∑k=0

g

(k

m

)− 1

2m+

1

12m2g ′(0)

=∞∑k=0

vkm k

mpx −

1

2m− 1

12m2(δ + µx)

= a(m)x − 1

2m− 1

12m2(δ + µx)

(98)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 91 / 283

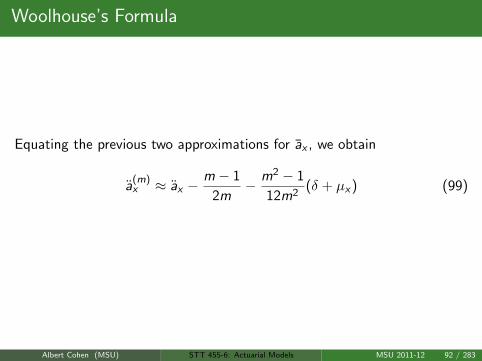

Woolhouse’s Formula

Equating the previous two approximations for ax , we obtain

a(m)x ≈ ax −

m − 1

2m− m2 − 1

12m2(δ + µx) (99)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 92 / 283

Woolhouse’s Formula

For term annuities, we obtain the approximation

a(m)x :n ≈ ax :n −

m − 1

2m(1−vn

npx)−m2 − 1

12m2(δ+µx−vn

npx(δ+µx+n)) (100)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 93 / 283

Woolhouse’s Formula

Letting m→∞, we get

ax ≈ ax −1

2− 1

12(δ + µx)

ax :n ≈ ax :n −1

2(1− vn

npx)− 1

12(δ + µx − vn

npx(δ + µx+n))

(101)

For ax with δ = 0, the approximation above reduces further to

ex ≈ (ex + 1)− 1

2− 1

12µx (102)

NB: For life tables, we can compute these quantities using theapproximation µx ≈ −1

2 [ln (px) + ln (px+1)]

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 94 / 283

Select and Ultimate Survival Models

Notation:

Aggregate Survival Models: Models for a large population, where

tpx depends only on the current age x .

Select (and Ultimate) Survival Models: Models for a select groupof individuals that depend on the current age x and

Future survival probabilities for an individual in the group depend onthe individual’s current age and on the age at which the individualjoined the group∃d > 0 such that if an individual joined the group more than d yearsago, future survival probabilities depend only on current age. So, afterd years, the person is considered to be back in the aggregatepopulation.

Ultimately, a select survival model includes another event upon whichprobabilities are conditional on.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 95 / 283

Select and Ultimate Survival Models

Notation:

d is the select period

The mortality applicable to lives after the select period is over isknown as the ultimate mortality.

A select group should have a different mortality rate, as they have beenoffered (selected for) life insurance. A question, of course, is the effect onmortality by maintaining proper health insurance.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 96 / 283

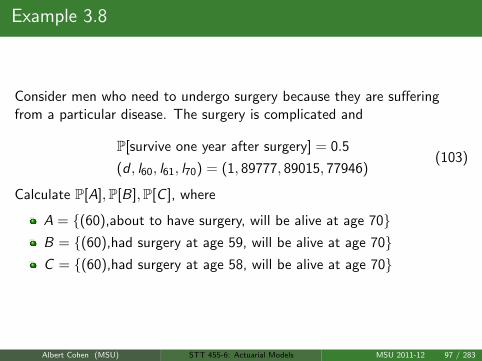

Example 3.8

Consider men who need to undergo surgery because they are sufferingfrom a particular disease. The surgery is complicated and

P[survive one year after surgery] = 0.5

(d , l60, l61, l70) = (1, 89777, 89015, 77946)(103)

Calculate P[A],P[B],P[C ], where

A = (60),about to have surgery, will be alive at age 70B = (60),had surgery at age 59, will be alive at age 70C = (60),had surgery at age 58, will be alive at age 70

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 97 / 283

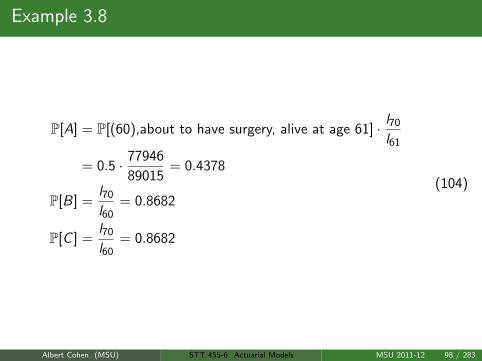

Example 3.8

P[A] = P[(60),about to have surgery, alive at age 61] · l70

l61

= 0.5 · 77946

89015= 0.4378

P[B] =l70

l60= 0.8682

P[C ] =l70

l60= 0.8682

(104)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 98 / 283

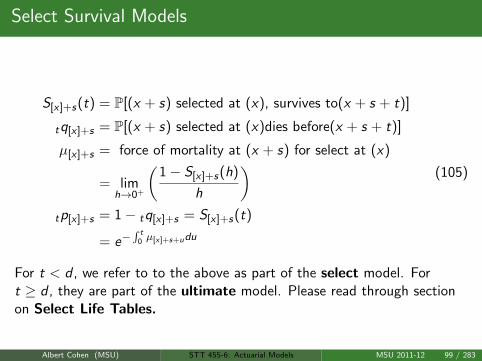

Select Survival Models

S[x]+s(t) = P[(x + s) selected at (x), survives to(x + s + t)]

tq[x]+s = P[(x + s) selected at (x)dies before(x + s + t)]

µ[x]+s = force of mortality at (x + s) for select at (x)

= limh→0+

(1− S[x]+s(h)

h

)tp[x]+s = 1− tq[x]+s = S[x]+s(t)

= e−∫ t

0 µ[x]+s+udu

(105)

For t < d , we refer to to the above as part of the select model. Fort ≥ d , they are part of the ultimate model. Please read through sectionon Select Life Tables.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 99 / 283

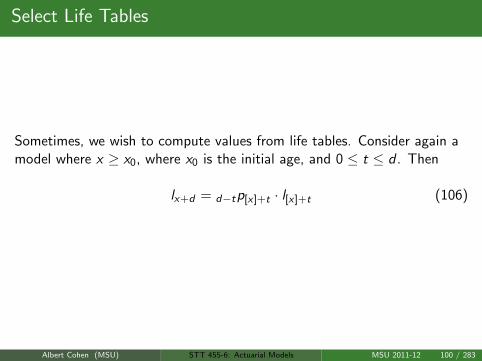

Select Life Tables

Sometimes, we wish to compute values from life tables. Consider again amodel where x ≥ x0, where x0 is the initial age, and 0 ≤ t ≤ d . Then

lx+d = d−tp[x]+t · l[x]+t (106)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 100 / 283

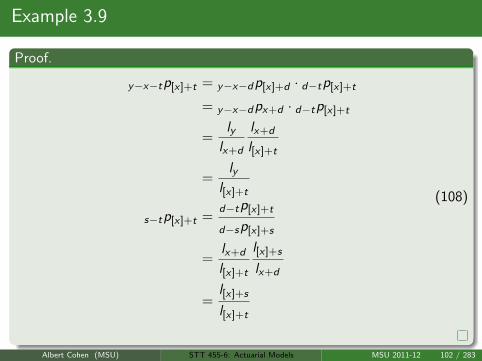

Example 3.9

Theorem

Consider y ≥ x + d > x + s > x + t ≥ x ≥ x0. Then

y−x−tp[x]+t =ly

l[x]+t

s−tp[x]+t =l[x]+s

l[x]+t

(107)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 101 / 283

Example 3.9

Proof.

y−x−tp[x]+t = y−x−dp[x]+d · d−tp[x]+t

= y−x−dpx+d · d−tp[x]+t

=ly

lx+d

lx+d

l[x]+t

=ly

l[x]+t

s−tp[x]+t =d−tp[x]+t

d−sp[x]+s

=lx+d

l[x]+t

l[x]+s

lx+d

=l[x]+s

l[x]+t

(108)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 102 / 283

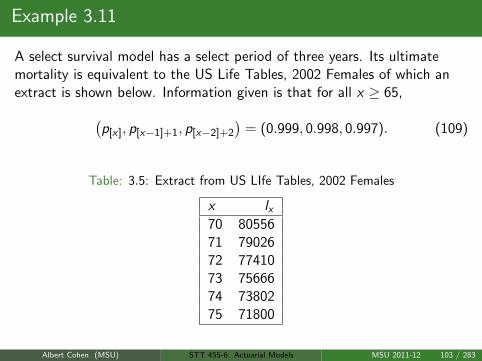

Example 3.11

A select survival model has a select period of three years. Its ultimatemortality is equivalent to the US Life Tables, 2002 Females of which anextract is shown below. Information given is that for all x ≥ 65,(

p[x], p[x−1]+1, p[x−2]+2

)= (0.999, 0.998, 0.997). (109)

Table: 3.5: Extract from US LIfe Tables, 2002 Females

x lx70 8055671 7902672 7741073 7566674 7380275 71800

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 103 / 283

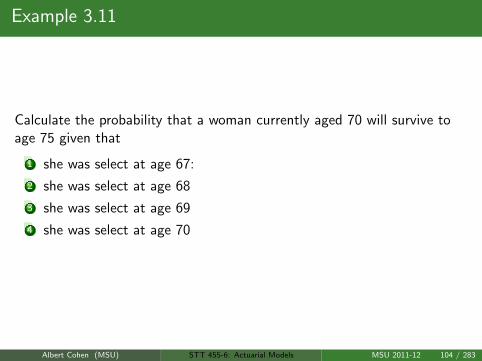

Example 3.11

Calculate the probability that a woman currently aged 70 will survive toage 75 given that

1 she was select at age 67:

2 she was select at age 68

3 she was select at age 69

4 she was select at age 70

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 104 / 283

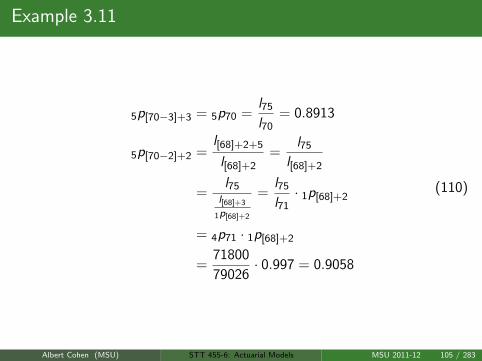

Example 3.11

5p[70−3]+3 = 5p70 =l75

l70= 0.8913

5p[70−2]+2 =l[68]+2+5

l[68]+2=

l75

l[68]+2

=l75

l[68]+3

1p[68]+2

=l75

l71· 1p[68]+2

= 4p71 · 1p[68]+2

=71800

79026· 0.997 = 0.9058

(110)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 105 / 283

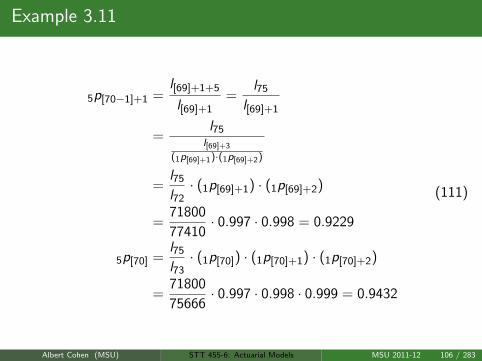

Example 3.11

5p[70−1]+1 =l[69]+1+5

l[69]+1=

l75

l[69]+1

=l75

l[69]+3

(1p[69]+1)·(1p[69]+2)

=l75

l72· (1p[69]+1) · (1p[69]+2)

=71800

77410· 0.997 · 0.998 = 0.9229

5p[70] =l75

l73· (1p[70]) · (1p[70]+1) · (1p[70]+2)

=71800

75666· 0.997 · 0.998 · 0.999 = 0.9432

(111)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 106 / 283

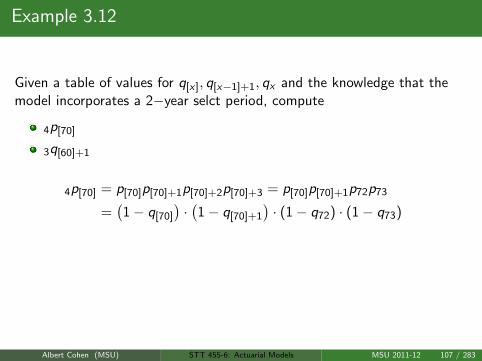

Example 3.12

Given a table of values for q[x], q[x−1]+1, qx and the knowledge that themodel incorporates a 2−year selct period, compute

4p[70]

3q[60]+1

4p[70] = p[70]p[70]+1p[70]+2p[70]+3 = p[70]p[70]+1p72p73

=(1− q[70]

)·(1− q[70]+1

)· (1− q72) · (1− q73)

3q[60]+1 = q[60]+1 + p[60]+1q62 + p[60]+1p62q63

= q[60]+1 +(1− q[60]+1

)· q62

+(1− q[60]+1

)· (1− q62) · q63

(112)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 107 / 283

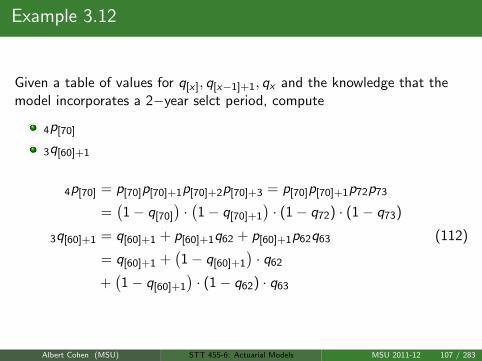

Example 3.12

Given a table of values for q[x], q[x−1]+1, qx and the knowledge that themodel incorporates a 2−year selct period, compute

4p[70]

3q[60]+1

4p[70] = p[70]p[70]+1p[70]+2p[70]+3 = p[70]p[70]+1p72p73

=(1− q[70]

)·(1− q[70]+1

)· (1− q72) · (1− q73)

3q[60]+1 = q[60]+1 + p[60]+1q62 + p[60]+1p62q63

= q[60]+1 +(1− q[60]+1

)· q62

+(1− q[60]+1

)· (1− q62) · q63

(112)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 107 / 283

Example 3.12

Given a table of values for q[x], q[x−1]+1, qx and the knowledge that themodel incorporates a 2−year selct period, compute

4p[70]

3q[60]+1

4p[70] = p[70]p[70]+1p[70]+2p[70]+3 = p[70]p[70]+1p72p73

=(1− q[70]

)·(1− q[70]+1

)· (1− q72) · (1− q73)

3q[60]+1 = q[60]+1 + p[60]+1q62 + p[60]+1p62q63

= q[60]+1 +(1− q[60]+1

)· q62

+(1− q[60]+1

)· (1− q62) · q63

(112)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 107 / 283

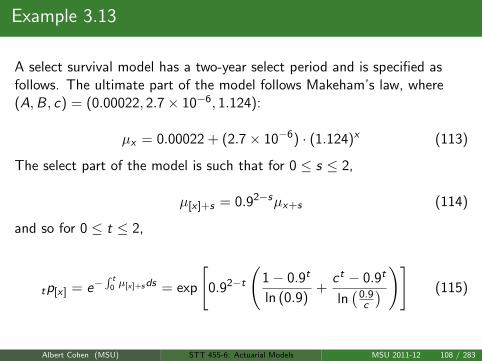

Example 3.13

A select survival model has a two-year select period and is specified asfollows. The ultimate part of the model follows Makeham’s law, where(A,B, c) = (0.00022, 2.7× 10−6, 1.124):

µx = 0.00022 + (2.7× 10−6) · (1.124)x (113)

The select part of the model is such that for 0 ≤ s ≤ 2,

µ[x]+s = 0.92−sµx+s (114)

and so for 0 ≤ t ≤ 2,

tp[x] = e−∫ t

0 µ[x]+sds = exp

[0.92−t

(1− 0.9t

ln (0.9)+

ct − 0.9t

ln(

0.9c

) )] (115)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 108 / 283

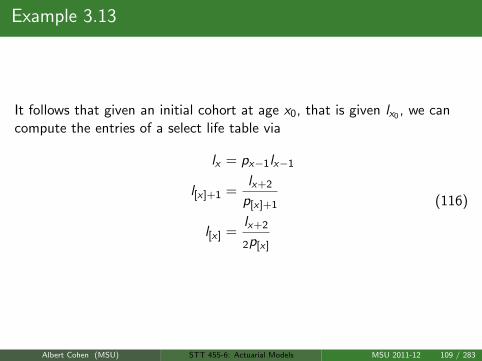

Example 3.13

It follows that given an initial cohort at age x0, that is given lx0 , we cancompute the entries of a select life table via

lx = px−1lx−1

l[x]+1 =lx+2

p[x]+1

l[x] =lx+2

2p[x]

(116)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 109 / 283

Homework Questions

HW: 3.1, 3.2, 3.4, 3.7, 3.8, 3.9, 3.10, 5.1, 5.3, 5.5, 5.6, 5.11, 5.14

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 110 / 283

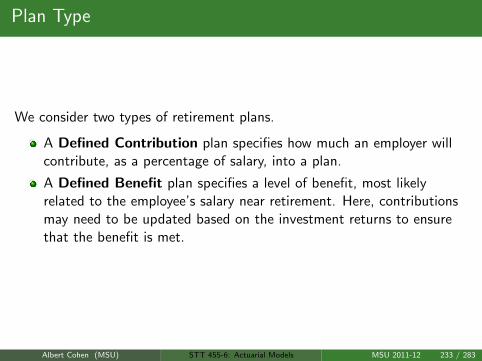

What is a Premium?

When entering into a contract, the financial obligations of all parties mustbe specified. In an insurance contract, the insurance company agrees topay the policyholder benefits in return for premium payments. Thepremiums secure the benefits as well as pay the company for expensesattached to the administation of the policy

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 111 / 283

Premium Types

A Net Premium does not explicitly allow for company’s expenses, while aOffice or Gross Premium does. There may be a Single Premium or or aseries of payments that could even match with the policyholder’s salaryfreequency.

It is important to note that premiums are paid as soon as the contract issigned, otherwise the policyholder would attain coverage before paying forit with the first premium. This could be seen as an arbitrage opportunity -non-zero probability of gain with no money up front.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 112 / 283

Premium Types

Premiums cease upon death of the policyholder. The premium payingterm is the maximum length of time that premiums are required.Certainly, premium term can be fixed so that upon retirement, say, nomore payments are required.

Also, the benefits can be secured in the future (deferred) by a singlepremium payment up front. For example, pay now to secure annuitypayments upon retirement until death.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 113 / 283

Assumptions

Recall the life model used in Example 3.13 : The select survival model hasa two-year select period and is specified as follows. The ultimate part ofthe model follows Makeham’s law, where(A,B, c) = (0.00022, 2.7× 10−6, 1.124):

µx = 0.00022 + (2.7× 10−6) · (1.124)x (117)

The select part of the model is such that for 0 ≤ s ≤ 2,

µ[x]+s = 0.92−sµx+s (118)

and so for 0 ≤ t ≤ 2,

tp[x] = e−∫ t

0 µ[x]+sds = exp

[0.92−t

(1− 0.9t

ln (0.9)+

ct − 0.9t

ln(

0.9c

) )] (119)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 114 / 283

Assumptions

Furthermore, we can extend the recursion principle when using a select lifemodel to obtain

ax = 1 + vpx ax+1

a[x]+1 = 1 + vp[x]+1ax+2

a[x] = 1 + vp[x]a[x]

(120)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 115 / 283

Basic Model

In general, an insurance company can expect to have a total benefit paidout, along with expense loading and other related costs. We represent thistotal benefit as Z . Similarly, to fund Z , the company can expect thepolicyholder to make a single payment, or stream of payments, that haspresent value P · Y . Here, P represents the level premium P and Yrepresents the present value associated to a unit payment or paymentstream.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 116 / 283

Future Loss Random Variable

For life contingent contracts, there is an outflow and inflow of moneyduring the term of the agreement. The premium income is certain, butsince the benefits are life contingent, the term and total income may notbe certain up front. To account for this, we define the Net Future LossLn

0 (which includes expenses) and the Gross Future Loss Lg0 (which does

not includes expenses) as

Ln0 = PV [benefit outgo]− PV [net premium income]

Lg0 = PV [benefit outgo] + PV [expenses]

− PV [gross premium income]

(121)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 117 / 283

Example 6.2

An insurer issues a whole life insurance to [60], with sum insured Spayable immediately upon death. Premiums are payable annually inadvance, ceasing at 80 or on earlier death. The net annual premium is P.What is the net future loss random variable Ln

0 for this contract in terms oflifetime random variables for [60]?

Ln0 = SvT[60] − Pa

minK[60]+1,20 (122)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 118 / 283

Example 6.2

An insurer issues a whole life insurance to [60], with sum insured Spayable immediately upon death. Premiums are payable annually inadvance, ceasing at 80 or on earlier death. The net annual premium is P.What is the net future loss random variable Ln

0 for this contract in terms oflifetime random variables for [60]?

Ln0 = SvT[60] − Pa

minK[60]+1,20 (122)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 118 / 283

Equivalence Principle

Absent a risk-neutral type pricing measure, insurers price theseevent-contingent contracts by setting the average value of the loss to bezero. Symbolically, this is simply (for net premiums) find P such that

E [Ln0] = 0 (123)

Note that this value P does not necessarily set Var [Ln0] = 0

Returning to our general set-up, we see that the equivalence pricingprinciple can be summarized as

P =E[Z ]

E[Y ](124)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 119 / 283

Equivalence Principle

As an introductory example, consider λ > 0 and a contract where (underno selection)

Z = vTx

Y = aTx

tpx = e−λt(125)

Hence, we have a unit whole-life insurance payable immediately upon deathof (x), where mortality is modeled to be exponential with parameter λ.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 120 / 283

Equivalence Principle

As an introductory example, consider λ > 0 and a contract where (underno selection)

Z = vTx

Y = aTx

tpx = e−λt(125)

Hence, we have a unit whole-life insurance payable immediately upon deathof (x), where mortality is modeled to be exponential with parameter λ.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 120 / 283

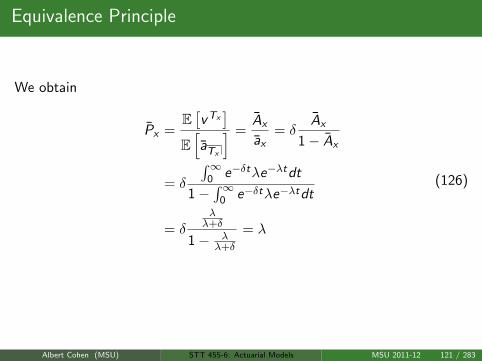

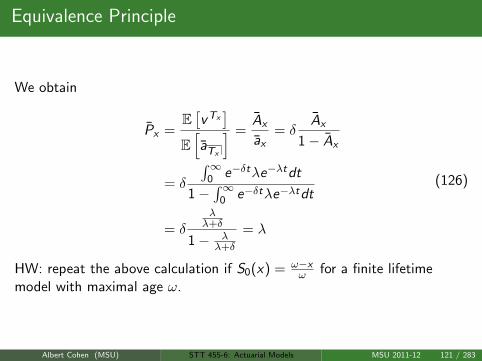

Equivalence Principle

We obtain

Px =E[vTx]

E[aTx

] =Ax

ax= δ

Ax

1− Ax

= δ

∫∞0 e−δtλe−λtdt

1−∫∞

0 e−δtλe−λtdt

= δλλ+δ

1− λλ+δ

= λ

(126)

HW: repeat the above calculation if S0(x) = ω−xω for a finite lifetime

model with maximal age ω.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 121 / 283

Equivalence Principle

We obtain

Px =E[vTx]

E[aTx

] =Ax

ax= δ

Ax

1− Ax

= δ

∫∞0 e−δtλe−λtdt

1−∫∞

0 e−δtλe−λtdt

= δλλ+δ

1− λλ+δ

= λ

(126)

HW: repeat the above calculation if S0(x) = ω−xω for a finite lifetime

model with maximal age ω.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 121 / 283

Equivalence Principle

If we repeat the previous example, but now for the case of of a unitwhole-life insurance contract with level annual premium payment andbenefit paid at the end of the death year, then

Z = vKx+1

Y = aKx+1

tpx = e−λt(127)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 122 / 283

Equivalence Principle

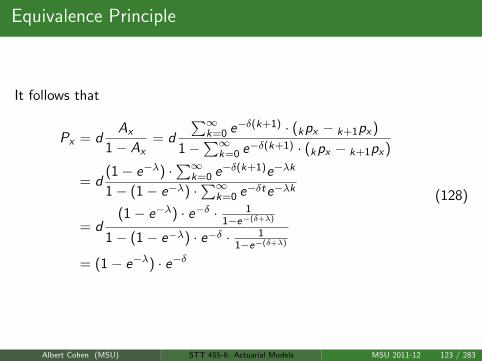

It follows that

Px = dAx

1− Ax= d

∑∞k=0 e−δ(k+1) · (kpx − k+1px)

1−∑∞

k=0 e−δ(k+1) · (kpx − k+1px)

= d(1− e−λ) ·

∑∞k=0 e−δ(k+1)e−λk

1− (1− e−λ) ·∑∞

k=0 e−δte−λk

= d(1− e−λ) · e−δ · 1

1−e−(δ+λ)

1− (1− e−λ) · e−δ · 11−e−(δ+λ)

= (1− e−λ) · e−δ

(128)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 123 / 283

Example 6.5

Consider an endowment insurance with sum insured 100000 issued to aselect life aged [45] with term 20 years under which the death benefit ispayable at the end of of the year of death. Using the Standard SelectSurvival Model with interest at 5% per year, calculate the total amount ofnet premium payable in a year if premiums are payable annually.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 124 / 283

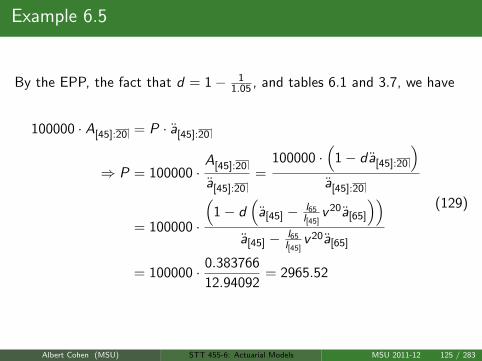

Example 6.5

By the EPP, the fact that d = 1− 11.05 , and tables 6.1 and 3.7, we have

100000 · A[45]:20 = P · a[45]:20

⇒ P = 100000 ·A[45]:20

a[45]:20

=100000 ·

(1− da[45]:20

)a[45]:20

= 100000 ·

(1− d

(a[45] − l65

l[45]v 20a[65]

))a[45] − l65

l[45]v 20a[65]

= 100000 · 0.383766

12.94092= 2965.52

(129)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 125 / 283

New Business Strain

Starting up an insurance company requires start-up capital like most othercompanies. Agents are charged with drumming up new business in theform of finding and issuing new life insurance contracts. This helps todiversify risk in the case of a large loss on one contract (more on thislater.)

However, new contracts can incur larger losses up front in the first fewyears even without a benefit payout. This is due to initial commisionpayments to agents as well as contract preparation costs. Periodicmaintenance costs can also factor into the premium calculation.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 126 / 283

An Example..

Consider offering an n−year endowment policy to an age (x) in theaggregate population where the benefit B is paid at the end of the year ofdeath or on maturity. There are periodic renewal expenses of r per policy.

Then the premium P is calculated via the EPP as

Pax :n = B · Ax :n + r ax :n

⇒ P = B · Ax :n

ax :n+ r

(130)

and we see that periodic expenses are simply passed on to the consumer!

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 127 / 283

An Example..

Consider offering an n−year endowment policy to an age (x) in theaggregate population where the benefit B is paid at the end of the year ofdeath or on maturity. There are periodic renewal expenses of r per policy.

Then the premium P is calculated via the EPP as

Pax :n = B · Ax :n + r ax :n

⇒ P = B · Ax :n

ax :n+ r

(130)

and we see that periodic expenses are simply passed on to the consumer!

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 127 / 283

Another Example..

Consider offering an n−year endowment policy to an age (x) in theaggregate population where the benefit B is paid at the end of the year ofdeath or on maturity. There are periodic renewal expenses of r per policyand an inital preparation expense of z per contract.

Then the premium P is calculated via

P = B · Ax :n

ax :n+ r +

z

ax :n(131)

and so the initial preparation expense is amortized over the lifetime of thecontract.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 128 / 283

Another Example..

Consider offering an n−year endowment policy to an age (x) in theaggregate population where the benefit B is paid at the end of the year ofdeath or on maturity. There are periodic renewal expenses of r per policyand an inital preparation expense of z per contract.

Then the premium P is calculated via

P = B · Ax :n

ax :n+ r +

z

ax :n(131)

and so the initial preparation expense is amortized over the lifetime of thecontract.

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 128 / 283

Example 6.6

An insurer issues a 25−year annual premium endowment insurance withsum insured 100000 to a select life aged [30]. The insurer incurs initialexpenses of 2000 plus 50% of the first premium and renewable expenses of2.5% of each subsequent premium. The death benefit is payableimmediately upon death. What is the annual premium P?

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 129 / 283

Example 6.6

We can see that

Lg0 = 100000v minT[30],25 + 2000 + 0.475P

+ 0.025PaminK[30]+1,25 − Pa

minK[30]+1,25

⇒ P =100000 · E

[v minT[30],25

]+ 2000

0.975 · E[

aminK[30]+1,25

]− 0.475

(132)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 130 / 283

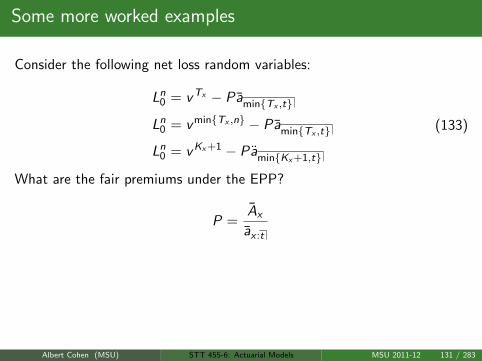

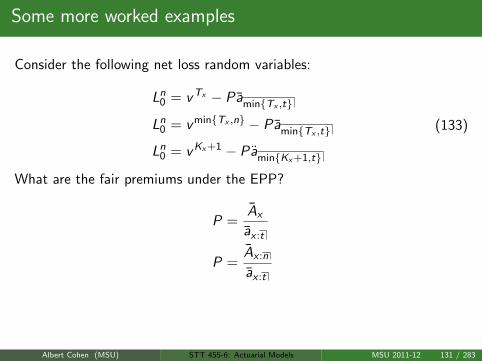

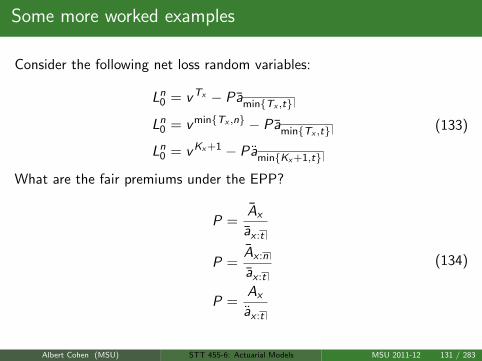

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

Some more worked examples

Consider the following net loss random variables:

Ln0 = vTx − PaminTx ,t

Ln0 = v minTx ,n − PaminTx ,t

Ln0 = vKx+1 − PaminKx+1,t

(133)

What are the fair premiums under the EPP?

P =Ax

ax :t

P =Ax :n

ax :t

P =Ax

ax :t

(134)

Albert Cohen (MSU) STT 455-6: Actuarial Models MSU 2011-12 131 / 283

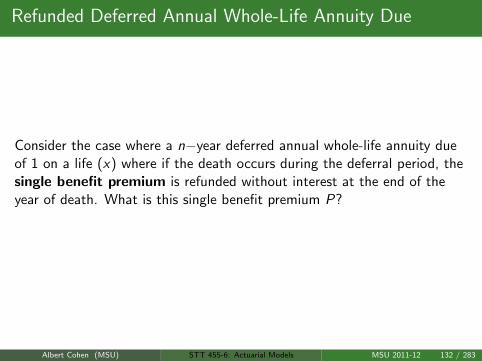

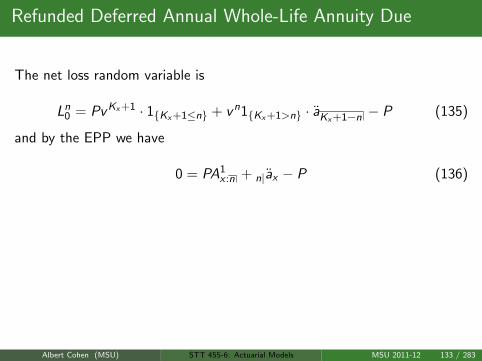

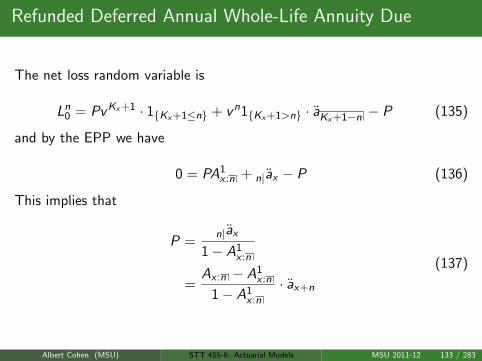

Refunded Deferred Annual Whole-Life Annuity Due