strong pipeline of new supply as market flourishes 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016...

TRANSCRIPT

MARKETVIEW

0

20

40

60

80

100

120

140

160

180

0

200

400

600

800

1,000

1,200

1,400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Q2

Take

-up M

W

Supply

MW

Projected SupplySupplyTake-upForecast Take-up

Strong pipeline of new supply

as market flourishes

16.9%

QUARTERLY REVIEW

Europe Data Centres, Q2 2017

Q2 2017 CBRE Research © 2017 | CBRE Limited 1

4.5%3.6%

Q2 SNAPSHOT

•

•

•

Figure 1: Europe Colocation Supply, Take-up and Year-End Projection as at Q2 2017

Source: CBRE Research, Q2 2017

MARKETVIEW

Retail let516 MW

Retail available65 MW

Wholesale let349 MW

Wholesale available102 MW

SUPPLY & AVAILABILITY

EUROPE DATA CENTRES

Q2 2017 CBRE Research 2© 2017 | CBRE Limited

Source: CBRE Research, Q2 2017

Figure 2: Europe Colocation Supply and Availability as at Q2 2017

MARKETVIEW

TAKE-UP & DEMAND

FEAST OR FAMINE

Q2 2017 CBRE Research © 2017 | CBRE Limited 3

EUROPE DATA CENTRES

Source: CBRE Research, Q2 2017

Figure 3: Europe Colocation Take-up as at Q2 2017

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MW

Q3-Q4 projection Paris London Frankfurt Amsterdam

MARKETVIEW

MARKET ABSORPTION

Q2 2017 CBRE Research © 2017 | CBRE Limited 4

EUROPE DATA CENTRES

Figure 4: Market Absorption Based on Average Take-up of Previous 5 Years

Source: CBRE Research, Q2 2017

Supply AvailabilityTake-up

(quarterly)Take-up

(year to date)

Amsterdam Q2 2017 234 40 10.0 13.5

Q2 2016 164 25 1.8 4.7

Frankfurt Q2 2017 213 29 2.6 5.9

Q2 2016 194 32 10.5 18.8

London Q2 2017 433 74 15.5 33.0

Q2 2016 371 66 15.8 21.7

Paris Q2 2017 152 24 3.0 5.3

Q2 2016 129 14 7.5 9.7

European Tier 1 Total Q2 2017 1,032 166 31.1 57.7

Q2 2016 858 136 35.5 54.9

Figure 5: Key Colocation Statistics – year on year comparison (MW)

Source: CBRE Research, Q2 2017

MARKETVIEW

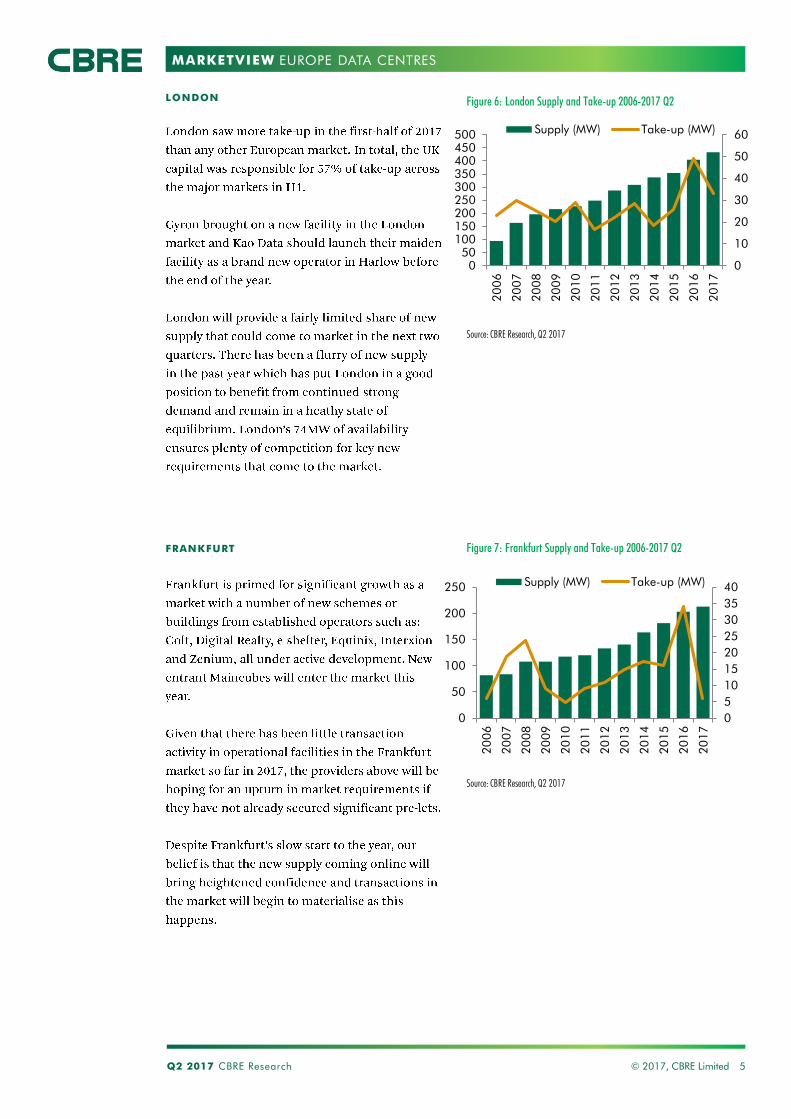

LONDON

EUROPE DATA CENTRES

Q2 2017 CBRE Research 5

Figure 6: London Supply and Take-up 2006-2017 Q2

© 2017, CBRE Limited

FRANKFURT Figure 7: Frankfurt Supply and Take-up 2006-2017 Q2

Source: CBRE Research, Q2 2017

Source: CBRE Research, Q2 2017

0

10

20

30

40

50

60

050

100150200250300350400450500

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Thousa

nds

Supply (MW) Take-up (MW)

0

5

10

15

20

25

30

35

40

0

50

100

150

200

250

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Thousa

nds

Supply (MW) Take-up (MW)

MARKETVIEW

AMSTERDAM

EUROPE DATA CENTRES

Q2 2017 CBRE Research 6© 2017, CBRE Limited

PARIS

Figure 8: Amsterdam Supply and Take-up 2006-2017 Q2

Figure 9: Paris Supply and Take-up 2006-2017 Q2

Source: CBRE Research, Q2 2017

Source: CBRE Research, 2017 Q2

0

10

20

30

40

50

60

0

50

100

150

200

250

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Thousa

nds

Supply (MW) Take-up (MW)

0

5

10

15

20

25

0

20

40

60

80

100

120

140

160

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

15

20

16

Thousa

nds

Supply (MW) Take-up (MW)

MARKETVIEW

DEFINITIONS

SUPPLY

AVAILABILITY

VACANCY RATE

COLOCATION TAKE-UP

EUROPEAN DATA CENTRES

SPACE TYPE

ABSORPTION

Q2 2017 CBRE Research © 2017 | CBRE Limited 7

EUROPE DATA CENTRES

MARKETVIEW

Disclaimer: information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy andcompleteness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of CBRE.

EMEA CONTACTS

EUROPE DATA CENTRES

CBRE DATA CENTRE SOLUTIONS

•

•

•

•

•

•

•

US CONTACT

ASIA CONTACT