strong interim result, dividend increased for personal use ... · treasury group limited (asx:trg,...

TRANSCRIPT

Treasury Group Limited

ABN: 39 006 708 792 Level 14, 39 Martin Place, Sydney NSW 2000

Phone +61 2 8243 0400 Facsimile +61 2 8243 0410 www.treasurygroup.com

ASX announcement Tuesday 25 February 2014

Strong Interim Result, Dividend Increased

• NPAT up 12% (on H1 2013) to $6.8 million

• Solid growth in underlying NPAT of $7.2 million, up 30% on H1 2013

• Total FUM at $19.1 billion, up 13% on H1 2012 driven by strong performances from RARE, IML and Celeste

• Dividend up 35% to 23 cents per share

• Portfolio rationalisation – sale of TAAM, merger of Evergreen Capital, closure of Orion Australian equities

• Solid momentum expected to continue into 2H 2014

Treasury Group Limited (ASX:TRG, “Treasury” of “the Company”) is pleased to report the Company’s Half Year results for the six month period ending 31 December 2013. Consolidated profit after tax (NPAT) totalled $6.76 million for the half, representing an increase of 12% on the prior corresponding period (H1 FY2013: $6.0 million). On an underlying basis, the Company’s profits were $7.2 million, representing an increase of 30% on H1 FY2013 ($5.5 million). The key drivers of profit growth were improved market conditions and strong performances from RARE Infrastructure (RARE), Investors Mutual Limited (IML) and Celeste Funds Management (Celeste). Total Funds Under Management (FUM) at 31 December 2013 was $19.1 billion, an increase of $2.2 billion or 13% on H1 FY2013 ($17.0 billion). The aggregated net retail funds inflow from RARE, IML and Celeste for the six-month period ending 31 December 2013 totalled $385 million, compared to $204 million in H1 FY2013. Retail funds inflow from RARE, IML and Celeste are driving net margins higher. Average net margin was 58 bps for H1 FY2014 (excluding Trilogy), compared to average net margin of 54 bps in H1 FY 2013. Following the strong Interim Result, the Board has declared a fully franked interim dividend of $0.23 per share, which represents a 35% increase on the Interim Dividend paid in H1 FY2013 ($0.17 per share). The dividend increase reflects the Board’s confidence in the Company’s financial strength and positive operating outlook. The Record Date for the Interim Dividend is 6 March 2014 and the Payment Date is 27 March 2014.

For

per

sona

l use

onl

y

Page 2 of 2

Treasury Group’s Managing Director, Mr Andrew McGill commented:

“This was a pleasing result for the Company, led by strong contributions from RARE, IML and Celeste. FUM inflows from retail investors is driving higher average margins across our portfolio and increased profits. “During the period, management was proactive in relation to management of TRG’s portfolio including in relation to the sale of TAAM, merger of Evergreen with Freehold Investment Management and restructure of Orion. “The increase in the interim dividend reflects the growth in the underlying profitability of the business”.

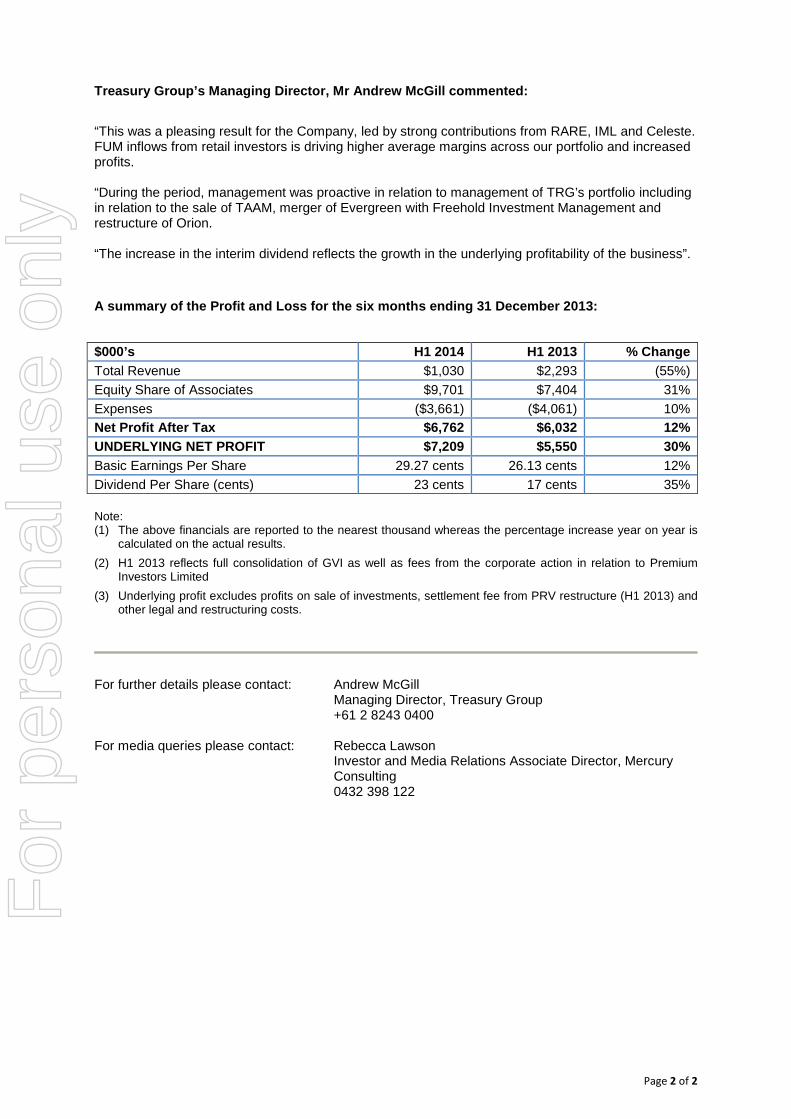

A summary of the Profit and Loss for the six months ending 31 December 2013:

$000’s H1 2014 H1 2013 % Change Total Revenue $1,030 $2,293 (55%) Equity Share of Associates $9,701 $7,404 31% Expenses ($3,661) ($4,061) 10% Net Profit After Tax $6,762 $6,032 12% UNDERLYING NET PROFIT $7,209 $5,550 30% Basic Earnings Per Share 29.27 cents 26.13 cents 12% Dividend Per Share (cents) 23 cents 17 cents 35% Note: (1) The above financials are reported to the nearest thousand whereas the percentage increase year on year is

calculated on the actual results. (2) H1 2013 reflects full consolidation of GVI as well as fees from the corporate action in relation to Premium

Investors Limited (3) Underlying profit excludes profits on sale of investments, settlement fee from PRV restructure (H1 2013) and

other legal and restructuring costs.

For further details please contact: Andrew McGill

Managing Director, Treasury Group +61 2 8243 0400

For media queries please contact: Rebecca Lawson

Investor and Media Relations Associate Director, Mercury Consulting

0432 398 122

For

per

sona

l use

onl

y

Treasury Group Limited Interim Results presentation 31 December 2013

For

per

sona

l use

onl

y

Agenda

2

1. Financial Highlights – 6 months ending 31 December 2013

2. Funds Under Management

3. Dividend

4. Outlook & Summary

For

per

sona

l use

onl

y

1. Financial Highlights

3

• NPAT up 12.1% (on H1 FY2013) to $6.8 million

• Solid growth in underlying profit – up 29.9% (on H1 FY2013) to $7.2 million

• Total FUM at 31 December 2013 – $19.1 billion, up $2.2 billion (or 12.7%) on H1 FY2013

• Strong performance across boutiques, particularly RARE, IML and Celeste:

› Retail net funds inflow (aggregate) for RARE, IML and Celeste – $385m vs $204m (H1 FY2013)

• Ongoing efficiency and expense management at TRG

• Portfolio rationalisation – sale of TAAM and merger of Evergreen Capital

• Dividend of 23 cents per share, up 35.3% on H1 FY2013 (17 cents per share)

Strong profit growth, driven by RARE, IML and Celeste

For

per

sona

l use

onl

y

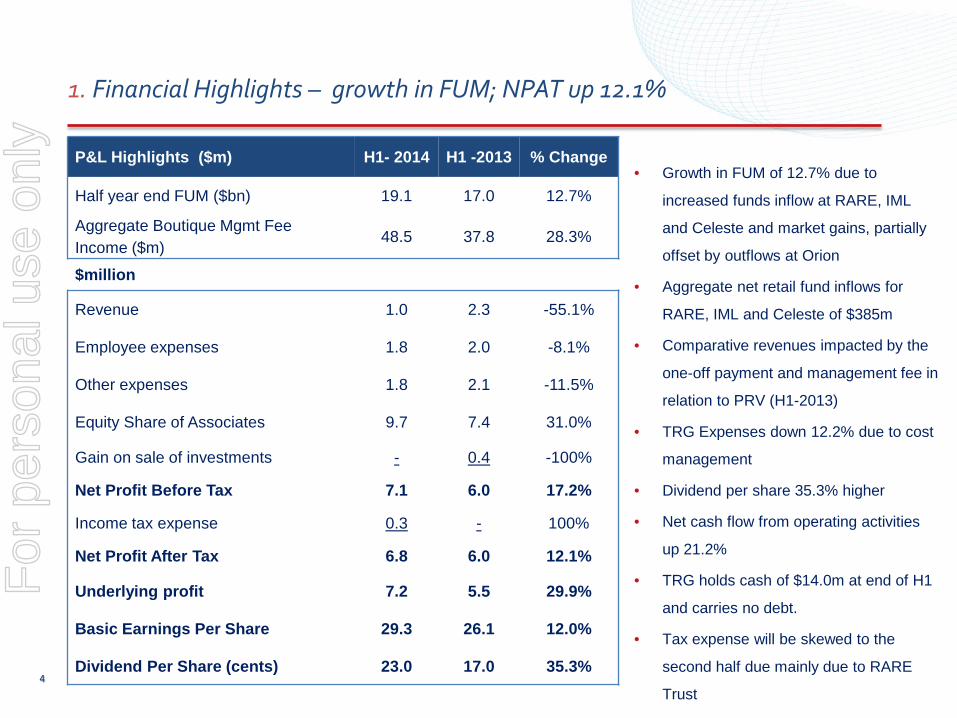

1. Financial Highlights – growth in FUM; NPAT up 12.1%

4

P&L Highlights ($m) H1- 2014 H1 -2013 % Change

Half year end FUM ($bn) 19.1 17.0 12.7%

Aggregate Boutique Mgmt Fee Income ($m) 48.5 37.8 28.3%

$million

Revenue 1.0 2.3 -55.1%

Employee expenses 1.8 2.0 -8.1%

Other expenses 1.8 2.1 -11.5%

Equity Share of Associates 9.7 7.4 31.0%

Gain on sale of investments - 0.4 -100%

Net Profit Before Tax 7.1 6.0 17.2%

Income tax expense 0.3 - 100%

Net Profit After Tax 6.8 6.0 12.1%

Underlying profit 7.2 5.5 29.9%

Basic Earnings Per Share 29.3 26.1 12.0%

Dividend Per Share (cents) 23.0 17.0 35.3%

• Growth in FUM of 12.7% due to

increased funds inflow at RARE, IML

and Celeste and market gains, partially

offset by outflows at Orion

• Aggregate net retail fund inflows for

RARE, IML and Celeste of $385m

• Comparative revenues impacted by the

one-off payment and management fee in

relation to PRV (H1-2013)

• TRG Expenses down 12.2% due to cost

management

• Dividend per share 35.3% higher

• Net cash flow from operating activities

up 21.2%

• TRG holds cash of $14.0m at end of H1

and carries no debt.

• Tax expense will be skewed to the

second half due mainly due to RARE

Trust

For

per

sona

l use

onl

y

1. Financial Results – Underlying NPAT up 29.9%

5

• Residual goodwill in relation to

AR capital written off

• Consulting and legal costs in

relation to the sale of TAAM,

advisory work on projects

Treasury Group P&L ($000) H1- 2014 H1 -2013 % Change

Profit After Tax 6,753.5 6,027.5 12.0%

Net gain on disposal of investments - (396.3)

Settlement fee from PRV restructure - (500.0)

Legal, consulting and restructuring costs

202.6 418.6

Impairment of goodwill 252.7 -

Underlying Profit 7,208.9 5,549.8 29.9%

For

per

sona

l use

onl

y

1. Financial Results – Aggregate Profit & Loss of TRG Boutiques

6

• Average net margin excludes

Trilogy. It is increasing due to

favourable change in mix

(increased retail FUM).

• TRG share of after tax profit

higher due to favourable

change in mix (increase

contribution from IML ,RARE

and Celeste).

• Total cash held across the

boutiques is $36.5 m (excl

TRG)

Aggregate P&L for Boutiques ($m) H1- 2014 H1 - 2013 % change

Half year end FUM ($bn) 19.1 17.0 12.7%

Average Net Margin (%) 58 bpts 54 bpts 7.4%

Base Management Fees 49.4 37.8 30.7%

Other income 2.7 1.4 92.9%

Gross Profit 52.1 39.2 32.9%

Employee expenses 13.1 10.0 31.0%

Other expenses 7.1 6.9 2.9%

NPBT 30.2 22.3 35.4%

Income Tax 6.8 4.2 61.9%

NPAT 23.4 18.1 29.3%

TRG Share of After Tax Profit 9.7 7.4 31.1% For

per

sona

l use

onl

y

2. FUM - diversification across boutiques lowers risks

7

$19.1 billion FUM as at 31 December 2013

IML, 25.1%

Orion, 3.0%

RARE, 41.3%

Celeste, 4.0%

Trilogy, 22.8%

Other TRG Boutiques, 3.8%

For

per

sona

l use

onl

y

2. FUM – Diversification away from Australian equities continues, funds from retail investors is increasing

8

-

2

4

6

8

10

12

14

16

18

20

$bn

FUM by Investor Type

Institutional

Retail

-

2

4

6

8

10

12

14

16

18

20

$bn

FUM by Investor Location

International Source

Domestic Source

Dec-12 Dec-130%

20%

40%

60%

80%

100%

FUM by Product Type

Alternatives

International Equities

Australian Equities

For

per

sona

l use

onl

y

3. FUM

9

• Inflows at RARE, IML

and Trilogy were offset

by outflows at Orion.

Note: Chart shows Net Flow, not change in FUM

-$2,000

-$1,500

-$1,000

-$500

$0

$500

$1,000

$1,500

$m

TRG Half Yearly Net New Funds Flow (Jan 2009 to Dec 2013)

For

per

sona

l use

onl

y

4. FUM - growth at RARE and IML drives average margin higher

10

0

10

20

30

40

50

60

70

80

0

5

10

15

20

25Avg Margin

(bps) FUM $bn

Composition of FUM vs Average Margin

Trilogy

Freehold (Evergreen) & AR Capital

Celeste

TAAM

Aubrey & Global Value Investors

RARE Infrastructure

Orion

Investors Mutual

% incl Trilogy (RHS)

% excl Trilogy (RHS)

For

per

sona

l use

onl

y

5. Dividend – increase reflects growth in underlying profit

11

• Interim dividend for FY2014 up

35.3% (on H1 FY2013) to 23 cents per share

• Balance sheet liquid and ungeared • Payout ratio of 79%

Dividend History

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013 2014

cps

Interim Final

For

per

sona

l use

onl

y

6. Summary & Outlook

12

• Solid underlying growth driven by improved market conditions, increased appetite from retail

investors and investment performance from key boutiques

• Strong growth from IML & RARE offset by reduced contribution from Orion

• Shift in FUM towards retail funds boosts overall margin and profits

• Interim dividend up 35.3% from 17 cents per share to 23 cents per share

• Long term fundamentals for funds management remain attractive – Australian industry large and growing

• Significant investment in assessment of new deal opportunities, particularly international

For

per

sona

l use

onl

y

Disclaimer

The information in this presentation is general background information about Treasury Group Limited and is current only at the date of this presentation. In particular, this presentation:

• is not an offer or recommendation to purchase or subscribe for securities in Treasury Group Limited, nor is it an invitation to any person to acquire securities in Treasury Group; • is not personal advice and does not take into account the potential and current individual investment objectives or the

financial situation of investors; and • contains information in summary form and does not purport to be complete.

Certain statements in this presentation may constitute “forward-looking” statements. Forward-looking statements are neither promises nor guarantees and involve known and unknown risks, uncertainties and other factors which may cause actual results to vary materially from any projection, future results or performance expressed or implied by such forward-looking statements.

13

For

per

sona

l use

onl

y