strategic report for american science &...

TRANSCRIPT

Strategic Report for American Science & Engineering

Joe Thorpe

Levon Balayon Alex Menenberg

April 20, 2009

American Science & Engineering

April 2009 Page 2

Table of Contents

Executive Summary..........................................................................................................................3 History...............................................................................................................................................4 Product Line & Current Model .....................................................................................................6

Competitive Analysis........................................................................................................................7 Internal Rivalry.................................................................................................................................7 Supplier Power.................................................................................................................................7 Buyer Power .....................................................................................................................................8 Entry and Exit..................................................................................................................................9 Substitutes.........................................................................................................................................9 Complements .................................................................................................................................10

SWOT .................................................................................................................................................11 Strengths .........................................................................................................................................11 Weaknesses.....................................................................................................................................11 Opportunities .................................................................................................................................11 Threats.............................................................................................................................................11

Financial Analysis ...........................................................................................................................13 Key Financial Metrics ...................................................................................................................13 Conclusion......................................................................................................................................14

Strategic Recommendations ........................................................................................................15 References .........................................................................................................................................19 Appendix – Financial Statements...............................................................................................20

Balance Sheet..................................................................................................................................20 Income Statement..........................................................................................................................21 Statement of Cash Flows..............................................................................................................22

American Science & Engineering

April 2009 Page 3

Executive Summary

American Science & Engineering is a technology company that produces X-ray

technology for government and private institutions to help detect contraband. While ASEI

has flourished in recent years as a result of the increase of the United State’s investment in

homeland security, the company has hired Oasis Consulting in order to continue growth in

an uncertain economic and political climate.

The United States currently has a new executive administration as well as a saturated

market for American Science & Engineering’s products. While a potential buyout should be

considered, we believe that by diversifying the company’s product line and also continuing

expansion into foreign markets, ASEI can continue with the exceptional growth that it has

experienced. This strategic report is broken up into five main sections: Company

Background, Competitive Analysis, SWOT, Financial Analysis and our Strategic

Recommendation. We will attempt to show that ASEI cannot be content with current

success and must look towards maintaining continued growth into the future.

American Science & Engineering

April 2009 Page 4

Company Overview

History

X-Ray Technology and Astronomy:

American Science and Engineering formed in 1958 as a developer of scientific

instruments and applications for NASA. In 1959, renowned scientist Dr. Riccardo Giacconi

joined the company and created a small astronomy team to focus research on X-rays. In

1963 Dr. Giacconi’s team launched a rocket equipped with X-ray detectors and discovered

Sco X-1, the first known X-ray source outside the solar system. Throughout the 1960's and

1970's the team carried on its innovative spirit by pioneering the discovery of X-ray related

astronomical phenomena and construction of X-ray detecting technology. Notable

achievements during this period include:

1965:

AS&E participates in launch operations for eight rocket and satellite payloads

carrying instrumentation designed and developed by AS&E. Among these flights is a

NASA rocket carrying an image-forming X-ray telescope designed by AS&E. This

experiment results in the first successful photograph of the sun in soft X-rays.

1967:

AS&E builds the first focusing X-Ray telescope, a model of which is now flying as

part of the Orbiting Solar Observatory launched on October 18. The telescope

returns an X-ray picture of the sun every five minutes for the next 15 years.

1969:

The first stop-action sequence ever taken of the development of a solar flare in X-

rays is obtained during a rocket launch of AS&E's telescope - the largest X-ray

telescope flown to date.

1970:

Dr. Giacconi's research group launches "Uhuru" - the first satellite dedicated

completely to X-ray astronomy. Uhuru completes its mission in 1973.

American Science & Engineering

April 2009 Page 5

An Expanding Focus

Beginning in the 1970 with the acquisition of Sippican Electronics Division of

Sippican Corporation, American Science and Engineering expanded its focus to include

other applications of X-Ray, such as defense, education, medicine, non-destructive testing,

and security. In 1975 American Science and Engineering became a public company and a

year later, introduced ASEP to the market, a field-leading system for public utility load

management, demand metering and automatic remote meter reading. ASEP became a major

revenue-generator for AS&E during the 1980s and provided AS&E with ample cash to fund

the increased scope of business.

AS&E has a strong and storied history of scientific innovation, particularly in the

field of X-ray technology. Formed in 1958, AS&E began as a developer of scientific

instruments and applications for NASA. In 1959, Dr. Riccardo Giacconi joined AS&E and

created an X-ray astronomy team. In the coming decades, Dr. Giacconi's team made a

succession of pioneering discoveries and developments in the field of X-ray technology,

including the discovery of the first known X-ray source outside the solar system (1962), the

first successful soft X-ray photograph of the sun (1965), the launch of the first satellite

dedicated completely to X-ray astronomy (1970), and the launch of the Einstein Observatory

– the world's largest X-ray telescope (1978). Dr. Giacconi's pioneering work at AS&E later

earned him the Nobel Prize in Physics.

In subsequent years, AS&E also developed innovative technologies in the fields of

defense, education, medicine, non-destructive testing, and security. AS&E's additional

technological achievements include: development of low energy, high resolution Computed

Tomography (CT) scanning of the human body, derivatives of which are used today in

medical scanning systems worldwide; as well as development of the first practical rail car

inspection system used by the U.S. Government to scan rail cars leaving Russian missile

factories, to confirm compliance with the 1972 Intermediate Range Nuclear Forces Treaty.

AS&E also designed and implemented high-resolution non-destructive testing systems to

inspect aluminum welds on the U.S. Space Station.

Beginning in the 1980's, American Science and Engineering introduced a new focus

of production to security products with the introduction of MICRO-DOSE X-ray System.

American Science & Engineering

April 2009 Page 6

Throughout the 1980's and 1990's the company narrowed its focus to solely developing

security products, and in 2005 sold its High Energy Systems Division. Currently, the

company's main customers are governments and private corporations interested in securing

ports, border crossings, and high-threat facilities and events.

Product Line & Current Model

American Science & Engineering currently develops, manufactures, markets and sells

X-ray imaging technologies used to inspect parcels, baggage, vehicles, pallets, cargo

containers and people in order to detect contraband. Current customers include: authorities

responsible for port and border security, aviation security agencies, military organizations

and high threat commercial and governmental facilities. After the attacks on the World

Trade Center on September 11, 2001, the United States government has significantly

increased homeland security spending and American Science & Engineering has secured the

United States government as its largest customer.

American Science & Engineering’s products and services can be grouped into six

different areas including Z Backscatter Systems, CargoSearch Inspection Systems, Personnel

Inspection, ParcelSearch Inspection Systems, Contract Research and Development, and

Service and Support.

American Science & Engineering

April 2009 Page 7

Competitive Analysis

FORCE STRATEGIC SIGNIFICANCE Internal Rivalry Low Supplier Power High Buyer Power High Entry and Exit Low Substitutes Low Complements Medium

Internal Rivalry

Main Competitor:

o Analogic Corporation (ALOG)

While both ALOG is listed as a major competitor, ASEI has significant monopoly power in

the X-ray security scanning industry (7). Analogic Corporation currently produces x-ray

technology mainly for healthcare purposes, which is not the type of product that American

Science and Engineering currently produces. ASEI’s main product is the Z-Backscatter Van,

which scans large cargo. ASEI currently holds a patent on this product and they are the only

company which manufactures anything of its kind. Furthermore, the ZBV is the main

product ASEI produces and the US government recently signed a contract with the

company explicitly saying ASEI would be their only producer of such a product. At this

point, ASEI does not have to worry much about internal rivalry and should only be

concerned if Analogic begins to shift production into homeland security scanning.

Supplier Power

American Science & Engineering relies on a small number of suppliers that provide core

materials and subsystems for their products. While their suppliers are not clear, it is implied

in their 10K that certain materials or subsystems may be available from a sole source or

limited number of suppliers, which increases the risk of supply disruption. Products would

have to be redesigned if one of the materials from their suppliers was no longer available;

this would be extremely costly and could potentially take an extremely long period of time.

Additionally, ASEI does not have any guaranteed supply arrangements with their suppliers

American Science & Engineering

April 2009 Page 8

and they have no assurance that their suppliers will continue to meet their product

requirements. It is clear that American Science & Engineering’s suppliers have a tremendous

amount of power and this is a high risk for the company.

Buyer Power

The main buyers of ASEI products are governments. The leading buyer is currently the

United States government, but the company has seemed to switch its focus to international

governments simply because the US government has purchased all they need to at the

current time. Homeland security is important to every government and it is the responsibility

of the government to purchase top of the line technology to protect its citizens (this has

been especially important in the United States, Israel, and other countries in the Middle East

due to the current political climate). ASEI does have power in the sense that the government

strongly prefers their security products and have not had to deal with much competition

recently. The problem is the small number of buyers. If governments decided to shift

spending in national security to some other department, American Science & Engineering

would take a strong hit in sales. The graph below shows that while ASEI is moving towards

acquiring more customers, they are still strongly dependent on a relatively small number of

buyers. They must continue to acquire more in order to eliminate the risk of folding if a large

buyer pulled out.

% Revenues Accounted for by Two Customers

0%

10%

20%

30%

40%

50%

60%

2006 2007 2008

American Science & Engineering

April 2009 Page 9

Entry and Exit

This is an especially difficult industry to both enter and exit. One major reason for this is the

high cost of entry. These are two major reasons ASEI has benefited by being a first mover in

the industry. They are currently the only producer of the Z-Backscatter Van, which is their

main product. Furthermore, exit is difficult for their manufacturing equipment is extremely

specialized and would be difficult to sell simply because there are not many companies who

would have a need to purchase such a product. Patents are another strong barrier to entry.

ASEI employs highly skilled engineers and holds a number of patents on their advanced

technology. American Science & Engineering currently has 63 unexpired patents with the

U.S. Patent and Trademark Office as well as with the patent offices of Norway, The Russian

Federation, Ukraine, Singapore, United Arab Emirates, Malaysia, Thailand, Egypt and under

the Gulf Cooperation Council and the Patent Cooperation Treaty. While the exact expiration

dates of all of their products are difficult to establish, it has been said that the duration of

their patents are adequate relative to the expected lives of their products.

Substitutes

Again, this does not seem like much of a problem for American Science & Engineering. At

the current time, there does not seem to be a viable substitute for their ZBVs and additional

x-ray technology. There is some discussion about possible retinal scans or RFID security,

however this is not much of a threat. The thought is that if a better identification technology

becomes standardized that traditional imaging technology will become obsolete. Even if

people are more easily accounted for in domestic and international travel, there is still a need

for cargo scanning as long as there are people entering and exiting countries or shipping

goods.

American Science & Engineering

April 2009 Page 10

Complements

Complements for this particular firm can be categorized as any product that would likely

lead to the purchase of an ASEI product. One such complement would be the construction

of a new airport, especially in the United States. As additional airports are constructed new

security systems must be installed that comply with federal regulations, and ASEI’s product

line is the most popular among such security systems. Another complement would be

popular live events that attract large crowds. Political conventions, sporting events, and

other such events all attract large crowds and demand high levels of security. This can be

considered a medium threat, for it is possible that ASEI could saturate their market, but with

the large amount of national security spending in foreign countries, it does not seem likely in

the near future.

American Science & Engineering

April 2009 Page 11

SWOT

Strengths

o Proprietary technology to provide scanning equipment – relatively new patents

established within the last five years

o The company is instrumental both domestically and on the two war front

o Little competition

o Established clientele and reputation

Weaknesses

o Company is reliant on government contracts

o An enormous portion of sales depend upon governmental agency decisions to

expand or upgrade security at high risk locations. Because of this, ASEI’s product

sales are subject to delays associated with the length approval processes that often

accompany such capital expenditures.

o ASEI’s revenues are made up of a relatively small number of expensive products.

Opportunities

o Shifting priorities in defense spending toward intelligence and surveillance

o Potential international growth

o Olympics in London, 2012 and other large events that demand a high level of

security

o Potential buyout from large defense contractor looking to diversify

Threats

o Round of consolidation in the defense technology market, especially in the light of

the recent reduction in stock prices

American Science & Engineering

April 2009 Page 12

o If ASEI fails to receive an order after expending resources, they may be unable to

generate sufficient revenue to recover incurred costs. This could be a result of the

lengthy sales cycle.

o US market for the ASEI product saturated

o Unclear prospects from the perspective of the Government Policy towards national

security. ASEI’s R&D is primarily government funded and in order to stay

competitive, they must continue to receive government funds, which are not

guaranteed in the new administration.

American Science & Engineering

April 2009 Page 13

Financial Analysis Stock Chart (ASEI v. ALOG v. S&P 500) 5 yr Trailing (5)

Key Financial Metrics

American Science & Engineering (ASEI) (4)

o Current Price: $58.64/share (04/17/09)

o Market Cap: $534.03 Million

o P/E: 22.93

o Beta: 0.40

o EPS: $2.56

o Debt/Capital: 5% (6)

Q4 (Dec '08) Annual

(2008)

Annual

(TTM)

Net profit margin 15.41% 10.48% 11.27%

Operating margin 22.69% 12.73% 15.86%

EBITD margin - 15.20% 17.95%

Return on average assets 15.92% 7.64% 8.93%

Return on average equity 23.62% 10.47% 13.06%

American Science & Engineering

April 2009 Page 14

Analogic Corporation (ALOG) (4)

o Current Price: $34.76/share (04/17/09)

o Market Cap: $444.89 Million

o P/E: 39.47

o Beta: 0.78

o EPS: $0.88

Q1 (Jan '09) Annual

(2008)

Annual

(TTM)

Net profit margin 1.38% 5.68% 2.76%

Operating margin -1.47% 5.88% 1.66%

EBITD margin - 9.42% 5.66%

Return on average assets 1.21% 4.84% 2.50%

Return on average equity 1.42% 5.72% 2.91%

Conclusion

It is clear from the financial analysis that ASEI does not have any liquidity concerns

(5% Debt/Capital) and has managed to stay profitable even during poor economic times

(15.41% Net Profit Margin in Q4 ’08) (1). The one immediate concern is the dependence on

government purchases and also the relatively flat stock price in the last two years. Large

jumps in stock price are directly correlated with large purchases from the U.S. government.

Stockholders will not continue to be satisfied with a relatively flat stock price, and potential

ways to fix this are listed in the Strategic Recommendations section below. Another issue is

that its main competitor, Analogic Corporation, has nearly twice the P/E ratio of ASEI. This

may be an indicator that ASEI is not as focused on growth, which is definitely a concern and

may be a reason to potentially look to sell off the company (see Strategic

Recommendations).

American Science & Engineering

April 2009 Page 15

Strategic Recommendations Market Expansion

The tremendous performance of American Science & Engineering over the past ten

years has been undeniable. Profits soared and as shown in the financial section above, the

stock price followed. This tremendous growth is mainly due to the success ASEI has had

inventing impressive products and establishing solid patents. It is with these products

(namely the Z-Scatter Van) that ASEI has been able to obtain large government and private

contracts. The largest customer of American Science & Engineering is undoubtedly the

United States Government (1).

% Sales in 2006 % Sales in 2008

It is clear that the main issue this company faces is market saturation. With highly

specialized products, the company can only sell so many to the US government before their

need is filled and the only billing they can receive is from maintenance.

Market saturation combined with a new executive administration could result in

significantly reduced demand and a subsequent decrease in the company’s profits. American

Science & Engineering currently invests heavily in R&D and has continued to increase its

investment in R&D over the past three years. While a new technological breakthrough could

help open new avenues for new contracts with the United States government, this is not a

safe plan and the company must look towards expanding to new markets.

77%

14%

9%

US Gov

Foreign Gov

Other

55%36%

9%

US Gov

Foreign Gov

Other

American Science & Engineering

April 2009 Page 16

Homeland Security is a vital part of every nation and this must be highly stressed

when looking to acquire new contracts from foreign governments. Lobbyists from foreign

nations (especially in potential high demand areas such as the Middle East, South America

and Northern Africa) must be used in an attempt to push for an increase in homeland

security investment in foreign nations. The company must be able to clearly demonstrate the

direct results of an increase in homeland security investment. Below is a list of projected

spending in homeland security over the next ten years. It is in ASEI’s best interest to target

countries at the top of the list, for they are the countries most likely to be potential

customers.

American Science & Engineering

April 2009 Page 17

Shifting Product Focus

American Science & Engineering is known as a company that produces imaging

technology for use in the aid of strengthening homeland security. While this has proven to

be profitable, it may be in the company’s best interest to diversify their product line in order

to open new avenues for additional revenue. Several possible pathways for diversification

include intelligence, surveillance and medical.

The company’s most profitable and most popular product is the Z-Backscatter Van.

This van, which emits X-rays in various directions rather than one, is mobile and extremely

effective in detecting concealed contraband. While the current uses for the technology have

proven to be effective, we believe that they could serve additional purposes. One potential

customer could be the Drug Enforcement Agency (DEA). Officers are currently put in

compromising positions when they raid homes believed to be distribution or production

centers for illegal substances (such as methamphetamine labs). The ZBV vans could be used

to detect laboratories and people within suspected homes before they conduct the raids,

which would help protect officers to a great degree.

Possible diversification into the medical imaging industry is another exciting

possibility for American Science & Engineering. The X-ray technology used by ASEI

currently produces about 1/6000th of the radiation that a traditional X-ray produces (3). If

the technology could be tweaked to perform traditional medical exams, the health care

industry would be pressured into providing a safer alternative to the traditional imaging

procedures offered to clients.

American Science & Engineering

April 2009 Page 18

Potential Buyout

Another possible option for American Science & Engineering is to look into selling

itself off to the right company. Defense spending has shifted away from weapons programs

to intelligence and surveillance (2). Large defense contractors with a plentiful supply of cash,

such as Lockheed Martin, Boeing and Northrop Grumman may begin to look toward

acquiring smaller companies with niche technologies. Axsys Technologies put itself up for

sale in early March and many analysts believe similar companies will begin to follow suit (8).

This may seem like an odd decision for a company that has been so successful in

recent years, but it does seem like a good option at this point. The market in the United

States is saturated (see above) and the financial assessment of ASEI when compared to their

competitors shows that they may not be committed to growth. Larger companies like

Lockheed and Boeing not only have the cash on hand to purchase a small attractive

company with minimal debt like ASEI, but many attractive synergies seem to be available.

Lockheed and Boeing have great distribution channels and are already known in foreign

countries. Additionally, by diversifying their product line, larger corporations would be able

to have steadier cash flows when sales in their original divisions are down.

American Science & Engineering

April 2009 Page 19

References

1. "10K - ASEI." EDGAR ONLINE - SEC FILINGS. 13 June 2008. 21 Apr. 2009

<http://yahoo.brand.edgar-online.com/DisplayFiling.aspx?dcn=0001104659-08-

039830>.

2. "American Science & Engineering: The Best Offense Is a Good Defense -- Seeking

Alpha." Stock Market News, Opinion & Analysis, Investing Ideas -- Seeking Alpha.

18 Aug. 2008. 21 Apr. 2009 <http://seekingalpha.com/article/91376-american-

science-engineering-the-best-offense-is-a-good-defense>.

3. AS&E: Advanced X-ray Inspection Systems. 21 Apr. 2009 <http://www.as-e.com/>.

4. "ASEI - American Science & Engineering, Inc. - Finance." Google Finance. 21 Apr. 2009

<http://www.google.com/finance?q=NASDAQ%3AASEI>.

5. "ASEI: Competitors for American Science and Engineerin -." Yahoo! Finance. 21 Apr.

2009 <http://finance.yahoo.com/q/co?s=asei>.

6. Price Target Research. American Science & Engineering, Inc. Rep. Billerica, 2009.

7. Roth Capital Partners. American Science & Engineering, Inc. Rep. Newport Beach, 2005.

8. "Small defense tech firms big bet for large contractors | Deals | Private Capital |

Reuters." Reuters.com - World News, Financial News, Breaking US & International

News. 26 Mar. 2009. 21 Apr. 2009

<http://www.reuters.com/article/euPrivateEquityNews/idUSTRE52P5T22009032

6>.

American Science & Engineering

April 2009 Page 20

Appendix – Financial Statements

Balance Sheet

Dollars in thousands December 31,

2008 March 31,

2008 Assets Current assets: Cash and cash equivalents $ 83,395 $ 52,418 Restricted cash and investments 59 319 Short-term investments, at fair value 47,934 72,687 Accounts receivable, net of allowances of $399 and $230 at December 31,

2008 and March 31, 2008, respectively 44,176 27,583 Unbilled costs and fees 4,917 6,114 Inventories 45,042 40,107 Prepaid expenses and other current assets 7,889 4,815 Deferred income taxes 2,571 1,577 Total current assets 235,983 205,620 Building, equipment and leasehold improvements, net 20,161 22,201 Restricted cash and investments — 2,204 Deferred income taxes 6,191 5,231 Other assets, net 965 278 Total assets $ 263,300 $ 235,534

Liabilities and Stockholders’ Equity Current liabilities: Accounts payable $ 13,958 $ 12,660 Accrued salaries and benefits 8,222 2,935 Accrued warranty costs 2,216 1,671 Accrued income taxes 2,198 — Deferred revenue 21,951 23,120 Customer deposits 16,249 6,547 Current portion of lease financing liability 1,146 1,134 Other current liabilities 6,976 8,097 Total current liabilities 72,916 56,164 Lease financing liability, net of current portion 8,679 9,540 Other long term liabilities 5,788 3,758 Total liabilities 87,383 69,462 Stockholders’ equity: Preferred stock, no par value, 100,000 shares authorized; no shares issued — — Common stock, $0.66 2/3 par value, 20,000,000 shares authorized; 8,845,497

and 8,945,633 shares issued and outstanding at December 31, 2008 and March 31, 2008, respectively 5,896 5,963

Capital in excess of par value 86,716 91,544 Accumulated other comprehensive income 12 114 Retained earnings 83,293 68,451 Total stockholders’ equity 175,917 166,072 Total liabilities and stockholders’ equity $ 263,300 $ 235,534

American Science & Engineering

April 2009 Page 21

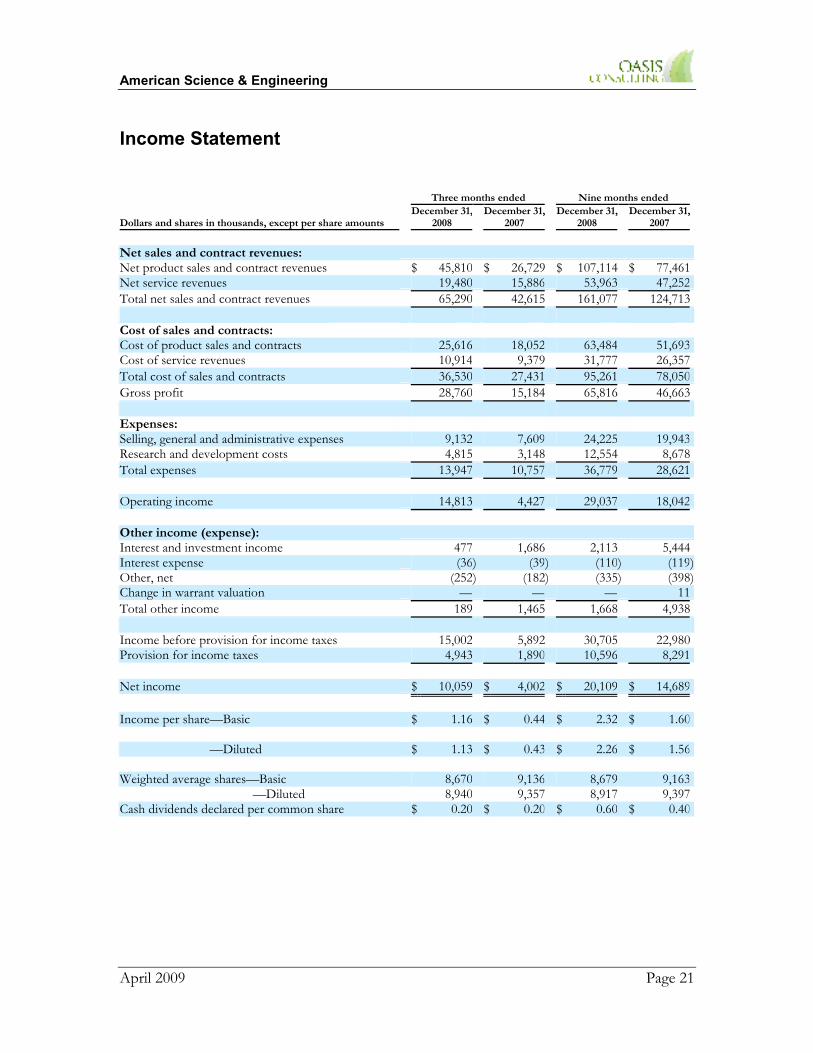

Income Statement

Three months ended Nine months ended

Dollars and shares in thousands, except per share amounts December 31,

2008 December 31,

2007 December 31,

2008 December 31,

2007

Net sales and contract revenues:

Net product sales and contract revenues

$ 45,810 $ 26,729

$ 107,114 $ 77,461

Net service revenues

19,480 15,886

53,963 47,252

Total net sales and contract revenues

65,290 42,615

161,077 124,713

Cost of sales and contracts:

Cost of product sales and contracts

25,616 18,052

63,484 51,693

Cost of service revenues

10,914 9,379

31,777 26,357

Total cost of sales and contracts

36,530 27,431

95,261 78,050

Gross profit

28,760 15,184

65,816 46,663

Expenses:

Selling, general and administrative expenses

9,132 7,609

24,225 19,943

Research and development costs

4,815 3,148

12,554 8,678

Total expenses

13,947 10,757

36,779 28,621

Operating income

14,813 4,427

29,037 18,042

Other income (expense):

Interest and investment income

477 1,686

2,113 5,444

Interest expense

(36 ) (39 ) (110 ) (119 ) Other, net

(252 ) (182 ) (335 ) (398 ) Change in warrant valuation

— —

— 11

Total other income

189 1,465

1,668 4,938

Income before provision for income taxes

15,002 5,892

30,705 22,980

Provision for income taxes

4,943 1,890

10,596 8,291

Net income

$ 10,059 $ 4,002

$ 20,109 $ 14,689

Income per share—Basic

$ 1.16 $ 0.44

$ 2.32 $ 1.60

—Diluted

$ 1.13 $ 0.43

$ 2.26 $ 1.56

Weighted average shares—Basic

8,670 9,136

8,679 9,163

—Diluted

8,940 9,357

8,917 9,397

Cash dividends declared per common share

$ 0.20 $ 0.20

$ 0.60 $ 0.40

American Science & Engineering

April 2009 Page 22

Statement of Cash Flows

For the nine months ended

Dollars in thousands December 31,

2008 December 31,

2007

Cash flows from operating activities: Net income $ 20,109 $ 14,689 Adjustments to reconcile net income to net cash provided by operating

activities: Depreciation and amortization 3,194 3,071 Provisions for contracts, inventory and accounts receivable reserves 1,874 77 Amortization of bond discount (401 ) (1,798 ) Deferred income taxes (1,954 ) (2,823 ) Stock based compensation expense 3,126 4,141 Change in value of warrants — (11 ) Changes in assets and liabilities:

Accounts receivable (16,754 ) (12,983 ) Unbilled costs and fees 1,197 3,940 Inventories (6,648 ) (19,453 ) Prepaid expenses and other assets (3,761 ) 1,645 Accounts payable 1,298 3,139 Accrued income taxes 2,198 1,031 Customer deposits 9,702 (2,181 ) Deferred revenue 881 21,052 Accrued expenses and other current liabilities 5,289 (749 ) Sale of leased asset 116 — Non-current liabilities (20 ) —

Net cash provided by operating activities 19,446 12,787

Cash flows from investing activities: Purchases of short-term investments (50,500 ) (125,282 ) Proceeds from maturities of short-term investments 75,650 100,725 Purchases of property and equipment (1,270 ) (2,271 )

Net cash provided by (used for) investing activities 23,880 (26,828 )

Cash flows from financing activities: Decrease in restricted cash and investments 2,464 278 Proceeds from exercise of warrants — 509 Proceeds from exercise of stock options 4,602 2,939 Repurchase of shares of common stock (14,382 ) (13,821 ) Payment of dividends (5,267 ) (3,704 ) Proceeds from financing of leasehold improvements — 417 Repayment of lease financing (849 ) (1,054 ) Reduction of income taxes paid due to the tax benefit from employee stock

option expense 1,181 1,221

Net cash used for financing activities (12,251 ) (13,215 )

Foreign currency translation effect on cash (98 ) (16 )

Net increase (decrease) in cash and cash equivalents 30,977 (27,272 ) Cash and cash equivalents at beginning of period 52,418 69,650

Cash and cash equivalents at end of period $ 83,395 $ 42,378