stellar diamonds annual report 2011

DESCRIPTION

Stellar Diamonds Annual Report 2011TRANSCRIPT

STELLARDIAMONDS PLC

Building a leading diamond company in West Africa

ANNUAL REPORT & ACCOUNTS 2011

Stellar Diamonds plc (AIM:STEL) is focussed on developing significant diamondresources from two key kimberlite assets in West Africa. The Company iscurrently establishing maiden resource estimates on the Droujba kimberlitepipe in Guinea and the Tongo kimberlite dyke in Sierra Leone, with both thesekimberlites demonstrating multi-million carat potential. In addition, Stellar hasbeen mining diamonds on the Mandala and Bomboko projects in Guinea forover two years, with diamond production having exceeded 134,000 carats to date.

STELLARDIAMONDS PLC

CONTENTS

OVERVIEW01 Highlights02 At a Glance04 Chairman’s Statement

BUSINESS REVIEW06 Chief Executive’s Statement08 Diamond Market Outlook09 Corporate Social Responsibility10 Droujba12 Tongo14 Mandala16 Kono + Bouro17 Bomboko

GOVERNANCE18 Board of Directors20 Key Management22 Directors’ Report24 Statement of Directors’ Responsibilities

FINANCIAL STATEMENTS25 Independent Auditor’s report26 Consolidated Statement of

comprehensive income27 Consolidated statement of financial position28 Consolidated statement of changes in equity29 Consolidated statement of cash flow30 Notes to the consolidated financial statements

ANNUAL REPORT & ACCOUNTS 2011

OPERATIONAL HIGHLIGHTS

DROUJBA

Drilling has significantly increased size and depth extension

of kimberlite pipe

Significant tonnage potential and remains open at below 400m depth

Processing plant being established on site for bulk sampling

Maiden resource statement expected Q1-2012

TONGO

Bulk sampling yielded grade of 101cpht

High quality diamonds, parcel of 949 carats valued at $185 per carat

Resource drilling commenced

Maiden resource statement expected Q1-2012

PRODUCTION

42,000 carats produced from Mandala

1,000 carats produced from Bomboko

Bomboko closed and plant relocated to Droujba for resource

estimation

FINANCIAL

$10 million equity financing in March 2011

Stellar fully funded to complete resource estimation work on

Droujba and Tongo

Debt free

DROUJBARESOURCEestimation in progress

TONGORESOURCEestimation in progress

$10 MILLIONraised in March 2011 - fully funded

43,000 CARATSproduced in financial year

$1.5 MILLIONrevenue in financial year

HIGHLIGHTS

01

OVERVIEW

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

02

OVERVIEW

SIGNIFICANT DIAMOND RESOURCE ESTIMATESBEING ESTABLISHED

DROUJBA

Location: GuineaStatus: Resource estimation

Drilling has revealed the Droujbakimberlite pipe to be over three times theoriginal size estimate at 3-hectares andthe pipe remains open at depth below thedeepest intersection (to date) of 400m.Independent geological modellingestimates that the Droujba pipe hassignificant tonnage potential with over 15million tonnes so far drilled out to a depthof 350m (not yet a compliant resourcestatement). Historical mining indicates thatthe pipe is high grade (over 100cpht) andStellar is currently establishing a DMSprocessing plant on site and willcommence bulk sampling as part of the resource estimation programme.

TONGO

Location: Sierra LeoneStatus: Resource estimation

A 1,600 tonne bulk sample of the 2.5kmlong Dyke 1 kimberlite has been processedand yielded an average grade of 101cpht.A parcel of 948 carats exported toAntwerp was valued at an average of $185per carat per carat. This would suggestthat the in-situ value for the Dyke 1kimberlite approaching $200 per tonne.The kimberlite is currently being drilledout to over 200m in depth and furtherbulk samples are in the process of beingcollected and processed as part of themaiden resource estimate programme.

MANDALA

Location: GuineaStatus: Production

Mining of the established diamondresource has continued with productionnow exceeding 128,000 carats sincemining commenced in April 2009.Production for the current financial yearwas 42,000 carats at an average grade of23cpht. More recently however, gradesrunning consistently over 50cpht havebeen achieved as a new and previouslyinaccessible mining area was opened up.

Stellar has an advanced portfolio of diamondassets in Guinea and Sierra Leone, in the heartof the renowned diamond area of the ManCraton. These projects are the culmination of ten years of exploration, discovery anddevelopment in a region that still remainsvastly under-explored for diamonds.

The strategy of the Company is currently focussed ongenerating substantial diamond resources in the Droujbakimberlite pipe and Tongo kimberlite dyke swarm throughdetailed drilling and large scale bulk sampling. A significantamount of work has already been completed and maidenresource statements are expected in the first quarter of 2012.CAE Mining has been appointed as the independentconsultant and competent person to verify, establish, and sign off on the resource statements.

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

03

KONO

Location: Sierra LeoneStatus: Trial mining (care and maintenance)

Trial mining at Kono has yet to re-commence. However the Company hasconducted further surface exploration andis in the process of collecting andprocessing a 300 tonne bulk sample fromthe Lion-5 kimberlite dyke which, fromprevious work undertaken by Stellar, has a grade of around 100cpht and highdiamond quality.

BOURO

Location: GuineaStatus: Bulk sampling

Previous work by De Beers andmicrodiamond analysis by Stellar suggestsa grade of over 400cpht for the 5km longBouro North dyke, however bulk samplingby Stellar from one centrally located sitehas returned an initial grade of 243cpht.The 550 carats produced are in Antwerpawaiting sale.

BOMBOKO

Location: GuineaStatus: Project closed

Trial mining at Bomboko was completed in early 2011 with disappointing results.Although the diamond value achieved wasin excess of $200 per carat the low graderendered the project uneconomic toadvance the project to full scale mining.The processing plant has recently beenrelocated to Droujba where it will processkimberlite as part of the resourceestimation programme.

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

04

Drilling at Droujba has rewarded us with a larger kimberlite than originallyenvisaged and independent geologicalmodelling of the pipe has demonstratedthat amulti-million tonne resource isevident. Considering that historicalmining of the pipe in the 1960’s yieldedhigh grades of over 100cpht, this isparticularly encouraging and reinforcesour belief that in Droujba we potentiallyhave an economic resource on our hands.

At Tongo we have continued to reportexciting bulk sampling grades comfortablyin excess of 100cpht with high diamondvalues evident. Drilling is now continuingto define the resource in the ground,which we hope to be sufficient for apositive economic scoping study once the resource has been confirmed.

Although we have continued to producediamonds at Mandala, we took thestrategic decision to cease trial mining atBomboko as the grades were insufficientto prove sustainably economic. Thisenabled us to relocate the many physicalassets and experienced personnel toDroujba where we are now in the processof establishing a fully functional DMSprocessing plant to undertake bulksampling of the Droujba pipe over thecoming months.

In March this year Stellar completed a $9.9 million (£6.2 million) equity financing,which at the time was heavilyoversubscribed. These funds have givenStellar the necessary financial means ofachieving its objective in delivering themaiden resource estimates for Tongo andDroujba as well as progressing our otherhigh interest kimberlite projects at Kono and Bouro.

For the year ended 30 June 2011, theGroup incurred an operating loss beforeinterest and tax of $6.25m (2010: $5.40m)before an impairment charge of $8.6million (2010: nil). The operating loss is inline with the Board’s expectations giventhe Group’s stage of development. Theimpairment charge is an accounting itemresulting from the Board’s decision to ceasemining at Bomboko and the reducedestimate of commercially minableresource at Mandala. At the balance sheetdate, the Group had net assets of $21.1million, including cash and cashequivalents of $6.5 million, and no debt.

CHAIRMAN’SSTATEMENT

Dear Shareholder,The past year has been a successful one for your company in that we have moved closer to our stated objective ofdeclaring significant diamond resources on our kimberliteassets. Considerable work has been completed and we areon track to deliver maiden resource estimates on Droujbaand Tongo during the first quarter of 2012.

OVERVIEW

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

05

The diamond market has been very strongfor most of the year with many companiesreporting record prices for roughdiamonds. Whilst the longer term pricingoutlook remains very bullish, the recenteconomic volatility and worries aboutsovereign and bank debt have resulted in a retracement of rough and polisheddiamond prices from these record highs.However, there is still very strong diamonddemand in India and China which are themain growth areas and we expect this tocontinue. Therefore, we still believe thatalthough there will be periods of priceweakness, as currently being experienced,the longer term trend for diamond priceswill be upwards driven by strong consumerdemand and lack of new production.

Your Company continues to strive todeliver on its strategic objectives and themanagement and team on the groundhave achieved considerable success. I would personally like to thank everyonein the Stellar team for their dedication and hard work this past twelve months.With the continued support of the Boardand the shareholders I am certain that theywill realise further success and that we willbe able to announce positive resourcestatements in early 2012.

Finally I would like once again to thankshareholders for their continued support.In a market environment such as this werealise that your support can bechallenged when there is so muchvolatility and a loss of value. However, we believe that the quality of our diamondportfolio will ultimately unlock significantvalue and I can confirm that we are well on the way to achieving that.

The current year will therefore be pivotalfor Stellar as we announce what we hopeto be significant resources on Droujba andTongo and then take these projects to thenext level of development and hopefullyinto future production.

PETER DARESBURYNON-EXECUTIVE CHAIRMAN

Chairman Peter Daresbury and COO Rowan Carr

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

06

BUSINESS REVIEW

CEO’SSTATEMENT

As planned, Stellar has rapidly advanced work on the Droujba and Tongo kimberlite projects and in the processhas generated exceptional results. We are on track to delivermaiden resource statements on both projects in the firstquarter of 2012 and we expect that these will provide thecatalyst for significant value accretion.

Our strategic focus this past financial yearhas been on drilling and bulk sampling toestablish diamond content and value forour key kimberlite projects of Droujba, insoutheast Guinea and Tongo, in easternSierra Leone. We have achieved consider-able success on both these projects.

We have recently appointed CAE Mining toverify our past work and oversee theprogrammes going forward and in Dr.Matthew Field we have retained the skillsof one of the most renowned kimberliteresource geologists in the world toindependently sign off the resourcestatements as Competent Person.

At Droujba the model of the pipe, asreported by the Russian Aid Mission duringtheir mining in the 1960’s, suggested aresource body of less than 1 hectare insize which tapered out at a mere 20mbelow surface, the depth to which theRussians mined the pipe before exitingGuinea. We were never convinced of thisand our work has thoroughly disprovedthis theory. In fact we have far exceededexpectations and have proven thekimberlite to be three hectares in size onsurface. The pipe has so far been drilled toa depth of 388m below surface and itcertainly continues beyond that.

Independent geological modelling hasdefined 15 million tonnes of hypabyssaland kimberlite breccia in the Droujba pipeto a depth of 350m and we have everyintention of significantly increasing thisand converting it into a JORC compliantresource by early 2012. This will require usto bulk sample the pipe and recover astatistically representative diamond parcelfrom the pipe for grade and valuationestimation. We are currently in the processof building a modern DMS sampling planton site and should commence bulksampling towards the end of 2011.

At Tongo we have been bulk sampling the2.5km long Dyke 1 which has consistentlyyielded average diamond grades of over100cpht. Two parcels totalling almost 949carats have been exported to Antwerp andvalued at an average price of $185 percarat. At these grades and values we aredealing with kimberlite ore that ispotentially valued at upto $200 per tonne,which would make it one of the highestvalue kimberlite ores worldwide.

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

07

Two drill rigs are now active at Tongo todrill out resource tonnes and bulksampling will continue so that we canestablish an initial resource estimate by thefirst quarter of 2012.

We believe that independent resourceestimates for Droujba and Tongo mayresult in a re-rating for Stellar andrecognition for the significant value wewill have created in the project. CAEMining will independently sign off on bothresources and will also undertake pre liminary economic scoping studies.This will form the basis of motivation forfuture work which would be to take bothprojects to the next level of resourcedevelopment and we hope eventually intocommercial production.

Concurrent with this work we havecontinued to mine at Mandala whereproduction has now exceeded 128,000carats sold at over $4 million. Productionwas erratic earlier in the year as adverseweather conditions forced mining intolower grade areas, but over the past fewmonths we have accessed the N’KeliyaniRiver resource area where average gradesof over 1 carat per cubic metre (55cpht)are being experienced. We will continue to mine this area as long as it remainsmodestly profitable.

Unfortunately our evaluation and trialmining at Bomboko was not successful.Although very well executed by ourgeological teams, the recovered gradeswere just too small to prove economic,even with a realised diamond value inexcess of $200 per carat. However, thisgave us the opportunity to re-allocate thesignificant amount of capital, plant,earthmoving equipment, campinfrastructure etc, to Droujba whichsignificantly reduced the capitalrequirement on that project. Oncerehabilitation of the Bomboko mined areasis completed the Company will return thelicences to the Government of Guinea.

We have also managed to undertake someexploration work on Bouro and Konothough this has not been significant.However, bulk sampling of Bouro wassuccessfully completed on one site where550 carats were produced giving a highdiamond grade of 243cpht for the 5kmlong Bouro North Dyke. At Kono,preparations have been made to collect a300 tonne bulk sample of the Lion-5 Dykewhich previously yielded excellent qualitydiamonds and a high grade from twosmall one tonne samples.

The acceleration of the work programmeswas made possible by a £6.2 millionfinancing in March and I would like tothank all shareholders for their support inthis successful fund raise. Current marketconditions remain volatile and uncertain,but Stellar has the necessary financialmeans to complete the resourceestimation work at Droujba and Tongo. Asfurther development of assets is warrantedon the basis of positive resource statementsand economic scoping studies, Stellar willrequire additional funding. However, thiswould be a very positive outcome and willessentially mean that there is clear eco-nomic potential at Droujba and/or Tongo.

The macro-outlook for the diamondsector remains very bullish as dwindlingsupplies and increased consumer demand,particularly from China and India, drivemarket forces. There will be times of priceweakness, as we are currentlyexperiencing, but Stellar takes a longerterm strategic view that the supply anddemand fundamentals remain in favour ofhigher diamond prices and consequentlydiamond producers.

Our strategy therefore remainsunchanged. Stellar intends to become a significant diamond producer within five years.

There are clearly inherent risks of doingbusiness in West Africa, such as a revisedmining code in Guinea, continued calls forresource nationalisation in some parts ofAfrica and the general logistical challengesthat present themselves on the ground.However, we believe that the quality ofour assets presently outweighs these ris ksand there is great opportunity in bothSierra Leone and Guinea. Stellar has beenat the forefront of diamond explorationand development in both these countriesfor a number of years and now it is clearthat this early risk taking is reaping therewards it deserves.

Your Stellar team has once again shownconsiderable dedication and resilience inadvancing its projects diligently,professionally and safely. Driven by theunending enthusiasm of COO RowanCarr, and with the support of the Boardand shareholders alike, I feel comfortablethat we will be able to deliver on ourstrategy to the benefit of all stakeholders.

My sincere thanks once againare extended to everyoneassociated with Stellar and I look forward to being able toreport on further success asthe current year progresses.

KARL SMITHSONCHIEF EXECUTIVE OFFICER

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Chairman and CEO onsite at Kono

Management team in front of Droujba pit

DIAMOND MARKETOUTLOOK

08

BUSINESS REVIEW

The outlook for the rough and polisheddiamond markets remains extremelyrobust. Rough prices have returned to, orare now exceeding the pre-crisis levels of2008 with all major producers reportingrecord prices and gains in the first half of2011 of up to 50%. However, in Augustand September the market correctedsomewhat, mainly as a consequence ofbuyer resistance to elevated rough pricesand economic worries resurfacing. Thesector sees this correction as overdue and prices going forward are expected to stabilise with the rest of 2011 and 2012unlikely to repeat the gains of thepreceding 18 months.

In the longer term, however, the diamondmarket is still forecast to have a significantsupply deficit. Although annual productionincreased slightly in 2010 to 133 millioncarats and RBC Capital Markets forecastthis to increase to 140 million carats asnew production comes on line, this is stillwell below the peak of 160 million caratsseen earlier in the decade. With existingmines becoming depleted or goingunderground annual diamond productionis expected to flat line or reduce over thenext decade as the additional supply fromnew producing mines in Canada, Russiaand to a lesser extent Africa is notsufficient to meet the growing demand.

Although the United States is still thelargest consumer of polished diamonds at 35% to 40%, the main growth areas areChina and India, which together areforecast to account for 50% of the growthdemand over the next five to ten years. The middle class of these burgeoningeconomies is set to double over the nextfive years and De Beers indicate thatChinese and Indian diamond consumptionwill equal that of the United States by2015. With such strong consumptiongrowth De Beers further forecasts that thediamond industry as a whole needs todouble annual supply to meet this demand,something that is very unlikely to happen.

With the supply deficit notional value setto reach $1billion by 2022, as forecast byRBC Capital Markets, driven by strongconsumer growth, depleting resourcesand no new discoveries due to lack of exploration, the outlook for diamondsas a commodity remains very healthy.There will be periods of diamond priceconsolidation or even retracement in theshorter term, particularly as the worldeconomy remains volatile, however thelonger term outlook on pricing remainsvery bullish and companies in productionare positioned to significantly benefit frominevitable price appreciation.

Angola

Australia

Botswana

Canada

DRC

Namibia

Russia

South Africa

Zimbabwe

Other Countries

200

180

160

140

120

100

80

60

40

20

2005A 2006A 2007A 2008A 2009A 2010A 2011E 2012E 2013E 2014E 2015E 2016E 2017E

Million carats

Supply

Demand

National shortage

60,000

50,000

40,000

30,000

20,000

10,000

2008E 2010E2009E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

$Million

Source: All figuresRBC Capital Markets estimates (includes Russia stockpile in supply)

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

World Diamond Production

Diamond Supply and Demand

09

BUSINESS REVIEW

CORPORATE SOCIALRESPONSIBILITY

MANDALA MINING AND PROCESSINGStellar remains a strong supporter of communities within theareas of its operations. It is often difficult to manage localexpectations when there is a limited exploration budget, howevera number of initiatives have been completed in the year that havehad a direct benefit to the local populace. STAFFThe Company still has a strong policy of local recruitment asmuch as possible. The reliance on expatriate skills, althoughnecessary, is not at the detriment of developing local skills in theworkforce. Out of a total workforce of 299 only 12 are expatriate.There has also been significant transfer of skills during this periodrelated to operation of processing plants, rock drilling and blasting.

ROAD AND BRIDGE CONSTRUCTIONStellar continues to believe that one of the most effective ways of local upliftment is by improving the transport network andinfrastructure. New and existing roads covering a distance of180km in length have been both built or maintained in all projectareas. This opens up the interior of the country to commerce and general accessibility in areas often too remote or difficult to previously reach.

COMMUNITY DEVELOPMENT AGREEMENTSIn Sierra Leone Stellar has signed up to a communitydevelopment agreement with the Lower Bambara Chiefdomwhere annual fees are paid towards a number of localdevelopment initiatives as decided upon by an executivecommittee of the forum.

SIERRA LEONE INDEPENDENCE CELEBRATIONSThis year saw the 50 year independence celebrations in SierraLeone. Stellar chose to mark this important occasion bysponsoring two large festivals in both the Kono and Tongocommunities where large swathes of the community enjoyed thehospitality provided. This proved particularly popular with everyone.

20 40 60 80 100 120

Nationals

Expatriates

Droujba

Mandala

Bomboko

Tongo

Kono

Conakry

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Tongo project manager Graham Radburnd and local community Road rehabilitation in Guinea

Staff Numbers

10

BUSINESS REVIEW

DROUJBA

Drilling of the Droujba kimberlite hasdelineated the pipe at three times the originallyreported surface area and made intersections atdepths of up to 400m, with the pipe still remainingopen at depth. The kimberlite has considerabletonnage potential and based on previouslyreported mining grades of over 100cpht asignificant carat resource is in the making.

LOCATION AND HISTORYThe Droujba kimberlite pipe is located some 60kms to the southeast of the Mandala mine in the diamond rich area of Bounundou.It was discovered in the early 1960’s by the Russian Aid Missionwhich delineated the pipe at 1 hectare in size. The Russians minedthe pipe down to a depth of 20m before the kimberlite becametoo hard to mine and process. Diamond grades around 100cpht,and in some samples as high as 200cpht, are reported.

Since the Russians abandoned Guinea in 1964 the Droujba pipehas remained unexploited and the old mine pit to 20m hasremained flooded. Diamond mining activity in the vicinity of thepipe has been restricted to alluvial mining by local artisanal minersand a 270-carat stone is reported to have been discovered in thealluvial gravels near to the pipe.

DRILL PROGRAMMECore drilling commenced in November 2010 with an initial3,000m drill programme aimed at delineating the pipe to 120mdepth. This programme was extended to 10,000m based on the very encouraging intersections achieved which basicallyconfirmed the pipe to have a surface area of 3 hectares and a vertical continuity to 400m and beyond.

By the end of August some 6,424m had been drilled from 33holes. Most of these holes were focussed on drilling of theDroujba pipe (5,391m), however, some holes were drilled into theKatcha kimberlite dyke that runs in proximity to the pipe (1,033m).

These holes drilled into Droujba were primarily located on theedge of the flooded pit and drilled at varying angles in order to intersect the kimberlite pipe at various depths. The deepestintersection made to date is 383m vertically below surface and the pipe remains open at depth.

The drilling to the end of 2011 will focus on more accuratedelineation of the pipe at between the 250m and 400m depthlevels in order that a robust geological model, with accuratelydetermined volumes and tonnages, can be determined as part of the initial resource estimation programme.

GEOLOGICAL MODELThe detailed logging andinterpretation of the drill core from Droujba has ledto the identification of threemain geological units, beingone hypabyssal and twobreccia units.

The core of the pipe iscomprised of two vents ofhypabyssal kimberlite thatare separated near to surfaceby a short distance but whichcoalesce at depth. One ofthese hypabyssal vents didnot break through to surface,whereas the other vent didand became the pipe thatwas mined in the 1960’s to adepth of 20m from surface.

The core of hypabyssal kimberlite is surrounded close to its contactwith country rock granite by two brecciated units that are potentiallyvolumetrically significant. The difference between these respectivebreccias is based on the percentage of kimberlite in the matrix.

Based on the country rock dilution it is clear that the diamondgrade of the breccia will be lower than that of the hypabyssalkimberlite which was previously mined. This has been confirmedfrom the microdiamond analysis so far undertaken, and theplanned bulk sampling from the base of the old mined out pit will independently test the units for diamond grade and quality.

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

Droujba Kimberlite

3D Model of Droujba pipe

11

FUTURE WORKThe drilling and bulk sampling will continue into Q1-12 when theresource estimate will be calculated and published. This will befollowed by a preliminary economic scoping study which will lookat various economic scenarios and valuations on the basis of theresource generated. Should the results prove encouraging theDroujba pipe will be subjected to large diameter drilling (17-inch) todepth in order to convert the inferred resource to indicated status.

MICRODIAMOND ANALYSISSome five separate samples have been analysed for microdiamond content at the Saskatchewan Research Council Laboratory inCanada. These samples were collected on the basis of their geology and separated into hypabyssal and kimberlite breccia samples. It is clear from the table that the diamond content of the hypabyssal kimberlite is significantly higher than the breccia. The diamondcounts for all samples are considered highly encouraging and consistent with the reported high grade of the kimberlite pipe.

BULK SAMPLING PROGRAMMEA processing plant is currently being established at the Droujba kimberlite site through which representative bulk samples will beprocessed in order to determine the individual diamond grade and values for the hypabyssal and kimberlite breccia units. The plant is comprised of a 5 ton per hour DMS unit with diamond recovery by X-Ray Flowsort and grease table back up. The front end crushingcircuit is being manufactured in South Africa and should be on site in late October. Processing of the bulk samples is expected tocommence in November and the results will be available in the first quarter of 2012.

RESOURCE ESTIMATEThe objective of the drilling and bulk sampling is to compile a maiden resource estimate to JORC (or equivalent) standards by the end of Q1-12. CAE Mining has been appointed as independent consultants and Dr. Matthew Field, a world renowned kimberlite resourcegeologist, has been appointed as the competent person overseeing the programme and signing off on the resource. The initial resourceestimate will be mainly of an inferred nature to 350m depth, though some of the resource will qualify for an indicated category.

Preliminary volume and tonnage estimations have been undertaken on the basis of the geological model to a depth of 350m below the surface. Whilst these are not yet classified as resources the indication is that to a depth of 350m there is approximately 5.2 milliontonnes of hypabyssal kimberlite and 9.9 million tonnes of diamondiferous kimberlite breccia. Clearly the kimberlite does extend beyondthe 350m depth and this further demonstrates the significant tonnage potential of the Droujba kimberlite pipe.

DROUJBA TONNAGE MODEL TO 350M BELOW SURFACE

Sample Number Kimberlite FaciesSampleWeight (kg)

+0.075+0.106-0.150

+0.150-0.212

+0.212-0.300

+0.300-0.425

+0.425-0.600

+0.600-0.850

+0.850-1.180

+1.180-1.700

+1.700-2.360

+2.360-3.350

Total Diamonds

Carats+0.85

GN04-2010-02 Hypabyssal 196.72 178 135 69 53 36 7 9 1 2 0 0 490 0.0647

GN04-2011-01 Hypabyssal 67.6 37 33 17 14 7 6 2 0 0 0 0 116 0

GN04-2010-02 Hypabyssal 136.55 115 110 49 40 19 8 2 2 0 1 0 346 0.1401

Totals 400.87 330 278 135 107 62 21 13 3 2 1 0 952 0.2048

Sample Number Kimberlite FaciesSampleWeight (kg)

+0.075+0.106-0.150

+0.150-0.212

+0.212-0.300

+0.300-0.425

+0.425-0.600

+0.600-0.850

+0.850-1.180

+1.180-1.700

+1.700-2.360

+2.360-3.350

Total Diamonds

Carats+0.85

GN04-2010-03 Kimberlite Breccia 94.54 10 14 9 7 3 2 1 1 0 0 1 48 0.1940

GN04-2011-03 Kimberlite Breccia 268.24 14 8 13 5 7 5 0 0 0 0 0 52 0

Totals 362.78 24 22 22 12 10 7 1 1 0 0 1 100 0.1940

Depth fromSurface

Kimberlite Breccia (t)

Hypabssal Kimberlite (t) Total Tonnes

0-50m 1,907,972 583,181 2,491,153

50-100m 1,552,953 694,360 2,247,313

100-150m 1,312,824 763,172 2,075,996

150-200m 1,400,907 698,234 2,099,141

200-250m 1,580,197 819,124 2,399,321

250-300m 1,070,681 913,176 1,983,857

300-350m 1,101,430 761,114 1,862,544

Total Tonnage 9,926,964 5,232,361 15,159,325

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Drilling at Droujba

DROUJBA KIMBERLITE TONNAGE CALCULATIONS

Note: Determined from Datamine Geological Model, not yet JORC complient

NUMBER OF DIAMONDS ACCORDING TO SIEVE SIZE FRACTION (mm)

NUMBER OF DIAMONDS ACCORDING TO SIEVE SIZE FRACTION (mm)

12

BUSINESS REVIEW

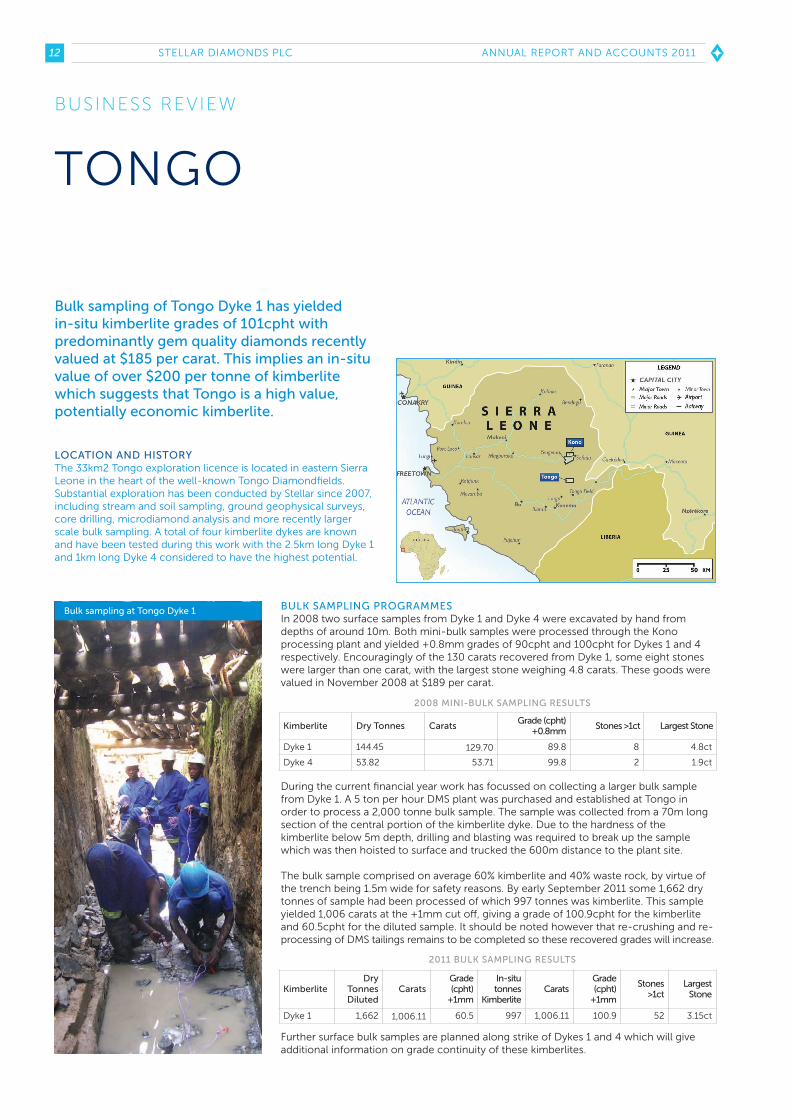

TONGO

Bulk sampling of Tongo Dyke 1 has yielded in-situ kimberlite grades of 101cpht withpredominantly gem quality diamonds recentlyvalued at $185 per carat. This implies an in-situvalue of over $200 per tonne of kimberlitewhich suggests that Tongo is a high value,potentially economic kimberlite.

BULK SAMPLING PROGRAMMESIn 2008 two surface samples from Dyke 1 and Dyke 4 were excavated by hand fromdepths of around 10m. Both mini-bulk samples were processed through the Konoprocessing plant and yielded +0.8mm grades of 90cpht and 100cpht for Dykes 1 and 4respectively. Encouragingly of the 130 carats recovered from Dyke 1, some eight stoneswere larger than one carat, with the largest stone weighing 4.8 carats. These goods werevalued in November 2008 at $189 per carat.

During the current financial year work has focussed on collecting a larger bulk samplefrom Dyke 1. A 5 ton per hour DMS plant was purchased and established at Tongo inorder to process a 2,000 tonne bulk sample. The sample was collected from a 70m longsection of the central portion of the kimberlite dyke. Due to the hardness of thekimberlite below 5m depth, drilling and blasting was required to break up the samplewhich was then hoisted to surface and trucked the 600m distance to the plant site.

The bulk sample comprised on average 60% kimberlite and 40% waste rock, by virtue ofthe trench being 1.5m wide for safety reasons. By early September 2011 some 1,662 drytonnes of sample had been processed of which 997 tonnes was kimberlite. This sampleyielded 1,006 carats at the +1mm cut off, giving a grade of 100.9cpht for the kimberliteand 60.5cpht for the diluted sample. It should be noted however that re-crushing and re-processing of DMS tailings remains to be completed so these recovered grades will increase.

Further surface bulk samples are planned along strike of Dykes 1 and 4 which will giveadditional information on grade continuity of these kimberlites.

LOCATION AND HISTORYThe 33km2 Tongo exploration licence is located in eastern SierraLeone in the heart of the well-known Tongo Diamondfields.Substantial exploration has been conducted by Stellar since 2007,including stream and soil sampling, ground geophysical surveys,core drilling, microdiamond analysis and more recently largerscale bulk sampling. A total of four kimberlite dykes are knownand have been tested during this work with the 2.5km long Dyke 1and 1km long Dyke 4 considered to have the highest potential.

ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

Kimberlite Dry Tonnes CaratsGrade (cpht)

+0.8mmStones >1ct Largest Stone

Dyke 1 144.45 129.70 89.8 8 4.8ct

Dyke 4 53.82 53.71 99.8 2 1.9ct

KimberliteDry

TonnesDiluted

Carats Grade(cpht)

+1mm

In-situtonnes

KimberliteCarats

Grade(cpht)

+1mm

Stones >1ct

LargestStone

Dyke 1 1,662 1,006.11 60.5 997 1,006.11 100.9 52 3.15ct

Bulk sampling at Tongo Dyke 1

2008 MINI-BULK SAMPLING RESULTS

2011 BULK SAMPLING RESULTS

13

DIAMOND VALUATIONTwo diamond parcels comprising some948 carats have been exported to Antwerpfor valuation. The first parcel of 638.74carats was valued at $191 per carat inAugust 2011. However, the second parcelof 309.94 carats realised a lower value of$176 per carat in September due to marketweakness as a consequence of worldwideeconomic concerns. The overall averagevalue for the 949 carats exported wastherefore $186.10 per carat.

The Tongo diamonds are primarily of gemquality with a large percentage of crystalsand sawable goods which drives apremium on price. It is important to notethat the exports valued to date did notcontain any “special” stones and thereforethe Company considers this value to be arun of mine which can be considerablyenhanced by the presence of larger stonesin a production scenario.

CORE DRILLINGTwo rigs are currently active on the Tongoproject. An initial 6,000m to 10,000mprogramme is planned to drill outresources on Dykes 1 and 4 to a minimumof 200m depth. The drilling commenced inAugust and by early Setember some eightholes totalling 506m had been drilled. At each collar position, three holes atvarying angles are being drilled so thatintersections of the kimberlite can bemade at approximately 50m, 100m and200m vertical depth from surface.

The drill core is logged and holes surveyedfor any apparent deviation. This data iscompiled into Datamine and modelled aspart of the resource estimation exercise.

Selections of samples will be consigned forpetrographic and microdiamond analysisso that geological continuity and hencediamond grade continuity can be inferredacross the resource.

RESOURCE ESTIMATECAE Mining has been appointed asindependent consultant, with Dr. MatthewField as competent person to establishmaiden diamond resource estimates forthe Tongo project. All previous work will be verified and the future work monitoredto best international standards by theconsultants. The objective is to establishan initial inferred resource to 200m depthand be independently signed off by theConsultants during the first quarter of2012. Simultaneously, CAE Mining willdeliver a preliminary economic scopingstudy on Tongo with a range of economicscenarios and valuations.

FUTURE WORKThe next six months will see an aggressivedrilling and bulk sampling programme onthe Dyke 1 and Dyke 4 bodies. This willyield the required information on resourcetonnage, diamond grade and diamondvalue for these kimberlites on which thebase the resource estimation. The programme is on track to becompleted during Q1-12.

Subject to positive economic scopingstudies shaft sinking will commence onDyke 1 and 4 with a view to commencingunderground trial stope mining andfeasibility studies in the latter part of 2012and into 2013.

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Date Carats Valuation US $

Export-1 Jun-11 638.74 $191.11/ct

Export-2 Aug-11 309.94 $176.10/ct

Total 948.68 $186.10/ct

Tongo 5tph DMS processing plant

Tongo diamonds

TONGO DIAMOND VALUATIONS

14

BUSINESS REVIEW

MANDALA

Mining at Mandala continued with the production of a further41,723 carats of diamonds in the period. This brings the totalproduction at Mandala since mining commenced in April 2009to 128,000 carats with a realised gross revenue of $4 million.

MANDALA MINING AND PROCESSINGThe Mandala mining licence covers anarea of 14km2 in the Macenta andKerouane districts of south east of Guinea.Production commenced in late April 2009after a 100tph DMS processing plant wasconstructed and a 60km stretch of roadfully rehabilitated. The diamonds beingmined are hosted in unconsolidatedgravels that are overlain by some 4m to5m of sandy overburden. The miningprocedure is simple, with the barren sandbeing stripped and the diamond bearinggravel extracted by CAT and Volvoexcavators. The gravel is then loaded ontohaul trucks and carried to the processingplant where it is stockpiled.

The processing is carried out through a100 ton per hour dense media separationplant (DMS) which has a 1.8mm bottomcut off. After the material has been fed tothe plant and passed through the scrubberand prep-screens the +1.8mm to -25mmsize fraction goes into the DMS, with threeconcentrate fractions being passed to theX-Ray flow sort for diamond recovery.The Flowsort tailings are also passed overgrease to scavenge any diamonds missedby the first pass.

Diamond recovery is done under strictsecurity conditions, with a Governmentmines monitor being present at all times.The diamonds are classified, weighed andplaced in a safe until exported to Conakryfor valuation before royalties are paid andthe Kimberley Process Certificate issuedprior to final export to Antwerp for sale.

ANNUAL REPORT AND ACCOUNTS 2011

Night mining at MandalaLamine Thiam grading Mandala diamondsMandala diamond

Senior Geologist Abdulaye Diallo at Mandala

STELLAR DIAMONDS PLC

MANDALA PRODUCTIONAlthough processing of gravel increased in the 2011 financial year(185,380t) compared to 2010 (179,747t) carat production waslower at 41,727cts versus 2010 (63,721cts) due to a prolongedrainy season which flooded the river valley where the mainMandala resource is located. As a consequence mining wasforced to higher terrace areas where recovered grades werelower, at an average of 22.5cpht compared 2010 grades of 35cpht.

Towards the end of the financial year, however the Companymade the decision to open up access to the N’Keliyani River areawhich is a tributary to the main Mandala River channel. Historicalexploration had indicated that this area yielded high diamondgrades and due to the thick overburden was relatively intact fromlocal artisanal diggings.

Mining subsequently confirmed higher grades and this area thenbecame the focus of activity, with grades consistently over50cpht, and sometimes over 100cpht, being recorded. For themonths of July and August some 3,429 carats were yielded from6,758 tonnes of gravel for a grade of just under 51cpht.

Mining ceased in mid-August for the height of the rainy seasonand is scheduled to resume in October. This area of the N’Keliyaniwill be the focus of mining over the coming months and willcontinue as long as it remains profitable.

MANDALA DIAMOND SALESDiamond sales for the financial year of 2011 were lower than 2010at $1.6million on the basis of fewer carats being produced.Although the average price per carat was similar over the past twoyears this does not truly reflect the appreciation in prices in thelatter part of Q2-11 where there was a significant increase inprices realised.

The Mandala goods are generally of low average quality,comprising approximately 80% industrial diamonds. However, the N’Keliyani goods are noticeably better when compared to theMandala goods and going forward, assuming consistent marketconditions, there should be an increase in the average price realised.

OUTLOOK FOR MANDALABased on the mining of higher grade areas at the N’Keliyaniresource area the Mandala project has returned to modestprofitability. However, close control on costs and efficient mining arecontinually required to ensure the project remains cash flow positive.

Although Mandala is not the key strategic focus, it is felt importantto remain in production as Stellar is the only commercial diamondproducing Company in Guinea. This brings recognition from theGuinean Government and raises the Company profile in a sectorthat is undeveloped and where Stellar is in the process ofhopefully developing a substantial diamond resource at Droujba.

15ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Tonnes Carats Grade (cpht)+1.8mm

2009 FY 37,578 19,115 50.87

2010 FY 179,747 63,721 35.45

2011 FY 185,380 41,723 22.51

2012 FY (Jul-Aug-11) 6,758 3,429 50.74

Total 409,463 127,988 31.26

Carats Sales US$ $ per carat

2009 FY 7,453 203,144 27.26

2010 FY 67,342 2,109,677 31.33

2011 FY* 53,157 1,618,304 30.44

Total 127,952 3,931,125 30.72

Mandala 100tph processing plant

MANDALA PRODUCTION

MANDALA PRODUCTION

Note: * Some diamonds in stock

16

BUSINESS REVIEW

KONO

Work during the period has focussed on surface explorationof high-interest kimberlites that have not previously beensubjected to any significant amount of test work. One suchkimberlite, designated Lion-5, is located in the easternextreme of the licence area and has been mapped over adistance of 5 kilometres.

The Lion-5 kimberlite runs into the adjacent mining licenceheld by Koidu Holdings, which is currently embarking on areported $150m capital development programme on itskimberlite property.

Previous testing of Lion-5 by Stellar, from two small 1,000kgsamples, indicated a diamond grade of around 100cpht withhigh quality diamonds. The Company therefore decided tocollect a 300 ton bulk sample from the kimberlite to ascertainthe diamond grade and value with more confidence.

In recent months Stellar has accessed the kimberlite and hasstripped the overburden, exposing the body over a length of30m at a depth of 4m. The width of the dyke is up to 1.8mand is very hard. The kimberlite will now be drilled and blastedand the ore hauled to the DMS processing plant at Tongo fordiamond recovery.

Based upon the results, further bulk sampling may be targetedor consideration be given to sinking a shaft from whichunderground trial mining can be conducted.

The previous shaft sites at Pol-K and Bardu remain on care andmaintenance and the Company is assessing means of resumingunderground trial mining, which will be subject to eitherfinancing or securing an appropriate joint venture partner.

BOURO

Bulk sampling of the Bouro North dyke was accomplished in the period under review, with an exceptionally high grade of 243cpht being realised.

The kimberlite was firstly mapped in detail along its entire 5kmlength and this revealed a complex series of en-echelondykes that had mostly been exploited by artisanal diggingsover the years. A suitable sample site in the centre of the dykelength was selected for the bulk sample site and over 15m ofoverburden was stripped (the depth to which the local diggershad penetrated).

The kimberlite was then opened up over a 70m length wherethe width varied considerably from closely spaced stringers ofa few centimetres to 70cm over a zone of approximately 2m.As such the sample was heavily diluted and this was taken intoconsideration when calculating the final kimberlite grade.

Detailed measurements of the kimberlite widths along the70m long trench were made and since the kimberlite washeavily decomposed the moisture content was calculated, ineffect giving a wet and dry weight figure for the sample.

Overall a total of 337t (wet) and 233t (dry) of kimberlite wereextracted as the bulk sample. This was trucked the 1kmdistance to the Mandala DMS plant where it was processed.Due to the decomposed nature of the kimberlite no crushingwas required at the plant.

A total of 565.2 carats of diamond were recovered at a+1.8mm cut off, giving an in-situ kimberlite grade of242.7cpht. The largest diamond recovered weighed 3.67carats and the average stone size was 0.15/ct. The diamondsare mainly of industrial quality and the parcel is currently inAntwerp awaiting sale.

A further two bulk samples were selected for excavation, buton the basis of narrow kimberlite width and very thickoverburden these were unsuccessful.

The Company therefore decided to postpone further work onBouro until the diamond parcel was sold in Antwerp and thenmake a decision on the future programme. This may includefurther attempts at bulk sampling and/or drilling.

ANNUAL REPORT AND ACCOUNTS 2011

WetTons

MoistureContent

DryTons

Carats Recovered

Gradecpht

(+1.8mm)

Number Diamonds

AverageStoneSize/ct

LargestStone

337.4 31% 232.8 565.2 242.7 3,767 0.15 3.67ct

Bulk sampling at Lion 5 Dyke

BOURO NORTH BULK SAMPLE

STELLAR DIAMONDS PLC

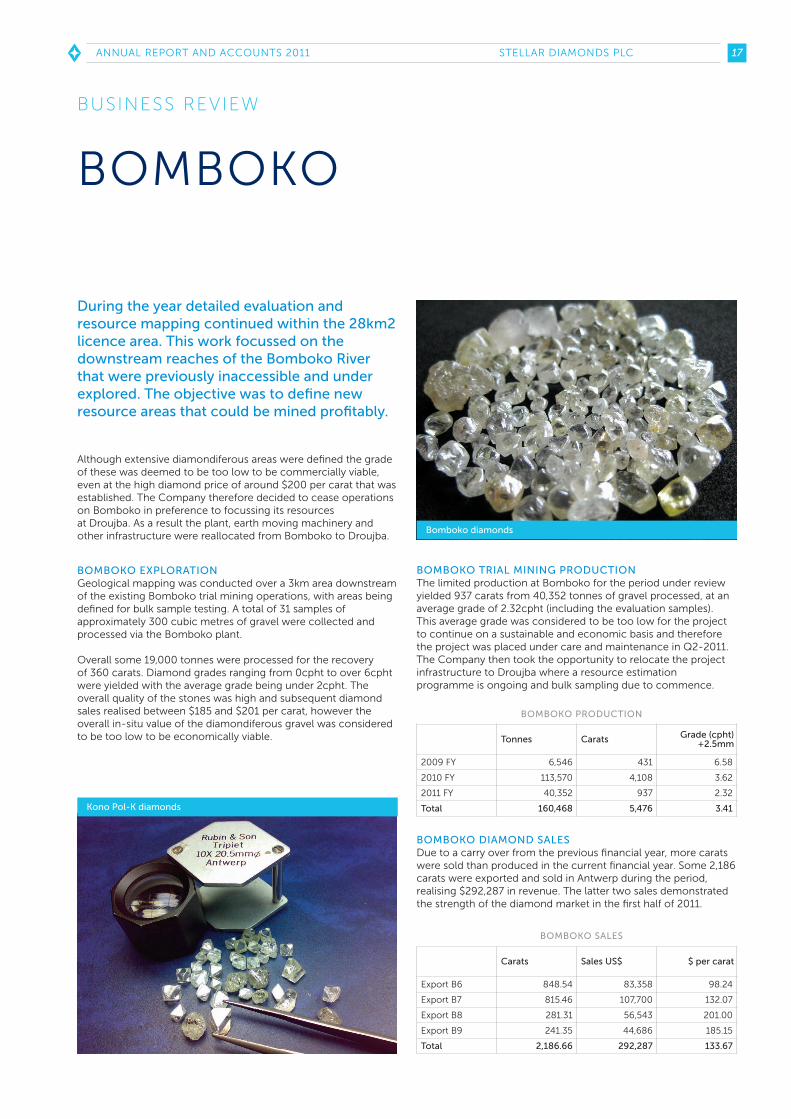

BOMBOKO

17

BUSINESS REVIEW

During the year detailed evaluation andresource mapping continued within the 28km2licence area. This work focussed on thedownstream reaches of the Bomboko Riverthat were previously inaccessible and underexplored. The objective was to define newresource areas that could be mined profitably.

BOMBOKO EXPLORATIONGeological mapping was conducted over a 3km area downstreamof the existing Bomboko trial mining operations, with areas beingdefined for bulk sample testing. A total of 31 samples ofapproximately 300 cubic metres of gravel were collected andprocessed via the Bomboko plant.

Overall some 19,000 tonnes were processed for the recovery of 360 carats. Diamond grades ranging from 0cpht to over 6cphtwere yielded with the average grade being under 2cpht. Theoverall quality of the stones was high and subsequent diamondsales realised between $185 and $201 per carat, however theoverall in-situ value of the diamondiferous gravel was consideredto be too low to be economically viable.

Although extensive diamondiferous areas were defined the gradeof these was deemed to be too low to be commercially viable,even at the high diamond price of around $200 per carat that wasestablished. The Company therefore decided to cease operationson Bomboko in preference to focussing its resources at Droujba. As a result the plant, earth moving machinery andother infrastructure were reallocated from Bomboko to Droujba.

BOMBOKO TRIAL MINING PRODUCTIONThe limited production at Bomboko for the period under reviewyielded 937 carats from 40,352 tonnes of gravel processed, at anaverage grade of 2.32cpht (including the evaluation samples).This average grade was considered to be too low for the projectto continue on a sustainable and economic basis and thereforethe project was placed under care and maintenance in Q2-2011.The Company then took the opportunity to relocate the projectinfrastructure to Droujba where a resource estimationprogramme is ongoing and bulk sampling due to commence.

BOMBOKO DIAMOND SALESDue to a carry over from the previous financial year, more caratswere sold than produced in the current financial year. Some 2,186carats were exported and sold in Antwerp during the period,realising $292,287 in revenue. The latter two sales demonstratedthe strength of the diamond market in the first half of 2011.

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Tonnes Carats Grade (cpht)+2.5mm

2009 FY 6,546 431 6.58

2010 FY 113,570 4,108 3.62

2011 FY 40,352 937 2.32

Total 160,468 5,476 3.41

Carats Sales US$ $ per carat

Export B6 848.54 83,358 98.24

Export B7 815.46 107,700 132.07

Export B8 281.31 56,543 201.00

Export B9 241.35 44,686 185.15

Total 2,186.66 292,287 133.67

Bomboko diamonds

Kono Pol-K diamonds

BOMBOKO PRODUCTION

BOMBOKO SALES

18

GOVERNANCE

BOARD OF DIRECTORS

ANNUAL REPORT AND ACCOUNTS 2011

LORD DARESBURY . NON-EXECUTIVE CHAIRMANPeter Daresbury has held numerous executive positions, including CEO from1997 to 2000 of the Greenalls Group, which had an annual turnover of £983million and a FTSE 100 market capitalisation of £1.7 billion. In 2000, thecompany was re-named The De Vere Group plc, and Peter Daresbury becameNon-Executive Chairman until he stood down in 2006. Peter Daresbury hasalso served as Non-Executive Chairman of Kazakhgold Group Ltd from 2005 to 2007 and Executive Chairman of Highland Gold from 2002 to 2004. Peter is currently Chairman of AIM quoted Nasstar plc, Aintree Racecourse CompanyLtd, Mallett plc and North West Business Finance Ltd, a new Private VentureCapital and Loan Fund (VCLF) for the Northwest.

Current directorships include Bespoke Hotels Ltd, Rusant Ltd and in addition,since 2005, Peter has been a member of the Fleming Family and PartnersPrivate Equity Investment Committee.

KARL SMITHSON . CHIEF EXECUTIVE OFFICERKarl Smithson was appointed as Stellar's Chief Executive Officer with effectfrom 1 January 2007, having built the portfolio of Stellar’s assets within ManoRiver Resources since 2000. He led the listing of Stellar on AIM through areverse takeover of West African Diamonds and has over the years successfullyraised over £15million in equity funding for Stellar.

Karl has 23 years of resource sector experience gained with a number ofcompanies in senior management positions, including De Beers (10 years),SouthernEra Diamonds (2 years) and Mano River/Stellar (11 years). Karl's working career has been focussed on diamond exploration anddevelopment in Africa and he has been responsible for a number of newdiamond discoveries in Botswana, Zimbabwe, Sierra Leone and Liberia. Karl is a geology graduate of Kingston University in the UK. He completed hisMBA with distinction in 2006 at the Graduate School of Business in Cape Town,South Africa and was awarded with the Old Mutual Gold Medal.

STELLAR DIAMONDS PLC

19ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

LUIS DA SILVA . NON-EXECUTIVE DIRECTORLuis is CEO of TSXV/AIM listed Afferro Mining Inc (TSXV/LSE: AFF), an iron ore explorer/developer in Liberia and Cameroon. He gained his extensiveinternational experience with multinationals Lafarge S.A. and Blue CircleIndustries Plc before joining the current Company in 2007. Luis is a graduateMining Engineer from Camborne School of Mines and read for his MBA at theCranfield School of Management. Additionally, Luis serves as a Non-ExecutiveDirector of Aureus Mining Inc. (TSX/LSE: AUE), a gold development company in west Africa born out of the African Aura split in April 2011.

JAMES CAMPBELL . NON-EXECUTIVE DIRECTORJames Campbell is currently Chief Executive Officer and President of RockwellDiamonds Inc. Prior to this he was Vice President - New Business for LucaraDiamond Corp, following Lucara’s acquisition of African Diamonds plc, wherehe was Managing Director for four years.

Preceding this, James was with De Beers for over twenty years, culminating inbeing General Manager responsible for advanced exploration and resourcedelivery in the Global Mining and Exploration group. During his career with DeBeers he also led a number of diamond exploration and evaluation programmesand small-scale mine development as well as being involved in corporate andstrategic management and being Nicky Oppenheimer's Personal Assistant.

James holds a degree in Mining & Exploration Geology from the Royal School ofMines (Imperial College, London University) and an MBA with distinction fromDurham University. James is a Fellow of the Institute of Mining, Metallurgy &Materials, Chartered Engineer (UK), Chartered Scientist (UK), a ProfessionalNatural Scientist (RSA) and a member of the Institute of Directors of South Africa.He is also a director of Bugeco sa, and Swala Resources plc.

STEVEN POULTON . NON-EXECUTIVE DIRECTORSteven Poulton holds an Honours degree in Geology from the University of Southampton (1997) and a Masters degree in Mining Geology from theCamborne School of Mines (1998). He is the Chief Executive and co-founder(2007) of Altus Strategies Ltd, a private natural resource company and adirector of its subsidiaries Altus Capital Ltd (the investment manager of AltusResource Capital Ltd [LSE:ARCL]), Arabian Gold Corporation plc, Aluvance plcand Altau Gold plc. Steven was a co-founder and director of African AuraMining Inc, which in 2011 de-merged its assets to create Aureus Mining Inc[AIM / TSX: AUE] and Afferro Mining Inc [AIM / TSX-V: AFF]. Steven is a fellow of the Geological Society of London and a fellow of the Institute of Materials,Minerals and Mining.

20

KEYMANAGEMENT

ROWAN CARR . CHIEF OPERATIONS OFFICERRowan graduated with a Masters in Mineral Exploration from Imperial College Londonand has 23 years of diamond industry experience throughout Africa. He spent 20 yearsworking for De Beers in senior management positions heading up exploration efforts in Botswana, South Africa, Angola, DR Congo, Guinea and the Central African Republic.Rowan joined Stellar in 2007 and has been at the forefront of project exploration and development on the ground.

PHILIP KNOWLES . FINANCIAL CONTROLLERPhilip joined Stellar in June 2011 as Financial Controller. He is a qualified accountanthaving gained membership to the ACCA in 2004 and holds a BA (Hons) in Accountingand Finance from Exeter University. Philip has over 10 years of accountancy experienceworking for a wide range of businesses while in practice and most recently was GroupFinancial Controller for Firestone Diamonds plc and for Kopane Diamonds plc, prior toFirestone’s takeover of Kopane, and brings with him strong experience of working forgrowing diamond mining companies. Philip is based in our London office but travelsregularly to the company’s assets in Guinea and Sierra Leone.

JOHN PEARTREE . LOGISTICS MANAGER, SIERRA LEONEJohn Peartree joined Stellar Diamonds in July 2011 and brings with him over 17 years of logistics and supply chain management experience. After completing 12 years in theBritish military (Royal Logistics Corps) John spent time in many and varied industriesincluding Banking, Financial Services, Bio Energy, before returning to the Logistics andSupply Chain industry most recently in Ghana and Nigeria, West Africa.

ALKALY YANSANE . COUNTRY REPRESENTATIVE, GUINEAAlkaly Yansane is a Guinean national with a USA university degree in geology. He was the Director of the CPDM in Conakry for a number of years, responsible for many aspects of the mineral sector. Yansane has also worked for 16 years in the private sector of theexploration and mining industry with Rio Tinto, West African Diamonds and now StellarDiamonds, where he holds the position of Company representative in Conakry.

WAYNE LAMBINON . LOGISTICS MANAGER, GUINEAWayne joined Stellar Diamonds in April 2010 as office and logistics manager in Conakry.After a long career in the military, French Foreign Legion as a Paramedic, Wayne hasspent the last eight years in the mining industry as office, logistics and security managerfor Anglo Gold Ashanti, Banro Corporation, Uramin and now Stellar Diamonds. He hasworked in many Africa countries including the DR Congo, Niger, Zambia and Guinea.

ANNUAL REPORT AND ACCOUNTS 2011

GOVERNANCE

STELLAR DIAMONDS PLC

21

KASSIM MANSARAY . SENIOR GEOLOGIST, SIERRA LEONEKassim is a qualified geologist with a Masters from Moscow, Russia. Kassim has over 30years of industrial experience, having started work in the Geological Survey of SierraLeone and working on a number of project evaluations in the country. He brings a vastwealth of multi-commodity experience having worked in Sierra Leone, Liberia, Guinea,Gabon and the Central African Republic, having spent the past 15 years with the ManoRiver-Stellar Diamonds group of companies.

GRAHAM RADBURND . TONGO PROJECT MANAGERGraham’s early career was focused in the civil construction sector in Africa and theMiddle East. He also brings 13 years of diamond industry experience in both productionand management roles in Angola, DR Congo, Russia, Guinea and Sierra Leone. Grahamhas been managing a number of Stellar’s mining and development projects since joiningthe Company in 2008.

FODÉ CAMARA . MANDALA PROJECT MANAGERFodé is a Guinean national with a degree in geology from the University of Conakry. He has 16 years diamond industry experience, 12 of which was with De Beers in seniorpositions in Guinea, South Africa, Botswana, Zimbabwe, Madagascar, Gabon and DRCongo. Fodé joined Stellar in 2008 and is currently project manager at the Mandala mine.

ABDULAYE DIALLO . SENIOR GEOLOGIST, DROUJBA PROJECTAbdulaye is a Guinean national with a degree in mining geology from the University ofBoke. After an early career in construction he joined Mano River Resources as projectgeologist exploring for gold and diamonds in Guinea, Sierra Leone and Liberia. Abdulayecontinued this work with Stellar Diamonds from 2007 and is currently responsible for thedrilling project at Droujba.

SULAIMAN SWARAY . PROJECT GEOLOGIST, TONGO PROJECTSulaiman is a Sierra Leone national with a degree in Geology from Fourah Bay Universityin Freetown. After two years in the National Statistics Office he joined Stellar in 2004 andwas project geologist in a regional diamond exploration joint venture with BHP Billiton.This led to the discovery and development of the Tongo kimberlites where Sulaiman isnow project geologist for the resource estimation programme.

ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

22 ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

DIRECTORS’REPORT

GOVERNANCE

The directors submit their report and the consolidated financial statements for Stellar Diamonds plc. (the “Company” or “Stellar” or on a consolidated basis the “Group”), for the year ended 30 June 2011.

PRINCIPAL ACTIVITIES, BUSINESS REVIEW AND FUTURE DEVELOPMENTSThe principal activity of the Company is that of diamond production and development in West Africa.

No dividends have been paid or are proposed for the period (2010: nil).

A detailed review of the significant developments and operating results of the Group, as well as the business environment, futureprospects and the main trends and factors that are likely to affect the future development, performance and position of the Group’sbusiness are contained in the Chairman’s Statement.

KEY PERFORMANCE INDICATORSGiven the early stage nature of the Group’s kimberlite portfolio, the Directors are of the opinion that analysis using financial KPIs is not appropriate for an understanding of the development, performance or position of the business at this time.

However, the Directors constantly review the planned exploration and evaluation expenditure and general operating costs to ensurethat cash resources are available prior to commitment to this expenditure.

In addition to the above, the Board also considers non-financial factors such as the Group’s compliance with Corporate GovernanceStandards and compliance with environmental, rehabilitation and other legislation within the Group’s areas of operations.

SHARE CAPITALOn 12 October 2010, a total of 38,000,000 ordinary shares of 5p each were allotted and issued for gross proceeds of $3,078,603.

On 29 March 2011, a total of 77,500,000 ordinary shares of 5p each were allotted and issued for gross proceeds of $9,922,891.

GOING CONCERNAs discussed in the Chairman’s Statement, the Company is focusing on advancing its kimberlite projects towards production. In March2011 the Company raised $9.9m (£6.2m) from an equity placing and at the balance sheet date had cash of $6.5m. Given the positiveresults being produced at both Tongo and Droujba and the stage of development of both projects, the directors believe that theCompany will continue to have the ability to access sufficient levels of finance to continue the Group’s projects for the foreseeablefuture. On that basis, the directors continue to adopt the going concern basis in preparing these financial statements.

CHARITABLE AND POLITICAL CONTRIBUTIONSThe Group made no political or charitable contributions during the year.

DIRECTORSDuring the year under review, the following directors held office:

Lord Daresbury Non-Executive ChairmanN. Karl Smithson Chief Executive Officer & Company SecretaryAngus Ogilvie Financial Director & Company Secretary (resigned 30/04/2011)James Campbell Non-Executive DirectorLuis Guilherme Cabrita da Silva Non-Executive DirectorSteven J. Poulton Non-Executive Director

DIRECTORS’ INTERESTSThe directors’ interests in the ordinary shares of the Company as of 30 June 2011 are disclosed in note 17 of the consolidated Financial Statements.

SUBSTANTIAL SHAREHOLDINGSAt 30 September 2011 so far as the Company is aware, the only holdings of 3% or more in the issued share capital are:

SUPPLIER PAYMENT POLICYThe Group’s policy is to settle terms of payment with suppliers when agreeing the terms of each transaction, ensure that suppliers aremade aware of the terms of payment and abide by the terms of payment. Trade creditors of the Group at 30 June 2011 were equivalentto 15 (2010: 17) days purchases.

PROPERTY PLANT AND EQUIPMENTDetails of the Group’s property plant and equipment is set out in Note 9 to the Group Financial Statements.

EMPLOYEE CONSULTATIONThe Group places considerable value on the involvement of its employees and has continued to keep them informed on mattersaffecting them as employees and on the various factors affecting the performance of the Group. This is achieved through formal and informal meetings.

FINANCIAL RISK MANAGEMENTDetails of the Group’s financial risk management policies are set out in Note 18 to the Group Financial Statements.

SUBSEQUENT EVENTSDetails of significant post balance sheet events affecting the Group and Company are set out in Note 19 to the Group FinancialStatements and Note 11 to the Company Financial Statements.

AUDITORSEach of the persons who is a director at the date of approval of this report confirms that:

1) so far as the director is aware, there is no relevant audit information of which the company’s auditors are unaware; and2) the director has taken all the steps that he/she ought to have taken as a director in order to make himself/herself aware of anyrelevant audit information and to establish that the company’s auditors are aware of that information.

This confirmation is given and should be interpreted in accordance with the provisions of s418 of the Companies Act, 2006.

A resolution to re-appoint Deloitte & Touche will be proposed at the forthcoming Annual General Meeting.

Approved by the Board and signed on its behalf by:

23ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

Mano Diamonds Limited 14.2%

Richmond Partners Master Limited 8.1%

Blackrock Investment Management (UK) Limited 5.5%

Blackrock Smaller Companies Trust PLC 3.6%

Barclayshare Nominees Limited 3.4%

N. KARL SMITHSON LORD DARESBURY

24 ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

STATEMENT OFDIRECTORS’ RESPONSIBILITY

GOVERNANCE

The directors are responsible for preparing the Annual Report and the financial statements in accordance with applicable law and regulations.

Company Law requires the directors to prepare financial statements for each financial year. The directors are required to prepare thefinancial statements in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union. Undercompany law the directors must not approve the financial statements unless they are satisfied that they give a true and fair view of thestate of affairs of the company and of the profit or loss of the company for that period. In preparing these financial statements,International Accounting Standard 1 requires that directors:

• properly select and apply accounting policies;• present information, including accounting policies in a manner that provides relevant, reliable, comparable and understandable

information;• provide additional disclosures when compliance with the specific requirements in IFRSs are insufficient to enable users to • understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial

performance; and• make an assessment of the company’s ability to continue as a going concern.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the company’stransactions and disclose with reasonable accuracy at any time the financial position of the company and enable them to ensure thatthe financial statements comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the companyand hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the corporate and financial information included on the company’swebsite. Legislation in the United Kingdom governing the preparation and dissemination of financial statements may differ fromlegislation in other jurisdictions.

25ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

INDEPENDANT AUDITOR’S REPORT TO THE SHAREHOLDERS OF STELLAR DIAMONDS PLC

FINANCIAL STATEMENTS

We have audited the group financial statements of Stellar Diamonds plc. for the year ended 30 June 2011 which comprise theconsolidated statement of comprehensive income, the consolidated statement of financial position, the consolidated statement ofchanges in equity, the consolidated statement of cash flows and the related notes 1 to 19 and the parent company financial statementsof Stellar Diamonds plc. for the year ended 30 June 2011 which comprise the company statement of financial position, the companystatement of changes in equity, the company statement of cash flows and the related notes 1 to 11. The financial reporting frameworkthat has been applied in their preparation is applicable law and International Financial Reporting Standards (IFRSs) as adopted by theEuropean Union and as applied in accordance with the provisions of the Companies Act 2006.

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006.Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them inan auditors’ report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyoneother than the company and the company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

RESPECTIVE RESPONSIBILITIES OF DIRECTORS AND AUDITORSAs explained more fully in the Statement of Directors’ Responsibilities, the directors are responsible for the preparation of the financialstatements and for being satisfied that they give a true and fair view. Our responsibility is to audit the financial statements in accordancewith applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the AuditingPractices Board’s (APB’s) Ethical Standards for Auditors.

SCOPE OF THE AUDIT OF THE FINANCIAL STATEMENTSAn audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance thatthe financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether theaccounting policies are appropriate to the group’s and the parent company’s circumstances and have been consistently applied and adequatelydisclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements.

OPINION ON FINANCIAL STATEMENTSIn our opinion:

• the financial statements give a true and fair view of the state of the group’s and the parent company’s affairs as at 30 June 2011 and of the group’s loss for the year then ended;

• the group financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union;• the parent company financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union

and as applied in accordance with the provisions of the Companies Act 2006; and• the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

EMPHASIS OF MATTERWithout qualifying our opinion, we draw your attention to notes 8 and 9 to the group financial statements and notes 3, 4 and 5 to theparent company financial statements concerning the valuation of intangible and tangible assets, the recoverability of amounts due fromsubsidiaries and the recoverability of investments in subsidiaries. The realisation of intangible assets of $7,168,005 and tangible assets of$7,150,956 included in the consolidated statement of financial position and intangible assets of $1,302,561, investment in subsidiaries of$4,157,484 and amounts due from subsidiaries of $15,787,711 included in the company statement of financial position are dependent onthe discovery and successful development of economic mineral reserves including the group's ability to raise sufficient finance todevelop the projects. The financial statements do not include any adjustments relating to these uncertainties and the ultimate outcomecannot, at present, be determined.

SEPARATE OPINION IN RELATION TO IFRSS AS ISSUED BY THE IASBAs explained in note 1 to the financial statements, the group in addition to complying with its legal obligation to apply IFRSs as adoptedby the European Union, has also applied IFRSs as issued by the International Accounting Standards Board (IASB). In our opinion thegroup financial statements comply with IFRSs as issued by the IASB.

OPINION ON OTHER MATTER PRESCRIBED BY THE COMPANIES ACT 2006In our opinion the information given in the Directors’ Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

MATTERS ON WHICH WE ARE REQUIRED TO REPORT BY EXCEPTIONWe have nothing to report in respect of the following matters where the Companies Act2006 requires us to report to you if, in our opinion:

• adequate accounting records have not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

• the parent company financial statements are not in agreement with the accounting records and returns; or

• certain disclosures of directors’ remuneration specified by law are not made; or• we have not received all the information and explanations we require for our audit.

KEVIN SHEEHAN(Senior Statutory Auditor)for and on behalf of Deloitte & ToucheChartered Accountants and Statutory Auditors Deloitte & Touche HouseEarlsfort Terrace, Dublin 2, Ireland5 October 2011

26 ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

CONSOLIDATED STATEMENT OFCOMPREHENSIVE INCOMEFOR THE YEAR ENDED 30 JUNE 2011 (STATED IN U.S. DOLLARS)

FINANCIAL STATEMENTS

Year ended Nine months ended

Notes 30 June 2011 30 June 2011

Revenue 3 1,518,002 2,032,762

Cost of sales (4,067,699) (4,233,730)

Gross loss (2,549,697) (2,200,968)

Impairment of tangible assets 9 (8,643,201) -

Administrative expenses (3,705,610) (3,201,700)

(12,348,811) (3,201,700)

Finance income - 317

Finance costs (35,488) (168,080)

Loss before tax (14,933,996) (5,570,431)

Income tax expense 6 - -

Loss after tax attributable to equity holders of the parent 4 (14,933,996) (5,570,431)

Total comprehensive income for the year/ period attributable to equity holders of the parent

(14,933,996) (5,570,431)

Weighted average number of shares 145,962,871 64,451,236

Basic and diluted loss per share 7 (0.10) (0.09)

30 June 30 June

Notes 2011 2010

Assets

Non-current assets

Intangible assets 8 7,168,005 4,943,544

Property, plant and equipment 9 7,150,956 17,057,939

Total non-current assets 14,318,961 22,001,483

Current assets

Inventories 10 507,242 357,499

Trade and other receivables 11 194,487 841,868

Cash and cash equivalents 6,518,640 689,650

Total current assets 7,220,369 1,889,017

Total assets 21,539,330 23,890,500

Equity and liabilities

Capital and reserves

Share capital 12 17,161,566 7,875,264

Share premium 12 25,055,393 22,023,543

Reverse acquisition reserve 2 17,073,279 17,073,279

Warrant reserve 12 155,235 143,024

Share option reserve 13 4,177,000 3,610,185

Convertible loan reserve 14 - 87,853

Accumulated loss (42,503,397) (27,712,425)

Total equity 21,119,076 23,100,723

Non-current liabilities

Convertible loan 14 - 397,209

Provision 15 104,369 54,369

Total non-current liabilities 104,369 451,578

Current liabilities

Trade and other payables 16 315,885 338,199

Total current liabilities 315,885 338,199

Total liabilities 420,254 789,777

Total equity and liabilities 21,539,330 23,890,500

27ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

CONSOLIDATED STATEMENT OFFINANCIAL POSITION AS AT 30 JUNE 2011 (STATED IN U.S. DOLLARS)

FINANCIAL STATEMENTS

The financial statements of Stellar Diamonds plc, registered number: 5424214 were approved by the Board of Directors and authorisedfor issue on. They were signed on its behalf by:

N. KARL SMITHSON LORD DARESBURY

28 ANNUAL REPORT AND ACCOUNTS 2011STELLAR DIAMONDS PLC

CONSOLIDATED STATEMENT OFCHANGES IN EQUITYFOR THE YEAR ENDED 30 JUNE 2011 (STATED IN U.S. DOLLARS)

FINANCIAL STATEMENTS

Share capital

(note 12)

Sharepremium(note 12)

Warrantreserve

(note 12)

Share option

reserve(note 13)

Convertibleloan reserve

(note 14)

Reverse acquisition

reserve(note 2)

Accumulatedloss

Totalequity

Balance at 30 September 2009 956,474 31,272,947 269,801 2,709,261 87,853 166,672 (22,411,795) 13,051,213

Total comprehensive income for the period

- - - - - - (5,570,431) (5,570,431)

Issue of shares to directors (note 12)

335 33,131 - - - - - 33,466

Conversion of debt to equity (note 12)

9,049 895,868 - - - - - 904,917

Reverse acquisition adjustment (note 12)

4,623,043 (16,443,279) - 639,292 - 16,906,607 - 5,725,663

Issue of placing shares (note 12)

1,951,938 5,784,958 - - - - 7,736,896

Share warrants issued (note 12)

- (143,024) 143,024 - - - - -

Share issue costs (note 12)

- (380,023) - - - - - (380,023)

Re-pricing of Stellar Diamonds Limited share options (notes 2 and 12)

- - - 261,632 - - - 261,632

Shares issued to directors on admission to AIM (note 12)

8,784 26,044 - - - - - 34,828

Other shares issued (note 12)

325,641 976,921 - - - - - 1,302,562

Expired warrants - - (269,801) - - - 269,801 -

Balance at 30 June 2010 7,875,264 22,023,543 143,024 3,610,185 87,853 17,073,279 (27,712,425) 23,100,723

Total comprehensive income for the year

- - - - - - (14,933,996) (14,933,996)

Repayment of convertible loan (note 14)

- - - - (87,853) - - (87,853)

Issue of placing shares (note 12)

9,280,410 3,721,084 - - - - - 13,001,494

Share warrants issued (note 12) - (155,235) 155,235 - - - - -

Share issue costs (note 12) - (539,757) - - - - - (539,757)

Warrants expired (note 12) - - (143,024) - - - 143,024 -

Other shares issued (note 12) 5,892 5,758 - - - - - 11,650

Share options issued (note 13) - - - 566,815 - - - 566,815

Balance at 30 June 2011 17,161,566 25,055,393 155,235 4,177,000 - 17,073,279 (42,503,397) 21,119,076

29ANNUAL REPORT AND ACCOUNTS 2011 STELLAR DIAMONDS PLC

CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 30 JUNE 2011 (STATED IN U.S. DOLLARS)

FINANCIAL STATEMENTS

Year ended Nine months ended

30 June 2011 30 June 2010

Cash flows from operating activities:

Net loss for the year/period (14,933,996) (5,570,431)

Adjustments for:

- Depreciation of property, plant and equipment 1,638,860 1,563,844

- Impairment of property, plant and equipment 8,643,201 -

- Share-based payment expense 566,815 261,632

- Shares issued to directors in lieu of fees 234,863 34,828

- Interest income - (317)

- Interest expense 35,488 168,080

- Net foreign exchange (gain)/loss (41,184) 79,606

Change in working capital items:

- Decrease/(Increase) in receivables 647,381 (200,327)

- (Increase)/Decrease in stock (149,743) 204,983

- Increase/(Decrease) in trade and other payables 87,381 (203,260)

Net cash used in operations (3,270,934) (3,661,362)