std. 12th book keeping and accountancy smart notes ... · sample content ii preface this book based...

TRANSCRIPT

SAMPLE C

ONTENT

Written as per the revised syllabus prescribed by the Maharashtra State Board of Secondary and Higher Secondary Education, Pune.

P.O. No. 158486 Balbharati Registration No.: 2018MH0022TEID: 13320

Printed at: Repro India Ltd., Mumbai

© Target Publications Pvt. Ltd. No part of this book may be reproduced or transmitted in any form or by any means, C.D. ROM/Audio Video Cassettes or electronic, mechanicalincluding photocopying; recording or by any information storage and retrieval system without permission in writing from the Publisher.

Now access the solutions to all the Homework Section Problems withinthis book through our Quill App.

Salient Features

• Based on MH – Board Syllabus• Simplified Theory• Contains Textual, Board as well as Homework problems • Type-wise sorting of sums• Covers Board Question Papers of March 2018, July 2018 and March 2019

STD. XII COMMERCE

SMART NOTES

BOOK-KEEPING & ACCOUNTANCY

for one month free trial.Scan the QR code to download the app and use the coupon code QUILL30D

SAMPLE C

ONTENT

ii

PREFACE This book based upon Book-Keeping & Accountancy is carefully curated to facilitate learning and instill conceptual understanding within students. This treasure trove of knowledge fosters robust conceptual clarity and inspires confidence within the nimble mind of students. Std.XII is a crucial year of a student’s academic life. Our Smart Notes not only help you to prepare for your final examinations but also equip you on a parallel ground to strengthen your foundation and lay the cornerstone of a bright future. Smart Notes comprehensively cover the entire syllabus as well as answer all questions that stand a probable chance of being asked in the Board Examinations. Through the medium of this book, we have explained the subject’s theory in an extremely lucid manner. The book is rife with practical problems, board problems and homework questions. Moreover, we have sorted the sums based on their type and difficulty level. We sincerely hope that this book helps you to comprehend the subject effortlessly and efficiently. Apart from the book, we’re also delighted to present you ‘Quill – The Padhai App’. Quill App takes an innovative approach towards learning with this book. It enables you to learn on the move. It also has a unique quiz section that tests your subject knowledge. Moreover, you can also view Board Question Papers of the previous years. With the purchase of this book, you’re entitled to avail a month’s Free access to the Quill App. We’re sure that students, parents and teachers alike would love our value proposition and unique presentation of content that we have created for students. The journey to create a complete book is strewn with triumphs, failures and near misses. If you think we've nearly missed something or want to applaud us for our triumphs, we'd love to hear from you. Please write to us on: [email protected]

Disclaimer This reference book is transformative work based on textual contents published by the Maharashtra State Board of Secondary and Higher Secondary Education, Pune. We the publishers are making this reference book which constitutes as fair use of textual contents which are transformed by adding and elaborating, with a view to simplify the same to enable the students to understand, memorize and reproduce the same in examinations. This work is purely inspired upon the course work as prescribed by the Maharashtra State Board of Secondary and Higher Secondary Education, Pune. Every care has been taken in the publication of this reference book by the Authors while creating the contents. The Authors and the Publishers shall not be responsible for any loss or damages caused to any person on account of errors or omissions which might have crept in or disagreement of any third party on the point of view expressed in the reference book. © reserved with the Publisher for all the contents created by our Authors. No copyright is claimed in the textual contents which are presented as part of fair dealing with a view to provide best supplementary study material for the benefit of students.

SAMPLE C

ONTENT

iii

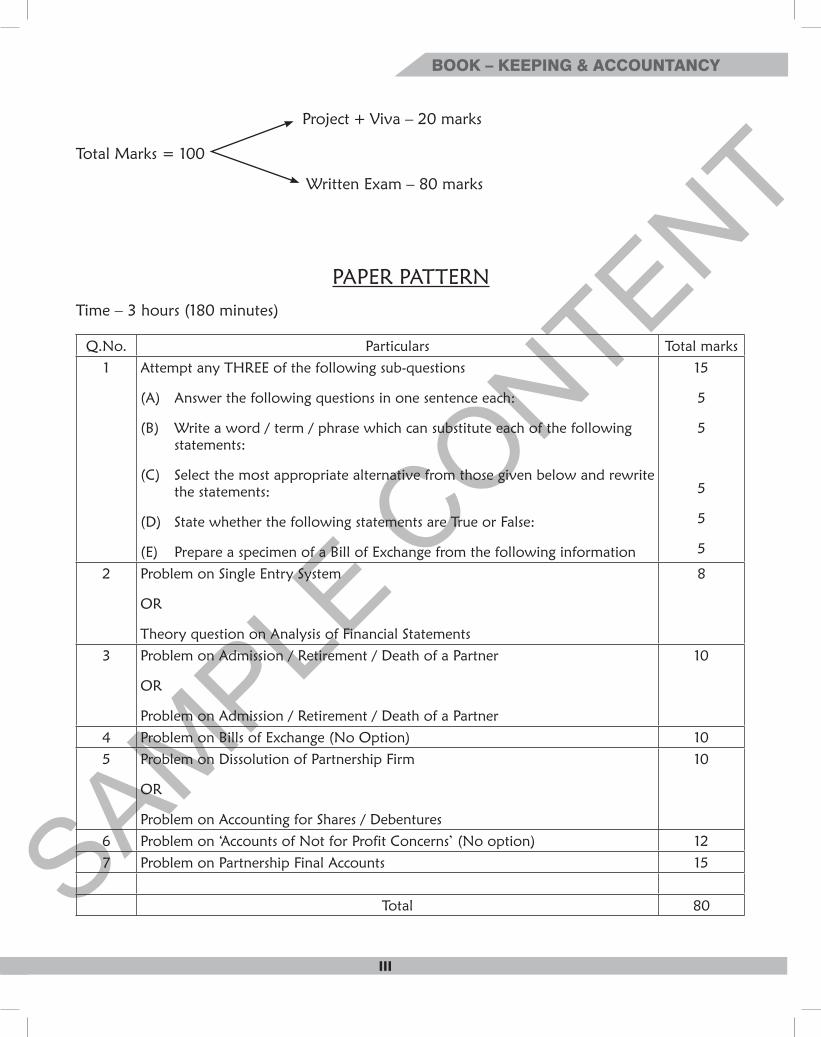

BOOK – KEEPING & ACCOUNTANCY

Project + Viva – 20 marks

Total Marks = 100

Written Exam – 80 marks

PAPER PATTERNTime – 3 hours (180 minutes)

Q.No. Particulars Total marks1 Attempt any THREE of the following sub-questions

(A) Answer the following questions in one sentence each:

(B) Write a word / term / phrase which can substitute each of the following statements:

(C) Select the most appropriate alternative from those given below and rewrite the statements:

(D) State whether the following statements are True or False:

(E) Prepare a specimen of a Bill of Exchange from the following information

15

5

5

5

5

5

2 Problem on Single Entry System

OR

Theory question on Analysis of Financial Statements

8

3 Problem on Admission / Retirement / Death of a Partner

OR

Problem on Admission / Retirement / Death of a Partner

10

4 Problem on Bills of Exchange (No Option) 105 Problem on Dissolution of Partnership Firm

OR

Problem on Accounting for Shares / Debentures

10

6 Problem on ‘Accounts of Not for Profit Concerns’ (No option) 127 Problem on Partnership Final Accounts 15

Total 80

SAMPLE C

ONTENT

iv

BOOK – KEEPING & ACCOUNTANCY

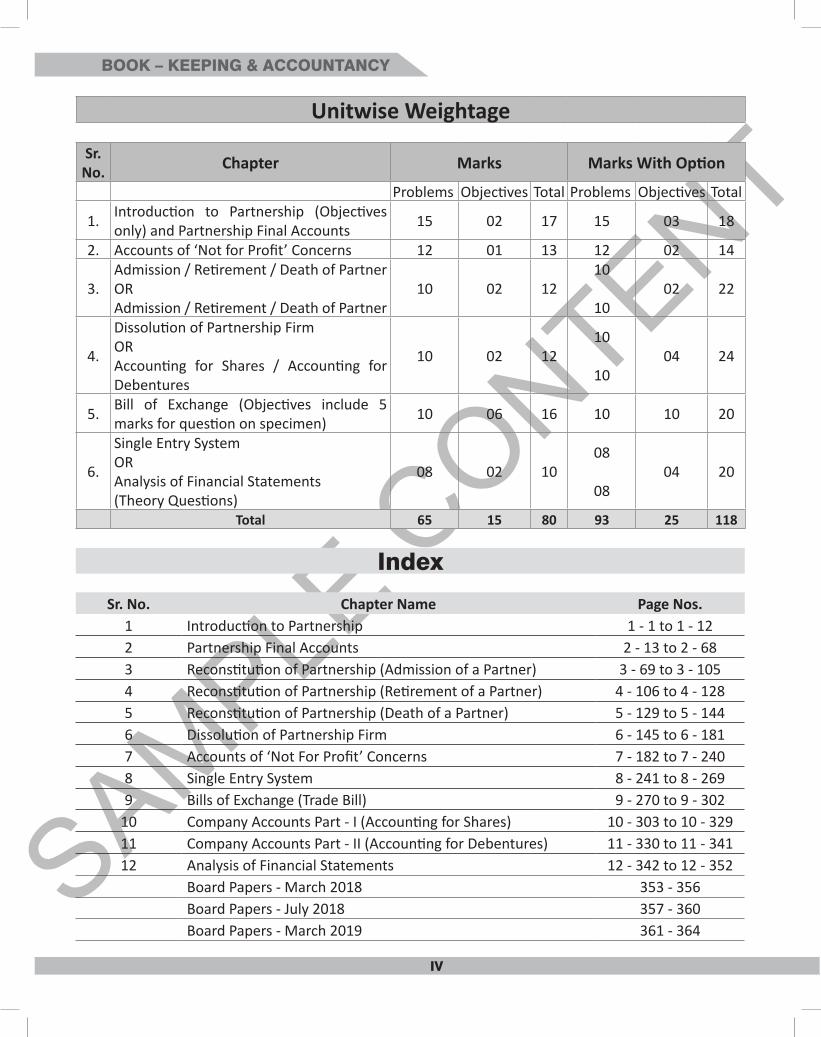

index

Sr. No. Chapter Name Page Nos.1 Introduction to Partnership 1 - 1 to 1 - 12 2 Partnership Final Accounts 2 - 13 to 2 - 683 Reconstitution of Partnership (Admission of a Partner) 3 - 69 to 3 - 1054 Reconstitution of Partnership (Retirement of a Partner) 4 - 106 to 4 - 1285 Reconstitution of Partnership (Death of a Partner) 5 - 129 to 5 - 1446 Dissolution of Partnership Firm 6 - 145 to 6 - 1817 Accounts of ‘Not For Profit’ Concerns 7 - 182 to 7 - 2408 Single Entry System 8 - 241 to 8 - 2699 Bills of Exchange (Trade Bill) 9 - 270 to 9 - 302

10 Company Accounts Part - I (Accounting for Shares) 10 - 303 to 10 - 32911 Company Accounts Part - II (Accounting for Debentures) 11 - 330 to 11 - 34112 Analysis of Financial Statements 12 - 342 to 12 - 352

Board Papers - March 2018 353 - 356Board Papers - July 2018 357 - 360Board Papers - March 2019 361 - 364

Unitwise Weightage

Sr. No. Chapter Marks Marks With Option

Problems Objectives Total Problems Objectives Total

1.Introduction to Partnership (Objectives only) and Partnership Final Accounts

15 02 17 15 03 18

2. Accounts of ‘Not for Profit’ Concerns 12 01 13 12 02 14

3.Admission / Retirement / Death of PartnerORAdmission / Retirement / Death of Partner

10 02 1210

1002 22

4.

Dissolution of Partnership Firm ORAccounting for Shares / Accounting for Debentures

10 02 1210

1004 24

5.Bill of Exchange (Objectives include 5 marks for question on specimen)

10 06 16 10 10 20

6.

Single Entry SystemORAnalysis of Financial Statements(Theory Questions)

08 02 1008

0804 20

Total 65 15 80 93 25 118

SAMPLE C

ONTENTSingle Entry System

8 - 241

CHAPTER 8: SINGLE ENTRY SYSTEM

Sr. No. Particulars Page No.

1. Theory 8 - 242

2. Section I :

Textbook Problems 8 - 246

3. Section II :

Board Problems 8 - 253

4. Section III :

Homework Problems 8 - 260

5. Section IV :

Objective Type Questions 8 - 267

Problem Type Textbook Section Homework SectionDrawings + Additional capital 1,2 1,2Depreciation + Bad debts+RDD 3,4,5,6 3,4,5Interest on capital and Interest on drawing 7,8,9,10 6,7,8Revaluation of assets 11,12 9,10Various adjustments 13,14 11,12Partnership firm 15,16,17,18 13,14,15Alternative method 19,20 16

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 242

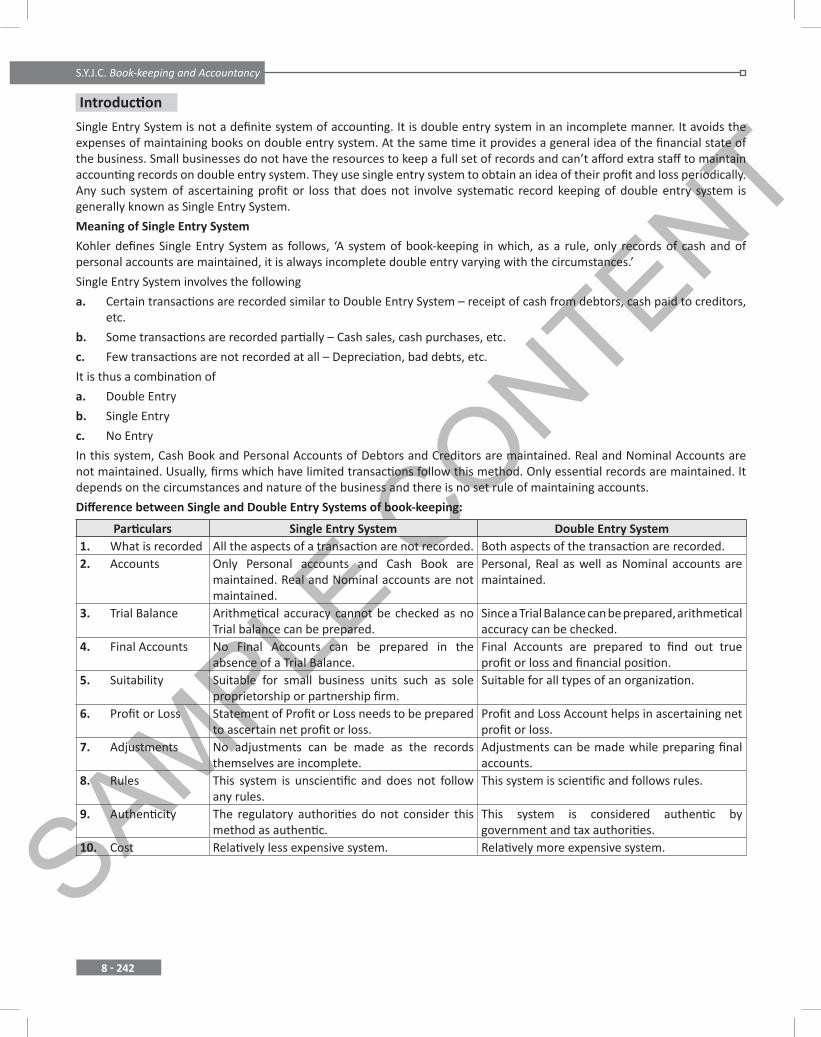

Introduction

Single Entry System is not a definite system of accounting. It is double entry system in an incomplete manner. It avoids the expenses of maintaining books on double entry system. At the same time it provides a general idea of the financial state of the business. Small businesses do not have the resources to keep a full set of records and can’t afford extra staff to maintain accounting records on double entry system. They use single entry system to obtain an idea of their profit and loss periodically. Any such system of ascertaining profit or loss that does not involve systematic record keeping of double entry system is generally known as Single Entry System.

Meaning of Single Entry System

Kohler defines Single Entry System as follows, ‘A system of book-keeping in which, as a rule, only records of cash and of personal accounts are maintained, it is always incomplete double entry varying with the circumstances.’

Single Entry System involves the following

a. Certain transactions are recorded similar to Double Entry System – receipt of cash from debtors, cash paid to creditors,etc.

b. Some transactions are recorded partially – Cash sales, cash purchases, etc.

c. Few transactions are not recorded at all – Depreciation, bad debts, etc.

It is thus a combination of

a. Double Entry

b. Single Entry

c. No Entry

In this system, Cash Book and Personal Accounts of Debtors and Creditors are maintained. Real and Nominal Accounts are not maintained. Usually, firms which have limited transactions follow this method. Only essential records are maintained. It depends on the circumstances and nature of the business and there is no set rule of maintaining accounts.

Difference between Single and Double Entry Systems of book-keeping:

Particulars Single Entry System Double Entry System1. What is recorded All the aspects of a transaction are not recorded. Both aspects of the transaction are recorded.2. Accounts Only Personal accounts and Cash Book are

maintained. Real and Nominal accounts are not maintained.

Personal, Real as well as Nominal accounts are maintained.

3. Trial Balance Arithmetical accuracy cannot be checked as no Trial balance can be prepared.

Since a Trial Balance can be prepared, arithmetical accuracy can be checked.

4. Final Accounts No Final Accounts can be prepared in the absence of a Trial Balance.

Final Accounts are prepared to find out true profit or loss and financial position.

5. Suitability Suitable for small business units such as sole proprietorship or partnership firm.

Suitable for all types of an organization.

6. Profit or Loss Statement of Profit or Loss needs to be prepared to ascertain net profit or loss.

Profit and Loss Account helps in ascertaining net profit or loss.

7. Adjustments No adjustments can be made as the records themselves are incomplete.

Adjustments can be made while preparing final accounts.

8. Rules This system is unscientific and does not follow any rules.

This system is scientific and follows rules.

9. Authenticity The regulatory authorities do not consider this method as authentic.

This system is considered authentic by government and tax authorities.

10. Cost Relatively less expensive system. Relatively more expensive system.

SAMPLE C

ONTENTSingle Entry System

8 - 243

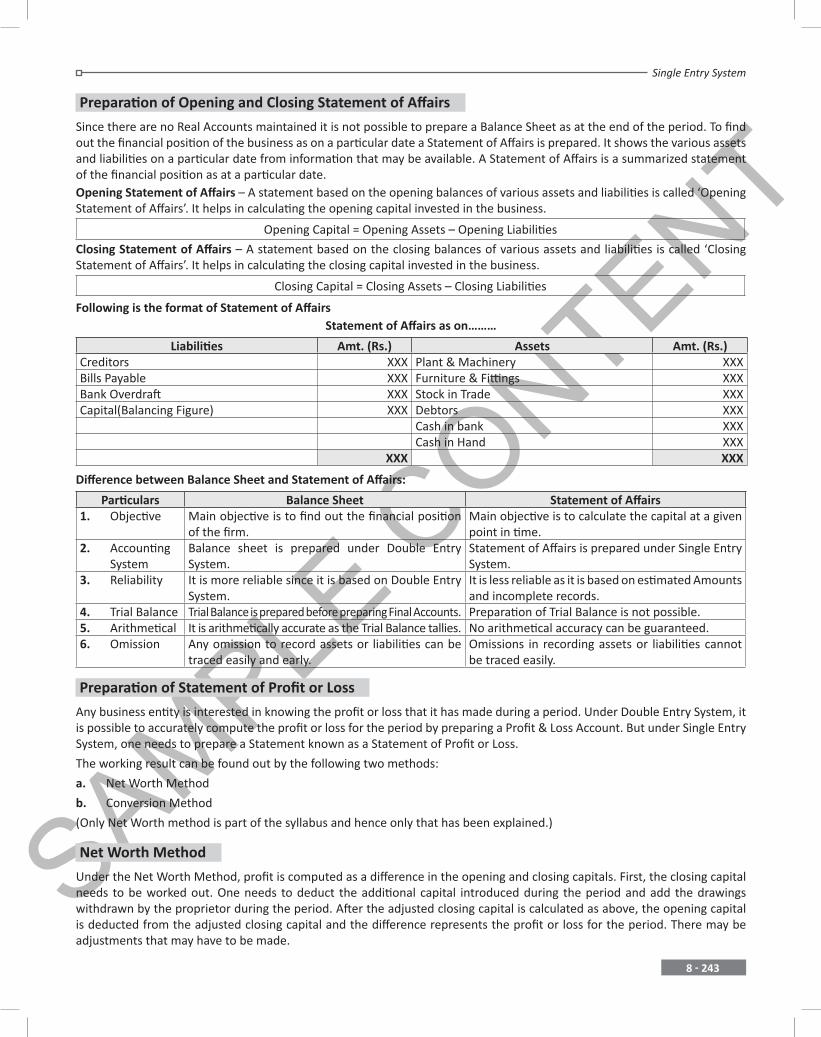

Preparation of Opening and Closing Statement of Affairs

Since there are no Real Accounts maintained it is not possible to prepare a Balance Sheet as at the end of the period. To find out the financial position of the business as on a particular date a Statement of Affairs is prepared. It shows the various assets and liabilities on a particular date from information that may be available. A Statement of Affairs is a summarized statement of the financial position as at a particular date.Opening Statement of Affairs – A statement based on the opening balances of various assets and liabilities is called ‘Opening Statement of Affairs’. It helps in calculating the opening capital invested in the business.

Opening Capital = Opening Assets – Opening Liabilities

Closing Statement of Affairs – A statement based on the closing balances of various assets and liabilities is called ‘Closing Statement of Affairs’. It helps in calculating the closing capital invested in the business.

Closing Capital = Closing Assets – Closing Liabilities

Following is the format of Statement of AffairsStatement of Affairs as on………

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Creditors XXX Plant & Machinery XXXBills Payable XXX Furniture & Fittings XXXBank Overdraft XXX Stock in Trade XXXCapital(Balancing Figure) XXX Debtors XXX

Cash in bank XXXCash in Hand XXX

XXX XXX

Difference between Balance Sheet and Statement of Affairs:

Particulars Balance Sheet Statement of Affairs1. Objective Main objective is to find out the financial position

of the firm.Main objective is to calculate the capital at a given point in time.

2. Accounting System

Balance sheet is prepared under Double Entry System.

Statement of Affairs is prepared under Single Entry System.

3. Reliability It is more reliable since it is based on Double Entry System.

It is less reliable as it is based on estimated Amounts and incomplete records.

4. Trial Balance Trial Balance is prepared before preparing Final Accounts. Preparation of Trial Balance is not possible.5. Arithmetical It is arithmetically accurate as the Trial Balance tallies. No arithmetical accuracy can be guaranteed.6. Omission Any omission to record assets or liabilities can be

traced easily and early.Omissions in recording assets or liabilities cannot be traced easily.

Preparation of Statement of Profit or Loss

Any business entity is interested in knowing the profit or loss that it has made during a period. Under Double Entry System, it is possible to accurately compute the profit or loss for the period by preparing a Profit & Loss Account. But under Single Entry System, one needs to prepare a Statement known as a Statement of Profit or Loss.

The working result can be found out by the following two methods:

a. Net Worth Method

b. Conversion Method

(Only Net Worth method is part of the syllabus and hence only that has been explained.)

Net Worth Method

Under the Net Worth Method, profit is computed as a difference in the opening and closing capitals. First, the closing capital needs to be worked out. One needs to deduct the additional capital introduced during the period and add the drawings withdrawn by the proprietor during the period. After the adjusted closing capital is calculated as above, the opening capital is deducted from the adjusted closing capital and the difference represents the profit or loss for the period. There may be adjustments that may have to be made.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 244

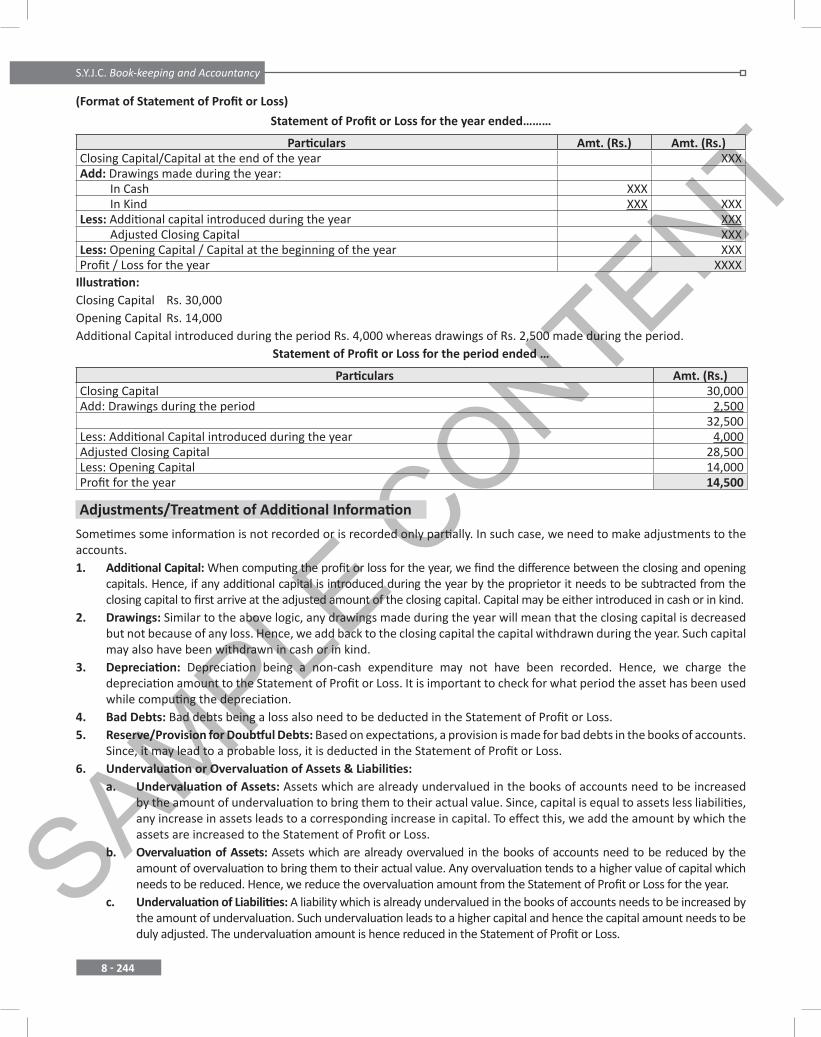

(Format of Statement of Profit or Loss)

Statement of Profit or Loss for the year ended………

Particulars Amt. (Rs.) Amt. (Rs.)Closing Capital/Capital at the end of the year XXX Add: Drawings made during the year: In Cash XXX In Kind XXX XXXLess: Additional capital introduced during the year XXX Adjusted Closing Capital XXXLess: Opening Capital / Capital at the beginning of the year XXXProfit / Loss for the year XXXX

Illustration:Closing Capital Rs. 30,000Opening Capital Rs. 14,000Additional Capital introduced during the period Rs. 4,000 whereas drawings of Rs. 2,500 made during the period.

Statement of Profit or Loss for the period ended …

Particulars Amt. (Rs.)Closing Capital 30,000Add: Drawings during the period 2,500

32,500Less: Additional Capital introduced during the year 4,000Adjusted Closing Capital 28,500Less: Opening Capital 14,000Profit for the year 14,500

Adjustments/Treatment of Additional Information

Sometimes some information is not recorded or is recorded only partially. In such case, we need to make adjustments to the accounts.1. Additional Capital: When computing the profit or loss for the year, we find the difference between the closing and opening

capitals. Hence, if any additional capital is introduced during the year by the proprietor it needs to be subtracted from the closing capital to first arrive at the adjusted amount of the closing capital. Capital may be either introduced in cash or in kind.

2. Drawings: Similar to the above logic, any drawings made during the year will mean that the closing capital is decreased but not because of any loss. Hence, we add back to the closing capital the capital withdrawn during the year. Such capital may also have been withdrawn in cash or in kind.

3. Depreciation: Depreciation being a non-cash expenditure may not have been recorded. Hence, we charge the depreciation amount to the Statement of Profit or Loss. It is important to check for what period the asset has been used while computing the depreciation.

4. Bad Debts: Bad debts being a loss also need to be deducted in the Statement of Profit or Loss.5. Reserve/Provision for Doubtful Debts: Based on expectations, a provision is made for bad debts in the books of accounts.

Since, it may lead to a probable loss, it is deducted in the Statement of Profit or Loss.6. Undervaluation or Overvaluation of Assets & Liabilities: a. Undervaluation of Assets: Assets which are already undervalued in the books of accounts need to be increased

by the amount of undervaluation to bring them to their actual value. Since, capital is equal to assets less liabilities, any increase in assets leads to a corresponding increase in capital. To effect this, we add the amount by which the assets are increased to the Statement of Profit or Loss.

b. Overvaluation of Assets: Assets which are already overvalued in the books of accounts need to be reduced by the amount of overvaluation to bring them to their actual value. Any overvaluation tends to a higher value of capital which needs to be reduced. Hence, we reduce the overvaluation amount from the Statement of Profit or Loss for the year.

c. Undervaluation of Liabilities: A liability which is already undervalued in the books of accounts needs to be increased by the amount of undervaluation. Such undervaluation leads to a higher capital and hence the capital amount needs to be duly adjusted. The undervaluation amount is hence reduced in the Statement of Profit or Loss.

SAMPLE C

ONTENTSingle Entry System

8 - 245

d. Overvaluation of Liabilities: A liability which is already overvalued in the books of accounts needs to be decreased by the amount of overvaluation. Such overvaluation leads to a lower capital and hence the capital amount needs to be duly adjusted. The overvaluation amount is hence added in the Statement of Profit or Loss.

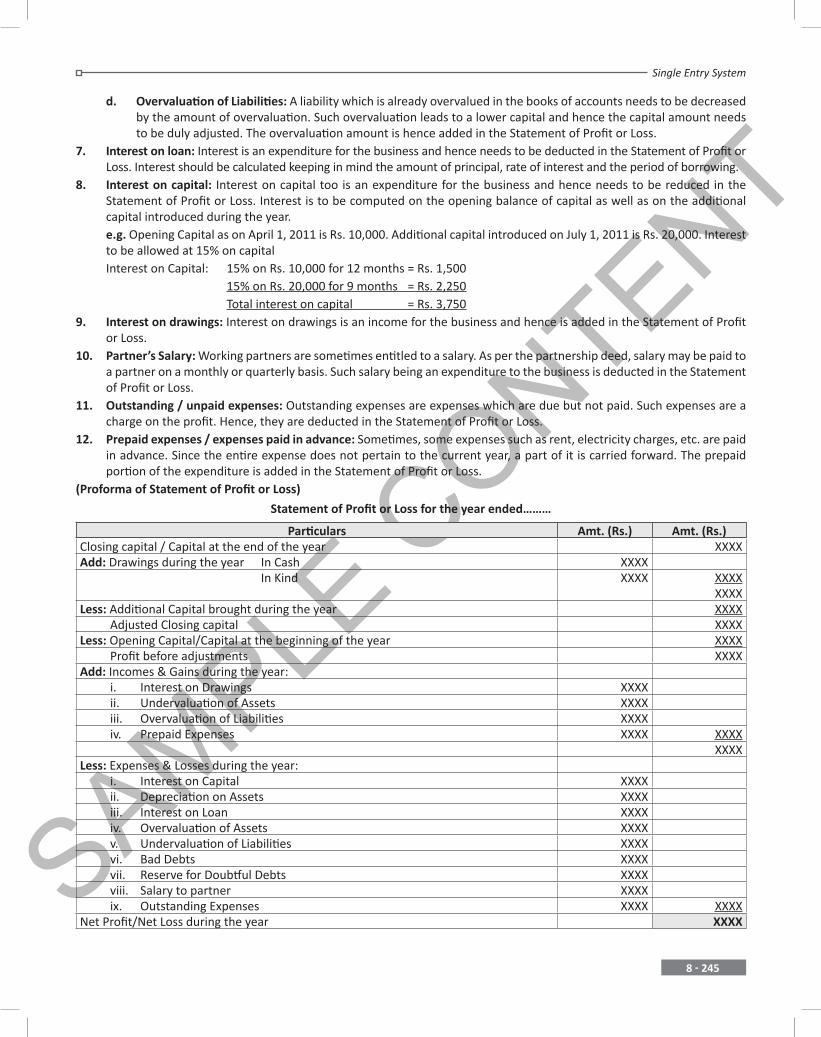

7. Interest on loan: Interest is an expenditure for the business and hence needs to be deducted in the Statement of Profit or Loss. Interest should be calculated keeping in mind the amount of principal, rate of interest and the period of borrowing.

8. Interest on capital: Interest on capital too is an expenditure for the business and hence needs to be reduced in the Statement of Profit or Loss. Interest is to be computed on the opening balance of capital as well as on the additional capital introduced during the year.

e.g. Opening Capital as on April 1, 2011 is Rs. 10,000. Additional capital introduced on July 1, 2011 is Rs. 20,000. Interest to be allowed at 15% on capital

Interest on Capital: 15% on Rs. 10,000 for 12 months = Rs. 1,500 15% on Rs. 20,000 for 9 months = Rs. 2,250 Total interest on capital = Rs. 3,7509. Interest on drawings: Interest on drawings is an income for the business and hence is added in the Statement of Profit

or Loss.10. Partner’s Salary: Working partners are sometimes entitled to a salary. As per the partnership deed, salary may be paid to

a partner on a monthly or quarterly basis. Such salary being an expenditure to the business is deducted in the Statement of Profit or Loss.

11. Outstanding / unpaid expenses: Outstanding expenses are expenses which are due but not paid. Such expenses are a charge on the profit. Hence, they are deducted in the Statement of Profit or Loss.

12. Prepaid expenses / expenses paid in advance: Sometimes, some expenses such as rent, electricity charges, etc. are paid in advance. Since the entire expense does not pertain to the current year, a part of it is carried forward. The prepaid portion of the expenditure is added in the Statement of Profit or Loss.

(Proforma of Statement of Profit or Loss)

Statement of Profit or Loss for the year ended………

Particulars Amt. (Rs.) Amt. (Rs.)Closing capital / Capital at the end of the year XXXXAdd: Drawings during the year In Cash XXXX In Kind XXXX XXXX

XXXXLess: Additional Capital brought during the year XXXX Adjusted Closing capital XXXXLess: Opening Capital/Capital at the beginning of the year XXXX Profit before adjustments XXXXAdd: Incomes & Gains during the year: i. Interest on Drawings XXXX ii. Undervaluation of Assets XXXX iii. Overvaluation of Liabilities XXXX iv. Prepaid Expenses XXXX XXXX

XXXXLess: Expenses & Losses during the year: i. Interest on Capital XXXX ii. Depreciation on Assets XXXX iii. Interest on Loan XXXX iv. Overvaluation of Assets XXXX v. Undervaluation of Liabilities XXXX vi. Bad Debts XXXX vii. Reserve for Doubtful Debts XXXX viii. Salary to partner XXXX ix. Outstanding Expenses XXXX XXXXNet Profit/Net Loss during the year XXXX

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 246

Section I : Textbook Problems

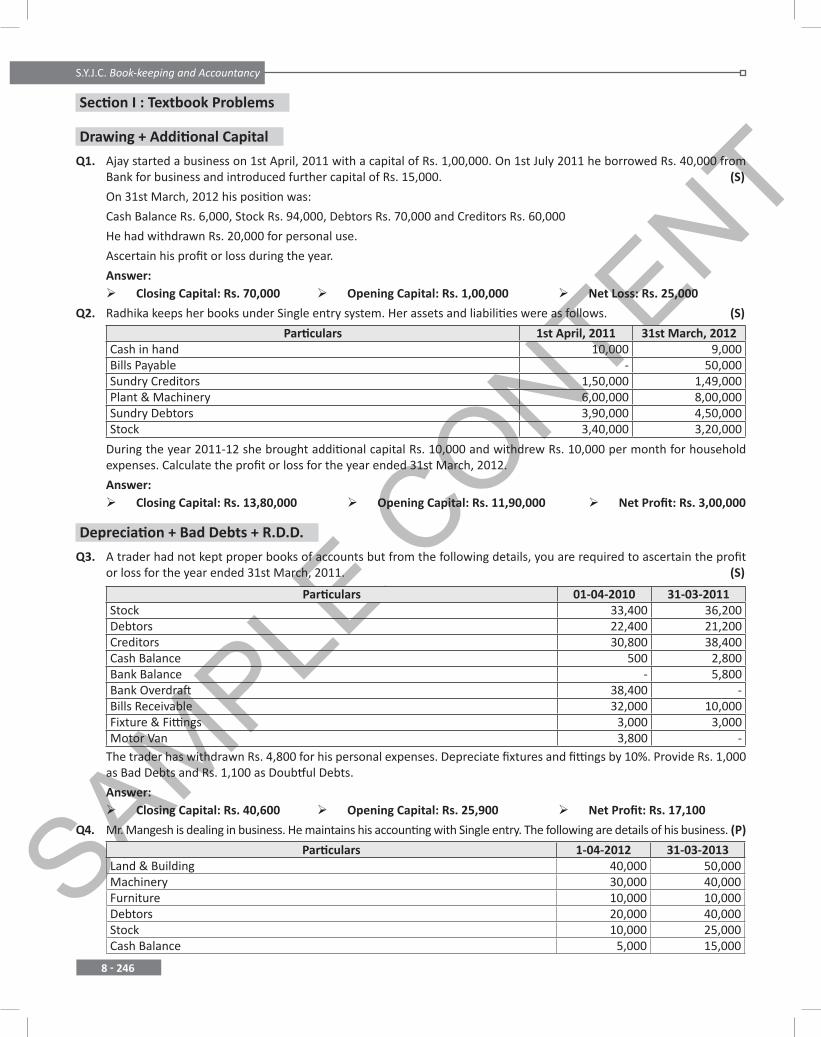

Drawing + Additional Capital

Q1. Ajay started a business on 1st April, 2011 with a capital of Rs. 1,00,000. On 1st July 2011 he borrowed Rs. 40,000 from Bank for business and introduced further capital of Rs. 15,000. (S)

On 31st March, 2012 his position was:

Cash Balance Rs. 6,000, Stock Rs. 94,000, Debtors Rs. 70,000 and Creditors Rs. 60,000

He had withdrawn Rs. 20,000 for personal use.

Ascertain his profit or loss during the year.

Answer: Closing Capital: Rs. 70,000 Opening Capital: Rs. 1,00,000 Net Loss: Rs. 25,000

Q2. Radhika keeps her books under Single entry system. Her assets and liabilities were as follows. (S)

Particulars 1st April, 2011 31st March, 2012Cash in hand 10,000 9,000Bills Payable - 50,000Sundry Creditors 1,50,000 1,49,000Plant & Machinery 6,00,000 8,00,000Sundry Debtors 3,90,000 4,50,000Stock 3,40,000 3,20,000

During the year 2011-12 she brought additional capital Rs. 10,000 and withdrew Rs. 10,000 per month for household expenses. Calculate the profit or loss for the year ended 31st March, 2012.

Answer: Closing Capital: Rs. 13,80,000 Opening Capital: Rs. 11,90,000 Net Profit: Rs. 3,00,000

Depreciation + Bad Debts + R.D.D.

Q3. A trader had not kept proper books of accounts but from the following details, you are required to ascertain the profit or loss for the year ended 31st March, 2011. (S)

Particulars 01-04-2010 31-03-2011Stock 33,400 36,200Debtors 22,400 21,200Creditors 30,800 38,400Cash Balance 500 2,800Bank Balance - 5,800Bank Overdraft 38,400 -Bills Receivable 32,000 10,000Fixture & Fittings 3,000 3,000Motor Van 3,800 -

The trader has withdrawn Rs. 4,800 for his personal expenses. Depreciate fixtures and fittings by 10%. Provide Rs. 1,000 as Bad Debts and Rs. 1,100 as Doubtful Debts.

Answer: Closing Capital: Rs. 40,600 Opening Capital: Rs. 25,900 Net Profit: Rs. 17,100

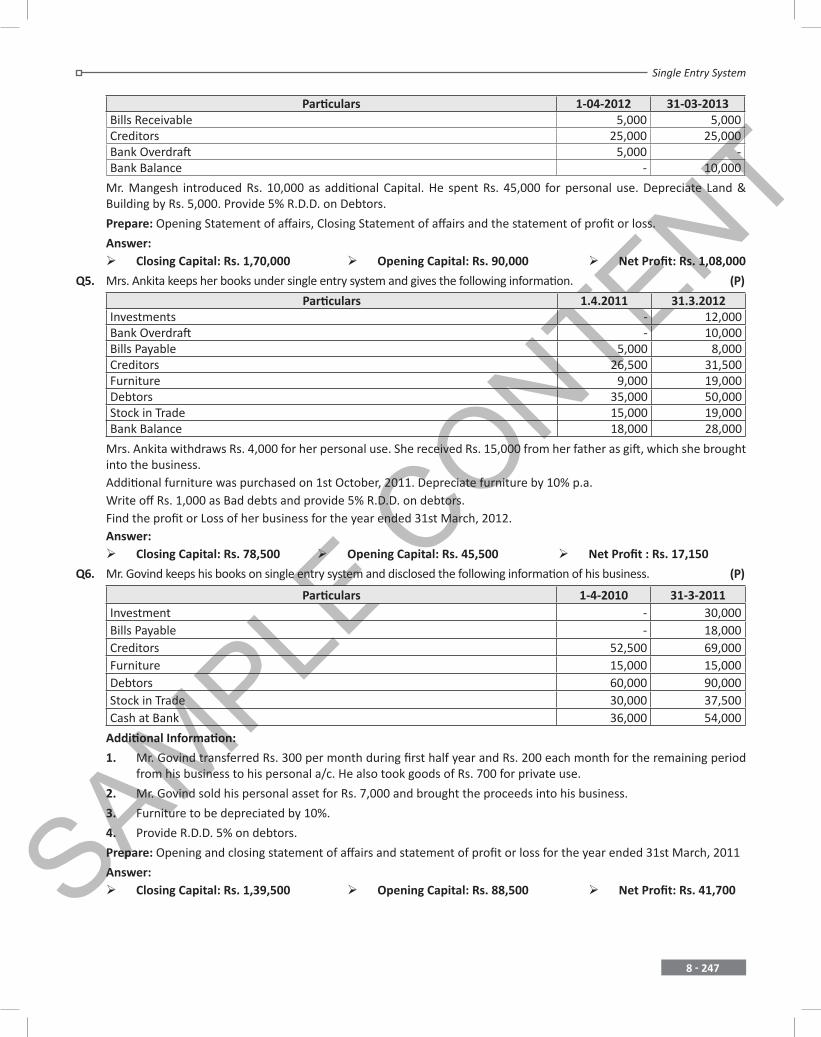

Q4. Mr. Mangesh is dealing in business. He maintains his accounting with Single entry. The following are details of his business. (P)

Particulars 1-04-2012 31-03-2013Land & Building 40,000 50,000Machinery 30,000 40,000Furniture 10,000 10,000Debtors 20,000 40,000Stock 10,000 25,000Cash Balance 5,000 15,000

SAMPLE C

ONTENTSingle Entry System

8 - 247

Particulars 1-04-2012 31-03-2013Bills Receivable 5,000 5,000Creditors 25,000 25,000Bank Overdraft 5,000 -Bank Balance - 10,000

Mr. Mangesh introduced Rs. 10,000 as additional Capital. He spent Rs. 45,000 for personal use. Depreciate Land & Building by Rs. 5,000. Provide 5% R.D.D. on Debtors.

Prepare: Opening Statement of affairs, Closing Statement of affairs and the statement of profit or loss.

Answer: Closing Capital: Rs. 1,70,000 Opening Capital: Rs. 90,000 Net Profit: Rs. 1,08,000

Q5. Mrs. Ankita keeps her books under single entry system and gives the following information. (P)

Particulars 1.4.2011 31.3.2012Investments - 12,000Bank Overdraft - 10,000Bills Payable 5,000 8,000Creditors 26,500 31,500Furniture 9,000 19,000Debtors 35,000 50,000Stock in Trade 15,000 19,000Bank Balance 18,000 28,000

Mrs. Ankita withdraws Rs. 4,000 for her personal use. She received Rs. 15,000 from her father as gift, which she brought into the business.Additional furniture was purchased on 1st October, 2011. Depreciate furniture by 10% p.a.Write off Rs. 1,000 as Bad debts and provide 5% R.D.D. on debtors.Find the profit or Loss of her business for the year ended 31st March, 2012.Answer: Closing Capital: Rs. 78,500 Opening Capital: Rs. 45,500 Net Profit : Rs. 17,150

Q6. Mr. Govind keeps his books on single entry system and disclosed the following information of his business. (P)

Particulars 1-4-2010 31-3-2011Investment - 30,000Bills Payable - 18,000Creditors 52,500 69,000Furniture 15,000 15,000Debtors 60,000 90,000Stock in Trade 30,000 37,500Cash at Bank 36,000 54,000

Additional Information:

1. Mr. Govind transferred Rs. 300 per month during first half year and Rs. 200 each month for the remaining periodfrom his business to his personal a/c. He also took goods of Rs. 700 for private use.

2. Mr. Govind sold his personal asset for Rs. 7,000 and brought the proceeds into his business.

3. Furniture to be depreciated by 10%.

4. Provide R.D.D. 5% on debtors.

Prepare: Opening and closing statement of affairs and statement of profit or loss for the year ended 31st March, 2011

Answer: Closing Capital: Rs. 1,39,500 Opening Capital: Rs. 88,500 Net Profit: Rs. 41,700

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 248

Interest on Capital and Interest on Drawings

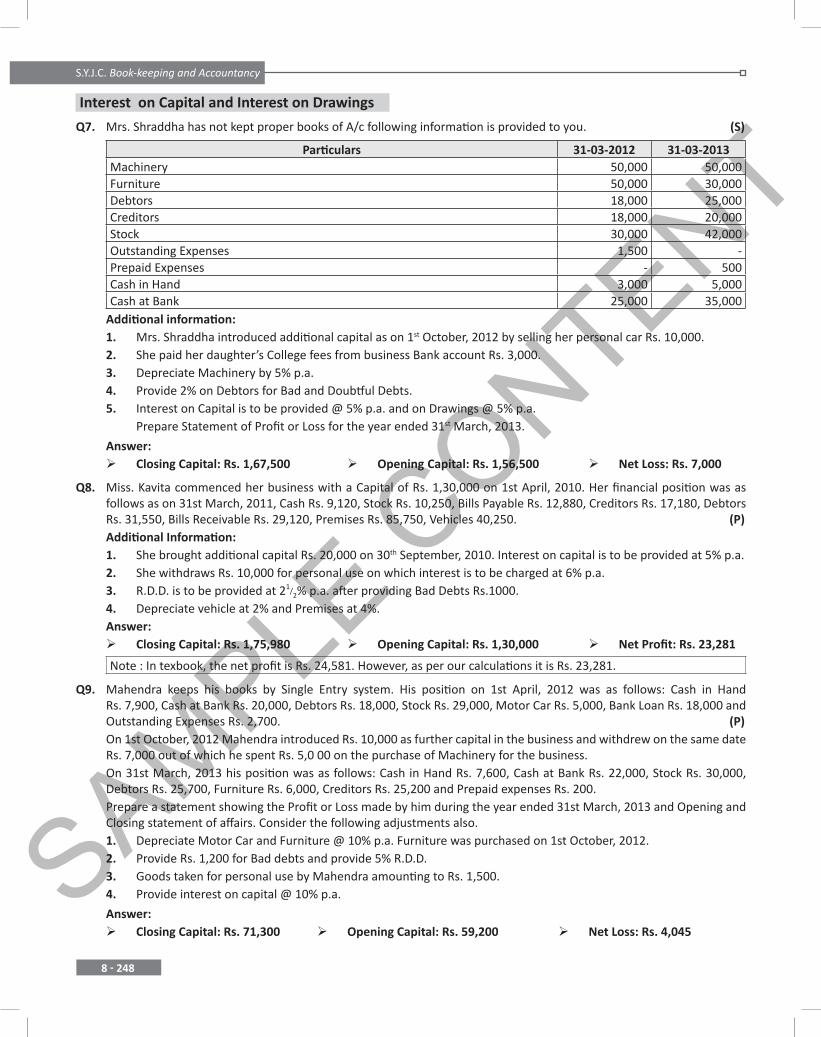

Q7. Mrs. Shraddha has not kept proper books of A/c following information is provided to you. (S)

Particulars 31-03-2012 31-03-2013Machinery 50,000 50,000Furniture 50,000 30,000Debtors 18,000 25,000Creditors 18,000 20,000Stock 30,000 42,000Outstanding Expenses 1,500 -Prepaid Expenses - 500Cash in Hand 3,000 5,000Cash at Bank 25,000 35,000

Additional information:1. Mrs. Shraddha introduced additional capital as on 1st October, 2012 by selling her personal car Rs. 10,000.2. She paid her daughter’s College fees from business Bank account Rs. 3,000.3. Depreciate Machinery by 5% p.a.4. Provide 2% on Debtors for Bad and Doubtful Debts.5. Interest on Capital is to be provided @ 5% p.a. and on Drawings @ 5% p.a.

Prepare Statement of Profit or Loss for the year ended 31st March, 2013.

Answer: Closing Capital: Rs. 1,67,500 OpeningCapital: Rs. 1,56,500 Net Loss: Rs. 7,000

Q8. Miss. Kavita commenced her business with a Capital of Rs. 1,30,000 on 1st April, 2010. Her financial position was as follows as on 31st March, 2011, Cash Rs. 9,120, Stock Rs. 10,250, Bills Payable Rs. 12,880, Creditors Rs. 17,180, Debtors Rs. 31,550, Bills Receivable Rs. 29,120, Premises Rs. 85,750, Vehicles 40,250. (P)Additional Information:1. She brought additional capital Rs. 20,000 on 30th September, 2010. Interest on capital is to be provided at 5% p.a.2. She withdraws Rs. 10,000 for personal use on which interest is to be charged at 6% p.a.3. R.D.D. is to be provided at 21/2% p.a. after providing Bad Debts Rs.1000.4. Depreciate vehicle at 2% and Premises at 4%.Answer: Closing Capital: Rs. 1,75,980 Opening Capital: Rs. 1,30,000 Net Profit: Rs. 23,281

Note : In texbook, the net profit is Rs. 24,581. However, as per our calculations it is Rs. 23,281.

Q9. Mahendra keeps his books by Single Entry system. His position on 1st April, 2012 was as follows: Cash in Hand Rs. 7,900, Cash at Bank Rs. 20,000, Debtors Rs. 18,000, Stock Rs. 29,000, Motor Car Rs. 5,000, Bank Loan Rs. 18,000 and Outstanding Expenses Rs. 2,700. (P)On 1st October, 2012 Mahendra introduced Rs. 10,000 as further capital in the business and withdrew on the same date Rs. 7,000 out of which he spent Rs. 5,0 00 on the purchase of Machinery for the business.On 31st March, 2013 his position was as follows: Cash in Hand Rs. 7,600, Cash at Bank Rs. 22,000, Stock Rs. 30,000, Debtors Rs. 25,700, Furniture Rs. 6,000, Creditors Rs. 25,200 and Prepaid expenses Rs. 200.Prepare a statement showing the Profit or Loss made by him during the year ended 31st March, 2013 and Opening and Closing statement of affairs. Consider the following adjustments also.1. Depreciate Motor Car and Furniture @ 10% p.a. Furniture was purchased on 1st October, 2012.2. Provide Rs. 1,200 for Bad debts and provide 5% R.D.D.3. Goods taken for personal use by Mahendra amounting to Rs. 1,500.4. Provide interest on capital @ 10% p.a.

Answer: Closing Capital: Rs. 71,300 Opening Capital: Rs. 59,200 Net Loss: Rs. 4,045

SAMPLE C

ONTENTSingle Entry System

8 - 249

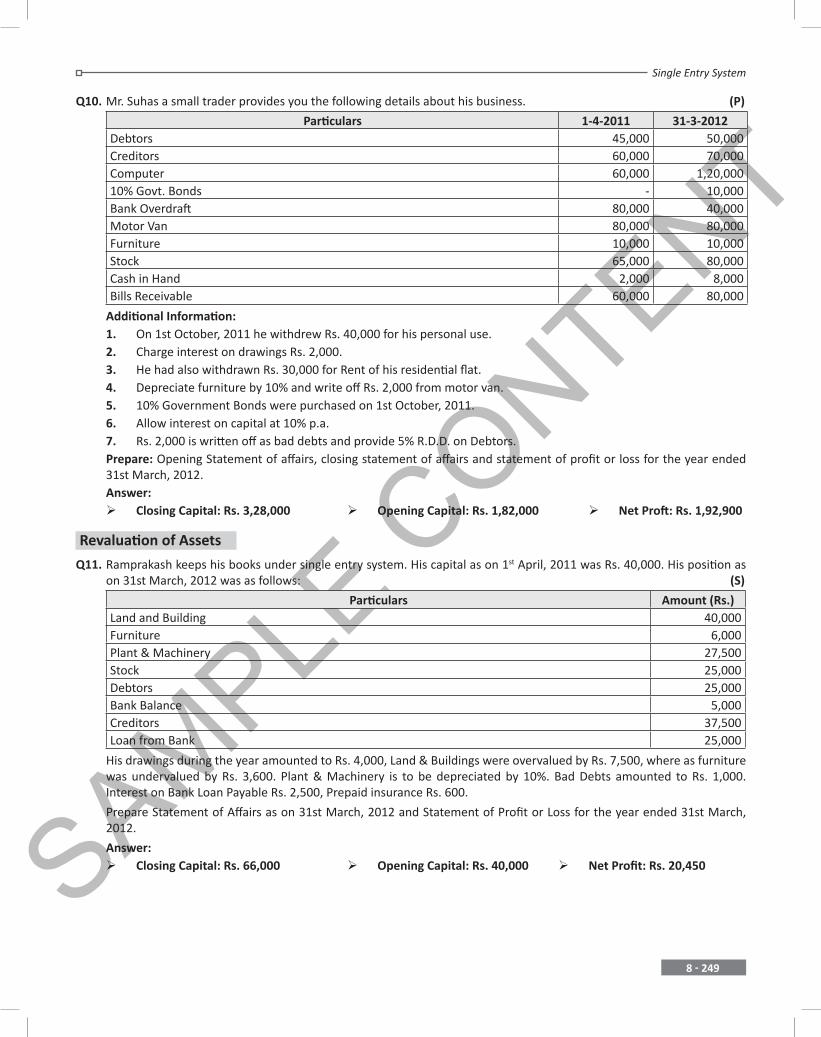

Q10. Mr. Suhas a small trader provides you the following details about his business. (P)

Particulars 1-4-2011 31-3-2012Debtors 45,000 50,000Creditors 60,000 70,000Computer 60,000 1,20,00010% Govt. Bonds - 10,000Bank Overdraft 80,000 40,000Motor Van 80,000 80,000Furniture 10,000 10,000Stock 65,000 80,000Cash in Hand 2,000 8,000Bills Receivable 60,000 80,000

Additional Information:1. On 1st October, 2011 he withdrew Rs. 40,000 for his personal use.2. Charge interest on drawings Rs. 2,000.3. He had also withdrawn Rs. 30,000 for Rent of his residential flat.4. Depreciate furniture by 10% and write off Rs. 2,000 from motor van.5. 10% Government Bonds were purchased on 1st October, 2011.6. Allow interest on capital at 10% p.a.7. Rs. 2,000 is written off as bad debts and provide 5% R.D.D. on Debtors.Prepare: Opening Statement of affairs, closing statement of affairs and statement of profit or loss for the year ended31st March, 2012.Answer: Closing Capital: Rs. 3,28,000 Opening Capital: Rs. 1,82,000 Net Proft: Rs. 1,92,900

Revaluation of Assets

Q11. Ramprakash keeps his books under single entry system. His capital as on 1st April, 2011 was Rs. 40,000. His position as on 31st March, 2012 was as follows: (S)

Particulars Amount (Rs.)Land and Building 40,000Furniture 6,000Plant & Machinery 27,500Stock 25,000Debtors 25,000Bank Balance 5,000Creditors 37,500Loan from Bank 25,000

His drawings during the year amounted to Rs. 4,000, Land & Buildings were overvalued by Rs. 7,500, where as furniture was undervalued by Rs. 3,600. Plant & Machinery is to be depreciated by 10%. Bad Debts amounted to Rs. 1,000. Interest on Bank Loan Payable Rs. 2,500, Prepaid insurance Rs. 600.

Prepare Statement of Affairs as on 31st March, 2012 and Statement of Profit or Loss for the year ended 31st March, 2012.

Answer: Closing Capital: Rs. 66,000 Opening Capital: Rs. 40,000 Net Profit: Rs. 20,450

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 250

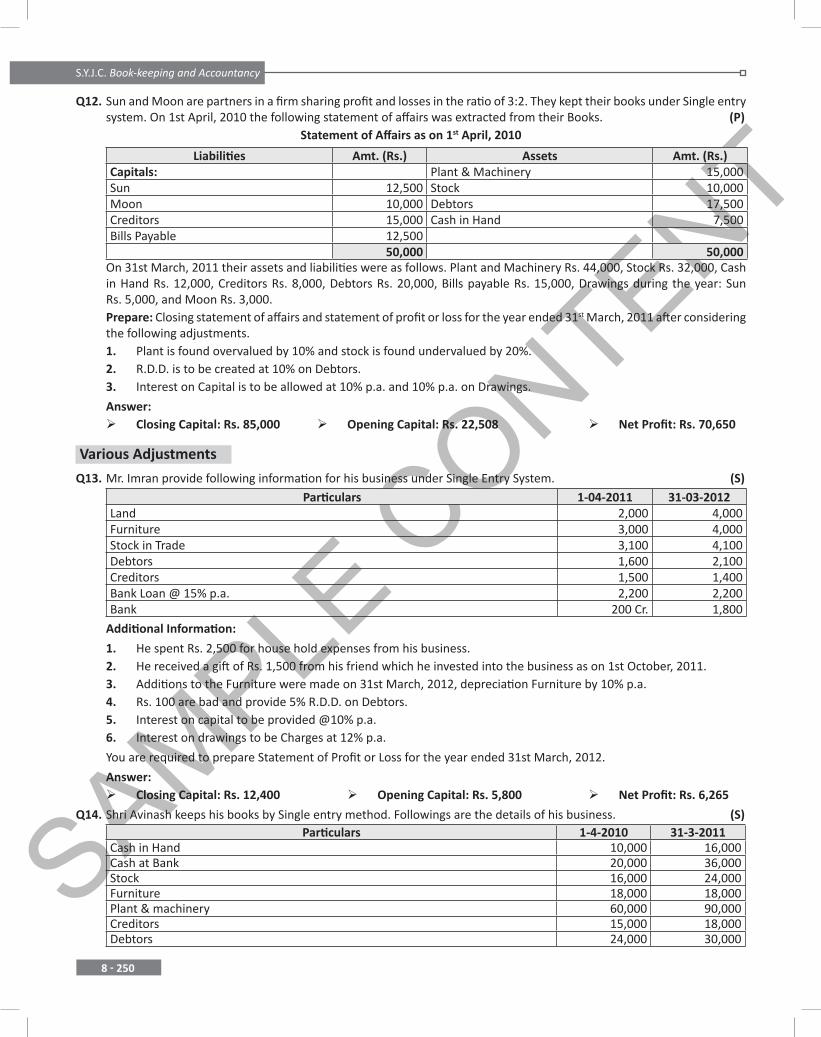

Q12. Sun and Moon are partners in a firm sharing profit and losses in the ratio of 3:2. They kept their books under Single entry system. On 1st April, 2010 the following statement of affairs was extracted from their Books. (P)

Statement of Affairs as on 1st April, 2010

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capitals: Plant & Machinery 15,000Sun 12,500 Stock 10,000Moon 10,000 Debtors 17,500Creditors 15,000 Cash in Hand 7,500Bills Payable 12,500

50,000 50,000On 31st March, 2011 their assets and liabilities were as follows. Plant and Machinery Rs. 44,000, Stock Rs. 32,000, Cash in Hand Rs. 12,000, Creditors Rs. 8,000, Debtors Rs. 20,000, Bills payable Rs. 15,000, Drawings during the year: Sun Rs. 5,000, and Moon Rs. 3,000.

Prepare: Closing statement of affairs and statement of profit or loss for the year ended 31st March, 2011 after considering the following adjustments.

1. Plant is found overvalued by 10% and stock is found undervalued by 20%. 2. R.D.D. is to be created at 10% on Debtors. 3. Interest on Capital is to be allowed at 10% p.a. and 10% p.a. on Drawings.

Answer: Closing Capital: Rs. 85,000 Opening Capital: Rs. 22,508 Net Profit: Rs. 70,650

Various Adjustments

Q13. Mr. Imran provide following information for his business under Single Entry System. (S)Particulars 1-04-2011 31-03-2012

Land 2,000 4,000Furniture 3,000 4,000Stock in Trade 3,100 4,100Debtors 1,600 2,100Creditors 1,500 1,400Bank Loan @ 15% p.a. 2,200 2,200Bank 200 Cr. 1,800

Additional Information:

1. He spent Rs. 2,500 for house hold expenses from his business. 2. He received a gift of Rs. 1,500 from his friend which he invested into the business as on 1st October, 2011. 3. Additions to the Furniture were made on 31st March, 2012, depreciation Furniture by 10% p.a. 4. Rs. 100 are bad and provide 5% R.D.D. on Debtors. 5. Interest on capital to be provided @10% p.a. 6. Interest on drawings to be Charges at 12% p.a.

You are required to prepare Statement of Profit or Loss for the year ended 31st March, 2012.

Answer: Closing Capital: Rs. 12,400 Opening Capital: Rs. 5,800 Net Profit: Rs. 6,265

Q14. Shri Avinash keeps his books by Single entry method. Followings are the details of his business. (S)Particulars 1-4-2010 31-3-2011

Cash in Hand 10,000 16,000Cash at Bank 20,000 36,000Stock 16,000 24,000Furniture 18,000 18,000Plant & machinery 60,000 90,000Creditors 15,000 18,000Debtors 24,000 30,000

SAMPLE C

ONTENTSingle Entry System

8 - 251

During the year he has withdrawn Rs. 10,000 for his private purpose and goods of Rs. 2,000 for household use. On 1st October, 2010 he sold his household Furniture for Rs. 2,000 and deposited same amount in business Bank A/c.

Provide depreciate on machinery at 10% p.a. (assuming additions were made on 1st October, 2010) and Furniture at 5%. Prepare Statement of Profit or Loss for the year ended 31st March 2011.

Answer: Closing Capital: Rs. 1,96,000 Opening Capital: Rs. 1,33,000 Net Profit: Rs. 64,600

Partnership Firm

Q15. Sanika and Monika are partners sharing Profit & loss in the ratio of 2:1. You are required to prepare a Statement of Affairs as on 31st March, 2012 and Statement of Profit or Loss for the year ended 31st March, 2012. (S)

Statement of Affairs as on 31st March, 2011

Liabilities Amount (Rs.) Assets Amount (Rs.)Creditors 16,000 Cash at Bank 3,000Bills Payable 3,000 Bill Receivable 6,000Capital : Sanika 30,000 Debtors 12,000

Monika 15,000 Stock 8,000Furniture 5,000Machinery 10,000Building 20,000

64,000 64,000

On 31st March, 2012 the following balances were extracted.

Creditors Rs. 18,000, Bills Payable Rs. 7,000, Stock Rs. 16,000, Bills Receivable Rs. 8,500, Cash at Bank Rs. 8,000, Debtors Rs. 17,500

Additional Information:

1. Sanika and Monika had withdrawn from the firm for personal use Rs. 4,500 and Rs. 3,500 respectively.

2. They had brought in additional capital of Rs. 2,500 and Rs. 1,500 respectively.

3. Provide depreciation on Building at 5% p.a. and Machinery and Furniture at 10% p.a.

4. Allow interest at 10% p.a. on capital.

5. Charge interest on drawings of Sanika Rs. 300 and Monika Rs. 200

Answer: Combined Closing Capital: Rs. 60,000 Opening Capital: Rs. 45,000 Net Profit: Rs. 12,500

Q16. A and B are partners sharing profits and losses in the ratio 3:2. Following are the details of their business as per the singleentry system. (S)

Particulars 1-4-2011 31-3-2012Cash in hand 1,000 2,000Cash at Bank 2,000 4,000Land & Building 20,000 20,000Plant & Machinery 2,000 2,000Stock in Trade 5,000 7,000Bills Receivable 1,000 1,500Bills Payable 1,000 2,500Sundry Debtors 3,000 4,000Sundry Creditors 3,000 2,000

Additional information:1. Interest on Capital is to be allowed at 10%.2. Plant & Machinery is to be depreciated by 10% p.a. and Land & Building by 5% p.a.3. Creditors are undervalued by Rs. 1,000.4. Provide R.D.D. at 5% on Debtors.5. A and B brought additional capital in the firm Rs. 2,000 and Rs. 3,000 respectively.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 252

6. Overvaluation of Bills Payable Rs. 500.Prepare Statement of Profit or Loss for the year ended 31st March, 2012

Answer: Combined Closing Capital: Rs. 36,000 Opening Capital: A - Rs. 18,000 Net Profit: Rs. 3,900 B - Rs. 12,000

Q17. A and B are in Partnership. Their Capitals on 1st April, 2010 were Rs. 30,000 each. The assets and liabilities as on 31st March, 2011 were as follows. Cash in hand Rs. 2,400, Cash at bank Rs. 16,000, Bills Receivable Rs. 4,000, Debtors Rs. 28,600, Stock Rs. 26,000. Machinery Rs. 14,000, Furniture Rs. 8,000, Bills Payable Rs. 3,000. Sundry Creditors Rs. 6,000 Outstanding salary Rs. 800. (P)

Additional Information:

1. Provide Rs. 600 as Bad Debts and 5% R.D.D.

2. Depreciate furniture @ 5%p.a. and Machinery@10% p.a.

3. Stock is found undervalued by Rs. 2,000.

4. Sundry creditors are found overvalued by Rs. 1,000.

5. Prepaid insurance Rs. 2,000.

6. Additional capital introduced by partners Rs. 4,000 each.

7. Drawings of ‘A’ Rs. 3,000 and ‘B’ Rs. 2,000

[Calculate the profit for the year ended 31st March, 2011.]

Answer: Closing Capital: Rs. 89,200 Net Proft: Rs. 27,400

Note: In textbook, A’s share of net profit is Rs. 18,840 and B’s share is Rs. 12,560. However, the profit sharing ratio is not given. Thus, we need to assume as 1:1. Thus, A & B’s share is Rs. 13, 700 each.

Q18. Asha and Usha were partners sharing profits and losses in the ratio of 2:1. Prepare their statement Profit or loss for the year ended 31st March, 2012 from the following Statement of Affairs as on 31st March, 2011. (P)

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Creditor 33,000 Cash at Bank 6,000Bills Payable 9,000 Cash in Hand 2,000Capital Building 41,000Asha 62,000 Machinery 21,000Usha 32,000 Furniture 10,000

Stock 18,000Debtors 25,000Bills Receivable 13,000

1,36,000 1,36,000

The assets and liabilities as on 31st March, 2012 were:

Sundry Creditors Rs. 35,000, Bills Receivable Rs. 18,000, Bills payable Rs. 15,000, Cash in hand Rs. 3,000, Stock Rs. 32,000, Cash of Bank Rs. 6,000, Debtors Rs. 38,000. There were no changes in fixed assets.

Further information:

1. Asha and Usha had drawn Rs. 10,000 and Rs. 8,000 respectively for personal use.

2. They also brought additional capital of Rs. 6,000 and Rs. 4,000 respectively.

3. Building to be depreciated by 5% and Machinery and Furniture at 10%.

4. Charge interest at 10% p.a. on opening capitals and allow interest on drawings of Asha and Usha of Rs. 700 andRs. 500 respectively.

Answer: Closing Capital: Rs. 1,19,000 Opening Capital: Rs. 94,000 Net Proft: Rs. 19,650

SAMPLE C

ONTENTSingle Entry System

8 - 253

Alternative Method

Q19. Mr. Prakash keeps his books in Single Entry System. On 1st April, 2011 his position was as follows : Creditors Rs. 40,000, Debtors Rs. 80,000, Cash in Hand Rs. 600, Machinery Rs. 40,000, Cash at Bank Rs. 21,000, Stock Rs. 20,000.

On 31st March, 2012 his position was as follows: Creditors Rs. 70,000, Cash at Bank Rs. 44,000, Cash in hand 1,000, Debtors Rs. 98,000, Stock Rs. 24,000, Machinery Rs. 90,000. He had withdrawn Rs. 1,000 every month for his personal expenses. He introduced Rs. 50,000 as an additional Capital on 1st August, 2011. He purchased additional Machinery for

business worth Rs. 50,000 on 31st October, 2011. (S) Adjustments: 1. Depreciate Machinery at 10% p.a. 2. Provide R.D.D. at 2.5% on debtors. You are required to prepare Statement of Profit or Loss. Answer: Closing Capital: Rs. 1,87,000 Opening Capital: Rs. 1,21,600 Net Profit: Rs. 18,450

Q20. On 1st April, 2011 X Y and Z started their business in Partnership and decided to share profits and losses in the ratio of 5:3:2. They introduced capital as X Rs. 50,000, Y Rs. 30,000, Z Rs. 20,000. (S)

On 31st March 2012 their financial position was as follows: Cash in hand Rs. 2,500, Bank Overdraft Rs. 15,000, Sundry Creditors Rs. 10,200, Sundry Debtors Rs. 17,300, Bills Payable

Rs. 3,500, Bills Receivable Rs. 4,000, Stock Rs. 20,400, Plant and Machinery Rs. 30,000, Furniture Rs. 9,800, Loan from bank Rs. 20,000, Building Rs. 70,000, Outstanding Salary Rs. 1,000

During the year the partners have withdrawn cash from the business for personal use X: Rs. 4,500, Y: Rs. 3,500 and Z: Rs. 6,900.

Additional Information: 1. Bad debts Rs. 300 are to be written off 2. Stock was overvalued by Rs. 400 and furniture was undervalued by Rs. 200. 3. Interest on bank loan was Rs. 1,000 payable. 4. Provide 10% R.D.D. on Debtors. 5. Salary Rs. 500 per month payable to Z. Prepare Statement of Profit or Loss for the year ended 31st March, 2012. Answer: Combined Closing Capital: Rs. 1,01,000 Opening Capital: Rs. 1,00,100

Net Profit: X : Rs. 5,000 Y: Rs. 3,000 Z: Rs. 2,000

Section II – Board Problems

Q1. Following incomplete information is available from the records maintained by Mr. Premnath. (March 2011)

Particular 1.4.2009 Amount (Rs.) 31.3.2010 Amount (Rs.) Cash Balance 12,000 13,000Bank Balance 26,000 30,000Sundry Debtors 20,000 26,000Stock 24,000 26,000Furniture 24,000 24,000Creditors 20,000 20,00010% Bank Loan 20,000 20,000

Additional Information

1. Mr. Premnath introduced additional capital in the business amounted to Rs. 15,000 on 1st January, 2010. 2. He has paid life insurance premium Rs.10, 000 from the business account and withdrawn goods worth Rs. 5,000

for his personal use. 3. Write off Rs. 1,000 as bad debts and maintain reserve for doubtful debts at 5% on remaining debtors. 4. Provide depreciation at 5% p.a. on Furniture. 5. The closing balance of sundry creditors has been overvalued by Rs. 2, 000 in the books of account

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 254

6. Provide Interest on Capital and Bank Loan @ 10% p.a.

Answer: Closing Capital: Rs. 79,000 Opening Capital: Rs. 66,000 Net Profit: Rs. 2,575

Q2. Mr. Anand gives you the following information: (October 2011)

Particular 31.3.2003 Amount (Rs.) 31.3.2004 Amount (Rs.)Cash 5,000 6,000Bank 15,000 18,000Debtors 10,000 8,000Stock 8,000 12,000Furniture 12,000 12,000Creditors 2,000 6,000Bill Payable 2,000 -

During the year Mr. Anand introduced Rs. 4,000 as further capital in the business.He has withdrawn cash Rs. 20,000 out of which he spent Rs. 15,000 on 1.10.2003 for purchase of scooter for business use.Adjustments :(1) Depreciated furniture @ 10% p.a.(2) Depreciated scooter @ 20% p.a.(3) Create provision for doubtful debts @ 5% of the debtor as on 31-03-2004(4) Provide interest on capital at 10% p.a.Prepare:(1) Statements of Affairs as on 31.03.2003(2) Statements of Affairs as on 31.03.2004.(3) Statements of Profit & Loss for the year ending 31.03.2004.Answer: Closing Capital: Rs. 61,900 Opening Capital: Rs. 46,000 Net Profit: Rs. 27,300

Q3. Mr. Prabhakar is a retail trader. He had no proper methods of accounting. But the following information is made available to you. (March 2012)

Particular 01.4.2009 Amount (Rs.) 31.3.2010 Amount (Rs.)Sundry Debtors 45,000 50,000Sundry Creditors 60,000 70,000Bank Overdraft 80,000 40,000Stock 65,000 80,000Cash in Hand 2,000 8,000Bills receivable 60,000 80,000Furniture 10,000 10,000Motor Van 80,000 80,000Computer 60,000 1,20,00010% Govt. Bonds – 10,000

Adjustments:1. On 1st October, 2009 Mr. Prabhakar had withdrawn Rs. 40,000 for his personal use2. 10% Government Bonds were purchased of Rs. 10,000 on 1st October, 2009.3. He had also withdrawn Rs. 30,000 for his daughter’s marriage.4. Depreciate furniture by 10% and write off Rs. 2,000 from motor van.5. Rs. 2,000 is written off as bad debts and provide 5% R.D.D. on debtors.6. Allow interest on capital at 10% p.a.7. Charge interest on drawings Rs. 2,000.Prepare after taking into consideration the adjustments:a. Opening Statement of affairs of 01.04.2009,b. Closing statement of affairs of 31.03.2010c. Statement showing Profit and Loss for the year ended on 31.03.2010.

Answer: Closing Capital: Rs. 3,28,000 Opening Capital: Rs. 1,82,000 Net Profit: Rs. 1,92,900

SAMPLE C

ONTENTSingle Entry System

8 - 255

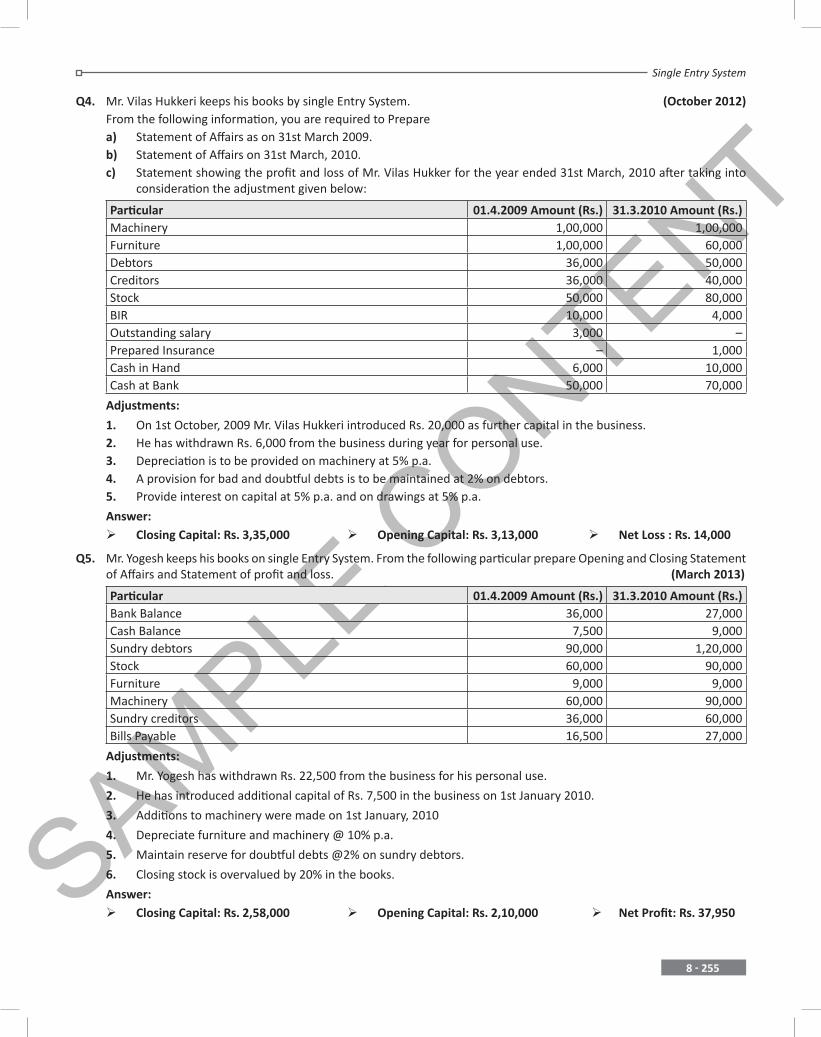

Q4. Mr. Vilas Hukkeri keeps his books by single Entry System. (October 2012) From the following information, you are required to Prepare a) Statement of Affairs as on 31st March 2009. b) Statement of Affairs on 31st March, 2010. c) Statement showing the profit and loss of Mr. Vilas Hukker for the year ended 31st March, 2010 after taking into

consideration the adjustment given below:

Particular 01.4.2009 Amount (Rs.) 31.3.2010 Amount (Rs.)Machinery 1,00,000 1,00,000Furniture 1,00,000 60,000Debtors 36,000 50,000Creditors 36,000 40,000Stock 50,000 80,000BIR 10,000 4,000Outstanding salary 3,000 –Prepared Insurance – 1,000Cash in Hand 6,000 10,000Cash at Bank 50,000 70,000

Adjustments:

1. On 1st October, 2009 Mr. Vilas Hukkeri introduced Rs. 20,000 as further capital in the business. 2. He has withdrawn Rs. 6,000 from the business during year for personal use. 3. Depreciation is to be provided on machinery at 5% p.a. 4. A provision for bad and doubtful debts is to be maintained at 2% on debtors. 5. Provide interest on capital at 5% p.a. and on drawings at 5% p.a.

Answer: Closing Capital: Rs. 3,35,000 Opening Capital: Rs. 3,13,000 Net Loss : Rs. 14,000

Q5. Mr. Yogesh keeps his books on single Entry System. From the following particular prepare Opening and Closing Statement of Affairs and Statement of profit and loss. (March 2013)

Particular 01.4.2009 Amount (Rs.) 31.3.2010 Amount (Rs.)Bank Balance 36,000 27,000Cash Balance 7,500 9,000Sundry debtors 90,000 1,20,000Stock 60,000 90,000Furniture 9,000 9,000Machinery 60,000 90,000Sundry creditors 36,000 60,000Bills Payable 16,500 27,000

Adjustments:

1. Mr. Yogesh has withdrawn Rs. 22,500 from the business for his personal use.

2. He has introduced additional capital of Rs. 7,500 in the business on 1st January 2010.

3. Additions to machinery were made on 1st January, 2010

4. Depreciate furniture and machinery @ 10% p.a.

5. Maintain reserve for doubtful debts @2% on sundry debtors.

6. Closing stock is overvalued by 20% in the books.

Answer: Closing Capital: Rs. 2,58,000 Opening Capital: Rs. 2,10,000 Net Profit: Rs. 37,950

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 256

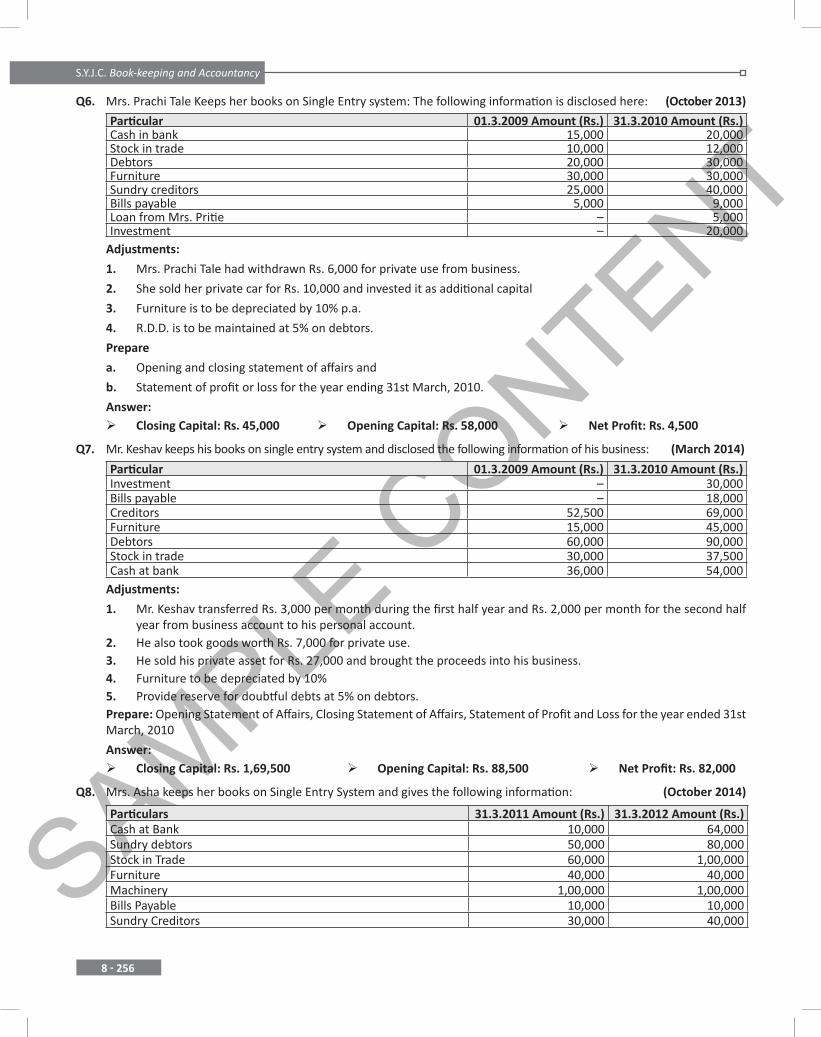

Q6. Mrs. Prachi Tale Keeps her books on Single Entry system: The following information is disclosed here: (October 2013)

Particular 01.3.2009 Amount (Rs.) 31.3.2010 Amount (Rs.)Cash in bank 15,000 20,000Stock in trade 10,000 12,000Debtors 20,000 30,000Furniture 30,000 30,000Sundry creditors 25,000 40,000Bills payable 5,000 9,000Loan from Mrs. Pritie – 5,000Investment – 20,000

Adjustments:

1. Mrs. Prachi Tale had withdrawn Rs. 6,000 for private use from business.

2. She sold her private car for Rs. 10,000 and invested it as additional capital

3. Furniture is to be depreciated by 10% p.a.

4. R.D.D. is to be maintained at 5% on debtors.

Prepare

a. Opening and closing statement of affairs and

b. Statement of profit or loss for the year ending 31st March, 2010.

Answer: Closing Capital: Rs. 45,000 Opening Capital: Rs. 58,000 Net Profit: Rs. 4,500

Q7. Mr. Keshav keeps his books on single entry system and disclosed the following information of his business: (March 2014)

Particular 01.3.2009 Amount (Rs.) 31.3.2010 Amount (Rs.)Investment – 30,000Bills payable – 18,000Creditors 52,500 69,000Furniture 15,000 45,000Debtors 60,000 90,000Stock in trade 30,000 37,500Cash at bank 36,000 54,000

Adjustments:

1. Mr. Keshav transferred Rs. 3,000 per month during the first half year and Rs. 2,000 per month for the second half year from business account to his personal account.

2. He also took goods worth Rs. 7,000 for private use. 3. He sold his private asset for Rs. 27,000 and brought the proceeds into his business. 4. Furniture to be depreciated by 10% 5. Provide reserve for doubtful debts at 5% on debtors. Prepare: Opening Statement of Affairs, Closing Statement of Affairs, Statement of Profit and Loss for the year ended 31st

March, 2010

Answer: Closing Capital: Rs. 1,69,500 Opening Capital: Rs. 88,500 Net Profit: Rs. 82,000

Q8. Mrs. Asha keeps her books on Single Entry System and gives the following information: (October 2014)

Particulars 31.3.2011 Amount (Rs.) 31.3.2012 Amount (Rs.)Cash at Bank 10,000 64,000Sundry debtors 50,000 80,000Stock in Trade 60,000 1,00,000Furniture 40,000 40,000Machinery 1,00,000 1,00,000Bills Payable 10,000 10,000Sundry Creditors 30,000 40,000

SAMPLE C

ONTENTSingle Entry System

8 - 257

Mrs. Asha withdrew from business Rs. 30,000 for personal use. She further introduced fresh capital of Rs. 50,000. Depreciation is to be charged @ 10% p.a. on furniture and machinery. Prepare: (a) Statement of affairs as on 31.3.2011(b) Statement of affairs as on 31.3.2012(c) Statement of Profit or Loss for the year ending 31.3.2012.

Answer: Closing Capital: Rs. 3,34,000 Opening Capital: Rs. 2,20,000 Net Profit: Rs. 80,000

Q9. Mr. Anil keeps his books by single entry method. Following are the details of his business (March 2015)

Particulars 01.04.2012Amount (Rs.)

31.03.2013Amount (Rs.)

Cash in hand 10,000 16,000Cash at bank 20,000 36,000Stock 16,000 24,000Furniture 18,000 18,000Plant and Machinery 60,000 90,000Creditors 15,000 18,000Debtors 24,000 30,000

During the year, Mr.Anil has withdrawn Rs.10,000 for his private purpose and bought goods of Rs.2,000 for household use.

On 1st October, 2012, he sold his household furniture for Rs.2,000 and deposited the same amount in the business bank account.

Provide depreciation on machinery @10% p.a. (assuming additions were made on 1st October, 2012) and on furniture @ 5%.

Prepare:a. Opening Statement of Affairsb. Closing Statement of Affairsc. Statement of Profit or Loss for the year ended 31st March, 2013.

Answer: Closing Capital: Rs. 1,96,000 Opening Capital: Rs. 1,33,000 Net Profit: Rs. 64,600

Q10. Shree Rajesh keeps his books by Single Entry Method. Following are the details of his business. (October 2015)

Particulars 01.04.2012Amount (Rs.)

31.03.2013Amount (Rs.)

Cash in hand 10,000 16,000Cash at bank 20,000 36,000Stock 16,000 24,000Furniture 18,000 18,000Plant and Machinery 60,000 90,000Creditors 15,000 18,000Debtors 24,000 30,000

During the year Shri Rajesh has withdrawn Rs. 10,000 for his private purpose and taken goods of Rs. 2,000 for household use. On 1st October 2012, he sold his household furniture for Rs. 2,000 and deposited the same amount in the business bank account. Provide depreciation on Machinery at 10% p.a. (assuming additions were made on 1st October, 2012) and furniture at 5% p. a.

Prepare: Opening and closing statement of affairs and Statement of Profit or loss for the year ended 31st March, 2013.

Answer: Closing Capital: Rs. 1,96,000 Opening Capital: Rs. 1,33,000 Net Profit: Rs. 64,600

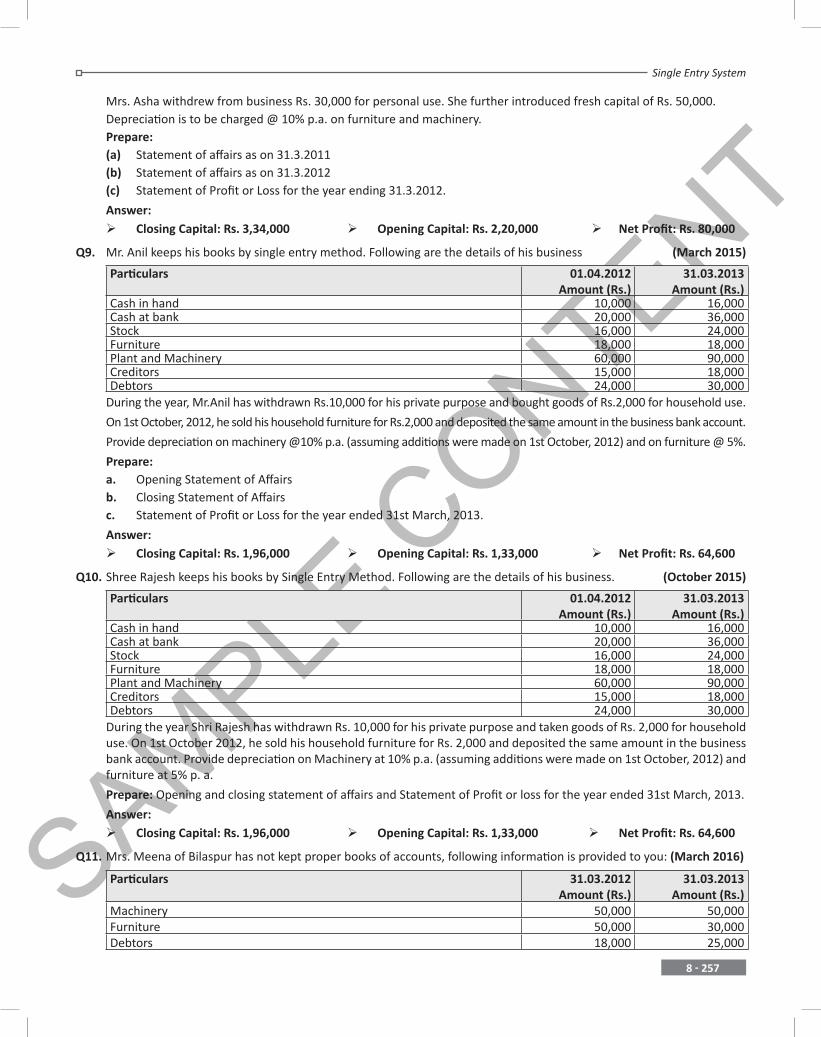

Q11. Mrs. Meena of Bilaspur has not kept proper books of accounts, following information is provided to you: (March 2016)

Particulars 31.03.2012Amount (Rs.)

31.03.2013Amount (Rs.)

Machinery 50,000 50,000Furniture 50,000 30,000Debtors 18,000 25,000

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 258

Particulars 31.03.2012Amount (Rs.)

31.03.2013Amount (Rs.)

Creditors 18,000 20,000Stock 30,000 42,000Outstanding Expenses 1,500 –Pre-paid Expenses – 500Cash at Bank 28,000 40,000

Further information:

(1) Mrs. Meena introduced additional capital as on 1st October, 2012 by selling her personal car for Rs. 10,000.

(2) She paid her daughter’s college fees from business bank account Rs. 3,000.

(3) Depreciate machinery by 5% p.a.

(4) Provide 2% on debtors for Bad and Doubtful debts.

(5) Interest on capital is to be provided @ 5% p.a. and on drawings @ 5% p.a.

Prepare:

a) Opening Statement of Affairs

b) Closing Statements of Affairs

c) Statements of profit and loss for the year ending 31.03.2013.

Answer: Opening Capital: Rs. 1,56,500 Closing Capital: Rs. 1,67,500 Net Profit: Rs. 7,000

Q12. Mrs. Ankita keeps her books under Single Entry System and gives the following information:

Particulars 01-04-2011(Rs.)

31-03-2012(Rs.)

Investments − 12,000Bank Overdraft − 10,000Bills Payable 5,000 8,000Creditors 26,500 31,500Furniture 9,000 19,000Debtors 35,000 50,000Stock in Trade 15,000 19,000Bank Balance 18,000 28,000

Mrs. Ankita withdrew Rs. 4,000 for her personal use. She received Rs. 15,000 from her father as gift, which she brought into the business.

Additional furniture was purchased on 1st October 2011. Depreciate furniture by 10% p.a.

Write off Rs. 1,000 as bad debts and provide 5% R.D.D. on debtors.

Find the Profit or Loss of her business for the year ended 31st March, 2012. (July 2016)

Answer:

Opening Capital = Rs. 45,500 Closing Capital = Rs. 78,500 Net Profit for the Year = Rs. 17,150

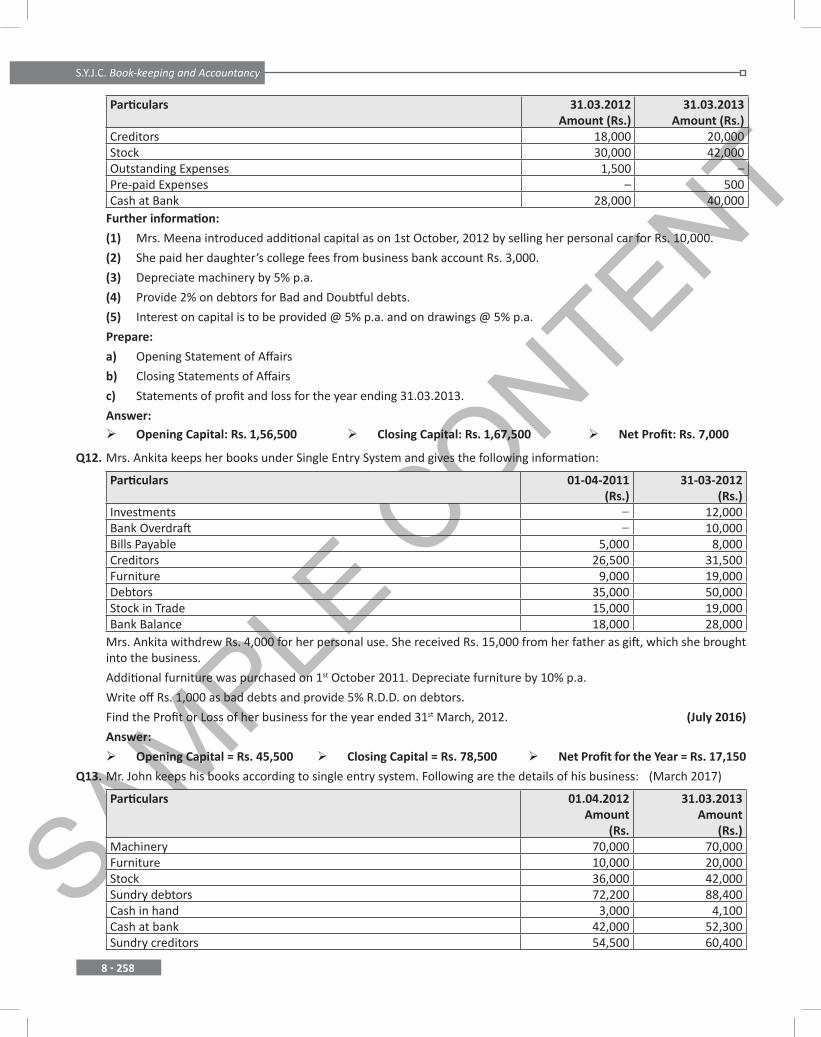

Q13. Mr. John keeps his books according to single entry system. Following are the details of his business: (March 2017)

Particulars 01.04.2012Amount

(Rs.

31.03.2013Amount

(Rs.)Machinery 70,000 70,000Furniture 10,000 20,000Stock 36,000 42,000Sundry debtors 72,200 88,400Cash in hand 3,000 4,100Cash at bank 42,000 52,300Sundry creditors 54,500 60,400

SAMPLE C

ONTENTSingle Entry System

8 - 259

Additional information:

(1) Mr. John had introduced Rs. 20,000 as additional capital on 1st October, 2012.

(2) Mr. John had withdrawn Rs. 15,000 for his personal use during the year.

(3) Additions to furniture were made on 1st October, 2012.

(4) Depreciate machinery at 10% p. a.and furniture at 20% p. a.

Prepare:

(1) Opening and Closing Statement of Affairs.

(2) Statement of Profit or Loss for the year ending on 31st March, 2013

Answer:

Opening Capital = Rs. 1,78,700 Closing Capital = Rs. 2,16,400 Net Profit for the Year = Rs. 22,700

Q14. Mr. Govind keeps his books on single entry system and disclosed the following information of his business: (July 2017)

Particulars 01.04.2012Amount

(Rs.)

31.03.2013Amount

(Rs.)Investments - 30,000Bills Payable - 18,000Creditors 52,500 69,000Furniture 15,000 15,000Debtors 60,000 90,000Stock in Trade 30,000 37,500Cash at Bank 36,000 54,000

Additional information:

(1) Mr. Govind transferred Rs. 300 per month during first half year and Rs. 200 each month for the remaining period from his business to his personal account. He also took goods of Rs. 700 for private use.

(2) Mr. Govind sold his personal assets for Rs. 7,000 and brought the proceeds into his business.

(3) Furniture is to be depreciated by 10%.

(4) Provide R.D.D. at 5% on debtors.

Prepare:

Opening and Closing statement of affairs and statement of Profit or Loss for the year ended 31st March, 2013.

Answer :

Opening Capital = Rs. 88,500 Closing Capital = Rs. 1,39,500 Net Profit for the Year = Rs. 41,700

Q15. Miss Kalpana started her business with a capital of Rs.,30,000 on 1st April, 2015.

Her financial position on 31st March 2016 was as follows : (March 2018)

Amount (Rs.) Amount (Rs.)Cash 9,120 Prepaid insurance 550Stock 10.250 Bills receivable 29,120Bills payable 12,880 Premises 85,800Creditors 17,180 Vehicles 40,200Debtors 31,000

Additional information :

(1) Miss Kalpana brought additional capital of Rs. 20,000 on 30th September, 2015.

(2) Interest on capital is to be allowed at 5% p.a.

(3) She withdrew Rs. 10,000 for personal use.

(4) Reserve for doubtful debts is to be provided at 21/2% after writing off bad debts of Rs.. 1,000.

(5) Depreciate vehicles at 10% p.a. and premises at 5% p.a.

(6) Creditors were overvalued by Rs2,180.

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 260

Prepare :

(1) Closing Statement of Affairs as on 31.03.2016.

(2) Statement of Profit or Loss for the year ended 31.03.2016.

Answer:

Closing Capital = Rs. 1,75,980 Net Profit for the Year = Rs. 21,100

Q16. Mrs. Sunita keeps her books on Single Entry System and gives the following information : (July 2018)

Particulars 01.04.2015 Amount (Rs.)

31.03.2016 Amount (Rs..)

Cash at BankDebtorsStockPlantBuildingBills payableCreditors

10,00050,00060,00040,000

1,00,00010,00030,000

64,00080,000

1,00,00040,000

1,00,00010,00040,000

Additional information :

Mrs. Suntia withdrew from business Rs. 30,000 for personal use and further introduced fresh capital of Rs. 50,000. Depreciation is to be charged @ 10% p.a. on plant and building.

Prepare:

(a) Statement of Affairs as on 01.04.2015.

(b) Statement of Affairs as on 31.03.2016.

(c) Statement of Profit or Loss for the year ending 31.03.2016. (July 2018)

Answer:

Opening Capital = Rs. 2,20,000 Closing Capital = Rs. 3,34,000 Net Profit for the year = Rs. 80,000

Section III – Homework Problems

Drawings + Additional capital given

Q1. Cain started his business on 1st April 2015 with a capital of Rs. 25,000. On 1st October 2015 he introduced a further capital of Rs. 25,000. His liabilities were as follows on 31st March, 2016.

Particulars Amount (Rs.)Stocks 20,000Debtors 24,000Cash 16,000Creditors 18,700Bills Payable 6,300

He withdrew Rs. 10,000 for personal use on 1st December, 2015. Ascertain profit and loss during the year.

Answer: Closing Capital: Rs. 35,000 Net Loss: Rs.5,000

Q2. Gopal keeps his books under single entry system. His assets and liabilities were as follows:

Particulars 1st April 2015 31st March 2016Furniture 8,000 10,000Machinery 15,000 25,000Stocks 8,000 6,500Debtors 18,000 18,300Cash 6,000 10,200Creditors 25,000 10,000Bank loan – 10,000

SAMPLE C

ONTENTSingle Entry System

8 - 261

On 1st July Gopal introduced further capital of Rs. 20,000. During the year, he also withdrew Rs. 1,000 p.m. for his personal use. Ascertain the profit and loss for the year ended 31st March, 2016.

Answer: Opening Capital: Rs.30,000 Closing Capital: Rs.50,000 Net Profit: Rs.12,000

Depreciation + Bad debts + R.D.D.

Q3. Rahul keeps his books under Single Entry System and gives the following information:

Particulars 31-Mar-12 31-Mar-13Debtors 58,000 75,400 Creditors 25,000 35,000 Furniture 20,000 30,000 Bills Payable 500 1,500 Stock 4,000 14,200 Cash 15,000 12,000 Bank 12,000 15,000 Investments 25,000 25,000

1. Additional furniture was bought on September 30, 2012. 2. Charge depreciation at 10% on furniture. 3. Write off bad debts of Rs. 1,000 and then provide RDD at 5% 4. Additional capital introduced during the year of Rs. 12,000. 5. Rahul withdrew Rs. 5,000 for his personal use. Find out the profit or loss for the business for the year ended 31st March, 2013.

Answer: Opening Capital: Rs. 1,08,500 Closing Capital: Rs. 1,35,100 Net Profit: Rs. 12,380

Q4. Maru keeps his books under Single Entry System and gives the following information:

Particulars 31-Mar-12 31-Mar-13Debtors 20,000 30,000 Creditors 5,000 2,000 Furniture 40,000 40,000 Bills Payable 2,000 3,000 Stock 25,000 65,000 Cash 5,000 15,000 Bank 10,000 12,000 Machinery 80,000 1,00,000

1. Additional machinery was bought on 30th September, 2012.

2. Charge depreciation at 10% on furniture and 5% on machinery.

3. Write off bad debts of Rs. 2,000 and then provide RDD at 5%.

4. Additional capital introduced during the year of Rs. 15,000.

5. Maru withdrew Rs. 6,000 for his personal use.

Find out the profit or loss for the business for the year ended 31st March, 2013.

Answer: Opening Capital: Rs. 1,73,000 Closing Capital: Rs. 2,57,000 Net Profit: Rs. 63,100

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 262

Q5. Dipesh keeps his books under single entry system. His assets and liabilities were as follows.

Particulars 1st April 2015 31st March 2016Land & building 40,000 40,000Furniture 12,000 14,000Machinery 25,000 23,500Stocks 10,000 12,000Debtors 12,000 18,000Cash balance 5,000 10,000Bank balance 12,000 35,000Creditors 18,000 28,000Bank overdraft 22,000 22,000

Additional information

1. He received Rs. 5,000 from his father as gift ,which he brought into the business 2. He also withdrew Rs. 25,000 for personal use. 3. Depreciate land & building by 10%. 4. Additional furniture Rs. 2,000 was purchased on 1st October, 2015. Depreciate furniture by 2.5% 5. Provide Rs.1,500 as bad debts and 5% as R.D.D.

Answer: Opening capital: Rs.76,000 Closing Capital: Rs. 1,02,500 Net profit: Rs.39,850

Interest on capital and interest on drawing

Q6. Mehta maintains his books under Single Entry System and provides the following information:

Particulars 31-Mar-12 31-Mar-13Cash 2,000 5,000 Bank 16,000 12,000 Motor Car 20,000 20,000 Bills Payable 5,000 10,000 Furniture 10,000 10,000 Stock 15,000 32,000 10% Government Bonds - 10,000 Creditors 20,000 25,000 Debtors 25,000 40,000

1. Mehta brought in cash of Rs. 20,000 on September 30, 2012. Provide interest on capital at 6% p.a.

2. He withdrew Rs. 5000 during the year. Provide interest on drawings at 5% p.a.

3. Government bonds were purchased on July 1, 2012.

4. Depreciate motor car and furniture at 10%.

5. Provide RDD at 5% on debtors.

Answer: Opening Capital: Rs. 63,000 Closing Capital: Rs. 94,000 Net Profit: Rs. 7,495

Q7. Shanta started her business on 1st April, 2012 with Rs. 23,000 cash. On 31st March, 2013 her position was as follows: Furniture Rs. 4,000, Stock Rs. 20,000, Cash Rs. 12,000, Debtors Rs. 23,000, Creditors Rs. 13,000 and Bank Rs. 2,000 Prepare Statement of Profit and Loss for the year ended 31st March, 2013 considering the following: 1. Depreciate furniture at 10% p.a. Furniture was bought on 1st October, 2012. 2. Write off bad debts of Rs. 1,000 and provide RDD at 5% on balance. 3. Goods taken by Shanta of Rs. 2,000 for personal use. 4. Charge interest on drawings at 7% p.a.

Answer: Closing Capital: Rs. 48,000 Net Profit: Rs. 24,770

SAMPLE C

ONTENTSingle Entry System

8 - 263

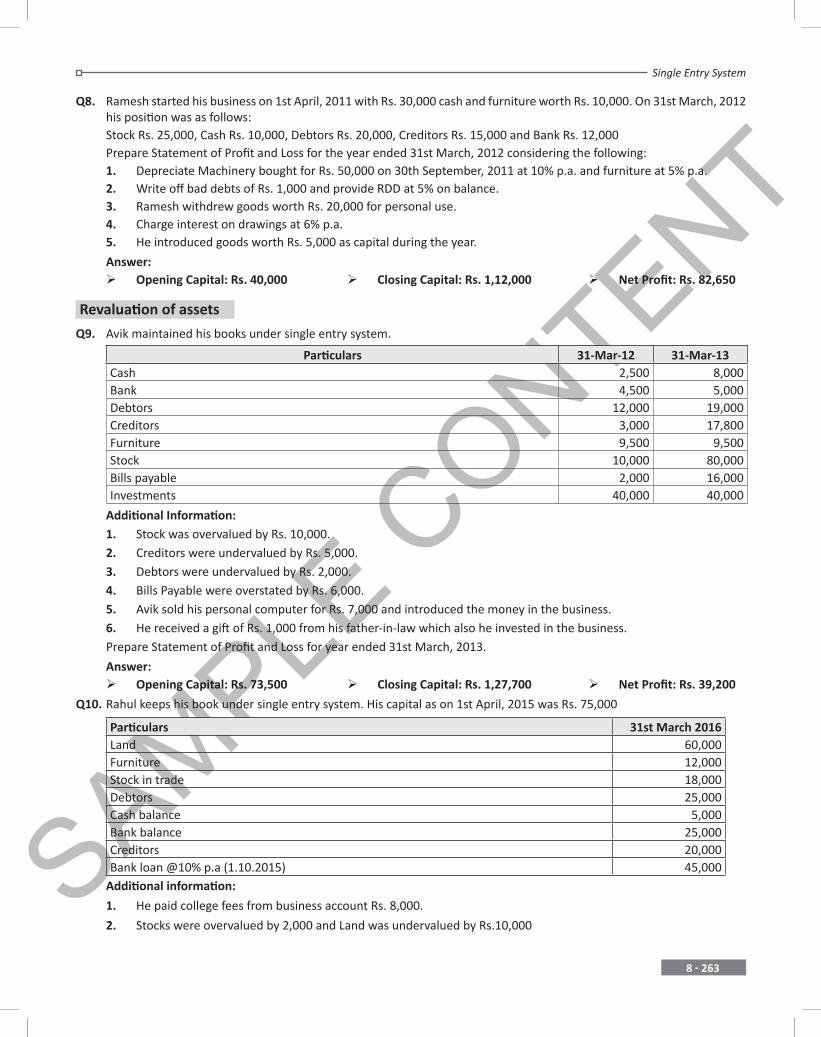

Q8. Ramesh started his business on 1st April, 2011 with Rs. 30,000 cash and furniture worth Rs. 10,000. On 31st March, 2012 his position was as follows:

Stock Rs. 25,000, Cash Rs. 10,000, Debtors Rs. 20,000, Creditors Rs. 15,000 and Bank Rs. 12,000 Prepare Statement of Profit and Loss for the year ended 31st March, 2012 considering the following: 1. Depreciate Machinery bought for Rs. 50,000 on 30th September, 2011 at 10% p.a. and furniture at 5% p.a. 2. Write off bad debts of Rs. 1,000 and provide RDD at 5% on balance. 3. Ramesh withdrew goods worth Rs. 20,000 for personal use. 4. Charge interest on drawings at 6% p.a. 5. He introduced goods worth Rs. 5,000 as capital during the year.

Answer: Opening Capital: Rs. 40,000 Closing Capital: Rs. 1,12,000 Net Profit: Rs. 82,650

Revaluation of assets

Q9. Avik maintained his books under single entry system.

Particulars 31-Mar-12 31-Mar-13Cash 2,500 8,000 Bank 4,500 5,000 Debtors 12,000 19,000 Creditors 3,000 17,800 Furniture 9,500 9,500 Stock 10,000 80,000 Bills payable 2,000 16,000 Investments 40,000 40,000

Additional Information: 1. Stock was overvalued by Rs. 10,000. 2. Creditors were undervalued by Rs. 5,000. 3. Debtors were undervalued by Rs. 2,000. 4. Bills Payable were overstated by Rs. 6,000. 5. Avik sold his personal computer for Rs. 7,000 and introduced the money in the business. 6. He received a gift of Rs. 1,000 from his father-in-law which also he invested in the business. Prepare Statement of Profit and Loss for year ended 31st March, 2013.

Answer: Opening Capital: Rs. 73,500 Closing Capital: Rs. 1,27,700 Net Profit: Rs. 39,200

Q10. Rahul keeps his book under single entry system. His capital as on 1st April, 2015 was Rs. 75,000

Particulars 31st March 2016Land 60,000Furniture 12,000Stock in trade 18,000Debtors 25,000Cash balance 5,000Bank balance 25,000Creditors 20,000Bank loan @10% p.a (1.10.2015) 45,000

Additional information:

1. He paid college fees from business account Rs. 8,000.

2. Stocks were overvalued by 2,000 and Land was undervalued by Rs.10,000

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 264

3. Depreciate furniture by 5%

4. Charge 5% p.a. interest on drawings

5. Provide 5% on Debtors for Bad and Doubtful Debts

Answer: Opening Capital: Rs.75,000 Closing Capital: Rs.80,000 Net Profit: Rs.17,100

Various adjustments

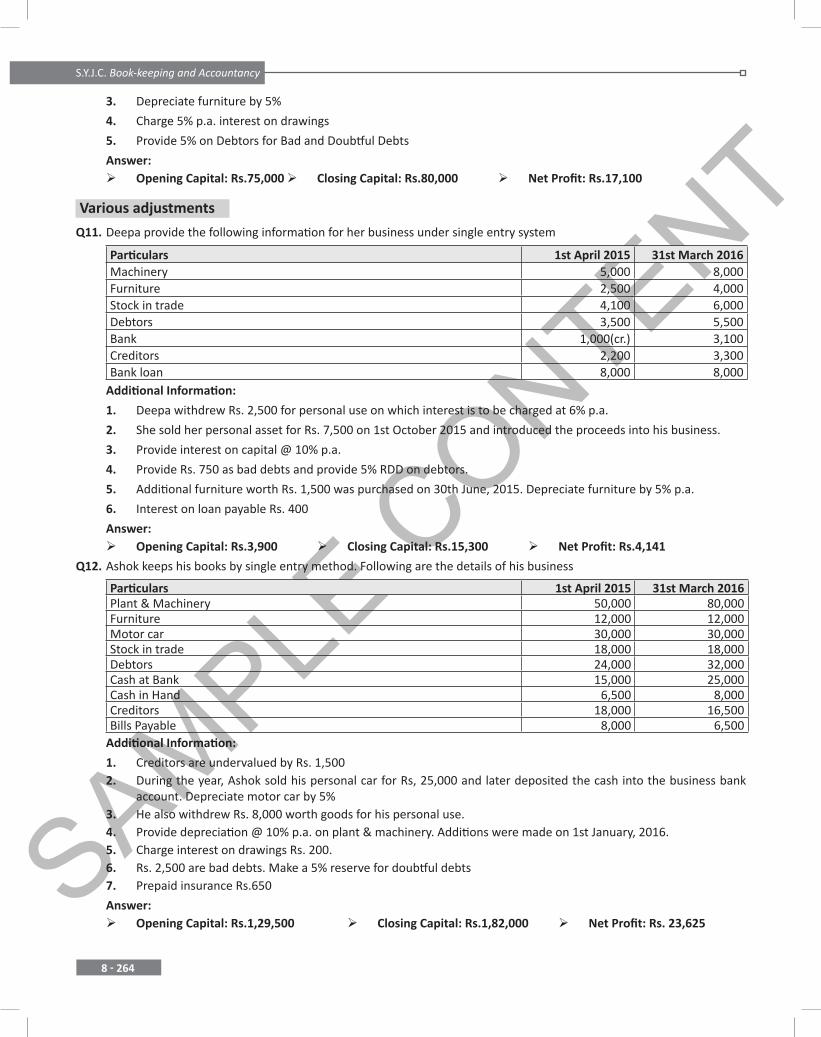

Q11. Deepa provide the following information for her business under single entry system

Particulars 1st April 2015 31st March 2016Machinery 5,000 8,000Furniture 2,500 4,000Stock in trade 4,100 6,000Debtors 3,500 5,500Bank 1,000(cr.) 3,100Creditors 2,200 3,300Bank loan 8,000 8,000

Additional Information:

1. Deepa withdrew Rs. 2,500 for personal use on which interest is to be charged at 6% p.a.

2. She sold her personal asset for Rs. 7,500 on 1st October 2015 and introduced the proceeds into his business.

3. Provide interest on capital @ 10% p.a.

4. Provide Rs. 750 as bad debts and provide 5% RDD on debtors.

5. Additional furniture worth Rs. 1,500 was purchased on 30th June, 2015. Depreciate furniture by 5% p.a.

6. Interest on loan payable Rs. 400

Answer: Opening Capital: Rs.3,900 Closing Capital: Rs.15,300 Net Profit: Rs.4,141

Q12. Ashok keeps his books by single entry method. Following are the details of his business

Particulars 1st April 2015 31st March 2016Plant & Machinery 50,000 80,000Furniture 12,000 12,000Motor car 30,000 30,000Stock in trade 18,000 18,000Debtors 24,000 32,000Cash at Bank 15,000 25,000Cash in Hand 6,500 8,000Creditors 18,000 16,500Bills Payable 8,000 6,500

Additional Information:

1. Creditors are undervalued by Rs. 1,5002. During the year, Ashok sold his personal car for Rs, 25,000 and later deposited the cash into the business bank

account. Depreciate motor car by 5%3. He also withdrew Rs. 8,000 worth goods for his personal use.4. Provide depreciation @ 10% p.a. on plant & machinery. Additions were made on 1st January, 2016.5. Charge interest on drawings Rs. 200.6. Rs. 2,500 are bad debts. Make a 5% reserve for doubtful debts7. Prepaid insurance Rs.650

Answer: Opening Capital: Rs.1,29,500 Closing Capital: Rs.1,82,000 Net Profit: Rs. 23,625

SAMPLE C

ONTENTSingle Entry System

8 - 265

Partnership firm

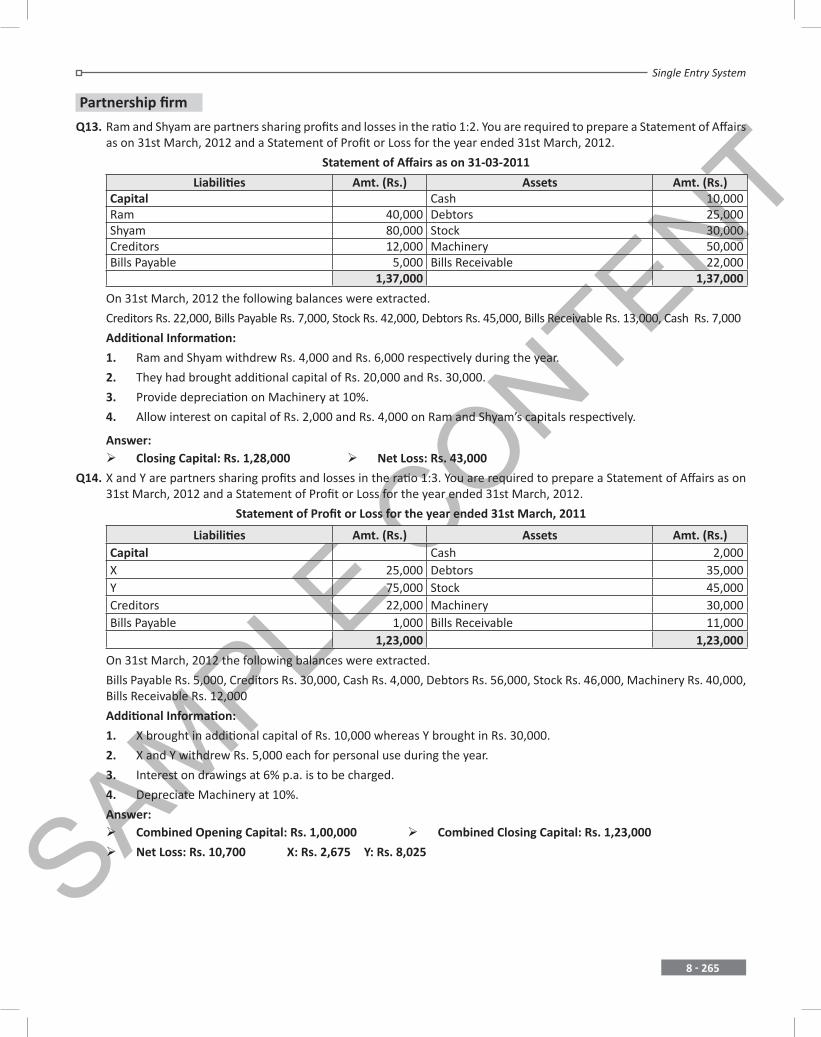

Q13. Ram and Shyam are partners sharing profits and losses in the ratio 1:2. You are required to prepare a Statement of Affairs as on 31st March, 2012 and a Statement of Profit or Loss for the year ended 31st March, 2012.

Statement of Affairs as on 31-03-2011

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Cash 10,000 Ram 40,000 Debtors 25,000 Shyam 80,000 Stock 30,000 Creditors 12,000 Machinery 50,000 Bills Payable 5,000 Bills Receivable 22,000

1,37,000 1,37,000

On 31st March, 2012 the following balances were extracted.

Creditors Rs. 22,000, Bills Payable Rs. 7,000, Stock Rs. 42,000, Debtors Rs. 45,000, Bills Receivable Rs. 13,000, Cash Rs. 7,000

Additional Information:

1. Ram and Shyam withdrew Rs. 4,000 and Rs. 6,000 respectively during the year.

2. They had brought additional capital of Rs. 20,000 and Rs. 30,000.

3. Provide depreciation on Machinery at 10%.

4. Allow interest on capital of Rs. 2,000 and Rs. 4,000 on Ram and Shyam’s capitals respectively.

Answer: Closing Capital: Rs. 1,28,000 Net Loss: Rs. 43,000

Q14. X and Y are partners sharing profits and losses in the ratio 1:3. You are required to prepare a Statement of Affairs as on 31st March, 2012 and a Statement of Profit or Loss for the year ended 31st March, 2012.

Statement of Profit or Loss for the year ended 31st March, 2011

Liabilities Amt. (Rs.) Assets Amt. (Rs.)Capital Cash 2,000 X 25,000 Debtors 35,000 Y 75,000 Stock 45,000 Creditors 22,000 Machinery 30,000 Bills Payable 1,000 Bills Receivable 11,000

1,23,000 1,23,000

On 31st March, 2012 the following balances were extracted.

Bills Payable Rs. 5,000, Creditors Rs. 30,000, Cash Rs. 4,000, Debtors Rs. 56,000, Stock Rs. 46,000, Machinery Rs. 40,000, Bills Receivable Rs. 12,000

Additional Information:

1. X brought in additional capital of Rs. 10,000 whereas Y brought in Rs. 30,000.

2. X and Y withdrew Rs. 5,000 each for personal use during the year.

3. Interest on drawings at 6% p.a. is to be charged.

4. Depreciate Machinery at 10%.

Answer: Combined Opening Capital: Rs. 1,00,000 Combined Closing Capital: Rs. 1,23,000

Net Loss: Rs. 10,700 X: Rs. 2,675 Y: Rs. 8,025

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 266

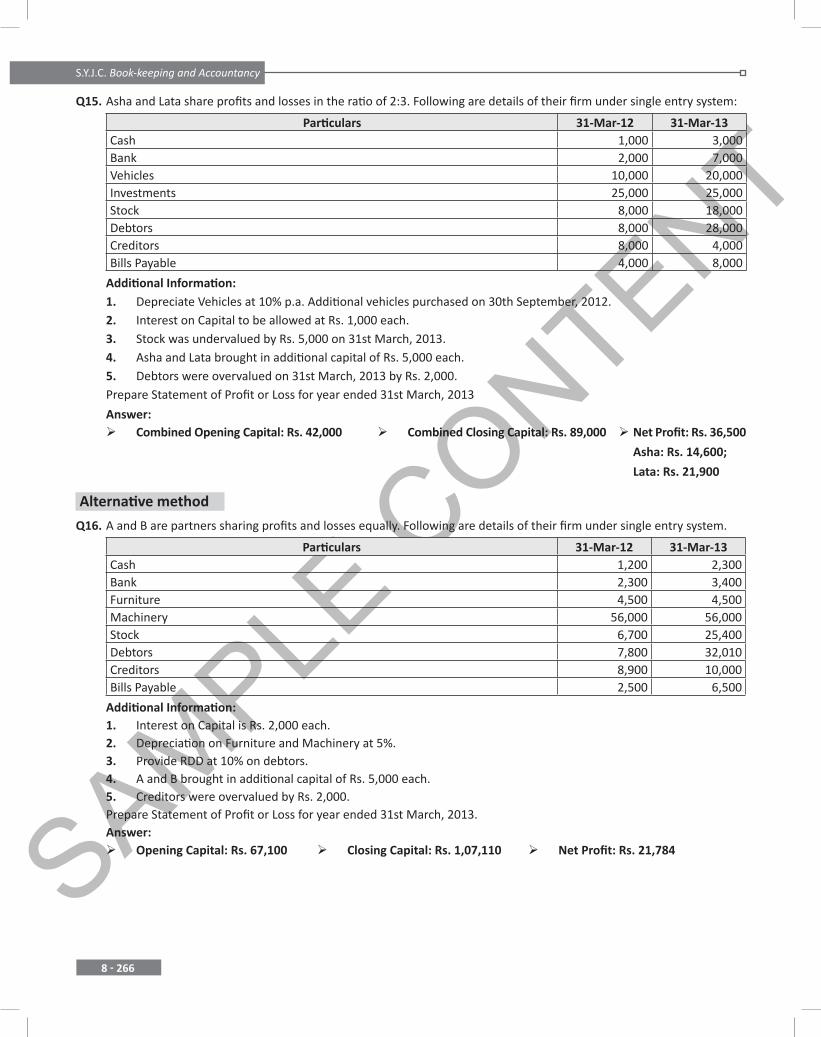

Q15. Asha and Lata share profits and losses in the ratio of 2:3. Following are details of their firm under single entry system:

Particulars 31-Mar-12 31-Mar-13Cash 1,000 3,000Bank 2,000 7,000Vehicles 10,000 20,000Investments 25,000 25,000Stock 8,000 18,000Debtors 8,000 28,000Creditors 8,000 4,000Bills Payable 4,000 8,000

Additional Information:1. Depreciate Vehicles at 10% p.a. Additional vehicles purchased on 30th September, 2012.2. Interest on Capital to be allowed at Rs. 1,000 each.3. Stock was undervalued by Rs. 5,000 on 31st March, 2013.4. Asha and Lata brought in additional capital of Rs. 5,000 each.5. Debtors were overvalued on 31st March, 2013 by Rs. 2,000.Prepare Statement of Profit or Loss for year ended 31st March, 2013

Answer: Combined Opening Capital: Rs. 42,000 Combined Closing Capital: Rs. 89,000 Net Profit: Rs. 36,500

Asha: Rs. 14,600;

Lata: Rs. 21,900

Alternative method

Q16. A and B are partners sharing profits and losses equally. Following are details of their firm under single entry system.

Particulars 31-Mar-12 31-Mar-13Cash 1,200 2,300Bank 2,300 3,400Furniture 4,500 4,500Machinery 56,000 56,000Stock 6,700 25,400Debtors 7,800 32,010Creditors 8,900 10,000Bills Payable 2,500 6,500

Additional Information:1. Interest on Capital is Rs. 2,000 each.2. Depreciation on Furniture and Machinery at 5%.3. Provide RDD at 10% on debtors.4. A and B brought in additional capital of Rs. 5,000 each.5. Creditors were overvalued by Rs. 2,000.Prepare Statement of Profit or Loss for year ended 31st March, 2013.Answer: Opening Capital: Rs. 67,100 Closing Capital: Rs. 1,07,110 Net Profit: Rs. 21,784

SAMPLE C

ONTENTSingle Entry System

8 - 267

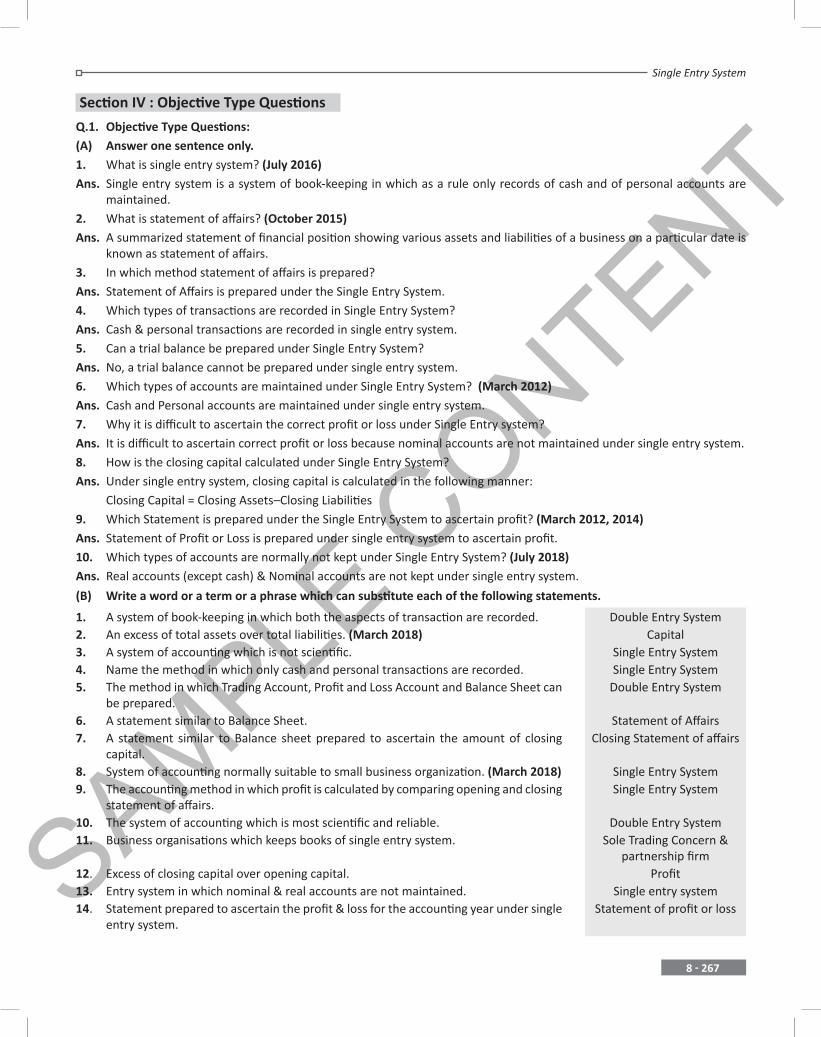

Section IV : Objective Type Questions

Q.1. Objective Type Questions:(A) Answer one sentence only.1. What is single entry system? (July 2016)Ans. Single entry system is a system of book-keeping in which as a rule only records of cash and of personal accounts are

maintained.2. What is statement of affairs? (October 2015)Ans. A summarized statement of financial position showing various assets and liabilities of a business on a particular date is

known as statement of affairs.3. In which method statement of affairs is prepared?Ans. Statement of Affairs is prepared under the Single Entry System.4. Which types of transactions are recorded in Single Entry System?Ans. Cash & personal transactions are recorded in single entry system.5. Can a trial balance be prepared under Single Entry System?Ans. No, a trial balance cannot be prepared under single entry system.6. Which types of accounts are maintained under Single Entry System? (March 2012)Ans. Cash and Personal accounts are maintained under single entry system.7. Why it is difficult to ascertain the correct profit or loss under Single Entry system?Ans. It is difficult to ascertain correct profit or loss because nominal accounts are not maintained under single entry system.8. How is the closing capital calculated under Single Entry System?Ans. Under single entry system, closing capital is calculated in the following manner:

Closing Capital = Closing Assets–Closing Liabilities9. Which Statement is prepared under the Single Entry System to ascertain profit? (March 2012, 2014)Ans. Statement of Profit or Loss is prepared under single entry system to ascertain profit.10. Which types of accounts are normally not kept under Single Entry System? (July 2018)Ans. Real accounts (except cash) & Nominal accounts are not kept under single entry system.

(B) Write a word or a term or a phrase which can substitute each of the following statements.

1. A system of book-keeping in which both the aspects of transaction are recorded. Double Entry System2. An excess of total assets over total liabilities. (March 2018) Capital3. A system of accounting which is not scientific. Single Entry System4. Name the method in which only cash and personal transactions are recorded. Single Entry System5. The method in which Trading Account, Profit and Loss Account and Balance Sheet can

be prepared.Double Entry System

6. A statement similar to Balance Sheet. Statement of Affairs7. A statement similar to Balance sheet prepared to ascertain the amount of closing

capital.Closing Statement of affairs

8. System of accounting normally suitable to small business organization. (March 2018) Single Entry System9. The accounting method in which profit is calculated by comparing opening and closing

statement of affairs.Single Entry System

10. The system of accounting which is most scientific and reliable. Double Entry System11. Business organisations which keeps books of single entry system. Sole Trading Concern &

partnership firm12. Excess of closing capital over opening capital. Profit13. Entry system in which nominal & real accounts are not maintained. Single entry system14. Statement prepared to ascertain the profit & loss for the accounting year under single

entry system.Statement of profit or loss

SAMPLE C

ONTENTS.Y.J.C. Book-keeping and Accountancy

8 - 268

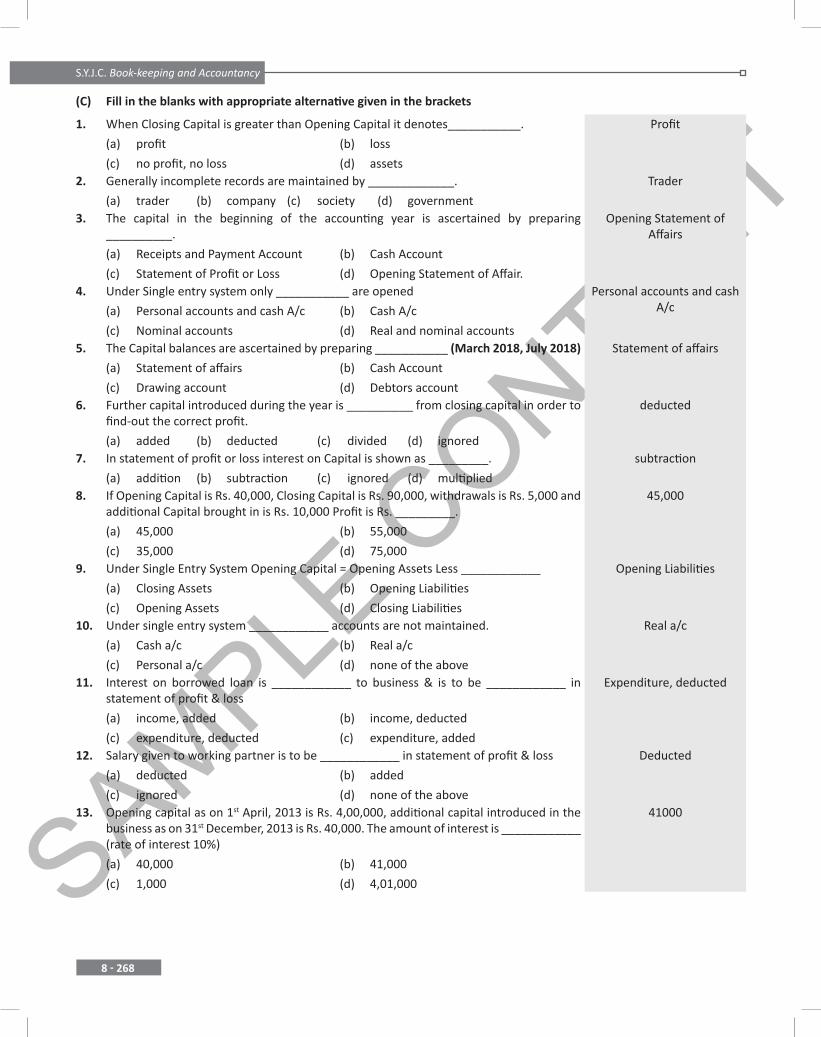

(C) Fill in the blanks with appropriate alternative given in the brackets

1. When Closing Capital is greater than Opening Capital it denotes___________.

(a) profit (b) loss

(c) no profit, no loss (d) assets

Profit

2. Generally incomplete records are maintained by _____________.

(a) trader (b) company (c) society (d) government

Trader

3. The capital in the beginning of the accounting year is ascertained by preparing__________.

(a) Receipts and Payment Account (b) Cash Account

(c) Statement of Profit or Loss (d) Opening Statement of Affair.

Opening Statement of Affairs

4. Under Single entry system only ___________ are opened

(a) Personal accounts and cash A/c (b) Cash A/c

(c) Nominal accounts (d) Real and nominal accounts

Personal accounts and cash A/c

5. The Capital balances are ascertained by preparing ___________ (March 2018, July 2018)

(a) Statement of affairs (b) Cash Account

(c) Drawing account (d) Debtors account

Statement of affairs

6. Further capital introduced during the year is __________ from closing capital in order to find-out the correct profit.

(a) added (b) deducted (c) divided (d) ignored

deducted

7. In statement of profit or loss interest on Capital is shown as _________.

(a) addition (b) subtraction (c) ignored (d) multiplied

subtraction

8. If Opening Capital is Rs. 40,000, Closing Capital is Rs. 90,000, withdrawals is Rs. 5,000 andadditional Capital brought in is Rs. 10,000 Profit is Rs. _________.

(a) 45,000 (b) 55,000

(c) 35,000 (d) 75,000

45,000

9. Under Single Entry System Opening Capital = Opening Assets Less ____________

(a) Closing Assets (b) Opening Liabilities

(c) Opening Assets (d) Closing Liabilities

Opening Liabilities

10. Under single entry system ____________ accounts are not maintained.

(a) Cash a/c (b) Real a/c

(c) Personal a/c (d) none of the above

Real a/c

11. Interest on borrowed loan is ____________ to business & is to be ____________ in statement of profit & loss

(a) income, added (b) income, deducted

(c) expenditure, deducted (c) expenditure, added

Expenditure, deducted

12. Salary given to working partner is to be ____________ in statement of profit & loss

(a) deducted (b) added

(c) ignored (d) none of the above

Deducted

13. Opening capital as on 1st April, 2013 is Rs. 4,00,000, additional capital introduced in the business as on 31st December, 2013 is Rs. 40,000. The amount of interest is ____________ (rate of interest 10%)

(a) 40,000 (b) 41,000

(c) 1,000 (d) 4,01,000

41000

SAMPLE C

ONTENTSingle Entry System

8 - 269

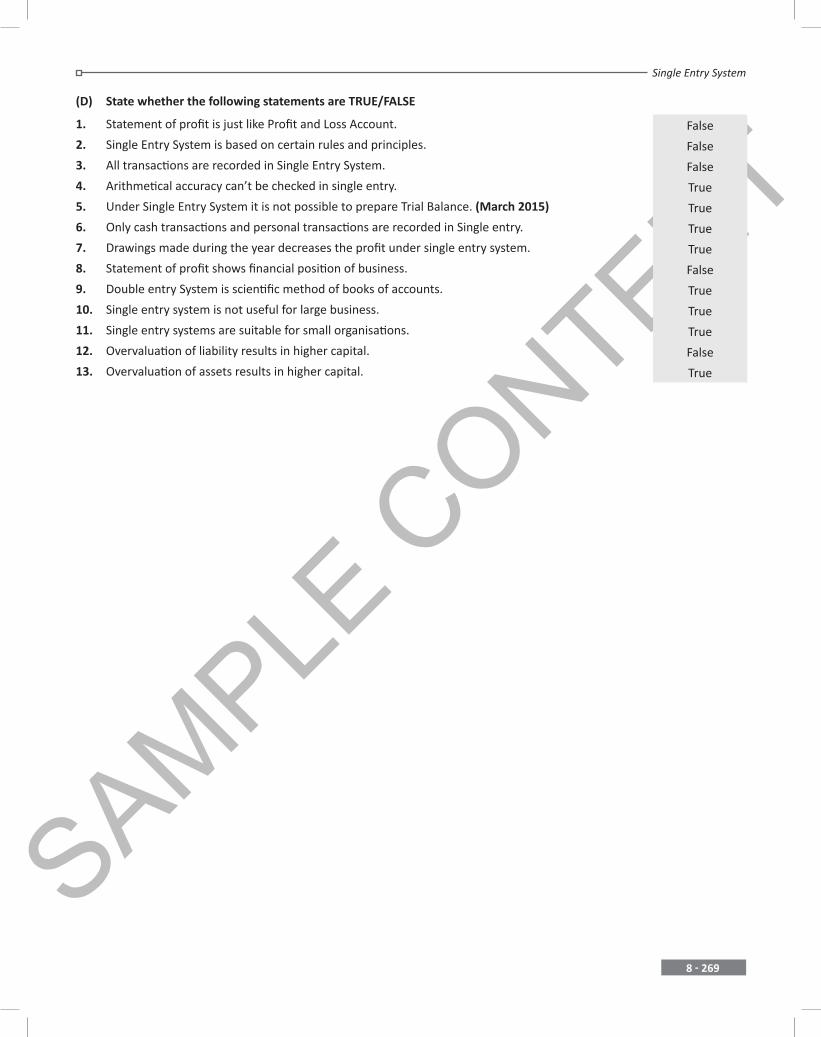

(D) State whether the following statements are TRUE/FALSE

1. Statement of profit is just like Profit and Loss Account. False

2. Single Entry System is based on certain rules and principles. False

3. All transactions are recorded in Single Entry System. False

4. Arithmetical accuracy can’t be checked in single entry. True

5. Under Single Entry System it is not possible to prepare Trial Balance. (March 2015) True

6. Only cash transactions and personal transactions are recorded in Single entry. True

7. Drawings made during the year decreases the profit under single entry system. True

8. Statement of profit shows financial position of business. False

9. Double entry System is scientific method of books of accounts. True

10. Single entry system is not useful for large business. True

11. Single entry systems are suitable for small organisations. True

12. Overvaluation of liability results in higher capital. False

13. Overvaluation of assets results in higher capital. True