statutory issue paper no. 40 real estate investments · real estate investments meet the definition...

TRANSCRIPT

IP 40–1

Statutory Issue Paper No. 40

Real Estate Investments

STATUS Finalized March 16, 1998

Original SSAP: SSAP No. 40; Current Authoritative Guidance: SSAP No. 40R

Type of Issue: Common Area

SUMMARY OF ISSUE

1. Current statutory accounting guidance for real estate investments is provided in the AccountingPractices and Procedures Manuals for Life and Accident and Health and for Property and CasualtyInsurance Companies. However, the Accounting Practices and Procedures Manuals contain nocomprehensive guidance on accounting for sale of real estate or for real estate construction projects.

2. GAAP guidance for real estate is established in FASB Statement No. 60, Accounting andReporting by Insurance Enterprises (FAS 60), FASB Statement No. 66, Accounting for Sales of RealEstate (FAS 66), FASB Statement No. 67, Accounting for Costs and Initial Rental Operations of RealEstate Projects (FAS 67), FASB Statement No. 121, Accounting for the Impairment of Long-Lived Assetsand for Long-Lived Assets to be Disposed Of, and AICPA Statement of Position 92-3, Accounting forForeclosed Assets (SOP 92-3). Current statutory guidance is similar to GAAP, except that GAAP requiresrecognition of impairment in the value of the investments through a writedown to the appropriate basiswith a charge to realized gains and losses. Current statutory accounting guidance states that “Generally,the value of investment real estate and property acquired in satisfaction of debt may not exceed the lowerof current market value or cost plus capitalized improvements, less normal depreciation.” The currentstatutory guidance gives reporting entities three options when an impairment is recognized: a) write downthe investment real estate, b) nonadmit part of the value, or c) establish a reserve for specific properties asa liability.

3. The purpose of this issue paper is to establish statutory accounting principles for real estateinvestments that are consistent with the Statutory Accounting Principles Statement of Concepts andStatutory Hierarchy (Statement of Concepts).

SUMMARY CONCLUSION

4. Real estate investments shall be defined as direct-owned real estate properties acquired inexchange for consideration (including but not limited to cash, a contract for deed or mortgage, or othernon-cash consideration), obtained through foreclosure or voluntary conveyance in satisfaction of amortgage loan, or received as contributed surplus. Real estate investments meet the definition of assetsdefined in Issue Paper No. 4—Definition of Assets and Nonadmitted Assets and are admitted assets to theextent they conform to the requirements of this issue paper.

5. Real estate investments include real estate occupied by the company, which is defined in IssuePaper No. 23—Property Occupied by the Company, and certain acquisition, development andconstruction arrangements (ADC) as defined in Issue Paper No. 38—Acquisition, Development andConstruction Arrangements (Issue Paper No. 38).

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–2

6. Real estate investments shall be reported net of encumbrances in the following balance sheet categories, with parenthetical disclosure of the amount of related encumbrances:

- Properties occupied by the company - Properties held for the production of income - Properties held for sale

7. Encumbrances represent outstanding mortgages or other debt related to the real estate investment and any unpaid accrued acquisition or construction costs. Interest expense shall be included in investment expenses. 8. The cost of real estate represents the fair market value of the consideration exchanged plus any costs incurred to place the real estate asset in usable condition, including but not limited to, brokerage fees, legal fees, demolition, clearing and grading, fees of architects and engineers, any additional expenditures made for equipment and fixtures that are made a permanent part of the structure and certain interest costs as provided for in Issue Paper No. 44—Capitalization of Interest. Where cost includes both land and building, the cost shall be allocated among the assets purchased based on the relative values determined using appraisals, as described in paragraph 12 below. The cost shall be reduced by any amounts received for sales of rights or privileges in connection with the property or by any cash recoveries received after acquiring title to the property. The cost of real estate which has been foreclosed upon shall be initially established in accordance with Issue Paper No. 36—Troubled Debt Restructurings. The cost of contributed real estate shall be initially established in accordance with Issue Paper No. 73—Transactions as a nonreciprocal transfer. 9. The cost of property included in real estate investments, other than land, shall be depreciated over the estimated useful life, not to exceed fifty years. Depreciation expense shall be included in investment expenses. 10. Properties occupied by the reporting entity and properties held for the production of income shall be carried at depreciated cost less encumbrances unless events or circumstances indicate the carrying amount of the asset (amount prior to reduction for encumbrances) may not be recoverable. Paragraph 5 of FAS 121 provides examples of events or changes in circumstances which indicate that the recoverability of the carrying amount of properties occupied by the reporting entity or properties held for the production of income should be assessed. If the events or changes in circumstances set forth in paragraph 5 of FAS 121 are present or if other events or changes in circumstances indicate that the carrying amount of properties occupied by the company or properties held for the production of income may not be recoverable, the reporting entity shall determine whether an impairment loss must be recognized in accordance with paragraph 6 of FAS 121. Property occupied by the reporting entity shall be evaluated using the asset grouping approach of paragraph 8 of FAS 121. FAS 121 is excerpted in paragraph 37 of this issue paper. An impairment loss is measured as the amount by which the individual carrying amounts exceed the fair value of properties occupied by the company or properties held for the production of income. Fair value is determined in accordance with paragraph 12 of this issue paper. If the fair value of the asset is less than the carrying value, the asset shall be written down to the fair value thereby establishing a new cost basis. The new cost basis shall not be changed for subsequent recoveries in fair value. The adjustment shall be recorded in the statement of operations as a realized loss. 11. Properties that the reporting entity has the intent to sell or is required to sell shall be classified as properties held for sale and carried at the lower of depreciated cost or fair value less encumbrances and estimated costs to sell the property consistent with paragraph 16 of FAS 121. The intent to sell a property exists when management, having the authority to approve the action, has committed to a plan to dispose of the asset, either by sale or abandonment. Fair value of the asset shall be determined in accordance with

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–3

paragraph 12 of this issue paper. Subsequent revisions to the fair value of the asset shall be accounted for in accordance with paragraph 17 of FAS 121. 12. The current fair value of real estate shall be determined on a property by property basis (i.e., increases in the fair value of one property shall not be used to offset declines in fair value of another) and shall be defined as the price that a property would bring in a competitive and open market under all conditions requisite to a fair sale (i.e., the buyer and seller acting prudently and knowledgeably with the price not affected by any undue stimulus). If market quotes are unavailable, estimates of fair value shall be determined by an appraisal (internal or third party), which is based upon an evaluation of all relevant data about the market, considering the following:

a. A physical inspection of the premises,

b. The present value of future cash flows generated by the property (Discounted Cash Flows), or capitalization of stabilized net operating income (Direct Capitalization),

c. current sales prices of similar properties with adjustments for differences in the properties

(Sales Comparison Approach),

d. costs to sell the property if the reporting entity does not have the intent or ability to hold the real estate as an investment,

e. replacement costs of the improvements, less depreciation, plus the value of the land (Cost

Approach).

All appraisals obtained to determine fair market value of real estate investments shall be no more than five years old. However, if conditions indicate there has been a significant decrease in the fair market value of a property, then a current appraisal shall be obtained. Additionally, appraisals shall be obtained for real estate investments at the time of foreclosure or contribution. Contributed real estate shall be supported by an independent third party appraisal at the date of contribution. If either of the previous conditions exist but an appraisal has not been obtained, the related property shall be considered a nonadmitted asset until the required appraisals are obtained. Income, Expenses, and Capital Improvements 13. Rental income on real estate leased is addressed in Issue Paper No. 22—Leases, which requires that rental income be included in investment income. Expenses incurred in operating the real estate investment, including but not limited to, real estate taxes, utilities, and ordinary repair and maintenance, shall be charged to expense as incurred and included in investment expenses. 14. Expenditures that are necessary to put the asset back into good operating condition or to keep it in good operating condition, shall be charged to expense as incurred. Expenditures that add to or prolong the life of the property shall be added to the cost of the real estate (capitalized) and depreciated over the remaining estimated useful life of the property. Sale of Real Estate 15. Recognition of profit on sales of real estate investments shall be accounted for in accordance with paragraphs 29, 33 and 34 below. Profit shall be recognized in full when real estate is sold, provided (a) the profit is determinable, that is, the collectibility of the sales price is reasonably assured or the amount that will not be collectible can be estimated, and (b) the earnings process is virtually complete, that is, the seller is not obliged to perform significant activities after the sale to earn the profit. Unless both conditions exist, recognition of all or part of the profit shall be postponed. Profit shall not be recognized by the full accrual method until all of the following criteria are met:

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–4

a. A sale is consummated,

b. The buyer's initial and continuing investments are adequate to demonstrate a commitment to

pay for the property,

c. The seller's receivable is not subject to future subordination, and

d. The seller has transferred to the buyer the usual risks and rewards of ownership in a transaction that is in substance a sale and does not have a substantial continuing involvement with the property after the sale.

DISCUSSION The calculation of the buyer's initial investment specified in subparagraph 9 of paragraph 29 below shall be modified to reflect that buyer's notes must be supported by letters of credit from institutions that are listed by the Securities Valuation Office of the National Association of Insurance Commissioners as meeting credit standards to be included in determining the buyer's initial investment. Any profit or loss is considered a realized gain or loss in the year of the sale in accordance with FAS 66. Real Estate Projects Under Development 16. Costs and initial rental operations of real estate projects under development, which include ADC arrangements accounted for as real estate under the provisions of paragraph 3 of Issue Paper No. 38, shall be accounted for in accordance with paragraph 30 below. Costs incurred in connection with real estate projects shall be expensed as incurred unless the criteria established in paragraph 30 are met. The admitted value of a real estate project, or parts thereof, held for sale or development and sale shall not exceed the estimated selling price in the ordinary course of business less estimated costs of completion (to stage of completion assumed in determining the selling price), holding, and disposal (net realizable value). If costs exceed net realizable value, capitalization of eligible costs shall continue, however, an allowance shall be provided to reduce the admitted value to estimated net realizable value. 17. The statutory principles in this issue paper are consistent with the current statutory guidance except as follows: - Paragraph 11 requires real estate held for sale to be carried at the lower of fair value less

estimated costs to sell or depreciated cost. There are at least two states, Nevada and Arizona, which allow real property to be carried in excess of depreciated cost if supported by an appraisal.

- Paragraphs 10 and 11 distinguish between real estate held for sale and real estate not held for sale.

Paragraph 11 requires the fair market value of real estate held for sale to be reduced by estimated selling costs in determining admitted value.

- Paragraph 10 provides that impairments for properties occupied by the company and properties

held for the production of income shall be recorded as a realized loss. After an impairment is recognized, the carrying amount of the asset shall be accounted for as its new cost. Current statutory guidance provides three options for recording valuation adjustments: (a) direct write-down of asset, (b) nonadmit part of the asset, or (c) establish a reserve liability.

- Paragraph 12 provides for the utilization of appraisals in determining fair market value. The

Accounting Practices and Procedures Manual for Life and Accident and Health and for Property and Casualty Insurance Companies define the term “appraised value” but do not require the use

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–5

of an appraisal to support valuation allowances. At least two states, Minnesota and Missouri, have regulations that require the use of appraisals for certain real estate properties.

- Paragraph 6 conforms the balance sheet categories to be consistent with FAS 121. These differ

from those required on the Property and Casualty Annual Statement and those required on the Life and Accident and Health Annual Statement. Real estate currently reported as “Other Properties” on the Property and Casualty Annual Statement shall be reported as “Properties held for the production of income” or “Properties held for sale.” Real estate currently reported as “Properties Acquired in the Satisfaction of Debt” on the Life and Accident and Health Annual Statement shall be reported as “Properties held for the production of income” or “Properties held for sale.”

- Paragraph 15 adopts the GAAP guidance for sales of real estate, which augments and clarifies the

current statutory guidance on sales of real estate. - Paragraph 16 adopts GAAP guidance for real estate construction projects; no current statutory

guidance exists. 18. The statutory accounting principles established in this issue paper: - Adopt FASB Statement No. 66, Accounting for Sales of Real Estate, with modification to

paragraph 9 to indicate that only letters of credit from institutions listed by the Securities Valuation Office shall be included in determining the buyer's initial investment. Additionally, as they relate to FASB Statement 66, the following are adopted: FASB Emerging Issues Task Force Issue No. 87-29, Exchange of Real Estate Involving Boot (EITF 87-29), FASB Emerging Issues Task Force Issue No. 86-6, Antispeculation Clauses in Real Estate Sales Contracts, FASB Emerging Issues Task Force Issue No. 88-12, Transfer of Ownership Interest as Part of Down Payment under FASB Statement No. 66, FASB Emerging Issues Task Force Issue No. 88-24, Effect of Various Forms of Financing under FASB Statement No. 66 and FASB Emerging Issues Task Force Issue No. 87-9, Profit Recognition on Sales of Real Estate with Insured Mortgages or Surety Bonds (EITF 87-9).

- This issue paper adopts FASB Emerging Issues Task Force No. 84-17, Profit Recognition on

Sales of Real Estate with Graduated Payment Mortgages or Insured Mortgages, FASB Emerging Issues Task Force No 89-13, Accounting for the Cost of Asbestos Removal, FASB Emerging Issues Task Force No. 89-14, Valuation of Repossessed Real Estate, FASB Emerging Issues Task Force No. 90-8, Capitalization of Costs to Treat Environmental Contamination, and FASB Emerging Issues Task Force No. 95-23, The Treatment of Certain Site Restoration /Environmental Exit Costs When Testing a Long-Lived Assets for Impairment.

- Adopt FASB Statement No. 67, Accounting for Costs and Initial Rental Operations of Real Estate

Projects. Foreclosed real estate held for sale should be valued as described within SOP 92-3, Accounting for Foreclosed Assets.

- Adopt SOP 92-1, Accounting for Real Estate Syndication Income and SOP 92-3, Accounting for

Foreclosed Assets. - Adopt FASB Statement No. 121, Accounting for the Impairment of Long-Lived Assets and for

Long-Lived Assets to Be Disposed Of, for real estate investments except for paragraphs 13, 14.c. and 14.d. which were rejected in Issue Paper No. 68—Business Combinations and Goodwill.

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–6

- Reject Accounting Research Bulletin No. 43, Restatement and Revision of Accounting Research Bulletins, “Chapter 10, Taxes, Section A-Real Estate and Personal Property Taxes”

19. The statutory accounting principles outlined in the conclusion above are consistent with the conservatism and recognition concepts in the Statement of Concepts. Pertinent excerpts follow:

Conservatism Conservative valuation procedures provide protection to policyholders against adverse fluctuations in financial condition or operating results. Statutory accounting should be reasonably conservative over the span of economic cycles and in recognition of the primary responsibility to regulate for financial solvency. Valuation procedures should, to the extent possible, prevent sharp fluctuations in surplus. Recognition

The ability to meet policyholder obligations is predicated on the existence of readily marketable assets available when both current and future obligations are due. Assets having economic value other than those which can be used to fulfill policyholder obligations, or those assets which may be unavailable due to encumbrances or other third party interests should not be recognized on the balance sheet but rather should be charged against surplus when acquired or when availability otherwise becomes questionable. Revenue should be recognized only as the earnings process of the underlying underwriting or investment business is completed. Accounting treatments which tend to defer expense recognition do not generally represent acceptable SAP treatment.

Drafting Notes/Comments - Accounting for investments in real estate ventures are addressed in Issue Paper No. 48—

Investments in Joint Ventures, Partnerships and Limited Liability Companies. - Accounting for leases and sale-leaseback transactions involving real estate transactions are

addressed in Issue Paper No. 22—Leases. - Issue Paper No. 36—Troubled Debt Restructurings addresses accounting for the foreclosure of

real estate; this paper addresses how to account for foreclosed real estate after foreclosure. - Issue Paper No. 34—Investment Income Due and Accrued addresses requirements related to

nonadmitted rental income due and accrued. - Accounting for real estate occupied by the company is addressed in Issue Paper No. 23—

Property Occupied by the Company. - Accounting for leasehold improvements is addressed in Issue Paper No. 31—Leasehold

Improvements Paid by the Reporting Entity as Lessee. - Issue Paper No. 44—Capitalization of Interest addresses capitalization of interest. - Accounting for real estate property acquired by mortgage guaranty insurers in settlement of a

claim is addressed in Issue Paper No. 88—Mortgage Guaranty Insurance. - Depreciation of assets, including acceptable and unacceptable methods and maximum lives and

disclosures, will be addressed in Issue Paper No. 67—Depreciation of Property and Amortization of Leasehold Improvements.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–7

RELEVANT STATUTORY ACCOUNTING AND GAAP GUIDANCE Statutory Accounting 20. The Accounting Practices and Procedures Manual for Life and Accident and Health Insurance Companies includes the following guidance in Chapter 4, Real Estate:

Directly-owned real estate is reported separately in the statutory financial statement. Holdings so reported are classified as properties (a) occupied by the company, (b) acquired in satisfaction of debt, and (c) investments in real estate. These classes may include real estate owned under contract of sale. When real estate is owned indirectly through partnerships or joint ventures, it is reported as “Other Invested Assets” in the statutory financial statement. Authorization and Limitations

Statutes and regulations promulgated by the states concerning limitations on investments in real property are widely divergent. Generally speaking, the thrust of these limitations is to provide an aggregate maximum investment value on holdings of real property. A typical example would be that real estate investments not exceed a stipulated percentage of total admitted assets or surplus. Also common among these limitations are provisions requiring the disposal of foreclosed properties within a certain period of time. Cost The cost of real estate acquired by purchase is the actual amount paid upon purchase, plus the costs incurred to place the real estate asset in usable condition. Elements of cost should also include brokerage fees, legal fees, demolition, clearing and grading, fees of architects and engineers, and any additional expenditures made for equipment and fixtures that are made a permanent part of the structure. Cost should be reduced by any amounts received for sales of rights or privileges in connection with the property or by any cash recoveries received after acquiring title to the property. Where more than one property is acquired at a group price, or where the cost includes both land and building, the price paid must be allocated among the assets purchased. This normally is done on the basis of relative values, which may be determined by appraisals made for insurance purposes, by assessed valuations made for property tax purposes, by independent appraisal, or by some other reasonable method such as the previous owner's percentage allocation or underwriting estimates.

If property is acquired in a non-cash transaction, the acquired property should be recorded at the fair market value of the property or other asset given if the market value of the property acquired cannot reasonably be determined. In determining the cost of investment real estate, an insurer should include the cost of personal property necessary to the income generating operations of the investment property. Furniture, fixtures, and equipment so capitalized should be depreciated over their useful lives. Real estate acquired in satisfaction of debt includes property acquired through foreclosure and through voluntary conveyance. The cost of real estate acquired through foreclosure or voluntary conveyance is recorded at the lower of fair market value at acquisition or cost. Cost includes the outstanding principal balance of the mortgage loan at the date of foreclosure or conveyance plus foreclosure costs, real estate taxes, insurance premiums, and all other costs necessary to obtain clear title and to place the property in good repair. Uncollected interest or unrecovered advances made before foreclosure should also be included in cost.

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

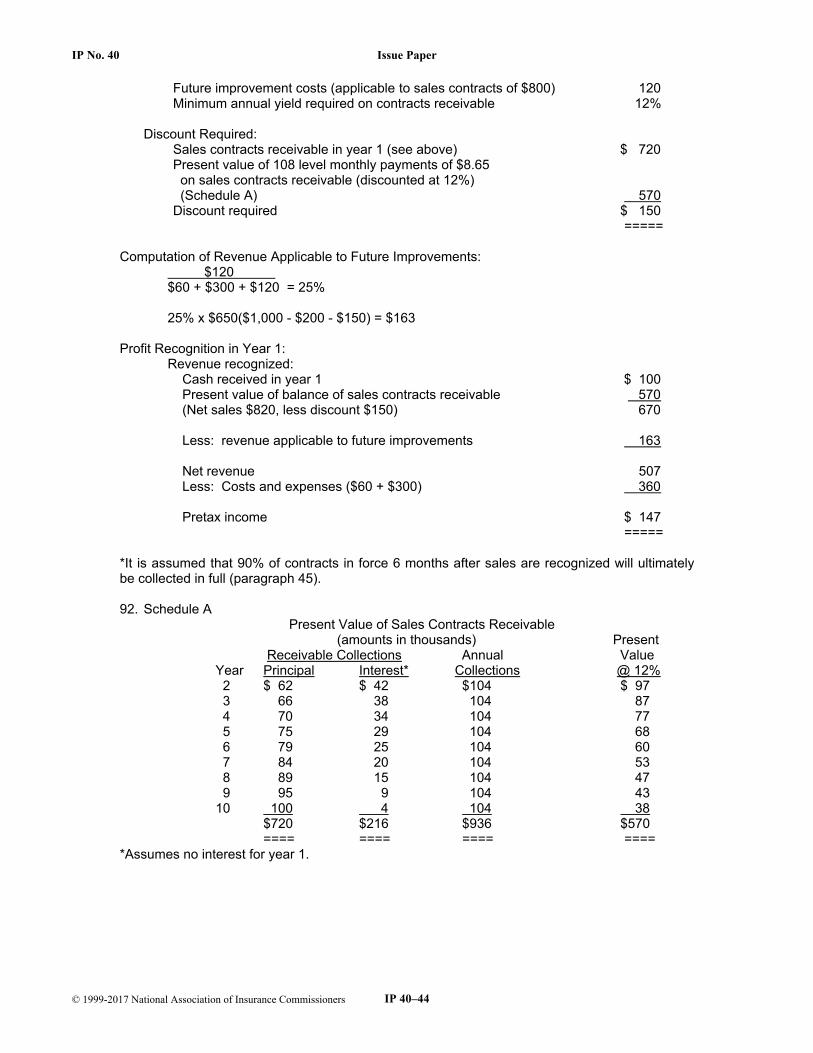

IP 40–8

Book Value For real estate that is occupied by the company and for investment real estate, book value would be the cost or other basic value, stated net of any encumbrance, plus additions and increases by adjustments, less retirements and decreases by adjustments, including depreciation. Encumbrances include mortgages and other related debt and may also include accrued costs of acquisition or construction. The book value of real estate sold under contract of sale is the balance resulting from the cost of the property, less reductions for cash received on account and for any purchase money mortgage that may have been accepted. Market Value Market value is the price that a property would bring in a competitive and open market under all conditions requisite to a fair sale the buyer and seller acting prudently and knowledgeably with the price not affected by any undue stimulus. Appraised Value An appraisal is an opinion of estimated market value for an adequately described property, as of a specified date, supported by the analysis of relevant data. To arrive at this value, three methods are used:

1. Market Data Approach - a comparative analysis of current sales prices of similar

properties, after making necessary adjustments for any difference in the properties. 2. Cost Approach - an estimated value based on the cost of reproduction or replacement of

the improvements, less depreciation, plus the value of the land. (Land value is usually determined by the market data approach.)

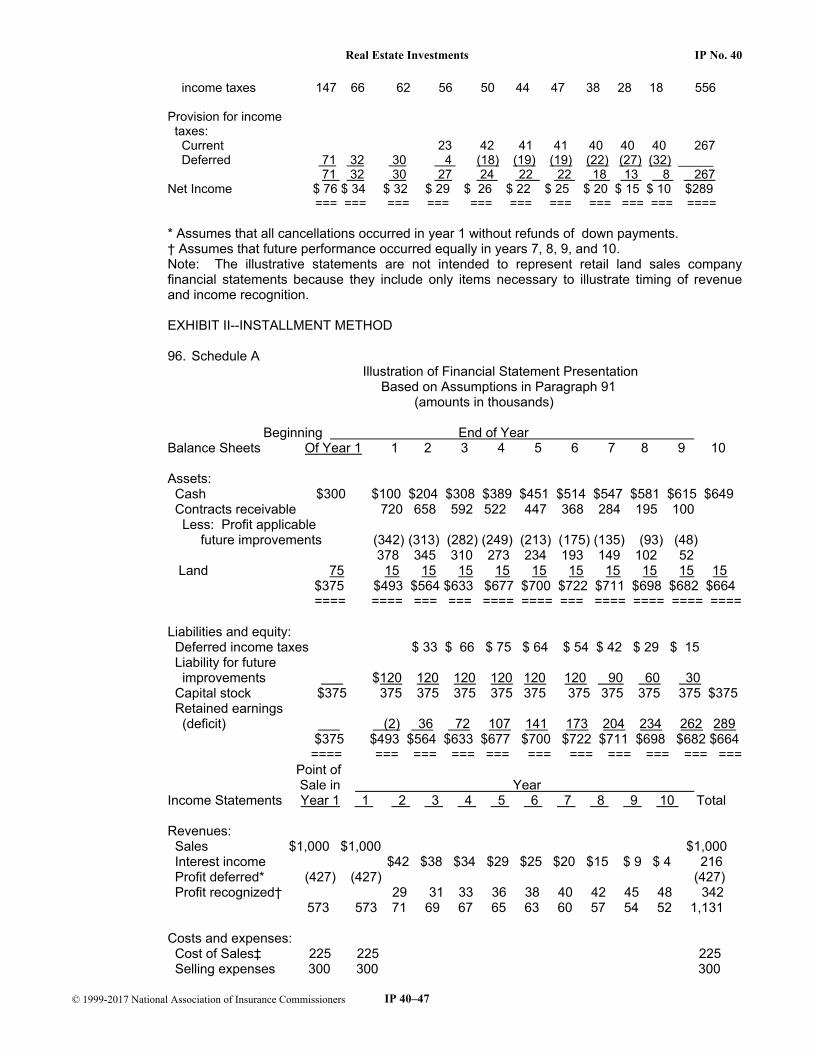

3. Income Approach - an estimated value based on the capitalization of income and

productivity. It is concerned with the present value of future income.

In most appraisals, all three approaches ordinarily will have something to contribute. Each is used independently to reach an estimated value. Then, by applying to each separate value a weight proportionate to its merits in that particular instance, a conclusion is reached concerning one appropriate value. This procedure is known as correlation. Statement Value The instructions for the annual statement require that the admitted value of properties occupied by the company (home office real estate) shall not exceed actual cost, plus capitalized improvements, less normal depreciation. This formula is to apply whether the property is held directly or indirectly by the company. Generally, the value of investment real estate and property acquired in satisfaction of debt may not exceed the lower of current market value or cost plus capitalized improvements, less normal depreciation. In lieu of writing down investment real estate or taking part of the value as nonadmitted when market value is less than book value, an insurer may establish a reserve for specific properties as a liability. Income Derived from Real Estate Income on real estate, or on space in buildings owned and occupied by the company, usually is received periodically and in advance and any amount not received at the end of an accounting period should be set up as investment income due and unpaid to the extent that the amount

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–9

applies to that accounting period. If the collectibility of unpaid rent is in doubt, or if the amount due exceeds a period specified by statute or regulation, most jurisdictions require that the entire amount be nonadmitted. Rental income paid in advance of the accounting period for which it is payable in whole or in part should be included in the liability for unearned investment income to the extent it applies to the succeeding accounting period. If rental income is to be received over a period shorter than the full lease period, the total rent to be received should be accrued periodically as if the rent were received over the total lease period. Interest expense on a mortgage is netted against the rental income for the period. In the statutory financial statement, a company must include in both its income and expenses an amount for rent relating to its occupancy of its own buildings. This amount can be the estimated current market rental value of the space involved, or it can be the amount derived from consideration of the repairs, expenses, taxes, and depreciation incurred, plus interest added at an average fair rate on the book value of the company's investment in its home office building. The figure thus determined, being both charged to expenses and credited to income, has no effect either on the company's overall net income or surplus. Sale of Real Estate

A company can recognize the sale of any real estate that it owns as an immediate cash sale or as a contract of sale. In a sale for cash and/or mortgage, title transfers to the buyer when the sale is consummated. Any profit or loss on the sale is considered to be realized in the year of sale. In a sale involving an installment contract, often referred to as land contracts, title is retained by the seller and transferred to the buyer only when he has paid the entire sales price, or a substantial portion of it. If the sale of real estate, including real estate occupied by the Company, includes a mortgage or other note from the Company, some states may require the transaction be reported as a financing transaction using the deposit method of accounting for sale-leaseback transaction. An insurer does not take credit for any profit from the sale or exchange of its assets when the consideration received and otherwise properly reported as an admitted asset is in the form of an installment contract, unless such profit is fully reserved by a liability established which is equal to the portion of such profit which is unrealized. In computing the realized portion of the profit on installment contracts, payments are allocated at the rate the principal is reduced by said payments. Depreciation and Amortization The cost of property, other than land, should be depreciated over its estimated useful life. Useful lives for buildings and improvements can best be obtained from contractors, appraisers, engineers, and manufacturers. Estimates published by the Internal Revenue Service can be helpful in the selection of useful lives for specific assets. Depreciable life may at times be fixed by contract, such as in a leasehold investment. A variety of depreciation methods is available and a company should select the method that is most appropriate provided, however, that the method is both systematic and rational. Depreciation methods in use include the straight-line method, and accelerated methods, such as sum-of-the-years digits and various declining balance methods. Because real estate leasehold improvements revert to the lessor at the end of the lease and the lessee receives benefits from the improvements only during the life of the lease, a leasehold improvement is subject to amortization over the lease life.

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–10

Expenses and Capital Improvements Repairs and maintenance expenditures may be classified as ordinary or extraordinary. As a general rule, expenditures for ordinary repairs that are necessary to put assets back into good operating condition, and for maintenance to keep them that way, are expensed as they are incurred. Extraordinary expenditures which add to or prolong the life of the property should be capitalized. In practice, most organizations establish a minimum capitalization amount. Individual expenditures below this minimum are expensed rather than capitalized to avoid capitalization of immaterial amounts. Other expenses in operating real estate are expensed as incurred. Other Real Estate Taxes Except for the development phase of a project, real and personal property taxes are charged against income. Real and personal property taxes are based upon the assessed valuation of property, as of a given date, as determined by the laws of a state or other taxing authority. The proper accounting treatment must determine when the liability for real and personal property taxes should be accrued. Consistency of application from year to year in establishing this liability is the most important consideration. The preferred basis for determining the liability and charges for real and personal property taxes should be established at the time of purchase. A practical aspect of the legal liability for these taxes must be considered when title to property is transferred during the taxable year, whereby the date of personal obligation generally controls. Adjustments for property taxes paid or accrued are frequently incorporated in agreements covering the sale of the real estate and determined between the buyer's and seller's obligations. Once established, this liability can be applied consistently throughout the ownership of the property.

21. The Accounting Practices and Procedures Manual for Property and Casualty Insurance Companies provides similar guidance to the above paragraph. 22. The Accounting Practice and Procedures Manual for Life and Accident and Health Insurance Companies, Chapter 22, General Expenses and Taxes, Licenses and Fees, includes the following guidance:

11. Real estate expenses include all costs except salaries and wages of company employees that relate to real estate, whether occupied by the company or not.

23. The Accounting Practices and Procedures Manual for Property and Casualty Insurance Companies, Chapter 19, Expenses, contains the following pertinent excerpts:

3. Taxes, Licenses, and Fees

These are state and local insurance taxes, insurance department licenses and fees, allocable payroll taxes, and all other taxes excluding federal and foreign income and real estate taxes. Real estate taxes on investment properties are generally included with investment expenses, and capital stock taxes and apportioned payroll taxes may be reported as investment expenses.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–11

24. Minnesota state regulations include the following specific guidelines related to valuation of real estate investments:

60A.122 Mortgage and real estate valuation An insurer shall establish written procedures, approved by the company's board of directors, for the valuation of commercial mortgage loans and real estate owned. The procedures must be made available to the commissioner upon request. The commissioner shall review the insurer's compliance with the procedures in any examination of the insurer under section 60A.031.

60A.123 Valuation of foreclosures; reserves Subdivision 1. Requirement. An insurer shall value its commercial mortgage loans and real estate acquired through foreclosure of commercial mortgage loans as provided in this section for the purpose of establishing reserves or carrying values of the investments and for statutory accounting purposes.

Subdivision 2. Performing mortgage loan. A performing mortgage loan must be carried at its amortized cost.

Subdivision 3. Distressed mortgage loan.

(a) The insurer shall make an evaluation of the appropriate carrying value of its commercial mortgage loans which it classifies as distressed mortgage loans. The carrying value must be based upon one or more of the following procedures:

(1) an internal appraisal; (2) an appraisal made by an independent appraiser; (3) the value of guarantees or other credit enhancements related to the loan.

(b) The insurer may determine the carrying value of its distressed mortgage loans through either an evaluation of each specific distressed mortgage loan or by a sampling methodology. Insurers using a sampling methodology shall identify a sampling of its distressed mortgage loans that represents a cross section of all of its distressed mortgage loans. The insurer shall make an evaluation of the appropriate carrying value for each sample loan. The carrying value of all of the insurer's distressed mortgage loans must be the same percentage of their amortized acquisition cost as the sample loans. The carrying value must be based upon an internal appraisal or an appraisal conducted by an independent appraiser. (c) The insurer shall either take a charge against its surplus or establish a reserve for the difference between the carrying value and the amortized acquisition cost of its distressed mortgage loans.

Subdivision 4. Delinquent mortgage loan.

(a) The insurer shall make an evaluation of the appropriate carrying value of each delinquent mortgage loan. The carrying value must be based upon one or more of the following procedures:

(1) an internal appraisal; (2) an appraisal by an independent appraiser; (3) the value of guarantees or other credit enhancements related to the loan.

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–12

(b) The insurer shall either take a charge against its surplus or establish a reserve for the difference between the carrying value and the amortized acquisition cost of its delinquent mortgage loans.

Subdivision 5. Restructured mortgage loan.

(a) The insurer shall make an evaluation of the appropriate carrying value of each restructured mortgage loan. The carrying value must be based upon one or more of the following procedures:

(1) an internal appraisal; (2) an appraisal by an independent appraiser; (3) the value of guarantees or other credit enhancements related to the loan.

(b) The insurer shall either take a charge against its surplus or establish a reserve for the difference between the carrying value and the amortized acquisition cost of its restructured mortgage loans. Subdivision 6. Mortgage loan in foreclosure.

(a) The insurer shall make an evaluation of the appropriate carrying value of each mortgage loan in foreclosure. The carrying value must be based upon an appraisal made by an independent appraiser. (b) The insurer shall take a charge against its surplus for the difference between the carrying value and the amortized acquisition cost of its mortgage loans in the process of foreclosure.

Subdivision 7. Real estate owned.

(a) The insurer shall make an evaluation of the appropriate carrying value of real estate owned. The carrying value must be based upon an appraisal made by an independent appraiser. (b) The insurer shall take a charge against its surplus for the difference between the carrying value and the amortized acquisition cost of real estate owned.

60A.125 Property and mortgage loan appraisal

Subdivision 1. Mortgage loans in the process of foreclosure. An insurer may rely upon an appraisal by an independent appraiser to determine the carrying value of mortgage loans in the process of foreclosure only if the date of the appraisal is within six months of the date the foreclosure procedure is begun. If no appraisal exists, the insurer shall acquire an appraisal within six months after the foreclosure proceeding has begun. Subdivision 2. Real estate owned. An insurer may rely upon an appraisal by an independent appraiser to determine the carrying value of real estate owned only if the date of the appraisal is within six months of the date when title to the property was acquired. If no appraisal exists, the insurer shall acquire an appraisal within six months after title to the property is acquired. Subdivision 3. Charge taken. An insurer shall take a charge against the surplus for mortgage loans in the process of foreclosure and real estate owned in the first calendar year in which it holds a current appraisal made by an independent appraiser as provided in this section.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–13

25. Missouri state regulations also include specific guidelines related to valuation of real estate investments:

20 CSR 200-13.100 Appraisal requirements Purpose: This rule upgrades the quality of real estate appraisals used by insurers by requiring appraisals meet the same standards as those applicable to federally-regulated financial institutions. This rule effectuates or aids in the interpretation of sections 375.330, 376.300 and 379.080, RSMo. Editor's Note: The secretary of state has determined that the publication of this rule in its entirety would be unduly cumbersome or expensive. The entire text of the material referenced has been filed with the secretary of state. This material may be found at the Office of the Secretary of State or at the headquarters of the agency and is available to any interested person at a cost established by state law.

(1) Any real estate held as an investment for the production of income pursuant to section 375.330.1(7), RSMo, or any mortgage loan made pursuant to section 376.300.1(9) or 379.080.1(2)(f), RSMo, excluding purchase money mortgages as identified in section 376.300.1(9), RSMo, may be held as an admissible asset only if the appraisal --

(A) Is made of real estate no more than one hundred twenty (120) days before the date the deed or mortgage is recorded in the appropriate public records;

(B) Is a written statement that is independently and impartially prepared by a licensed or certified appraiser setting forth an opinion of defined value of an adequately described property as of a specific date, supported by presentation and analysis of relevant market information;

(C) Provides the current market value of the real estate, that is the value of the real estate in an arms-length sale as of the date of the appraisal; and

(D) Is made by an individual who is --

1. On the national registry of state-certified and licensed appraisers who are eligible to perform appraisals in federally related transactions, which national registry is maintained pursuant to United States P.L. 101-73, Title XI, Section 1103 (12 USC Section 3332); and

2. Certified or licensed to make the appraisal by the state in which the real estate is located.

(2) Notwithstanding any provision of section (1) of this rule to the contrary, no appraisal is necessary in order to admit as an asset the holding of any debt or security issued, assumed or guaranteed by the United States, any state, territory or possession of the United States, the District of Columbia or any administration, agency, authority or instrumentality of them, but only to the extent that the debit or security is issued, assumed insured or guaranteed by any such entity. (3) Notwithstanding any provision of section (1) of this rule to the contrary, an insurer may establish written procedures, approved by the company's board of directors, for the valuation of its real estate and mortgage loans, which shall exempt the insurer from all of the provisions of section (1). The written procedures must be approved by the director. The director may review the insurer's compliance with these procedures. The director must be notified of any material changes to the written procedures. To be exempt under this section, an insurer's mortgage loan and real estate operations shall meet the following minimum standards:

(A) The insurer shall hold a combined mortgage loan and real estate portfolio valued at three hundred (300) million dollars or more;

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–14

(B) The insurer shall establish written procedures and obtain board approval and approval by the director within one hundred twenty (120) days (August 6, 1993) of the effective date of this rule (April 8, 1993);

(C) The insurer, as part of the written procedures, shall establish a reasonable system of valuation of its mortgage loans and real estate which includes the following elements:

1. A system to value its real estate acquired through foreclosure for the purpose of establishing reserves or carrying values of the investments and for statutory accounting purposes;

2. A program for the training, education and certification of employees, at least one (1) of whom must be certified as described in paragraph (1)(D)1. of this rule, who conducts internal appraisals of investments, or a system involving the use of independent certified appraisers as described in paragraph (1)(D)1. of this rule. Any internal appraiser shall not be compensated, directly or indirectly, on the basis of the outcome of appraisals performed and shall have direct reporting access to the chief investment officer of the insurer; and 3. Carrying values for the foreclosed real estate shall be based upon the internal appraisal or an independent appraisal and the value of the guarantees or other credit enhancements related to the investment; and

(D) The audit report of the independent certified public accountant which prepares the audit of the insurer's annual statement shall contain findings by the auditor that --

1. The insurer has adopted valuation procedures meeting the requirements of section (3) of this rule;

2. The procedures adopted by the board of directors have been uniformly applied by the insurer in conformance with section (3) of this rule; and

3. The management of the insurer has an adequate system of internal controls.

26. Nevada Statutes - Insurance Laws, TITLE 57 --- INSURANCE - Chapter 681B - ASSETS AND LIABILITIES provides the following guidance on real estate valuation:

681B.180 Real property 1. Real property acquired pursuant to a mortgage loan or contract for sale, in the absence of a recent appraisal deemed by the commissioner to be reliable, shall not be valued at an amount greater than the unpaid principal of the defaulted loan or contract plus interest due and accrued at the date of such acquisition, together with any taxes and expenses paid or incurred in connection with such acquisition, and the cost of improvements thereafter made by the insurer and any amounts thereafter paid by the insurer on assessments levied for improvements in connection with the property. 2. Other real property held by an insurer shall not be valued at an amount in excess of fair value as determined by recent appraisal. If valuation is based on an appraisal more than 3 years old, the commissioner may, at his discretion, call for and require a new appraisal in order to determine fair value.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–15

27. Arizona Statutes - Insurance Laws, TITLE 20-- INSURANCE, Chapter 3 FINANCIAL PROVISIONS AND PROCEDURES, Article 1. Assets and Liabilities provides similar guidance:

20-513 Real and personal property valuation A. Real property acquired pursuant to a mortgage loan or contract for sale, in the absence of a recent appraisal deemed by the director to be reliable, shall not be valued at an amount greater than the unpaid principal of the defaulted loan or contract at the date of such acquisition, together with any taxes and expenses paid or incurred in connection with such acquisition, and the cost of improvements thereafter made by the insurer and any amounts thereafter paid by the insurer on assessments levied for improvements in connection with the property. B. Other real property held by an insurer shall not be valued at an amount in excess of fair value as determined by recent appraisal. If valuation is based on an appraisal more than three years old, the director may at his discretion call for and require a new appraisal in order to determine fair value. C. Personal property acquired pursuant to chattel mortgages made in accordance with section 20-555 shall not be valued at an amount greater than the unpaid balance of principal on the defaulted loan at the date of acquisition, together with taxes and expenses incurred in connection with the acquisition, or the fair value of the property, whichever amount is the lesser.

Generally Accepted Accounting Principles 28. FASB Statement No. 60, Accounting and Reporting by Insurance Enterprises, provides the following guidance:

48. Real estate investments shall be reported at cost less accumulated depreciation and an allowance for any impairment in value. Depreciation and other related charges or credits shall be charged or credited to investment income. Changes in the allowance for any impairment in value relating to real estate investments shall be included in realized gains and losses.

29. FASB Statement No. 66, Accounting for Sales of Real Estate, provides the following guidance:

INTRODUCTION

1. This Statement establishes standards for recognition of profit on all real estate sales transactions without regard to the nature of the seller's business. The Statement distinguishes between retail land sales and other sales of real estate because differences in terms of sales and selling procedures lead to different profit recognition criteria and methods. Accounting for real estate sales transactions that are not retail land sales is specified in paragraphs 3-43. Accounting for retail land sales transactions is specified in paragraphs 44-50. This Statement does not cover exchanges of real estate for other real estate, the accounting for which is covered in APB Opinion No. 29, Accounting for Nonmonetary Transactions.

2. Although this Statement applies to all sales of real estate, many of the extensive provisions were developed over several years to deal with complex transactions that are frequently encountered in enterprises that specialize in real estate transactions. The decision trees on pages 75-79 highlight the major provisions of the Statement and will help a user of the Statement identify criteria that determine when and how profit is recognized. Those using this Statement to determine the accounting for relatively simple real estate sales transactions will need to apply only limited portions of the Statement. The general requirements for recognizing all of the profit on a nonretail land sale at the date of sale are set forth in paragraphs 3-5 and are highlighted on the decision tree on page 75. Paragraphs 6-18 elaborate on those general provisions. Paragraphs 19-43 provide more detailed guidance for a variety of more complex transactions.

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–16

STANDARDS OF FINANCIAL ACCOUNTING AND REPORTING

Real Estate Sales Other Than Retail Land Sales

Recognition of Profit by the Full Accrual Method

3. Profit shall be recognized in full when real estate is sold, provided (a) the profit is determinable, that is, the collectibility of the sales price is reasonably assured or the amount that will not be collectible can be estimated, and (b) the earnings process is virtually complete, that is, the seller is not obliged to perform significant activities after the sale to earn the profit. Unless both conditions exist, recognition of all or part of the profit shall be postponed. Recognition of all of the profit at the time of sale or at some later date when both conditions exist is referred to as the full accrual method in this Statement.

4. In accounting for sales of real estate, collectibility of the sales price is demonstrated by the buyer's commitment to pay, which in turn is supported by substantial initial and continuing investments that give the buyer a stake in the property sufficient that the risk of loss through default motivates the buyer to honor its obligation to the seller. Collectibility shall also be assessed by considering factors such as the credit standing of the buyer, age and location of the property, and adequacy of cash flow from the property.

5. Profit on real estate sales transactions1 shall not be recognized by the full accrual method until all of the following criteria are met:

________________________________

1 Profit on a sale of a partial interest in real estate shall be subject to the same criteria for profit recognition as a sale of a whole interest. ________________________________

a. A sale is consummated (paragraph 6). b. The buyer's initial and continuing investments are adequate to demonstrate a

commitment to pay for the property (paragraphs 8-16). c. The seller's receivable is not subject to future subordination (paragraph 17). d. The seller has transferred to the buyer the usual risks and rewards of ownership in a

transaction that is in substance a sale and does not have a substantial continuing involvement with the property (paragraph 18).

Paragraphs 19-43 describe appropriate accounting if the above criteria are not met.

Consummation of a Sale

6. A sale shall not be considered consummated until (a) the parties are bound by the terms of a contract, (b) all consideration has been exchanged, (c) any permanent financing for which the seller is responsible has been arranged, and (d) all conditions2 precedent to closing have been performed. Usually, those four conditions are met at the time of closing or after closing, not when an agreement to sell is signed or at a preclosing.

________________________________

2 Paragraph 20 provides an exception to this requirement if the seller is constructing office buildings, condominiums, shopping centers, or similar structures. ________________________________

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–17

Buyer's Initial and Continuing Investment

7. “Sales value” shall be determined by: a. Adding to the stated sales price the proceeds from the issuance of a real estate option

that is exercised and other payments that are in substance additional sales proceeds. These nominally may be management fees, points, or prepaid interest or fees that are required to be maintained in an advance status and applied against the amounts due to the seller at a later date.

b. Subtracting from the sale price a discount to reduce the receivable to its present value

and by the net present value of services that the seller commits to perform without compensation or by the net present value of the services in excess of the compensation that will be received. Paragraph 31 specifies appropriate accounting if services are to be provided by the seller without compensation or at less than prevailing rates.

8. Adequacy of a buyer's initial investment shall be measured by (a) its composition (paragraphs 9-10) and (b) its size compared with the sales value of the property (paragraph 11).

9. The buyer's initial investment shall include only: (a) cash paid as a down payment, (b) the buyer's notes supported by irrevocable letters of credit from an independent established lending institution,3 (c) payments by the buyer to third parties to reduce existing indebtedness on the property, and (d) other amounts paid by the buyer that are part of the sales value. Other consideration received by the seller, including other notes of the buyer, shall be included as part of the buyer's initial investment only when that consideration is sold or otherwise converted to cash without recourse to the seller.

________________________________

3 An “independent established lending institution” is an unrelated institution such as a commercial bank unaffiliated with the seller. ________________________________

10. The initial investment shall not include:

a. Payments by the buyer to third parties for improvements to the property b. A permanent loan commitment by an independent third party to replace a loan made by

the seller c. Any funds that have been or will be loaned, refunded, or directly or indirectly provided to

the buyer by the seller or loans guaranteed or collateralized by the seller for the buyer4

________________________________

4 As an example, if unimproved land is sold for $100,000, with a down payment of $50,000 in cash, and the seller plans to loan the buyer $35,000 at some future date, the initial investment is $50,000 minus $35,000, or $15,000. ________________________________

11. The buyer's initial investment shall be adequate to demonstrate the buyer's commitment to pay for the property and shall indicate a reasonable likelihood that the seller will collect the receivable. Lending practices of independent established lending institutions provide a reasonable basis for assessing the collectibility of receivables from buyers of real estate. Therefore, to qualify, the initial investment shall be equal to at least a major part of the difference between usual loan limits and the sales value of the property. Guidance on minimum initial investments in various types of real estate is provided in paragraphs 53 and 54.

12. The buyer's continuing investment in a real estate transaction shall not qualify unless the buyer is contractually required to pay each year on its total debt for the purchase price of the property an amount at least equal to the level annual payment that would be needed to pay that

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–18

debt and interest on the unpaid balance over no more than (a) 20 years for debt for land and (b) the customary amortization term of a first mortgage loan by an independent established lending institution for other real estate. For this purpose, contractually required payments by the buyer on its debt shall be in the forms specified in paragraph 9 as acceptable for an initial investment. Except as indicated in the following sentence, funds to be provided directly or indirectly by the seller (paragraph 10.c.) shall be subtracted from the buyer's contractually required payments in determining whether the initial and continuing investments are adequate. If a future loan on normal terms from an established lending institution bears a fair market interest rate and the proceeds of the loan are conditional on use for specified development of or construction on the property, the loan need not be subtracted in determining the buyer's investment.

Release Provisions

13. An agreement to sell property (usually land) may provide that part or all of the property may be released from liens securing related debt by payment of a release price or that payments by the buyer may be assigned first to released property. If either of those conditions is present, a buyer's initial investment shall be sufficient both to pay release prices on property released at the date of sale and to constitute an adequate initial investment on property not released or not subject to release at that time in order to meet the criterion of an adequate initial investment for the property as a whole.

14. If the release conditions described in paragraph 13 are present, the buyer's investment shall be sufficient, after the released property is paid for, to constitute an adequate continuing investment on property not released in order to meet the criterion of an adequate continuing investment for the property as a whole (paragraph 12).

15. If the amounts applied to unreleased portions do not meet the initial and continuing-investment criteria as applied to the sales value of those unreleased portions, profit shall be recognized on each released portion when it meets the criteria in paragraph 5 as if each release were a separate sale.

16. Tests of adequacy of a buyer's initial and continuing investments described in paragraphs 8-15 shall be applied cumulatively when the sale is consummated and annually afterward. If the initial investment exceeds the minimum prescribed, the excess shall be applied toward the required annual increases in the buyer's investment.

Future Subordination

17. The seller's receivable shall not be subject to future subordination. This restriction shall not apply if (a) a receivable is subordinate to a first mortgage on the property existing at the time of sale or (b) a future loan, including an existing permanent loan commitment, is provided for by the terms of the sale and the proceeds of the loan will be applied first to the payment of the seller's receivable.

Continuing Involvement without Transfer of Risks and Rewards

18. If a seller is involved with a property after it is sold in any way that results in retention of substantial risks or rewards of ownership, except as indicated in paragraph 43, the absence-of-continuing-involvement criterion has not been met. Forms of involvement that result in retention of substantial risks or rewards by the seller, and accounting therefore, are described in paragraphs 25-42.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–19

Recognition of Profit When the Full Accrual Method Is Not Appropriate

19. If a real estate sales transaction does not satisfy the criteria in paragraphs 3-18 for recognition of profit by the full accrual method, the transaction shall be accounted for as specified in the following paragraphs.

Sale Not Consummated

20. The deposit method of accounting described in paragraphs 65-67 shall be used until a sale has been consummated (paragraph 6). “Consummation” usually requires that all conditions precedent to closing have been performed, including that the building be certified for occupancy. However, because of the length of the construction period of office buildings, apartments, condominiums, shopping centers, and similar structures, such sales and the related income may be recognized during the process of construction, subject to the criteria in paragraphs 41 and 42, even though a certificate of occupancy, which is a condition precedent to closing, has not been obtained.

21. If the net carrying amount of the property exceeds the sum of the deposit received, the fair value of the unrecorded note receivable, and the debt assumed by the buyer, the seller shall recognize the loss at the date the agreement to sell is signed.5 If a buyer defaults, or if circumstances after the transaction indicate that it is probable the buyer will default and the property will revert to the seller, the seller shall evaluate whether the circumstances indicate a decline in the value of the property for which an allowance for loss should be provided.

________________________________

5 Paragraph 24 of FASB Statement No. 67, Accounting for Costs and Initial Rental Operations of Real Estate Projects, specifies the accounting for an excess of costs over net realizable value for property that has not yet been sold. ________________________________

Initial or Continuing Investments Do Not Qualify

22. If the buyer's initial investment does not meet the criteria specified in paragraphs 8-11 for recognition of profit by the full accrual method and if recovery of the cost of the property is reasonably assured if the buyer defaults, the installment method described in paragraphs 56-61 shall be used. If recovery of the cost of the property is not reasonably assured if the buyer defaults or if cost has already been recovered and collection of additional amounts is uncertain, the cost recovery method (described in paragraphs 62-64) or the deposit method (described in paragraphs 65-67) shall be used. The cost recovery method may be used to account for sales of real estate for which the installment method would be appropriate.

23. If the initial investment meets the criteria in paragraphs 8-11 but the continuing investment by the buyer does not meet the criteria in paragraphs 12 and 16, the seller shall recognize profit by the reduced profit method described in paragraphs 68 and 69 at the time of sale if payments by the buyer each year will at least cover both of the following:

a. The interest and principal amortization on the maximum first mortgage loan that could be obtained on the property b. Interest, at an appropriate rate,6 on the excess of the aggregate actual debt on the property over such a maximum first mortgage loan

____________________________ 6 Paragraphs 13 and 14 of APB Opinion No. 21, Interest on Receivables and Payables, provide criteria for selecting an appropriate rate for present-value calculations. ____________________________

If the criteria specified in this paragraph for use of the reduced profit method are not met, the seller may recognize profit by the installment method (paragraphs 56-61) or the cost recovery method (paragraphs 62-64).

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–20

Receivable Subject to Future Subordination

24. If the seller's receivable is subject to future subordination as described in paragraph 17, profit shall be recognized by the cost recovery method (paragraphs 62-64).

Continuing Involvement without Transfer of Risks and Rewards

25. If the seller has some continuing involvement with the property and does not transfer substantially all of the risks and rewards of ownership, profit shall be recognized by a method determined by the nature and extent of the seller's continuing involvement. Generally, profit shall be recognized at the time of sale if the amount of the seller's loss of profit because of continued involvement with the property is limited by the terms of the sales contract. The profit recognized shall be reduced by the maximum exposure to loss. Paragraphs 26-43 describe some common forms of continuing involvement and specify appropriate accounting if those forms of involvement are present. If the seller has some other form of continuing involvement with the property, the transaction shall be accounted for according to the nature of the involvement. 26. The seller has an obligation to repurchase the property, or the terms of the transaction allow the buyer to compel the seller or give an option7 to the seller to repurchase the property. The transaction shall be accounted for as a financing, leasing, or profit-sharing arrangement rather than as a sale.

________________________________

7 A right of first refusal based on a bona fide offer by a third party ordinarily is not an obligation or an option to repurchase. ________________________________

27. The seller is a general partner in a limited partnership that acquires an interest in the property sold (or has an extended, noncancelable management contract requiring similar obligations) and holds a receivable from the buyer for a significant8 part of the sales price. The transaction shall be accounted for as a financing, leasing, or profit-sharing arrangement.

____________________________ 8 For this purpose, a significant receivable is a receivable in excess of 15 percent of the maximum first-lien financing that could be obtained from an independent established lending institution for the property. It would include:

a. A construction loan made or to be made by the seller to the extent that it exceeds the minimum funding

commitment for permanent financing from a third party that the seller will not be liable for b. An all-inclusive or wraparound receivable held by the seller to the extent that it exceeds prior-lien financing

for which the seller has no personal liability c. Other funds provided or to be provided directly or indirectly by the seller to the buyer d. The present value of a land lease when the seller is the lessor (footnote 15) ____________________________

28. The seller guarantees9 the return of the buyer's investment or a return on that investment for a limited or extended period. For example, the seller guarantees cash flows, subsidies, or net tax benefits. If the seller guarantees return of the buyer's investment or if the seller guarantees a return on the investment for an extended period, the transaction shall be accounted for as a financing, leasing, or profit-sharing arrangement. If the guarantee of a return on the investment is for a limited period, the deposit method shall be used until operations of the property cover all operating expenses, debt service, and contractual payments. At that time, profit shall be recognized on the basis of performance of the services required, as illustrated in paragraphs 84-88.

____________________________ 9 Guarantees by the seller may be limited to a specified period of time. ____________________________

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–21

29. The seller is required to initiate or support operations or continue to operate the property at its own risk, or may be presumed to have such a risk, for an extended period, for a specified limited period, or until a specified level of operations has been obtained, for example, until rentals of a property are sufficient to cover operating expenses and debt service. If support is required or presumed to be required10 for an extended period of time, the transaction shall be accounted for as a financing, leasing, or profit-sharing arrangement. If support is required or presumed to be required for a limited time, profit on the sale shall be recognized on the basis of performance of the services required. Performance of those services shall be measured by the costs incurred and to be incurred over the period during which the services are performed. Profit shall begin to be recognized when there is reasonable assurance that future rent receipts will cover operating expenses and debt service including payments due the seller under the terms of the transaction. Reasonable assurance that rentals will be adequate would be indicated by objective information regarding occupancy levels and rental rates in the immediate area. In assessing whether rentals will be adequate to justify recognition of profit, total estimated future rent receipts of the property shall be reduced by one-third as a reasonable safety factor unless the amount so computed is less than the rents to be received from signed leases. In this event, the rents from signed leases shall be substituted for the computed amount. Application of this method is illustrated in paragraphs 84-89.

________________________________

10 Support shall be presumed to be required if: (a) a seller obtains an interest as a general partner in a limited partnership that acquires an interest in the property sold; (b) a seller retains an equity interest in the property, such as an undivided interest or an equity interest in a joint venture that holds an interest in the property; (c) a seller holds a receivable from a buyer for a significant part of the sales price and collection of the receivable depends on the operation of the property; or (d) a seller agrees to manage the property for the buyer on terms not usual for the services to be rendered, and the agreement is not terminable by either the seller or the buyer. ________________________________

30. If the sales contract does not stipulate the period during which the seller is obligated to support operations of the property, support shall be presumed for at least two years from the time of initial rental unless actual rental operations cover operating expenses, debt service, and other contractual commitments before that time. If the seller is contractually obligated for a longer time, profit recognition shall continue on the basis of performance until the obligation expires. Calculation of profits on the basis of performance of services is illustrated in paragraphs 84-89.

31. If the sales contract requires the seller to provide management services relating to the property after the sale without compensation or at compensation less than prevailing rates for the service required (paragraph 7) or on terms not usual for the services to be rendered (footnote 10(d)), compensation shall be imputed when the sale is recognized and shall be recognized in income as the services are performed over the term of the management contract.

32. The transaction is merely an option to purchase the property. For example, undeveloped land may be “sold” under terms that call for a very small initial investment by the buyer (substantially less than the percentages specified in paragraph 54) and postponement of additional payments until the buyer obtains zoning changes or building permits or other contingencies specified in the sales agreement are satisfactorily resolved. Proceeds from the issuance of the option by a property owner shall be accounted for as a deposit (paragraphs 65-67). Profit shall not be recognized until the option either expires or is exercised. When an option to purchase real estate is sold by an option holder,11 the seller of the option shall recognize income by the cost recovery method (paragraphs 62-64) to the extent nonrefundable cash proceeds exceed the seller's cost of the option if the buyer's initial and continuing investments are not adequate for profit recognition by the full accrual method (paragraphs 7-16).

________________________________

11 When an option to purchase real estate is sold by an option holder, the sales value includes the exercise price of the option and the sales price of the option. For example, if the option is sold for $150,000 ($50,000 cash and a $100,000 note) and the exercise price is $500,000, the sales value is $650,000. ________________________________

© 1999-2017 National Association of Insurance Commissioners

IP No. 40 Issue Paper

IP 40–22

33. The seller has made a partial sale. A sale is a partial sale if the seller retains an equity interest in the property or has an equity interest in the buyer. Profit (the difference between the sales value and the proportionate cost of the partial interest sold) shall be recognized at the date of sale if:

a. The buyer is independent of the seller. b. Collection of the sales price is reasonably assured (paragraph 4). c. The seller will not be required to support the operations of the property or its related

obligations to an extent greater than its proportionate interest.

34. If the buyer is not independent of the seller, for example, if the seller holds or acquires an equity interest in the buyer, the seller shall recognize the part of the profit proportionate to the outside interests in the buyer at the date of sale. If the seller controls the buyer, no profit on the sale shall be recognized until it is realized from transactions with outside parties through sale or operations of the property. 35. If collection of the sales price is not reasonably assured, the cost recovery or installment method of recognizing profit shall be used.

36. If the seller is required to support the operations of the property after the sale, the accounting shall be based on the nature of the support obligation. For example, the seller may retain an interest in the property sold and the buyer may receive preferences as to profits, cash flows, return on investment, and so forth. If the transaction is in substance a sale, the seller shall recognize profit to the extent that proceeds from the sale, including receivables from the buyer, exceed all of the seller's costs related to the entire property. Other examples of support obligations are described in paragraphs 29-31.

37. If individual units in condominium projects12 or time-sharing interests are being sold separately and all the following criteria are met, profit shall be recognized by the percentage-of-completion method on the sale of individual units or interests:

________________________________

12 A condominium project may be a building, a group of buildings, or a complete project. ________________________________

a. Construction is beyond a preliminary stage.13

________________________________

13 Construction is not beyond a preliminary stage if engineering and design work, execution of construction contracts, site clearance and preparation, excavation, and completion of the building foundation are incomplete. ________________________________

b. The buyer is committed to the extent of being unable to require a refund except for

nondelivery of the unit or interest.14

________________________________

14 The buyer may be able to require a refund, for example, if a minimum status of completion of the project is required by state law and that status has not been attained; if state law requires that a “Declaration of Condominium” be filed and it has not been filed, except that in some states the filing of the declaration is a routine matter and the lack of such filing may not make the sales contract voidable; if the sales contract provides that permanent financing at an acceptable cost must be available to the buyer at the time of closing and it is not available; or if the condominium units must be registered with either the Office of Interstate Land Sales Registration of the Department of Housing and Urban Development or the Securities and Exchange Commission, and they are not so registered. ________________________________

c. Sufficient units have already been sold to assure that the entire property will not revert to

rental property. In determining whether this condition has been met, the seller shall consider the requirements of state laws, the condominium or time-sharing contract, and the terms of the financing agreements.

© 1999-2017 National Association of Insurance Commissioners

Real Estate Investments IP No. 40

IP 40–23

d. Sales prices are collectible (paragraph 4).

e. Aggregate sales proceeds and costs can be reasonably estimated. Consideration shall be given to sales volume, trends of unit prices, demand for the units including seasonal factors, developer's experience, geographical location, and environmental factors.

If any of the above criteria is not met, proceeds shall be accounted for as deposits until the criteria are met.