states and sourcing: heads i win, tails you lose · 2016 ipt annual conference learning objectives...

TRANSCRIPT

2016 IPT Annual Conference

States and Sourcing: Heads I Win, Tails You Lose

Chuck Jones Director

Grant Thornton LLP Chicago, IL

Kelli Murphy State & Local Tax Attorney Ford Motor Company

Dearborn, MI [email protected]

2016 IPT Annual Conference

Learning Objectives

2

• Differentiate between cost-of-performance approach and market-based method for sourcing service revenue

• Assess impact of Equifax decision from Mississippi and resulting legislative response

• Analyze issue that are relevant to Vodafone decision from Tennessee

2016 IPT Annual Conference

Learning Objectives (cont'd)

3

• Evaluate administrative decisions from Indiana and Florida that apply a market-based sourcing approach

• Determine sourcing methodology that will be applied by the revenue departments in these states

2016 IPT Annual Conference 4

Cost of Performance

• Traditionally, Multistate Tax Compact used an equally-weighted three-factor apportionment formula

• Cost of performance (COP) method used to source sales other than sales of tangible personal property (TPP) • Methodology applies to services

2016 IPT Annual Conference 5

Cost of Performance (cont'd)

• Article IV provided sales, other than sales of TPP, are in state if • Income-producing activity performed in

state • Income-producing activity performed both

in and outside state and greater proportion of income-producing activity performed in the state than any other state, based on COP

• COP: Preponderance (all or nothing) v. proportionate (pro rata)

2016 IPT Annual Conference 6

Market-Based Sourcing

• General apportionment trend: single or heavily weighted sales factor

• As more states move to rely heavily on sales factor to apportion income, definition of a sale, and what income is considered sourced to a state, is more important

• States changing from COP to market-based sourcing (MBS) • Sourced to where customer receives

benefit of service or to where service is delivered

2016 IPT Annual Conference 7

Market-Based Sourcing (cont'd)

• In 2014, Article IV of Compact amended: • Double-weighted sales factor

recommended • Changed from COP to MBS • Sales of other than TPP are sourced to

state if, and to extent, taxpayer's market for sale is in state

• Sale of service sourced to state if, and to extent, service is delivered to location in state

2016 IPT Annual Conference 8

Market-Based Sourcing (cont'd)

• Lack of uniformity by states in determining market

• Some states (for example, CA, IL, MI and WI) follow a "benefits received" approach rather than the MTC's location of delivery approach

• Distinction between sales to individuals and sales to other businesses

• Unlike the Compact, some states (for example, CA, MI, PA and WI) do not have a throw-out rule

2016 IPT Annual Conference 9

Market-Based Sourcing (cont'd) • Reasons for moving to MBS

• Difficulty in determining location of costs of production for services or intangibles

• Attempt to match receipts to source of corresponding revenue stream

• Desire to reduce tax burden on in-state economic factors and to reduce tax burden on mobile capital

• As states have increased weight of sales factor, MBS makes theoretical and economic sense

• Move away from "all or nothing approach"

2016 IPT Annual Conference

AK

ME

RI

VT NH MA NY

CT

PA

DE

VA WV

NC

SC

GA

FL

IL OH IN

MI WI

KY

TN

AL MS

AR

LA TX

OK

MO KS

IA

MN

ND

SD

NE

NM AZ

CO UT

WY

MT

WA

OR

ID

NV

CA

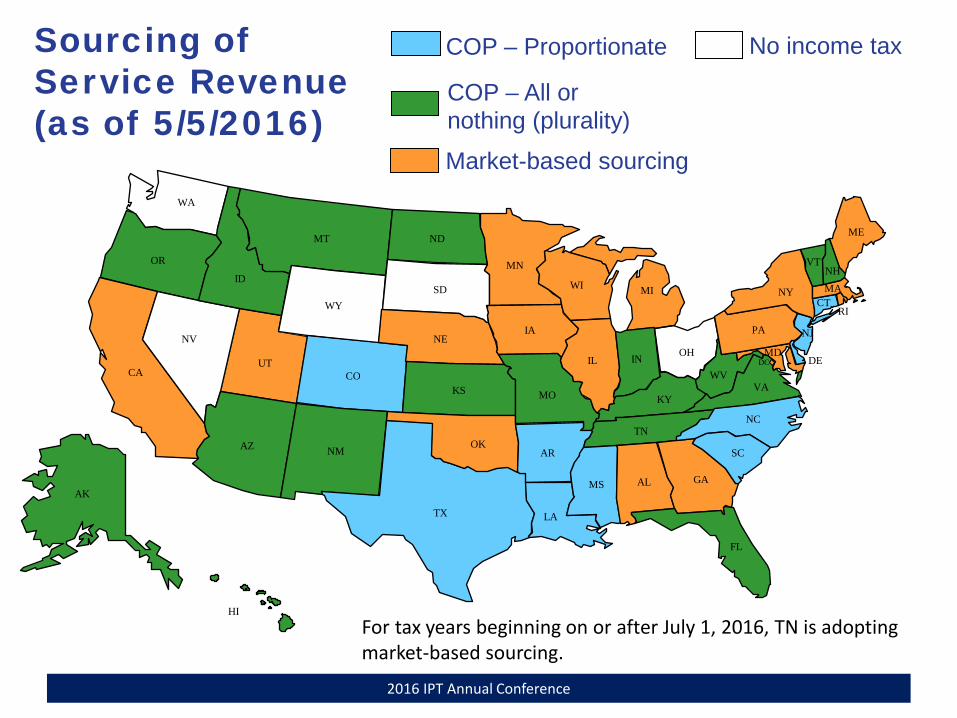

Market-based sourcing

COP – All or nothing COP – All or nothing (plurality) COPCO:L

MD

NJ

DC

HI

For tax years beginning on or after July 1, 2016, TN is adopting market-based sourcing.

Sourcing of Service Revenue (as of 5/5/2016)

COP – Proportionate

Market-based sourcing

No income tax

2016 IPT Annual Conference 11

Alternative Apportionment

• Under Multistate Tax Compact, Article IV, Section 18, if general apportionment provisions do not fairly represent extent of taxpayer's business activity in state, taxpayer may petition for or tax administrator may require an alternative apportionment method

• Adopted in most states (or similar provisions) • Purpose is to promote uniformity • Permitted in limited circumstances involving

unusual facts

2016 IPT Annual Conference 12

Alternative Apportionment (cont'd) • In 2014, MTC added new paragraph:

• If apportionment provisions do not fairly represent extent of business activity of taxpayers engaged in specific industry, transaction or activity, tax administrator may establish regulations for determining alternative apportionment

• Regulation must be applied uniformly, but taxpayer may petition for or tax administrator may require adjustment to fairly represent extent of taxpayer's business activity in state

2016 IPT Annual Conference 13

Alternative Apportionment (cont'd) • In 2015, MTC further amended Section 18:

• Relevant burden of proof necessary to support alternative apportionment is left up to each state

• Party seeking change must overcome same burden of proof to establish need for change in apportionment method

• However, tax administrator does not have burden to require taxpayer to use alternative method if taxpayer used other than standard method or approved method during any two of prior five years

2016 IPT Annual Conference 14

Equifax Case • In Equifax, Inc. v. Mississippi Department of

Revenue, 125 So.3d 36 (Miss. 2013), MS Supreme Court endorsed Department's alternative apportionment approach requiring taxpayer to use MBS in lieu of statutory COP method

• GA corporation in business of consumer credit reporting that employed three MS residents and had approximately 800 MS-based customers, but did not have any property located in state

• Applying COP, taxpayer concluded that it had no income subject to tax in MS

2016 IPT Annual Conference 15

Equifax Case (cont'd)

• DOR determined standard apportionment method did not accurately reflect extent of taxpayer's business in state

• Taxpayer required to use MBS • Taxpayer had burden of proving by

preponderance of evidence that alternative method imposed by DOR was arbitrary and capricious or violated its constitutional rights

• Decision received considerable attention and criticism as being adverse to business climate

2016 IPT Annual Conference 16

Legislative Response • In April 2014, MS enacted legislation

addressing Equifax (H.B. 799, Laws 2014, effective Jan. 1, 2015)

• Party requesting alternative apportionment bears burden of proof by preponderance of evidence to show two elements: • Statutory or regulatory method does not

fairly represent taxpayer's MS business activity; and

• Proposed method more fairly represents the activity than any other reasonable method

2016 IPT Annual Conference 17

Legislative Response (cont'd) • Legislation benefits taxpayers by replacing

Equifax burden of proof standard that favored state with new standard that places burden on moving party

• Alternative apportionment is intended to be invoked only in "limited and unique, nonrecurring circumstances" where use of statute or regulation unfairly represents business activity in state

• DOR may not routinely reject standard apportionment methodology and arbitrarily invoke alternative apportionment to increase sales assigned to state

2016 IPT Annual Conference 18

Vodafone Case • On March 23, 2016, in Vodafone Americas

Holding, Inc. v. Roberts, TN Supreme Court upheld authority of Commissioner to require alternative apportionment when statutory COP method did not fairly represent extent of taxpayer's business activity in state

• Commissioner imposed variance requiring telecommunications company to source its receipts using MBS approach

• CA-based telecommunications company that held 45% interest in partnership that operated telecommunications business

2016 IPT Annual Conference 19

Vodafone Case (cont'd) • In its original return, taxpayer calculated its

sales factor by using MBS method that sourced to TN sales of services that were made to customers with TN billing address

• Filed refund claim arguing that statutory COP method should be used to apportion income instead of MBS method

• Under COP, majority of costs associated with services were incurred in NJ

• Use of COP resulted in over $1 billion in previously taxable earnings no longer being taxable in TN or any other state (apportionment reduced by 89%)

2016 IPT Annual Conference 20

Vodafone Case (cont'd)

• Commissioner issued apportionment variance letter and argued that sales should be sourced using MBS method

• In a split decision, TN Court of Appeals held that Commissioner properly issued variance requiring taxpayer to apportion sales using MBS based on a customer's billing address

• In affirming lower court's decision, TN Supreme Court held imposition of variance was not an abuse of discretion

• Use of statutory formula was not fair reflection of taxpayer's business activity in TN

2016 IPT Annual Conference 21

Vodafone Case (cont'd) • Alternate formula selected by Commissioner in

the variance was reasonable • Did not violate regulation allowing alternative

apportionment "only in limited and specific cases . . . where unusual fact situations . . . produce incongruous results"

• Variance was within range of acceptable alternatives available to Commissioner, given the facts and circumstances

2016 IPT Annual Conference 22

Vodafone Case (cont'd) • TN Supreme Court seemed very concerned

about concept of nowhere income • Taxpayers in cases in which statutory formula

results in less income being sourced to TN than another apportionment method should be wary of potential impact of decision

• For tax years beginning on or after July 1, 2016, TN is replacing COP method for sourcing sales other than sales of TPP with MBS method

• Special sourcing provision applies to certain qualified telecommunications companies that are members of a qualified group

2016 IPT Annual Conference 23

Alternative Apportionment • States have been invoking alternative

apportionment under Section 18 (or an analogous provision) to achieve MBS where COP sourcing results in zero sales being attributed to state

• Many states are applying MBS on a case-by-case basis through either their audit process or by administrative rulings • FL • IN • MS • NY • PA (prior to amended statute)

2016 IPT Annual Conference 24

Indiana Rulings

• Indiana's apportionment statute and regulation parallel MTC's COP language

• Although IN has extensive COP regulation that includes examples, state has issued a series of administrative decisions that apply MBS

• Argument can be made that IN has unofficially adopted MBS through these rulings

2016 IPT Annual Conference 25

Indiana Rulings (cont'd)

• Out-of-state company providing online educational services to students within and outside IN could not use COP method to source income that it received from IN students to its out-of-state location (Letter of Findings No. 02-20140455, Jan. 28, 2015)

• Taxpayer charged tuition fees based on "credit hours"

• Because substantially all the costs of providing the services to IN student were incurred outside IN, taxpayer argued that tuition received from IN students should be sourced outside state

2016 IPT Annual Conference 26

Indiana Rulings (cont'd)

• According to the IN DOR, tuition from IN students constituted a principal source of the taxpayer's income and should be apportioned among states based on MBS

• Services were "rendered" in IN because that is where the students purchased the services

2016 IPT Annual Conference 27

Indiana Rulings (cont'd)

• In another ruling, out-of-state taxpayer that franchised restaurants to people in IN not allowed to use COP method to source franchise services (Letter of Findings No. 02-20130402, Feb. 25, 2015)

• Taxpayer argued that majority of income-producing activity performed in conjunction with its IN franchisees occurred in another state

• DOR determined that services "rendered" in IN because it was location where franchisees purchased services

2016 IPT Annual Conference 28

Indiana Rulings (cont'd)

• Appropriate for healthcare provider in another ruling to use MBS rather than standard COP (Revenue Ruling No. 2014-01IT, March 18, 2015)

• Taxpayer was in process of moving from CA to IN, and requested permission to use MBS to reduce its future audit burdens

• Under COP, taxpayer would likely have no IN sales because CA would be predominate state where sales should be sourced

• Under MBS, there were sales that would be sourced to IN because benefit of service received in IN

2016 IPT Annual Conference 29

Indiana Rulings (cont'd)

• Out-of-state service provider who sold online financial research and information services to customers in IN, but performed all research and information gathering outside state, was required to source gross receipts from those sales to IN (Letter of Findings 02-20130238, Sep. 25, 2013)

• Delivery of services to IN customers was income-producing activity rather than the functions performed outside state

2016 IPT Annual Conference 30

Florida Rulings

• FL apportionment statute and regulation use COP approach

• Similar to the IN DOR, the FL DOR has issued administrative rulings that require taxpayers to use MBS approach

2016 IPT Annual Conference 31

Florida Rulings (cont'd)

• A cable television network provided content directly to distributors that broadcasted the programming and had no direct contact with the final customers (Technical Assistance Advisement, No. 11C1-008, Sep. 15, 2011)

• According to FL DOR, sales should be sourced to distributor's location

• Although activities related to production of income may occur within or outside FL, these activities cannot rightly be called income-producing activity

• Advertising revenue constituted a FL sale when distributor was located in FL

2016 IPT Annual Conference 32

Florida Rulings (cont'd)

• A FL taxpayer offered courses through its physical classroom locations and through the Internet (Technical Assistance Advisement, No. 12C1-006, May 17, 2012)

• Sales attributed to FL if income-producing activity is within state

• Income-producing activity is defined as transaction and activity directly engaged in by taxpayer for ultimate purpose of obtaining gains or profits

• Tuition receipts from student who resided in FL should be sourced to FL

2016 IPT Annual Conference 33

Florida Rulings (cont'd)

• In another TAA, the DOR determined that receipts incurred from the licensing of television programming to cable operators should be sourced to customer locations (Technical Assistance Advisement, No. 12C1-004, May 21, 2013)

• The DOR reached a similar result in another TAA when it ruled that a data and analytics provider must source its service receipts to the location of its customers (Technical Assistance Advisement, No. 13C1-011, May 21, 2013)

2016 IPT Annual Conference 34

Sourcing Methodology Applied

• Important to consider how traditional COP states have recently interpreted their rules because many states have begun to apportion income using MBS approach

• Some COP states seem to have unofficially adopted MBS without enacting legislation

• This approach may be unexpected and misleading for corporate taxpayers

• Determination of appropriate sourcing methodology is fact specific

• Imposition of MBS is particularly common for taxpayers that provide online educational services or telecommunications services

2016 IPT Annual Conference 35

Uncertainty in Sourcing

• The recent sourcing developments seem to raise more questions than answers

• Because many of the COP states have been unofficially adopting MBS, the appropriate sourcing methodology may not be clear

• MBS statutes and regulations are not consistent among states

• Due to the recent adoption of MBS in some states, various state taxing authorities are still issuing guidance on their interpretation and application of the new statutes

• Risk of double counting sales