state of the u.s. office market -...

TRANSCRIPT

page 1

State of the U.S. Office Market 2016 Q4 Review and Forecast

page 2

• Overview

• Economy

• Fundamentals

• Capital Markets

• Danger Zone

• Most And Least

Agenda

page 3

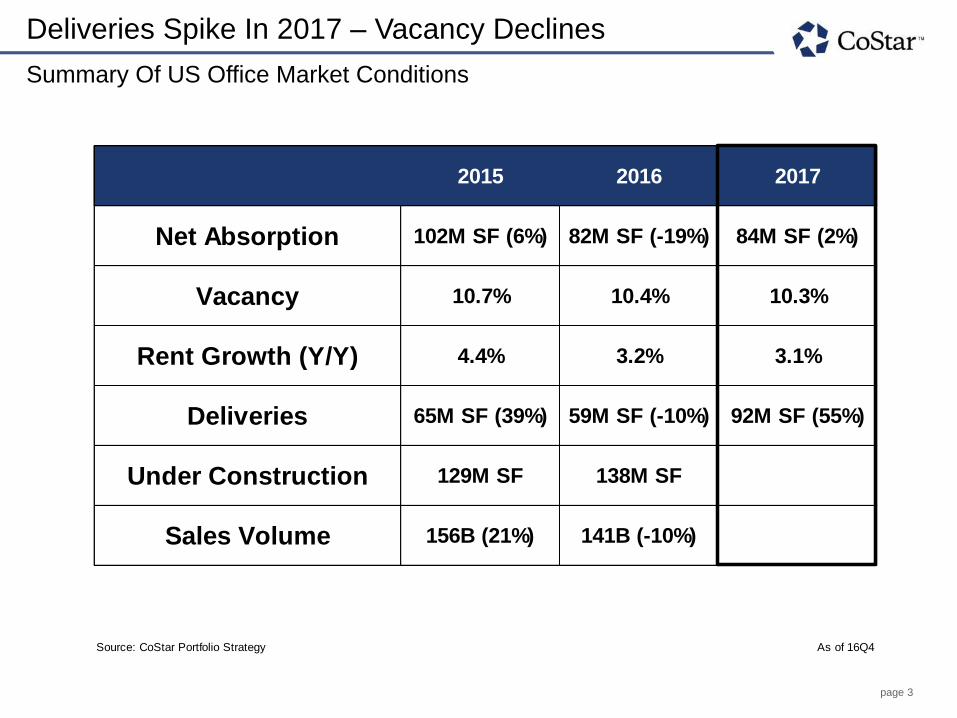

Deliveries Spike In 2017 – Vacancy Declines

Summary Of US Office Market Conditions

Source: CoStar Portfolio Strategy As of 16Q4

Sales Volume 156B (21%) 141B (-10%)

Deliveries 65M SF (39%) 59M SF (-10%) 92M SF (55%)

Under Construction 129M SF 138M SF

Vacancy 10.7% 10.4% 10.3%

Rent Growth (Y/Y) 4.4% 3.2% 3.1%

2015 2016 2017

Net Absorption 102M SF (6%) 82M SF (-19%) 84M SF (2%)

page 4

Economy

page 5

Demographic Headwinds Will Limit Trump-Era Growth

GDP Growth By Presidency

Sources: BEA; Moody's Analytics; CoStar Portfolio Strategy As of 16Q4

2.8%

5.3%5.1%

2.7%

2.9%

3.2%

3.6%

2.2%

3.8%

1.8%1.8%

2.2%

0%

1%

2%

3%

4%

5%

6%

52 56 60 64 68 72 76 80 84 88 92 96 00 04 08 12 16 20 24

Avg. GDP Growth

EisenhowerTrump

Ford

Carter

Reagan

Bush

Clinton Obama

BushNixon

Johnson

Kennedy

Republican

Democrat

page 6

Demographic Headwinds Will Limit Trump-Era Growth

GDP Growth By Presidency & Working-Age Population Growth*

Sources: BEA; Moody's Analytics; CoStar Portfolio Strategy As of 16Q4

*Ages 20-64

2.8%

5.3%5.1%

2.7%

2.9%

3.2%

3.6%

2.2%

3.8%

1.8%1.8%

2.2%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0%

1%

2%

3%

4%

5%

6%

52 56 60 64 68 72 76 80 84 88 92 96 00 04 08 12 16 20 24

Avg. GDP Growth

EisenhowerTrump

Ford

Carter

Reagan

Bush

Clinton Obama

BushNixon

Johnson

Kennedy

Republican

Democrat

Y/Y Change Working Age Population

Y/Y Change Working Age Population

Avg. Ann. GDP Growth Of President's Tenure

page 7

GDP Trending Up

Contributions To GDP Growth

Updated Date:Frequency:

Sources: Moody's Analytics; BEA; CoStar Portfolio Strategy As of 16Q3

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

07 08 09 10 11 12 13 14 15 16

Goods (Manufacturing) Services Structures (Construction) GDP

Contribution to GDP Growth

page 8

Sales & Profits Still Positive

Corporate Profit, Sales, Employment Trends

Sources: Moody's Analytics; BEA; Barron's; CoStar Portfolio Strategy As of 16Q4

Q4 S&P 500 Profit Growth Estimate, 4.4%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

50%

60%

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Financial Profit Non Financial Profit Foreign Profit Profit Margin as % of GDP

Corporate Profit Growth (Y/Y) Profits As % Of GDP

page 9

Office-Using Employment Remains Strong

Total And Office-Using Employment Growth (Y/Y)

Sources: Moody's Analytics; BLS; CoStar Portfolio Strategy As of 16Q4

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Total Employment Office-Using Employment Net Office Absorption

Employment Growth (Y/Y)

Y/Y 15Q4 16Q4 17Q4Total Jobs 2.0% 1.6% 1.4%Office Jobs 2.7% 2.4% 1.9%Net Absorption 1.4% 1.1% 1.1%

page 10

Job Growth Slowed In 2016 In Most Markets

Employment Growth By Metro

123456789

101112131415161718192021

Source: Moody's Analytics; CoStar Group As of 16Q4

0%

1%

2%

3%

4%

5%

6%S

ea

ttle

De

nver

San

Jose

Da

llas-

FW

Las V

egas

East

Bay

San

Fra

ncis

co

Na

shvill

e

Austin

Port

land O

R

Ora

ng

e C

ounty

Atlan

ta

Washin

gto

n…

San

Die

go

Bosto

n

Phila

delp

hia

Los A

ngele

s

Ne

w Y

ork

Ch

icago

Pitts

burg

h

Ho

usto

n

Avg Annual Employment Growth

East Midwest South West 2015

(2.1%)(2.5%)

page 11

Generally The Job Picture Is Moderating

Office-Using Employment Y/Y Change By Metro

As of 16Q4 Source: CoStar Portfolio Strategy

page 12

Rig Count Bottomed--Houston Economy May Turn In 2017

Global Oil Production And Rig Count

U.S.

Rest of World

Rig Count

Sources: IEA, EIA, Baker Hughes, CoStar Portfolio Strategy As of 16Q4

0

500

1000

1500

2000

2500

3000

3500

4000

0

20

40

60

80

100

120

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

U.S. Rest of World Rig Count

Oil Production(Million Barrels Per Day)

International Oil Rig Counts

62% Decline in Active Rigs

14% Increase

page 13

Fundamentals

page 14

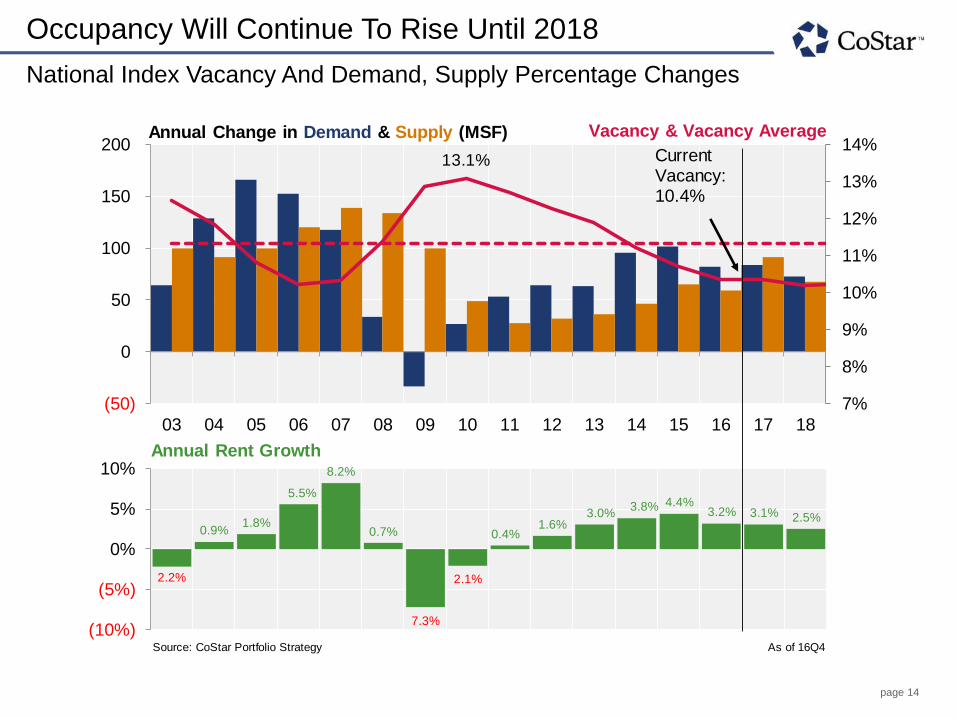

Occupancy Will Continue To Rise Until 2018

National Index Vacancy And Demand, Supply Percentage Changes

Current Vacancy:End of ForecastForecast MinHistorical Avg.Recession Max

Source: CoStar Portfolio Strategy As of 16Q4

7%

8%

9%

10%

11%

12%

13%

14%

(50)

0

50

100

150

200

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Current Vacancy: 10.4%

2.2%

0.9%1.8%

5.5%

8.2%

0.7%

7.3%

2.1%

0.4%1.6%

3.0%3.8% 4.4%

3.2% 3.1% 2.5%

(10%)

(5%)

0%

5%

10%

Annual Change in Demand & Supply (MSF) Vacancy & Vacancy Average

Annual Rent Growth

13.1%

page 15

Top Quality Assets Capturing Most Demand

Net Office Absorption By Building Star

12/31/19993/31/20006/30/20009/30/2000

12/31/20003/31/20016/30/20019/30/2001

12/31/20013/31/20026/30/20029/30/2002

12/31/20023/31/20036/30/20039/30/2003

12/31/20033/31/20046/30/20049/30/2004

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/2007

Source: CoStar Portfolio Strategy As of 16Q4

1.8%

0.8%

1.0%

(2.0%)

(1.0%)

0.0%

1.0%

2.0%

3.0%

4.0%

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

4 & 5 Star 3 Star 1 & 2 Star

Annualized Demand Growth (Two-Quarter Moving Average)

Huge Decline In Demand For Lower Quality Assets

page 16

Huge Drop-Off For New York, Houston, And Chicago

2016 Net Absorption & Y/Y Change

Source: CoStar Portfolio Strategy As of 16Q4

Cumulative Net Absorption (Millions SF)

-5

-4

-3

-2

-1

0

1

2

3

4

5

Washin

gto

n, D

.C.

Los A

ngele

s

San

Die

go

Pho

enix

Mia

mi

San

Fra

ncis

co

Sea

ttle

Bosto

n

De

nver

Ne

w Y

ork

Da

llas -

FW

Ho

usto

n

Austin

Atlan

ta

Ch

icago

San

Jose

Y/Y Change In Net Absorption 2016 Net Absorption

Tech Markets Energy Markets Housing Bust Markets Other

page 17

Suburban Office Market Demand Shows Strength

Year Over Year Net Absorption

3

CBD

19

18

17

14

13

11

10

9

7

6

5

3

2

1

Source: CoStar Portfolio Strategy As of 16Q4

CBDs include metros with greater than 100,000 SF or less than 100,000 SF of net absorption

Suburban include metros with greater than 400,000 SF

-0.8 MSF

-0.3 MSF

-0.2 MSF

0.6 MSF

0.4 MSF

0.6 MSF

1 MSF

1.3 MSF

0.2 MSF

0.1 MSF

0.3 MSF

0.3 MSF

2.4 MSF

1 MSF

(3%) (1%) 2% 5% 7% 10%

Dallas - FW

Denver

Houston

Washington, D.C.

Philadelphia

Atlanta

Boston

San Francisco

Ft. Lauderdale

Las Vegas

San Jose

San Diego

Seattle

Nashville

-1.2 MSF

0.4 MSF

1 MSF

1.4 MSF

1 MSF

1.3 MSF

4.9 MSF

1.3 MSF

1.2 MSF

2 MSF

1.4 MSF

1 MSF

1.8 MSF

3.8 MSF

(3%) (1%) 2% 5% 7% 10%

Chicago

New York

East Bay

Denver

Austin

San Diego

Dallas - FW

Portland

San Francisco

San Jose

Nashville

Orange County

Charlotte

Phoenix

CBD Suburban

West South East Midwest

page 18

Construction Trending Up, Except in Texas

Under Construction RBA By Region

3/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

12/31/20103/31/20116/30/20119/30/2011

12/31/20113/31/20126/30/20129/30/2012

12/31/20123/31/20136/30/2013

Source: CoStar Portfolio Strategy As of 16Q4

Texas Includes Austin, Dallas, Houston, and San Antonio; Southern California Includes Los Angeles, Orange

County, and San Diego; California Bay Area Includes East Bay, San Francisco, and San Jose

0

20

40

60

80

100

120

140

160

180

20007Q

307Q

408Q

108Q

208Q

308Q

409Q

109Q

209Q

309Q

410Q

110Q

210Q

310Q

411Q

111Q

211Q

311Q

412Q

112Q

212Q

312Q

413Q

113Q

213Q

313Q

414Q

114Q

214Q

314Q

415Q

115Q

215Q

315Q

416Q

116Q

216Q

316Q

4

Texas California Bay Area All Other Markets Southern California New York

RBA Under Construction (Millions SF)

page 19

New Construction Activity

Select Office Starts - 16Q4

2050 M St NW CBD

Metro: Washington, D.C.

SF: 364,000

Submarket Vacancy: 8.2%

Leased: 40%

Owner: Tishman Speyer

Delivery Date: December 2019

Source: CoStar Portfolio Strategy As of 16Q4

771 Spring St Midtown/Pershing Point

Metro: Atlanta

SF: 760,000

Submarket Vacancy: 10.4%

Leased: 60%

Owner: Portman Holdings, LLC

Delivery Date: January 2019

5050 S Syracuse St Denver Tech Center

Metro: Denver

SF: 185,000

Submarket Vacancy: 16.8%

Leased: 0%

Owner: Corum Real Estate

Group Inc.

Delivery Date: June 2018

6002 Stoneridge Mall Rd Pleasanton-North

Metro: East Bay

SF: 409,998

Submarket Vacancy:

4.8%

Leased: 100%

Owner: BRIDGE Housing

Corporation

Delivery Date: June 2018

page 20

Most Metros Have Above Average Construction

Office Construction Vs. Historical Norms

3

Rank123456789

10111213141516171819202122

Source: CoStar Portfolio Strategy As of 16Q4

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%T

am

pa

Min

ne

ap

olis

Orla

nd

o

Ea

st

Ba

y

Ph

oe

nix

Ho

usto

n

Ch

arl

ott

e

Lo

s A

ng

ele

s

Ch

ica

go

Bo

sto

n

Atla

nta

Mia

mi

Wa

sh

ing

ton

D.C

.

Ne

w Y

ork

Na

sh

ville

Ra

leig

h

Au

stin

Da

lla

s F

W

De

nve

r

Sa

n F

ran

cis

co

Se

att

le

Sa

n J

ose

Current Construction Average Annual Office Supply Growth

SF As % Of Market RBA

Limited Development/ Supply Cooling Down

Supply Ramping Up

19

10

9

11 5

10

6

page 21

Newest Generation Tight In San Francisco, Not So In DC

Vacancy Rates For Buildings 0-10 Years Old

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Source: CoStar Portfolio Strategy As of 16Q4

0%

5%

10%

15%

20%

25%S

an

Fra

ncis

co

Bosto

n

Min

nea

polis

Na

shvill

e

East

Bay

Tam

pa

Orlando

Fort

Laud

erd

ale

Port

land,

OR

Ch

arlotte

Sea

ttle

Ora

ng

e C

ounty

San

Die

go

Palm

Be

ach C

ounty

De

nver

Phila

delp

hia

Da

llas -

Fort

Wort

h

Austin

Mia

mi

Ne

w Y

ork

Los A

ngele

s

Ch

icago

Atlan

ta

San

Jose

Pho

enix

Washin

gto

n, D

.C.

2006 Or Newer Vacancy

2006-Newer Vacancy

page 22

Newest Generation Tight In San Francisco, Not So In DC

Vacancy Rates For Buildings 0-10 Years Old

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Source: CoStar Portfolio Strategy As of 16Q4

0%

5%

10%

15%

20%

25%S

an

Fra

ncis

co

Bosto

n

Min

nea

polis

Na

shvill

e

East

Bay

Tam

pa

Orlando

Fort

Laud

erd

ale

Port

land,

OR

Ch

arlotte

Sea

ttle

Ora

ng

e C

ounty

San

Die

go

Palm

Be

ach C

ounty

De

nver

Phila

delp

hia

Da

llas -

Fort

Wort

h

Austin

Mia

mi

Ne

w Y

ork

Los A

ngele

s

Ch

icago

Atlan

ta

San

Jose

Pho

enix

Washin

gto

n, D

.C.

2006 Or Newer Vacancy Including Available Under Construction

2006-Newer Vacancy

page 23

Occupancy Gains Are Broadly Based

Market And Submarket Relative Vacancies

60%

65%

12/31/2003

3/31/2004

6/30/2004

9/30/2004

12/31/2004

3/31/2005

6/30/2005

9/30/2005

12/31/2005

3/31/2006

6/30/2006

9/30/2006

12/31/2006

3/31/2007

6/30/2007

9/30/2007

Source: CoStar Portfolio Strategy As of 16Q4

0%

10%

20%

30%

40%

50%

60%

70%

80%

08 09 10 11 12 13 14 15 16

Submarkets With Declining Vacancies

Markets With Vacancies Lower Than 2006-07 Peak

Percentage of Markets/Submarkets

60%

65%

page 24

Markets Like New Buildings

Vacancy By Building Age

Current Quarter

12/31/2016

0-5

6-10

11-20

20+

12/31/2009

3/31/2010

6/30/2010

9/30/2010

12/31/2010

3/31/2011

6/30/2011

9/30/2011

12/31/2011

3/31/2012

6/30/2012

9/30/2012

12/31/2012

3/31/2013

6/30/2013

9/30/2013

Source: CoStar Portfolio Strategy As of 16Q4

5%

10%

15%

20%

25%

08 09 10 11 12 13 14 15 16

0-5 Years 6-10 Years 11-20 Years 20+

Vacancy

14.8%

11.1%

7.4%

8.6%

New Supply Matching

New Demand Since 2013

Stabilized New Buildings Doing Well

page 25

Sublease Availability May Have Peaked In Houston

Sublet Available SF As A Percent Of Inventory

3/31/20046/30/20049/30/2004

12/31/20043/31/20056/30/20059/30/2005

12/31/20053/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/20099/30/2009

12/31/20093/31/20106/30/20109/30/2010

Source: CoStar Portfolio Strategy As of 16Q4

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

05 06 07 08 09 10 11 12 13 14 15 16

Seattle Houston San Francisco New York National San Jose

Sublet Available As A % Of Inventory

Houston

San Francisco

Seattle

New York

National

San Jose

page 26

Vacancies Continue To Increase In Houston

Vacancy Rates For Metros, Current Vs. Last Year

Rank

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Source: CoStar Portfolio Strategy As of 16Q4

4%

6%

8%

10%

12%

14%

16%

18%

Ho

usto

n

Da

llas-

FW

Ch

icago

De

troit

Atlan

ta

De

nver

Los A

ngele

s

San

Die

go

Phila

delp

hia

Mia

mi

Ne

w Y

ork

Ora

ng

e C

ounty

Washin

gto

n D

.C.

Bosto

n

Min

nea

polis

San

Jose

Port

land O

R

Sea

ttle

San

Fra

ncis

co

West South East Midwest 15Q4 Vacancy

16Q4 Vacancy Rate

page 27

Many Office Markets Have Sub 9% Vacancy!

Office Vacancy Rates By Metro

As of 16Q4 Source: CoStar Portfolio Strategy

page 28

Rent Growth In Most Suburbs Has Picked Up

Rent Growth For 2016

3

SCROLL RIGHT FOR UPDATE INSTRUCTIONS

CBD

11

10

9

8

7

6

5

4

3

2

1

Source: CoStar Portfolio Strategy As of 16Q4

1.1%

1.3%

1.9%

3.4%

3.7%

5.8%

6.6%

6.6%

6.8%

8.2%

21.8%

0% 5% 10% 15% 20%

Denver

Dallas - FW

New York

San Francisco

Wash D.C.

Seattle

Boston

Los Angeles

Miami

Atlanta

East Bay

0.2%

1.3%

1.9%

2.4%

3.3%

3.6%

3.8%

3.8%

4.2%

6.3%

11.8%

0% 5% 10% 15% 20%

New York

Wash D.C.

Seattle

Los Angeles

Miami

Denver

Dallas - FW

Boston

Atlanta

East Bay

San Francisco

CBD Prime Suburban

West South East Midwest

page 29

Rent Growth In Most Suburbs Has Picked Up

Rent Growth For 2016 & 2015

3

SCROLL RIGHT FOR UPDATE INSTRUCTIONS

CBD

11

10

9

8

7

6

5

4

3

2

1

Source: CoStar Portfolio Strategy As of 16Q4

1.1%

1.3%

1.9%

3.4%

3.7%

5.8%

6.6%

6.6%

6.8%

8.2%

21.8%

0% 5% 10% 15% 20%

Denver

Dallas - FW

New York

San Francisco

Wash D.C.

Seattle

Boston

Los Angeles

Miami

Atlanta

East Bay

0.2%

1.3%

1.9%

2.4%

3.3%

3.6%

3.8%

3.8%

4.2%

6.3%

11.8%

0% 5% 10% 15% 20%

New York

Wash D.C.

Seattle

Los Angeles

Miami

Denver

Dallas - FW

Boston

Atlanta

East Bay

San Francisco

2015 Rent Growth

CBD Prime Suburban

West South East Midwest

-1.1%

page 30

CBD/Suburban Rent Growth Gap Closing

National Index District Rent Growth Y/Y

Select Market:

ZPPR54

National Index District Rent Growth Y/Y

Select Variable:

Rent

Spread

4%

3%

1%

-1%

-3%

-5%

-5%

-5%

-3%

-2%

-1%

0%

1%

2%

2%

3%

3%

3%

3%

Sources: CoStar Portfolio Strategy As of 16Q4

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

5%

6%

7%

11 12 13 14 15 16

Spread CBD/Secondary Business District/Urban Prime Suburban/Suburban

Rent Growth Y/Y

page 31

Construction Concentrated In CBDs

CBD Construction As A Percentage Of Total Metro Construction

123456789

10111213

Source: CoStar Portfolio Strategy As of 16Q4

37% 14%

27%(3%)

27% 25%

23% 18%

10% 6% (7%)

(3%)

(7%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ch

icago

Ne

w Y

ork

Sea

ttle

San

Fra

ncis

co

De

nver

Washin

gto

n D

.C.

Los A

ngele

s

Phila

delp

hia

Ho

usto

n

Mia

mi

Bosto

n

Atlan

ta

Da

llas F

W

CBD Share of Metro Construction CBD Share Of Metro Office Stock

Percent of Metro Total Construction and Stock

Difference Between Stock& Construction Share

page 32

Rent Growth Trends By Metro

CBD Rent Growth Minus Suburban Rent Growth

Sources: CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

11 12 13 14 15 16

National Index Washington, DC

Rent Growth Spread (4Q-Avg)

National

Washington, DC

page 33

Rent Growth Trends By Metro

CBD Rent Growth Minus Suburban Rent Growth

Sources: CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

11 12 13 14 15 16

National Index New York San Francisco

Rent Growth Spread (4Q-Avg)

New York

National

San Francisco

page 34

Rent Growth Trends By Metro

CBD Rent Growth Minus Suburban Rent Growth

Sources: CoStar Portfolio Strategy As of 16Q4

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

11 12 13 14 15 16

National Index Boston Los Angeles

Rent Growth Spread (4Q-Avg)

Boston

Los Angeles

National

page 35

Capital Markets

page 36

Gap In CBD Vs. Suburban Cap Rates Narrows

CBD Vs. Suburban Office Cap Rates

Cap Rate

06Q12006 2q06Q32006 4q07Q107Q22007 3q07Q408Q108Q22008 3q08Q409Q109Q22009 3q09Q410Q110Q210Q310Q411Q111Q211Q311Q412Q112Q212Q312Q413Q1

Source: CoStar Portfolio Strategy As Of 16Q4

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

06Q1 07Q1 08Q1 09Q1 10Q1 11Q1 12Q1 13Q1 14Q1 15Q1 16Q1

CBD Suburban

1.3%1.4%

1.5%

1.6%1.9%

page 37

Suburbs See More Value Growth Than CBDs

Price Per Square Foot Index

3/31/20066/30/20069/30/2006

12/31/20063/31/20076/30/20079/30/2007

12/31/20073/31/20086/30/20089/30/2008

12/31/20083/31/20096/30/2009

09Q410Q110Q210Q310Q411Q111Q211Q311Q412Q112Q212Q312Q413Q113Q2

Source: CoStar Portfolio Strategy As of 16Q4

118

124

100

105

110

115

120

125

13Q4 14Q2 14Q4 15Q2 15Q4 16Q2 16Q4

CBD Suburban

Price/SF, Rolling 4-Quarter Average, 2013Q4=100

5% More Value Growth In Subrubs Than CBD

Since 13Q4

page 38

Sales Volume Slowing & Likely Slow More In 2017

Annual Sales Volume By Property Type

Date200520062007200820092010201120122013201420152016

Source: CoStar Portfolio Strategy As of 16Q4

0

50

100

150

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Office Industrial Multi-Family Retail

Annual Sales Volume $B

YoY Change:

Multi-Family: -5%

Office: -10%

Retail: -14%

Industrial: -23%

page 39

Share Of Foreign Investment In Office Steadily Increasing

% Of Foreign Investment In Office Over Time

04

05

06

07

08

09

10

11

12

13

14

15

16

Source: CoStar Portfolio Strategy As of 16Q4

$0

$5

$10

$15

$20

$25

4%

6%

8%

10%

12%

14%

16%

05 06 07 08 09 10 11 12 13 14 15 16

Foreign % Of Total Volume (2-Year Avg.) Foreign Investment ($B)

page 40

Sales Volume Declining In A Majority Of Markets

Annual Change In Office Sales Volume For Major Metros

Los AngelesMiamiPhiladelphiaDallas - FWSan FranciscoNew YorkSeattleAtlantaBostonWashington D.C.Orange CountySan DiegoMinneapolis

Source: CoStar Portfolio Strategy As of 16Q4

(60%)

(40%)

(20%)

0%

20%

40%

60%

$0

$5

$10

$15

$20

$25

$30

$35

Los A

ngele

s

Mia

mi

Phila

delp

hia

Da

llas -

FW

San

Fra

ncis

co

Ne

w Y

ork

Sea

ttle

Atlan

ta

Bosto

n

Washin

gto

n D

.C.

Ora

ng

e C

ounty

San

Die

go

Min

nea

polis

Pho

enix

De

nver

Austin

Ch

icago

Ho

usto

n

San

Jose

2015 2016 Percent Change Y/Y

Sales Volume ($ Billions) Percent Change Y/Y

page 41

Private Equity Investors Most Active Recently

U.S. Net Office Acquisitions By Investor Type - 16Q4

31425

12345

Source: CoStar Portfolio Strategy As of 16Q4

2.3

0.9 0.7

(0.3)

(1.2)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

2.5

Private Equity Private Institutional User REIT/Public

Net Acquisitions ($ Billions)

page 42

Big Apple Home To The Big Trades

Top Office Deals of 2016

Property Name Market Bldg SF Sale Price (M) Price Per SF Cap Rate Buyer Company

Equitable Building New York City 1,706,007 1,950$ 1,143$ 4.1% CalPERS

UBS New York City 1,800,000 1,650$ 917$ 4.7% RXR Realty

Sony Building New York City 852,830 1,400$ 1,642$ Olayan America

Shearson Lehman Plaza New York City 1,869,756 1,255$ 671$ Citigroup Inc.

Salesforce Tower New York City 1,484,325 1,153$ 1,995$ 4.1% Hong Kong Monetary Authority

Metropolitan Life Insurance Plaza New York City 2,285,043 1,040$ 1,138$ 4.0% PGIM Real Estate

Rockefeller Center New York City 2,652,712 1,030$ 863$ Invesco Ltd.

10 Hudson Yards New York City 1,800,000 946$ 1,194$ 3.7% Allianz Real Estate America

Rockefeller Center New York City 2,014,062 858$ 869$ Invesco Ltd.

One New York Plaza New York City 2,545,000 678$ 543$ 4.3% China Investment Corporation (CIC)

1250 Broadway New York City 770,000 565$ 734$ 2.9% 1250 Broadway Associates LLC

Southeast Financial Center South Florida 1,194,832 517$ 432$ 5.7% Ponte Gadea USA, Inc.

390 Greenwich St New York City 764,918 513$ 671$ Citigroup Inc.

One Front St (Multi-Property Sale) San Francisco 651,000 490$ 753$ One Front Street EAT, LLC

Source: CoStar Portfolio Strategy As of 16Q4

page 43

Selected Top Office Deals – 2016Q4

CitiGroup Center

Los Angeles, CA

Hines sold the 891,056 SF Office

property to Coretrust Capital

Partners, LLC for $336 Million

($377.08/SF).

4.6% Cap Rate

Southeast Financial Center

Miami, FL

JP Morgan Chase & Co. sold the

1.195 Million SF Office property to

Ponte Gadea USA, Inc. for $516.6

Million ($432.36/SF).

5.7% Cap Rate

Foundry Square III

San Francisco, CA

A JV of Tishman Speyer and JP

Morgan Asset Management sold

the 291,032 SF Office property

to American Realty Advisors for

$332,030,500 ($1140.87/SF).

4.8% Cap Rate

Hines REIT West Coast Portfolio

Hines REIT, Inc. sold the 3.239

Million SF portfolio to The Blackstone

Group, LP for $1.162 Billion

($358.73/SF).

5% Cap Rate

page 44

Danger Zone

page 45

Interest Rates Are Moving Up

Futures Market For The 10 Year Treasury At Different Points

Sources: Bloomberg; CoStar Portfolio Strategy As of 1/19/17

1.5%

2.0%

2.5%

3.0%

3.5%

2016 2017 2018 2020 2026

10 Year Bond Yield

Post-Election Pre- Election Jan-17

+18 BP

+52 BP

page 46

Could Spike In Interest Rates Cause Values To Fall?

Sensitivity Of Office Prices To A Rise In Cap Rates

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Q

Sources: Bloomberg; CoStar Portfolio Strategy As Of January 19, 2017

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

2.6%

5.2%

5.4%

5.6%

5.8%

6.0%

6.2%

6.4%

14Q1 14Q3 15Q1 15Q3 16Q1 16Q3 Jan-17

Office Cap Rate 10 Year Treasury

Office Cap Rate 10 Year Treasury

0%-2%

-3%

-5%

-7%

-8%

-10%

-11%

-12%

-14%

-15%(16%)

(14%)

(12%)

(10%)

(8%)

(6%)

(4%)

(2%)

0%

0 10 20 30 40 50 60 70 80 90 100

% Change In Value

Cap Rate Increase In Basis Points

Likely Cap

Rate Change Recession Fear

Future ?

page 47

Most And Least

page 48

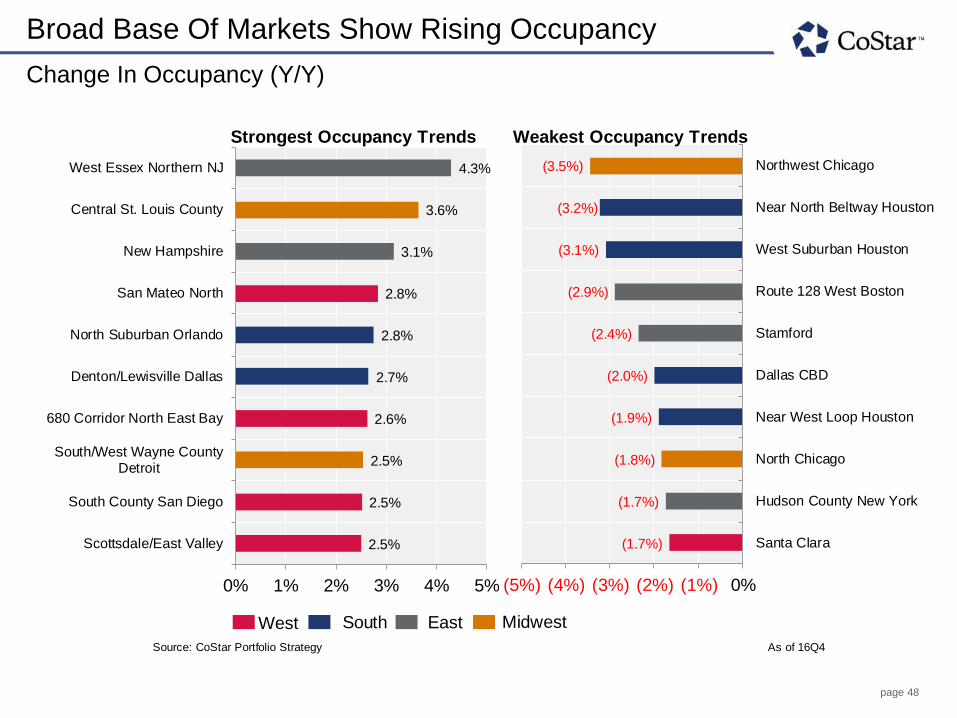

Broad Base Of Markets Show Rising Occupancy

Change In Occupancy (Y/Y)

10987654321

Metro CodeAKROALBAALBUALLEANCHANNAAPPLASHEATLAATLCAUGUAUSTBAKE

Source: CoStar Portfolio Strategy As of 16Q4

2.5%

2.5%

2.5%

2.6%

2.7%

2.8%

2.8%

3.1%

3.6%

4.3%

0% 1% 2% 3% 4% 5%

Scottsdale/East Valley

South County San Diego

South/West Wayne CountyDetroit

680 Corridor North East Bay

Denton/Lewisville Dallas

North Suburban Orlando

San Mateo North

New Hampshire

Central St. Louis County

West Essex Northern NJ

Strongest Occupancy Trends

(1.7%)

(1.7%)

(1.8%)

(1.9%)

(2.0%)

(2.4%)

(2.9%)

(3.1%)

(3.2%)

(3.5%)

(5%) (4%) (3%) (2%) (1%) 0%

Santa Clara

Hudson County New York

North Chicago

Near West Loop Houston

Dallas CBD

Stamford

Route 128 West Boston

West Suburban Houston

Near North Beltway Houston

Northwest Chicago

Weakest Occupancy Trends

West South East Midwest

page 49

Demand Growth Dominates

Net Absorption (Y/Y)

Get Data from Rob

AKROALBAALBUALLEANCHANNAAPPLASHEATLAATLCAUGUAUSTBAKEBALTBATOBATT

Source: CoStar Portfolio Strategy As of 16Q4

0.5 MSF

0.8 MSF

1.2 MSF

1.0 MSF

1.5 MSF

0.9 MSF

0.6 MSF

2.5 MSF

1.3 MSF

1.6 MSF

0% 2% 4% 6% 8%

Denton/Lewisville Dallas

Baltimore City

Nashville CBD

Outlying Charlotte

South/East Suburban KansasCity

West Essex Northern NJ

Bronx

Scottsdale/East Valley

East Valley Salt Lake City

Sunnyvale/Cupertino

Strongest Net Absorption

(0.4) MSF

(0.3) MSF

(0.2) MSF

(0.5) MSF

(0.2) MSF

(0.5) MSF

(0.6) MSF

(0.6) MSF

(1.5) MSF

(0.5) MSF

(4%) (3%) (2%) (1%) 0%

Metro West Boston

South End Seattle

Ft Worth CBD

NoVA Inner Beltway D.C.

North & West Las Vegas

Hudson County

Dallas CBD

Near North Beltway Houston

Northwest Chicago

Stamford

Weakest Net Absorption

West South East Midwest

page 50

Rent Growth - Winners And Losers

Rent Growth (Y/Y)

10987654321

AKROALBAALBUALLEANCHANNAAPPLASHEATLAATLCAUGUAUSTBAKEBALTBATOBATT

Source: CoStar Portfolio Strategy As of 16Q4

7.92%

7.97%

8.03%

9.05%

9.40%

9.59%

10.03%

11.63%

13.43%

23.85%

0% 5% 10% 15% 20% 25%

Santa Clara

San Mateo South

Portland CBD

Miami Downtown

Mid-Wilshire Los Angeles

South/West SuburbanNashville

San Jose CBD

I-80/Hwy 4 Corridors EastBay

Memphis CBD

Oakland

Strongest Rent Trends

(0.9%)

(1.1%)

(1.1%)

(1.2%)

(1.8%)

(1.8%)

(1.9%)

(2.3%)

(3.8%)

(4.8%)

(5%) (4%) (3%) (2%) (1%) 0%

South/West Suburban Cleveland

Richmond CBD

West Suburban Houston

Upper Fairfield County Stamford

Stamford

West Valley Salt Lake City

Milwaukee County

South & East Las Vegas

Ft Worth CBD

North & West Las Vegas

Weakest Rent Trends

West South East Midwest

page 51

© Copyright 2017 CoStar Group, Inc. All Rights Reserved. Although CoStar makes efforts to ensure the accuracy and reliability of the information contained herein, the following information includes projections that are

based on various assumptions by CoStar concerning future events and circumstances, as well as historical and current data maintained in CoStar’s database. Actual results may vary from the projections presented.

The information in this presentation is provided ‘as is’ and CoStar expressly disclaims any guarantees, representations or warranties of any kind, including those of merchantability and fitness for a particular purpose.

Features shown in this presentation may require additional subscriptions.

Thank You!