state of the automotive finance market - experian...market share of total financing (new/used units...

TRANSCRIPT

1©2016 Experian Information Solutions, Inc. All rights reserved.

Experian Public.

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company

names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian.

Experian Public.

www.experian.com/automotive

State of the Automotive Finance Market A look at loans and leases in Q2 2016

Presented by: Melinda Zabritski | Sr. Director, Financial Solutions

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 2

Market Overview

Outstanding balances

Total risk distributions

Delinquency

Originations

New and Used financing

Lender and transaction types

Loan & lease characteristics

Session overview

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 3© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 3

A look balances and delinquencies on all open automotive loans & leases

Overall Automotive Finance Market

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 4

Loan balances break record highs while Credit Unions experience largest YOY growth (loans regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 5

11.86%

8.03% 8.10%

7.05%

8.42%

Deepsubprime

Subprime Nonprime Prime Super prime

Year-over-year volume change

Unit distribution remains stable with growth occurring across all risk segments (loans and leases regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

3.27% 3.28% 3.40%

15.43% 15.44% 15.44%

17.81% 17.77% 17.78%

28.00% 27.62% 27.37%

35.49% 35.89% 36.02%

2014 Q2 2015 Q2 2016 Q2

Risk distribution of open loans & leases

Deep Subprime Subprime Nonprime Prime Super Prime

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 6

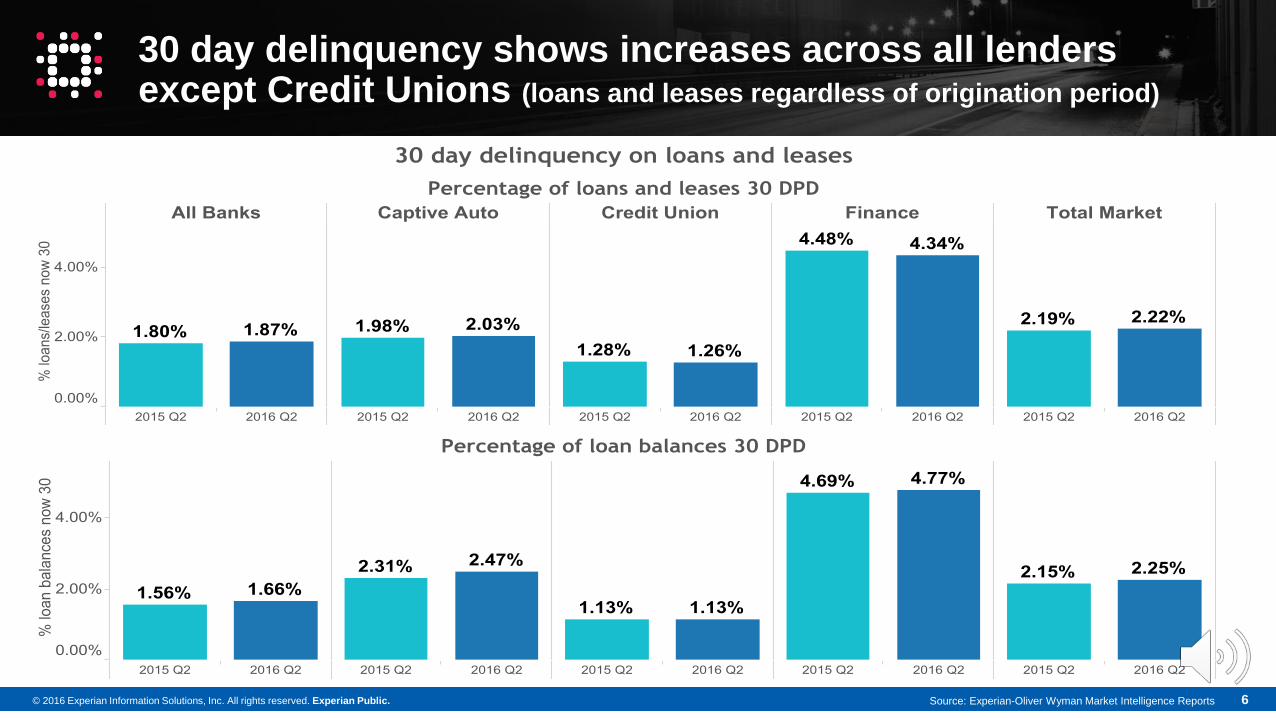

30 day delinquency shows increases across all lenders except Credit Unions (loans and leases regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 7

30-day delinquency balances by state(loans and leases regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

HI = 1.88%

1.44%

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 8

60 day delinquency growth across all lender types(loans and leases regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 9

60-day delinquency balances by state(loans and leases regardless of origination period)

Source: Experian-Oliver Wyman Market Intelligence Reports

HI = 0.48%

0.32%

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 10© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 10

Trends in automotive loans and leases

Originations in Q2 2016

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 11

Automotive financing: snapshot of how and what consumers are financing

3.26% 3.71%

Q2 2015 Q2 2016

Used % of lease market

45.70% 44.39%

54.30% 55.61%

Q2 2015 Q2 2016

Finance Market: new v used units

New Used

85.8% 86.5%

55.5% 55.9%

Q2 2015 Q2 2016

Percentage of vehicles with financing

New Used

26.92%31.44%

Q2 2015 Q2 2016

% of all new vehicles that are leased

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 12

Credit Unions pick up market share across the board while Finance companies show decreases (loan and lease units combined)

34

.7%

7.4

%

27

.3%

17

.2%

13

.4%

34

.8%

7.1

%

27

.7%

18

.7%

11

.6%

Bank BHPH Captive CreditUnion

FinanceCo

Market Share of Total Financing(new/used units & loan/lease)

Q2 2015 Q2 2016

34

.0%

0.2

%

50

.0%

10

.3%

5.5

%

31

.7%

0.2

%

52

.2%

11.4

%

4.6

%

Bank BHPH Captive Credit Union Finance Co

Market Share of New Financing

Q2 2015 Q2 2016

35

.3%

13

.6%

7.7

% 23

.3%

20

.2%

37

.3%

13

.0%

7.4

%

24

.9%

17

.5%

Bank BHPH Captive Credit Union Finance Co

Market Share of Used Financing

Q2 2015 Q2 2016

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 13

39.34%

0.70%

10.14%

21.75%

8.61%

19.46%

12.19%

19.02%

0.35%

12.45%15.94%

40.05%

BANK BUY HERE/PAYHERE

CAPTIVE CREDIT UNION FINANCE NO LENDERLISTED

Financing by dealer type

Franchise Independent

Independent used Dealers experience higher cash penetration caused by more subprime and older MY vehicles

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 14

724

720

712711

710

722

717

711709

708

732

724

717716 716

Q2 2012 Q2 2013 Q2 2014 Q2 2015 Q2 2016

Average new credit scores

All New New Loan New Lease

Credit scores stabilize for new while used scores increase

647 645 644 645 648

674 673 672 671 674

602 601 600 603608

Q2 2012 Q2 2013 Q2 2014 Q2 2015 Q2 2016

Average used credit scores

All Used Franchise Used

Independent Used

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 15

Score range refresh

Note: ranges above are those used by Experian Automotive for automotive finance market analysis and trending purposes. Other industries and lenders may use other ranges based on unique scores, portfolio and industry trends.

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 16

Total finance market (loan & lease) becomes increasingly more prime across all, new and used financing

9.97% 9.76%17.86% 17.86%

44.69% 44.97%

26.79% 26.72%

Q2 2015 Q2 2016

New risk distribution

6.00% 5.83%28.19% 26.95%

22.03% 22.22%

33.24% 34.20%

10.56% 10.80%

Q2 2015 Q2 2016

Used risk distribution

3.54% 3.54%

19.76% 19.28%

20.10% 20.28%

38.54% 39.01%

18.07% 17.90%

Q2 2015 Q2 2016

Total (new & used units) risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 17

7.24% 7.41%

17.50% 17.17%

48.48% 48.10%

26.36% 26.82%

Q2 2015 Q2 2016

New lease risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime21.9%

29.8%

31.9%

26.5%

33.6%

36.5%

Deep &Sub

Nonprime

Prime +

%of new borrowers choosing leasing

Q2 2016

Q2 2015

Leasing remains very prime as more consumers across all risk tiers choose to lease (loans not included)

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 18

Loan market appears more subprime as prime consumers defect to leasing

11.17% 11.02%18.02% 18.24%

43.04% 43.29%

26.98% 26.67%

Q2 2015 Q2 2016

New loan risk distribution

5.93% 5.79%28.17% 26.98%

22.08% 22.28%

33.27% 34.20%

10.54% 10.75%

Q2 2015 Q2 2016

Used loan risk distribution

4.00% 4.06%

21.78% 21.46%

20.55% 20.88%

36.95% 37.34%

16.73% 16.26%

Q2 2015 Q2 2016

Total (new & used units) loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 19

Prime and Super Prime borrowers choose used vehicles at an increasing rate resulting in shifts among all dealer types

Source: Experian Automotive

19.92% 18.71%

23.72% 23.78%

40.68% 41.63%

13.59% 13.92%

Q2 2015 Q2 2016

Used Franchise loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

92.5

7%

80.7

1%

67.0

1%

56.1

8%

39.3

2%

93.2

5%

82

.24%

69.7

9%

59.9

0%

43.2

6%

DeepSubprime

Subprime Nonprime Prime SuperPrime

Percentage of consumers by risk tier choosing used loans

Q2 2015 Q2 2016

11.78% 11.18%

41.24% 39.00%

20.26% 20.78%

21.59% 23.48%5.12% 5.57%

Q2 2015 Q2 2016

Used Independent loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 20

$28,5

24

$18,6

71

$20,4

26

$16,1

08

$29,8

80

$19,1

01

$20,9

40

$16,4

56

Avg new loanamount

Avg used loanamount

Avg Franchiseused loanamount

AvgIndependent

used loanamount

Average loan amount

Q2 2015 Q2 2016

Average used loan amount reaches record high while new drops below $30k

$24,849

$14,356

$16,359

$13,402

$27,841

$16,227

$18,376

$14,451

$31,222

$19,112

$20,998

$16,498

$31,406

$20,804

$22,115

$18,570

$27,454

$20,281

$21,185

$18,705

Avg New

All Used

Franchise used

Independent used

Average loan amount by tier

Super Prime Prime Nonprime Subprime Deep Subprime

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 21

67

36

68

36

New loan New lease

Average new term

Q2 2015 Q2 2016

71.94

36.82

72.25

37.15

72.23

36.85

69.33

36.26

61.98

35.37

New loan

New lease

Avg new term by risk tier

Super Prime Prime Nonprime Subprime Deep Subprime

New loan term at 68 months with higher terms on the small high risk, lower loan amounts in sub and deep subprime

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 22

65

58

62

66

59

63

Franchise used Independent used All used

Average used term

Q2 2015 Q2 2016

Used terms rise as more prime consumers, who have longer terms, choose used vehicles

Source: Experian Automotive

65.79

53.69

57.91

67.18

56.43

61.47

67.97

60.27

64.86

67.06

62.60

65.48

62.44

60.08

61.58

Franchise used

Independentused

All used

Average term by risk tier

Super Prime Prime Nonprime Subprime Deep Subprime

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 23

772751

695677

770753

695679

37 - 48 49 - 60 61 - 72 73 - 84

Average new score by loan term

Q2 2015 Q2 2016

Average scores by term stabilize and increaselease is not included

646

680

656 662648

680

656668

37 - 48 49 - 60 61 - 72 73 - 84

Average used score by loan term

Q2 2015 Q2 2016

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 24

$483

$394

$499

$404

New loan New lease

Average new payment

Q2 2015 Q2 2016

Payments rise on new vehicles while leasing becomes more attractive

Source: Experian Automotive

$494

$422

$512

$424

$516

$411

$503

$404

$477

$397

New loan

New lease

Avg new payment by risk tier

Super Prime Prime Nonprime Subprime Deep Subprime

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 25

$375

$351

$361

$378

$352

$364

Franchise used Independent used All used

Average used payment

Q2 2015 Q2 2016

Average used payment reaches record high of $364

Source: Experian Automotive

$384

$377

$376

$390

$371

$376

$384

$347

$366

$372

$335

$357

$370

$336

$358

Franchise used

Independent used

All used

Average payment by risk tier

Super Prime Prime Nonprime Subprime Deep Subprime

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 26

4.8

1%

9.1

3%

7.9

5%

12.0

7%

4.8

2%

8.9

7%

7.6

8%

11.6

9%

Avg new rate Avg used rate Franchiseused rate

Independentused rate

Average rates

Q2 2015 Q2 2016

Average new rate rises while prime shift to used results in lower rates in the used market

13.37%

19.29%

18.01%

20.17%

10.59%

16.10%

14.57%

17.82%

6.49%

9.78%

8.96%

11.57%

3.70%

5.23%

4.98%

5.94%

2.64%

3.41%

3.36%

3.46%

Avg New

All Used

Franchise used

Independentused

Average rates by tier

Super Prime Prime Nonprime Subprime Deep Subprime

Source: Experian Automotive

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian Public. 27

Portfolio balances reach record levels as loan amounts grow toall-time highs

Increases in both 30 & 60-day delinquency rates rise as the percentage of loans in the subprime portion of open portfolios grow

Leasing continues to surpass 30% of all new consumer vehicle sales as consumers across all risk tiers increasingly choose to lease

Prime consumers also increasing choosing used vehicles resulting in score increases, greater percentages of used financing in the prime risk tier and lower average used rates

Loan amounts and payments reach all-time highs for new loans while terms continue to extend

Summary

28©2016 Experian Information Solutions, Inc. All rights reserved.

Experian Public.

© 2016 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company

names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian.

Experian Public.

www.experian.com/automotive

Insights about the market, the vehicles

and the people who buy them