startup myths and models

TRANSCRIPT

STARTUP MYTHS

AND MODELS

WHAT YOU WON’T LEARN

IN BUSINESS SCHOOL

BY RIZWAN VIRK

Contents

Figure 0.1 3

Figure 1.1 4

Startup Tool #1: Prioritizing Founder Motivations 5

Startup Tool #2: Uncovering Founder Expectations 6

Figure 3.1 7

Figure 5.1 8

Figure 7.1 9

Figure 8.1 10

Figure 8.2 11

Figure 11.1 12

Startup Tool #3: Calculating LTV and CAC 13

Figure 14.1 15

Figure 15.1 16

Startup Tool #4: Stated (Logical) Reasons for

Acquisitions

17

Startup Tool #5: Real (Underlying, Emotional) Reasons

for Acquisitions

18

Figure 17.1 19

Figure ApA.1 20

Figure ApA.2 21

What people thinkit looks like

What it reallylooks like

Startup success Startup success

Figure 0.1What Success Looks Like. This popular internet meme applies to startups perfectly! Recreated by the author

3

Figure 1.1 Evolution of Startup Markets and Valuations (The Startup Market Lifecycle). Created by the author

30

Actual valuations Total market sizeValuation multiples

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

100B

10B

5B

1B

100M

50M

10M

4

26 T H E C A L L T O A D V E N T U R E

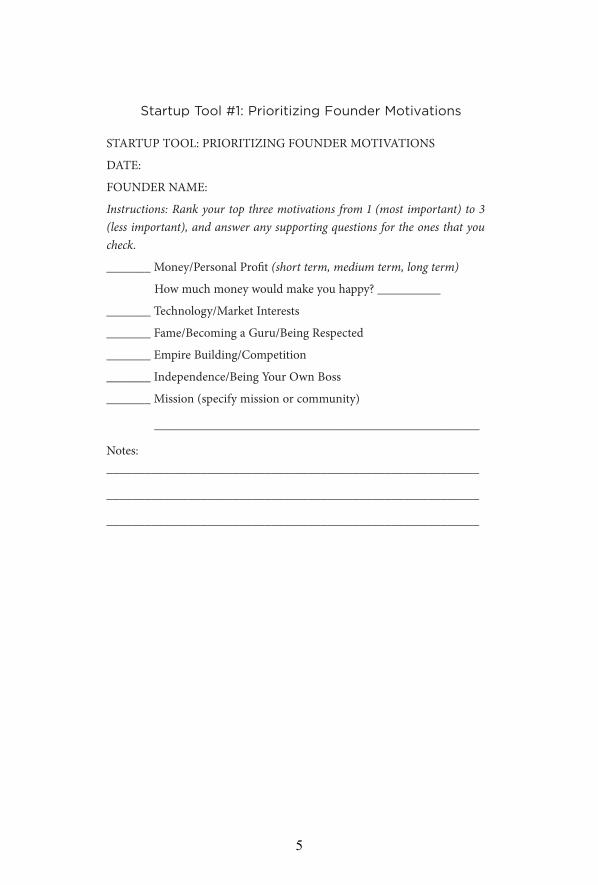

startup Tool #1: prioritizing Founder Motivations

STARTUP TOOL: PRIORITIZING FOUNDER MOTIVATIONS

DATE:

FOUNDER NAME:

Instructions: Rank your top three motivations from 1 (most important) to 3 (less important), and answer any supporting questions for the ones that you check.

_______ Money/Personal Profit (short term, medium term, long term)

How much money would make you happy? __________

_______ Technology/Market Interests

_______ Fame/Becoming a Guru/Being Respected

_______ Empire Building/Competition

_______ Independence/Being Your Own Boss

_______ Mission (specify mission or community)

____________________________________________________

Notes:___________________________________________________________

___________________________________________________________

___________________________________________________________

5

startup Tool #2: Uncovering Founder Expectations

• What happens if the company doesn’t raise money in six months?What if it doesn’t raise money in five years?(1 = not happy, 2 = indifferent, 3 = happy)

unhappy ← 1 2 3 → happy

• What if someone offers to buy the company for $5 million beforethe product is even released? Would you sell?

no way ← 1 2 3 → yes

• What if you were offered $5 million in another company’s stock vs.$5 million in cash?

no way ← 1 2 3 → yes

• What if your startup became the most popular company in SiliconValley, raised $25 million or more, but eventually flamed out.How would you feel?

unhappy ← 1 2 3 → happy

• What if your company started out as direct to consumer, and youended up pivoting to a b2b company dealing with an enterprisesales cycle (or vice versa)—would you be happy in this scenario?

unhappy ← 1 2 3 → happy

What if you are still running this company ten years from now, it’s profitable and surviving but not really an acquisition target?

unhappy ← 1 2 3 → happy

Extra Credit Expectations Exercise: Come up with one scenario that would make you happy and one that would make you unhappy. Then see how your cofounders would score each of those scenarios.

6

Figure 3.1 The Startup Market Opportunity Curve (aka the Goldilocks Curve). Created by the author

30

Actual valuations

Capital required

Valuation curve

Startupopportunitycurve

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

100BTotal market size

10B

5B

1B

100M

50M

10M

7

30

Capital required

Startupopportunitycurve

First half: Two guys and a businessplan are better

Second half: Two guys and abusiness are better

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

100B

10B

5B

1B

100M

50M

10M

Figure 5.1Two Halves of the Market and Two Guys and a Business Plan. Created by the author

8

Figure 7.1 Two Ways to Think About Valuation—Pie vs. High-Jump Bar. Pie created by the author, high-jump bar used under license from iDraw/Shutterstock.com

20%

9

Low fit

Low High

High/high

(hire/keep)(???)

(???)(reject/fire)

High

Low

Cultural fit

Figure 8.1 The Four Quadrants of Hiring. Created by the author

Expe

rienc

e/co

mpe

tenc

e

High experience

Low experienceHigh fit

?

?Low/Low

10

Low fit

Low High

High/high

(hire/keep)(don’t hire/fire)

(hire/keep)(reject/fire)

High

Low

Cultural fit

Figure 8.2 Conclusions for employees in the Four Quadrants of Hiring. Created by the author

Expe

rienc

e/co

mpe

tenc

e

High experience

Low experienceHigh fit

Low/Low

11

Figure 11.1 Focusing vs. Exploring. Created by the author

Large oilpocket

ExploreExplore/focus

D

Explore

B

Focus

A

C

12

Startup Tool #3: Calculating LTV and CAC

Some Basic Date Information

Campaign Start Date: __________ (a) The date your marketing spend started.

Example: April 1

Campaign End Date: __________ (b)The date your marketing spend ended (for this measurement).

Example: April 5

# of Days in Campaign: __________ (c)If you want to measure per day, you can calculate this as (b)–(a)

Example: 4 days

Total Lifetime Period: __________ (c)The time period you are measuring revenue for.

Example: 60 days, 90 days, or 1 year.

Customer Calculation Worksheet

Total Amount Spent: __________ (1)Total amount spent during that period.

Example: $10,000

Total Paid Users: __________ (2)Users that were acquired directly by marketing spend.

Example: 2,000

Total New Users: __________ (3)The total number of new users you got during the campaign period.

Example: 5,000

Total Organic Users: __________ (4) Calculate by (3) – (2)

Example: 5,000–2,000 = 3,000

CAC (paid): __________ (5)This is the cost of customer acquisition for a paid user. Divide (1) by (2).

Example: $10,000/2,000 = $5 per user

13

Customer Calculation Worksheet

CAC (effective): __________ (6)This is your real CAC, or effective CAC. Divide (1) by (3).

Example: $10,000/5000 = $2 per user

Total Revenue for Cohort: __________ (7)This is the total revenue generated over your target period by the users in (3).

Example: 3,000 users generated $15,000 in revenue

LTV: Lifetime Value for a Customer:

__________ (8)This is how much money per customer. Divide (7) by (3).

Example: $15,000 / 5,000 users = $3 LTV per customer

Finally, your LTV (8) should be greater than your CAC (6) for you to prof-itably acquire users. How much more it needs to be depends on factors beyond marketing spend.

Profitability Calculator: __________ (9) Take (8) – (6)

Example: $3 – $2 = $1 profit per user

14

Same Different

Same DifferentAxis: Market

Figure 14.1 The Four Quadrants of Pivoting. Created by the author

Different productdifferent market

Different

Same

Different

Same

Axi

s: p

rodu

ct/

tech

nolo

gy

Different product techsame market

Same productdifferent market

Current productcurrent market

2 3

1 4

15

Figure 15.1 Multiples of Revenues on Exit for Startups. Created by the author

30

Multiples Valuations

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

16

startup Tool #4: stated (Logical) reasons for acquisitions

Why is acquirer _______________ (X) interested in buying your startup?

Please rank from 1 (most important reason) to 5 (least important or n/a).Repeat for each potential acquirer.___ Strategic market buy (expand into market)___ Geography buy (expand to a specific location)___ Product buy (product into their product line)___ Technology buy (component of your product into theirs)___ Numbers buy (put an X next to the number most important) ___ Revenue ___ Customers ___ Profits___ Acqui-hire / Talent

° What will you work on after the acquisition?

° What will happen to your product?

Other comments:________________________________________________________________________________________________________

17

startup Tool #5: real (underlying, emotional) reasons for acquisitions

Why is acquirer _______________ (X) interested in buying your startup?

Please rank from 1 (most important reason) to 5 (least important or n/a).Repeat for each potential acquirer.___ FOMO (fear of missing out)___ Frustration___ Checkbox___ Master of the universe___ Shiny new toy!___ Security___ Embarrassment

Usually, a combination of these emotional reasons underlie an acquisition; it’s just that most CEOs or management teams aren’t totally honest or forth-coming about these emotional reasons.

18

100

90

80

70

60

50

Perc

ent

40

30

20

10

0Seed A B

Series

Figure 17.1 Value of Common Stock vs. Preferred Stock. Created by the author

D IPOC

PreferredCommon

19

30

Actual valuations

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

100B

Valuation multiples Total market size

10B

5B

1B

100M

50M

10M

figure apa.1Market Size Evolution with Stages. Created by the author

20

figure apa.2The Startup Market Opportunity and Related Curves. Created by the author

30

Actual valuations

Capital required

Valuation curve

Startupopportunitycurve

25

20

15

10

5

0Nascent Growing Super-hot Maturing Mature

100BTotal market size

10B

5B

1B

100M

50M

10M

21