sri lanka the competitiveness program (tcp)

TRANSCRIPT

Sri Lanka The Competitiveness Program (TCP) Final Report

January 2008

This publication was produced by Nathan Associates Inc. for review by the United States Agency for International Development.

Sri Lanka The Competitiveness Program (TCP) Final Report

Task Order 841 Under Contract No. PCE-I-00-98-00016-00, SEGIR GBTI I July 2004 to November 2007

DISCLAIMER

This document is made possible by the support of the American people through the United States Agency for

International Development (USAID). Its contents are the sole responsibility of the author or authors and do not

necessarily reflect the views of USAID or the United States government.

Contents 1. Introduction 1

Purpose and Approach 1 Results 2 Lessons 3 Report Organization 3

2. Program Review 5

Design and Objectives 5 Funding and Modifications 6 Staffing and Level of Effort 6 Management 7 Achievements 7

3. Ceramics Cluster 15

Industry Competitiveness 16 TCP Achievements 18 Cluster Acheivements 20 Rural Impact 21 Industry Leaders’ Opinions about TCP 21

4. Coir Cluster 23

Industry Competitiveness 23 TCP Achievements 26 Cluster Achievements 28 Rural Impact 29 Industry Leaders’ Opinions about TCP 29

5. Gems & Jewelry Cluster 31

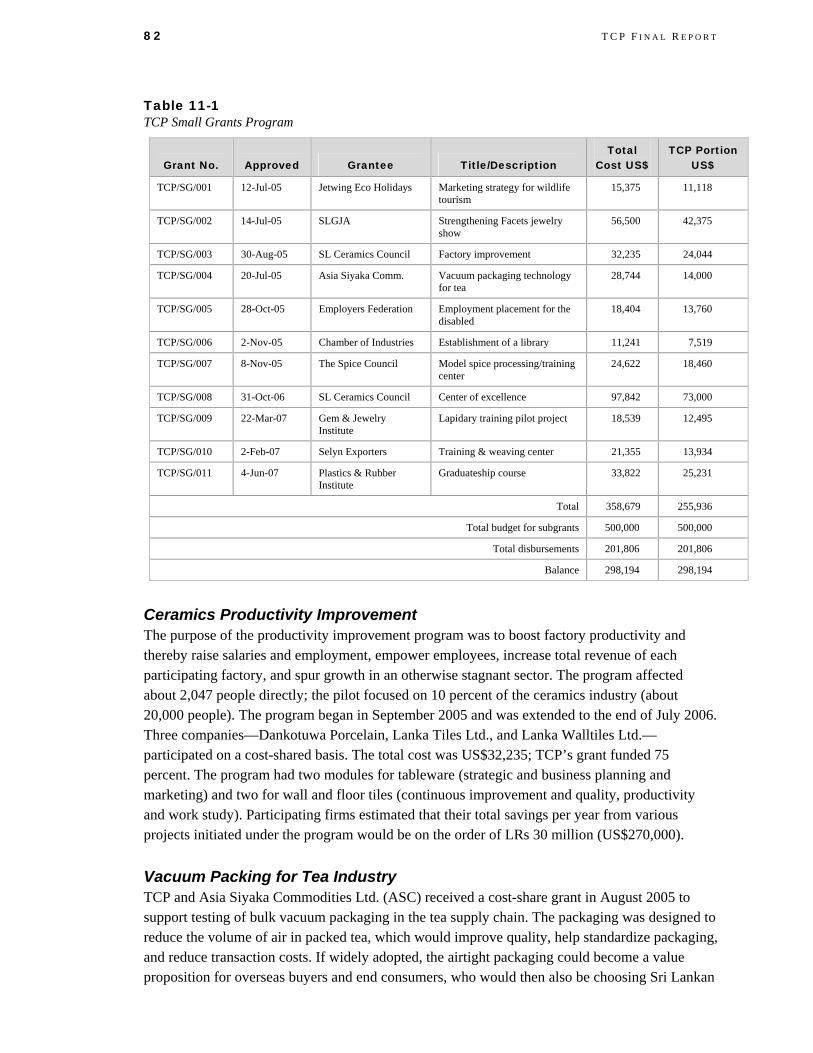

Industry Competitiveness 31 TCP Achievements 34 Cluster Achievements 34 Small Grants 35 Rural Impact 35 Industry Leaders’ Opinions about TCP 36

I I

6. Information & Communication Technology Cluster 37

Industry Competitiveness 37 TCP and Industry Achievements 39 Industry Leaders’ Opinions About TCP 43

7. Rubber Cluster 45

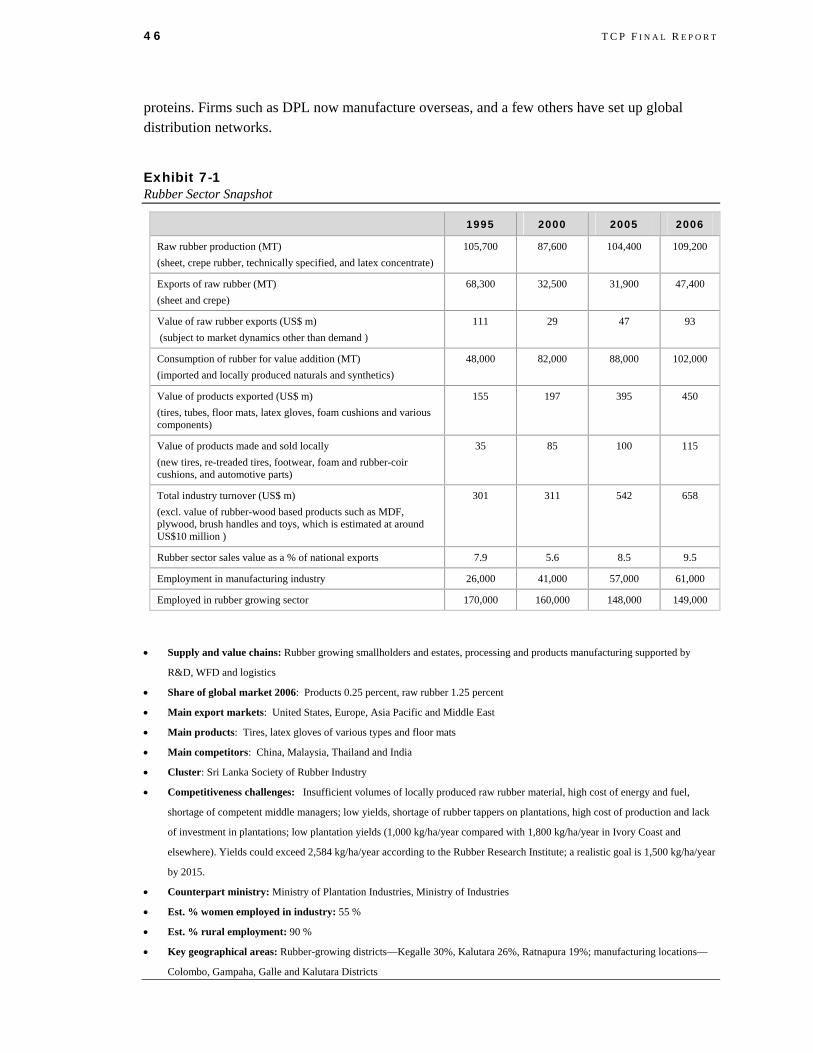

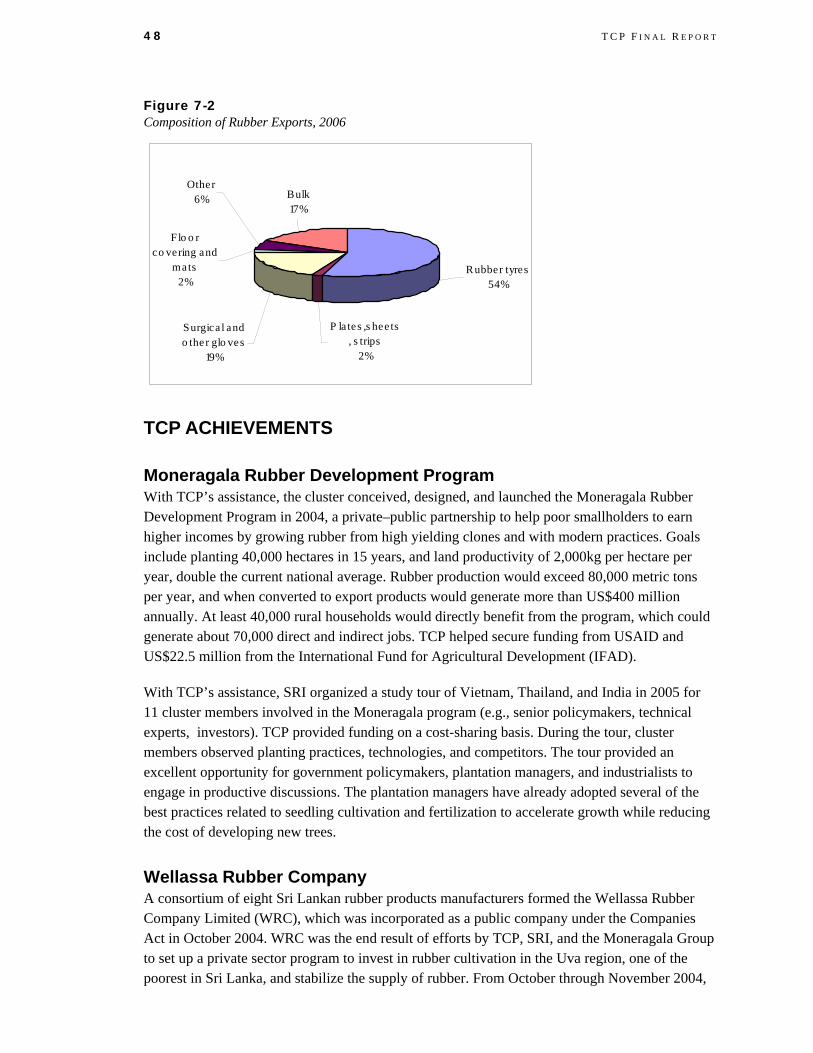

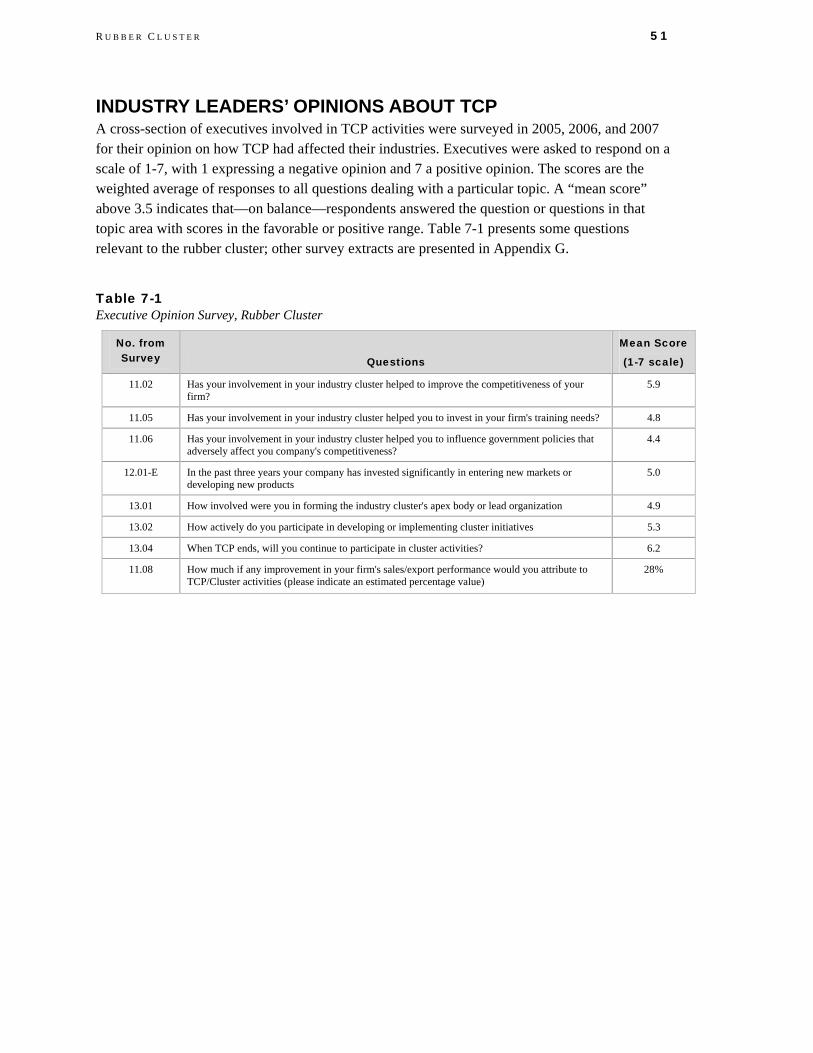

Industry Competitiveness 45 TCP Achievements 48 Rural Impact 50 Small Grants 50 Industry Leaders’ Opinions about TCP 51

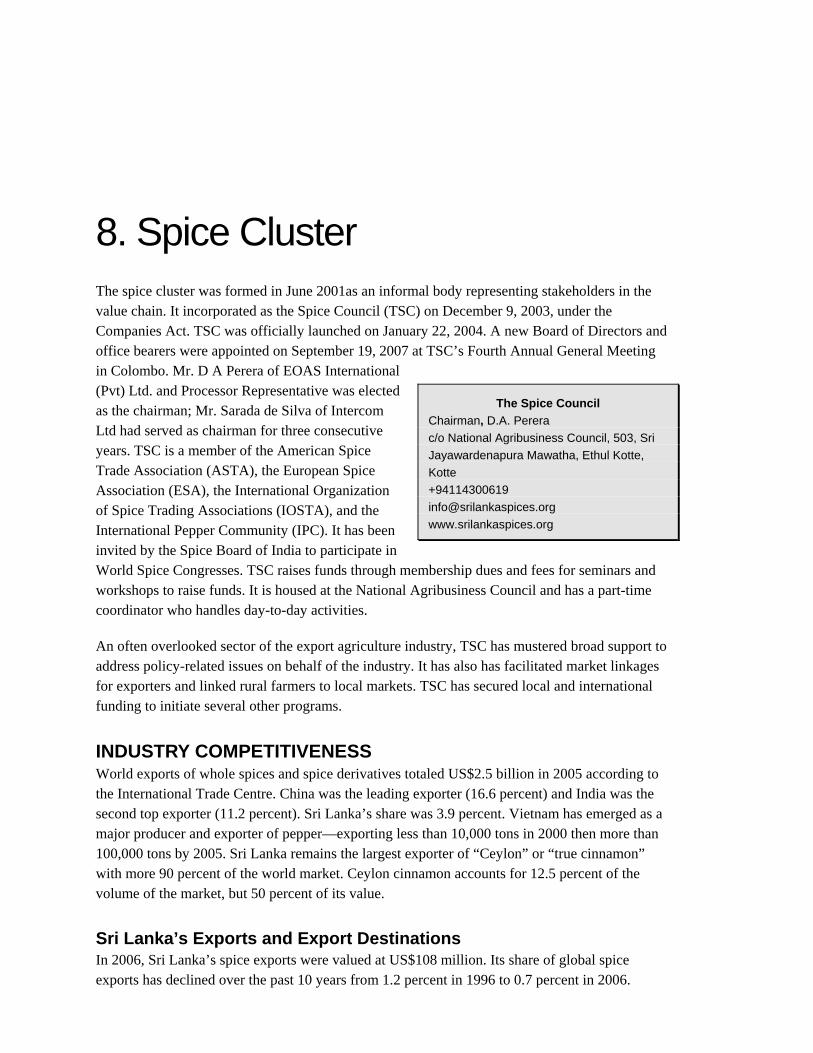

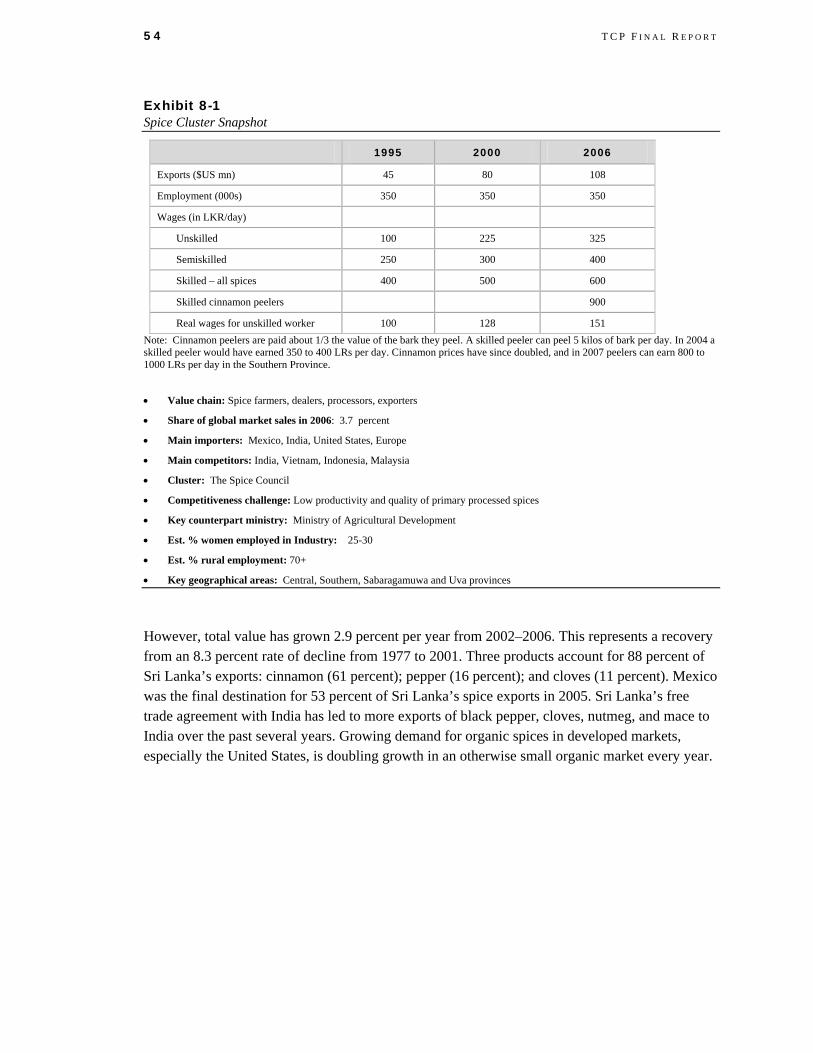

8. Spice Cluster 53

Industry Competitiveness 53 TCP Achievements 55 Cluster Achievements 57 Rural Impact 57 Industry Leaders’ Opinions about TCP 58

9. Tea Cluster 59

TCP Achievements 62 Cluster Achievements 63 Rural Impact 64 Small Grants 64 Industry Leaders’ Opinions about TCP 65

10. Tourism Cluster 67

Industry Competitiveness 67 TCP Achievements 69 Cluster Achievements 71 Rural Impact 72 Campaign to Revitalize Tourism 72 Industry Leaders’ Opinions about TCP 74

11. Cross-cutting Activities 75

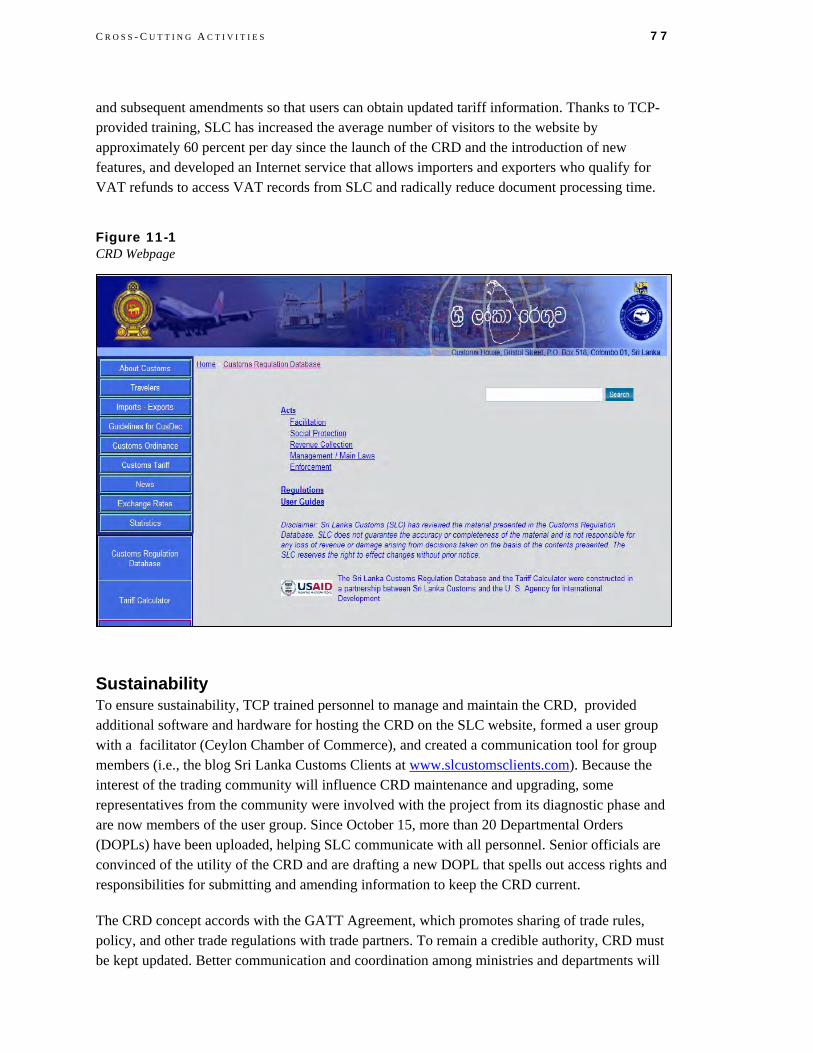

Customs Regulation Database 75 Logistics Performance 78 Small Grant Program 80

12. Other Activities 87

Workforce Development 87 Global Competitiveness Report 88 Firm Competitiveness Studies 89

I I I

WWW.Competitiveness.LK 91 Monitoring and Reporting 92

13. Lessons Learned and Implications for Other Projects 99

Lessons Learned 99 Implications for Other Projects 101 What Clusters Have Learned 106

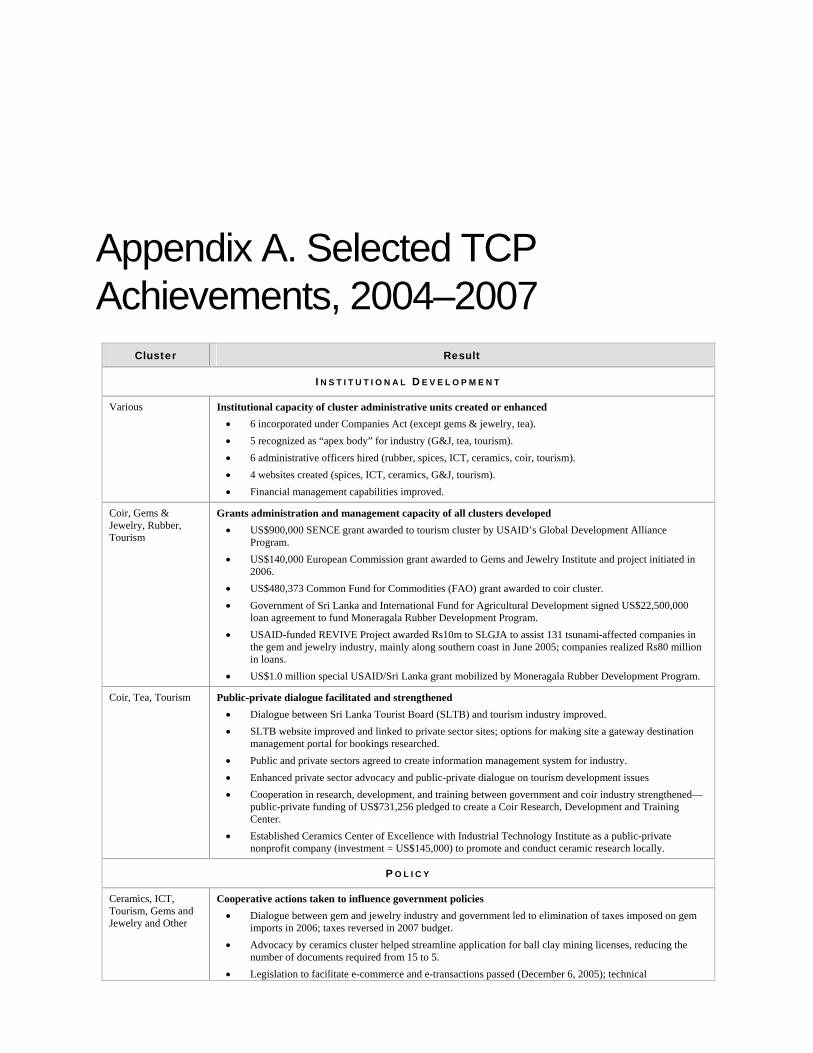

Appendixes A. Selected TCP Achievements, 2004-2007 B. TCP Work Plan and Deliverables C. Short-term Technical Assistance Level of Effort D. Technical Assistance Purchase Orders E. Technical Reports F. Cluster Association Development Index G. Executive Opinion Survey of TCP-assisted Clusters, 2007 H. Exports from Sectors with TCP Clusters

Illustrations

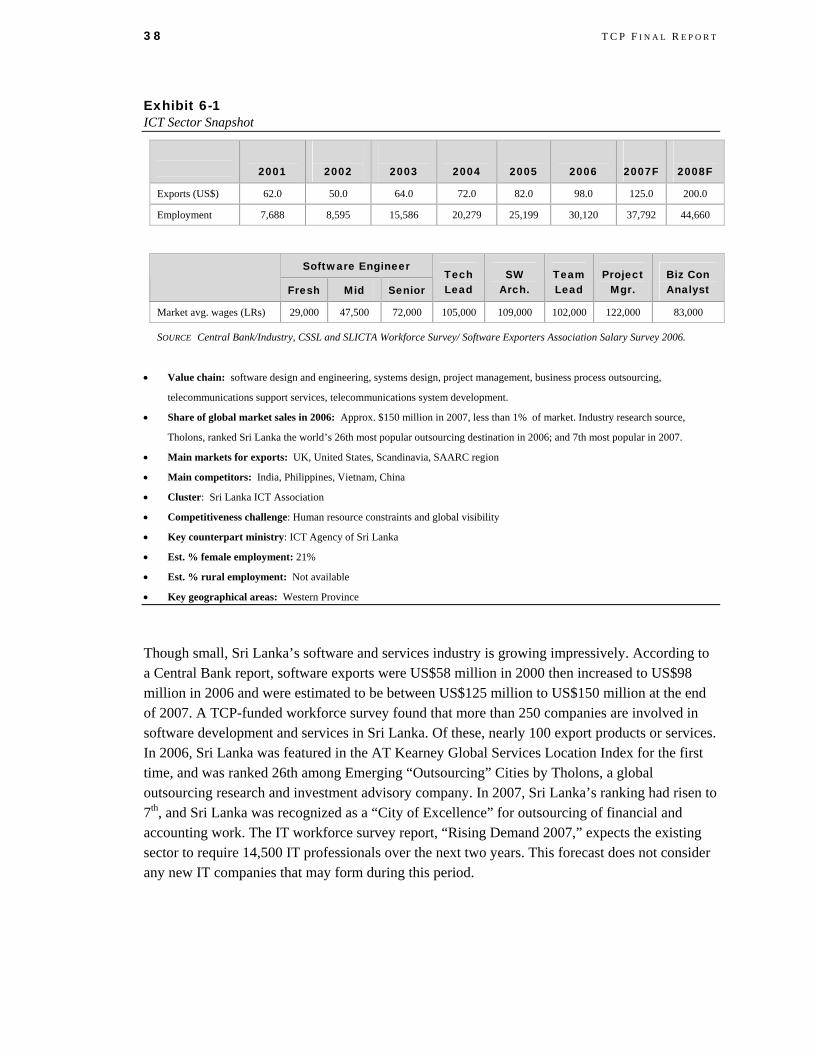

Figures Figure 2-1. Exports Earnings of Eight Sectors with TCP Clusters, 1995-2006 9 Figure 2-2. Five Years of Export Earnings Before and After TCP 9 Figure 2-3. Value Added and Non-Value Added Exports for Eight Sectors 10 Figure 3-1. Annual Rate of Growth in Ceramic Exports, 1995-2006 17 Figure 3-2. Composition of Ceramics Exports, 2006 17 Figure 3-3. CENTEC Opening 19 Figure 3-4. Annual Rate of Growth in Coir Exports, 1995–2006 25 Figure 4-1. Composition of Coir Exports, 2006 25 Figure 4-2. Geotextile Loom 28 Figure 5-1. Annual Rate of Growth in Gem and Jewelry Exports, 1995–2006 33 Figure 5-2. Composition of Gem and Jewelry Exports, 2006 33 Figure 5-3. Gem and Jewelry Training 36 Figure 6-1. Estimated Growth of Software Exports 39 Figure 6-2. Overall IT Workforce Growth Trend 39 Figure 6-3. Launch of the National IT Workforce Survey 41 Figure 7-1. Annual Rate of Growth in Rubber Exports 47 Figure 7-2. Composition of Rubber Exports, 2006 48 Figure 7-3. Wellassa Seedlings 49 Figure 8-1. Annual Rate of Growth in Spice Exports 55 Figure 8-2. Composition of Spice Exports, 2006 55 Figure 8-3. Spice Drying Machine 57 Figure 9-1. Annual Rate of Growth in Tea Exports 61

I V

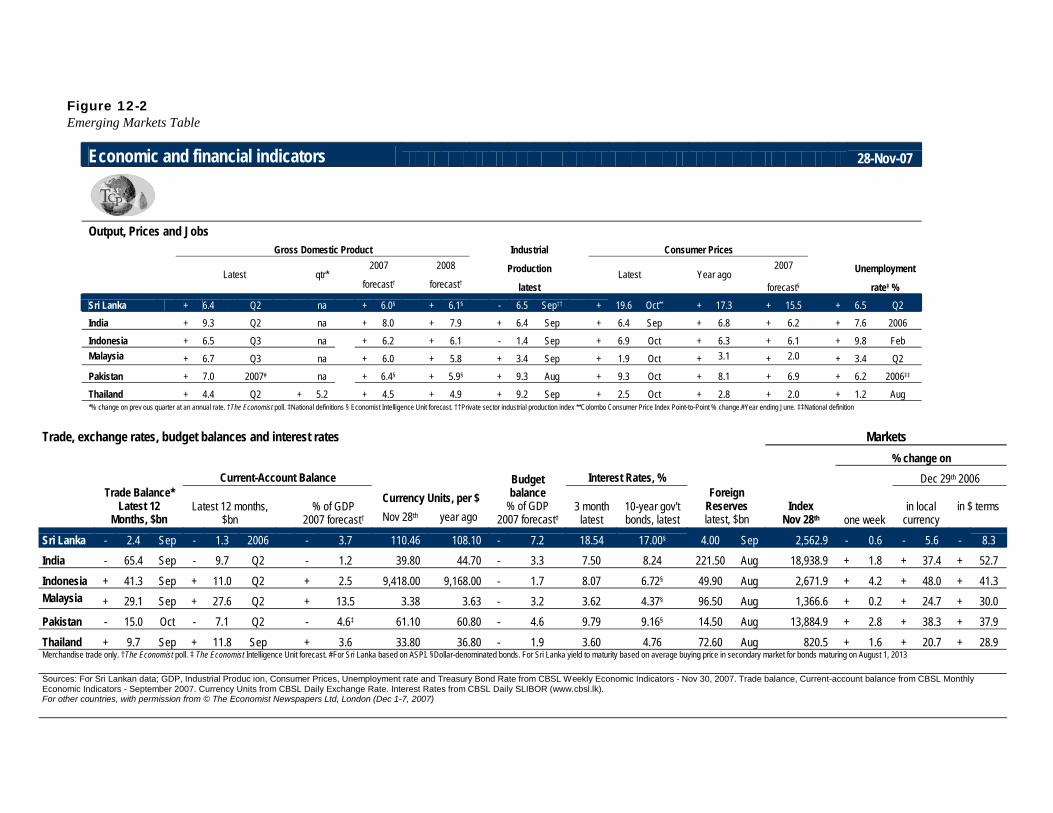

Figure 9-2. Composition of Tea Exports, 2006 61 Figure 9-3. Vacuum Packed Tea 65 Figure 10-1. Annual Rate of Growth in Tourism Earnings 69 Figure 10-2. Top Ten Markets for Tourism, 2006 69 Figure 10-3. Rainforest Ecolodge Brochure 71 Figure 10-4. Smibt Elephant Poster 73 Figure 11-1. CRD Webpage 77 Figure 12-1. Hemas and CBL Case Studies 90 Figure 12-1. Emerging Markets Table 93

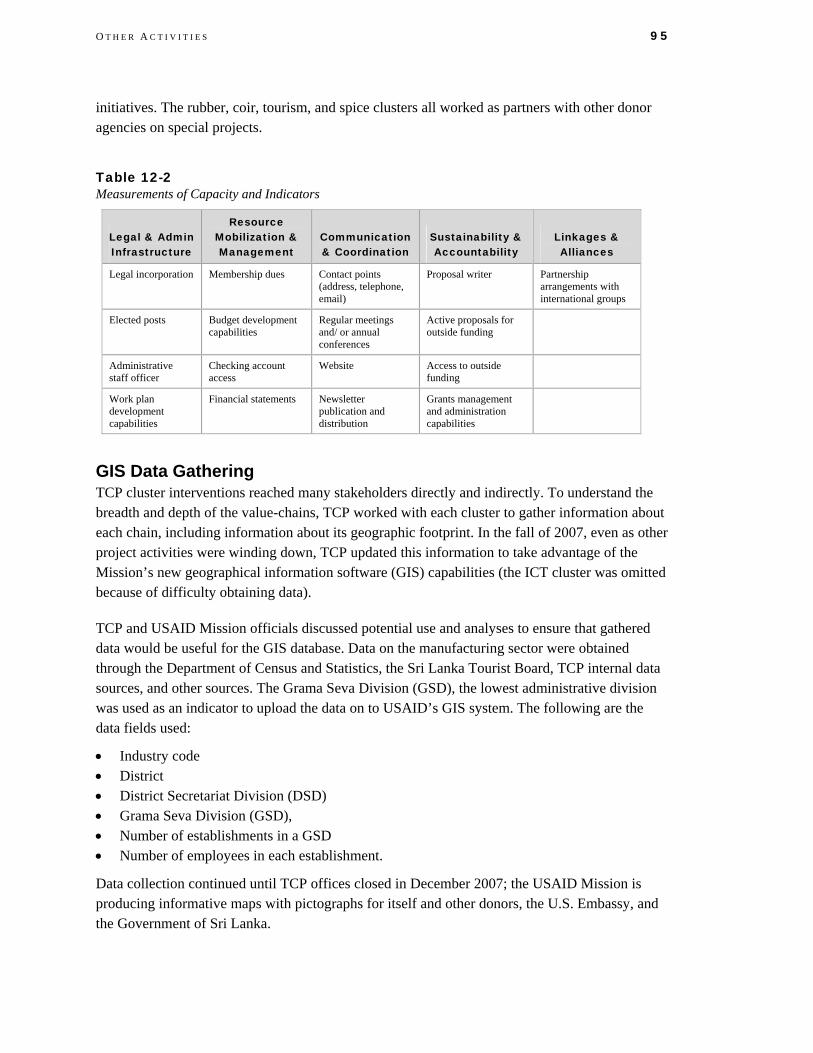

Tables Table 2-1. Strategic Initiatives/Investments Specific to a Geographical Location 11 Table 3-1. Executive Opinion Survey, Ceramics Cluster 21 Table 4-1. Executive Opinion Survey, Coir Cluster 30 Table 5-1. Executive Opinion Survey, Gem & Jewelry Cluster 36 Table 6-1. Executive Opinion Survey, ICT Cluster 43 Table 7-1. Executive Opinion Survey, Rubber Cluster 51 Table 8-1. Executive Opinion Survey, Spice Cluster 58 Table 9-1. Executive Opinion Survey, Tea Cluster 65 Table 10-1. Executive Opinion Survey, Tourism Cluster 74 Table 11-1. TCP Small Grants Program 82 Table 12-1. Sri Lanka’s Competitiveness Rankings, 2001–2007 89 Table 12-2. Measurements of Capacity and Indicators 95

Exhibits Exhibit 2-1. Changes in Private Sector and Public Sector Attitudes 12 Exhibit 3-1. Ceramic Sector Snapshot 16 Exhibit 4-1. Coir Sector Snapshot 24 Exhibit 5-1. Gem & Jewelry Sector Snapshot 32 Exhibit 6-1. ICT Sector Snapshot 38 Exhibit 7-1. Rubber Sector Snapshot 46 Exhibit 8-1. Spice Cluster Snapshot 54 Exhibit 9-1. Tea Sector Snapshot 60 Exhibit 10-1. Tourism Sector Snapshot 68

1. Introduction This is the final report on activities under contract PCE-I-00-98-00016-00, SEGIR General Business, Trade and Investment IQC, Task Order 841 for The Competitiveness Program, carried out in Sri Lanka from July 2004 to November 2007. The program was implemented by the Nathan–MSI consortium with Nathan Associates Inc. as the prime contractor and J.E. Austin Associates as the subcontractor.

PURPOSE AND APPROACH The purpose of TCP was to improve the competitiveness of Sri Lanka in the global marketplace by continuing the support provided under the predecessor task order, The Competitiveness Initiative (TCI) (2000-2003). TCP was USAID’s primary private sector development activity in Sri Lanka. It continued working with the eight industry “clusters” that it had formed under TCI: ceramics, coir, gems and jewelry, ICT spices, rubber, tea, and tourism. In 2006, these industries employed an estimated 2.2 million persons or 31 percent of the workforce, and accounted for 58 percent of non-apparel exports, or one-third of all of Sri Lanka’s exports, valued at US$2.3 billion or 21.4 percent of GDP.

The clusters were composed of representatives from across the value chain—from raw material producers to manufactures to traders and even retailers—as well as representatives from government, such as regulators, and from supporting industries such as packaging, shipping, financial services, and information technology. So constituted, clusters served as a proxies for entire value chains in Sri Lanka. Working together, cluster members reached a better understanding of and appreciation for their strategic position in global value chains and jointly pursued policy reforms to advance those positions. They learned about the full scope and opportunities for value addition and their industry’s ability to add value. This enabled them to devise consensus-based strategies and action plans for becoming more competitive.

Using the strategies as a framework, TCP worked with each cluster to devise initiatives and then mobilize expertise and other resources to execute them. From 2004 to 2007, each cluster implemented a half dozen or more such initiatives. TCP provided guidance through resident advisers and short-term technical specialists, helped fund and arrange workshops and conferences, and administered a small grants program. These complementary measures enabled the clusters to act as catalysts for improving their industries. Clusters raised awareness about the opportunities as well as the challenges of globalization and improved the ability of each industry to mobilize resources to face challenges, research options, and take effective action.

2 T C P F I N A L R E P O R T

TCP also worked on trade facilitation and logistics. Its “FastPath” study evaluated the shipping and logistics sectors, and its technical assistance with the Department of Customs put tariff and customs information onto the department’s website in a searchable format, along with other information for importers and exporters. TCP also worked to raise awareness of competitiveness and extend the impact of competitiveness activities to rural areas.

RESULTS TCP helped the clusters coalesce around strategies and initiatives to improve competitiveness and achieve impressive results. Clusters completed 20 initiatives, improved public–private dialogue and regulatory decisions, influenced the content and passage of a new tourism law, and generated eight public-private and joint venture investments in all areas—from market research to energy conservation to workforce development. Numerous individual firms also made strategic investments to improve their own competitiveness.

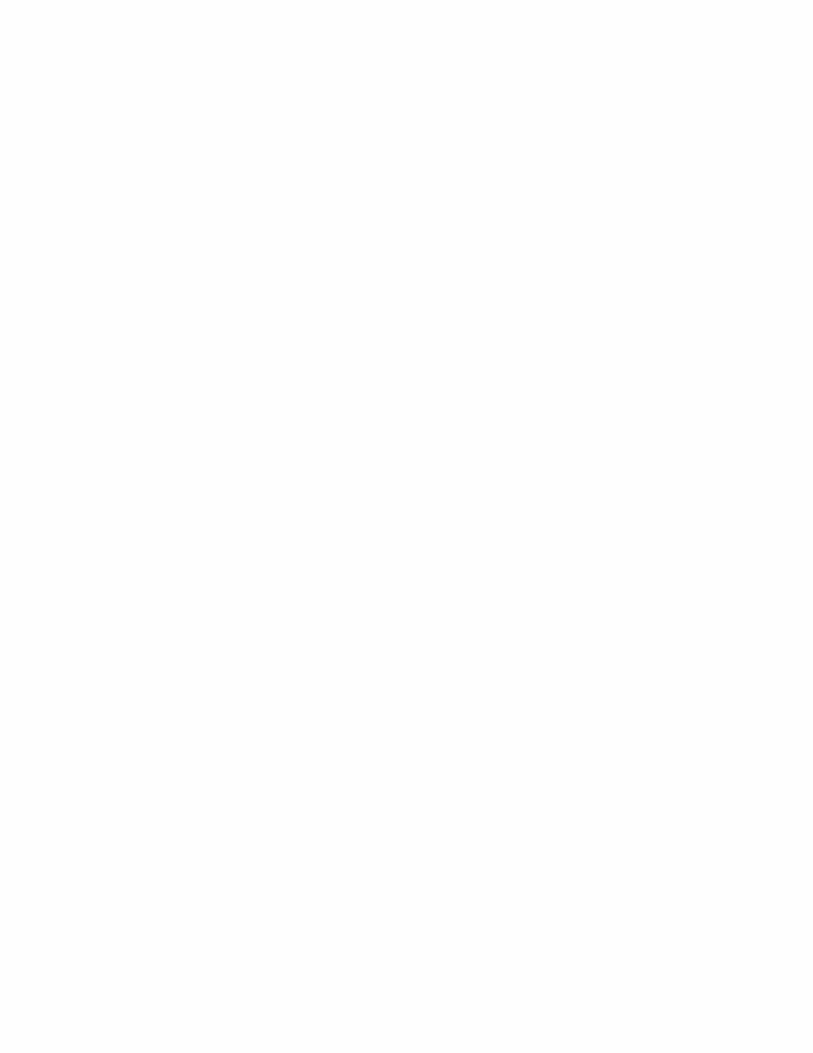

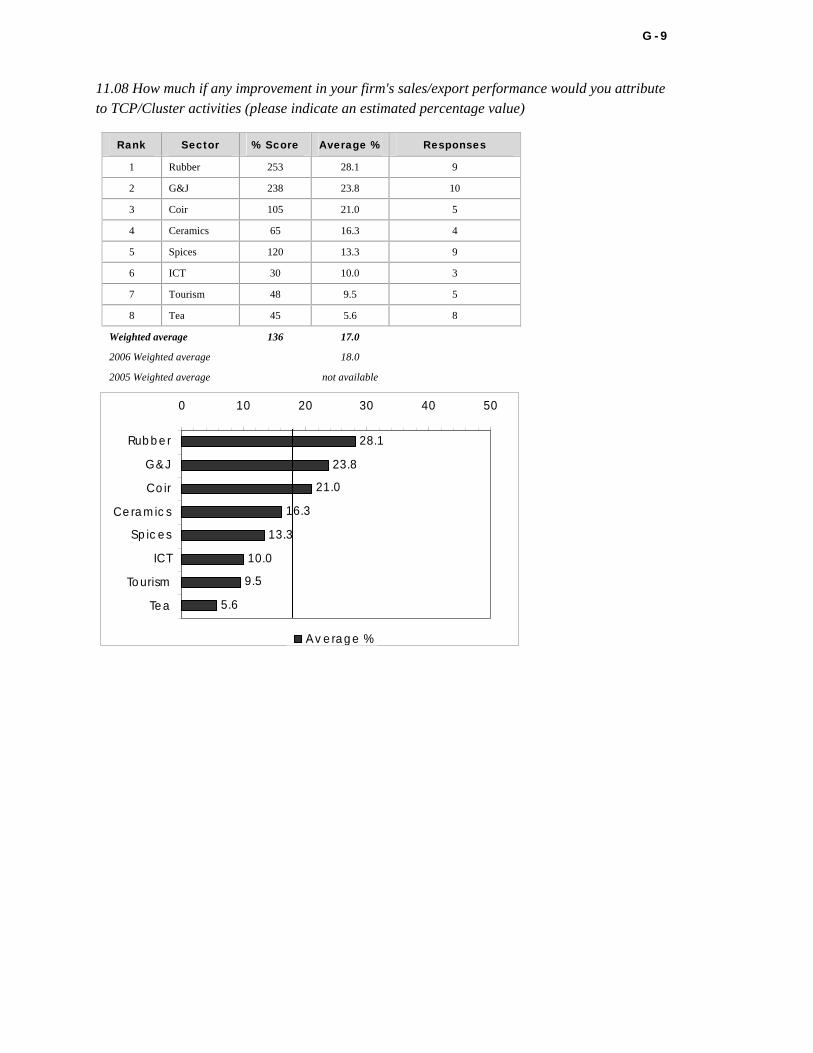

The best broad measure of competitiveness was improved export performance in industries that worked with TCP. The clusters increased their exports by US$885 millions or 62 percent from 2001 to 2006. That growth was US$576 million or 35 percentage points better than the five years before TCP (1995–2000) when exports increased by only US$309 million or 20 percent. Export growth during TCP more than doubled not only because of favorable economic circumstances, but also because the clusters followed sound strategies to overcome unfavorable events and shocks. Executives in all clusters report that their firms and industries are better positioned to compete in global markets thanks to having been a part of TCP. In fact, those surveyed in 2007 attributed 17 percent of recent improved export performance to participation in TCP and cluster activities.

The faster pace of export growth amounted to an additional US$500 million in export earnings for Sri Lanka, and the 17 percent attribution suggests that TCP was worth US$85 million of those earnings for 2001 to 2006. Three things can be said about the attribution percentage. First, the estimate is conservative because benefits stemming from TCP’s work will continue well after the end of the project in 2007, and range well beyond the domain of export performance. Second, the improved export performance compares very favorably with the total cost of US$25.1 million (including US$12.5 million for TCP) that USAID invested in three competitiveness task orders from 2001 through 2007. Third, while export numbers are factual and attribution of causality is subjective, it is grounded in the opinion of the businessmen who worked most directly with the project. In their opinion, TCP’s impact on competitiveness in Sri Lanka will continue into the future. As project managers, we believe that this indicates that other unquantifiable benefits will also continue and eventually prove to be more important to Sri Lanka’s long-term development than last five years of export results.

Complementary successes included improved dialogue between the private and public sector on the competitiveness of exports. During TCP, all clusters engaged in policy dialogue and advocacy with ministries and government offices important to their sectors. The ICT and tourism clusters succeeded in getting major new legislation passed for their sectors. The coir, rubber, ceramics, and gems and jewelry clusters improved the regulatory environment so businesses can operate and export more competitively.

I N T R O D U C T I O N 3

LESSONS We can draw some lessons from TCP’s approach to providing this particular type of technical assistance. First, private sector commitment is indispensable. Each industry that joined TCP was formally enlisted and committed to work toward consensus on strategic priorities and initiatives. This means that each company or association was a stakeholder and partner in designing and implementing technical assistance assignments. Each cluster member made commitments to their colleagues and to TCP well before any short-term specialists arrived in Sri Lanka. They understood their role in technology and information transfer, and worked with dedication and intelligence to make the best use of foreign and local advisers.

Second, consensual decisions and cost-sharing requirements revealed and confirmed priorities. Because most clusters consisted of private firms, decisions about time and resources were made quickly and simply. Cost-sharing for events assured both the industry and TCP that events dealt with an industry’s true priorities.

Third, highly targeted, high quality assistance built credibility and cooperation. Nathan Associates and J.E. Austin Associates were able to provide the diverse expertise requested by clusters, from specialists in marketing gems at U.S. gem and jewelry trade fairs, to agro-engineers with experience improving survival rates in rubber seedling nurseries, to technical experts in gamma irradiation to sterilize food products and surgical examination gloves of natural rubber. Finding and fielding such experts was not easy, and TCP’s private sector partners cooperated with and made the best use of experts.

Lastly, TCP’s advisers and cluster coordinators acting as neutral parties and facilitators proved vital to the efficient and timely implementation of activities. Many cluster participants had been working with each other for generations and the presence of a neutral party broke negative patterns of the past and imparted a new sense of enthusiasm and dynamism.

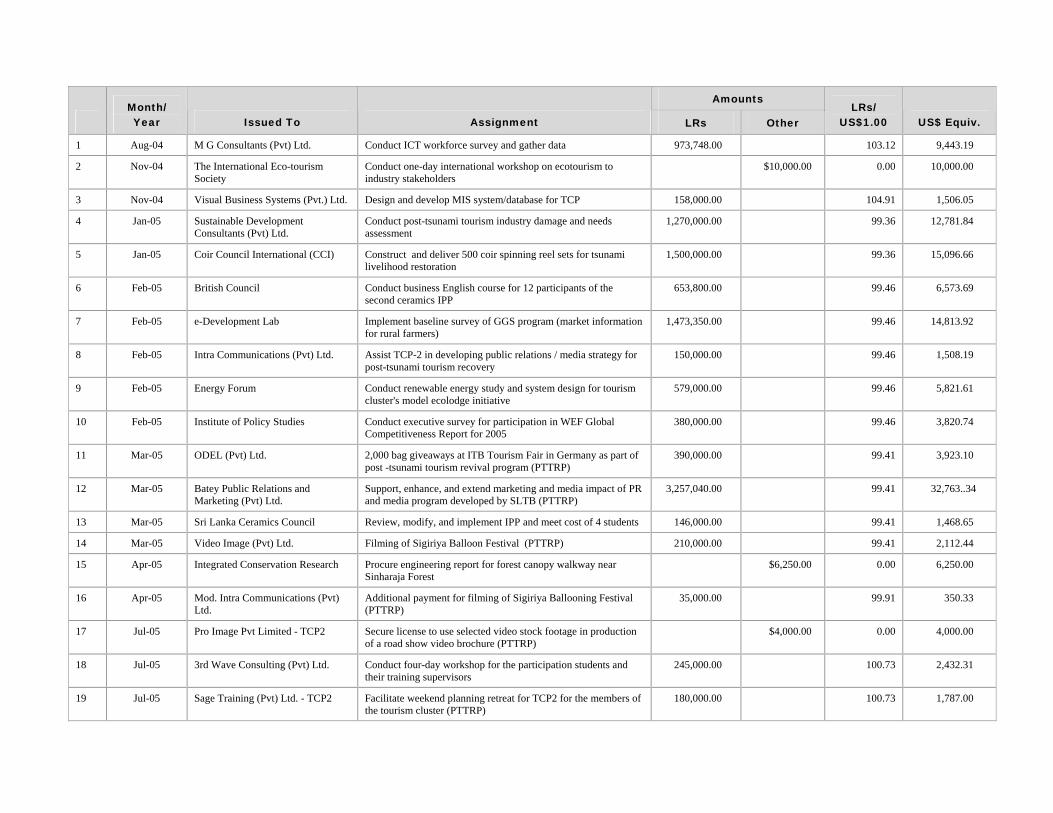

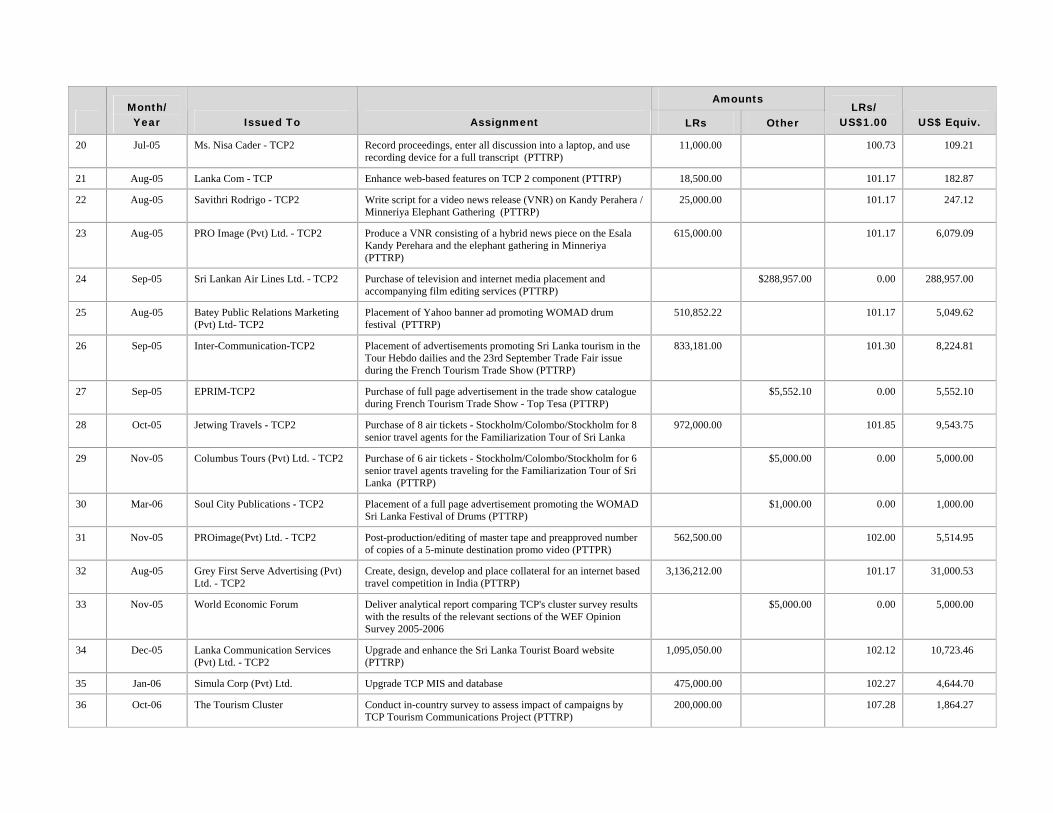

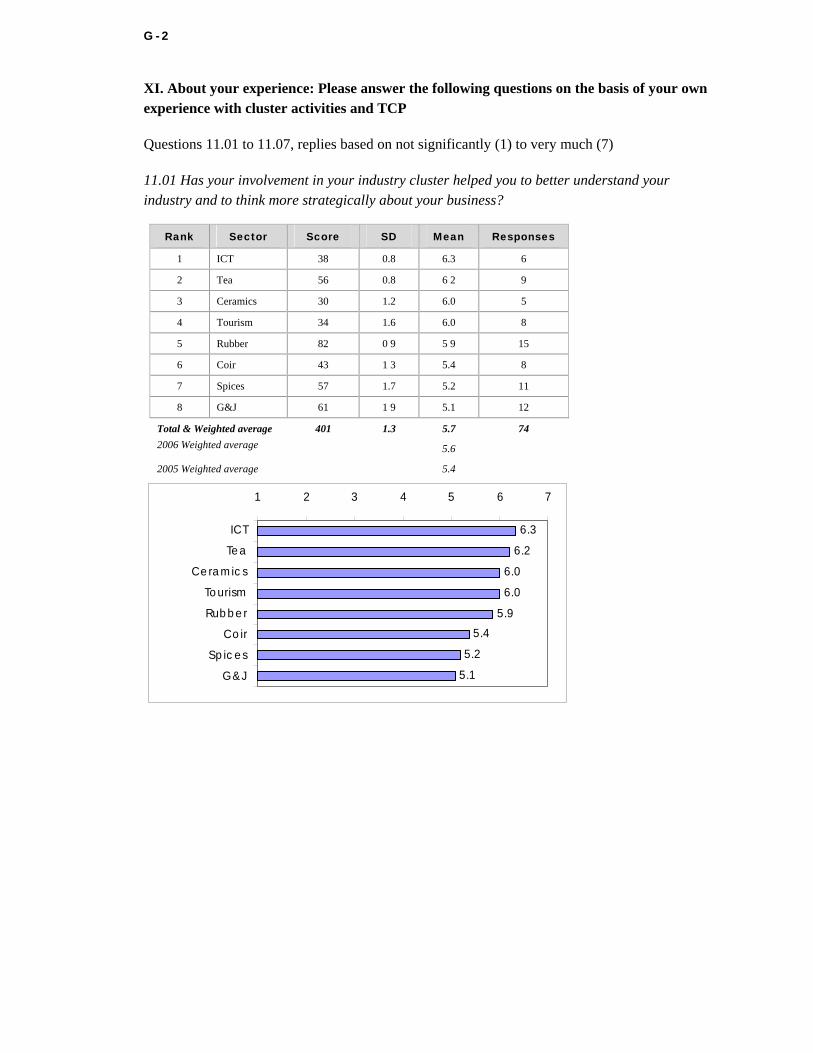

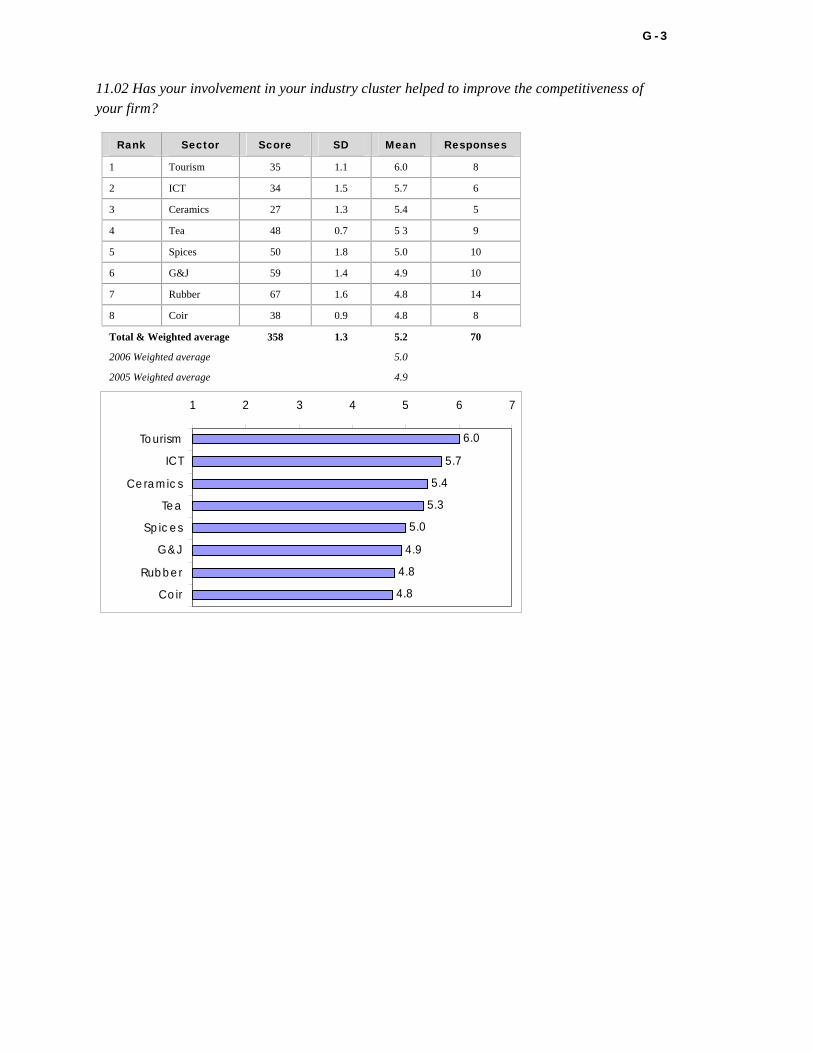

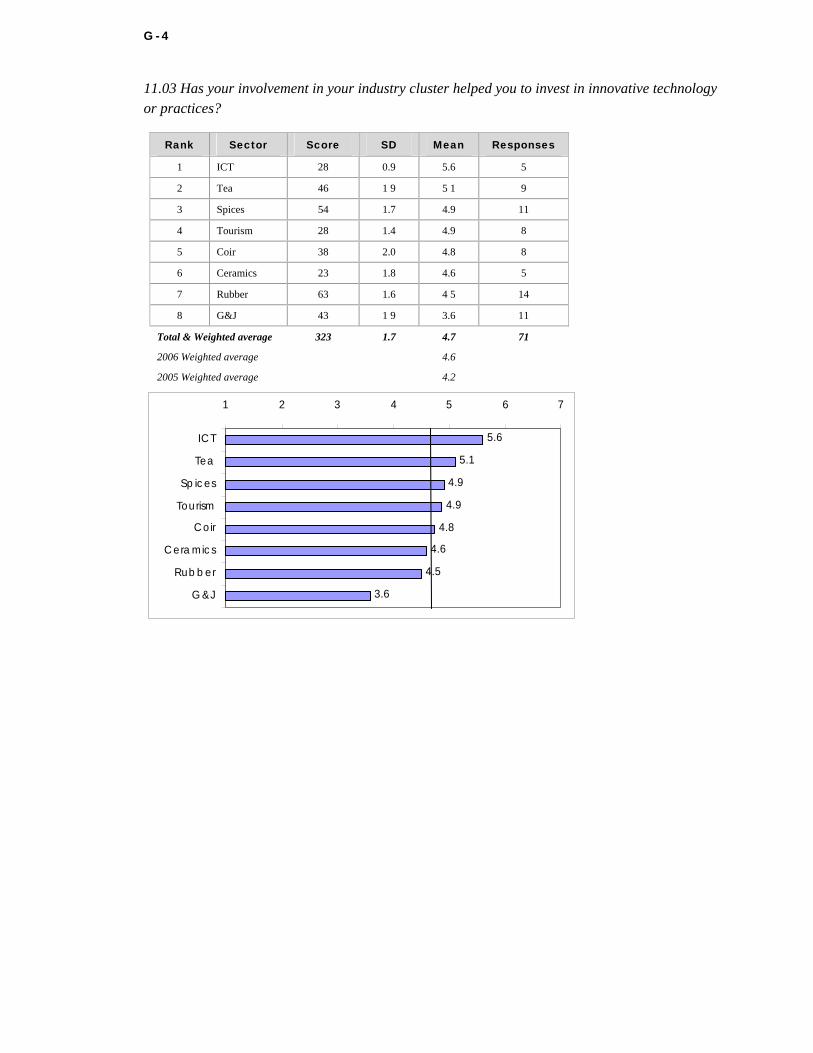

REPORT ORGANIZATION This report provides details on TCP’s objectives, activities, and accomplishments and draws lessons from program activities that will help cluster partners, Sri Lanka, and the broader development community advance private sector led development. Chapter 2 describes TCP’s design, purpose, funding and modifications, general quantitative and qualitative achievements, and effect on sector-level economic performance. Chapters 3 through 10 provide details on work in the eight clusters. Chapters 11 and 12 describe cross-cutting and complementary activities, including workforce development, trade facilitation, logistics, customs, and English language training. (TCP’s post-tsunami support to revive tourism is discussed in the chapter on the tourism cluster.) Each of these chapters provides a comprehensive review of major activities, including workshops, reports, and other deliverables, and the results of those activities. The final chapter presents lessons learned, the impact and influence of TCP methods on other projects, the aspects of TCP that can and have been replicated elsewhere, and setbacks—many of them outside the scope of TCP’s influence—that affected program success. The appendixes summarize program achievements, deliverables status, short-term level of effort, purchase order data, and sector export data, and list major reports, criteria for the Cluster Association Development Index, and excerpts from the 2007 executive opinion survey.

2. Program Review DESIGN AND OBJECTIVES The Competitiveness Program (TCP) was funded through a contract from USAID/Sri Lanka as part of the Mission’s country strategic plan for FY 2003–FY2007, Supporting Peace and Reform in Sri Lanka (September 30, 2003). Strategic Objective 4 (later SO 8) of that plan is “foundation set for rapid and sustainable economic growth.” USAID/Sri Lanka identified three intermediate results for that objective: sound economic policy implemented, more competitive products sold in the global market, and improved and more relevant skills for the private sector workforce. TCP was designed to promote and apply the principles of private sector led development to achieve the first two results directly and the third result indirectly. Indicators for the results were as follows:

• Growth in value of exports. • Number of companies investing in competitiveness-enhancing activities. • Amount invested by companies and public sector in competitiveness. • Policy changes supporting or enhancing competitiveness. • Capacity of clusters as member service organizations.

TCP also contributed to the IR 8.3 “Improved workforce skills” through training and other activities implemented by member clusters.

In July 2004 USAID/Sri Lanka entered into a two-year contract with Nathan Associates to provide senior resident advisers and an office to manage short-term technical assistance to be defined and implemented mainly with and by partners in the eight industry clusters that were formed as part of the predecessor project, The Competitiveness Initiative (TCI). The clusters had reached consensus on competitiveness strategies and were implementing a few strategic initiatives. Under TCI, several clusters were already or were in the process of incorporation under Sri Lanka’s Companies Act. TCP would also provide those and other interested clusters with technical assistance to form durable member service associations and become industry “apex” bodies, if desired.

Including modifications, TCP had eight components:

• Cluster strengthening • Administrative and contract management support • Economic growth policy reform • Trade facilitation and logistics practices evaluation • Rural economy linkages

6 T C P F I N A L R E P O R T

• Job skills enhancement and competitiveness awareness • Small grants • Tourism recovery communications support (post-tsunami).

FUNDING AND MODIFICATIONS The initial award for Task Order 841 was made on July 2004 in the amount of US$8,406,361 for a 24-month program. Modification 01 of October 2004 clarified the scope of work, added a small grant component, and increased the ceiling price to US$9,063,701. Modifications 02 and 03 in April and May 2005 added a component and US$3.43 million to support a media campaign in Europe and India and other efforts to help Sri Lanka recover from the drop in tourist arrivals that followed the tsunami of December 2004. The campaign was designed to convey that Sri Lanka was a safe and healthy destination, offering an alternative to the negative images portrayed in the media of the tsunami and conflict. The revised ceiling price was US$12,493,701.

Modification 04 of August 2006 extended the project to September 30, 2007, revised the SOW to include additional technical assistance to clusters and restructured trade capacity building activities to focus on trade facilitation and logistics analysis through two programs. The first was to help the Sri Lanka Customs Authority post tariff and regulatory procedures on its website in a searchable form. The second was to work with shippers, freight forwarders, importers, exporters, and the public sector to review the performance of Colombo and Sri Lanka as a logistics hub and identify how it could improve and maintain its status as a regional hub. Modification 05 of June 2007 and 06 of November 2007 extended the project completion date, allowing for additional time to draft the final report, and arrange for storage of equipment and other assets to be used on contracts to be awarded in 2008.

STAFFING AND LEVEL OF EFFORT The project began in July 2004, a seamless a continuation of TCI, which had run from September 2000 to June 2004. Offices were located in The World Trade Center, East Tower, Level 13, Echelon Square, Colombo 1. More office space was leased in May 2005 to accommodate the tourism recovery communications support component (TPC-2).

Key personnel consisted of the Chief of Party, John Varley, and Deputy Chief of Party, David Dyer, who was replaced by Pradeep Liyanamana after Mr. Dyer left to head the post-tsunami REVIVE project in February 2005. Eight Sri Lankan professionals served as program specialists for the clusters and assisted with other activities:

• Ms Zahra Cader, Coir • Ms. Sharmilla Aboosally, Gems and Jewelry • Mr. Lakna Paranwithana, Rubber • Mr. Alex Ponweera, Spices • Ms. Dilhara Goonewardena, Tea • Mr. Tuan Jamaldeen, ICT • Ms. Pri Ratnayake, Tourism • Mr. Preminda Fernando, Ceramics and Tourism

P R O G R A M R E V I E W 7

The specialists served as cluster coordinators under TCI and many continued to refer to them as such. Early on, clusters graduated from the TCI coordinator-assisted phase of assistance to assume responsibility for all their own administrative and association functions, freeing TCP’s program specialists to concentrate on technical assistance and other work. Three other expatriate advisers worked with the program specialists—Mr. Dyer, James Mudge, and Jagdesh Mirchandani. TCP also had nine support staff, including four drivers.

From July 2004 to October 31, 2007, TCP provided 13,730 person days of professional services. These included 2,775 work days from the four expatriate resident advisers: Mr. Varley (717 days), Mr. Liyanamana (754 days), Dr. Mudge (627 days), and Mr. Mirchandani (677 days) and 5,580 person days from the program specialists. This core group provided technical and management services including management of 5,375 person days of short-term technical assistance: 2,536 person-days from 58 expatriate specialists and 2,839 person-days from 41 local specialists. More than 100 persons worked directly for TCP as individual consultants. Many other Sri Lankans worked with TCP as part of groups contracted under purchase orders for services. The contributions of TCP’s local partners—private sector and government leaders and staff—were neither compensated for nor charged to the project budget, but TCP managers estimate that the contribution exceeded 10,000 person-days over the 40-month life of TCP.

MANAGEMENT Mr. Varley, who had been living in Colombo since May 2002 under TCI, managed TCP. Activities followed the program in the Task Order SOW as amended and specific activities were presented for approval to the CTO. Three staff in Nathan Associates’ home office supported the project at different times: Matt Lutkenhouse, Khalida Fazli, and Alex Bittner. The lead subcontractor, J.E. Austin Associates assisted with all aspects of program implementation, especially in identifying and recruiting specialists for clusters and on procedures for monitoring and evaluating impact. Mr. Liyanamana, Deputy COP, was Austin’s on-site staff and Austin’s home office also provided support, most recently through Jessica Reynolds. TCP also benefited from the technical insight and advice of Kevin Murphy, Austin’s President and designer of TCI.

During TCP, each industry cluster considered 10-15 strategic initiatives and each implemented 5-8. Not all were successful. Those that were tended to have significant results. The initiatives were typically identified by the industry itself in the form of a problem to be addressed. TCP advisers screened, critiqued, and refined identified problems and sometimes suggested or inspired the strategic initiatives. TCP assistance included other components such as policy reform, private-public dialogue, and workforce development, but its distinguishing feature was the focus on working with and through clusters in contrast to a focus on government agencies, firms (e.g. business development services), or sectors (e.g. agro-exports or SME finance).

ACHIEVEMENTS The purpose of TCP was to improve the competitiveness of Sri Lankan products and business practices in the global marketplace. As measured by changes in attitudes and improved export performance by firms and value chains as well as reforms in policy and procedures, TCP was

8 T C P F I N A L R E P O R T

successful. The sections below discuss project achievements, first those that can be relatively easily quantified, and then those that are less or non-quantifiable in the short-run.

Quantitative—Export Growth, Value Added, Cluster Incorporation The most significant and readily quantifiable achievements of the TCP were improved export performance, institutional developments by the eight clusters, and investment activity in the eight clusters.

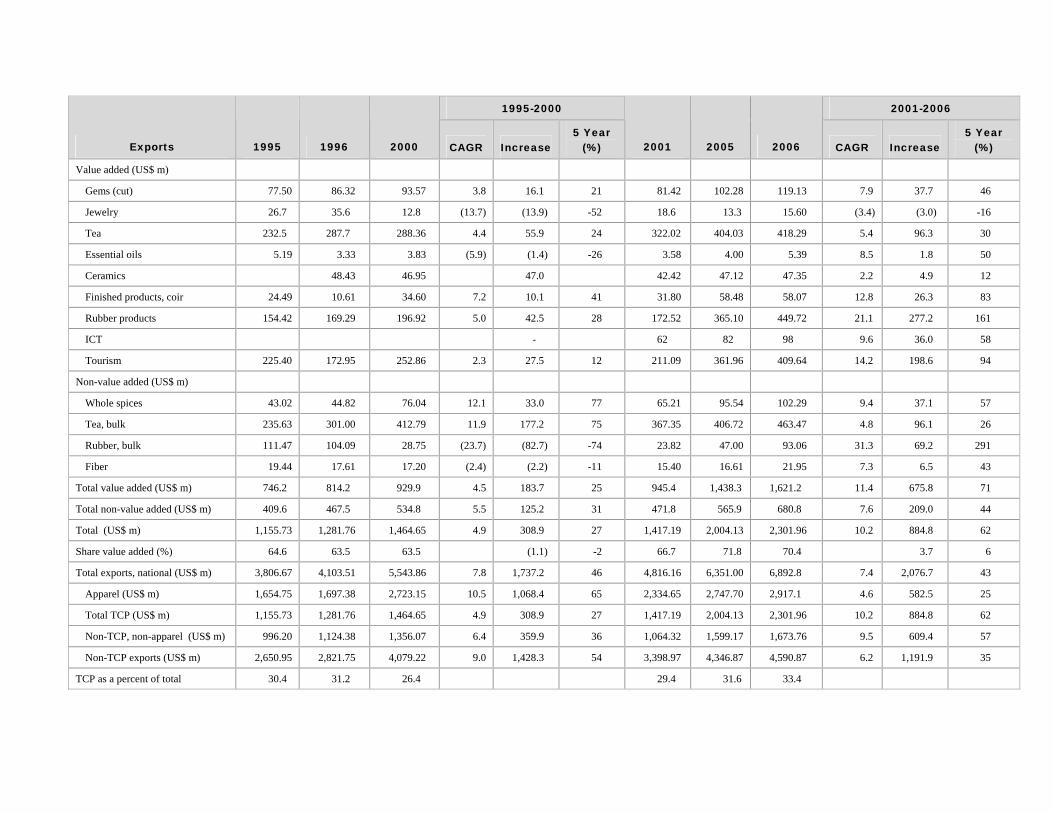

Export Performance As a group, the eight industry sectors with clusters participating in TCI and TCP significantly improved their export performance from 2000 to 2006—the last full year for which data are available. The best results measure, and the one used in TCP’s performance monitoring plan, was exports by sector using published statistics from the Central Bank of Sri Lanka (CBSL). (Those statistics are usually taken from Inland Revenue data based on export volumes and “cess” collections or industry reports).

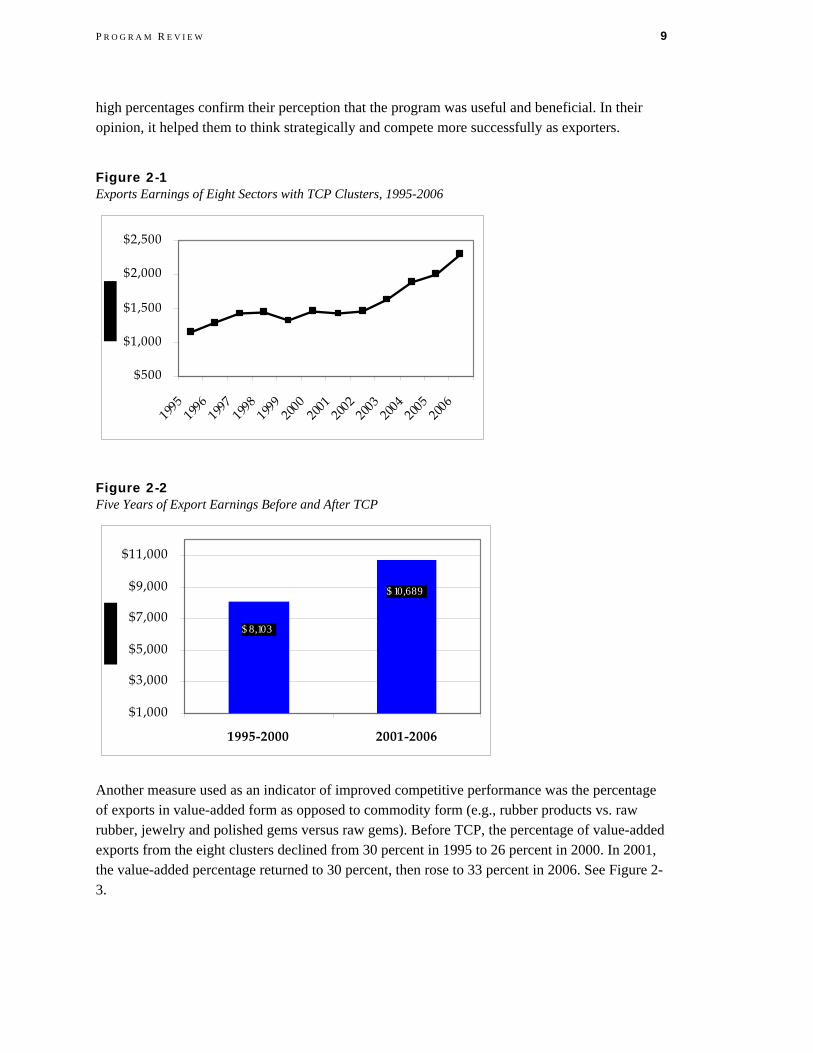

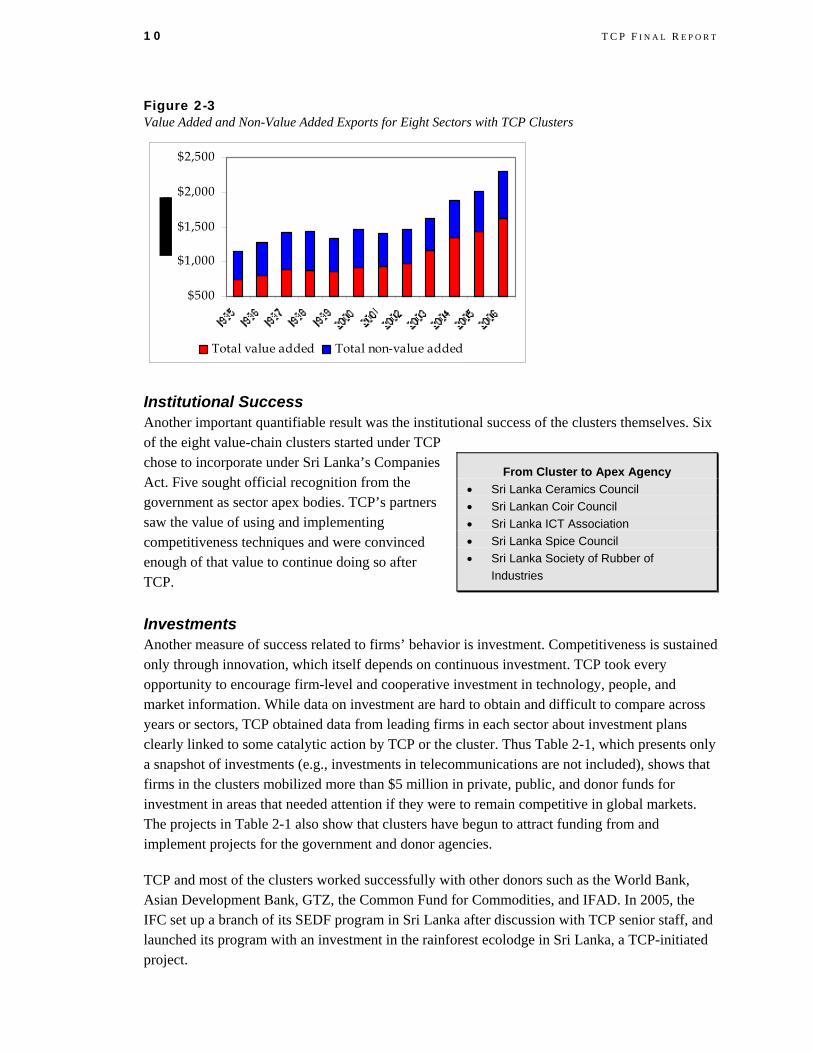

Prior to TCP, in the period from 1995 to 2000, exports from the eight industries increased at an average annual rate of 3.5 percent, from $1.16 billion in 1995 to US$1.46 billion in 2000. As TCP started in 2001, exports first declined to US$1.42 billion, but then rose from 2001 to 2006 at an average annual rate of 10.2 percent, nearly triple the previous pace. By 2006, exports had risen to US$2.3 billion. During the five years after the start of TCP, export earnings from the eight industries increased by US$885 million, roughly triple the US$309 million increase in earnings achieved by all eight sectors from 1995 to 2000. In short, the same industries generated US$550 million more in export earnings for Sri Lanka in 2006 than would have been predicted on the basis of the anemic growth trend of the period before TCP (see Figures 2-1 and 2-2).

A number of demand factors energized this rise in exports, including the growth of the Chinese and Indian economies, the Indo-Lanka free trade agreement, the 2002 cease-fire agreement in Sri Lanka, and generally good weather. But it was still the firms and value-chains in Sri Lanka that responded successfully to those factors against global competition while contending with such adversities as the tsunami of 2004 and nearly continual political instability from 2001 to 2007. TCP’s impact on sector-wide export performance was catalytic; global market conditions and private sector firms and value chains produced the “improved performance” result.

Attribution is an inexact science, even when aided by sophisticated economic modeling. TCP’s attribution methodology was direct and simple. In surveys carried out in 2006 and 2007, we asked Sri Lankan executives who understood the export markets and had worked with TCP to place a percentage value (including zero) on improved export performance they attribute to having worked with TCP and the clusters. The average attribution was 17 percent, ranging from 5.6 percent for tea to a 28.1 percent for rubber. TCP’s professionals had expected a response ranging from 1 to 7 percent. Setting quantitative accuracy aside for a moment makes it easier to appreciate two qualitative results for which the attribution percentages serve as a rough quantitative indicator. First, the attribution figures indicate that CEOs and senior managers who worked with TCP grasped that their export performance could be vastly improved even in competition with economies such as China and Vietnam and the developed world. Second, the

P R O G R A M R E V I E W 9

high percentages confirm their perception that the program was useful and beneficial. In their opinion, it helped them to think strategically and compete more successfully as exporters.

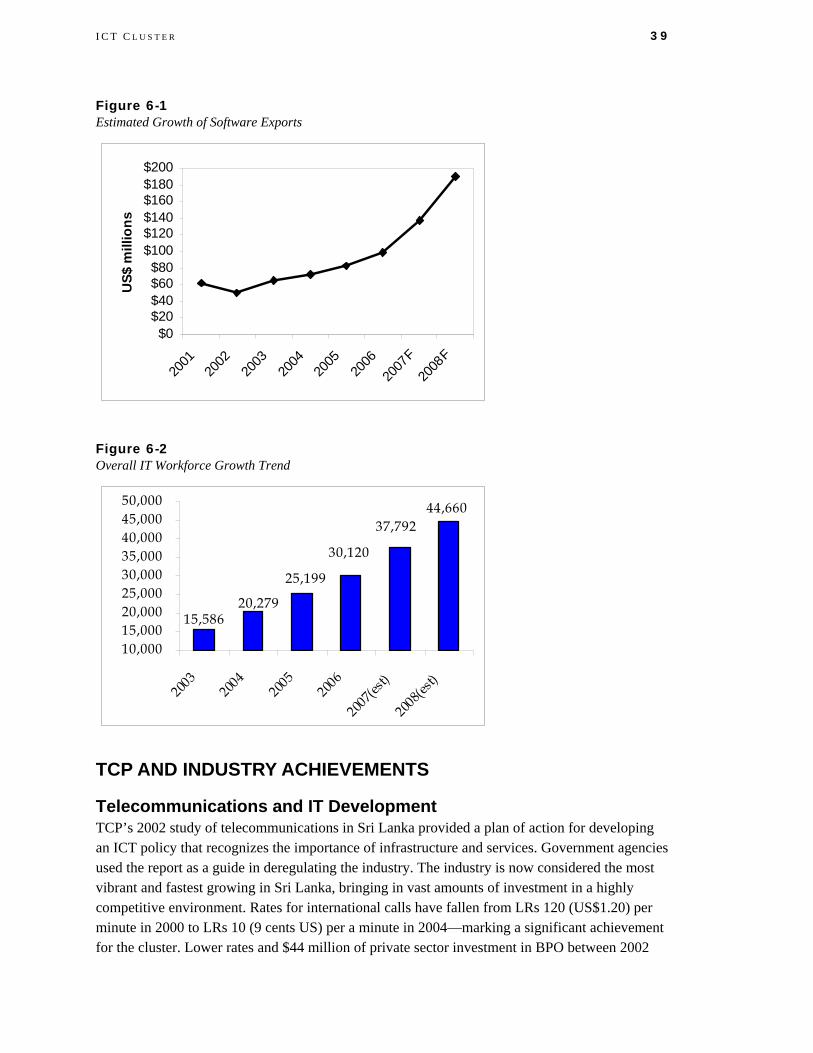

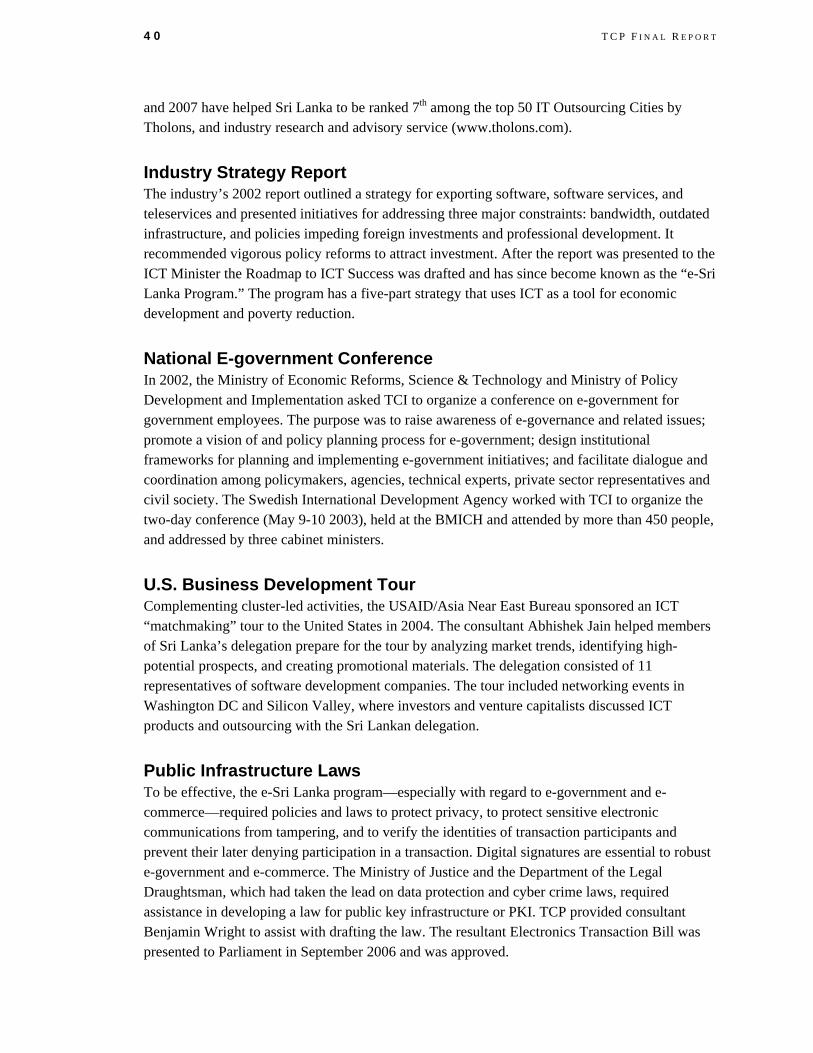

Figure 2-1 Exports Earnings of Eight Sectors with TCP Clusters, 1995-2006

$500

$1,000

$1,500

$2,000

$2,500

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Figure 2-2 Five Years of Export Earnings Before and After TCP

$ 10,689

$ 8,103

$1,000

$3,000

$5,000

$7,000

$9,000

$11,000

1995-2000 2001-2006

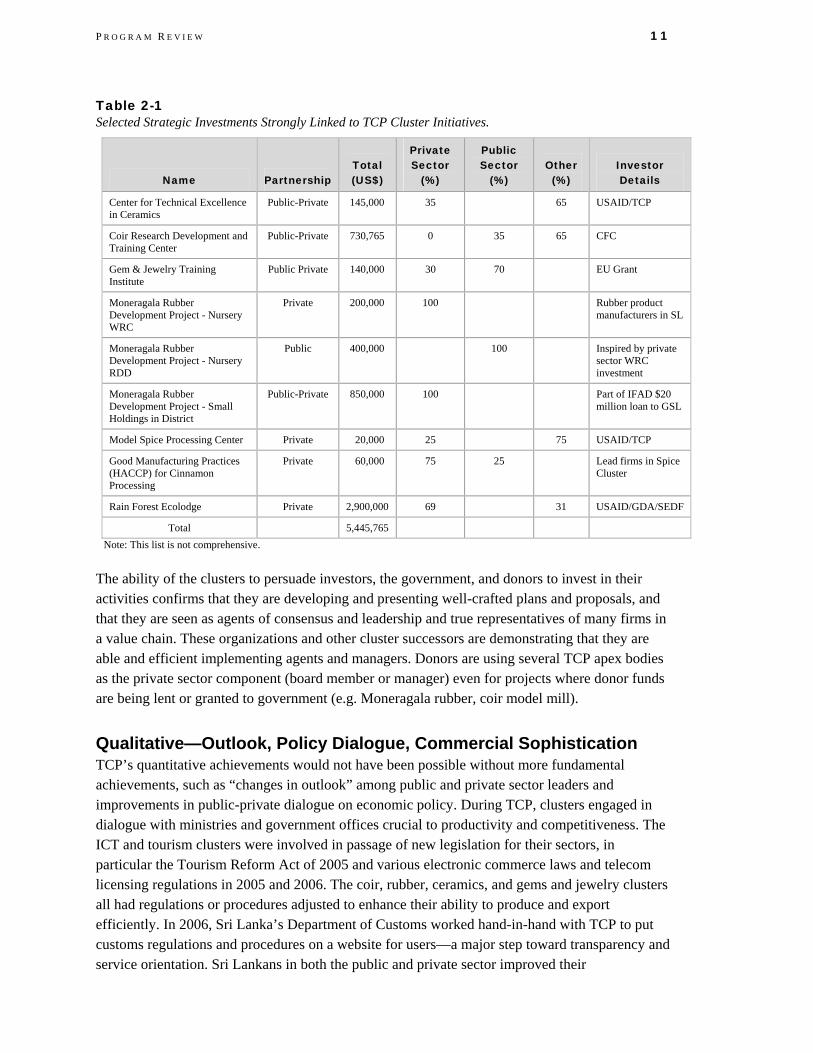

Another measure used as an indicator of improved competitive performance was the percentage of exports in value-added form as opposed to commodity form (e.g., rubber products vs. raw rubber, jewelry and polished gems versus raw gems). Before TCP, the percentage of value-added exports from the eight clusters declined from 30 percent in 1995 to 26 percent in 2000. In 2001, the value-added percentage returned to 30 percent, then rose to 33 percent in 2006. See Figure 2-3.

10 T C P F I N A L R E P O R T

Figure 2-3 Value Added and Non-Value Added Exports for Eight Sectors with TCP Clusters

$500

$1,000

$1,500

$2,000

$2,500

Total value added Total non-value added

Institutional Success Another important quantifiable result was the institutional success of the clusters themselves. Six of the eight value-chain clusters started under TCP chose to incorporate under Sri Lanka’s Companies Act. Five sought official recognition from the government as sector apex bodies. TCP’s partners saw the value of using and implementing competitiveness techniques and were convinced enough of that value to continue doing so after TCP.

From Cluster to Apex Agency • Sri Lanka Ceramics Council • Sri Lankan Coir Council • Sri Lanka ICT Association • Sri Lanka Spice Council • Sri Lanka Society of Rubber of

Industries

Investments Another measure of success related to firms’ behavior is investment. Competitiveness is sustained only through innovation, which itself depends on continuous investment. TCP took every opportunity to encourage firm-level and cooperative investment in technology, people, and market information. While data on investment are hard to obtain and difficult to compare across years or sectors, TCP obtained data from leading firms in each sector about investment plans clearly linked to some catalytic action by TCP or the cluster. Thus Table 2-1, which presents only a snapshot of investments (e.g., investments in telecommunications are not included), shows that firms in the clusters mobilized more than $5 million in private, public, and donor funds for investment in areas that needed attention if they were to remain competitive in global markets. The projects in Table 2-1 also show that clusters have begun to attract funding from and implement projects for the government and donor agencies.

TCP and most of the clusters worked successfully with other donors such as the World Bank, Asian Development Bank, GTZ, the Common Fund for Commodities, and IFAD. In 2005, the IFC set up a branch of its SEDF program in Sri Lanka after discussion with TCP senior staff, and launched its program with an investment in the rainforest ecolodge in Sri Lanka, a TCP-initiated project.

P R O G R A M R E V I E W 11

Table 2-1 Selected Strategic Investments Strongly Linked to TCP Cluster Initiatives.

Name Partnership Total (US$)

Private Sector

(%)

Public Sector

(%) Other (%)

Investor Details

Center for Technical Excellence in Ceramics

Public-Private 145,000 35 65 USAID/TCP

Coir Research Development and Training Center

Public-Private 730,765 0 35 65 CFC

Gem & Jewelry Training Institute

Public Private 140,000 30 70 EU Grant

Moneragala Rubber Development Project - Nursery WRC

Private 200,000 100 Rubber product manufacturers in SL

Moneragala Rubber Development Project - Nursery RDD

Public 400,000 100 Inspired by private sector WRC investment

Moneragala Rubber Development Project - Small Holdings in District

Public-Private 850,000 100 Part of IFAD $20 million loan to GSL

Model Spice Processing Center Private 20,000 25 75 USAID/TCP

Good Manufacturing Practices (HACCP) for Cinnamon Processing

Private 60,000 75 25 Lead firms in Spice Cluster

Rain Forest Ecolodge Private 2,900,000 69 31 USAID/GDA/SEDF

Total 5,445,765 Note: This list is not comprehensive.

The ability of the clusters to persuade investors, the government, and donors to invest in their activities confirms that they are developing and presenting well-crafted plans and proposals, and that they are seen as agents of consensus and leadership and true representatives of many firms in a value chain. These organizations and other cluster successors are demonstrating that they are able and efficient implementing agents and managers. Donors are using several TCP apex bodies as the private sector component (board member or manager) even for projects where donor funds are being lent or granted to government (e.g. Moneragala rubber, coir model mill).

Qualitative—Outlook, Policy Dialogue, Commercial Sophistication TCP’s quantitative achievements would not have been possible without more fundamental achievements, such as “changes in outlook” among public and private sector leaders and improvements in public-private dialogue on economic policy. During TCP, clusters engaged in dialogue with ministries and government offices crucial to productivity and competitiveness. The ICT and tourism clusters were involved in passage of new legislation for their sectors, in particular the Tourism Reform Act of 2005 and various electronic commerce laws and telecom licensing regulations in 2005 and 2006. The coir, rubber, ceramics, and gems and jewelry clusters all had regulations or procedures adjusted to enhance their ability to produce and export efficiently. In 2006, Sri Lanka’s Department of Customs worked hand-in-hand with TCP to put customs regulations and procedures on a website for users—a major step toward transparency and service orientation. Sri Lankans in both the public and private sector improved their

12 T C P F I N A L R E P O R T

understanding of how global markets work and how competitiveness determines success in global commerce, economic development, and job creation. Clusters and firms gained experience in devising strategies for adding value and competing in export markets.

Perhaps the most important qualitative impact was a fundamental change in the outlook or attitude of private sector leaders (Exhibit 2-1) about their own potential for competing. Industry executives learned how to strategically reposition themselves, to cooperate with other firms on mutually beneficial programs in training, research, marketing, standards, and even technology and product development. Owners and managers who once saw themselves as rival growers or traders of raw materials and commodities or services now recognize possibilities for adding or capturing value as part of a global value chain. Producers now take a far greater interest in understanding and meeting market demand. The spice cluster, for example, sponsored market research about what happens to shipments of cinnamon to Mexico and Central America, learning that “Ceylon Cinnamon” is added to coffee as well a bakery items and is prized for its health properties as well as its flavor. Firms grasp the value of cooperating to meet export standards and to offer quality, brands, and fashions that consumers prefer. Firms are also thinking strategically about investing in “up-market” opportunities and keeping more value Sri Lanka.

Exhibit 2-1 Changes in Private Sector and Public SectorOutlooks

TCP partner firms

• Know they have the ability to compete in global

markets even against countries like China and

India.

• Perceive themselves as important links in a global

value chain

• Explore how to capture value by raising quality and

innovating, not just increasing output

• Are willing to advise government on how policies

affect competitiveness.

• Understand the role of intellectual property and

branding in global markets and are investing in

brands, geographic indicators, and quality marks

(e.g., tea, spice, coir, gems and jewelry and IT).

• Are trying to capitalize on and enhance Sri Lanka’s

status as a South Asian trade hub.

• Understand Sri Lanka’s position as a source of

“lifestyle” products (apparel, tea, spices, ayurvedic

medicine, gems & jewelry, ceramics, specialty

tourism) and are committed to branding Sri Lanka

as supplier of quality goods that surpass

international standards for sustainability and ethical

manufacture.

The public sector now

• Understands the challenge of globalization and the

need for policies that promote competitiveness

• Is more willing to engage with private sector and

uses the “cluster” concept in constructing dialogue

fora with businesses

• Appreciates the leadership of the private sector in

economic growth

• Has interest in developing public-private

partnerships for competitiveness.

Although a “government knows best” legacy still dominates the economy, more leaders recognize the achievements of the private sector and the need for firms to be globally competitive. In 2002, when TCP helped the private sector publicize the World Economic Forum’s first issue of the Global Competitiveness Report (GCR) that included scores for Sri Lanka, an official in Sri

P R O G R A M R E V I E W 13

Lanka’s Central Bank dismissed the ratings as a “beauty contest” for businesses. Today, Sri Lanka’s Board of Investment monitors the GCR and five other international arbiters of competitiveness, analyzing the rankings (e.g. infrastructure, time to start a business, policy, labor regulations) for ways to improve Sri Lanka’s scores. H.E the President and some ministers frequently quote the GCR.

TCP worked directly with the government on customs reform, improving Colombo’s status as a regional transport hub, tourism websites, and English education. We also took every opportunity to discuss the GCR and other issues and specific policies with government leaders. But TCP worked mainly with and through industry clusters. Doing so enhanced not only the credibility of advice offered to the public sector, but also the credibility of private sector leaders as competitiveness advocates. By working with and through the clusters and by achieving the export growth and the value addition described earlier, TCP helped the private sector to recast the reform dialogue. Policies are now judged by the criteria of competitiveness and globalization; only a decade ago these forces were simply not taken into account.

Despite significant changes in outlook, Sri Lanka cannot yet be considered a successful emerging economy. It remains a small island economy with many government and commercial traditions rooted in colonialism and a post-independence embrace of socialism and state management. Its development depends to a large extent on the continued emergence of a more vigorous private sector—one that that can grow quickly, creating jobs in new sectors and improving productivity in the agricultural sector. Many Sri Lankans still embrace the traditional view that future jobs will and should be in the agricultural sector or provided by the government. TCP played a vital role in equipping private and public sector leaders with the knowledge and tools needed to change this view. That will be the most important legacy TCP can lay some claim to.

The sections that follow discuss specific TCP’s achievements and activities to improve competitiveness in each value chain cluster and the cross-cutting activities that will help support Sri Lanka’s reemerging private sector.

3. Ceramics Cluster Sri Lanka’s modern ceramics industry was originally the result of significant tax and investment incentives provided by the government in the 1970s. Over time, the high cost of imported inputs and fuel and inefficient production that made poor use of both compromised the industry’s competitiveness. In addition, Sri Lankan companies were unable to enter into high tech ceramics product lines because the island lacked a facility to research and test new products and the workforce to engage in these activities.

In 2001, with the assistance of TCI, the ceramics industry formed a cluster to devise and implement a unified, industry-wide strategy to enhance sector competitiveness. On November 19, 2003, the Sri Lanka Ceramics Council (SLACC) was incorporated under the Companies Act and has since been operating as the sector’s apex body under the aegis of the Ceylon Chamber of Commerce, the official secretariat. The council’s 25 members represent manufacturing firms (ceramics, cement, glass, and electronics), raw material and energy suppliers, government agencies, and academic and R&D institutions.

Members of the council’s Board of Directors in 2007 include the President, Mr. Dayasiri Warnakulasooriya, of Midaya Ceramics Pvt. Ltd.; the Vice President, Mr. Mahendra Jayasekere of Lanka Tiles Ltd.; the Treasurer, Mr Nimal Perera, of Noritake Lanka Porcelain Ltd.; the Secretary, Mr. Niranjan Jawawickrema, of Lanka Walltiles Ltd.; and the Assistant Secretary, Mr. J. Atuapattu of Royal Ceramics. Mr. Sunil G. Wijesinha, Chairman of Dankotuwa Porcelain Limited and former president of the council holds an honorary position on the board. Membership dues, symposia, and training programs provide funding for the council. An annual report with an audited financial statement is issued to members at the annual general meeting. A part-time program coordinator assists the council with administrative and program activities.

Sri Lanka Ceramics Council President, Dayasiri Warnakulasooriya Contact, Lakmali Udugampola Ceylon Chamber of Commerce Building No 50 Nawam Mawatha, Colombo 2 +941 2423476 [email protected] www.ceramics.lk

Membership has increased 50 percent since 2003. SLACC’s strategy for improving sector competitiveness has resulted in the branding of Sri Lankan ceramics products, the brokering of an agreement on fuel prices, the creation of a center of technical excellence, and workforce upgrades. The center of excellence, operating on a fee-for-service basis, helps companies meet immediate requirements for testing and research and development. The SLACC conducts an international ceramics symposium on a bi-annual basis. Several international manufacturing and supply companies have participated in this program.

16 T C P F I N A L R E P O R T

The SLACC is also a policy focal point. Large exporters and SMEs advocate their policy issues through the cluster. Several issues—such as raw material taxes, monopoly fuel prices, lack of consistent and quality electricity, problems in obtaining a mining licenses, and transportation of clay—have been resolved through dialogue between the SLACC and government ministries.

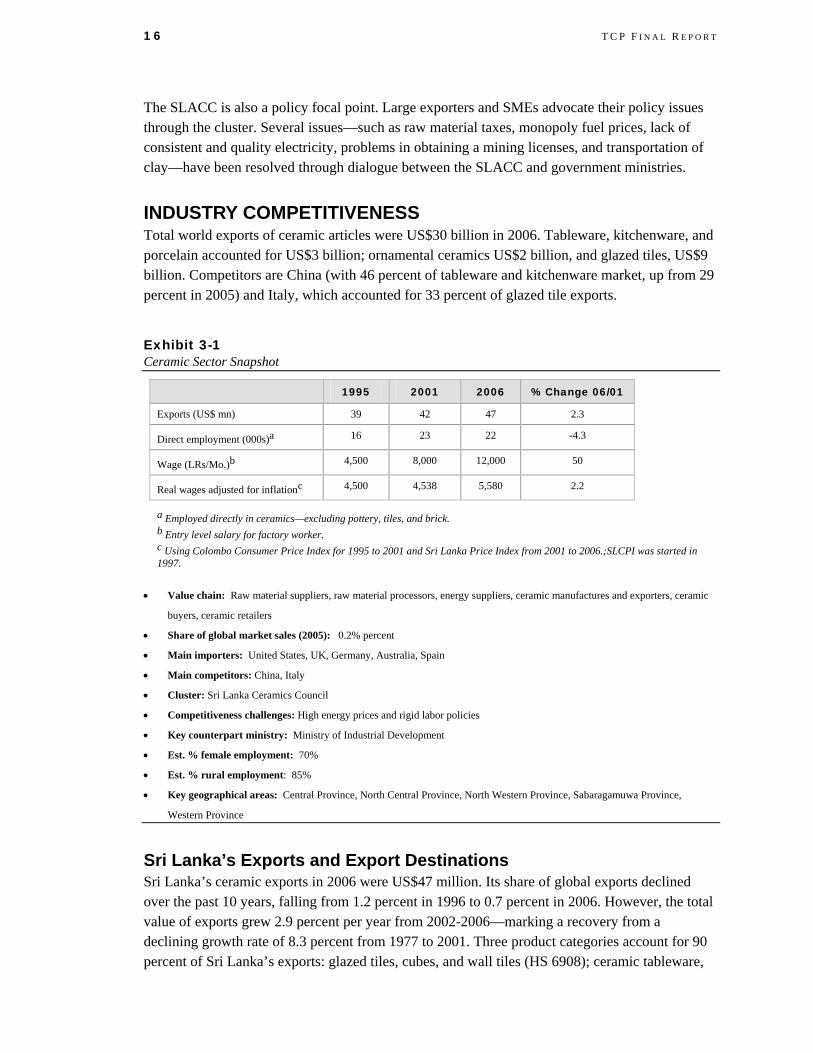

INDUSTRY COMPETITIVENESS Total world exports of ceramic articles were US$30 billion in 2006. Tableware, kitchenware, and porcelain accounted for US$3 billion; ornamental ceramics US$2 billion, and glazed tiles, US$9 billion. Competitors are China (with 46 percent of tableware and kitchenware market, up from 29 percent in 2005) and Italy, which accounted for 33 percent of glazed tile exports.

Exhibit 3-1 Ceramic Sector Snapshot

1995 2001 2006 % Change 06/01

Exports (US$ mn) 39 42 47 2.3

Direct employment (000s)a 16 23 22 -4.3

Wage (LRs/Mo.)b 4,500 8,000 12,000 50

Real wages adjusted for inflationc 4,500 4,538 5,580 2.2

a Employed directly in ceramics—excluding pottery, tiles, and brick. b Entry level salary for factory worker. c Using Colombo Consumer Price Index for 1995 to 2001 and Sri Lanka Price Index from 2001 to 2006.;SLCPI was started in 1997.

• Value chain: Raw material suppliers, raw material processors, energy suppliers, ceramic manufactures and exporters, ceramic

buyers, ceramic retailers

• Share of global market sales (2005): 0.2% percent

• Main importers: United States, UK, Germany, Australia, Spain

• Main competitors: China, Italy

• Cluster: Sri Lanka Ceramics Council

• Competitiveness challenges: High energy prices and rigid labor policies

• Key counterpart ministry: Ministry of Industrial Development

• Est. % female employment: 70%

• Est. % rural employment: 85%

• Key geographical areas: Central Province, North Central Province, North Western Province, Sabaragamuwa Province,

Western Province

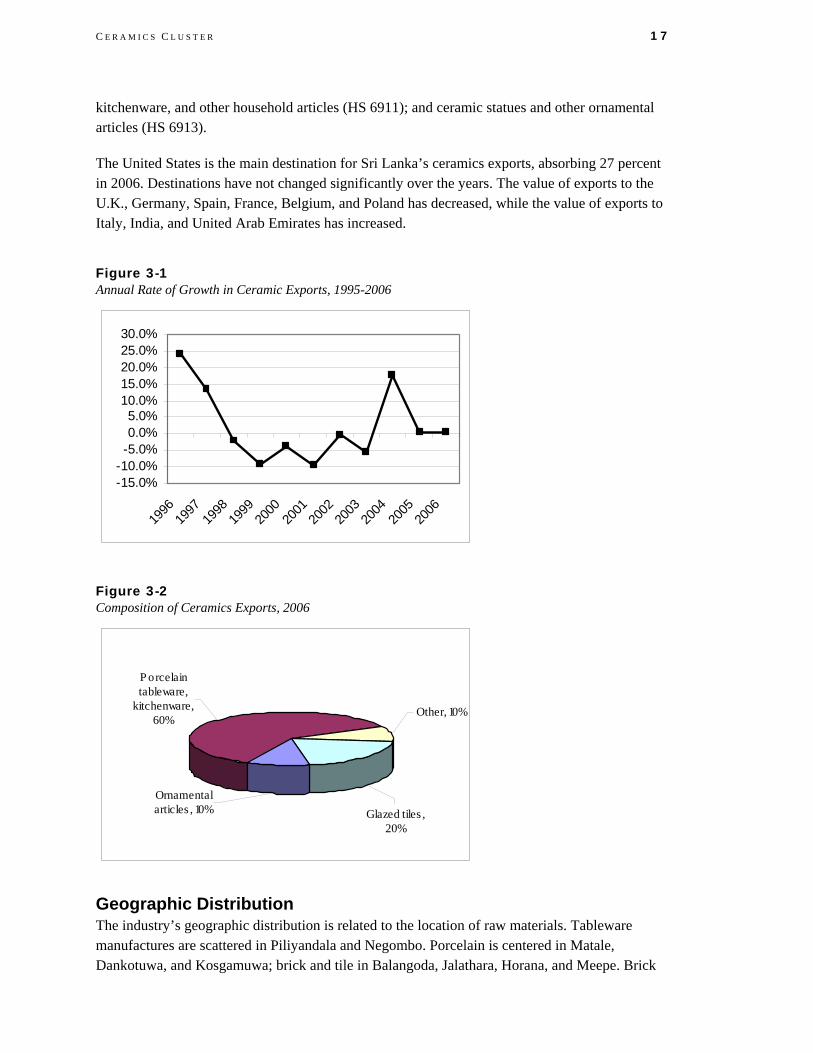

Sri Lanka’s Exports and Export Destinations Sri Lanka’s ceramic exports in 2006 were US$47 million. Its share of global exports declined over the past 10 years, falling from 1.2 percent in 1996 to 0.7 percent in 2006. However, the total value of exports grew 2.9 percent per year from 2002-2006—marking a recovery from a declining growth rate of 8.3 percent from 1977 to 2001. Three product categories account for 90 percent of Sri Lanka’s exports: glazed tiles, cubes, and wall tiles (HS 6908); ceramic tableware,

C E R A M I C S C L U S T E R 17

kitchenware, and other household articles (HS 6911); and ceramic statues and other ornamental articles (HS 6913).

The United States is the main destination for Sri Lanka’s ceramics exports, absorbing 27 percent in 2006. Destinations have not changed significantly over the years. The value of exports to the U.K., Germany, Spain, France, Belgium, and Poland has decreased, while the value of exports to Italy, India, and United Arab Emirates has increased.

Figure 3-1 Annual Rate of Growth in Ceramic Exports, 1995-2006

-15.0%-10.0%-5.0%0.0%5.0%

10.0%15.0%20.0%25.0%30.0%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

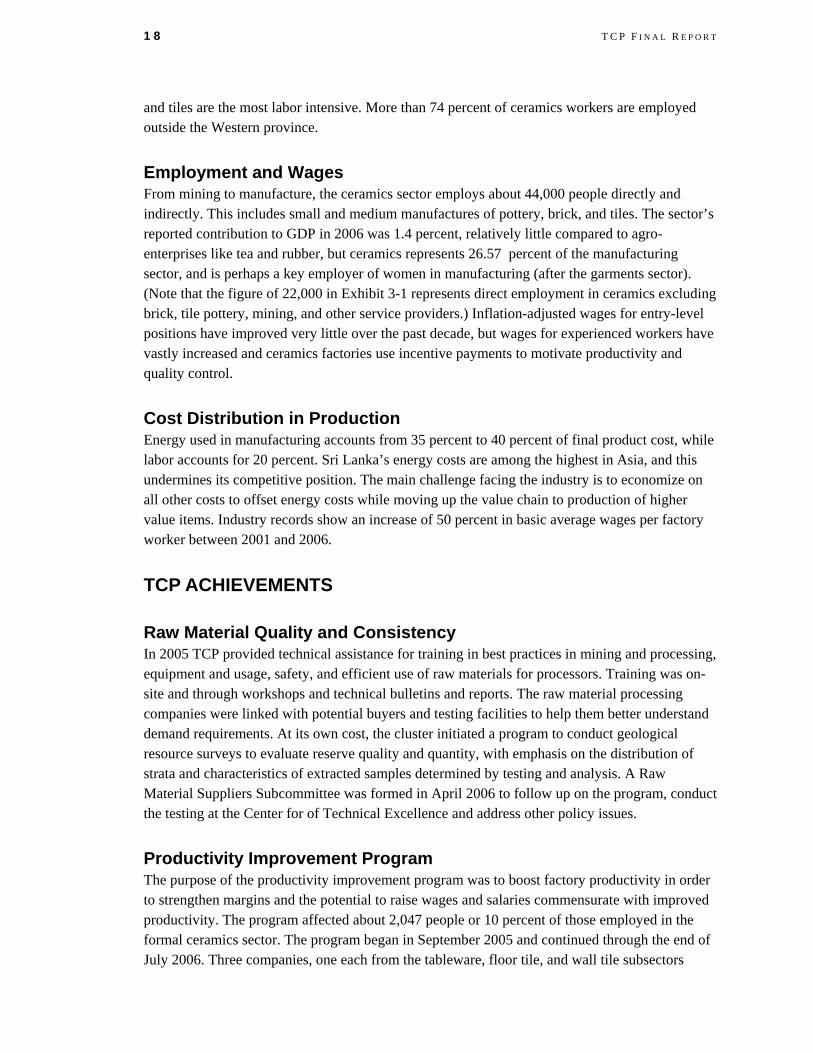

Figure 3-2 Composition of Ceramics Exports, 2006

Other, 10%

Glazed tiles , 20%

Ornamental articles , 10%

P orcelain tableware,

kitchenware, 60%

Geographic Distribution The industry’s geographic distribution is related to the location of raw materials. Tableware manufactures are scattered in Piliyandala and Negombo. Porcelain is centered in Matale, Dankotuwa, and Kosgamuwa; brick and tile in Balangoda, Jalathara, Horana, and Meepe. Brick

18 T C P F I N A L R E P O R T

and tiles are the most labor intensive. More than 74 percent of ceramics workers are employed outside the Western province.

Employment and Wages From mining to manufacture, the ceramics sector employs about 44,000 people directly and indirectly. This includes small and medium manufactures of pottery, brick, and tiles. The sector’s reported contribution to GDP in 2006 was 1.4 percent, relatively little compared to agro-enterprises like tea and rubber, but ceramics represents 26.57 percent of the manufacturing sector, and is perhaps a key employer of women in manufacturing (after the garments sector). (Note that the figure of 22,000 in Exhibit 3-1 represents direct employment in ceramics excluding brick, tile pottery, mining, and other service providers.) Inflation-adjusted wages for entry-level positions have improved very little over the past decade, but wages for experienced workers have vastly increased and ceramics factories use incentive payments to motivate productivity and quality control.

Cost Distribution in Production Energy used in manufacturing accounts from 35 percent to 40 percent of final product cost, while labor accounts for 20 percent. Sri Lanka’s energy costs are among the highest in Asia, and this undermines its competitive position. The main challenge facing the industry is to economize on all other costs to offset energy costs while moving up the value chain to production of higher value items. Industry records show an increase of 50 percent in basic average wages per factory worker between 2001 and 2006.

TCP ACHIEVEMENTS

Raw Material Quality and Consistency In 2005 TCP provided technical assistance for training in best practices in mining and processing, equipment and usage, safety, and efficient use of raw materials for processors. Training was on-site and through workshops and technical bulletins and reports. The raw material processing companies were linked with potential buyers and testing facilities to help them better understand demand requirements. At its own cost, the cluster initiated a program to conduct geological resource surveys to evaluate reserve quality and quantity, with emphasis on the distribution of strata and characteristics of extracted samples determined by testing and analysis. A Raw Material Suppliers Subcommittee was formed in April 2006 to follow up on the program, conduct the testing at the Center for of Technical Excellence and address other policy issues.

Productivity Improvement Program The purpose of the productivity improvement program was to boost factory productivity in order to strengthen margins and the potential to raise wages and salaries commensurate with improved productivity. The program affected about 2,047 people or 10 percent of those employed in the formal ceramics sector. The program began in September 2005 and continued through the end of July 2006. Three companies, one each from the tableware, floor tile, and wall tile subsectors

C E R A M I C S C L U S T E R 19

participated on a cost-share basis. The total cost was US$32,235 of which TCP contributed US$24,044 as a grant to the cluster. Participants covered the balance.

For tableware, the program had modules on strategic and business planning and marketing; for wall and floor tile, it offered modules on continuous improvement and quality, productivity and work study. CEOs developed baseline indicators and TCP consultants implemented the modules. A local firm, 3rd Wave, developed and implemented the continuous improvement program. After six months, factories experienced an average 2 percent increase in productivity, which equates to an estimated annual savings of US$300,000.

Ceramics Center of Technical Excellence In partnership with the Industrial Technology Institute (ITI), SLACC set up the Center of Technical Excellence for Ceramics in Sri Lanka with US$125,000. Open since April 2007, the center facilitates testing and R&D. Universities engaged in the sector are also part of the center. TCP contributed three pieces of testing equipment and books valued at US$76,000. Industry contributed cash and equipment to cover the balance. TCP also provided input on setting up the center and established contacts between the center and a leading U.S. ceramics institution, the Kazuo Inamori School of Engineering, New York State College of Ceramics at Alfred University.

Figure 3-3 CENTEC Opening

In response to skyrocketing energy costs (ceramics are twice fired at extremely high temperatures), SLACC launched several R&D programs within six months of the center’s opening. The total value of these projects is US$95,000. Research is focusing on energy usage, raw material improvement, and red clay. Making the firing process more energy efficient will reduce production costs and improve the competitiveness of the industry significantly. Initial lab tests have been positive. The success of the center, especially as a public–private partnership, led

20 T C P F I N A L R E P O R T

the Ministry of Industrial Development to urge other industries to replicate the center of excellence concept.

CLUSTER ACHEIVEMENTS

Long-term Pricing Agreement for Liquid Petroleum Gasoline In 2002, the cluster was instrumental in negotiating transparent pricing agreement formulas with Shell Gas. Participating companies received LPG at global market prices with a specified discount for entering into a long-term contract with Shell Lanka. Participants estimate that their annual savings from 2002 through 2006 averaged approximately 5 percent of their pre-contract LPG costs.

Workforce Development Program The council, with technical assistance from TCP and the University of Moratuwa, developed a six-month industry placement program starting in 2005. The purpose was to place third-year materials engineering students in the industry so they could acquire direct experience. After its second session, the program was completely funded by industry. Graduates who participated in the program found jobs more quickly and at higher salaries than those who did not. The university is keen to replicate the program for other industries.

Raw Material Mining Policies The council’s raw material suppliers subcommittee, with support from the Ministry of Industrial Development, pursued an amendment to regulations governing ball clay mining in abandoned paddy fields. Under Agrarian Development Act regulations, cluster firms were forced to either import ball clay—an important raw material—or obtain it from illicit mining. The subcommittee worked with the Ministry of Agrarian Services and the Geographical Services and Mining Bureau (GSMB) to identify problems in obtaining licenses to mine in abandoned paddy lands. Issues resolved included determinations as to which agencies would give approvals for licenses and how land would be refilled and restored after being mined for ball clay. The number of agencies involved in issuing licenses was reduced from 15 to 5 in April 2006.

Renewable Energy The monthly rise in energy prices has driven the ceramics industry to explore alternative energy sources. While significant research on ceramics firing is underway, the cluster has taken the lead in introducing renewable energy to supplement gas and kerosene. In the autumn of 2007, the council began discussions with the Ministry of Science and Technology and potential investors to explore using wood chips made from glyricidia, a renewable energy source. At prevailing prices, the cost of generating heat from glyricidia is 25 percent of the cost of generating the same amount of heat from petroleum fuels. Petroleum fuels are still widely used because glyricidia is not available in sufficient quantities. The ceramics industry consumes 37,000 tons of petroleum fuel, accounting for 14 percent of petroleum fuels consumed by the island’s entire industrial sector. Two leading companies plan to invest more than US$100,000 to test new glyricidia technology.

C E R A M I C S C L U S T E R 21

RURAL IMPACT The ceramics industry employs more than 44,000 persons, including many small and medium manufacturers of pottery, brick, and tiles as well as informal laborers. Seventy-four percent work outside the Western province, and a large percentage are women. Without TCP assistance, it is unlikely that the price negotiations and cooperative industry research and development would have taken place and the industry’s competitive position would have continued to erode. Now the industry is well positioned for growth. In linking rural miners and manufactures to the ceramics center of excellence and in helping the cluster increase exports, TCP had a direct impact on rural areas. (More than 95 percent of cluster members are outside of the Western province.) SLACC is contemplating a program with the Ministry of Industrial Development to provide technical and management assistance to SMEs involved in ceramics.

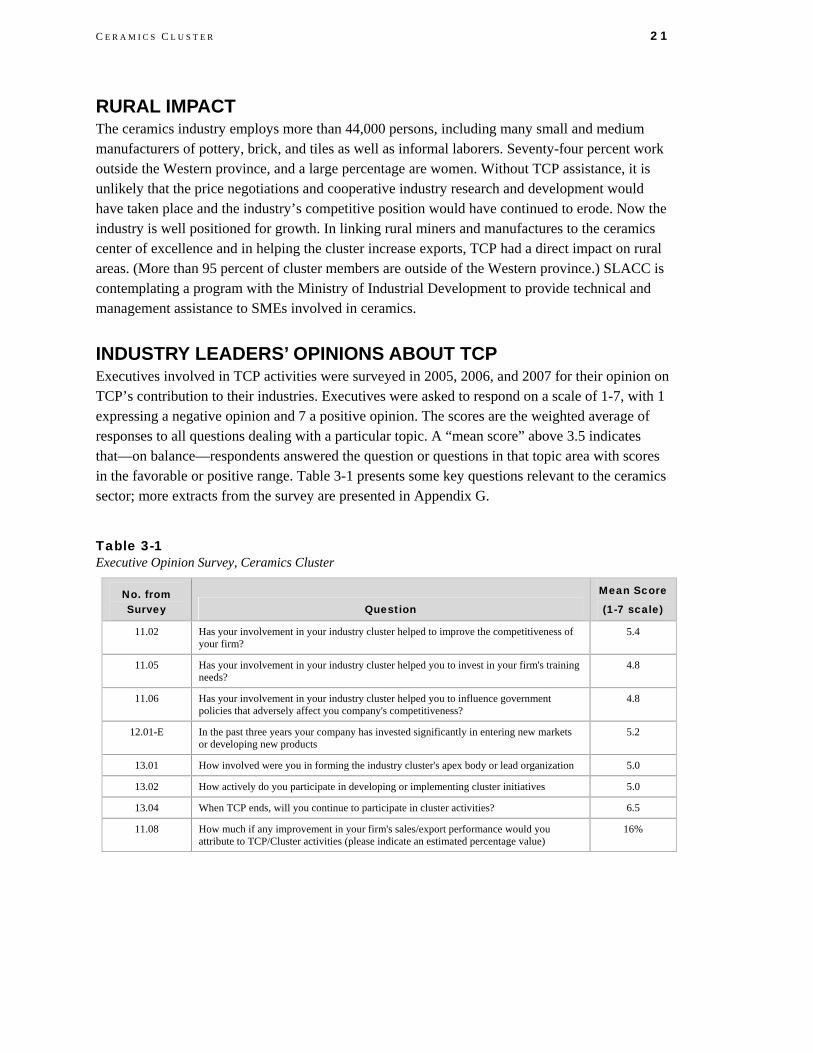

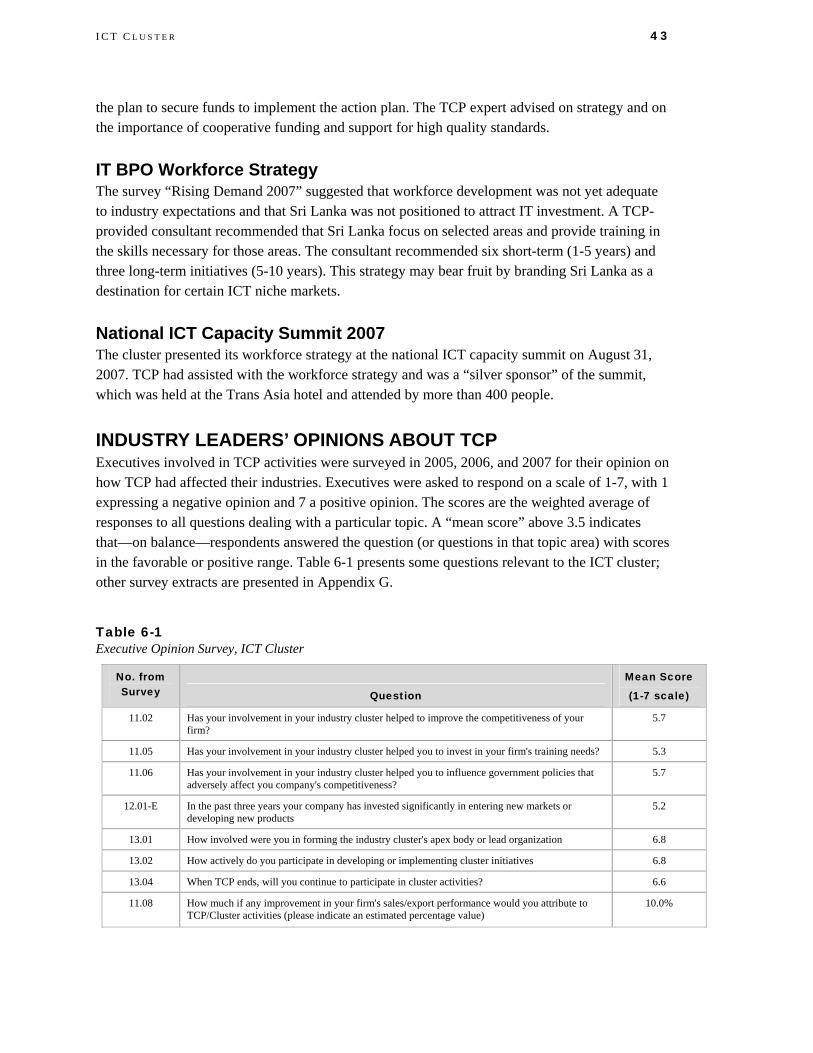

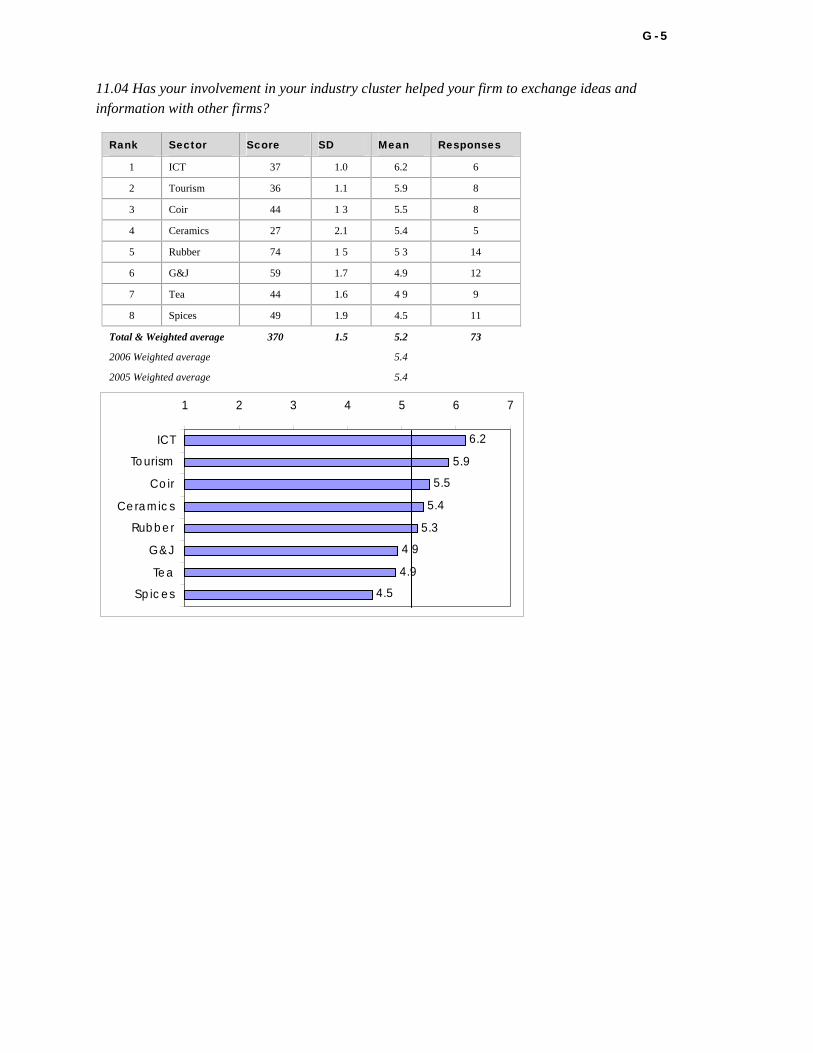

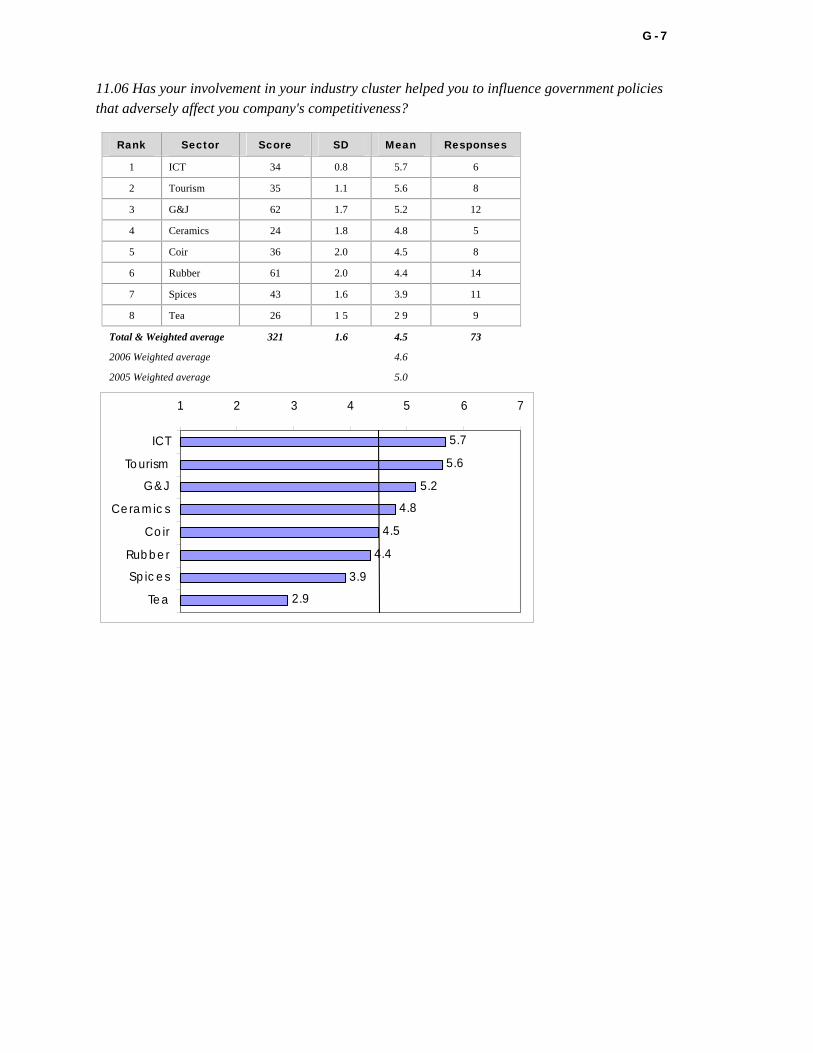

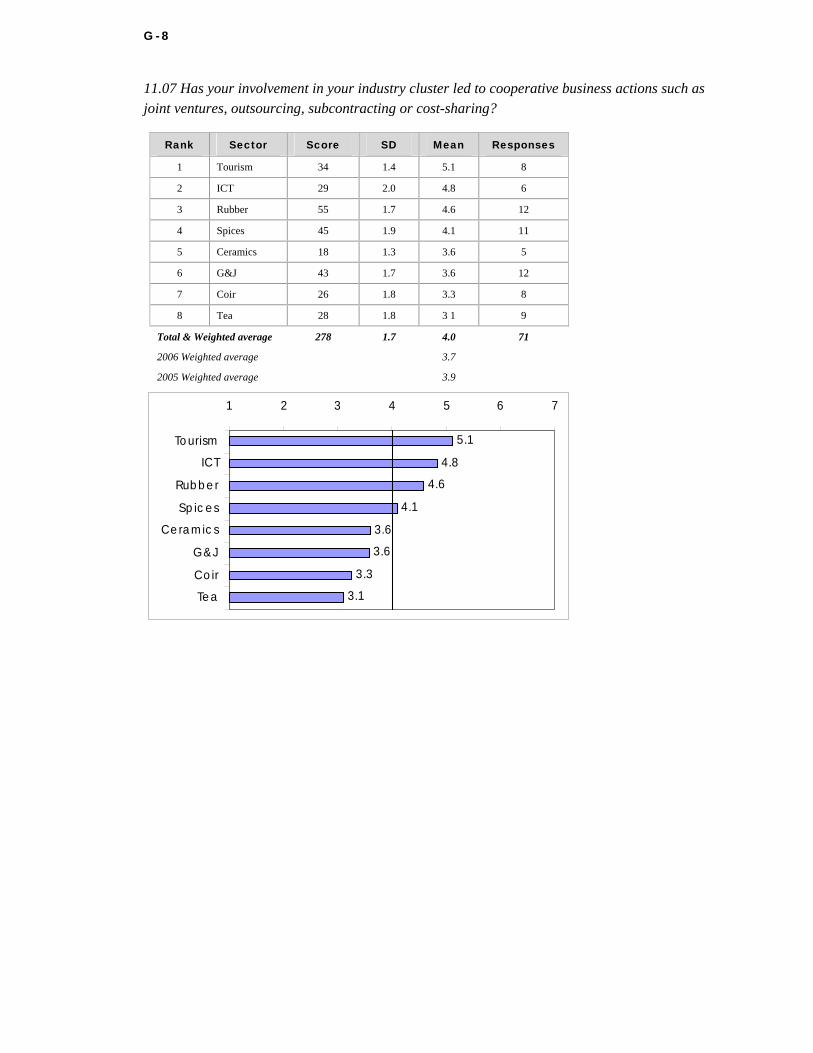

INDUSTRY LEADERS’ OPINIONS ABOUT TCP Executives involved in TCP activities were surveyed in 2005, 2006, and 2007 for their opinion on TCP’s contribution to their industries. Executives were asked to respond on a scale of 1-7, with 1 expressing a negative opinion and 7 a positive opinion. The scores are the weighted average of responses to all questions dealing with a particular topic. A “mean score” above 3.5 indicates that—on balance—respondents answered the question or questions in that topic area with scores in the favorable or positive range. Table 3-1 presents some key questions relevant to the ceramics sector; more extracts from the survey are presented in Appendix G.

Table 3-1 Executive Opinion Survey, Ceramics Cluster

No. from Survey Question

Mean Score

(1-7 scale)

11.02 Has your involvement in your industry cluster helped to improve the competitiveness of your firm?

5.4

11.05 Has your involvement in your industry cluster helped you to invest in your firm's training needs?

4.8

11.06 Has your involvement in your industry cluster helped you to influence government policies that adversely affect you company's competitiveness?

4.8

12.01-E In the past three years your company has invested significantly in entering new markets or developing new products

5.2

13.01 How involved were you in forming the industry cluster's apex body or lead organization 5.0

13.02 How actively do you participate in developing or implementing cluster initiatives 5.0

13.04 When TCP ends, will you continue to participate in cluster activities? 6.5

11.08 How much if any improvement in your firm's sales/export performance would you attribute to TCP/Cluster activities (please indicate an estimated percentage value)

16%

4. Coir Cluster The Coir Council International (CCI) was incorporated under the Companies Act on November 19, 2003, as the apex body of the coir industry. CCI’s membership is a broad cross-section of the coir industry representing growers, millers, manufacturers, and exporters. The 22-member board includes representatives from the Ministry of Industries, Coconut Development Authority (CDA), Coconut Research Institute (CRI), and the Industrial Technology Institute (ITI). CCI has a chairman, an executive committee, and project subcommittees for the model mill, erosion control products, promotional activity, and tsunami rehabilitation.

Coir Council International Chairman, Mr. Indrajith Piyasena c/o Hayley’s Exports Ltd 138/4, Minuwangoda Road, Ekala, Ja-Ela +94112232475

On August 15, 2005, CCI convened a board meeting to agree on changes to its memorandum and articles of association. An executive committee with all powers of the board was appointed to serve between board meetings. To ensure transparency and build confidence among stakeholders, a representative from each of the five member associations was appointed to the committee. Members unanimously agreed to increase dues from LRs 100 to LRs 5,000 per association. Officials of the committee are Chairman Mr. Piyasena; Vice Chairman Mr. Wimalasiri Herath; Secretary Mr. Shalinda Perera; and Treasurer Mr. Murtaza Jafferjee.

Because CCI has been recognized by the government as the private sector apex body for the coir industry, the CDA works directly with it in implementing projects and addressing policy issues. One result of this partnership is that more miller associations in coconut growing areas (the “coconut triangle”) and in the south are working with the council to implement programs. One joint initiative is the setting of standards for coir fiber recognized by the Sri Lanka Standards Institute, industry, and foreign buyers.

Segments of the coir industry in Sri Lanka function as a cottage industry, where women are able to spin coir fiber into yarn in their homes to generate additional income. Increasing competitiveness while preserving this vital link in the supply chain required the industry to develop standards and quality improvement programs, and to research and adopt technology to pursue higher value added technological applications and composites using coir.

INDUSTRY COMPETITIVENESS South East Asia accounts for almost all coir produced in the world. Coir exports from the region amounted to 195,000MT in 2004, with Sri Lanka and India accounting for 32 percent and 40

24 T C P F I N A L R E P O R T

percent, respectively. Coir exports rose by 66 percent in volume from 2000 to 2004 because of growing demand for mattress and twisted fiber in China. This has encouraged Thailand and Vietnam to emerge as producers and exporters. Export volumes from Thailand grew 500 percent, going from 7,255 MT in 2000 to 44,625 MT in 2004. In the same period, exports from Sri Lanka grew only 18 percent in volume.

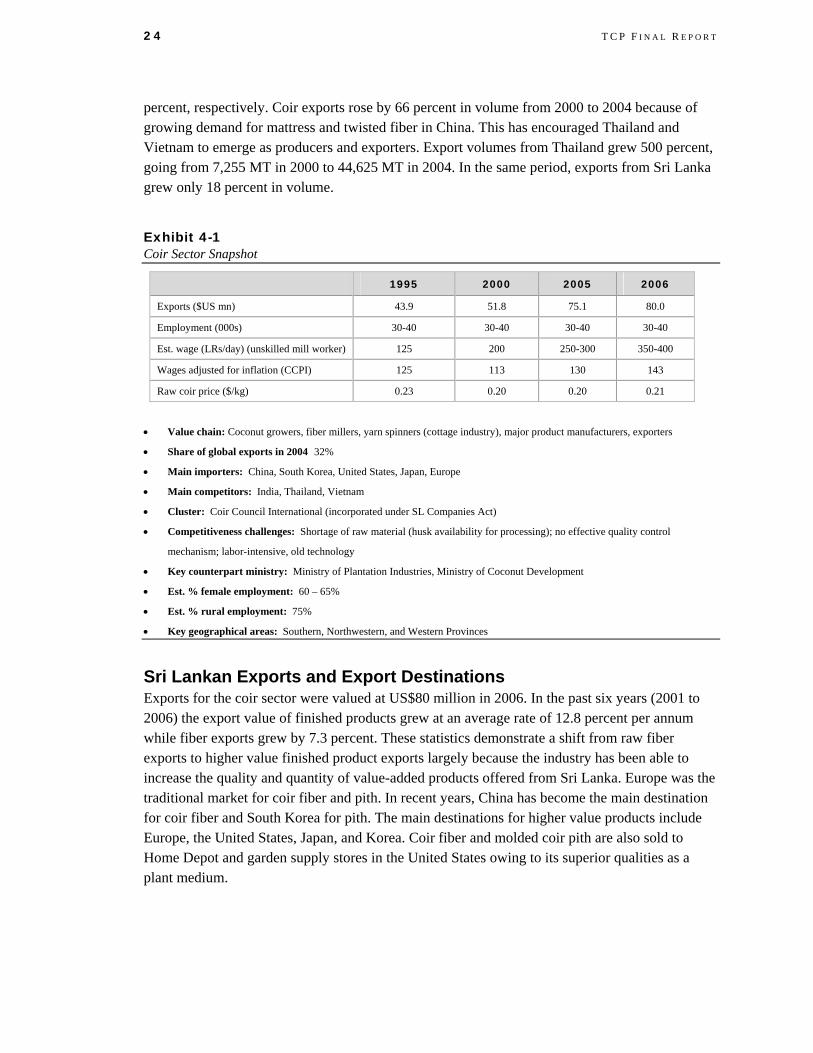

Exhibit 4-1 Coir Sector Snapshot

1995 2000 2005 2006

Exports ($US mn) 43.9 51.8 75.1 80.0

Employment (000s) 30-40 30-40 30-40 30-40

Est. wage (LRs/day) (unskilled mill worker) 125 200 250-300 350-400

Wages adjusted for inflation (CCPI) 125 113 130 143

Raw coir price ($/kg) 0.23 0.20 0.20 0.21

• Value chain: Coconut growers, fiber millers, yarn spinners (cottage industry), major product manufacturers, exporters

• Share of global exports in 2004 32%

• Main importers: China, South Korea, United States, Japan, Europe

• Main competitors: India, Thailand, Vietnam

• Cluster: Coir Council International (incorporated under SL Companies Act)

• Competitiveness challenges: Shortage of raw material (husk availability for processing); no effective quality control

mechanism; labor-intensive, old technology

• Key counterpart ministry: Ministry of Plantation Industries, Ministry of Coconut Development

• Est. % female employment: 60 – 65%

• Est. % rural employment: 75%

• Key geographical areas: Southern, Northwestern, and Western Provinces

Sri Lankan Exports and Export Destinations Exports for the coir sector were valued at US$80 million in 2006. In the past six years (2001 to 2006) the export value of finished products grew at an average rate of 12.8 percent per annum while fiber exports grew by 7.3 percent. These statistics demonstrate a shift from raw fiber exports to higher value finished product exports largely because the industry has been able to increase the quality and quantity of value-added products offered from Sri Lanka. Europe was the traditional market for coir fiber and pith. In recent years, China has become the main destination for coir fiber and South Korea for pith. The main destinations for higher value products include Europe, the United States, Japan, and Korea. Coir fiber and molded coir pith are also sold to Home Depot and garden supply stores in the United States owing to its superior qualities as a plant medium.

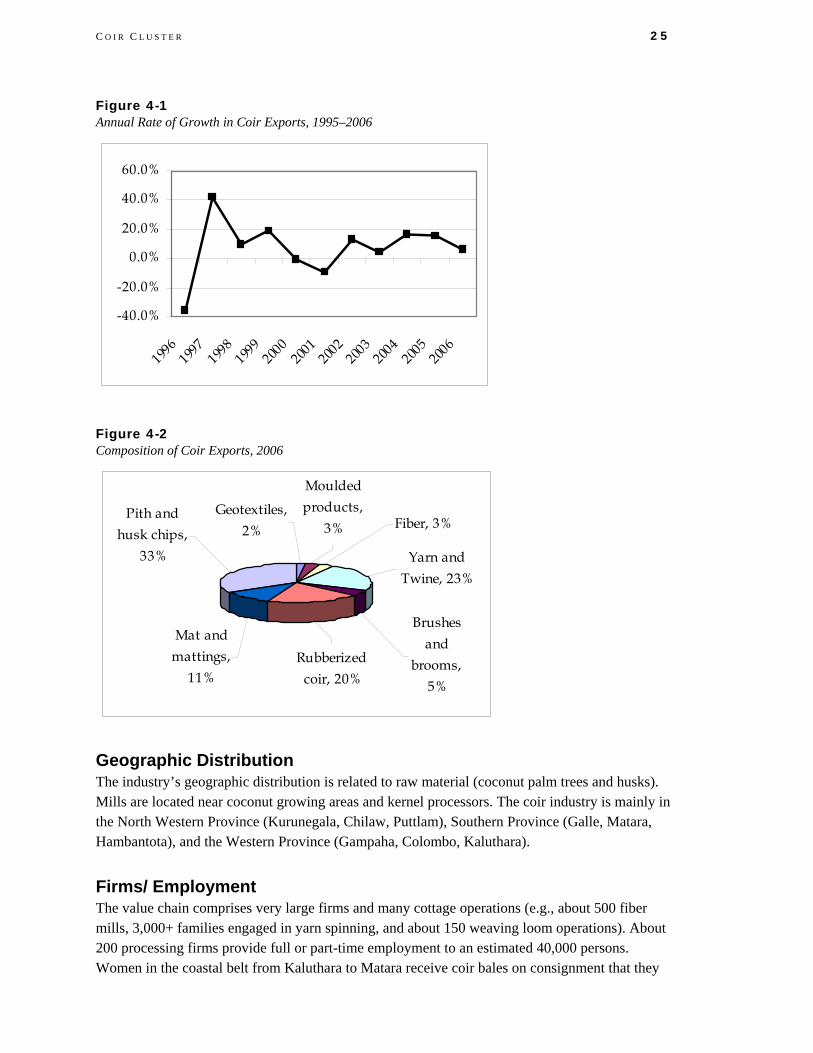

C O I R C L U S T E R 25

Figure 4-1 Annual Rate of Growth in Coir Exports, 1995–2006

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Figure 4-2 Composition of Coir Exports, 2006

Mat and mattings,

11%Rubberized

coir, 20%

Brushes and

brooms, 5%

Yarn and Twine, 23%

Fiber, 3%Geotextiles,

2%

Moulded products,

3%Pith and

husk chips, 33%

Geographic Distribution The industry’s geographic distribution is related to raw material (coconut palm trees and husks). Mills are located near coconut growing areas and kernel processors. The coir industry is mainly in the North Western Province (Kurunegala, Chilaw, Puttlam), Southern Province (Galle, Matara, Hambantota), and the Western Province (Gampaha, Colombo, Kaluthara).

Firms/ Employment The value chain comprises very large firms and many cottage operations (e.g., about 500 fiber mills, 3,000+ families engaged in yarn spinning, and about 150 weaving loom operations). About 200 processing firms provide full or part-time employment to an estimated 40,000 persons. Women in the coastal belt from Kaluthara to Matara receive coir bales on consignment that they

26 T C P F I N A L R E P O R T

spin into yarn or twine. Three women spinning on manual wheels can produce 15 to 20 kgs of yarn in 6 hours at a rate of 15 LRs per kg., or approximately a dollar per person per day (2007). With TCP’s assistance, the cluster is pioneering and encouraging use of motorized wheels that consume little electricity while spinning 20kgs of better yarn in less than 4 hours with only two workers—more than doubling earnings per person.

Although demand for spun yarn is growing, most spinning in Sri Lanka remains manual. We expect that for the near future coir spinning will continue to provide a small supplemental and irregular income for women in rural areas, with the benefit that female heads of households and family members can earn this income in their spare time without leaving their homes. As electricity reaches more rural areas, the new technology developed through TCP and the cluster will spread, raising earnings in these areas. Until then, the new technology will spread to centers with electricity and small factory shops where workers will go.

TCP ACHIEVEMENTS

Impact of International Coir Convention In June 2002, the coir cluster coordinated and hosted a convention under the patronage of FAO and funded by the Common Fund for Commodities (CFC), the cluster, TCI, and the government. The theme was “Beyond Nature’s Versatility, Towards Global Excellence.” Foreign and local experts presented papers to 148 attendees from 14 countries. Proceedings were published as an official technical paper (No. 20) of the CFC. The convention reinforced Sri Lanka’s position in the industry and gave representatives a chance to meet buyers and international experts. It was also a factor in CFC’s later decision to fund a project to research the potential of coir in advanced composites and a consultancy to finalize the project proposal on technology upgrading in the coir sector (i.e., the model mill project). The cluster build on the foundation laid by the convention to remain a force in the region and in coconut-exporting countries and obtain CFC funding for a model coir mill in 2006—funding premised on the recipient’s ability and willingness to share and disseminate with other countries.

Coir Council International The cluster brought together disparate elements and stakeholders in the value chain for the first time in 2002. It focused on strategies for dealing with heightened global competition. Suppliers and competing exporters who had rarely confided in each other (or saw themselves only as makers of a low-value byproduct of coconut processing) agreed to cooperate in a strategic overview of the entire value chain. They also agreed to cooperate in shared research on markets and technical specifications for their products. Recognizing the value of an industry-led approach, the cluster incorporated into a council in November 2003 under the Companies Act. The council’s unified approach has enhanced the industry’s position as an advocacy group and enabled industry-led strategy implementation with the public sector. For the first time the industry as a group is coordinating research and development, market development, workforce development, and training.

C O I R C L U S T E R 27

Research Partnerships The cluster was instrumental in providing a forum for R&D partnerships. At the request of the industry, the government research institute for coconut conducted a retting1 study in 2004, recommencing research after a lapse of more than two years. Earlier under TCI, the cluster facilitated and co-funded research on coir in advanced composites with the University of Delft, Holland, and Sri Lanka’s Industrial Technology Institute in 2003-04. The cluster lobbied CFC for co-funding and TCI for the cost of training the ITI research officer in Delft. This project built local research capacity and led to an assessment of opportunities for using coir in natural fiber composites, a market with double-digit growth in Europe.

Restored Livelihoods of Tsunami-affected Spinners Coir spinning thrives in villages along the southern coast and provides extra income for 3,000 families. Thousands of spinning wheels were washed away by the tsunami when homes were destroyed. The impact on livelihoods extended beyond the spinners to manufacturers of geotextiles (used in land erosion control) and handwoven doormats, for which coir-yarn is essential. In February 2005, TCP provided 500 spinning wheel sets complemented with a 25kg bale of coir fiber each to women who had lost their wheels and coir stock in the tsunami. This grant restored a key part of the livelihoods of approximately 1,500 women (3 women per reel set); re-started the value chain supply of coir twine used in the production of geotextiles for export from Sri Lanka to Korea and Japan; and enabled the export companies to fulfill their orders without interruption. Other NGOs and relief agencies followed TCP’s lead and began offering to wheels to hundreds more women in the tsunami-damaged coastal belt. Within four months the spinning capacity was regenerated in the tsunami-affected areas.

Cottage Weaving Technology for Geotextiles To break into the higher value geotextile market,2 millers found that they needed to be able to produce woven coir netting that met the international standard width of two meters. The cluster developed loom technology for manufacture of wider rolls of high quality geotextiles. A motorized 2-meter wide wooden loom for use in a cottage setting was developed and tested during 2006. Commercialization of the technology requires increasing the speed of the machine, which has a direct effect on productivity. Better specifications were developed for further trials in 2007. The International Erosion Control Association and industry co-funded this effort. The industry has implemented a follow-up program with the Ministry of Industries to test two more looms in 2008. This initiative will provide the industry with an opportunity to capitalize the demand for 2-meter wide, high quality geotextiles in the more discerning and higher priced markets of Europe and the United States.

1 Retting is the process where raw fiber is separated from the husk. In Sri Lanka this is often done in retting ponds, which can be a health hazard.

2 Geotextiles are used by Departments of Transportation and in construction projects to control erosion.

28 T C P F I N A L R E P O R T

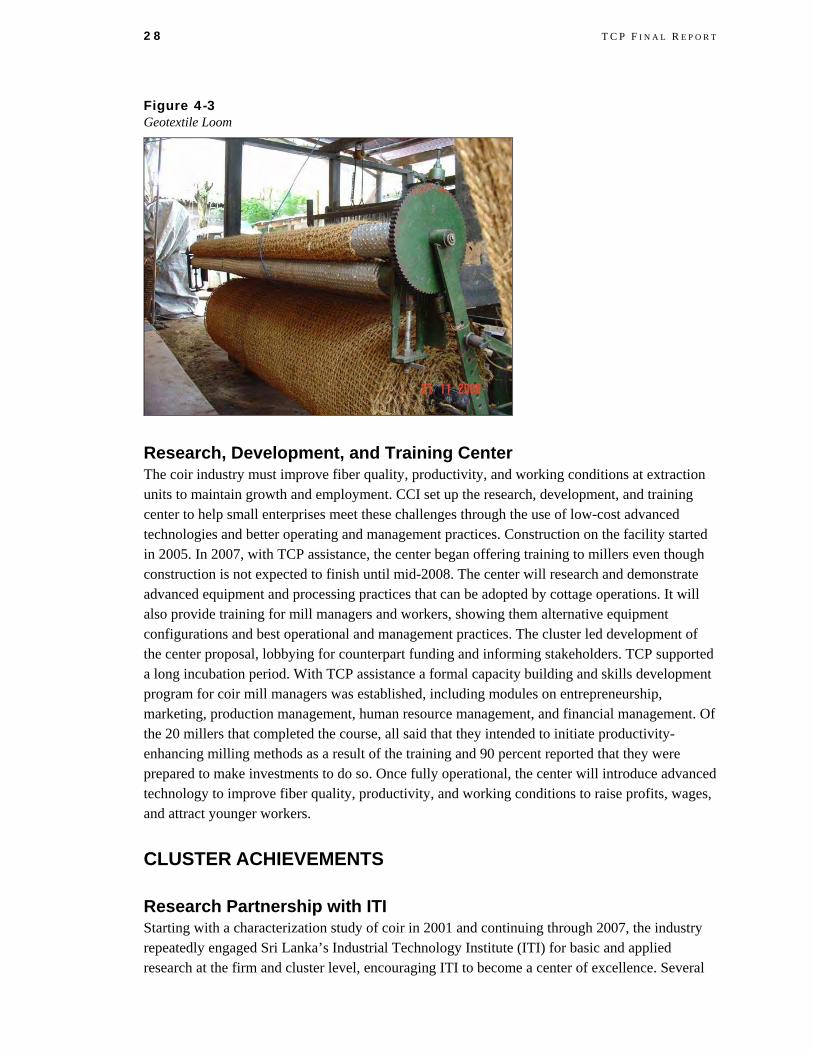

Figure 4-3 Geotextile Loom

Research, Development, and Training Center The coir industry must improve fiber quality, productivity, and working conditions at extraction units to maintain growth and employment. CCI set up the research, development, and training center to help small enterprises meet these challenges through the use of low-cost advanced technologies and better operating and management practices. Construction on the facility started in 2005. In 2007, with TCP assistance, the center began offering training to millers even though construction is not expected to finish until mid-2008. The center will research and demonstrate advanced equipment and processing practices that can be adopted by cottage operations. It will also provide training for mill managers and workers, showing them alternative equipment configurations and best operational and management practices. The cluster led development of the center proposal, lobbying for counterpart funding and informing stakeholders. TCP supported a long incubation period. With TCP assistance a formal capacity building and skills development program for coir mill managers was established, including modules on entrepreneurship, marketing, production management, human resource management, and financial management. Of the 20 millers that completed the course, all said that they intended to initiate productivity-enhancing milling methods as a result of the training and 90 percent reported that they were prepared to make investments to do so. Once fully operational, the center will introduce advanced technology to improve fiber quality, productivity, and working conditions to raise profits, wages, and attract younger workers.

CLUSTER ACHIEVEMENTS

Research Partnership with ITI Starting with a characterization study of coir in 2001 and continuing through 2007, the industry repeatedly engaged Sri Lanka’s Industrial Technology Institute (ITI) for basic and applied research at the firm and cluster level, encouraging ITI to become a center of excellence. Several

C O I R C L U S T E R 29

research projects were transferred from ITI to industry; some, such a new bleaching technology have helped reduce costs and improve quality. Others are leading to new marketable coir products including stronger coir pith “bio-pots” in a variety of shapes and sizes for the horticulture industry. The industry and ITI submitted a proposal for a product development and technology transfer center catering to coir SMEs. Accepted in principle by the ADB, the proposal seeks to establish prototypes for erosion control and composite product development, both areas in which TCP facilitated exposure and training for ITI staff.

Yarn Quality and Productivity Geotextile and mat manufacturers demand yarn of exceptional and consistent quality. Those exporting to discerning markets use high value twine to compete with products from India. Better yarn will allow Sri Lanka to tap into a larger segment of U.S. and European markets. The CCI and the Ministry of Industries will embark on a project to improve yarn quality and productivity at the cottage level. They will focus on semi-automation of traditional spinning wheels and testing of semi-automated spinning technology from India. Results will include more efficient and less costly production, higher profits for cottage operations, and better wages for cottage-level workers.

RURAL IMPACT Most of the 40,000 jobs in coir mills and related services are outside of the Western Province. Therefore, almost all cluster initiatives focused on issues upstream in the value chain, catering to the needs of the millers and mill workers in rural Sri Lanka. TCP assistance focused on productivity and quality improvement with the aim of preserving spinning and weaving as a cottage industry. Most spinners work on a per kilogram basis and so productivity enhancements resulted in a direct benefit of increased household income. The model mill and training program also heavily stressed the importance of safety and labor standards in mill operations, which will provide the long-term benefit of fewer workplace accidents and make the coir industry a more attractive employment option in the future.

INDUSTRY LEADERS’ OPINIONS ABOUT TCP Executives involved in TCP activities were surveyed in 2005, 2006, and 2007 for their opinion on how TCP had affected their industries. Executives were asked to respond on a scale of 1-7, with 1 expressing a negative opinion and 7 a positive opinion. A “mean score” above 3.5 indicates that—on balance—respondents answered the question (or questions in that topic area) with scores in the favorable or positive range. Table 4-1 presents some questions relevant to the coir sector; more survey extracts are presented in Appendix G.

30 T C P F I N A L R E P O R T

Table 4-1 Executive Opinion Survey, Coir Cluster

No. from Survey Questions

Mean Score

(1-7 scale)

11.02 Has your involvement in your industry cluster helped to improve the competitiveness of your firm? 4.8

11.05 Has your involvement in your industry cluster helped you to invest in your firm's training needs? 4.4

11.06 Has your involvement in your industry cluster helped you to influence government policies that adversely affect you company's competitiveness?

4.5

12.01-E In the past three years your company has invested significantly in entering new markets or developing new products

4.6

13.01 How involved were you in forming the industry cluster's apex body or lead organization 4 9

13.02 How actively do you participate in developing or implementing cluster initiatives 5.3

13.04 When TCP ends, will you continue to participate in cluster activities? 5.5

11.08 How much if any improvement in your firm's sales/export performance would you attribute to TCP/Cluster activities (please indicate an estimated percentage value)

21%

5. Gems & Jewelry Cluster Although Sri Lankan gems are widely viewed as some of the highest quality gems in the world, the gem industry lacked the capacity and knowledge to translate this competitive advantage into high value jewelry exports. In addition, export and regulatory policy diminished the competitiveness of the sector by heavily taxing jewelry making inputs. To address this situation, the Sri Lanka Gem and Jewelry Association (SLGJA) was incorporated under the Companies Act on November 28, 2003. A merging of four trade associations, it is now the apex body representing Sri Lanka’s gem and jewelry industry. The gem and jewelry cluster is a permanent subcommittee for strategy.

Sri Lanka Gem and Jewelry Association Sr. Spokesperson, Mr. David Hill, CEO Chairman, Chanaka Ellawala No 38, Frankfurt Place, Colombo 4 +94 11 259 7226 [email protected] www.lankajewels.com

The SLGJA has more than 360 members from across the industry value chain including mining, lapidary, jewelry manufacture and retail, as well as gemstone wholesale, retail, and export. It has a 35-member executive committee and committees on lapidary, jewelry, gemstones, and marketing. Funding is provided through membership dues and subscription fees. Co-funding is being sought through earmarking a part of the “cess” (export tax) on exports of gems and jewelry.

The SLGJA executive committee meets on the last Thursday of every month and each subcommittee reports on activities. In August 2005, Chanaka Ellawala was elected chairman. Vice presidents elected were Sheriff Rahuman, gem sector; Ismeth Majeed, jewelry; Donald Perera, lapidary; and Macky Hashim, promotions/trade fairs. The industry portal Lanka Jewels (www.lankajewels.com) is used for promotional and informative purposes.

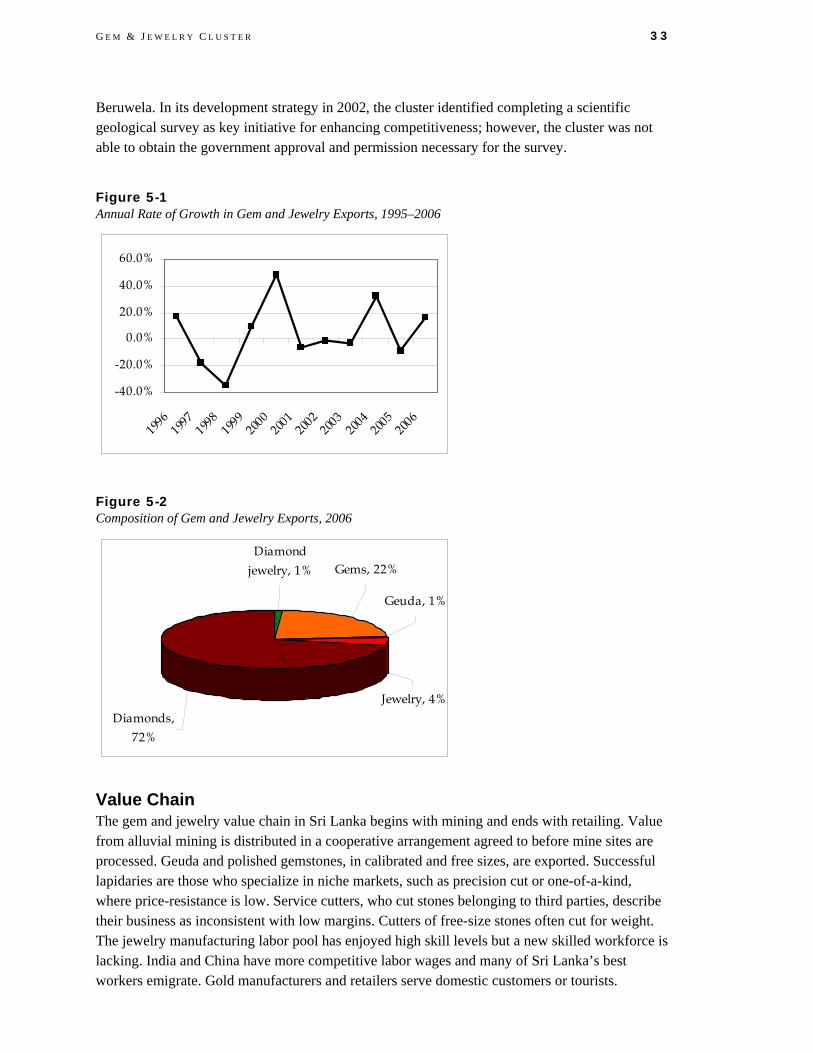

INDUSTRY COMPETITIVENESS The world gemstone and jewelry market is estimated to be US$170 billion. The principal markets for jewelry are the United States, Japan, Italy, the United Kingdom, Germany, and France. The size of the U.S. market is estimated to be US$48 billion, Japan US$30 billion, and Europe US$30 billion.

Sri Lankan Exports and Export Destinations Sri Lanka’s gem and jewelry exports increased 35 percent to US$135 million in 2006 from $100 million in 2001. Most of the growth came in the form of gem exports, which grew from $81 million in 2001 to $119 in 2006. Jewelry exports actually declined slightly from $18.6 million in 2001 to $15.6 million in 2006. In 2004, the last year before the tsunami and re-escalation of civil

32 T C P F I N A L R E P O R T

conflict, Sri Lanka exported $18.7 million in jewelry. The United States—where spending on jewelry correlates closely with GDP growth and even more so with discretionary spending— remains the main destination for Sri Lanka’s gem and jewelry exports.

Exhibit 5-1 Gem & Jewelry Sector Snapshot

1995 2001 2006

Exports (US$ million) 104.20 100.02 134.73

Type of Employment Official (apprx.)

Unofficial (apprx.) Total 2001

Gem mining 85,000 20,000 105,000

Gem cutting, incl. diamond cutting 20,000 --- 20,000

Gem dealers 3,200 5,000 8,200

Heat treatment 200 --- 200

Jewelry manufacturing 18,000 5,000 23,000

Gemologists 350 --- 350

Total 126,750 30,000 156,750

SOURCE Sectoral Plan for the Gem & Jewellery Industry, Ministry of Enterprise Development, 2002.

• Value chain: Mining, heat treatment, gemstone and jewelry manufacture, retailers