spring 2017 meeting slides - mccombs school of business/media/files/msb/development/… · ryan...

TRANSCRIPT

T

SPRING 2017 ADVISORY BOARD

MEETING

WELCOMEAND CALL TO ORDER

SARA ORTWEINChair, Cockrell School of Engineering Advisory Board

UPDATE FROM THE TOWER

GREGORY FENVESPresident, The University of Texas at Austin

UPDATE ON THEMcCOMBS SCHOOL

JAY HARTZELLDean, McCombs School of Business

Jay C. Hartzell, Dean

Dean’s Update

School Highlights

Students

Faculty and staff

Alumni engagement

Rowling Hall

McCombs Scholar of the Year

Branding/Marketing Study

Dean’s Update

School Highlights: Students

Student Success

National competitions: Six National Championships

National women’s case competition

Application strength and trends

School Highlights: Students

School Highlights: Graduate Student Stories

TR Geng — from China moved to US at age 18

PhD in Mathematics

Texas Venture Labs helped him gain business skills to get a job at BCG

Giving back by mentoring current TVL students

Ryan Crouser — Master of Science in Finance – May 2016 Top of his MSF Class

Competed in the Rio 2016 Olympics and won gold

Patrick Puryear — Master of Science in Marketing – May 2017

Graduate of United States Military Academy at West Point

Served in the US Army for 8 years and currently serves in the Texas Army National Guard

After graduation will go to work for JP Morgan as a Product Strategy Associate

School Highlights: Graduate Student Stories

School Highlights: Faculty and Staff

Faculty and Staff

Associate Dean for Research — Dr. Susan Broniarczyk

New senior faculty hires — Diwakar Gupta, William Fuchs, and Gregor Matvos

Chief Marketing Officer in Residence — Teri Thompson

Rob Malcolm — Endowed Chair in Marketing Innovation

School Highlights: Alumni

Alumni Engagement

Goff Real Estate Labs

Wall Street/Bay Area for McCombs

New boards

Center for Leadership and Ethics

Entrepreneurship

Healthcare

School Highlights: Rowling Hall

John Adams Scholar of the Year Award

Eila R. Motley, Finance and Business Honors Program, May 2018

McCombs Brand Refresh Project Update

McCombs Brand Steering Committee

Rob MalcolmMcCombs Executive in Residence

Lamar Johnson Associate Director, Center for Customer Insight and Marketing Solutions

Teri ThompsonMcCombs CMO in Residence

Stephen LimbergGraduate Programs Associate Dean

Shannon HicksonBBA Assistant Director, Career Services

Wayne HoyerChair, Marketing Department

Susan BroniarczykProfessor in Marketing

Erin Nelson McCombs Advisory Council, Exec. VP and CMO, SunPower

Paul KinscherffMcCombs Advisory Council, VP Corporate Development, Boeing

Jolene Hood AshcraftMBA Marketing Manager

David WengerDirector of Communications

Janaya LavalaisBBA Representative, UBC, BBA International Office

Simi FafoworaMBA Representative, Marketing Fellows

Brand Audit

Competitive Review

Quantitative and

Qualitative Discovery

PHASE 1 PHASE 2 PHASE 3 PHASE 4

Brand Cornerstones

Positioning Development

Design/Messaging

Concepting and Development

In-market Execution

(tagline, updated look-and-feel,

etc.)

Complete May-June Jul-Aug Aug-Sept

Progress Update

193 qualitative respondents:Group discussions 9 Program leader/director groups

4 student focus groups

Interviews 11 Select faculty/staff

8 Power influencers and advisory council members

9 Corporate partners and recruiters

10 External deans/professors

4 Higher education reporters/writers

1 MBA consultant

3 International partners

2,227 quantitative respondents: Alumni/Advisory Council –– 668

Current Students – 435

Faculty/Staff – 152

Prospective Students – 222

CBHS Panel – Fielding – 250

Parents Panel – Fielding – 250

Prospective Grads Panel –250

Phase 1: Discovery

1. Business education is highly undifferentiated space; despite

decades of built up equity, few of the top-end business school brands

stand out with their strategy or messaging

2. The market-level conversation is about features shared by nearly

every business school – leadership, innovation, diversity

3. In order to stand out, McCombs must build a brand that extends

beyond traditional notions of leadership

Competitive Analysis

McCombs performs well on the attributes that are most important to various audiences

McCombs is credited with being at the forefront of innovation and entrepreneurship

McCombs benefits from the University of Texas at Austin’s strong research reputation

McCombs students embody the competitive yet collaborative nature of Texas

Austin is an even more powerful differentiator

1

Topline Findings: Areas of Strength

2

3

4

5

“Chicago, Wharton, HBS…they think they know everything, or are too good to do certain things.

McCombs guys don’t have a chip on their shoulder. They’re happy in teams, work hard. They know the hours are brutal, but they’re happy to do it, no attitude of ‘I’m too good to work ‘til 2am.’ ”

— CORPORATE RECRUITER

“The people who come here are problem solvers, they're people who aren't afraid to kind of get in there, roll up their sleeves, get their hands dirty, do the work.”

— INTERNAL LEADERSHIP

Competitive Yet Collaborative

“You can sell the Austin experience, whether SXSW, the

culture, the entertainment scene. It’s a unique

city…There’s so much happening in the tech space, I

think Austin has the ability to be not a Silicon Valley, but

certainly in that space in terms of the tech scene and

entrepreneurial scene that is there. That’s what I would

be leveraging.”

— ASPIRANT DEAN

Austin is a Differentiator

Creating the Businesses of Tomorrow“When someone chooses to go

to McCombs, it says that

they’re looking to the future.

The future of business is in

places like Austin, and they

want to be a part of that.”

— HIGHER ED MEDIA

“Who's going to create the

businesses of tomorrow?

I think that’s where we want

to hang our hat, and the

combination of the business

curriculum and the access to

these high growth businesses

in a growing dynamic city like

Austin.”

— POWER INFLUENCER

Creating the Businesses of Tomorrow

EnterprisingEnergetic, ambitious, adventurous, collaborative, cooperative, industrious, entrepreneurial, agile, dynamic, pioneering, risk takers

TenaciousPersistent, grit, hard-working, dogged, unyielding, “do-ers”, action-oriented, hopeful, fit, initiative

Curious

Inquisitive, singular, inquiring, questioning, innovative, flexible, open

AuthenticReliable, honest, transparent, credible, inclusive, accountable, generous, friendly

Brand Core

BRAND CORNERSTONESDRAFT – WORK IN PROGRESS

1. Many jobs as we know them today will not exist in the future

2. Disruption will accelerate and come from unexpected places

3. Distributed leadership will proliferate

4. People will hone leadership skills through immersive experiences

5. Clarity, grit, humanity and fitness will be qualities that enable next-

gen leaders

6. Generation Z has a high degree of hope and optimism

Institute for the Future: Key takeaways

McCombs School of Business students are:

“Fit for the future….”

Transformative learning experiences built on a foundation of groundbreaking research, head-turning faculty, and a symbiotic relationship with one of the fastest growing and future-oriented cities in the world create seekers with the clarity and stamina to lead the dynamic organizations of the future.

DRAFT – WORK IN PROGRESS

Creating Leaders of the Future

1. The only certainty about the future is that certainty will cause failure.

We build agile leaders with the clarity and curiosity to navigate exponential disruption.

2. Top-down leadership will lose effectiveness; winning businesses will be those who constantly shift their shapes with leadership often coming from the edges.

We prepare leaders not only to be CEOs but to effectively lead in a variety of situations. We train for leadership fitness – persistence of body, mind, and heart.

DRAFT – WORK IN PROGRESS

Brand Manifesto

3. Future business talent thrives on discovery, iteration, and adaptation in the face of uncertainty and constant change.

We move beyond conventional notions of going to business school to only study specific business disciplines. We equip students to actively explore and mix diverse disciplines so they can lead in endeavors the world is only beginning to comprehend.

DRAFT – WORK IN PROGRESS

Brand Manifesto

4. Knowledge will have an increasing impact on the business world.

We treasure curiosity, discovery, and clarity in both research and teaching. We encourage and reward relevant groundbreaking research and knowledge creation that have the power to shape the changing practice of business.

5. The future of innovation isn’t just on the coasts.

Innovation is in Austin where smart, imaginative thinkers and doers gather to solve seemingly unsolvable problems in novel ways.

DRAFT – WORK IN PROGRESS

Brand Manifesto

UPDATE ON THECOCKRELL SCHOOL

SHARON WOODDean, Cockrell School of Engineering

John HaltonASSOCIATE DEAN FOR DEVELOPMENT

• Retiring after 42 years of service toUT Austin

• Cockrell School has raised over $720 million under his leadership

• John C. and Cheryl M. Halton Engineering Excellence Endowment: $190,000

• John C. Halton III Seminar RoomEER 0.708

Chris HigginsCHIEF DEVELOPMENT OFFICER

• Joined the Cockrell School in February

• Previously the Assistant Dean for Advancement and Alumni Relations in the College of Law at the University of Illinois at Urbana-Champaign

On the Rise

2018 RankingsU.S. News & World Report

Ranked No. 9 Best Graduate Program in the U.S.

$180.8 MillionTotal 2015-16 Research Expenditures

66% Federal

20% Industry

9% State

5% Nonprofit/Foundation

Graduate Specialty Rankings2018 RankingsU.S. News & World Report

No. 1 Petroleum

No. 4 Civil

No. 4 Environmental

No. 6 Chemical

No. 7 Computer

No. 8 Aerospace

No. 8 Electrical

No. 11 Mechanical

Center for World University Rankings2017 Rankings

No. 1 Mathematics, Interdisciplinary Applications

No. 2 Engineering, Petroleum

No. 3 Engineering, Multidisciplinary

No. 8 Transportation

No. 9 Engineering, Aerospace

No. 10 Mechanics

2017 RankingsU.S. News & World Report

Ranked No. 11 Best Undergraduate Program in the U.S.

Undergraduate Specialty Rankings2017 RankingsU.S. News & World Report

No. 1 Petroleum

No. 3 Chemical

No. 4 Civil

No. 7 Computer

No. 7 Environmental

No. 8 Aerospace

No. 9 Electrical

No. 9 Mechanical

No. 14 Biomedical

Undergraduate Enrollment

• Over 38% increasein undergraduate enrollment over the past 20 years

0

2,000

4,000

6,000

8,000

1996 2000 2004 2008 2012 2016

Undergraduate En

rollm

ent

Graduation Rates

• Over 54% increase in number of BS degrees awarded in the past 20 years

0

500

1,000

1,500

2,000

1996 2000 2004 2008 2012 2016

Number of BS Degrees

Conferred

Diversity and Inclusiveness

No. 3 Number of B.S. Degrees to URM Students in the U.S.Diverse: Issues in Higher Education

No. 15 Number of B.S. Degrees to Women in the U.S.American Society for Engineering Education

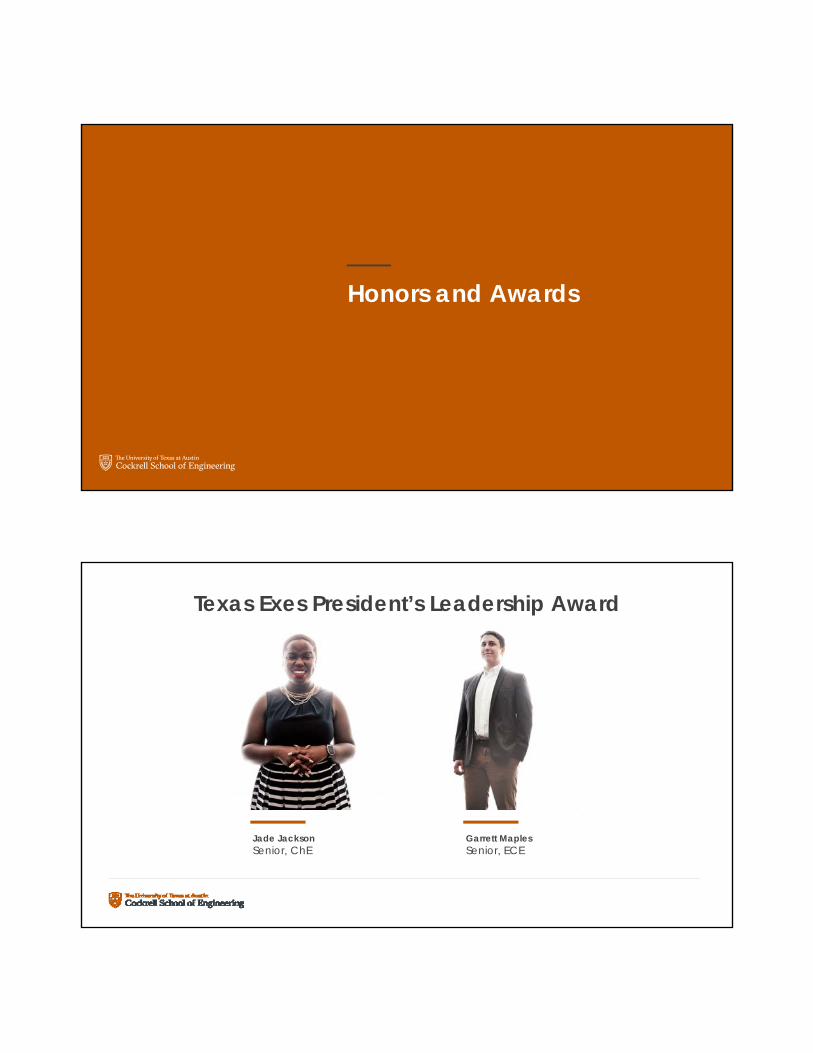

Honors and Awards

Jade JacksonSenior, ChE

Garrett MaplesSenior, ECE

Texas Exes President’s Leadership Award

David Allen

National Academy of Engineering

Professor, ChEMelvin H. Gertz Regents Chair in Chemical Engineering

For contributions to improving air quality and for developments in the education and practice of sustainable engineering.

Delia Milliron

2017 Norman HackermanAward

Welch Foundation

Associate Professor, ChEFellow of the Henry Beckman Professorship; Fellow of the Frank A. Liddell, Jr. Fellowship in Chemical Engineering

Deji Akinwande

2016 Moore Inventor Fellow

Gordon and Betty Moore Foundation

Associate Professor, ECEDavid & Doris Lybarger Endowed Faculty Fellowship in Engineering

Nicholas Peppas

American Academy of Arts and Sciences

Professor, BME and ChECockrell Family Regents Chair in Engineering #6

National Academy of Inventors

John GoodenoughProfessor, ME and ECE

S.V. SreenivasanProfessor, ME

Yale Patt

2017 Friar Centennial Teaching Award

The Friar Society

Professor, ECEErnest Cockrell Jr. Centennial Chair in Engineering

Ramesh Yerraballi

Dads’ Association Centennial Teaching Fellowship

The University of Texas at Austin

Distinguished Senior Lecturer, ECE

Record-Breaking Media Placement

Development of next-gen rechargeable battery technology

John Goodenough

Advancing the Engineering Campus

Engineering Education and Research Center

Energy Engineering Building (EEB)

Highest priority in the Cockrell School’s Strategic Master Plan (updated 2014)

Focus for energy education and research within the Cockrell School

Address the severe shortage of wet research laboratory space

Board of Regents committed $100 million in PUF bond proceeds

Advantages of LocationProminent location

Site accommodates efficient floor plan

Utility connections are optimized

Modern building for ASE/EM

CurrentSchedule

Select Architect of Record (21 Mar 2017)

Programming (31 July 2017)

Board of Regents’ approval of schematic design (9 Nov 2017)

Board of Regents’ approval of detailed design (17 May 2018)

@CockrellSchool

BREAK

Conference Break Area

ADVANCEDMANUFACTURING

JOE BEAMANProfessor, Mechanical Engineering

DAVID LEIGHSenior VP of Emerging Technologies, Stratasys

Additive Manufacturing (Solid Freeform Fabrication, 3D Printing)

External Advisory BoardsSchools of Engineering & Business

April 21, 2017

Joseph J Beaman

Advanced Manufacturing & Design Center

University of Texas at Austin

Early GoalFabrication of complex freeform solid objects directly from a computer model of an object without part‐specific tooling or human intervention.

Art to Part

Voxel Manufacturing ‐ 1985

Layered Manufacturing,Additive Manufacturing

Early Commercial Systems

Sterolithography

Selective Laser Sintering

Three critical enabling innovations in the 1980’s

Economic Lasers: power & information

Solid Modeling: 3D geometry information

The PC: Information processing

SLS History at UT

Early (1987) SLS

First Parts

First Machine

Early (1988) SFF Roller & HeatFeed Hopper Heat Lamp

Roller

First SLS System

DTM Corporation

• Texas Startup company 1989

• Started by UT student, faculty, entrepreneurs

• Grew to ~ 100 employees ~$25 million annual sales

• Now part of 3D Systems

• Spun off other commercial entities

UT Develops 1st SLS Machine (Deckard & Beaman)

UT Commercializes to DTM

First Commercial SLS Parts Sold

1988

Ti, SuperAlloy SLS Parts

SiC Laser Sintered Parts (indirect)

Custom Nylon Ankle‐Foot Orthotics

Flame Retardant Nanocomposites SLS Characterization

Next Generation High Temperature Polymer SLS Testbed

Silicon Infiltrated Silicon Carbide Fuel Reformer

1987

1989First SLS Direct Metal Parts &

First SLS machine sold to Sandia1992

1998

2014

2011

2002

2010

2007

BAMBI

UT Historical AM Contributions

Strength

Accuracy

3D Printing – Concept Models

Prototypes

Machining Forms

PatternsManufacturing

SFF Markets

Direct Manufacture

(A) Conventional Duct fabricated from Vac Formed plasticPart Count = 16 (plus glue)

(B) Component modified and consolidated for fabrication via Additive Rapid Direct Manufacture

Part Count = 1

Part Count = 1

Courtesy of 3D Systems / Boeing

Short Runs are Important for SFF

From: Anderson, C., Wired Magazine

Barriers to Additive Manufacturing

• Surface finish

• Production speed

• Cost

– Machines

– Materials

• Variation from part to part– Inadequate process control

• Materials availability

LAMPS Machine (AFRL)

OCT Laser (boresightedwith CO2 laser)

David Leigh

• Entrepreneur in Additive Manufacturing

• Developed the best Additive Manufacturing Service Bureau in SLS

• Commercial Activities in Central Texas

3D Printing Timeline

3D Printing Timeline

3D Systems (SLA) –1988

3D Printing Timeline

3D Systems (SLA) – 1988EOS (SLA) – 1990DTM (SLS) – 1990

3D Printing Timeline

3D Systems (SLA) – 1988EOS (SLA) – 1990DTM (SLS) – 1990EOS (SLS) – 1994

3D Printing Timeline

2001 - 3D Systems acquires DTM

3D Printing Timeline

2001 - 3D Systems acquires DTM- Eventually Combines Operations- EOS Enters US Market

3D Printing Timeline

2001 - 3D Systems acquires DTM- Eventually Combines Operations

3D Printing Timeline

2001 - 3D Systems acquires DTM- Eventually Combines Operations- EOS Enters US Market

3D Printing Timeline

2001 - 3D Systems acquires DTM- Eventually Combines Operations- EOS Enters US Market

• DTM (3D Systems)• Harvest Technologies (Stratasys)• Integra Services (EOS)• Advanced Laser Materials (EOS)• Solid Concepts (Stratasys)• Forecast Product Development (Alcoa)• EOS• Concept Laser (GE)

Concept Laser (GE)

EOS

Stratasys

Alcoa

Additive Manufacturing

3D Rollup

2001 Acquisition of DTM by 3D Systems

2002 First AM parts for F-18

2012 EOS acquires ALM and Integra

2012 GE acquires Morris Technologies

2014 Protolabs acquires Fineline

2014 3D Systems acquires Medical Modeling

2014 Stratasys acquires Harvest and Solid Concepts

Additive Manufacturing in US

Alaska Hawaii

2016 Venture Funding

Venture Funding in US

Alaska Hawaii

Additive Manufacturing in US

Alaska Hawaii

PRIVATE EQUITY PANEL

GARY BINNINGManaging Partner, Dominus Capital L.P.

BRIEN SMITHManaging Director, Neuberger Berman, LLC

ROBERT PARRINODirector, HMTF Center, McCombs School of Business

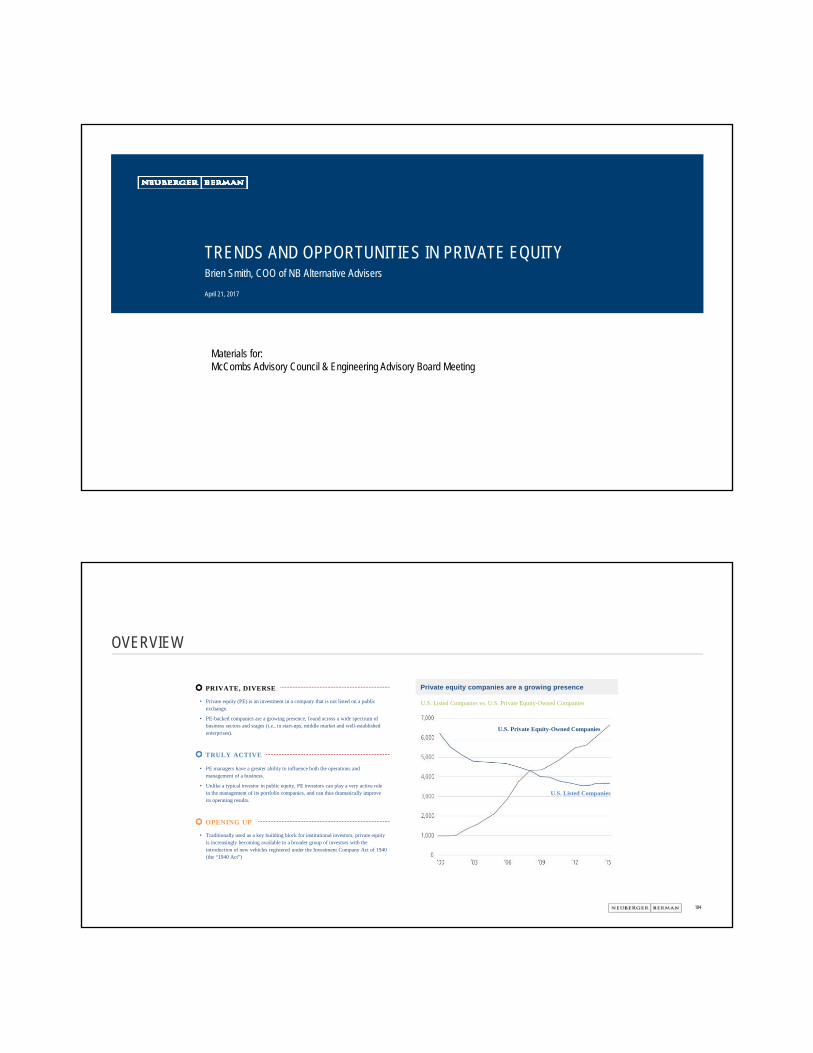

TRENDS AND OPPORTUNITIES IN PRIVATE EQUITYBrien Smith, COO of NB Alternative Advisers

April 21, 2017

Materials for:McCombs Advisory Council & Engineering Advisory Board Meeting

104

OVERVIEW

Private equity companies are a growing presence

U.S. Listed Companies vs. U.S. Private Equity-Owned Companies

U.S. Private Equity-Owned Companies

U.S. Listed Companies

• PE managers have a greater ability to influence both the operations and management of a business.

• Unlike a typical investor in public equity, PE investors can play a very active role in the management of its portfolio companies, and can thus dramatically improve its operating results.

• Traditionally used as a key building block for institutional investors, private equity is increasingly becoming available to a broader group of investors with the introduction of new vehicles registered under the Investment Company Act of 1940 (the “1940 Act”)

• Private equity (PE) is an investment in a company that is not listed on a public exchange.

• PE-backed companies are a growing presence, found across a wide spectrum of business sectors and stages (i.e., in start-ups, middle market and well-established enterprises).

PRIVATE, DIVERSE

TRULY ACTIVE

OPENING UP

105

P R I VAT E E Q U I T Y

PRIVATE EQUITY vs PUBLIC EQUITY

• Daily Liquidity • 10+ Year Investment

• Invested immediately • Invested over several years

• Daily market pricing • Estimated fair value on quarterly basis

• Regulated reporting • Transparency can be limited

• Typically managed to a benchmark • Managed on a cash return basis

• Little to no activism • Highly active in value creation

P U B LI C EQ U I TY

106

ADVANTAGES OF PRIVATE EQUITYPrivate equity and public stocks operate in the same economic and regulatory environment, but private equity has certain advantages

Source: Neuberger Berman.1. Source: Cambridge. Public return reflects MSCI World Index; Private Equity Return reflects the Global Private Equity Only Index. As of Q4 2014.

PUBLIC

STOCKS

10-Year Return(1): 6.0%15-Year Return(1): 3.1%20-Year Return(1): 7.1%

PRIVATE

PRIVATE EQUITY

10-Year Return(1): 12.6%15-Year Return(1): 11.3%20-Year Return(1): 13.3%

On the Buy

On the Sell

• Access to private information

• Opportunity to diligence management and operations

• Use of financing structures

• Less efficient market

• Multiple options for exit, including IPO and sale

• Ability to position the company for exit

During the Hold

• Ability to control change and hold management accountable

• Focus on operational improvements and long-term success

On the Buy

On the Sell

• Limited to no information advantages

• Efficient market

• Limited to no ability to “position” company at sale

During the Hold • Limited to no ability to effect change

107

RISKS OF PRIVATE EQUITY

• Once invested, the LP’s money is locked up for several years, until distribution or the end of the fund’s life

• Exiting the investment early can be challenging

‒ Secondary markets are inefficient and relatively small, but are evolving and becoming more important liquidity providers.

• Range of potential returns is wider than that implied by relatively low periodic mark-to-market volatility

• Fund performance depends on broad economic conditions when capital is drawn and invested, equity market conditions when exit liquidity is being sought, and the skill of the GP.

• Investment values are estimates until investment is realized

• FAS 157 accounting rules have introduced more discipline into the process of quarterly valuation marking

• Fund life typically lasts 7-12 years, depending on strategy

• It is difficult to know the ultimate success of fund until most investments are realized

• This creates a large amount of uncertainty and makes the asset class difficult to evaluate over short time frames

Liquidity

Volatility

Imprecision in Valuation

Long-term nature of the private equity investment cycle

108

CURRENT MARKET ENVIRONMENT

CURRENT MARKET

• Charged political environment stemming from Brexit and U.S. elections

• High valuations across asset classes

• Robust financing markets

• Potential future public market volatility

WHAT DOES THIS MEAN FOR PRIVATE EQUITY?

Source: NB Alternative Advisers

109

PRIVATE EQUITY BUYOUT VOLUMESSolid volumes over the last four years, particularly in the United States

0

50

100

150

200

250

2009

2010

2011

2012

2013

2014

2015

2016

US LBO Volume Europe LBO Volume

Source: S&P Leveraged Buyout Quarterly Review . EU volume converted at average FX rate during period.

110

PRIVATE EQUITY MARKET VALUATIONS: COMPARISON TO PUBLIC MARKETS (U.S.)• U.S. private equity valuations appear to be easing • Private equity valuations continue to exhibit a persistent discount vs public markets

8.8x 8.7x 8.8x9.7x 10.3x 10.0x10.2x 10.6x

12.7x

15.9x17.5x

19.9x

0x

2x

4x

6x

8x

10x

12x

14x

16x

18x

20x

2011 2012 2013 2014 2015 2016US Private US Public

Source: S&P Leveraged Buyout Quarterly Review. Bloomberg.Note: Public multiples based on Russell 2000.

PUBLIC VS. PRIVATE VALUATIONS (EV/EBITDA MULTIPLES)

111

PRIVATE EQUITY MARKET VALUATIONS: COMPARISON TO PUBLIC MARKETS (EUROPE)• European private equity valuations are beginning to show a discount vs public markets

8.8x9.3x

8.7x

10.0x9.2x

10.0x

8.7x 9.0x9.6x

10.1x 10.2x

12.9x

0x

2x

4x

6x

8x

10x

12x

14x

2011 2012 2013 2014 2015 2016Europe Private Europe Public

Source: S&P Leveraged Buyout Quarterly Review. Bloomberg.Note: Public multiples based on MSCI Europe Small Cap.

PUBLIC VS. PRIVATE VALUATIONS (EV/EBITDA MULTIPLES)

112

CAPITAL CONTRIBUTIONS VS. DISTRIBUTIONS FOR GLOBAL BUYOUT FUNDSGlobal buyout funds have been cash flow positive for the past six years

-$200

-$100

$0

$100

$200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 H1 2016Contributions Distributions Net cash flows

1. Source: Bain Global Private Equity Report 2017.

CAPITAL CALLS VS. DISTRIBUTIONS ($BN)1

113

BUYOUT NET ASSET VALUESThe rise in contributions and valuation has not been enough to offset distributions, so overall NAV is declining

$469

$589 $610 $660 $696

$662 $610

$101

$90 $88 $64 $96 $81

-$77 -$112 -$129 -$155

-$194 -$184

$96 4292

12664

51

$0

$200

$400

$600

$800

2010 2011 2012 2013 2014 2015 2016NAV Contributions Distributions Valuation change

1. Source: Bain Global Private Equity Report 2017.

GLOBAL BUYOUT NAV ($BN)1

114

COMPARISON OF PRIVATE AND PUBLIC EQUITY RETURNS• Private equity has performed well in absolute and risk-adjusted terms vs. public equities• Private equity has outperformed public markets on a medium- and long-term basis

6.9%

11.1%

5.1%

10.3%

12.3% 12.3%

0%

2%

4%

6%

8%

10%

12%

14%

MSCI World All Private Equity MSCI World All Private Equity MSCI World All Private Equity

15-YEAR 10-YEAR 5-YEAR

Past performance is not indicative of future results. Represents the investment horizon for Global Private Equity and Venture Capital Index from Thomson Reuters as of September 30, 2016, which is the latest data available.

COMPARISON OF HORIZON RETURNS – PUBLIC VS. PRIVATE

115

HOW DOES THE CURRENT U.S. POLITICAL ENVIRONMENT AFFECT OUR INVESTMENTS?

• Overall policy uncertainty

• Potential swing to protectionism

• Potential tax law changes

• Potential infrastructure spending

• Potential deregulation

Source: NB Alternatives.

116

OUR VIEWS

• We believe private equity is the most nimble asset class for taking advantage of change

• Whenever you have industries / companies that are in need of restructuring, consolidation, etc., these are all areas that play to the advantage of private equity

• Relative to other asset classes, private equity is particularly well adapted to take advantage of these changes

– Private equity has the ability to invest only when they find an attractive opportunity

– Private equity managers generally control their portfolio company’s businesses and have the operating resources to affect change

– Private equity managers are generally aligned with the interests of the management teams and investors

– Private nature allows managers to focus on proper multi-year strategy, not quarterly earnings

• While the inherent long-term structure of private equity is suited for the current market environment, investors should be patient and remain both discerning and opportunistic with new investments

Source: NB Alternatives.

117

SUMMARY RISK FACTORSProspective investors should be aware that an investment in any NB Private Equity Fund (the “Fund” or “Funds”) is speculative and involves a high degree of risk that is suitable only for those investors who have the financial sophistication and expertiseto evaluate the merits and risks of an investment in the Fund and for which the Fund does not represent a complete investment program. An investment should only be considered by persons who can afford a loss of their entire investment. Thefollowing is a summary of only certain considerations and is qualified in its entirety by the Confidential Private Placement Memorandum of the Fund (the “Memorandum”) and prospective investors are urged to consult with their own tax and legal advisorsabout the implications of investing in the Fund. Fees and expenses can be expected to reduce the Fund’s return.

Market Conditions. The Fund’s strategy is based, in part, upon the premise that investments will be available for purchase by the Fund at prices that the Fund, the general partner of the Fund (the “General Partner”) considers favorable and which arecommensurate with the targeted returns described herein. To the extent that current market conditions change or change more quickly than Neuberger Berman Group, LLC or an affiliate (“Neuberger Berman”) currently anticipates, investmentopportunities may cease to be available to the Fund or investment opportunities that allow for the targeted returns described herein may no longer be available.

No Assurance of Investment Return. There can be no assurance or guarantee that the Fund’s objectives will be achieved, that the past, targeted or estimated results presented herein will be achieved or that investors in the Fund (“Investors”) willreceive any return on their investments in the Fund. The Fund’s performance may be volatile. An investment should only be considered by persons who can afford a loss of their entire investment. Past activities of investment entities sponsored byNeuberger Berman provide no assurance or guarantee of future results. The Fund’s intended strategy relies, in part, upon the continuation of existing market conditions in certain countries (including, for example, supply and demand characteristics orcontinued growth in GDP) or, in some circumstances, upon more favorable market conditions existing prior to the termination of the Fund. No assurance or guarantee can be given that investments meeting the Fund’s investment objectives can beacquired or disposed of at favorable prices or that the market for such investments (or market conditions generally) will either remain stable or, as applicable, recover or improve, since this will depend upon events and factors outside the control of theFund’s investment team. Notwithstanding anything in this presentation to the contrary, Neuberger Berman or the General Partner may vary its investment processes and/or execution from what is described herein.

Legal, Tax and Regulatory Risks. Legal, tax and regulatory changes (including changing enforcement priorities, changing interpretations of legal and regulatory precedents or varying applications of laws and regulations to particular facts andcircumstances) could occur during the term of the Fund that may adversely affect the Fund or its partners.

Performance of the Fund and No Operating History. The Fund and the General Partner are newly-formed entities with no operating history for prospective investors to evaluate.

Default or Excuse. If an Investor defaults on or is excused from its obligation to contribute capital to the Fund, other Investors may be required to make additional contributions to the Fund to replace such shortfall. In addition, an Investor mayexperience significant economic consequences should it fail to make required capital contributions.

Indemnification. Under certain circumstances, the Fund is responsible for indemnifying the General Partner and its affiliates for losses or damages.

Leverage. The Fund’s investments are expected to include underlying portfolio companies whose capital structures may have significant leverage. These companies may be subject to restrictive financial and operating covenants. The leverage mayimpair these companies’ ability to finance their future operations and capital needs. The leveraged capital structure of such investments will increase the exposure of the portfolio companies to adverse economic factors such as rising interest rates,downturns in the economy or deteriorations in the condition of the portfolio company or its industry.

Highly Competitive Market for Investment Opportunities. The activity of identifying, completing and realizing attractive investments is highly competitive, and involves a high degree of uncertainty. There can be no assurance or guarantee that theFund will be able to locate, consummate and exit investments that satisfy the Fund’s rate of return objectives or realize upon their values or that it will be able to invest fully its committed capital.

Reliance on Key Management Personnel. The success of the Fund will depend, in large part, upon the skill and expertise of certain Neuberger Berman professionals. In the event of the death, disability or departure of any key Neuberger Bermanprofessionals, the business and the performance of the Fund may be adversely affected.

Potential Conflicts of Interest. There may be occasions when the General Partner and/or advisors to the Fund and their affiliates will encounter potential conflicts of interest in connection with the Fund’s activities including, without limitation, theactivities of Neuberger Berman and key personnel, the allocation of investment opportunities, conflicting fiduciary duties and the diverse interests of the Fund’s limited partner group. There may be disposition opportunities that the Fund cannot takeadvantage of because of such conflicts.

Limited Liquidity. There is no organized secondary market for Investors’ interests in the Fund, and none is expected to develop. There are restrictions on withdrawal and transfer of interests in the Fund.

Material, Non-Public Information. By reason of their responsibilities in connection with other activities of Neuberger Berman, certain employees of the General Partner, the advisors and their respective affiliates may acquire confidential or materialnon-public information or be restricted from initiating transactions in certain securities. The Fund will not be free to act upon any such information. Due to these restrictions, the Fund may not be able to initiate a transaction that it otherwise might haveinitiated and may not be able to sell an investment that it otherwise might have sold.

THE FOREGOING DOES NOT PURPORT TO BE A COMPLETE EXPLANATION OF THE RISKS AND CONFLICTS INVOLVED IN THIS OFFERING OR AN INVESTMENT IN THE FUND. POTENTIAL INVESTORS SHOULD READ THISPRESENTATION, THE MEMORANDUM, THE SUBSCRIPTION AGREEMENT AND THE LIMITED PARTNERSHIP AGREEMENT OF THE FUND IN THEIR ENTIRETY BEFORE DECIDING WHETHER TO INVEST IN THE FUND AND SHOULDCONDUCT THEIR OWN DILIGENCE OF THE OPPORTUNITY AND IDENTIFY AND MAKE THEIR OWN ASSESSMENT OF THE RISKS INVOLVED.

TRENDS AND OPPORTUNITIES IN PRIVATE EQUITY

118

DISCLOSURESThis document contains highly confidential information regarding investments, strategy and organization of NB Alternatives Advisers LLC (“NB Alternatives”). If you are a limited partner in any fund managed by NB Alternatives, this entire documentconstitutes “Partnership Information”, non-public information or information related to the partnership or its affairs, as applicable, and is covered by the provisions of the Confidentiality section of the applicable partnership agreement. Regardless ofwhether you are a limited partner in any NB Alternatives managed fund, your acceptance of this document from NB Alternatives constitutes your agreement to (i) keep confidential all of the information contained in this document, as well as anyinformation derived by you from the information contained in this document (collectively, “Confidential Information”) and not disclose any of the Confidential Information to any other person, (ii) not use any of the Confidential Information for any purposeother than to monitor investments in NB Alternatives’ managed funds, (iii) not use the Confidential Information for the purpose of trading any security, including, without limitation, securities of NB Alternatives’ managed funds or their portfolio companies,(iv) not reproduce this document without the prior consent of NB Alternatives, and (v) promptly return this document and any copies hereof to NB Alternatives upon NB Alternatives’ request. This document is for informational and discussion purposesonly and does not constitute an offer to sell or a solicitation of an offer to purchase any security. Any such offer or solicitation shall be made only pursuant to additional documentation relating to such fund, which documentation describes risks related toan investment in the fund as well as other important information about the fund and its sponsor. The information set forth herein does not purport to be complete and is subject to change. This document is qualified in its entirety by all of the informationset forth in any such additional documentation.

This document may include information from a number of funds managed by NBAA and its predecessors-in-interest. Neuberger Berman and its affiliates are the successor to all of the predecessors’ operational assets, and employ substantially all oftheir key personnel, and NBAA became either the advisor or sub-advisor to the funds previously advised by the predecessors. Historical information contained herein is for illustrative purposes only; such information is based on market and otherconditions at the time that may significantly change, and should not be relied upon.

Past performance is not necessarily indicative of future results. There can be no assurance that the funds described herein or their investments will achieve comparable results, that targeted, diversification or asset allocations will be met or that the fundswill be able to implement their investment strategy and investment approach or achieve their investment objectives. Actual returns on unrealized investments will depend on, among other factors, future operating results, the value of the assets andmarket conditions at the time of disposition, legal and contractual restrictions on transfer that may limit liquidity, any related transaction costs and the timing and manner of sale, all of which may differ from the assumptions and circumstances on whichthe valuations used in the prior performance data contained herein are based. Accordingly, the actual realized returns on unrealized investments may differ materially from the returns indicated herein.

Statements contained in this document that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of NB Alternatives and its affiliates. Such statements involve known and unknown risks, uncertainties andother factors, and undue reliance should not be placed thereon. In addition, this document contains "forward-looking statements." Actual events or results or the actual performance of the funds and their investments may differ materially from thosereflected or contemplated in such forward-looking statements. No representation or warranty is made as to future performance or such forward-looking statements. Financial or other projections described herein are illustrative and intended fordiscussion purposes only. Alternative assumptions may result in significant differences in such illustrative projections. Opportunities described in such illustrative projections may not be found nor is prospective performance of the type describedguaranteed, and a fund may not be able to achieve its objective or implement its strategy.

Certain economic and market information contained herein has been obtained from published sources prepared by third parties and in certain cases has not been updated through the date hereof. While such sources are believed to be reliable, neitherNB Alternatives, its affiliates nor employees assume any responsibility for the accuracy or completeness of such information.

None of Neuberger Berman Group LLC nor any of its affiliates have made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information containedherein (including but not limited to information obtained from third parties unrelated to Neuberger Berman Group LLC), and they expressly disclaim any responsibility or liability therefore. None of Neuberger Berman Group LLC nor any of its affiliateshave any responsibility to update any of the information provided in this document.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there isno representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higherdegree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee offuture results.

All information as of December 31, 2016, except as otherwise noted. Firm data, including employee and assets under management figures, reflect collective data for the various affiliated investment advisers that are subsidiaries of Neuberger BermanGroup LLC (the “firm”). Investment professionals referenced include portfolio managers, research analysts/associates, traders, and product specialists and team dedicated economists/strategists.

The views expressed herein include those of those of Neuberger Berman’s Asset Allocation Committee which comprises professionals across multiple disciplines, including equity and fixed income strategists and portfolio managers. The AssetAllocation Committee reviews and sets long-term asset allocation models and establishes preferred near-term tactical asset class allocations . The views of the Asset Allocation Committee may not reflect the views of the firm as a whole and NeubergerBerman advisers and portfolio managers may recommend or take contrary positions to the views of the Asset Allocation Committee. The Asset Allocation Committee views do not constitute a prediction or projection of future events or future marketbehavior. Due to a variety of factors, actual events or market behavior may differ significantly from any views expressed. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors,actual events may differ significantly from those presented.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

© 2017 Neuberger Berman Group LLC. All rights reserved.

TRENDS AND OPPORTUNITIES IN PRIVATE EQUITY

Dual Honors Degrees

Associate Professor, McCombs School of Business

JAY HARTZELLDean, McCombs School of Business

SHARON WOODDean, Cockrell School of Engineering

CARLOS CARVALHO

Dual DegreesBusiness Honors + Engineering

BHP + Engineering

• Main idea: create dual degrees between McCombs and Cockrell by combining honors business education with strong, technical and computational skills.

• Focus: tech innovation, product development, entrepreneurship, business analytics.

• Honors Focus: unique experience, dedicated small cohort courses. Aim to attract top talent from Texas and beyond. ~50 students per cohort.

• Austin and UT offer a perfect environment for such programs.

“... dual degree academic program globally providing future leaders with exceptional opportunities to combine engineering andbusiness knowledge in designing and implementing cutting‐edge solutions to important commercial and social problems.”

“You’ll get hands‐on practice turning great ideas into real‐world solutions... Match your engineering talent with business expertise and become the kind of entrepreneurial leader the world needs.”

“... it is crucial to build and offer a challenging and rigorous program that provides graduates with skills and experiences that will make them successful in the future.”

“Understanding both entrepreneurship and product development is crucial for success in the current business environment where innovation, understanding markets, and knowing how what you do contributes to the bottom line are all keys for success.”

MS Business Analytics

• 10-month program: combination of business and data science classes.

• 3 graduated classes: 55 students per cohort.

• Salary: $89,000 on average ($125,000 top)

• Notable employers: Capital One, Booz Allen Hamilton, Facebook, IBM, Indeed, Deloitte, PwC, Wal-Mart, McKinsey, AT&T, GoPro, Starbucks, NFL, Amazon, Google, USAA

BHP + BSA in CS blueprintCore Curriculum 54 hours 2 Science, 2 Liberal Arts, etc

Business Courses 38 hours

2 ACC, 3 BA, 2 ECO, 1 MIS, 2 STA, 1 FIN, 1 MAN, 1 MKT,1 LEB

CS Courses 35 Hours 6 core CS, 4CS electives

Total 127 Hours

Challenges for Dual Degree with Engineering

Existing Dual Degree and Joint Degree Programs

• Geosystems Engineering and Hydrogeology• Joint with Jackson School of Geosciences• Students receive BS from Cockrell School• 132 hr

• Architectural Engineering / Architecture• Dual degree with School of Architecture• 197 hr (minimum of 6 years to complete)

• Engineering and Plan II Honors• Dual degree with College of Liberal Arts

(Typically takes 5 years to complete)

BHP + ME blueprintCore Curriculum 44 hours 2 Math, 2 PHY, 1 CH

Business Courses 38 hours

2 ACC, 3 BA, 2 ECO, 1 MIS, 2 STA, 1 FIN, 1 MAN, 1 MKT,1 LEB

Engineering Courses 58 Hours18 ME, 2 Math, 2 EM,2 PHY Labs

Total 140 Hours

Curriculum Integration

• Linking courses: summer session program connecting the two degrees.

• Practicum: experiential learning program focused on innovation, product development and entrepreneurship.

• Example: Rice’s Engineering Design Kitchen.http://oedk.rice.edu/about

TEXAS 4000STUDENT PRESENTATION

ERIC HIRSTSenior Associate Dean for Academic Affairs,

McCombs School of Business

Sharing Hope, Knowledge and Charity from Texas to Alaska

MISSIONCultivate student leaders.

Engage communities in the fight against cancer.

CHRIS CONDIT, FOUNDERCockrell School of Engineering B.S. in Biomedical Engineering, 2004, M.S.E., 2011

• Diagnosed with Stage III Hodgkin’s Lymphoma at age 11

• As a student at UT, founded Texas 4000 for Cancer, a leadership program cultivating UT students to engage communities in the fight against cancer

• Rode in the 2004 inaugural ride more than 4,500 miles from Austin, Texas, to Anchorage, Alaska with fellow students from Cockrell School of Engineering

• Currently, Senior R&D engineer at Abbott’s Neuromodulation division

Chris Condit (Center) with 2004 Riders in Austin

2004 Riders in Alaska

600+ Students from the University of Texas at Austin have participated

90+ Riders from the Cockrell School of Engineering

60+ Riders from the McCombs School of Business

Kris Novak, 2017 RiderSenior, Electrical Engineering

Catherine Butschi , 2017 RiderSenior, MPA

TEXAS 4000 LEADERSHIP PROGRAM

An 18‐month Leadership Development Program for students at The University of Texas at Austin

Three Core Pillars – Hope, Knowledge, & Charity

Eight Foundational Leadership Skills• Self Awareness• Communication• Resiliency• Efficient Planning• Peer Respect• Situational Leadership• Technical Knowledge & Skills• Vision & Action

Culminates in a 70‐Day Ride of 4,500 Miles along Three Routes from Austin, Texas, to Anchorage, Alaska

Over 70 Student Riders participate annually and each one:

• Logs more than 2,000 training miles prior to the summer ride

• Volunteers more than 50 hours during the program

• Raises at least $4,500 to help fight cancer

Students plan the entire ride from Austin to Anchorage

Students share cancer prevention information locally and throughout the communities along the ride

Texas 4000 Riders in San Francisco

Cancer Prevention Presentation by the Riders

TEXAS 4000 CHARITY MILESTONES

More than $7 million donated toward Cancer Research and Support Services

Highlights

• Donated more than $605,000 to the UT Austin Department of Biomedical Engineering for seed grants and to establish an endowment

• Donated more than $1,455,000 to the UT MD Anderson Cancer Center

• Donated more than $130,000 to the UT Southwestern Medical Center for research to explore the metabolism of cancer cells and identify targets in lung cancer cells

Sharing Hope, Knowledge and Charity from Texas to Alaska

TEXAS 4000 SUPPORT ACROSS THE COUNTRY

Texas 4000 Alumni and Texas Exes support riders across the country during the summer ride by hosting riders, organizing dinners, local cancer prevention speaking engagements, and fundraisers benefitting Texas 4000.

WAYS TO BE INVOLVED

Mentor a student rider—share your time with the teamHire a rider—you won’t find better talent!Ride with us on June 3—the Atlas RideBring your friends and join us at the Tribute Gala, August 25th

Become a donor—financial support fuels our mission

Scott CrewsExecutive Director

Texas 4000 for Cancer

[email protected]‐300‐2318 office512‐2975037 cell

www.Texas4000.org

Eric HirstBoard Chair

Texas 4000 for Cancer

Senior Associate DeanMcCombs School of BusinessUniversity of Texas at Austin

INTERESTED IN LEARNING MORE?

GENESIS PROGRAM

VIVEK SAKHRANIPresident, Longhorn Engineering Advisory Delegation (LEAD)

JACOB CORDOVAVice President, Longhorn Engineering Advisory Delegation (LEAD)

Genesis Program Executive Director

LEAD

LEAD

Engage recent alumni

Enhance the engineering student experience

LEAD

imealentreasuret LEAD

Engage recent alumni

Enhance the engineering student experience

LEAD

imealentreasuret LEAD Task

forces

Engage recent alumni

Enhance the engineering student experience

1st of its kind at UT AustinEarly stage funding

Applied learning

Jeff AusterGenesis Director of Development Chemical Engineering 2019

Solution to a critical need

https://www.youtube.com/watch?v=gM6xVy1F6g0

Michael JohnsGenesis Director of OperationsFinance and Business Honors 2017

Fully interdisciplinaryRewarding excellence

Impacting the lives of students

Joint Ventures

imealentreasuret

Joint Ventures

Give First

imealentreasuret

Joint Ventures

What starts(up) here changes the world

Engage recent alumni

LEAD

WRAP UPAND ADJOURN

RAY NIXONChair, McCombs School of Business Advisory Board

TTHANK YOU