spring 2011 fini619 habib bank limited

TRANSCRIPT

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 1/62

Virtual University of Pakistan

Evaluation Sheet for InternshipReport

Spring 2011

FINI619: Internship Report (Finance)Credit Hours: 3

Name of Student:

Student’s ID:

Evaluation Criteria Result

Report writing Pass

Presentation & Viva

voceFinal Result

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 2/62

Mistakes have been highlighted. Make corrections and

carefully read the comments given in your evaluated report

and prepare yourself for presentation. You must be very clear

about the each and every task performed by you during your

training period.You should be able to interpret the results of the ratios. You

also need to be very clear about the units of the ratios.

Interpretation of ratios should cover two steps:

Step # 1) Result understanding: i.e. what does the answer

derived from ratio calculation indicates? You have to critically

analyze the result of calculated ratio by explaining the

relationship of numerator with that of a denominator.

Step #2) Trend Analysis: i.e. what are the variations in a

company’s ratio results i.e. the trend for the same company

and the reasons for that change in trend?

Carefully read lesson 07 and prepare your presentation slides

accordingly. You can contact your course instructor, if find

any difficulty.

AN INTERNSHIP REPORT ON HABIB BANK

, 4th semester

August 5, 2011

VIRTUAL UNIVERSITY

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 3/62

DEPARTMENT OF BUSINESS MANAGEMENT SCIENCES

VIRTUAL UNIVERSITY OF PAKISTANVIRTUAL UNIVERSITY OF PAKISTAN

A REPORT SUBMITED IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE DEGREE OF

MASTER IN BUSINESS ADMINISTRATION (MBA)

LETTER OF UNDERTAKING:

LETTER OF INTERNSHIP:

4. ACKNOWLDGEMENT

I am very grateful to Almighty Allah, the most merciful and beneficial who gave

me encourages completing this task and made me able to complete the work accessible in

the report. I am also thankful to my parents whose prayers make possible to reach this

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 4/62

stage.

I am highly thankful to my instructor who guides me for the completion of this

report along with I am thankful to my fellows who helped me and gave me own precious

time to complete this report.

I am also very thankful to the staff of Habib Bank Water Works Road Branch,

Jarawala particularly to RIA Shahzad (branch manager) who helped and guided me

throughout this whole work.

It was an honor for me to learn and work with:-

Mr. Ria Shahzad (Branch Manager)

Mr. XYZ (Cashier)

Mr. DEF (Admininstrator)

5.EXECUTIVE SUMMARY

Every student of master has to practically work for six to eight weeks for more

learning of theoretical concept which he read during the session. It is very helpful during

practical life and awareness about the economy of the country. This purpose is to explain

the student with practical work that how to apply what they have learnt in practical work. It

is nice opportunity for the student to have shut relationship in theoretical concept and

practical work.

I got the chance to get my internship from one of the renowned bank of Pakistan

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 5/62

“The Habib Bank Limited, Pakistan”, it was a nice opportunity for me to apply my

theoretical work and learn from seniors having years of experience. All the efforts on the

way are summarized in shape of this Internship Report. Internship Report contains the

Short History of Banking, Banking in Pakistan, Introduction of Habib Bank Limited,

Organization Breakdown structure, Organization Hierarchy Chart, Introduction of different

departments.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 6/62

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 7/62

TABLE OF CONTENETS

AN INTERNSHIP REPORT ON HABIB BANK ..........................................................2

4. ACKNOWLDGEMENT ......................................................................................................3

5.EXECUTIVE SUMMARY ...................................................................................................4

..................................................................................................................................................6TABLE OF CONTENETS .......................................................................................................7

6. EVOLUTION OF BANKING .............................................................................................8

BANKING IN PAKISTAN: ....................................................................................................8ABOUT HABIB BANK LIMITED: ........................................................................................9

BRIEF HISTORY: ...............................................................................................................9

ORGANIZATIONAL CHART .........................................................................................10BOARD OF DIRECTORS ................................................................................................11

ORGANIZATIONAL STRUCTURE ...............................................................................11

VISION, MISSION AND VALUES .................................................................................11Vision: ...........................................................................................................................11

Enabling people to advance with confidence and success............................................11Values: ...........................................................................................................................11

Our values are the fundamental principles that define our culture and are brought tolife in our attitude and behaviors. It is these values that make us unique and

unmistakable. Our values are defined below: ................................................................11

DEPARTMENTS & RESPONSIBILITIES: .....................................................................12AWARDS: ..........................................................................................................................60

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 8/62

6. EVOLUTION OF BANKING

This history of banking is traced to as early as 2000 B.C. The priests in Greece used

to keep money and valuables of the people in temples. The origin of banking is also traced

to early goldsmiths. They used to keep strong safes for storing the money and valuables of

the people. The goldsmiths used to issue receipts for the money and other valuable assets

deposited with them. These receipts could be used for settlement of transactions because

people had confidence in the integrity and solvency of goldsmiths. When it was found that

these receipts were fully accepted in payment of debts; then the receipts were drawn in

such a way that it entitled any holder to claim the specified amount of money from

goldsmiths. A depositor who is to make the payments may now get the money in cash from

goldsmiths or pay over the receipt to the creditor. These receipts were the earlier bank

notes. The second stage in the development of banking thus was the issue of bank notes.

BANKING IN PAKISTAN:

I observed during my internship was that I came to known the historical

background of Banking & Financial sector and its improvement and growth since the

formation of Pakistan.

At the time of partition there were only 631 bank branches in area which came

under Pakistani control. But due to blood shed and violence at large scale, most of the

branches were closed. At that time Bank of India was acting as central bank for both

countries and same currency notes were used in both territories. But Reserve Bank of India

was biased and Set down Pakistan on many occasions such as the issue of funds transfer

etc.

Thus some drastic steps were taken in government sector for the improvement of

overall position. The private sector also responded positively. Some of the steps taken by

the government in this regard were as under:

• Inauguration of State Bank of Pakistan (SBP) on 1st July, 1948.

• Setting up of National Bank of Pakistan in November.

• Banking Companies Ordinance 1962 for protection and guidance to banks.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 9/62

• Establishment of specialized banks, such as ADBP (1952);

o HBFC (Nov, 1952)

o P1CIC (Oct, 1957)

o IDBP (Aug. 1961)

o NDFC (Jan, 1973)

In 1990 the government decided to denationalize all the nationalized institutes. For

this purpose, amendments were made to Nationalization Act 1974 and two nationalized

banks were privatized. Along with this a permission to open banks in private sector was

also granted.

The- privatized banks are;

o MCB taken up by a private group in April, 1991

o ABL taken up by its own employees in September, 1991.

o UBL taken up by UAE party in 2002.

o December 29, 2003 HBL was taken by AKFED

ABOUT HABIB BANK LIMITED:

BRIEF HISTORY:

HBL was the first commercial bank established in 1947. HBL is one of the largest

commercial bank of Pakistan. It accounts for a substantial share (20%) of the total

commercial banking market in Pakistan with a network of 1,705 domestic branches; 55

overseas branches in 26 countries spread over Europe, the Middle East, Far East, Asia,

Africa and the United States; 3 HBL wholly owned Subsidiaries namely Habib Bank

Financial Services (PVT) LTD. Karachi, Habib Finance International LTD (Hong Kong)

and Habib Finance Australia Ltd. – Sydney; 2 Joint Ventures namely Habib Nigeria Bank

Ltd. (40%) and Himalayan Bank Ltd. (20%) and 2 representative offices in Iran and Egypt.

HBL is currently rated AA+ (Long term) and A1+ (Short term)*. It is the first Pakistani

bank to raise Tier II Capital from external sources.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 10/62

Business Operations

1. Banking Sector Overview

2. HBl’s Performance Overview

3. Products and Services

Personal Banking

Corporate Banking

Online Services

. Virtual Banking

Islamic Banking

4. HBL’s Competitive Strategies

ORGANIZATIONAL CHART

PRESIDENT

↓

BOARD OF DIRECTOR

↓

MEMBER EXECUTIVE BOARD

↓

REGIONAL CHIEF

↓

ZONAL CHIEF

↓

BRANCH MANAGERS

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 11/62

BOARD OF DIRECTORS

Sultan Ali Allana

Chairman

Sajid Zahid

Director

Ahmed Jawad

Director

Sikandar Mustafa Khan

Director

Moez Jamal

Director

ORGANIZATIONAL STRUCTURE

HBL is organized along functional lines with eight core divisions namely Corporate &

International Banking, Retail Banking, International Banking, Audit & B.R.R., Credit

Policy, Asset Remedial Management (ARM), Information Technology Group and Human

Resources Group.

VISION, MISSION AND VALUES

Vision:

Enabling people to advance with confidence and success.

Mission:

To make our customers prosper, our staff excel and create value for shareholders.

Values:

Our values are the fundamental principles that define our culture and are

brought to life in our attitude and behaviors. It is these values that make us unique

and unmistakable. Our values are defined below:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 12/62

• Excellence

• Integrity

• Customer Focus

•

Meritocracy• Progressiveness

PRODUCTS AND SERVICES OFFERED BY HBL

PRODUCTS:

o HBL Muhafiz Rupee Travellers Cheques

o HBL Auto Finance

o HBL Flexi Loans for salaried personnel

o HBL LifeStyles Financing Scheme

o HBL i-Card

o HBL House Financing Loans

o HBL Easy Access

o HBL Fast Transfer

o Haryali Agricultural Loans

o HBL E-Bank

DEPARTMENTS & RESPONSIBILITIES:

During my internship, I came to known about the following departments functioning in my

branch

1. Account opening department.

2. Cash department.

3. Credit department.

4. Lockers department.

5. Bill clearing department.

6. Foreign exchange department.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 13/62

7. I.T department

Account opening department:

In this department customer open the account in the bank. This give facility to the

customer for opening new account with the bank that they allow him and operate this

account.

These require many document to open this account:

Copy of CNIC

Utility bill

Student card

Provisional receipt

Address of customer

Specimen Signature of the customer

Posting the account on the system

Cheque book issue to the customer

Secrecy of the customer

Types of the Account

1. Individual account

2. joint account

3. Business account

4. Current account

5. Saving account

Individual account:

Bank opens this account by individually. It involves single person only.

Bank opens this account for one person.

Joint account:

Bank opens this account by one or two person. The two people use one

account in the bank. Bank considers one account by two people. The two people of

joint account show one account according to the law.

Business account:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 14/62

In this account, bank only business transaction. It is opened by companies,

institution, organization and partnership business. It is purpose of deal with the

businessmen.

Current account:

Bank opens current account to every person. Usually, some current account

have to pay interest by the customer but its rate is low other accounts. Current account

offers any facilities to the customer which is mentioned below:

• Debit card

• Cheque book to the customer

• Automatic bill payments from account

• Overdraft facility

• Clearing services etc.

Reason for closing customer account:

Bank ay close this account due to some reason:

1. Death of a customer

2. Notice by a customer

3. Customer insanity

Death of a customer:

In the case death of the customer, bank may close the account and stop all transaction

related to the person. Bank stop further transaction such as cheque issue, money transfer

etc.

Notice by the customer:

Bank may close this account on the demand of the customer. Customer gives

application to the bank for closing this account.

Customer’s insanity:

Bank terminates this account due to mental of the customer. Bank stop thistransaction with this customer. It is all too easy for the customer’s needs by the desires of

others within a bank who interpret the customer needs through their own prism. His

insanity of the customer, to the knowledge of the bank, has the effect of revoking this

authority, and the bank would not be necessary in paying the acceptances. That the bank

has not been officially notified of the customer's insanity does not indicate

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 15/62

Cash department

Cash department has vital role in the banking sector. All cash transaction represent in this

account such as cash received fro customer, import and export transaction, bill payment

etc. It involves cash payment and receipt transaction in it.

These are following perform various function in this department:

• Acceptance of deposit

• Cheque payment

• Collection of funds

• Remittances

• Transfer of funds from one account to another

• Verification of signature

• Posting

• Heading of prize bond

There are some functions of cash department in the bank:

Receipts and payments:

Cash will be received by the Receipts from the customers in the bank. In the receipts, the

name of the account holder, account number, name of the branch, dates etc are involved.

Customer must also make certain that the receipts are signed by the person which deposit

cash. In some cases, cash is received from receipt department.

Deposit cash in customer account:

When the customer wants to deposit amount in his account .The account in which the

cash wi ll be deposited. Then customer will receive amount and credit the customer’s

account that shows increase in customer’s bank accounts.

Cheque encashment procedure:

• The cash is paid to the customer in the cash department such as:

• Cheque is drawn on some branches

• Cheque is not posted on date

• It should be bearer cheque

Payment of cash:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 16/62

After posting the cheque the operation manager cancelled the cheque and

returned back to cashier . The cashier enters the cheque in cash paid

regi stered and pays against the second signature of receiver on the back of the

cheque.

Credit department

A simple but practical definition of credit is "the ability to buy with a promise to pay," in

other words, to obtain present value for a promise to pay in the future. The word "credit" is

derived from the Latin "credo. The banker knows that he may be asked to expand credit.

He first satisfies himself that the ability is such as to defend assurance. This information is

obtained from personal knowledge of the borrower. Trade inquiries are directed to people

selling goods to and competitors of the borrower. If all this information is satisfactory, the

capital factor is studied in the borrower's financial statement which balance sheet should be

taken off at normal intervals. This ratio is often called the 2 to 1 ratio, but differs in

business. In short, the distinguish between a safe risk and an unsafe one that is the quality

that marks the good banker.

This is including different latter issue in the credit department:

Establishment of letter of credit:

In case party enjoying regular limit, the L.C is established without adopting the procedure

mentioned above. However the amount of L.C should not exceed the regular limit. Themajor non-fund based facilities that are considered as a part of regular credit facilities are

letter of Credit an d Ba nk Gu ar an te e. Banks charge commission for the

services rendered by them and commitments on the pact of the bank these are

allowed after making out a very careful and detailed assessment of borrower’s

requirement.

Types of credit

These are many types of credit of habib bank which are given below:

Demand finance:

• Packing credit

• Demand finance to student

• Loan to staff

Loans are offered to the staff in various categories

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 17/62

1. loan for purchasing vehicles

2. loan correspondent to month’s salary

3. mortgage loan

Running finance:

It include old name overdraft which are meet requirements to the customer.

For example:

• secured

Which are diifernt forms given below

1. share certificate

2. deposits

3. mortgage of property etc

unsecured

DEPOSIT DEPARTMENT

Bank deals in money and they are merely mobilizing funds within the economy. They

borrow from one person and lend to another, the difference between the rate of borrowing

lending forms their spread or gross profit. Therefore we can rightly state that deposits are

the blood of the bank which causes the body of an institution to get to work. These depositsare liability of the bank so from point of view of bank we can refer to them as liabilities.

“REMITTANCES”

DEMAND DRAFT:

Demand draft is a written order drawn by a branch of a bank upon the branch of

same or any other bank to pay certain sum of money to or to the order of specified person.

It can be issued to the customers as well as non customer against cash chaque and letter of

instruction. Demand draft is negotiable instruments that can be negotiating at any time

before its cancellation. Its Legal provisions are same as that of cheque.

Following parties are involved in demand draft:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 18/62

Applicant

issuing branch

Drawee branch

Beneficiary

A demand draft may be issued against the written request of the customer before issuing it

must be seen that the demand draft is in order.

The DD application must be scrutinized by the counter clerk in respect of following points.

There should be branch where payment is to be made.

Full name of payer should be mentioned.

Amount in words and figures must be same

The applicant on two places should sign application.

TELEGRAPHIC TRANSFER:

Telegraphic transfer means the transfer of funds from one branch to another

branch of the same bank or upon other bank under special arrangements just like a

telegram. Telegraphic transfer is not negotiable and the funds are not payable to bearer.

Minor cannot avail this facility. In telegraphic transfer the bankers use secret codes.

One code is with issuing person and the second is with an other person. When they

combine the codes it’s become an amount that is called check. The payment is made

after the confirmation of the check.

Following parties are involved in TT

Applicant

Drawing branch

Drawee branch

Beneficiary

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 19/62

Following important things should be included in TT:

Full name of the beneficiary or account number should be mentioned in the

application form.

Instruction regarding mode of payment should be obtained.

A record in the remittance outward register should be maintained.

All the remittance must be controlled through number or codes.

PAY ORDER:

Pay order is an instrument through which payment can be made from one bank to

another bank. Pay order is meant for bank own payment but in practice they are also issued

to customers.

Following parties are involved in pay order:

Applicant

issuing branch

Payee

MAIL TRANSFER:

Mail transfer is not negotiable and the procedure of it is same with the procedure

of DD.When a customer request the bank to transfer his money from this bank to any other

bank of the branch of same bank in the city, outside the city of outside the country the first

thing he has to do is to fill an application form. In which he states that I want to transfer the

money from this bank to that specific bank by mail. If the customer is the account holder of

this bank, the bank will debit his account and the concerned officer will fill forms to make

the mail transfer complete.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 20/62

If the customer is not the account holder of the bank, then firstly he has to deposit

the money and then rest of the procedure will be adopted to transfer his money.

“ SBP ERF Scheme”

SBP had introduced this scheme to promote country ‘s export and to earn foreign

exchange. This scheme is operated through authorized dealers under SBP control.

This scheme had been amended by time to time.

Features:

• Concessions rate of markup as compare to commercial banks rate of markups.

• Export refinance allow to exporters via authorized dealers.

• In case of default, the SBP recover its principal loan amount, markup & penalty

through the bank to which exporter has submitted his refinance claim.

• Refinance allows against value added products i.e. garments, print, dyed cloths, bed

sets.

• Proceeds repatriated through banking channels.

• Allow credit loan amount within 248 hrs.

• Misutilization of SBP funds has been prohibited, if any violation occurs SBPimposed penalty.

Risk:

• If the exporter has been / will be defaulted the laps of funds of authorized dealers.

• Cheating or misuse of funds, SBP may cause to impose not any penalty but also

termination of bank employee or change of management or authorized dealer’s

reputation may destroy.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 21/62

How to operate this scheme?

SBP ERF scheme

Part I Part II

Post shipment EE EF

Preshipment Party request statement statement

Party request letter L/C sales contract total realization it include

L/C sales contract Under taking & negotiation totalUndertaking DP note SBP financed realization

DP note Form D Form E & not but on which

Form D Commercial invoice availed SBP finance Form E SBPProof of purchase Bill of Lading finance

of raw material Form E availed not

include.

“Part A”

This means after making a shipment the exporter prepare all relevant shippingdocuments and evidence of shipment. The exporter contact his bank w.r.t to lodge the

documents and send a one set of shipping documents to export finances department to

allow him post shipment part I under SBP scheme.Required documents at the time of finance allow to party

D/Pnote

Under taking on non judicial stamp paper

L/C

Party request letter

Form D

Commercial invoice

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 22/62

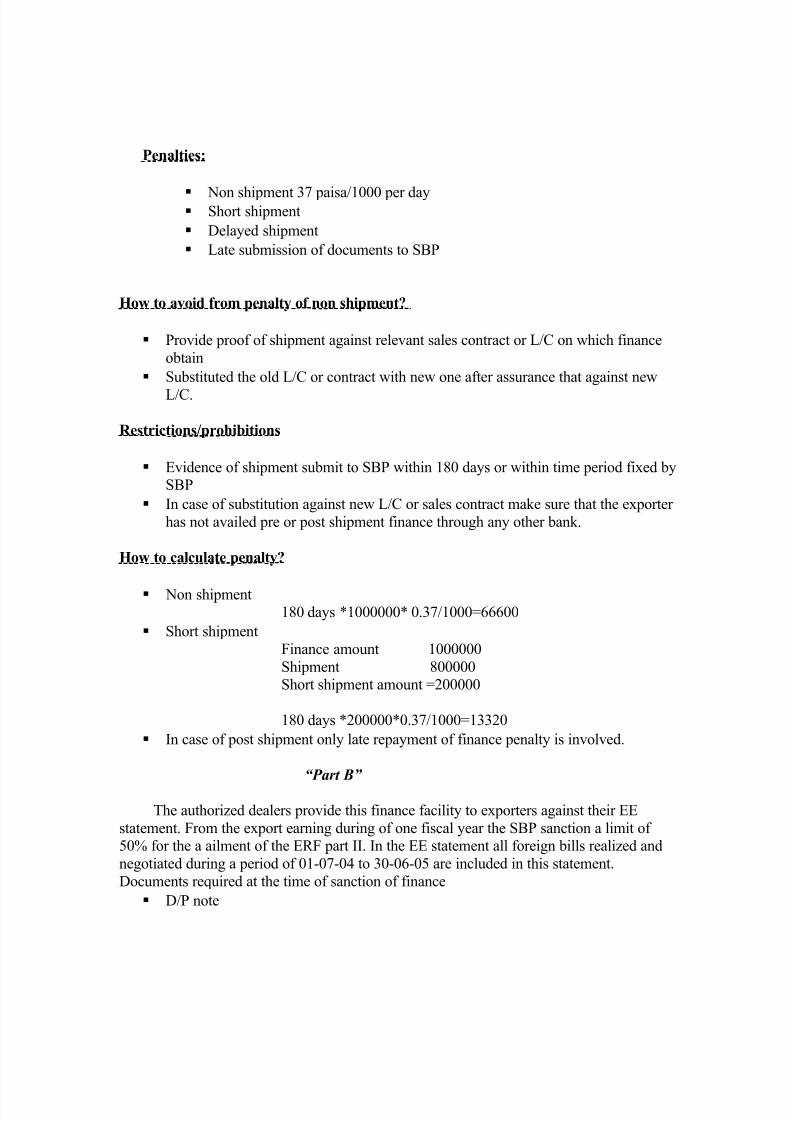

Penalties:

Non shipment 37 paisa/1000 per day Short shipment

Delayed shipment

Late submission of documents to SBP

How to avoid from penalty of non shipment?

Provide proof of shipment against relevant sales contract or L/C on which finance

obtain

Substituted the old L/C or contract with new one after assurance that against new

L/C.

Restrictions/prohibitions

Evidence of shipment submit to SBP within 180 days or within time period fixed bySBP

In case of substitution against new L/C or sales contract make sure that the exporter

has not availed pre or post shipment finance through any other bank.

How to calculate penalty?

Non shipment180 days *1000000* 0.37/1000=66600

Short shipment

Finance amount 1000000

Shipment 800000Short shipment amount =200000

180 days *200000*0.37/1000=13320

In case of post shipment only late repayment of finance penalty is involved.

“Part B”

The authorized dealers provide this finance facility to exporters against their EE

statement. From the export earning during of one fiscal year the SBP sanction a limit of 50% for the a ailment of the ERF part II. In the EE statement all foreign bills realized and

negotiated during a period of 01-07-04 to 30-06-05 are included in this statement.

Documents required at the time of sanction of finance

D/P note

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 23/62

Under taking on non judicial paper

Party request letter

Short fall in EE statement penalty:

Days*amount of finance*rate(0.37)/day/1000

Short fall in EF:

SBP calculate case to case basis daily product and match this with his EF performance, if

he avail excess Refinance from SBP and Business performance is short the SBP imposed a

short fall penalty.Total short product*number of days*0.37/180

Demand Finance & Running Finance:

Demand finance:

This is common form of financing to commercial industrial concerns and is made

available either on pledge or hypothecation of goods, produce or merchandise. In demand

finance the party is finance up to certain limit either at once or as and when required.The party due to facility of a paying mark prefers the financing up only on the amount it

actually utilizes.

Running Finance:

This form of financing was known as Overdraft when a bank customer requirestemporary accommodation, his banker allows withdrawals from his account and runningfinance thus occurs. The accommodations generally allowed against collateral security. The

customer is in advantageous position in a running finance because he has to pay mark up

only on balance outstanding against him on daily products basis.

Pledge:

It is entitled to the exclusive possession of the property until the debt is charged.

Hypothecation:

When the property in the goods is charged as security of loan from the bank but the

ownership & possess

“FAPC & FAFB”

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 24/62

FAPC (finance against packing credit):

It is a type of bank’s own source finance provided to clients engaged in export

trade. As the term packing indicates that the credit line is granted to an exporter for the

purpose of packing merchandise for shipment to an importer abroad. An exporter shouldgive documentary proof to the bank consist of L/C in favor of exporter indicating the

description of the merchandise, the purchase price, date of delivery along with other terms.

FAFB(finance against foreign bills):

It is a post shipment finance facility which is provided by the banks to its clients

after providing the evidence of shipment, he contacts his bank to request him to lodge thedocuments. He then provide the request letter with sale contract to grant him finance & this

department grant him finance (90% value of commercial invoice).

“Imports and exports department”

Exports:

Introduction and registration:

Imports and exports act 1950 have empowered the federal Govt to control the import

and export in Pakistan. Pakistan is developing country and like other developing countries

its imports exceeds than exports. To control this situation the registration of import and

export has been made obligatory under the registration order 1993. The authority of

registration has been given to export promotion bureau. No importer and exporter who has

no granted registration shall indent, import and export of any good into or out of Pakistan.

The requirements for getting registration are as under:

Application form.

Photocopy of I.D card.

Copy of memorandum and article of association (in case of limited company).

Ownership deed of office.

Fee payment.

Certificate of incorporation.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 25/62

Applicant should regular taxpayer.

The major exports from Pakistan are surgical goods, sports goods hand noted goods,

leather goods, textile goods, etc.

Export procedure:

All the exports work under the imports and exports act that is changed by the state

in every year. When the importer send the L.C to bank in respect to import or when the L.C

comes to the advising bank from the issuing bank then the concerned officer allot the

number to the L.C and get registered. The concerned officer write down the name of

issuing bank and the party name in a register and intimate the party about L.C. the exporter

after receiving the L.C from bank will prepare the documents as per the L.C usually the

following documents have to be prepared by the exporter:

Bill of lading

Covering letter

E- Form

Bill of exchange

Packing list

Commercial invoice

Quota documents in case of quota country

Certificate of origin

Special custom invoice

The export form (E-FORM):

E-FORM means “export form” which is the first and foremost requirement for the

exports from Pakistan. It is control instrument by Govt of Pakistan by which it monitors the

receipts from exports and checks the goods that are transferred without foreign exchange.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 26/62

all banks which are engaged with the foreign exchange are required to print and maintained

the E form that is checked by the state bank of Pakistan. For export an e form is issued by

the bank on the request letter of a company. Two separate registers are maintained by the

bank one for his use and the other one are for the requirement of the SBP. On issuance of E

forms the banker lists it in the register and makes sign from the exporters. Banks record the

name of party, amount, the goods description, port of destination, importer name port of

loading etc.

The functional utility of E-FORM:

The export form has four copies. The exporters and banks use it. Without it the

exporter can not make export. These copies are used as:

Original copy is for SBP that is checked by the higher authority.

Duplicate copy is for the bank use that is upraised by the custom authorities.

Triplicate for the use to report of SBP at the time of payment received.

Quartiplacte is for the company used.

Usage of E- FORM:

E- FORM is an important document for export. It has its own importance such as

this form is used as a checker means it monitor that what things are going abroad and in

return what things we are getting. So it creates a check and balance on the foreign

exchange. It shows the total quantity and quality of the goods that is sending to another

country. An E –Form shoe the party worth that is very helpful for the party and the bank.

Bank can create a party limit for the credit on the behalf of it and a party can arrange a loan

for its future requirements from the bank. It shows the terms of payment by the importer

and the delivery terms by the both parties that is helpful in case of any discrepancy during

the contact.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 27/62

Short shipment notice:

A shipment may be cancelled by the importer or exporter due to many reasons.

The cancellation of the export letter is called short shipment notice. In this situation the

company has to inform the bank. Company has to give a written letter to the bank that he is

not the export so please cancelled their e form. On the other hand bank at the time of

receiving the letter will stop the e form and cancelled the all documents.

“ IMPORTS”

Imports regulation:

Import is being regulated by the ministry of commerce and the government of

Pakistan under the import and export act:

Categories of imports:

Imports are classified into the following categories:

Commercial sector imports

Industrial sector imports

Public sector imports

Registration of importers:

A person who wants to approach the bank for importing goods from abroad, he

should have to get himself registered with the export promotion bureau under

registration of imports and exports act. He must fulfill the following conditions before

getting himself registered:

NIC NUMBER

NATIONAL TAX NUMBER

MEMBER OF REGISTERED ASSOSITATION

Documentary letter of credit:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 28/62

A documentary letter of credit is an instrument or document issued by the bank

on the behalf of a customer, authorizing a beneficiary to draw a draft and drafts or

sometimes the requirement of a draft, which will be honored, on presentation by the

bank if drawn accordance with the te3rm and condition specified in the letter of credit.

It is the written undertaking by the bank (issuing bank) pay to the seller

(beneficiary) at the request or as per the instruction given by the opener (applicant) pay

at sight or at the future date, a stated sum of money against the required documents.

The documents include the commercial invoice, certificate of origin, insurance policy

or certificate and the documents of transport relating to the mode sending goods. L/C is

therefore is an arrangement of security for the parties. The conditional guarantee is

related to the documents only and not on the underlying

goods or services.

“Establishment of letter of credit”

Procedure:

The person applying for the letter of credit must be registered with the EPB. The

opening bank verifies this registration or otherwise exemption. This is mentioned in the “I”form. The importer also shows the valid certificate of an organization membership. A

category pass book is issued by the EPB for registered importer specifying his category.

This book is centralized by the centralized banks in the city. It is not necessary for the bank

to hold the original copy of the pass book of all the importers. But some times the importer

gets L.C from more than one bank so the bank have to hold the photo copy of this pass

book. The applicant can get the application from any branch of the Habib Bank Limited.

However only some branches are authorized to open L.C. That branches how are not

authorized have to contact with the authorized branches to open an L.C. The authorized

branches in such case require the certificate from the applicant branch that the required

formalities are fulfilled and the approval was obtained with required margin.

For establishment of letter of credit, the importer requests the opening bank with the

following documents:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 29/62

1) Application and agreement form IB-8:

Credit application form is an agreement between the bank and the customer on the

basis of which the letter of credit is opened. This form contains the undertaking of the

importer that get the documents from the bank at the mark up price. It contains the

following information:

Name and address of importer.

Name and address of exporter.

Amount in foreign currency.

Terms of credit.

Description of goods.

Origin of goods.

Port of loading and discharge.

Last date of shipment.

Foreign bank charges.

Terms of shipment. (Partial shipment or transshipment)

Insurance cover note, policy no, and name of insurance company.

Forward booking.

Mode of transmission.

Import registration no.

Any other documents required.

Detailed documents.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 30/62

2) Performa invoice/ purchase order:

A Performa invoice is quotation of seller containing the description and the

specification of the goods, price, and terms of the sale. Some times the exporter has

their agent in the country. The agent must be registered from the EPB.

3) Insurance cover note:

All the goods imported under the documentary credit must always be insured.

In accordance with our country import policy, insured must be issued by a Pakistani

insurance company or the foreign company operating in Pakistan and such company

must be approved by the bank. Insurance covered based on the following:

It is issued in the name of issuing bank A/C importer.

The rider should cover against war.

The port of shipment and the port of destination.

Amount of premium prepaid.

Shipment period. The description of goods should be the same as per the form.

4) Appendix B:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 31/62

This Performa replaces the import license and is submitted along with L.C

application form duly filled in triplicate. It is conditional undertaking that the imports

goods are not banned, not smuggled. It is also an undertaking that if the bank is unable to

arrange the said currency the importer have to purchase it from other banks or from any

other place. It includes the details and description of goods, codes, class, type, source of

import, country of import, Performa invoice no etc.

5) “I” FORM:

This form is used at the time of retirement of documents against L.C established

earlier for reporting to the transaction to SBP through the bill of entry deptt. It has four

copies that is used as follows:

Original is for the use of SBP.

Duplicate for the authorized dealer to be used for processing exchange control.

Triplicate for the authorized dealer record.

Quartiplacte is for the submission in SBP in the case of import where the

documents are not retired.

“ Approval for establishment of letter of credit”

After scrutiny of the documents, IB-8 along with attached documents is put before the

corporate head for approval. If the amount of application exceeds the power of the

corporate head the branch concerned prepared the memorandum for the corporate banking

head for obtaining his approval.

In case party enjoying regular limit, the L.C is established without adopting the procedure mentioned above. However the amount of L.C should not exceed the regular

limit.

Types of letter of credit:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 32/62

1) Revocable credit:

The letter of credit that can be cancel with the consent of importer, without

giving any prior information to the exporter.

2) Irrevocable letter of credit:

The letter of credit that can be cancelled by the mutual consent of the both

parties. Only one party cannot cancel it.

3) Irrevocable confirmed letter of credit:

When an issuing bank authorizes and or request to an other bank to

confirm his irrevocable credit and adds its confirmation. Such confirmation constitutes

a definite undertaking of such bank in addition to that of the issuing bank. There are

following other letter of credits:

1. Revolving Credit

2. Transferable Credit

3. Back to Back Credit

4. Green Clause Credit

5. Red Clause Credit

6. Clean Documentary Credit

7. Transit Credit

8. Stand by Credit

9. Sight Credit

Parties to a credit:

The applicant:

The applicant of the letter of credit is called the importer or buyer. The buyer

requests to the bank to open a documentary letter of credit in favor of the seller.

Opening bank (issuing bank or importer bank):

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 33/62

At the request of the importer an issuing bank issues a credit under the instructions

in the favor of the seller.

Advising bank:

An advising bank is a bank in the seller’s country. The issuing bank forwards the

advice of the credit by mail or by any mode to the correspondent bank in the exporter

country as instructions of the opener.

Beneficiary (exporter):

The person or body receiving the letter of credit from the importer that is opened

in favor of him.

Confirming bank:

The bank that on the requests of the issuing bank adds confirmation to a credit. It is

definite undertaking of the confirming bank, in addition to the issuing bank.

Negotiating bank:

It May or may not be the advising bank. An authorized bank that gives the value to

the draft for processing and payments.

Reimbursing bank:

Reimbursing bank is the bank, which on the behalf of the opening bank, honors the

Reimbursing claim lodged by the negotiating bank.

Modes of payment :

Sight letter of credit:

The seller submit all the documents with draft in the importer country

Complying with the all terms and conditions. The payments are made on the presence

of the documents.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 34/62

Usance letter of credit:

Under these circumstances it is agreed that the payment will be made after a

specified period. So the payment is made after or on the expiry of that date.

Risks for importer and exporter:

Importer’s risks:

He does not know the seller.

He does not know that goods will be delivered in time.

He does not know how to check the goods.

Exporter’s risks:

He does not know the buyer.

He does not know the credit worthiness of the buyer.

He does not wait for payment.

He does not wait for exchange control.

Buyers and sellers obligations:

The seller’s obligations:

Provision of goods as per contract.

License authorization and formalities.

Contract of carriage and insurance.

Delivery at time.

Transfer of risk.

Division of cost.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 35/62

Notice to buyer.

Proof of delivery.

Good checking marking and packing.

Other obligations.

Buyer’s obligations:

Payment of price.

License authorization and formalities.

Contract of carriage and insurance.

Taking Delivery at time.

Transfer of risk.

Division of cost.

Notice to seller.

Proof of delivery.

Inspection of goods.

Possible problems in international trade:

Non-payment.

Delay in delivery.

Financing, how and against what.

Currency restrictions.

Regulatory restrictions.

Documentation and mode of settlement.

ICC rules and INCO terms.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 36/62

HUMAN RESOURCE DEPARTMENT

FUNCTIONAL RESPONSIBILITIES:

Right Now the responsibilities assigned to HR department at Corporate Center

can be categorized under three heads:

Staff matters / Basic HR Functions Expenses control

Security matters

Now I’ll discuss these one by one::

Background:

The banking council of Pakistan was responsible for the recruitment, selection and

allocation of human resources. After the dissolution of the Pakistan Banking Council, theBanking & Financial Services Commission of Pakistan is responsible for these activities.

Procedure:

Staff requirements are met according to the changing needs of macro environment

scenario and particularly the arising needs of the bank itself. A need analysis is conducted.

After assessing the human resources requirements and screening of the applications, most probably, the suspects are invited for a written test.

Short listed candidates are called for an interview for personality and social appraisal.

Interviews are a mix of direct and indirect interviewing techniques and informationrequired.

The selected candidates are sent for training of six months training from MDI’s.

The training is through the lectures regarding banking procedural guidelines and other

behavioral aspects. After the completion of training employees are allocated to differentoffices. The effective management of people in an organization requires an understanding

of motivation, job design, reward systems, and group influence.

Recruiting Retention

Succession planning

Risk Management

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 37/62

Diversity in our workforce

Management information

Progressive compensation and benefits design and implementation Employee communications and relations

Training needs analysis, program design and implementationTraining needs analysis, program design and implementation

Performance evaluationPerformance evaluation

Work-life initiatives

“CREDIT & ADMINISTRATION DEPARTMENT”

The responsibility of providing administrative support for the lending activities of the Bank, and day-to-day monitoring of credit-exposure, is vested in the Credit

Administration Department (CAD).

FUNCTIONAL RESPONSIBILITIES:

The main responsibilities under this department are:

Implementation of credit facility and their maintenance according to terms of credit

approved.

Ensure that standard loan documentation for each credit facility is maintained and

the correctness & completeness of such documentation and also responsible for

custody of all credit files.

Maintain the safe custody of all collateral as per bank’s standard operating

procedures; undertake periodic evaluation and inspection of hypothecated/ pledgedinventories in accordance with the terms of credit.

Ensure compliance with

Institutional credit policies & procedures

Local regulatory requirements.

Prepare various portfolio composition reports and other documentation for submission to GRM’s & RM’s.

CREDIT FACILITY IMPLEMENTATION PROCEDURE:

Upon approval of credit proposal, the credit proposal and approval are handed over

to CAD. Now CAD determines the nature of documentation required and on receipt of same ensures that all legal documents are obtained and are legally enforceable. After all

these activities it can release the facility for utilization.

“ MARKETING DEPARTMENT”

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 38/62

The marketing department in HABIB BANK LIMITED is very strong. It is the

main source of gaining and maintains the customers that can give a large profit to the bank.There are five relationship managers in Habib bank and every person is responsible for the

credit of his party.

CUSTOMER DEALING:

HBL corporate center only deal with the following categories of business:

The organization that have minimum 250 million sales in a year.

The organization that have availed 80 million finance

Agri based industry.

HBL do not deal with the agriculture sector.

PROCEDURE FOR CREDIT APPROVAL:

It is the responsibility of the relationship manager to provide or fulfill the

requirement of the customer by checking his financial and position. The procedure of

credit approval starts with the credit proposal. First of all the customer request to the bank for credit and on the behalf of him the RM check the memorandum. The

Memorandum includes:

The company information.

Purpose of credit. Assessment of management.

Risks.

Financial analysis.

Third party or other bank information.

Conclusion and recommendations.

Then the RM sends it to the authorities who accept or reject the proposal. If they accept the

proposal they announced a credit range for the party. At the end RM sends the proposal to

CAD deptt custody and check.

EXCESS FACILITY CREDIT BY RM:

Relationship manager is authorized to provide the excess facility to the customer than the credit line. It may be up to

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 39/62

10 percent of excess amount

OR

12.5 million Whichever is less?

It is not more than 15 days if the customer wants to increase this facility he has to contact

with the head office.

TYPES OF CREDIT FACILITY:

1) fund based:It is first type of credit facility. In this facility the bank actually provides fund to

customers.

2) non fund base:

Second type of credit facility that does not provides fun but only give the guarantee.If the customer is unable to make the payment at maturity date then bank will be

responsible to make the payment.

10. PLAN OF INTERNSHIP PROGRAMME

Every body knows that knowledge does not increase without practice .practice is animportant mean to improve the knowledge. Therefore university provides internship

programmed of six to eight week in different organization during MBA so that we could

able to apply in theoretical concepts to practical.I started internship on 5th may to 25th June in water works road branch of habib bank.

Work done by me in HBL in different departments:

1. Account opening department.

2. Data punching department.

3. Public dealing department.

ACCONTS OPENING DEPARTMENT

In this account department I gain the particle knowledge about opening. This department

deals with opening account and saving account for its customer and all matters regarding

there off. The customer opening account/saving accounts can be categorized as following:

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 40/62

1) individual

2) firm

3) company

4) trust

5) staff

6) others

OPENING AN ACOOUNT:

In order to open an account first of all the customer has to fill a form prescribed by

the bank. The person is required to bring some reference or introduction for opening the

account. Introducer may be a person who has an account with HBL.

Some important information regarding introducer e.g. the name and account

number of the introducer is written on the space provided on the specimen signature cards.

Then in order to find out whether he is a true introducer or not a letter is sent to him

thanking him for this introduction, so that any thing wrong may come into notice.

There are different requirement for different types of accounts and account holders. An

important thing is that the customer should have a corporate customer. The corporate

customer limit is 40 million and this branch always deals the corporate customer.

General rules for opening an account:

One person can open only one account in the same branch with the same

category.

In the event of death of an account holder the credit balance will be transfer to

the heirs of the diseased individual account.

Services charges will be deducted periodically as prescribed from time to time

on the accounts that are under the limit of specific account.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 41/62

Services charges are not applicable on that accounts that are prescribed as

exempted.

A distinctive number will be allotted to the each account.

The bank can close those accounts that are under the minimum limit of the

bank.

Any sum to be deposited in the account should be accompanied by paying in

slip showing the party account number and the name.

Account holder can only withdraw the sum of money by his own account by

cheque.

Cheque should be signed by the account holder by the specimen given by the

bank.

Post dated and defective cheque is not accepted.

If statement of account spoiled a new will be issued on cost.

Any change in the address should immediately communicate to the bank.

The account holder wishing to close the account must surrender the cheque

book.

Account may be transfer from one branch to another same branch without any

charges etc.

Data punching

Data punching means feeding of data collected into the computer daily or weekly. We

punch data daily which include in the account. First, we enter transaction of customer on

the basis of buying and selling daily in the customer account then we punch customer data

one by one according to dates and sequence. Through data punching, we can easily transfer

the data and money to another account and determine the account information. After debt

and credit amount, we punch data according to their account in the computer so that we

could check data easily. We make cash debit vouchers.cash credit vouchers,sundry debtor

and sudry credit vouchers,transfer vouchers,internal account vouchers ,cross branch

vouchers. We give detail in the system .these all

Public dealing

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 42/62

Public dealing means have good behavior with the public for increasing efficiency and

growth. Bank deals with the customer and provides information of accounts and others

which relates to the accounts. Bank guides that how to open account and forms fill to open

new account. Bank issues cheque to the customer for opening new accounts. Bank asks to

the customer about their needs and requirements and fulfill on time.

Following are includes in public dealing: Accounts Opening, Check book issuance,

Standing instructions, Marking stock payments, Debit Credit card issuance, Activation of

dormant accounts, Making inoperative account into operation, Recovering of multiple

charges availing bank facilities, issuance of bank account statements

Open new accounts to the customer.

Issuance cheque to the customer.

Provides information for opening new account to the customer.

Establish good behavior with the customer to increase our product and services.

To solve their problems which create open accounts etc.

13 .Financial Analyses

Balance Sheet 2010 2009 2008

As at December 31, 2007 (Rupees in '000)

Assets

Cash & Balances with Treasury Banks 81,516,883 79,527,191 5 6,533,134

Balances with other Banks 35,990,301 29,560,309 39,364,297

Landings to Financial Institutions 30,339,344 5,352,873 6,193,787

Investments 245,016,986 209,421,147 129,833,446

Advances 434,998,560 432,283,588 456,355,507

Other Assets 15,876,545 16,475,939 34,588,444

Operating Fixed Assets 8,835,326 8,172,590 14,751,252

Deferred Tax Asset 34,478,466 40,333,882 12,186,848

887,052,411 821,127,519 749,806,715

Liabilities

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 43/62

Bills Payable 9,774,749 10,041,203 9,828,082

Borrowings From Financial Institutions 37,430,333 48,121,649 46,961,165

Deposits and other Accounts 721,069,137 653,452,460 597,090,545

Subordinated Loans 4,281,835 4,212,080 3,954,925

Liabilities against assets subject to finance lease

Other Liabilities 24,971,618 26,204,580 2 5,663,411Deferred Tax Liability

797,527,672 742,031,972 683,498,128

Net Assets 8 9,524,739 79,095,547 6 6,308,587

Represented By:

Shareholder's Equity

Share Capital 10,018,800 9,108,000 7 ,590,000

Reserves 27,671,813 25,801,889 23,656,044

Un appropriate Profit 4 4,121,103 36,325,458 3 1,933,178

Total equity attributable to the equity holders of the

Bank 8 1,811,716 71,235,347 6 3,179,222

Minority Interest 7,713,023 7,860,200 8 90,099

Surplus on revaluation of assets - net of tax

8 9,524,739 79,095,547 6 6,308,587

Profit and Loss Account 2010 2009 20

For the year ended December 31, 2007 (Rupees in '000)

Mark-up/return/interest earned 7 9,999,852 74,751,375 63,376,0

Mark-up/return/interest expensed 3 4,090,368 33,088,536 26,525,5

Net Mark-up/interest income 4 5,909,484 41,662,839 36,850,4

Provision against Non-performing loans and advance-net 7 ,559,458 8,276,180 6,904,9

Reversal/provision against off-balance sheet obligations 3 0,895 (51,396) 3 72,5

Reversal of provision against diminution in value of

investments 3 89,273 1 ,387,354 1,909,8Bad debts written off directly

7 ,979,626 9,612,138 9,187,4

Net mark-up/interest income after provisions 3 7,929,858 32,050,701 27,663,0

Non-market/interest income

Fee,commision and brokerage income 4 ,928,705 4,620,148 4,518,4

Income/gain on investments 6 07,440 452,823 1 ,300,9

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 44/62

Income from dealing in foreign currencies 2 ,893,454 1,692,776 2 ,374,3

other income 2 ,619,905 3,176,865 3 ,088,9

Total non-mark-up/interest income 1 1,049,504 9,942,612 1 1,282,6

4 8,979,362 41,993,313 3 8,945,7

Non-market/interest expense

administrative expenses 2 3,053,860 21,733,407 21,425,3other provision offs-net 1 78,148 372,957 2 00,1

other charges 1 78,700 3 ,540 64,7

Total non-mark-up/interest expenses 5 11,373 397,668 3 23,5

Profit Before Taxation 2 3,922,081 22,507,572 22,013,8

2

5,057,281 19,485,741

16,931

32

Taxation

current 9 ,331,828 7 ,827,137 8 ,308,6

prior years 6 94,898 (1,079,473) 2 33,1

deferred (582,499) 4 39,434 (2,473,89

9 ,444,227 7 ,187,098 6,067,8

Profit after taxation 1 5,613,054 12,298,643 10,864,1

Attributable to:

Equity holders of the Bank

Minority Interest

Basic and diluted earnings per share 1 5.58 1 2.28 1 1

Cash Flow Statement 2010 2009 200

For the year ended December 31, 2007 (Rupees in '000)

CASH FLOWS FROM OPERATING ACTIVITIES

Profit before taxation 25,057,281 19,485,741 16,931,93

Less: Dividend income and share of profit of associated

and

joint venture companies (318,539) (281,152) ( 1,111,810)

Gain on sale of investments - net (288,836) (171,403) (197,242

(607,375) (452,555) (1,309,052

24,449,906 19,033,186 15,622,88

Adjustment for:

Depreciation/amortization/adjustments 1,666,058 1,670,958 1 ,625,94

Reversal against diminution in the value of investments 389,273 1,387,354 1 ,909,88

Provision against Non-performing loans and advances-net

of reversals 7,559,458 8,276,180 6 ,904,91

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 45/62

Amortization of premium on investments (65) (268) 8 ,07

Gain on sale of property and equipment-net 69,755 257,155 8 54,92

Miscellaneous provisions (16,993) (29,386) ( 41,840

209,043 321,561 5 72,76

9,876,529 11,883,554 11,834,67

34,326,435 30,916,740 27,457,55Increase/decrease in operating assets

Government securities

Landings to financial institutions (24,986,471) 840,914 (4,565,657

Loans and advances (10,274,430) (4,851,108) ( 81,087,69

Other assets-net 5,859,907 (1,951,264) (6,355,923

(29,400,994) (5,961,458) ( 92,009,27

Increase/decrease in operating liabilities

Deposits and other accounts 67,616,677 81,053,273 6 5,792,41

Borrowings from financial institutions (10,691,316) 4,098,973 ( 12,033,444

Bills payable (266,454) 260,126 (5,590,148

Other liabilities-net (1,350,947) 4,083,696 5 ,657,0855,307,960 89,496,068 53,825,91

60,233,401 114,451,350 (10,725,809

Income tax paid-net (10,137,565) (12,265,104) (11,600,790

Net cash flows from operating activities 50,095,836 102,186,246 ( 22,326,599

CASH FLOWS FROM INVESTING ACTIVITIES

Net investments in securities, associated and joint venture

companies (35,957,034) (78,588,907) 37,444,49

Dividend income received 319,465 624,628 2 37,29

Fixed capital expenditure (948,433) (1,835,161) ( 2,662,83Proceeds from sale of fixed assets 51,667 104,288 1 08,03

Effect of translation of net investment in foreign branches

308,61

9 1,689,707

3 ,

037,018

subsidiaries and joint ventures

Net cash flows from investing activities (36,225,716) (78,005,445) 38,163,99

CASH FLOWS FROM FINANCING ACTIVITIES

Sub-ordinate Loans

(58,868)

Dividend Paid (5,450,436) (4,173,059) ( 2,730,25

Net cash flows from (used in )financing activities (5,450,436) (4,173,059) (2,789,119

Increase in cash and cash equivalents during the year 8,419,684 20,007,742

1 3,048,281

Cash and cash equivalents at beginning of the year 108,541,351 84,639,657 7 5,518,83

Effects of exchange rate changes on cash and cash

equivalents 546,149 4,440,101 7,330,32

109,087,500 89,079,758 82,849,15

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 46/62

Cash and cash equivalents at end of the year 117,507,184 109,087,500 9 5,897,43

Liquidity Ratios

In graphs 2008 should be near origin . Round the

figures upto 2 decimal places

You need to provide complete working of the ratios. You are required

to carefully study the table regarding “maturities of assets and

liabilities”. Where you can easily find the current and long

term part of assets and liabilities. Assets and liabilities having

upto 1 year maturity are considered as current assets and

current liabilities . This table is given in the annual report of

the selected bank. You need to re-calculate the current andlong-term parts of assets and liabilities according to this table.

The liquidity of a firm is measured by its ability to satisfy its short term

obligations as they come due. These are includes:

Current Ratio:

Current ratio = current asset/current liabilities

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

843738619/770745837 772621047/737819892 666335481/679543203

1.0947041 1.0471675 0.9805638

0.9

0.95

1

1.05

1.1

2010 2009 2008

habib bank

limited

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 47/62

Comments:The current ratio of 2010 and 2009 is quite acceptable as compare to 2008.

It means that its current ratio is less liquid. There is small increase in industry’s ratio which

can meet the short term obligations of 2010 and 2009 as compare to 2008.

Acid Test Ratio:

Acid test ratio =

0

0.2

0.4

0.6

0.8

1

2010 2009 2008

HABIB BANK

LIMITED

current

asset – inventories – prepaid expanses/current liabilities.

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

843738619-434998560

/770745837

772621047-432283588

/737819892

666335481-45635507

/679543203

0.5303176 0.4612744 0.9134077

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 48/62

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2010 2009 2008

HABIB BANK

LIMITED

Comments:

The acid test ratio indicates good sign in the overall liquidity of industry. It is

a small increase in the acid test ratio.

Working capital:

Working capital = current asset/-current liabilities

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

843738619/770745837 772621047/737819892 666335481/6795432031.0947041 1.0471675 0.9805638

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 49/62

0.92

0.94

0.96

0.98

1

1.02

1.04

1.06

1.08

1.1

2010 2009 2008

HABIB BANK

LIMITED

Comments:

Working capital ratio is increasing than previous ratio. In the year of 2010, the

current assets is high than current liabilities. Therefore, working capital ratio is also high ascompare to others year because its assets and liabilities are lower.

Leverage RatiosThe leverage ratio may be defined as financial ratio which is magnification of risk and

return introduced through the use of fixed cost financing such as debt and preferred stock Leverage ratios measure the degree of protection of suppliers of long term

funds.

These include:

• Times Interest Earned= Earning Before Interest and Taxes (EBIT)

Interest Expenses

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”2 3,922,081/34090368 22,507,572/33088536 22,013,850/26525556

0.7017255 0.6802227 0.829911

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 50/62

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

2010 2009 2008

HABIB BANK

LIMITED

Comments:

The time interest ratio shows the lower value. Firm is not able to fulfill its

interest obligations. It is also called interest coverage ratio.

Debt Ratio:

Debt Ratio= Total liabilities/ total assets.

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

797,527,672/887,052,411 742,031,972/821,127,519 683,498,128/749,806,715

0.8990762 0.9036745 0.9115658

0.89

0.895

0.9

0.905

0.91

0.915

2010 2009 2008

HABIB BANK

LIMITED

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 51/62

Comments:

These values indicate that the firm has financed close to total of its assets with

debt. The higher this ratio, the greater the firm’s degree of indebtedness and the more

financial leverage it has.

Debt-Equity Ratio:

Debt-equity ratio = total liabilities / total share holder equity.

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

797,527,672/81811716 742,031,972/71235347 683,498,128/63179222

9.7483308 10.416626 10.818401

0.89

0.895

0.9

0.905

0.91

0.915

2010 2009 2008

HABIB BANK

LIMITED

Comments: It is a ratio of amount invested by outsiders to the amount invested by the

owners of the business. This ratio indicates the low margin of safety to the creditors.2009and 2008 has high ratio as compare to 2010. The firm would not be able to meet the

creditors claim because of low assets or shareholder equity.

Debt to Tangible Net worth Ratio:

Tangible Net worth Ratio:

Tangible net worth ratio =total assets- intangible asset-total liabilities.

Debt to tangible net worth ratio= Total Debt / Tangible Net worth Ratio.

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 52/62

working of Tangible net worth required

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

9.7483308 /80689413 10.416626/70922957 10.818401 /51557334

1.2081 1.4687 2.0983

0

0.5

1

1.5

2

2.5

2010 2009 2008

HABIB BANK

LIMITED

Total Capitalization Ratio:

Debt to total capital ratio =long term debt/ (long term debt -+shareholder equity).

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

750322590/(750322590-+8

1,811,716)

683869120/(683869120-

71,235,347)

856678881/(856678881-6

3,179,222)

750322590/668510874 683869120/612633773 856678881/793499659

1.122379 1.1162772 1.079621

0

0.2

0.4

0.6

0.8

1

1.2

2010 2009 2008

habib bank

limited

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 53/62

Comments:

This ratio is relating the long-term debt to the permanent capital of the bank. It

shows that the fixed assets decrease than previous years which show a good sign. This ratio

is considered to be satisfactory.

Profitability Ratios

“Profitability measures enable the analyst to evaluate the bank or firm’s profits with respect

to a given level of sales, a certain level of assets or the owner’s investment . Without

profits, a bank or firm could not attract outside capital”

Net Profit Margin:

Net profit margin = (Net income/ Net sale) * 100

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

(15,613,054/79,999,852)*100 (12,298,643/74,751,375)*100 (10,864,112/63,376,047)*100

19.52% 16.45 % 17.14%

14

15

16

17

18

19

20

2010 2009 2008

HABIB BANK

LIMITED

Return on Assets:

Return on Asset = Profit before Tax / Total Assets *100

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 54/62

(23,922,081/887,052,411)*100 (22,507,572/821,127,519)*100 (22,013,850/749,806,715)*100

2.69681 2.74106 2.93594

2.55

2.6

2.65

2.7

2.75

2.8

2.85

2.9

2.95

2010 2009 2008

Comments:

This ratio shows that the returns on assets are decreasing as compare to

previous years but overall profit with its available assets is increasing.

DuPont Return on Assets:

DuPont return on assets = (Net income/sale)*(sale/total asset) *100

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”

(15,613,054/79,999,852)*( 79,999,852/887,052,411)*100

(12,298,643/74,751,375)*(74,751,375/821,127,519)*100

(10,864,112/63,376,047)*(63,376,047/749,806,715)*100

1.7604 1.4975 1.4487

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2010 2009 2008

HABIB BANK

LIMITED

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 55/62

Operating Income Margin:

Operating income margin = (EBIT/ Net sale) *100

0

0.2

0.40.6

0.8

1

1.2

1.4

1.6

1.8

2010 2009 2008

HABIB BANK

LIMITED

Return on Operating Assets:

Return on operating assets = (EBIT/operating asset)*100

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”( 2 3,922,081

/887,052,411)*100(22,507,572/821,127,519)*100 (22,013,850/749,806,715)*100

2.69681 2.74106 2.93594

2.55

2.6

2.65

2.7

2.75

2.8

2.85

2.9

2.95

2010 2009 2008

HABIB BANK

LIMITED

8/2/2019 Spring 2011 FINI619 Habib Bank Limited

http://slidepdf.com/reader/full/spring-2011-fini619-habib-bank-limited 56/62

Comments:

This ratio indicates that bank’s growth is not good. It can not cover all assets

or expenses through net profit before tax easily. Its not able because its ratio is decreasing

than previous years.

Return on Total Equity:

Return on total equity = (Net income/ total equity)*100

2010

Rs. In “000”

2009

Rs. In “000”

2008

Rs. In “000”