spreckels community services district · spreckels community services district regular meeting of...

TRANSCRIPT

Spreckels Community Services District REGULAR MEETING OF THE BOARD OF DIRECTORS

January 17, 2018 6:30pm

Spreckels Veterans Memorial Building, 5th & Llano, Spreckels, CA 93962

AGENDA Agenda order may be adjusted by Chair for purposes of meeting flow and to be respectful of the time

concerns of guests present.

If you will be attending a meeting and would like to request translation into a language other than English, including sign language interpretation, please notify the office at (831} 455-7855 or by email to <[email protected]> at least 48 hours prior to the time of the meeting. In compliance with the Americans with Disabilities Act, for those requiring special assistance to access the Board meeting room, to access written documents being discussed at the Board meeting, or to otherwise participate at Board meetings, please contact the Business Manager's Office at {831} 455-7855 for assistance. Notification of at least 48 hours before the meeting will enable the Spreckels Community Services District to make reasonable arrangements to ensure accessibility to the Board meeting and to provide any required accommodations, auxiliary aids or services. Documents provided to a majority of the Board of Directors regarding an open session item on this agenda will be made available for public inspection in the Business Manager's Office located at the Spreckels Veterans Memorial Building, 5th & Llano, Spreckels, CA 93962 during normal business hours.

1. Opening Business

1.1 Call to Order

1.2 Roll Call & Establishment of Quorum

Ron Eastwood, President James Riley, Vice President Scott Henningsen, Director Otto Kramm, Director Cathy McDougall, Director Paul Ingram, Business Manager & Clerk to the Board

1.3 Pledge of Allegiance

1.4 Adoption of Agenda Changes, additions and approval of the Agenda as presented. 2/3 vote required if any item is added to the Agenda.

1.4.1 Changes to the Agenda 1.4.2 Additions to the Agenda 1.4.3 Adoption of the Agenda

1

2

RECOMMENDATION/ACTION: Paul Ingram, Business Manager

"That the Board of Directors of the Spreckels Community Services District adopts the agenda as presented."

2. Communications

2.1 Correspondence:

2.2 Oral Comments from the Public

(At this time any person may comment on any item not on the agenda. Please state your name and address for the record. Action will not be taken on any item that is not on the agenda. If it requires action, it will be referred to staff and/or placed on the next agenda. Board members may briefly respond to statements made or questions posed as permitted by Government Code Section 54954.2. In order that all interested parties have an opportunity to speak, please limit comments to a maximum of five (5) minutes. Any member of the public may comment on any matter listed on this agenda at the time the matter is being considered by the Board of Directors.)

3. Approval of the Minutes

RECOMMENDATION/ACTION: At the Pleasure of the Board

3.1 Approval of the Minutes of the Regular Meeting of the Board of Directors November 17, 2017.

4. Business Manager's Report

4.1 Monthly Financials

5. Unfinished Business Action Items

5.1 Approval of Spreckels Community Services District Board Policies document.

5.2 Selection of Officers CV 2018.

5.3 Approval of contract for installation of new streetlight at NE corner of Hatton Avenue and Spreckels Boulevard.

5.4 Authorize Plumber to cap water service from defective backflow prevention device at 2nd Street Pump House for closed account in order to prevent backflow prevention device testing cost in future years.

6. New Business Action Items

6.1 Review of Accounts Payable:

2

3

a. Paul J. Ingram Company Management Services $ 500.00

b. Clarke's Turf & Water Landscape Services $ 600.00

c. Spreckels Memorial Dist. AT&T $ 49.18

d. Spreckels Water Company $ 174.41

e. PG&E New Streetlight $ 1,310.60

f. PG&E Streetlights & Pump $ 775.00

TOTAL $ 3,409.19

RECOMMENDATION/ACTION: Paul Ingram, Business Manager

"That the Board of Directors of the Spreckels Community Services District approves the Accounts Payable for the period of January 2018."

6.2 Comparison/analysis of proposals for audit services

6.2.A Possible approval of Letter of Engagement with McGilloway, Ray, Brown and Kaufman for audits of fiscal years 2011, 2012, 2013, 2014.

6.2.B Possible approval of Proposal for Fiscal Auditing Service with Fechter & Company for audits of FY's 2011, 2012, 2013, 2014 and 2015.

6.3 Approval of contract for installation of new streetlight at NE corner of Hatton Avenue and Spreckels Boulevard.

6.4 Approve Business Manager 4 hours additional time for each two-year audit for delinquent years for Audit Request List preparation and research.

7. Unfinished Business Non Action Items

7.1 LAFCO Research on combining Spreckels Community Services District and Spreckels Memorial District.

8. New Business Non Action Items

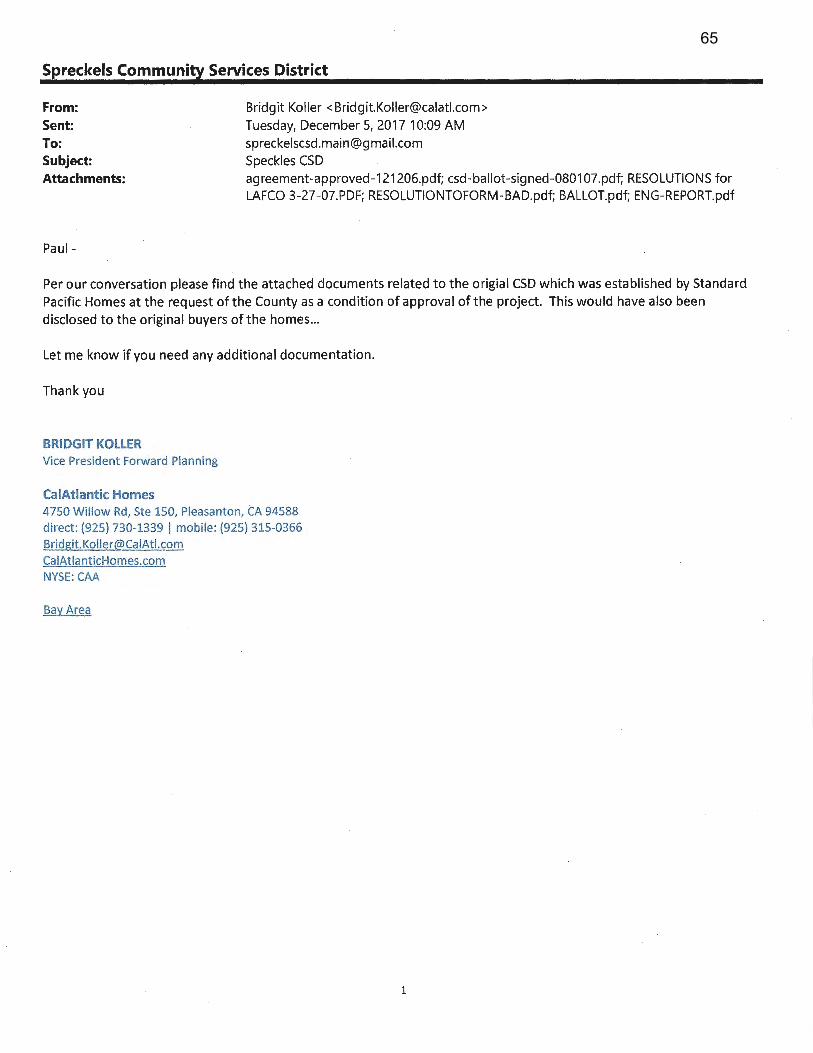

8.1 Form 700: Statement of Economic Interest Deadline April 2, 2018 823 Research on possible additional PG&E accounts for service to pump stations. 8.3 Research on original documentation for Zone 2 Standard Pacific assessment received

from CalAtlantic Homes.

9. Comments by Members of the Board

9.1 Board Members:

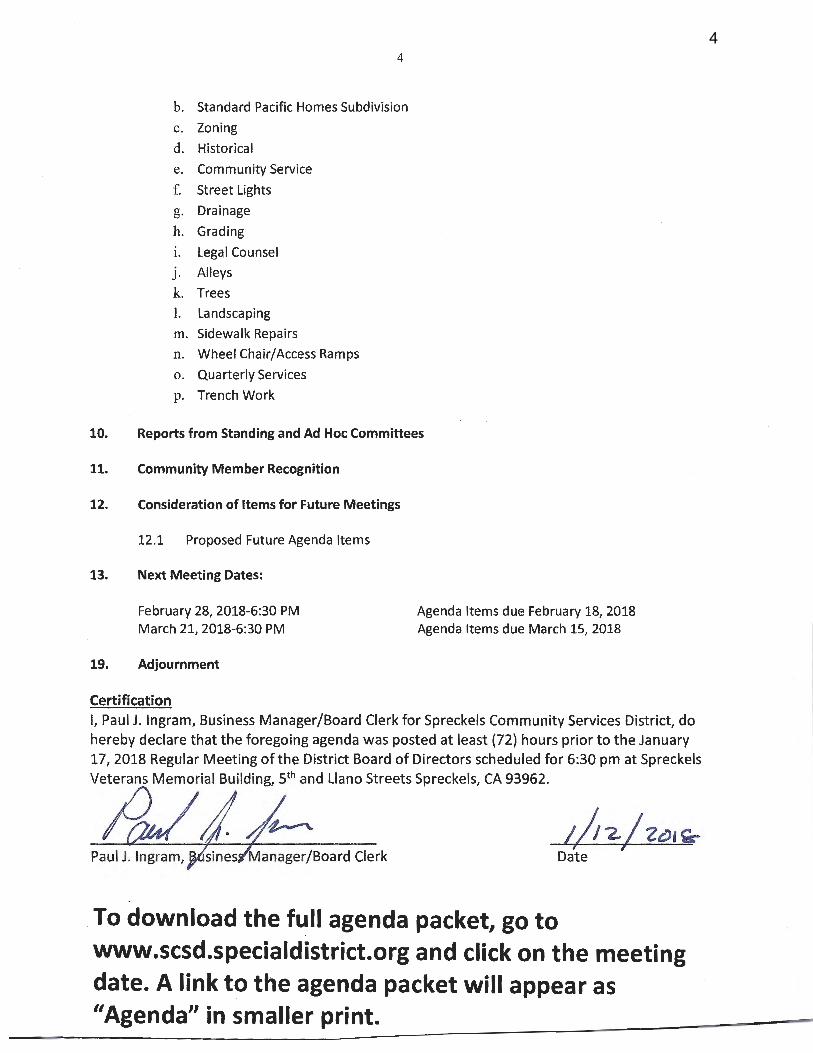

a. Mitigation Fees

3

4

b. Standard Pacific Homes Subdivision

c. Zoning

d. Historical

e. Community Service

f. Street Lights

g. Drainage

h. Grading

1. Legal Counsel

j. Alleys

k. Trees

I. Landscaping

m. Sidewalk Repairs

n. Wheel Chair/Access Ramps

o. Quarterly Services

p. Trench Work

10. Reports from Standing and Ad Hoc Committees

11. Community Member Recognition

12. Consideration of Items for Future Meetings

12.1 Proposed Future Agenda Items

13. Next Meeting Dates:

February 28, 2018-6:30 PM March 21, 2018-6:30 PM

19. Adjournment

Certification

Agenda Items due February 18, 2018 Agenda Items due March 15, 2018

I, Paul J. Ingram, Business Manager/Board Clerk for Spreckels Community Services District, do hereby declare that the foregoing agenda was posted at least (72) hours prior to the January 17, 2018 Regular Meeting of the District Board of Directors scheduled for 6:30 pm at Spreckels VA Memorial Building, S'" and Llano Streets Spreckels, CA 93962.

;/t-z/zi>1~ Date

To download the full agenda packet, go to www.scsd.specialdistrict.org and click on the meeting date. A link to the agenda packet will appear as "Agenda" in smaller print.

4

Spreckels Community Services District MINUTES OF THE REGULAR MEETING OF THE BOARD OF DIRECTORS

November 15, 2017 6:30pm

Spreckels Veterans Memorial Building, 5th & Llano, Spreckels, CA 93962

1. Opening Business

1.1 Call to Order

The meeting was called to order by President Ea

1.2 Roll Call & Establishment of Quorum

1.3

1.4

Ron Eastwood, President James Riley, Vice President Scott Henningsen, Director Otto Kramm, Director Cathy McDougall, Director Paul Ingram, Business Manag

o he Agenda as presented. 2/3 vote required if any

ION/ACTION: Paul Ingram, Business Manager

Board of Directors of the Spreckels Community Services District adopts the agenda as presented."

Motion to adopt agenda {McDougall] 2nd [Kramm] Ayes: Eastwood, Kramm, McDougall Noes: None MOTION CARRIED

2. Communications

5

2

2.1 Correspondence:

2.2 Oral Comments from the Public

Resident Rick Gutierrez reported a desire for homeowners that use the alley between First Street and Spreckels Boulevard to perform some patching repairs by themselves. They would hire a backhoe operator to grade the surface, then they would order a load of DG. They would spread the material and use a roller to compact. He understood that the District does not have funding for any repairs, but asked if the District could fund the pure ase of the DG. The board chose to respond by saying the issue would have to be agendized January regular meeting. The board expressed a consensus that none woulds rt a motion to expend funds on this project. Mr. Gutierrez then asked if they needed pel rom the District to perform the project without District support. The recom e datio the board was that he contact the Monterey County Resource Management the project.

3. Consent Agenda

4.

3.1 Approval of the Minutes of tti

b.

2017.

MOTION CARRIED

ith Local Agency Formation Commission

Business M ger Ingram reported a meeting with LAFCO Executive Kate McKenna and Senior Ana st Joe Serrano on possible changes to SCSD. They will present a report before the January meeting that will address all possibilities and ramifications of either dissolving SCSD or merging with Spreckels Memorial District. Director McDougall asked for contact information for Ms. McKenna. She also asked permission from President Eastwood to have conversations with LAFCO. Permission was approved.

c. Report on research regarding of special assessments by each zone in the County Fund 634 monthly report.

6

3

The board had directed BM Ingram to ask the County Auditor-Controller or Tax Collector about why assessments for Zone 1 and Zone 2 could not be reported separately on the monthly report for Fund 634. BM Ingram turned the question over to Chris Coulter of SCI Consulting to research. He reported conversations with Roger Martinez-Pio of the AuditorControllers office, who stated they would not report amounts separately. The recommendation from Chris Coulter was to request the county report for uncollected property taxes in January and May. An assessments receivable spreadsheet could be created for each zone and amounts paid tracked by the uncollected property taxes report. An accurate report of assessments received would be entered i o District records for each fiscal year.

d. Fire Services Refund Zone 1: Report on returned or e $1,133.77 sent from SCI Consulting Group.

direction from our accountant as to how. re they no longer restricted.

5. Unfinished Business Action Items

6. New Business Action Items

6.1

MOTION CARRIED

6.3

a. Management Services $ 500.00

b. Landscape Services $ 600.00

c. Spreckels Memorial Dist. AT&T $ 49.18

d. Spreckels Water Company $ 182.58

e. PG&E Streetlights & Pump $ 488.47

f. Monterey County Counsel Audit Questions $ 39.89

g. McGilloway, Ray, Brown & Kaufman Audit FY 2010 s 8,100.00

TOTAL $ 9,960.12

7

7.

8.

9.

4

RECOMMENDATION/ACTION: Paul Ingram, Business Manager

"That the Board of Directors of the Spreckels Community Services District approves the Accounts Payable for the period of October 2017."

A motion to approve these payable and also to approve up to $25,000 for December payables [Kramm] 2nd [McDougall] Ayes: Eastwood, Kramm, McDougall Noes: None

6.2 Possible approval of Letter of Engagement with Mc for audits of fiscal years 2011, 2012, 2013, 2014.

There was not motion to approve. Busine MRBKthat they may resubmit the LOE January meeting. BM Ingram is also l McDougall suggested the auditing firm t Federation of Teachers, of which her husbanctbfllf/lh,

6.3 Possible approval of contra Avenue and Spreckels Boulev

a.

or Kramm. No further action is needed.

9.1

a. b. Standard Pacific Homes Subdivision

c. Zoning

d. Historical

e. Community Service

f. Street Lights

g. Drainage

h. Grading

8

5

i. Legal Counsel

J. Alleys

k. Trees

1. Landscaping

m. Sidewalk Repairs

n. Wheel Chair/Access Ramps

o. Quarterly Services

p. Trench Work

Director Kramm asked BM Ingram to notify Landscape

spur branches from walnut tree at Spreckels Boulev

10. Reports from Standing and Ad Hoc Committees

11. Community Member Recognition

12. Consideration of Items for Future

12.1

13. Next Meeting Dates:

19.

Approval Date ________ _

9

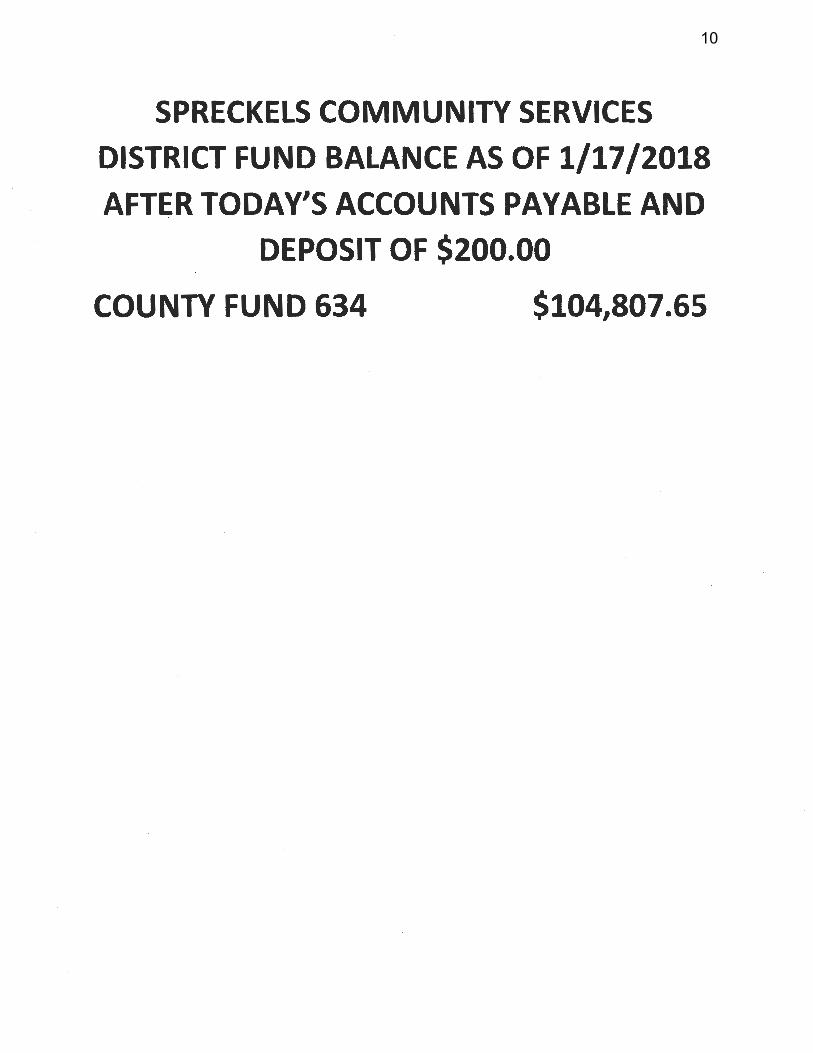

SPRECKELS COMMUNITY SERVICES

DISTRICT FUND BALANCE AS OF 1/17 /2018

AFTER TODAY'S ACCOUNTS PAYABLE AND

DEPOSIT OF $200.00

COUNTY FUND 634 $104,807.65

10

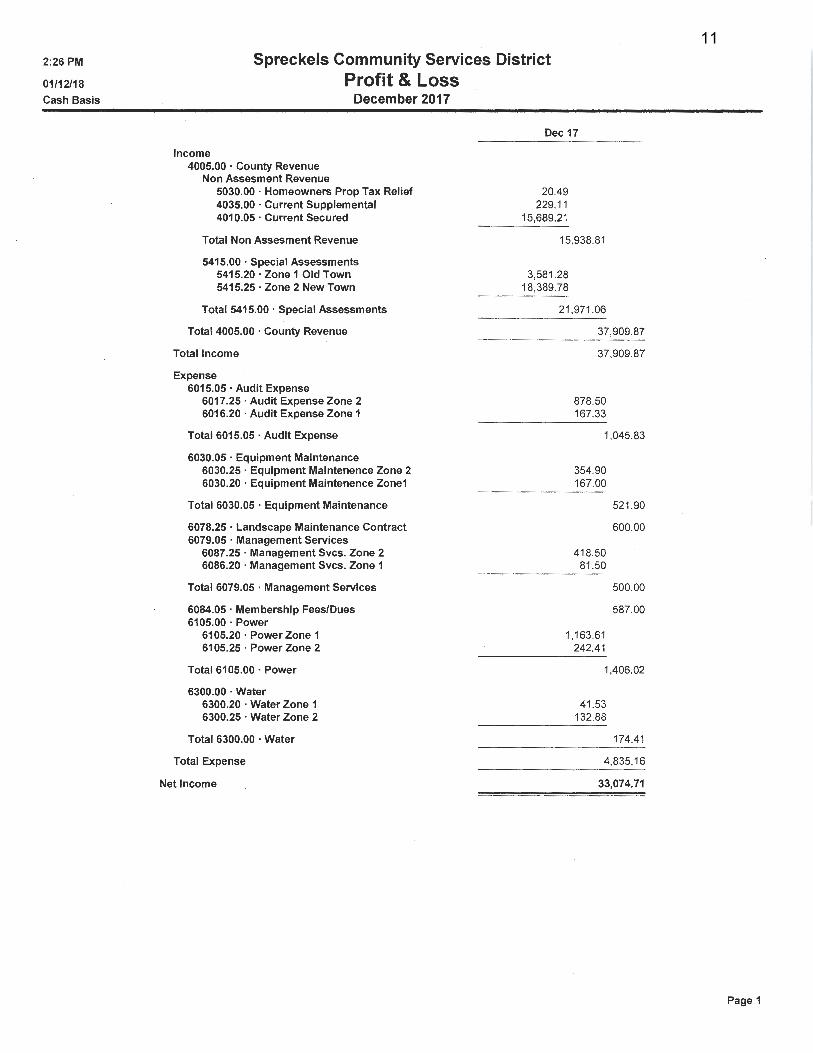

2:26 PM

01/12/18

Cash Basis

Spreckels Community Services District Profit & Loss

December 2017

Income 4005.00 · County Revenue

Non Assesment Revenue 5030.00 · Homeowners Prop Tax Relief 4035.00 · Current Supplemental 4010.05 · Current Secured

Total Non Assesment Revenue

5415.00 ·Special Assessments 5415.20 ·Zone 1 Old Town 5415.25 ·Zone 2 New Town

Total 5415.00 ·Special Assessments

Total 4005.00 ·County Revenue

Total Income

Expense 6015.05 · Audit Expense

6017.25 ·Audit Expense Zone 2 6016.20 ·Audit Expense Zone 1

Total 6015.05 ·Audit Expense

6030.05 · Equipment Maintenance 6030.25 · Equipment Maintenence Zone 2 6030.20 · Equipment Maintenence Zone1

Total 6030.05 · Equipment Maintenance

6078.25 · Landscape Maintenance Contract 6079.05 · Management Services

6087.25 ·Management Svcs. Zone 2 6086.20 · Management Svcs. Zone 1

Total 6079.05 · Management Services

6084.05 · Membership Fees/Dues 6105.00 ·Power

6105.20 · Power Zone 1 6105.25 · Power Zone 2

Total 6105.00 ·Power

6300.00 · Water 6300.20 · Water Zone 1 6300.25 · Water Zone 2

Total 6300.00 · Water

Total Expense

Net Income

Dec 17

20.49 229.11

15,689.21

15,938.81

3,581.28 18,389.78

21,971.06

37,909.87

37,909.87

878.50 167.33

1,045.83

354.90 167.00

418.50 81 .50

1,163.61 242.41

521.90

600.00

500.00

587.00

1,406.02

41.53 132.88

174.41

4,835.16

33,074.71

Page 1

11

L

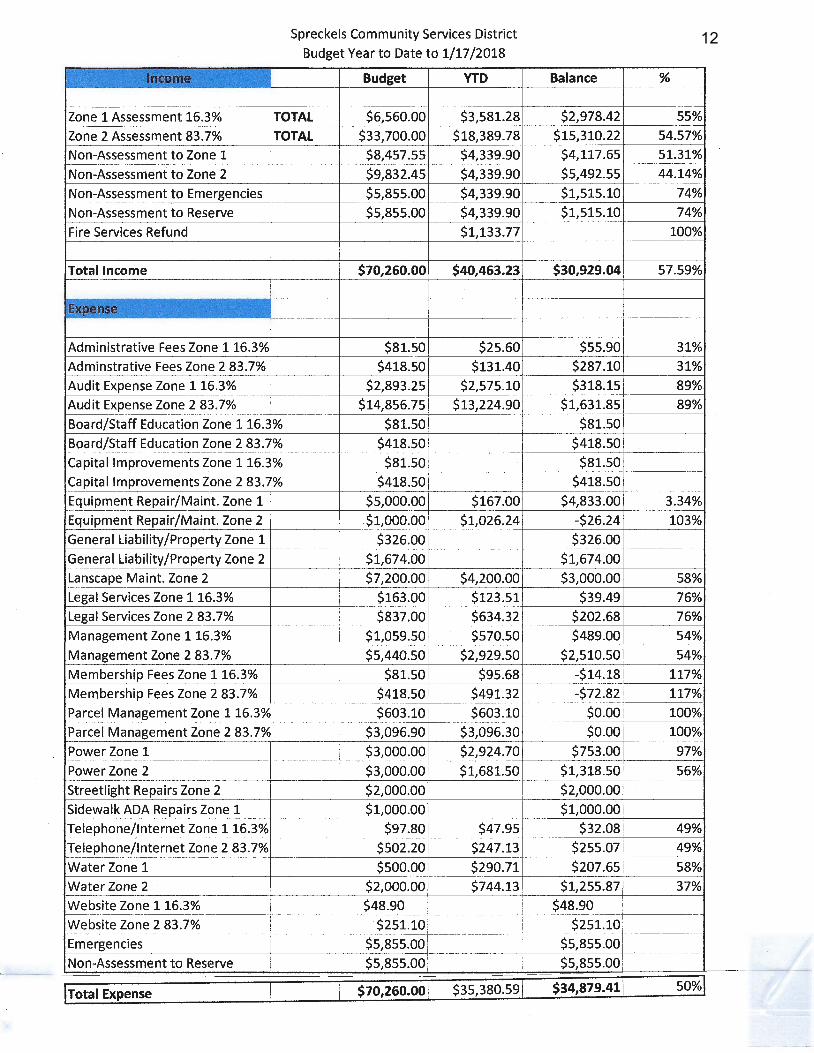

Spreckels Community Services District

Budget Year to Date to 1/17 /2018

Budget YTD

Zone 1Assessment16.3% TOTAL $6,560.00 $3,581.28

Zone 2 Assessment 83.7% TOTAL $33,700.00 $18,389.78

Non-Assessment to Zone 1 $8,457.55 $4,339.90

Non-Assessment to Zone 2 $9,832.45 $4,339.90

Non-Assessment to Emergencies $5,855.00 $4,339.90

Non-Assessment to Reserve $5,855.00 $4,339.90

Fire Services Refund $1,133.77

Total Income $70,260.00 $40,463.23

Administrative Fees Zone 116.3% $81.50 $25.60

Adminstrative Fees Zone 2 83.7% $418.50 $131.40

Audit Expense Zone 116.3% $2,893.25 $2,575.10

Audit Expense Zone 2 83.7% $14,856.75 $13,224.90

Board/Staff Education Zone 116.3% $81.50

Board/Staff Education Zone 2 83.7% $418.50

Capital Improvements Zone 116.3% $81.50

Capital Improvements Zone 2 83.7% $418.50

Equipment Repair/Maint. Zone 1 $5,000.00 $167.00

Equipment Repair/Maint. Zone 2 $1,000.00 $1,026.24

General Liability/Property Zone 1 $326.00

General Liability/Property Zone 2 $1,674.00

Lanscape Maint. Zone 2 $7,200.00 $4,200.00

Legal Services Zone 116.3% $163.00 $123.51

Legal Services Zone 2 83.7% $837.00 $634.32

Management Zone 116.3% $1,059.50 $570.50

Management Zone 2 83.7% $5,440.50 $2,929.50

Membership Fees Zone 116.3% $81.50 $95.68

Membership Fees Zone 2 83.7% $418.50 $491.32

Parcel Management Zone 116.3% $603.10 $603.10

Parcel Management Zone 2 83.7% $3,096.90 $3,096.30

Power Zone 1 $3,000.00 $2,924.70

Power Zone 2 $3,000.00 $1,681.50

Streetlight Repairs Zone 2 $2,000.00

Sidewalk ADA Repairs Zone 1 $1,000.00

Telephone/Internet Zone 116.3% $97.80 $47.95

Telephone/Internet Zone 2 83.7% $502.20 $247.13

Water Zone 1 $500.00 $290.71

Water Zone 2 $2,000.00 $744.13

Website Zone 116.3% $48.90

Website Zone 2 83.7% $251.10

Emergencies $5,855.00

Non-Assessment to Reserve $5,855.00

Total Expense $70,260.00 $35,380.59

Balance %

$2,978.42 55%

$15,310.22 54.57%

$4,117.65 51.31%

$5,492.55 44.14%

$1,515.10 74%

$1,515.10 74%

100%

$30,929.04 57.59%

$55.90 31%

$287.10 31%

$318.15 89%

$1,631.85 89%

$81.50

$418.50

$81.50

$418.50

$4,833.00 3.34%

-$26.24 103%

$326.00

$1,674.00

$3,000.00 58%

$39.49 76%

$202.68 76%

$489.00 54%

$2,510.50 54%

-$14.18 117%

-$72.82 117%

$0.00 100%

$0.00 100%

$753.00 97%

$1,318.50 56%

$2,000.00

$1,000.00

$32.08 49%

$255.07 49%

$207.65 58%

$1,255.87 37%

$48.90

$251.10

$5,855.00

$5,855.00

$34,879.41 50%

12

SPRECKELSCOMMUNITYSERVICESDISTRICTBOARDPOLICIESFIRSTREADING:January17,2018ADOPTED:

Page1of5

ARTICLEI.NAMEThenameshallbetheSpreckelsCommunityServicesDistrict,hereafterknownasthe"SCSD."TheSCSDisorganizedasaSpecialDistrictandisgovernedbytheapplicablegenerallawsoftheStateofCalifornia.ARTICLEII.PURPOSEANDOBJECTIVESThepurposeoftheSCSDistoprovideservicestothoselivingandworkingwithintheDistrict'sgeographicalboundaries,pursuanttotheapplicablegenerallawsoftheStateofCalifornia.TheSCSDisformedundertheCommunityServicesDistrictLawCaliforniaGovernmentCodeSection56036andthereafter).Theselawsempowerdistricts“toachievelocalgovernance,provideneededpublicfacilities,andsupplypublicservices.”TheSpreckelsCommunityServicesDistrictmaintainsthestormdrains,streetlighting,sidewalksandalleywaysofthecommunity.ARTICLEIII.BOARDOFDIRECTORSandMEETINGSAfive-memberBoardofDirectorsgovernstheSCSD.Directorsareelectedat-largebythecommunityandservestaggeredfour-yearterms.Whenanelectionisscheduledandthenumberofcandidatesequalsthenumberofeligibleseats,oriftherearenocandidates,theBoardofSupervisorscanappointmemberstotheSCSD’sBoardofDirectors,pursuanttoElectionsCodesection10515.BeforeanySCSDmemberentersintothedutiesofthisoffice,he/sheshalltakeanoathoraffirmationsetforthinArticleXX,Section3oftheCaliforniaConstitution.AcertifiedcopyoftheoathshallbefiledintheofficeoftheClerkoftheSCSDBoard.TheBoardmeetsregularlyeverythirdWednesdayofthemonthat6:30pmattheSpreckelsVeteransMemorialBuildingat90FifthStreet,Spreckels.Themeetinglocationshallbeaccessibletopeoplewithphysicalhandicaps.QuorumandVotingRequirements:Aquorumisnecessarytoconductbusinessandmakerecommendations.Aquorumshallbeconstitutedbythepresenceofamajorityofthemembership.Amajorityvoteofthosepresentisrequiredtotakeanyaction.Eachmembershallbeentitledtoonevote.Votingmustbeinperson,orundersuchcircumstancesasare

13

SPRECKELSCOMMUNITYSERVICESDISTRICTBOARDPOLICIESFIRSTREADING:January17,2018ADOPTED:

Page2of5

authorizedbytheRalphM.BrownAct,GovernmentCode§§54950,etseq.;noproxyvoteswillbeaccepted.ThenamesofBoardMembersattendingandabsentshallberecordedintheofficialminutes.Membersareresponsibleforassuringthattheirpresenceisrecorded.IfaBoardMemberrecordsthreeabsenceswithinasinglecalendaryear,thePresidentoftheBoardshallmeetwiththeDirectortoascertaintheirinterestandabilitytoremainontheBoardandfullyparticipateatallmeetings.ItistheexpectationthatallBoardMemberswillfullyreviewallmaterialsprovidedtothempriortothemeetingsandwillbefullypreparedtoengageindiscussion.Foritemsrequiringclarificationoradditionalinformation,theinquiringDirectorshallsubmittotheBusinessManager,withacopytotheBoardPresident,writtencommunicationseekingtheadditionalinformationatleast24hourspriortothescheduleRegularorSpecialmeeting.SpecialMeetings.Toholdaspecialmeeting,actualadvancenoticeofsuchmeetingshallbegiventoeachmemberoftheSCSDatleasttwenty-four(24)hoursbeforethetimeofthemeeting,statingthetime,placeandthebusinesstobetransacted,andnootherbusinessshallbeconsideredataspecialmeeting.PublicNoticeofspecialmeetingsshallbeinaccordancewiththeRalphM.BrownAct.AspecialmeetingmaybecalledbythePresident,orbyatwo-thirds(2/3)voteofthevotingmembershipoftheSCSD.OFFICERSandROTATAIONOFOFFICERS:Designation.ThereshallbeaPresident,aVicePresident,andaSecretaryoftheSCSD.Eachofficershallserveasingletermofonecalendaryear.Atthebeginningofcalendaryear2018assignmentofofficersshallbeestablishedbythedrawingofadeckofplayingcardstobedoneinanopenmeeting.TheDirectorselectingthehighestcard(Aceshallbehighest,withtheJokercardbeingexcluded)shallbePresident.ThesecondhighestcardshallbeVicePresident,andthethirdhighestshallbeSecretary.TheforthandfifthhighestcardsshallentertheofficeofSecretarywhenthepositionbecomesvacantorbyrotationattheendofthecalendaryear.Intheeventofmultiplecardsofthesamedomination,aredrawingwillbeheldbetweentheDirectorswhodrewthesamedominationcards.Beginningwithcalendaryear2018,theofficersandtheirrotationshallbe:2018President:

14

SPRECKELSCOMMUNITYSERVICESDISTRICTBOARDPOLICIESFIRSTREADING:January17,2018ADOPTED:

Page3of5

VicePresident:Secretary:ForthPositionFifthPosition.Atthefinalmeetingof2018,theofficersshallrotatetothenexthighestpositionwiththeoutgoingPresidentmovingtothefifthpositionandtheDirectorholdingtheforthpositionin2018movingintotheofficeofSecretaryfor2019.NewDirectorstotheBoardshalloccupythefifthpositionupontakingoffice.PowersandDutiesofOfficers:ThePresidentshall:

A.PresideatallmeetingsoftheSCSD.

B.PlanandcarryouttheagendaforeachBoardmeeting.However,eachBoardmembershallhavetherighttoagendizesubject(s)fordiscussionand/oractionbytheBoard.C.FacilitatethepurposesoftheBoardbyhavingsuchpowersanddutiesasmaybeprescribedfromtimetotimebymajorityvoteoftheBoard.D.AddressalloperationalorpolicyimplementationquestionsinbetweenmeetingsoftheBoardinconcertwiththeBusinessManager.E.Delegateareasonableportionofhis/herdutiestotheViceChairperson.

2.TheViceChairpersonsshall:

A.AssisttheChairpersoninhis/herduties,asneeded.B.PerformthedutiesoftheChairpersonintheeventofhis/heabsence;resignation,orinabilitytoperformhis/herduties,untilsuchtimeaseithertheChairpersonreturnsoranewChairpersonassumesofficeundertheprovisionsoftheseBy-Laws.

3.Secretary:

15

SPRECKELSCOMMUNITYSERVICESDISTRICTBOARDPOLICIESFIRSTREADING:January17,2018ADOPTED:

Page4of5

A.TheSecretaryshallkeeptherecordsoftheDistrict,shallactasSecretaryofthemeetingsoftheDistrict,recordallvotesandshallkeeparecordoftheproceedingsoftheDistrictinajournalofproceedingstobekeptforsuchpurposeandshallperformalldutiesincidenttohisorheroffice.He/Shewillkeepinsafecustody,allcontractsandinstrumentsauthorizedtobeexecutedbytheDistrict.

AdditionalDuties:TheofficersoftheSCSDshallperform,withBoardapproval,suchotherdutiesasallowedbythepoliciesoftheSCSDandStatelaw.Vacancies:AllvacanciesthatoccurregardingtheBoardofDirectorsshallbefilledaccordingtotheprovisionsofCaliforniaGovernmentCodesection1780,andthereafter,andanyothercodesectionsoftheCaliforniaGovernmentCodeand/orspecialdistrict’scodesthenapplicable.ARTICLEVIII.CONFLICTSOFINTEREST.

A. Nospouse,child,parent,siblingofamemberoftheBoardshallbeanemployeeorcontractoroftheDistrict.

B. VotingPrivileges.NoBoardmembershallvoteinanymatterwhichcomesbeforetheBoard,orparticipateinanymatterinwhichhe/sheisrequiredtoactinhis/hercapacityasaBoardmember,whenthememberhasormayhaveadirectorindirecteconomicinterestwhichmaybeaffectedasaresultofsuchaction,unlessbynecessity.Nomembershallundertakeanyemployment,activity,oreconomicenterpriseforcompensationthatisinconsistent,incompatible,inconflictwithorinimicaltohis/herdutiesasaBoardmember.

ARTICLEXI:BOARDREVIEWOFPOLICY:

TheseBoardPoliciesshallbereviewedannuallyatthefirstregularmeetinginFebruary.ThereviewshallbeprovidedbyDistrictCounselandratifiedbyBoardaction.

16

SPRECKELSCOMMUNITYSERVICESDISTRICTBOARDPOLICIESFIRSTREADING:January17,2018ADOPTED:

Page5of5

17

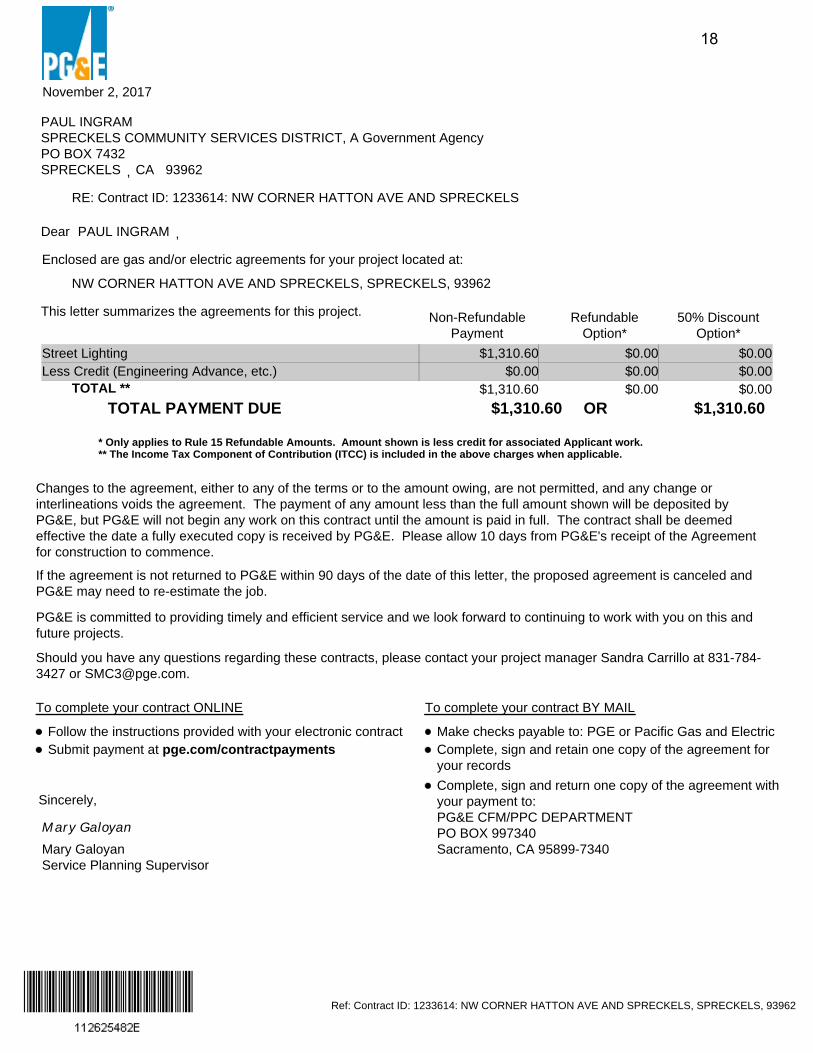

Ref: Contract ID: 1233614: NW CORNER HATTON AVE AND SPRECKELS, SPRECKELS, 93962

November 2, 2017

PAUL INGRAM

PO BOX 7432SPRECKELS

PAUL INGRAMDear ,

* Only applies to Rule 15 Refundable Amounts. Amount shown is less credit for associated Applicant work.

Please sign both copies of the agreement and return one copy of the agreement to the address below along with your paym

This letter summarizes the agreements for this project.

CA 93962

NW CORNER HATTON AVE AND SPRECKELS, SPRECKELS, 93962

Street Lighting $1,310.60 $0.00 $0.00

$1,310.60 $0.00 $0.00

TOTAL PAYMENT DUE

Non-RefundablePayment

RefundableOption*

50% DiscountOption*

TOTAL **

$1,310.60 $1,310.60OR

Enclosed are gas and/or electric agreements for your project located at:

Less Credit (Engineering Advance, etc.) $0.00 $0.00 $0.00

SPRECKELS COMMUNITY SERVICES DISTRICT, A Government Agency

** The Income Tax Component of Contribution (ITCC) is included in the above charges when applicable.

Mary Galoyan

Sincerely,

Service Planning Supervisor

Should you have any questions regarding these contracts, please contact your project manager Sandra Carrillo at 831-784-3427 or [email protected].

Complete, sign and return one copy of the agreement with your payment to:PG&E CFM/PPC DEPARTMENTPO BOX 997340Sacramento, CA 95899-7340

RE: Contract ID: 1233614: NW CORNER HATTON AVE AND SPRECKELS

,

PG&E is committed to providing timely and efficient service and we look forward to continuing to work with you on this andfuture projects.

Changes to the agreement, either to any of the terms or to the amount owing, are not permitted, and any change orinterlineations voids the agreement. The payment of any amount less than the full amount shown will be deposited byPG&E, but PG&E will not begin any work on this contract until the amount is paid in full. The contract shall be deemedeffective the date a fully executed copy is received by PG&E. Please allow 10 days from PG&E's receipt of the Agreementfor construction to commence.

Mary Galoyan

To complete your contract ONLINE

Follow the instructions provided with your electronic contractSubmit payment at pge.com/contractpayments

To complete your contract BY MAIL

Make checks payable to: PGE or Pacific Gas and ElectricComplete, sign and retain one copy of the agreement for your records

If the agreement is not returned to PG&E within 90 days of the date of this letter, the proposed agreement is canceled andPG&E may need to re-estimate the job.

18

62-4527 (Rev 1/91)Service Planning

Advice No. 1633-G/1342-EEffective 4/02/91

Automated document, Preliminary Statement, Part A

Page 1 of 2

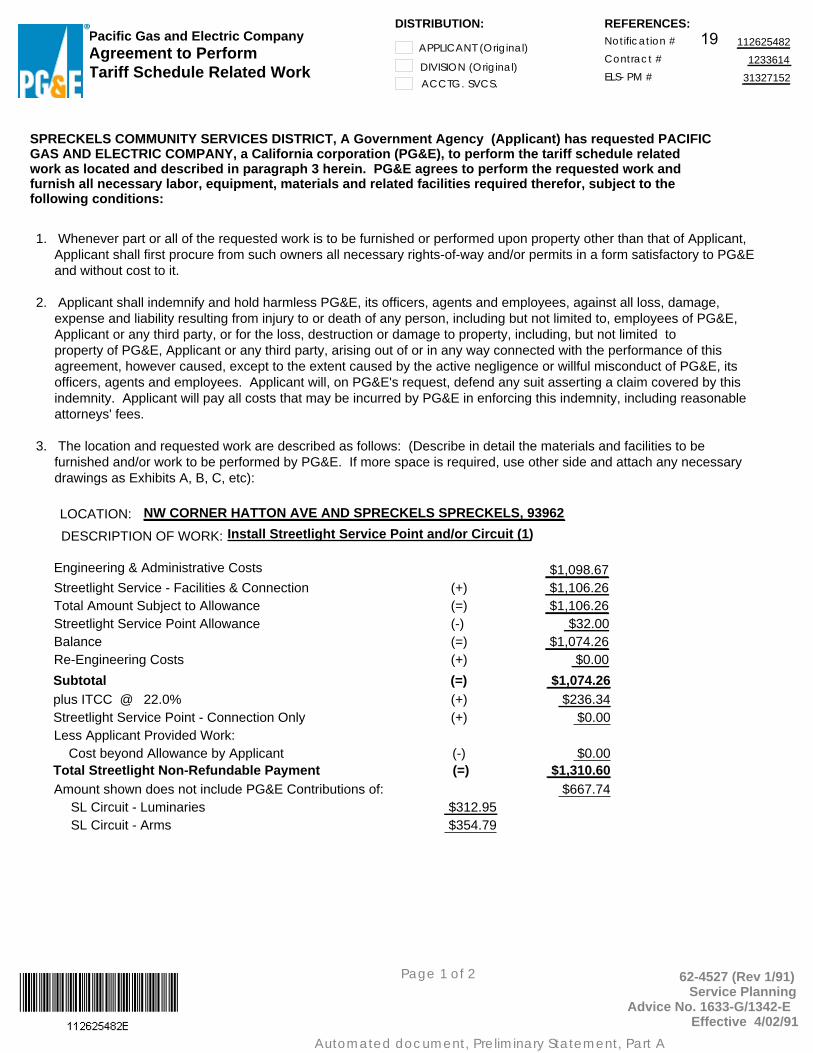

Pacific Gas and Electric CompanyAgreement to PerformTariff Schedule Related Work

REFERENCES: Notification #

Contract #

ELS-PM #

112625482

1233614

31327152

APPLICANT (Original)

DIVISION (Original)ACCTG. SVCS.

1. Whenever part or all of the requested work is to be furnished or performed upon property other than that of Applicant, Applicant shall first procure from such owners all necessary rights-of-way and/or permits in a form satisfactory to PG&E and without cost to it.

2. Applicant shall indemnify and hold harmless PG&E, its officers, agents and employees, against all loss, damage, expense and liability resulting from injury to or death of any person, including but not limited to, employees of PG&E, Applicant or any third party, or for the loss, destruction or damage to property, including, but not limited to property of PG&E, Applicant or any third party, arising out of or in any way connected with the performance of this agreement, however caused, except to the extent caused by the active negligence or willful misconduct of PG&E, its officers, agents and employees. Applicant will, on PG&E's request, defend any suit asserting a claim covered by this indemnity. Applicant will pay all costs that may be incurred by PG&E in enforcing this indemnity, including reasonable attorneys' fees.

3. The location and requested work are described as follows: (Describe in detail the materials and facilities to be furnished and/or work to be performed by PG&E. If more space is required, use other side and attach any necessary drawings as Exhibits A, B, C, etc):

LOCATION:

DESCRIPTION OF WORK:

NW CORNER HATTON AVE AND SPRECKELS SPRECKELS, 93962

Install Streetlight Service Point and/or Circuit (1)

plus ITCC @ $1,074.26Subtotal

$236.34 22.0% (+) Streetlight Service Point - Connection Only $0.00(+)

Total Streetlight Non-Refundable Payment $1,310.60(=)

$1,098.67Streetlight Service - Facilities & Connection $1,106.26Total Amount Subject to Allowance $1,106.26Streetlight Service Point Allowance $32.00Balance $1,074.26

(-) (=) (+)

(=)

Engineering & Administrative Costs

Less Applicant Provided Work:

SPRECKELS COMMUNITY SERVICES DISTRICT, A Government Agency (Applicant) has requested PACIFICGAS AND ELECTRIC COMPANY, a California corporation (PG&E), to perform the tariff schedule relatedwork as located and described in paragraph 3 herein. PG&E agrees to perform the requested work andfurnish all necessary labor, equipment, materials and related facilities required therefor, subject to thefollowing conditions:

Cost beyond Allowance by Applicant $0.00(-)

(=)

DISTRIBUTION:

Amount shown does not include PG&E Contributions of: $667.74

Re-Engineering Costs (+) $0.00

$312.95 $354.79

SL Circuit - LuminariesSL Circuit - Arms

19

62-4527 (Rev 1/91)Service Planning

Advice No. 1633-G/1342-EEffective 4/02/91

Automated document, Preliminary Statement, Part A

Page 2 of 2

4. Applicant shall pay to PG&E, promptly upon demand by PG&E, as the complete contract price hereunder, the sum of

($1,310.60)

Upon completion of requested work, ownership shall vest in: PG&E Applicant

One Thousand Three Hundred Ten Dollars And Fifty-Nine Cents

X

SPRECKELS COMMUNITY SERVICES DISTRICT,A Government Agency

PACIFIC GAS & ELECTRIC COMPANY

Mailing Address: PO BOX 7432SPRECKELS,

Title: Title:

CA 93962

Service Planning Supervisor

Applicant

day of

By:

PAUL INGRAM Mary GaloyanPrint/Type/Name

By: Mary Galoyan

Executed this #signDayWPA# #signMonWPA# #signYrWPA#

#sigWPA#

#titleWPA#

#Form 62-4527#

20

November 7, 2017 Spreckels Community Services District Attn: Paul Ingram P.O. Box 7432 Spreckels, CA 93962 Governmental Yellow Book Audit Engagement Letter To Spreckels Community Services District and the Board of Directors, We are pleased to confirm our understanding of the services we are to provide Spreckels Community Services District for the years ended June 30, 2011, June 30, 2012, June 30, 2013, and June 30, 2014. We will audit the financial statements of the governmental activities, the business-type activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information, including the related notes to the financial statements, which collectively comprise the basic financial statements of Spreckels Community Services District as of and for the years ended June 30, 2011, June 30, 2012, June 30, 2013, and June 30, 2014. Accounting standards generally accepted in the United States of America provide for certain required supplementary information (RSI), such as management’s discussion and analysis (MD&A), to supplement Spreckels Community Services District’s basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. As part of our engagement, we will apply certain limited procedures to Spreckels Community Services District’s RSI in accordance with auditing standards generally accepted in the United States of America. These limited procedures will consist of inquiries of management regarding the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We will not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. The following RSI is required by generally accepted accounting principles and will be subjected to certain limited procedures, but will not be audited: 1. Management’s Discussion and Analysis Audit Objectives The objective of our audit is the expression of opinions as to whether your financial statements are fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles and

21

to report on the fairness of the supplementary information referred to in the second paragraph when considered in relation to the financial statements as a whole. Our audit will be conducted in accordance with auditing standards generally accepted in the United States of America and the standards for financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States, and will include tests of the accounting records of Spreckels Community Services District and other procedures we consider necessary to enable us to express such opinions. We will issue a written report upon completion of our audit of Spreckels Community Services District’s financial statements. Our report will be addressed to the Board of Directors of Spreckels Community Services District. We cannot provide assurance that unmodified opinions will be expressed. Circumstances may arise in which it is necessary for us to modify our opinions or add emphasis-of-matter or other-matter paragraphs. If our opinions are other than unmodified, we will discuss the reasons with you in advance. If circumstances occur related to the condition of your records, the availability of sufficient, appropriate audit evidence, or the existence of a significant risk of material misstatement of the financial statements caused by error, fraudulent financial reporting, or misappropriation of assets, which in our professional judgment prevent us from completing the audit or forming an opinion on the financial statements, we retain the right to take any course of action permitted by professional standards, including declining to express an opinion or issue a report, or withdrawing from the engagement. We will also provide a report (that does not include an opinion) on internal control related to the financial statements and compliance with the provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a material effect on the financial statements as required by Government Auditing Standards. The report on internal control and on compliance and other matters will include a paragraph that states (1) that the purpose of the report is solely to describe the scope of testing of internal control and compliance, and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control on compliance, and (2) that the report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. The paragraph will also state that the report is not suitable for any other purpose. If during our audit we become aware that Spreckels Community Services District is subject to an audit requirement that is not encompassed in the terms of this engagement, we will communicate to management and those charged with governance that an audit in accordance with U.S. generally accepted auditing standards and the standards for financial audits contained in Government Auditing Standards may not satisfy the relevant legal, regulatory, or contractual requirements. Audit Procedures: General An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; therefore, our audit will involve judgment about the number of transactions to be examined and the areas to be tested. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We will plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether from (1) errors, (2) fraudulent financial reporting, (3) misappropriation of assets, or (4) violations of laws or governmental regulations that are attributable to the government or to acts by management or employees acting on behalf of the government. Because the determination of abuse is subjective, Government Auditing Standards do not expect auditors to provide reasonable assurance of detecting abuse.

22

Because of the inherent limitations of an audit, combined with the inherent limitations of internal control, and because we will not perform a detailed examination of all transactions, there is a risk that material misstatements may exist and not be detected by us, even though the audit is properly planned and performed in accordance with U.S. generally accepted auditing standards and Government Auditing Standards. In addition, an audit is not designed to detect immaterial misstatements or violations of laws or governmental regulations that do not have a direct and material effect on the financial statements. However, we will inform the appropriate level of management of any material errors, fraudulent financial reporting, or misappropriation of assets that comes to our attention. We will also inform the appropriate level of management of any violations of laws or governmental regulations that come to our attention, unless clearly inconsequential, and of any material abuse that comes to our attention. Our responsibility as auditors is limited to the period covered by our audit and does not extend to later periods for which we are not engaged as auditors. Our procedures will include tests of documentary evidence supporting the transactions recorded in the accounts, and direct confirmation of receivables and certain other assets and liabilities by correspondence with selected individuals, funding sources, creditors, and financial institutions. We will request written representations from your attorneys as part of the engagement, and they may bill you for responding to this inquiry. At the conclusion of our audit, we will require certain written representations from you about your responsibilities for the financial statements; compliance with laws, regulations, contracts, and grant agreements; and other responsibilities required by generally accepted auditing standards. Audit Procedures: Internal Control Our audit will include obtaining an understanding of the government and its environment, including internal control, sufficient to assess the risks of material misstatement of the financial statements and to design the nature, timing, and extent of further audit procedures. Tests of controls may be performed to test the effectiveness of certain controls that we consider relevant to preventing and detecting errors and fraud that are material to the financial statements and to preventing and detecting misstatements resulting from illegal acts and other noncompliance matters that have a direct and material effect on the financial statements. Our tests, if performed, will be less in scope than would be necessary to render an opinion on internal control and, accordingly, no opinion will be expressed in our report on internal control issued pursuant to Government Auditing Standards. An audit is not designed to provide assurance on internal control or to identify significant deficiencies or material weaknesses. However, during the audit, we will communicate to management and those charged with governance internal control related matters that are required to be communicated under AICPA professional standards and Government Auditing Standards. Audit Procedures: Compliance As part of obtaining reasonable assurance about whether the financial statements are free of material misstatement, we will perform tests of Spreckels Community Services District’s compliance with the provisions of applicable laws, regulations, contracts, agreements, and grants. However, the objective of our audit will not be to provide an opinion on overall compliance and we will not express such an opinion in our report on compliance issued pursuant to Government Auditing Standards.

23

Other Services We will also prepare the financial statements and related notes of Spreckels Community Services District in conformity with U.S. generally accepted accounting principles based on information provided by you. These nonaudit services do not constitute an audit under Government Auditing Standards and such services will not be conducted in accordance with Government Auditing Standards. We will perform the services in accordance with applicable professional standards. The other services are limited to the financial statement preparation services previously defined. We, in our sole professional judgment, reserve the right to refuse to perform any procedure or take any action that could be construed as assuming management responsibilities. Management Responsibilities Management is responsible for establishing and maintaining effective internal controls, including evaluating and monitoring ongoing activities, to help ensure that appropriate goals and objectives are met; following laws and regulations; and ensuring that management and financial information is reliable and properly reported. Management is also responsible for implementing systems designed to achieve compliance with applicable laws, regulations, contracts, and grant agreements. You are also responsible for the selection and application of accounting principles, for the preparation and fair presentation of the financial statements and all accompanying information in conformity with U.S. generally accepted accounting principles, and for compliance with applicable laws and regulations and the provisions of contracts and grant agreements. Management is also responsible for making all financial records and related information available to us and for the accuracy and completeness of that information. You are also responsible for providing us with (1) access to all information of which you are aware that is relevant to the preparation and fair presentation of the financial statements, (2) additional information that we may request for the purpose of the audit, and (3) unrestricted access to persons within the government from whom we determine it necessary to obtain audit evidence. Your responsibilities include adjusting the financial statements to correct material misstatements and for confirming to us in the written representation letter that the effects of any uncorrected misstatements aggregated by us during the current engagement and pertaining to the latest period presented are immaterial, both individually and in the aggregate, to the financial statements taken as a whole. You are responsible for the design and implementation of programs and controls to prevent and detect fraud, and for informing us about all known or suspected fraud affecting the government involving (1) management, (2) employees who have significant roles in internal control, and (3) others where the fraud could have a material effect on the financial statements. Your responsibilities include informing us of your knowledge of any allegations of fraud or suspected fraud affecting the government received in communications from employees, former employees, grantors, regulators, or others. In addition, you are responsible for identifying and ensuring that the government complies with applicable laws, regulations, contracts, agreements, and grants and for taking timely and appropriate steps to remedy fraud and noncompliance with provisions of laws, regulations, contracts or grant agreements, or abuse that we report.

24

You are responsible for the preparation of the supplementary information, which we have been engaged to report on, in conformity with U.S. generally accepted accounting principles. You agree to include our report on the supplementary information in any document that contains and indicates that we have reported on the supplementary information. You also agree to include the audited financial statements with any presentation of the supplementary information that includes our report thereon or make the audited financial statements readily available to users of the supplementary information no later than the date the supplementary information is issued with our report thereon. Your responsibilities include acknowledging to us in the written representation letter that (1) you are responsible for presentation of the supplementary information in accordance with GAAP; (2) you believe the supplementary information, including its form and content, is fairly presented in accordance with GAAP; (3) the methods of measurement or presentation have not changed from those used in the prior period (or, if they have changed, the reasons for such changes); and (4) you have disclosed to us any significant assumptions or interpretations underlying the measurement or presentation of the supplementary information. Management is responsible for establishing and maintaining a process for tracking the status of audit findings and recommendations. Management is also responsible for identifying and providing report copies of previous financial audits, attestation engagements, performance audits or other studies related to the objectives discussed in the Audit Objectives section of this letter. This responsibility includes relaying to us corrective actions taken to address significant findings and recommendations resulting from those audits, attestation engagements, performance audits, or other studies. You are also responsible for providing management’s views on our current findings, conclusions, and recommendations, as well as your planned corrective actions, for the report, and for the timing and format for providing that information. With regard to using the auditor’s report, you understand that you must obtain our prior written consent to reproduce or use our report in bond offering official statements or other documents. With regard to the electronic dissemination of audited financial statements, including financial statements published electronically on your website, you understand that electronic sites are a means to distribute information and, therefore, we are not required to read the information contained in these sites or consider the consistency of other information in the electronic site with the original document. You agree to assume all management responsibilities relating to the financial statements and related notes and any other nonaudit services we provide. You will be required to acknowledge in the management representation letter our assistance with preparation of the financial statements and related notes and that you have reviewed and approved the financial statements and related notes prior to their issuance and have accepted responsibility for them. Further, you agree to oversee the nonaudit services by designating an individual, preferably from senior management, with suitable skill, knowledge, or experience; evaluate the adequacy and results of those services; and accept responsibility for them. Engagement Administration, Fees, and Other You may request that we perform additional services not addressed in this engagement letter. If this occurs, we will communicate with you regarding the scope of the additional services and the estimates fees. We also may issue a separate engagement letter covering the additional services. In the absence of any other written communication from us documenting such additional services, our services will continue to be governed by the terms of this engagement letter.

25

We understand that your employees will prepare all cash, accounts receivable, or other confirmations and schedules we request and will locate any documents selected by us for testing. We expect to provide a draft audit report four weeks after we receive the trial balance and all competent audit requested documentation. Our estimated time of completion is to have the 2011 fiscal year end draft audit report completed by February 15, 2018 and the 2012 fiscal year end draft audit report completed by March 15, 2018. We will schedule the engagement based in part on deadlines, working conditions, and the availability of your key personnel. We will plan the engagement based on the assumption that your personnel will cooperate and provide assistance by performing tasks such as preparing requested schedules, retrieving supporting documents, and preparing confirmations. If for whatever reason your personnel are unavailable to provide the necessary assistance in a timely manner, it may substantially increase the work we have to do to complete the engagement within the established deadlines, resulting in an increase in fees over our original fee estimate. We will not undertake any accounting services (including but not limited to reconciliation of accounts and preparation of requested schedules) without obtaining approval through a written change order or additional engagement letter for such additional work. We will provide copies of our reports to Spreckels Community Services District; however, management is responsible for distribution of the reports and the financial statements. Unless restricted by law or regulation, or containing privileged and confidential information, copies of our reports are to be made available for public inspection. The audit documentation for this engagement is the property of McGilloway, Ray, Brown & Kaufman and constitutes confidential information. However, subject to applicable laws and regulations, audit documentation and appropriate individuals will be made available upon request and in a timely manner to a Regulator or its designee, a federal agency providing direct or indirect funding, or the U.S. Government Accountability Office for purposes of a quality review of the audit, to resolve audit findings, or to carry out oversight responsibilities. We will notify you of any such request. If requested, access to such audit documentation will be provided under the supervision of McGilloway, Ray, Brown & Kaufman personnel. Furthermore, upon request, we may provide copies of selected audit documentation to the aforementioned parties. These parties may intend, or decide, to distribute the copies or information contained therein to others, including other governmental agencies. The audit documentation for this engagement will be retained for a minimum of five years after the report release date or for any additional period requested by a Regulator. If we are aware that a federal awarding agency or auditee is contesting an audit finding, we will contact the party(ies) contesting the audit finding for guidance prior to destroying the audit documentation. Patricia M. Kaufman is the engagement partner and is responsible for supervising the engagement and signing the reports or authorizing another individual to sign them.

26

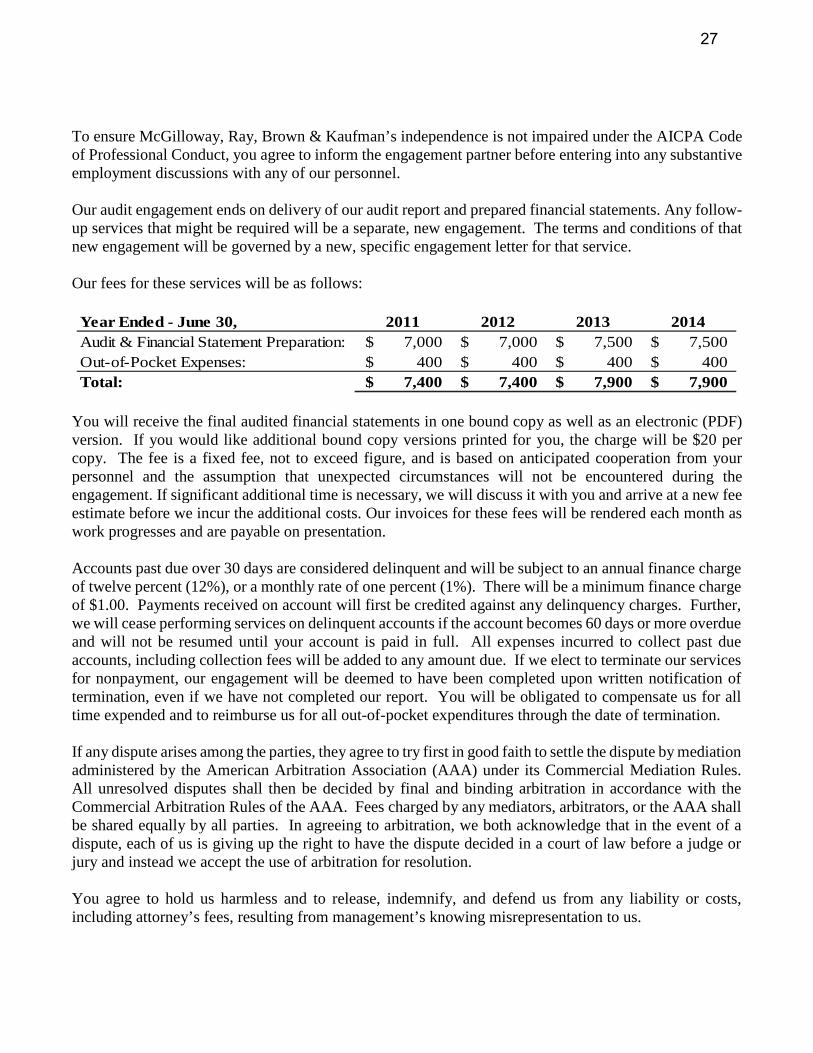

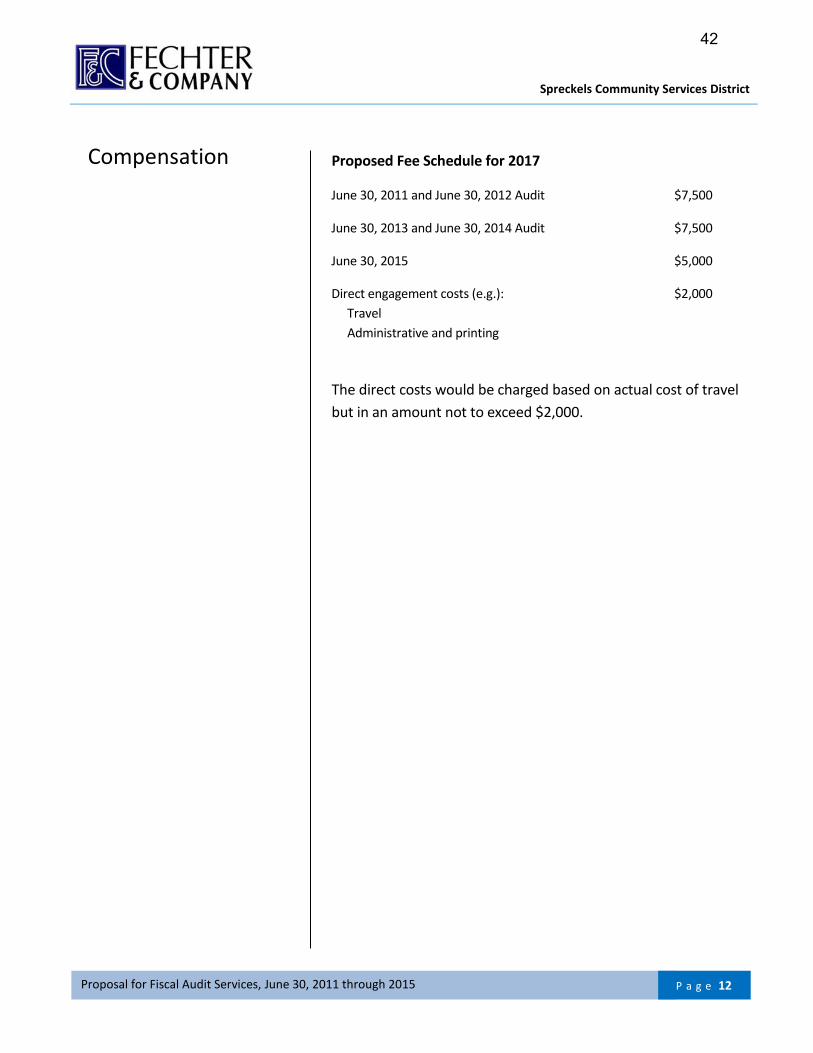

To ensure McGilloway, Ray, Brown & Kaufman’s independence is not impaired under the AICPA Code of Professional Conduct, you agree to inform the engagement partner before entering into any substantive employment discussions with any of our personnel. Our audit engagement ends on delivery of our audit report and prepared financial statements. Any follow-up services that might be required will be a separate, new engagement. The terms and conditions of that new engagement will be governed by a new, specific engagement letter for that service. Our fees for these services will be as follows: Year Ended - June 30, 2011 2012 2013 2014Audit & Financial Statement Preparation: 7,000$ 7,000$ 7,500$ 7,500$ Out-of-Pocket Expenses: 400$ 400$ 400$ 400$ Total: 7,400$ 7,400$ 7,900$ 7,900$

You will receive the final audited financial statements in one bound copy as well as an electronic (PDF) version. If you would like additional bound copy versions printed for you, the charge will be $20 per copy. The fee is a fixed fee, not to exceed figure, and is based on anticipated cooperation from your personnel and the assumption that unexpected circumstances will not be encountered during the engagement. If significant additional time is necessary, we will discuss it with you and arrive at a new fee estimate before we incur the additional costs. Our invoices for these fees will be rendered each month as work progresses and are payable on presentation. Accounts past due over 30 days are considered delinquent and will be subject to an annual finance charge of twelve percent (12%), or a monthly rate of one percent (1%). There will be a minimum finance charge of $1.00. Payments received on account will first be credited against any delinquency charges. Further, we will cease performing services on delinquent accounts if the account becomes 60 days or more overdue and will not be resumed until your account is paid in full. All expenses incurred to collect past due accounts, including collection fees will be added to any amount due. If we elect to terminate our services for nonpayment, our engagement will be deemed to have been completed upon written notification of termination, even if we have not completed our report. You will be obligated to compensate us for all time expended and to reimburse us for all out-of-pocket expenditures through the date of termination. If any dispute arises among the parties, they agree to try first in good faith to settle the dispute by mediation administered by the American Arbitration Association (AAA) under its Commercial Mediation Rules. All unresolved disputes shall then be decided by final and binding arbitration in accordance with the Commercial Arbitration Rules of the AAA. Fees charged by any mediators, arbitrators, or the AAA shall be shared equally by all parties. In agreeing to arbitration, we both acknowledge that in the event of a dispute, each of us is giving up the right to have the dispute decided in a court of law before a judge or jury and instead we accept the use of arbitration for resolution. You agree to hold us harmless and to release, indemnify, and defend us from any liability or costs, including attorney’s fees, resulting from management’s knowing misrepresentation to us.

27

We appreciate the opportunity to be of service to Spreckels Community Services District and believe this letter accurately summarizes the significant terms of our engagement. If you have any questions, please let us know. If you agree with the terms of our engagement as described in this letter, please sign the enclosed copy and return it to us. Very truly yours, McGilloway, Ray, Brown & Kaufman

Patricia M. Kaufman, CPA, CGMA Partner, Salinas Office Response: This letter correctly sets forth the understanding of Spreckels Community Services District. Management Signature: ______________________ Print: _____________________________________ Title: _____________________________________ Date: _____________________________________ Governance Signature: _______________________ Print: _____________________________________ Title: _____________________________________ Date: _____________________________________

Rev 10/04/2016 – PPC ALG (2/16) G:\Data\Clientdata\Begins210000\217625\Engagement Letters\2011-2014 Audit Engagement Letter Yellow Book - GAAP.docx

28

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015

Spreckels Community Services District June 30, 2011 through June 30, 2015

November 27, 2017

Fechter & Company

Certified Public Accountants

3445 American Rive Drive Suite A

Sacramento, CA 95864

Contact: Craig R. Fechter, CPA

T (916) 333-5360 F (916) 333-5370

Email: [email protected]

Proposal for Fiscal Auditing Services

29

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015

Contents

TRANSMITTAL LETTER ................................................................................................................. 1

FIRM PROFILE ........................................................................................................................ 2 – 4

Licensing and Independence

Engagement Partner and Staff

Internal Quality Control Procedures

Technology and Security

REFERENCES .......................................................................................................................... 5 – 6

SPECIFIC AUDIT APPROACH ................................................................................................ 7 – 10

AUDIT TIMELINE ........................................................................................................................ 11

COMPENSATION ....................................................................................................................... 12

QUALIFICATIONS .............................................................................................................. 13 – 17

30

Spreckels Community Services District

November 27, 2017

Paul Ingram

Spreckels Community Services District

PO Box 7432

Spreckels, CA 93962

Dear Paul:

Fechter & Company, Certified Public Accountants, is pleased to present our proposal to provide audit or review

services to the Spreckels Community Services District (the District). The Firm Profile and the credentials listed in the

resumes of our team will demonstrate our qualifications, competence, and capacity to perform the audit services

requested within the time frame required by the District.

This proposal is an irrevocable offer valid for 90 days after the date of the proposal. I am authorized to

represent and to obligate the firm contractually to the District. I am located at 1870 Avondale Avenue, Suite

4, Sacramento, CA 95825, and you can contact me by telephone at (916) 333-5360.

Thank you for considering our proposal. We look forward to a long and successful working relationship with

you and your management team.

Very Truly Yours,

Craig R. Fechter, CPA, President

Fechter & Company, Certified Public Accountants

31

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 2

Fechter & Company is based in Sacramento, with a staff of 4 certified

public accountants. Our relatively small practice offers several advantages

to you:

Experienced auditors perform all audit procedures from initial planning meetings through fieldwork to financial statement preparation.

You receive a high level of personal service with easy access to professionals who can answer your questions and facilitate the audit process.

Because the firm president performs and supervises on-site fieldwork, the turnaround time from the end of our fieldwork to the report draft is typically only 10 days.

Working with the same auditors from year to year greatly reduces the time your staff spends familiarizing us with your business procedures. Your audit process becomes increasingly efficient.

Licensing and Independence

Our firm is licensed as a certified public accounting firm in the state of California.

Each CPA in our firm meets the independence requirements of the American Institute of Certified Public Accountants and the Government Auditing Standards, 2003 revision, published by the U.S. General Accounting Office.

Our firm has had no disciplinary action taken or pending since its inception in 2005.

There are no conflicts of interest with the District or its personnel.

We will continue to maintain requisite insurance coverage—professional liability, workers compensation, business occupancy and auto insurance—throughout the course of our engagement.

We have had no turnover of audit staff since inception in 2005.

Firm Profile

Fechter & Company, CPAs is a

professional corporation formed

in April 2005. We provide finance

consulting and auditing services

to governmental and non-profit

entities. We specialize in serving

agencies with annual budgets of less

than $25 million.

32

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 3

Engagement Partner and Staff for This Assignment

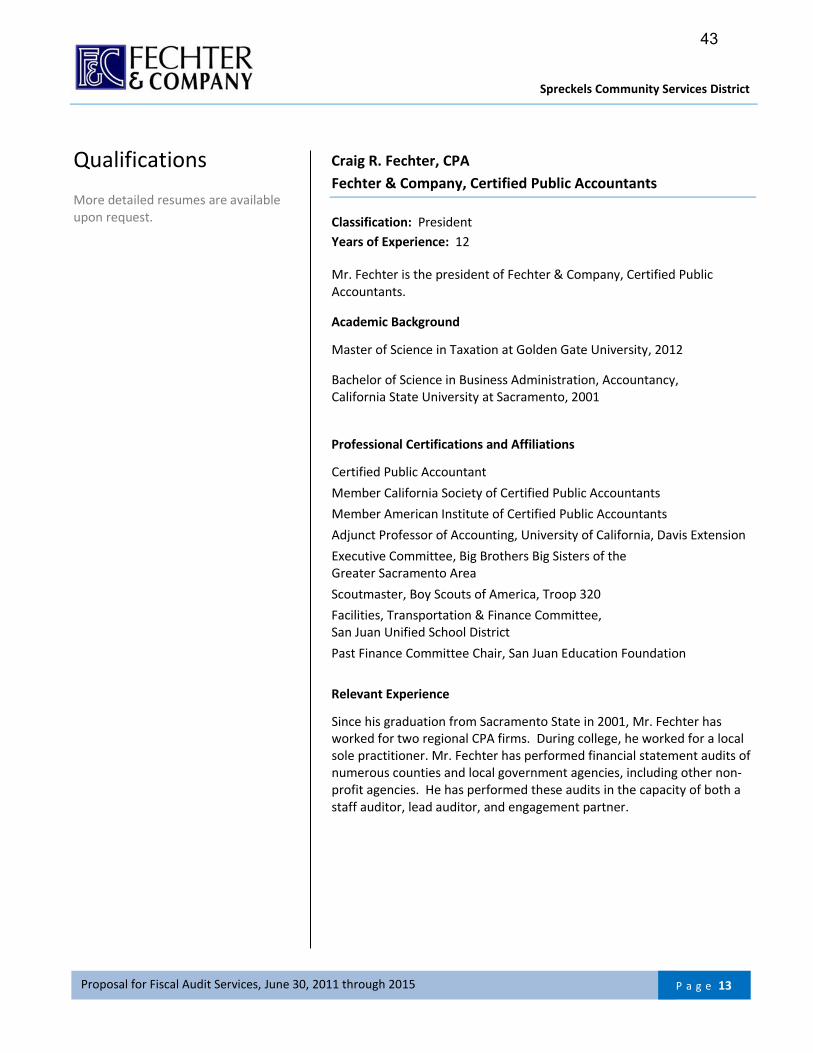

Mr. Craig Fechter will serve as partner in charge for the audit

engagement. He will review the progress of the audit team, assist in

resolving technical issues, and evaluate reports and deliverables for

overall quality. Craig is licensed to practice as a certified public accountant

in California.

Ms. Sandy Sup will serve as the on-site audit manager and will be

responsible for the daily management and delivery of services. She will be

responsible for planning the audit and assuring that the design of audit

programs dictate the audit procedures we believe are necessary to

accomplish the objectives of the audit. Sandy will work closely with the

client to ensure issues are identified and addressed and that the delivery

of services is timely. Sandy is also licensed to practice as a certified public

accountant in California.

Mr. Robert White, an audit senior, will assist with the fieldwork. He will

test those transactions that are significant to the financial statements

including cash disbursements and receipts, payroll, and capital assets.

Internal Quality Control Procedures

Each member of our firm meets the continuing education and

external quality control review requirements contained in the

Government Auditing Standards, 2003 revision, published by the

U.S. General Accounting Office.

Each audit staff is required to complete annual update courses for

both Government/A-133 and non-profit audits. These courses,

which together comprise 26 hours of continuing education, help

our audit staff maintain awareness of technical changes in both

regular and single audits.

During the years our firm is not peer reviewed, we conduct annual

internal reviews. A principal inspects 4 randomly selected audits

and makes notations and recommendations in the same manner

as an external peer review. This helps to keep our working papers

and audit processes fresh.

Prior to being released, each audit is reviewed by a partner who is

not involved with the audit or the client. This independent partner

makes observations and suggestions as to additional audit

Firm Profile

33

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 4

procedures that should be performed. For new clients, a second

partner reviews our audit planning memorandum prior to our

beginning the fieldwork in order to ascertain why certain

procedures were selected while others were not.

Although our audit staff is extremely experienced, we continually

strive to improve our audit quality, from the planning stages to

the final report. We actively encourage all staff to suggest new or

different procedures.

Technology and Security

We maximize both efficiency and security by using technology recognized

as standard in the accounting industry. These are some examples:

Microsoft Office Applications

Since most of our clients use Microsoft applications, we likewise

use the programs, which enable us to collaborate on projects.

Engagement CS

We use Engagement CS paperless auditing system to cut

processing time and costs. All information can be uploaded to our

secure file transfer website.

Biometric User Security

All staff computers are protected with biometric access

restrictions.

Data Storage

All data is backed up to our local server daily through our secure

VPN. In addition, our server data is backed up daily off-site.

Our firm subscribes to approximately a dozen industry periodicals

and newsletters. We proactively inform our clients about

potential changes in related accounting legislation and standards

so they can quickly assess the impact on their organizations. In

addition, we offer an annual Government Accounting Standards

Board (GASB) and Financial Accounting Standards Board (FASB)

update course to our clients at no additional charge.

Firm Profile

34

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 5

Park Districts Audited

Approximately 70 percent of our firm’s revenues are derived from

governmental and non-profit audits under Government Auditing

Standards as published by the U.S. General Accounting Office. Current

clients and services performed are as follows:

Mission Oaks Recreation & Park District

Scope of audit: Fechter & Company, CPAs was engaged to provide a

financial statement audit for the Mission Oaks Recreation & Park District

under Government Auditing Standards and OMB A-133.

Services provided: Audit of the financial statements, management letter and

report on internal control structure.

Engagement partner: Craig R. Fechter, CPA

Contact information:

Cindy Paredes-Banville, Finance Director

3344 Mission Avenue

Carmichael, CA 95608

916-488-2810

Sunrise Recreation & Park District

Scope of audit: Fechter & Company, CPAs was engaged to provide a special

district financial statement and single audit of Sunrise Recreation & Parks

District under Government Auditing Standards and OMB A-133.

Services provided: Audit of the financial statements, single audit,

management letter, and report on internal control structure.

Engagement partner: Craig R. Fechter, CPA

Contact information:

Lee Hollingsworth, Finance Director

7801 Auburn Blvd.

Citrus Heights, CA 95610

916-725-1585

References

35

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 6

Auburn Recreation District

Scope of audit: Fechter & Company, CPAs was engaged to provide a

financial statement audit for the Auburn Recreation District under

Government Auditing Standards and OMB A-133.

Services provided: Audit of the GASB 34 financial statements, management

letter and report on internal control structure, and preparation of annual

report of financial transactions of special districts.

Engagement partner: Craig R. Fechter, CPA

Contact information:

Joe Fecko, Finance Director

471 Maidu Drive #200

Auburn, CA 95603

530-885-0611

Fulton-El Camino Recreation & Park District

Scope of audit: Fechter & Company, CPAs was engaged to provide a

financial statement audit for the Fulton-El Camino Recreation & Park

District under Government Auditing Standards and OMB A-133.

Services provided: Audit of the GASB 34 financial statements, management

letter and report on internal control structure, and preparation of annual

report of financial transactions of special districts. We also assisted the

District with financial statement preparation and presentation.

Engagement partner: Craig R. Fechter, CPA

Contact information:

Michael Grace, District Manager

2201 Cottage Way

Sacramento, CA 95821

916-927-3802

References

Additional references are available upon request.

36

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 7

The District requests that the auditor express an opinion on the fair

presentation of its financial statements in accordance with accounting

principles generally accepted in the United States of America. We propose

that the engagement be divided into the following segments:

Phase I

Initial planning and preparation

Preliminary analysis, report preparation, cash and other confirmations

Information gathering

Evaluating internal controls

Phase II

Fieldwork

Post-field-work activities (e.g., follow-up on pending items,

collection of confirmation letters, etc.)

Phase III

Report finalization and final analysis

Report delivery and Board of Directors presentation

Initial Planning and Preparation

As the first step in our planning and preparation phase, we will meet with the

staff of your company to establish a working relationship. We expect this

meeting will involve the District’s manager and its controller.

We will deliver a Prepared-by-Client list (PBC), which details the items we will

need to perform the audit. We will resolve any ambiguities or questions we or

the District might have about the services we are to perform.

We will gather contact information for the District’s bankers, attorneys, prior

accountant, and other relevant parties, and make inquiries as required by

Government Auditing Standards.

We will examine prior year’s financial statements to develop audit plans for

each significant balance sheet and income statement account.

Specific Audit

Approach

F

e

c

h

t

e

r

&

C

o

m

p

a

n

y,

C

P

A

s,

is

r

u

n

a

s

a

s

ol

e

p

r

o

p

ri

e

t

o

rs

hi

37

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 8

Preliminary Analysis

The primary focus of an audit is to develop expectations and compare actual

financial results against those expectations. We will compare the current

year’s results with budgetary expectations to identify any areas of material

misstatement.

Report Preparation

Unlike other firms, we prepare financial statements prior to field work. Doing

so allows us to focus on the overall financial position of the organization and

limits our testing of clearly insignificant areas.

Cash and Other Confirmations

We will confirm cash with the bank, any material year-end accounts or grants

receivable, grants or donations received during the year, debt outstanding at

the end of the year, and any other financial transaction that we consider

material to the financial statements as a whole. The decision to confirm a

statement item depends on the materiality of the item, the susceptibility of

the item to misstatement, or the likelihood of fraud.

Information Gathering

We will obtain the information requested in the PBC along with any

associated report required.

1. Testing statistical samples

During sample selection we consider three questions: (1) purpose of the

test—attribute or balance testing, (2) susceptibility of the population or

process to fraud or misstatement, and (3) size of transactions—small and

numerous, or large and infrequent.

2. Testing revenues and disbursements

In testing revenues and disbursements, we determine that the attribute

being tested is applied to the transaction as approved by the District’s

Management and Board; we do not determine whether a balance is

valued properly. For example, our sample for disbursements test has two

purposes—attributes testing, and control testing. In attribute testing we

see whether the amounts posted to the general ledger agree with the

invoices and canceled checks. Since disbursements have the potential for

defalcation, we check for any suspect or significant transactions that

appear to be out of place in your detailed general ledger. We may select

20 items based on the results of a random number generator, and select

another 20 to 40 items by scanning the detailed general ledger. The

result is an overall sample of 40 to 60 invoices to confirm compliance

Specific Audit

Approach (continued)

F

e

c

h

t

e

r

&

C

o

m

p

a

n

y,

C

P

A

s,

is

r

u

n

a

s

a

s

ol

e

p

r

o

p

ri

e

t

o

rs

hi

38

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 9

with board-approved procedures. We determine sample sizes in

accordance with the objective of the test, the population to be sampled,

and the risk associated with that population. The sample size also

depends on the size of the population and whether or not we will be able

to properly stratify populations into individually significant and

individually insignificant items.

3. Examining the District’s internal control structure

Among the items included in the PBC is a questionnaire regarding

internal controls. We will review the completed questionnaires and

compare them with procedures the District has established for actions

such as purchasing, cash and check collections, inventorying fixed assets,

billing, payroll disbursement, and budgeting. We will then audit each area

of internal control that will materially affect the audit.

4. Determining pertinent laws and regulations

We will examine items such as grant agreements to determine their

effect on the District, and audit them if necessary. We will also examine

pertinent ordinances to determine whether the District is in compliance.

5. Assessing risk

Generally accepted auditing standards require that we assess the risks of

material misstatement and fraud. After analyzing internal controls and

evaluating potential weaknesses, we will determine which areas of the

audit carry the risk of material misstatement, and take steps to mitigate

that risk.

6. Testing for functionality of internal controls

We will conduct random tests on a year-to-year basis to determine the

functionality of the District’s internal controls. We will randomly select

customers and trace each step of each payment into the system over the

course of a year. We will audit any area of potential weakness with a

specifically designed test.

7. Park District specific procedures

Park Districts have a number of different risk factors and areas due to the

nature of the district, with the many different types of programs and

services offered. We design specific audit procedures to address these

risks. Specifically, we would conduct secret shopping tests where we

would attempt to register for classes at the district at various classes and

locations and then trace the registrations to deposits during the audits.

Specific Audit

Approach (continued)

F

e

c

h

t

e

r

&

C

o

m

p

a

n

y,

C

P

A

s,

is

r

u

n

a

s

a

s

ol

e

p

r

o

p

ri

e

t

o

rs

hi

39

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 10

Fieldwork

With the assistance of Company personnel, we will test the balances resulting

from the following procedures:

Cash deposits

Internal control of disbursements

Payroll

Revenues

Inventory control

Billing and collections

Unrecorded liabilities

We will also discuss with the Board any specific concerns or procedures they

want performed.

Post-fieldwork Activities

Once we complete our fieldwork, we will resolve any pending items and

ensure that all requested third-party confirmations have been received. After

the District has reviewed the financial statements and any proposed adjusting

journal entries, we will obtain signed representation letters from the District

and from its counsel that confirm or explain any pending litigation against the

District and its effect on the audited financial statements.

Report Finalization and Final Analysis

Prior to finalizing the financial statements, we will perform a second

comparison of current year results with prior year results, and budgetary

expectations to actual results. Performing these tests subsequent to the audit

work provides additional assurance that the financial statements are free of

material misstatement.

Report Delivery and Board of Directors Presentation

We will deliver our report in person to the Board of Directors. We will also

attend a board meeting to answer questions that the Board may have. Our

aim is to create an open line of communication between our firm and your

organization so the Board feels comfortable asking for help with any

questions or issues that may arise during the year.

Specific Audit

Approach (continued)

F

e

c

h

t

e

r

&

C

o

m

p

a

n

y,

C

P

A

s,

is

r

u

n

a

s

a

s

ol

e

p

r

o

p

ri

e

t

o

rs

hi

40

Spreckels Community Services District

Proposal for Fiscal Audit Services, June 30, 2011 through 2015 P a g e 11

Audit Timeline

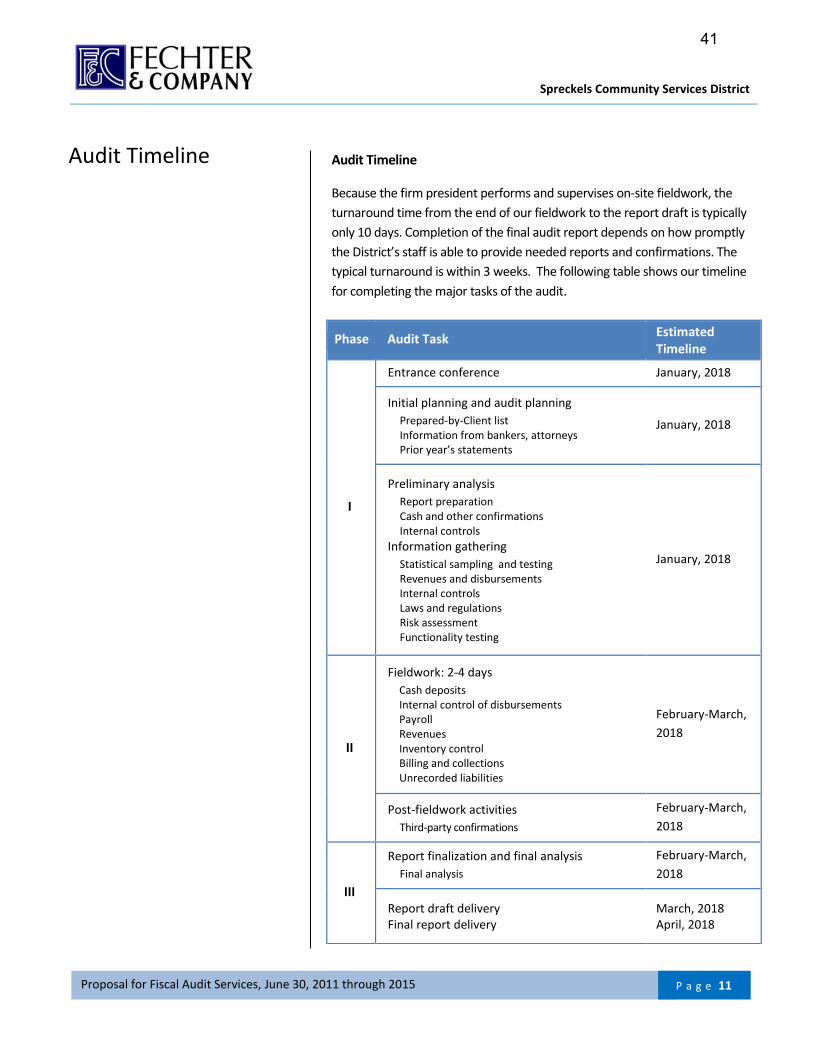

Because the firm president performs and supervises on-site fieldwork, the

turnaround time from the end of our fieldwork to the report draft is typically

only 10 days. Completion of the final audit report depends on how promptly