spnerstilnégf ulplr yeearss rceosnfultse 2007 rence

TRANSCRIPT

Name of chairman

Nestlé Full Year Results 2007

Name of chairman

SPRING PRESS CONFERENCE

February 21, 2008

2 Name of chairmanSPRING PRESS CONFERENCE 2008

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

Disclaimer

3 Name of chairmanSPRING PRESS CONFERENCE 2008

Key Figures

• Sales of CHF 107.6bn, up CHF 9.1bn (+9.2%)

• Above-target Organic Growth of 7.4%

• EBIT CHF 15 024m, up 12.9%, to 14% of sales

• Net Profit CHF 10 649m, up 15.8%

• Dividend up 17.3% to CHF 12.20

4 Name of chairmanSPRING PRESS CONFERENCE 2008

5 Name of chairmanSPRING PRESS CONFERENCE 2008

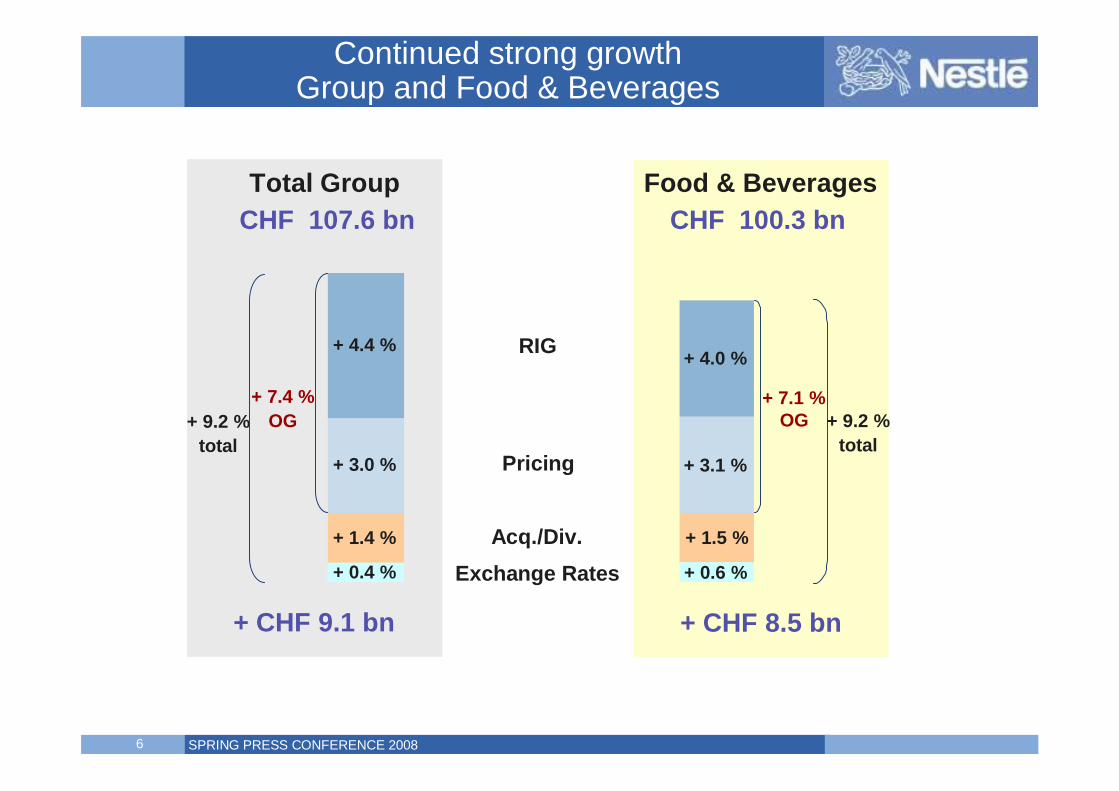

Continued strong growthGroup and Food & Beverages

Pricing

Acq./Div.Exchange Rates

CHF 107.6 bnTotal Group

+ CHF 9.1 bn

+ 9.2 %total

+ 3.0 %

+ 1.4 %

+ 0.4 %

+ 4.4 %

+ 7.4 %OG

RIG

6 Name of chairmanSPRING PRESS CONFERENCE 2008

Continued strong growthGroup and Food & Beverages

CHF 100.3 bnFood & Beverages

Pricing

Acq./Div.Exchange Rates

CHF 107.6 bnTotal Group

+ CHF 9.1 bn

+ 9.2 %total

+ 3.0 %

+ 1.4 %

+ 0.4 %

+ 4.4 %

+ CHF 8.5 bn

+ 7.1 %OG + 9.2 %

total

+ 4.0 %

+ 0.6 %

+ 1.5 %

+ 3.1 %

+ 7.4 %OG

RIG

7 Name of chairmanSPRING PRESS CONFERENCE 2008

2007 Highlights – all metrics improveDelivering the Nestlé Model

+ 9.2 %+ 7.4 %

+ 12.9 %+ 50 bps

+ 15.8 %+ 60 bps

- 10 bps

+ 15.1 %

+ 100 bps+ 50 bps

CHF 107.6 bn

CHF 15.0 bn14.0 %

CHF 10.6 bn9.9 %

6.6 %

CHF 13.4 bn

22.2 %12.2 %

+ CHF 9.1 bn

+ CHF 1.7 bn

+ CHF 1.4 bn

+ CHF 1.7 bn

Sales – totalOrganic growth

EBITEBIT margin

Net profitNet profit margin

Working capital (% of sales)

Operating cash flow

ROIC- before goodwill- after goodwill

Improvements FY 07 v 06 FY 07 Total

8 Name of chairmanSPRING PRESS CONFERENCE 2008

Food and BeveragesAll metrics improve

2007

2006

RIG OG EBIT margin

Sales

CHF 100.3 bn

CHF 91.8 bn

+ 9.2 % + 40 bps

12.6 %

12.2 %

Strongon-goinggrowth

4.0 %

7.1 %

5.9 %

4.2 %

EBIT

+ 12.7 %

CHF 12.6 bn

CHF 11.2 bn

9 Name of chairmanSPRING PRESS CONFERENCE 2008

Dairy(incl. Ice cream)

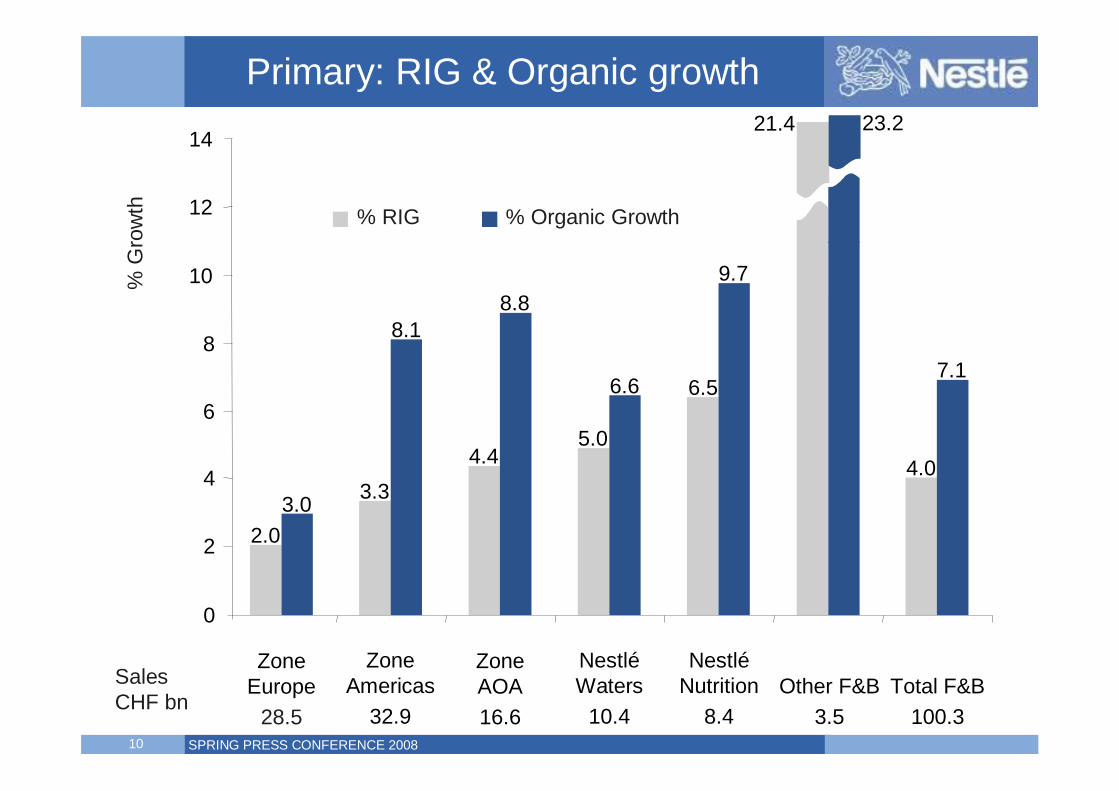

Product groups RIG & organic growth

% RIG % Organic growth

% G

row

th

7.6

5.0

1.7

6.5

3.22.3

3.8

10.210.3

6.6

7.8

9.7

4.0

5.3

7.0

11.0

0

2

4

6

8

10

12

Powdered & Liquid Beverages(ex-Nestlé Waters)

NestléWaters

NestléNutrition

Prepared dishes & cooking aids

Confectionery PetCare Pharma

SalesCHF bn 17.9 10.4 20.7 8.4 18.5 12.3 7.312.1

Total Beverages (RIG 6.6 % OG 8.9 %) Total Milk, Nutrition & Ice cream (RIG 2.8 % OG 8.3 %)

10 Name of chairmanSPRING PRESS CONFERENCE 2008

% G

row

th % RIG % Organic Growth

SalesCHF bn

Primary: RIG & Organic growth

2.0

3.34.4

5.0

6.5

21.4

4.0

3.0

8.18.8

6.6

9.7

23.2

7.1

ZoneEurope

28.5

ZoneAmericas

32.9

ZoneAOA16.6

NestléWaters

10.4

NestléNutrition

8.4Other F&B

3.5Total F&B

100.3

0

2

4

6

8

10

12

14

11 Name of chairmanSPRING PRESS CONFERENCE 2008

F&B "Billionaire Brands" represent about 70 % of F&B sales

12 Name of chairmanSPRING PRESS CONFERENCE 2008

Superpremium ChocolateLaunch of premium product range

Key Innovation & Renovation 2007 -supporting our Billionaire Brands

DibsLow Temperature Freezing

Chocolate & Malted Beverages60/40+ (Actigen-E & Protomalt)

NAN, BEBA, NIDINA, NIDALwith BABs strengthening and

enhancing the infants immune system

Dolce GustoFrom 3 countries in 2006 to 11 in 2007

NIDO Nutrition SystemAge specific nutrition solution

with probiotics (lactobacillus protectus)

13 Name of chairmanSPRING PRESS CONFERENCE 2008

Quality & Technology

R&D Development Platformswill drive further Innovation

60/40 Profiling Systems & Packaging

Nutrition, Health & Wellness

Functional Quality

Taste Packaging

14 Name of chairmanSPRING PRESS CONFERENCE 2008

2007 Full Year ResultsKey factors of margin improvement

EBIT2006

COGS Distribution Marketing R&D EBIT2007

13.5 %

+ Operation Excellence+ Mix

- Input costs

- 60

GROUP EBIT MARGIN + 50 bps (+ 60 constant currency)F&B EBIT MARGIN + 40 bps (+ 50 constant currency)

Spend+ 8.1 % 14.0 %

EBIT + 12.9 %+ CHF 1.7 bn

+ 20

CHF spend + 1.5 bnMedia % up with sales+ Trade spend efficiencies+ Volume growth

+ 90

+ GNBS+ Growth+ Efficiencies

Administration- 10

+ 10+ 50

15 Name of chairmanSPRING PRESS CONFERENCE 2008

Increased earnings per share, proposed dividend and payout ratio

Dividend per share CHFEarnings per share (Full) CHF

19.51

17.04

+ 16.4%

7.20

16.05

8.00

10.40

23.90

20062003 2004 2005 2007

9.00

20.78

12.20

27.81

+ 17.3%

CHF 4.4 bn of shares bought backin 2007 – on going

16 Name of chairmanSPRING PRESS CONFERENCE 2008

Improved management of working capital

Working capital total (in % sales)

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

Working capital total includes Trade receivables, Inventories, Trade payables, Other receivables, Prepayments, Accruals, Current tax payables and Other short term payables. Calculation is based on year-end figures.

10 bpsimprovement

2003 2004 2005 2006 2007

7.2

6.9

7.7

6.7 6.6

17 Name of chairmanSPRING PRESS CONFERENCE 2008

Free cash flow (FCF)

Strong cash flow generation

Operating cash flow (OCF)

0

2

4

6

8

10

6.64

10.41

6.56

10.21

7.02

11.68

2005 2006 20072003 2004

6.36

10.13

CH

F bi

llion 12

OCF+ CHF 1.76 bn

FCF+ CHF 1.21 bn

8.23

13.4414

18 Name of chairmanSPRING PRESS CONFERENCE 2008

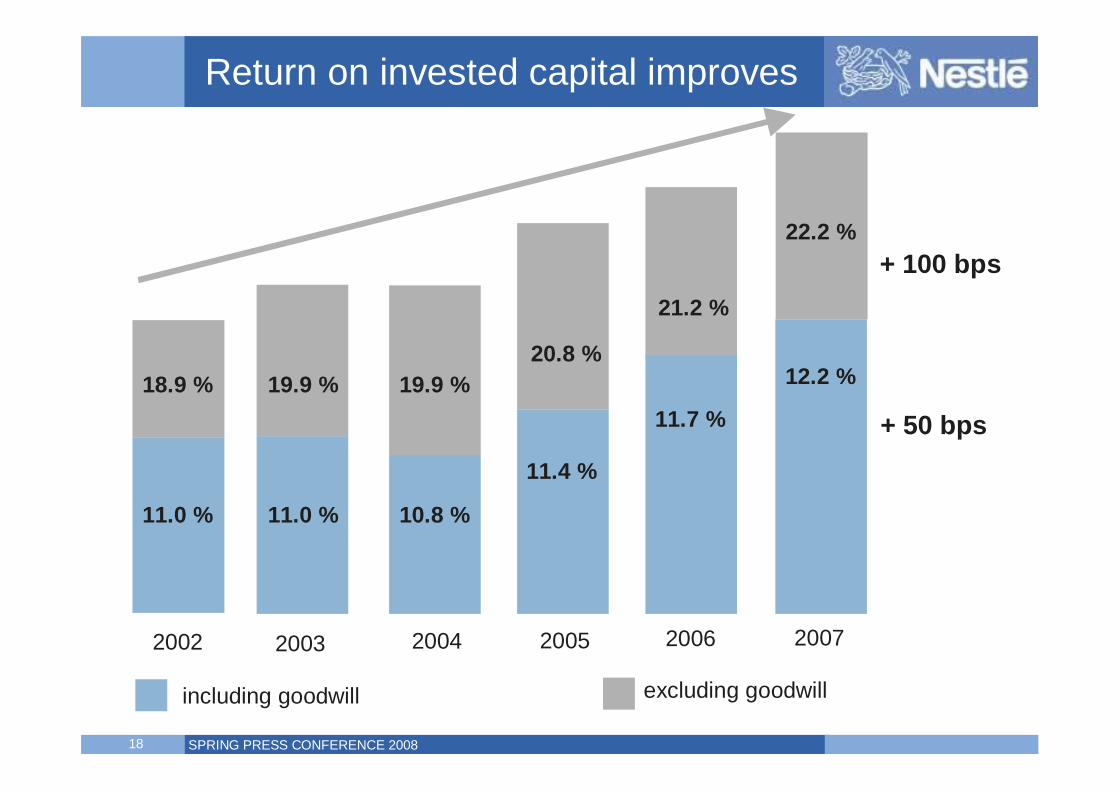

Return on invested capital improves

excluding goodwillincluding goodwill

2005

20.8 %

2002

18.9 %

11.0 %

2003

19.9 %

11.0 %

2004

19.9 %

10.8 %

+ 100 bps

+ 50 bps11.4 %

2006

21.2 %

11.7 %

12.2 %

22.2 %

2007

19 Name of chairmanSPRING PRESS CONFERENCE 2008

Acquisitions

Acquisition of Novartis Medical Nutrition

Acquisition of Gerber

Acquisition of Henniez water in Switzerland

Strategic partnership with Belgian luxury chocolate maker Pierre Marcolini

Acquisition of Ruzskaya Confectionery Factory in Russia

20 Name of chairmanSPRING PRESS CONFERENCE 2008

Disposal of canned and powdered milk category in Canada

Disposal of all Nestlé Canada Roast & Ground brands such as CLUB COFFEE, GOOD HOST, ANTHOS COFFEE, SANTOS COFFEE and MARTICAN

Schöller Private Label ice cream business in Germany

Other disposals: Margarine & Fat business in Chile, Negro confectionery business in Hungary, Jam’s culinary products (sauces and others) in Czeck/Slovak, ... Nestlébroadens strategic co-operation with Barry Callebaut in Europe

Disposal of home delivery service for ice-cream and frozen food in Germany

Divestitures

Liquid milk businesses in Thailand, Malaysia, Singapore and Brunei

Disposal of Turtle confectionery brand in USA. Kept brand in Canada

21 Name of chairmanSPRING PRESS CONFERENCE 2008

2007 Summarised

Ø 9.2 % sales growth; 7.4 % organic growth

Ø EBIT margin up 50 bps to 14 %

Ø Nestlé generated an additional - CHF 9.1 billion of sales- CHF 1.7 billion of EBIT- CHF 1.4 billion of net profit- CHF 1.7 billion of operating cash flow

Ø Well placed for further improvement in 2008 - another year of delivering the Nestlé Model- Strong EPS & share buyback contribute to outperforming long-term shareholder value creation

22 Name of chairmanSPRING PRESS CONFERENCE 2008

23 Name of chairmanSPRING PRESS CONFERENCE 2008

11 yearsaverage

Acquisitions

DivestituresForex

OG: OrganicGrowth

3.7%

2.2%

2.5%

-1.2%

OG5.9%

-1.5%

RIG Pricing & Other Acquisitions Divestitures FX Impact

Consistent Top-Line Organic Growth for the past 11 Years

% Growth

-10%

-5%

0%

5%

10%

15%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

24 Name of chairmanSPRING PRESS CONFERENCE 2008

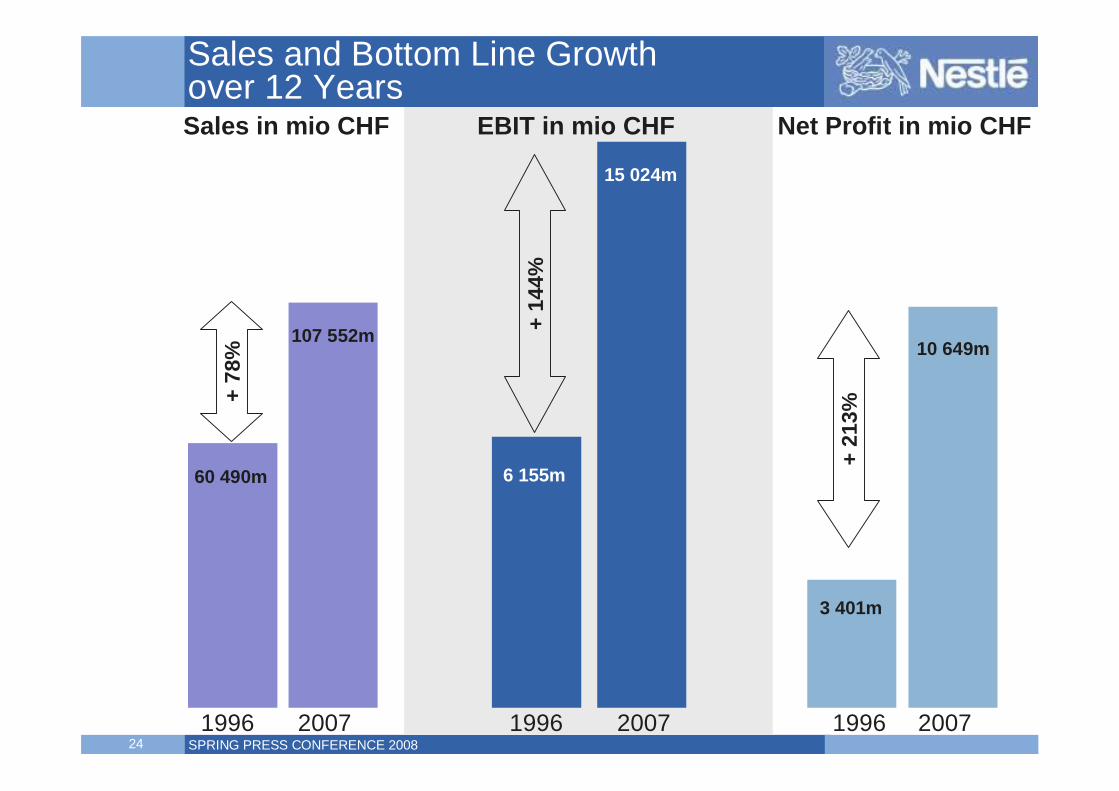

Sales and Bottom Line Growthover 12 Years

1996 1996 19962007

Sales in mio CHF

2007 2007

EBIT in mio CHF Net Profit in mio CHF

+ 78

%

+ 14

4%

+ 21

3%

60 490m

107 552m

6 155m

3 401m

10 649m

15 024m

25 Name of chairmanSPRING PRESS CONFERENCE 2008

Sales and Bottom Line Growthover 12 Years

1996 1996 19962007

Sales in mio $

2007 2007

EBIT in mio $ Net Profit in mio $

+ 84

%

+ 15

3%

+ 22

5%

48 782m

89 927m

4 964m

2 743m

8 904m

12 562m

26 Name of chairmanSPRING PRESS CONFERENCE 2008

SustenancePleasure andPleasure anddiversitydiversity

ConvenienceConvenience

5,000 13,000 22,000

Per-capita income (PPP)

Consumption of food manufacturing value-added

actual US$, per capita

28,000

Nestlé per capita sales

Sources: UNIDO (value-added), WIDER and World Bank; Nestlé F&C; analysis EIR

Growth scenario (2005-15)

+ US$ 170bn5.9% p.a.

Growth scenario (2005-15)

+ US$ 70bn6.9% p.a.

Demographics Focusing on the Low and High Ends

US$ 1,500

PPP

$240 billion opportunity PREMIUMIZATION

27 Name of chairmanSPRING PRESS CONFERENCE 2008

The Nestlé Fleet Strategy

28 Name of chairmanSPRING PRESS CONFERENCE 2008

GLOBE

• leverage our size as a strength

• unite/align the Group internally to be more

competitive externally

• exploit the power of e-technology

29 Name of chairmanSPRING PRESS CONFERENCE 2008

Total Shareholder Return over 12 Years

30 Name of chairmanSPRING PRESS CONFERENCE 2008

Nestlé Rated 7TH in Barron’s Survey: Most Respected Companies

31 Name of chairmanSPRING PRESS CONFERENCE 2008

Articles of AssociationQuorum, Majority

OLD:

attendance quorum, super majority

NEW:

two third majority of shares represented at AGM

32 Name of chairmanSPRING PRESS CONFERENCE 2008

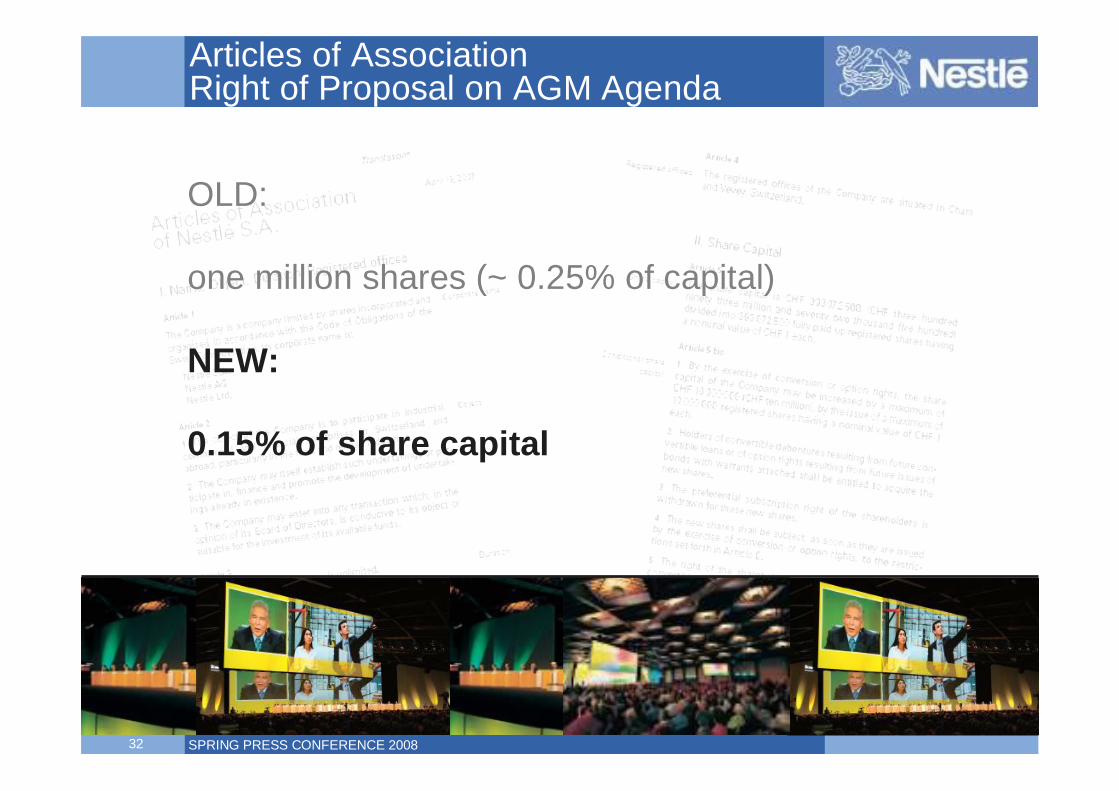

Articles of Association Right of Proposal on AGM Agenda

OLD:

one million shares (~ 0.25% of capital)

NEW:

0.15% of share capital

33 Name of chairmanSPRING PRESS CONFERENCE 2008

Articles of AssociationTerms of Office for Board Members

OLD: 5 years

NEW: 3 years

34 Name of chairmanSPRING PRESS CONFERENCE 2008

Articles of AssociationVoting Limitations

OLD: 3 percent

NEW: 5 percent

35 Name of chairmanSPRING PRESS CONFERENCE 2008

36 Name of chairmanSPRING PRESS CONFERENCE 2008

Outlook 2008 – The Nestlé Model

• Organic Growth 5 – 6 %

• Further improvement of EBIT margins

in constant currencies

• Further capital efficiency improvement

37 Name of chairmanSPRING PRESS CONFERENCE 2008

38 Name of chairmanSPRING PRESS CONFERENCE 2008

Next Media Events

10 April 2008 – Annual General Meeting21 April 2008 – First Quarter Sales

7 August 2008 – Half-Year Results23 October 2008 – Autumn Press Conference