spm 9541 december 2010 - tu delft … 9541 december 2010 aad correljé june 29, 2011 2 programme...

TRANSCRIPT

Pricing, markets and investments

SPM 9541

December 2010Aad Correljé

June 29, 2011 2

Programme

Visions on gas prices

Gasmarkets

Market prices?

Pricing systems

June 29, 2011 3

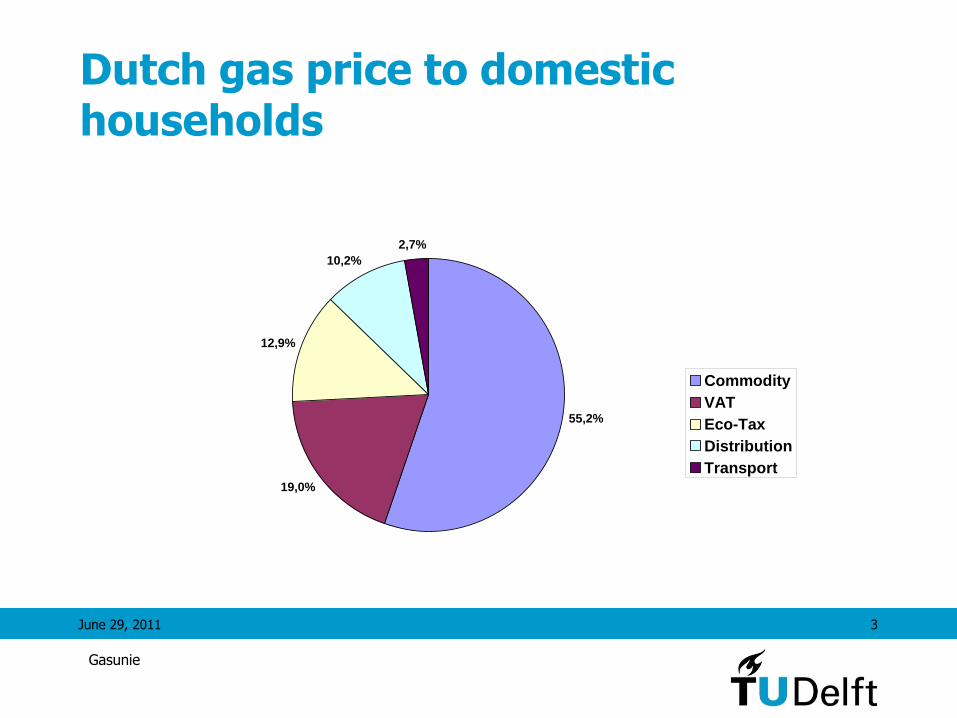

Dutch gas price to domestic households

55,2%

19,0%

12,9%

10,2%

2,7%

Commodity

VAT

Eco-Tax

Distribution

Transport

Gasunie

June 29, 2011 4

Hybrid gas pricing

• Production: Long term term Take or Pay, Destination clause, Net Back contracts

• Transmission: Cost plus

• Storage: Cost plus or….

• Distribution: Cost plus or….

• Retail: Oil parity pricing, market segmentation…

• En Title Transfer Facility

June 29, 2011 5

Market places NL

• GOS: bilateral, long term (1 y.), specific oil parity based contract

• TTF: bilateral, short term (1 m.), standard contract, gas-to-gas price

• TTF: APX, short term (1 d.), standard contract, gas-to-gas price

• TTF: Endex, Long term future (1 j.), standard contract, gas-to-gas prijzen

June 29, 2011 6

Consumer contracts via traders

Contractprijs

Marktprijs

Variable prijs

Prijs range

Vaste prijs

Max. prijs

A. Correlje

June 29, 2011 7

Gas prices since 1993

Gasunie

June 29, 2011 8

Once there was a country….

FERC

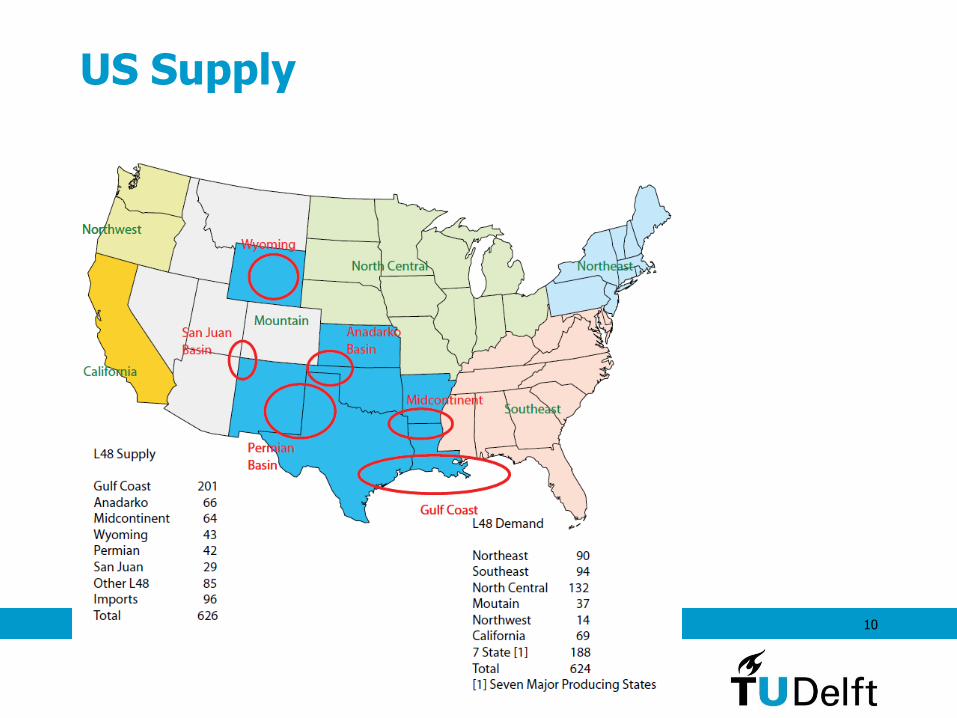

USA Gas Transport Infrastructure

5-10 major ‘interstate’ Gas Infrastructure Companies

US Supply

June 29, 2011 10

28

CONSTRUCTEDA. Everett, MA : 1.035 Bcfd (Tractebel - DOMAC)B. Cove Point, MD : 1.0 Bcfd (Dominion - Cove Point LNG)C. Elba Island, GA : 0.68 Bcfd (El Paso - Southern LNG)D. Lake Charles, LA : 1.0 Bcfd (Southern Union - Trunkline LNG)E. Gulf of Mexico: 0.5 Bcfd, (Gulf Gateway Energy Bridge - Excelerate Energy)APPROVED BY FERC1. Lake Charles, LA: 1.1 Bcfd (Southern Union - Trunkline LNG)2. Hackberry, LA : 1.5 Bcfd, (Sempra Energy)3. Bahamas : 0.84 Bcfd, (AES Ocean Express)*4. Bahamas : 0.83 Bcfd, (Calypso Tractebel)*5. Freeport, TX : 1.5 Bcfd, (Cheniere/Freeport LNG Dev.)6. Sabine, LA : 2.6 Bcfd (Cheniere LNG)7. Elba Island, GA: 0.54 Bcfd (El Paso - Southern LNG)8. Corpus Christi, TX: 2.6 Bcfd, (Cheniere LNG)9. Corpus Christi, TX : 1.0 Bcfd (Vista Del Sol - ExxonMobil)10. Fall River, MA : 0.8 Bcfd, (Weaver's Cove Energy/Hess LNG)11. Sabine, TX : 1.0 Bcfd (Golden Pass - ExxonMobil)12. Corpus Christi, TX: 1.0 Bcfd (Ingleside Energy - Occidental Energy Ventures)APPROVED BY MARAD/COAST GUARD13. Port Pelican: 1.6 Bcfd, (Chevron Texaco)14. Louisiana Offshore : 1.0 Bcfd (Gulf Landing - Shell)CANADIAN APPROVED TERMINALS15. St. John, NB : 1.0 Bcfd, (Canaport - Irving Oil)16. Point Tupper, NS 1.0 Bcf/d (Bear Head LNG - Anadarko)MEXICAN APPROVED TERMINALS17. Altamira, Tamulipas : 0.7 Bcfd, (Shell/Total/Mitsui)18. Baja California, MX : 1.0 Bcfd, (Sempra)19. Baja California - Offshore : 1.4 Bcfd, (Chevron Texaco)PROPOSED TO FERC20. Long Beach, CA : 0.7 Bcfd, (Mitsubishi/ConocoPhillips - Sound Energy Solutions)21. Logan Township, NJ : 1.2 Bcfd (Crown Landing LNG - BP)22. Bahamas : 0.5 Bcfd, (Seafarer - El Paso/FPL )23. Port Arthur, TX: 1.5 Bcfd (Sempra)24. Cove Point, MD : 0.8 Bcfd (Dominion)25. LI Sound, NY: 1.0 Bcfd (Broadwater Energy - TransCanada/Shell)26. Pascagoula, MS: 1.0 Bcfd (Gulf LNG Energy LLC)27. Bradwood, OR: 1.0 Bcfd (Northern Star LNG - Northern Star Natural Gas LLC)28. Pascagoula, MS: 1.3 Bcfd (Casotte Landing - ChevronTexaco)29. Cameron, LA: 3.3 Bcfd (Creole Trail LNG - Cheniere LNG)30. Port Lavaca, TX: 1.0 Bcfd (Calhoun LNG - Gulf Coast LNG Partners)31. Freeport, TX: 2.5 Bcfd, (Cheniere/Freeport LNG Dev. - Expansion)PROPOSED TO MARAD/COAST GUARD32. California Offshore: 1.5 Bcfd (Cabrillo Port - BHP Billiton)33. So. California Offshore : 0.5 Bcfd, (Crystal Energy)34. Louisiana Offshore : 1.0 Bcfd (Main Pass McMoRan Exp.)35. Gulf of Mexico: 1.0 Bcfd (Compass Port - ConocoPhillips)36. Gulf of Mexico: 2.8 Bcfd (Pearl Crossing - ExxonMobil)37. Gulf of Mexico: 1.5 Bcfd (Beacon Port Clean Energy Terminal - ConocoPhillips)38. Offshore Boston, MA: 0.4 Bcfd (Neptune LNG - Tractebel)39. Offshore Boston, MA: 0.8 Bcfd (Northeast Gateway - Excelerate Energy)

Existing and Proposed North American LNG

Terminals

As of July 21, 2005

FERC

Office of Energy Projects

A

3 4

22

3220

34

33

14

B

1

24

35

US Jurisdiction

FERC

US Coast Guard

* US pipeline approved; LNG terminal pending in Bahamas

26

1025

21

29

7C

2D11

2336

37

13

5,31

9

6

3827

E

15

17

16

1819

39

8

1230

Utilization…

June 29, 2011 12

13

The gas market

June 29, 2011 14

TTF Gasprices

0,00000

0,10000

0,20000

0,30000

0,40000

0,50000

0,60000

0,70000

0,80000

0,90000

1,00000

Gas

day

15-1

-200

8

15-1

2-20

07

14-1

1-20

07

14-1

0-20

07

13-9

-200

7

13-8

-200

7

13-7

-200

7

12-6

-200

7

12-5

-200

7

11-4

-200

7

11-3

-200

7

8-2-

2007

8-1-

2007

8-12

-200

6

7-11

-200

6

7-10

-200

6

6-9-

2006

6-8-

2006

6-7-

2006

5-6-

2006

5-5-

2006

4-4-

2006

4-3-

2006

1-2-

2006

1-1-

2006

Imbalance prices HGP €/m3 Neutral Gasprice Imbalance prices LGP €/m3 Neutral Gasprice Imbalance prices TTF price €/m3 Neutral Gasprice

Gasunie

June 29, 2011 15

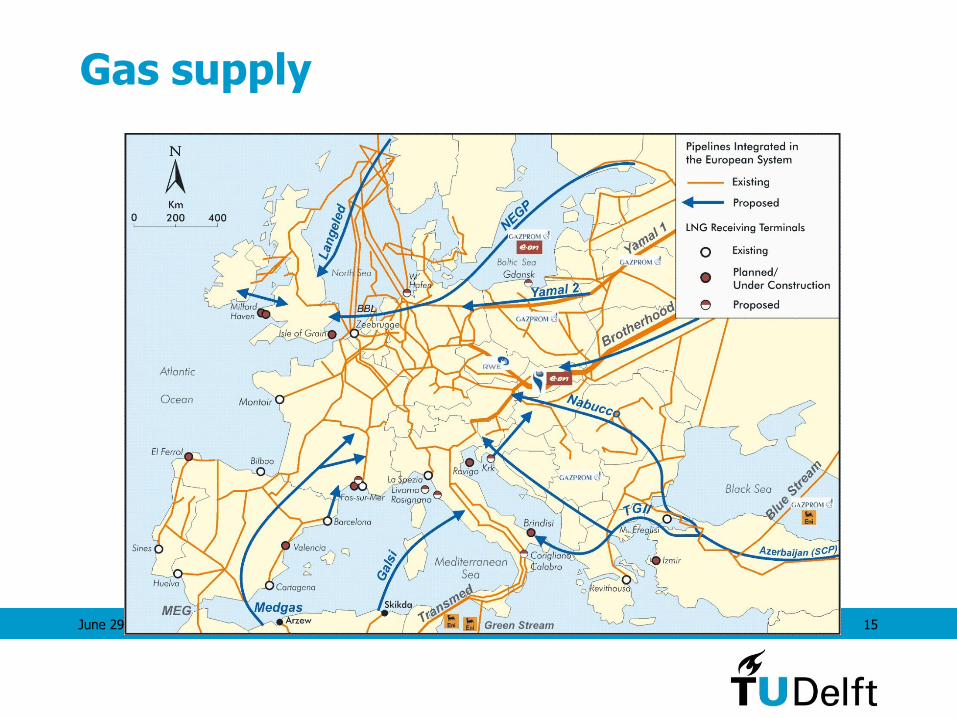

Gas supply

Daily volumes TTF

1 Jan 2003 - 9 Feb 2008

0

20

40

60

80

100

120

140

160

180

200

1-0

1-2

003

1-0

1-2

004

1-0

1-2

005

1-0

1-2

006

1-0

1-2

007

1-0

1-2

008

Mil

lio

n m

3

0

10

20

30

40

50

60

70Traded volume

Net volume

Number of active

parties

June 29, 2011 16

Existing and potential gas hubs in Europe

CERR

European Gas Infrastructure Companies

Most transport companies are private and belong to integrated

midstream players

June 29, 2011 18

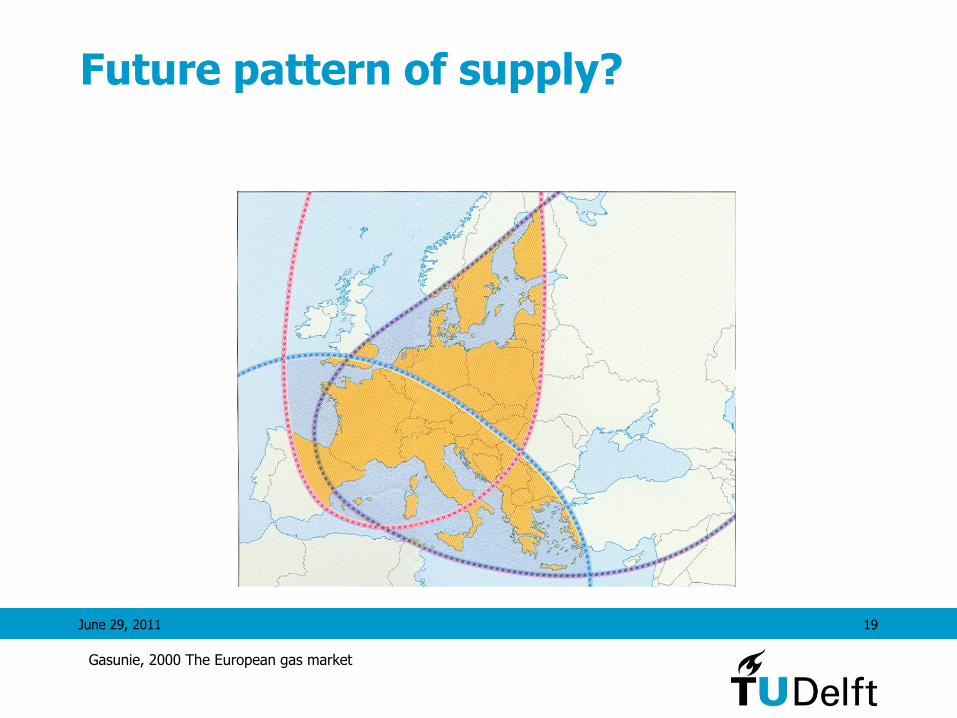

Current pattern of supply

Gasunie, 2000 The European gas market

June 29, 2011 19

Future pattern of supply?

Gasunie, 2000 The European gas market

June 29, 2011 20

Market power: Reduces welfare

Price (P)

Quantity (Q)

supply

demand

Pe

QeQm

Pm

Supply Monopoly

Dead-weight loss

A. Correlje

June 29, 2011 21

Competitive market?

• Many suppliers

• Many consumers

• U-shaped average cost function

• Homogeneous product

• Full information

• No transaction costs

• Free entry and exit

Producers

June 29, 2011 22

EDI, 2007

Producers consume a lot

June 29, 2011 23

EDI, 2007

June 29, 2011 24

Reality

• Complexity

• Uncertainty

• Strategic behaviour

25

European Gas Supply/Demand Outcomes

HighGrowth

DEMAND

LowGrowth

TightSUPPLY

Abundant

Gas Shortages

Managed Market

Low Gas Prices

High Gas Prices

MC Kinsey

26

Pressures that Can Change the Supply/Demand Outcome for European Gas High

Growth

DEMAND

LowGrowth

TightSUPPLY

Abundant

GasShortages

ManagedMarket

Low GasPrices

High GasPrices

Gas - PowergenFuel of Default

Recession

Coal PlantsSelected

EfficiencyPrograms

LNG Hiatus

Gazprom CaspianConstraints

Yamal Delays

Infrastructure Delays

Norway

GASPEC

Sonatrach Controls

Policy

Egypt/Libya exports

Iran Exports

Low Russian Domestic Market

North SeaIndependents

N American Unconventional Gas

MC Kinsey

June 29, 2011 27

6) Gas markets as a globalizing system

• Transit issues become important

• Value chains stretches out over several (different) jurisdictions

• Systems of governance stem from different institutional traditions

• Variation in maturity and spatial characteristics of systems