special meeting of shareholders - avantimining.com · share price (nov 24, 2014) $0.060 ... site...

TRANSCRIPT

TSX-V:AVT

Special Meeting of Shareholders

www.avantimining.com

Strictly Private and Confidential

November 28th, 2014

This presentation contains certain forward-looking information concerning the business of Avanti Mining Inc. (the “Corporation”). All statements, other than statements of historical fact, included herein including, without

limitation; the availability, timing and structure of financing for the Corporations’ working capital and for construction of the project; the estimated project timeline including anticipated dates for receipt of permits and

approvals, construction, start-up and production, and other milestones; anticipated mine design or life of mine; anticipated results of the enterprise optimization plan and other analyses; resource and reserve estimates;

the future demand and supply of molybdenum; the terms and timing of any off take arrangements; estimated timing and amounts of future expenditures, and the Corporation’s future production, operating and capital

costs, internal rate of return, tax rates, anticipated timing to pay back capital investments, operating or financial performance, potential taxes to be paid and potential jobs created are forward-looking statements. These

forward-looking statements are based on the opinions of management at the date the statements are made and are based on assumptions and subject to a variety of risks and uncertainties and other factors that could

cause actual events to differ materially from those projected in forward-looking statements. Important factors that could cause actual results to differ materially from the Corporation’s expectations include fluctuations in

commodity prices and currency exchange rates; the need to obtain financing to construct a mine and uncertainty as to the availability and terms of future financing; uncertainties relating to interpretation of drill results

and the geology, continuity and grade of mineral deposits; uncertainty of estimates of capital and operating costs, recovery rates, production estimates and estimated economic return; the need for cooperation of

government agencies and native groups in the exploration and development of properties and the issuance of required permits; the possibility of delay in exploration or development programs or in construction projects

and uncertainty of meeting anticipated program milestones; uncertainty as to timely availability of permits and other governmental approvals; and other risks and uncertainties disclosed in the Corporation’s Annual

Information Form dated May 29, 2014, which is available at www.sedar.com. The Corporation is under no obligation to update forward-looking statements if circumstances or management’s opinions should change,

except as required by applicable securities laws. The viewer is cautioned not to place undue reliance on forward-looking statements.

This presentation may also contain future-oriented financial information (“FOFI”) and information which could be considered to be in the nature of a “financial outlook”. Such FOFI or financial outlook was approved by

Management as of the date of presentation for the purpose of providing Management’s reasonable estimate of what return investors might expect to earn based on the assumptions set forth in such estimates and the

information may not be appropriate for other purposes. Management cautions that such FOFI or financial outlook reflects the Corporation’s current beliefs and are based on information currently available to the

Corporation and on assumptions the Corporation believes are reasonable. Actual results and developments may differ materially from results and developments discussed in the FOFI or financial outlook as they are

subject to a number of significant risks and uncertainties. Certain of these risks and uncertainties are beyond the Corporation’s control. Consequently, all of the FOFI or financial outlook are qualified by these cautionary

statements, and there can be no assurances

This presentation uses the terms “proven and probable reserves”, “measured resources”, “indicated resources” and “inferred resources”. The Company advises readers that although these terms are recognized and

required by Canadian regulations (under National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”)), the United States Securities and Exchange Commission does not recognize resources.

Readers are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. In addition, “inferred resources” have a great amount of uncertainty as to their

existence, and economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral

resources may not form the basis of feasibility or pre-feasibility studies, or economic studies, except for a Preliminary Assessment as defined under NI 43-101. Investors are cautioned not to assume that part or all of an

inferred resource exists, or is economically or legally mineable.

Certain technical data in this presentation was taken from the technical report entitled “Kitsault Molybdenum Project, British Columbia, Canada, NI 43-101 Technical Report” with an effective date of March 14, 2014,

prepared by Scott Fulton, P.Eng., David G. Thomas, P.Geo., Ramon Mendoza Reyes, P.Eng. and Simon Allard, P.Eng. of AMEC Americas Limited, Peter Healey, P.Eng. and Michael Levy, P.E. of SRK Consulting

(Canada) Inc. and Bruno Borntraeger, P.Eng of Knight Piésold Ltd., and is subject to all of the assumptions, qualifications and procedures described therein. The Qualified Person who supervised the preparation of the

technical information in this presentation is Jeff Lowe.

THIS PRESENTATION IS NOT AN OFFER TO PURCHASE SECURITIES AND DOES NOT CONSTITUTE AN OFFERING DOCUMENT UNDER SECURITIES LEGISLATION. ANY UNAUTHORIZED

DISSEMINATION OR USE OF THIS PRESENTATION IS STRICTLY PROHIBITED.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

All figures in CAD unless otherwise noted

Avanti at a Glance

3

Prince Rupert

Operations Office

(Vancouver)

Head Office

(Toronto)

Kitsault mine

British Columbia

Canada

Strategy: Become the unique supplier of

steel alloy metals

Cornerstone to this strategy: The

development of the Kitsault molybdenum

project (“Kitsault”)

Once Kitsault is developed, Avanti will

look to grow through the acquisition of

other assets producing steel alloys

commodities

Terrace

4

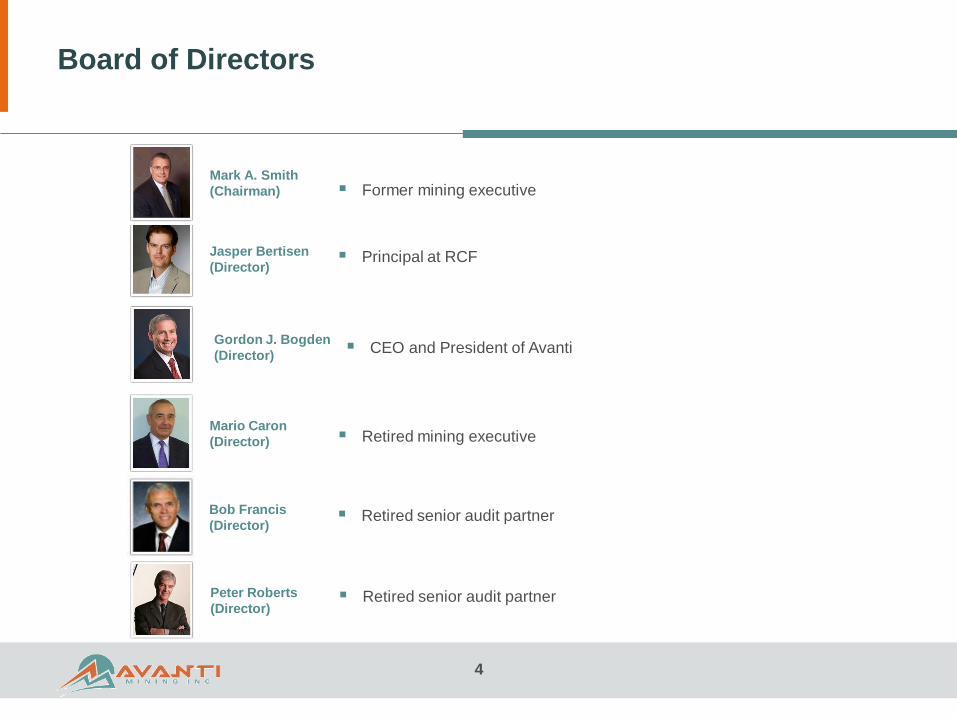

Board of Directors

Bob Francis

(Director) Retired senior audit partner

Jasper Bertisen

(Director) Principal at RCF

Mark A. Smith

(Chairman) Former mining executive

Peter Roberts

(Director) Retired senior audit partner

Mario Caron

(Director) Retired mining executive

Gordon J. Bogden

(Director) CEO and President of Avanti

5

Avanti Management Team

Gordon J. Bogden

CEO, President and Director

Graham du Preez

CFO

Shawn Howarth

VP, Corporate Development

and Investor Relations

Shane Uren

VP, Environmental

Greg Miazga

Construction Manager, Kitsault Project

Luke Klemke

General Manager, Kitsault Project

Kimberly A. Humphreys

VP, Human Resources

Jeff Lowe

COO

6

Capital Structure

1. US$20 million Bridge Loan with option to convert at $0.07/share; US$50 million Pre-Construction Loan with option to convert at $0.055/share; figures

converted to CAD at CAD/USD rate 0.8800

2. Calculated on basic market capitalization; adjusted for estimated cash balance and debt outstanding

Share Price (Nov 24, 2014) $0.060

Shares Outstanding

Basic, Pre-Consolidation 550 million

Fully Diluted, Pre-Consolidation 1.9 billion

Market Capitalization (Basic) $33 million

Market Capitalization (Fully Diluted) $114 million

Debt Facilities

Bridge Loan (Convertible)1 $23 million

Pre-Construction Loan (Convertible)1 $57 million

Bridge Loan (Currently Undrawn) $49 million

Cash Balance $27 million

7

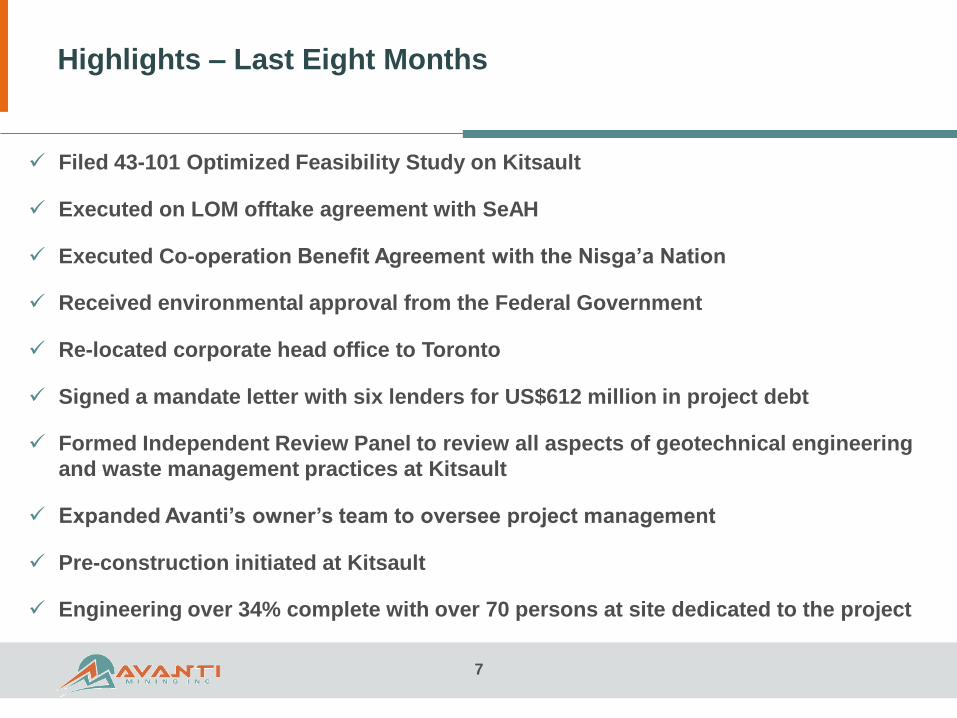

Highlights – Last Eight Months

Filed 43-101 Optimized Feasibility Study on Kitsault

Executed on LOM offtake agreement with SeAH

Executed Co-operation Benefit Agreement with the Nisga’a Nation

Received environmental approval from the Federal Government

Re-located corporate head office to Toronto

Signed a mandate letter with six lenders for US$612 million in project debt

Formed Independent Review Panel to review all aspects of geotechnical engineering

and waste management practices at Kitsault

Expanded Avanti’s owner’s team to oversee project management

Pre-construction initiated at Kitsault

Engineering over 34% complete with over 70 persons at site dedicated to the project

8

Kitsault Molybdenum Project

9

Avanti’s Corporate Responsibility

Employee Wellness

First Nations Engagement

Environmental Responsibility

Operations Engagement

Government (Provincial

and Federal) Engagement

Safety

Nisga’a

Gitanyow

Metlakatla

Wilp Luxxhon

Capital

Foundation

10

Community Engagement

First Nations Support

CBA signed between the Nisga’a Lisims Government and Avanti

Kitsault Mines Ltd. on June 1, 2014

Training / Workshops

Avanti Kitsault has hosted three workshops in relation to

business contracting, employment and training

Partnership with Nisga’a Employment and Skills Training

Landmark, Precedent

Setting Agreement

Provides commercial and training initiatives with our economic

partner in the region

Site specific water quality standards at the highest level

High Quality Primary Molybdenum Project

11

Ownership 100% Avanti

Mineralization Molybdenum – Silver

Molybdenum Reserves 190,600 t @ 0.082% Mo

Mining Method Conventional Open Pit

Throughput Rate 45,000 tpd

Strip Ratio 1:1

Processing Method Milling and Flotation

Average Metallurgical Recovery 88.5% Mo, 39% Ag1

Mine Life (Reserves Only) 14 Years

Average Molybdenum Production 11,570 tpa

Initial Capital $818 million

Operating Costs (Before By-Product) $6.78 / US$5.96 per lb

Operating Costs (Net of By-Product) $5.82 / US$5.12 per lb

Planned Start-Up 2017

Source: Kitsault Optimization Study (April 2014)

1. Currently looking to improve silver recovery through additional metallurgical test work

Kitsault Project

Kitsault Project

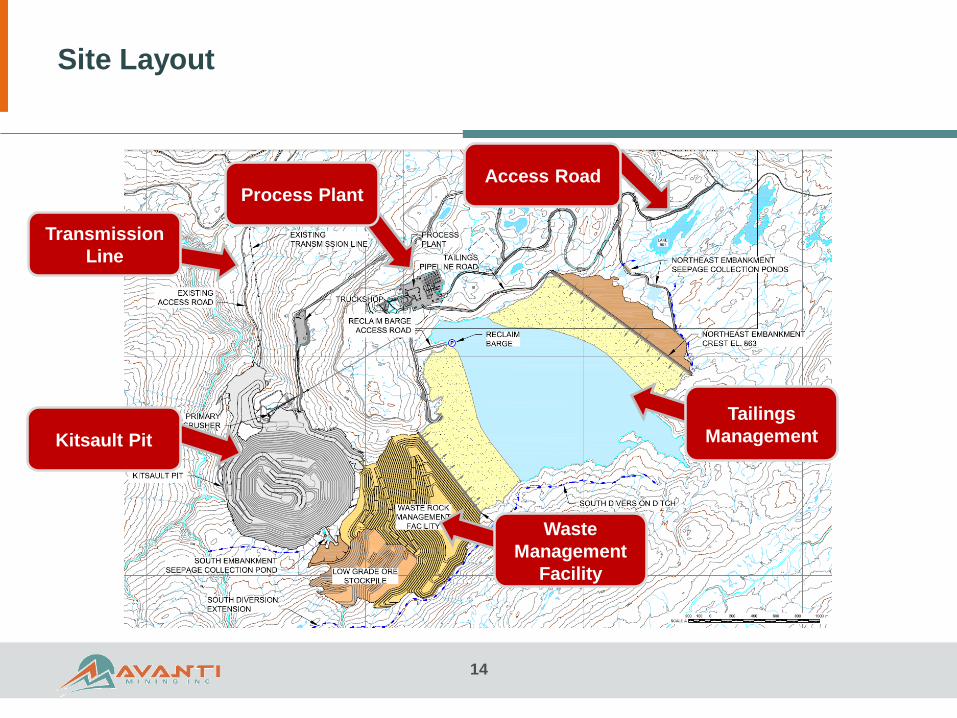

Site Layout

14

Process PlantAccess Road

Transmission

Line

Kitsault Pit

Waste

Management

Facility

Tailings

Management

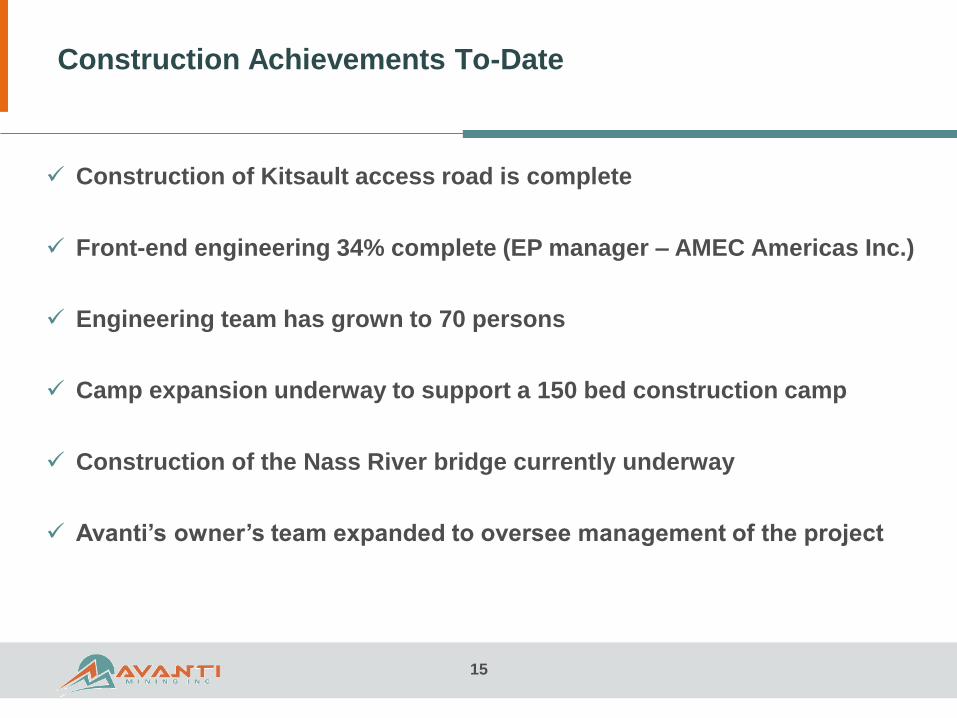

Construction Achievements To-Date

15

Construction of Kitsault access road is complete

Front-end engineering 34% complete (EP manager – AMEC Americas Inc.)

Engineering team has grown to 70 persons

Camp expansion underway to support a 150 bed construction camp

Construction of the Nass River bridge currently underway

Avanti’s owner’s team expanded to oversee management of the project

16

Environmental Management

Independent Review Panel

‒ Comprised of three highly-experienced and knowledgeable geoscientists

‒ Review all aspects of geotechnical engineering and waste management practices:

‒ Selecting optimal tailings dam technology

‒ Reviewing site characteristics (hydrometeorology and seismic characteristics)

‒ Analyzing site investigation results

‒ Developing governance guidelines in accordance with permitting requirements

‒ Establishing policies for effective storm water and wastewater management

17

Description Cost Estimate (C$ mm)Cost Estimate (US$

mm)1

Mining 119.3 110.9

Site preparation and roads 26.8 24.9

Process facilities 230.0 213.9

Tailings management and reclaim 81.3 75.6

Utilities 36.1 33.6

Ancillary buildings and facilities 33.9 31.5

Owner’s costs 32.2 29.9

Indirects 150.3 139.8

Total Directs + Indirect Costs 709.9 660.2

Contingency 108.1 100.5

Total Capital Costs 818.0 760.7

Capital Cost Summary

EPCM: 34%

Construction support: 21%

Freight: 19%

Camp / Catering: 15%

Other: 11%1. CAD figures have been converted to USD based on CAD/USD rate 0.9300

18

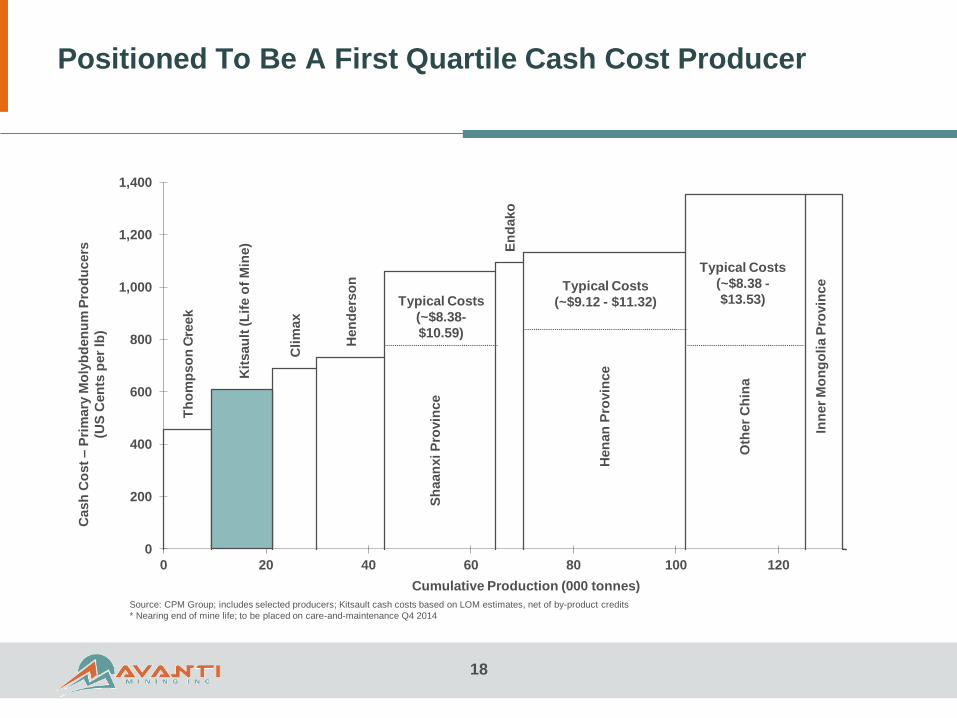

Positioned To Be A First Quartile Cash Cost Producer

Th

om

pso

n C

reek

Kit

sau

lt (

Lif

e o

f M

ine)

Cli

max

Hen

ders

on

Sh

aan

xi P

rovin

ce

En

dako

Hen

an

Pro

vin

ce

Oth

er

Ch

ina

Inn

er

Mo

ng

oli

a P

rovin

ce

0

200

400

600

800

1,000

1,200

1,400

0 20 40 60 80 100 120

Typical Costs

(~$9.12 - $11.32)

Typical Costs

(~$8.38 -

$13.53)Typical Costs

(~$8.38-

$10.59)

Cash

Co

st

–P

rim

ary

Mo

lyb

den

um

Pro

du

cers

(US

Cen

ts p

er

lb)

Cumulative Production (000 tonnes)

*

Source: CPM Group; includes selected producers; Kitsault cash costs based on LOM estimates, net of by-product credits

* Nearing end of mine life; to be placed on care-and-maintenance Q4 2014

19

Established Strategic Partnerships

Offtake agreement for 50% of moly

production

Offtake agreement for up to 20% of moly

production

20

Update on Financing – Project Debt

Lending Syndicate of Six Banks

Lending syndicate in discussions to provide secured debt financing facilities for US$612

million

21

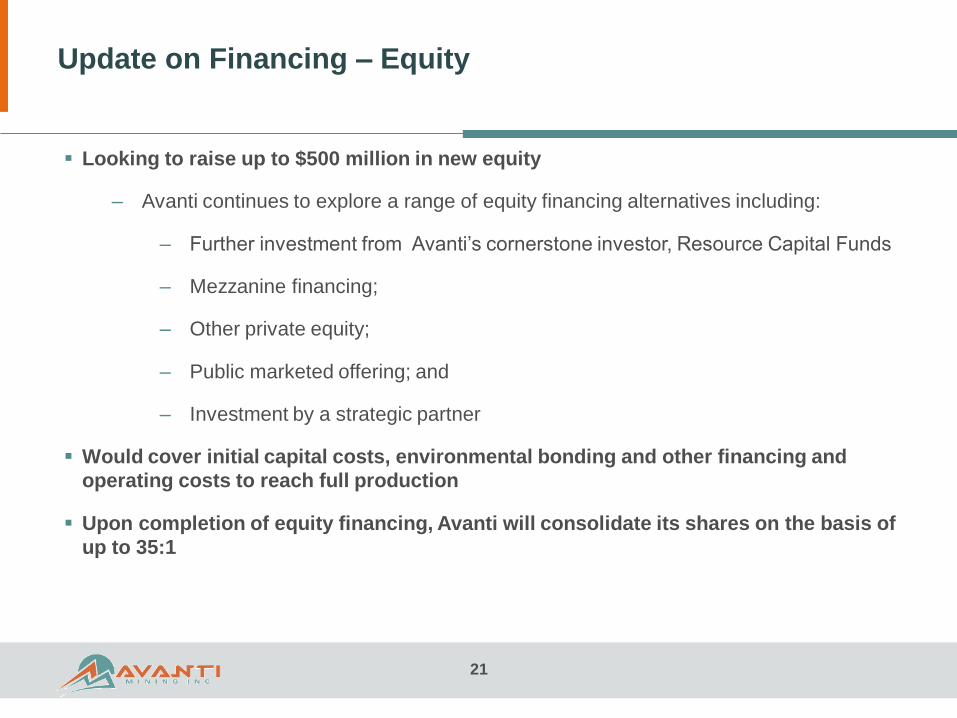

Update on Financing – Equity

Looking to raise up to $500 million in new equity

‒ Avanti continues to explore a range of equity financing alternatives including:

‒ Further investment from Avanti’s cornerstone investor, Resource Capital Funds

‒ Mezzanine financing;

‒ Other private equity;

‒ Public marketed offering; and

‒ Investment by a strategic partner

Would cover initial capital costs, environmental bonding and other financing and

operating costs to reach full production

Upon completion of equity financing, Avanti will consolidate its shares on the basis of

up to 35:1

22

Kitsault NPV

$173

$458 $520

$889

$496

$0

$250

$500

$750

$1,000

US$12.50 US$14.50 US$15.00 US$18.00 US$14.50

Kitsault Optimization Study (April 2014)Analyst

Estimates1

Kit

sa

ult

NP

V (

C$

mm

)

1. Source: Cormark,

Molybdenum Price (per lb)

Positive NPV at a range of prices

23

Molybdenum Market Update

Kitsault

Concentrate trucked to

Vancouver or Prince

Rupert

Stainless and

construction steels

Stainless and

construction steels

Remaining

Concentrate to

Molymet in

Belgium

Concentrate processed at

Molymet’sChilean facilities

(up to 4,500 tonnes annually)

Processed MoO2 to

ThyssenKrupp

Concentrate to

SeAH (4,200

tonnes annually)

O&G Infrastructure Investment Underpins North

American Stainless Steel Demand

24

US$500 billion anticipated be invested in energy infrastructure in North America over the next 7 years

Source: Pipeline & Gas Journal

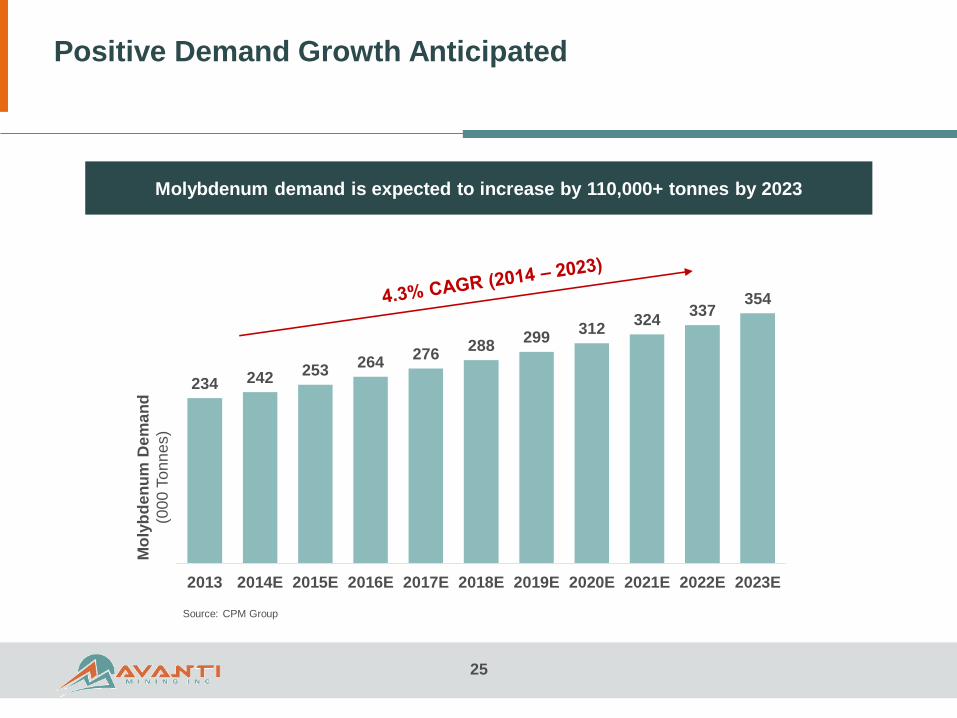

Positive Demand Growth Anticipated

25

234 242253

264276

288299

312324

337354

2013 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

Source: CPM Group

Molybdenum demand is expected to increase by 110,000+ tonnes by 2023

Mo

lyb

de

nu

m D

em

an

d

(00

0 T

on

ne

s)

Kitsault Is Timed to Meet An Expected Supply Deficit

26

Source: CPM Group, Avanti management estimates

0

50

100

150

200

250

300

350

400

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Kitsault Supply

Primary Supply (Ex. Kitsault)

New By-Product Supply

Existing By-Product Supply

World Demand (CPM Group)

Kitsault expected to

contribute ~4% of total

supply

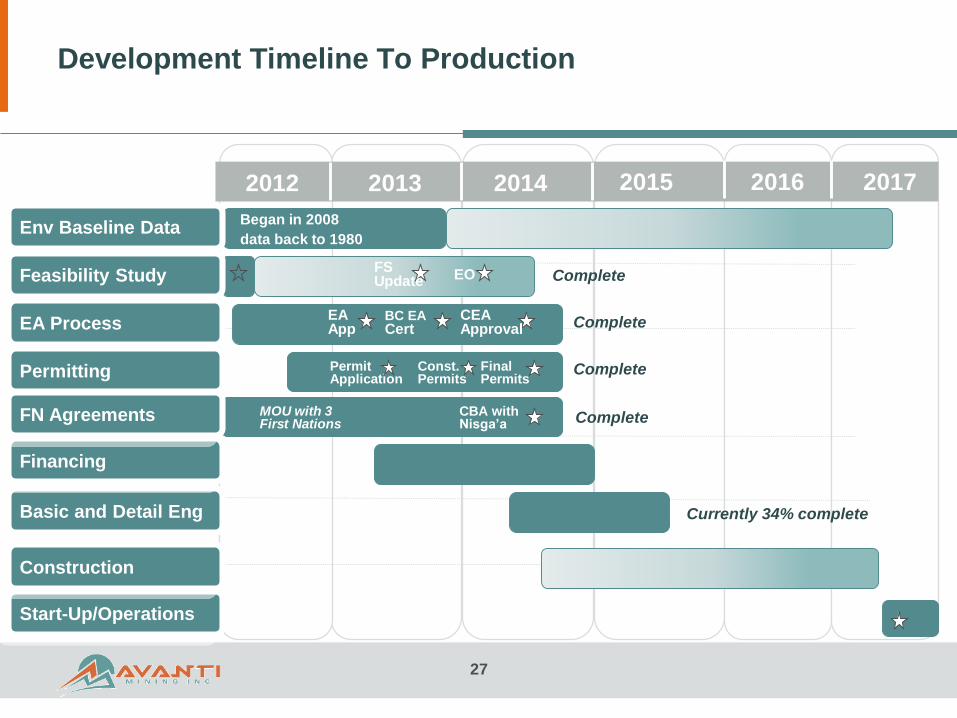

27

2012 2013 2014

Env Baseline DataBegan in 2008

data back to 1980

2015

Const. Permits

Feasibility Study

Start-Up/Operations

Basic and Detail Eng

EA Process

Construction

Permitting

EA App

Permit Application

BC EA Cert

Final Permits

CEA Approval

FS Update EO

2016 2017

Financing

Complete

Complete

Complete

Currently 34% complete

FN Agreements MOU with 3 First Nations

CBA with Nisga’a Complete

Development Timeline To Production

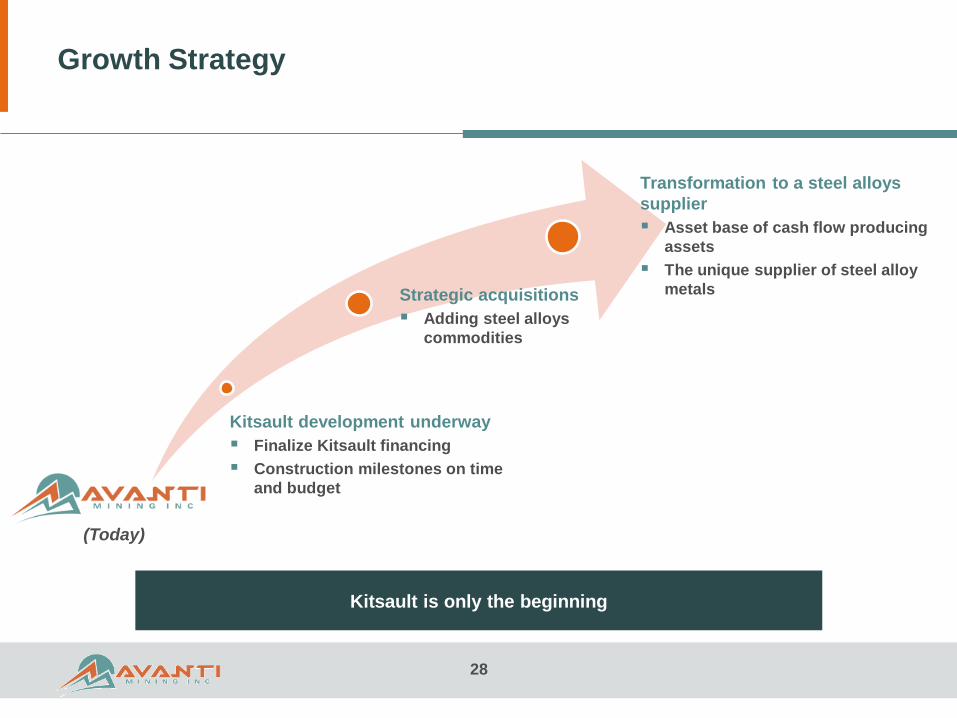

28

Growth Strategy

Kitsault is only the beginning

(Today)

Kitsault development underway

Finalize Kitsault financing

Construction milestones on time

and budget

Transformation to a steel alloys

supplier

Asset base of cash flow producing

assets

The unique supplier of steel alloy

metalsStrategic acquisitions

Adding steel alloys

commodities

29

Corporate Re-branding – Alloycorp Mining Inc.