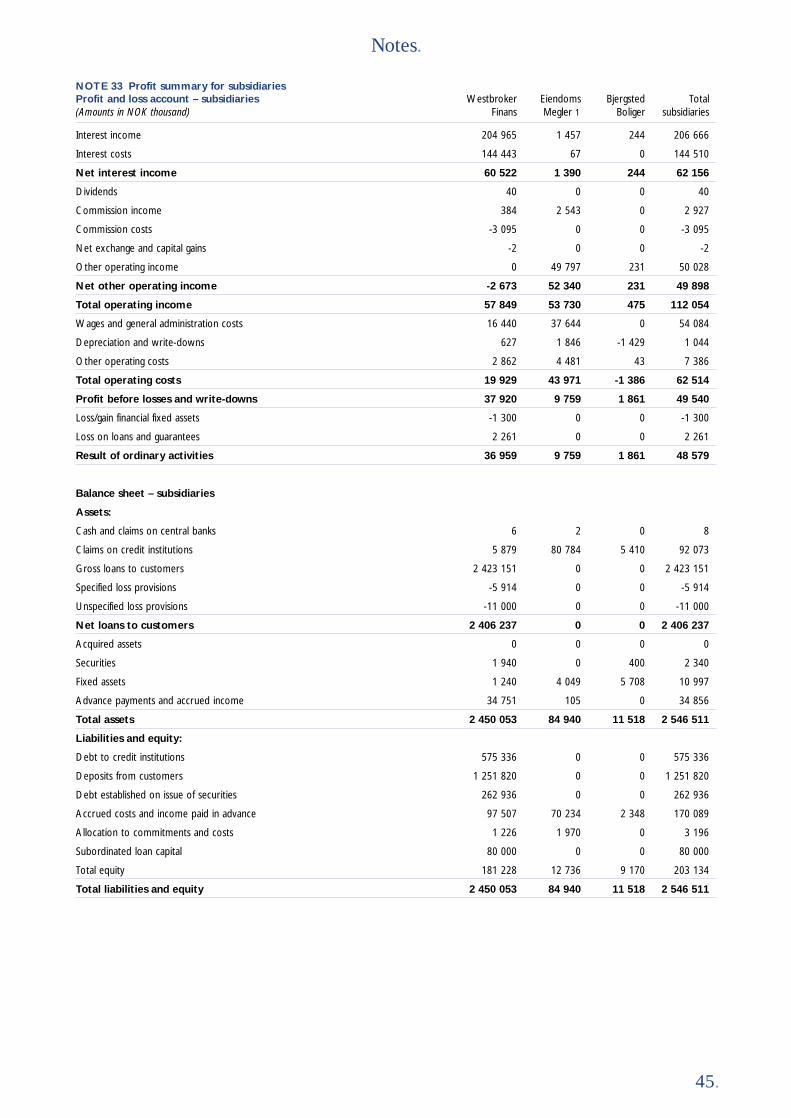

sparebank 1 sr-bank - cisionmb.cision.com/main/2876/9318352/54613.pdf · the sparebank 1 sr-bank...

TRANSCRIPT

Contents.

2.

3.

4.

6.

10.

14.

20.

22.

25.

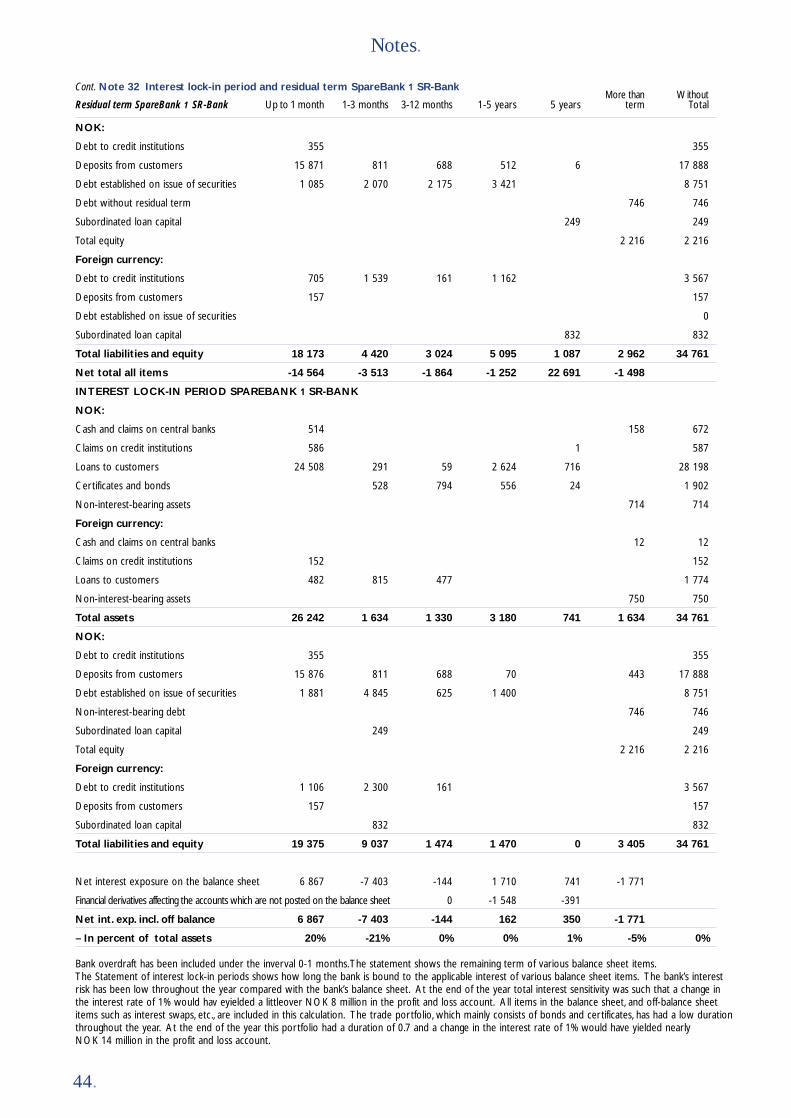

46.

47.

48.

49.

50.

51.

53.

54.

55.

56.

SpareBank 1 SR-Bank

Main and key figures

A bank for everyone

A bank for all generations

A bank for business and industry

Directors Report for 1999

Annual Accounts for 1999

Accounting Principles

Notes

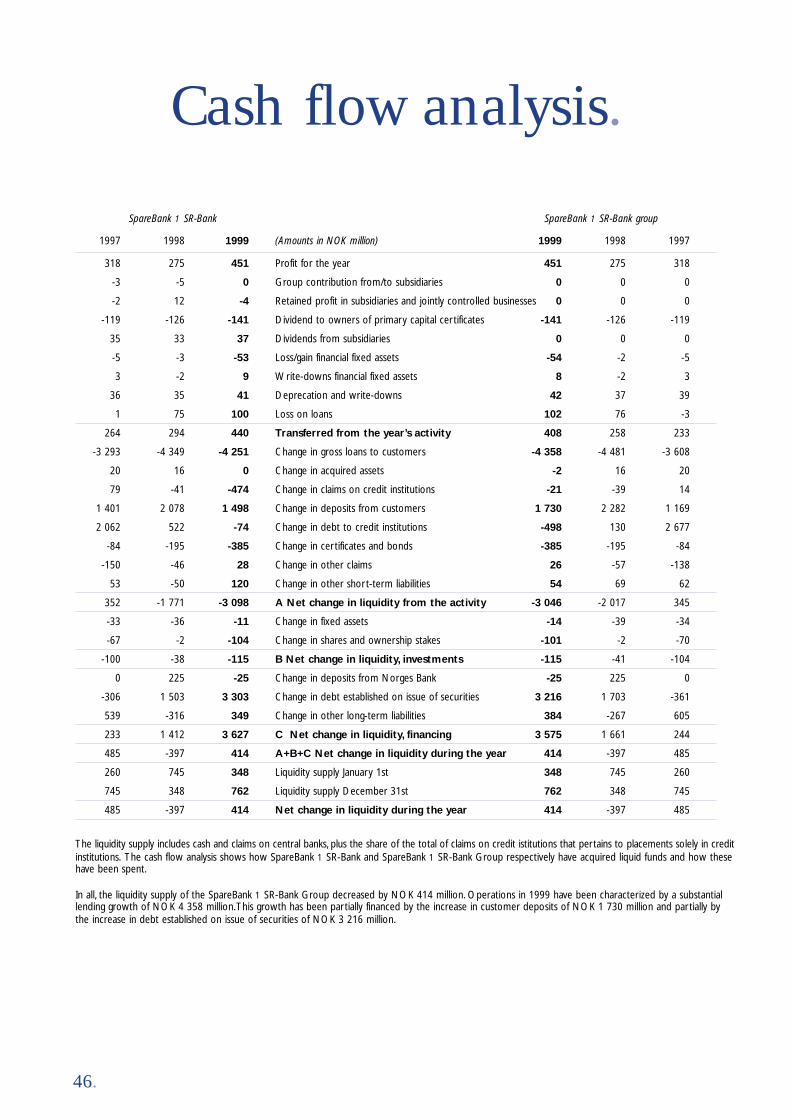

Cash flow analysis

Auditors’ and The Audit Committee’s Report

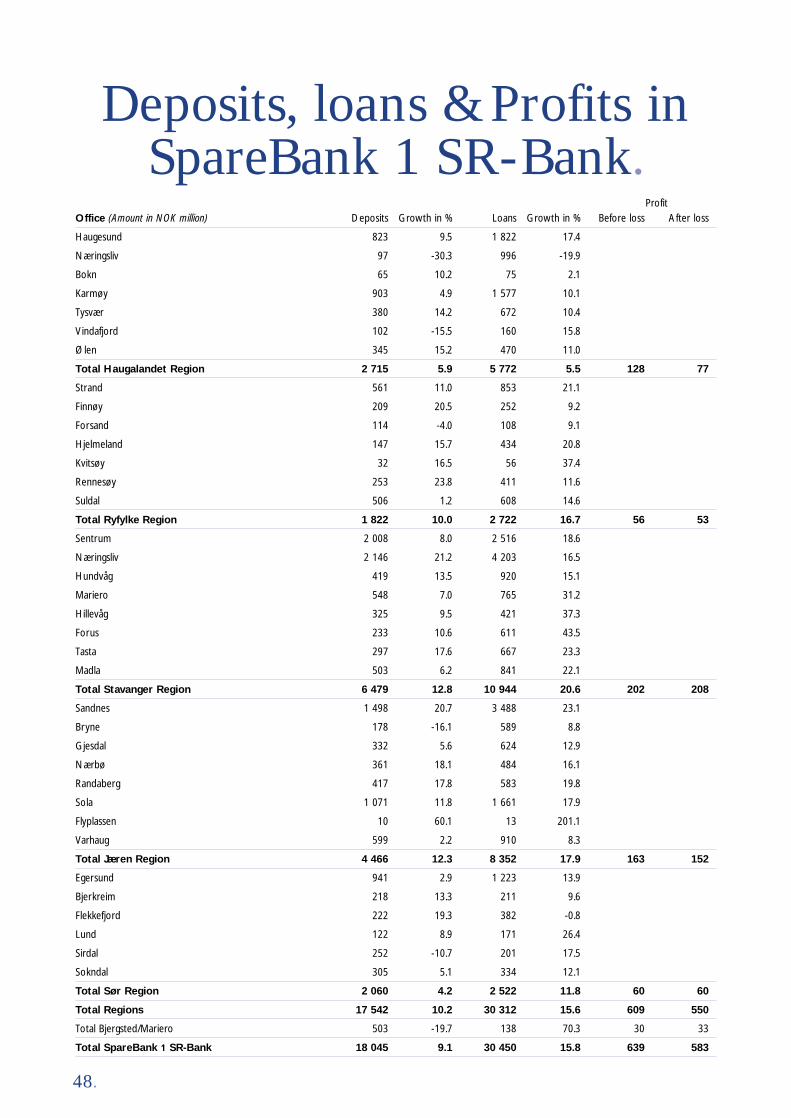

Deposits, Loans and Profits

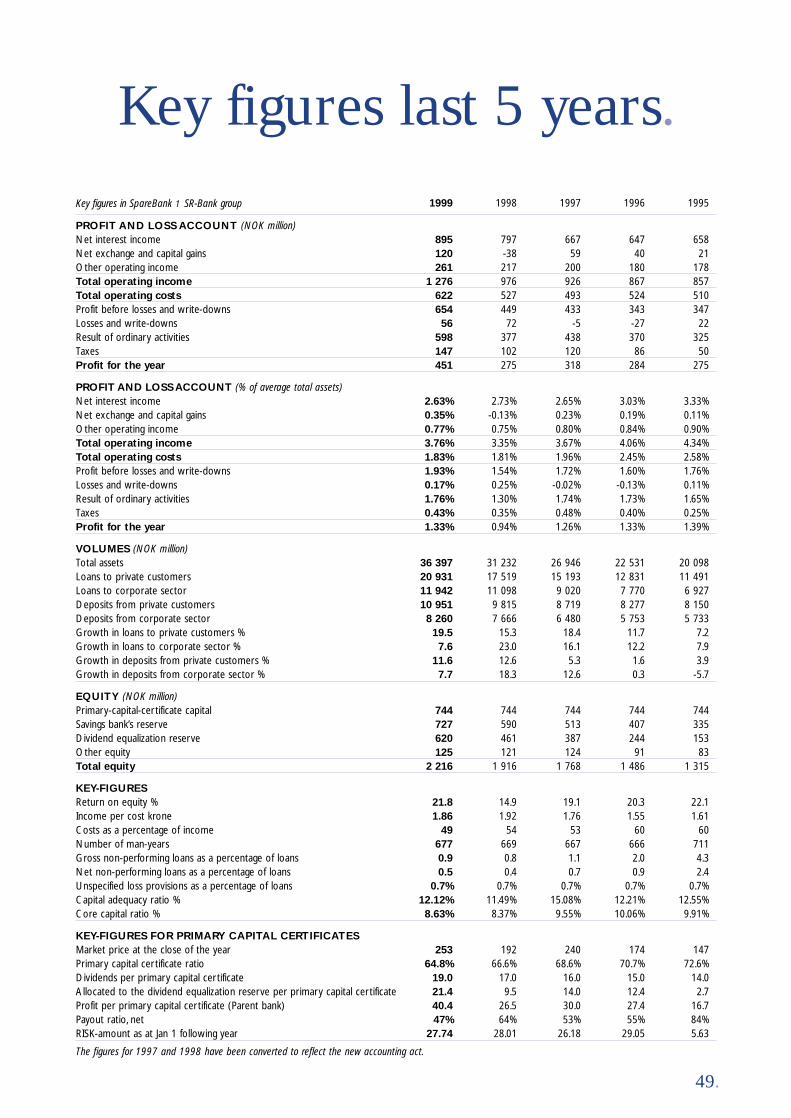

Five-year Overviews in key figures

Five-year Overviews in Graphs

Primary Capital Certificates

Representatives

Organisational Chart

Map of branch offices

Addresses overview

1.

2.

SpareBank 1 SR-Bank is organized into five districts:Haugaland, Ryfylke, Jæren, Egersund and Stavanger. The main office is in Stavanger. We have a total of 665employees and manage a total of NOK 35 billion as of 31 December 1999. SpareBank 1 SR-Bank is the dominant bank in the region and the market leader within the markets for private customers, corporate customers and public administration. We have a total of 173,800 customers, divided among 165,000 privatecustomers and 8,800 corporate customers.

The SpareBank 1 SR-Bank group consists of SpareBank1 SR-Bank and the bank's two subsidiaries – the real estateagency EiendomsMegler 1 Rogaland A/S and the financecompany Westbroker Finans A/S with a total of 82 employees.EiendomsMegler 1 Rogaland A/S has offices in Stavanger,Sandnes, Sola, Bryne, Egersund and Haugesund. In addition,the brokerage firm Garde ASA is an affilicated company.

Our job is to offer all financial services needed byour customers, finance homes and businesses, offer

insurance and payment services, sell real estate, securitiesand be financial advisers.

We play an active role on the local level, for example byfinancing businesses that create new jobs, as well asthrough supporting local associations and organizations.

Our vision: SpareBank 1 SR-Bank shall be regardedby the customer as the recommended and leading bankwithin its market.

Customers: SpareBank 1 SR-Bank shall be viewed bythe customer as the recommended and preferred partner.

Products: SpareBank 1 SR-Bank shall offer competitivefinancial products and services that cover customer needs.

Distribution: SpareBank 1 SR-Bank shall offer itsproducts through modern, easily accessible and local distribution channels, which ensure that the customerreceives good quality and service.

Employees: SpareBank 1 SR-Bank shall secure thebank's position as the recommended and leading bankthrough ensuring that its employees are customer-oriented and qualified.

Community: SpareBank 1 SR-Bank shall actively participate in the effort to strengthen growth anddevelopment within its market.

The bank: SpareBank 1 SR-Bank shall be a profitable and independent bank with local ties, andshall be a regional alternative to the competing financialconglomerates through the SpareBank 1 alliance.

SpareBank 1 was established on 1 November 1996 inorder to ensure a nation-wide and regional alternativeto the large financial conglomerates with headquartersin Oslo. SpareBank 1 is a binding cooperation betweenSpareBank 1 Nord-Norge, SpareBank 1 Midt-Norge,SpareBank 1 Vest, SpareBank 1 SR-Bank andSamarbeidende Sparebanken A/S (16 local savingsbanks in the eastern part of Norway – Samspar).

SpareBank 1's Vision: SpareBank 1 shall satisfy the customers' individual expectations regardingproximity, local ties and cooperation.

SpareBank 1 Gruppen A/S is the holding company in thealliance and owns the product companies SpareBank 1Livsforsikring AS, SpareBank 1 Skadeforsikring A/S,SpareBank 1 Fondsforsikring A/S, SpareBank 1 KredittkortA/S, Odin Forvaltning AS (51%), First Securities AS (54%).EiendomsMegler 1 is also a part of this collaboration.

In August 1998, SpareBank 1 and Sweden's secondlargest bank, FöreningsSparbanken AB, decided toenter into a strategic alliance in order to strengthen the regional/local competitiveness in both countries.As of 31 December 1999, FöreningsSparbanken ABmanage assets totaling SEK 834 billion.

In November 1999, Vår Gruppen ASA and SpareBank 1entered into a proposal for a framework agreementregarding cooperation and integration. This entails thatthe trade unions, represented by the NorwegianFederation of Trade Unions, become a 10 % owner inSpareBank 1 Gruppen A/S. The ownership distribution inSpareBank 1 Gruppen A/S after the transaction will bethat the SpareBank 1 banks own 65%, the NorwegianFederation of Trade Unions owns 10% andFöreningsSparbanken AB owns 25%.

After the merger with VÅR Bank og Forsikring, which iscurrently Norway's fourth largest insurance company andthe country's seventh largest commercial bank, the newSpareBank 1-alliance will be the fourth largest bankingand financing group in Norway with solid geographicalcoverage and nearly NOK 180 billion in total assets. The agreement is contingent upon approval by theauthorities on satisfactory terms.

SpareBank 1 SR-Bank.

«SpareBank 1 SR-Bank isthe region's leading bankwith 54 offices in 26 munici-palities ranging from Ølen inHordaland to Flekkefjord inVest-Agder.The bank consistsof 39 former local savingsbanks and has a historydating back to 1839.»

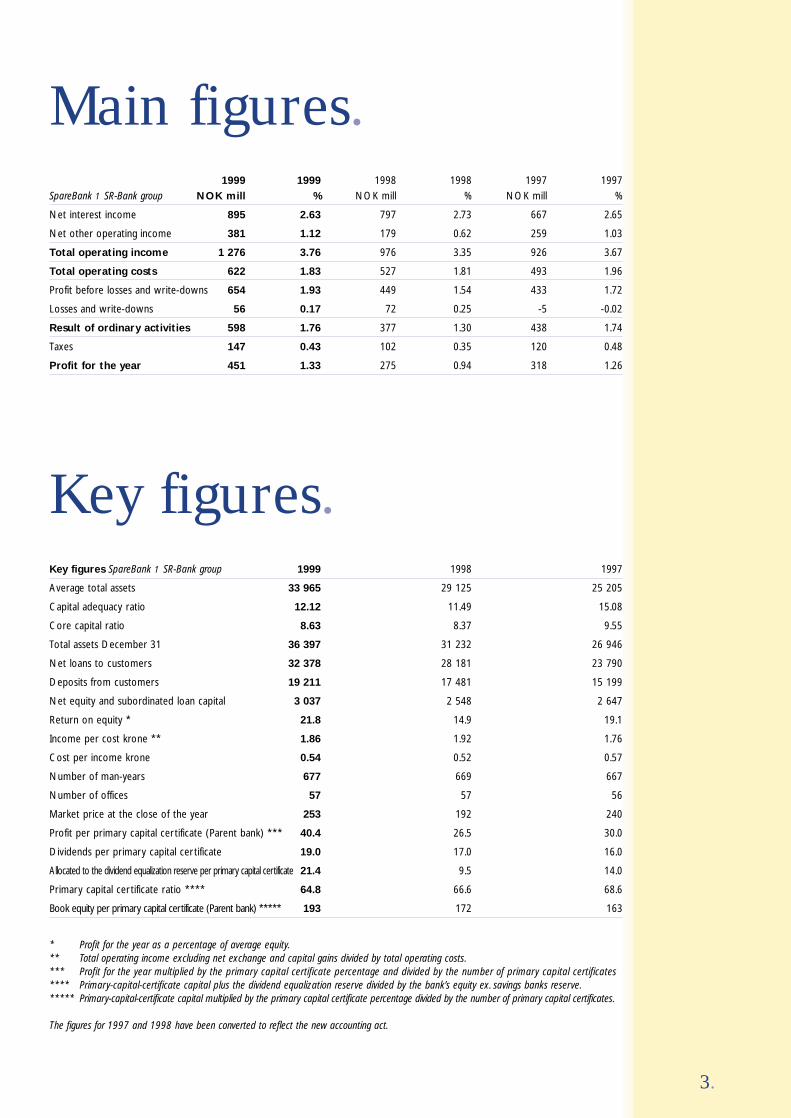

SpareBank 1 SR-Bank group NOK mill % NOK mill % NOK mill %

Net interest income 895 2.63 797 2.73 667 2.65

Net other operating income 381 1.12 179 0.62 259 1.03

Total operating income 1 276 3.76 976 3.35 926 3.67

Total operating costs 622 1.83 527 1.81 493 1.96

Profit before losses and write-downs 654 1.93 449 1.54 433 1.72

Losses and write-downs 56 0.17 72 0.25 -5 -0.02

Result of ordinary activities 598 1.76 377 1.30 438 1.74

Taxes 147 0.43 102 0.35 120 0.48

Profit for the year 451 1.33 275 0.94 318 1.26

Key figures SpareBank 1 SR-Bank group 1999 1998 1997

Average total assets 33 965 29 125 25 205

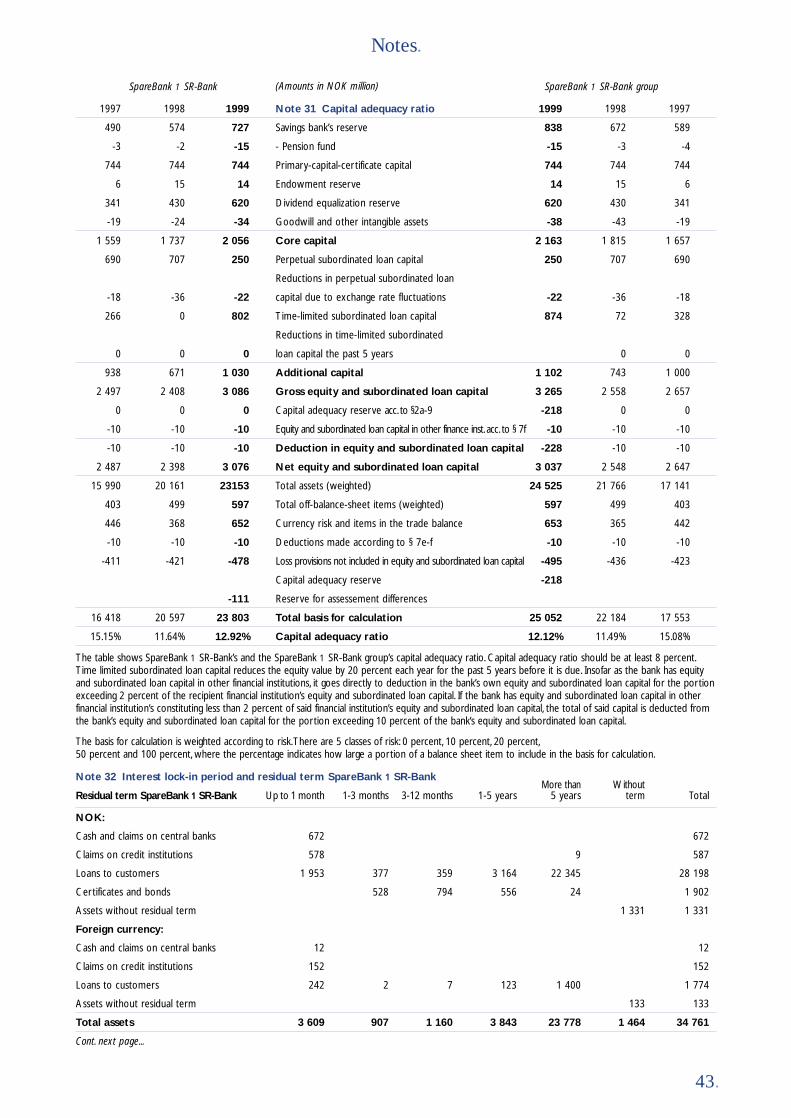

Capital adequacy ratio 12.12 11.49 15.08

Core capital ratio 8.63 8.37 9.55

Total assets December 31 36 397 31 232 26 946

Net loans to customers 32 378 28 181 23 790

Deposits from customers 19 211 17 481 15 199

Net equity and subordinated loan capital 3 037 2 548 2 647

Return on equity * 21.8 14.9 19.1

Income per cost krone ** 1.86 1.92 1.76

Cost per income krone 0.54 0.52 0.57

Number of man-years 677 669 667

Number of offices 57 57 56

Market price at the close of the year 253 192 240

Profit per primary capital certificate (Parent bank) *** 40.4 26.5 30.0

Dividends per primary capital certificate 19.0 17.0 16.0

Allocated to the dividend equalization reserve per primary capital certificate 21.4 9.5 14.0

Primary capital certificate ratio **** 64.8 66.6 68.6

Book equity per primary capital certificate (Parent bank) ***** 193 172 163

3.

Key figures.

Main figures.1999 1999 1998 1998 1997 1997

* Profit for the year as a percentage of average equity.** Total operating income excluding net exchange and capital gains divided by total operating costs.*** Profit for the year multiplied by the primary capital certificate percentage and divided by the number of primary capital certificates**** Primary-capital-certificate capital plus the dividend equalization reserve divided by the bank’s equity ex. savings banks reserve.***** Primary-capital-certificate capital multiplied by the primary capital certificate percentage divided by the number of primary capital certificates.

The figures for 1997 and 1998 have been converted to reflect the new accounting act.

«We will do our utmost toensure that the customersin our region always have a competitive financialpartner with local ties.»

4.

A bank for everyone.

SpareBank 1 SR-Bank consolidated its position in1999 as the bank for everyone in our region. We arehappy to see the good results and progress made inthe quality of the services provided to the customers.We have set an ambitious goal; we want to be therecommended bank for our customers. Thus, we aimhigh. A motivated and competent organization workshard every day to meet the customers' needs. Themarkets are undergoing major changes. New productsare added and the customers' needs change – alsodepending on what phase of life they are goingthrough. Our challenge as a bank is to be able tooffer our customers competitive products and goodcounseling in a world where framework conditionsand the competition change with an enormous speed.

Closeness of a local bankThe technological development entails major changesin how we meet our customers. The Internet bank isin the process of taking over many of the simple andtraditional banking operations. The number of trans-actions via the Internet bank is currently increasing by20 percent per month and will in a short time exceedthe number of transactions on bank premises. Thiswill of course change the workday for many of ouremployees. However, we are not of the opinion that theposition of the local bank is threatened by technolog-ical changes, but the contents of the tasks will bechanged. We believe that future customers will needmore counseling. Good advice is based on trust and thisis where the human factor is essential. Our ambitionis clearly stated; through the closeness of the localbank and its knowledge of the market, we wish to bethe leading financial partner for private and corpo-rate customers. Through good advice and good finan-cial solutions, we will contribute to improved privatefinances and improved profitability for our customers.

Strength of a large-scale bankDevelopment of technology, good products and a strongbrand name is expensive and these are important forcesthat explain concentration and mergers within thefinancial industry. Through the SpareBank 1-allianceand collaboration with FöreningsSparbanken inSweden, we have established Scandinavia's leadingbanking alliance. This is not goal in itself, but ameans of reaching our local goals. We want to takeadvantage of the economies of scale without the dis-advantages associated with large mergers.Through the SpareBank 1 Alliance we are offeredcompetitive products and cost-effective technological

solutions adapted to the future requirements regarding good banking operations.

Financial partner with local tiesOur region enjoys the benefits of a very competitivefinancial services industry with both local, national andinternational players. This is good for the customers.

Through the SpareBank 1-alliance, SpareBank 1 SR-Bank is now a competitive financial partner withlocal ties. We want to combine the closeness of alocal bank with the strength of a large-scale bank. It is essential for us that all decisions concerning thecustomers are based on local ties.

We are of the opinion that a financial alternativebased on our model warrants a role within this competitive picture. We will do our utmost to ensurethat the customers in our region always have a competitive financial partner with local ties.

The bank for everyoneSpareBank 1 SR-Bank is currently the leading bankin the region. We want to strengthen this position,both in relation to private customers and industry andcommerce. Industry and commerce are facing majorchallenges in the years ahead, and many new jobsmust be created through innovations and offsprings.We want to be a good financial partner for businessdevelopment and setting up house in our region.

Through the SpareBank 1 group's acquisition of VårBank og Forsikring, we have a good foundation forstrengthening the position in our region even further.We are significantly stronger in the insurance marketand make contact with large, new customer groupswith a need for good financial products.

We want to become an even better bank and to con-solidate our position as the bank for everyone and weare making good progress. You, the customer, decide.We will always do our best to meet your expectationsin order that you safely can recommend us to yourbest friends and connections.

Stavanger, February 2000

Terje VarebergManaging Director

Ryfylke is a growing region.We wantto be a bank committed to the localcommunity.We have offices in allmunicipalities in Ryfylke. GeneralManager Njål Skår in Årdal is headof an active local bank.

«The airport is hub of action!» Thebranch bank at Stavanger Airport atSola is the «latest addition to thefamily» and has customer-friendlybusiness hours. Foreign currency andcredit-cards can be collected hereprior to travelling abroad.

SpareBank 1 SR-Bank’s group manage-ment and staff have offices in BjergstedTerrasse in Stavanger.The head office is alsoa meeting place for business and industry.

Head picture: The bank’s top man-agement listens to customers. ManagingDirector Terje Vareberg talking with acustomer at the local office at Randaberg.

SpareBank 1 SR-Bank was founded as a result of 22 local savings banks joining forces in 1976, andeven more banks have joined over time. Thirty yearslater, in 1996, the bank joined the SpareBank 1-alliance together with other long-established savingsbanks. The oldest bank is Egersund Sparebank whichcelebrated its 160-year anniversary last year. For generations this bank and the other savingsbanks have safeguarded our customers' money.SpareBank 1 SR-Bank's vision encompasses the corevalues from the local savings banks: «SpareBank 1SR-Bank shall be regarded by the customer as therecommended and leading bank within its market».

This vision focuses on the customers and their needs.The bank is founded on trust, quality, close customerrelations and local ties. Even though the bank haslocal ties, it is also facing the world at large. But themain focus is our customers from Rogaland and wehave now taken care of them for 160 years.Currently, our customers include almost half the population of Rogaland. SpareBank 1 SR-Bank has a strong local presence with 54 offices in 26 munici-palities ranging from Ølen to Flekkefjord. We wish tomaintain a close physical presence and accessibilityin the years to come, while we simultaneously develop a new electronic bank channel. We wish tomake it possible for our customers to chose how theywant to use the bank at any given time – both regarding automated self-service and personal problem-solving and counseling.

We have many different customers and SpareBank 1SR-Bank wants to be «a bank for everyone». Life has manyphases – characterized by different circumstances,

problems and opportunities. Elements include beingyoung, going to school, getting a job, buying a house,having children, becoming grandparents and retiring.Our private finances are affected in many ways as wepass through these phases. As a bank we are requiredto adapt our products to the phases our customersare going through and their everyday finances.

The bank for children and young peopleSmall children need to learn good habits regardingsaving money early on. For many years Sparius wastheir trusted companion. Today their new savingscompanions are called Labb and Line, and currentlythe new savings club has more than 26,000 savings

friends. We have introduced Labb and LineBarneforsikring (Children's Insurance) and

we will introduce Labb and Line mutualfund savings in the future. Mutual

fund savings for children is a newbut very exciting product for

many. It is all about getting a good start in life. Last year,children between elevenand fifteen were offeredmembership in – youguessed it, ElleveFemten-Klubben (the Eleven-FifteenClub). Currently,this club has almost

9,000 members, and it keeps on growing. The prod-uct is adapted to the customers' young age and theprocess of becoming more financially independent.

Students and other young people just starting outhave been very receptive of our «På Egne Ben» (On Your Own) program, which is a unique preferredcustomer program for young adults. More than12,000 customers above 16 years of age signed up for the product in the past year. They have beenassigned their own advisor and receive an offerregarding favorable home-ownership savings contracts.When they need their own home, SpareBank 1 SR-Bankoffers the market's best financing (up to 90 percentof the value of the home) as one of the benefits of På Egne Ben. For many years, the bank has supportedvarious youth activities related to sports, culture andeducation. This has benefited young people and wewill strengthen our efforts on behalf of young people and competence training in the near future through a dedicated endowment fund.

«We value good customersthat have shown us theirtrust by using SpareBank 1SR-Bank as their mainbank. As more and morepeople elect to use elec-tronic bank services,the bank’s operations will be less costly.»

6.

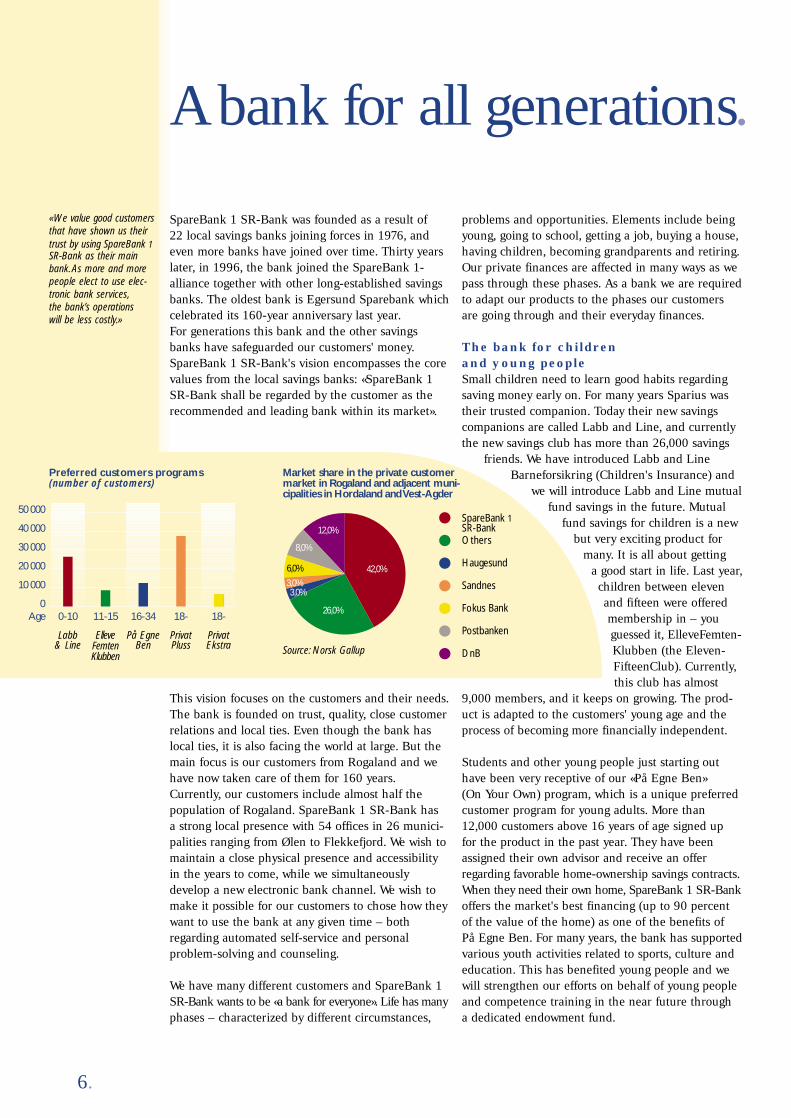

A bank for all generations.

50 000

40 000

30 000

20 000

10 000

00-10 11-15 16-34 18- 18-Age

Labb & Line

ElleveFemtenKlubben

På EgneBen

PrivatPluss

PrivatEkstra Source: Norsk Gallup

Preferred customers programs(number of customers)

Market share in the private customermarket in Rogaland and adjacent muni-cipalities in Hordaland and Vest-Agder

42,0%

26,0%

3,0%3,0%

6,0%

8,0%

12,0%

Sandnes

Haugesund

Others

Postbanken

DnB

SpareBank 1SR-Bank

Fokus Bank

Good savings habits last a lifetime.Children now have Labb and Linepiggy banks.When the piggy banksare emtied the children receiveprices. Labb and Line will release aCD in the year 2000 with fairy talesand music. Saving is fun!

When I am 13 I can have my own membership card in theElleveFemten Klubben (ElevenFifteenClub).When I am 16 I can join the«På Egne Ben» (On Your Own) program.

SR-Nettbank now has more than20,000 users. It is practical to sit athome and have an overview of yourown accounts.The bank’s job is to bean adviser, not a giro handler.

Head picture: The bank council inHaugesund handed out reflector badgesto six-year olds when school started.

Children now have a Labb and Linetrain. SpareBank 1 SR-Bank made anagreement with the local bus service.Children all over the county havesomething to look forward to.

«På Egne Ben» (On Your Own) is tailoredto young people starting out. Young people from the age of 16 can becomemembers.After having been a memberand saved under the BSU scheme, Spare-Bank 1 SR-Bank can offer the banks´smost favorable housing loan.Your ownpersonal advisor is part of the bargain.

Head picture: Our oldest customersneed a good bank. A bank that alsooffers social events and activities.«Den Gyldne Spaserstokk» (GoldenWalking Stick) is a popular initiativefor senior citizens.

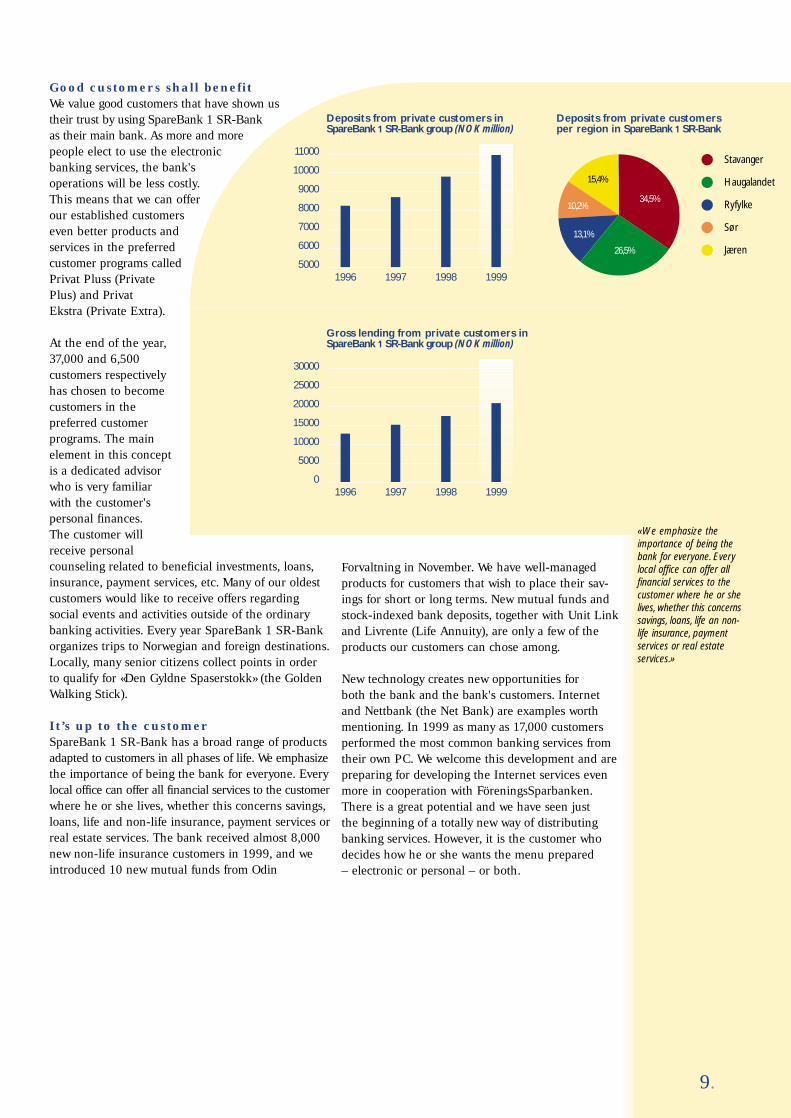

Good customers shall benefitWe value good customers that have shown ustheir trust by using SpareBank 1 SR-Bankas their main bank. As more and morepeople elect to use the electronicbanking services, the bank'soperations will be less costly.This means that we can offerour established customerseven better products andservices in the preferredcustomer programs calledPrivat Pluss (PrivatePlus) and Privat Ekstra (Private Extra).

At the end of the year,37,000 and 6,500 customers respectivelyhas chosen to becomecustomers in the preferred customer programs. The main element in this conceptis a dedicated advisorwho is very familiar with the customer's personal finances. The customer willreceive personal counseling related to beneficial investments, loans,insurance, payment services, etc. Many of our oldestcustomers would like to receive offers regardingsocial events and activities outside of the ordinarybanking activities. Every year SpareBank 1 SR-Bankorganizes trips to Norwegian and foreign destinations.Locally, many senior citizens collect points in orderto qualify for «Den Gyldne Spaserstokk» (the GoldenWalking Stick).

It’s up to the customerSpareBank 1 SR-Bank has a broad range of productsadapted to customers in all phases of life. We emphasizethe importance of being the bank for everyone. Everylocal office can offer all financial services to the customerwhere he or she lives, whether this concerns savings,loans, life and non-life insurance, payment services orreal estate services. The bank received almost 8,000new non-life insurance customers in 1999, and weintroduced 10 new mutual funds from Odin

Forvaltning in November. We have well-managedproducts for customers that wish to place their sav-ings for short or long terms. New mutual funds andstock-indexed bank deposits, together with Unit Linkand Livrente (Life Annuity), are only a few of theproducts our customers can chose among.

New technology creates new opportunities for both the bank and the bank's customers. Internetand Nettbank (the Net Bank) are examples worthmentioning. In 1999 as many as 17,000 customersperformed the most common banking services fromtheir own PC. We welcome this development and arepreparing for developing the Internet services evenmore in cooperation with FöreningsSparbanken.There is a great potential and we have seen just the beginning of a totally new way of distributingbanking services. However, it is the customer whodecides how he or she wants the menu prepared – electronic or personal – or both.

9.

11000

10000

9000

8000

7000

6000

50001996 1998 1999

Deposits from private customers inSpareBank 1 SR-Bank group (NOK million)

1997

30000

25000

20000

15000

10000

5000

01997 1998 1999

Gross lending from private customers inSpareBank 1 SR-Bank group (NOK million)

1996

Deposits from private customers per region in SpareBank 1 SR-Bank

34,5%

26,5%

13,1%

10,2%

15,4%

Sør

Ryfylke

Haugalandet

Stavanger

Jæren

«We emphasize theimportance of being thebank for everyone. Everylocal office can offer allfinancial services to thecustomer where he or shelives, whether this concernssavings, loans, life an non-life insurance, paymentservices or real estateservices.»

When local industry and commerce do well,SpareBank 1 SR-Bank does well. That is the way it is when we do business in the same market and aremutually dependent on each other. We have a stronginvolvement in local industry and commerce and arevery interested in making a contribution to the futuredevelopment. As part of the local industry and com-merce, we have a close relationship with the busi-nesses. We know the companies and their line ofbusiness from the inside and are able to make quickdecisions when needed. Our corporate customershave taught us that accessibility is the most impor-tant product a bank can supply. This is something we intend to maintain and strengthen in the future.

In 1999 we performed a market position survey incooperation with Norsk Gallup in order to acquireknowledge about the bank's position in relation to itscompetitors with a focus on market share, preferenceshare and product potential in the corporate market.As many as 1200 interviews were conducted withrandomly selected companies within our market area. The following main conclusions emerged:

• Knowledge about SpareBank 1 SR-Bank as a corporate bank has increased significantly and the development has been especially positiveamong large businesses.

• The bank has strengthened its position in relationto its competitors. The profile is increasing and itshould be possible to convert it into an increasedmarket share.

• The bank's market share is 39% measured in relation to the number of businesses within themarket area.

Building networksOur position within local industry and commerce isthe basis for a unique network. As a large and localbusiness bank, we probably represent the largestbusiness network in the district. It gives us theopportunity to create a forum for companies that willbenefit from talking together. We regularly initiatecontact between customers and organize variousgatherings and professional seminars. Our hope is tocontribute to general competency training and toestablish relations that will hopefully create newbusiness opportunities.

In this connection, we would mention our breakfastmeetings which are held about 6-8 times a year.

Several well-known local and national speakershave participated at the meetings. Several

seminars have been held as part of the business sector alliance in

SpareBank 1.

In addition to building net-works among companies and increasing expertise,the events also profileSpareBank 1 SR-Bank as a business bank andstrengthen the relation-ship between the bankand its customers. In

our industry it does not take long before a successfulproduct has been copied by several competitors.Lasting success is dependent upon continuous development of people and human relationships.

Loans and financingWe have a wide range of products and services toensure correct financing for companies. Combinedwith our extensive expertise within various industries,this makes us a strong partner. By customizing ourproducts, we can solve the financing challenges facing industry and commerce, and we are happy to contribute input on how a company can reducecosts by efficient use of financing products.

Investment and asset managementThe interest in alternatives to the traditional place-ment of money in the bank has shown a strongincrease in recent years. The range of managementproducts has expanded significantly with many newsecurities products and capital instruments.

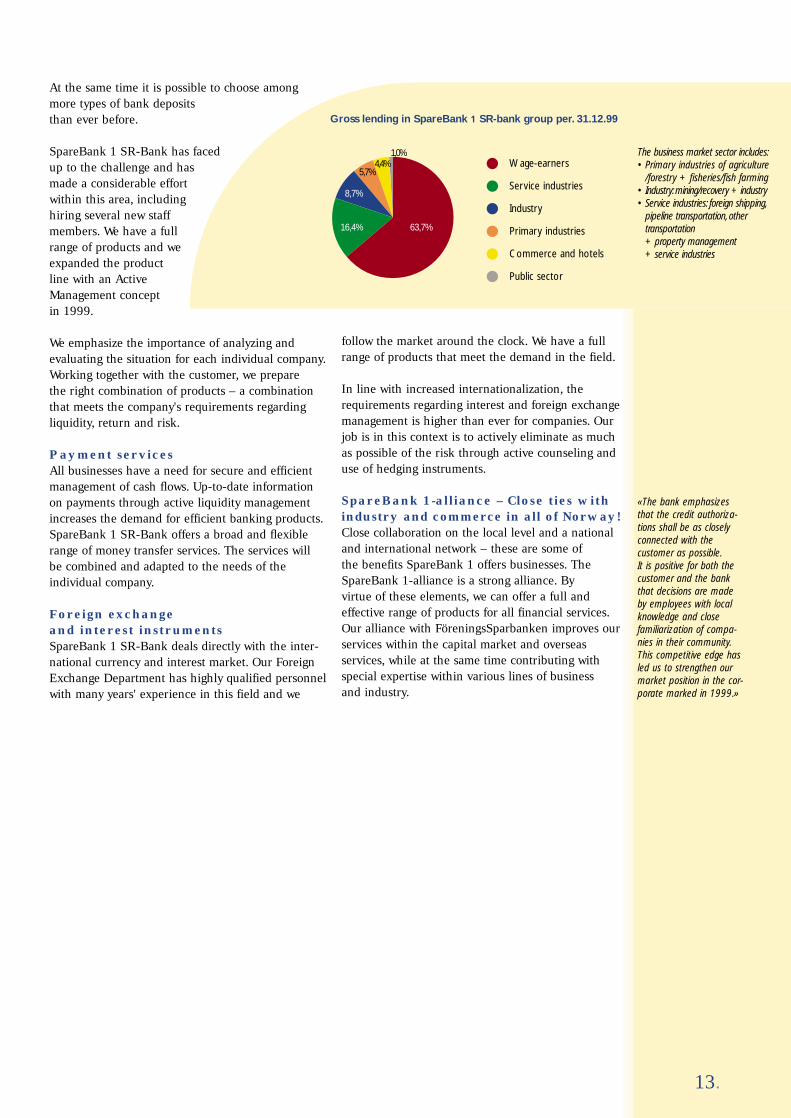

«In 1999 SpareBank 1SR-Bank group had agrowth in lending to business and industry of7.6%. Growth in depositsfor the same year was7.7%. Loans to businessand industry account forabout 36.3% of the bank’stotal loans.»

10.

A bank for business and industry.

15000

12500

10000

7500

5000

2500

01996 1998 1999

Gross lending corporate market inSpareBank 1 SR-Bank group (NOK million)

1997

10000

9000

8000

7000

6000

5000

40001997 1998 1999

Deposits corporate market inSpareBank 1 SR-Bank group (NOK million)

1996

Our coast still provides fertile conditionsfor rich and diverse business and industry.The entire value chain from raw materialto finished product is an interesting commitment area for the bank.

Head picture: Our foreign exchange de-partment is the only one in Rogaland thattrades directly in the international market.

Brødrene Risa A/S is one of the largestcontractors in Rogaland and acquiredAS Betong in 1999.The Brødrene Risagroup is involved in large and smalldevelopments, cultivation, road con-struction, concrete production, pilingand construction of buildings.Thegroup’s headquarters are in Nærbø.

The IT company Lan-x AS in Sandnesstarted operations in September 1998. Itsobjects are to conduct sales of goods andservices within information technology.Thecompany currently has 17 employees andsales of nearly NOK 43 million. Lan-x aimsat being the preferred professional bodywithin structured data processing. Its custo-mers consist of more than 200 companies.

In 1999 SpareBank 1 SR-Bank intro-duced a new concept for measuringand managing strategy and operati-ons: Balanced Scorecard.The processand system are among the leadingand most efficient in Norway today.

SpareBank 1 SR-Bank is committedto investment and active manage-ment. Christoffer Hovda is a goodrepresentative of our expertise in this area.

BedriftsNett simplifies banking services for our corporate customers. It is a verypractical solution for efficient paymenttransmission services.

Head picture: Hydro Seafood Rogaland AS is the largest player in fish farming in Rogaland and among the 10 largest in Norway.

At the same time it is possible to choose amongmore types of bank deposits than ever before.

SpareBank 1 SR-Bank has facedup to the challenge and hasmade a considerable effortwithin this area, includinghiring several new staffmembers. We have a fullrange of products and weexpanded the productline with an ActiveManagement concept in 1999.

We emphasize the importance of analyzing and evaluating the situation for each individual company.Working together with the customer, we prepare the right combination of products – a combinationthat meets the company's requirements regarding liquidity, return and risk.

Payment servicesAll businesses have a need for secure and efficientmanagement of cash flows. Up-to-date informationon payments through active liquidity managementincreases the demand for efficient banking products. SpareBank 1 SR-Bank offers a broad and flexiblerange of money transfer services. The services will be combined and adapted to the needs of the individual company.

Foreign exchange and interest instrumentsSpareBank 1 SR-Bank deals directly with the inter-national currency and interest market. Our ForeignExchange Department has highly qualified personnelwith many years' experience in this field and we

follow the market around the clock. We have a full range of products that meet the demand in the field.

In line with increased internationalization, therequirements regarding interest and foreign exchangemanagement is higher than ever for companies. Ourjob is in this context is to actively eliminate as muchas possible of the risk through active counseling anduse of hedging instruments.

SpareBank 1-alliance – Close ties withindustry and commerce in all of Norway!Close collaboration on the local level and a nationaland international network – these are some of the benefits SpareBank 1 offers businesses. TheSpareBank 1-alliance is a strong alliance. By virtue of these elements, we can offer a full andeffective range of products for all financial services.Our alliance with FöreningsSparbanken improves ourservices within the capital market and overseas services, while at the same time contributing withspecial expertise within various lines of business and industry.

13.

Gross lending in SpareBank 1 SR-bank group per. 31.12.99

63,7%16,4%

8,7%

5,7%4,4%

1,0%

Primary industries

Industry

Service industries

Public sector

Wage-earners

Commerce and hotels

The business market sector includes:• Primary industries of agriculture

/forestry + fisheries/fish farming• Industry:mining/recovery + industry• Service industries: foreign shipping,

pipeline transportation, othertransportation+ property management+ service industries

«The bank emphasizesthat the credit authoriza-tions shall be as closelyconnected with the customer as possible.It is positive for both thecustomer and the bankthat decisions are madeby employees with localknowledge and closefamiliarization of compa-nies in their community.This competitive edge hasled us to strengthen ourmarket position in the cor-porate marked in 1999.»

Earnings and growth The SpareBank 1 SR-Bank group's profit before lossand write-downs was NOK 654 million, which is NOK205 million more than last year's profit of NOK 449million. Net losses of NOK 62 million and unspecifiedloss allocations in the amount of NOK 40 million,together with gains from capital assets worth NOK 46million, resulted in a group profit before tax of NOK598 million. Tax costs are estimated at NOK 147 million, which gives a profit for the year of NOK 451million. Total assets increased in 1999 by 17% to NOK

36.4 billion. At the end of the year, the group's equityand subordinated loan capital was NOK 3,037 millionand the capital adequacy ratio 12.12%.

1999 turned into a good year for SpareBank 1 SR-Bank. The profit from the ordinary banking operationindicates an efficient bank as regards sales and opera-tions. Combined with stock market gains and goodmanagement of the bank's securities, this produced anunprecedented profit for SpareBank 1 SR-Bank. Theresult also reflects an organization with products, servicesand customer relations adapted to the market for private

700

600

500

400

300

200

100

0

Operating profit before losses and write-downs

«1999 turned into a good year for SpareBank 1SR-Bank.The profit fromthe ordinary banking oper-ation indicates an efficientbank as regards sales andoperations. Combined withstock market gains andgood management of the bank's securities, thisproduced an unprecedentedprofit for SpareBank 1SR-Bank.»

Operating profit after losses and write-downs

1995 1996 1997 1998 1999

Operating profit in the SpareBank 1 SR-Bank group

Equity and subordinated loans in the SpareBank 1 SR-Bank group

800

750

700

650

600

550

500

450

SpareBank 1 SR-BankSubsidiaries

1995 1996 1997 1998 1999

Man-years in SpareBank 1 SR-Bank and subsidiaries for the last five years

3500

3000

2500

2000

1500

1000

500

0

EquitySubordinated Loan Capital

1995 1996 1997 1998 1999

14.

Directors Report for 1999.

Well run banking operation produce unprecedented earnings

• Operating profit of NOK 598 million before tax

• SpareBank 1 SR-Bank is the district's savings bank

• 12% and NOK 1,100 million in increased private deposits

• NOK 410 million in sales of securities products

• 15% increase in lending

• NOK 120 million in capital gains

• Cost percentage of 1.83

• 21.8% return on equity capital after tax

• NOK 40.40 in profit on primary capital certificates

• The Board proposes to pay NOK 19 in dividends

Strong alliance strengthens distribution and product development

• Acquisition of 51% of First Securities

• Acquisition of Vår Bank og Forsikring

• EiendomsMegler 1 becomes nationwide chain

and corporate customers. A 15% growth in lendingresulted in increased market shares in a region with acontinued high level of activity and the 10% growth indeposits and new growth in alternative forms of savingsindicate customers that have solid finances. Total operating income (excluding gains from securities) in-creased by 20% and cost-effectiveness was maintainedat the same level. Gross default remains stable. Dueto the improved balance, the group has increased theunspecified loss allocations by NOK 40 million. Marketsurveys confirm the bank's strong position as the leading bank in the region.

Norwegian economy and framework conditionsThe Norwegian economy experienced slower growthin 1999 as expected. The growth for the grossdomestic product was reduced to less than 1% in1999 as compared with the long-lasting averageannual growth for the Norwegian mainland of morethan 3%. However, the temperature in parts of theeconomy was still high and the likelihood of a signifi-cant downturn has been reduced. The growth in pub-lic and private consumption will ensure that labormarket demand in respect of the service industry andthe public sector will remain high. A turnaround inthe Norwegian economy will probably be limited toindustry due to lower profitability and weakenedcompetitiveness, but will also be due to permanentlyreduced investments in the petroleum sector. Thiswill entail a significant restructuring of the shipbuild-ing industry and parts of the engineering industry.The consequences for the affected companies willdepend on their ability to restructure their activities.

The development in Rogaland At the beginning of 1999, the businesses in Rogalandwere characterized by a high level of activity, but clearlyexpecting a change in climate. This was related to anexpected unfavorable development within the engineeringand agriculture industry and for production of ships and oilplatforms, all of which are very important for the county.Even though employment was satisfactory in 1999, theactivity level at the beginning of 2000 is significantly lower.

Few new orders are being placed, the oil companiesare adapting to new framework conditions

and industry is being restructured bymergers of national and inter-

national companies. The effectsare first seen as lower

employment levels and a reorganization of the

labor market. The oil industry hasannounced start-upof new developmentprojects, but theeffects of these willnot be noticeable

in the short term. The investment level will never-theless be considerable lower than the peak years in1998 and 1999.

With a leveling off of the petroleum investments in2001, positive effects on household consumption dueto lower interest rates, somewhat stronger export and acontinued moderate growth in public consumption andemployment, the growth in the Norwegian economycan again reach normal levels in 2001. Even thoughRogaland probably at first will not benefit as muchfrom the more positive outlook as the rest of the country, the fall in employment can be softened andthe increase in unemployment reduced.

Continuous positive development in the ninetieshas provided businesses and private households withsolid finances that can handle a short-term downturn.

Group developmentThe SpareBank 1 SR-Bank group's performance hasbeen characterized by a very high level of activity in1999. The group continued its emphasis on the need toadapt to the market's demand for products and servicesdelivered quickly and effectively in close cooperationwith the customers. Advantageous programs for full-service customers, new savings plans and, not least, thefocus on young people and customers starting out havebeen well received. Our home financing plans haveimproved and closeness through personal customer follow-up has been prioritized. The challenge in thecorporate market has been to strengthen the relation-ship with the traditional customer in the market forsmall and medium-sized businesses, while simultane-ously offering a wider range of counseling services and products to the larger businesses. Alliance withinthe Norwegian and Scandinavian alliance results inincreased power and expertise, which can be offered tocurrent and new groups of customers. This entails par-ticipation in projects requiring high levels of expertiseand substantial capital supply, as well as products in linewith the broad range of Norwegian industry and com-merce. Through the Norwegian and Scandinavianalliance, the SpareBank 1 group has the capacity toparticipate in the restructuring taking place in industriessuch as the power industry and the aquaculture industry.

In 1999 the group initiated an extensive projectwhich will reassess and adjust the most important busi-ness processes. This is done in order to increase the effi-ciency and strengthen the level of expertise and thus thegroup's competitiveness. This work is supported by newtechnology developed in cooperation with the alliance. Over the next two years, the alliance will focus on busi-ness processes that make use of common technology.

Market surveys in 1999 confirm that SpareBank 1 SR-Bank is on the right track and is increasing its marketshares. The same surveys also show that the group mustdevelop even further in order to satisfy increasinglyhigher expectations from the customers regarding activecooperation in order to support private households andthe region's industrial and commercial development.

«Alliance within the Nor-wegian and Scandinavianalliance results in increasedpower and expertise, whichcan be offered to currentand new groups of custo-mers.»

15.

«In 1999 the group initiated an extensive project which will reassessand adjust the most im-portant work procedures.This is done in order toincrease the efficiency andstrengthen the level ofexpertise and thus thegroup's competitiveness.»

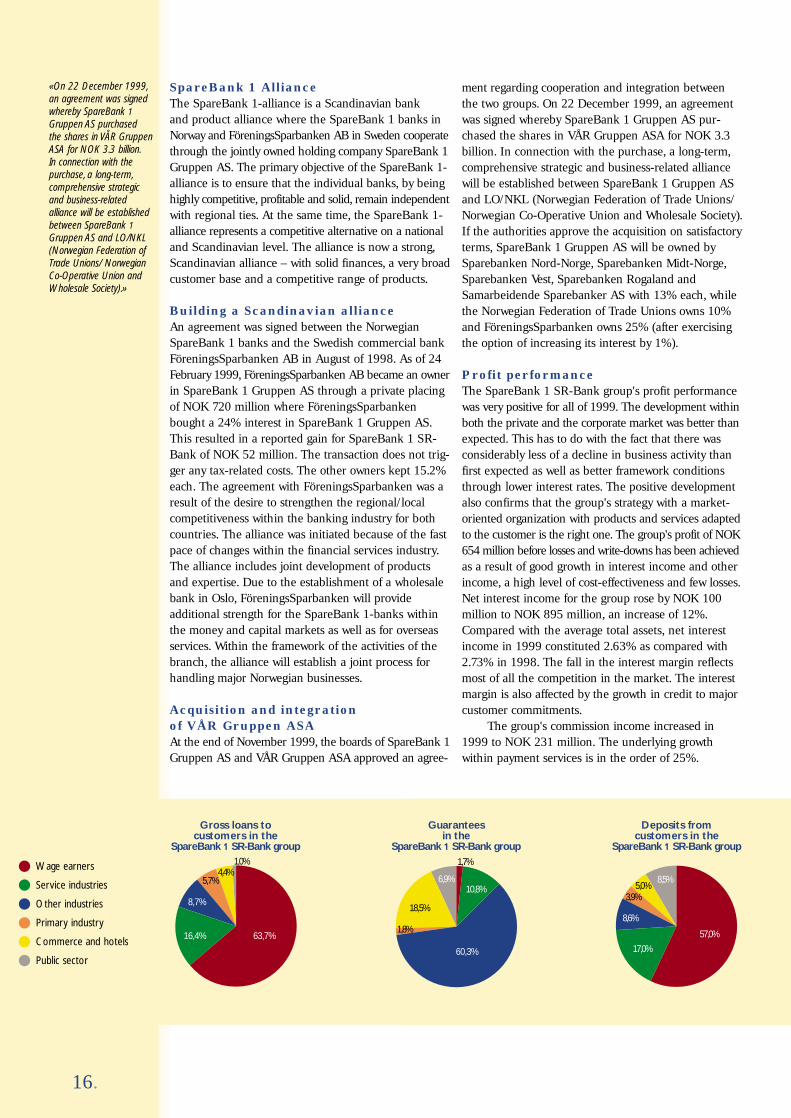

SpareBank 1 Alliance The SpareBank 1-alliance is a Scandinavian bank and product alliance where the SpareBank 1 banks inNorway and FöreningsSparbanken AB in Sweden cooperatethrough the jointly owned holding company SpareBank 1Gruppen AS. The primary objective of the SpareBank 1-alliance is to ensure that the individual banks, by beinghighly competitive, profitable and solid, remain independentwith regional ties. At the same time, the SpareBank 1-alliance represents a competitive alternative on a nationaland Scandinavian level. The alliance is now a strong,Scandinavian alliance – with solid finances, a very broadcustomer base and a competitive range of products.

Building a Scandinavian alliance An agreement was signed between the NorwegianSpareBank 1 banks and the Swedish commercial bankFöreningsSparbanken AB in August of 1998. As of 24February 1999, FöreningsSparbanken AB became an ownerin SpareBank 1 Gruppen AS through a private placingof NOK 720 million where FöreningsSparbankenbought a 24% interest in SpareBank 1 Gruppen AS.This resulted in a reported gain for SpareBank 1 SR-Bank of NOK 52 million. The transaction does not trig-ger any tax-related costs. The other owners kept 15.2%each. The agreement with FöreningsSparbanken was aresult of the desire to strengthen the regional/localcompetitiveness within the banking industry for bothcountries. The alliance was initiated because of the fastpace of changes within the financial services industry.The alliance includes joint development of productsand expertise. Due to the establishment of a wholesalebank in Oslo, FöreningsSparbanken will provide additional strength for the SpareBank 1-banks withinthe money and capital markets as well as for overseasservices. Within the framework of the activities of thebranch, the alliance will establish a joint process forhandling major Norwegian businesses.

Acquisition and integration of VÅR Gruppen ASA At the end of November 1999, the boards of SpareBank 1Gruppen AS and VÅR Gruppen ASA approved an agree-

ment regarding cooperation and integration betweenthe two groups. On 22 December 1999, an agreementwas signed whereby SpareBank 1 Gruppen AS pur-chased the shares in VÅR Gruppen ASA for NOK 3.3billion. In connection with the purchase, a long-term,comprehensive strategic and business-related alliancewill be established between SpareBank 1 Gruppen ASand LO/NKL (Norwegian Federation of Trade Unions/Norwegian Co-Operative Union and Wholesale Society).If the authorities approve the acquisition on satisfactoryterms, SpareBank 1 Gruppen AS will be owned bySparebanken Nord-Norge, Sparebanken Midt-Norge,Sparebanken Vest, Sparebanken Rogaland andSamarbeidende Sparebanker AS with 13% each, whilethe Norwegian Federation of Trade Unions owns 10%and FöreningsSparbanken owns 25% (after exercisingthe option of increasing its interest by 1%).

Profit performanceThe SpareBank 1 SR-Bank group's profit performancewas very positive for all of 1999. The development withinboth the private and the corporate market was better thanexpected. This has to do with the fact that there wasconsiderably less of a decline in business activity thanfirst expected as well as better framework conditionsthrough lower interest rates. The positive developmentalso confirms that the group's strategy with a market-oriented organization with products and services adaptedto the customer is the right one. The group's profit of NOK654 million before losses and write-downs has been achievedas a result of good growth in interest income and otherincome, a high level of cost-effectiveness and few losses.Net interest income for the group rose by NOK 100million to NOK 895 million, an increase of 12%.Compared with the average total assets, net interestincome in 1999 constituted 2.63% as compared with2.73% in 1998. The fall in the interest margin reflectsmost of all the competition in the market. The interestmargin is also affected by the growth in credit to majorcustomer commitments.

The group's commission income increased in1999 to NOK 231 million. The underlying growthwithin payment services is in the order of 25%.

16.

Primary industry

Other industries

Service industries

Public sector

Wage earners

Commerce and hotels

Gross loans to customers in the

SpareBank 1 SR-Bank group

63,7%16,4%

8,7%

5,7%4,4%

1,0% 1,7%

10,8%

60,3%

1,8%

18,5%

6,9%

Guarantees in the

SpareBank 1 SR-Bank group

57,0%

17,0%

8,6%

3,9%5,0%

8,5%

Deposits from customers in the

SpareBank 1 SR-Bank group

«On 22 December 1999,an agreement was signedwhereby SpareBank 1Gruppen AS purchased the shares in VÅR GruppenASA for NOK 3.3 billion.In connection with the purchase, a long-term,comprehensive strategicand business-relatedalliance will be establishedbetween SpareBank 1Gruppen AS and LO/NKL(Norwegian Federation ofTrade Unions/ NorwegianCo-Operative Union andWholesale Society).»

However, price reductions through the programs forpreferred customers, which includes giving full-servicecustomers free use of electronic payment services withincertain limits, reduced the growth for commission incometo 14%. The good economy and the development onthe stock exchange increased savings in securities andinsurance over the last half year. The group's total salesof alternative savings products were NOK 800 million.Sales of non-life insurance increased and providedcommission income in the amount of NOK 10 millionlast year.

At the end of the year the bank's holding of shares,primary capital certificates and securities were posted atNOK 269 million. The return of 50.8% including primarycapital certificates is 5.3 percent better than the total gainon the Oslo Stock Exchange and resulted in NOK 96 mil-lion in capital gains last year. The holding of certificatesand bonds valued at NOK 1,902 million, which coversthe liquidity requirement, provided capital gains in theamount of NOK 1.4 million. Currency trading, for cus-tomers and the bank, gave a gain of NOK 25 million in1999. Total other income accounted for 30% of the group'sincome compared with 18% in 1998.

Operating costs for the group in 1999 amountedto NOK 622 million, an increase of NOK 95 millioncompared with 1998. Measured in relation to thebank's total assets, this constituted 1.83%, the sameratio as for last year. Measured in relation to totaloperating income, the costs amounted to 49%. Thenominal increase in costs is mainly a result of wagesettlements and expertise, technology and processcosts. Costs associated with profit-oriented bonuses,including social security costs, have increased by NOK

18 million to NOK 34 million for the group. IT costshave increased by NOK 14 million due to in-

creased transaction volumes. Costs asso-ciated with business process engine-

ering is estimated to be NOK 10million. Investments in new

processes and technologyare necessary in order to

maintain the quality ofthe group's servicesand will provide ad-ditional capacity.The current level ofcost-effectivenesswill be maintained.

Default trends are still satisfactory. Net losses of NOK102 million include an increase in unspecified loss allo-cations of NOK 40 million. During the year, default over90 days increased by NOK 45 million to NOK 284 million.

Balance sheetThe group's total assets increased by 16.5% to NOK36.4 billion in 1999, while the increase for the bankwas 18.9% to NOK 34.8 billion. Over the course of theyear, lending to the private market increased by NOK3,412 million (19.5%) and to corporate and the publicsector by NOK 844 million (7.6%). This means an annualgrowth of 14.9% in the group's lending. Deposits fromcustomers in 1999 have increased by NOK 1,730 milliondivided between NOK 1,136 million for private customers(11.6%) and NOK 594 million for businesses (7.7%).This is equal to an overall annual growth of 10%.

Risk ManagementCredit risk is managed through the Board's guidelines forcredit policy, risk profile and authorizations. The guide-lines are managed through established procedures for creditratings, credit committees and reporting of risk classes.

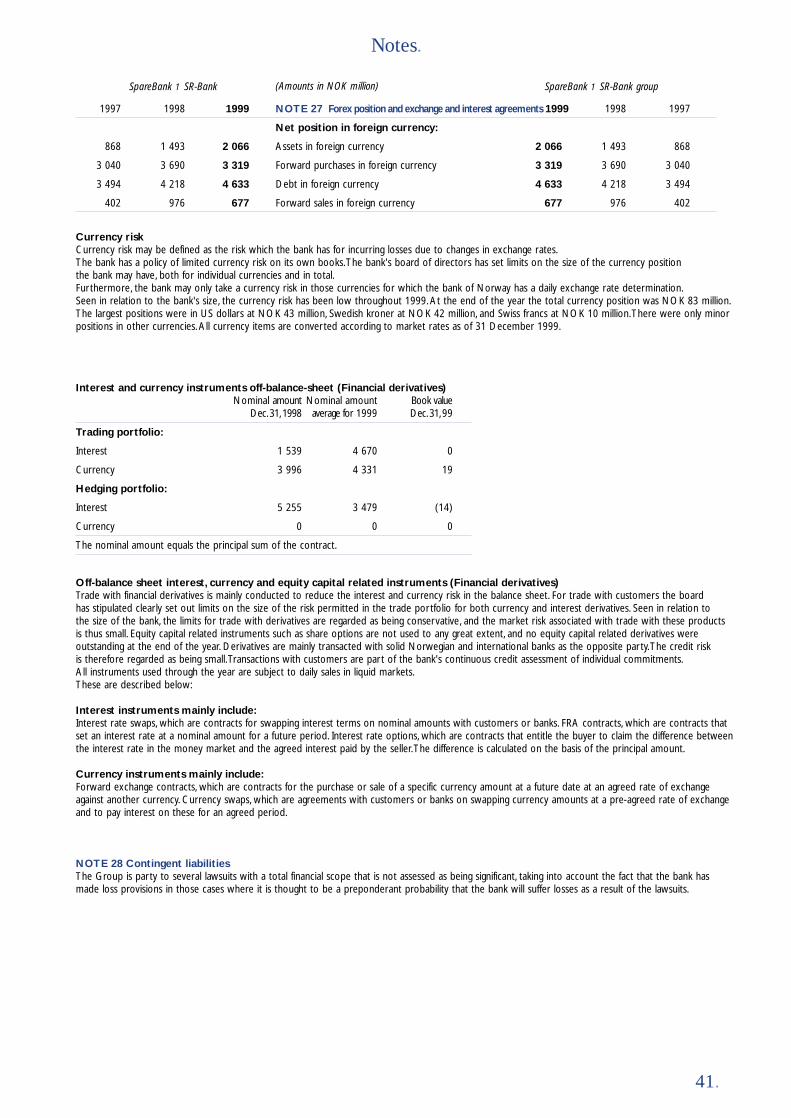

The group's foreign exchange activities are con-ducted according to a policy with limited positions onits own books. The holding of bonds is adjusted to theauthorities' requirements regarding liquid reserves. The interest risk for the bank's bond portfolio is reported to the Board on a monthly basis. This risk hasbeen moderate throughout the past year. Investmentsin equity capital securities are at a moderate level inrelation to the bank's balance sheet figures.

SubsidiariesThe real estate agents in the SpareBank 1-alliance haveestablished a nationwide chain from 1999 under thename EiendomsMegler 1. SR-Eiendom A/S haschanged its name to EiendomsMegler 1 Rogaland A/Sin order to strengthen development of the brand name.EiendomsMegler 1 Rogaland A/S is Rogaland's largestreal estate agency in both the residential and corporatemarket and had a good year with more than 2000transactions at a total value of more than NOK 2 billion.Operating income increased to NOK 54 million, result-ing in a profit before tax of NOK 9.8 million.

Westbroker Finans AS is the leading finance com-pany in Rogaland and had total assets of NOK 2,450million at the end of the year. The company increased

17.

Geir WorumCHAIRMAN

Tor HaverVICE-CHAIRMAN

Dominikus N. Bjordal

«At the end of the yearthe bank's holding ofshares, primary capitalcertificates and securitieswere posted at NOK269 million.»

«The real estate agents inthe SpareBank 1-alliancehave established a nation-wide chain from 1999under the nameEiendomsMegler 1.»

18.

its total assets by NOK 77 million, an increase of 3,3%.The main products are leasing, special financing, loanswith mortgage in real property and vehicles, and loanbrokering. The company offers products to the corpo-rate, public and private sectors. The company achieveda profit before tax of NOK 37 million, which gives a return on equity capital of 20.4%.

New accounting actThe new Accounting Act was implemented on 1 January1999. The new accounting principles increased the equi-ty capital for the group by NOK 55 million because ofcapitalization of deferred tax assets. The correspondingresult for the bank is NOK 153 million due to capitaliza-tion, as mentioned above, and valuation of subsidiariesand affiliates at NOK 98 million based on the equity method. On 1 January 2000 Terje Vareberg assumed the position of Managing Director.

Capital adequacy and capital market fundingAt year-end, the group's capital adequacy ratio was 12.12%,of which 8.63% was core capital. The correspondingkey figures for the bank at the end of the year were12.92% and 8.64% respectively. In the third quarter,the bank redeemed a perpetual loan in the amount ofUSD 60 million. At the same time, the bank raised a10-year subordinated loan in the USA in the amount ofUSD 100 million. The loan matures in 10 years and isstepped up after 5 years. This is the first loan the bankhas raised in the USA. During the year, the bankincreased long-term Norwegian bond funding (maturitymore than 12 months) by about NOK 1 billion. In addi-tion, the bank raised a five-year loan in the amount ofUSD 100 million in the international market.

Employees and working environmentAt the end of 1999 the group had 745 employees, corresponding to 677 man-years. The bank's staff hasbeen increased by four man-years to 604 man-yearsduring the course of the year.

Since 1993 the bank has performed annualorganization and working environment surveys, whichshow that the employees have a good relationship tothe bank and good faith in the bank's competitiveness.SpareBank 1 SR-Bank is characterized by employeeswho are willing to adapt and have a good service andsales attitude. They are very satisfied as regards job

content and the working environment. Absence due tosickness is at 3.29%, which is low compared with otherfinancial institutions. Cooperation with the employeesand their organization has been very good. During thecourse of 1999, a great number of employees havereceived extensive training, and the formal and profes-sional expertise has been strengthened even further.Currently, about 70% of the bank's employees have further education at the university level.

We are actively working on Health, Safety andEnvironment measures. In 1999 the bank experiencedthree robberies and the focus has mostly been on rob-beries and the threath of robberies. The employees havemade a great effort vis-à-vis the bank's customersthroughout the year and this has resulted in increasedconfidence in the bank and strengthened the bank'sposition as the leading bank in the region. The Boardwould like to thank the employees for their solid com-mitment throughout the year. This has contributed toimproved service for the customer and a good financialresult for the group. The Board extends its gratitude toArne Norheim for doing an outstanding job forSpareBank 1 SR-Bank since 1991. Geir Worum waselected as the new Chairman on 23 September 1999.In the opinion of the Board, the bank's activities do notpollute the external environment.

Bank advisory councilsThe cooperation with the local bank councils ensures aclose relationship with the local community and theconcerns of the bank's customers. The councils alsofunction as an important means of communication inthe ongoing change process and contribute to ensurethat all opportunities in the local market are recognized.

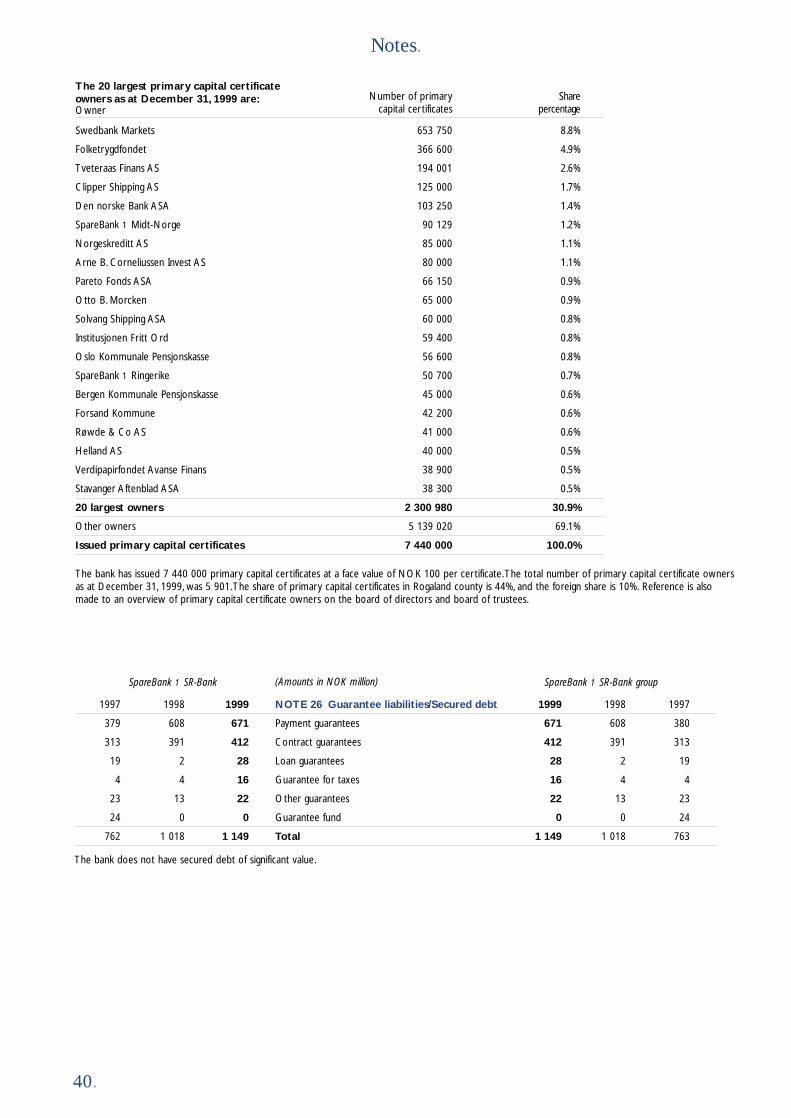

Primary capitalPrimary capital certificates equivalent to 39% of theoutstanding number were sold in 1999. This is a declineof 48% compared with the previous year. The number ofprimary capital certificate holders increased from 5,698 atthe beginning of the year to 5,901 at the end of the year.The percentage of primary capital certificates owned byforeigners was 10.1%, while 44.2 % resided in Rogaland.The 20 largest owners owned 30.9% of the primary capital.

SpareBank 1 SR-Bank emphasizes the importanceof competitive dividends. In the proportional distributionbetween cash dividend and the dividend equalizationreserve, the bank's equity capital development will be

«SpareBank 1 SR-Bank is characterized byemployees who are willing to adapt and havea good service and salesattitude.»

Kristian Eidesvik Ole Gladhaug Åse Holmane

19.

given priority. In keeping with the bank's dividend policy,the results of the year and the core capital, the Boardproposes to pay NOK 19 in dividends, as well as to allocateNOK 21.40 to the equalization reserve per primary capitalcertificate for the 1999 accounting year. After thisappropriation, the equalization reserve will amount to NOK83.33 per certificate. The RISK amount as of 1 January1999 was stipulated at NOK 27.74 per primary capital certificate. The corresponding RISK amount as of 1January 2000 is provisionally estimated to be NOK 28.

Application of profit/dividendsThe Board proposes the following application ofSparebanken Rogaland's profit for the year of NOK 451 mill.:NOK millionProfit for the year 451Dividend, NOK 19 per certificate 141Equalization reserve 159Endowment fund 10The Savings Bank's reserve 137Dividend equalization reserve 4Total 451

Continued operationsThe annual report and accounts have been issuedbased on the assumption of continued operations.This assumption is based on profit projections for2000 and the group's long-term strategic projectionsfor the years ahead. The group has good solidity andcore capital and the capital adequacy ratio is goodseen in relation to the authorities' requirements.

Outlook for the futureThe Board expects a somewhat weaker economicdevelopment in the region in 2000. However, theactivity level at the beginning of the year provides a good foundation for good operations. In spite ofpossibly reduced employment as well as a reducedlevel of activity for the petroleum sector, the Board is of the opinion that the financial basis for the customers is satisfactory. The foundation for goodoperations in 2000 is good. The Board expects a satisfactory result for the SpareBank 1 SR-Bankgroup in 2000.

Magne Vathne Karl A. Naley Terje VarebergADM. DIREKTØR

Geir WorumChairman

Kristian Eidesvik

Magne Vathne

Tor HaverVice-chairman

Ole Gladhaug

Karl A. Naley

Dominikus N. Bjordal

Åse Holmane

Terje VarebergManaging director

«In keeping with the bank's dividend policy, theresults of the year and thecore capital, the Boardproposes to pay NOK 19in dividends, as well as toallocate NOK 21.40 tothe equalization reserveper primary capital certi-ficate for the 1999accounting year.»

Stavanger, 24 February 2000

The Board of Directors Sparebanken Rogaland

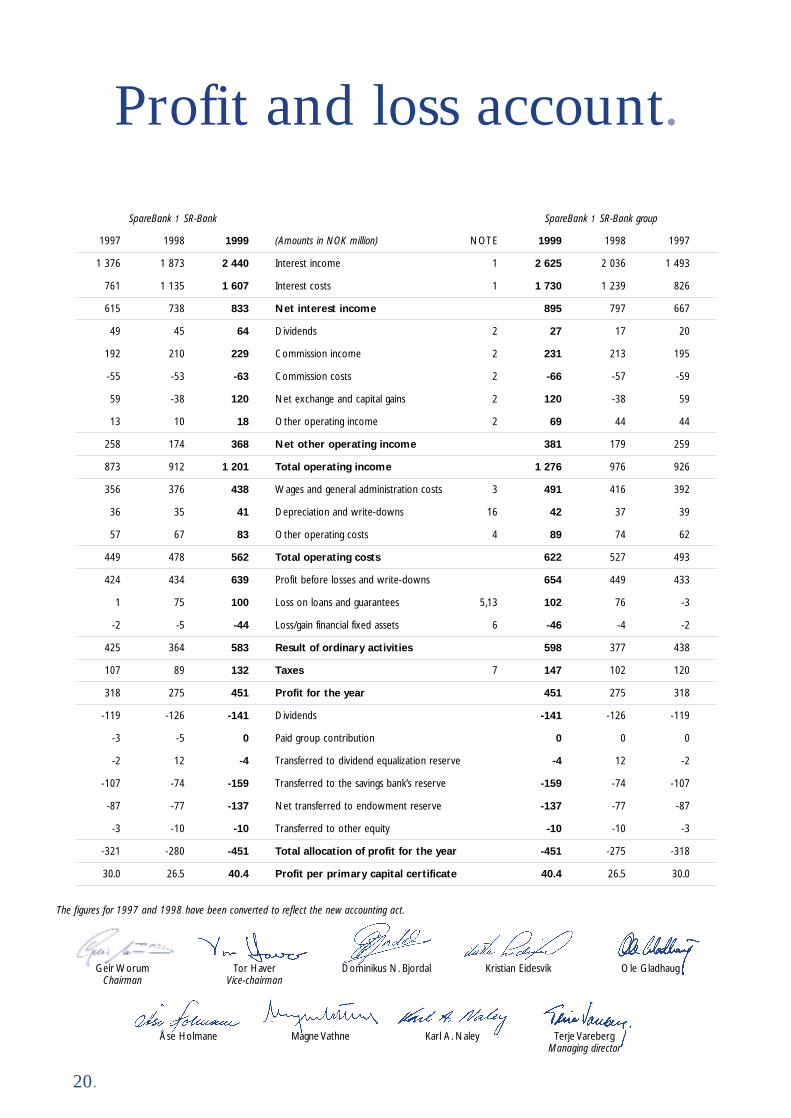

Profit and loss account.

1997 1998 1999 (Amounts in NOK million) NOTE 1999 1998 1997

1 376 1 873 2 440 Interest income 1 2 625 2 036 1 493

761 1 135 1 607 Interest costs 1 1 730 1 239 826

615 738 833 Net interest income 895 797 667

49 45 64 Dividends 2 27 17 20

192 210 229 Commission income 2 231 213 195

-55 -53 -63 Commission costs 2 -66 -57 -59

59 -38 120 Net exchange and capital gains 2 120 -38 59

13 10 18 Other operating income 2 69 44 44

258 174 368 Net other operating income 381 179 259

873 912 1 201 Total operating income 1 276 976 926

356 376 438 Wages and general administration costs 3 491 416 392

36 35 41 Depreciation and write-downs 16 42 37 39

57 67 83 Other operating costs 4 89 74 62

449 478 562 Total operating costs 622 527 493

424 434 639 Profit before losses and write-downs 654 449 433

1 75 100 Loss on loans and guarantees 5,13 102 76 -3

-2 -5 -44 Loss/gain financial fixed assets 6 -46 -4 -2

425 364 583 Result of ordinary activities 598 377 438

107 89 132 Taxes 7 147 102 120

318 275 451 Profit for the year 451 275 318

-119 -126 -141 Dividends -141 -126 -119

-3 -5 0 Paid group contribution 0 0 0

-2 12 -4 Transferred to dividend equalization reserve -4 12 -2

-107 -74 -159 Transferred to the savings bank’s reserve -159 -74 -107

-87 -77 -137 Net transferred to endowment reserve -137 -77 -87

-3 -10 -10 Transferred to other equity -10 -10 -3

-321 -280 -451 Total allocation of profit for the year -451 -275 -318

30.0 26.5 40.4 Profit per primary capital certificate 40.4 26.5 30.0

The figures for 1997 and 1998 have been converted to reflect the new accounting act.

SpareBank 1 SR-Bank SpareBank 1 SR-Bank group

20.

Geir WorumChairman

Tor HaverVice-chairman

Dominikus N. Bjordal Kristian Eidesvik Ole Gladhaug

Åse Holmane Magne Vathne Karl A. Naley Terje VarebergManaging director

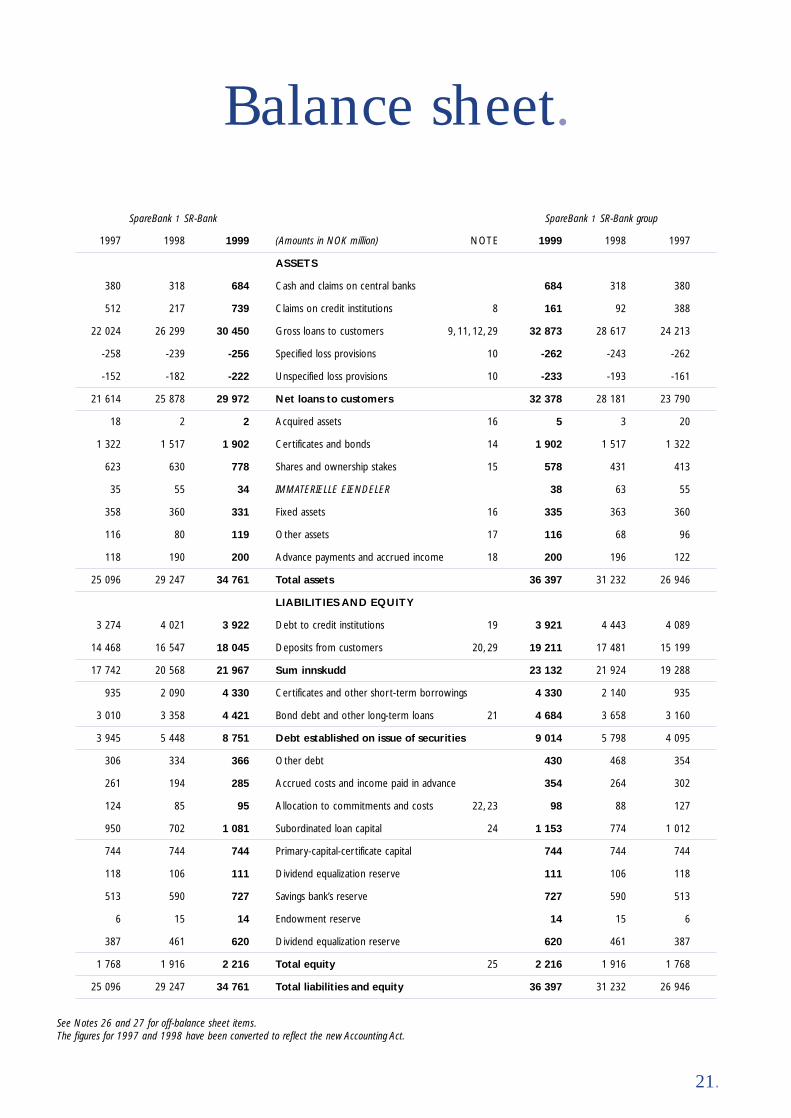

Balance sheet.

1997 1998 1999 (Amounts in NOK million) NOTE 1999 1998 1997

ASSETS

380 318 684 Cash and claims on central banks 684 318 380

512 217 739 Claims on credit institutions 8 161 92 388

22 024 26 299 30 450 Gross loans to customers 9, 11, 12, 29 32 873 28 617 24 213

-258 -239 -256 Specified loss provisions 10 -262 -243 -262

-152 -182 -222 Unspecified loss provisions 10 -233 -193 -161

21 614 25 878 29 972 Net loans to customers 32 378 28 181 23 790

18 2 2 Acquired assets 16 5 3 20

1 322 1 517 1 902 Certificates and bonds 14 1 902 1 517 1 322

623 630 778 Shares and ownership stakes 15 578 431 413

35 55 34 IMMATERIELLE EIENDELER 38 63 55

358 360 331 Fixed assets 16 335 363 360

116 80 119 Other assets 17 116 68 96

118 190 200 Advance payments and accrued income 18 200 196 122

25 096 29 247 34 761 Total assets 36 397 31 232 26 946

LIABILITIES AND EQUITY

3 274 4 021 3 922 Debt to credit institutions 19 3 921 4 443 4 089

14 468 16 547 18 045 Deposits from customers 20, 29 19 211 17 481 15 199

17 742 20 568 21 967 Sum innskudd 23 132 21 924 19 288

935 2 090 4 330 Certificates and other short-term borrowings 4 330 2 140 935

3 010 3 358 4 421 Bond debt and other long-term loans 21 4 684 3 658 3 160

3 945 5 448 8 751 Debt established on issue of securities 9 014 5 798 4 095

306 334 366 Other debt 430 468 354

261 194 285 Accrued costs and income paid in advance 354 264 302

124 85 95 Allocation to commitments and costs 22, 23 98 88 127

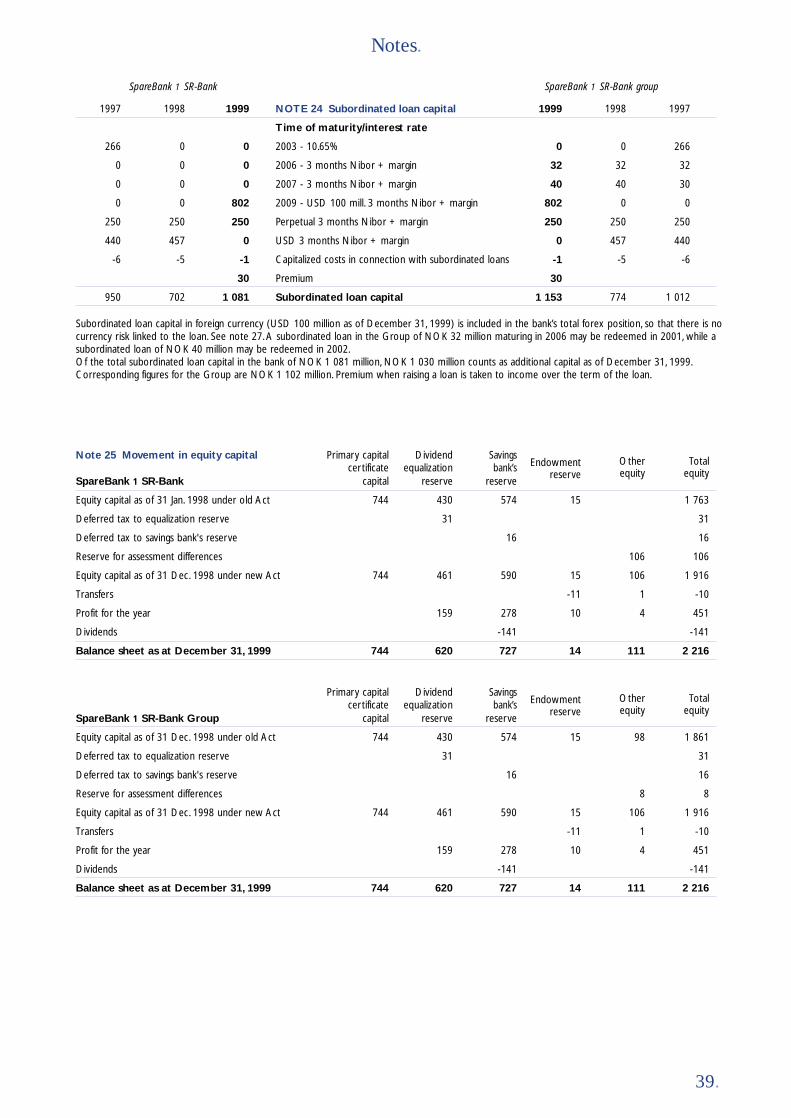

950 702 1 081 Subordinated loan capital 24 1 153 774 1 012

744 744 744 Primary-capital-certificate capital 744 744 744

118 106 111 Dividend equalization reserve 111 106 118

513 590 727 Savings bank’s reserve 727 590 513

6 15 14 Endowment reserve 14 15 6

387 461 620 Dividend equalization reserve 620 461 387

1 768 1 916 2 216 Total equity 25 2 216 1 916 1 768

25 096 29 247 34 761 Total liabilities and equity 36 397 31 232 26 946

See Notes 26 and 27 for off-balance sheet items.The figures for 1997 and 1998 have been converted to reflect the new Accounting Act.

SpareBank 1 SR-Bank groupSpareBank 1 SR-Bank

21.

22.

Accounting Principles.

GeneralThe annual accounts for 1999 have been prepared inaccordance with Accounting Act, regulations andgenerally accepted accounting principles. All figuresare stated in NOK million unless otherwise indicated.

The same accounting principles are applied to theparent bank's and the group's accounts.

The annual accounts for 1999 comply with the newAccounting Act, which entered into force on 1 January1999. The two preceding annual accounts have beenrevised correspondingly for comparison purposes.

ConsolidationSubsidiariesThe group accounts include SpareBank 1 SR-Bank andcompanies in which SpareBank 1 SR-Bank directlyand indirectly owns more than 50% of the shares orhas controlling influence on the company's operations.The investments in subsidiaries have been consolidatedaccording to the acquisition method in the group accountsand the equity method in the company's accounts.

Affiliated CompaniesAffiliated companies are defined as companies inwhich the bank has a long-term investment with anownership interest of 20 to 50 percent and in whichthe bank has significant influence. Such investmentsare appraised according to the equity method both inthe company's accounts and the group accounts.

Jointly Controlled OperationsJointly controlled operations are financial operationsgoverned by an agreement between the bank and oneor more participants, so that the bank and the partic-ipants have joint control of the operations. No partic-ipants have controlling influence alone.

The bank has established SpareBank 1 Gruppen ASin collaboration with SpareBank 1 Nord Norge,SpareBank 1 Midt Norge, SpareBank 1 Vest andSamarbeidende Sparebanker AS.

In 1999 FöreningsSparbanken purchased 24% ofSpareBank 1 Gruppen, leaving the other banks withan ownership interest of 15.2% each. The manage-ment structure of Sparebank 1 Gruppen is governedby a framework agreement between the owner banks.The ownership interest is regarded as jointly controlled operations.

In the accounts for SpareBank 1 SR-Bank the sharesin SpareBank 1 Gruppen have been appraisedaccording to the equity method, both in the company'saccounts and the group accounts, as the operations ofSpareBank 1 Gruppen are considerably different thanthe bank's other operations where the use of thegross method of depreciation would provide accounting information that is not easily accessible.

Entering Income and CostsInterest and fees are entered in the profit and lossaccount as they are earned as income or accrue ascosts. Fees that are a direct payment for services rendered are taken to income when they are paid.Arrangement fees are taken to income in accordancewith the costs that accrue for arranging loans.

The accruals principle is applied to prepaid incomeand accrued non-paid costs at the end of the year,which are entered as debt in the balance sheet.Accrued income is taken to income and entered asreceivables in the balance sheet.

Dividends are taken to income in the year they arereceived. Dividends and group contributions fromsubsidiaries, affiliated companies and jointly con-trolled businesses are entered directly against bookownership interest in the associated business.

Securities and SharesShares, primary capital certificates and shares in unittrusts that are traded on the stock exchange or in aregulated market and have good ownership diversifi-cation and liquidity, are included in the portfolio andare appraised at market value on the balance sheet date.Securities that are not listed on the stock exchange areappraised at the lower of original cost or market value.

Long-term shareholdings are appraised at original cost.If the real value is considerably lower the originalcost, and the decline in value is not deemed to be ofa temporary nature, the share is written down to thereal value. The write-down is reversed when there nolonger is a basis for the write-down.

Certificates and BondsCertificates and bonds classified as current assets areappraised at market value on the balance sheet date.Long-dated bonds that have been purchased to beheld until maturity have been entered at cost adjustedfor amortised premiums or discounts. Premiums

23.

and/or discounts are accrued linearly over theremaining life of the bond as a correction to thenominal interest rate.

Foreign CurrencyThe bank's assets and liabilities in foreign currencyare converted to middle rates as of 31 December.Income and costs in foreign currency are convertedto NOK at the rates at the time of the transaction.

The currency items are mainly hedged against corre-sponding items on the opposite side of the balancesheet or by off-balance sheet hedging transactions.

Financial InstrumentsFinancial instruments include negotiable financialasset and liability items plus financial derivatives.Financial instruments in the balance sheet includeshares, primary capital certificates, bonds and certifi-cates. Financial derivatives are agreements that areentered into with financial institutions or customersto set financial values in the form of interest terms,foreign exchange rates and the value of equity instru-ments for definite periods of time. These agreementsinclude forward exchange contracts, interest rate swaps(currency swaps), currency and interest rate options,and agreements to set future interest terms (FRAs).

A distinction is made between agreements that are astage in own-account transactions in order to achieveearnings through price differences and price changes(the trading portfolio) and agreements that are enteredinto in the ordinary business. Interest rate and mone-tary agreements are classified at the time they areentered into as part of the trading portfolio or bankingbusiness depending on the individual agreement. Thetrading portfolio consists of certificates and bonds,shares and primary capital certificates in the bank'sbalance sheet, plus currency, interest and equityinstruments not included in the balance sheet.

The off-balance sheet portfolios of transactions areappraised according to the market value method, andchanges in market values are entered in the profitand loss account under the item of net profit and losson exchange. Agreements that are entered into toreduce the bank's exposure to fluctuations in interestand/or exchange rates for items in the balance sheet,are defined as hedging transactions.

In order for monetary or interest rate agreements tode defined as hedging transactions, the expectedtrend in the value of the hedging transactions mustbe closely associated with the balance sheet item thatis hedged. Income and expenses related to the hedg-ing agreements and their respective balance sheetitems are entered in the accounts as accruals andclassified in the same way.

Losses on LoansLoans are appraised at nominal value with the exceptionof problem, non-performing and renegotiated loans.

Non-performing/Problem LoansA customer's aggregate loans are regarded as non-performing and included in the bank's overviews ofnon-performing loans when the installment or interestdue has not been paid within 90 days after the duedate or when the line of credit has been overdrawnfor 90 or more days.Loans and other commitments that are not non-per-forming, but where the customer's financial situationmakes it likely that the bank will incur a loss, areclassified as problem loans.

Specified loss provisionsWhen loans have been have been non-performing formore than 60 days or are classified as problem loans,credited interest is reversed and further crediting ishalted unless the loan is covered by underlying collateral. The difference between the loan's nominalvalue and the value of the securities plus the customer's assumed earning capacity is charged as an expense under losses on loans and guarantees.

There is generally a great deal of uncertainty associatedwith the appraisal of loans that are presumed to be problem loans, the value of securities and the customer's financial earning capacity.

Unspecified loss provisionsUnspecified loss provisions are to cover losses that,on the basis of conditions that prevail on the balancesheet date, are expected to come in addition to lossesthat have been identified and estimated for individualcustomers. Such provisions are estimated on the basisof appraisals of portfolios, experience and generaldevelopment trends. Changes in the size of the lending portfolio are taken into consideration.

Actual loan lossesWhen it is highly likely that the losses are final, thelosses are classified as actual loan losses. Actual loanlosses that are covered by specified loan provisionsthat have previously been made are charged againstthese provisions. Actual loan losses without coverageby loan loss provisions are charged to the results.

Acquired assetsAs part of the handling of non-performing loans andguarantees, the bank in some cases acquires assetsthat have been furnished as security for these com-mitments. At the time of acquisition, the assets areappraised at the assumed realisation value. Acquiredassets that are to be realised are classified as currentassets. Any losses and/or gains at the time of disposalor reappraisal of the value of these assets are enteredas a loss or reduction in the loss on the loan.

24.

LeasingThe leasing portfolio is classified for accounting purposes as leasing agreements under the main category of loans to and claims on customers. Leasingincome is entered as leasing income under interestincome and the expenditures as interest costs.

Tangible fixed assetsTangible fixed assets are entered in the accounts atcost with the addition of previous revaluation, andthe deduction of write-downs and ordinary accumu-lated depreciation. Ordinary depreciation is based on the cost price and the depreciation is distributedlinearly over the useful life of the assets.

If the actual value of a tangible fixed asset is considerablyless than the book value, and the decrease in valuecannot be expected to be temporary, the asset is writtendown to the actual value. The write-down is reversedwhen there no longer is a basis for the write-down.

Issued Bonds and Other LoansIssued bonds are entered in the balance sheet atnominal value with premiums added and discountsdeducted. Premiums are taken to income and discountsare charged against income according to a scheduleas an adjustment of the current interest costs untilthe bond matures or until the first time the interestrate is adjusted. Direct costs related to issuance ofbonds and other loans are charged against incomeaccording to a schedule as an adjustment to the current interest cost until the bond or loan matures.

Pension LiabilitiesIn the balance sheet net pension funds in the collec-tive plan are treated as fixed assets, whereas netunfunded pension liabilities are classified as long-term debt. The employer's National Insurance contri-butions that will accrue at the current rates are alsoincluded in the amount for unfunded pension liabili-ties. Net pension costs are classified under wage costsin the profit and loss account, and include the earnedpension for the period and interest costs on the liabilities minus the estimated return on the pensionfunds. The economic effects of changes in pensionplans are amortised over the average remaining earning time. Other changes and differences are evaluated in total against the highest value of thetotal pension liabilities and total pension funds. Iftotal changes and estimated differences representmore than 10 percent of this basis at the end of thefiscal year, the remaining amount will be amortisedover the remaining earning time.

TaxesThe annual tax expenditures in the profit and lossaccount consist of taxes payable on the income forthe year adjusted for surplus or deficit allocated fromprevious years plus changes in deferred taxes.

Deferred taxes are calculated on the basis of tempo-rary differences between accounting and tax values atthe close of the accounting year. The nominal taxrate is employed in the calculation. Positive and neg-ative differences are appraised against each other andare shown as net in the balance sheet. Deferred taxbenefits arise if there are temporary differences thatgive rise to tax deductions in the future.

LiabilitiesLiabilities are entered at original cost. Interest is con-tinuously carried to expense in the profit and loss account.

Business AreasSparebank 1 SR-Bank appraises business in the bankas an aggregate business area.

Individual TransactionsSpareBank 1 SR-Bank has reduced its shareholdingin Sparebank 1 Gruppen from 20% to 15% in thecourse of the year. This reduction resulted in anaccounting gain of NOK 52.6 million.

Changes in Accounting PrinciplesAs a result of the new Accounting Act, the bank madesome changes in the accounting principles with effectfrom 1 January 1999. The following changes have been made:Listed shares and bonds that are part of the tradingportfolio shall be appraised at their real value.Investments in subsidiaries, affiliated companies andjointly controlled businesses shall be appraisedaccording to the equity method in the parent bank.The difference between the investment's valueentered in the balance sheet according to the equitymethod and the original cost is transferred toreserves for appraisal differences.

Deferred tax benefits shall be appraised according tothe general appraisal rules. This means that deferredtax entered in the balance sheet is no longer anupper limit for balance sheet entry.

The comparison figures in the profit and loss account have been revised in accordance with thenew principles for the years 1998 and 1997.

The effect of the new principles on profit and equityin NOK million amounted to:

SpareBank 1 SpareBank 1

SR-Bank SR-Bank group

1997 1998 1997 1998

Profit for the year 305 314 312 309

Securities at actual value 19 -43 19 -43

Dividend - 1 -17 0 0

Tax -5 21 -13 9

Revised profit for the year 318 275 318 275

Equity – ref. Note 25

25.

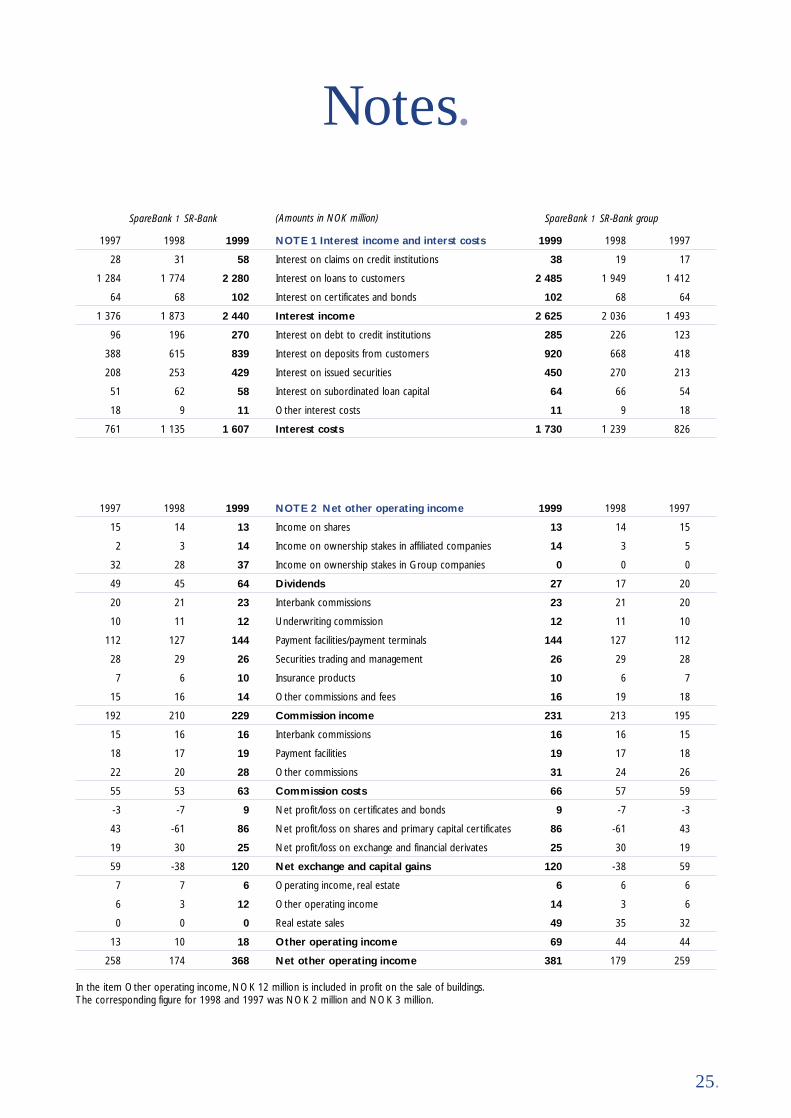

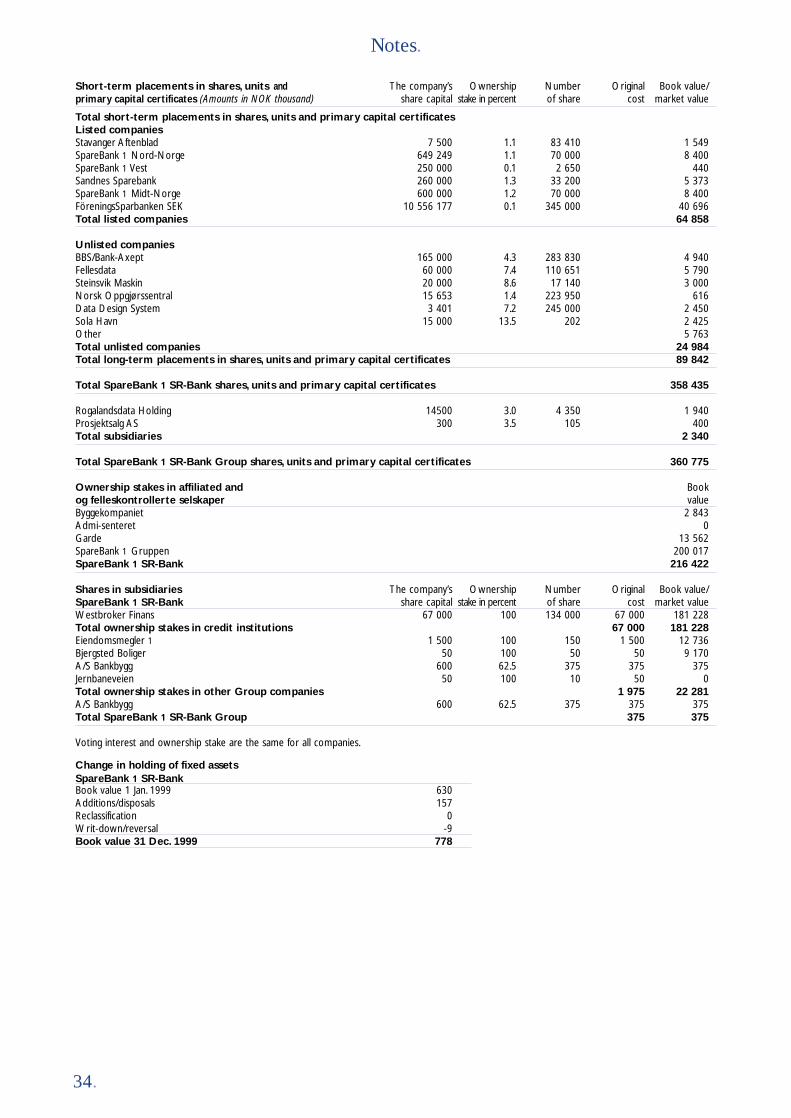

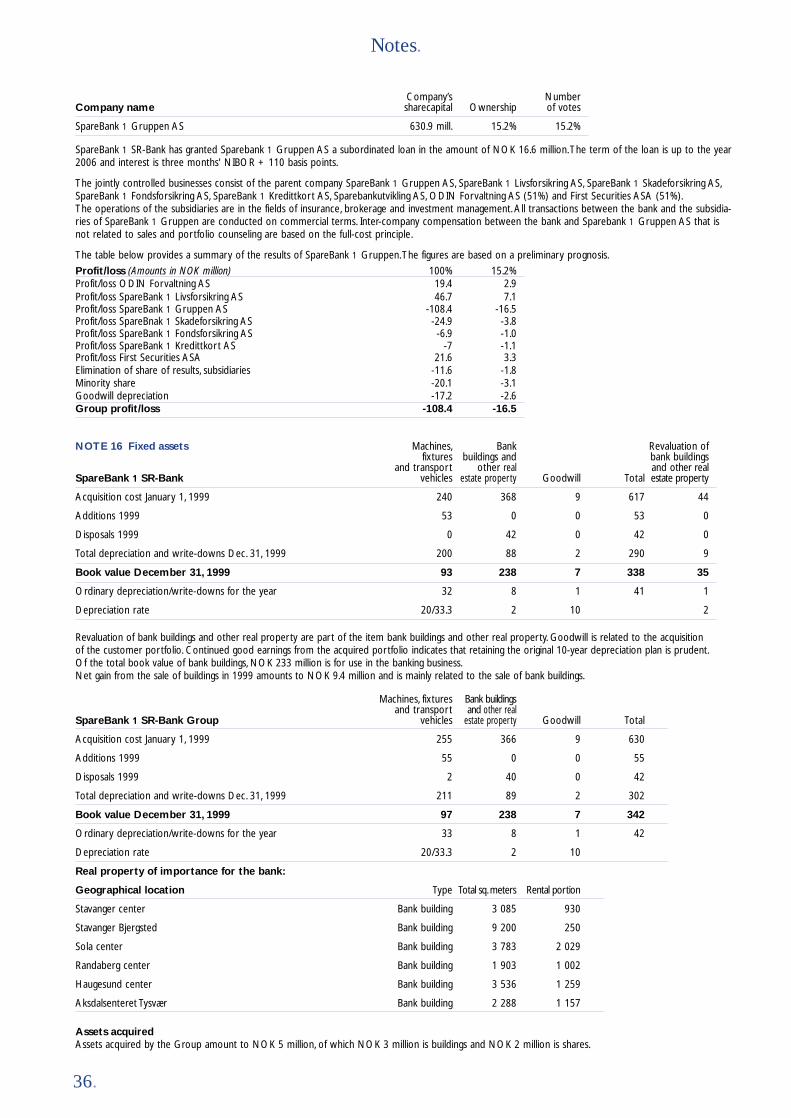

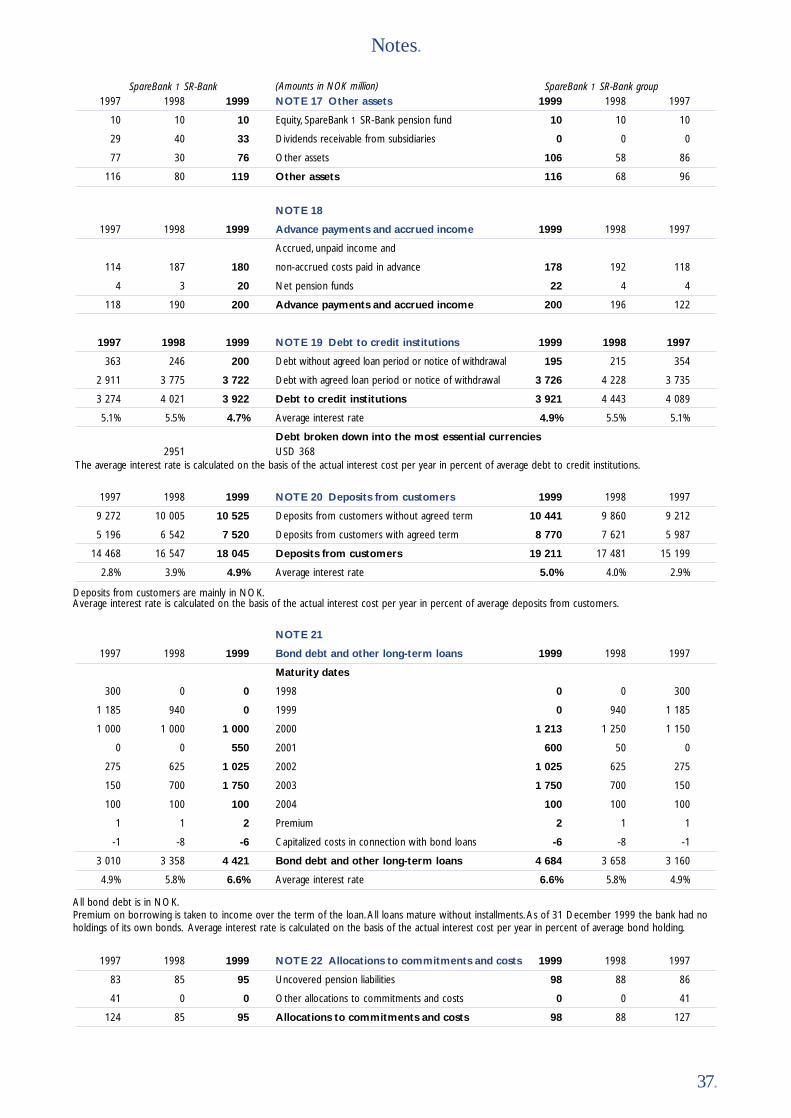

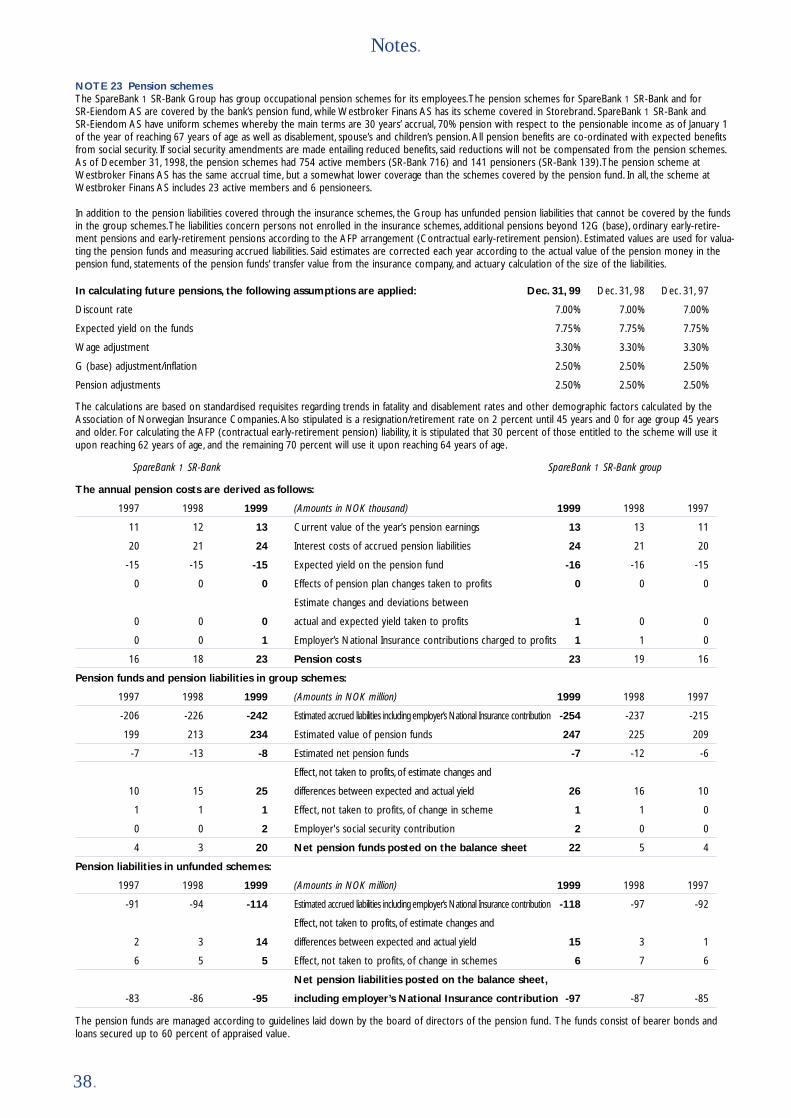

Notes.

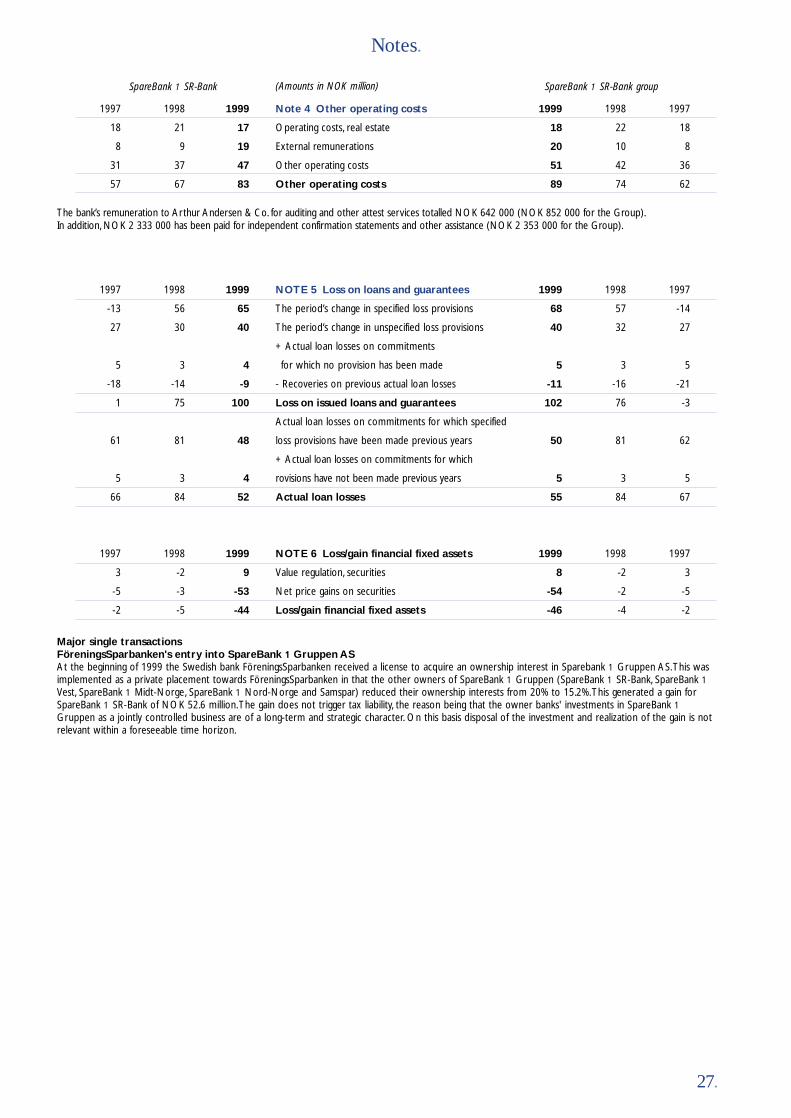

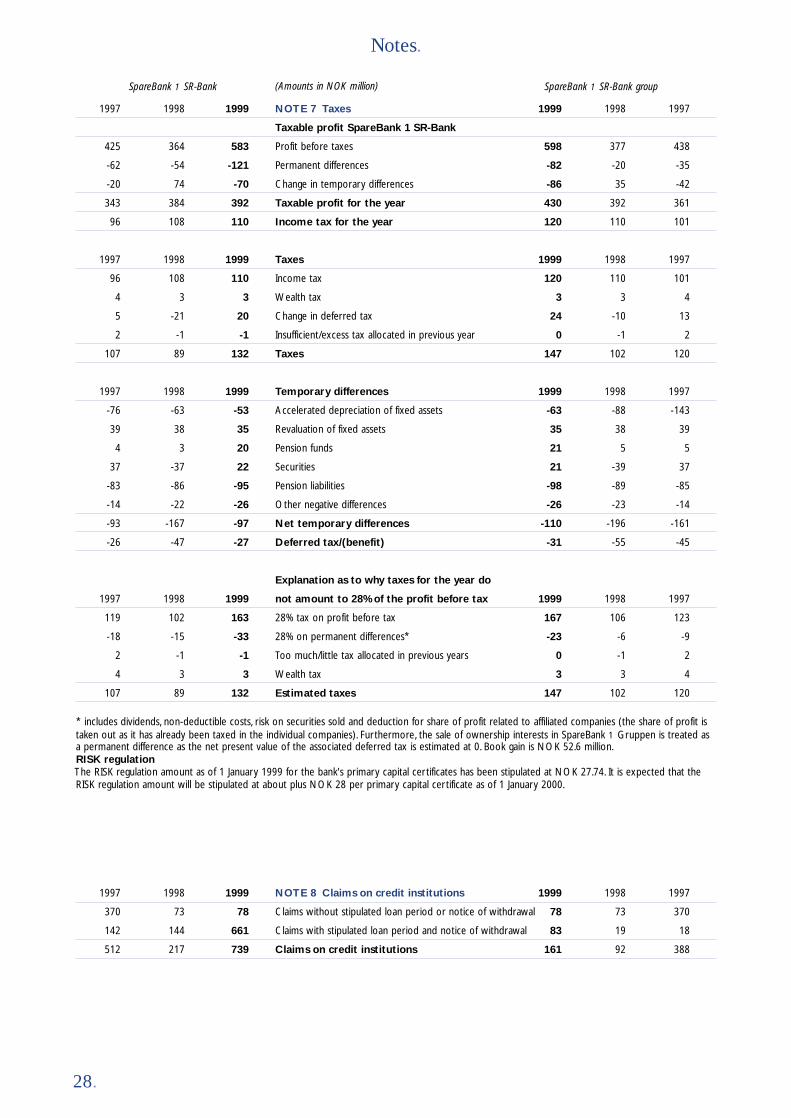

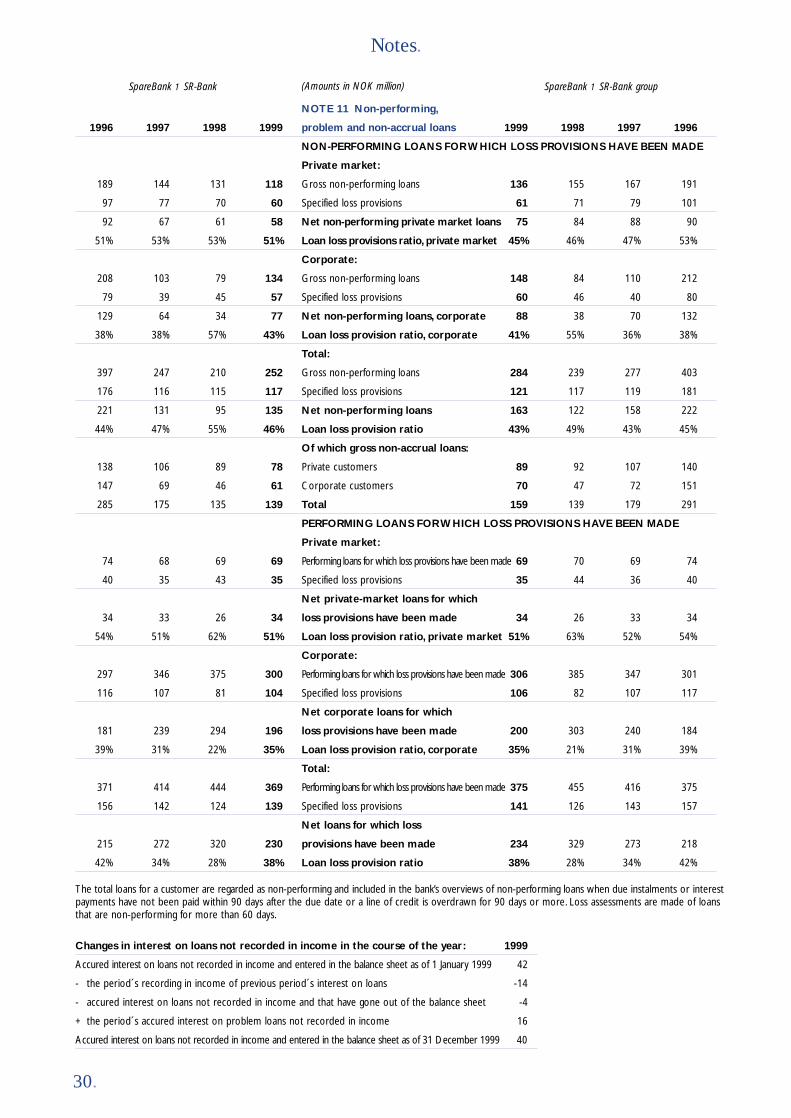

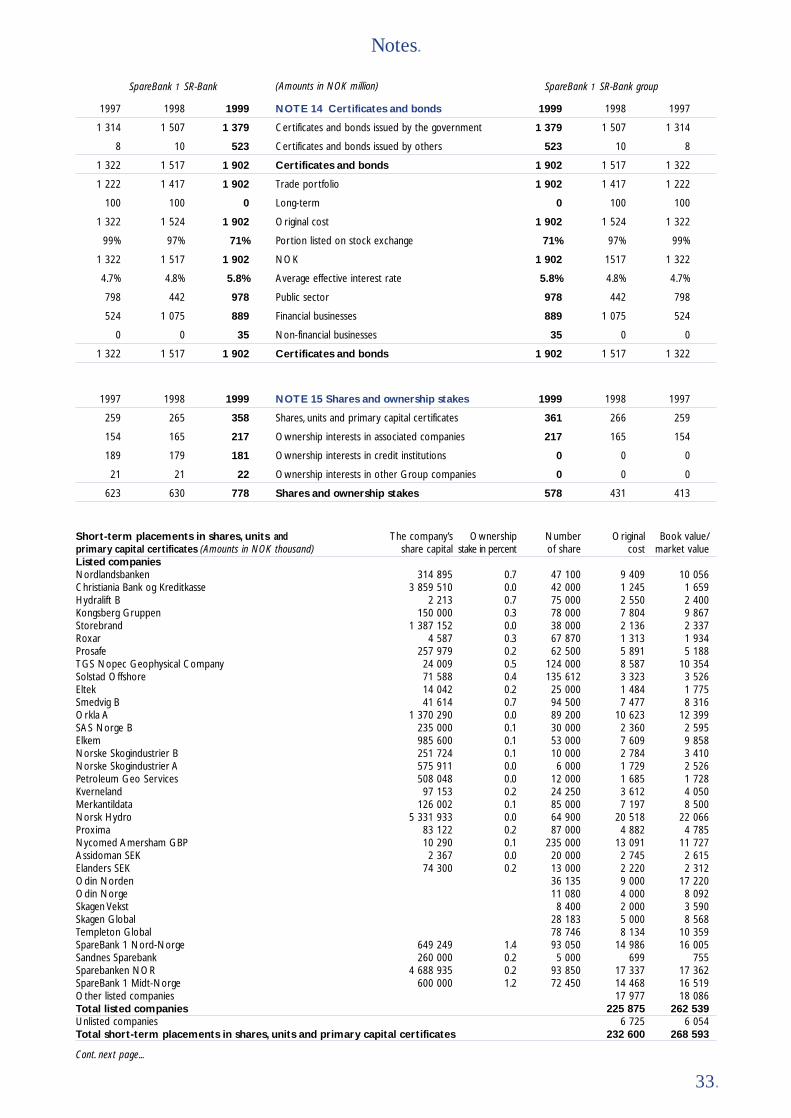

1997 1998 1999 NOTE 1 Interest income and interst costs 1999 1998 1997

28 31 58 Interest on claims on credit institutions 38 19 17

1 284 1 774 2 280 Interest on loans to customers 2 485 1 949 1 412

64 68 102 Interest on certificates and bonds 102 68 64

1 376 1 873 2 440 Interest income 2 625 2 036 1 493

96 196 270 Interest on debt to credit institutions 285 226 123

388 615 839 Interest on deposits from customers 920 668 418

208 253 429 Interest on issued securities 450 270 213

51 62 58 Interest on subordinated loan capital 64 66 54

18 9 11 Other interest costs 11 9 18

761 1 135 1 607 Interest costs 1 730 1 239 826

1997 1998 1999 NOTE 2 Net other operating income 1999 1998 1997

15 14 13 Income on shares 13 14 15

2 3 14 Income on ownership stakes in affiliated companies 14 3 5

32 28 37 Income on ownership stakes in Group companies 0 0 0

49 45 64 Dividends 27 17 20

20 21 23 Interbank commissions 23 21 20

10 11 12 Underwriting commission 12 11 10

112 127 144 Payment facilities/payment terminals 144 127 112

28 29 26 Securities trading and management 26 29 28

7 6 10 Insurance products 10 6 7

15 16 14 Other commissions and fees 16 19 18

192 210 229 Commission income 231 213 195

15 16 16 Interbank commissions 16 16 15

18 17 19 Payment facilities 19 17 18

22 20 28 Other commissions 31 24 26

55 53 63 Commission costs 66 57 59

-3 -7 9 Net profit/loss on certificates and bonds 9 -7 -3

43 -61 86 Net profit/loss on shares and primary capital certificates 86 -61 43

19 30 25 Net profit/loss on exchange and financial derivates 25 30 19

59 -38 120 Net exchange and capital gains 120 -38 59

7 7 6 Operating income, real estate 6 6 6

6 3 12 Other operating income 14 3 6

0 0 0 Real estate sales 49 35 32

13 10 18 Other operating income 69 44 44

258 174 368 Net other operating income 381 179 259

SpareBank 1 SR-Bank groupSpareBank 1 SR-Bank (Amounts in NOK million)

In the item Other operating income, NOK 12 million is included in profit on the sale of buildings.The corresponding figure for 1998 and 1997 was NOK 2 million and NOK 3 million.

26.

Notes.

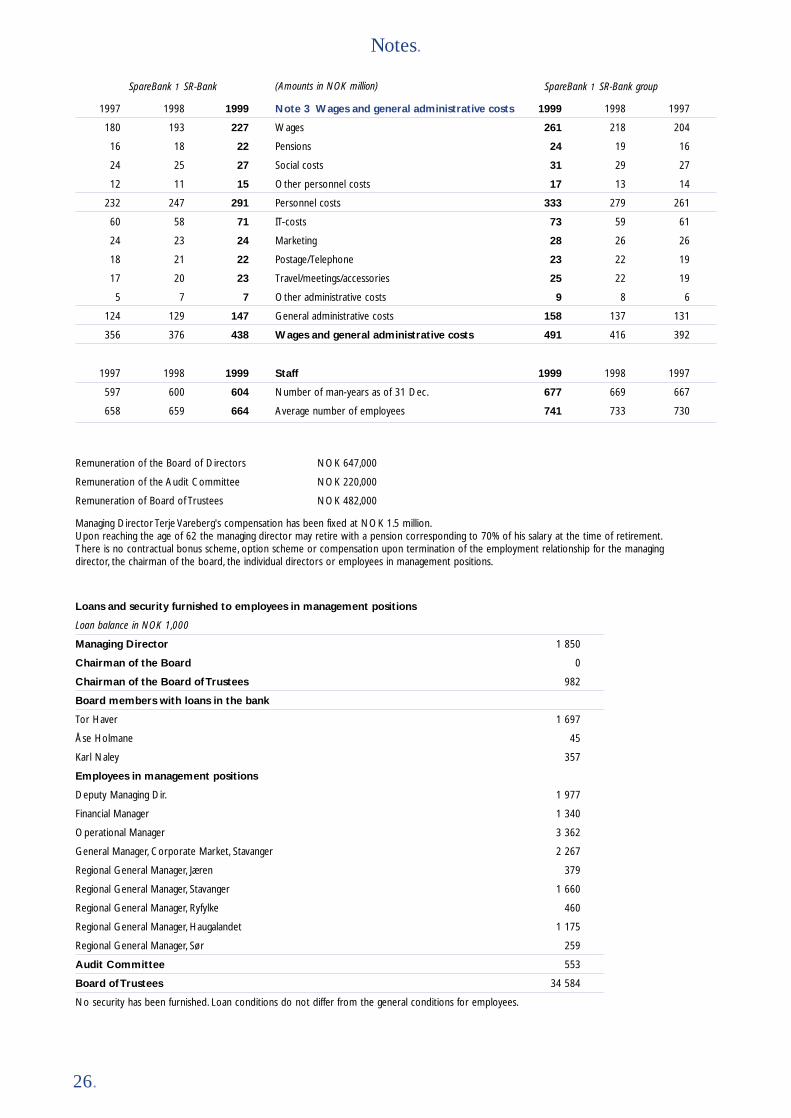

1997 1998 1999 Note 3 Wages and general administrative costs 1999 1998 1997

180 193 227 Wages 261 218 204

16 18 22 Pensions 24 19 16

24 25 27 Social costs 31 29 27

12 11 15 Other personnel costs 17 13 14

232 247 291 Personnel costs 333 279 261

60 58 71 IT-costs 73 59 61

24 23 24 Marketing 28 26 26

18 21 22 Postage/Telephone 23 22 19

17 20 23 Travel/meetings/accessories 25 22 19

5 7 7 Other administrative costs 9 8 6

124 129 147 General administrative costs 158 137 131

356 376 438 Wages and general administrative costs 491 416 392

Loans and security furnished to employees in management positions

Loan balance in NOK 1,000

Managing Director 1 850

Chairman of the Board 0

Chairman of the Board of Trustees 982

Board members with loans in the bank

Tor Haver 1 697

Åse Holmane 45

Karl Naley 357

Employees in management positions

Deputy Managing Dir. 1 977

Financial Manager 1 340

Operational Manager 3 362

General Manager, Corporate Market, Stavanger 2 267

Regional General Manager, Jæren 379

Regional General Manager, Stavanger 1 660

Regional General Manager, Ryfylke 460

Regional General Manager, Haugalandet 1 175

Regional General Manager, Sør 259

Audit Committee 553

Board of Trustees 34 584

No security has been furnished. Loan conditions do not differ from the general conditions for employees.

Remuneration of the Board of Directors NOK 647,000

Remuneration of the Audit Committee NOK 220,000

Remuneration of Board of Trustees NOK 482,000