space diplomacy for business · 2019-09-19 · space economic diplomacy, a pillar of a wider eu...

TRANSCRIPT

W H Y ( A N D H O W ) E U R O P E A N E C O N O M I C D I P L O M A C Y M AT T E R S F O R T H E S PA C E S E C T O R

1

SPACE DIPLOMACY FOR BUSINESS

Lucas Buthion19/09/2019

A E U R O P E A N U N I Q U E N E S S I N S PA C E

A R AT I O N A L E F O R S PA C E E C O N O M I C D I P L O M A C YA C T I O N S

2

HIGHLIGHTS ON PROMINENT SPACE MARKETS DYNAMICS

The European space industry & the world: main features

3

USA30%

ex-USSR36%

Europe4%

China21%

Japan2%

India7%

Employment in the space manufacturing sector worldwide (est.)

Space industry output (past 5 years / 2014-2018)

China15%

Europe16%

Russia29%

Ind…

Japan6%

USA32%

China15%

Europe16%

Ex-USSR22%

India3%

Japan7%

USA37%

Total Spacecraft Mass by SC supplier

Total mass launched to orbit by launcher supplier

>> Space industry workforce worldwide: about 700.000 people

(c) copyright - reproduction forbidden

Suppliers exposure to captive/open SC markets (2014-2018)Mass launched (tons) – SC Supplier perspective

4

0

100

200

300

400

ChinaSupply

EuropeSupply

Ex-USSRSupply

IndiaSupply

JapanSupply

USASupply

captive

open

Special agreement NASA/Roskosmos for ISS

servicing, not Open market

(c) copyright - reproduction forbidden

Global Launch services marketby launch country (M$)

(c) copyright - reproduction forbidden

5

0

500

1000

1500

2000

2500

3000

3500

2014 2015 2016 2017 2018

China Europe Ex-USSR India Japan USA Others

Commercial Launch services marketBy launch country (M$)

(c) copyright - reproduction forbidden

6

-

200

400

600

800

1.000

1.200

2014 2015 2016 2017 2018

China Europe Ex-USSR India Japan USA Others

A R E L AT I V E LY N E W ( A N D S T I L L L I M I T E D ) P H E N O M E N O N

T H E E U R O P E A N S I T U AT I O N : B E T W E E NC O M P E T I T I V E N E S S O N E X P O R T M A R K E T S E G M E N T S A N D S AT E L L I T E T R A D E D E F I C I T W I T H T H E U S A …

7

A FEW HINTS ON SATELLITE EXPORTS WORLDWIDE

A brief history of worlwide satellite exports

8

0

100

200

300

400

500

600

700

19

57

19

59

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

Ton

s

Satellite Exports vs Domestic procurement 1957-2018 (mass)

Domestic Markets Export/Import

(c) copyright - reproduction forbidden

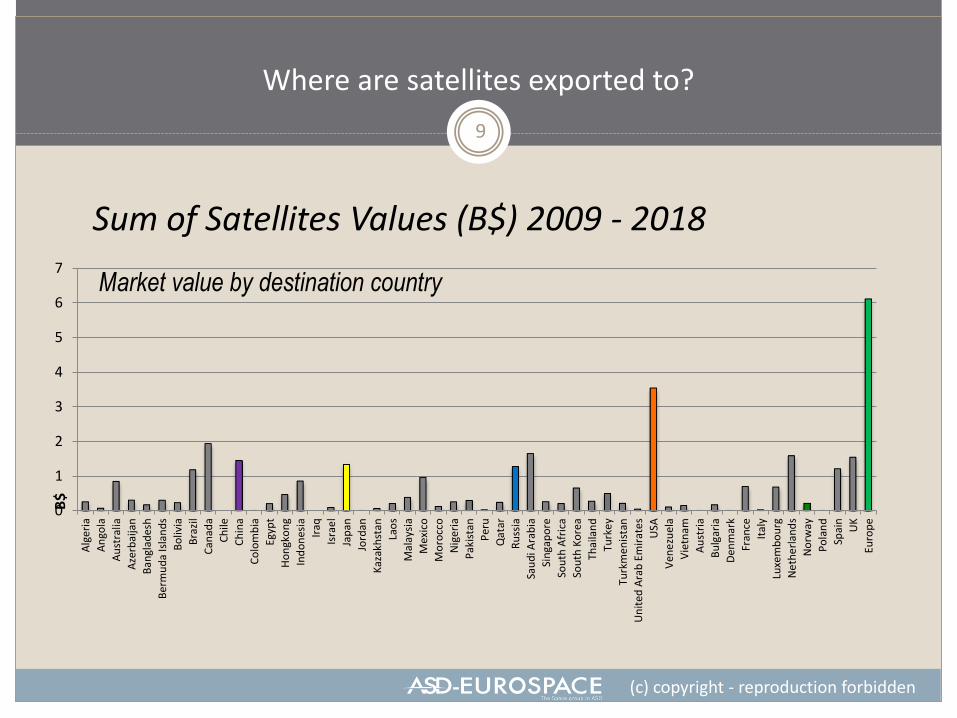

Where are satellites exported to?

9

0

1

2

3

4

5

6

7

Alg

eria

An

gola

Au

stra

lia

Aze

rbai

jan

Ban

glad

esh

Ber

mu

da

Isla

nd

s

Bo

livia

Bra

zil

Can

ada

Ch

ile

Ch

ina

Co

lom

bia

Egyp

t

Ho

ngk

on

g

Ind

on

esia

Iraq

Isra

el

Jap

an

Jord

an

Kaz

akh

stan

Lao

s

Mal

aysi

a

Mex

ico

Mo

rocc

o

Nig

eria

Pak

ista

n

Per

u

Qat

ar

Ru

ssia

Sau

di A

rab

ia

Sin

gap

ore

Sou

th A

fric

a

Sou

th K

ore

a

Thai

lan

d

Turk

ey

Turk

men

ista

n

Un

ited

Ara

b E

mir

ate

s

USA

Ven

ezu

ela

Vie

tnam

Au

stri

a

Bu

lgar

ia

Den

mar

k

Fran

ce

Ital

y

Luxe

mb

ou

rg

Ne

the

rlan

ds

No

rway

Po

lan

d

Spai

n

UK

Euro

pe

B$

Market value by destination country

Sum of Satellites Values (B$) 2009 - 2018

(c) copyright - reproduction forbidden

Satellite trade balance: between strenghths & weaknesses

10

-6 -3 0 3 6 9 12 15 18

USA

Europe

China

Russia (CIS)

Japan

India

B$Imports Exports

-6 -3 0 3 6 9 12 15 18

USA

Europe

China

Russia (CIS)

Japan

India

B$Imports Exports

Sum of S/C Values 1999 – 2008 B$ Sum of S/C Values 2009 – 2018 B$

(c) copyright - reproduction forbidden

Satellite exports: supply & demand synthesis

11

0 5 10 15 20

China Supplier

Europe Supplier

India Supplier

Others Supplier

Russia Supplier

USA Supplier

B$

Satellite export countries and destinations 1999 – 2008 (B$)

China Import

Europe Import

Japan Import

Russia Import

USA Import

Others Import

0 5 10 15 20

China Supplier

Europe Supplier

India Supplier

Japan Supplier

Russia Supplier

USA Supplier

B$

Satellite export countries and destinations 2009 – 2018 (B$)

China Import

Europe Import

Japan Import

Russia Import

USA Import

Others Import

(c) copyright - reproduction forbidden

B E T W E E N A « D E F E N S I V E » A N D A N « O F F E N S I V E » D I M E N S I O N , A T W O - S I D E D A P P R O A C H

S PA C E E C O N O M I C D I P L O M A C Y, A P I L L A R O F A W I D E R E U S PA C E I N D U S T R I A L S T R AT E G Y I N S U P P O R T T O I N D U S T R Y C O M P E T I T I V E N E S S

N E W E U R O P E A N C O M M I S S I O N : A N O P P O R T U N I T Y T O B E E F U P S PA C E E C O N O M I C D I P L O M A C Y - R E L AT E DA C T I O N S

12

TOWARDS AN EU SPACE ECONOMIC DIPLOMACY – RECOMMENDATIONS OF

THE EUROPEAN SPACE INDUSTRY

Eurospace proposals in a nutshell*

13

“Defensive approach”

Tailor-made institutional support

Encourage coordination between institutional stakeholders (DG

GROW, TRADE, DEVCO, CONNECT, EEAS) to help identify export

opportunities and potential existing synergies between the EU and

industry’s targeted customers.

Use of EU R&D programmes

Further support, through EU R&D programmes, to the development of

critical components associated with non-dependence

Set up a flexible instrument under Horizon Europe-space allowing

industry to initiate early contacts with potential governmental

customers

Trade policy instruments

Revise EC guidelines for the elaboration/ negotiation of trade

agreements to make sure that (when relevant) specificities of the

European space industry are taken into account, with the objective to

establish a level playing field

*Towards a « space economic diplomacy », Eurospace position paper, 2017

Eurospace proposals in a nutshell*

14

“Offensive approach”

Tailor-made

institutional

support

Deploy diplomatic efforts, in transparent coordination with national diplomatic efforts, to

provide advocacy for European solutions, open doors and provide support with the local

decision-making bodies / encourage the expression of political support at higher political level

Lead regular “awareness-raising campaigns” within EU delegations involving representatives

from the European space industry

EU development

policy as a

leverage

Promote further synergies between DG GROW and DG DEVCO so that space-based

technologies & services support the objectives of DG DEVCO’s multiannual indicative

programme

Support training of third countries professionals in space-related activities (ground segments,

services centers…)

Promote requests from potential third beneficiary countries of procurement of European

space-related infrastructures

Trade policy

instruments

Reflect on the opportunity to set-up a European export financing credit-like agency to provide

insurance and loans to domestic companies for their export operations

When relevant, include “space” in trade negotiations to ensure a fair treatment of the

European space industry’ on third markets

*Towards a « space economic diplomacy », Eurospace position paper, 2017

Developing space economic diplomacy: in line with the ambitions of the next European Commission…

Economic diplomacy, to be part and parcel of a wider EU spaceindustrial policy?