southern california chapter healthcare financial management association chapter education program #...

TRANSCRIPT

Southern California ChapterHealthcare Financial Management Association

Chapter Education Program # 3

March 18, 2008

Long Term Care Track

Skilled Nursing FacilityAB 1629 Reimbursement Update

Darryl Nixon, CAHF

Mike Harrold, DHCS

Dan Giardinelli, DHCS

Presenter Contact Information

Darryl Nixon, Director of Reimbursement and Data Systems, California Association of Health Facilities (CAHF), [email protected], 916-441-6400, ext. 112

Mike Harrold, Chief, Financial Audits Section-Fresno, [email protected]

Dan Giardinelli, Chief, Financial Audits Section – Burbank,1405 N. San Fernando Blvd., Room 203Burbank, CA 91504, [email protected],818-295-2626

Overview/Historical Perspective

Public Policy Intent Methodology Refresher Fiscal Impact Summary Reporting Issues

– Ongoing– Supplemental Reporting

Other Issues– Rate Development Issues– QA fee Payment/Collection– Audits

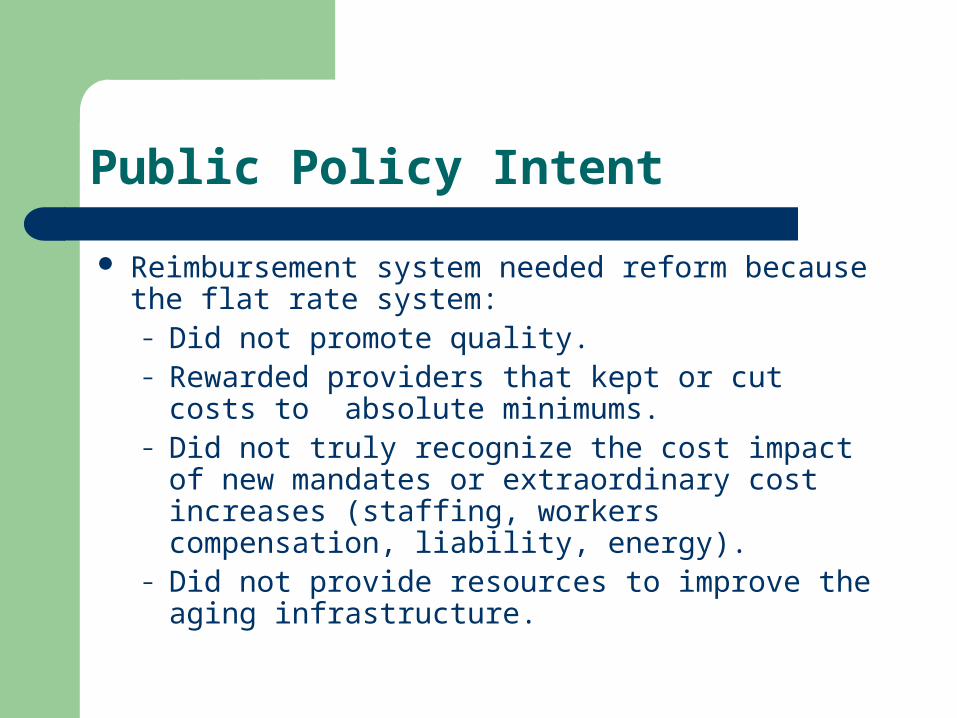

Public Policy Intent

Reimbursement system needed reform because the flat rate system:– Did not promote quality.– Rewarded providers that kept or cut costs to

absolute minimums. – Did not truly recognize the cost impact of new

mandates or extraordinary cost increases (staffing, workers compensation, liability, energy).

– Did not provide resources to improve the aging infrastructure.

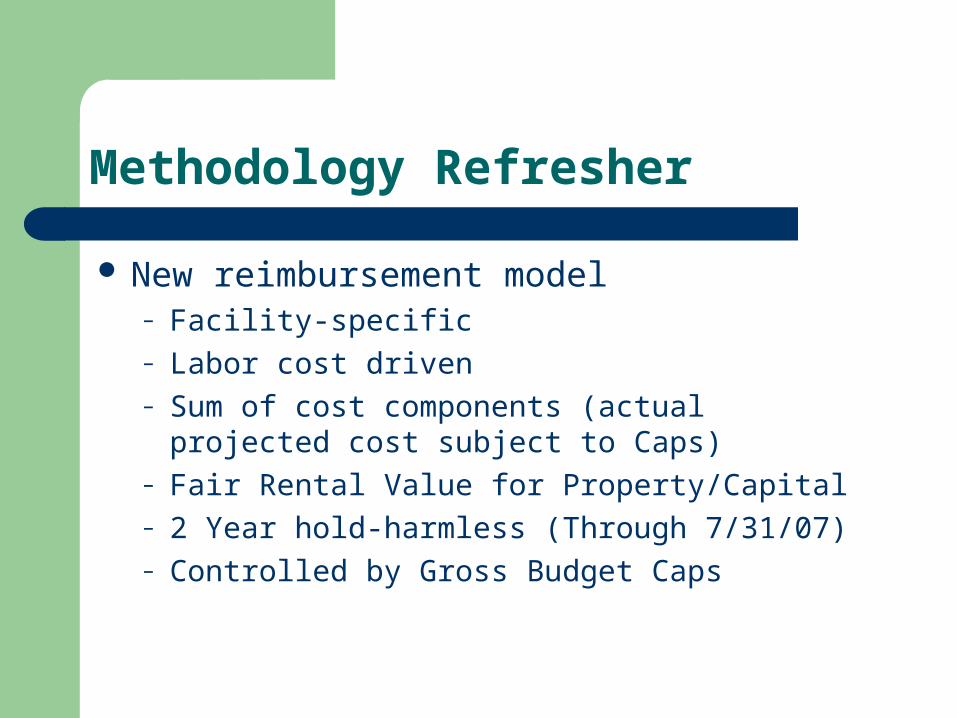

Methodology Refresher

New reimbursement model– Facility-specific– Labor cost driven– Sum of cost components (actual projected cost

subject to Caps)– Fair Rental Value for Property/Capital– 2 Year hold-harmless (Through 7/31/07)– Controlled by Gross Budget Caps

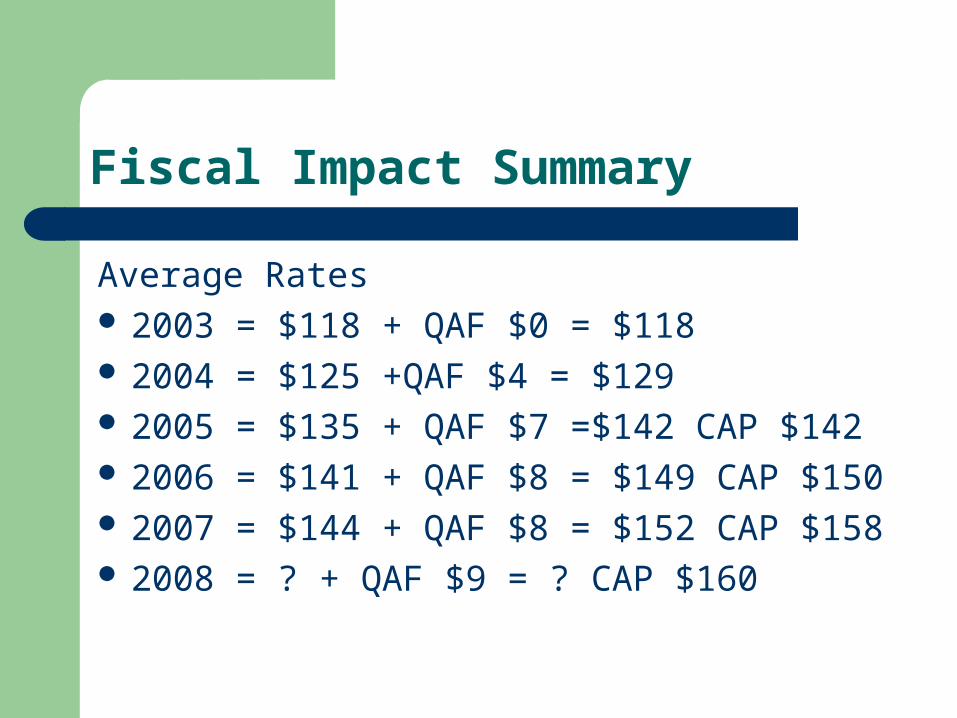

Fiscal Impact Summary

Average Rates 2003 = $118 + QAF $0 = $118 2004 = $125 +QAF $4 = $129 2005 = $135 + QAF $7 =$142 CAP $142 2006 = $141 + QAF $8 = $149 CAP $150 2007 = $144 + QAF $8 = $152 CAP $158 2008 = ? + QAF $9 = ? CAP $160

Reporting Issues

Cost Report Submission– Timeliness– Errors – Amended Reports

Supplemental Reports– Information Required– Timely Submission– Failure to Submit

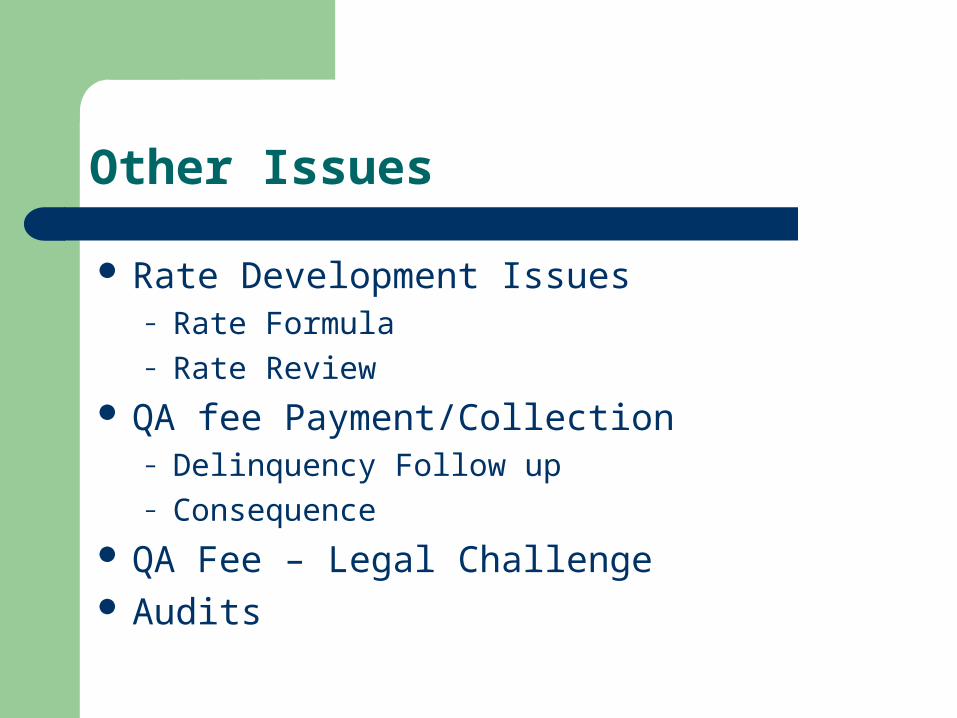

Other Issues

Rate Development Issues– Rate Formula– Rate Review

QA fee Payment/Collection– Delinquency Follow up– Consequence

QA Fee – Legal Challenge Audits

Follow Up Issues

2007/08 Rates– Updating Rates– Retroactive Rate Adjustments– Collection of Overpayments

Share of Cost Corrections– February 20 EDS Notification

DHCS responses to Rate Issues– Subacute

Current Issues

2008/09 Rates– Supplemental Schedules– Labor Supplemental– Rate Projection

Reauthorization of AB 1629– Strategic Issues– Technical Issues

Audits

AB 1629 ReauthorizationStrategic Issues

Current Sunset Date Extension– Minimum 3 to 5 years

Funding– Global Rate CAP (s)

Improve Efficiency in Rate Determination– Cost Reporting– Rate Review (Include Audit Appeal)

Quality Award Rate Enhancement

AB 1629 Technical Issues - General

Current cost report doesn’t meet AB 1629 parameters, thus the supplemental reporting requirements.

AB 1629 Law, State Plan Amendment (SPA,) and Medi-Cal Provider bulletins don’t provide clear guidance.

Audit results impact AB 1629 rates therefore, policy guidance has to be clear.

AB 1629 ReauthorizationTechnical Issues

Resolved– Contract labor clarification– Proper classification of DON and MDS Nurse– Proper classification of Home Office capital costs

Recognition– Insurance issues– Cost Reporting

Unresolved– Liability insurance, Pharmacy consultant fees, FRVS –small

item/equipment capitalization or expense.

Audits

Audit Organization Process Overview Provider Preparation Provider Issues – Audit Perspective Provider Rights

– Ongoing communication– Exit conference– Audit appeal

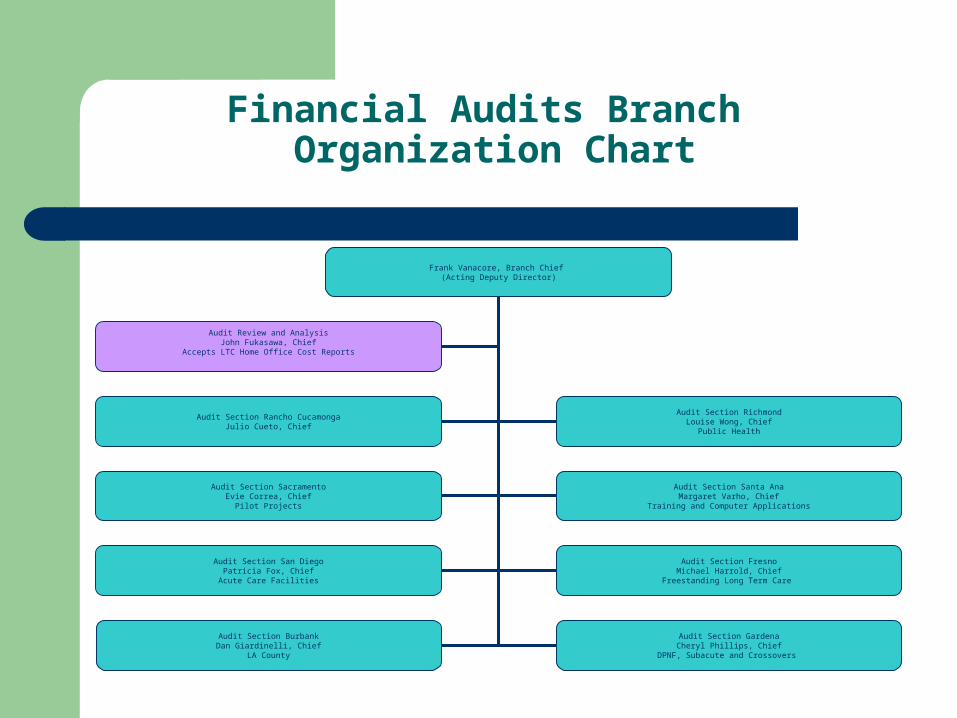

Financial Audits Branch Organization Chart

Frank Vanacore, Branch Chief (Acting Deputy Director)

Audit Section Rancho CucamongaJulio Cueto, Chief

Audit Section RichmondLouise Wong, Chief

Public Health

Audit Section SacramentoEvie Correa, Chief

Pilot Projects

Audit Section Santa AnaMargaret Varho, Chief

Training and Computer Applications

Audit Section San DiegoPatricia Fox, Chief

Acute Care Facilities

Audit Section FresnoMichael Harrold, Chief

Freestanding Long Term Care

Audit Section BurbankDan Giardinelli, Chief

LA County

Audit Section GardenaCheryl Phillips, Chief

DPNF, Subacute and Crossovers

Audit Review and AnalysisJohn Fukasawa, Chief

Accepts LTC Home Office Cost Reports

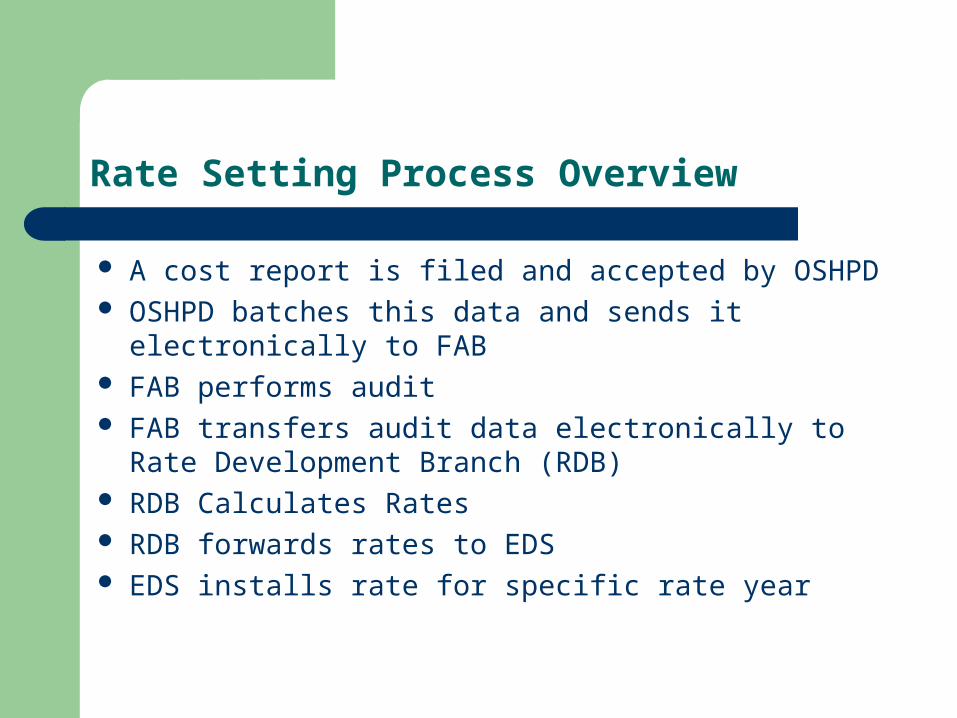

Rate Setting Process Overview

A cost report is filed and accepted by OSHPD OSHPD batches this data and sends it electronically

to FAB FAB performs audit FAB transfers audit data electronically to Rate

Development Branch (RDB) RDB Calculates Rates RDB forwards rates to EDS EDS installs rate for specific rate year

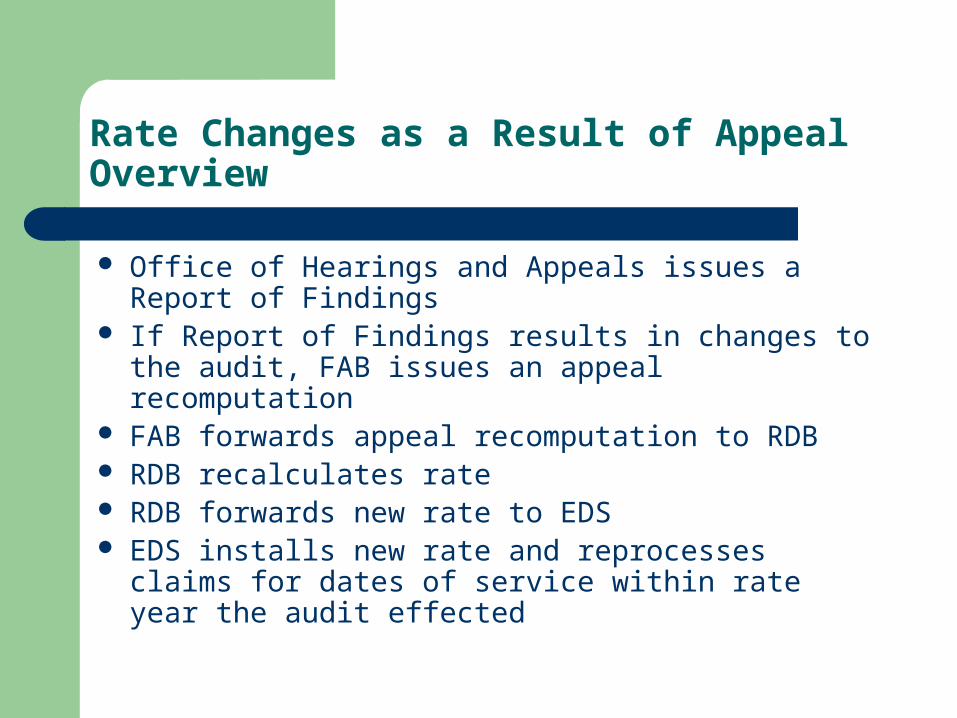

Rate Changes as a Result of AppealOverview

Office of Hearings and Appeals issues a Report of Findings

If Report of Findings results in changes to the audit, FAB issues an appeal recomputation

FAB forwards appeal recomputation to RDB RDB recalculates rate RDB forwards new rate to EDS EDS installs new rate and reprocesses claims for

dates of service within rate year the audit effected

Provider Preparation

We try to accommodate scheduling problems, but we cannot always reschedule an audit because of issuance due dates imposed upon us, thus we will not always be able to agree to a requested rescheduling of the audit.

Provider Preparation

Review the entrance letter and gather the records and materials that are identified. The following are examples:

Financial Statements General Ledger and Working Trial Balance Cash Receipts and Disbursements Journal with

Supporting Documents Working Papers and Supporting Documentation Used

in the Cost Report and/or OSHPD Report Preparation Cost Report Grouping Schedule Payroll Records

Provider Preparation

Census Report Billing Records Medi‑Cal Program Remittance Advice Details

(RADs) Billing Procedures for Share of Cost Charges Chart of Accounts and, if the facility is not using the

account numbers established by the Office of Statewide Health Planning and Development (OSHPD), a cross reference of the facility's account numbers to OSHPD's account numbers and vice versa

Provider Preparation

Please use the contact person identified on the entrance letter if there are any questions or problems; it will facilitate the audit if we can respond to questions or concerns before we go to the field

Timely submission of other requested information during the audit.

Identify contact person who will be available during the audit.

Provider Preparation

Incorporate prior year audit adjustments into current year’s filed cost report.

Freestanding Subacute facilities should properly identify the ancillary charges for the Subacute and SNF.

Provider being prepared for appeals.

Provider Issues

Reimbursement consultants and cost report preparers – You are responsible to ensure that records are

made available to the auditors, not the consultants

– If requested records are not made available the auditor will make an audit adjustment disallowing the relevant costs.

Provider Issues

The LTC Disclosure Report from OSHPD has not yet been revised to reflect the changes resulting from AB 1629

– Make the supplemental worksheets available to the auditors– The number of audit adjustments must go up to

accommodate the AB1629 reclassifications– If possible review the audit adjustments prior to the exit

conference – Carefully review the audit adjustments during the exit

Provider Issues

Cost Shifting From A&G to Skilled Nursing– Medical Directors– Admissions clerks – Software costs and other IT costs– Central Supply personnel – Telephone costs

Provider Issues

Quality Assurance Fees– Please segregate them so that they can be

easily identified by the audit staff Quality Assurance Fees are an add-on and therefore

not reimbursed based on the cost report information The objective of the audit is to segregate QAF fees

from other reimbursable costs

Provider Issues

Liability insurance please keep the following things separately identified– Liability insurance– Trust Bonds – Legal Fees– Finance Charges associated with liability

insurance– Losses and Deductibles

Provider Issues

Daily Rate Items– Please keep legend drugs separate – Please keep separately billable supplies separate– Only include things that are included in the rate

Provider Rights

Ongoing communication Exit Conference

– Title 22, Section 51021 The provider shall be afforded a reasonable opportunity to participate in an exit conference after the conclusion of any field audit or examination of records or reports of a provider…prior to the issuance of the Audit Report.

– The provider must make available to the Department any records which were identified as unavailable for review or missing within 15 calendar days of the exit conference to be included in the Audit Report.

Provider Rights

Informal Appeal Title 22, Section 51022 – A written request (Statement of Disputed Issues)

shall be filed with the Department within 60 calendar days of the receipt of the written notice of the audit or examination findings.

– Usually does not involve lawyers, the provider and the DHCS staff interact freely to resolve issues and support positions

Provider Rights

Formal Audit AppealTitle 22, Section 51024

– An Institutional provider shall have 30 calendar days following the receipt of the written Report of Findings within which to file a request for formal hearing with the Director.

– Usually but not always involves lawyers

Questions?

And

Answers