southeast asia m&a outlook not too hot, not too cold is our poster boy a seller‟s market –5...

TRANSCRIPT

Southeast Asia M&A Outlook Not too hot, not too cold

Ho Han Tsung

Director – Corporate Finance

Deloitte & Touche Corporate Financial Advisory

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 2 M&A: Your Growth Accelerator

Agenda

A quick look from a global perspective

Big picture outlook for 2013

Current buyer / seller trends

The ASEAN Economic Community

Conclusion

A quick look from a global perspective

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 4 M&A: Your Growth Accelerator

Three problem children in the global economy

Source: EIU

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016

Nominal US$ GDP Index at 2010

China

USA

Eurozone

In the medium term, we have reason to be optimistic for at least two out of three

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 5 M&A: Your Growth Accelerator

Inflation and growth

• Loose monetary policy: low interest rates

• Slow growth, low inflation in affluent countries

• Higher growth, higher inflation in emerging economies

Global GDP Growth (%) Consumer prices (% YoY)

Source: IMF staff estimates

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Source: MergerMarket

6 M&A: Your Growth Accelerator

In the midst of a global decline in M&A, APAC mid-market M&A

remains resilient

In 2011, the APAC region saw 2,066 deals come to market, making it the single-

largest region for mid-market M&A by volume and the third by value

-22%

10%

1%

36%

-38% -25%

-

50,000

100,000

150,000

200,000

250,000

Europe NorthAmerica

APAC LatinAmerica

MENA Other

Deal value (US$‟m)

Global deal value fell by 5.6% from US$574bn in 2008 to US$543bn in 2011

2008 2011 2008-2011 change

-24%

-4%

-9%

16%

-48% -31%

-

500

1,000

1,500

2,000

2,500

3,000

Europe APAC NorthAmerica

LatinAmerica

MENA Other

Deal volume

Global deal volume fell by 13.5% from 7,372 deals in 2008 to 6,376 deals in 2011

2008 2011 2008-2011 change

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 7 M&A: Your Growth Accelerator

The picture in Southeast Asia is similar to the rest of APAC

Inbound / domestic Mid Market M&A activity – Southeast Asia

Source: MergerMarket

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Big picture outlook for 2013

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 9 M&A: Your Growth Accelerator

Big picture outlook for 2013

Position in the economic cycle will drive volumes

Liquidity for investment remains strong

Southeast Asia is a strategic growth market…

… Indonesia is our poster boy

A seller‟s market – buyer challenge to make heady economics work

Sustained investments will continue in consumer, financial services, and

energy & resources

1

2

3

4

5

6

Despite the uncertainty in the global economy, corporates need think ahead and

seek growth… Southeast Asia is one region that offers opportunities for growth

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

1. Position in the economic cycle will drive deal volume

10 M&A: Your Growth Accelerator

-10

-8

-6

-4

-2

0

2

4

6

8

10

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GD

P g

row

th (

%)

Real GDP growth (market exchange rates) World vs. ASEAN

Source: EIU

ASEAN‟s GDP growth has been holding up well in the slow global environment

We will generally continue to see lower (but still healthy) GDP growth

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

2. Liquidity for investment remains strong

11 M&A: Your Growth Accelerator

Source: IMF

• Western public finances and financial institutions: negative

• MNCs: profitability and cash levels high, low gearing, strong equity prices

• Regional corporates: same or better

Global Liquidity (I

n b

illi

on

s o

f U

.S.

do

lla

rs;

GD

P-w

eig

hte

d;

qu

art

erl

y d

ata

)

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

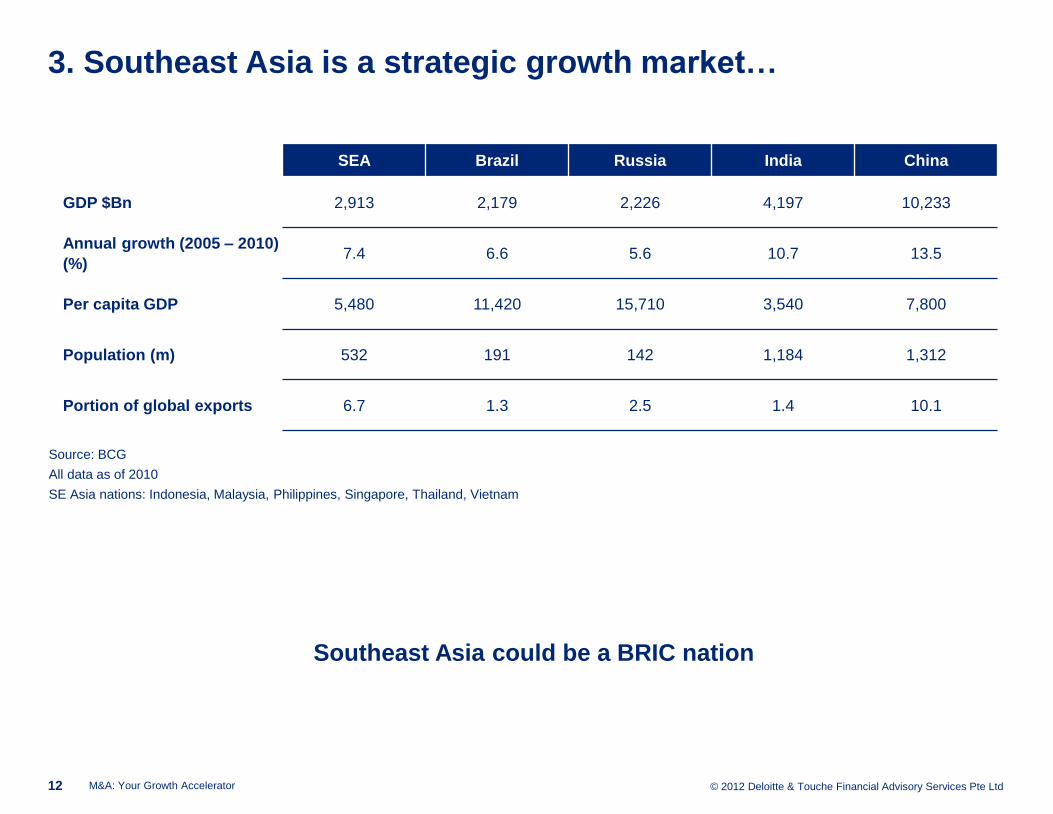

3. Southeast Asia is a strategic growth market…

12 M&A: Your Growth Accelerator

Source: BCG

All data as of 2010

SE Asia nations: Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam

Southeast Asia could be a BRIC nation

SEA Brazil Russia India China

GDP $Bn 2,913 2,179 2,226 4,197 10,233

Annual growth (2005 – 2010)

(%) 7.4 6.6 5.6 10.7 13.5

Per capita GDP 5,480 11,420 15,710 3,540 7,800

Population (m) 532 191 142 1,184 1,312

Portion of global exports 6.7 1.3 2.5 1.4 10.1

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

4. … Indonesia is our poster boy

13 M&A: Your Growth Accelerator

Indonesia today

• #16 largest economy in the world

• 45 million members of the consuming

class

• 53% of the population in cities

producing 74% of GDP

• 55 million skilled workers in the

Indonesian economy

Source: McKinsey

A $0.5 trillion market opportunity today will grow to $1.8 trillion in 2030

Indonesia in 2030

• #7 largest economy in the world

• 135 million members of the

consuming class

• 71% of the population in cities

producing 86% of GDP

• 113 million skilled workers in the

Indonesian economy

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

5. A seller‟s market – buyer challenge to make heady

economics work

14 M&A: Your Growth Accelerator

Source: MergerMarket

Limited availability of quality assets is resulting in frothy valuations

Outsized demand for regional acquisitions is leading to price rises

50

55

60

65

70

75

80

85

90

95

100

2005 2006 2007 2008 2009 2010 2011

Mean

deal

siz

e (

US

$m

per

deal)

Average mid-market M&A deal sizes – Southeast Asia

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

-

5,000

10,000

15,000

20,000

25,000

30,000

Consumer FinancialServices

Energy &Resources

Industrials Real Estate TMT Otherservices

Construction Medical Agriculture

US

$m

Southeast Asia M&A Deals (YTD Oct 2012)

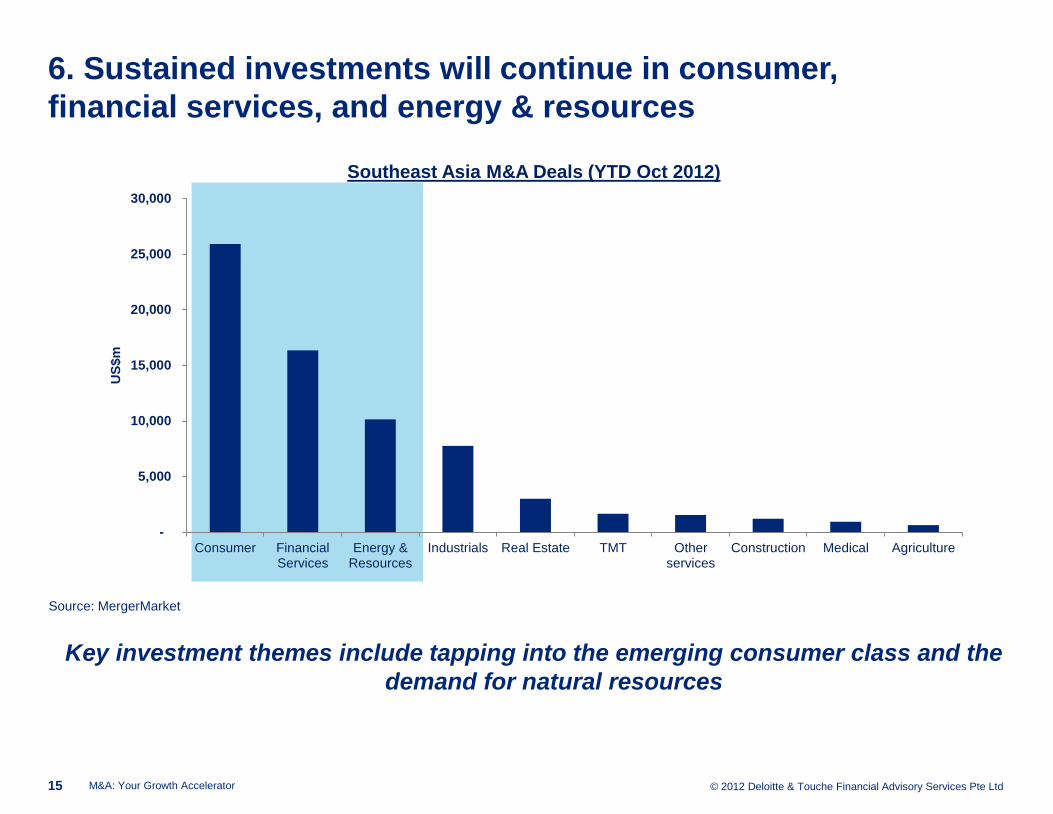

6. Sustained investments will continue in consumer,

financial services, and energy & resources

15 M&A: Your Growth Accelerator

Source: MergerMarket

Key investment themes include tapping into the emerging consumer class and the

demand for natural resources

Current buyer / seller trends

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 17 M&A: Your Growth Accelerator

Southeast Asian Mid-Market buyers and sellers

Buyers

• MNCs from developed markets with low domestic growth potential (e.g. US,

Europe, Japan & Korea)

• Regionals

• Chinese State-Owned Enterprises (SOEs) are also looking to acquire out of

China in order to gain access to resources supporting their current growth

• Global and Regional Private Equity: challenging environment to compete

against strategics

Sellers

• MNCs disposing their mid-market non-core businesses

• Private Equity

• Small-to-mid-sized domestic players; often family-owned

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 18 M&A: Your Growth Accelerator

Buyer behaviour highlights

Portfolio review

• Core vs. Peripheral : driving buy-side & sell-side M&A

Deal sizes

• Shift from transformatory deals towards mid-market deals

Corporates are playing globally

• Making multiple acquisitions concurrently

Stretched corporate development resources

• Having to focus on quality assets

• Real need for intermediation

1

2

3

4

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 19 M&A: Your Growth Accelerator

Seller issues

Succession issues

• Prevalent in small-to-mid-sized family businesses owned by baby

boomers with generation X & Y offspring

Globalisation challenge

• Small-to-mid-sized businesses without critical mass finding it difficult

to compete with big global players

Governance gap

• Small-to-mid-sized sellers vs Big MNC buyers

Value / pricing gap

• Seller vs Buyer value expectations

1

2

3

4

The ASEAN Economic Community

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

An intent in 4 parts ~ a single market; a highly competitive region; a region with

equitable economic development; and fully linked into the global economy

What does economic integration mean?

21 M&A: Your Growth Accelerator

5 Steps

Free flow of

goods

Free flow of

services

Free Flow

of Skilled

Labour

Free flow of

capital

Free flow of

investment

Single Market and Production Base

It may will not happen by 2015, but it should be on the investment agenda

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 22 M&A: Your Growth Accelerator

Why does it matter?

It‟s necessary to sustain growth

• Historically, diversity has been Southeast Asia‟s dominant characteristic

• The economic potential of Southeast Asia is the next pillar of growth in Asia;

but integration is a necessary condition to make that potential real

It will bring substantial net economic benefit

• European Union experience is that integration has sustained positive effects

on levels of FDI; share of FDI increased from 30% (‟80s) to 50% („90s after

single market introduction)

• For M&A guys, the real story is around industrial re-structuring & rationalization

FDI & rationalisation mean profound change for corporates & a substantial increase

in M&A across the region in the medium term

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Who will lead?

• Corporates from Singapore, Thailand & Malaysia will likely lead

• Those in Indonesia and Philippines do not see the pressing need yet

23 M&A: Your Growth Accelerator

Conclusion

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd 25 M&A: Your Growth Accelerator

Conclusion

• There have been tough times in the global economy, and it has impacted deal

flow in Southeast Asia (to a lesser extent)

• We see continued investments into Southeast Asia driven by cashed-up

corporates seeking growth

• The Asian Economic Community is a significant opportunity for M&A through

FDI and rationalization

It‟s a good time to be sell side with a quality asset

On buy side, patience pays when allied with boldness & discipline

Doing Deals in Southeast Asia

Common issues and possible solutions

Keoy Soo Earn, Partner

Leader – M&A Transaction Services and Valuation Services

Deloitte Southeast Asia

M&A life cycle

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

28

Introduction to M&A life cycle

Each of the phases requires critical decisions to be made. Due

diligence is one of several phases along the M&A lifecycle

Client involvement

Divestiture

Integration Due diligence

Transaction execution Target

screening

M&A

strategy

Merger

strategy

development

Target

screening and

identification

Preliminary

due

diligence

Synergy and

value driver

quantification

Implementation

and transaction

closing

preparation

Definitive

due

diligence

Negotiation

of letter of

intent Negotiation

of final

transaction

Closing and

execution of

implementation

plan

Board or steering

committee

approval

Completed

letter of intent

Term

sheet

Executed

purchase

agreement

Transfer of

ownership/

closing

documentation

“On-the-ground” Deloitte specialists

Strategy

specialists

Industry

specialists

Valuation

specialists

Accounting/Tax

specialists Operations

specialists IT

specialists

HR

specialists

Integration

specialists

Implementation planning

M&A: Your Growth Accelerator

M&A strategy

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A strategy

30 M&A: Your Growth Accelerator

M&A strategy

Growth strategy

Business strategy

Corporate strategy

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Determining your Growth Strategies

31 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Acquisitions versus organic expansion

32 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

33 M&A: Your Growth Accelerator

Exis

ting

New

M

ark

ets

Client X Target

Future

Client X

Acquire / complement capabilities Gain competencies in key areas

Access alternative channels or move

forward in the value chain

First move has deal pricing advantage

Filling gaps

Client X Target

Future

Client X

New Segments Enter new market

Acquire new capabilities

Extend brand

Expanding segments

Client X Target

Future

Client X

Extend geographically Enter new markets by location

Regional service / operations depth

High concentration of small / mid-side

cases

Build scale

Expanding footprint

Client X Target

Future

Client X

Capture market share Maintain market leadership

Build scale

Dominate segments

Force competitors to scramble

Building on strength

Client X Target Future

Client X Target Target(s)

Strong base operations and

integration skills

Lower costs through

economies of scale

Consolidate Small Players Fragmented industry

Uneconomical small players

Rolling up the “tail”

Existing Capabilities New

Rationale for acquisitions

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 1 in Southeast Asia

Strategic Partner, for who?

34

• Strategic fit to your expansion plan

• Reliable partner to navigate local business

environment

• Good distribution network for your products

Are you your local partner‟s

Strategic Partner?

M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 2 in Southeast Asia

Maintaining confidentiality

35

• Attitude towards confidentiality is far more relaxed

• Be selective in disseminating information

• Signing NDA doesn‟t mean information will be

treated confidentially

Be prepared to manage if

information leaks

M&A: Your Growth Accelerator

Pricing the deal

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

“Price is what you paid.

Value is what you get.”

Warren Buffett

37 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

• Improve sales

• Reduce cost

• Improve productivity

• Improve capital structure, etc

Intrinsic value

• Access new markets

• Access to know-how

• Economies of scale, etc

Synergistic value

• Forward or backward integration

• Block competitors

• Minimise potential infringement, etc

Strategic value

Rationale for acquisitions in value terms

38 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

39

No Transaction

No Transaction

Transaction

Transaction

value

Transaction

value

range

Acquirer

upper limit

Acquirer's

Investment value

Acquirer

lower limit

Vendor‟s

Investment value

Vendor

lower limit

Vendor

upper limit

Different owners perceive value differently

Investment values and pricing limits

Upper

limit

Lower

limit

M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

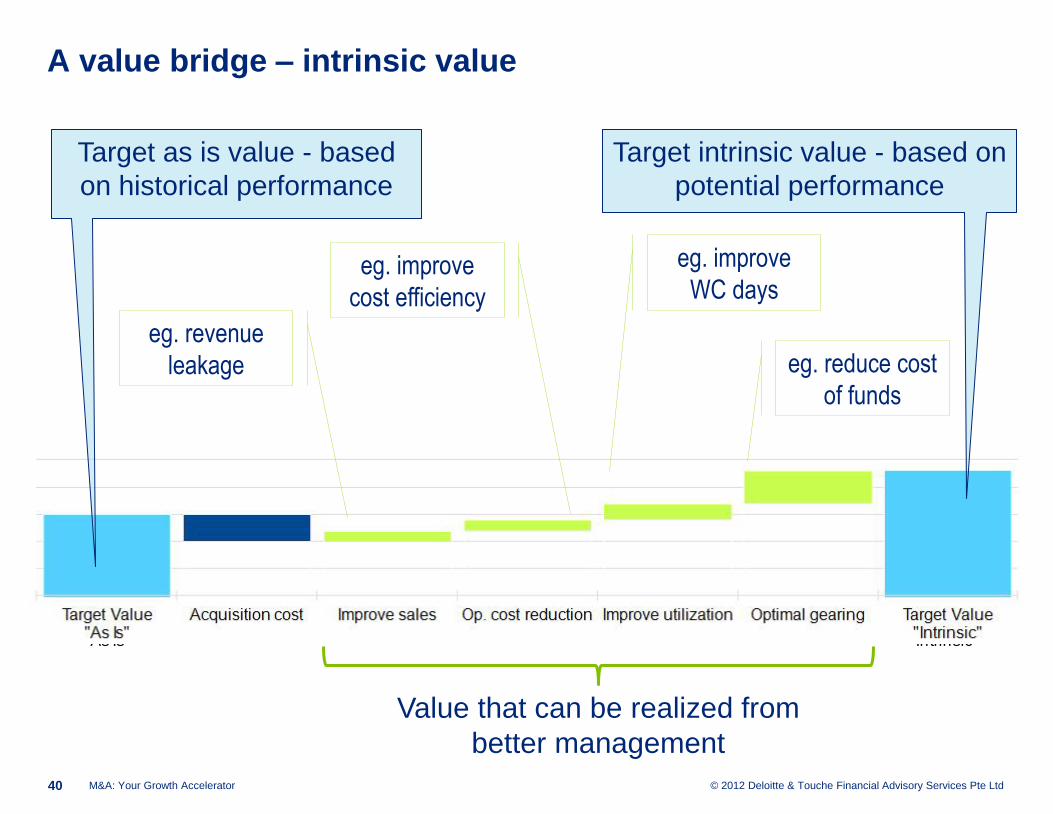

A value bridge – intrinsic value

40

Target Value "As Is"

Acquisition cost Improve sales Op. cost reduction Improve utilization Optimal gearing Target Value "Intrinsic"

Value that can be realized from

better management

M&A: Your Growth Accelerator

Target as is value - based

on historical performance

eg. revenue

leakage

eg. improve

cost efficiency

eg. improve

WC days

Target intrinsic value - based on

potential performance

eg. reduce cost

of funds

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

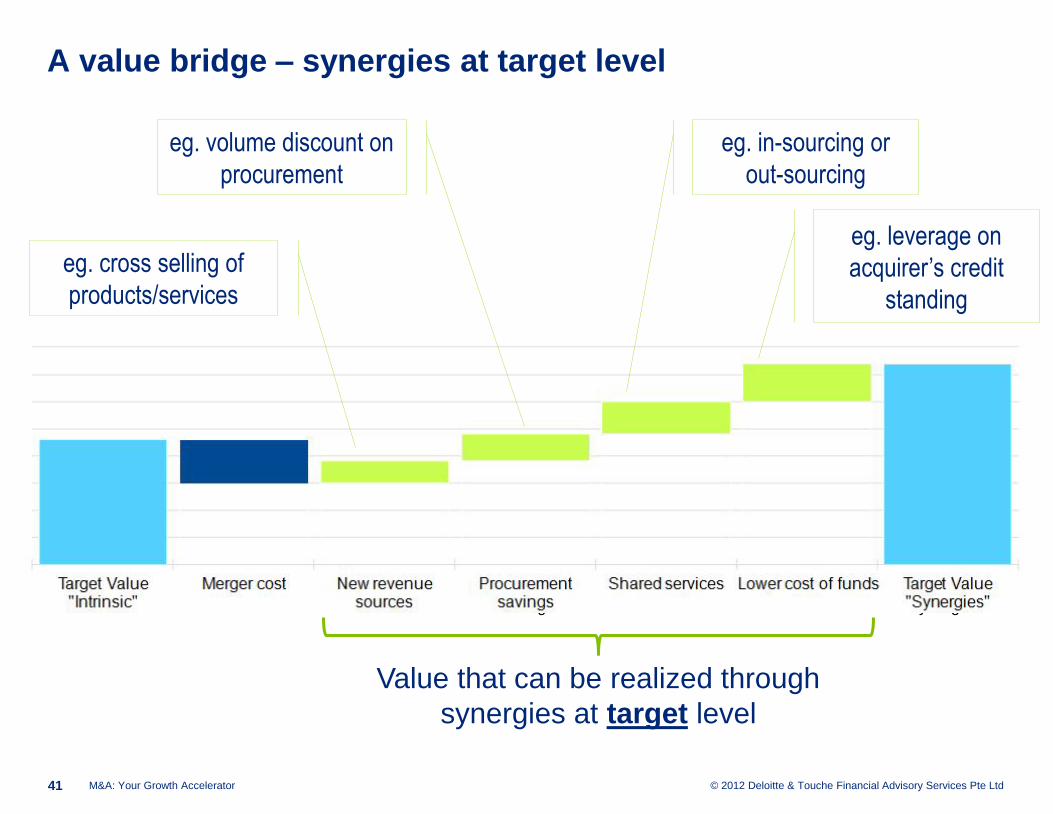

A value bridge – synergies at target level

41

Target Value "Intrinsic"

Merger cost New revenue sources

Procurement savings

Shared services Lower cost of funds Target Value "Synergies"

Value that can be realized through

synergies at target level

M&A: Your Growth Accelerator

eg. cross selling of

products/services

eg. volume discount on

procurement

eg. in-sourcing or

out-sourcing

eg. leverage on

acquirer’s credit

standing

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

A value bridge – acquirer‟s perspective

42

Target Value "Synergies"

Retrenchment cost

New revenue sources

Procurement savings

Shared services cost

Value to Acquirer

"Synergies"

Improve pricing

Increase market share

Value to Acquirer

"Strategic"

Strategic value that

can be realized

M&A: Your Growth Accelerator

Value that can be realized through

synergies at acquirer level

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 3 in Southeast Asia

Everything is for sale if the price is right

43

• At what price?

• Highest and most attractive bid will secure the

deal?

• Some assets seem to be forever for sale but

never get sold

Understand the motive of

the vendor is critical

M&A: Your Growth Accelerator

Due diligence

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

45 M&A: Your Growth Accelerator

What our clients look for…

• Early notice of deal breakers

• Integrity of the information included in

Information Memorandum, management

presentations and dataroom

• Identify information that can be used to

assess value and negotiate deal price

• Identify risks that need to be managed

• Assess potential post acquisition accounting

impact

• Provide advice on matters that will need to be

addressed post transaction

• Guidance on structuring of a deal

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

46 M&A: Your Growth Accelerator

Deal characteristics affect due diligence scope

Acquirer - strategic vs financial

Vendor - corporate vs PE

Target - locations, private vs public

Asset vs stock purchase

Vendor vs new share

Buyout vs growth

Pricing mechanism

Integration plan and exit strategy

Quality of information

Target- standalone vs carve-out

No one size fits all due

diligence

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

47 M&A: Your Growth Accelerator

Due diligence

Financial & accounting

Operations

Human resource

Taxation Commercial

& Market

Legal & regulatory

Information technology

Due diligence scope

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

48 M&A: Your Growth Accelerator

The scope of due diligence is usually

a balance of costs and risks

Target‟s jurisdiction

Target‟s industry

Buyer‟s familiarity of Target & its management

Future financial losses Due diligence costs

Balancing due diligence costs versus transaction risks

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

49 M&A: Your Growth Accelerator

Clarity…

Past performance, financial position, etc

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

50 M&A: Your Growth Accelerator

Quality of Earnings

Normalized EBITDA Bridge – Year on Year

EBITDA FYX1 Price increase Operating cost saving

New product line (net)

Volume reduction Production cost increase

EBITDA FYX2

Sustainability of

earnings

Price setter

or taker? What drives

the cost

savings?

Prospect?

Market size? Reason for reduction?

Lost of market share?

Controllable? Pass

on to customers?

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 4 in Southeast Asia

Multiple books – Which one to use?

51

• Availability and quality of information

• Different books serve different purposes

• What‟s real and what‟s not

• Unrecorded liabilities

Look beyond financial numbers!

M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 5 in Southeast Asia

Acceptable business practices… or are they?

52

• Norms of acceptable business practices vary

from country to country.

• What constitutes bribery in US or Europe may

be acceptable business practices in certain

Southeast Asia countries.

Don‟t assume,

verify specific transactions

M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 6 in Southeast Asia

Company is mine; My expenses is the company‟s

53

• Owner-managed business may treat non-

business or private expenses as company

expenses

• Selected business expenses may be tagged as

personal expenses for pricing purposes

• May be construed as willful incorrect claim of

expenses or evasion of taxes

Dissecting personal expenses

from business

M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

54 M&A: Your Growth Accelerator

Visibility…

Future performance, financial impact, exit, etc

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

55 M&A: Your Growth Accelerator

EBITDA – Which EBITDA?

Clarity

FC million FY08 FY09 Q2LTM Out-turn Run-rate

Mgmt Reported EBITDA xx xx xx xx xx

Due diligence adjustments xx xx xx xx xx

Adjusted EBITDA xx xx xx xx xx

Normalisation adjustments xx xx xx xx xx

Normalised EBITDA xx xx xx xx xx

Normalised EBITDA –

constant currency xx xx xx xx xx

Pro-forma adjustments xx xx xx xx xx

Normalised pro-forma

EBITDA xx xx xx xx xx

Normalised pro-forma EBITDA

– constant currency Visibility

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Acquisition

implied

enterprise

value of

FC 1.5 mil

PPA process

Acquisition accounting – Financial Impact Analysis

Impact on balance sheet

B/S of target before acquisition

FC „000

Non current assets 500

Current assets 600

Current liabilities (400)

Net operating

assets

700

Financed by:

Total debts 300

Shareholders fund 400

Invested capital 700

B/S of target after acquisition

FC „000

Goodwill 350

Non current assets (FV) 400

Intangible assets (FV) 300

Current assets (FV) 650

Current liabilities (FV) (400)

Contingent liabilities

(FV)

(50)

Net operating assets 1,250

Financed by:

Total debts (FV) 250

Shareholders fund 1,000

Invested capital 1,250

56 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

PPA Process

Amortisation of

intangibles

and other fair

value

adjustments

Acquisition accounting – Financial Impact Analysis

Impact on acquirer‟s P&L

Target‟s expected P/L

FC „000

EBITDA 50

Depreciation (15)

Amortisztion (2)

Impairment --

EBIT 33

Interest (10)

Taxation (5)

NPAT 18

Target‟s expected P/L post

acquisition

FC „000

EBITDA 50

Depreciation (12)

Amortisation of

Intangibles

(47)

Impairment --

EBIT (9)

Interest (10)

Taxation (5)

NPAT (24)

57 M&A: Your Growth Accelerator

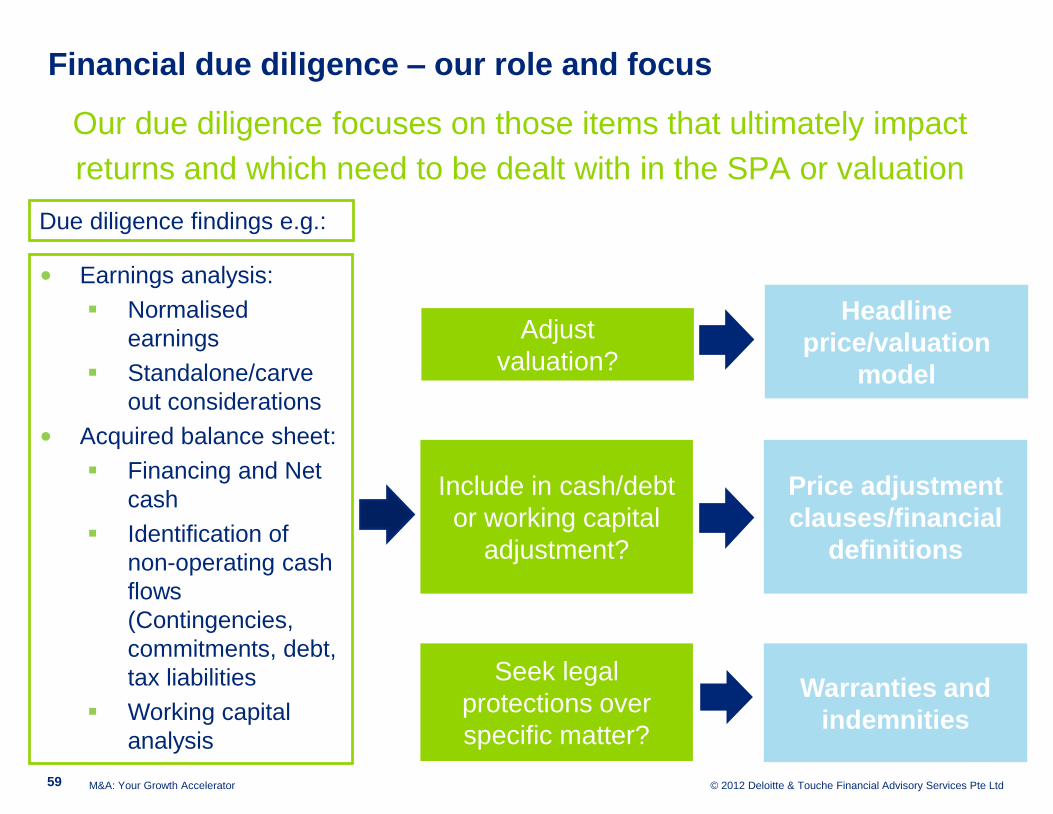

SPA - Accountants perspective

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Our due diligence focuses on those items that ultimately impact

returns and which need to be dealt with in the SPA or valuation

• Earnings analysis:

Normalised

earnings

Standalone/carve

out considerations

• Acquired balance sheet:

Financing and Net

cash

Identification of

non-operating cash

flows

(Contingencies,

commitments, debt,

tax liabilities

Working capital

analysis

Price adjustment

clauses/financial

definitions

Warranties and

indemnities

Due diligence findings e.g.:

Headline

price/valuation

model

Adjust

valuation?

Include in cash/debt

or working capital

adjustment?

Seek legal

protections over

specific matter?

Financial due diligence – our role and focus

59 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

60 M&A: Your Growth Accelerator

Operating

Intangible

assets

Net

working

capital

Non-

current

tangible

assets

Financing

Net debt

Equity

Accounting view

Non-

current

assets

Current

assets

Current

liabilities

Equity

Non-

current

liabilities

Invested

capital or

enterprise

value

Debit Credit

Financial aspect of the target

Business perspective

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

61 M&A: Your Growth Accelerator

Financial due diligence scope

Return

Net operating profit

Revenue growth

Volume

Price

Product mix Cash/EBITDA

margin

Effective tax paid

Net operating assets

Working capital

Capital assets

Quality of assets

Quality of

earnings

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

62 M&A: Your Growth Accelerator

Financial due diligence scope

Net operating assets

Financing

Shareholders‟ equity

Convertible bonds

Bank loans

Capital assets

Net working capital

Intangible assets

Financing & net

debt

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

63 M&A: Your Growth Accelerator

Quality of net assets

Recorded assets

- valuation / impairment

Fixed Assets

• Utilisation rate

• Fully depreciated/idle assets

• Growth vs Replacement capex

• Capex commitments

Working capital

• Narrow vs Broad definition

• Include cash? Trapped cash

• DSO, DPO, Inventory Turns

• Seasonality of sales vis-à-vis production

plan

• Target Working Capital

• Bad debt/obsolete inventories experience

• Capitalisation policies - CWIP

• Costing methodologies

Operating leases

• Favorable or onerous

There could be

hidden value

To consider including in

net debt definitions

Operating

Fixed assets

Working Capital

Operating leases

Contacts or agreements

Intangible assets

Non-operating

Surplus Assets

Once-off liabilities

Penalty charges

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

64 M&A: Your Growth Accelerator

Two different approaches

Purchase price adjustments

(e.g. Completion Accounts

and Earn Outs)

Fixed price

(including „locked box‟)

SPA - Two approaches

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

Adjustments to enterprise value should depend on valuation assumptions

$m

Enterprise value X

Plus $ for $ for Cash X

Less $ for $ for Debt (X)

Plus $ for $ Actual Working Capital X

Less Normal Working Capital (X)

Other? X

Price payable for equity $Xm

Net debt &

non- operating cash

flows

Working capital

eg. DCF, normalised

EBITDA: „multiple‟

impact

Capex,

guarantees, etc

Purchase price

– cash free, debt free basis

65 M&A: Your Growth Accelerator

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

66 M&A: Your Growth Accelerator

Determining equity value

Some value issues to consider: cash and debt

• Cash not available? e.g. „Trapped cash‟

• Cost associated with liquidation/repatriation?

• Group structure (non wholly owned subsidiaries:

100% or MI%?)

• Nominal ledger versus bank statements

(important for completion accounts)

Definition

of „cash‟

• Financial debt

• Corporation (income) tax

• Deferred income?

• Accounting does not recognise many liabilities

until trigger point is reached and therefore all

“debt” items may not be visible

• Any future cash costs excluded from EBITDA

(finance leases, provisions, deficits)

Definition

of „debt‟

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

67 M&A: Your Growth Accelerator

Determining equity value

What is an appropriate working capital „target‟?

Estimated

Closing

WC high point

Funding

required

Understanding working capital is important for both pricing and funding purposes

WC low point

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

68 M&A: Your Growth Accelerator

Determining equity value

Value considerations: working capital

• Time period: consider seasonality and also intra-month (can be

significant)

• Removal of cash or 'debt' like items (capex, deferred income, tax, etc)

• Remove non-trade (e.g. inter-company balances often distort trends) and

one offs

• Adjust for expected or recent changes in terms of trade?

• Judgement areas:

‒ Valuation methods – e.g. inventory, calculation of rebates and trade

discounts

‒ Provisions and allowances – e.g. inventory, debtor recoverability,

contingencies

‒ Revenue recognition

„Normal‟

There is

no magic

formula…

• Value of normal working capital is a key value

issue

• For pricing purposes, the Purchaser wants to

have a target as high as possible (more positive,

less negative)

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

69 M&A: Your Growth Accelerator

Price mechanisms

Price adjustment mechanisms – causes of dispute

Causes of disputes: areas to avoid!

• Accounting policies: failing to set a clear order of precedence

between the bases/getting order wrong

‒ Beware: “GAAP APPLIED ON A CONSISTENT BASIS”

• Not specifying policies/values for material judgmental items

(e.g. impairment of fixed assets, provisions, deferred tax)

• Specifying policies that are too vague/imprecise e.g. „general‟

provisions, loose wording

Disputes can be HUGE and COSTLY

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

70 M&A: Your Growth Accelerator

Price mechanisms

Price adjustments: Completion accounts

Some myths:

• „It‟s just process‟

‒ There is real $ for $ value at stake

• „Accounts show a “true or accurate position”‟

‒ They are inherently judgmental

‒ There will be a range of reasonableness for most balance

sheet values

‒ Direct conflict of interest between the parties

• „The auditors prepare the completion accounts/ We will let the

accountants sort it out‟

‒ They don‟t (or shouldn‟t)

‒ Should be parties responsibility – with the helps of their

advisers

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

71 M&A: Your Growth Accelerator

Price mechanisms

Earn out arrangements

Advantages

• Tool to keep key talent

• Defers cash consideration

payable

• Can bridge expectation gap on

value BUT…

Dangers

• Breakdown in trust

• Earnings may be manipulated

where a multiple is payable

• May prevent synergies

• Short term profitability focus

• Succession planning issues

Factors to consider:

• Same as Completion accounts

but WORSE

• “Shunting” of revenues and

costs between period and

entities: focus on accounting

policies for income items

• Calculation of payment

• Changes in accounting policy

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

M&A Lie No. 6 in Southeast Asia

Right pocket or left pocket?

72

• Common to have related party transactions

• Different minority shareholders in different

related entities

• Competing related entities

Alignment of interest is critical

M&A: Your Growth Accelerator

73 Deloitte PowerPoint timesaver – September 2011

Running out of time!!!

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

74 M&A: Your Growth Accelerator

Structuring issues

Deal issues

Valuation issues SPA issues

Accounting issues Post acquisition

issues

Mechanisms to manage risk & extract hidden value

Managing risk, extracting value

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd

75 M&A: Your Growth Accelerator

Conclusion - Summary

Business

model Risk & value

Clear

purpose

Controlled

process

Proper management of the

process

Manage risks, extract

values

Understand the deal intent,

transaction structure & exit

plan

Assess and validate the target

business model

Provide visibility on future

performance

Obtain clarity of past

performance

Clarity Visibility

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent

entity. Please see www.deloitte.com/sg/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150

countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte has in the region of

200,000 professionals, all committed to becoming the standard of excellence.“

© 2012 Deloitte & Touche Financial Advisory Services Pte Ltd