south carolina’s state optional retirement program focus ... · start planning for a comfortable...

TRANSCRIPT

Focus on your futurePlan your retirement

South Carolina’s State Optional Retirement Program

* “MetLife” refers to Metropolitan Life Insurance Company and its affiliates.

** Interest rates will vary. The Fixed Account Option guarantees are subject to the financial strength and claims-paying ability of Brighthouse Life Insurance Company.

The amounts allocated to the variable investment options of your account balance are subject to market fluctuations so that, when withdrawn or annuitized it may be worth more or less than its original value.1 Prior to investing, please review each Fund’s prospectus for information about investment risks, fees, expenses and other important disclosures

Start planning for a comfortable retirement.The State ORP enables you to control your retirement funding options and to select the retirement plan that best meets your specific long-term needs. To help you take full advantage of all the benefits that the State ORP has to offer, we are pleased to provide you with a State ORP information kit. Here, you will find easy-to-understand information about your potential State ORP account including resource information on the funding options.

Funding options to help you build your State ORP account Your employer makes a variety of fixed and variable funding options available to you through MetLife:

• Mutual Fund Select Portfolios (MFSP) offers a wide array of non-proprietary, no-load and load-waived Funds from well-known mutual fund families across a range of asset classes and risk levels, to appeal to every type of participant - from conservative to the aggressive.1 You choose how you want to allocate your plan contributions among a variety of Funds offered in your retirement savings plan, based on your individual risk tolerance and investment style. Then, you can monitor your Funds and adjust as your goals change over time. The full Fund lineup can be found on www.metlife.com/scorp.

• Brighthouse Life Insurance Company offers the Gold Track Select Registered Fixed Account Option, a fixed annuity contract, which provides a guaranteed interest rate.**

Enrolling in South Carolina’s State ORP is easy. You may choose one of the two ways to enroll:

• By mail. After reading through the enclosed material, complete and mail MetLife’s State ORP enrollment form. Also, you must submit the State Form 1100 to your employer along with a copy of the Enrollment/Participation Agreement Form, or

• By phone. Contact David Johnson at 980-260-5175 to obtain the contact information for the financial representative in your area. Your representative will sit down with you, explain the benefits available in the State ORP and review your funding options.

We hope this information kit provides you with an even greater understanding of South Carolina’s State Optional Retirement Program and empowers you to take full advantage of this important benefit.

Again, welcome and thank you for your interest in the State ORP.

Welcome

Congratulations on your new career, and welcome to an alternative retirement investment opportunity available to you: South Carolina’s State Optional Retirement Program (“State ORP”). MetLife* is proud to have been selected by the South Carolina Public Employee Benefit Authority as one of the approved providers for the retirement savings program.

Please visit www.metlife.com/scorp for fund options, performance and prospectuses.

2

Why choose the State Optional Retirement Program?There can be many benefits to choosing the State ORP. Here are a few:

You are 100% vested in your State ORP account, including the part your employer contributes on your behalf.

Your State ORP savings are 100% portable if you permanently leave to pursue a new career opportunity. Most Americans have several different jobs over their lifetime, making portability an important benefit.*

You control your investment choices and your retirement destiny.

For more detailed information, please review the “Select Your Retirement Plan” brochure. The brochure includes an overview of the State ORP, a defined contribution plan, and a comparison to the South Carolina Retirement System (SCRS), a defined benefit plan. The brochure is available through your employer’s benefits office, from the SCRS, on the Internet at www.peba.sc.gov, or from your State ORP fund provider.

The website also contains a benefits comparison calculator which can show you how much retirement savings you could accumulate in the State ORP based on using hypothetical investment returns and other assumptions.

* Because a distribution is subject to ordinary income taxes and a payment before age 59½ may incur an additional 10% Federal income tax penalty, you may prefer to make a direct rollover to another eligible retirement plan, which includes an Individual Retirement Account or Annuity (IRA).

Life Settlement AccountHelps employeesmake confident

decisions

Making a choice between these different plans is an important decision. You should carefully consider all available information, together with your needs and preferences. While we’re pleased to help you consider information, this brochure should not be construed as tax or legal advice.

South Carolina’s State Optional Retirement Program 3

Features of your plan Am I eligible to participate in the plan?You are eligible to participate in your Plan upon date of hire if you are at least 21 years of age.

What are the benefits of pre-tax savings?Contributing to the Plan in pre-tax dollars is a powerful advantage because it reduces your current taxable income every year and your contributions and earnings are not taxed until you withdraw them. It is also easy. Your contributions will be automatically deducted from your paycheck and deposited into your account.

How much can I contribute?You must make pre-tax contributions of 9.00% of your eligible pay. For employees with a Date of Membership after January 1, 1996, the calendar year 2018 compensation limit under Internal Revenue Code of 1986, as amended, section 401(a)(17) is $275,000. Employees with a Date of Membership prior to that date must contribute on their total salary.

Can I roll over money from another retirement plan?If you have an existing qualified retirement plan account with a prior employer or an IRA, you may be able to transfer or roll over all or some of that account into this plan once you enroll.

Does my employer make a contribution to the plan?One of the best features of the Plan is the Employer contribution. In addition to the 9.00% contribution you make to your Plan, your Employer will contribute an amount equal to 5.0% of your pre-tax compensation.

What is vesting and how does it work?“Vesting” refers to whether you have an absolute right to your plan account or whether something else must occur before you have a right to it, such as additional years of service or reaching a certain age. Anything you contribute — including rollover or transfer contributions and any earnings on that money — is always 100% vested. You are 100% vested immediately on the value of your Employer’s contributions.

How do I direct my investments?You may choose from a range of funding options to direct your contributions. Learn more about your Plan’s selections by visiting www.metlife.com/scorp. You may change your allocation among the funding options for your current account balance and your future contributions virtually anytime by visiting our website at mlr.metlife.com or calling our toll-free number 1-800-543-2520.

Can I take a loan against my account?

Loans are not permitted at this time.

4

Can I withdraw money from my account?Since your Plan is designed primarily to help you save for retirement, the Internal Revenue Service has placed restrictions on when money may be withdrawn from your plan account before you retire. You may withdraw money from your account under the following circumstances, in accordance with your employer’s plan document:

• Retirement — In general, once you have reached age 59½, you may take distributions from your retirement account without a Federal income tax penalty.

• Termination of employment — You may receive all of your vested account value at termination of employment. Additional requirements may apply.

• Death — Any account balance that a participating employee has at death will be paid to his/her designated beneficiaries, as outlined in the Beneficiary Designation Form on file with your employer.

Your State ORP Plan Document provides more details about making withdrawals from your Plan. To obtain a copy, contact your employer. Also, always consult your tax advisor or investment professional about the income tax consequences of any withdrawals. Ordinary Federal income taxes generally apply to withdrawals. Federal income tax rules generally prohibit withdrawals prior to age 59½. Where these withdrawals are allowed, a 10% Federal income tax penalty may apply.

What if I need money in an emergency?Hardship withdrawals are not permitted at this time.

What if I have more questions about the plan?For more information regarding your Plan, please contact your Employer or representative.

How do I obtain information about my account?Each quarter, you will receive a personal account statement with a detailed summary of all activity including: account transactions and history, ending account balance and vesting information. You can contact us virtually any time directly over the phone or on the web for further assistance. Please refer to the back cover of this guide for all your access information.

Are there costs to participate in the program? Yes. An annual administrative fee of 20 basis points (0.20%) will apply to your MetLife mutual fund accounts under the State ORP. Each mutual fund has its own investment management fees and other expenses. The plan participant will pay the fees and expenses for any of the investment options selected.

South Carolina’s State Optional Retirement Program 5

This enrollment brochure is not intended to be a summary of your plan’s provisions. It only includes highlights of certain plan provisions. The plan document governs the terms of the plan and is available from your employer. Your employer may also provide a summary plan description. In general, if any conflicts occur between this material and the plan documents provided by your employer, the plan documents provided by your employer will govern.

This brochure should not be construed as tax or legal advice. Any discussion of taxes herein or related to this document is for general information purposes only and does not purport to be complete or cover every situation. Tax law is subject to interpretation and change. Tax results and the appropriateness of any product for any specific taxpayer may vary depending on the facts and circumstances. You should consult with and rely on your own independent legal and tax advisors regarding your particular set of facts and circumstances.

The information in this brochure is for informational purposes only and shall not be constructed as an offer, or solicitation of an offer, to purchase any securities or variable insurance products, or a recommendation to buy, sell or hold any securities or participate in any investment advisory program or service. Nothing in this brochure is intended to target any particular individual or analyze the financial condition of any particular individual for suitability to transact in any securities or participate in any investment advisory programs. Please consult with your representative and your independent tax advisor, review all applicable offering documents and disclosures for risks and applicable fees, charges and expenses, and consider your own financial conditions, risk tolerance, investment objectives and time horizon before investing.

6

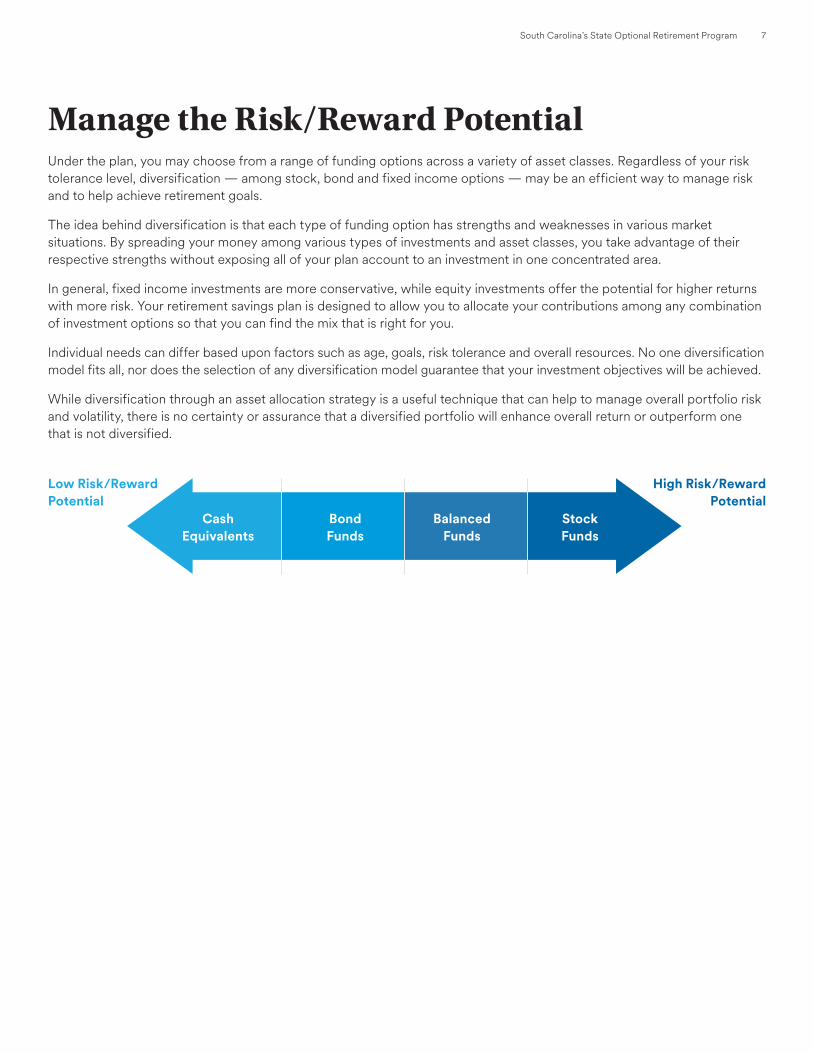

Manage the Risk/Reward PotentialUnder the plan, you may choose from a range of funding options across a variety of asset classes. Regardless of your risk tolerance level, diversification — among stock, bond and fixed income options — may be an efficient way to manage risk and to help achieve retirement goals.

The idea behind diversification is that each type of funding option has strengths and weaknesses in various market situations. By spreading your money among various types of investments and asset classes, you take advantage of their respective strengths without exposing all of your plan account to an investment in one concentrated area.

In general, fixed income investments are more conservative, while equity investments offer the potential for higher returns with more risk. Your retirement savings plan is designed to allow you to allocate your contributions among any combination of investment options so that you can find the mix that is right for you.

Individual needs can differ based upon factors such as age, goals, risk tolerance and overall resources. No one diversification model fits all, nor does the selection of any diversification model guarantee that your investment objectives will be achieved.

While diversification through an asset allocation strategy is a useful technique that can help to manage overall portfolio risk and volatility, there is no certainty or assurance that a diversified portfolio will enhance overall return or outperform one that is not diversified.

Low Risk/RewardPotential

High Risk/RewardPotential

Cash Equivalents

Bond Funds

Balanced Funds

Stock Funds

South Carolina’s State Optional Retirement Program 7

Your funding optionsMutual fundsYour retirement savings plan offers a variety of funding options. You can create your own investment mix by choosing any combination. Then you can monitor your plan investments and make adjustments as your goals change over time. The full mutual fund lineup can be found on www.metlife.com/scorp.

Morningstar Investment Management, LLC (“Morningstar”) believes that the list shows the approximate risk relationships among the asset classes for the mutual funds from the most conservative to the most aggressive. Within each asset class mutual funds are listed in alphabetical order. The ranking of asset classes is based on an analysis by Morningstar Investment Management, LLC. In determining the ranking, Morningstar Investment Management, LLC utilized certain quantitative risk measures in conjunction with its fundamental investing experience and portfolio construction philosophy. Other methodologies for ranking asset classes may produce different results. Since past performance of investments is no guarantee of future performance, no assurance can be given that the ranking of asset classes shown here will correspond to rankings in the future. Purchasers should understand that each mutual fund incurs its own risks, which will be dependent upon the investment decisions made by the respective portfolio manager. This chart is intended to be a guide; please consult the appropriate prospectus for more complete information including costs, expenses, and risks for each mutual fund.

Target date fundsYour retirement savings plan offers target date funds. Each one is a diversified mutual fund managed by a professional portfolio management team.

A target date fund invests in a set of underlying mutual funds with different investment styles which invest in different asset classes, such as stocks, bonds and cash. The “target date” refers to your potential retirement date or the date when you plan to begin withdrawing money, usually at retirement. Typically, the investments within a target date fund are weighted more towards stocks when the target date is far away and adjusts over time, so that it becomes more heavily weighted towards bonds as the target date approaches. Keep in mind that some types of bonds may be more risky than stocks.

However, each target date fund determines its own mix of stocks and bonds so that two funds with the same target date may have different asset allocations between equities and bonds, different investment strategies and different risk profiles. In addition, while the “target date” may align with your goal for withdrawing money, a particular fund’s asset mix may not coincide with your risk tolerance and financial situation. You should consult the prospectus for the fund for more details before you decide to invest.

Target date funds are designed as a one-step approach. They assume that the target date fund is your only investment and that no contributions are made after the “target date” is reached.

There is no guarantee that the fund will not lose money or that it will provide sufficient assets for retirement. The principal value of the fund is not guaranteed at any time, including the target date. You must monitor your investment in the target date fund periodically to make sure that it is appropriate for you. Because a target date fund is typically a “fund of funds,” investors bear two levels of fees for the underlying funds and the target date fund.

Securities distributed by MetLife Investors Distribution Company (member FINRA).

8

Fee disclosureAbout your mutual fund select portfolios (“MFSP”) account: MFSP is a program that MetLife makes available to participants in retirement plans and deferred compensation arrangements that are permitted to invest their plan accounts in mutual fund shares. Your employer or a third party appointed by your employer (other than MetLife) selects the mutual funds (each a “Fund”) that are offered as investment options under its plan.

Mutual funds and fixed account annuity products that are subject to a market adjusted value are sold by prospectus, which is available on www.metlife.com/scorp. Please carefully consider investment objectives, risks, charges, and expenses before investing. For this and other information about any mutual fund investment or the fixed annuities that are subject to market adjusted value, please obtain a prospectus and read it carefully before you invest. Investment return and principal value will fluctuate with changes in market conditions such that mutual fund shares may be worth more or less than original cost when redeemed. Withdrawals from the annuity are also subject to withdrawal charges.

Your expenses for investing in the MFSP funds: You pay Fund investment management fees, other expenses, 12b-1 fees and redemption fees (if any) on each Fund in your plan MFSP account. These fees and expenses vary by the Fund. Please refer to each Fund’s prospectus for a description of these fees and expenses.

MetLife compensation received from the funds: MetLife and/or its affiliates also receive compensation from the Funds and/or their affiliates with respect to participant account balances for certain recordkeeping, administration and distribution services, which also vary by Fund. Different Funds provide MetLife and/or its affiliates different amounts and types of compensation, which change from time to time. Accordingly, compensation received by MetLife varies over time based on the amounts and types of compensation paid by the Funds, Funds that are made available under the plan and participants’ account allocations in the various Funds. MetLife may pay all or a portion of such compensation to unaffiliated broker dealer, MML Investors Services, LLC, for certain services provided on MetLife’s behalf.

Plan administrative fees and other expenses paid by you and/or the plan: MetLife receives compensation for administrative and recordkeeping services it provides for the plan. Depending on the arrangement authorized by your employer, MetLife’s compensation for these services (1) consists of (a) the compensation it receives from Funds (described above), (b) a separate per participant fee or basis point fee on plan assets, or (c) a combination of both; and (2) generally, is paid by charging participants’ plan accounts or from the plan expense account. At the employer’s direction, MetLife also may be required to charge participants’ plan accounts or the plan expense account and remit fees to third parties for plan services they provide, such as administrative, trust, custodial, investment advisory, or consulting services they provide. Please see below for additional information about the way that plan administrative fees and other expenses are paid by you and/or the plan.

An annual plan administrative fee of 22 basis points (or 0.22%) on mutual fund assets in your State ORP account with MetLife will be charged in quarterly installments. This fee will be offset by fund compensation that MetLife receives with respect to mutual fund assets in your State ORP account. If your employer directs MetLife to pay fees that are charged by other third parties for the services they provide to the plan, the annual plan administrative fee may be increased and/or the Fund compensation retained by MetLife may be net of such payments.

Reliance Trust Company (RTC) provides directed trust and/or custodial services for your plan. Your employer has authorized and directed MetLife to pay RTC’s fee on behalf of the plan. The fee is paid from the Fund compensation that MetLife receives with respect to plan assets or from administrative fees charged to participants’ MFSP accounts or to the plan.

If these fees change, you will be notified.

South Carolina’s State Optional Retirement Program 9

Upon written request, MetLife will provide the current rates of compensation for Funds in your plan and any related information reasonably requested. Please direct any such request to MetLife Resources, 11225 North Community House Road, Client Services, Mail Stop 3.663, Charlotte, NC 28277. Please make sure you understand all the fees and expenses related to the investment of your MFSP account in the Funds. If you need additional information, please contact MetLife at the address indicated above.

Disclosure materials: If your plan offers a fixed annuity that is subject to a market adjusted value, you have been provided a prospectus for that product. You will also be provided with a prospectus for each MFSP Fund when your contribution is first allocated to that Fund. Withdrawals from the annuity are also subject to withdrawal charges. If you would like to receive other prospectuses (or any other disclosure information), visit www.metlife.com/scorp.

Securities distributed by MetLife Investors Distribution Company (MLIDC) (member FINRA). MLIDC and MetLife are not affiliated with Morningstar, Inc.

10

Important enrollment disclosures Mutual fund select portfolios disclosure statement About your MFSP account: MFSP is a program that Metropolitan Life Insurance Company and its affiliates (“MetLife”) make available to participants in retirement plans and deferred compensation arrangements that are permitted to invest their plan accounts in mutual fund shares. Your employer or a third party appointed by your employer (other than MetLife or any of its affiliates) selects the mutual funds (“Funds”) that are offered as investment options under its plan.

Investment risks: Mutual funds are sold by prospectus, which is available on www.metlife.com/scorp. Please carefully consider investment objectives, risks, charges, and expenses before investing. For this and other information about any mutual fund investment, please obtain a prospectus and read it carefully before you invest. Investment return and principal value will fluctuate with changes in market conditions such that mutual fund shares may be worth more or less than original cost when redeemed.

Your expenses for investing in the MFSP funds: You pay Fund investment management fees, other expenses, 12b-1 fees and redemption fees (if any) on each mutual fund investment in your plan MFSP account. These fees and expenses vary by the Fund. Please refer to each Fund’s prospectus for a description of these fees and expenses.

MetLife compensation received from the funds: Metropolitan Life Insurance Company and/or its affiliates also receive compensation from the Funds and/or their affiliates with respect to participants’ account balances for certain recordkeeping, administration and distribution services, which also vary by Fund. Different Funds provide MetLife and/or its affiliates different compensation. Therefore, this compensation may vary over time based on the Funds that are made available under the plan and participants’ account allocations in the various Funds. MetLife may pay all or a portion of such compensation to an unaffiliated broker dealer, MML Investors Services, LLC, for certain services provided on MetLife’s behalf. Upon written request, MetLife will provide the current rates of compensation for Funds in your plan and any related information reasonably requested. Please direct any such request to MetLife Resources, 11225 North Community House Road, Client Services, Mail Stop 3.663, Charlotte, NC 28277. Please make sure you understand all the fees and expenses related to the investment of your MFSP account in the Funds. If you need additional information, please contact MetLife at the address indicated above.

Plan expense account: Your employer may establish an account under your plan for the payment of plan expenses. Depending on the arrangement authorized by your employer, MetLife may credit this account with all or a portion of the compensation it receives from MFSP Funds (described in the preceding paragraph).

Plan administrative fees and other expenses paid by you and/or the plan: MetLife receives compensation for administrative and recordkeeping services it provides for the plan. Depending on the arrangement authorized by your employer, MetLife’s compensation for these services (1) consists of (a) the compensation it receives from Funds (described above), (b) a separate per participant fee or basis point fee on plan assets, or (c) a combination of both; and (2) generally, is paid by charging participants’ plan accounts, or, at the employer’s direction, from the plan expense account. At the employer’s direction, MetLife also may be required to charge participants’ plan accounts or the plan expense account and remit fees to third parties for plan services they provide, such as administrative, trust, custodial, investment advisory, or consulting services.

South Carolina’s State Optional Retirement Program 11

For information about your plan’s fee arrangement with MetLife, please see the Mutual Fund Select Part/alias Disclosure Statement that has been prepared specifically for your plan, which is included in the Enrollment book or can be obtained from the representative or your employer.

Investment instructions: You may give investment instructions on any Business Day (which usually includes all days the New York Stock Exchange is open). You must call the Service Center on the telephone number listed on your quarterly statement before 4:00 p.m. Eastern Time (or the earlier close of regular trading on the NYSE) in order for us to process your investment instructions on the same Business Day. Any investment instructions received in good order after that time will be processed on the next Business Day. In addition, your plan may impose additional restrictions on investment transactions.

Investment advice/recommendations: Neither MetLife, nor any of its employees or agents, will provide investment recommendations or give investment advice of any kind in regard to your plan MFSP account. By signing the Enrollment Form, you confirm that no MetLife employee or agent made any investment recommendations or gave any investment advice of any kind. If you’re interested in asset allocation services, please ask your representative.

Prospectus: If you allocate plan contributions or transfer any part of your plan account into a Fund for which you do not have an account balance, you will be provided a prospectus for that Fund. Whenever you want a prospectus please visit www.metlife.com/scorp.

Securities are distributed by MetLife Investors Distribution Company (MLIDC) (member FINRA).

12

Access your retirement account

You may access your account in two ways:

✓ Log onto mlr.metlife.com

✓ Call 800-543-2520

Through either the website or the toll-free telephone number, you can obtain:

✓ Account balance

✓ Contribution amount (deferral amount)

✓ Contribution history

✓ Current allocations

✓ Transfer history

✓ Monthly mutual fund performance

✓ Fund fact sheets

You can also:

✓ Use the financial calculators

✓ Change contribution amount (deferral amount)

✓ Redirect future contributions

✓ Rebalance investments

✓ Change Personal Identification Number (PIN)

✓ Opt in to receive paperless, electronic account documents

In addition, you can speak to a Client Service Representative, Monday through Friday from 9:00 a.m. to 8:00p.m. (Eastern Time).

* Access to the website and phone system may be limited or unavailable during periods of peak demand, market volatility, system upgrades/maintenance, or other reasons. Transfer requests made via the website received and in good order on business days prior to the close of the New York Stock Exchange (4:00 p.m. Eastern Time or earlier on some holidays or in other special circumstances) will be processed at the close of business the same day the request was received. Requests received after this time are processed on the next business day.

Account access virtually 24/7*mlr.metlife.com | 800-543-2520

To help monitor and manage your plan account, you can obtain information and make transactions virtually 24 hours a day, 7 days a week*.

South Carolina’s State Optional Retirement Program 13

Focus on your futureWith proper planning and action, you can get on track for a comfortable retirement — today. The sooner you enroll in the South Carolina’s State Optional Retirement Program, the more you may be able to enjoy the benefits in the future. Contact your representative today.

14

Mutual Funds are sold by prospectus only, which is available from your registered representative. Please carefully consider investment objectives, risks, charges, and expenses before investing. For this and other information about any mutual fund investment please obtain a prospectus and read it carefully before you invest. Investment return and principal value will fluctuate with changes in market conditions such that shares may be worth more or less than original cost when redeemed. Diversification cannot eliminate the risk of investment losses, and past mutual fund performance is not a guarantee of future results.

Any discussion of taxes is for general informational purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax or accounting advice. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

The Registered Fixed Account Option (Gold Track Select) is offered by prospectus only, which is available from your registered respresentative. You should carefully consider the product’s features, risks, charges and expenses. This and other information is available in the prospectus, which you should read carefully before investing. Product availability and features may vary by state. All product guarantees are subject to the financial strength and claimspaying ability of the issuing insurance company. Withdrawals may be subject to withdrawal charges and a market adjusted value. The market adjusted value may be lower or higher than your contract value.

The Registered Fixed Account Option of the Gold Track Select Variable Annuity credits an annual interest rate declared by Brighthouse Life Insurance Company. The Gold Track Select Annuity is issued on policy form numbers L-14666, L-14669, L-14672, L-14672 CA, L-14669 MO, L-14672 MO, L-14669 ND, L-14672 ND, L-14669 NE, L-14672 NE, L-14634A, L-14669 NYNON4223, L-14672 NYNON4223, L-14669 NY4223, L-14672 NY4223, L-14666 OR, L-14669 OR, L-14672 OR, L-14666 PA, L-14669 PA, L-14672 PA, L-14666 TX, L-14669 TX, L-14672 TX, L-14669 UT, L-14672 UT, L-14669 WA, L-14672 WA, L-14666 WI, L-14669 WI, L-14672 WI by Brighthouse Life Insurance Company, 11225 North Community House Road, Charlotte, NC 28277.

Annuities are issued by Brighthouse Life Insurance Company, Charlotte, NC 28277 and in New York only by Brighthouse Life Insurance Company of NY, New York, NY 10017. Variable annuity products are distributed through Brighthouse Securities, LLC (member FINRA). Product guarantees are solely the responsibility of Brighthouse Life Insurance Company or in New York only Brighthouse Life Insurance Company and not MetLife. MetLife, a registered service mark of Metropolitan Life Insurance Company, is used under license to Brighthouse Services, LLC and its affiliates. Brighthouse Financial is a service mark of Brighthouse Financial, Inc. or its affiliates.

Brighthouse Life Insurance Company policies and contracts contain exclusions, holding periods, termination provisions, limitations, reduction of benefits, surrender charges and terms for keeping them in force. Please see your representative for complete costs and details.

Securities distributed by MetLife Investors Distribution Company (MLIDC) (member FINRA). MLIDC and MetLife are not affiliated with Morningstar, Inc.

South Carolina’s State Optional Retirement Program 15

Metropolitan Life Insurance Company | New York, NY 101661801 955081 MLR1900011177-8 L0419514040[exp0921][SC] ©2019 MetLife Services and Solutions, LLC

metlife.com