solid strategy, confident execution lehman brothers 2003 high yield conference march 21, 2003 kevin...

Post on 21-Dec-2015

216 views

TRANSCRIPT

Solid Strategy, Confident Execution

Lehman Brothers 2003 High Yield Conference

March 21, 2003

Kevin DeNicolaSenior Vice President and CFO

2

Safe Harbor Language

Statements in this presentation relating to matters that are not historical facts are forward-looking statements. These forward-looking statements are just predictions or expectations and are subject to risks and uncertainties. Actual results could differ materially, based on factors including but not limited to the cyclical nature of the chemical and refining industries; availability, cost and volatility of raw materials and utilities; governmental regulatory actions and political unrest; global economic conditions; industry production capacity and operating rates; the supply/demand balance for Lyondell's and its joint ventures' products; competitive products and pricing pressures; access to capital markets; and technological developments and other risk factors. For more detailed information about the factors that could cause our actual results to differ materially, please refer to Lyondell Chemical Company’s Annual Report on Form 10-K for the year ended December 31, 2002, filed in March 2003.

3

Lyondell Has Built a Balanced Portfolio

Lyondell

IC&D

LCR

Equistar

Commodity Leverage-- A leading North American producer of ethylene, propylene

and polyethylene-- Low cost position based on feedstock flexibility and scale

Stability & Growth-- A leading global producer of PO and derivatives-- Process technology strength

Cash Generation-- Unique capability to refine heavy crude oils-- Contractually stable business; strong cash flow generator

($ MM)

Revenues EBITDALyondell

OwnershipIC&D $3,262 $410 100.0%Equistar 5,537 256 70.5LCR 3,392 362 58.75

2002

4

The Recent Years Have Been a Period of Optimization

Mid 1990’s

Formation years

LCR Contract and JV

Equistar JV

IC&D Acquisition

1999-2002Position and Optimize

Portfolio Adjustments

Capacity Rationalization

Project Reorientation

Organization Effectiveness– Best practices

– Organization design

5

0102030405060708090

1998 2002

Lyondell Equistar

0

30

60

90

120

150

180

Lyondell Equistar PO11 Spending

Processes and Systems Have Steadily Improved the Capital Utilization Within the Enterprise

$MM

1999 2002

Capital Spending Days of Working Capital*

* Based on accounts receivable (including those sold), inventories and accounts payable as of 12/31, and fourth-quarter days of sales

6

A Snapshot of Operating Metrics Highlights the Success

0

10

20

30

40

50

60

70

80

90

LYO/EQU EQU LYO/EQU Polymers

Safety Downtime Environment Quality

% Improvement*

* 1998 to 2002

7

A Brief Portfolio Review

IC&D

LCR

Equistar

8

Our Propylene Oxide and Derivatives Business (IC&D) Benefits from a Strong Position

PG33%

Merchant PO33%

Deicer6%

P-Solvents10%

BDO18%

Bayer45%

ProductCapacityPosition

MarketGrowth

Merchant PO 1

PG 1 Moderate

BDO 2 High

P-Solvents 2 Low

Deicers 1 Low

PO 4-5%/yr

Lyondell55%

Lyondell PO Capacity

Source: LYO databook and SRI Post PO-11 Project

9

PO Technology Development

H2

OxidationOxygen

PropylenePropylene Oxide

H2O

Peroxidation

Direct PO

EB

IC4

H2

Oxygen

Oxidation

Propylene

Epoxidation

H2O

Styrene

MTBE

Propylene Oxide

Cumene Cumene

Chlorohydrin

Electricity

SaltChlor-Alkali Chlorohydrin

Propylene

PO

10

LCR Important Cash Generator

Operating Reliability and Crude Deliveries Drive Performance

1 4Q01: Scheduled maintenance turnaround

0

50

100

150

200

250

300

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 Q402

0

20

40

60

80

100

120

140CSA Spot Mkt EBITDA

MB/day $MM

1

11

Refining Spreads Have Increased By $4-5/Bbl

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

3/2/

1 R

efin

ing

Sp

read

($/

Bb

l)

WTI Crude Oil Refining Margin

Source: Platt’s

12

Equistar is a Leading Ethylene Producer

#2 in North America

Competitive position based on feedstock flexibility

1991 2002

Top 5 North America

Shell9%

Dow9%

Equistar15%Nova

8%

Union Carbide7%

Exxon7%

Dow/Carbide20%

ExxonMobil13%

ChevronPhillips10%

Nova 8%

40%

66%

Source: CMAI

13

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2002 1995 Margins¹ 1988 Margins¹

LCR IC&D Equistar

Significant Cash and Earnings Generation in Up-Cycle

Cycle EBITDA Potential

1 1988/1995 Chem Data/CMAI margins for Ethylene, Polyethylene and Styrene applied to current capacities and ownership Note: Assumes current capital structure; 160MM shares

($MM)

$6.20/share

$1.35/share

14

Equistar Capability

NGL

37%

Liquid

63%

N. American Industry

(ex. Equistar)

NGL

78%

Liquid

22%

Liquid Cracking Provides an Advantage

Source: CMAI and Lyondell.

Ethane - Light Naphtha Cost of Ethylene Spread

0

1

2

3

4

5

6

7

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

¢/lb

eth

yle

ne Average

Liquid Cracking Variable Cost Advantage

Source: ChemData,

15

The Oil/Gas Price Ratio has Moved in FavorThe Oil/Gas Price Ratio has Moved in Favorof Liquid Feedstockof Liquid Feedstock

0

5

10

15

02-Jan 02-Apr 02-Jul 02-Oct 03-Jan 03-Feb 03-Mar

Oil/

Ga

s

Oil/Gas Ratio

Energy Value Parity

CMAI -3/03

16

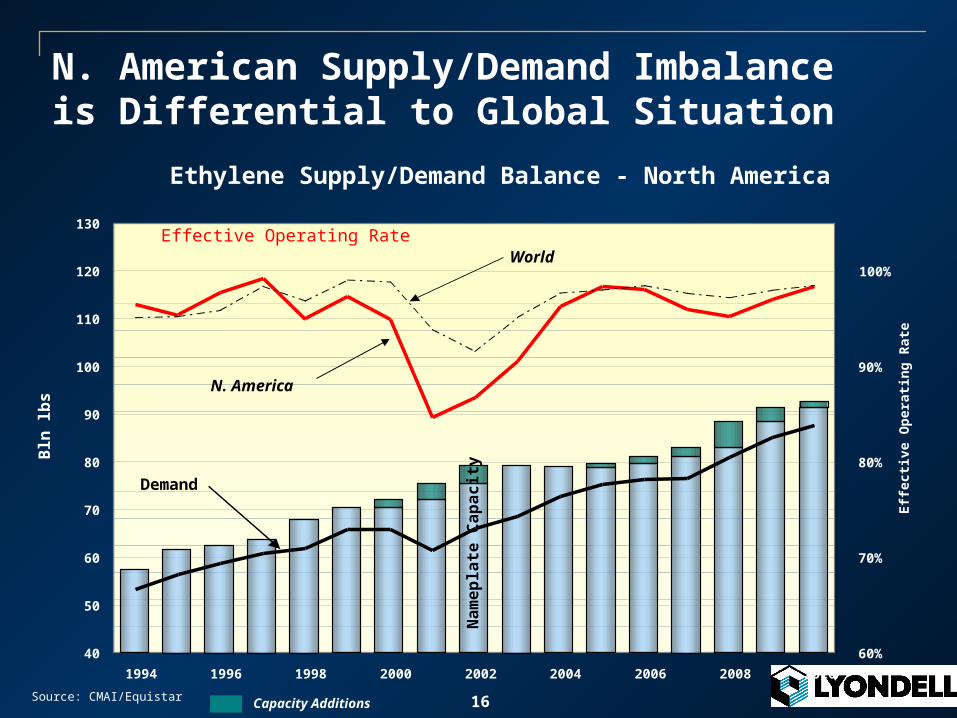

Ethylene Supply/Demand Balance - North America

40

50

60

70

80

90

100

110

120

130

1994 1996 1998 2000 2002 2004 2006 2008 2010

Bln

lb

s

60%

70%

80%

90%

100%

Eff

ecti

ve O

per

atin

g R

ate

Na

me

pla

te C

ap

ac

ity

Effective Operating Rate

Source: CMAI/Equistar

Demand

World

N. American Supply/Demand Imbalance is Differential to Global Situation

N. America

Capacity Additions

17

Effective Ethylene Operating Rates Move Effective Ethylene Operating Rates Move Toward 95% Early in 2003Toward 95% Early in 2003

U.S. Ethylene Supply/Demand

Quarterly - 2002 > 2004

CMAI-2/03

2002 20032002 2003

12000

14000

16000

18000

20000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2004QtrlyAvg

Millio

ns

Ca

pa

cit

y L

bs

70

75

80

85

90

95

100

Op

era

tin

g R

ate

, %

Effective Capacity Downtime Operating Rate

18

0

5

10

15

20

25

30

35

40

02-Jan 02-Apr 02-Jul 02-Oct 03-Jan 03-Feb 03-Mar

$/B

l

0

1

2

3

4

5

6

7

8

9

10

$/M

n B

tu

Ethylene Cash CostNat Gas ($/MM BTU)WTI ($/Bbl)

CMAI -3/03

As Energy Rose Ethylene Cash Cost As Energy Rose Ethylene Cash Cost Increased AccordinglyIncreased Accordingly

19

Market Prices Have Increased in Recent Months

Price Increases

Jan. Feb.

EQUISTAR

Ethylene 2.25 ¢/lb 1.75 ¢/lb

Propylene 2.0 ¢/lb 2.0 ¢/lb

Polyethylene 2.5 ¢/lb 2.5 ¢/lb

MEG 2.0 ¢/lb 4.5 ¢/lb

LYONDELL

Styrene 2.0 ¢/lb 5.5 ¢/lb

20

Typically It Has Taken Time to Move These Increases Through The Supply Chain: $3 Bbl Impact At Equistar

(30)

(20)

(10)

0

EB

ITD

A I

mp

act

( $

MM

/mo

)

Hours Days Weeks Months

Naphtha Impact

NGLs Follow

Petro -chemicals

Rise

FuelCo-Products

Rise

Polymers/ Derivatives

Rise

21

Our Financial Strategy is Unchanged

Maintain Sufficient Liquidity

Repay Debt

22

We Have Maintained Significant Liquidity

Lyondell Equistar

Cash & ST Investments* $330MM $27MM

Revolver* $350MM $450MM

Total Liquidity $680MM $477MM

1 1

1 – does not include 12/31 amounts committed against letters of credit : (LYO-$49MM, Equ-$16MM) * As of 12/31/2002

23

1 Capitalization = debt + book value of equity + minority interest

De-leveraging Will Benefit All Stakeholders

Impact of Lyondell debt reduction at constant capitalization1:

Debt Reduction

$1B $2B

Debt to capitalization 54% 36%

Avoided interest expense $100MM/Yr $200MM/Yr

Earnings improvement 40¢/share 80¢/share

Share price improvement atconstant capitalization $6/share $12/share