social investor meeting on responsible inclusive finance · 8 international: acep, advans, cif west...

TRANSCRIPT

Social Investor Meeting on

Responsible Inclusive Finance

Monday 18 June, 2018

Hosted by the Government of the Grand Duchy of Luxembourg -Ministry of Foreign

and European Affairs

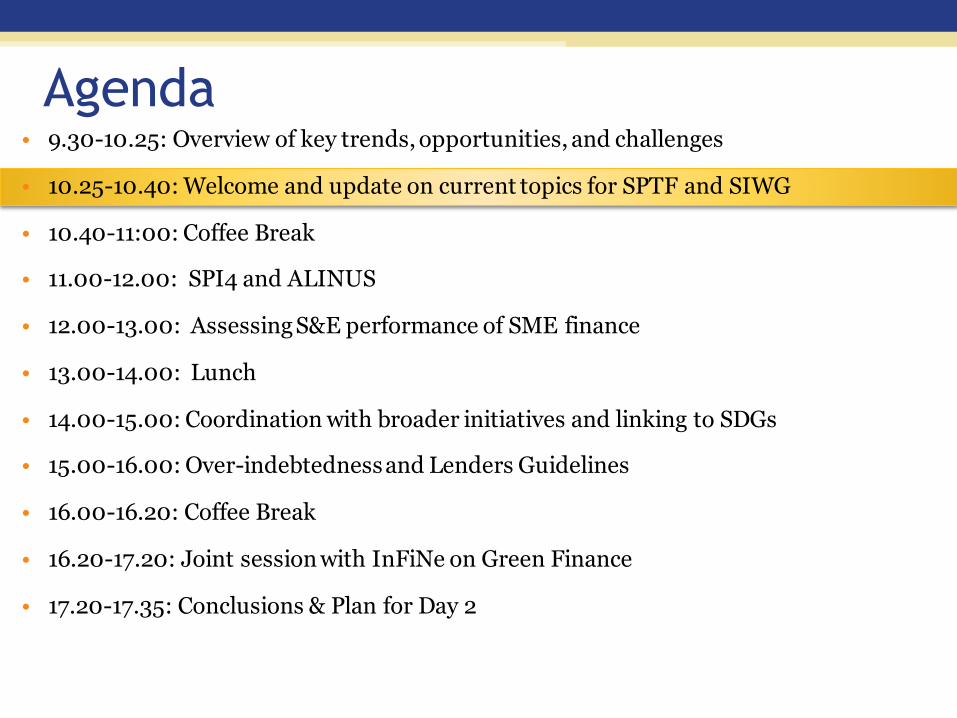

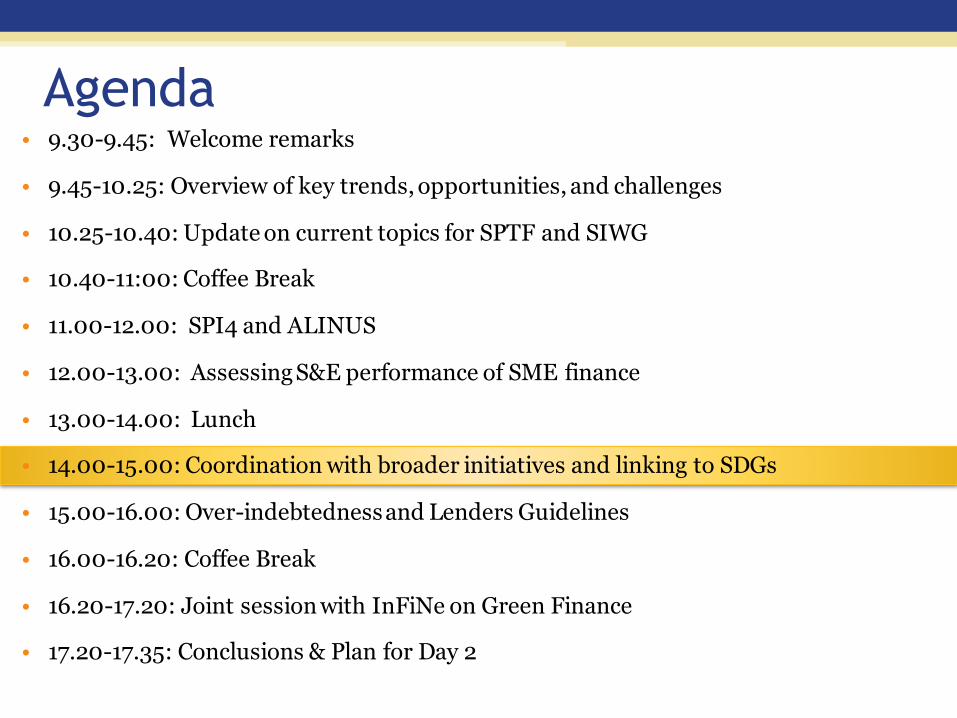

Agenda• 9.30-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Overview of Key Trends

Agenda• 9.30-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Welcome and update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

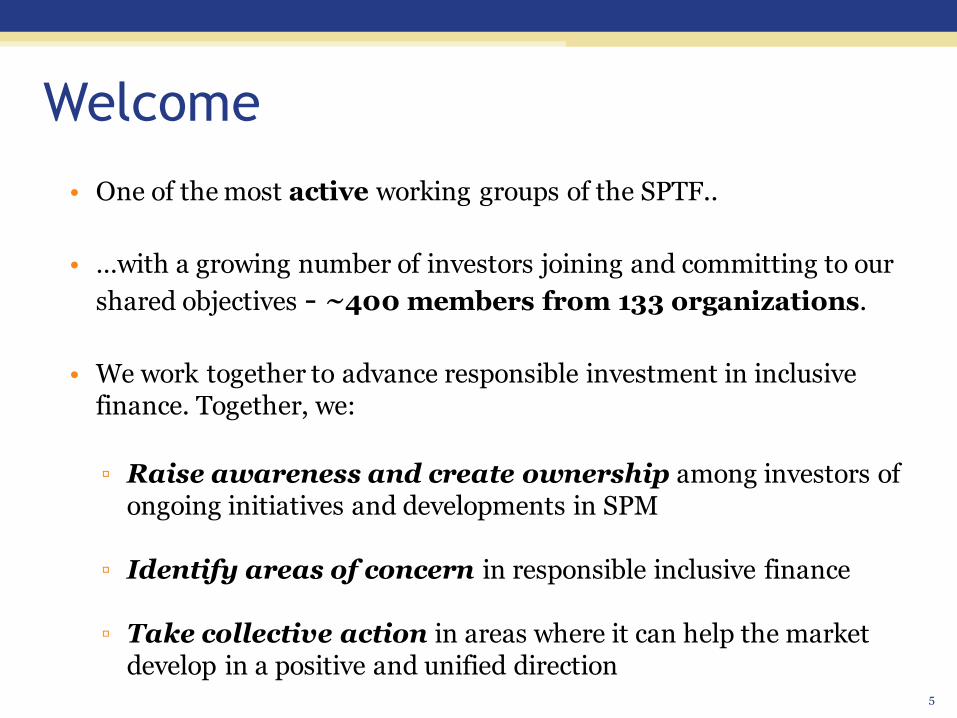

• One of the most active working groups of the SPTF..

• …with a growing number of investors joining and committing to our

shared objectives - ~400 members from 133 organizations.

• We work together to advance responsible investment in inclusive finance. Together, we:

▫ Raise awareness and create ownership among investors of ongoing initiatives and developments in SPM

▫ Identify areas of concern in responsible inclusive finance

▫ Take collective action in areas where it can help the market develop in a positive and unified direction

Welcome

5

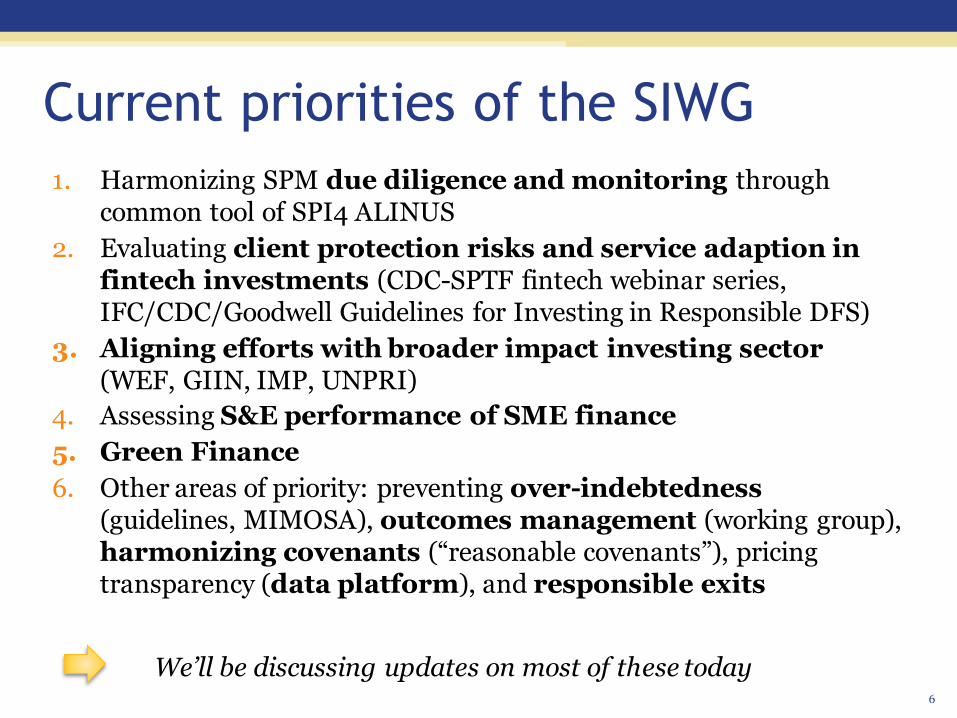

1. Harmonizing SPM due diligence and monitoring through common tool of SPI4 ALINUS

2. Evaluating client protection risks and service adaption in fintech investments (CDC-SPTF fintech webinar series, IFC/CDC/Goodwell Guidelines for Investing in Responsible DFS)

3. Aligning efforts with broader impact investing sector(WEF, GIIN, IMP, UNPRI)

4. Assessing S&E performance of SME finance

5. Green Finance

6. Other areas of priority: preventing over-indebtedness(guidelines, MIMOSA), outcomes management (working group), harmonizing covenants (“reasonable covenants”), pricing transparency (data platform), and responsible exits

Current priorities of the SIWG

6

We’ll be discussing updates on most of these today

• 2017: Zurich (March), Mexico (May)

• 2018: India (February)

• We also meet several times throughout the year via webinars in areas of common interest to group members

In-person meetings: 2x a year

7

Thank you to our investor organizational members!

8

Thank you to our collaborating partners!

9

Agenda• 9.30-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Update onSPI4-

ALINUS

Photo: A. Alvarado

The common social

data collection tool

for ALigning

INvestors

due diligence with

the

Universal Standards

June 18, 2018

Luxembourg

Cécile Lapenu and

SIWG members

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

SPI4-ALINUS, Why?

CONCENTRATE

CONVINCE

COMPILE

COMPARE

COMMUNICATE

www.cerise-spi4.org

MIV/DFIs using ALINUS

• Full use (direct or aligned indicators)

ADA/LMDF, AFD, Alterfin, Blue Orchard, BNP Paribas, Cordaid,

European Investment Fund, Gawa, GCAMF, Incofin, Oikocredit,

Pamiga, Proparco, Sidi, Stromme MF/EA

Testing/strategic planning

BOPA, Deutsche Bank, DID – Development International

Desjardins, European Investment Bank, FAS, Gojo & Company,

GrassRoots, Symbiotics, Triple Jump, Verdant Capital

• Awareness raising

In contact with CERISE/SPTF for strategic discussions

15

10

17

International/National Networks using

SPI4/ ALINUS• Networks using SPI4

8 International: ACEP, Advans, CIF West Africa, Microcred, Opportunity Intern’l, Oxus, Pamiga, Vision Fund7 National: Amcred Brazil, Copeme Peru, FinruralBolivia, MCPI Philippines, PMN Pakistan, RadimArgentina, RFD Ecuador

• Networks in training/awareness or using

reduced network option3 International: AgaKhan, Grameen Foundation, CICM, etc.9 National: AMA Albania, AMFA Azerbaijan, AMFI Kyrgistan, AMFOT Tajikistan, ASOMIF Nicaragua, CMF Nepal, LMWG Laos, RedFasco Guatemala, UCORA Armenia, etc.

15

12

54

85

174184

230

20

40

60

80

100

120

140

160

180

200

2014 2015 2016 2017 Untilapril2018

Numbers of completed SPI4

April, 2018

520 SPI4 audits completed

30% filled the green index

88 different countries

389 questionnaires in SPI4 database

67% are accompanied self-assessments

+970 people trained in SPI4 (CERISE & SPTF)

109 qualified auditors

15 investment funds using

Growing use of SPI4

10 underway74 pipeline

Use of SPI4 today

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

Making Microfinance Investment Responsible

MIR Action group – Feedback from surveysSurvey (direct/online) conducted Q1 2018

Investors (12), networks (8), FSP (22), SPI4 auditors (80)

What users like most?

What users like the least?

Call for action

• Common language, intern’lrecognition (credibility)

• Role of n’l networks in raising awareness

• Learning by doing (audit process)

• Concrete resources, comprehensive framework

• Benchmarks on Univ. Standards

• Funding facilities, targetedto most needed regions

• Low awareness in someregions (e.g. SEA exceptCambodia, CAC + Brazil)

• Overwhelming for somelevels (tool, implementation, smallorganizations) VS. advanced FSP remain on confort zone; standardization smoothesspecificities

• Not seen as strategic by some Boards or Management teams

• Quality of assessments

• Continuing awareness, support in implementation, quality control

• Engagement of regulatorsand investors (incentives for FSP)

• Information on facilities (and support extended)

• Platform to share experienceand practices

• Integrate with Risk Management and other key management issues (HR, product, MIS, etc.)

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

Free access

to Good

Return RIF

Academy for

this online

30-minute

course on

ALINUS

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

Client-centered finance

through

data-based managementSPI Web Application

Build a fully-fledged data-based management

system by leveraging internet technologies

• Put client well-being at the center of strategy and operations of FSP (and later, social enterprises)

▫ Go farther: Build a user-friendly web-app to guide FSPs as they conduct their assessments and define annually their social statements

▫ Go broader: FSPs to use SPI4 on a regular basis, helping refocus the sectors’ activities around the clients needs and adaptation of products

SPIWAPP - a user-friendly, online application▫ A web app as a one-stop tool for data collection related to SPM

for field organisations

▫ A powerful engine to store and explore the data on SPM for each FSP

▫ Innovative data visualization to produce meaningful social dashboards

▫ A web app development based on iterative and agile methodology to adapt to the needs of the FSPs and SPI4 users

▫ An interface enabling foreseen in-house content development and minimum maintenance costs

CERISE is looking for partners to support its digitaltransformation, so that together we can build a common good for the financial inclusion ecosystem

Agenda of the session

• Progress on implementation of ALINUS

• Feedback from the field (eMFP Action group surveys)

• New resources to support users (e-learning on ALINUS)

• Next steps for SPI4: Go Digital!!

• Testimonies from practitionners

Testimonies from other users

• EIF : Customized ALINUS

• ADA : Implementation for due-diligence

• EIB : How to mitigate social risks and keep manageable DD on the microfinance business line?

Feedback from the group and Q&A

Thank you!

CERISE: spi4@cerise-

microfinance.org

Two companion guides to assess

and improve

Resources on ALINUS +

Qualified auditors

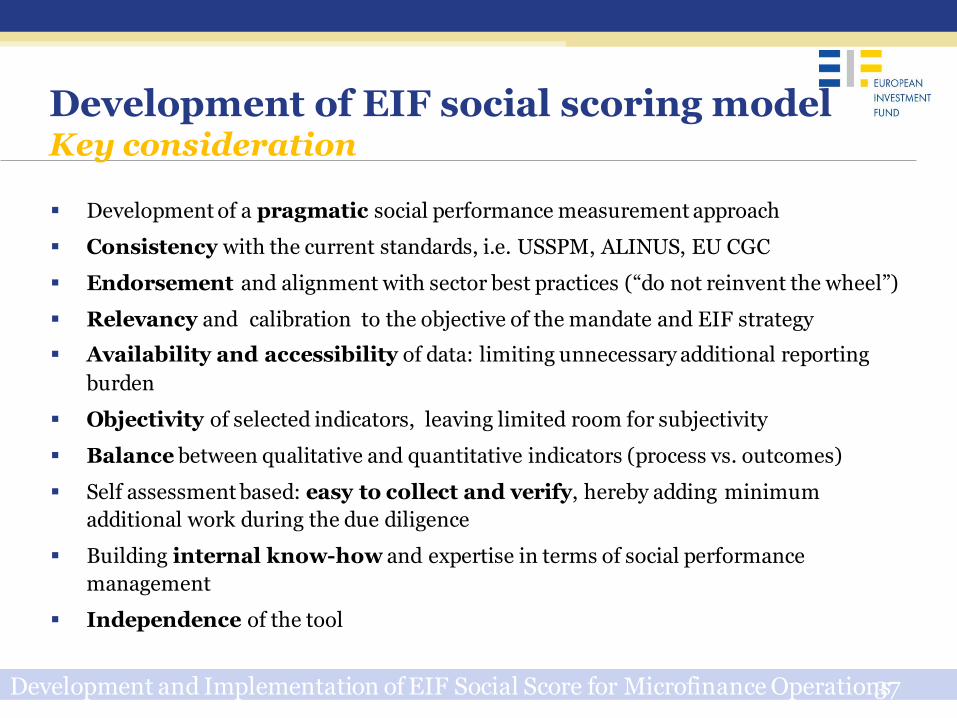

Development and Implementation of EIF Social Score for Microfinance Operations

Development of EIF social scoring model Social performance management at EIF

▪ Support from CERISE on the development and implementation of EIF’s social performance assessment tool

▪ Objectives : Development of a pragmatic SPM approach, drawing from international experience and European context

▪ Challenge: Aligning to the universal standards in social performance assessment while addressing the specific socio-economic challenges of European markets and EIF investment strategy

36

➢ USSPM➢ Alinus/SPI-4➢ EU CGC➢ EaSI DA➢ EU context

➢ Identification and selection of key qualitative/ quantitative indicators

➢ Preliminary model

based on SPI-4

➢ Pilot test with a sample of FIs, incl.

feedback survey

➢ Adjustment & recalibration

➢ Improved guidance

➢ Case study

➢ Re-appropiation of

model – change of tool format

➢ Leveraging on

extensive work achieved with Cerise

PreliminaryMapping WorkshopI

Development

&PilotWorkshopII

Validationprocess Implementation

Development and Implementation of EIF Social Score for Microfinance Operations

Development of EIF social scoring modelKey consideration

▪ Development of a pragmatic social performance measurement approach

▪ Consistency with the current standards, i.e. USSPM, ALINUS, EU CGC

▪ Endorsement and alignment with sector best practices (“do not reinvent the wheel”)

▪ Relevancy and calibration to the objective of the mandate and EIF strategy

▪ Availability and accessibility of data: limiting unnecessary additional reporting

burden

▪ Objectivity of selected indicators, leaving limited room for subjectivity

▪ Balance between qualitative and quantitative indicators (process vs. outcomes)

▪ Self assessment based: easy to collect and verify, hereby adding minimum

additional work during the due diligence

▪ Building internal know-how and expertise in terms of social performance

management

▪ Independence of the tool

37

Development and Implementation of EIF Social Score for Microfinance Operations

Implementation of EIF’s social scoring tool Balancing social processes and outcome

38

• 12 qualitative indicators accounting for 60% of total score

• 10 quantitative indicators accounting for 40% of total score

• 22 criteria

3 9

• Promoting SP is a goal that has been integrated in ADA’s strategic and action plan.

• Alinus is the tool we decided to use both for the investment process (LMDF) and Capacity Building projects

• 2017 we benchmarked with Cerise database 32 partners that have completed a SPI4

ADA&LMDF experience in using SPI4-Alinus_strategy

4 0

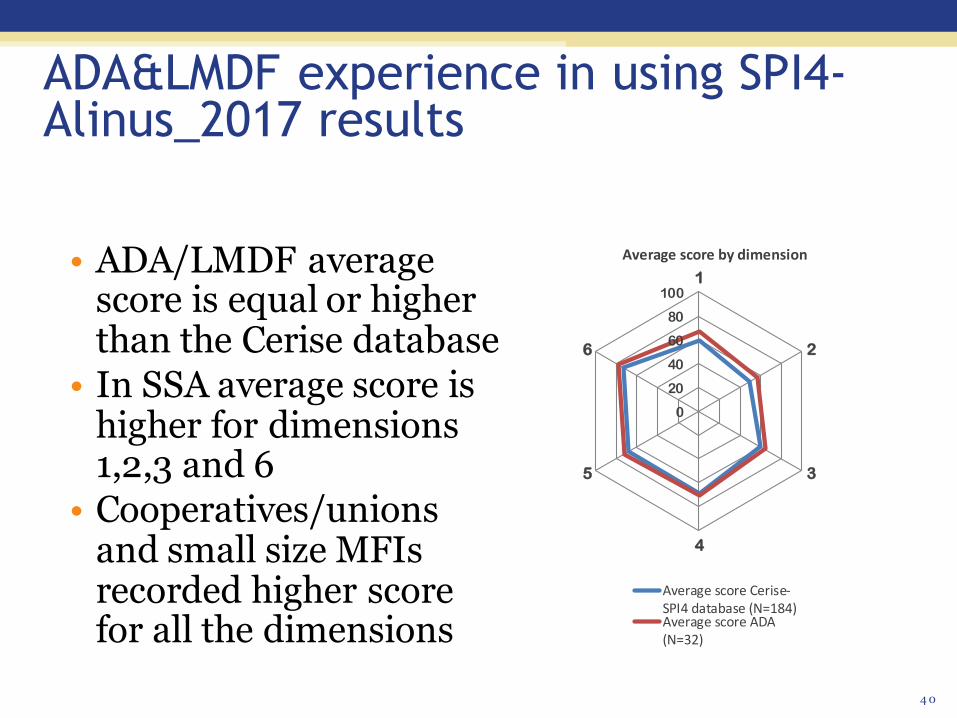

ADA&LMDF experience in using SPI4-Alinus_2017 results

• ADA/LMDF average score is equal or higher than the Cerise database

• In SSA average score is higher for dimensions 1,2,3 and 6

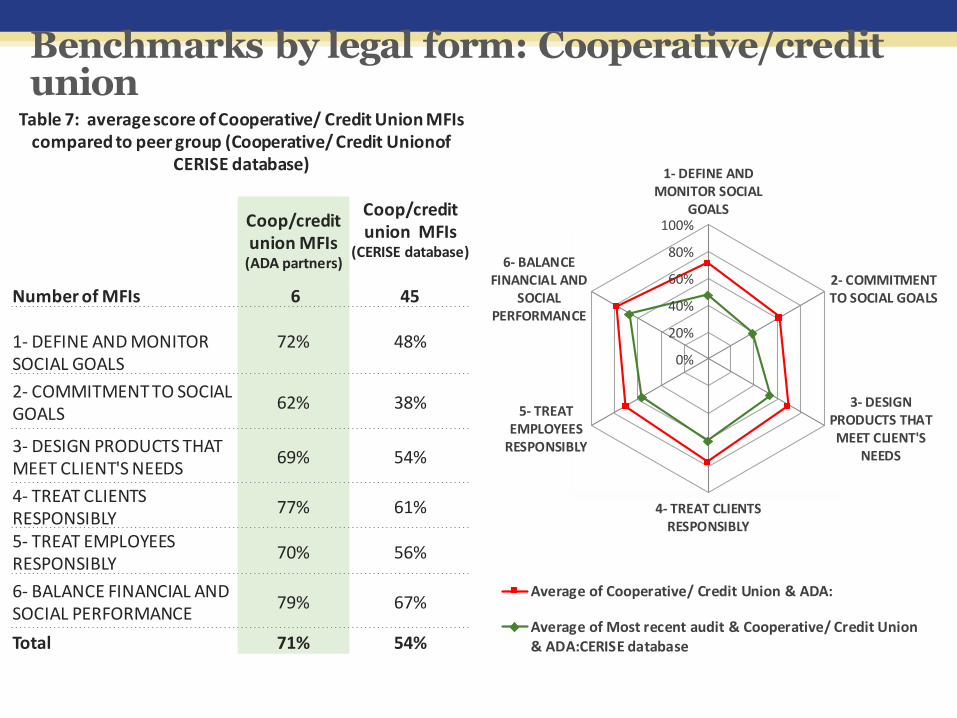

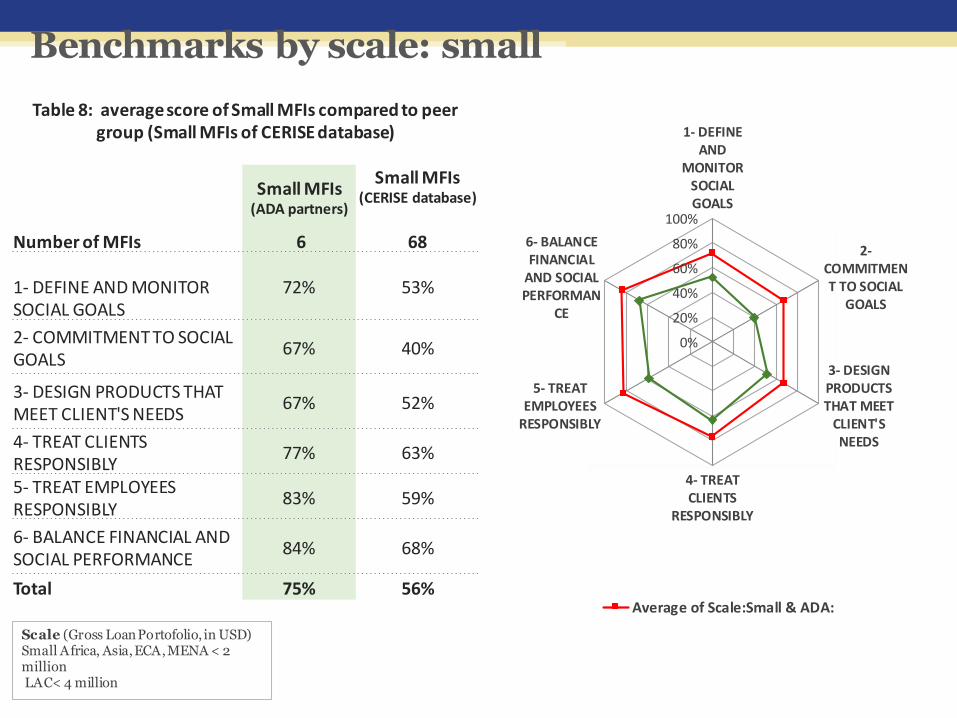

• Cooperatives/unions and small size MFIs recorded higher score for all the dimensions

0

20

40

60

80

1001

2

3

4

5

6

Average score by dimension

Average score Cerise-SPI4 database (N=184)Average score ADA(N=32)

Benchmarks by SSA region

Table 4: average score of SSA MFIs compared to peer group (SSA region of CERISE database)

SSA MFIs(ADA partners)

SSA MFIs(CERISE

database)

Number of MFIs7

60

1- DEFINE AND MONITOR SOCIAL GOALS

65% 50%

2- COMMITMENT TO SOCIAL GOALS

48% 37%

3- DESIGN PRODUCTS THAT MEET CLIENT'S NEEDS

56% 49%

4- TREAT CLIENTS RESPONSIBLY

60% 58%

5- TREAT EMPLOYEES RESPONSIBLY

57% 58%

6- BALANCE FINANCIAL AND SOCIAL PERFORMANCE

73% 66%

Total 60% 53%

0%

20%

40%

60%

80%

100%

1- DEFINEAND

MONITORSOCIALGOALS

2-COMMITMENT TO SOCIAL

GOALS

3- DESIGNPRODUCTSTHAT MEET

CLIENT'SNEEDS

4- TREATCLIENTS

RESPONSIBLY

5- TREATEMPLOYEES

RESPONSIBLY

6- BALANCEFINANCIAL

AND SOCIALPERFORMANC

E

Average of SSA & ADA:

Average of Most recent audit & SSA & ADA:CERISE database

Benchmarks by legal form: Cooperative/creditunion

Table 7: average score of Cooperative/ Credit Union MFIs compared to peer group (Cooperative/ Credit Unionof

CERISE database)

Coop/creditunion MFIs

(ADA partners)

Coop/creditunion MFIs

(CERISE database)

Number of MFIs 6 45

1- DEFINE AND MONITOR SOCIAL GOALS

72% 48%

2- COMMITMENT TO SOCIAL GOALS

62% 38%

3- DESIGN PRODUCTS THAT MEET CLIENT'S NEEDS

69% 54%

4- TREAT CLIENTS RESPONSIBLY

77% 61%

5- TREAT EMPLOYEES RESPONSIBLY

70% 56%

6- BALANCE FINANCIAL AND SOCIAL PERFORMANCE

79% 67%

Total 71% 54%

0%

20%

40%

60%

80%

100%

1- DEFINE ANDMONITOR SOCIAL

GOALS

2- COMMITMENTTO SOCIAL GOALS

3- DESIGNPRODUCTS THATMEET CLIENT'S

NEEDS

4- TREAT CLIENTSRESPONSIBLY

5- TREATEMPLOYEES

RESPONSIBLY

6- BALANCEFINANCIAL AND

SOCIALPERFORMANCE

Average of Cooperative/ Credit Union & ADA:

Average of Most recent audit & Cooperative/ Credit Union& ADA:CERISE database

Benchmarks by scale: small

Scale (Gross Loan Portofolio, in USD) Small Africa, Asia, ECA, MENA < 2 millionLAC< 4 million

Table 8: average score of Small MFIs compared to peer group (Small MFIs of CERISE database)

Small MFIs(ADA partners)

Small MFIs(CERISE database)

Number of MFIs 6 68

1- DEFINE AND MONITOR SOCIAL GOALS

72% 53%

2- COMMITMENT TO SOCIAL GOALS

67% 40%

3- DESIGN PRODUCTS THAT MEET CLIENT'S NEEDS

67% 52%

4- TREAT CLIENTS RESPONSIBLY

77% 63%

5- TREAT EMPLOYEES RESPONSIBLY

83% 59%

6- BALANCE FINANCIAL AND SOCIAL PERFORMANCE

84% 68%

Total 75% 56%

0%

20%

40%

60%

80%

100%

1- DEFINEAND

MONITORSOCIALGOALS

2-COMMITMENT TO SOCIAL

GOALS

3- DESIGNPRODUCTSTHAT MEET

CLIENT'SNEEDS

4- TREATCLIENTS

RESPONSIBLY

5- TREATEMPLOYEES

RESPONSIBLY

6- BALANCEFINANCIAL

AND SOCIALPERFORMAN

CE

Average of Scale:Small & ADA:

4 4

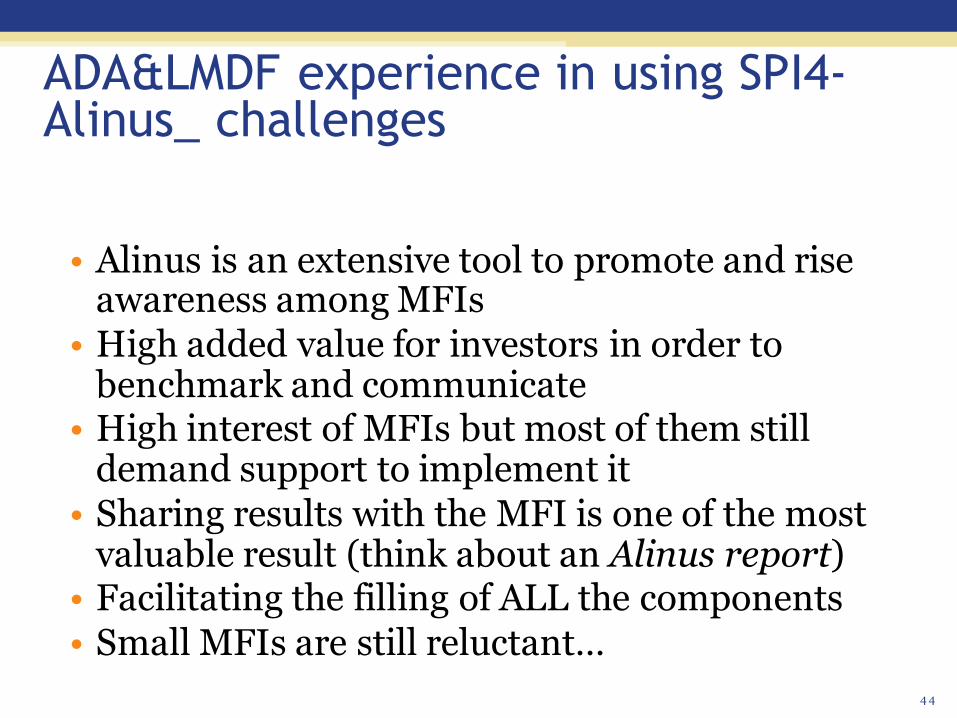

ADA&LMDF experience in using SPI4-Alinus_ challenges

• Alinus is an extensive tool to promote and rise awareness among MFIs

• High added value for investors in order to benchmark and communicate

• High interest of MFIs but most of them still demand support to implement it

• Sharing results with the MFI is one of the most valuable result (think about an Alinus report)

• Facilitating the filling of ALL the components• Small MFIs are still reluctant…

Agenda• 9.30-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Assess E&S in SME finance institutions

May 2018

Lucia Spaggiari, Business Development Director, MicroFinanza Rating

4 7

"The bigger is the enterprise, the more you need to understand the enterprise in addition to the entrepreneur." Matthew Gamser, CEO of the SME Finance forum

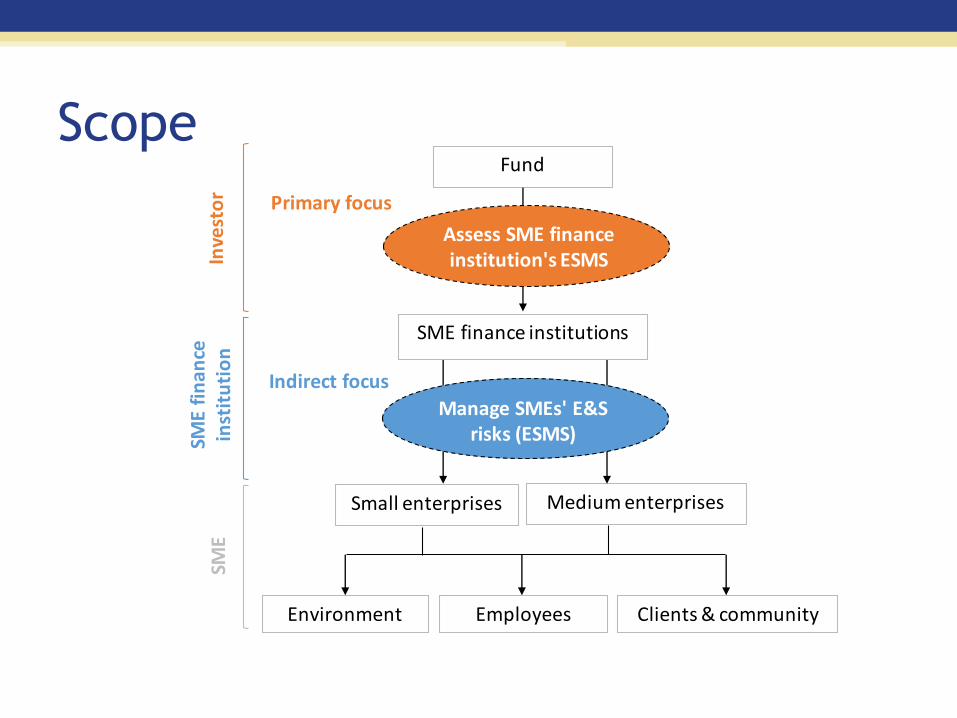

Scope

SME finance institutions

Fund

Assess SME finance institution's ESMS

Small enterprises Medium enterprises

Environment Employees Clients & community

Manage SMEs' E&S risks (ESMS)

Inve

sto

rSM

E fi

nan

ce

inst

itu

tio

nSM

EPrimary focus

Indirect focus

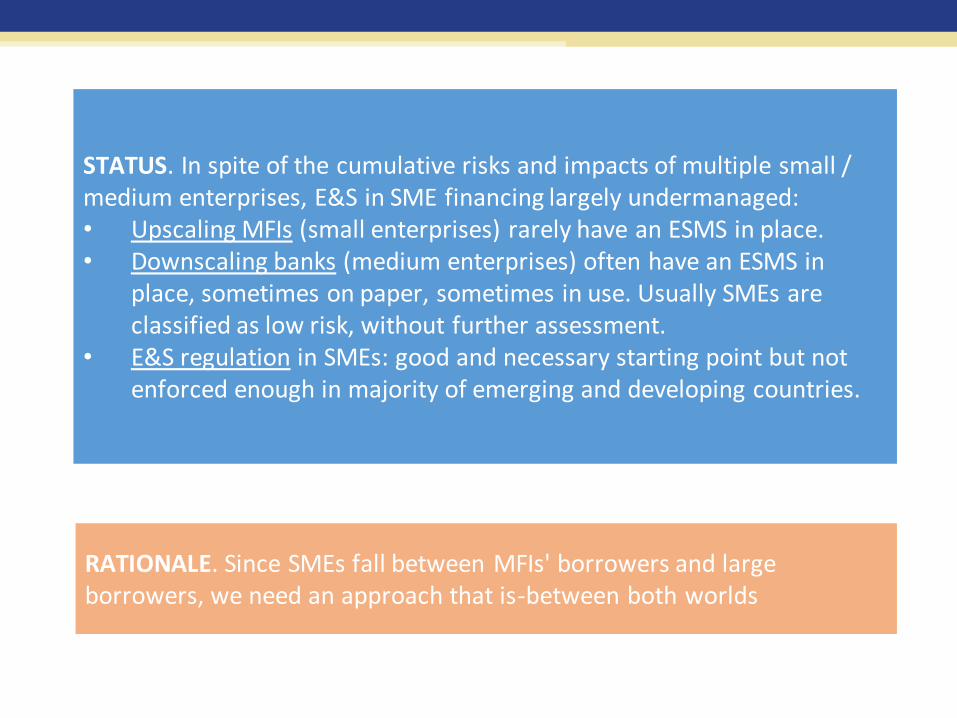

STATUS. In spite of the cumulative risks and impacts of multiple small / medium enterprises, E&S in SME financing largely undermanaged: • Upscaling MFIs (small enterprises) rarely have an ESMS in place.• Downscaling banks (medium enterprises) often have an ESMS in

place, sometimes on paper, sometimes in use. Usually SMEs are classified as low risk, without further assessment.

• E&S regulation in SMEs: good and necessary starting point but not enforced enough in majority of emerging and developing countries.

RATIONALE. Since SMEs fall between MFIs' borrowers and large borrowers, we need an approach that is-between both worlds

Objective

✓Promote Environmental and Social Management Systems (ESMS) commensurate to SMEs, that support incremental improvement of SMEs E&S practices.

X Not only about exclusion

X Achieving alignment with good E&S practices requires a pragmatic approach

ESMS = Environmental and Social Management System

Risks but alsoopportunities

Principle 1: Modular

Modularity allows having a common ESMS framework applicable to FSPs financing very different types of SMEs.

SAME. ESMS framework, logic and process.

DIFFERENT. Definitions, depth of analysis.

E.g. E&S checklists will always be integrated in loan appraisals. But: the high risks checklist of an FSP financing small enterprises will be very basic compared to the one of an FSP financing medium enterprises

Principle 2: Commensurate

Opportunity.Use the ESMS to turn gaps into opportunities and prioritize measures with a positive impact on E&S, business performance and business capacity to meet loan repayments.

ESMS should be commensurate to:

✓E&S risks/impacts faced by the FI (driven by the borrowers’ activities, regional/local contextual risks)

ESMS should take into consideration:✓type of financing

✓leverage the FI has in obtaining mitigation measures from borrowers

✓E&S opportunities

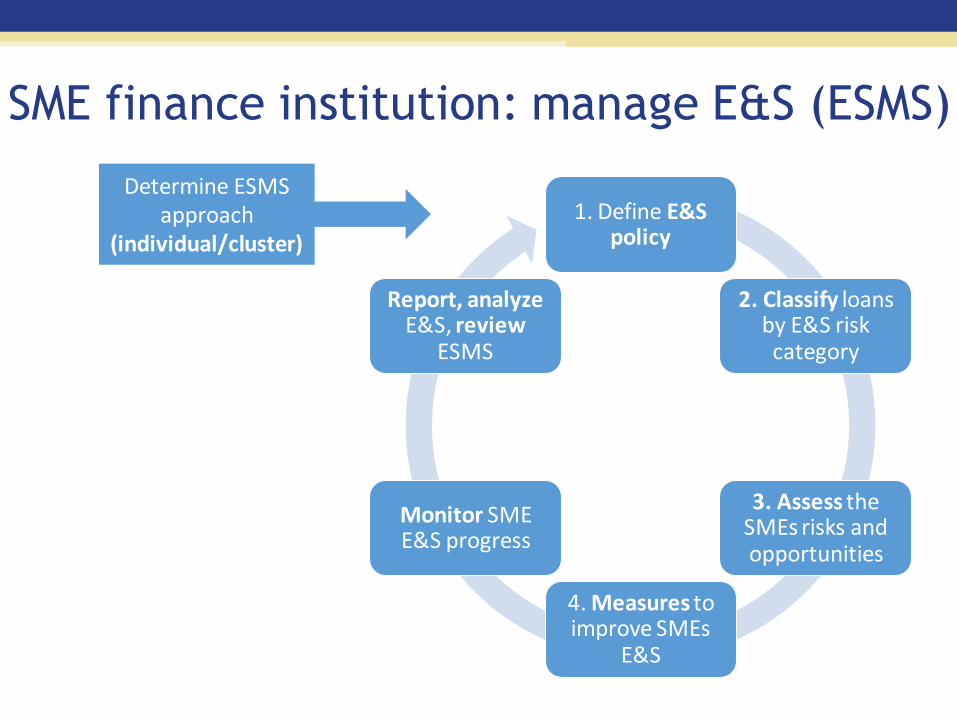

SME finance institution: manage E&S (ESMS)

1. Define E&S policy

2. Classify loans by E&S risk category

3. Assess the SMEs risks and opportunities

4. Measures to improve SMEs

E&S

Monitor SME E&S progress

Report, analyzeE&S, review

ESMS

Determine ESMS approach

(individual/cluster)

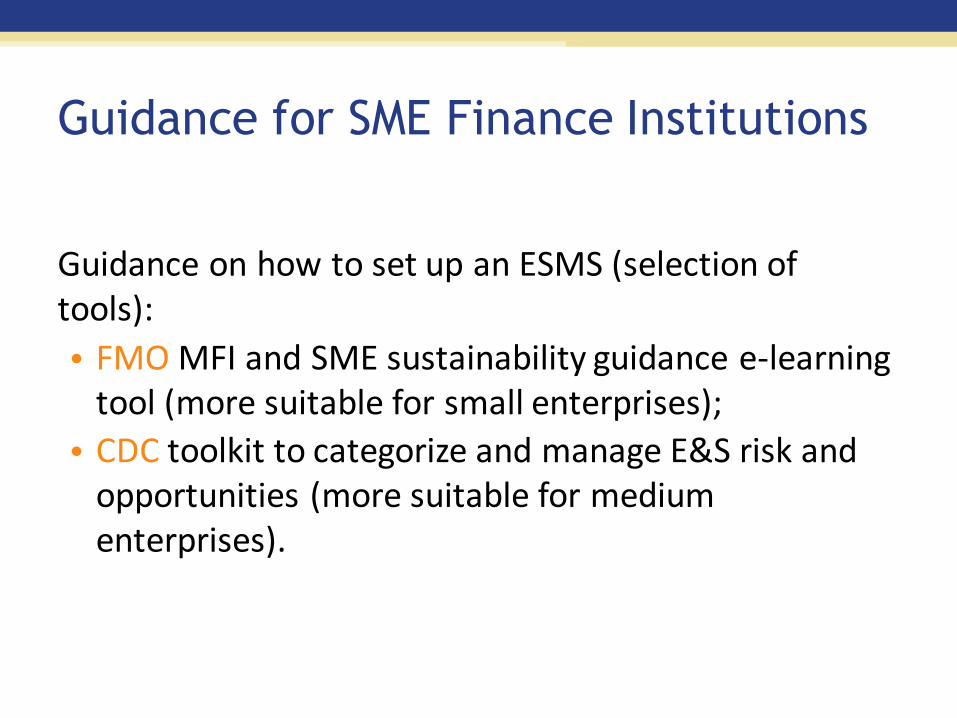

Guidance for SME Finance Institutions

Guidance on how to set up an ESMS (selection of tools):

• FMO MFI and SME sustainability guidance e-learning tool (more suitable for small enterprises);

• CDC toolkit to categorize and manage E&S risk and opportunities (more suitable for medium enterprises).

FMO

sectoral

matrix

…

…

CDC

sectoral

matrix

Investor: assess SME finance

institutions’ E&S

1. Identify SME

2. Identify SME finance institutions

3. Classify SME finance

institutions by E&S category

4. Assess the Sustainable

performance of SME finance

institutions

5. Promotethe

improvementof the SME

finance institutions'

systems

6. Monitor the

improvement of SME finance

institutions systems

1. Identify SME

a. Common definition of SMEs for all investments in all countries

b. National definition of SME for all investments in the same country;

c. Adopt the definition of SME used by each investee;d. Adopt the definition provided by the fund investor

2. Identify SME finance institutions

a. Adopt a common definition of SME finance institution(e.g.: >50% outstanding portfolio in SMEs) and of MFI with a SME component (e.g. >20%-30% outstanding portfolio in SMEs).

b. Adopt the way investees define themselves

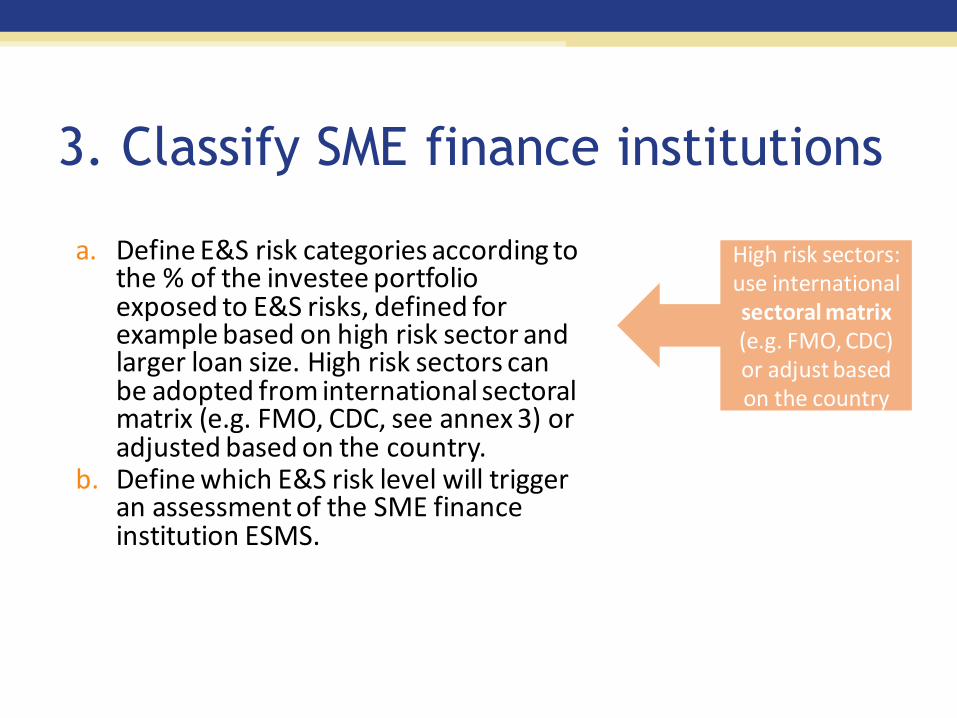

3. Classify SME finance institutions

a. Define E&S risk categories according to the % of the investee portfolio exposed to E&S risks, defined for example based on high risk sector and larger loan size. High risk sectors can be adopted from international sectoral matrix (e.g. FMO, CDC, see annex 3) or adjusted based on the country.

b. Define which E&S risk level will trigger an assessment of the SME finance institution ESMS.

High risk sectors: use international sectoral matrix(e.g. FMO, CDC) or adjust based on the country

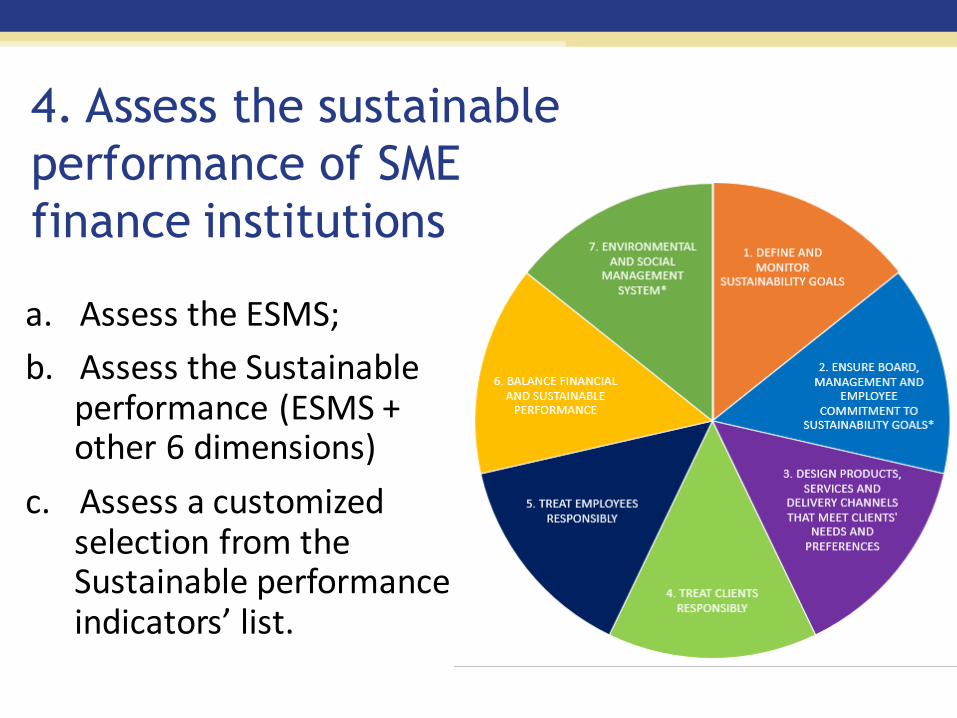

4. Assess the sustainable

performance of SME

finance institutions

a. Assess the ESMS;

b. Assess the Sustainable performance (ESMS + other 6 dimensions)

c. Assess a customized selection from the Sustainable performance indicators’ list.

5. Promote the ESMS improvement

a. Agree on E&S Action Plans to improve the ESMS based on the assessment;

b. Investor leverage to promote improvements depends on the type of financing (debt / equity; short / long term) and TA to support the ESMS development

6. Monitor the ESMS improvement

a. Monitor the improvement of SME finance institutions ESMS during the course of the loan or at loan renewal

at responsAbility Investments AGOUR APPROACH TO ESG

Pedro FernándezJune 18th, 2018

How we Manage ESG Issues

74

responsAbility’s ESG POLICY

Available on our website:https://www.responsability.com/sites/default/files/2017-09/ESG%20Policy.pdf

a System Based on International Standards

• Implemented by Investment Teams w/ support

• Content based on International Standards

75

ESG ASSESSMENT @ responsAbility

ESG Policy ESG Guidelines ESG Scorecards & Tools

Progressive Throughout the Investment Process

76/6

ESG ASSESSMENT @ responsAbility

Cr

ed

it A

na

lysi

s /

Inv

estm

ent

Com

mit

tee

Compliance with Exclusion List and

Reputational CheckCategorizeCounterpart

y on E&S Risk

MediumE&S Risk

Validate ESG Assessment

DefineESG Action

Plan

Monitor ESG Performance

Evaluate Anti-Money Laundering and Governance

Practices

Check HR / Labor Practices

Record Key

Findings

Evaluate

Client Protection

HighE&S Risk

LowE&S Risk

Assess Environmental & Social Practices

76

Depth and Length Defined by Risk LevelOUR ESG ASSESSMENT IS ALSO MODULAR

MediumE&S Risk

HighE&S Risk

LowE&S Risk

Governance Client Protection Social Environment

& other sources

77

responsAbility Investments AG | Josefstrasse 59 | 8005 ZürichTel. +41 44 250 99 30 | Fax +41 44 250 99 31 | [email protected]

© 2018 responsAbility Investments AG. All rights reserved.

Agenda• 9.30-9.45: Welcome remarks

• 9.45-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Coordination with broader impact

investing sector initiatives

• Overview of Initiatives: UNPRI Market Maps, EIL, Navigating Impact Project

• Introduction to Navigating Impact Project: Overview of key participants and work involved

• Introduction to Panelists

• Q&A

Agenda

8 1

As impact investing continues to grow, several

initiatives are working to help investors navigate

the different investment opportunities

SPTF is coordinating efforts with these initiatives to help shape the tools and resources being developed on financial inclusion

8 2

Why is SPTF involved and how is this

relevant to you?

8 3

• Share the experience of financial inclusion

▫ Collaboration, working towards common objectives

▫ Development and implementation of standards, common audit and monitoring tools, advancement of outcomes management work, etc

• Financial inclusion is a large sector of impact investment and can help pave the way of less-mature sectors – seen as “example”

• Ensure coordination with broader impact investment initiatives – as prioritized by many of you

• Opportunity to shape frameworks and tools that can be used by asset owners and investors throughout the broader investments sector

8 4

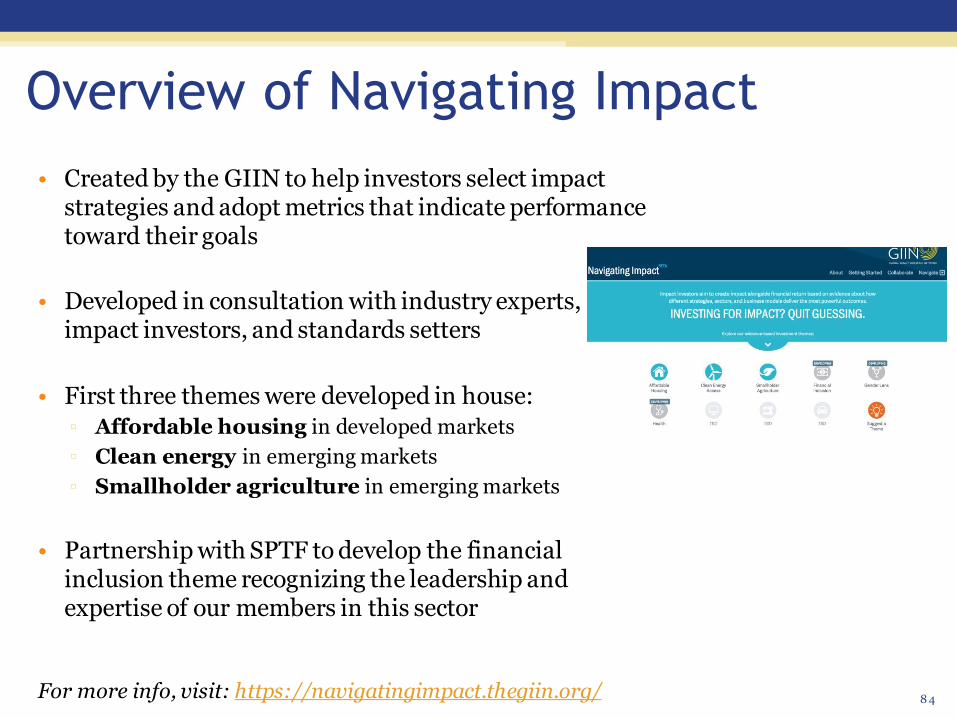

• Created by the GIIN to help investors select impact strategies and adopt metrics that indicate performance toward their goals

• Developed in consultation with industry experts, impact investors, and standards setters

• First three themes were developed in house:

▫ Affordable housing in developed markets

▫ Clean energy in emerging markets

▫ Smallholder agriculture in emerging markets

• Partnership with SPTF to develop the financial inclusion theme recognizing the leadership and expertise of our members in this sector

For more info, visit: https://navigatingimpact.thegiin.org/

Overview of Navigating Impact

Select your objectives

Or explore all strategies

Signposts to SDGs

Aligned with IMP’s Dimensions of Impact:

What, Who, How Much, Contribution, Risk

Evidence mapped by outcome/impact

“Starter kit” of 5-10 core metrics

Additional metrics for more targeted IMM

Financial Inclusion : ~50 collaborators

8 8

• Alterfin – Caterina Giordano

• Best Seller Foundation - Christian Wandel

• Blue Orchard – Lisa Sherk & Nadina Stodiek

• CERISE – Cecile Lapenu & Jon Salle

• CGAP – Mayada El-Zoghbi

• Community Investment Management – Jacob Haar

• EDA Rural – Frances Sinha

• EVPA – Priscilla Boiardi & Alessia Gianoncelli

• FM BBVA - Stephanie Garcia Van Gool

• Gawa Capital – Luca Torre

• Grameen Foundation - Devahuti Choudhury & Bobbi Gray

• Grassroots – Anna Kanze

• ILO – Patricia Ritcher

• Innpact – Asish Sharma & Adriana Balducci

• IPA – Rebecca Rouse, Lisa Corsetto, Julie Peachey

• JPAL – Lucia Diaz-Martin, Clara Walsh

• MicroSave - Jennifer Shapiro, Akhand Tiwari, Bhavana Srivastava, Joyce Murithi & Anup Singh

• Microvest – Tanay Tatum-Edwards

• NMI – Lone Søndergaard

• Oikocredit – Mitzi Perez Padilla

• Opportunity International – Calum Scott

• Pacific Community Ventures – Daniel Brett

• Quona Capital – Allison Steitz & LizannFernandez

• responsAbility - Pedro Fernandez Diaz & Paul Hailey

• Triple Jump– Christophe Bochatay & Andres Van del Linden

• UNCDF – Heew Kim

• University of Zurich – Annette Krause

• Womens World Banking – Jaclyn Berfond

8 9

Financial Inclusion: 5 strategies

• Improve access and usage of responsible financial services for historically underserved populations1

• Improve financial health2

• Support creation of quality jobs and foster economic development3

• Increase Gender Equality Through Financial Inclusion4

• Improve rural prosperity 5

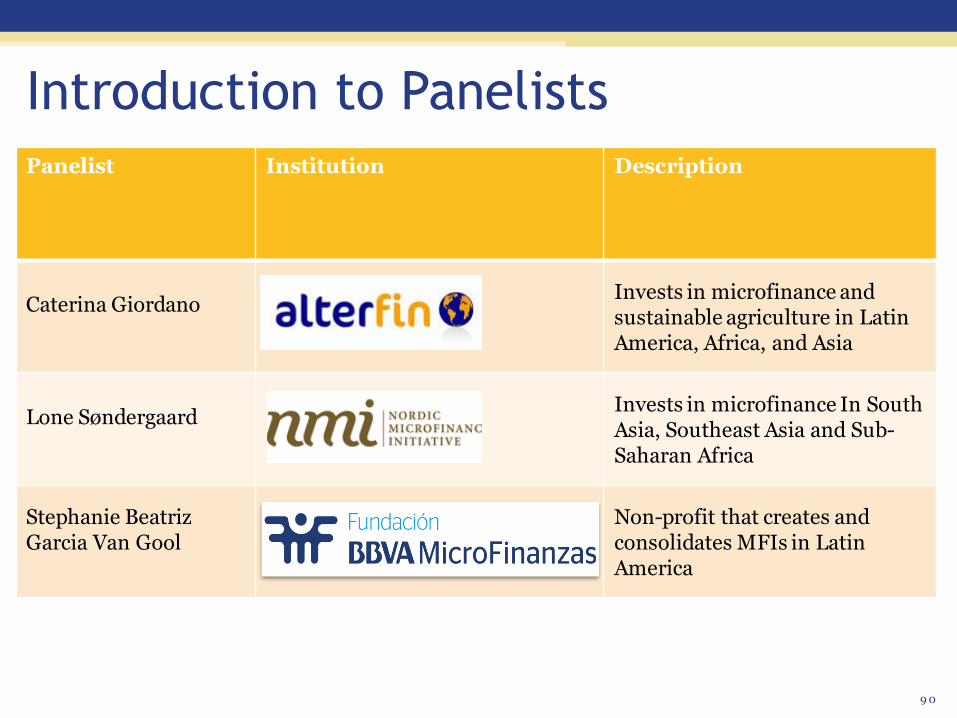

Panelist Institution Description

Caterina GiordanoInvests in microfinance and sustainable agriculture in Latin America, Africa, and Asia

Lone SøndergaardInvests in microfinance In South Asia, Southeast Asia and Sub-Saharan Africa

Stephanie Beatriz Garcia Van Gool

Non-profit that creates and consolidates MFIs in Latin America

9 0

Introduction to Panelists

9 1

Questions?

Agenda• 9.30-9.45: Welcome remarks

• 9.45-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Smart Campaign OID tool for India

Examining Over indebtedness : Triangulation approach

Reasons for heating up of markets and client issues

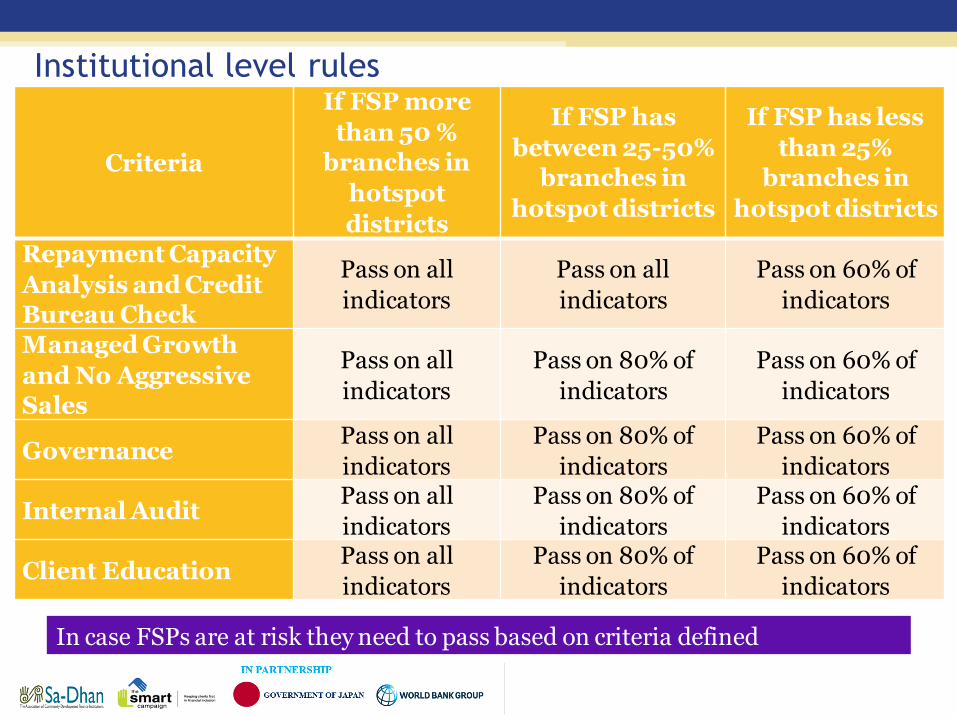

Institutional Level Approach MFIs with High Risks

‘Hotspots’ at state/district level

Market Level Approach

Institutional level: in high risk

areas, identify providers with high

exposures and weak policies and

procedures to prevent OID

Market level: identify high risk

areas

Client level: in high risk areas, survey

clients to identify reasons for OID and

priority issues

Each Rule is assessed by 3-4 criteria with benchmarks. For example:

Rule 10: Write Off Ratio:- More than 10% - Between 6 to 10% - Between 2 to 5%

- Less than 1%

Benchmarking: Based on pilot and historical data from industry

Market level rules

Rules (Applies for States/Districts)

Rule 1: Top 10 (% of total account to working population).

Rule 2: % of total account to total population.

Rule 3: Highest total account and HDI lower than national average.

Rule 4: More than 3+ loans.

Rule 5: % of clients with defaults on existing loans.

Rule 6: Lowest 5 (% of borrowers with first loans).

Rule 7: Portfolio growth versus client outreach growth.

Rule 8: Outreach & Portfolio growth versus branch and field staff growth.

Rule 9: PAR > = 30 days.

Rule 10: Write Off Ratio.

Rule 11: Refinancing loans.

Rule 12: % of loan rejection.

Criteria

If FSP more

than 50 %

branches in

hotspot

districts

If FSP has

between 25-50%

branches in

hotspot districts

If FSP has less

than 25%

branches in

hotspot districts

Repayment Capacity

Analysis and Credit

Bureau Check

Pass on all

indicators

Pass on all

indicators

Pass on 60% of

indicators

Managed Growth

and No Aggressive

Sales

Pass on all

indicators

Pass on 80% of

indicators

Pass on 60% of

indicators

GovernancePass on all

indicators

Pass on 80% of

indicators

Pass on 60% of

indicators

Internal AuditPass on all

indicators

Pass on 80% of

indicators

Pass on 60% of

indicators

Client EducationPass on all

indicators

Pass on 80% of

indicators

Pass on 60% of

indicators

Institutional level rules

In case FSPs are at risk they need to pass based on criteria defined

Mystery Shopping : Voice from the Field

• Develop survey using MIMOSA client

survey and MCWG (PRFI) Risk Study.

• Administer survey on field staff and

clients in the hotspot areas.

• Analyze results to inform priority issues.

➢ Survey will help understand drivers of OID,

such as the level of competition amongst

FSPs, capacity and commitment of field

staff, reasons for client default, stress levels

at client level and other issues that could

drive OID.

Platform for digitization of the OID Tool

Collect, clean and structure data to perform analysis through intuitive user

interface without writing a codeUnderstand data

Reports - Sample

Next steps

Roll-out and usage:

• Sa-Dhan – SRO

• Financial Service Providers

• Reserve Bank of India, SIDBI

Improvement of the tool:

• Identify priority areas

• Dig deeper on these areas – e.g., integration of lender guideline monitoring report (adapt Cambodia guidelines) for more details on multiple borrowing, refinancing, and loan to income

Can self-regulation work in overheating

markets?

Lessons from the Lender Guidelines project in

Cambodia

• SPTF Investor Working Group

• Luxembourg, June 2018

Boom Bust

102

SPTF IWG -Lu xembourg, June 2018

GDP

Credit

Ponzi Finance

Hyman Minsky Financial Instability Hypothesis

103

Self-regulation: India, 2010

SPTF IWG - Lu xembourg, June 2018103

So how do you self-regulate?

SPTF IWG -Lu xembourg, June 2018

104

SPTF IWG - Lu xembourg, June 2018105

Self-Regulation

Met

rics

Mo

nit

ori

ng

Sa

nct

ion

s

SPTF IWG - Lu xembourg, June 2018106

Metrics:

Multiple borrowing

Refinancing

Loan-to-income ratio

SPTF IWG - Lu xembourg, June 2018107

SPTF IWG - Lu xembourg, June 2018108

SPTF IWG - Lu xembourg, June 2018109

SPTF IWG - Lu xembourg, June 2018110

Independent monitoring:

Credit Bureau of Cambodia (dashboard)

Rating agencies (Smart certifications &

ratings)

SPTF IWG - Lu xembourg, June 2018111

Oversight & Sanctions:

Investors

Smart Campaign

Central Bank (?)

SPTF IWG - Lu xembourg, June 2018112

Weaknesses:

Cheating

Outside competition

SPTF IWG - Lu xembourg, June 2018113

Lender GuidelinesL

G D

ash

bo

ard

CB

C/R

ate

rs

Inve

sto

rs/S

ma

rt

SPTF IWG - Lu xembourg, June 2018114

Only one long-term solution:

Formal regulation

SPTF IWG - Lu xembourg, June 2018115

Thank you!

Agenda• 9.30-9.45: Welcome remarks

• 9.45-10.25: Overview of key trends, opportunities, and challenges

• 10.25-10.40: Update on current topics for SPTF and SIWG

• 10.40-11:00: Coffee Break

• 11.00-12.00: SPI4 and ALINUS

• 12.00-13.00: Assessing S&E performance of SME finance

• 13.00-14.00: Lunch

• 14.00-15.00: Coordination with broader initiatives and linking to SDGs

• 15.00-16.00: Over-indebtedness and Lenders Guidelines

• 16.00-16.20: Coffee Break

• 16.20-17.20: Joint session with InFiNe on Green Finance

• 17.20-17.35: Conclusions & Plan for Day 2

Green Finance

Joint Session With:

Green Inclusive Finance

1 19

Agenda

→ Introduction InFine & SPTF

→ Panel discussion with → Triodos

→ Innpact

→ LuxFLAG

→ Discussion

Corinne Molitor, Innpact

Sachin Vankalas, LuxFLAG

Adysti Raissa Fitri, Triodos Investment

1) Approach to green inclusive finance

2) Measure & track green investments

Innpact – what we do

Investment Vehicle Design and

Structuring

Impact strategy and Methodology

STRUCTURING SERVICES

MANAGEMENT SERVICES

General Secretary -Board and

Governance Support

Fund Management Services

Independent Directorships

Investment Fund Advisory

Impact Investment Placement

INVESTMENT SERVICES

Triodos Investment Management

Exclusion list 61%

Green office procedure 39%

Green financial products 25%

Environmental training for

customers 18%

Donations for

environmental protection 11%

Triodos Green finance activities:• Investing in FIs that extend finance to entrepreneurs or activities that

create benefit to the environment or reduce harmful impact to the environment

• NpM Green Inclusive Finance working group• Current activities: developing a publication of case studies and a

paper on green indicator (Q4 2018)• Providing in-kind assistance to investees and organizing knowledge

sharing workshop on green finance

Environmental indicator -2017“Green Inclusive Finance comprisesfinancial services for the ultimate benefit of low incomepeople and communities, through such channelsas FIs, MSMEs,, cooperatives etc., in developingcountries and emergingeconomies, resulting in environmental benefits, whilemeeting societal needs and stimulatingsustainableeconomic growth.”

-NpM Green Inclusive Finance Working Group

Challenges & Needs

• What challenges have you encountered in mainstreaming green finance?

• And what do you need?

Source : www.ecobusiness.fund

Other funds with similar intermediaries approach :

managed by

1. Organic agriculture and agri-processing

2. Sustainable fishery and aquaculture

3. Sustainable forestry

4. Eco-tourism

• “Use of Proceeds” clause as part of loan

agreement with Financial Institution

• Disbursement only based on eligible

underlying loans

• Strong need of Technical Assistance

How about the investors in the

room?