smartquotes insurance research 2013

DESCRIPTION

Results of a survey of Irish consumers about drivers of insurance purchasing for Smartquotes. Further details here: http://www.smartquotes.ie/blog/TRANSCRIPT

Smartquotes Omnibus Research

A Presentation Prepared For smartquotes.ie

March 2013

By

MMCL/MG

S12-249

2

Research Methodology

Sample Profile

MAIN FINDINGS:

SECTION 1: Household Income

SECTION 2: Switching and Cancelation of Financial Products

SECTION 3: Household Charge

Table of Contents

3

A number of questions were placed on the Amárach Research March Omnibus to investigate trends in switching and cancellation of financial products. Additionally questions were also asked in relation to the Household charge which is being introduced in 2013. The omnibus survey is a syndicated survey whereby clients can include questions within the survey. A total sample of 1,018 was achieved with quotas set on gender, age, social class and region to achieve a sample aligned with national population. Due to the high proliferation of the internet among the Irish population, the Amárach Research omnibus is completed fully online. Interviewing fieldwork dates were March 15th – 22nd.

Research Methodology

4

Sample Profile

Male

Gender Age Social Class Region

% % % %

Female

15-24

35-44

45+

ABC1 F50+

C2DE F50-

Dublin

Rest of Leinster

Munster

Conn/ Ulster

25-34

(Base: All respondents - 1018)

55+

MAIN FINDINGS

SECTION 1: Household

Income

7

Household Financial Responsibility

Mainly

Responsible

Not

Responsible

Jointly

Responsible

Q: Are you responsible for managing the

finances of your household?

% €1 to €1000

€1001 to €2000

€2001 to €3000

€3001 to €4000

€4001 to €5000

€5001+

Don’t know

Refused

10

24

18

7

6

4

16

14

Q: What is your current monthly household

income after tax?

Responsibility of respondent in relation to managing finances

Current monthly household income after Tax

(Base: All respondents – 1018)

%

(Base: All responsible for

managing finances – 930)

8

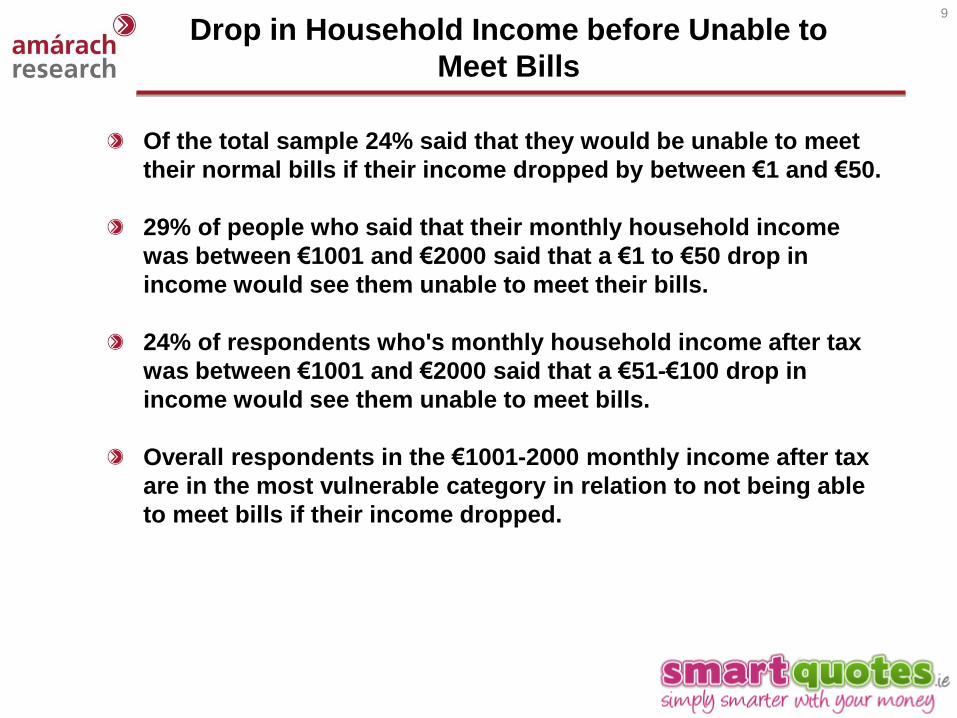

Drop in Household Income before Unable to

Meet Bills

Monthly Household Income

After Tax Total

*€1-

1000

€1001

-2000

€2001

-3000

*€3001

-4000

*€4001

-5000 *€5001+

Don’t

know

Refuse

d

Base 930 92 227 167 65 58 37 151 138

€1 to €50 drop in monthly income 24% 54% 29% 14% 19% 3% 11% 26% 19%

€51 to €100 drop in monthly income 21% 23% 24% 22% 5% 15% 15% 22% 24%

€101 to €150 drop in monthly income 17% 14% 19% 19% 17% 13% 5% 20% 12%

€151 to €200 drop in monthly income 12% 5% 12% 13% 12% 17% 10% 12% 15%

€201 to €300 drop in monthly income 9% 3% 7% 13% 10% 12% 8% 8% 12%

€301+ drop in monthly income 17% 0% 10% 19% 37% 39% 50% 12% 17%

Q: By how much would your monthly household income after tax have to fall before you would be unable to meet your

normal bills?

* Denotes small base size.

9

Of the total sample 24% said that they would be unable to meet

their normal bills if their income dropped by between €1 and €50.

29% of people who said that their monthly household income

was between €1001 and €2000 said that a €1 to €50 drop in

income would see them unable to meet their bills.

24% of respondents who's monthly household income after tax

was between €1001 and €2000 said that a €51-€100 drop in

income would see them unable to meet bills.

Overall respondents in the €1001-2000 monthly income after tax

are in the most vulnerable category in relation to not being able

to meet bills if their income dropped.

Drop in Household Income before Unable to

Meet Bills

SECTION 2:

Switching and Cancellation

of Financial Products

11

Financial Products – I

%

Car insurance

Home insurance

Health insurance

Life insurance

Mortgage protection

Pension contributions

Income protection

I hold no financial products

Q: Which of these financial products do you have?

(Base: All respondents – 1018)

% that have

cancelled

financial product

in past 12

months Car insurance 10% 10%

Home insurance 42% 7%

Health insurance 56% 19%

Life insurance 62% 9%

Mortgage protection 79% 3%

Pension contributions 82% 7%

Income protection 91% 5%

Products Held

(Base: Don’t have each financial

product)

Cancelled in past 12 months

Q: Have you cancelled any of these financial services in

the past 12 months?

% that do not have

financial product

mentioned

12

Financial Products – II

%

Car insurance

Home insurance

Health insurance

*Income protection

Life insurance

Mortgage protection

Pension

(Base: Those who held each

financial product - 894)

Switched Financial Products in past 12 months

%

Health insurance

Home insurance

Car insurance

Life insurance

Other

Downgrading of financial products

Q: Have you switched provider on any of these financial

services in the past 12 months ?

Q: Have you downgraded any of the following financial

policies in the past 12 months?

Other = mortgage protection, income protection and pension contributions

*Denotes small base

(Base: Those who held each

financial product - 894)

13

Why are Products being Cancelled? – I

%

No longer afford it

Other expenses were

more important

It was a product I

could do without

Bad experience with

provider

Q: Why did you cancel <insert financial product>?

(Base: All who cancelled

health insurance – 110)

Health Insurance

(Base: All who cancelled

pension contributions – 63)

(Base: All who cancelled life

insurance - 53)

Pension Contributions

Life Insurance

%

No longer afford it

Other expenses were

more important

Bad experience with

provider

It was a product I

could do without

%

No longer afford it

Other expenses were

more important

It was a product I

could do without

Bad experience with

provider

14

Why are Products being Cancelled? – II

%

No longer afford it

Other expenses were

more important

It was a product I

could do without

Bad experience with

provider

Q: Why did you cancel <insert financial product>?

(Base: All who cancelled

income protection – 45)

Income Protection

(Base: All who cancelled home

insurance – 27)*

(Base: All who cancelled

Mortgage Protection - 26)*

Home Insurance Mortgage Protection

%

No longer afford it

Other expenses were

more important

Bad experience with

provider

It was a product I

could do without

%

No longer afford it

Other expenses were

more important

It was a product I

could do without

Bad experience with

provider

* Denotes low base

15

Why are People Switching Financial Products – I

%

Saved money by doing so

Had bad experience with

previous provider

It was recommended to me

by a family member

Had other policies with the

company I switched to

(Base: All who switched car

insurance – 344)

Car Insurance

%

(Base: All who switched home

insurance in last 12 months – 165)

Home Insurance

Saved money by doing so

Had bad experience with

previous provider

It was recommended to me

by a family member

Had other policies with the

company I switched to

Q: Why did you switch provider on <insert financial product> in

the past 12 months?

16

Why are People Switching Financial Products – II

%

Saved money by doing so

It was recommended to me

by a family member

Had bad experience with

previous provider

Had other policies with the

company I switched to

(Base: All who switched health insurance

provider in last 12 months – 87)

Health Insurance

%

(Base: All who switched Life

insurance in last 12 months – 45)

Life Insurance

Saved money by doing so

It was recommended to me

by a family member

Had bad experience with

previous provider

Had other policies with the

company I switched to

Q: Why did you switch provider on <insert financial product> in

the past 12 months?

* Base too low for mortgage protection and income protection

17

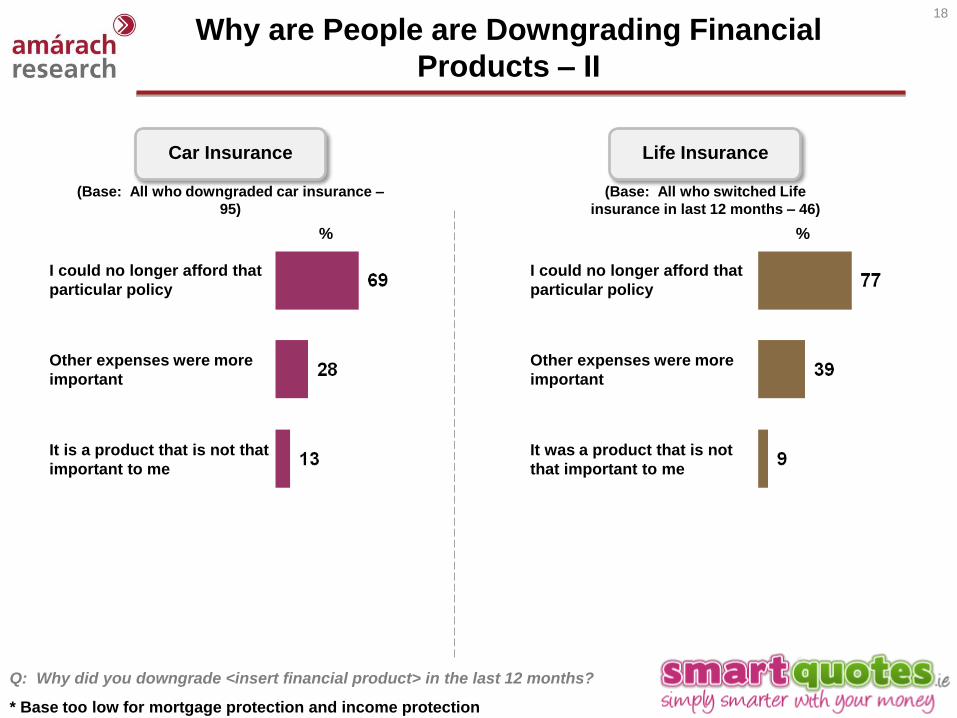

Why are People are Downgrading Financial

Products – I

%

I could no longer afford that

particular policy

Other expenses were more

important

It is a product that is not that

important to me

(Base: All who downgraded health

insurance – 135)

Health Insurance

%

(Base: All who switched Life

insurance in last 12 months – 45)

Home Insurance

I could no longer afford that

particular policy

Other expenses were more

important

Our house value has fallen

It was a product that is not

that important to me

Q: Why did you downgrade <insert financial product> in the last 12 months?

18

Why are People are Downgrading Financial

Products – II

%

I could no longer afford that

particular policy

Other expenses were more

important

It is a product that is not that

important to me

(Base: All who downgraded car insurance –

95)

Car Insurance

%

(Base: All who switched Life

insurance in last 12 months – 46)

Life Insurance

I could no longer afford that

particular policy

Other expenses were more

important

It was a product that is not

that important to me

Q: Why did you downgrade <insert financial product> in the last 12 months?

* Base too low for mortgage protection and income protection

19

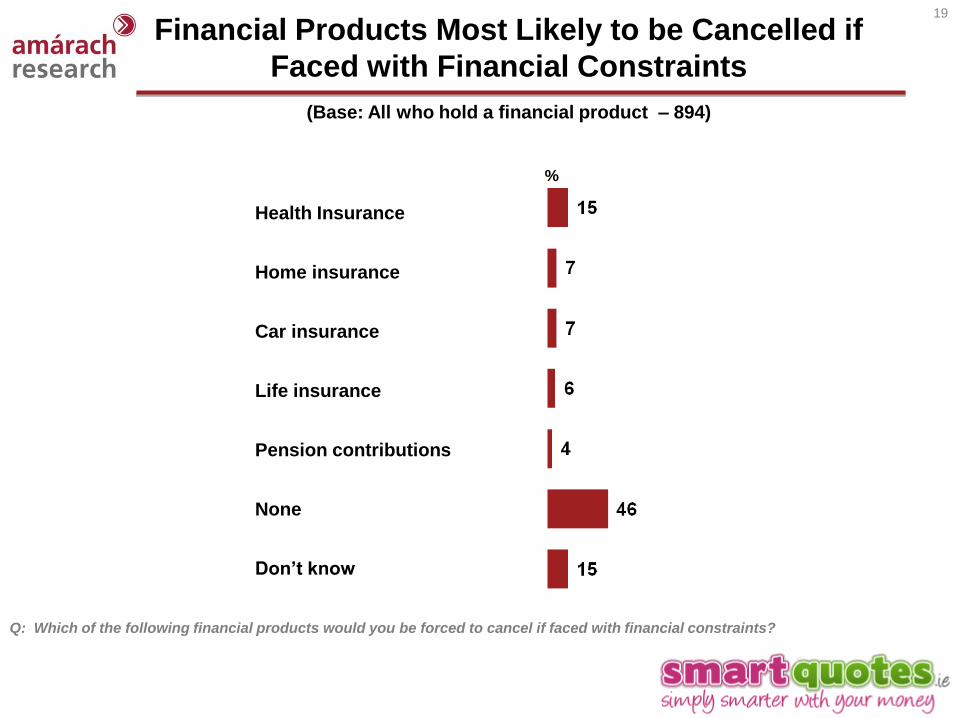

Financial Products Most Likely to be Cancelled if

Faced with Financial Constraints

%

Health Insurance

Home insurance

Car insurance

Life insurance

Pension contributions

None

Don’t know

Q: Which of the following financial products would you be forced to cancel if faced with financial constraints?

(Base: All who hold a financial product – 894)

SECTION 3: Household

Charge

21

Household Charge

Yes Don’t know

No

Q: Do you currently own the home that you

are living in?

%

€50-€100

€101-€200

€201-€300

€301-€400

€401-€500

€501-€1000

€101+

Don’t know

Owns

home

Q: How much do you think you will have to

pay in property tax in 2013?

Do you own your home?

Property tax

%

(Base: All respondents – 1018)

Own it

jointly

(Base: All who own home – 614)