small and medium enterprises (smes): past, present...

TRANSCRIPT

1

Small and Medium Enterprises (SMEs): Past, Present and Future in India

KD Raju

Abstract

SMEs form the backbone of the Indian manufacturing sector and have become engine of

economic growth in India. It is estimated that SMEs account for almost 90% of industrial units in

India and 40% of value addition in the manufacturing sector. This paper closely analyses the

growth and development of the Indian mall scale sector from opening of the economy in 1991.

Third part looks into the present scenario of SMEs and the problems they phases like lending,

marketing, licenseraj issues in detail. The Micro, Small and Medium Enterprises Act, 2006 is

intended to boost the sector. The provisions of the Act are examined closely. The final part

provides some future policy framework for the sustainability of the sector.

I. Introduction

Small industry has been one of the major planks of India's economic development strategy

since Independence. India accorded high priority to small and medium enterprises (SMEs)

from the very beginning and pursued support policies to make these enterprises viable and

vibrant and over time, these have become major contributors to the GDP. Despite

numerous protection and policy measures for the past so many years, SMEs have

remained mostly small, technologically backward and lacking in competitiveness. The

opening of the Indian economy in 1991 added problems to the SMEs. At the beginning,

small scale enterprises found it difficult to survive. In the last decade, the economic

environment has changed in favour of SMEs. Presently, the SMEs in India are at a cross-

road and intense debate is centered around questions like what would be the future of the

small enterprises? How these enterprises can survive in the international trade arena?

2

What role can the government play in making these SMEs more competitive? In this

context, it is important to re-look into the basic issues of SMEs, past, present and future

prospects, especially in the policy framework.

Today, small and medium industry occupies a position of strategic importance in the

Indian economic structure due to its significant contribution in terms of output, exports and

employment. The small scale industry accounts for 40% of gross industrial value addition

and 50% of total manufacturing exports. More than 3.2 million units are spread all over the

country producing about 8000 items, from very basic to highly sophisticated products. The

SMEs are the biggest employment-providing sectors after agriculture, providing

employment to 29.4 milllion people. However SMEs, which constitute more than 90% of

total number of industrial enterprises, are now facing a tough competition from their global

counterparts due to liberalization, change in manufacturing strategies, technological

changes, and turbulent and uncertain market scenario.

This contribution is despite the sector being exposed to intensified competition since

liberalisation of Indian economy in 1991. Small industry in India has been confronted with

an increasingly competitive environment due to: (1) liberalisation of the investment regime

in the 1990s, favouring foreign direct investment (FDI); (2) the formation of the World Trade

Organisation (WTO) in 1995, forcing its member-countries (including India) to drastically

scale down quantitative and non-quantitative restrictions on imports, and (3) domestic

economic reforms. The cumulative impact of all these developments is a remarkable

transformation of the economic environment in which small industry operates, implying that

the sector has no option but to 'compete or perish'.

This paper is an attempt to discuss the following questions:

3

- Why should global and national policy developments affect small industry in India,

and how? What are its implications?

- How far has small industry been able to cope with the present competitive

environment?

- What are the future prospects of small industry in India in the era of globalisation?

- What steps need to be taken to strengthen small industry to ensure its sustained

contribution to Indian economy?

The definition of medium enterprises is a recent entrant in India, and part of

Government’s policy focus lately. The small scale segment is a manifestation of India’s

socio-economic development model and has met with the country’s long-term expectations

in terms of contribution to GDP, industrial base, employment and exports. This segment

forms a major part of India’s industrial base.

Recognising the importance of SMEs in the industrial development of the country,

the Government has initiated a range of programmes in diverse areas, viz. financing,

technology, innovation, market information, technical training and developmental

assistance. These initiatives are important in facilitating the growth of SMEs. But it will be

the internal dynamics of industries, and the path India’s industrial development takes, that

will give a thrust to the development of SMEs.

II. Liberalisation and Impact on SMEs

The decade of the 1990s was an eventful one in terms of policy changes, nationally as well

as internationally. Since the beginning of the 1990s, policy changes have been taking

place at three different levels - global, national and sectoral - which have implications for

small industry functioning and performance in India. The first and the foremost development

4

is the 'globalisation' process at the international level. Globalisation would mean free

movement of inputs (both labour and capital) as well as output between countries.

According to Stiglitz (2002), globalisation is the closer integration of the countries and

peoples of the world, which has been brought about by the enormous reduction of costs of

transportation and communication, and the breaking down of artificial barriers to the flow of

goods, services, capital, knowledge, and (to a lesser extent) people across borders.

However, the developments that have been taking place since the early 1990s are mostly

with reference to the free movement of only one of the factor inputs - capital, commonly

known as FDI and free movements of goods, more from developed to developing countries.

The formation of the World Trade Organisation (WTO) in 1995 has accelerated the

process of scaling down of tariff and non-tariff restrictions on imports. India, as a member of

the WTO, had substantially done away with its quantitative restrictions. As a result, industry

has had to face much stronger international competition. The process of removal of

quantitative and non-quantitative restrictions across countries has led to free movement of

goods between countries including India. As a result, world exports grew in dollar terms at

an average annual rate of 5.9 per cent during 1990-99 as against 5.2 per cent during 1980-

90 (MoF 2003). The reduction of restrictions on the movement of goods between countries

and the subsequent increase in world exports would have benefited multinational

corporations much more than small enterprises.

This has to be viewed along with the process of economic reforms launched by the

Indian government at the national level. This has resulted in considerable freedom for

enterprises, domestic as well as foreign, to enter, expand or diversify their investments in

Indian industry. India's economic reforms have seen two major outcomes, amongst others.

Firstly, the growth of the public sector has declined considerably since 1991 than in the

5

earlier period in terms of not only investment and employment but also production. The

public sector has been a major customer of small enterprises in India. The relative role of

the public sector as a distinct entity will decline further in the course of the Tenth Plan. This

will most probably further bring down public sector demand for small industry products.

The introduction of an exclusive policy for small industry, which laid emphasis on

imparting more vitality and growth impetus to the sector, is the sectoral dimension of the

major policy changes relevant to small industry. The policy marked: (1) the beginning of the

end of protective measures for small industry, and (2) promotion of competitiveness by

addressing the basic concerns of the sector, namely, technology, finance and marketing.

Subsequently, the number of items reserved exclusively for small industry manufacturing

has been gradually brought down from 842 in 1991 to 239 in 2007.

Thus policy changes that have occurred at the global, national and sectoral levels

have radically changed the environment for the functioning of small industry in India. The

growth of small industry in the country has to be analysed against this backdrop.

Small enterprises in India have come up in an unplanned, uncontrolled and

haphazard manner. They have emerged anywhere and everywhere – closer to the location

of resources as well as markets, in clusters as well as in a dispersed manner, in industrial,

commercial and residential areas. Of these, the 2000-odd small industry clusters vary in

size with a population ranging from 100 to 1,000 units. Approximately, these clusters would

account for 1/3 to ½ the total small industry units in the country. A considerable majority of

these clusters are based on natural and traditional skills. By and large, these clusters lack

reliable and efficient infrastructural facilities such as power, road, water, transportation and

communications, information and technical inputs. But the infrastructural problem is more

acute in case of units that are located in a dispersed manner.

6

The central issue of concern for the growth of small industry is how to strengthen its

competitiveness. First of all, if small industry has to thrive, infrastructural bottlenecks must

be overcome to enable it to compete on its inherent potential. And it is the responsibility of

the government to remove any structural bottleneck in small industry performance

especially when market forces are given prominence through the removal of ‘protective

elements’. It is essential to provide the much-needed ‘level playing field’ to small enterprises

through infrastructure development. But overcoming infrastructural bottlenecks for small

enterprises is easier said than done.

III. The SMEs in India: Present Scenario

In the recent past, small companies have performed better than their larger counterpart.

Between 2001-06, net companies with net turnover of Rs. 1 crore – 50 crore had a higher

growth rate of 701 per cent as compared to 169 per cent for large companies with turnover

of over Rs. 1,000 crore (Business World Jan. 2007). The total SSI production, which had

reached the all time high of Rs. 1,89,200 crores in 1989-90 dropped dramatically in the next

10 years and only in 2001-02 the level of production was surpassed. But after 2002, the

production has risen at a faster rate. Since 2000, there is a continuous growth in number

of units, production, employment and in exports. The average annual growth in the number

of units was around 4.1%. At the

Table I : Performance of Micro and Small Enterprises

Year No. of Units (in Lakh))_______________________ Regd. Unregd. Total

Production (Rs. Crore) (at current (at constant

prices) prices)

Employment (in lakh)

Exports (Rs. Crore)

2002-03

15.91 93.58 109.49 (4.1)

3,11,993 (10.5)

2,10,636 (7.7)

260.21 (4.4)

86,013 (20.7)

2003-04

16.97 96.98 113.95 (4.1)

3,57,733 (14.7)

2,28,730 (8.6)

271.42 (4.3)

97,644 (13.5)

2004-05

17.53 101.06 118.59 (4.1)

4,18,263 (16.9)

2,51,511 (10.0)

282,57 (4.1)

1,24,417 (27.4)

2005-06

18.71 104.71 123.42 (4.1)

4,76,201 (13.9)

2,77,668 (10.4)

294.91 (4.4)

N.A.

7

Note : Figures in parenthesis Indicate percentage growth over previous years

Source: Development Commissioner (SSI)

Today, some of the SMEs are acquiring companies abroad as part of the globalisation

process. Mostly, these units are ancillaries and are export oriented. The SME sector have

transformed to the need of large local manufacturers and suppliers to global manufacturers

like Auto Industry. Today some SMEs are investing in R&D in order to compete globally.

Outsourcing from multi-national companies has played a vital role in the emergence of

Indian SMEs as world leaders in specified products. The advantages in labour-intensive

manufacturing units, lower transport costs and lose labour policies of the small scale sector

have led to major outsourcing in manufacturing and services.

With the elimination of Multi Fibre Agreement (MFA)in 2005, lot of opportunities have

opened for the Indian textile sector. Presently, SMEs in this sector have shown an average

growth rate of 32% for the past two years. The auto component sector grew at an average

35% over the past two years and expects to maintain this momentum. Besides this sector,

food processing and construction have also been growing. The IT sector services is

another success story of SMEs. The retail business in India has become an area of

immense opportunity. In the retail sector, the SMEs will act as a supply source for the big

retailers like Reliance Retail, Big Bazar, etc.

The Indian experience with SMEs is common to other East Asian economies also.

The SMEs are acting as entrepreneural engines of growth in the whole of Asia. About 70%

of the employment growth comes from the SMEs in the Asian region. This is the case with

China, Vietnam and Indonesia, which are the rising countries in East Asia. It is expected

that this phenomena is also common in Europe and the US. The SMEs will provide major

8

employment all over the world. Even when SMEs are contributing so much to employment

generation and exports, the policy support and capital supply are not so encouraging in

countries like India.

The way forward would be to create an environment of risk-taking by the

government for providing a start-up capital to SMEs and to facilitate technology transfers

and training in skill development. The Micro, Small and Medium Enterprises Act, 2006 is a

legal framework for more capital investment in the SME sector. However, the

implementation of the Act would need more precision and authority with different agencies.

IV. Current Issues

i. Lending Facilities to SMEs

The mind set of banks towards SMEs have somewhat changed in the recent past. With the

entry of private banks, increased competition has led to a rush for lending to prime

customers. The multiple financial options from the capital market have also compelled

banks to take more risks in the case of SMEs. The increased lending to SMEs is propelled

by the compulsion of the market as well as by the rapid expansion of these companies.

There was no agreement among the banks on what constitutes an SME. This confusion

was removed by the new Act. But private and foreign banks have their own definition of

SMEs. They follow the International standard of turnover between Rs. 10 crore and Rs.

700 crore. The lending to the SME sector grew by 69% between 2000-01 and 2005-06.

But there exists a stark disparity amongst small players and big players within the SMEs

sector. Loans to bigger companies are growing at a faster pace than loans to the SSI

sector. By the end of 2006, the proportion of SSI loans to total loans has remained small at

6.4 per cent.

9

Presently, private banks are adopting new methodologies for priority lending to

SMEs. In the past, loans were made without proper study of the viability of the project and

mostly bankers in this sector had no expertise in handling small loans. Now private banks

like ICICI and Kotak Mahindra Bank have separate SMEs division. Today, most of the

lendings are concentrated on priority sectors like auto ancillaries, pharmaceuticals and IT

sector where India had a proven record of competitive advantage. The SMEs sector is still

facing an acute shortage of capital. It needs more pumping of money into capital

investment for further growth and competitiveness of SMEs. For further growth of the

SMEs, in addition of loan facilities, there is need for venture capital investment.

The Small Industries Development Bank of India (SIDBI) was set up in 1990 under

the Act of Indian Parliament as the principal financial institution for promotion, financing,

development of industry in the small sector and coordinating the financial activities of other

institutions engaged in similar activities. Since its inception, the bank is promoting SSI

sector to meet the requirement of setting up of new projects, expansion, diversification and

modernisation of the sector. However, after working more than 1-1/2 decades, the

institution has not proved to be sufficient to meet the requirement of SMEs in India. This

can be mainly attributed to the governmental clutches on the banks.

The main identified sources of finance to SSI units are:

• Public Sector/Commercial banks

• State Financial Corporations

• Small Industries Development Bank of India

• Informal sources

Out of these financial resources, banks are a preferred source of financing by virtue of their

better reach and accessibility. Two-thirds of the small entrepreneurs meet financial

10

requirements from their own funds and informal sources. They have to resort to other

sources of finance because raising finance from the financial institutions has the following

draw backs:

• The rate of interest charged is higher

• Insufficient collateral

• Restrictive and conditional working capital limits

• Time consuming and cumbersome procedures

• Indifferent attitude of the branch manager/staff

• Non-availability of assistance at banks for completion of forms and formalities

• The terms of credit are hard

• Improper assessment of requirements

• Arbitrary curtailments of credit limits

• Repeated and time consuming visits to banks

• Release of limits sanctioned in installments

ii. Marketing

Next to finance, marketing is the big problem area for small entrepreneurs. The survival of

small entrepreneurs very much depends on sound marketing techniques. One of the most

important tools in the hands of small entrepreneurs for promoting their sales is low prices

coupled with credit to buyers, which give rise to number of problems at a later stage.

Marketing as a profession has not yet developed in the SME sector. Professional agencies

are not engaged by small entrepreneurs on account of paucity of funds. The concept of

marketing is not known to the majority of small entrepreneurs. For majority, marketing

means advertisement or personal contacts. There are many ad-hoc initiatives taken by the

11

Government to promote marketing of products/services of small units but no concrete action

plan has been chalked out or targets made.

iii. Technological Upgradation

Modernisation, technological and quality upgradation have assumed great significance in

the present day context. With the inflow of latest technology reducing the cost of production

and the increasing competition from within and outside, the small scale sector will have to

attach more importance and pay attention to the areas of technology upgradation and

modernization. However, due to lack of information on the areas of technology

upgradation, entrepreneurs who have plans for technical upgradation are not to go ahead.

iv. Sickness in SSI Sector

A host of developmental schemes launched by the Government for solving the problems of

small scale industries have yet to achieve their goals to arrest sickness in SSI sector. The

plight of existing small scale industries is visible in many industrial complexes wherein the

industrial sheds have been converted into allied activities like showrooms, banquet halls,

restaurants, etc. There seems to be some lacuna in the implementation part of the

developmental schemes.

v. Removal of Inspector Regime and Simplification of Procedures One of the major grievances of the small scale sector is that the frequent inspections by

multiple government agencies are a source of harassment. At present, 55 inspectors of

different levels are visiting the small scale units, which is a cause of major concern to the

small scale units. It is suggested that the government should stream line the inspection

procedure. It should also include repeal of laws and regulations applicable to the sector

that has become redundant.

12

Indian SMEs are finding it difficult to sell their products in the domestic and

international markets because of increasing competition. To make their products globally

competitive, Indian SMEs need to up-grade their technology and put more emphasis on

innovation per se. In India SSI Sector manufactures more than 7500 items. Since its

inception, it continued to maintain more than 8% growth rate. At present there exist about

3.2 million registered and approximately 6. 5 million are unregistered units. Among these

units 97% are tiny. These units contribute 50% of production, 40% export and 65% of

labour employment in manufacturing sector. However, it is surprising to know that most of

the SSI’s investments are less than Rs.7 Lac.

It is estimated that there are 400 modern SME and 2000 rural and artisan based

clusters exist in India. These contribute to 60 % of India’s manufacturing exports. Some of

the clusters are so big that they produce 70 to 80 % of the total volume of that particular

product produced in India. For example, Panipat produces 75 % of the total woollen

blankets produced in the country; Tirupur produces 80% of the country’s cotton hosiery.

Despite its importance, the SME sector has long faceted extreme obstacles in

accessing finance and markets. Some of these obstacles include inability to access finance

and working capital loans from banks, inability to access capital from other sources,

mistreatment by large procurement companies, difficult bureaucratic procedures for

registration, and lack of management skills, etc. The increasing availability of cheap foreign

imports has further hindered the development of Indian micro, small and medium

enterprises. These obstacles have compelled the SME lobbies and the Government of India

to develop government intervention to ensure the continued growth and success of SMEs.

13

The problems faced by the SMEs, particularly in accessing technology and

maintaining competitiveness have been formidable. It has been found that sharing of

information at local and national clusters are mostly informal. Information regarding the

latest development and competency understanding is much less. Work sharing is not seen

in the local and national clusters, as it is a fight for the same customer, in the same market.

Even though the product and technology used by the entrepreneurs are similar, the

tendency to share is less among the cluster participants.

The concept of cluster development offers new insights into the potential role of

SMEs, in enhancing their access to new technology. Characteristics of a successful cluster

are inter-firm cooperation, cooperation blended with competition, the importance of local

value systems, flexibility and innovative capacity, geographic proximity, sectoral

specialization, a local pool of skilled labour and the presence of a large number of firms. It

also includes willingness to work together to resolve potential clashes of interest,

widespread entrepreneurial spirit and ability, promotion of a social compromise.

SMEs find it difficult to match the wage rate, job security and career development

opportunities, available in larger organizations and therefore are not in a position to hire

skilled and competent manpower. Often, as a result a bottleneck develops in the SME

organisation, it may result in just one or two people controlling the organisation, whether at

the decision making level or at the operational level. Even in moderately large sized firms

employing several hundred workers, these bottleneck points seem to exist. The decision-

makers at the bottleneck points are obviously busy people. They must handle many day-to-

day problems that demand immediate attention, e.g., payroll, inventory, finances,

personnel, suppliers, and customer demands. These problems must be solved quickly, or

14

the company will be unable to function. Clearly, there is little chance for them to think about

making major changes or risk taking, which is essentially required for innovation process.

Small traditional enterprises, with poor support system and little exposure face

difficulties in the new e-business environment. SMEs usually are diffident about adopting IT

or solutions based on IT. Limited human resources, especially those familiar with IT or

corresponding backend processes, place these SMEs in an unfavourable position, in an e-

commerce environment where the preferred physical channels of distribution and delivery

still favour large enterprises. Further, adding to the limitations of SMEs, are lack of

formalized contractual relations and the reliance on cash payments.

Today organizations are knowledge based and their success and survival depend on

creativity, innovation, discovery and inventiveness. An effective reaction to these demands

lead to innovative change in the organization, to ensure their existence. The rate of

changes is accelerating rapidly, as new knowledge idea generation and global diffusion are

increasing. Creativity and innovation have a bigger role in this change process for survival.

V. The Micro, Small and Medium Enterprises Act, 2006

The Government of India passed “The Micro, Small and Medium Enterprises Development

Act” in June 2006 after wide consultation with more than 300 industry associations, different

government departments and multiple stake-holders across the country. The Act is geared

towards promotion and enhancing the competitiveness of Micro, Small and Medium

Enterprises. The Act tries to accomplish many long standing demands of multi stake-

holders in the MSME sector. The Act establishes a National Board for Micro, Small and

Medium Enterprises. The main function of the Board is to oversee and regulate the

development of MSMEs in India. The Board’s duties include monitoring cluster

15

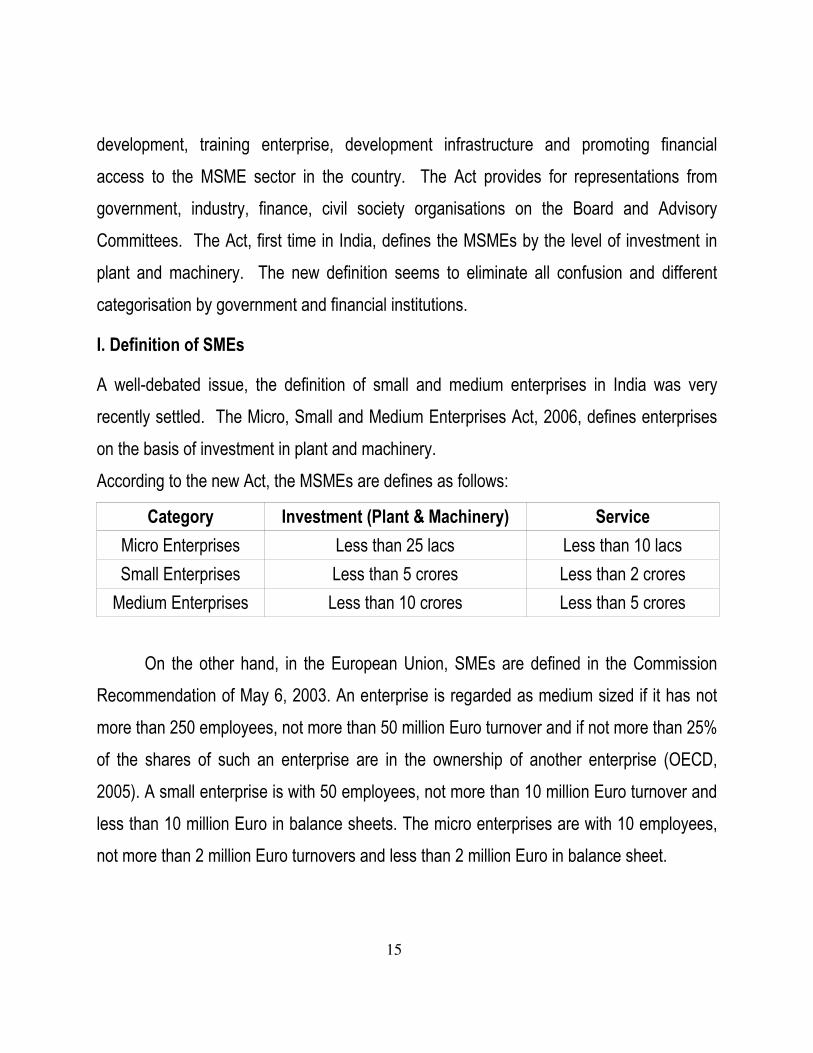

development, training enterprise, development infrastructure and promoting financial

access to the MSME sector in the country. The Act provides for representations from

government, industry, finance, civil society organisations on the Board and Advisory

Committees. The Act, first time in India, defines the MSMEs by the level of investment in

plant and machinery. The new definition seems to eliminate all confusion and different

categorisation by government and financial institutions.

I. Definition of SMEs

A well-debated issue, the definition of small and medium enterprises in India was very

recently settled. The Micro, Small and Medium Enterprises Act, 2006, defines enterprises

on the basis of investment in plant and machinery.

According to the new Act, the MSMEs are defines as follows:

Category Investment (Plant & Machinery) Service

Micro Enterprises Less than 25 lacs Less than 10 lacs

Small Enterprises Less than 5 crores Less than 2 crores

Medium Enterprises Less than 10 crores Less than 5 crores

On the other hand, in the European Union, SMEs are defined in the Commission

Recommendation of May 6, 2003. An enterprise is regarded as medium sized if it has not

more than 250 employees, not more than 50 million Euro turnover and if not more than 25%

of the shares of such an enterprise are in the ownership of another enterprise (OECD,

2005). A small enterprise is with 50 employees, not more than 10 million Euro turnover and

less than 10 million Euro in balance sheets. The micro enterprises are with 10 employees,

not more than 2 million Euro turnovers and less than 2 million Euro in balance sheet.

16

Small and medium enterprises, both in size and shape, are not uniform across the

globe. This asymmetry exists due to the nature of economic development in each country.

The EU’s definition is based mainly on the number of people employed. The UK definition is

on the basis of turnover. The US definition is based both on number of employees as well

as turnover. In China, the categorization is between the sectors based on number of

employees and turnover. The Indian definition based only on the basis of investment in

plant and machinery is not in consonance with the growth of the economy in the recent

past.

The Act simplifies the registration process for new MSMEs by submitting simplified

Memoranda. The Act stipulates that Central Government may, from time to time, for the

purpose of facilitating and promoting the competitiveness of Micro, Small and Medium

Enterprises, by way of development of skills in the employees, management and

entrepreneurs, provision for technology upgradation, market assistance, infrastructure

facilities and cluster development with a view to strengthening backward and forward

linkages which is necessary for the development of MSMEs in the rural areas. The

Reserve Bank guidelines, from time to time, may ensure timely and smooth flow of credit to

the enterprises, minimize the incidents of sickness and enhance the competitiveness of

MSMEs. The Act provides for constituting a fund by the Central Government for providing

necessary credits to the MSMEs.

The Act sets the agenda for specific policies that it will create and implement, the

procurement preference policy, which will guide Government bodies on how much of their

supplies should be purchased from MSMEs. Another important policy is the closure of

business or excide policy, which will regulate the liquidation of sick units. Another policy

measure under the Act is penal provisions for delayed payments to Micro and Small

17

Enterprises. The Act compels big manufacturers and buyers to make payments within 45

days. If the buyer fails to make payments in time, he will be liable to pay compound interest

from the due date. Any dispute with regard to the amount or payment will be referred to

Micro and Small Enterprises Facilitation Council. The Council has the powers of an

Arbitrator to deal with the dispute. The State Governments have to notify the constitution of

Micro and Small Enterprises Facilitation Councils in each State.

The finalisation of the new Act raises many question and controversies among the

industry as well as the government. First, the expansion of the investment limits extends

the priority sector. Banks have to lend upto 40% of their priority lending to this sector. Too

many banks use the methodologies of “Pick and Chose” by looking at safest borrowers,

most of which are larger companies with better financial capacity and strength. Indirectly,

this will be disadvantage to small enterprises and the priority lending will go to the largest

enterprises among MSMEs.

Secondly, any Indian business enterprise, with net worth of less than 10 crores,

cannot raise capital from the stock market. The larger companies can bargain with banks

on interest rates and lower lending rates. The smaller enterprises have no other choice of

finance and they will be forced to borrow on higher interest rates and some will end-up in

closure and sickness.

Third, the Act provides for need for procurement preference policy, which is yet to be

formulated under Section 11 of the Act. The Government proposed a policy of 20% of

annual value of purchases by PSEs, Central govt. departments etc. from MSMEs.

Presently, 358 items, out of 7,500 items that are manufactured by SSI, are reserved for

exclusive purchase from Micro and Small enterprises. In the new policy, this reservation is

dispensed with.

18

ii. The Proposed Procurement Policy

The Central Government Ministries, Departments, its aided institutions and public

enterprises to procure at least 20% of the value of their total annual purchases from

MSMEs, whether it is products or services. There is a special reservation for

disadvantages section of the Society (SCs/STs/Women). At least 22.5% of the value of

total annual procurement of goods and services should be procured from the above section.

There is a special reservation for 10% of the value of total annual procurement of goods

and services from MSMEs owned by women enterprises.

The MSMEs quoting prices higher upto 15% of the lowest eligible price bid, will be

given preference for procuring at least 50% of the required quantity, in case such enterprise

agrees in writing to match the lowest eligible price.

VI. Future Policy Frame Work i. Priority Sector Lending

The target fixed for priority sector lending by domestic and foreign banks is 40% and 32% of

their net bank credit (NBC) respectively. The declining share of the SSI sector in the

outstanding priority sector advances of public and private sector banks since 1999-2000 is

a cause for concern. The share of SSI advances in the NBC declined from 16% at the end

of March 2000 to 11% at the end of March 2003 in respect of public sector banks. For the

private sector banks, the share declined from 19% to about 8% in the same period. The

limited access of SSI sector to funds needs to be addressed on a priority basis. Large

corporates are able to access bank loans at below PLR besides accessing international

markets. But, for the SSI sector, the cost of funds continues to remain high despite falling

deposit rates.

19

The RBI in the mid–year reviews of monetary and credit policy for 2003-04 had

announced a number of measures aimed at improving credit delivery to the SSI sector.

These measures included raising the loan limit from Rs.1.5 million upto Rs.2.5 million

without the requirement of collateral, rationalizing interest rate on the deposits of foreign

banks placed with the Small Industries Development Bank of India (SIDBI) towards their

priority sector shortfall (reduction of interest from 6.75% to the prevailing bank rate).

ii. Price Preference for SSIs

In the past, 15% price preference was being extended to SSI units for supplies to

PSUs/Government bodies. Now it is fixed as 20% and at the same time, the exclusion list

will go. The price preference should be fixed on empirical data which will act as a measure

of assistance to SSI units for utilizing their capacity adequately.

Iii Reformation of Labour Laws

Multiplicity of labour laws is responsible to a large extent for slow growth of industry in our

country. Labour laws provide too much protection to labour force by the provision of

minimum wages, PF, bonus, gratuity and ESI etc. On the other hand, the employers are

required to seek prior permission even for getting overtime work from labour, on payment

and in spite of mutual consent. There has to be performance or productivity linked wage

structure. The more efficient and hard workers may be suitably rewarded, and there should

be a provision to deduct the wages for shirking and laziness. Supportive labour laws are an

important pre-requisite for Indian industry to face the international competition.

IV The Opportunity

Globalisation and liberalisation need not affect Indian small industry only adversely. It

would have created beneficial opportunities as well. The removal of quantitative restrictions

20

and the reduction of import duties, particularly after the setting up of WTO in 1995, have

opened up foreign markets to Indian small industry as much as the Indian market has

opened up to foreign goods. Many efficient and export-oriented small firms would have

gained out of this development. Such opportunities should act as an incentive to many a

small firm in India to enhance their competitiveness to penetrate the global market. This

could also be achieved by small firms becoming vendors or subcontractors to foreign large-

scale industries. The trend is outsourcing of supplies by TNCs and they are always on the

lookout for firms that could supply reliable and quality products.

V. Networking of SMEs for Competitiveness

The promotion of inter-firm linkages is another issue deserving more recognition. The

increasing presence of transnational corporations (TNCs) in the country would open up new

opportunities for subcontracting / outsourcing. This is because FDI has flowed into

industries such as telecommunications, transportation, electrical equipment (including

computer software), metallurgical industries and automobiles, among others, where

opportunities for obtaining subcontracting / outsourcing are high for small industry. The

potential of such outsourcing opportunities must be tapped to the maximum possible extent

to the advantage of small and medium industry. Infrastructure of SME is the route to growth

of world economy.

VII. Conclusion

Small industry in India has found itself in an intensely competitive environment since 1991,

thanks to globalisation, domestic economic liberalisation and dilution of sector-specific

protective measures. The international and national policy changes have thrown open new

opportunities and markets for the Indian small industry. Concerted effort is needed from the

government and small industry to imbibe technological dynamism. Technological

21

upgradation and in-house technological innovations and promotion of inter-firm linkages

need to be encouraged consciously and consistently. Financial infrastructure needs to be

broadened and adequate inflow of credit to the sector be ensured taking into consideration

the growing investment demand, including the requirements of technological transformation.

Small industry should be allowed to come up only in designated industrial areas for better

monitoring and periodic surveys. A technologically vibrant, internationally competitive small

and medium industry should be encouraged to emerge, to make a sustainable contribution

to national income, employment and exports. It is essential to take care of the sector to

enable it to take care of the Indian economy.