slack to keep shrinking, fed to keep tightening€¦ · slack to keep shrinking, fed to keep...

TRANSCRIPT

www.hifreqecon.com/WebinarJuly2017

Slack To Keep Shrinking, Fed To Keep Tightening– Jim O’Sullivan, Chief U.S. Economist

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

0

2

4

6

8

10

12

83 87 91 95 99 03 07 11 15

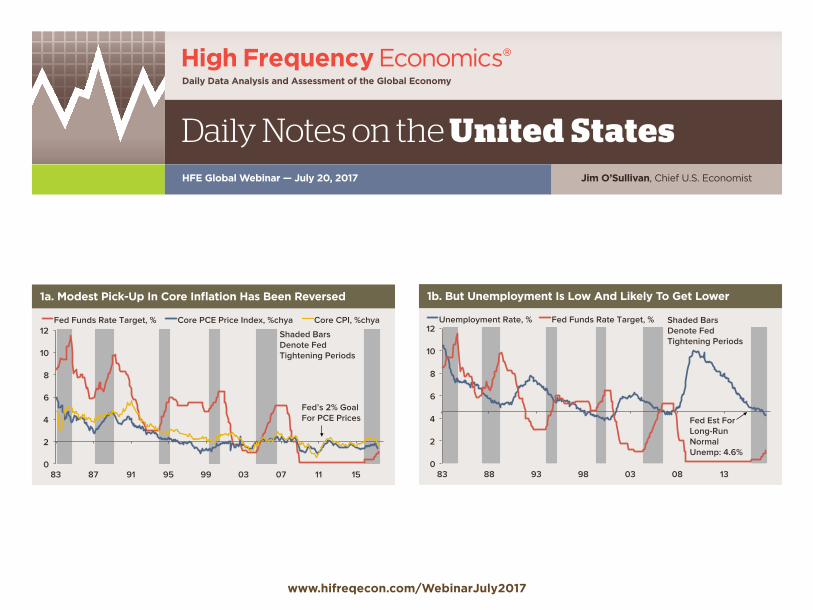

Fed Funds Rate Target, % Core PCE Price Index, %chya Core CPI, %chya

Shaded Bars Denote Fed Tightening Periods

Fed’s 2% Goal For PCE Prices

1a. Modest Pick-Up In Core Inflation Has Been Reversed

0

2

4

6

8

10

12

83 88 93 98 03 08 13

Unemployment Rate, % Fed Funds Rate Target, % Shaded Bars Denote Fed Tightening Periods

Fed Est For Long-Run Normal Unemp: 4.6%

1b. But Unemployment Is Low And Likely To Get Lower

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

-3.0

-2.4

-1.8

-1.2

-0.6

0.0

0.6

1.2

-5

-4

-3

-2

-1

0

1

2

85 90 95 00 05 10 15

CBO Estimate Of Unemployment Gap* (Left) Acceleration/Deceleration In Core PCE Price Index† (Right)

*Reported unemployment rate minus CBO estimate of NAIRU. †%chya minus %chya one year earlier.

2b. Upward Pressure On Inflation From Reduced Slack Just Starting

-2.4

-1.2

0.0

1.2

-5.0

-2.5

0.0

2.5

83 87 91 95 99 03 07 11 15

CBO Estimate Of Unemployment Gap* (Left) Acceleration/Deceleration In Private Wage Component Of ECI† (Right)

*Reported unemployment rate minus CBO estimate of NAIRU. †%chya minus %chya one year earlier.

2a. Upward Pressure On Wages From Reduced Slack Just Starting

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

1.0

2.2

3.4

4.6

07 08 09 10 11 12 13 14 15 16 17

Average of Three Measures, %chya ECI: Private Sector Wages Per Hour, %chya Employment Report: Average Hourly Earnings, %chya Atlanta Fed Per-Hour Wage Tracker, %chya

3a. Hourly Earnings Have Stopped Accelerating—Temporarily?

-8

-4

0

4

8

12

00 02 04 06 08 10 12 14 16

Wage And Salary Income, %chya, 3-Month Average Federal Withheld Employment-Based Tax Receipts Adjusted For Tax Law Changes, %chya, Smoothed 13-Week Average Acceleration Of

Income Into 2012

Delay Of Income Into 2017

3b. Withheld Receipts Are Outpacing Reported Wage Income

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

1

14

27

40 2

5

8

11

86 89 92 95 98 01 04 07 10 13 16

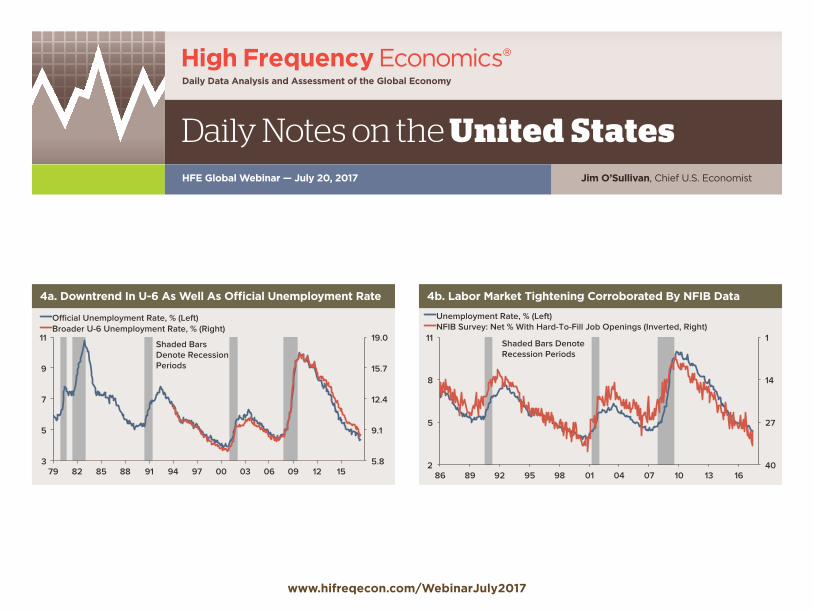

Unemployment Rate, % (Left) NFIB Survey: Net % With Hard-To-Fill Job Openings (Inverted, Right)

Shaded Bars Denote Recession Periods

4b. Labor Market Tightening Corroborated By NFIB Data

5.8

9.1

12.4

15.7

19.0

3

5

7

9

11

79 82 85 88 91 94 97 00 03 06 09 12 15

Official Unemployment Rate, % (Left) Broader U-6 Unemployment Rate, % (Right)

Shaded Bars Denote Recession Periods

4a. Downtrend In U-6 As Well As Official Unemployment Rate

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

200

300

400

500

600

700

70 75 80 85 90 95 00 05 10 15

Weekly Four-Week Average Shaded Bars Denote Recession Periods

Initial Claims, Thousands Per Week

5a. Jobless Claims Remain Low

5b. Payrolls Gains Remain Strong, With Offsets In The Details

Change, Thousands Per Month

20162017 Thru

June ChangePayrolls 187 180 -7

Government 17 9 -8Private 170 171 1

Manufacturing -1 9 10Mining & Logging -6 8 14Construction 13 19 6Wholesale Trade 3 6 3Retail Trade 17 -6 -23Trans & Warehousing 8 3 -4Utilities 0 0 0Information 0 -7 -7Financial Activities 15 14 -1Prof & Business Services 45 48 4

Temporary Help 3 12 9Education 7 2 -5Health & Social Assistance 39 36 -3Leisure & Hospitality 28 30 2Other Services 4 10 6

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

-6

-5

-4

-3

-2

-1

0

0 4 8 12 16 20 24 28 32 36

1961-69 1970-73 1975-80 1980-81 1982-90 1991-2001 2001-07 2009- Change In Unemployment Rate From Peak During Recoveries, Percentage Points

Quarters After Peak

Current Cycle

6b. ...Yet Unemployment Rate Has Been Falling Rapidly

100

110

120

130

140

150

160

0 4 8 12 16 20 24 28 32 36

1961-69 1970-73 1975-80 1980-81 1982-90 1991-2001 2001-07 2009- Real GDP During Recoveries, Trough=100

Quarters After Trough

Current Cycle

6a. GDP Growth Has Been Weak By Past Standards

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

74

84

94

104

114

-10

-5

0

5

10

86 89 92 95 98 01 04 07 10 13 16

Real GDP, %q/q, Annual Rate (Left) NFIB Small Business Optimism Index (Right)

Shaded Bars Denote Recession Periods

7b. NFIB Optimism Index Is Still High Enough For 5% Growth

25

45

65

85

105

125

-5

-3

0

3

5

8

91 93 95 97 99 01 03 05 07 09 11 13 15 17

Real Consumer Spending, %ch From 3 Months Ago In 3-Month Avg, AR (Left)* Expectations Component Of Conference Board Confidence Index (Right)

2011 Debt-Limit Scare

Fiscal Cliff Threat

Shutdown

Clinton Election

*Including HFE estimate for June 2017

7a. Spending Has Not Been As Strong As The Confidence Data

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

-36

-27

-18

-9

0

9

18

27

26

32

38

44

50

56

62

68

96 99 02 05 08 11 14 17

Manufacturing ISM Export Orders Index (Left) Real Good Exports, %ch From 6 Months Ago In 3-Month Avg, Annual Rate (Right)

1998

8b. Exports Have Picked Up, Albeit Not As Much As ISM Data

31

37

43

49

55

61

67

-9

-6

-3

0

3

6

9

97 00 03 06 09 12 15

Real GDP, %ch, Q/Q, Annual Rate (Left) Composite ISM Index (Manufacturing And Non-Manufacturing Combined, Right)

8a. ISM Indexes Look High Enough For Near-4% Growth

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

-20

-10

0

10

20

30

40

50

92 96 00 04 08 12 16

Bloomberg Consumer Comfort Polarization Index: Republican Minus Democrats Vertical Lines Mark Presidential Elections

9b. The “Polarization” Index Has Continued To Rise

10

24

38

52

66

80

06 08 10 12 14 16

Overall Index Democrats Republicans Independents

Vertical Lines Mark Presidential Elections

Weekly Bloomberg Consumer Comfort Index

9a. Confidence Data Have Shown Increased Partisanship

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

Nominal Funds Rate Target (%) Change In Funds Rate (Pct Pts) Core PCE Prices (%chya) Real Funds Rate*Start End Start End First 12 Months Full Cycle Start End Start EndMar 83 Aug 84 8.50 11.50 0.9 3.0 5.9 4.0 2.6 7.5Apr 87 Feb 89 6.00 9.75 0.8** 3.8 2.8 4.7 3.2 5.1Feb 94 Feb 95 3.00 6.00 2.5 3.0 2.2 2.3 0.8 3.7Jun 99 May 00 4.75 6.50 1.8 1.8 1.2 1.7 3.5 4.8Jun 04 Jun 06 1.00 5.25 2.0 4.3 1.9 2.4 -0.9 2.9Dec 15 0.13 0.5 1.4 -1.3* Deflated with %chya in core PCE prices. **The 1987-89 cycle was temporarily interrupted by the 1987 stock market crash.

10a. Fed Tightening Cycles

10b. Fed Officials’ Estimates For Appropriate Fed Funds Rate

% At Year-End, as of Jun 2017 FOMC Meeting

2017 2018 2019Longer

RunMedian Estimate 1.375 2.125 2.938 3.0Mean Estimate 1.38 2.23 2.85 2.92

10c. Fed Officials’ Economic Projections

Median, %ch Q4/Q4, Unless Noted, as of Jun 2017 FOMC Meeting

2017 2018 2019Longer

RunReal GDP 2.2 2.1 1.9 1.8Unemploy. Rate 4.3 4.2 4.2 4.6PCE Prices 1.6 2.0 2.0 2.0Core PCE Prices 1.7 2.0 2.0

*Q4 Level, %

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

23

45

67

89

54

76

98

120

61 65 69 73 77 81 85 89 93 97 01 05 09 13 17

University of Michigan Sentiment Index (Left) Gallup Approval Rating For The President, % (Right)

BHO GWB WJC

DJT

LBJ

JFK

RMN

GHWB

GRF

JEC RWR

11b. Consumer Confidence Vs. The President’s Approval Rating

-14

-12

-10

-8

-6

-4

-2

0

2

95 98 01 04 07 10 13 16

Bloomberg U.S. Financial Conditions

*Based on nine financial markets series, covering money markets, bond markets and equity markets; positive readings imply accomodative financial conditions.

Shaded Bars Denote Periods Of Recession

1998

European Sovereign Debt Fears

U.S. Debt-Limit Saga

Early 2016

11a. Despite Fed Tightening, Financial Conditions Have Eased

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

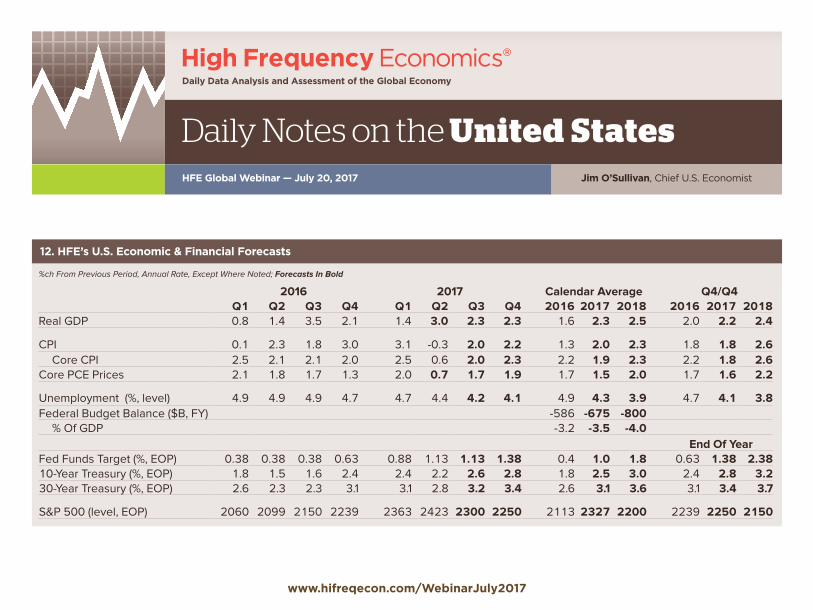

%ch From Previous Period, Annual Rate, Except Where Noted; Forecasts In Bold

2016 2017 Calendar Average Q4/Q4Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2016 2017 2018 2016 2017 2018

Real GDP 0.8 1.4 3.5 2.1 1.4 3.0 2.3 2.3 1.6 2.3 2.5 2.0 2.2 2.4

CPI 0.1 2.3 1.8 3.0 3.1 -0.3 2.0 2.2 1.3 2.0 2.3 1.8 1.8 2.6Core CPI 2.5 2.1 2.1 2.0 2.5 0.6 2.0 2.3 2.2 1.9 2.3 2.2 1.8 2.6

Core PCE Prices 2.1 1.8 1.7 1.3 2.0 0.7 1.7 1.9 1.7 1.5 2.0 1.7 1.6 2.2

Unemployment (%, level) 4.9 4.9 4.9 4.7 4.7 4.4 4.2 4.1 4.9 4.3 3.9 4.7 4.1 3.8Federal Budget Balance ($B, FY) -586 -675 -800

% Of GDP -3.2 -3.5 -4.0End Of Year

Fed Funds Target (%, EOP) 0.38 0.38 0.38 0.63 0.88 1.13 1.13 1.38 0.4 1.0 1.8 0.63 1.38 2.3810-Year Treasury (%, EOP) 1.8 1.5 1.6 2.4 2.4 2.2 2.6 2.8 1.8 2.5 3.0 2.4 2.8 3.230-Year Treasury (%, EOP) 2.6 2.3 2.3 3.1 3.1 2.8 3.2 3.4 2.6 3.1 3.6 3.1 3.4 3.7

S&P 500 (level, EOP) 2060 2099 2150 2239 2363 2423 2300 2250 2113 2327 2200 2239 2250 2150

12. HFE’s U.S. Economic & Financial Forecasts

www.hifreqecon.com/WebinarJuly2017

HFE Global Webinar — July 20, 2017 Jim O’Sullivan, Chief U.S. Economist

Daily Notes on the United States

-6

-3

0

3

6

9

-2

-1

0

1

2

3

77 80 83 86 89 92 95 98 01 04 07 10 13 16

Yield Curve: 10-Year Minus 2-Year Treasury Yield, Percentage Points (Left) Real GDP, %chya (Right)

Shaded Bars Denotes Recession Periods

13c. Yield Curve Inversions Generally Precede Recessions

13a. Long Expansion, But “Expansions Do Not Die Of OldAge”

RecessionsDuration (Months) Expansions

Duration (Months)

1945 8 1945-48 371948-49 11 1949-53 451953-54 10 1954-57 391957-58 8 1958-60 241960-61 10 1961-69 1061970 11 1970-73 361973-75 16 1975-80 581980 6 1980-81 121981-82 16 1982-90 921990-91 8 1991-2001 1202001 8 2001-07 732008-09 18 2009-? 96 So Far

Averages: Averages:1854-1919 21.6 1854-1919 26.61919-45 18.2 1919-45 35.0 1945-2009 11.1 1945-2009 58.4

-4

0

4

8

12

16

20

24

77 83 89 95 01 07 13

Real Fed Funds Rate, Deflated With %Y/Y In Core PCE Prices, % Nominal Fed Funds Rate, %

Shaded Bars Denote Recession Periods

13b. Recent Recessions Preceded By Fed Tightening Cycles

www.hifreqecon.com/WebinarJuly2017

Slack To Keep Shrinking, Fed To Keep Tightening– Jim O’Sullivan, Chief U.S. Economist