skh leung kwai yee secondary school pre– mock...

TRANSCRIPT

2010-LKY CE-P ACCT PRE-MOCK - 1

SKH Leung Kwai Yee Secondary School

PRE– Mock Examination 2010

F.5 Principles of Accounts

23.3.2010

8.15 am – 10.45 am (2.5 hours)

This paper must be answered in English

Instructions:

1. Answer FIVE questions: THREE from Section A (42%), and TWO from Section B (58%).

2. Write your answers on the answer book provided.

3. Show your workings.

Setter: WHF

2010-LKY CE-P ACCT PRE-MOCK - 2

Section A

Answer any THREE questions from this section. Each question carries 14 marks. Write your

answers on the answer sheets provided.

Question 1 The following are the final accounts of Hong Tai Ltd which has stores selling textile goods:

Trading and Profit and loss account for the year ended 31 December

2009 2008

$’000 $’000

Sales (all credit) 18,000 30,000

Less: Cost of goods sold

Opening stock 3,000 3,000

Add: Purchases (all credit) 14,400 18,000

17,400 21,000

Less: Closing stock 3,000 3,000

14,400 18,000

Gross profit 3,600 12,000

Less: Operating expenses 1,800 3,000

Net profit 1,800 9,000

Balance sheet as at 31 December

2009 2008

Fixed assets $’000 $’000 $’000 $’000

Tangible at cost 30,000 22,000

Less: Accumulated depreciation 3,750 2,250

26,250 19,750

Current assets

Stock 3,000 3,000

Trade debtors 4,500 5,000

Bank - 1,000

7,500 9,000

Less: Current liabilities

Trade creditors 3,000 3,750

Bank overdraft 750 -

3,750 3,750

Net current assets 3,750 5,250

30,000 25,000

Less: Long-term liabilities

Debentures 7,500 5,000

22,500 20,000

Financed by:

Issued share capital 10,000 9,500

Share premium 500 300

2010-LKY CE-P ACCT PRE-MOCK - 3

Profit and loss account 12,000 10,200

22,500 20,000

Required: (a) Calculate the following ratios for Hong Tai Ltd for 2008 and 2009, showing clearly the

figures used in calculation.

(i) Return on shareholders’ fund

(ii) Gross profit ratio

(iii) Net profit ratio

(iv) Current ratio

(v) Quick ratio

(vi) Stock turnover (months)

(vii) Trade debtors collection period (months)

(viii) Trade creditors payment period (months). (8 marks)

(Calculations must be rounded to 1 decimal place)

(b) Comment briefly on the profitability and liquidity of the company for 2009 based on the

information revealed by the statements. (6 marks)

2010-LKY CE-P ACCT PRE-MOCK - 4

Question 2 (A)

Sunny runs a French restaurant which is experiencing a loss this year. Its financial year ends on

31 December. During the year, Sunny paid insurance of his apartment for 14 months ended 28

February 2010, amounted to $28,000. He charged the full amount into the profit and loss account

of the restaurant for the current year.

Required: State the accounting principle or concept that has been violated and give an explanation.

(4 marks)

(B)

The Black & White Manufacturing Co. sells self-manufactured goods. The following balances

were taken from the ledger as at 31 December 2009

$

Stocks, 1 January 2009

Raw materials 3,000

Work in progress 1,800

Finished goods 5,200

Manufacturing wages 16,000

Discounts received 350

Discounts allowed 450

Selling expenses 3,500

Administrative expenses 950

Purchases of raw materials 37,000

Factory general expenses 2,600

Carriage inwards 1,400

Carriage outwards 1,250

Sales 85,000

Returns inwards 850

Accumulated depreciation on Office equipment (1 Jan 2009) 500

Office expenses 2,100

Rates and insurance 1,000

Plant and machinery at cost 40,000

Office equipment 3,000

Power and gas 6,500

You are provided with the following additional information:

(i) Stocks as at 31 December 2009 were valued at:

$

Raw materials 5,000

Work in progress 1,900

Finished goods 4,500

(ii) Depreciation is to be charged on assets held at the year end as follows:

Plant and machinery – 5% on cost

Office equipment – 10% on a reducing-balance basis

2010-LKY CE-P ACCT PRE-MOCK - 5

(iii) Prepaid rates amounted to $300 as at 31 December 2009.

(iv) 3/5 of rates and insurance and 4/5 of power and gas were the expenses of the factory.

You are required to: Prepare the manufacturing account of Black & White Manufacturing Co. for the year ended 31

December 2009. Some information given above may not be useful in answering this question.

(10 marks)

2010-LKY CE-P ACCT PRE-MOCK - 6

Question 3 (A)

Greeney Ltd rented a warehouse from Wintery Ltd starting from 1 January 2009 at an annual

rental of $96,000. For the financial year ended 31 December 2009, Greeney Ltd paid $88,000

only and this was the amount recorded in the rental expense account.

Required: State the accounting principle or concept that has been violated and give an explanation.

(4 marks)

(B)

Owing to staff shortage, Billy’s annual stocktaking did not take place on 30 September 2009.

However, stocktaking had been carried out at an earlier date on 25 September 2009. On that day,

the value of the actual stock on the premises was found to be $15,010 at cost price. The following

information is available:

(i) Sales made during the period from 25 to 30 September totaled $1,600.

(ii) A sales return credit note for $100 was issued on 28 September for goods returned on that

day.

(iii) Purchases invoices received for the financial year totaled $1,200. $300 worth of goods

purchased was not received yet.

(iv) Goods with a retail price of $250 had been sent to a customer on a sale or return basis on

15 September. The goods were still unsold on 30 September 2009.

(v) Goods with an original cost of $100 have been found to be damaged. It has been decided

to scrap them.

(vi) Goods costing $200 have been withdrawn for Billy’s own use.

(vii) A total of one stock sheet amounting to $370 had been recorded as $730 in the summary.

(viii) Free samples received from the wholesaler, valued at $400, had been included in the

stock valuation.

(ix) The gross profit ratio of the company is 40% on average.

Required: Prepare a statement to calculate the value of Billy’s stock at 30 September 2009. (10 marks)

2010-LKY CE-P ACCT PRE-MOCK - 7

Question 4 In preparing the financial statements for the year ended 31 December 2009, the accountant of a

trading company found that the sales ledger control account balance did not agree with the total

of the list of balances as extracted from the sales ledger of $107,700. Upon investigation, the

following errors were discovered:

(i) Sales daybook total for December had been undercast by $1,000.

(ii) The total of sales returns daybook for the month of December $690 had been posted to

the control account as $960.

(iii) Discounts allowed of $195 for the month of December had been posted to the wrong side

of discounts allowed account and the control account.

(iv) A sales invoice of $5,640 had been entered into a customer’s account as $8,640.

(v) Sales of $3,000 had been entered on the wrong side of a customer’s account.

(vi) The credit side of a customer’s personal account had been under-added by $300.

(vii) On listing-out and calculating the total of debtors’ balances, an individual debit balance

of $300 has been incorrectly treated as credit.

(viii) The balance on a customer’s account of $5,000 had been completely omitted from the

list of individual personal accounts’ balances.

(ix) Contras with the purchases ledger, amounting to $2,010 have been correctly treated in

the individual accounts but no entry had been made in the control account.

(x) Bad debts of $3,100 had been written off in the sales ledger accounts, but no entry was

made in the general ledger and the control account.

Required: (a) Draw up the sales ledger control account to find out the correct balance. (7 marks)

(b) Prepare a statement to show the revised total of the sales ledger balances. (7 marks)

2010-LKY CE-P ACCT PRE-MOCK - 8

Section B

Answer any TWO questions from this section. Each question carries 29 marks. Write your

answers on the answer sheets provided.

Question 5 The following information was available from the books of Leisure Golf Club as at 1 January

2009:

$

Bar inventory, at cost 5,500

Bar payables 2,400

Subscriptions in advance 3,600

Subscriptions in arrears 1,800

Club premises 1,536,000

Motor vehicles, at carrying amount 182,000

Furniture and equipment, at carrying amount 96,300

Loan from members 800,000

On 31 December 2009, some records and cash of snack bar were stolen.

The following is the summarized receipts and payments account of the club for the year ended 31

December 2009:

$ $

Bal b/f 58,200 Payments to bar payables 88,800

Members’ subscriptions Coaching fees 23,300

– 2008 1,600 Sundry expense 8,600

– 2009 105,000 Annual dinner – hotel and catering 85,200

– 2010 4,500 Staff wages 19,000

Cash banked from bar sales 82,400 Electricity and water 10,000

Annual dinner – ticket sales 123,000 Golf competition – prizes 35,000

Sales of equipment 3,500 – general expenses 16,200

Golf competition – ticket sales 98,000 Motor van expenses 8,760

Charitable donations 2,900

Bal c/d 178,440

476,200 476,200

Additional information:

(i) All sales in the snack bar were cash sales and all stocks were sold to members at a gross

profit margin of 40%. The cash surplus, after paying the following bar expenses per

month, was immediately banked:

$

Bar wages 1,500

Cash purchases 300

Sundry bar expenses 250

(ii) Bar inventory, at cost, at 31 December 2009, amounted to $6,300.

(iii) Payments to bar payables included the payment for acquisition of furniture costing

$25,000.

(iv) The cash stolen from the snack bar was to be written off as a bar expense. 20% of

2010-LKY CE-P ACCT PRE-MOCK - 9

electricity and water was to be allocated to the snack bar.

(v) The equipment sold during the year had a carrying amount of $5,700 on the date of

disposal.

(vi) Depreciation on non-current assets is to be provided at the following rates on carrying

amount:

Club premises 2%

Motor vehicles 25%

Furniture and equipment 20%

It is the club’s policy to charge a full year’s depreciation in the year of acquisition and

no depreciation in the year of disposal.

(vii) There were still $2,200 subscriptions not yet received and unpaid staff salaries amounted

to $3,300.

(viii) The club owed the bar supplies $1,800 at the year end and 2% interest on loan from

members was accrued during the year.

Required: (a) Prepare the snack bar trading account for the year ended 31 December 2009; (6 marks)

(b) Draw up the cash account to ascertain the amount of cash stolen; (3 marks)

(c) Prepare the income and expenditure account for the year ended 31 December 2009; and

(10 marks)

(d) Prepare the balance sheet as at 31 December 2009, detailed workings on the balance of

accumulated fund as at 1 January 2009 should be shown. (10 marks)

2010-LKY CE-P ACCT PRE-MOCK - 10

Question 6 Betty Limited is a wholesaler company with its financial year ends on 31 December. Its

authorized share capital consists of 800,000 8% preference shares of $1 each and 1,500,000

ordinary shares of $1 each. The following trial balance was extracted from its books as at 31

December 2009:

Dr Cr

$ $

Land and buildings 1,800,000

Office equipment, at cost 255,000

Motor vehicles, at cost 460,000

Accumulated depreciation – Office equipment as at 1 January 2009 50,000

Accumulated depreciation – Motor vehicles as at 1 January 2009 184,000

Debtors 291,500

Creditors 351,200

Stock as at 1 January 2009 49,200

Cash at bank 1,170,000

Interim preference dividend 16,000

Interim ordinary dividend 47,500

Bad debts 16,500

Provision for doubtful debts as at 1 January 2009 8,500

Directors’ fees 95,000

Purchases and sales 1,154,200 2,535,000

Returns 30,000 23,000

Discounts 8,100 9,300

Selling and distribution expenses 52,000

Wages and salaries 230,000

Rent and rates 250,000

Interest income 10,500

10% debentures 430,000

Debenture interest 21,500

General reserves 200,000

Share premium 250,000

Retained profits 25,000

950,000 Ordinary shares of $1 each, fully paid 950,000

400,000 8% Preference shares of $1 each, fully paid 400,000

Suspense 520,000

5,946,500 5,946,500

Additional information:

(i) Stock-take as at 31 December 2009 showed a stock value of $47,300. It was found that

goods costing $1,200 received on sale or return terms from suppliers was counted in the

stock-take and recorded as credit purchases in the books. In addition, goods with a selling

price of $5,000 sent to customers on sale or return basis had been omitted from the

stock-take figure and included as credit sales as well. The gross profit margin on goods

2010-LKY CE-P ACCT PRE-MOCK - 11

sent on sale or return basis is 20%.

(ii) Depreciation was to be provided as follows:

Office equipment 15% per annum on net book value

Motor vehicles 20% per annum on cost

(iii) On 31 December 2009, accrued rent and rates and prepaid wages and salaries were

$25,000 and $6,000 respectively.

(iv) Provision for doubtful debts was to be maintained at 3% of the outstanding trade debtors.

(v) On 31 December 2009, a traffic accident happened and a motor vehicle was destroyed

and became un-usable. The cost of that vehicle was $60,000 and its accumulated

depreciation was $24,000. No entry has been made in respect of this event. It is the

company's policy not to charge depreciation in the year of disposal.

(vi) The directors decided to transfer $25,000 to the general reserves, distribute final

dividends to the preference shareholders and propose a final dividend of 3% on ordinary

shares.

(vii) In December 2009, all unissued preference shares were offered to the public at $1.3 per

share. The company had debited the amount to the cash at bank account only. The new

shares were not entitled to dividends distributed at the year end.

Required: (a) Prepare the trading, profit and loss and appropriation account for the year ended 31

December 2009; (17 marks)

(b) Prepare the balance sheet as at 31 December 2009. (12 marks)

2010-LKY CE-P ACCT PRE-MOCK - 12

Question 7 Ann, Ben and Chan were in partnership sharing profit and loss in the ratio of 3:2:1. Each partner

is entitled to a monthly salary of $3,000. The balance sheet as at 31 December 2008 was as

follows:

Balance sheet as at 31 December 2008

Fixed assets $ $ Capital accounts $ $

Office equipment (net) 62,000 Ann 40,000

Motor vans (net) 48,000 Ben 30,000

110,000 Chan 50,000

120,000

Current assets Current accounts

Stock 24,600 Ann (6,500)

Debtors 32,120 Ben 10,500

Less: Provision for

doubtful debts

2,800 29,320 Chan 88,000 92,000

Bank 83,080 Current liabilities

Creditors 35,000

247,000 247,000

Additional information:

(i) Ann retired on 31 December 2008, Ben and Chan continued to operate as partners sharing

profits and loss equally.

(ii) The provision for doubtful debts should be reduced to $2,160.

(iii) Office equipment was revalued at $45,000.

(iv) An item of stock costing $1,400 was estimated to have a net realizable value of $400.

(v) One of vans at net book value of $8,000 was taken over by Ann for $5,000. The rest of

the vans were revalued at $30,000.

(vi) It was agreed that goodwill was valued at $30,000 but no account for goodwill was to be

maintained in the books.

(vii) Out of the total amount due to Ann, $25,000 was to be left as loan to the partnership with

an annual interest rate of 10% and the balance was to be repaid in cash.

You are required to prepare: (a) the revaluation account. (5.5 marks)

(b) the capital accounts of Ann, Ben and Chan in columnar form to record the retirement of Ann.

(7.5 marks)

(c) the balance sheet of the new partnership as at 1 January 2009. (5 marks)

During the year ended 31 December 2009, the partnership made a net profit (before deducting

Ann’s loan interest) of $92,500 and depreciation had been provided on the net book value of fixed

assets at 20% per annum.

Required: (d) Draw up the Profit and Loss Appropriation account for the year ended 31 December 2009.

(3 marks)

2010-LKY CE-P ACCT PRE-MOCK - 13

On 1 January 2010, the partners decided to dissolve the partnership and the following extracted

balances were given:

$

Office equipment (net) ?

Motor vans (net) ?

Stock 21,000

Debtors (net) 24,000

Bank 164,820

Creditors 4,000

Loan from Ann 25,000

(i) All assets except for cash were sold for $125,000.

(ii) The creditors were settled by cash and a 5% discount was received.

(iii) All amount due to Ann (including accrued interest) was paid by cash.

(iv) Ben was personally liable to the realization expense of $2,500.

You are required to prepare: (e) the realization account; and (5 marks)

(f) the capital accounts of Ben and Chan in columnar form as at 1 January 2010.

(3 marks)

END OF PAPER

2010-LKY CE-P ACCT PRE-MOCK - 14

SKH Leung Kwai Yee Secondary School

PRE – Mock Examination 2010

F5 Principles of Accounts

Suggested Solutions

Question 1 (a)

(i) Return on shareholders’

fund

Net profit � Shareholders’ fund � 100%

2009 1,800 � 22,500 � 100% 8% 0.5 2008 9,000 � 20,000 � 100% 45% 0.5

(ii) Gross profit ratio Gross profit � Sales � 100% 2009 3,600 � 18,000 � 100% 20% 0.5 2008 12,000 � 30,000 � 100% 40% 0.5

(iii) Net profit ratio Net profit � Sales � 100% 2009 1,800 � 18,000 � 100% 10% 0.5 2008 9,000 � 30,000 � 100% 30% 0.5

(iv) Current ratio Current assets � Current liabilities 2009 7,500 � 3,750 2 0.5 2008 9,000 � 3,750 2.4 0.5

(v) Quick ratio (Current assets – Inventory) � Current

liabilities

2009 4,500 � 3,750 1.2 0.5 2008 6,000 � 3,750 1.6 0.5

(vi) Stock turnover period Average inventory � Cost of goods sold �

12 months

2009 3,000 � 14,400 � 12 2.5 months 0.5 2008 3,000 � 18,000 � 12 2 months 0.5 (vii) Debtors collection

period

Debtors � Sales � 12 months

2009 4,500 � 18,000 � 12 3 months 0.5 2008 5,000 � 30,000 � 12 2 months 0.5 (viii) Creditors payment

period

Creditors � Purchases � 12 months

2009 3,000 � 14,400 � 12 2.5 months 0.5 2008 3,750 � 18,000 � 12 2.5 months 0.5

2010-LKY CE-P ACCT PRE-MOCK - 15

(b) Profitability

The profitability has worsened.

Gross profit ratio decreased.

Net profit ratio decreased.

Return on shareholders’ fund decreased.

Low gross profit ratios because of lower selling prices.

Lower net profit ratios may due to the drop in gross profit.

Lower return on capital employed may due to the drop in net profit and the new issuance of

shares.

Longer stock turnover period means stock had to be held for long before selling. This

adversely affected the profitability.

(0.5 mark each, Max 3.5)

Liquidity

The liquidity has worsened.

Current ratio decreased.

Acid test ratio decreased.

Low current ratio / acid test ratio implies that the company has liquidity problem, the

company would have difficulty in paying its short-term debts.

Longer credit period allowed to debtors implies that the company became looser in credit

policy. This also explains why the company may have liquidity problems.

(0.5 mark each, Max 2.5)

2010-LKY CE-P ACCT PRE-MOCK - 16

Question 2 (A)

Business Entity Concept (1)

– A business is considered as a separate entity distinguishable from its owner and from

all other entities. A separate set of financial records is maintained for the business and

the financial statements represent the financial position and results of operations of the

business only. (1.5)

– The payment of insurance of the owner’s apartment should be treated as drawings and

not as an expense of the business. (1.5)

(B)

Black & White Manufacturing Co.

Manufacturing account for the year ended 31 December 2009

$ $

Opening stock of raw materials 3,000 0.5 Purchases of raw materials 37,000 0.5

Carriage inwards 1,400 0.5

41,400

Less: Closing stock of raw materials consumed 5,000 0.5

Cost of raw materials consumed 36,400 0.5 Manufacturing wages 16,000 0.5

Prime cost 52,400 1 Factory overheads

Factory general expenses 2,600 1

Rates and insurance [($1,000 – 300) � 3/5] 420 1

Power and gas ($6,500 � 4/5) 5,200 1

Depreciation on plant and machinery ($40,000 � 5%) 2,000 10,220 1

62,620

Add: Opening work in progress 1,800 0.5

64,420

Less: Closing work in progress 1,900 0.5

Production cost of finished goods 62,520 1

2010-LKY CE-P ACCT PRE-MOCK - 17

Question 3 (A)

Accrual concept (1)

– Under the accrual concept, revenues and expenses are accrued, i.e. revenues and

expenses are recognized and included in the financial statements when they are earned

or incurred, not when they are received or paid in cash. (1.5)

– Although one month’s rent of $8,000 was not paid at year end, it had already been

incurred. Therefore, this amount should be included in the firm’s rental expenses for

the year ended 31 December 2009. (1.5)

(B) Billy

Statement to calculate the value of stock as at 30 September 2009

$ $

Stock at 25 September 2009 15,010 1 Add (ii) Sales returns ($1000 � 60/100) 60 1 (iii) Purchases ($1,200 – 300) 900 1 (iv) Goods sent on sale or return basis 250 1,210 1

16,220 Less (i) Sales ($1,600 � 60/100) 960 1 (v) Stock written off 100 1 (vi) Drawings 200 1 (vii) Stock sheet overstated 360 1 (vii) Free samples 400 2,020 1

Stock at 30 September 2009 14,200 1

2010-LKY CE-P ACCT PRE-MOCK - 18

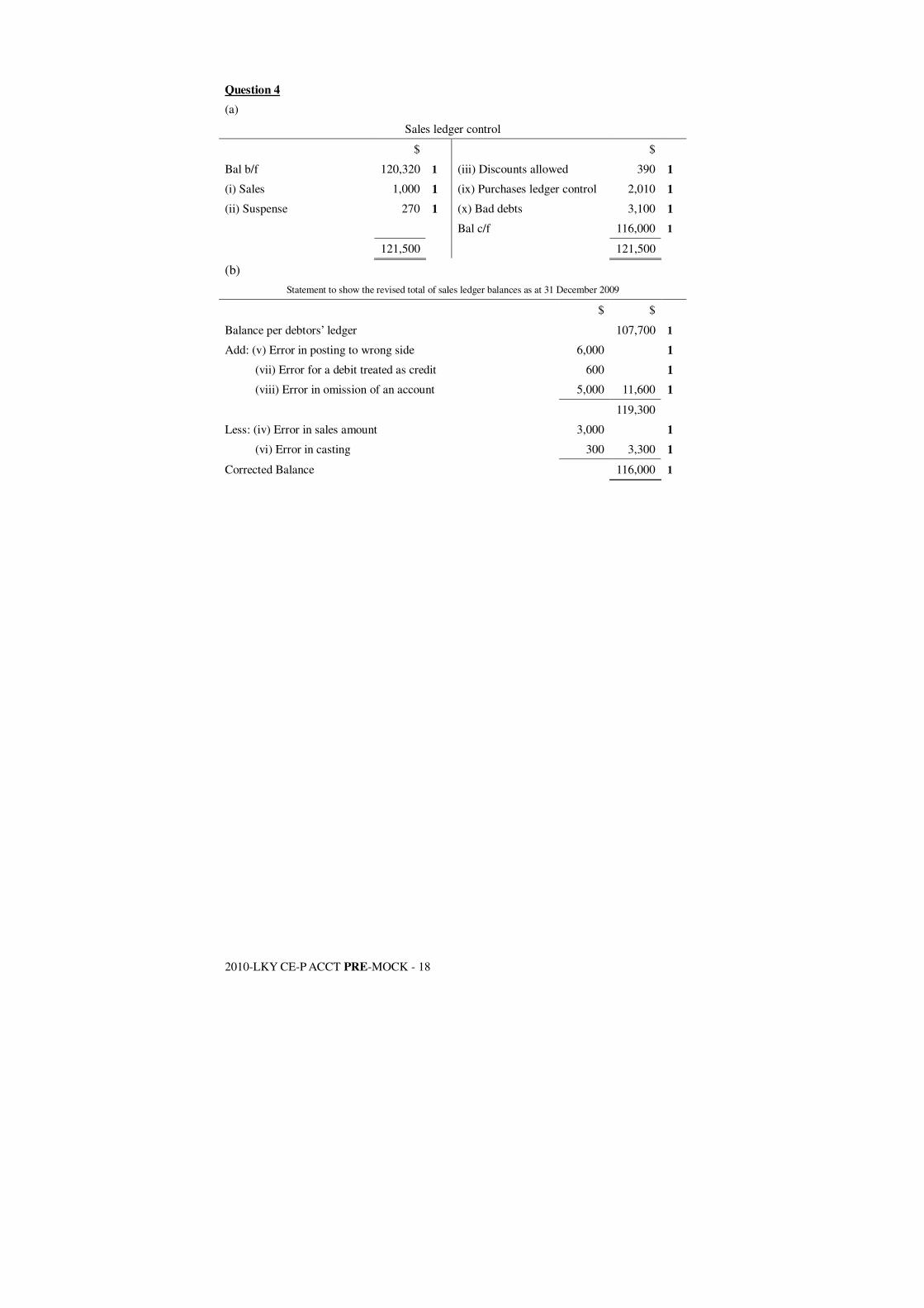

Question 4 (a)

Sales ledger control

$ $

Bal b/f 120,320 1 (iii) Discounts allowed 390 1 (i) Sales 1,000 1 (ix) Purchases ledger control 2,010 1 (ii) Suspense 270 1 (x) Bad debts 3,100 1 Bal c/f 116,000 1

121,500 121,500

(b) Statement to show the revised total of sales ledger balances as at 31 December 2009

$ $

Balance per debtors’ ledger 107,700 1

Add: (v) Error in posting to wrong side 6,000 1 (vii) Error for a debit treated as credit 600 1 (viii) Error in omission of an account 5,000 11,600 1

119,300 Less: (iv) Error in sales amount 3,000 1 (vi) Error in casting 300 3,300 1

Corrected Balance 116,000 1

2010-LKY CE-P ACCT PRE-MOCK - 19

Question 5 (a)

Leisure Golf Club

Bar trading and profit and loss account for the year ended 31 December 2009

$ $

Bar takings ($66,000 � 100/60) 110,000 1 Less: Cost of sales Opening inventory 5,500

Add: Purchases ($88,800 – 25,000 – 2,400 + 1,800 + 300 �

12)

66,800 1.5

72,300 Less: Closing inventory 6,300 66,000

Gross profit ($66,000 � 40/60) 44,000 1

Less: Bar wages ($1,500 � 12) 18,000 0.5

Sundry bar expenses ($250 � 12) 3,000 0.5

Electricity and water ($10,000 � 20%) 2,000 0.5 Cash stolen 3,000 26,000 0.5

Bar profit 18,000 0.5

(b)

Cash account

$ $

Bar takings 110,000 0.5 Bar takings banked 82,400 0.5 Bar wages 18,000 0.5 Cash purchases 3,600 0.5 Bar sundry expenses 3,000 0.5 Cash stolen (bal. fig.) 3,000 0.5

110,000 110,000

(c) Leisure Golf Club

Income and expenditure account for the year ended 31 December 2009

$ $ Income Profit from bar 18,000 0.5 Subscriptions ($105,000 + 3,600 + 2,200) 110,800 1.5 Profit from annual dinner ($123,000 – 85,200) 37,800 0.5 Profit from golf competition ($98,000 – 35,000 – 16,200) 46,800 0.5

213,400 Less: expenditure Loss on disposal of equipment ($5,700 – 3,500) 2,200 0.5 Coaching fees 23,300 0.5 Sundry expense 8,600 0.5 Staff wages ($19,000 + 3,300) 22,300 0.5

Electricity and water ($10,000 � 80%) 8,000 0.5

2010-LKY CE-P ACCT PRE-MOCK - 20

Subscriptions written off 200 0.5 Motor van expenses 8,760 0.5 Charitable donations 2,900 0.5

Depreciation – club premises ($1,536,000 � 2%) 30,720 0.5

Depreciation – Motor vehicles ($182,000 � 25%) 45,500 0.5 Depreciation – Furniture and equipment ($96,300 – 5,700 +

25,000) � 20%

23,120 1

Loan interest ($800,000 � 2%) 16,000 191,600 0.5

Surplus of income over expenditure 21,800 0.5

(d) Leisure Golf Club

Balance sheet as at 31 December 2009

$ $ $ Non-current assets Club premises ($1,536,000 – 30,720) 1,505,280 0.5 Motor vehicles ($182,000 – 45,500) 136,500 0.5 Furniture and equipment ($96,300 – 5,700 + 25,000 –

23,120)

92,480 1

1,734,260

Current assets Bar stock 6,300 0.5 Membership subscription in arrears 2,200 0.5 Bank 178,440 0.5

186,940 Less: Current liabilities Bar creditors 1,800 0.5 Membership subscriptions in advance 4,500 0.5 Accrued expenses ($3,300 + 16,000) 19,300 25,600 0.5

Net current liabilities 161,340

1,895,600 Less: Long-term liabilities Loan from members 800,000 0.5

1,095,600

Accumulated fund (5,500 – 2,400 – 3,600 + 1,800 +

1,536,000 + 182,000 + 96,300 – 800,000 + 58,200)

1,073,800 4

Add: Surplus 21,800 0.5

1,095,600

2010-LKY CE-P ACCT PRE-MOCK - 21

Question 6 (a)

Betty Limited

Trading, profit and loss and appropriation account for the year ended 31 December 2009

$ $ $ Sales ($2,535,000 – 5,000) 2,530,000 0.5 Less: Returns inwards 30,000 0.5

2,500,000 Less: Cost of goods sold Opening stock 49,200 0.5 Purchases ($1,154,200 – 1,200) 1,153,000 0.5 Less: Returns outwards 23,000 1,130,000 0.5

1,179,200

Less: Closing stock ($47,300 – 1,200 + 5,000 �

80%)

50,100 1,129,100 1

Gross profit 1,370,900 0.5 Add: Discounts received 9,300 0.5 Interest income 10,500 19,800 0.5

1,390,700 Less: Expenses Bad debts 16,500 0.5 Directors’ fees 95,000 0.5 Discounts allowed 8,100 0.5 Selling and distribution expenses 52,000 0.5 Wages and salaries ($230,000 – 6,000) 224,000 0.5 Rent and rates ($250,000 + 25,000) 275,000 0.5 Debentures interest 43,000 0.5

Depreciation – Office equipment ($255,000 –

50,000) � 15%

30,750 1

Depreciation – Motor vehicles ($460,000 –

184,000 – 60,000 + 24,000) � 20%

48,000 1.5

Loss on disposal ($60,000 – 24,000) 36,000 0.5 Increase in provision for bad debts ($291,500 –

5,000) � 3% – 8,500

95 828,445 1

Net profit 562,255 0.5

Add: Retained profit b/f 25,000 0.5

587,255 Less: Appropriation Transfer to general reserve 25,000 0.5 Preference share dividends – paid 16,000 0.5 – proposed 16,000 1 Ordinary share dividends – paid 47,500 0.5

– proposed (950,000 � 28,500 133,000 0.5

2010-LKY CE-P ACCT PRE-MOCK - 22

3%)

Retained profits c/f 454,255 0.5

(b)

Betty Limited

Balance sheet as at 31 December 2009

$ $ $ Fixed assets Cost Acc.

Dep

NBV

Land and buildings 1,800,000 1,800,000 0.5 Office equipment 255,000 80,750 174,250 1 Motor vehicles 400,000 208,000 192,000 2

2,166,250

Current assets Stock 50,100 0.5 Debtors 286,500 0.5 Less: Provision for bad debts 8,595 277,905 0.5

Prepayment 6,000 0.5 Cash at bank 1,170,000 0.5

1,504,005 Less: Current liabilities Creditors 350,000 0.5 Accruals ($25,000 + 21,500) 46,500 396,500 0.5

1,107,505

3,273,755 Less: Long term liabilities 10% Debentures 430,000 0.5

2,843,755

Financed by: Authorized share capital 1,500,000 ordinary shares of $1 each 1,500,000 0.5 800,000 8% preference shares of $1 each 800,000 0.5

2,300,000

Issued and fully paid share capital

950,000 ordinary shares of $1 each 950,000 0.5 800,000 5% preference shares of $1 each 800,000 0.5

1,750,000 Reserves Share premium ($250,000 + 120,000) 370,000 0.5 General reserves 225,000 0.5 Retained profits 454,255 0.5 Proposed dividends 44,500 1,093,755 1

2,843,755

2010-LKY CE-P ACCT PRE-MOCK - 23

Question 7 (a)

Revaluation

$ $

Office equipment 17,000 1 Provision for doubtful debts 640 1 Stock 1,000 1 Capital – Ann 15,180 0.5 Motor van ($48,000 –

5,000 – 30,000)

13,000 1 Capital – Ben 10,120 0.5

Capital – Chan 5,060 0.5

31,000 31,000

(b)

Capital accounts

Ann Ben Chan Ann Ben Chan

$ $ $ $ $ $

Motor van 5,000 0.5 Bal b/d 40,000 30,000 50,000 1.5 GW write

off

15,000 15,000 GW 15,000 10,000 5,000 1.5

Revaluation 15,180 10,120 5,060 1.5 Current 6,500 0.5 Loan 25,000 0.5 Cash 3,320 0.5 Bal c/d 14,880 34,940 1

55,000 40,000 55,000 55,000 40,000 55,000

(c)

Ben and Chan

Balance sheet as at 1 January 2009

$ $ $ Fixed assets Office equipment 45,000 0.5 Motor vans 30,000 0.5

75,000 Current assets Stock 23,600 0.5 Debtors 32,120 Less: Provision for doubtful debts 2,160 29,960 0.5

Bank ($83,080 – 3,320) 79,760 0.5

133,320 Less: Current liabilities Creditors 35,000

98,320

173,320 Less: Long-term liabilities Loan from Ann 25,000 0.5

2010-LKY CE-P ACCT PRE-MOCK - 24

148,320

Financed by: Capital – Ben 14,880 0.5 Capital – Ann 34,940 0.5

49,820 Current – Ben 10,500 0.5 Current – Chan 88,000 98,500 0.5

148,320

(d)

Ben and Chan

Profit and loss and appropriation account for the year ended 31 December 2009

$ $

Net profit ($92,500 – 25,000 � 10%) 90,000 1 Less: Salary – Ben 36,000 0.5 Salary – Chan 36,000 72,000 0.5

18,000

Share of profit

– Ben ($18,000 � 1/2) 9,000 0.5

– Chan ($18,000 � 1/2) 9,000 0.5

18,000

(e)

Realisation

$ $

Office equipment ($45,000 �

80%)

36,000 1

Bank 125,000 0.5

Motor vans ($30,000 � 80%) 24,000 1 Discounts received 200 0.5 Stock 21,000 0.5

Debtors (net) 24,000 0.5

Capital – Ben 10,100 0.5

Capital – Chan 10,100 0.5

125,200 125,200

(f)

Capital accounts

Ben Chan Ben Chan

$ $ $ $

Bank 80,480 178,040 1 Bal b/d 14,880 34,940 Current 55,500 133,000 1 Realization 10,100 10,100 1

80,480 178,040 80,480 178,040

2010-LKY CE-P ACCT PRE-MOCK - 25

(Workings)

Current accounts

Ben Chan Ben Chan

$ $ $ $

Capital 55,500 133,000 Bal b/d 10,500 88,000 Salary 36,000 36,000 Share of profit 9,000 9,000

55,500 133,000 55,500 133,000

(Workings)

Bank

$ $

Bal b/d 164,820 Creditors 3,800 Bank 125,000 Loan from Ann 25,000 Loan interest 2,500 Capital – Ben 80,480 Capital – Chan 178,040

289,820 289,820

END OF PAPER