signs of life - · pdf file!positive absorption in grade b buildings as grade a tenants...

TRANSCRIPT

CBRE RESEARCH & CONSULTANCY

Presented by:Marc TownsendManaging DirectorCB Richard Ellis (Vietnam) Co., Ltd.

Signs of Life

CB RICHARD ELLIS VIETNAM2 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

FIRST QUARTER HIGHLIGHTS

! External pressures driving changes across the HCMCproperty market.

! Residential developers, office landlords and some vendorsin the investment market have taken steps to sparkdemand.

! Outside Vietnam, there is a consensus that we may benearing “the end of the beginning” of the global crisis.

! New expectations in the market will increase pressure onlandlords and developers to adapt to the new reality.

! How long can they tough it out before painful decisionsbecome preferable to empty properties, or a true recoveryappears on the horizon?

CB RICHARD ELLIS VIETNAM3 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

VIETNAM ECONOMIC OVERVIEW

! The GDP growth rate of 3.1% in the first quarter of 2009 wasthe lowest quarterly result in more than a decade.

! However, with many of the world’s largest economiescontracting, any growth can be seen as a positive sign.

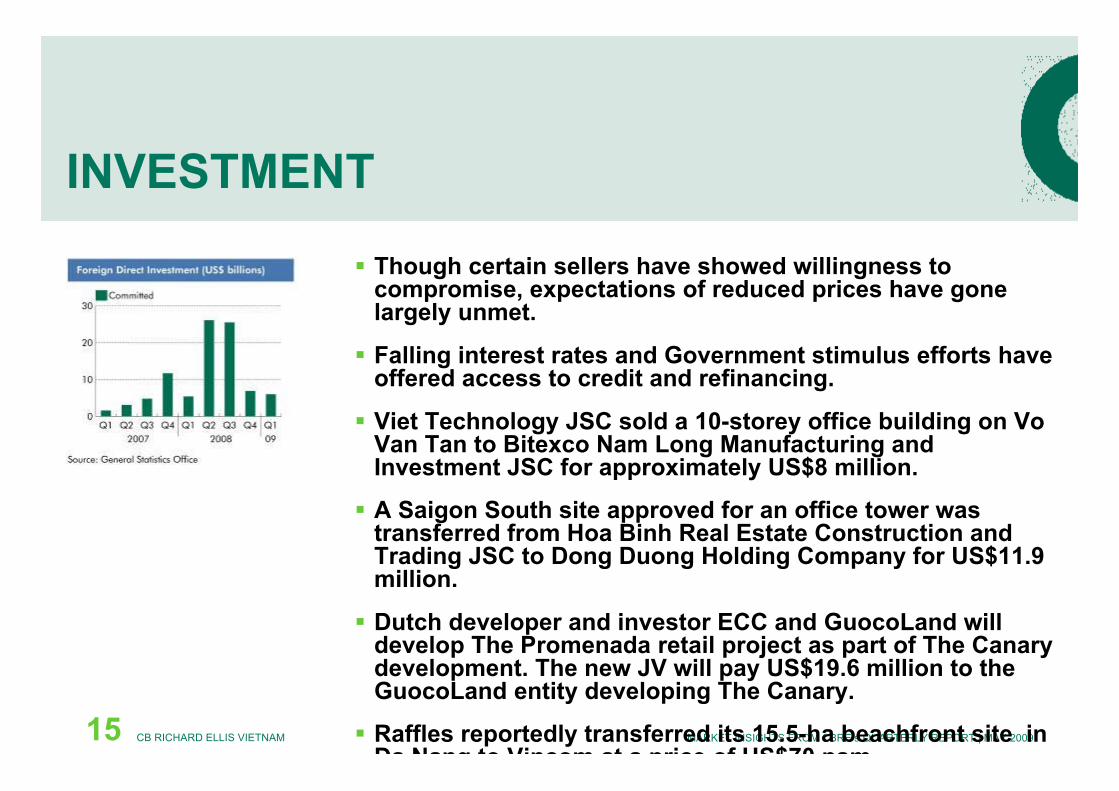

! FDI commitments fell to US$2.2 billion in the first quarter of2009 – a decrease of 45% q-o-q.

! The US$1 billion Government interest rate subsidyprogramme has been expanded to include medium-termloans - US$13.8 billion has already been extended tobusinesses.

! For underlying structural reasons, Vietnam remains one ofAsia’s most attractive long-term investment destinations.

CB RICHARD ELLIS VIETNAM4 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

HCMC ECONOMIC OVERVIEW

! GDP growth slowed to 4.0% y-o-y in the first quarter, from11.4% in the fourth quarter of 2008.

! HCMC continued to outperform Vietnam as a whole. TheGDP growth target for 2009 has been lowered from 10% to6%.

! Committed FDI dropped 73% y-o-y in the first quarter of2009.

! The number of newly established FDI enterprises in HCMCwas down 35% q-o-q and 32% y-o-y in the first quarter of2009.

! The number of newly established non–state Vietnameseenterprises was down 8.4% q-o-q, but increased 9% y-o-y.

! Real estate and consultancy projects accounted forUS$410.3 million of committed FDI in the first quarter asopposed to US$7.6 billion in 2008 as a whole.

CB RICHARD ELLIS VIETNAM5 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

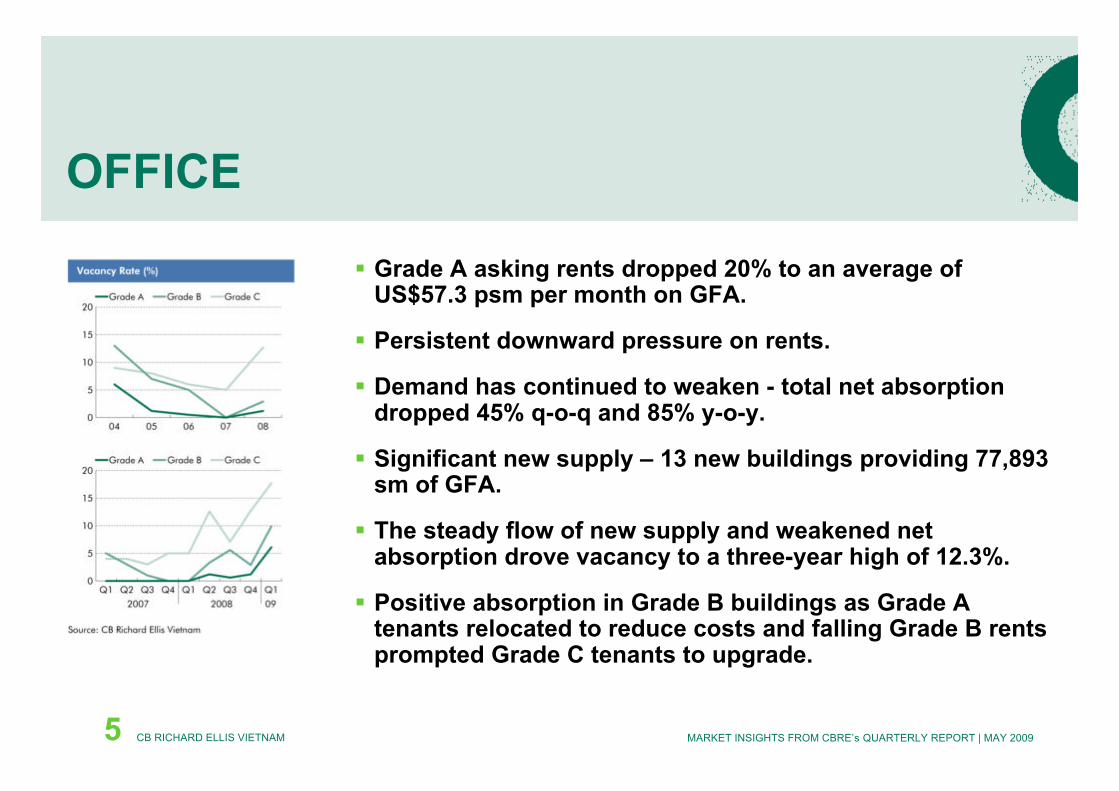

OFFICE

! Grade A asking rents dropped 20% to an average ofUS$57.3 psm per month on GFA.

! Persistent downward pressure on rents.

! Demand has continued to weaken - total net absorptiondropped 45% q-o-q and 85% y-o-y.

! Significant new supply – 13 new buildings providing 77,893sm of GFA.

! The steady flow of new supply and weakened netabsorption drove vacancy to a three-year high of 12.3%.

! Positive absorption in Grade B buildings as Grade Atenants relocated to reduce costs and falling Grade B rentsprompted Grade C tenants to upgrade.

CB RICHARD ELLIS VIETNAM6 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

OFFICE

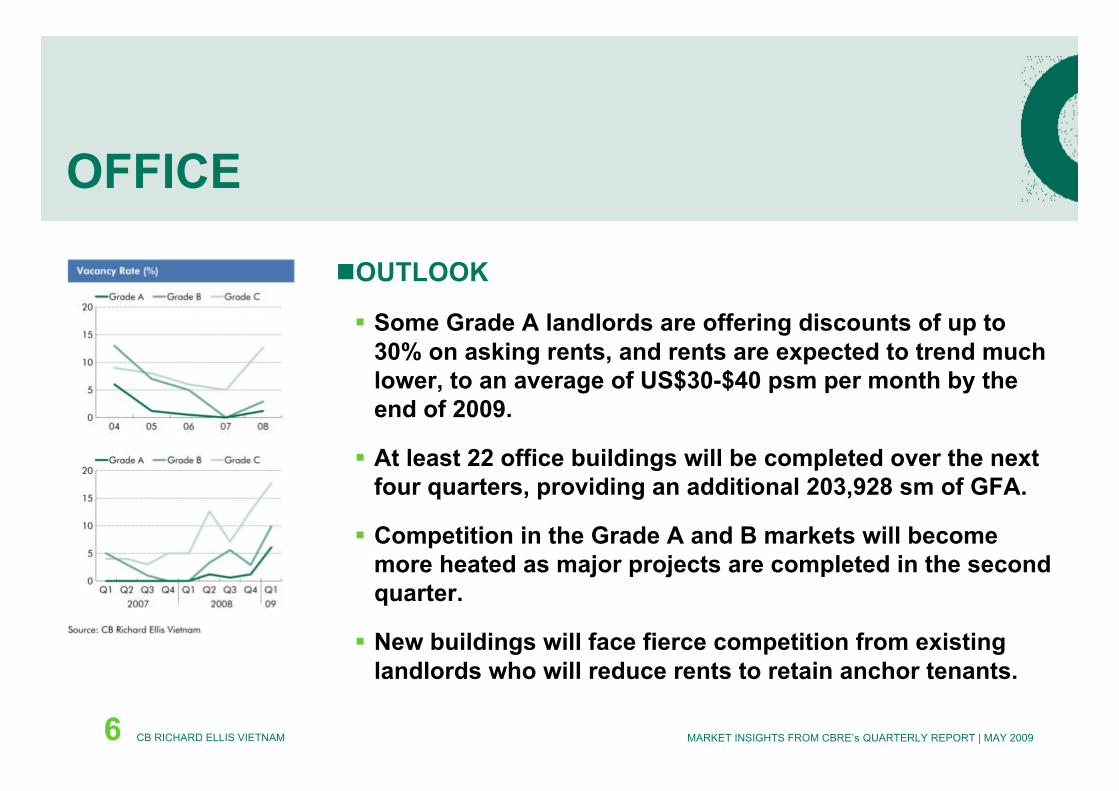

"OUTLOOK

! Some Grade A landlords are offering discounts of up to30% on asking rents, and rents are expected to trend muchlower, to an average of US$30-$40 psm per month by theend of 2009.

! At least 22 office buildings will be completed over the nextfour quarters, providing an additional 203,928 sm of GFA.

! Competition in the Grade A and B markets will becomemore heated as major projects are completed in the secondquarter.

! New buildings will face fierce competition from existinglandlords who will reduce rents to retain anchor tenants.

CB RICHARD ELLIS VIETNAM7 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

RESIDENTIAL FOR SALE

! Hoang Anh Gia Lai jump-started sales by reducing prices intwo projects by an average of 38%. At least nine domesticdevelopers followed suit.

! All eyes will be watching to see if cash-strapped developersblink first in the standoff with buyers holding out for lowerprices.

! Buyers will still pay a premium for certain projects.Riverside Residence sold virtually all units, increasingprices for each phase from 5% - 8%.

! We expect further differentiation between local and foreignprojects, with international developers less willing to lowerprices.

! Average developer and resale asking prices continued tofall in all price ranges, dropping by a further 2%-10% q-o-q.

CB RICHARD ELLIS VIETNAM8 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

RESIDENTIAL FOR SALE

"OUTLOOK

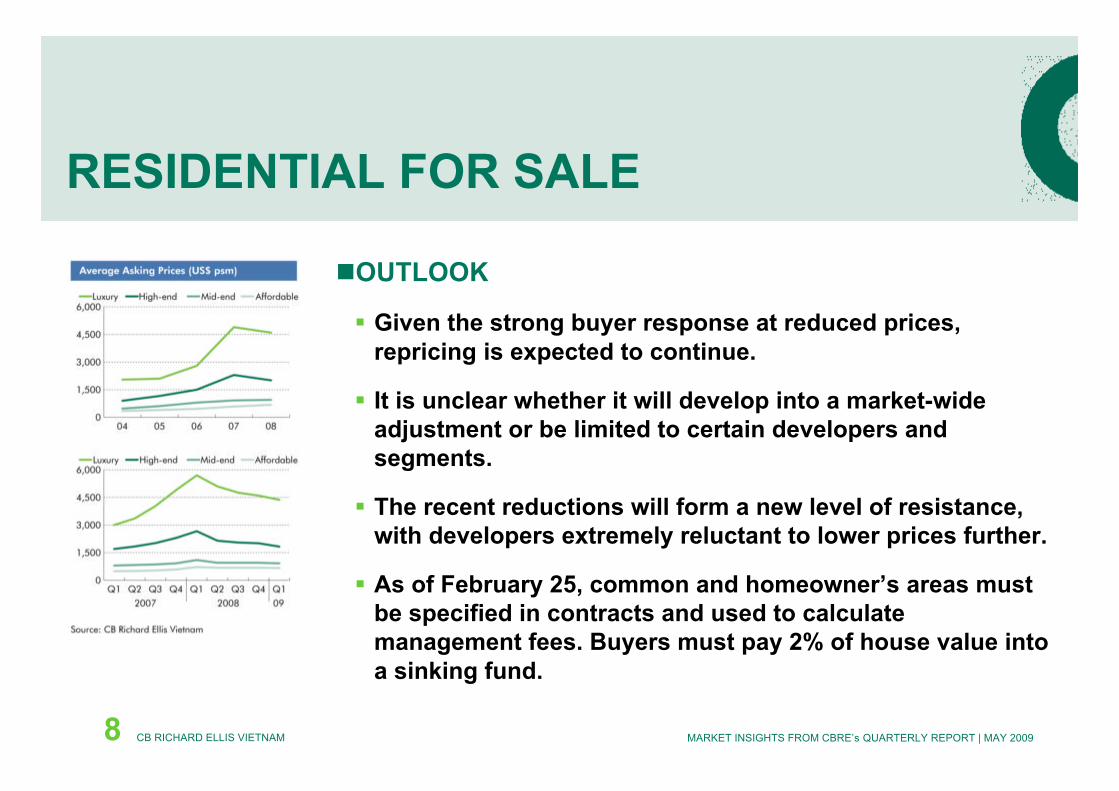

! Given the strong buyer response at reduced prices,repricing is expected to continue.

! It is unclear whether it will develop into a market-wideadjustment or be limited to certain developers andsegments.

! The recent reductions will form a new level of resistance,with developers extremely reluctant to lower prices further.

! As of February 25, common and homeowner’s areas mustbe specified in contracts and used to calculatemanagement fees. Buyers must pay 2% of house value intoa sinking fund.

CB RICHARD ELLIS VIETNAM9 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

RETAIL

! Though growth in retail sales has slowed, domesticdemand has proved more resilient than in much of the restof the world.

! Saigon Paragon opened in March at 80% occupancy. Realground floor rents were US$60-$70 psm per month.

! CBD shopping centre rents increased 1.3% q-o-q, whileshopping centre rents outside the CBD dropped 6.7% q-o-q.

! Local retailers continue to open in key locations to buildbrand awareness and visibility.

! The number new international entrants has dwindled, andbrands already present have delayed expansionprogrammes.

CB RICHARD ELLIS VIETNAM10 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

RETAIL

"OUTLOOK

! Seeking to enhance brand awareness and visibility,Vietnamese retailers will remain the most vigorous playersin the market.

! CBD retail rents are expected to remain stable. Fringe CBDrents are expected to decrease 5%-10%, with rentselsewhere facing greater downward pressure.

! 1.4 million sm (GFA) of space scheduled to be launchedbefore 2013. However only half is likely to be completed onschedule.

! The development trend is towards projects with retail areaslarger than 100,000 sm, built in emerging suburbanlocations.

! Large numbers of these projects are expected to moveforward to meet anticipated demand when the marketrevives.

CB RICHARD ELLIS VIETNAM11 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

SERVICED APARTMENTS

! Grade A rents declined 4% q-o-q, the first decline since thesecond quarter of 2007. Grade B and C rents also declined,falling 5% q-o-q.

! The weakening in Grade A rents was in larger units,reflecting changes in the key expatriate market ascompanies replace older, married employees with single orproject-based staff.

! As demand from the expat tenant base softens, landlordshave begun to offer leases as short as a week.

! Short-term leases have helped underpin occupancy - GradeA and Grade B occupancy actually increased slightly.

! No new supply during the quarter.

! Owners of ’buy to let’ apartments have reduced rents inorder to draw tenants from serviced apartments.

CB RICHARD ELLIS VIETNAM12 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

SERVICED APARTMENTS

"OUTLOOK

! The steady trickle of departing expatriates will continue toerode the base of demand for serviced apartments over thecourse of 2009.

! Demand for larger units will continue to decline, but stabledemand should continue to underpin rents for smallerunits.

! Declines of 8-10% in Grade A rents and 10-15% in Grade Brents are anticipated by the end of the year.

! The level of new supply will remain limited, with only twoprojects slated to come on stream in 2009, adding 290units.

! ‘Buy to let’ condominiums or villas are becoming moreattractive due to their increasingly competitive pricing.

CB RICHARD ELLIS VIETNAM13 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

3-5 STAR HOTELS

! The downturn in global toursim and business travelcontinues to impact the hotel sector.

! Five-star occupancy plunged 31.5% y-o-y and average five-star room rates fell approximately 6.6% y-o-y.

! Most four- and three-star hotels reduced room ratesthrough promotional campaigns.

! Taiwanese developer Fei Yueh broke ground on the NikkoSaigon Hotel, part of the mixed-use Royal Centredevelopment. Approximately 335 rooms are scheduled toopen in 2011.

CB RICHARD ELLIS VIETNAM14 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

3-5 STAR HOTELS

"OUTLOOK

! The new supply anticipated in the second half of 2009 willpose further challenges in an already difficult environment.

! Most hotels will continue to offer promotional campaigns,including discounted room rates and value-added services.

! However, a significant discount in room rates leading to aprice war is not anticipated.

! The second quarter is the traditional low season, thoughthe recent political unrest in Thailand could boost arrivals.

! Up to 2,500 four or five-star hotel rooms could come onstream by end-2010.

CB RICHARD ELLIS VIETNAM15 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

INVESTMENT

! Though certain sellers have showed willingness tocompromise, expectations of reduced prices have gonelargely unmet.

! Falling interest rates and Government stimulus efforts haveoffered access to credit and refinancing.

! Viet Technology JSC sold a 10-storey office building on VoVan Tan to Bitexco Nam Long Manufacturing andInvestment JSC for approximately US$8 million.

! A Saigon South site approved for an office tower wastransferred from Hoa Binh Real Estate Construction andTrading JSC to Dong Duong Holding Company for US$11.9million.

! Dutch developer and investor ECC and GuocoLand willdevelop The Promenada retail project as part of The Canarydevelopment. The new JV will pay US$19.6 million to theGuocoLand entity developing The Canary.

! Raffles reportedly transferred its 15.5-ha beachfront site inDa Nang to Vincom at a price of US$70 psm.

CB RICHARD ELLIS VIETNAM16 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

CONSTRUCTION COSTS

! Construction costs continued to decline in the first quarterof 2009, dropping an average of 4%-5% q-o-q.

! DLS forecast that overall Vietnam construction costs willgenerally move within a range of –14.1% to +5.7% over2009.

! Falls in construction material prices, notably steel (-6.5%)and glass products (up to -7.5%).

! Cost falls in some Mechanical, Electrical and Plumbingequipment.

! Contractors and subcontractors are narrowing margins inorder to remain competitive in a tightening market.

! Contractors are reducing inflation forecasts in fixed pricecontracts.

THIS SECTION CONTRIBUTED BY DAVIS LANGDON & SEAH VIETNAM WWW.DAVISLANGDON-ASIA.COM

CB RICHARD ELLIS VIETNAM17 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

"Investment Sales change shape

! Foreigners to Locals

! Locals to Foreigners

! Sale of Shares of single asset companies

! En-bloc Sales during construction

! Sale of a Retail Podium of a mixed-use development

! Sale of 1 tower (out of several)

"MORE assets have changed hands but below the radarscreen

Investment – New Ways toPlay

CB Richard Ellis Fearless Forecasts 2009

CB RICHARD ELLIS VIETNAM18 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

"Militancy in Property Management – both developers and ownersstruggle for control of their homes and common areas through the useof Owner Management Committees (OMCs)

"Division of Interests – what is common area? – podium, retail, carpark? Where does the developer stop and the OMC start?

"Transparency – OMCs ask - what are we buying and what are wepaying for? Who should pay for maintenance of common areas?

Property Management – OMC’s vs.Developers

CB Richard Ellis Fearless Forecasts

2009

CB RICHARD ELLIS VIETNAM19 MARKET INSIGHTS FROM CBRE’s QUARTERLY REPORT | MAY 2009

Over 300 markets in more than 50 countries

Thank You

www.cbrevietnam.com