short sale brochure

TRANSCRIPT

An Option to Avoid Foreclosure

Short Sale

In most cases the primary reason to consider a short sale is to AVOID FORECLOSURE.

Foreclosure is one of the most damaging things that can happen to a person’s credit. The impact of a foreclosure to a consumer’s credit is huge and long lasting.

There are several options that one may consider to avoid foreclosure, and we will identify those options in a future slide.

However, in many cases a short sale is the single best option to avoid foreclosure.

Avoid Foreclosure

Like most homeowners you never intended to miss a mortgage payment. But it happened. You missed a payment, and then another.

Before long you owe thousands of dollars, can’t pay the huge sum of money that is past due, and don’t know what to do.

Quite often at this point homeowners are overwhelmed and think they have no way to get out of the hole in which they find themselves. And… then they just give up.

Behind on payments?

Job Loss/

Income

Reduction

Failed

Business

Illness/

Medical

Costs

Divorce

SHORT SALE

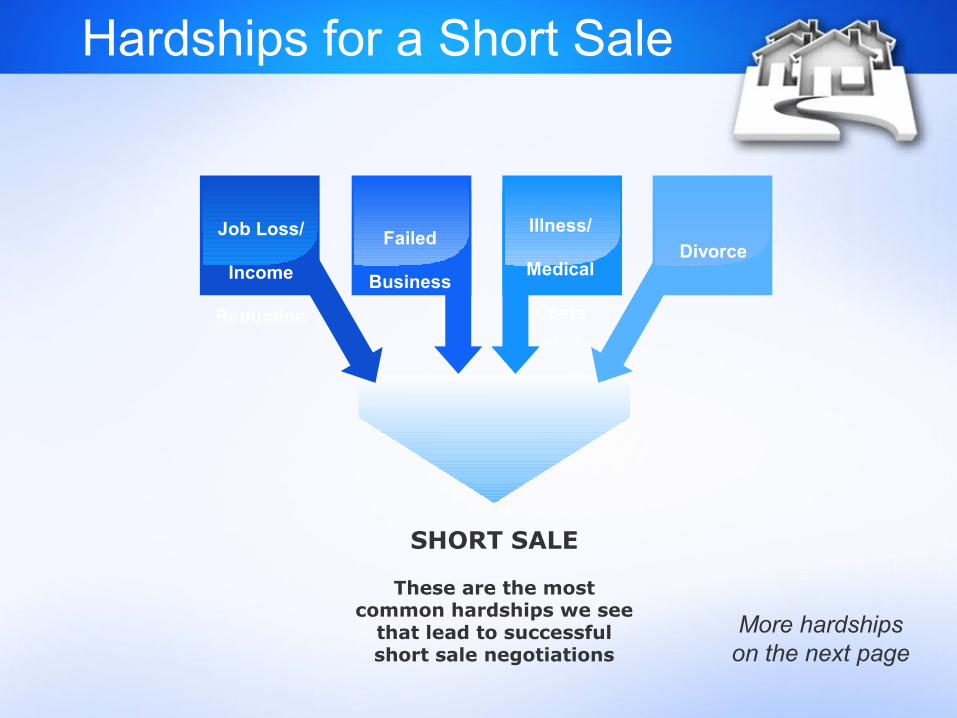

These are the most common hardships we see

that lead to successful short sale negotiations

Hardships for a Short Sale

More hardships on the next page

Death of

Spouse

Natural

Disasters

Bankruptcy No Assets

SHORT SALE

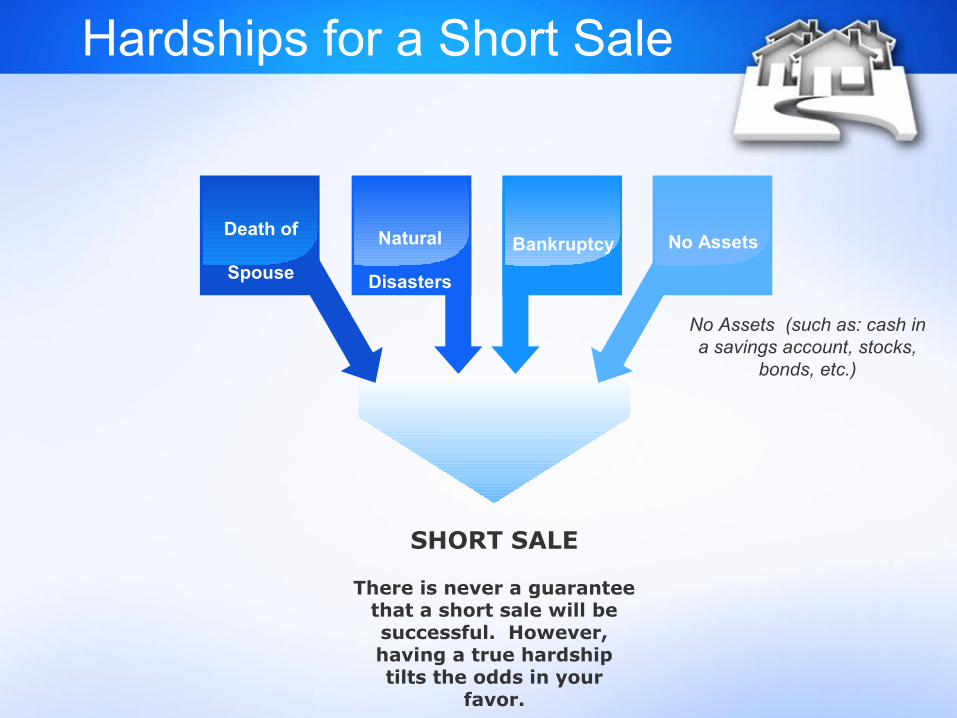

There is never a guarantee that a short sale will be successful. However, having a true hardship tilts the odds in your

favor.

Hardships for a Short Sale

No Assets (such as: cash in a savings account, stocks,

bonds, etc.)

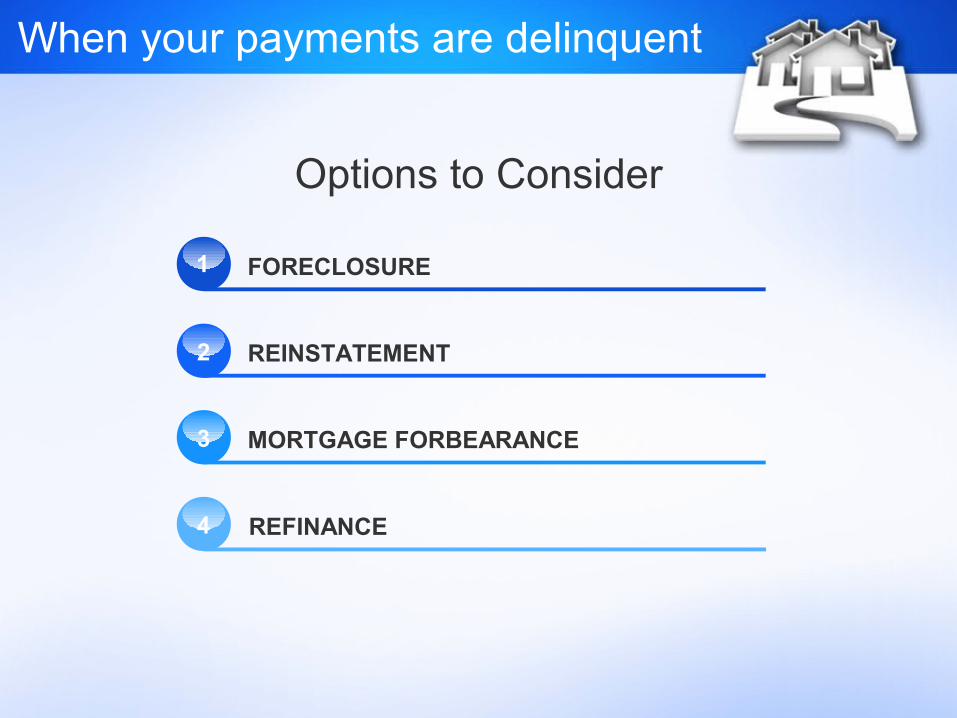

1 FORECLOSURE

REINSTATEMENT

MORTGAGE FORBEARANCE

REFINANCE

Options to Consider

2

3

4

When your payments are delinquent

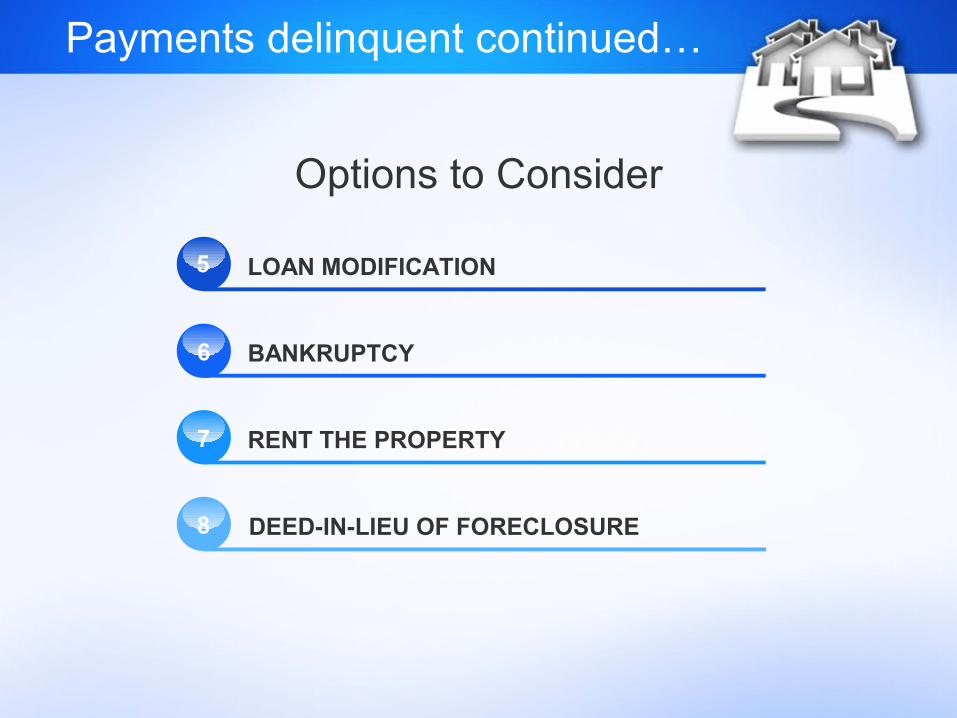

5 LOAN MODIFICATION

BANKRUPTCY

RENT THE PROPERTY

DEED-IN-LIEU OF FORECLOSURE

Options to Consider

6

7

8

Payments delinquent continued…

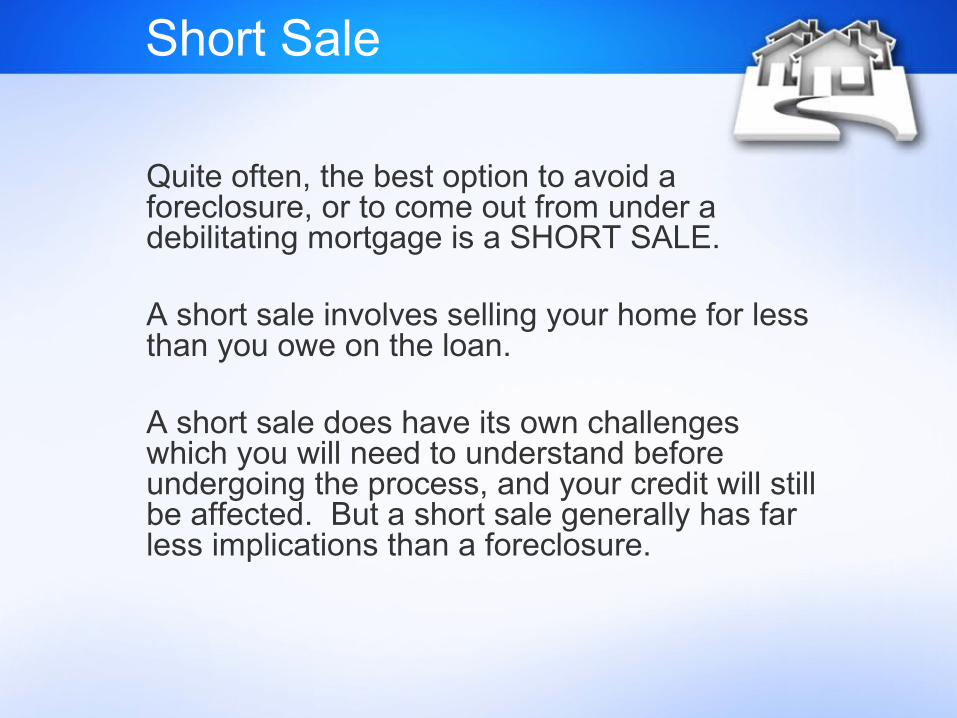

Quite often, the best option to avoid a foreclosure, or to come out from under a debilitating mortgage is a SHORT SALE.

A short sale involves selling your home for less than you owe on the loan.

A short sale does have its own challenges which you will need to understand before undergoing the process, and your credit will still be affected. But a short sale generally has far less implications than a foreclosure.

Short Sale

Q: How do I know if I owe more than I can sell my home for?

The simplest and most affordable way is to ask a qualified real estate agent to perform a Comparable Market Analysis (CMA.)

There should be no cost involved, and a good agent can give you an accurate assessment of your home’s value.

FAQ

Q: Can a foreclosure be stopped?

Yes. You can slow down and stop a foreclosure. If you have missed payments and the bank is “demanding payment” there are a couple of ways to stop the foreclosure.

•Reinstatement – pay all that is due•Attempt a loan modification•Offer a deed-in-lieu of foreclosure•Short sale

FAQ

There is no guarantee that your foreclosure will be stopped via any of the above methods. We have however successfully stopped foreclosures several times through the short sale process. It is imperative that you act quickly in contacting a real estate professional to begin the short sale if you choose that path.

Q: How long does it take to do a short sale?

It depends on a variety of factors… primarily though it depends on the bank or banks involved in the process.. Generally speaking short sales take somewhere between 2 and 6 months to complete.

The process can be somewhat streamlined if you choose a seasoned, experienced short sale agent, and you act timely in providing all the documentation the agent requests.

FAQ

Q: How much will a short sale cost me?

Generally it will not cost you anything. The bank, as part of the negotiation process, will agree to pay closing costs, agent fees, and contractual seller concessions.

However, if you have outstanding liens on your property, the bank will likely not pay those things. A few examples would be…

•Outstanding HOA fees•Outstanding utility bills•Outstanding taxes or other liens

FAQ

Q: Will I still owe the bank money after the short sale is complete?

That is a question that cannot be answered upfront. By the nature of the situation there is a deficiency between the sales price and the loan amount. Homeowners, unless it is forgiven by the bank, are responsible for that deficiency.

The goal is to negotiate with the bank to provide an approval letter that doesn’t state that the bank reserves the right to collect on that deficiency.

If they will not issue the letter in this manner, you have the right to not complete the short sale.

FAQ

Q: So, a short sale will affect my credit?

Yes. Anytime you don’t fulfill a financial obligation as originally agreed it will have a negative impact on your credit.

However, in the vast majority of cases, a short sale is far less damaging to your credit than a foreclosure.

FAQ

Q: What about tax considerations?

If the bank(s) issue you a 1099C (Cancellation of Debt) then the amount cancelled is considered income and could become a taxable event.

However, if the home is a primary residence, it likely falls under the 2007 Mortgage Debt Relief Act, which would likely exclude you from any tax liability regarding the short sale.

There are limits and restrictions within the Act. We encourage anyone with concerns about the tax ramifications to seek the advice of a qualified tax attorney or CPA. Nothing in this presentation should be construed as legal or tax advice.

FAQ

NOTE: Protection under the 2007 Mortgage Debt Relief Act is set to expire at the end of 2013. If you are considering a short sale, you should do so sooner, rather than later.

Q: Do I need a REALTOR to do a short sale?

You will be required to contract with a licensed real estate agent to do a short sale.

CAUTION! – There are a LOT of real estate agents attempting to negotiate short sales. Many of them are inexperienced and less than competent concerning the process.

We HIGHLY recommend you hire a REALTOR who is an experienced short sale agent and who has a proven record of success in negotiating and navigating this difficult process.

FAQ

Act Before It Is Too LateA final word of caution…

It is part of human nature for many people to hide from, or attempt to ignore a problem, hoping it will go away. Being delinquent on your mortgage will NOT go away.

It is IMPORTANT that you act right away to improve your chances for success in the short sale process. Like…. right now!

Seriously, I cannot stress this enough. Act today to give yourself the best possible odds of avoiding the damaging impact of a FORECLOSURE!

Disclaimer

We are not attorneys or tax consultants. As such, we cannot offer legal or tax advice, and always suggest that our clients seek the appropriate legal or tax advice as necessary.

To that end, nothing in this presentation is intended, nor should it be interpreted as legal advice or tax advice. This is strictly intended as an educational presentation of the considerations available to a consumer who is considering a short sale.

Jeff Edmisten and Ruthie Buck, nor Coldwell Banker Elite or any parent companies assume any liability for the information contained within this presentation, or for any actions taken or encountered as a result of the use or implementation of the information in this presentation.