shane theriault pierre-olivier lachance garik theriault sierra daigle

TRANSCRIPT

Strategic Management Plan

Shane TheriaultPierre-Olivier Lachance

Garik TheriaultSierra Daigle

2

Overview

Company Overview• Company Background

• Existing Mission and Vision• Proposed Mission and Vision• Current StrategiesExternal Assessment• Industry Analysis• Opportunities and Threats • EFE Matrix• CPM MatrixInternal Assessment• Organizational Structure• Segment Analysis• Financial Conditions• Strengths and Weaknesses• IFE Matrix

Strategy Formulation• SWOT Matrix• Space Matrix• Grand Strategy Matrix• BCG & IE Matrix• Matrix Analysis• Possible Strategies• QSPM MatrixStrategic Implementation• 3 Year Objectives• Strategies & Cost• EPS/EBIT• Projected FinancialsStrategic Evaluation• Balanced Score CardCompany Update

3

Company Background: Origins

Coca Cola Animated History

4

Company Background: History

• 1928 – Coca-Cola traveled with the US Olympics team to Amsterdam, and began global expansion

• 1935 – Coca-Cola was certified Kosher by Rabbi Tobias Geffen

• 1941 – Fanta is introduced in World War II during a trade embargo against Germany on cola syrup

• 1944 – The one billionth gallon of Coca-Cola Syrup was made

• 1963 – Coca-Cola’s first attempt to make a diet drink using saccharin

• 1982 - Coca-Cola purchased Columbia Pictures, sold to Sony in 1989

• 1985 – New Coke was presented to test tasters who enjoyed it better then Coke and Pepsi; however, top management kept the old formula “Coca-Cola Classic” (which uses a high fructose corn syrup as sweeter instead of the proposed sugar can) in order to avoid possible backlash from customers. It is now only available in select countries

• 1990s – Introduction of healthier beverages including Minute Maid Juices to Go, Powerade sports beverage, flavored tea Nestea (in a joint venture with Nestle), Fruitopia fruit drink and Dasani water

• 2007 – World of Coca-Cola was built

5

Company Background: Owned Brands

6

Existing Vision Statement

People: Be a great place to work where people are inspired to be the best they can be.Portfolio: Bring to the world a portfolio of quality beverage brands that anticipate and satisfy people's desires and needs.Partners: Nurture a winning network of customers and suppliers, together we create mutual, enduring value. Planet: Be a responsible citizen that makes a difference by helping build and support sustainable communities.Profit: Maximize long-term return to shareowners while being mindful of our overall responsibilities.Productivity: Be a highly effective, lean and fast-moving organization.

7

Existing Mission Statement

To refresh the world...To inspire moments of optimism and happiness...To create value and make a difference.

8

Proposed Vision Statement

Coca-Cola aspires to refresh the world, to inspire moments of optimism and happiness, and to

create value and make a difference.

9

Proposed Mission Statement

People: Be a great place to work where people are inspired to be the best they can be(9)(6).Portfolio: Bring to the world(3) a portfolio of quality beverage brands that anticipate and satisfy people's desires and needs(2).Partners: Nurture a winning, network of customers(1) and suppliers, together we create mutual, enduring value. Planet: Be a responsible citizen that makes a difference by helping build and support sustainable communities(5).Profit: Maximize long-term return to shareowners(8) while being mindful of our overall responsibilities(7).Productivity: Be a highly effective, lean and fast-moving organization(4). 1. Customers

2. Products or services3. Markets4. Technology5. Concern for survival, growth, and profitability6. Philosophy7. Self-concept8. Concern for public image9. Concern for employees

10

Current Strategies

• Vision 2020• Profit, People, Portfolio, Partners, Planet, Productivity• Double the numbers of servings of its products -- water,

soft-drinks, juices and the like -- consumed per day to more than 3 billion.

• 12 month multicultural plans • 5by20™ program• Expedition 206• 2020 water use reduction and replenishment

11

Million Dollar Question

“Should Coke strive to enter the snack or food business in order to remain competitive with

Pepsi Co”?

12

External Assessment

13

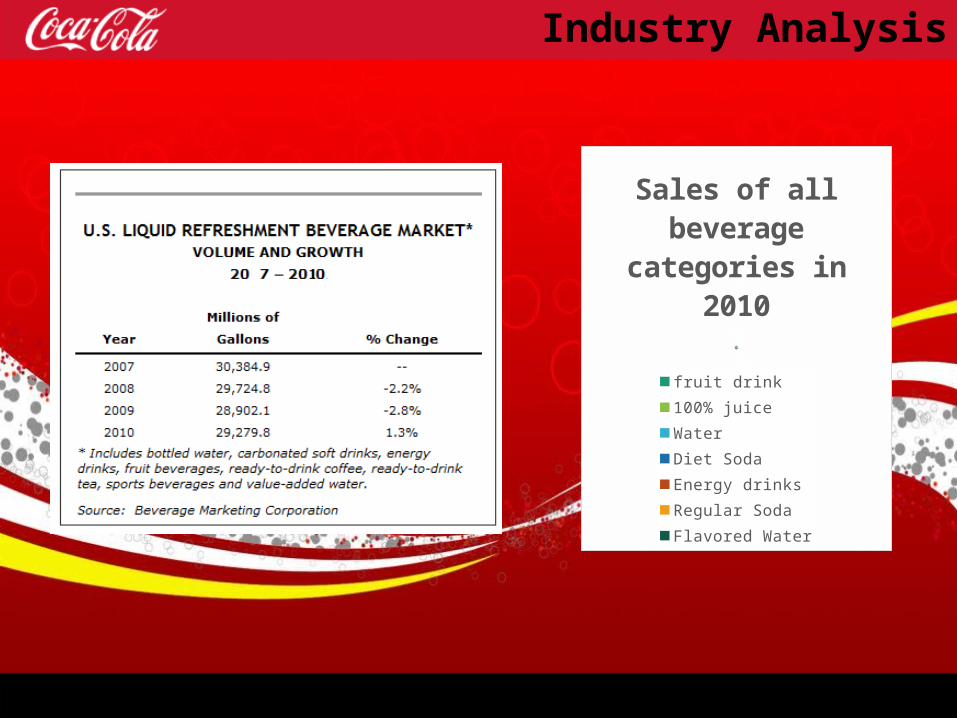

Industry Analysis

11%

13%

13%

14%14%

32%

2%

Sales of all bev-erage categories

in 2010

fruit drink 100% juiceWater Diet SodaEnergy drinks Regular SodaFlavored Water

14

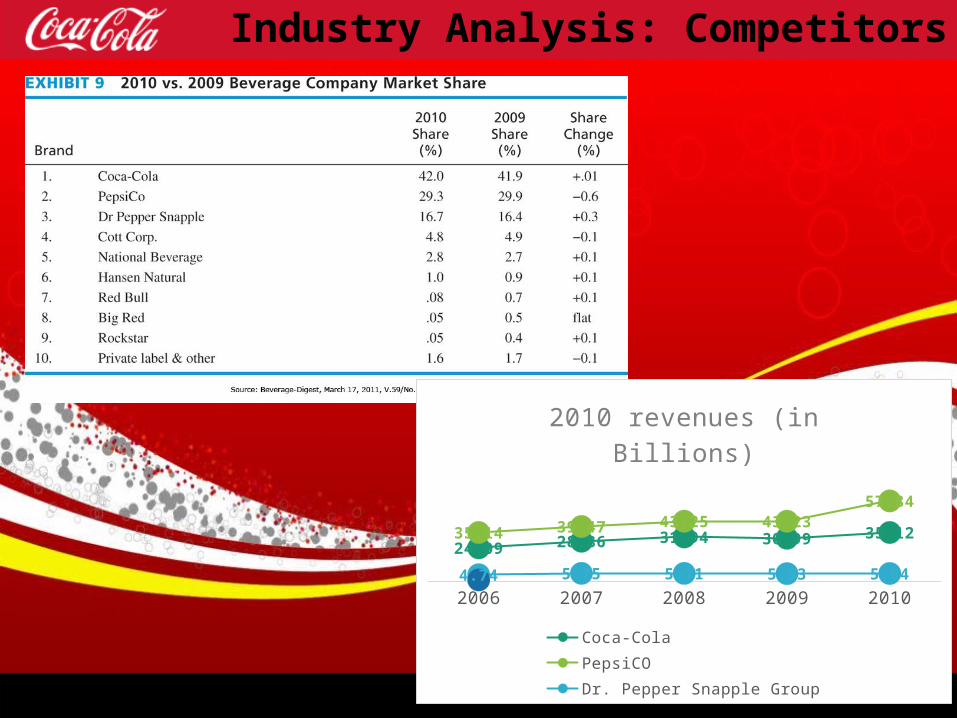

Industry Analysis: Competitors

2006 2007 2008 2009 2010

24.0928.86 31.94 30.99

35.1235.1439.47

43.25 43.23

57.84

4.74 5.75 5.71 5.53 5.64

2010 revenues (in Billions)

Coca-Cola PepsiCODr. Pepper Snapple Group

15

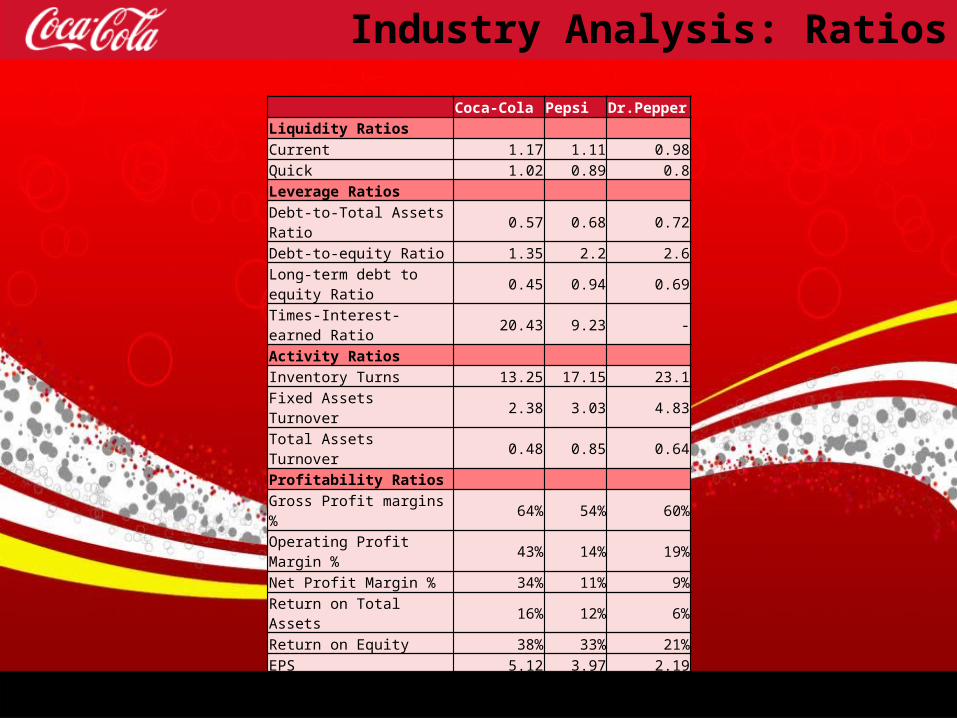

Industry Analysis: Ratios

Coca-Cola Pepsi Dr.PepperLiquidity Ratios Current 1.17 1.11 0.98Quick 1.02 0.89 0.8Leverage Ratios Debt-to-Total Assets Ratio 0.57 0.68 0.72Debt-to-equity Ratio 1.35 2.2 2.6

Long-term debt to equity Ratio 0.45 0.94 0.69

Times-Interest-earned Ratio 20.43 9.23 -Activity Ratios Inventory Turns 13.25 17.15 23.1Fixed Assets Turnover 2.38 3.03 4.83Total Assets Turnover 0.48 0.85 0.64Profitability Ratios Gross Profit margins % 64% 54% 60%Operating Profit Margin % 43% 14% 19%Net Profit Margin % 34% 11% 9%Return on Total Assets 16% 12% 6%Return on Equity 38% 33% 21%EPS 5.12 3.97 2.19P/E ratio 6.03 15.35 16.o5Growth Ratios (5 years) Sales 8.74% 12.18% 11.95%Net Income 19.37% 9.16% 2.05EPS 19.92% 10.35 -

16

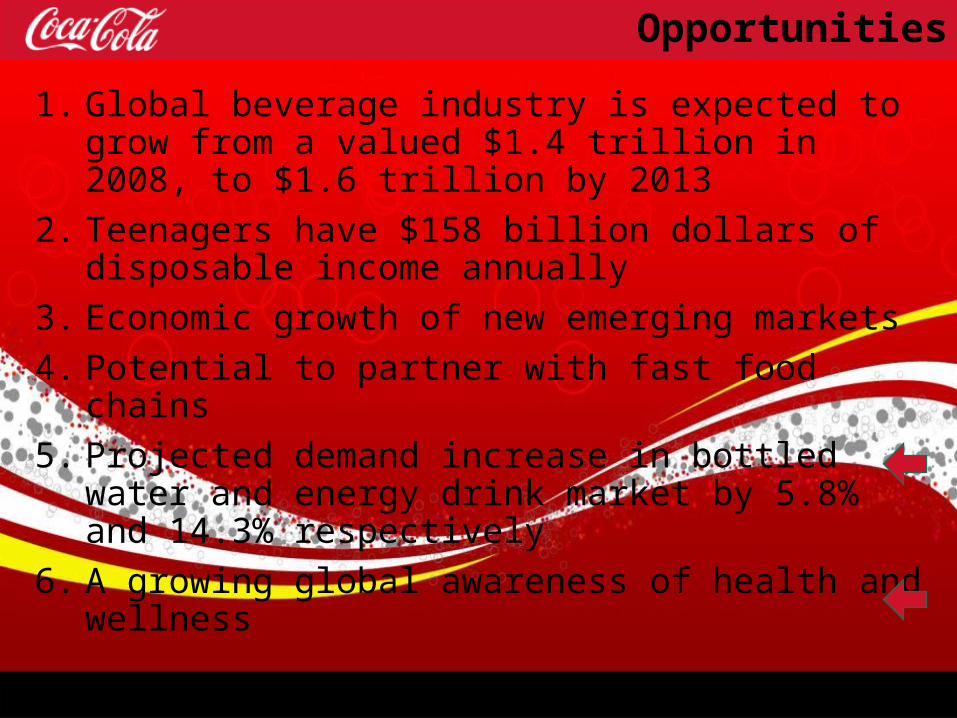

Opportunities

1. Global beverage industry is expected to grow from a valued $1.4 trillion in 2008, to $1.6 trillion by 2013

2. Teenagers have $158 billion dollars of disposable income annually

3. Economic growth of new emerging markets

4. Potential to partner with fast food chains

5. Projected demand increase in bottled water and energy drink market by 5.8% and 14.3% respectively

6. A growing global awareness of health and wellness

17

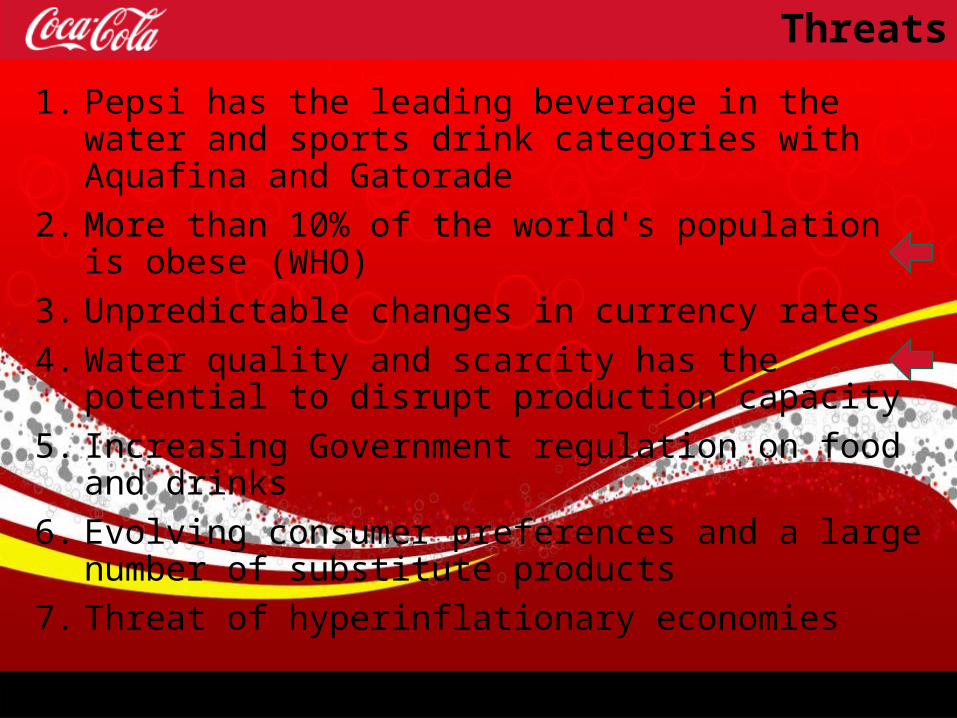

Threats

1. Pepsi has the leading beverage in the water and sports drink categories with Aquafina and Gatorade

2. More than 10% of the world's population is obese (WHO)

3. Unpredictable changes in currency rates

4. Water quality and scarcity has the potential to disrupt production capacity

5. Increasing Government regulation on food and drinks

6. Evolving consumer preferences and a large number of substitute products

7. Threat of hyperinflationary economies

18

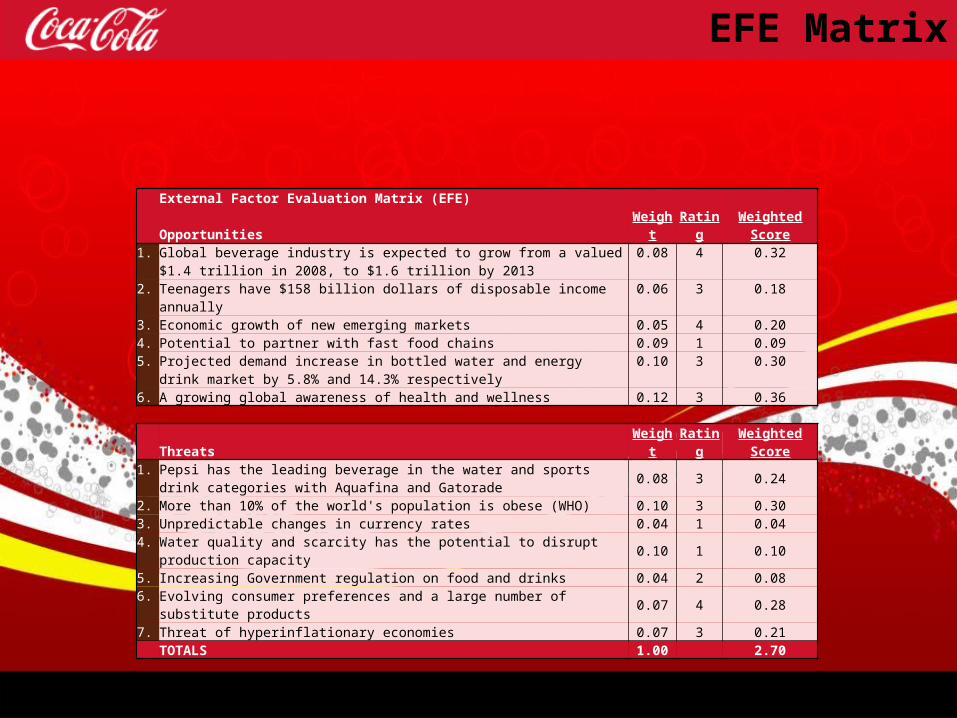

EFE Matrix

External Factor Evaluation Matrix (EFE) Opportunities Weight Rating Weighted Score1. Global beverage industry is expected to grow from a valued $1.4 trillion in 2008, to

$1.6 trillion by 20130.08 4 0.32

2. Teenagers have $158 billion dollars of disposable income annually 0.06 3 0.183. Economic growth of new emerging markets 0.05 4 0.204. Potential to partner with fast food chains 0.09 1 0.095. Projected demand increase in bottled water and energy drink market by 5.8% and

14.3% respectively0.10 3 0.30

6. A growing global awareness of health and wellness 0.12 3 0.36

Threats Weight Rating Weighted Score1. Pepsi has the leading beverage in the water and sports drink categories with Aquafina

and Gatorade 0.08 3 0.24

2. More than 10% of the world's population is obese (WHO) 0.10 3 0.303. Unpredictable changes in currency rates 0.04 1 0.044. Water quality and scarcity has the potential to disrupt production capacity 0.10 1 0.10

5. Increasing Government regulation on food and drinks 0.04 2 0.086. Evolving consumer preferences and a large number of substitute products 0.07 4 0.28

7. Threat of hyperinflationary economies 0.07 3 0.21

TOTALS 1.00 2.70

19

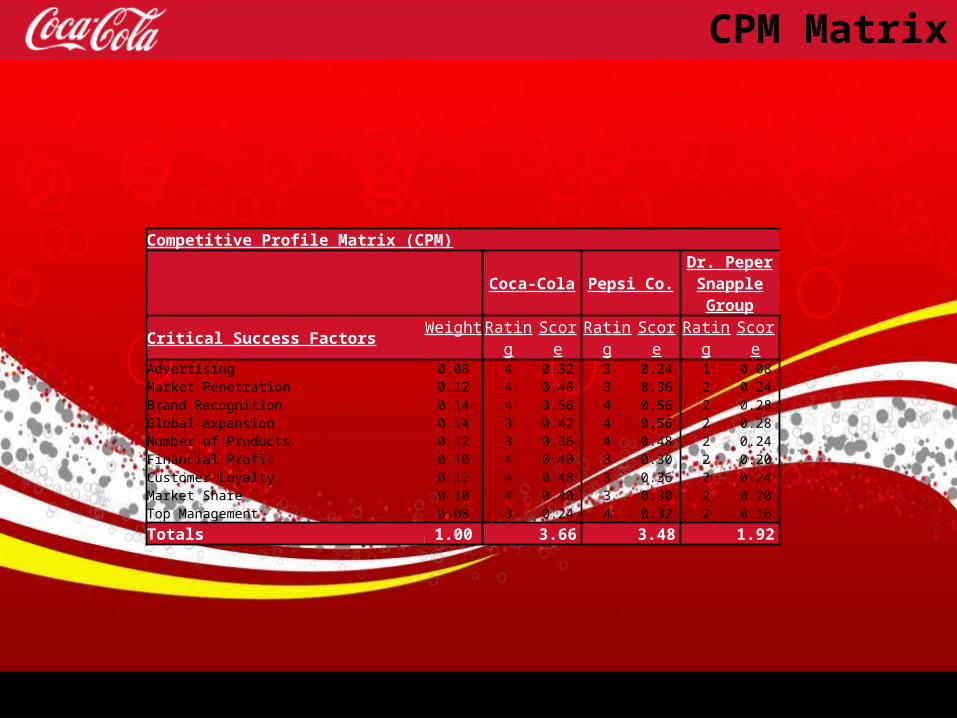

CPM Matrix

Competitive Profile Matrix (CPM)

Coca-Cola Pepsi Co.Dr. Peper Snapple Group

Critical Success Factors Weight Rating Score Rating Score Rating ScoreAdvertising 0.08 4 0.32 3 0.24 1 0.08

Market Penetration 0.12 4 0.48 3 0.36 2 0.24Brand Recognition 0.14 4 0.56 4 0.56 2 0.28Global expansion 0.14 3 0.42 4 0.56 2 0.28Number of Products 0.12 3 0.36 4 0.48 2 0.24Financial Profit 0.10 4 0.40 3 0.30 2 0.20Customer Loyalty 0.12 4 0.48 3 0.36 2 0.24Market Share 0.10 4 0.40 3 0.30 2 0.20

Top Management 0.08 3 0.24 4 0.32 2 0.16

Totals 1.00 3.66 3.48 1.92

20

Internal Assessment

21

Organizational Structure

Mahtar Kent, CEO, Chairman of the Board of

Directors

Gary P. Fayard, EVP &

VPO

Joseph V. Tripodi, EVP

& Chief Marketing/ Commercial

Officer

Jerry S. Wilson, SVP,

Chief Customer

and commercial

Officer

Harry L. Anderson, SVP, Global

Business and Technology

Services

Alexander B. Cummings Jr.

EVP, Chief Administrative

Officer

Ahmet C. Bozer,

President of Eurasia &

Africa Group

J Alexander M Douglas Jr., President of

the North America Group

Glenn G. Jordan S.,

President of Pacific Group

Dominique Reiniche,

President of Europe Group

Steven A. Cahillane,

President/ CEO of Coca-Cola

Refreshments

José Octavio Reyes,

President of the Latin America Group

Irial Finan, EVP & President,

Bottling Investments/ Supply Chain

Geoffrey J. Kelly,

SVP, General Counsel

Guy Wollaert, SVP and

Chief Technical

Officer

Clyde C Tuggle, SVP,

Global Affaires/

Communica-tions

Ingrid Saunders

Jones, SVP, Global

Community Connections

Ceree Eberly, Chief

People Officer

22

Segment Analysis

Eurasia & Africa7%

Europe13%

Latin America11%

North America32%

Pacific14%

Bottleing Investments23%

Coporate0%

Revenues by segment in 2010 (%)

23

Regional Boundaries

24

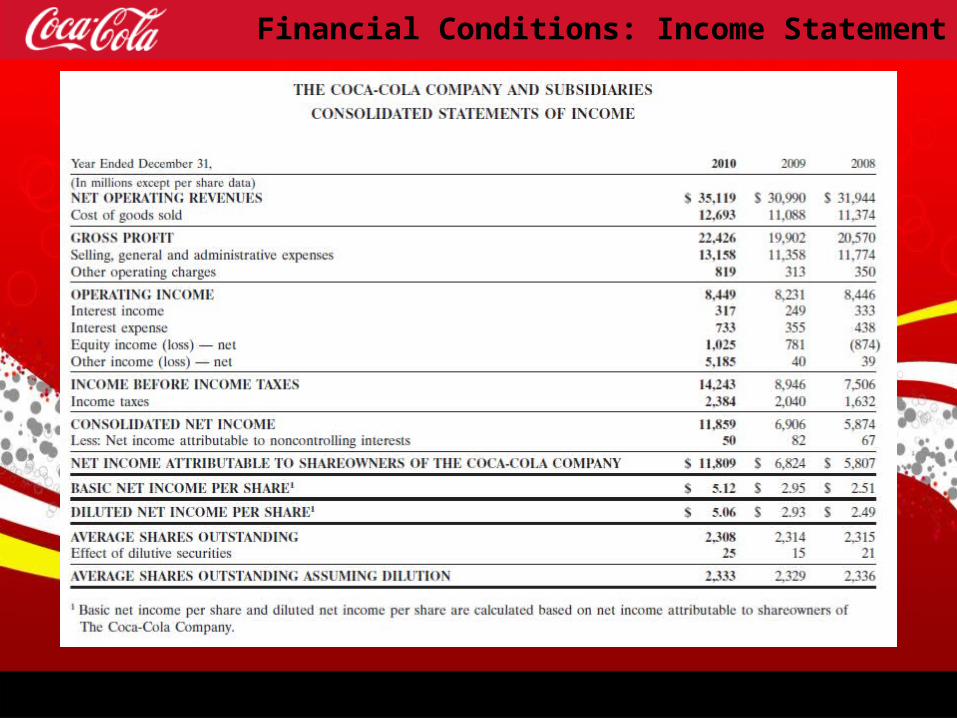

Financial Conditions: Income Statement

25

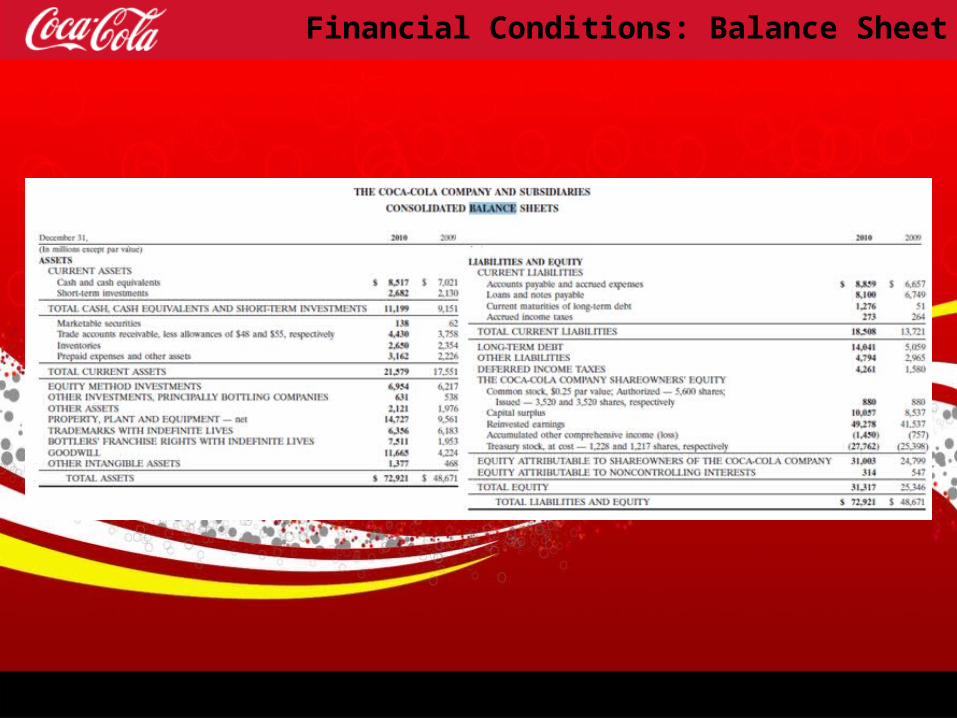

Financial Conditions: Balance Sheet

26

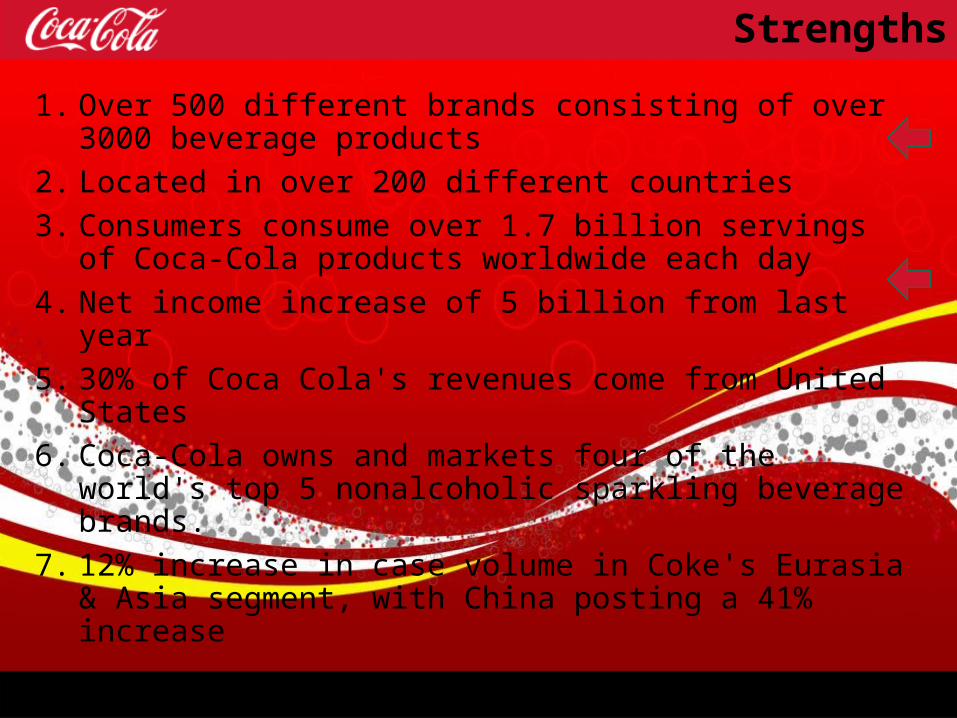

Strengths

1. Over 500 different brands consisting of over 3000 beverage products

2. Located in over 200 different countries

3. Consumers consume over 1.7 billion servings of Coca-Cola products worldwide each day

4. Net income increase of 5 billion from last year

5. 30% of Coca Cola's revenues come from United States

6. Coca-Cola owns and markets four of the world's top 5 nonalcoholic sparkling beverage brands.

7. 12% increase in case volume in Coke's Eurasia & Asia segment, with China posting a 41% increase

27

Weaknesses

1. Coke is not competing in the snack and food industries

2. 20% of the bottle supply are from companies Coca Cola does not have controlling interest

3. There are not a huge amount of sub-industries in the beverage market in which Coca-Cola does not operate

4. Only 3 of the 18 top executives are women

5. Long-term debt of 14 billion, up from last year's 5 billion

6. Trademark Coca-Cola beverages accounted for 51% of US case volume

28

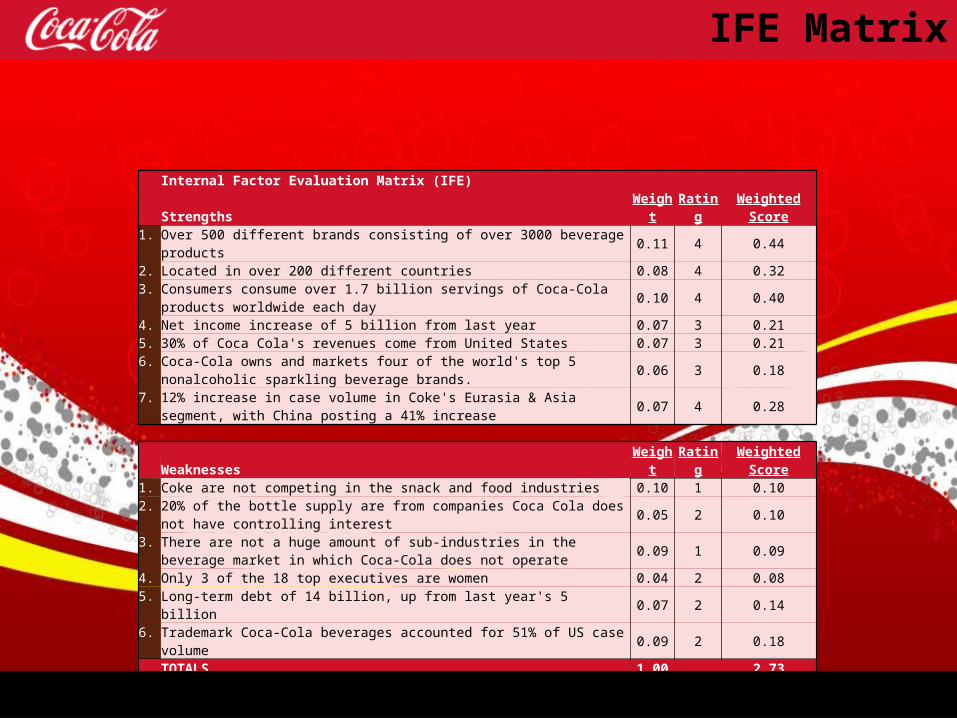

IFE Matrix

Internal Factor Evaluation Matrix (IFE) Strengths Weight Rating Weighted Score1. Over 500 different brands consisting of over 3000 beverage products 0.11 4 0.442. Located in over 200 different countries 0.08 4 0.323. Consumers consume over 1.7 billion servings of Coca-Cola products worldwide each

day 0.10 4 0.40

4. Net income increase of 5 billion from last year 0.07 3 0.215. 30% of Coca Cola's revenues come from United States 0.07 3 0.216. Coca-Cola owns and markets four of the world's top 5 nonalcoholic sparkling beverage

brands. 0.06 3 0.18

7. 12% increase in case volume in Coke's Eurasia & Asia segment, with China posting a 41% increase 0.07 4 0.28

Weaknesses Weight Rating Weighted Score1. Coke are not competing in the snack and food industries 0.10 1 0.102. 20% of the bottle supply are from companies Coca Cola does not have controlling

interest 0.05 2 0.10

3. There are not a huge amount of sub-industries in the beverage market in which Coca-Cola does not operate 0.09 1 0.09

4. Only 3 of the 18 top executives are women 0.04 2 0.085. Long-term debt of 14 billion, up from last year's 5 billion 0.07 2 0.146. Trademark Coca-Cola beverages accounted for 51% of US case volume 0.09 2 0.18

TOTALS 1.00 2.73

29

Strategy Formulation

30

SWOT Matrix

SO Strategies

SO1 - Move to the alcoholic beverage industry (S2, O1)SO2 - Increase expedition 206 (S6, O2, O6)SO3 - Increase number of healthy products(S1, S2, O5, O6)SO4 - Increase number of culturally specific products (S2, S5, O1)

ST Strategies

ST1 - Increase health programs (S1, S2, T2, T5)ST2 – Expansion and increased marketing for energy drinks (S6, T1)

WO Strategies

WO1 - Move to the snack and foods industry (W1, W3, O2, O3, O4,)

WT Strategies

WT - Increase Marketing and Advertising (W3, T1, T6)

31

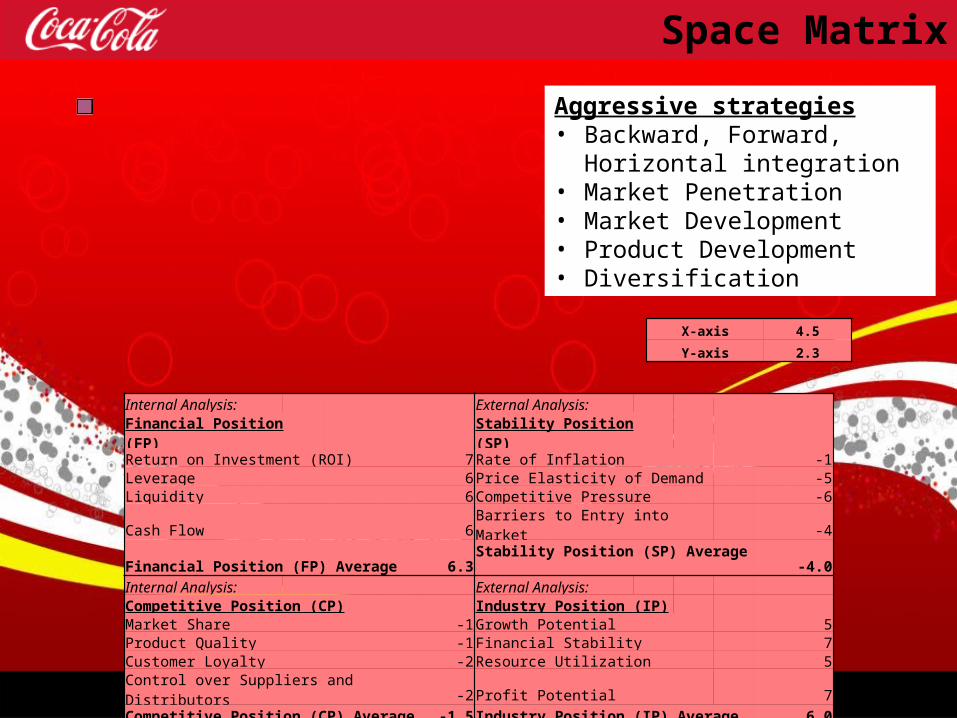

Space Matrix

Aggressive strategies• Backward, Forward, Horizontal

integration• Market Penetration• Market Development• Product Development• Diversification

X-axis 4.5

Y-axis 2.3

Internal Analysis: External Analysis: Financial Position (FP) Stability Position (SP) Return on Investment (ROI) 7Rate of Inflation -1Leverage 6Price Elasticity of Demand -5Liquidity 6Competitive Pressure -6Cash Flow 6Barriers to Entry into Market -4Financial Position (FP) Average 6.3Stability Position (SP) Average -4.0Internal Analysis: External Analysis: Competitive Position (CP) Industry Position (IP) Market Share -1Growth Potential 5Product Quality -1Financial Stability 7Customer Loyalty -2Resource Utilization 5Control over Suppliers and Distributors -2Profit Potential 7Competitive Position (CP) Average -1.5Industry Position (IP) Average 6.0

32

Grand Strategy Matrix

Rapid Market Growth

Quadrant II Quadrant I

Weak Competitive

Position

Strong

Competitive Position

Quadrant III Quadrant IV

Slow Market Growth

Quadrant IV Strategies• Related Diversification• Unrelated diversification• Joint ventures

33

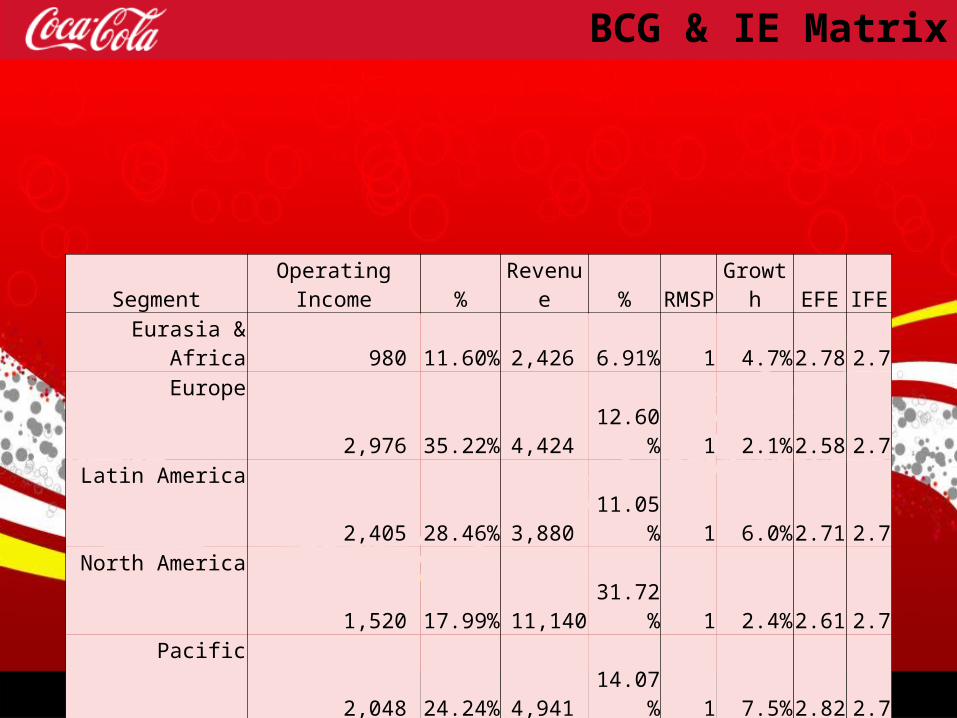

BCG & IE Matrix

Segment Operating Income % Revenue % RMSP Growth EFE IFE

Eurasia & Africa 980 11.60% 2,426 6.91% 1 4.7% 2.78 2.7Europe 2,976 35.22% 4,424 12.60% 1 2.1% 2.58 2.7

Latin America 2,405 28.46% 3,880 11.05% 1 6.0% 2.71 2.7North America 1,520 17.99% 11,140 31.72% 1 2.4% 2.61 2.7

Pacific 2,048 24.24% 4,941 14.07% 1 7.5% 2.82 2.7Bottling Investments 227 2.69% 8,216 23.39%

Corporate (1,707) -20.20% 92 0.26% Total 8,449 1 35,119 1

34

BCG Matrix

1 010

-10

0.5Relative Market Share

0Growth Rate

4

53

1

2

Star Strategies• Backward, Forward, Horizontal

integration• Market Penetration• Market Development• Product Development

35

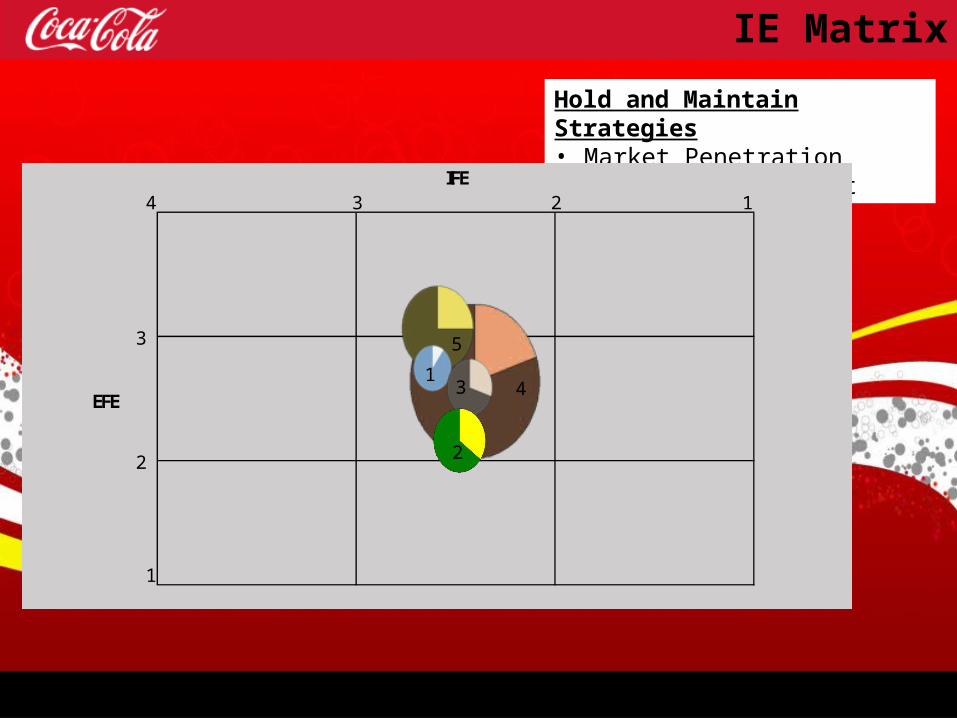

IE Matrix

4 1

EFE

1

IFE23

3

2

4

5

13

2

Hold and Maintain Strategies• Market Penetration• Product Development

36

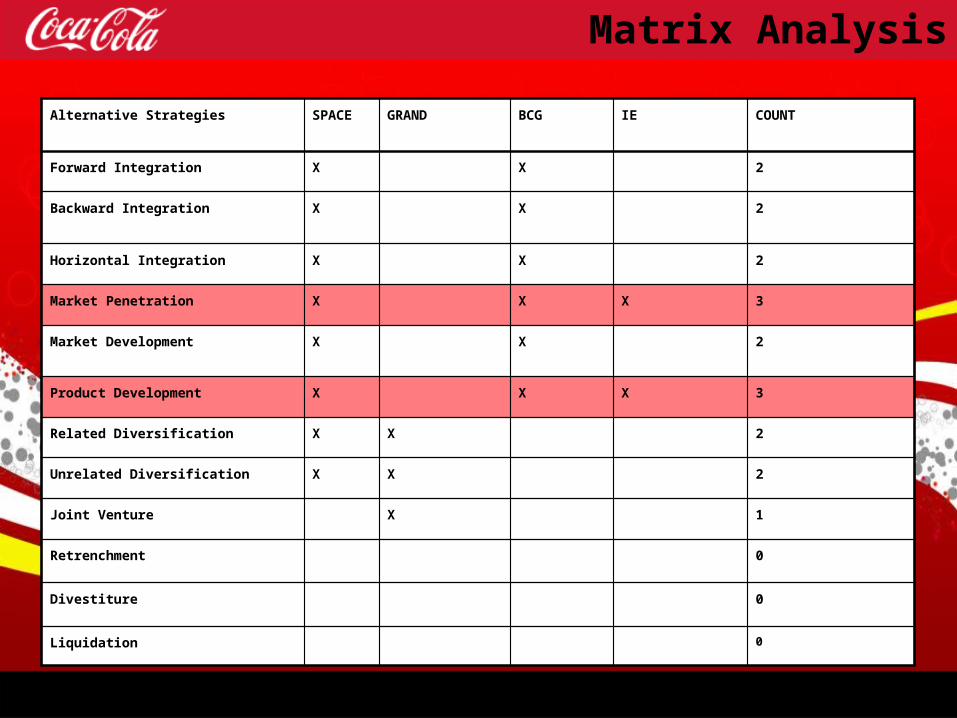

Matrix Analysis

Alternative Strategies SPACE GRAND BCG IE COUNT

Forward Integration X X 2

Backward Integration X X 2

Horizontal Integration X X 2

Market Penetration X X X 3

Market Development X X 2

Product Development X X X 3

Related Diversification X X 2

Unrelated Diversification X X 2

Joint Venture X 1

Retrenchment 0

Divestiture 0

Liquidation 0

37

Million Dollar Question

“Should Coke Strive to enter the snack or food business in order to remain competitive with

Pepsi Co”?

38

Million Dollar Question

No

39

Possible Strategies

• Market Penetration• SO4 - Increase number of culturally specific products

• Product development• SO3 - Increase number of healthy products• SO4 - Increase number of culturally specific products

40

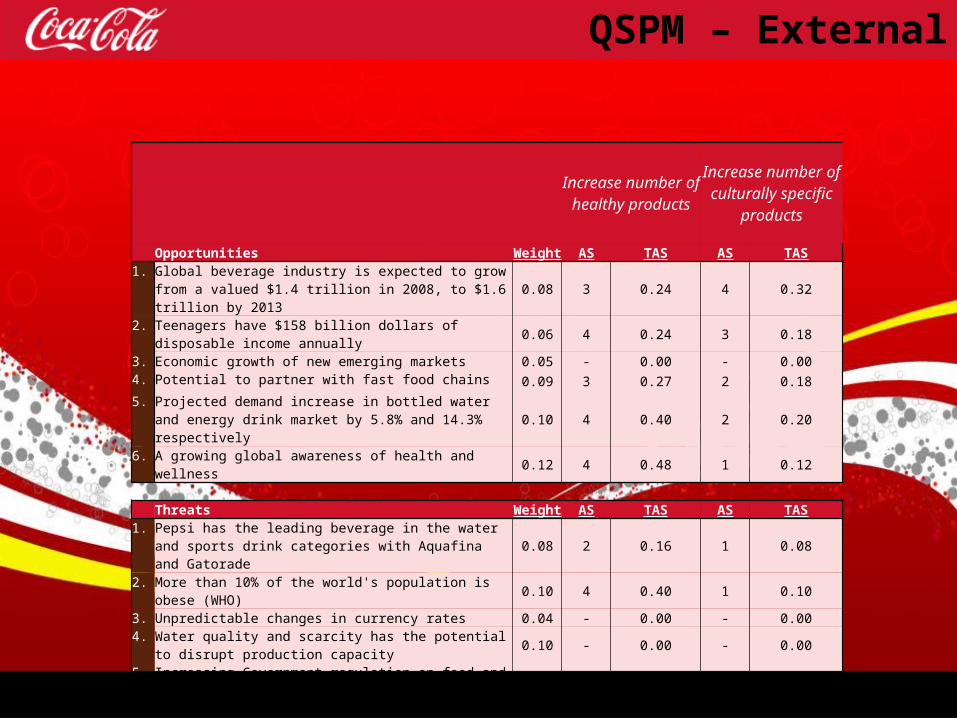

QSPM – External

Increase number of healthy products

Increase number of culturally specific

products

Opportunities Weight AS TAS AS TAS1. Global beverage industry is expected to grow from a valued $1.4

trillion in 2008, to $1.6 trillion by 2013 0.08 3 0.24 4 0.32

2. Teenagers have $158 billion dollars of disposable income annually0.06 4 0.24 3 0.18

3. Economic growth of new emerging markets 0.05 - 0.00 - 0.004. Potential to partner with fast food chains 0.09 3 0.27 2 0.185. Projected demand increase in bottled water and energy drink

market by 5.8% and 14.3% respectively 0.10 4 0.40 2 0.20

6. A growing global awareness of health and wellness 0.12 4 0.48 1 0.12

Threats Weight AS TAS AS TAS1. Pepsi has the leading beverage in the water and sports drink

categories with Aquafina and Gatorade 0.08 2 0.16 1 0.08

2. More than 10% of the world's population is obese (WHO) 0.10 4 0.40 1 0.103. Unpredictable changes in currency rates 0.04 - 0.00 - 0.004. Water quality and scarcity has the potential to disrupt production

capacity 0.10 - 0.00 - 0.00

5. Increasing Government regulation on food and drinks 0.04 - 0.00 - 0.006. Evolving consumer preferences and a large number of substitute

products 0.07 3 0.21 4 0.28

7. Threat of hyperinflationary economies 0.07 - 0.00 - 0.00

41

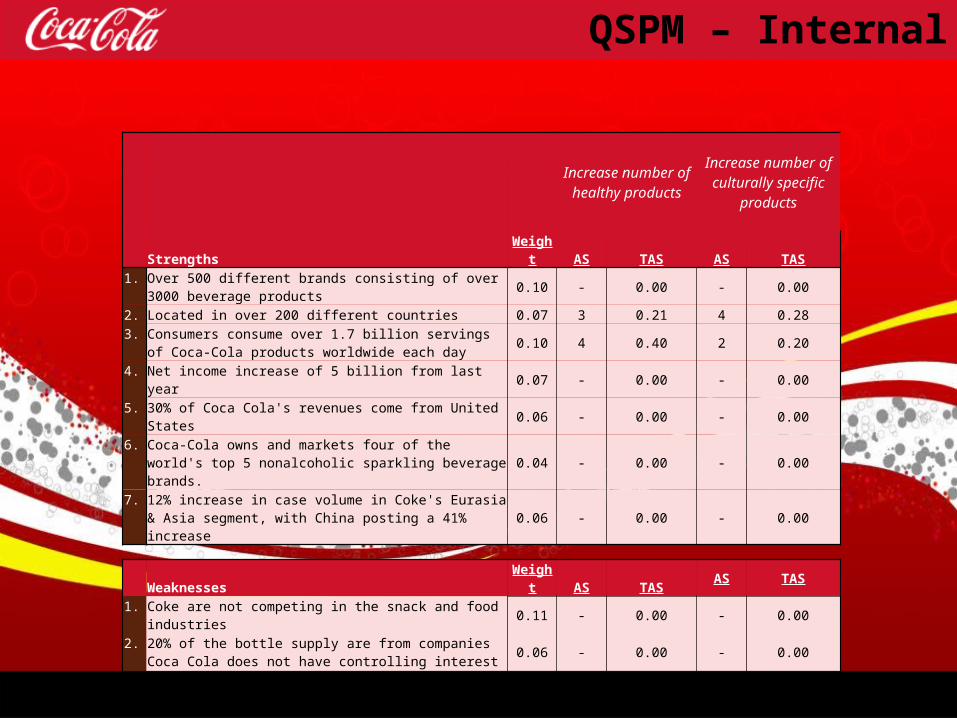

QSPM – Internal

Increase number of healthy products

Increase number of culturally specific

products

Strengths Weight AS TAS AS TAS1. Over 500 different brands consisting of over 3000 beverage

products 0.10 - 0.00 - 0.00

2. Located in over 200 different countries 0.07 3 0.21 4 0.283. Consumers consume over 1.7 billion servings of Coca-Cola

products worldwide each day 0.10 4 0.40 2 0.20

4. Net income increase of 5 billion from last year 0.07 - 0.00 - 0.005. 30% of Coca Cola's revenues come from United States 0.06 - 0.00 - 0.006. Coca-Cola owns and markets four of the world's top 5

nonalcoholic sparkling beverage brands. 0.04 - 0.00 - 0.00

7. 12% increase in case volume in Coke's Eurasia & Asia segment, with China posting a 41% increase 0.06 - 0.00 - 0.00

Weaknesses Weight AS TAS AS TAS1. Coke are not competing in the snack and food industries 0.11 - 0.00 - 0.002. 20% of the bottle supply are from companies Coca Cola does not

have controlling interest 0.06 - 0.00 - 0.00

3. There are not a huge amount of sub-industries in the beverage market in which Coca-Cola does not operate 0.10 3 0.30 4 0.40

4. Only 3 of the 18 top executives are women 0.05 - 0.00 - 0.005. Long-term debt of 14 billion, up from last year's 5 billion 0.08 - 0.00 - 0.006. Trademark Coca-Cola beverages accounted for 51% of US case

volume 0.10 - 0.00 - 0.00

TOTALS 3.31 2.34

42

Strategy Implementation

43

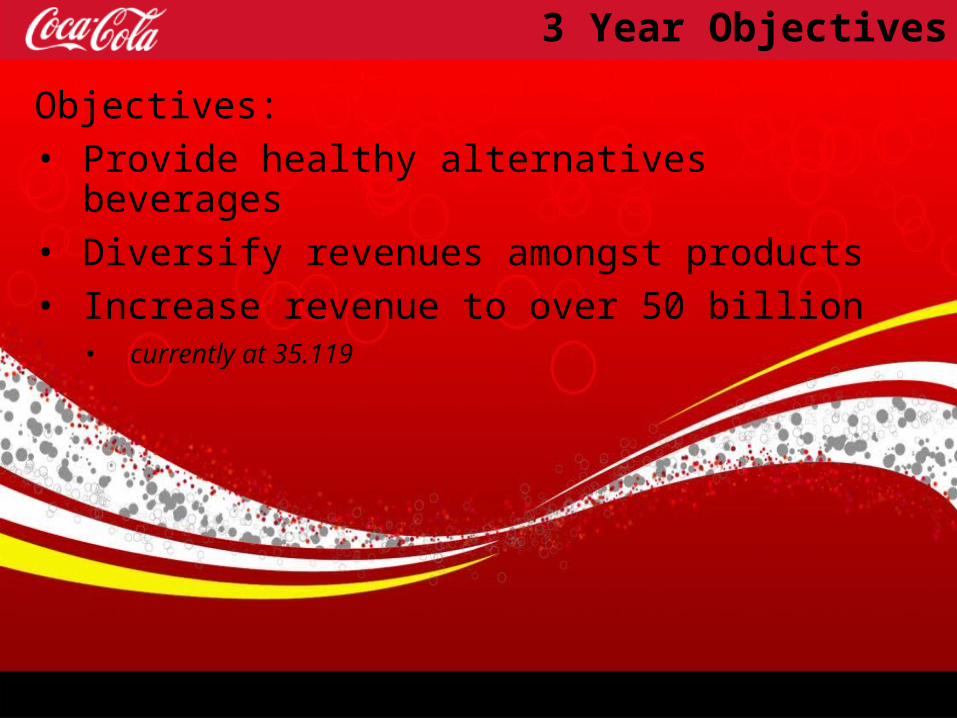

3 Year Objectives

Objectives:

• Provide healthy alternatives beverages

• Diversify revenues amongst products

• Increase revenue to over 50 billion• currently at 35.119

44

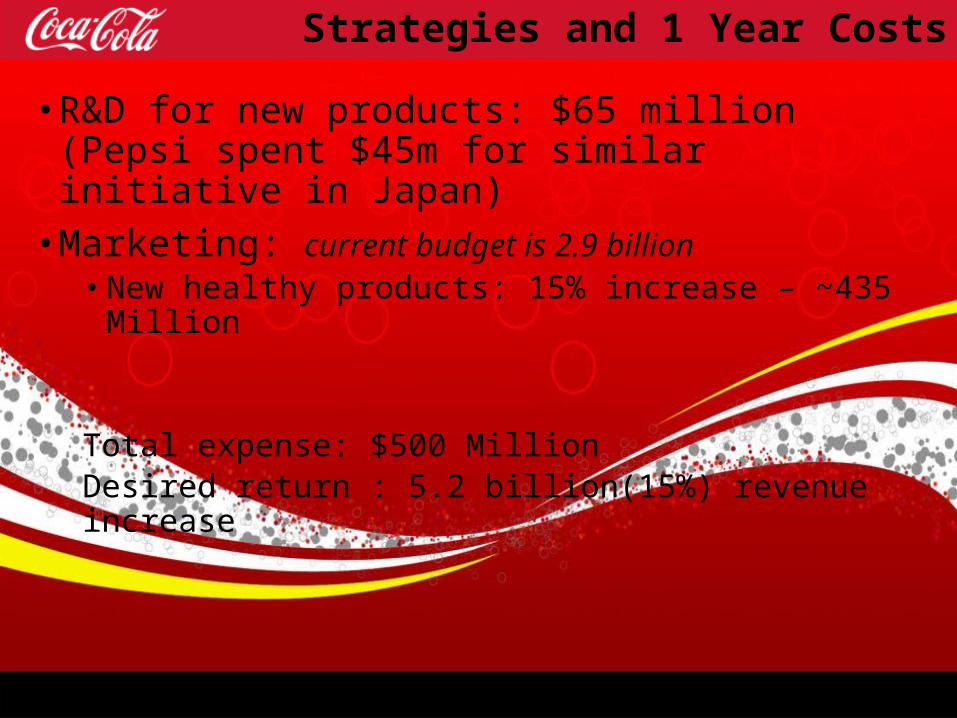

Strategies and 1 Year Costs

• R&D for new products: $65 million (Pepsi spent $45m for similar initiative in Japan)

• Marketing: current budget is 2.9 billion• New healthy products: 15% increase – ~435 Million

Total expense: $500 MillionDesired return : 5.2 billion(15%) revenue increase

45

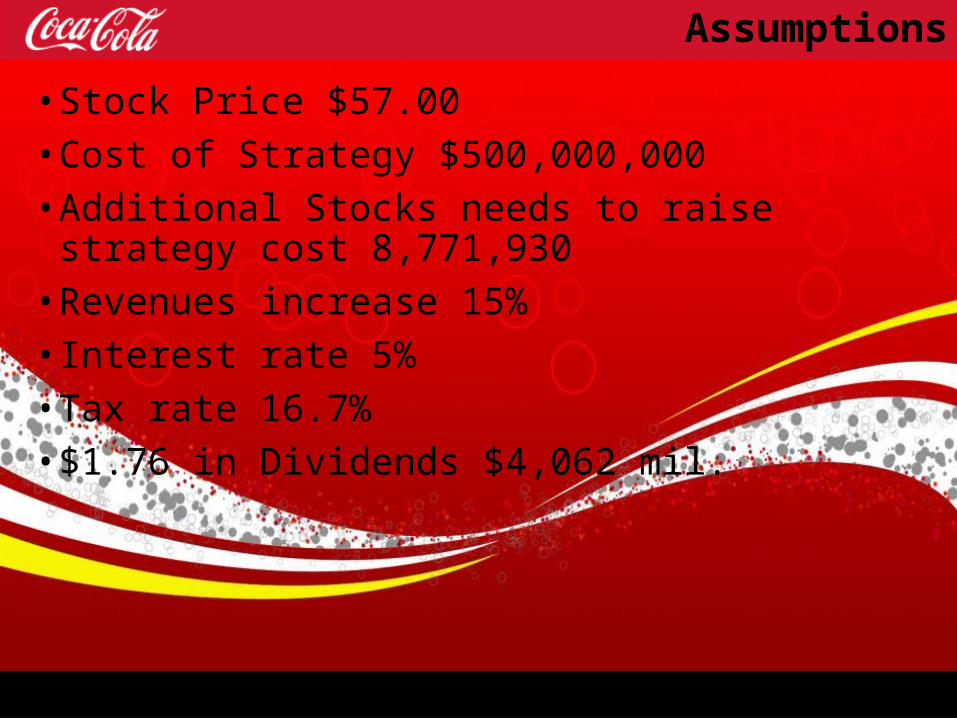

Assumptions

• Stock Price $57.00

• Cost of Strategy $500,000,000

• Additional Stocks needs to raise strategy cost 8,771,930

• Revenues increase 15%

• Interest rate 5%

• Tax rate 16.7%

• $1.76 in Dividends $4,062 mil.

46

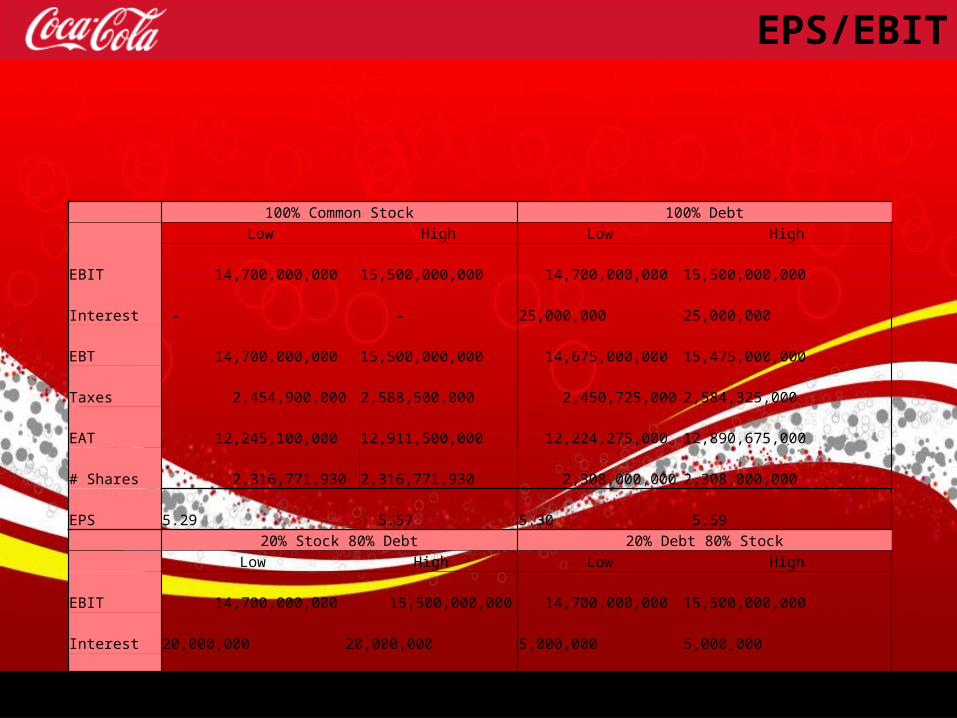

EPS/EBIT

100% Common Stock 100% Debt Low High Low HighEBIT 14,700,000,000 15,500,000,000 14,700,000,000 15,500,000,000 Interest - - 25,000,000 25,000,000 EBT 14,700,000,000 15,500,000,000 14,675,000,000 15,475,000,000 Taxes 2,454,900,000 2,588,500,000 2,450,725,000 2,584,325,000 EAT 12,245,100,000 12,911,500,000 12,224,275,000 12,890,675,000 # Shares 2,316,771,930 2,316,771,930 2,308,000,000 2,308,000,000 EPS 5.29 5.57 5.30 5.59 20% Stock 80% Debt 20% Debt 80% Stock Low High Low HighEBIT 14,700,000,000 15,500,000,000 14,700,000,000 15,500,000,000 Interest 20,000,000 20,000,000 5,000,000 5,000,000 EBT 14,680,000,000 15,480,000,000 14,695,000,000 15,495,000,000 Taxes 2,451,560,000 2,585,160,000 2,454,065,000 2,587,665,000 EAT 12,228,440,000 12,894,840,000 12,240,935,000 12,907,335,000 # Shares 2,309,754,386 2,309,754,386 2,315,017,544 2,315,017,544 EPS 5.29 5.58 5.29 5.58

47

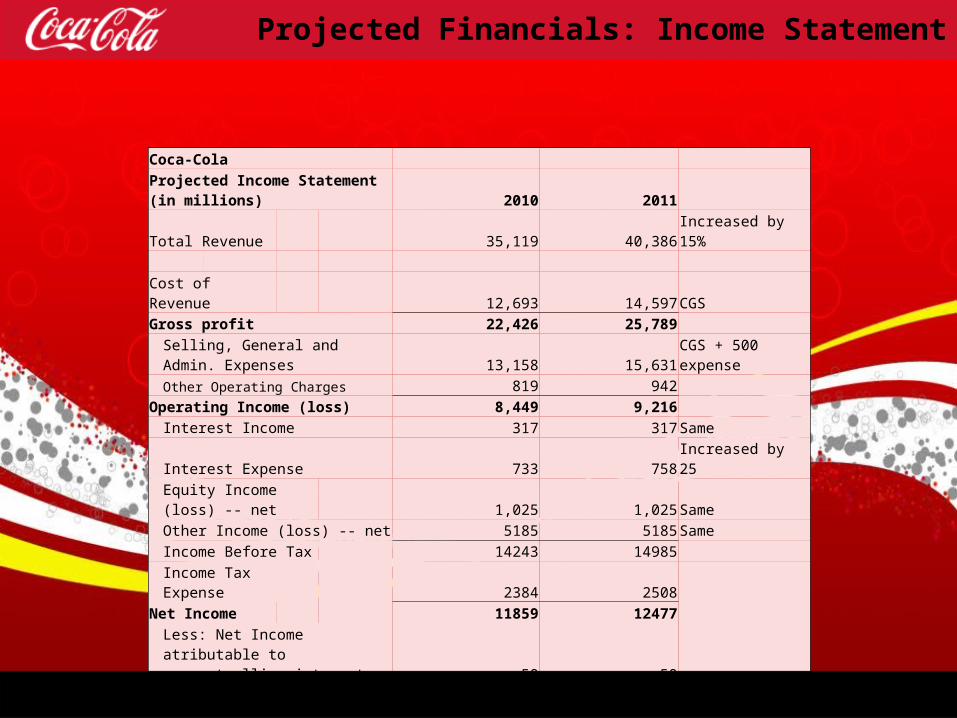

Projected Financials: Income Statement

Coca-Cola Projected Income Statement (in millions) 2010 2011 Total Revenue 35,119 40,386 Increased by 15% Cost of Revenue 12,693 14,597 CGSGross profit 22,426 25,789

Selling, General and Admin. Expenses 13,158 15,631 CGS + 500 expenseOther Operating Charges 819 942

Operating Income (loss) 8,449 9,216 Interest Income 317 317 SameInterest Expense 733 758 Increased by 25Equity Income (loss) -- net 1,025 1,025 SameOther Income (loss) -- net 5185 5185 SameIncome Before Tax 14243 14985 Income Tax Expense 2384 2508

Net Income 11859 12477

Less: Net Income atributable to noncontrolling interests 50 50

Net Income Attributable to Shareowners of The Coca-Cola Company 11809 12427

48

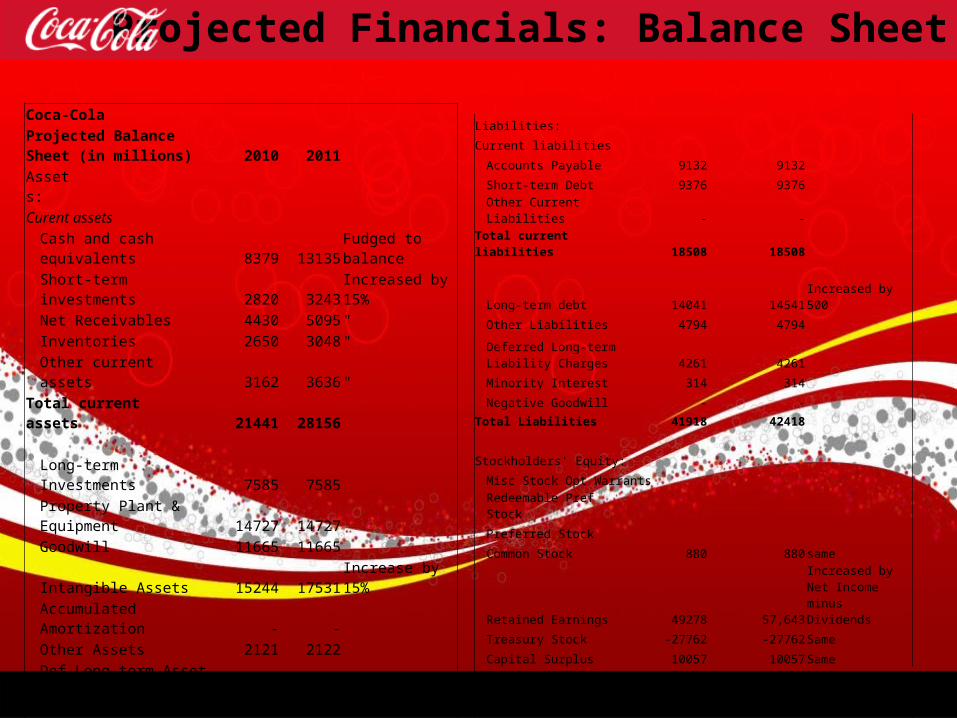

Projected Financials: Balance Sheet

Coca-Cola Projected Balance Sheet (in millions) 2010 2011 Assets: Curent assets

Cash and cash equivalents 8379 13135 Fudged to balanceShort-term investments 2820 3243 Increased by 15%Net Receivables 4430 5095 "Inventories 2650 3048 "Other current assets 3162 3636 "

Total current assets 21441 28156

Long-term Investments 7585 7585 Property Plant & Equipment 14727 14727 Goodwill 11665 11665 Intangible Assets 15244 17531 Increase by 15%Accumulated Amortization - - Other Assets 2121 2122 Def Long-term Asset Charges - -

Total Assets 72783 81786

Liabilities:

Current liabilities

Accounts Payable 9132 9132

Short-term Debt 9376 9376

Other Current Liabilities - -

Total current liabilities 18508 18508

Long-term debt 14041 14541 Increased by 500

Other Liabilities 4794 4794

Deferred Long-term Liability Charges 4261 4261

Minority Interest 314 314

Negative Goodwill - -

Total Liabilities 41918 42418

Stockholders' Equity:

Misc Stock Opt Warrants

Redeemable Pref Stock

Preferred Stock

Common Stock 880 880 same

Retained Earnings 49278 57,643

Increased by Net Income minus Dividends

Treasury Stock -27762 -27762 Same

Capital Surplus 10057 10057 Same

Other Stockholders' equity -1450 -1450

Total Stockholders' Equity 31003 39368

Total Liabilities and SE 72921 81786

49

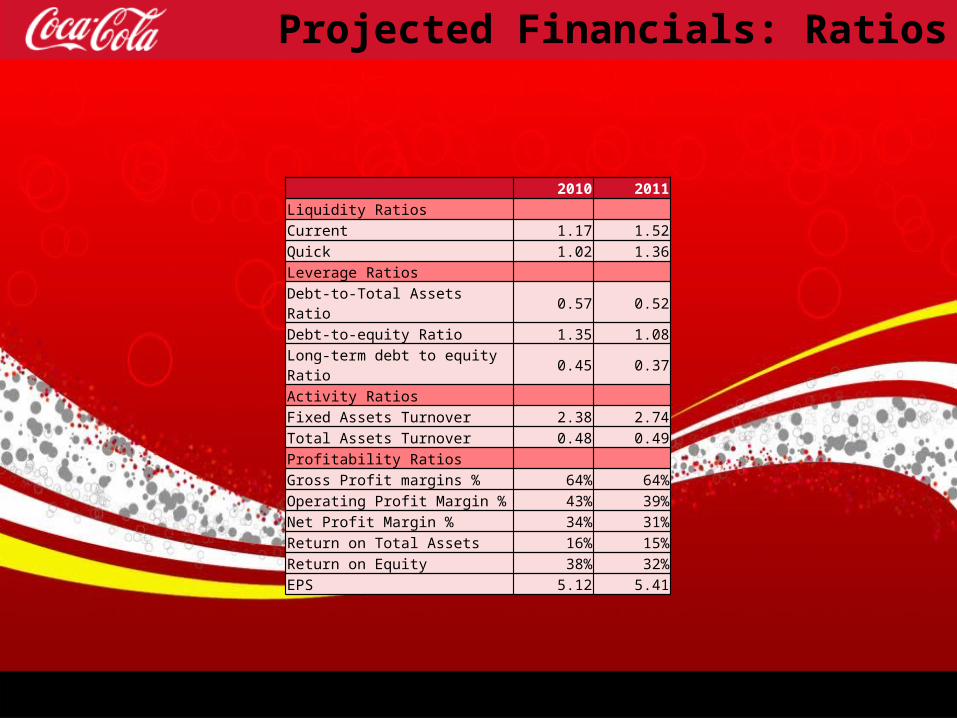

Projected Financials: Ratios

2010 2011Liquidity Ratios Current 1.17 1.52Quick 1.02 1.36Leverage Ratios Debt-to-Total Assets Ratio 0.57 0.52Debt-to-equity Ratio 1.35 1.08Long-term debt to equity Ratio 0.45 0.37Activity Ratios Fixed Assets Turnover 2.38 2.74Total Assets Turnover 0.48 0.49Profitability Ratios Gross Profit margins % 64% 64%Operating Profit Margin % 43% 39%Net Profit Margin % 34% 31%Return on Total Assets 16% 15%Return on Equity 38% 32%EPS 5.12 5.41

50

Foreseeable problems

• Lack of recognition from efforts

• Keeping related development costs under control

• Cost of goods sold may be higher for healthy alternatives

51

Strategic Evaluation

52

Balanced Scorecard

Area of Objectives Measure or TargetTime

Primary ResponsibilityExpectation

Consumers

1 Satisfaction Customer Survey results Yearly Chief Customer and commercial officer

2 Brand recognition Industry Reports Yearly Chief Customer and commercial officer

3 Customer loyalty Customer Survey results Yearly Chief Customer and commercial officer

Employees

1 Quality and service training On site and webinars Yearly Chief People Officer

2 Employee Satisfaction Survey Yearly Chief People Officer

Product Quality

1 Number of healthy alternatives Number of pruducts YearlyChief Customer and commercial Officer

Financial

1 Revenues increase 15% (2011), over 10% for following 2 years Quarterly VPO

2 Ratio analysis Better than Industry & PepsiCo Yearly VPO

Business Ethics/Natural Environment

1 Waste reduction Volume of recyclable materials Quarterly Global community connections Officer

2 Ethics Training number of ethics training sessions Yearly Global community connections Officer

53

Company Update

54

Update

• Well Being: In advancing one of our global commitments to help address obesity, we offer more than 800 low- and no-calorie options worldwide—nearly 25 percent of our global portfolio. In 2012, we introduced more than 500 new products globally, including portion-controlled options for regular calorie products, and more than 100 new low- or no-calorie options. Since 2000, our average number of calories per serving has decreased by 9 percent globally. In 2012, we supported more than 290 active healthy living programs in 118 countries.

• Women: In our third year, we continue our journey to economically empower 5 million women entrepreneurs across our value chain by 2020 through our 5by20™ program.

• Water: We are partnering around the world to meet our 2020 water use reduction and replenishment goals. This work has improved our water efficiency by 21.4 percent since 2004 and supported an estimated replenishment of approximately 52 percent of the water we used in our finished beverage products through 2012.

55

Update

56

Questions

57

References

• Babal, A. (2013). Coca-Cola Company - 2011. In F. R. David, Strategic Management; A competitive approach (pp. 235-243). Florence: Pearson.

• Coca-Cola Corporation. (2011). 2010 Annual Report. Atlanta.• David, F. R. (2013). Strategic Management; A Competitive Advantage

Approach. Florence: Pearson.• Harrison, J. S. (2013). Dr. Pepper Snapple Group. In F. R. David, Strategic

Management; A Competitive Approach (pp. 224-234). Florence: Pearson.• PepsiCo. (2011). 2010 Annual Report. Purchase.• Press Release: The U.S. Liquid Refreshment Beverage Market Remained

Flat in 2013. (2014, March 31). Retrieved from Beverage Marketing Corporation: http://www.beveragemarketing.com/news-detail.asp?id=299

• Wikinvest. (2014, April 27). Coca-Cola Company (KO). Retrieved from Wikinvest: http://www.wikinvest.com/stock/Coca-Cola_Company_%28KO%29

• Zmuda, N. (2009, November 22). Coca-Cola Lays Out Its Vision for the Future at 2010 Meeting. Retrieved from Advertizing Age: http://adage.com/article/news/coca-cola-lays-vision-future-2010-meeting/140664/