(setup by an act of parliament) hyderabad branch of … 2017.pdf · shri venkaiah naidu garu...

TRANSCRIPT

www.hydicai.org [email protected] Volume: 18 / Issue: 12 / July, 2017

Felicitation to Shri. M. Venkaiah Naidu, Minister of Housing and Urban Poverty Alleviation, Urban Development and Information and Broadcasting by Hyderabad Branch of SIRC of ICAI During Launching of GST on 1st July,2017

Seminar on GST Shri. Arjun Ram Meghawal Union Minister of State Finance and Corporate Affairs on 15th June ,2017

The Institute of Chartered Accountants of India (Setup by an Act of Parliament)

HYDERABAD BRANCH OF SIRC

NEWSLETTER

1

Chairman Writes….

Dear Professional Friends,

I wish you all a Very Happy CA Day.

1st July is a day when we all chartered accountants look forward to as it is celebrated as CA day all over the India. 1st July 2017 was more significant as GST was launched on the early hours of 01st July 2017. On this day the respect for our profession increased leaps and bounds when our Worthy Prime Minister Shri. Narendra Modiji and the entire Central Cabinet addressed the professional fraternity on the CA day celebration and the day of GST Implementation. The new revised syllabus of ICAI education also was launched by Shri Narendra Modiji on 1st July, 2017. GST is perceived as a major breakthrough in the economic reforms. The birth of the GST marked the beginning of a new era in country’s financial history”.

Hyderabad Branch celebrated the foundation day at Shanti Sarovar Auditorium Gachibowli. We are proud to inform you that the Said Programme was graced by two Union Ministers, Shri Venkaiah Naidu Garu Hon’ble Union Minister of Urban Development, Information and Broadcasting, Shri Bandaru Dattatreya Garu Hon’ble Minister of State (IC) of Labour and Employment. Hon’ble Finance Minister of Telengana State Shri Etela Rajendra Garu was also one of the distinguished guests of honour to address the delegates on the occasion and addressed about 2000 members and students present on the occasion .Overall this year's CA Day celebration was a remarkable event in the history of Hyderabad Branch and also the involvement of the departments is very encouraging.

We also happy to inform you that the Hyderabad branch organised a 3 day GST Seminar for Members on the GST from 16th to 18th June 2017 at The FTAPPCI. The Programme was graced by Union minister Shri. Arjun Ram Meghawal Union Minister of State Finance and Corporate Affairs, as chief guest and addressed the members.

2

Programmes held in the month of June 2017:

We at Hyderabad branch conducted Workshops on GST - Maintenance of Records & Books, Provision, Overview of Audit and Appeal, Inspection, Offences and penalties including general principles’ for imposing not imposing penalty, Transition Issues for Implementation of GST, One day Seminar on ICDS, Three day Seminar on GST, RRC SRISAILAM Jointly Organised by Hyderabad & Bangalore Branches.

We are proud to say that, First time Hyderabad Branch along with Karimnagar and Warangal Branches organised a Telengana State level Conference on the GST on 27th & 28th June 2017. Which was a grand success with almost 500 members participated in the event.

Programmes For the Forthcoming month July 2017.

We Hyderabad Branch along with the Department of Central Excise are organising a Programme on the GST on 8th July 2017 at The Institute of Engineers khairatabad. The Programme will be graced by Two union ministers: Shri Mukhtar Abbas Naqvi Garu Union Minister of Minority Affairs, Shri Bandaru Dattatreya garu Hon’ble Minister of State (IC) of Labour and Employment, and Senior Officials from Central Government and State Government who will be addressing the members on on GST Registration, Invoice Rules, Transitional Provisions, ITC & Returns. The other programmes are Overview on the GST on Works Contract, Returns in GST etc

July month will be a busy day for many Small and medium Practitioners due to last date of filing Income Tax Returns and ETDS returns. We will also be busy with GST implementation and understanding in this month. Hyderabad branch will continue to be focussing more on GST related seminars in the month of July the details of which will be hosted in website from time to time and intimation will also be sent to you couple of days before the event.

I request all the members to participate in the programmes conducted by branch.

Yours Sincerely,

CA. Chengal Reddy R

Chairman [email protected]

3

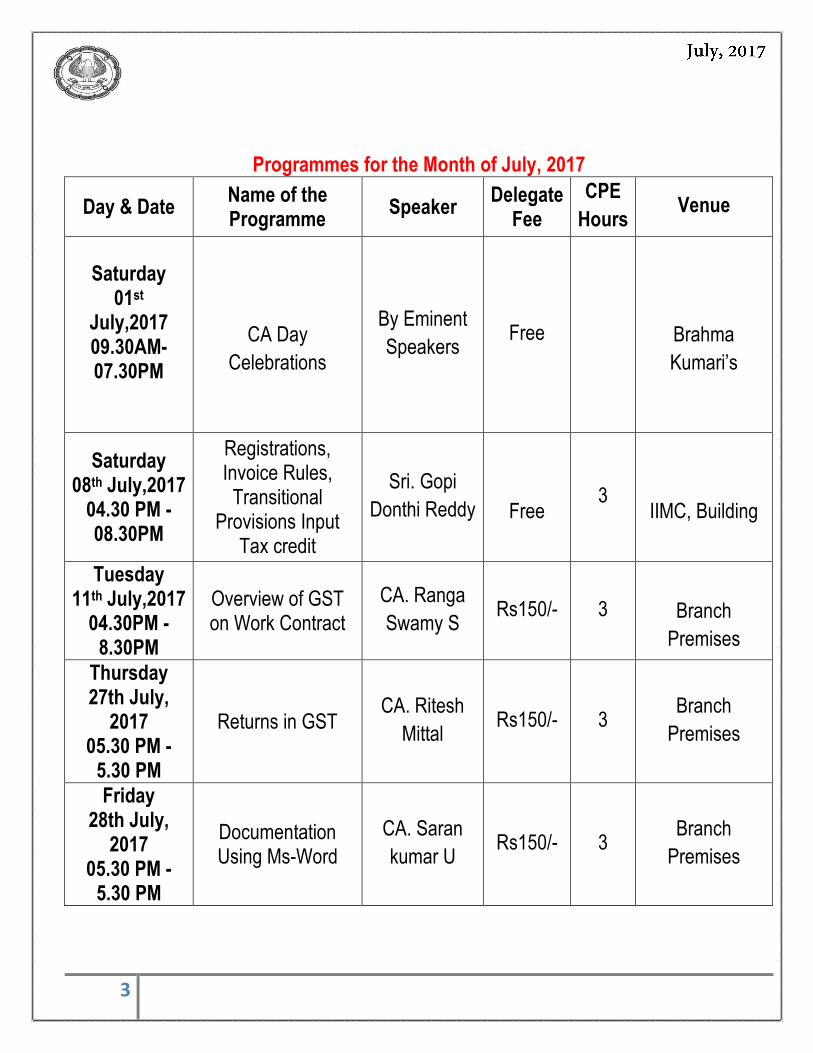

Programmes for the Month of July, 2017

Day & Date Name of the Programme

Speaker Delegate

Fee

CPE

Hours Venue

Saturday

01st July,2017 09.30AM-07.30PM

CA Day

Celebrations

By Eminent

Speakers Free

Brahma

Kumari’s

Saturday 08th July,2017

04.30 PM -08.30PM

Registrations, Invoice Rules,

Transitional Provisions Input

Tax credit

Sri. Gopi

Donthi Reddy

Free 3

IIMC, Building

Tuesday 11th July,2017

04.30PM -8.30PM

Overview of GST on Work Contract

CA. Ranga

Swamy S Rs150/- 3

Branch

Premises

Thursday 27th July,

2017 05.30 PM -

5.30 PM

Returns in GST CA. Ritesh

Mittal Rs150/- 3

Branch

Premises

Friday 28th July,

2017 05.30 PM -

5.30 PM

Documentation Using Ms-Word

CA. Saran

kumar U Rs150/- 3

Branch

Premises

4

VAT COURT

-compiled by CA Satish Saraf [email protected] 96 1818 4567

Evidence for claiming Input Tax Credit:

In order to claim Input Tax Credit in respect of second hand motor vehicle, it is required to produce

evidence before the assessing authority showing that the vehicle purchased by the dealer has been subject

to VAT at the time of its initial registration under the Motor Vehicles Act, 1988 either within the erstwhile

composite State of Andhra Pradesh or the State of Telangana.

Sree Krishna Automotives Hyderabad(P) Ltd Vs. State of Telangana & others – 63 APSTJ 190 (HC – T & AP).

Self-Loading Mobile Concrete Mixer:

Self-loading Mobile Concrete Mixer with HSN classification 84743110 producing cement concrete used in

Civil Works is classifiable as Machinery falling under Clause 39 of item 102 of the Schedule – IV to the

Telangana Value Added Tax Act, 2005 exigible to tax @ 5%.

Ajax Fiori Engineering (I) (P) Ltd Vs. State of Telangana – 63 APSTJ 181 TVATAT

Glass Jars & Plastic Jars:

Sale of Glass Jars & Plastic Jars falls under the entry No: 90 and sub-entry 4 & 12 of the Schedule – IV of

the Telangana Value Added Tax Act, 2005 and liable to tax @ 5%. The order of the Assessing officer

levying higher rate of tax @ 14.5% under general entry is set aside on the ground that the when specific

entry exists under the statute general entry need not be looked into.

East Coast Distributors (P) Ltd Vs. State of Telangana – 30 TTR 181 TVATAT

CORPORATE SOCIAL RESPONSIBILITY

ARTICLES

5

-compiled by CA. P Ravindranadh Reddy

I. INTRODUCTION: Companies Act 2013 has made Corporate Social Responsibility (CSR) mandatory to companies with certain net worth or turnover or net profit of certain amount under section 135 of the Companies Act (the Act) read with Companies (Corporate Social Responsibility policy) Rules 2014. (Rules). Those Companies are supposed to spend some percentage of profits towards development of the society as specified in the act and the same is termed as social responsibility. A brief discussion is made in the article on the subject.

II. DEFINATIONS: a)Corporate Social Responsibility (CSR): It means and includes but is not limited to i) Projects or Programs relating to activities specified in schedule VII to the Act or ii) Projects or Programs relating to activities undertaken by the Board of Directors of a Company (Board) in pursuance or recommendations of the CSR committee of the Board as per declared CSR Policy of the company subject to the conditions that such policy will cover subjects enumerated in Schedule VII of the Act. b) CSR Committee: it means the Corporate Social Responsibility committee of the Board

referred to in section 135 of the Act.

c) CSR Policy: It relates to the activities to be undertaken by the company as specified in

schedule VII to the Act and the expenditure thereon, excluding activities undertaken in

pursuance of normal course of business of a company.

d) Net Profit: it means the net profit as per its financial statements prepared in accordance

with the applicable provisions of the Act, but shall not include the following namely: i) any

profit arising from any overseas branch or branch of the company whether operated as a

separate company or otherwise and ii) any dividend received from other companies in India,

which are covered under and complying with the provisions of the section 135 of the Act.

III. APPLICABILITY: CSR is applicable to every company having a net worth of Five hundred crore rupees or more or a turnover of One thousand Crore rupees or more or a net profit of five crore rupees of more during any financial year. Such companies shall constitute Corporate Social Responsibility committee of the Board of Directors consisting of three or more directors out of which one shall be an independent director (Sec 135(1) of the Act).

IV. EXCEPTIONS: a) All unlisted companies or private companies covered under Sec. 135 but not required to appoint an independent director shall have their committees without such director. b) a private company having only two directors shall constitute its CSR committee with two

such directors.

c) a foreign company covered under the rules the committee shall comprise two persons, one

shall be a specified in Sec 380 (1) (d) of the Act and another person nominated by the foreign

company.

V. DUTIES OF CSR COMMITTEE: The CSR Committee shall a) formulate and recommend to the Board a CSR policy which shall indicate the activities to be undertaken by the company as specified in Schedule VII. b) Recommend the amount of expenditure to be incurred on the CSR activities and c) monitor the CSR policy of the company from time to time through a transparent monitoring mechanism to implement CSR projects or programs or activities undertaken by the company.

6

VI. CSR POLICY: The CSR policy shall include a) a list of CSR projects or programs that a company plans to undertake within the preview of the Act, specifying the modalities of execution of such projects or programs and the schedule of implementation of the same and b) monitoring the process of the same. The policy of the company shall specify that the surplus arising out of the CSR projects,

programs or activities shall not from part of business profit of a company

VII. CSR ACTIVITIES: They include activities relating to i) eradicating hunger, poverty and malnutrition, promoting preventive health care and sanitation ii) promoting education including special education and employment enhancing vocation skills especially among children, women, elderly and the differently abled and livelihood enhancement projects iii) promoting gender equality, empowering women, setting up homes and hostels for women and orphans, setting up old age homes, day care center etc., iv) ensuring environment sustainability ecological balance, conservation of natural resources etc. v) Protection of national heritage, art and culture, setting up public libraries, promotion and development of traditional arts and handicrafts. Vi) Measures for the benefit of armed forces veterans war widows and their dependents. Vii) Training for promoting rural sports, nationally recognized sports, Paralympic sports and Olympic sports. Viii) Contribution to the Prime Minister’s National Relief fund or any other fund set up by the Central Government for Socio- economic development and relief and welfare of the schedule castes, scheduled tribes, other backward classes, minorities and women. Ix) Contributions or funds provided to technology incubators located within academic institutions approved by the Central Government. X) rural development projects. (Schedule VII). The CSR activities shall be undertaken by the company as stated in its CSR policy. The

Board of Directors may decide to undertake its activities approved by the committee

concerned through a registered trust or a registered society or a company established under

section 8 of the Act.

Further if such trust society or company is not established by the company or its holding or

subsidiary or associate company, it shall have a track record of three years in undertaking

similar programs or projects and the company has specified the same to be undertake

through these entities, the modalities of utilization of funds on such projects and programs

and the monitoring and reporting mechanism.

VIII. CSR Expenditure: The Board of Directors of the Company shall ensure that the company spends at least two percent of the average net profits of the company made during the three immediately preceding financial years in pursuance of its Corporate Social Responsibility Policy. CSR expenditure does not include any expenditure not in conformity with the activities within the purview of schedule VII of the Act. Further the company shall give

preference to the local area and areas around its operation for spending the amount for CSR activities.

IX. CSR Reporting: The report of Board of Directors shall include an annual report on CSR containing particulars specified in the annexure. In case the company fails to spend sufficient amount on CSR, the Board of Directors shall state the reasons for the same in the Directors Report.

X. Display on website: The Board of Directors of the Company shall after considering the recommendations of the CSR Committee approve the CSR policy for the company and

7

disclose contents of such policy in its report and the same shall be displaced on the company’s website as per the particulars specified in the Annexure.

XI. CONCLUSION: It is the responsibility of every company to constitute a CSR committee and undertake CSR activities and spend such amount as CSR expenditure who come within the preview of Sec.135 of the Act. It is also the responsibility of the Board to disclose the details of CSR in its report and display the contents of CSR policy in its website.

Direct tax and transfer pricing updates

(Contributed by CA Vikram Doshi, CA Vaibhav Mehta and CA Kranthi Palivela)

1. Income from sub-licensing of property is taxable as income from house property and not income from

business or profession

Recently, the Hon’ble Supreme Court of India (‘Hon’ble SC’) in the case of Raj Dadarkar & Associates1

(‘Assessee’) held that the income from sub-licensing of property is taxable as income from house property and not

income from business or profession.

- The Assessee was allotted a plot of land by the Market Department of Municipal Corporation Greater

Bombay on monthly license basis, permitting it to carry out additions/ alterations and allowing sub-letting of

the shops and stalls. The Assessee constructed a shopping centre on such premises and sub-licensed it to

various shopkeepers.

- The Assessee has filed its return of income offering the aforesaid income from shops and stalls sub-licensed

by it under the head “Profits and Gains of Business or Profession” of the Income-tax Act, 1961 (‘Act’).

- For the Financial Year (‘FY’) 1999-2000, re-assessment was initiated by the assessing officer (‘AO’) by

issuing notice under section 148 of the Act. Thereafter, reassessment order was passed by the AO treating the

income from the shops and the stalls under head “Income from House Property”.

- The Commissioner of Income Tax (Appeals) [‘CIT(A)’] allowed the appeal of the Assessee and reversed the

action of the AO. However, the Income-tax Appellate Tribunal (‘ITAT’) reversed the order of the CIT(A) and

confirmed the action of the AO.

- Being aggrieved by the order of the ITAT, the Assessee preferred an appeal before the Hon’ble High Court

(‘Hon’ble HC’). The Hon’ble HC dismissed the appeal filed by the Assessee.

- On further appeal, the Hon’ble SC held as follows:

1 Raj Dadarkar & Associates v. ACIT [2017] 81 taxmann.com 193 (SC)

8

Wherever there is an income from leasing out of premises and collecting rent, normally such an income is

to be treated as income from house property if the provisions of section 22 of the Act are satisfied with

primary ingredient that the assessee is the owner of the said building or lands appurtenant thereto.

‘Owner of the house property’ is defined in section 27 of the Act which includes certain situations where

a person not actually the owner shall be treated as deemed owner of a building or part thereof. In the

present case, the Assessee is held to be deemed owner of the property in question by virtue of section

27(iiib) of the Act.

However, relying on the decision of the Hon’ble SC in the case of Chennai Properties & Investments

Limited2 and Rayala Corporation Private Limited

3, the Assessee argued that even if it was treated as

deemed owner of the premises in question, since the letting out the place and earning rents therefrom was

the main business activity of the Assessee, the income generated from sub-licensing the area should be

treated as business income.

Distinguishing the Assessee’s reliance in the case of Chennai Properties & Investments Limited

(Supra) and Rayala Corporation Private Limited (Supra), the Hon’ble SC observed that the facts in

the case of Rayala Corporation Private Limited (Supra) were similar to the case of Chennai

Properties & Investments Limited (Supra) and for this reason Rayala Corporation Private Limited

(Supra) followed the decision of Chennai Properties & Investments Limited (Supra). However, the

Hon’ble SC held the decision of Chennai Properties & Investments Limited (Supra) to be inapplicable

in the case of the Assessee.

The Hon’ble SC further observed that it was for the Assessee to produce sufficient material on record to

show that its entire income/ substantial income was earned from sub-letting of properties which was its

principal business activity. However, the Assessee did not argue on this aspect and did not make any

efforts to show as to how the aforesaid findings were perverse to the Assessee.

Further, the Hon’ble SC clarified that, merely because there is an entry in the object clause of the business

showing a particular object, it would not be the determinative factor to arrive at a conclusion that the

income is to be treated as income from business or profession or as income from house property.

Thus, the Hon’ble SC dismissed the case of the Assessee and upheld the order of Hon’ble HC.

2 Chennai Properties and Investments Limited v. CIT Central III [2015] 56 taxmann.com 456 (SC)

3 Rayala Corporation Private Limited v. ACIT [2016] 15 SCC 201 (SC)

9

2. Disallowance under section 40(a)(ia) of the Income-tax Act, 1961 (‘Act’) can be made even for the amount

paid during the year

Recently, the Hon’ble Supreme Court of India (‘Hon’ble SC’) in the case of Palam Gas Service4 (‘Assessee’)

held that section 40(a)(ia) of the Act not only covers those cases where the amount is payable but also when it is

paid and tax has not been deducted on the same.

- The Assessee is engaged in the business of purchase and sale of LPG cylinders. During the relevant Financial

Year (‘FY’), the Assessee entered into a contract with Indian Oil Corporation for carriage of LPG.

Subsequently, the Assessee had sub-contracted the same and got the transportation of LPG done through three

persons to whom freight payment was made without deducting tax at source.

- As per section 40(a)(ia) of the Act certain payments made would not be allowed as expenditure in case the tax

is deductible at source on the said payment under Chapter XVIIB of the Act and such tax has not been

deducted or, after deduction, has not been paid during the previous year or in the subsequent year before the

expiry of the time prescribed under section 200(1) of the Act.

- It can be seen that section 40(a)(ia) of the Act use the expression ‘payable’ therefore a controversy arises

whether this section would cover only those contingencies where the amount is due and still payable or it

would also cover the situation where the amount is already paid but no tax was deducted thereon.

- The Assessing Officer (‘AO’) observed that the Assessee is liable to deduct tax at source from the payment

made to sub-contractors within the meaning of section 194C of the Act. Thus, the AO disallowed these

expenses under section 40(a)(ia) of the Act.

- The Commissioner of Income Tax (Appeals) [‘CIT(A)’] and the Income-tax Appellate Tribunal (‘ITAT’)

upheld the order of AO. On further appeal, the Hon’ble High Court (‘Hon’ble HC’) too ruled in favour of the

AO.

- The Hon’ble SC held as follows:

As per section 194C of the Act, it is the statutory obligation of a person, who is making payment to sub-

contractor to deduct tax at source. Tax is to be deducted at the time of credit of such sum or when it is

actually paid to the contractor, whichever was earlier. Further, section 200 of the Act imposes obligation

on the person deducting tax to deposit the same to the Central Government or Board within the prescribed

time.

4 Palam Gas Service v. CIT [2017] 81 taxmann.com 43 (SC)

10

A combined reading of these two sections, would undeniably mean that every person who is not only

paying but also who has paid to the contractor was liable to deduct tax thereon and deposit the said tax to

the credit of Central Government or Board.

The Hon’ble SC relied on the decision of the Punjab & Haryana HC in the case of P.M.S. Diesels5

wherein it was held that the word 'payable' is an antonym of the word 'paid'. However, the same is not

significant to the interpretation of section 40(a)(ia) of the Act. When the entire scheme of obligation to

deduct the tax at source is read holistically, it can be understood that section 40(a)(ia) of the Act not only

covers those cases where the amount is payable but also when it is paid and tax has not been deducted on

the same. It was held that the liability to deduct tax at source under the provisions of Chapter XVII of the

Act is mandatory in nature.

Further, the Hon’ble SC overruled the decision of the Hon’ble Allahabad HC in the case of Vector

Shipping Service (P.) Ltd6 wherein the HC after noticing that the amounts have already been paid,

concluded without any discussion that Section 40(a)(ia) of the Act would apply only when the amount is

‘payable’. The Hon’ble HC dismissed the appeal stating that the question of law framed did not arise for

consideration. The Hon’ble SC held that Vector Shipping Services (P) Ltd. (supra) did not decide the

question of law correctly.

The Hon’ble SC further held that, if section 40(a)(ia) of the Act was interpreted as contended by the Assessee,

a person who has violated provisions of Chapter XVII B of the Act would go unpunished without suffering

monetary default. Thus, Hon’ble SC observed that a comprehensive reading of the obligation to deduct tax and

crediting thereon to Central Government would lead to a understanding that section 40(a)(ia) of the Act not only

covers amount which is ‘payable’ but also amount which is ‘paid’.

Thus, Hon’ble SC upheld the order of Hon’ble HC and dismissed the Assessee’s appeal.

3. The Delhi High Court held that in the event of non-compliance of Section 144C of Income-tax Act 1961 i.e.

failure to pass a draft assessment order to an eligible assessee, would result in invalidation of final

assessment order passed, consequent demand notices issued and penalty proceedings initiated by the

assessing officer.

Background

5 P.M.S Diesel v. CIT [2015] 374 ITR 562/59 taxmann.com 100 (P & H HC)

6 CIT v. Vector Shipping Service (P.) Ltd [2013] 357 ITR 642 (All. HC)

11

The Delhi High Court (‘HC’) in the case of Turner International Limited7 (‘taxpayer’), for Assessment Years

(‘AY’) 2007-08 and 2008-09 held that the failure of Assessing Officer (‘AO’) to adhere to mandatory

requirements of Section 144C(1) of the Income-tax Act, 1961 (‘the Act’) i.e. failure to pass a draft assessment

order to an eligible assessee, even in case of remand proceedings, would nullify the final assessment order passed,

consequent demand notices issued and penalty proceedings initiated by the AO.

Facts of the case

The taxpayer is a wholly-owned subsidiary of Turner Broadcasting System Asia Pacific Inc. and is engaged in

the business of sub-distribution of distribution rights and sale of advertisement inventory on satellite

delivered channels.

For AY 2007-08, the taxpayer filed its return of income (‘RoI’) on 31 October 2007 by declaring a total

income of INR 106,943,491. This was later revised on 31 March 2009 to claim a higher tax deducted at

source (‘TDS’). For AY 2008-09 the taxpayer filed its RoI on 30 September 2008 declaring a total income of

INR 350,423,465.

In respect of both the returns, since there were international transactions entered by the taxpayer, a reference

was made by the AO to the Transfer Pricing Officer (‘TPO’). In respect of both the AYs, two separate orders

were passed by the TPO on 29 October 2010 (for AY 2007-08) and 17 October 2011 (for AY 2008-09).

On the basis of the above orders of the TPO, the AO passed the draft assessment orders confirming the

adjustments proposed by the TPO. These were objected by the taxpayer before the Dispute Resolution Panel

(‘DRP’). DRP however, upheld the adjustments proposed by the TPO and issued directions confirming the

same. Post DRP directions, the AO passed the final assessment orders and the same were appealed against

by the taxpayer before the Income Tax Appellate Tribunal (‘Tribunal’).

By a common order dated 14 January 2013, in both the appeals pertaining to AY 2007-08 & AY 2008-09, the

Tribunal observed that neither the taxpayer nor the TPO had taken into consideration appropriate

comparables and therefore, the determination of arm’s length price was not justifiable. While setting aside

the directions issued by the DRP, the Tribunal remanded the matters to the AO for undertaking a transfer

pricing study afresh and framing an assessment in accordance with law.

7 W.P (C) 4260/2015 & W.P (C) 4261/2015

12

Pursuant to the orders of the Tribunal, the TPO issued fresh notices to initiate the remand proceedings. During

the remand proceedings the TPO made an upward adjustment to the total income of the taxpayer for both AY

2007-08 & AY 2008-09.

Pursuant to the orders passed by the TPO, the AO passed final assessment orders under Sections

254/143(3)/144( c) (13) read with Section 92CA(4) of the Act confirming the additions proposed by the

TPO. Along with the final assessment orders, the AO also issued demand notices under Section 156 of the

Act and also initiated penalty proceedings under Section 271(1)(c) of the Act. Aggrieved, the taxpayer filed a

writ petition before the Delhi HC.

Taxpayer’s Contentions

The taxpayer contended that the final assessment orders passed by the AO stands vitiated for failure to adhere

with the mandatory provisions of Section 144C(1) of the Act.

Tax Department’s Contentions

The department contended that the failure to adhere to the mandatory requirement of issuing a draft

assessment order under Section 144C (1) of the Act would be a curable defect and that the matter must be

restored to the AO to pass a draft assessment order and thereafter the assessment proceedings would continue.

Delhi HC’s Ruling

The Delhi HC held that the failure by AO to adhere to mandatory requirement of Section 144C (1) of the Act

and to pass final assessment order would result in invalidation of the final assessment order passed and the

consequent demand notices and penalty proceedings initiated.

The Delhi HC relied on the Andhra Pradesh HC decision in the case of Zuari Cement Ltd.8, which held that

the failure to pass a draft assessment order under Section 144C (1) of the Act would result in rendering the

final assessment order “without jurisdiction, null and void and unenforceable”.

The Delhi HC further relied on the Madras HC’s decision in the case of Vijay Television (P) Ltd.9 wherein

the department sought to rectify its mistake by issuing a corrigendum after passing the final assessment order.

Consequently, not only the final assessment order but also the corrigendum issued thereafter was challenged.

Following the Andhra Pradesh HC’s decision in the case of Zuari Cement Ltd., the Madras HC quashed the

final assessment order passed by the AO.

8 WP(C) No. 5557/2012 9 369 ITR 113 (Mad.)

13

Conclusively, the Delhi HC held that non-compliance of mandatory provision of Section 144(C) (1) of the

Act and passing a final assessment order first would result invalidation of final assessment order, demand

notices issued and penalty proceedings initiated thereafter. In the current case, the final assessment order

passed, demand notices issued by the AO and penalty proceedings initiated are all set aside.

4. The Tribunal deleted an adhoc transfer pricing adjustment proposed by the assessing officer, held that

since the transfer pricing provisions were not complied with, the adhoc adjustment proposed has no merit.

Background

The Income Tax Appellate Tribunal (‘Tribunal’) in the case of John Deere India Pvt. Ltd.10

(‘taxpayer’), for

assessment year (‘AY’) 2009-10 held that non-compliance of transfer pricing provisions by the transfer pricing

officer (‘TPO’) while computing adjustments does not result in any merit. Further, the Tribunal held that the rate

of royalty approved by the Reserved Bank of India (‘RBI’) would constitute Comparable Uncontrolled Price

(‘CUP’) data and that the transaction would be at arm’s length price (‘ALP’).

Facts of the case

The taxpayer was a joint venture between Larsen & Toubro Limited (L&T), India and Deere & Co. During

the financial year (‘FY’) 2005-06, John Deere India Pvt. Ltd. acquired 48% of L&T’s stake due to which the

taxpayer became a wholly-owned subsidiary of John Deere India Pvt. Ltd. John Deere India Pvt. Ltd. is in

turn is a wholly-owned subsidiary of Deere & Co., USA. The taxpayer is engaged in the business of

manufacturing of tractors, aggregates and parts which were sold in the domestic market as well as foreign

market.

During the said AY, the taxpayer had entered into international transactions with its associated enterprises

(‘AEs’) amounting to INR 976.43 crores consisting of import of raw materials & components, re-export of

defective material, export of tractors, export of aggregates & spares, import of harvester machines for

demonstration purposes, payment of royalty, reimbursement and recovery of expenses.

10

ITA No. 828/PUN/2014

14

During the transfer pricing assessment proceedings, the TPO made an adjustment amounting to INR 43.63

crores to the international transaction pertaining to export of tractors. No other adjustments were proposed by

the TPO in the transfer pricing order.

However, in the show-cause notice issued by the TPO, he made reference to payment of royalty on both old

and new products. The TPO was of the view that payment of royalty on old products was unwarranted and

proposed an adjustment of INR 7.50 crores.

The AO passed the draft assessment order proposing an adjustment of INR 43.63 crores. Aggrieved, the

taxpayer filed its objections before the Dispute Resolution Panel (‘DRP’). The DRP issued directions in

favour of the taxpayer by deleting the adjustment proposed in the draft assessment order.

Subsequently, the AO, while passing the final assessment order proposed a transfer pricing adjustment of INR

7.50 crores in respect of payment of royalty, since, the same was initiated by the TPO in the show-cause

notice. Aggrieved, the taxpayer filed an appeal before the Tribunal.

Taxpayer’s Contentions

The taxpayer contended that the adjustment of INR 7.50 crores in respect of payment of royalty is adhoc in

nature and that the taxpayer incurred INR 46.05 crores towards royalty. Materialising this adjustment would

mean a double adjustment to the taxpayer.

The taxpayer further contended that payment of royalty was a separate international transaction with its

associated enterprises for which no adjustment was proposed by the TPO, accordingly, the AO does not have

jurisdiction to propose an adjustment while passing the final assessment order.

The taxpayer placed reliance on the Technical Collaboration Agreement with its associated enterprises,

wherein the rate of payment of royalty was fixed at a rate less than 3%, the same was in accordance with the

approval obtained by the RBI.

Further, the taxpayer referred to the Section 144C(13)of the Income-tax Act, 1961 (‘the Act’) wherein it was

mentioned that the AO is bound to follow the directions of the DRP and cannot go beyond the scope and

propose a transfer pricing adjustment.

Tax Department’s Contentions

The department contended that the TPO’s action of proposing an adjustment on royalty was justified, as the

payment of royalty was unwarranted on old products exported by the taxpayer.

15

Though the payment of royalty was included in the cost base of the taxpayer, the department contended that a

separate adjustment is necessary for the payment of royalty on old products sold and computed the adjustment

at INR 7.50 crores.

Tribunal’s Ruling

The Tribunal referred to the Sections 92C, 92CA and 144C of the Act which define the transfer pricing

provisions to be complied by the TPO / AO.

The Tribunal held that the TPO is at liberty to make any separate adjustment on a particular transaction,

where adjustment is made in respect of any other international transaction. However, the TPO is not

empowered to propose an adhoc adjustment which admittedly, is not as per law.

The objection of the TPO was that the taxpayer was paying royalty to associated enterprises on both old and

new products and as per the TPO, the payment of royalty on old products is unwarranted. It is not the role of

TPO to determine whether the payment of royalty is justified or not on an adhoc basis, but the arm's length

price of same has to be determined by following the procedures laid down in the Income Tax Act. The TPO

has failed to do so. Further, since the TPO had not proposed the adjustment as per the Act, there was no

occasion for the taxpayer to raise any objections before the DRP and hence, the order of DRP is silent on

this issue.

The AO while passing final assessment order under section 144C(13) of the Act, has made the said addition

on the ground that show cause notice was issued by the TPO in this regard and the taxpayer had already

replied. However, such adhoc disallowance of royalty is not warranted by applying the provisions relating to

transfer pricing. The Tribunal held that the procedure laid down under the transfer pricing provisions has

not been followed by the TPO and hence, there is no merit in the adhoc disallowance of royalty.

On the merits of the case, the Tribunal relying on the decision of Bombay High Court’s decision in the case

of SGS India Pvt. Ltd. and Pune Tribunal’s decision in the case of Spicer India Ltd. held that the rates

approved by RBI would constitute CUP data and that the transactions are at ALP. Accordingly, the Tribunal

in the present case, held that, the payment of royalty by the taxpayer to its associated enterprises at rate less

than 3%, is liable to be considered at arm's length rate and no further addition is warranted on this

respect.

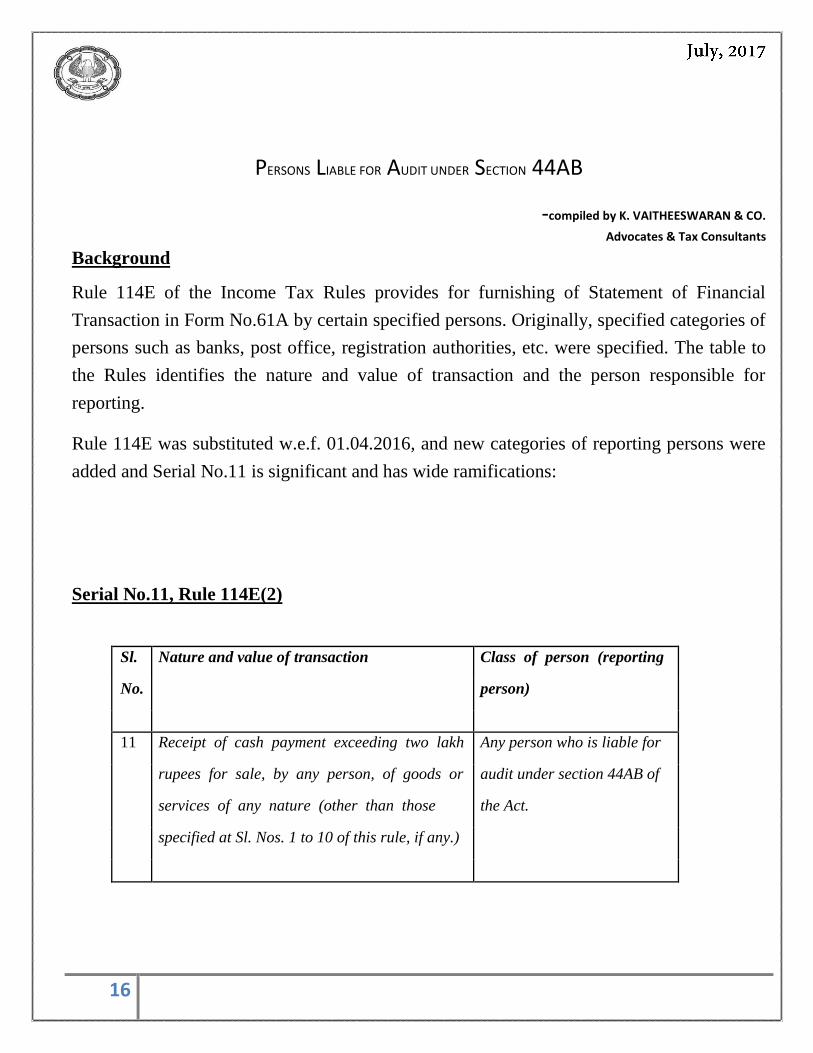

DIRECT TAX ALERT – STATEMENT OF FINANCIAL TRANSACTION (SFT) –

16

PERSONS LIABLE FOR AUDIT UNDER SECTION 44AB

-compiled by K. VAITHEESWARAN & CO.

Advocates & Tax Consultants

Background

Rule 114E of the Income Tax Rules provides for furnishing of Statement of Financial

Transaction in Form No.61A by certain specified persons. Originally, specified categories of

persons such as banks, post office, registration authorities, etc. were specified. The table to

the Rules identifies the nature and value of transaction and the person responsible for

reporting.

Rule 114E was substituted w.e.f. 01.04.2016, and new categories of reporting persons were

added and Serial No.11 is significant and has wide ramifications:

Serial No.11, Rule 114E(2)

Sl. Nature and value of transaction Class of person (reporting

No. person)

11 Receipt of cash payment exceeding two lakh Any person who is liable for

rupees for sale, by any person, of goods or audit under section 44AB of

services of any nature (other than those the Act.

specified at Sl. Nos. 1 to 10 of this rule, if any.)

17

Rule 114E(3)

In terms of Rule 114E(3), a reporting person (other than the persons at Sl.No.10 and

Sl.No.11) shall while aggregating the amounts for determining the threshold amount for

reporting in respect of any person as specified in the table,—

(a) take into account all the accounts of the same nature maintained in respect of that person during the financial year;

(b) aggregate all the transactions of the same nature recorded in respect of that person

during the financial year;

(c) attribute the entire value of the transaction or the aggregated value of all the

transactions to all the persons, in a case where the account is maintained or transaction

is recorded in the name of more than one person;

Press Release

(i) The Ministry of Finance vide Press Release dated 22.12.2016 has stated that the

norms of aggregation contained in sub-rule 3 of Rule 114E have been amended vide

CBDT’s Notification No. 91/2016 dated 6th October, 2016 clearly indicating that the said

transactions did not require aggregation and the reporting requirement under SFT for this

purpose is on receipt of cash payment exceeding Rupees two lakh for sale of goods or

services per transaction.

(ii) The Ministry of Finance vide Press Release dated 26th May 2017 has stated that

• The due date for filing such SFT in Form 61A is 31st May 2017.

• In case there are reportable transactions for the year, the reporting person/entity is

required to register with the Income Tax Department and generate Income Tax Department

Reporting Entity Identification Number (ITDREIN) The same can be generated by logging-

in to the e-filing website (https://incometaxindiaefiling.gov.in/) with the log in ID used for

the purpose of filing the Income Tax Return of the reporting person / entity. Entity having

PAN can take only PAN based ITDREIN. Entity having TAN can generate an ITDREIN

only when such TAN's Organisational PAN is not available.

18

• The registration of reporting person (ITDREIN registration) is mandatory only when

at least one of the Transaction Type is reportable. A functionality "SFT Preliminary

Response" has been provided on the e-

Filing portal for the reporting persons to indicate that a specified transaction type is

not reportable for the year.

Persons who are liable to tax audit under Section 44AB are the reporting persons referred to

in Serial No.11 who now have to mandatorily file the SFT for the financial year ending

31.03.2017 in Form No.61A in case there is receipt of cash payment exceeding

Rs.2,00,000/- for sale of goods or services of any nature (other than those specified at Sl.

Nos. 1 to 10). The last date for filing the SFT is 31.05.2017.

Failure to furnish the SFT attracts penalty of Rs.100/- per day during which such failure

continues in terms of Section 271FA.

This provision is also in line with Section 269ST which prohibits receipt of an amount of

Rs.2,00,000/- or more otherwise by way of account payee cheque or bank draft or electronic

remittance. Section 269ST was introduced by Finance Act, 2017 w.e.f. 01.04.2017.

Disclaimer:- This Tax Alert is only for the purpose of information and does not constitute or

purport to be an advise or opinion in any manner. The information provided is not intended

to create an attorney-client relationship and is not for advertising or soliciting.

K.Vaitheeswaran & Co. do not intend in any manner to solicit work through this Tax Alert.

The Tax Alert is only to share information based on recent developments and regulatory

changes. K.Vaitheeswaran & Co. is not responsible for any error or mistake or omission in

this Tax Alert or for any action taken or not taken based on the contents of this Tax Alert.

SURVEY,SEARCH& SEIZURE UPDATE

Compiled by: Hari Agarwal,FCA

Vivek Agarwal,ACA,CS

19

1. The Asstt. Commissioner of Income Tax, Central Circle-IV (2) , Chennai Versus M/s. S. & P Foundation Pvt Ltd 2015 (6) TMI 283 - ITAT CHENNAI - Income Tax Reopening of assessment - assessee challenged the issue of notice u/s.148 in respect of assessment completed u/s.

153A - Held that:- Proceeding initiated u/s. 153A for all six years shall become a subject matter to assessment

u/s.153(A) of the Act and the Assessing officer shall have freehand, on assessment, only on the proceeding that are pending to frame the assessment afresh. But in the case where the proceedings have reached finality, the

assessment u/s.153A r.w.s.143(3) and where certain material document have been found indicating undisclosed income, the addition shall have to be restricted to those documents or incrementing documents, clubbed only to

assessment framed originally. As law does not permit the Assessing Officer to disturb already concluded assessment,

whether on the date of intimation of search u/s.132 or requisition of books, no proceedings is pending in the search, materials found indicating incrementing materials, the Assessing Officer engrosses a jurisdiction where he has

clubbed two sets of income, return income and unearthed income, had arrived at the total income. Thereafter, if he had a reason to believe the said assessment can be re-assessed u/s.148 of the Income Tax Act as discussed in the

earlier paras so as to reopen the assessment, there should be sufficient materials. There is no arbitrary power to the Assessing Officer to reopen on the basis of change of opinion. In the present case

we have gone through the reasons for reopening of assessment. It cannot be proper reason to reopening. The

Assessing Officer has no power to review his own order. The re-assessment has to be made on fulfillment of certain free condition and if the concept stating ‘'change of opinion" is removed in the graph of re-assessment or/of

assessment, redo take place. Once again treat the concept of change of opinion inbuilt test to check to abusive power by Assessing Officer. Hence, the Assessing Officer has power to reopen, provided there is ‘tangible material" to come

to the conclusion that there is escapement of income from assessment. The reason must have live link with the

foundation of belief.

2. Balarampur Chini Mills Ltd v.Commissioner of Income-tax, Central-II, Kolkata*

SPECIAL LEAVE TO APPEAL (C) NOS. 28286 & 28287 OF 2015† MARCH 6, 2017, 80 taxmann.com 36 (SC) Section 271(1)(c), read with section 37(1), of the Income-tax Act, 1961 - Penalty - For concealment of income (Disallowance of claim, effect of) - Assessment years 2003-04 and 2004-05 - Assessment was completed in case of assessee under section 143(3) - Search proceedings initiated by Director (Inv.) at office premises of another assessee unearthed some records which showed that assessee made certain payments to 'another' assessee were disallowable - Assessee filed revised return and offered said amount as disallowable item under section 37(1) - Assessing Officer held that there was deliberate concealment of income on part of assessee, since assessee disclosed additional income only after he was confronted by Director (Inv.), with evidence - He, thus, passed a penalty order under section 271(1)(c) - High Court by impugned order held that since assessee himself admitted that return originally filed by him included expenditure disallowable under section 37(1), it would follow that original return contained inaccurate particulars and therefore, assessee was liable for penalty under section 271(1)(c) - Whether Special Leave Petition filed against impugned order was to be granted - Held, yes [Para 1] [In favour of assessee]

3. Disclosure of additional income in revised return filed under sec. 153A notice won't call for penalty,

Principal Commissioner of Income-tax-19 v. Neeraj Jindal*

FEBRUARY 9, 2017 [2017] 79 taxmann.com 96 (Delhi)

Section 271(1)(c), read with section 153A of the Income-tax Act, 1961 - Penalty - For concealment of income (Revised return) - Assessment years 2005-06 and 2006-07 - Whether when an assessee has filed revised returns after search has been conducted, and such revised return has been accepted by Assessing Officer, then merely by virtue of fact that such return showed a higher income, penalty under section 271(1)(c) cannot be automatically imposed - Held, yes - Whether once Assessing Officer accepts revised return filed under section 153A, original return under section 139 abates and becomes non-est, and, thus, 'concealment' has to be seen with reference to revised return filed by assessee - Held, yes - Whether in order for Explanation 5 to section 271(1)(c) to apply, it is necessary that there must be certain assets found in possession of assessee during search, and assessee must claim that such

20

assets have been acquired by him by utilising (wholly or in part) his income - Held, yes [Paras 16, 21 & 26] [In favour of assessee]

4. Rich Udyog Network Ltd.v.Chief Commissioner of Income tax

[2015] 63 taxmann.com 88 (Allahabad)

Section 132, read with section 133A of the Income-tax Act, 1961 - Search and seizure (Conversion of survey into search) - Assessment year 2014-15 - During course of survey under section 133A, certain huge cash and incriminating documents were found from business premises of assessee-company - Director of assessee in a statement recorded under section 131(1A) failed to explain source of cash and various dubious entries in seized documents - Whether on facts it could be said that authority had reasons to believe that an action under section 132 was warranted and department was justified to convert survey into search and seizure under section 132 after due approval of competent authority - Held, yes [Paras 11, 12, 13, 14, 15, 16, 20, 21, 22, 23 and 25] [In favour of revenue]

Words and Phrases : The words 'has reasons to believe' as occurring in section 132(1).

Disclaimer : The views and opinions expressed or implied in the Hyderabad Branch of SIRC

of ICAI E- Newsletter are those of the authors and do not necessarily reflect those of

Hyderabad Branch of SIRC of ICAI. Material in the Publication may not be reproduced,

whether in part or in whole, without the consent of Hyderabad Branch of SIRC of ICAI

21

CA. Chengal Reddy R Chairman

09000181104 [email protected]

CA. Sunil Kumar M Vice- Chairman 09866996662

CA. Bhanu Narayan Rao Y. V Secretary

09951782950 [email protected]

CA. Prakash Chokda Treasurer

09949101411 [email protected]

22